new china investing in a ‘new normal’ growth...

TRANSCRIPT

November 6, 2015

China Strategy

New China investing in a

‘new normal’ growth era

Portfolio Strategy Research

Top-down case; ‘New China’ ideas; implications

A ‘new normal’ growth era: Less could be more

After growing at around 10% p.a. for 30 years, China’s trend growth could

fall to around 5-6% in the next decade with continuing high cyclicality, but

the growth drivers will be different, and growth quality should improve.

New framework for investing in ‘New China’

Macro rebalancing, policy bias, reforms, and demographic shifts are

ushering in new waves of demand and reshaping the China story. Rising

consumption and services is a secular theme but high sectoral growth

variances imply a more nuanced equity story and implementation strategy.

Investors need to adjust their conventional framework to these macro

shifts. We identify 30 sub-industries (from 143) with high/stable revenue

growth and low sensitivity to GDP growth to form our ‘New China’

universe (671 companies, 21% of total A/H/ADR market cap). We add cross-

country profitability and valuation parameters to pick 19 stocks (9 A shares

and 10 offshore stocks), averaging 28% revenue and 31% EPS CAGR in

2015-17E, 23x 2016E P/E, and 1.1x PEG.

Implications for different types of investor

Index users: We prefer MXCN over HSCEI/HSI, CSI300 over SHCOMP.

Global corporates/funds: The classic EM story has largely played out

and local competition has risen: Adaptability is the key to success.

EM investors: China’s index weight in EM is set to rise over time; New

China stocks offer a sensible vehicle to close the underweight gaps.

China funds: Build core holdings around New China, trade Old China.

Commodities: Our commodity strategists expect prices to be lower for

longer but see demand shifting to ‘opex’ from ‘capex’ commodities.

‘New normal’ unleashes new demand, offering l-t alpha opportunities

Source: Bloomberg, Wind, Goldman Sachs Global Investment Research.

Kinger Lau, CFA +852-2978-1224 [email protected] Goldman Sachs (Asia) L.L.C.

Timothy Moe, CFA +852-2978-1328 [email protected] Goldman Sachs (Asia) L.L.C.

Jack Wang +852-2978-1220 [email protected] Goldman Sachs (Asia) L.L.C.

Alvin So +852-2978-1585 [email protected] Goldman Sachs (Asia) L.L.C.

Chenjie Liu, Ph.D +86(10)6627-3324 [email protected] Beijing Gao Hua Securities Company Limited

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investorsshould be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investorsshould consider this report as only a single factor in making their investment decision. For Reg AC certification and otherimportant disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed bynon-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

The Goldman Sachs Group, Inc. Global Investment Research

-10

-5

0

5

10

15

20

Ja

n-1

4

Ap

r-14

Ju

l-14

Oct-

14

Ja

n-1

5

Ap

r-15

Ju

l-15

Total consumption

Metal consumption

(%, YoY)

35%

0%

-10%

0%

10%

20%

30%

40%

2006

2007

2008

2009

2010

2011

2012

2013

2014

1H

15

New China Old China

Revenue growth (yoy)

197

118

50

100

150

200

250

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

New China

Old China

Market cap-weighted price returns

November 6, 2015 China

Goldman Sachs Global Investment Research 2

Table of contents

Investing in a ‘new normal’ era 2

A ‘new normal’ growth era: Less could be more 5

‘New normal’ creates ‘New China’, plotting a new story 12

New framework for investing in Chinese equities 17

Index users: Choose your ‘New’ indexes 22

Global funds/corporates: Adaptability is the key to success 23

EM investors: Buy ‘New China’ to reduce tracking errors 24

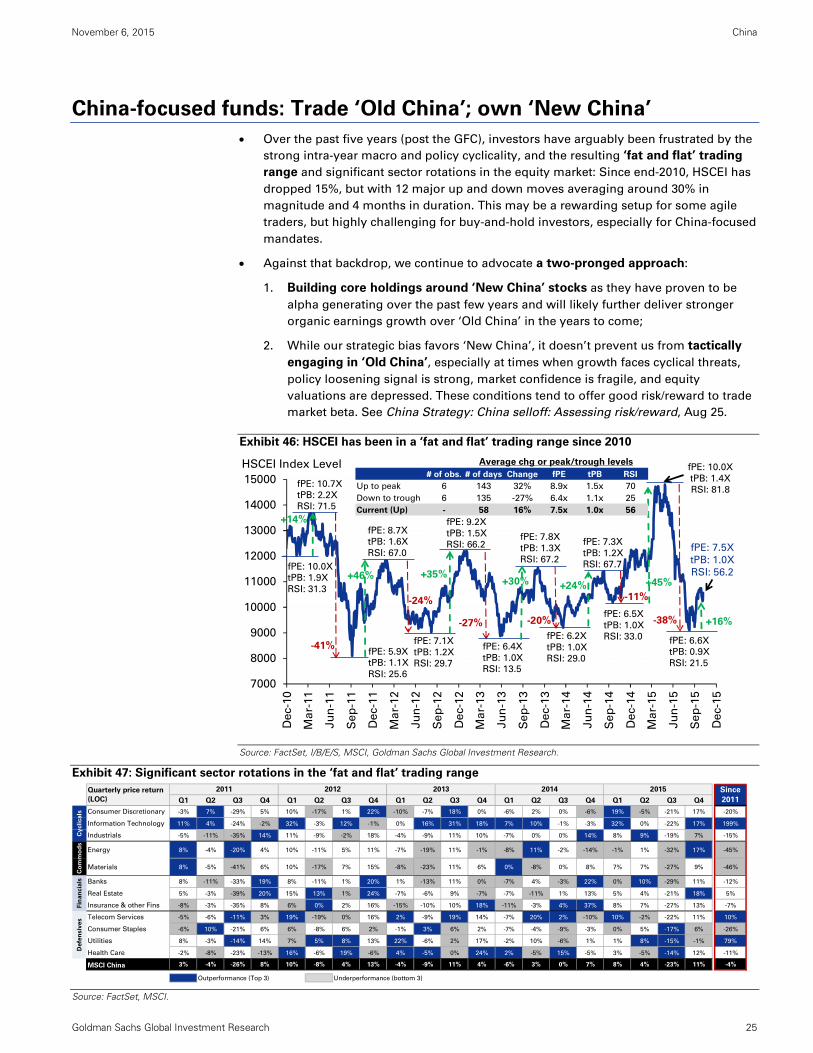

China-focused funds: Trade ‘Old China’; own ‘New China’ 25

Commodities: The divide between ‘opex’ and ‘capex’ commodities 26

Appendix 27

Disclosure Appendix 30

Investing in a ‘new normal’ era

The concept of a ‘new normal’ has been gathering investors’ attention. The expression

has been used repeatedly by senior policymakers in China to frame their views on the

economy and policy trends. But it also comes against a backdrop where headline GDP

growth is moderating, the policy/reform calendar is still active, asset markets volatility is

high, and global investors have widespread and entrenched concerns about China’s macro

situation. Hence there is considerable demand from investors to understand what a ‘new

normal’ era may entail and how that might impact their portfolio.

In this report, we aim to provide a refined analytical framework to help investors better

comprehend the ongoing macro and micro changes in China, and the resulting

structural investment implications, leveraging the detailed work from our macro

colleagues and single-stock analysts. Our logic and arguments are structured as follows:

A ‘new normal’ growth era: Less could be more

We believe the ‘new normal’ will be characterized by:

Lower potential growth rates (our economists project approximately 5-6% trend GDP

growth in the next decade) than the 10% pace achieved in the past 30 years;

Different growth drivers, notably more consumption/services, less investment and

exports, although the composition of the latter two is also changing;

Higher growth quality than before, given a more balanced and sustainable growth

profile, and less social deadweight losses (e.g. pollution, corruption);

Macro cyclicality will likely stay high as China needs reform and proactive cyclical

management to contain macro risks, facilitate the rebalancing, and to unleash/realize

its growth potential at the time when global demand is lackluster, and local macro

imbalances (high leverage, overcapacity, capital misallocation) are significant.

November 6, 2015 China

Goldman Sachs Global Investment Research 3

‘New normal’ creates ‘New China’, plotting a new story

Deep-rooted perceptions of China as ‘the world’s factory’ and the largest

infrastructure/property builder globally need to evolve into a new narrative under

the ‘new normal’.

China will likely invest more in ‘soft infrastructure’ than just building highways and

bridges; China is inevitably losing global market share in low-value-added goods (like

textiles and toys) but is now a dominant global and local player in high-end

electronics and industrial equipment, with rising momentum in infrastructure

exports. Demand for commodities is inevitably weak, but opex commodities should

continue to outperform capex commodities as China becomes richer.

As compelling as it might appear from a top-down perspective, consumption/services

is a broad concept and there is wide variation in growth between different items of

consumption due to changing consumer preferences and demographics, suggesting

the equity story could be more nuanced than headline growth potential may indicate.

New framework to find the bright spots

Investors need to adjust their investment framework as the economy morphs into a

new growth era: Popular equity indexes are not a good proxy for the economy, and

focusing on conventional macro indicators like IP and manufacturing PMI to formulate

market views could miss the big picture, and forgo potentially rewarding investment

opportunities.

