netw rks - pc\|macimages.pcmac.org/sisfiles/schools/al/mobilecounty/dunbarmiddle... · satisfy all...

TRANSCRIPT

NAME DATE CLASS

Copyright © The M

cGraw

-Hill Com

panies, Inc.

netw rks

ESSENTIAL QUESTIONSWhy and how do people make economic choices?How do economic systems influence societies?

GUIDING QUESTIONS1. What is scarcity, and how does it affect economic choices?

2. What determines how societies make economic choices?

Terms to Knowwant things people would like to haveresource anything that can be used to make goods or serviceseconomics the study of how people use limited resources to satisfy unlimited wantsscarcity not having enough resources to satisfy all one’s needs and wantsindividual a persondistribute to delivereconomic system a nation’s way of producing the things its people want and need

traditional economy an economic system in which major economic decisions are based on custom or habitmarket economy an economic system in which people and businesses own all resources and make economic decisions on the basis of pricecommand economy an economic system in which the government makes the major economic decisionsmixed market economy an economy in which businesses and individuals make the major economic decisions but in which the government also plays a role

What Do You Know?In the first column, answer the questions based on what you know before you study. After this lesson, complete the last column.

Now... Later...

How do people fill their wants and needs when there are not enough resources?

What are economic choices?

Lesson 1: What Is Economics?

Our Wants and ResourcesWhen people shop, they often want to buy more than they can afford. For example, Jayna is shopping for a new dress. She finds a dress she likes, but she also sees a sweater she wants. She does not have enough money to buy both.

Jayna must decide how best to use her money to satisfy her wants. Wants are desires that can be met by getting a product or a service. Most of us want many things. In fact, our wants are almost without limit.

Vocabulary 1. What are wants?

Introduction to Economics

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

198

198_201_BCCE_RESG_C16_L1_660008.indd Page 198 24/05/11 7:29 PM s-087198_201_BCCE_RESG_C16_L1_660008.indd Page 198 24/05/11 7:29 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME _______________________________________ DATE _______________ CLASS _________

Copy

righ

t © T

he M

cGra

w-H

ill C

ompa

nies

, Inc

.netw rks

Examining Details

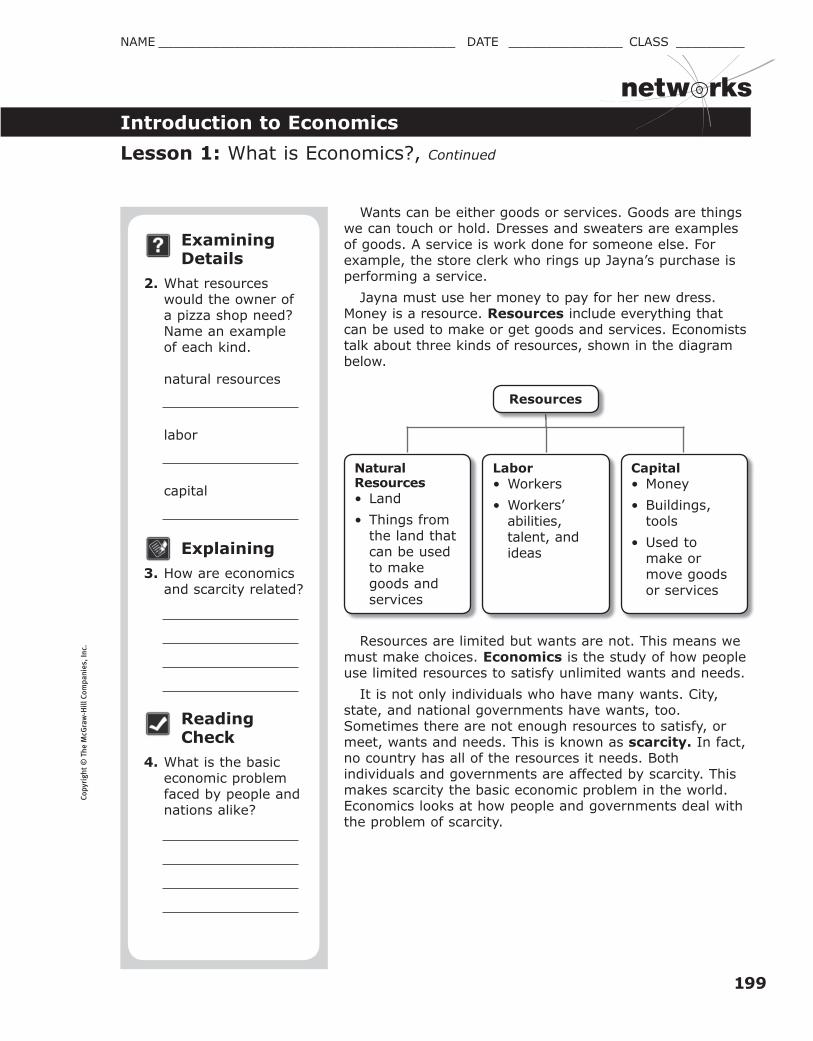

2. What resources would the owner of a pizza shop need? Name an example of each kind.

natural resources

labor

capital

Explaining3. How are economics

and scarcity related?

Reading Check

4. What is the basic economic problem faced by people and nations alike?

Wants can be either goods or services. Goods are things we can touch or hold. Dresses and sweaters are examples of goods. A service is work done for someone else. For example, the store clerk who rings up Jayna’s purchase is performing a service.

Jayna must use her money to pay for her new dress. Money is a resource. Resources include everything that can be used to make or get goods and services. Economists talk about three kinds of resources, shown in the diagram below.

Natural Resources• Land

• Things from the land that can be used to make goods and services

Labor• Workers

• Workers’ abilities, talent, and ideas

Capital• Money

• Buildings, tools

• Used to make or move goods or services

Resources

Resources are limited but wants are not. This means we must make choices. Economics is the study of how people use limited resources to satisfy unlimited wants and needs.

It is not only individuals who have many wants. City, state, and national governments have wants, too. Sometimes there are not enough resources to satisfy, or meet, wants and needs. This is known as scarcity. In fact, no country has all of the resources it needs. Both individuals and governments are affected by scarcity. This makes scarcity the basic economic problem in the world. Economics looks at how people and governments deal with the problem of scarcity.

Introduction to Economics

Lesson 1: What is Economics?, Continued

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

199

198_201_BCCE_RESG_C16_L1_660008.indd Page 199 21/05/11 8:53 PM s-087198_201_BCCE_RESG_C16_L1_660008.indd Page 199 21/05/11 8:53 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME DATE CLASS

Copyright © The M

cGraw

-Hill Com

panies, Inc.

netw rks

5. Place a two-tab Foldable along the dotted line. Label the anchor tab Economics. Label the two tabs Limited and Unlimited. Use both sides of the tabs to explain what you know about limited resources and unlimited wants.

Reading Check

6. What determines the kind of economy a nation has?

Explaining7. What must a society

consider when deciding what goods and services to produce?

Mark the Text8. Underline the words

that tell you the meaning of economic system.

Glue Foldable here

What Creates Scarcity

Limited Unlimited wants Scarcityresources and needs

Societies and Economic ChoicesIndividuals, or people, make economic choices all the time. So do countries. Nations must decide how to use their limited resources in the best way to care for and protect their citizens. For example, a government must decide whether it will spend more money on health care or defense, education or the environment. The scarcity of resources forces societies to make these types of choices.

These choices can be summed up by three basic questions:

1. What goods and services will be produced?

2. How will the goods and services be produced?

3. Who will consume, or use, goods and services?

What goods and services will be produced? For example, should a piece of land be used for farming or to build an airport? It cannot be used for both. Should a government improve roads or build schools? To decide such questions societies must think about their resources. A nation with good soil and a long growing season might use much of its land to grow crops.

How will goods and services be produced? For example, should food be produced on big factory farms or small family farms?

Who will get the goods and services? Societies must decide who gets goods and how much people can have. They have different ways of distributing goods. Should new cars go to public officials or to the highest bidder? Should new housing units be reserved for low-income people or should they be available to anyone?

Societies answer these questions in different ways. Every country has its own economic system, or way of producing the things people want and need.