The definition of ‘New China’ varies among investors. We systemically select 30 sub-

industries (GICS level 4) from our 3,636-company database (143 sub-industries) which

have delivered high and stable top-line growth (>10% revenue growth in each of the

past three years) and low revenue sensitivity to GDP growth to form our ‘New China’

universe. 671 companies (483 A shares, 200 offshore, 12 dual-listed) fall under this

group, representing 21% of total Chinese equity market cap (A+H+ADR).

High valuations and profitability normalization are two common risks and concerns

when investing in emerging and fast-growing themes. We focus on PEG ratios and

cross-country ROE comparison to drive our implementation ideas and to improve

risk/reward. We highlight 19 New China names under our coverage universe (9 A

shares and 10 offshore names), averaging 28% revenue and 31% EPS CAGR in 2015-

17E, 23x 2016E P/E, and 1.1x PEG.

Implications for different types of investor

1. Index users: China indexes have generated a wide range of returns over the past three

years—HSCEI has dropped 3% but ChiNext has rallied 268%—primarily reflecting their

‘New China’ content. MSCI China (offshore) and CSI300 (onshore), while not perfect,

are better proxies for the underlying (and changing) economic fundamentals, and

implementation tools on a risk/reward basis.

2. Global funds/corporates: The classic EM playbook—low per capita income, low

product penetration, high pent-up demand—has largely played out in China, in our

view. Local competition is intensifying and the strategy relying on untapped demand

and perception arbitrage is probably outdated. Global firms which adapt to the

evolving demographics, income levels, and consumer tastes should see higher chance

to succeed.

November 6, 2015 China

Goldman Sachs Global Investment Research 4

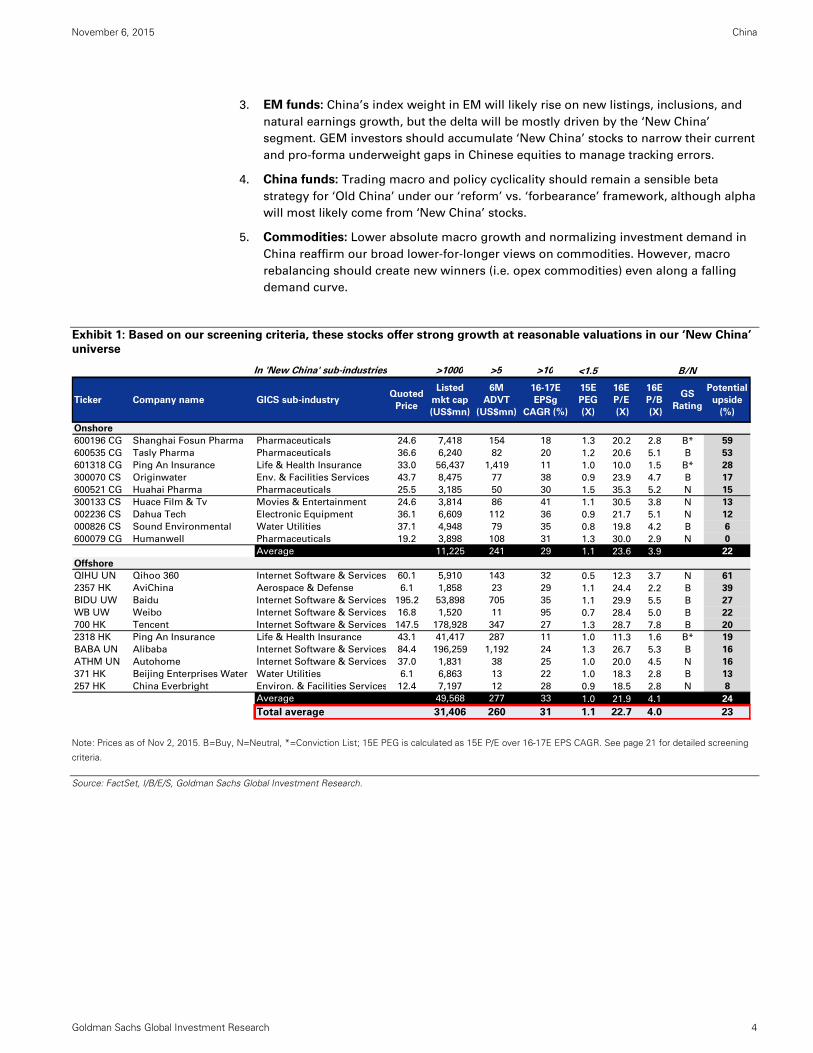

3. EM funds: China’s index weight in EM will likely rise on new listings, inclusions, and

natural earnings growth, but the delta will be mostly driven by the ‘New China’

segment. GEM investors should accumulate ‘New China’ stocks to narrow their current

and pro-forma underweight gaps in Chinese equities to manage tracking errors.

4. China funds: Trading macro and policy cyclicality should remain a sensible beta

strategy for ‘Old China’ under our ‘reform’ vs. ‘forbearance’ framework, although alpha

will most likely come from ‘New China’ stocks.

5. Commodities: Lower absolute macro growth and normalizing investment demand in

China reaffirm our broad lower-for-longer views on commodities. However, macro

rebalancing should create new winners (i.e. opex commodities) even along a falling

demand curve.

Exhibit 1: Based on our screening criteria, these stocks offer strong growth at reasonable valuations in our ‘New China’

universe

Note: Prices as of Nov 2, 2015. B=Buy, N=Neutral, *=Conviction List; 15E PEG is calculated as 15E P/E over 16-17E EPS CAGR. See page 21 for detailed screening

criteria.

Source: FactSet, I/B/E/S, Goldman Sachs Global Investment Research.

In 'New China' sub-industries >1000 >5 >10 <1.5 B/N

Ticker Company name GICS sub-industryQuoted

Price

Listed

mkt cap

(US$mn)

6M

ADVT

(US$mn)

16-17E

EPSg

CAGR (%)

15E

PEG

(X)

16E

P/E

(X)

16E

P/B

(X)

GS

Rating

Potential

upside

(%)

Onshore

600196 CG Shanghai Fosun Pharma Pharmaceuticals 24.6 7,418 154 18 1.3 20.2 2.8 B* 59

600535 CG Tasly Pharma Pharmaceuticals 36.6 6,240 82 20 1.2 20.6 5.1 B 53

601318 CG Ping An Insurance Life & Health Insurance 33.0 56,437 1,419 11 1.0 10.0 1.5 B* 28

300070 CS Originwater Env. & Facilities Services 43.7 8,475 77 38 0.9 23.9 4.7 B 17

600521 CG Huahai Pharma Pharmaceuticals 25.5 3,185 50 30 1.5 35.3 5.2 N 15

300133 CS Huace Film & Tv Movies & Entertainment 24.6 3,814 86 41 1.1 30.5 3.8 N 13

002236 CS Dahua Tech Electronic Equipment 36.1 6,609 112 36 0.9 21.7 5.1 N 12

000826 CS Sound Environmental Water Utilities 37.1 4,948 79 35 0.8 19.8 4.2 B 6

600079 CG Humanwell Pharmaceuticals 19.2 3,898 108 31 1.3 30.0 2.9 N 0

Average 11,225 241 29 1.1 23.6 3.9 22

Offshore

QIHU UN Qihoo 360 Internet Software & Services 60.1 5,910 143 32 0.5 12.3 3.7 N 61

2357 HK AviChina Aerospace & Defense 6.1 1,858 23 29 1.1 24.4 2.2 B 39

BIDU UW Baidu Internet Software & Services 195.2 53,898 705 35 1.1 29.9 5.5 B 27

WB UW Weibo Internet Software & Services 16.8 1,520 11 95 0.7 28.4 5.0 B 22

700 HK Tencent Internet Software & Services 147.5 178,928 347 27 1.3 28.7 7.8 B 20

2318 HK Ping An Insurance Life & Health Insurance 43.1 41,417 287 11 1.0 11.3 1.6 B* 19

BABA UN Alibaba Internet Software & Services 84.4 196,259 1,192 24 1.3 26.7 5.3 B 16

ATHM UN Autohome Internet Software & Services 37.0 1,831 38 25 1.0 20.0 4.5 N 16

371 HK Beijing Enterprises Water Water Utilities 6.1 6,863 13 22 1.0 18.3 2.8 B 13

257 HK China Everbright Environ. & Facilities Services 12.4 7,197 12 28 0.9 18.5 2.8 N 8

Average 49,568 277 33 1.0 21.9 4.1 24

Total average 31,406 260 31 1.1 22.7 4.0 23

November 6, 2015 China

Goldman Sachs Global Investment Research 5

A ‘new normal’ growth era: Less could be more

What is the ‘new normal’?

The term ‘new normal’ became common when used by PIMCO co-founder Bill Gross

and CEO Mohamed El-Erian in 2009 to describe the sluggish growth and deflationary

pressure globally post the Global Financial Crisis (GFC)1.

In May 2014, when President Xi Jinping visited Henan Province, he used this term to

describe China’s changing macro dynamics2.

During the APEC summit in Beijing in November 2014, President Xi characterized a

‘new normal’ growth era as: 1) growth shifting from high speed to medium-to-high

speed; 2) an improved and more efficient economic growth structure; and 3) growth

increasingly driven by innovation instead of inputs and investment3.

To better frame our discussion around this broad concept and subsequently translate this

into equity market views, we use ‘new normal’ to mean: a) decelerating potential (trend)

growth; b) changing macro growth propellants; c) possibly better quality of growth;

and, d) persistently high macro and policy cyclicality.

1. The pace of growth will further moderate

China has been able to grow 10% CAGR in the past 30 years essentially by

leveraging its cost competitiveness (labor, land, environment, FX), reform dividends

(opening up since 1979, Deng Xiaoping’s Southern tour in 1992, the SOE reform led by

Zhu Rongji from 1998 to 2002, the property market reform in the late 1990s, and WTO

accession in 2001), and its unique socioeconomic setup (state’s strong influence in

the economy).

However, that winning formula seems to have reached its limit given China’s cost

competitiveness has eroded, SOEs’ operating efficiency has deteriorated, cumulative

leverage and the pace at which leverage has been built is high on a global basis, and

China’s policy efficacy is now in question after the recent volatility in the asset markets.

Indeed, our economists expect China to go through a ‘bumpy deceleration’ process

over the medium to long term. Specifically, they forecast China’s (potential) GDP

growth to further slow to around 5.8% for the next 5 years, and then to 4.8% in the

decade thereafter, after factoring in the potential productivity gains as a result of

structural reforms but also the growth drag from the significant debt buildup since the

GFC. See Asia Econ Analyst: China’s bumpy deceleration continues, pulling region

along for the ride (Aug 31).

The slowing growth path is consistent with cross-country experiences. China’s per

capita GDP now stands at US$7,600 (current FX), similar to the US, Japan, Germany,

and UK in their mid-to-late 1970s. These economies on average registered less than 3%

growth (2.9% and 2.8% to be exact) in the subsequent 5 and 10 years after they

reached a per capita GDP level of US$8,000, which suggests the following:

1. The growth moderation in China shouldn’t be a major surprise, especially

considering China’s size and the high growth rate that it has delivered historically.

1 http://global.pimco.com/EN/Insights/Pages/Gross%20Sept%20On%20the%20Course%20to%20a%20New%20Normal.aspx

2 http://www.bloomberg.com/news/articles/2014-05-11/xi-says-china-must-adapt-to-new-normal-of-slower-growth

3 http://news.xinhuanet.com/english/china/2014-11/09/c_133776839.htm

November 6, 2015 China

Goldman Sachs Global Investment Research 6

2. If China manages to grow at 6.5% p.a. in the next five years as stated in the 13th

Five Year Blueprint, China would still be one of the fastest growing economies

in the G20.

3. The biggest question, in our view, would be how China will manage the

deceleration without triggering systemic events against a challenging local and

external backdrop. This requires a balancing act between pursuing reforms and

supporting growth, which we will address in the later sections.

Exhibit 2: After growing at 10% in the past 3 decades, China will likely see growth

moderating to around 5-6% in the next 5 to 10 years

Note: Average numbers indicates 10y real GDP CAGR.

Source: CEIC, Goldman Sachs Global Investment Research.

Exhibit 3: The slowdown should not be surprising given the size and maturity of the

Chinese economy

Note: Our per capita GDP comparison is based on current FX and on a nominal basis. On that basis: t=0 in 2014 for China, in

1974 for US, in 1975 for Germany, in 1977 for Japan, and in 1978 for UK.

Source: CEIC, Goldman Sachs Global Investment Research.

0

2

4

6

8

10

12

14

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

China real GDP growth (%, rolling 5y CAGR)

Avg: 7.2

Avg: 8.1

Avg: 10.4

Avg: 9.1

Avg: 10.0

Avg10-14: 8.6

15-19E: 5.8

20-24E: 5.1

25-30E: 4.5

-2

0

2

4

6

8

10

12

-15 -10 -5 0 5 10 15 20 25 30 35 40

China Japan US

Germany UK

Real GDP growth (%, rolling 5y CAGR)

t years

GDP per capita = 7.6k US$ (China current)

DM Avg: 2.9%DM Avg: 1.7%

November 6, 2015 China

Goldman Sachs Global Investment Research 7

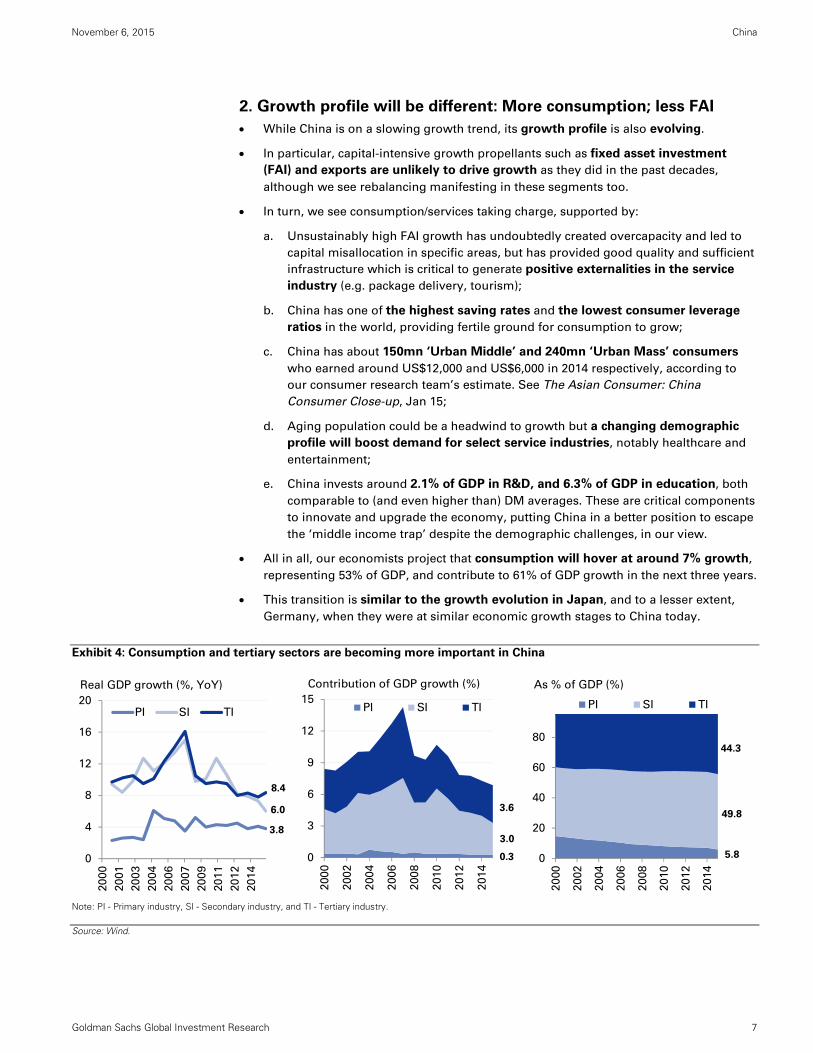

2. Growth profile will be different: More consumption; less FAI

While China is on a slowing growth trend, its growth profile is also evolving.

In particular, capital-intensive growth propellants such as fixed asset investment

(FAI) and exports are unlikely to drive growth as they did in the past decades,

although we see rebalancing manifesting in these segments too.

In turn, we see consumption/services taking charge, supported by:

a. Unsustainably high FAI growth has undoubtedly created overcapacity and led to

capital misallocation in specific areas, but has provided good quality and sufficient

infrastructure which is critical to generate positive externalities in the service

industry (e.g. package delivery, tourism);

b. China has one of the highest saving rates and the lowest consumer leverage

ratios in the world, providing fertile ground for consumption to grow;

c. China has about 150mn ‘Urban Middle’ and 240mn ‘Urban Mass’ consumers

who earned around US$12,000 and US$6,000 in 2014 respectively, according to

our consumer research team’s estimate. See The Asian Consumer: China

Consumer Close-up, Jan 15;

d. Aging population could be a headwind to growth but a changing demographic

profile will boost demand for select service industries, notably healthcare and

entertainment;

e. China invests around 2.1% of GDP in R&D, and 6.3% of GDP in education, both

comparable to (and even higher than) DM averages. These are critical components

to innovate and upgrade the economy, putting China in a better position to escape

the ‘middle income trap’ despite the demographic challenges, in our view.

All in all, our economists project that consumption will hover at around 7% growth,

representing 53% of GDP, and contribute to 61% of GDP growth in the next three years.

This transition is similar to the growth evolution in Japan, and to a lesser extent,

Germany, when they were at similar economic growth stages to China today.

Exhibit 4: Consumption and tertiary sectors are becoming more important in China

Note: PI - Primary industry, SI - Secondary industry, and TI - Tertiary industry.

Source: Wind.

0

4

8

12

16

20

20

00

20

01

20

03

20

04

20

06

20

07

20

09

20

11

20

12

20

14

PI SI TI

Real GDP growth (%, YoY)

8.4

6.0

3.8

0

20

40

60

80

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

PI SI TI

As % of GDP (%)

44.3

49.8

5.80

3

6

9

12

15

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

PI SI TI

Contribution of GDP growth (%)

3.6

3.0

0.3

November 6, 2015 China

Goldman Sachs Global Investment Research 8

Exhibit 5: China has one of the highest saving rates among major economies globally, while its consumer leverage is low

Note: Data is as of 2013.

Source: Haver.

Source: Haver, Goldman Sachs Global Investment Research.

Exhibit 6: China invested 2.1% of GDP in R&D in 2014,

comparable to OECD averages

Exhibit 7: China’s spending on education is high relative

to its income level on a global basis

Source: OECD.