Introduction to Economics

Lesson 1: What is Economics?, Continued

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

200

198_201_BCCE_RESG_C16_L1_660008.indd Page 200 24/05/11 7:32 PM s-087198_201_BCCE_RESG_C16_L1_660008.indd Page 200 24/05/11 7:32 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME _______________________________________ DATE _______________ CLASS _________

Copy

righ

t © T

he M

cGra

w-H

ill C

ompa

nies

, Inc

.netw rks

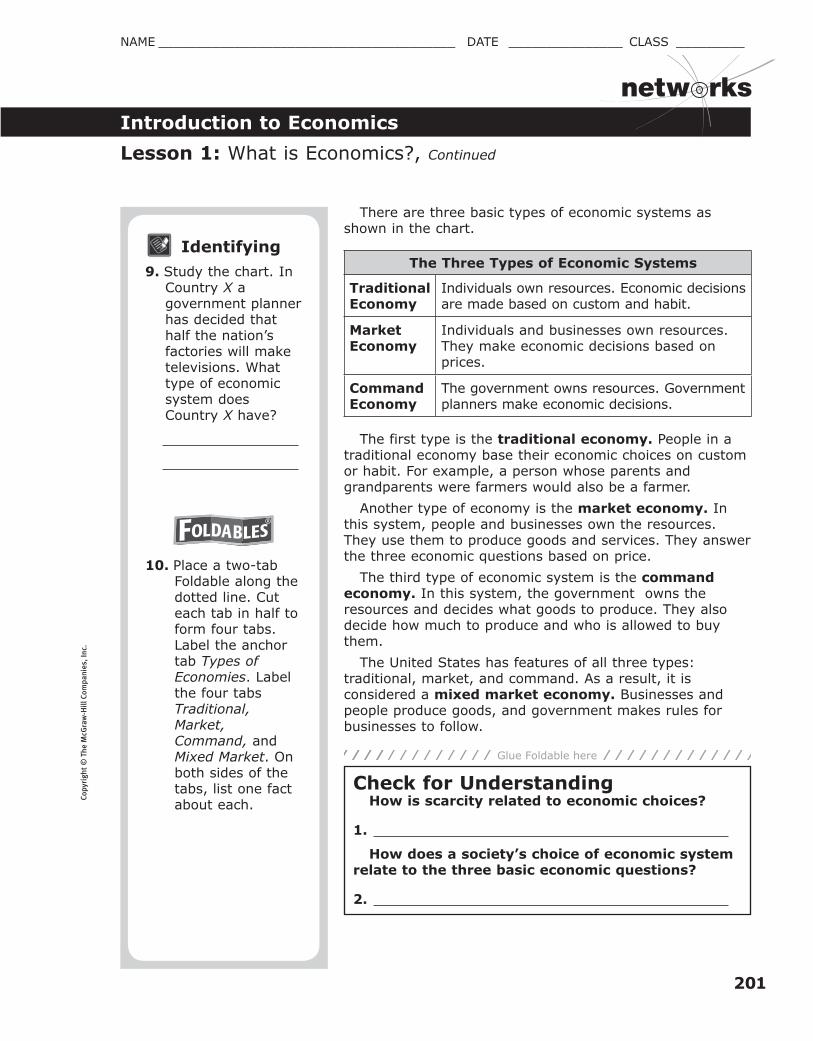

There are three basic types of economic systems as shown in the chart.

The Three Types of Economic Systems

Traditional Economy

Individuals own resources. Economic decisions are made based on custom and habit.

Market Economy

Individuals and businesses own resources. They make economic decisions based on prices.

Command Economy

The government owns resources. Government planners make economic decisions.

The first type is the traditional economy. People in a traditional economy base their economic choices on custom or habit. For example, a person whose parents and grandparents were farmers would also be a farmer.

Another type of economy is the market economy. In this system, people and businesses own the resources. They use them to produce goods and services. They answer the three economic questions based on price.

The third type of economic system is the command economy. In this system, the government owns the resources and decides what goods to produce. They also decide how much to produce and who is allowed to buy them.

The United States has features of all three types: traditional, market, and command. As a result, it is considered a mixed market economy. Businesses and people produce goods, and government makes rules for businesses to follow.

Identifying9. Study the chart. In

Country X a government planner has decided that half the nation’s factories will make televisions. What type of economic system does Country X have?

10. Place a two-tab Foldable along the dotted line. Cut each tab in half to form four tabs. Label the anchor tab Types of Economies. Label the four tabs Traditional, Market, Command, and Mixed Market. On both sides of the tabs, list one fact about each.

Introduction to Economics

Lesson 1: What is Economics?, Continued

Check for UnderstandingHow is scarcity related to economic choices?

1.

How does a society’s choice of economic system relate to the three basic economic questions?

2.