Source: OECD, Haver.

Exhibit 8: Consumption (as a % of growth) rose in Japan

after it reached the 8K per capita income threshold

Exhibit 9: Investment as a % of GDP also moderated in

Japan and Germany as the economy matured

Note: Our per capita GDP comparison is based on current FX and on a nominal basis. On that basis: t=0 in 2014 for China, in 1974 for US, in 1975 for Germany, in 1977 for Japan, and in 1978 for UK.

Source: CEIC.

Source: CEIC.

0

10

20

30

40

50

60

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

China US UK

Japan Germany

Saving rate (%)

50%

13%

18%21%

25%

0

20

40

60

80

100

120

140

Sw

iss

Au

str

alia

Can

ad

a

No

rwa

y

UK

Ko

rea

Sw

ed

en

US

Ma

laysia

Th

aila

nd

Jap

an

Eu

ro A

rea

Pe

ru

Taiw

an

Co

lum

bia

Isra

el

S. A

fric

a

Ch

ina

Po

lan

d

Ch

ile

Cze

ch

Hu

ng

ary

Bra

zil

Tu

rkey

Ru

ssia

Ind

on

esia

Mexic

o

Ind

ia

Ph

ilip

pin

es

Household debt as % of GDP (%)

1.0

1.5

2.0

2.5

3.0

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

R&D spending as % of GDP

China: 2.1%

North Asia

+ SG: 3.0%

USA: 2.8%

Europe: 1.9%

OECD: 2.0%

Note: Averages for regional numbers4

5

6

7

8

0 10 20 30 40 50 60

Education expenditure as % of GDP (%, as of 2011)

Per capita income (k US$)

Canada

China France

Italy

Japan

UK

US

Argentina Australia

Korea

Mexico

Russia

45%

55%

65%

75%

85%

95%

-25 -20 -15 -10 -5 0 5 10 15 20 25 30 35 40

China Japan US

Germany UK

Final consumption as % of GDP

t years

GDP per capita = 7.6k US$

(China current)

30%

40%

50%

60%

70%

80%

-25 -20 -15 -10 -5 0 5 10 15 20 25 30 35 40

China Japan US

Germany UK

Household consumption as % of GDP

t years

GDP per capita = 7.6k US$

(China current)

November 6, 2015 China

Goldman Sachs Global Investment Research 9

3. Quality of growth should be better

Growth quality is admittedly hard to quantify. But, in the context of China macro and

markets, we define quality of growth as a more balanced and sustainable growth profile

which results in higher growth efficiency and less social deadweight losses. We see the

macro rebalancing enhancing growth quality in the following manners:

Reducing investment, especially in overcapacity and polluted sectors, and promoting

consumption should help divert capital to areas where supply hasn’t caught up with

demand (e.g. healthcare). In theory, this, with the appropriate policy support and

incentive, should help improve the Incremental Capital Output Ratio (ICOR) and the

Pareto efficiency for the economy, in our view.

The rising awareness of environmental issues and increasing investment in the related

areas should ease the pollution pressures, which have become a serious concern in

China. Not only are they creating economic losses which are not being accounted for

in the headline GDP, but they are threatening social stability if the situation continues

to worsen.

China’s Gini coefficient is high in a global context. The wealth disparity (or income

distribution inequality) between household and corporate sector should narrow as

FAI-driven growth tends to disproportionately benefit owners of capital than labor, and

vice versa for consumption-led growth, everything else being equal.

Rising consumption demand could also stimulate job creation in the tertiary sector,

which typically offers higher wages and is more labor-intensive than the secondary

industry, thereby buttressing income growth and helping to absorb the potential slack

from the challenging industrial sector.

In the end, private consumption has proven to be the key and sustainable growth

lever for major developed markets globally—we think this is the path that China should

follow.

Exhibit 10: ICOR at the macro level and ROIC in the

equity market have both moderated

Exhibit 11: The gaps between rich and poor in China are

quite significant

Note: Data is as of 2008 for Japan; 2009 for India; 2010 for China(WB), Indonesia, Australia and Canada; 2011 for S. Africa and Germany; 2012 for Mexico, Russia, Turkey, Italy, France and UK; 2013 for Colombia, Brazil, Argentina and US; and 2014 for China (Wind).

Source: Bloomberg, Wind, CEIC, Goldman Sachs Global Investment Research.

Source: CEIC.

2.5

3.0

3.5

4.0

4.5

5.0

5.5

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

1H

15

Trailing 5Y ICOR - RHS

All China ROIC

All China ex fin. ROIC

ROIC (%) ICOR (X)

0

10

20

30

40

50

60

70

S. A

fric

a

Co

lom

bia

Bra

zil

Mexic

o

Ch

ina (

Win

d)

Arg

en

tin

a

Ch

ina (

WB

)

Ru

ssia

US

Tu

rkey

Ind

on

esia

Italy

Au

str

ali

a

Ind

ia

Can

ad

a

Fra

nce

UK

Ja

pa

n

Germ

an

y

GINI Index (World Bank est.)

November 6, 2015 China

Goldman Sachs Global Investment Research 10

Exhibit 12: High growth has partly come at the expense

of the environment

Exhibit 13: The service industry is becoming a major

source of job creation

Source: Knoema, World Bank, Bloomberg.

Source: Wind.

4. Growth and policy cyclicality should stay high; ‘Growth’ vs.

‘Forbearance’ remains in place

Transforming a deep-rooted growth model which has been effective for the past three

decades in the second-largest economy in the world with more than 1.3bn people is

not an easy task.

Also, the fiscal stimulus program in 2008 has created and aggravated a number of

macro imbalances, notably overcapacity, high leverage, low SOE efficiency, and

potentially high NPLs. These macro issues have further complicated the transition.

As such, we believe macro (and market) volatility will likely stay high as China is still in

the process of optimizing conflicting objectives (reform, rebalancing, reasonable

growth) against a backdrop where global demand is lackluster, and domestic macro

imbalances remain significant.

The analytical framework that we have been using to comprehend the strong intra-year

macro and policy cyclicality is what we called as ‘reform’ vs. ‘forbearance’.

Specifically, striking a delicate balance between supporting short-term growth and

reducing systemic risk appears the key policy objective in the reform era, with the

policy pendulum (actions) swinging between a ‘proactive approach’ (i.e. pursuing

reform to address existing problems and pre-empt further risks) and ‘forbearance’ (i.e.

delay addressing the problems). This policy dynamics have also resulted in strong

intra-year volatility in the equity markets, in our view. See, inter alia, China Portfolio

Strategy: The China credit conundrum: Risks, paths and implications, Jul 26, 2013.

Overall, China needs structural reforms to correct these imbalances, facilitate the

rebalancing, and to unleash/realize its growth potential. We believe easy monetary

policy is required to buffer the downside risk and the ‘pain’ of reform. So far, we think

some progress has been made, but more is needed, especially in the SOE sector. See

China A-share Strategy: Retreat, repair, and reform, Oct 8, for detail.

2,081

2,017

1,993

1,940

1,960

1,980

2,000

2,020

2,040

2,060

2,080

2,100

20

07

20

12

20

14

Total renewable water

resources (m^3/inhab/yr)

11.6

11.5

11.3

11.3

11.1

11.2

11.3

11.4

11.5

11.6

20

07

20

09

20

11

20

13

Arable land

(as % of land area)

6.9

7.7

8.5

9.4

9.8

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

20

06

20

08

20

10

20

12

20

14

CO2 emission (mn tonnes)

0

200

400

600

800

1,000

0

20

40

60

80

100

196

5

196

8

197

1

197

4

197

7

198

0

198

3

198

6

198

9

199

2

199

5

199

8

200

1

200

4

200

7

201

0

201

3

PI SI TI Total employment - RHS

As % of total employment (%) Total employment (mn)

November 6, 2015 China

Goldman Sachs Global Investment Research 11

Exhibit 14: China has announced and implemented a number of key reforms since the 3rd party Plenum in Nov 2013

Source: PBoC, Xinhua News, Sina, Caixin, Reuters, Bloomberg, compiled by Goldman Sachs Global Investment Research.

Exhibit 15: China needs accommodative policy to soften

the ‘pain’ of reforms...

Exhibit 16: ...especially those relating to the significant

buildup of leverage

Source: WDI, Penn World Table, IMFWEO, BIS, Bloomberg, Goldman Sachs Global Investment Research.

Source: CEIC, PBOC, NBS, FactSet, Goldman Sachs Global Investment Research.

Obje

ctives

Policie

s/d

evelo

pm

en

ts

Key areas of reform since the third plenum meeting in Nov 2013

Fiscal reformsFinancial market

reformsSOE reformsSocial reforms

Division of responsibility and

spending rights between the

central and local

governments, more

transparency on spending,

and a more sustainable fiscal

revenue model.

Value added tax (VAT) and

resource tax reforms

Removed and lowered

consumption taxes in

selected products

LGFVs to include public

welfare debt in the fiscal

budget

Exempted VAT and Business

Tax for small firms with

quarterly revenues less than

Rmb 90K

Further infrastructure

investment to modernize

urban underground pipe

systems

Launched a bond-for-debt

swap program to help local

governments to convert thier

high-interest-bearing debts

into low-cost bonds with the

current quota of Rmb 3.2tn

Public-Private-Partnership

(PPP) to be further enhanced

to entice more private capital

participation.

Increasing the role of market

forces, improving

transparency and efficiency

of financial markets,

reinforcing capital account

opening and RMB

internationalization.

Expanded CNY/USD trading

band from 1% to 2%

Preferred share issuance pilot

program for banks

SH-HK Stock Connect

scheme started in Nov 2014

Launched deposit insurance

scheme

Asset-backed securities (ABS)

issuance will no longer need

PBoC‘s pre-approval

The Mainland-HK Mutual

Recognition of Funds (MRF)

started on July 1, 2015.

Introduced large-

denomination negotiable

certificates of deposit with

market-based interest rates

Removed the regulatory 75%

loan/deposit (L/D) cap for

banks, making the L/D ratio

used for reference only

Removed the interest rate

cap of bank deposits longer

than 1 year

The PBoC adjusted the CNY

fixing mechanism to allow

the CNY to weaken reflecting

market supply/demand

condition.

Reduced restrictions on

foreign investment by

making a 'negative list' of

industries other than which

foreigners can invest freely.

Promoting competition

between SOEs and private

companies, opening up more

SOE ownership to private

capital, and encouraging

M&A to reduce over-

capacity.

Opened up 80 state popjects

for private investment

Reduction and tighter

regulation on SOE

executives' compensation

and perks

Selected 6 SOEs as SOE

ownership reform pilots

Mixed ownership reform in

oil and gas sectors

The State Council released

plans to open up China’s

credit card clearing services

industry to foreign firms.

Six central SOEs started pilot

programs on mixed-

ownership reform

Compensation reforms in

central SOEs

BoCom, CMB and BOC

announced mixed-ownership

reform plans to introduce

more private shareholders.

AVIC asset restructuring

Shipping sector

consolidation

Released the "top-level

design" of SOE reforms, as

well as a more specific

guideline on SOE mixed-

ownership reforms

China Reform Holdings to

buy 6% stake in China Tower

to build electric-car charging

stations.

China Mobile, China Telecom

and China Unicom to sell

their tower assets to a new

entiy - China Tower

Encouraging further

urbanization, reforming

Hukou (household

registration system),

loosening up one-child

policy and expanding the

social welfare system.

Rural land reform to grant

farmers mortgage and

transfer rights of their land

Families will be allowed two

children if one parent is an

only child

Cut prices of more than 400

drugs to reduce health care

costs

Deregulated prices in 9

products and services

including tobacco, rail and

air freight, port services and

property brokerage

The PBoC provided Rmb

260bn of PSL to CDB for

shanty town development.

Plans to integrate health

care system for urban

residents with rural hukous

Plan for tax-deductible

private health insurance

allowing up to Rmb2,400

taxdeductible spending per

person per year on eligible

private health insurance

products.

Accelerated investment in

environmental protection

and stepped up regulation

on air, water and soil

polution

Fully abolished "one-child"

policy and replaced with

"two-child" policy

Legal reforms / anti-

corruption

Promoting the rule of law

and enhancing corruption

punishment, improving

oversight and prevention

structures.

Plans to separate the

jurisdiction of courts from

administrative divisions

Tightening regulations

concerning business

involvements and overseas

immigration of public

officials’ relatives

Launched a large -scale anti-

corruption campaign aiming

to catch both "tigers" and

"flies"

The Central Commission for

Discipline Inspection (CCDI)

to inspect all central SOEs

for corruption cases in 2015

Initiated a global anti-

corruption campain to bring

back corrupt officials

overseas

Further reduction of 'san

gong' spending

-3

-2

-1

0

1

Between 5-

10 years

before

5-years

before

0-1 years 2-3 years 4-5 years

30pp 40pp 50pp 60pp

Size of debt buildup (change in debt-to-GDP ratio)

Prior 10-yr average

Median policy rates relative to prior 10y avg (%)

0

2

4

6

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

7D repo (%)

1.5%

4 6 9 12 12 12 11 12 12 16 19 19 20 22 24 2622 22 24 25 26 32 28 30 28 29 27 25 24 23 23 24

79 11 12

13 15 15 1624 27 24 26 31 34 36

109103

107114 106 98 98 93 94

110119 123

134143

145157

135 138149

161 156 155 152 150 150

178192 190

204219

226

242

0

30

60

90

120

150

180

210

240

270

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

E

Corporate leverage

LGFV leverage(loan, bond)

Govt. Leverage

Consumer loans

Percent of GDP (%)

November 6, 2015 China

Goldman Sachs Global Investment Research 12

‘New normal’ creates ‘New China’, plotting a new story

The ongoing macro rebalancing in a ‘new normal’ growth era is apparent in the gaps

between manufacturing and service PMIs, the divergence between CPI and PPI, and

based on our proprietary indicators, the disparity between GS China Consumption

Tracker and GS Metal Consumption Index (MCI), among many others. Macro aside,

rebalancing is also happening within key growth drivers and asset markets.

Exhibit 17: Macro rebalancing appears in play

Source: Wind, Goldman Sachs Global Investment Research.

1. China is still building, but less ‘hard infra’ and property, more

public goods

FAI growth has clearly slowed in the manufacturing and property sectors while

infrastructure spending growth has remained resilient, mainly reflecting the proactive and

expansionary fiscal policy but anemic investment demand from the private sector.

That said, underneath the broad infra investment category, ‘soft’ infrastructure (hospitals,

schools, sewage system, and other environmental-related and ‘public goods’ projects) is

showing moderately higher momentum vs. the traditional ‘hard’ infrastructure, which

typically focuses on transportation infra investment including highways, bridges, and high-

speed railways. We think this trend is likely to extend as ‘public goods’ related investment

is regarded by policymakers as one of the key levers to sustain and enhance growth going

forward, as stated in the 13th Five Year Blueprint.

Exhibit 18: Infra spending has held up well despite the weakening trends in property and

manufacturing FAI

Source: CEIC.

48

50

52

54

56

58

Jan

-12

Ju

l-12

Jan

-13

Ju

l-13

Jan

-14

Ju

l-14

Jan

-15

Ju

l-15

Service PMI

Manufacturing PMI

Index

-8

-6

-4

-2

0

2

4

6

Jan

-12

Ju

l-12

Jan

-13

Ju

l-13

Jan

-14

Ju

l-14

Jan

-15

Ju

l-15

CPI PPI

(%, YoY)

-10

-5

0

5

10

15

20

Ju

l-12

Oct-

12

Jan

-13

Ap

r-13

Ju

l-13

Oct-

13

Jan

-14

Ap

r-14

Ju

l-14

Oct-

14

Jan

-15

Ap

r-15

Ju

l-15

GS total consumption tracker

GS metal consumption index (MCI)

(%, YoY)

-10

0

10

20

30

40

50

Ap

r-1

0

Au

g-1

0

De

c-1

0

Ap

r-1

1

Au

g-1

1

De

c-1

1

Ap

r-1

2

Au

g-1

2

De

c-1

2

Ap

r-1

3

Au

g-1

3

De

c-1

3

Ap

r-1

4

Au

g-1

4

De

c-1

4

Ap

r-1

5

Au

g-1

5

Manufacturing+Property

Infra (Transportation)

Infra (Water/Edu/Health/Sports)

China FAI yoy growth (%, 3m rolling avg)

November 6, 2015 China

Goldman Sachs Global Investment Research 13

2. China isn’t just selling toys and textiles, it is exporting high-

speed rail and nuclear technology

China is losing market share (in the US and EU) in low-value-added products (textiles, toys)

to other developing nations on compressing cost advantage but it is still grabbing global

(and domestic) market shares in higher value-added goods, notably consumer electronics

and industrial equipment.

Looking ahead, we see China moving further up the value-added curve, with

transportation (high-speed rail), telecommunication, power-related (nuclear and coal-fire)

infrastructure equipment/technology potentially being the emerging exports growth drivers

given China’s rising R&D intensity and structural policy tailwinds (the ‘one-belt, one-road’

strategy).

Exhibit 19: China’s aggregate market shares in the US

and EU have remained stable

Exhibit 20: China has actually gained market shares in

the high-end tech products

Source: CEIC.

Source: CEIC, OECD, Goldman Sachs Global Investment Research.

Exhibit 21: China isn’t just selling toys and textiles, it is exporting power equipment and

high-end machinery

Source: CEIC.

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

Ju

n-0

6

Ju

n-0

7

Ju

n-0

8

Ju

n-0

9

Ju

n-1

0

Ju

n-1

1

Ju

n-1

2

Ju

n-1

3

Ju

n-1

4

Ju

n-1

5China Japan MalaysiaMexico Korea Taiwan

Indonesa

Market share in exports to the US and EU (non-energy, non-

materials) (indexed to May 2006)

0%

10%

20%

30%

40%

Dec-0

1

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Dec-1

3

Dec-1

4

lowest tech

medium-low tech

medium-high tech

high tech

China's market share in the US and EU by tech intensity

(12m moving avg)

42.8

39.97.5

9.7

2

3

4

5

6

7

8

9

10

20

25

30

35

40

45

50

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Miscellaneous Articles (incl. toys,

footwear, textiles)

Power Machinery & Equip - RHS

China as % of total US + EU imports(%) (%)

November 6, 2015 China

Goldman Sachs Global Investment Research 14

3. China is still consuming commodities, but more ‘opex’ less ‘capex’

In their recent pieces, our commodity strategists decompose commodities into ‘capex’ and

‘opex’ categories. Capex commodities are used in heavy industry to create infrastructure

and the foundations of an economy; they include iron ore, coking coal, steel, cement and,

to a lesser extent, copper. In contrast, opex commodities are consumed to keep the

economy operating and include oil, natural gas, nickel (stainless steel) and aluminum

(packaging). In other words, buildings are constructed with capex commodities, but are

maintained—heated and cooled—with opex commodities.