Glue Foldable here

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

201

198_201_BCCE_RESG_C16_L1_660008.indd Page 201 21/05/11 8:53 PM s-087198_201_BCCE_RESG_C16_L1_660008.indd Page 201 21/05/11 8:53 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME DATE CLASS

Copyright © The M

cGraw

-Hill Com

panies, Inc.

netw rks

ESSENTIAL QUESTIONSWhy and how do people make economic choices?How do economic systems influence societies?

GUIDING QUESTIONS1. Why are trade-offs important in making economic decisions?

2. How do costs and revenues influence economic decision making?

Terms to Knowoption a choice or alternativetrade-off giving up one option in order to get something of greater valueopportunity cost the loss of the next-best option when choosing to do one thing or anotherfixed cost an expense that does not change no matter how much a business producesvariable cost an expense that changes depending on how much a business producesvary to change

total cost the sum of all fixed and variable costsmarginal cost the additional expense of producing one more unit of somethingrevenue the money a business gets from selling a good or servicemarginal revenue the additional income received from selling one more unit of somethingbenefit-cost analysis a comparison of the costs and benefits of a decision

What Do You Know? In the first column, answer the questions based on what you know before you study. After this lesson, complete the last column.

Now... Later...

What is a trade-off?

Lesson 2: Economic Decisions

Trade-OffsWhen you make a choice between two things you want to buy, you are making an economic decision. To make a good decision, you must think about the benefits and costs of each choice.

Once you choose you give up one option in favor of a better one. This is called a trade-off. Suppose you turn down a night out with friends in order to study for a test. You have made a trade-off with your time.

Businesses and governments also make trade-offs. A town might have to choose between building a new school or a new road. Trade-offs are made when money, time, and other resources are limited.

Reading Check

1. What is a trade-off in an economic decision?

Introduction to Economics

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

202

202_205_BCCE_RESG_C16_L2_660008.indd Page 202 24/05/11 7:34 PM s-087202_205_BCCE_RESG_C16_L2_660008.indd Page 202 24/05/11 7:34 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME _______________________________________ DATE _______________ CLASS _________

Copy

righ

t © T

he M

cGra

w-H

ill C

ompa

nies

, Inc

.netw rks

Prior Knowledge

2. Why might governments have to make more trade-offs when economic times are hard?

Drawing Conclusions

3. What does it say about your choice if the opportunity cost is more valuable than your choice?

Vocabulary4. What is revenue?

Explaining5. Why would the cost

of labor and supplies go up if Joe’s stays open longer?

In making a trade-off, a person chooses one option over all others. The next-best use of your time or money when you choose to do one thing over another is called opportunity cost. For example, when you chose to study you gave up the chance to visit friends. Your opportunity cost is the fun you would have had with your friends.

Choices made by businesses and governments also have opportunity costs. A city might decide to spend money to improve a park rather than to fix sidewalks. The opportunity cost is the sidewalks that do not get fixed.

Opportunity costs are not always measured in money or things. One example for a business is the work time that is lost while employees are trained in a new computer program. If the training will improve employees’ future work, then the opportunity cost is worthwhile.

Measuring Costs and RevenuesBusiness people have to make economic decisions every day. In order to better understand how those decisions are made, let us look at an example. Joe owns a restaurant called Joe’s Seafood Depot. It is open from four o’clock in the afternoon to ten o’clock at night. Joe wonders if his restaurant would make more money if he kept it open longer every day.

In order to find out if it will be profitable to stay open longer, Joe has to figure out his fixed costs and his variable costs. His fixed costs, like rent and insurance, will not increase if he stays open a few more hours. But his variable costs will vary, or change. His variable costs include the money he pays his workers, his electric and gas bills, and the supplies he uses to produce his product. His total costs for running the business are the sum of his fixed costs and his variable costs.

Before deciding how many hours longer he wants to stay open, Joe will figure out his marginal costs. Economists define marginal cost as the increase in expense caused by producing one more unit of something. In Joe's case this additional unit is staying open for one more hour.

Once Joe knows his costs for staying open later he has to decide if he can make enough revenue to pay the costs and still make a profit. Revenue is the money Joe's customers pay him when they eat in his restaurant. The chart on the next page shows both the marginal cost and the marginal revenue Joe expects to make for each added hour he keeps his restaurant open.

Introduction to Economics

Lesson 2: Economic Decisions, Continued

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

203

202_205_BCCE_RESG_C16_L2_660008.indd Page 203 27/05/11 4:07 PM s-50202_205_BCCE_RESG_C16_L2_660008.indd Page 203 27/05/11 4:07 PM s-50 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANCILLARY.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANCILLARY...