Based on this classification, our commodity strategists find that the more investment- or

capex-intensive the commodity, the weaker the demand growth, and the more consumer-

or opex-intensive the commodity, the stronger the demand growth. For example, demand

is declining by 5.0% yoy for cement, a highly investment-intensive commodity, while

demand for gasoline, an extremely consumer-intensive commodity, is growing at 17.4%

yoy. This demand pattern suggests that the much-talked rebalancing is also underway in

the ‘old economy’ space.

See Commodities Research: What China’s rebalancing means for commodities, Oct 12.

Exhibit 22: The demand between opex and capex commodities is also a strong statement

of the rebalancing

Source: IEA, WoodMackenzie, CRU, USDA, Goldman Sachs Global Investment Research.

4. Consumption is a secular theme, but with many facets

So far, our top-down economic expectations and arguments suggest that consumption/

services could be a secular and compelling macro theme in China for years to come;

however, we acknowledge that consumption is a broad concept and not all consumption

items may fare well in the ‘new normal’.

For example, in Exhibit 23, we note significant growth variances among consumption

items ranging from necessities like food and clothes to discretionary spending on

entertainment and travel.

-10 -5 0 5 10 15 20

Cement

Thermal Coal

Steel

Iron Ore

Met Coal

Wheat*

Cotton*

Copper

Corn*

Sugar*

Diesel

Naptha

Oil (total)

Nickel**

Coffee*

Soybean*

Aluminium

Zinc***

Kerosene

Gasoline

Op

Ex

co

mm

od

itie

Ca

pE

x

co

mm

od

itie

s

*Est. 2015 annual consumption growth (no monthly data) ; **calculated from apparent Stainless

Steel demand; ***calculated from zinc galv. production

China consumption growth

2015 ytd (% yoy)

November 6, 2015 China

Goldman Sachs Global Investment Research 15

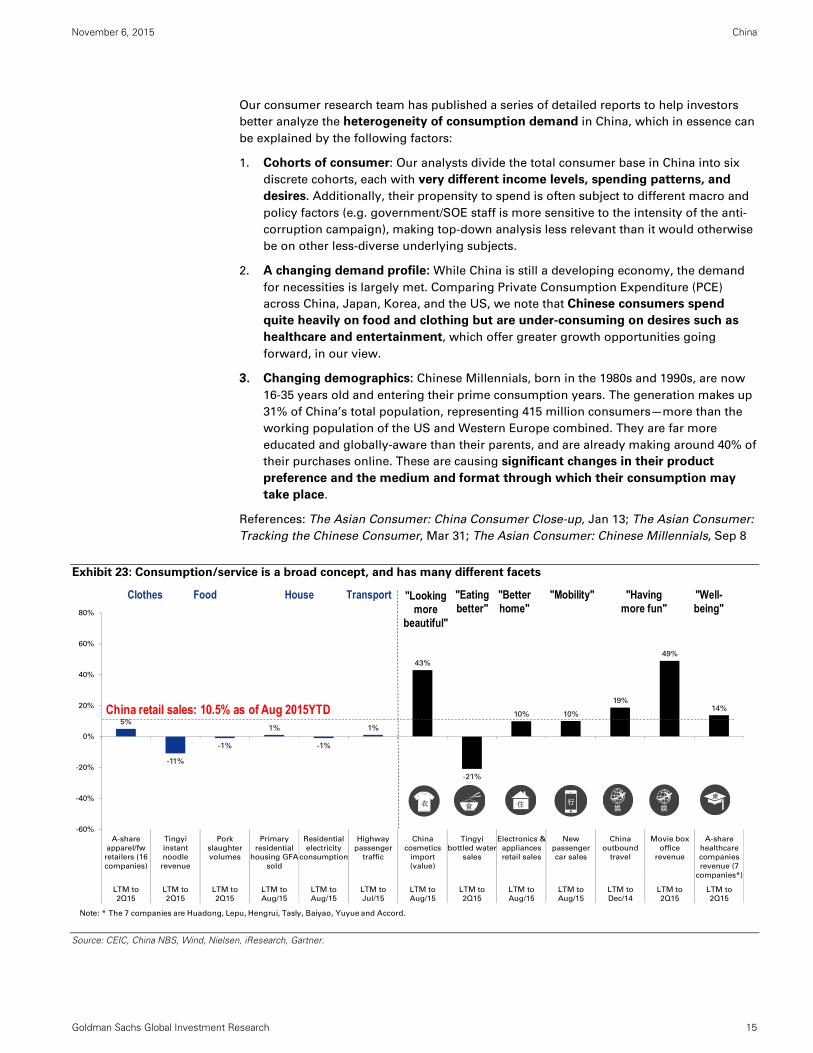

Our consumer research team has published a series of detailed reports to help investors

better analyze the heterogeneity of consumption demand in China, which in essence can

be explained by the following factors:

1. Cohorts of consumer: Our analysts divide the total consumer base in China into six

discrete cohorts, each with very different income levels, spending patterns, and

desires. Additionally, their propensity to spend is often subject to different macro and

policy factors (e.g. government/SOE staff is more sensitive to the intensity of the anti-

corruption campaign), making top-down analysis less relevant than it would otherwise

be on other less-diverse underlying subjects.

2. A changing demand profile: While China is still a developing economy, the demand

for necessities is largely met. Comparing Private Consumption Expenditure (PCE)

across China, Japan, Korea, and the US, we note that Chinese consumers spend

quite heavily on food and clothing but are under-consuming on desires such as

healthcare and entertainment, which offer greater growth opportunities going

forward, in our view.

3. Changing demographics: Chinese Millennials, born in the 1980s and 1990s, are now

16-35 years old and entering their prime consumption years. The generation makes up

31% of China’s total population, representing 415 million consumers—more than the

working population of the US and Western Europe combined. They are far more

educated and globally-aware than their parents, and are already making around 40% of

their purchases online. These are causing significant changes in their product

preference and the medium and format through which their consumption may

take place.

References: The Asian Consumer: China Consumer Close-up, Jan 13; The Asian Consumer:

Tracking the Chinese Consumer, Mar 31; The Asian Consumer: Chinese Millennials, Sep 8

Exhibit 23: Consumption/service is a broad concept, and has many different facets

Source: CEIC, China NBS, Wind, Nielsen, iResearch, Gartner.

5%

-11%

-1%

1%

-1%

1%

43%

-21%

10% 10%

19%

49%

14%

-60%

-40%

-20%

0%

20%

40%

60%

80%

A-share

apparel/fw

retailers (16

companies)

Tingyi

instant

noodle

revenue

Pork

slaughter

volumes

Primary

residential

housing GFA

sold

Residential

electricity

consumption

Highway

passenger

traffic

China

cosmetics

import

(value)

Tingyi

bottled water

sales

Electronics &

appliances

retail sales

New

passenger

car sales

China

outbound

travel

Movie box

office

revenue

A-share

healthcare

companies

revenue (7

companies*)

LTM to

2Q15

LTM to

2Q15

LTM to

2Q15

LTM to

Aug/15

LTM to

Aug/15

LTM to

Jul/15

LTM to

Aug/15

LTM to

2Q15

LTM to

Aug/15

LTM to

Aug/15

LTM to

Dec/14

LTM to

2Q15

LTM to

2Q15

康行

娱住食衣

娱

China retail sales: 10.5% as of Aug 2015YTD

Clothes Food House "Eating better"

Transport "Mobility" "Havingmore fun"

"Well-being"

"Better home"

"Looking more

beautiful"

Note: * The 7 companies are Huadong, Lepu, Hengrui, Tasly, Baiyao, Yuyue and Accord.

November 6, 2015 China

Goldman Sachs Global Investment Research 16

Exhibit 24: Chinese consumers are already spending a lot on food and clothing, but under-spend on healthcare and

entertainment, which offer the greater growth opportunities going forward, in our view

Source: Euromonitor, CEIC, Goldman Sachs Global Investment Research.

0

1

2

3

4

5

6

7

8

9

10

Looking more

beautiful

Eating better Better home Mobility/connectivity Having more fun Well-being

China

Korea

Japan

US

PCE per capita (k US$, 2013)

0%

5%

10%

15%

20%

25%

30%

35%

Looking more

beautiful

Eating better Better home Mobility/connectivity Having more fun Well-being

China

Korea

Japan

US

As % of aggregate PCE per capita (%, 2013)

November 6, 2015 China

Goldman Sachs Global Investment Research 17

New framework for investing in Chinese equities

Drawbacks of the conventional top-down framework

1. In our view, widely-followed Chinese equity indexes are not a good proxy for the

Chinese economy. For instance, Financials account for 72%/33%/42% of

HSCEI/SCHOMP/MXCN index cap, vs. around 13% in value-added terms by GDP

accounting. Similarly, while the service sector (ex Financials) currently represents 35%

of the economy, the associated equity sectors (healthcare, consumer

discretionary/staples, and transportation) have a smaller weighting in the indexes. Due

to this fundamental mismatch, we would caution against the common practice of

extracting macro views from aggregate index performance.

2. Returns variation within each index has also risen, possibly reflecting the fundamental

divergences between ‘New’ and ‘Old’ China (more on this below). Indeed, indexes

with higher ‘New China’ weightings have performed well in the past three years,

reinforcing the argument that deriving macro views from equity indexes could lead to

markedly different conclusions.

3. Investors often trade and formulate their views on Chinese equities based on ‘Old

China’ oriented indicators, such as IP and manufacturing PMI. We concur that these

indicators still provide useful signals in the industrial/manufacturing part of the

economy, but they may not offer a comprehensive macro view as they did in the past

given the rising GDP shares of consumption and other emerging industries.

Exhibit 25: We don’t think the commonly-followed Chinese equity indexes are good

representation of the underlying economy

Source: CEIC, Goldman Sachs Global Investment Research.

9%

7%

36%

10%

13%

5%

20%

0%

20%

40%

60%

80%

100%

2014 GDP

composition

TI - Others

TI - Transport

TI - Financials

TI - Wholesale

& Retail

SI - Industrials

SI -

Construction

PI

China GDP Composition

5% 3% 5%

11% 8%

14%

4%

9%

20%

42%

72%

33%

8% 12%

11%

5% 3% 9%

0%

20%

40%

60%

80%

100%

MXCN HSCEI SHCOMP

Cons Disc

Cons Stap

Energy

Financials

Health Care

Industrials

IT

Materials

Telecom

Utilities

Index sector weight

November 6, 2015 China

Goldman Sachs Global Investment Research 18

Exhibit 26: US equity index seems to be a reasonable proxy for the US economy

Note: Consumers include Wholesale and retail trade, professional services, recreation and other services; Industrials include manufacturing and transportation

Source: CEIC, Goldman Sachs Global Investment Research.

Exhibit 27: Investors have been trading HSCEI based on

IP momentum until recently

Exhibit 28: Indexes with high ‘New China’ content have

generally performed well, although with high volatility

Source: Bloomberg, NBS, Goldman Sachs Global Investment Research.

Source: Bloomberg, FactSet, Goldman Sachs Global Investment Research.

Exhibit 29: Return variances have been high in both offshore and onshore markets, partly reflecting the divergent

fundamental trends among various economic groups

Source: FactSet, Goldman Sachs Global Investment Research.

Source: FactSet, Goldman Sachs Global Investment Research.

3%

21%

10%

15%

16%

7%

10%

14%

0%

20%

40%

60%

80%

100%

GICS sector

Cons Disc

Cons Stap

Energy

Financials

Health Care

Industrials

IT

Materials

Telecom

Utilities

MXUS sector weight

13%

5%

15%

8%

20%

3%

30%

0%

20%

40%

60%

80%

100%

2014 GDP

composition

Consumers

Mining

Financials

Education &

Health CareIndustrials

Information

Construction

Utilities

Agriculture

US GDP composition

0

4

8

12

16

20

6000

8000

10000

12000

14000

16000

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Dec-1

3

Dec-1

4

Dec-1

5

HSCEI index

IP growth (qoq ann)

HSCEI index IP growth (qoq ann, %)

-10%

0%

10%

20%

30%

40%

50%

60%

12% 16% 20% 24% 28% 32%

3-y

ear

retu

rn C

AG

R (

Lo

c)

Annualized volatility (3-year daily return)

Bubble size represents New

China as % of Index Cap

MXCN

MXCN

(+ADRs)

HSCEI

SZCOMP

SHCOMP

Chi-

next

CSI300

China

ADRs

HSI

A50

Note: We use MXOCN for China ADRs

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Ma

y-1

1

Au

g-1

1

No

v-1

1

Fe

b-1

2

Ma

y-1

2

Au

g-1

2

No

v-1

2

Fe

b-1

3

Ma

y-1

3

Au

g-1

3

No

v-1

3

Fe

b-1

4

Ma

y-1

4

Au

g-1

4

No

v-1

4

Fe

b-1

5

Ma

y-1

5

Au

g-1

5

Rolling12M ReturnsIndex Constituent Return (+/- 1SD)

MXCN Index

-3%

+1SD: 24%

-1SD: -31%

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

Ma

y-1

1

Au

g-1

1

No

v-1

1

Fe

b-1

2

Ma

y-1

2

Au

g-1

2

No

v-1

2

Fe

b-1

3

Ma

y-1

3

Au

g-1

3

No

v-1

3

Fe

b-1

4

Ma

y-1

4

Au

g-1

4

No

v-1

4

Fe

b-1

5

Ma

y-1

5

Au

g-1

5

Rolling12M ReturnsIndex Constituent Return (+/- 1SD)

CSI 300 Index

41%

+1SD: 83%

-1SD: -1%

November 6, 2015 China

Goldman Sachs Global Investment Research 19

Our top-down framework for identifying ‘New China’

Given the constraints described above, and the need for a more systematic recognition of

the economic transformation, we enhance our ‘New China’ analytical framework based on

the following approach/logic (also see China Strategy: China FAQs, Sep 7):

1. Leveraging the financial database we compiled in our report: China Strategy: Key

micro trends in a macro-driven market, Sep 25, we aggregate 3,636 listed Chinese

companies (A, H, and ADRs) and organize them according to their GICS-4 sub-

industries (143 in total), the most granular industry level based on MSCI sector

classification.

2. We then group the sub-industries which have generated at least 10% revenue growth

since 2012 (i.e. FY2012, 2013, 2014). We prefer revenue growth over earnings growth

as the former appears a better proxy for underlying demand and is less subject to

industry competition and capital structure differences which impact earnings. This

procedure results in 52 sub-industries.

3. Then, we run correlation analysis to further screen for sub-industries which have

exhibited low revenue growth correlation with GDP growth, with an implicit view

that these sub-industries have been able to deliver consistently high top-line growth on

untapped and new demand despite the economic slowdown and policy cyclicality—the

essence of ‘New China’. This gives us 30 sub-industries which form our ‘New China’

universe, after eliminating those with insignificant number of companies and market

cap, and special revenue recognition accounting (e.g. property developers). For the

sub-industries which don’t fall into the ‘New China’ group, we put them in the ‘Old

China’ bucket.

Exhibit 31 shows the sectoral composition of our ‘New China’ universe, which comprises

671 companies (18% of total) with an aggregate market cap of US$1.8tn (21% of total),

across the A, H, and ADR markets.

In fundamental terms, ‘New China’ managed to grow top-line and bottom-line by 35%

and 47% respectively in 1H15 despite investors’ prevalent concerns about China macro.

At the other side of the spectrum, revenue growth for ‘Old China’ was essentially flat in

1H15, although slight margin expansion (mostly from Financials due to the buoyant stock

markets in 1H) helped lift earnings growth to 7%.

Valuation-wise, ‘New China’ trades at much higher absolute valuations than ‘Old China’ but

the valuation premiums look less discomforting when the former’s earnings growth

potential is put into perspective: ‘New China’ is trading at 1.1X PEG, vs. 1X of ‘Old

China’.

These attributes have led to strong outperformance of ‘New’ vs. ‘Old’: Over the past 3/5

years, ‘New China’ has rallied 126%/97%, while ‘Old China’ has gained 55%/18% vs.

benchmark (MSCI All China) of 35%/30%. See comparison on other fundamental metrics

in the Appendix.

Exhibit 30: Our top-down logic and process to identify ‘New China’ sectors and stocks

Source: Goldman Sachs Global Investment Research.

• 3636 companies

• US$8.7tn mkt

cap

• 143 GICS sub-

industries

2012,13,14 revenue growth ≥ 10%

≥ 2 companies in a sub-industry

Correlation between 2011-1H15 revenue growth and real GDP growth ≤ 54% (median of 143 sub-industries)

• 1113

companies

• US$3.7tn

mkt cap

• 52 GICS

sub-

industries

• 885

companies

• US$2.3tn mkt

cap

• 35 GICS sub-

industries

• 671 companies

• US$1.8tn mkt

cap

• 30 GICS sub-

industries

November 6, 2015 China

Goldman Sachs Global Investment Research 20

Exhibit 31: We form our ‘New China’ universe based on the following sub-industries

Source: FactSet, Goldman Sachs Global Investment Research.

Exhibit 32: ‘New China’ has significantly outperformed ‘Old China’ at both top- and bottom-line levels

Source: Bloomberg, Wind, MSCI, Goldman Sachs Global Investment Research.

Exhibit 33: ‘China New’ trades at much higher absolute

valuations than ‘Old China’....

Exhibit 34: ...but the valuation premiums look more

moderate when forward growth is taken into account

Note: f-PEG = forward 12-month PE / second 12-month EPS growth

Source: FactSet, I/B/E/S, Goldman Sachs Global Investment Research.

Source: FactSet, I/B/E/S, Goldman Sachs Global Investment Research.

GICS sector

Cable & Satellite Internet Retail

Education Services Movies & Entertainment

Consumer Staples Drug Retail Household Products

EnergyOil & Gas Equipment &

Services

Asset Management & Custody

BanksProperty & Casualty Insurance

Consumer Finance Real Estate Services

Life & Health Insurance

Biotechnology Health Care Technology

Health Care Distributors Life Sciences Tools & Services

Health Care Equipment Pharmaceuticals

Health Care Services

Aerospace & DefenseHuman Resource &

Employment Services

Diversified Support Services Trucking

Environmental & Facilities

Services

Electronic Equipment &

InstrumentsIT Consulting & Other Services

Internet Software & Services Systems Software

Telecom Alternative Carriers

Utilities Water Utilities

Consumer Discretionary

Health Care

Industrials

Information Technology

GICS sub-industry

Financials

3% 4%5%

10%

37% 7%

7%

20%

25%

15%

29%

2%

8%

6%

8% 12%

0%

20%

40%

60%

80%

100%

New China Old China

Cons Disc

Cons Stap

Energy

Financials

Health Care

Industrials

Tech

Materials

Telecom

Utilities

Sector weight

47%

7%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

2006

2007

2008

2009

2010

2011

2012

2013

2014

1H

15

New China

Old China

Earnings growth (yoy)

35%

0%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2006

2007

2008

2009

2010

2011

2012

2013

2014

1H

15

New China Old China

Revenue growth (yoy)

25

12

5

10

15

20

25

30

35

Ja

n-1

0

Ju

n-1

0

No

v-1

0

Ap

r-1

1

Sep

-11

Fe

b-1

2

Ju

l-1

2

De

c-1

2

Ma

y-1

3

Oct-

13

Ma

r-14

Au

g-1

4

Ja

n-1

5

Ju

n-1

5

New China

Old China

Market cap-weighted f-P/E (x)

1.1

1.0

0.5

0.7

0.9

1.1

1.3

Jan

-10

Ju

n-1

0

No

v-1

0

Ap

r-1

1

Sep

-11

Feb

-12

Ju

l-12

Dec-1

2

May-1

3

Oct-

13

Mar-

14

Au

g-1

4

Jan

-15

Ju

n-1

5

New China

Old China

Market cap-weighted f-PEG (x)

November 6, 2015 China

Goldman Sachs Global Investment Research 21

Improving risk/reward: Our select 19 New China ideas

While we believe our ‘New China’ universe provides a sensible hunting ground for long-

term investment opportunities, we also acknowledge that high valuations and risks about

profitability normalization, which is common for emerging industries due to lower entry

barrier and intensifying competition, have historically deterred investors from this

attractive macro story.

As such, we add two qualifiers—valuation and profitability—to our ‘New China’ universe

to improve our implementation strategy. Specifically, we further narrow the universe by

selecting stocks which fulfill the following criteria:

a. At least 10% revenue and earnings CAGR from 2015 to 2017;

b. At least 10% average ROE from 2015 to 2017;

c. Price-to-earnings-growth (PEG) ratio below 1.5;

d. Average 2015-2017 ROE not higher than 10pp above global comps (based on MSCI

All Country World index constituents);

e. Non Sell-rated by GS/GH analysts (i.e. rated Buy or Neutral).

We believe these considerations should help reduce the risk of buying ‘New China’

stocks at unsustainably high valuations at peak profitability, which would have

‘double-whammy’ impact on returns when growth starts to normalize.

These parameters yield 19 names, 10 in offshore and 9 in onshore markets, and based on a

back-test have resulted in greater outperformance vs. the broad ‘New China’ universe and

‘Old China’ (see Exhibit 35).

Conviction Buy names include: Shanghai Fosun Pharma (A), and PingAn (A). Names that

are not under GS/GH coverage are shown in the Appendix.

Exhibit 35: ‘New China’ has meaningfully outperformed ‘Old China’

Source: FactSet, MSCI, Goldman Sachs Global Investment Research.

236

197

130

118

50

100

150

200

250

300

Ja

n-1

0

May-1

0

Se

p-1

0

Ja

n-1

1

May-1

1

Se

p-1

1

Ja

n-1

2

May-1

2

Se

p-1

2

Ja

n-1

3

May-1

3

Se

p-1

3

Ja

n-1

4

May-1

4

Se

p-1

4

Ja

n-1

5

May-1

5

Se

p-1

5

Select New China names (19 stocks)

New China

MSCI All China Index

Old China

Market cap-weighted price returns

November 6, 2015 China

Goldman Sachs Global Investment Research 22

Index users: Choose your ‘New’ indexes

The return profile (risk and return) is substantially different among key Chinese

equity indexes. For example, HSCEI has lost 3% in the past three years, while at the

other extreme ChiNext has rallied 268% during the same period.

The strong returns variations (and the extent of multiple expansion) seem positively

correlated with the index weighting of ‘New China’, which ultimately reflects the

earnings growth differentials among these indexes. These observations reinforce our

view that:

1. Strategically, MSCI China should continue to outperform HSCEI in the offshore

market given the former’s higher exposure in ‘New China’, especially after the

ADRs inclusion to the MSCI universe which will begin in mid-November. See

China Musings: Q&As on ADRs inclusion in MSCI, Oct 23;

2. In similar vein, we believe the fundamental outlook for SZCOMP and ChiNext is

more promising than SHCOMP or A50, although the high valuation premiums of

the former two over the ‘Old China’ indexes have complicated the expected return

function. As such, CSI300 looks like a more balanced index considering its

relatively high ‘New China’ weighting than SHCOMP and A50, but more moderate

valuation profile compared with SZCOMP and ChiNext.

Exhibit 36: Chinese equity indexes have delivered

markedly different returns...

Exhibit 37: ...with the ones with higher ‘New China’

weighting seeing higher PE expansion and returns

Source: Bloomberg, Goldman Sachs Global Investment Research.

Source: Bloomberg, Goldman Sachs Global Investment Research.

Exhibit 38: We think MSCI China and CSI300 offer a more balance growth and valuation trade-off to investors

Source: Bloomberg, FactSet, Goldman Sachs Global Investment Research.

268%

142%

94%63% 57%

41%

5% 4%

-3%-50%

0%

50%

100%

150%

200%

250%

300%

-50%

0%

50%

100%

150%

200%

250%

300%

Ch

ine

xt

SZ

CO

MP

CN

AD

Rs

SH

CO

MP

CS

I 3

00

A5

0

MX

CN

HS

I

HS

CE

I

Price Performance

Forward EPS change

Forward P/E change

% change % changeReturn decomposition, past 3 years

-10%

-5%

0%

5%

10%

15%

20%

25%

0% 5% 10% 15% 20% 25% 30% 35%

f-P

/E C

han

ge

(3

-yr

CA

GR

)

Forward EPS growth (3-year CAGR)

Bubble size represents New

China as % of Index Cap

MXCN

HSCEI

SZCOMP

SHCOMP

Chi-

next

CSI300

China

ADRs

HSIA50

Note: We use MXOCN for China ADRs

0

20

40

60

80

100

5

10

15

20

25

30

35

40

45

Ch

inex

t

CN

AD

Rs

SZ

CO

MP

SH

CO

MP

CS

I 3

00

HS

I

MX

CN

A5

0

HS

CE

I

2016E P/E (X) (LHS)

New China proportion (%) (RHS)

16E P/E (X) (%)

Note: we use MXOCN for China ADRs

0

20

40

60

80

100

0.5

0.7

0.9

1.1

1.3

1.5

Ch

inex

t

SZ

CO

MP

CS

I 3

00

SH

CO

MP

HS

I

A50

CN

AD

Rs

MX

CN

HS

CE

I

2016E PEG ratio (X) (LHS)

New China proportion (%) (RHS)

16E PEG ratio (X) (16E PE/ 17E EPSg) (%)

Note: we use MXOCN for China ADRs

November 6, 2015 China

Goldman Sachs Global Investment Research 23

Global funds/corporates: Adaptability is the key to success

The changing Chinese growth dynamics are impacting the way that global

corporates are doing business in China, and global funds which invest in these

companies. Indeed, from a macro perspective, China has become an important final-

demand destination for many economies globally.

But, selling into China isn’t as easy as in the past: Local firms are gaining market

share in a number of consumer/industrial products at the expense of foreign brands.

We attribute this to: a) rising local technological capability on strong R&D inputs; b)

greater focus by local firms on building brands to defend margins; c) better

understanding of customer needs; and d) more flexible selling/distribution channels

thanks to the proliferation of e-commerce (e.g. Xiaomi sells its smartphones online).

The situation isn’t gloomy for all foreign brands, notably in personal consumption

areas where Japanese/Western beer brands are outperforming domestic ones, H&M,

Uniqlo, Nike, Starbucks, and Korean cosmetic brands are still logging robust revenue

growth, although luxury retailers, global fast food chains, high-end hotels, and dairy

companies have been struggling. These micro data-points suggest that:

1. The classic EM story—low per capita income, low product penetration, high

pent-up demand—has largely played out in China. This means business

strategy relying on untapped demand and perception arbitrage (foreign brand

image) is probably outdated.

2. Global companies with strong brand equity, unique product offering and value

proposition, and those which target the right consumer cohorts with the right

products should have a higher likelihood of success.

Exhibit 39: China is an important end-customer for many

Asian and EM countries

Exhibit 40: Local players have gained market share in a

number of consumer and industrial products

Source: CEIC, Haver, Goldman Sachs Global Investment Research. Source: Gartner, Shangshi Consulting, GS Global Investment Research.