NAME DATE CLASS

Copyright © The M

cGraw

-Hill Com

panies, Inc.

netw rks

Examining Details

6. Study the chart. If Joe’s stays open for five extra hours, how much revenue will he make in the fifth hour? Should he stay open that long?

Examining Details

7. Look at the Marginal Cost column. How much does it cost Joe to stay open each hour?

Mark the Text 8. Circle the two things

that are compared in a benefit-cost analysis.

Reading Check

9. What two things are compared in a marginal analysis?

$30

Marginal Cost

$30

$30

$30

$30

$30

1

Added Hours

2

3

4

5

6

Marginal Revenue

$70

$60

$50

$40

$30

$20

Marginal Cost and Revenue for Joe’s Seafood Depot

Sometimes business people, like Joe, want to grow their business, serve more customers, and make more money. When trying to decide between different options, they will likely use a benefit-cost analysis. In Joe's case, he might be trying to decide if he should build an addition onto the Seafood Depot or perhaps open a second Seafood Depot in a neighboring town.

Benefit-cost analysis compares the size of the benefit with the size of the cost by dividing the two. This type of analysis helps businesses choose among two or more options. For example it will help a business choose between options A and B. If option A creates revenue of $100 at a cost of $80, the benefit-cost ratio is 1.25. We get the number 1.25 by dividing $100 by $80. If option B creates revenue of $150 and costs $90, the benefit-cost ratio is 1.67. In order to be profitable, businesses will choose the option with the higher benefit-cost number.

Business people also use another type of analysis to compare two options. It is called marginal analysis.Marginal analysis compares the additional benefit of doing something with its additional cost. If the additional benefit is greater than the additional cost, the choice is a good one.

Joe could use marginal analysis to help him decide how many more hours to stay open. Look at the Marginal Analysis For Joe's Seafood Depot graph on the next page. The graph shows that the marginal revenue of staying open one more hour is $70 and the marginal cost is $30. Because the benefit is greater than the cost, Joe will likely stay open at least one more hour and perhaps longer.

Introduction to Economics

Lesson 2: Economic Decisions, Continued

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

204

202_205_BCCE_RESG_C16_L2_660008.indd Page 204 24/05/11 7:36 PM s-087202_205_BCCE_RESG_C16_L2_660008.indd Page 204 24/05/11 7:36 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME _______________________________________ DATE _______________ CLASS _________

Copy

righ

t © T

he M

cGra

w-H

ill C

ompa

nies

, Inc

.netw rks

When looking at marginal analysis, the rule is to continue doing something until the marginal cost is equal to the marginal revenue. For Joe, they are equal at five hours. Costs and benefits both equal $30. Then benefits go down.

$0

$10

$20

$30

$40

$50

$60

$70

$80

1 2 3 4 6NUMBER OF ADDED HOURS OF OPERATION

5

KEYMarginal RevenueMarginal Cost

KEYenut

Marginal ReveMarginal Cost

Marginal Analysis for Joe’s Seafood Depot

Marginal analysis even works for decisions that are not about money. It can apply to a decision about how long a nap should be! The benefits of the nap are highest during the first hour. After that they gradually decline.

The cost of taking a nap would be the opportunity cost of what you were not doing while you napped. The ideal length of your nap is the point at which the declining benefits equal the rising costs.

Analyzing 10. Examine the key

on the Marginal Analysis for Joe's Seafood Depot graph. What two things are being graphed? Explain what happens when the two lines cross.

11. Place a two-tab Foldable along the dotted line. Cut each tab in half to form four tabs. Write the title Costs and Revenues on the anchor tab. Label the four tabs Fixed Costs, Variable Costs, Total Cost, Marginal Cost. Write the definition of each on the reverse side of the tabs. G

lue

Fold

able

her

e

Introduction to Economics

Lesson 2: Economic Decisions, Continued

Check for UnderstandingHow are trade-offs and opportunity costs related?

1.

Why is it important for a business to analyze costs and revenues before deciding to expand?

2.

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

205

202_205_BCCE_RESG_C16_L2_660008.indd Page 205 21/05/11 8:54 PM s-087202_205_BCCE_RESG_C16_L2_660008.indd Page 205 21/05/11 8:54 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME DATE CLASS

Copyright © The M

cGraw

-Hill Com

panies, Inc.

netw rks

ESSENTIAL QUESTIONSWhy and how do people make economic choices?How do economic systems influence societies?

GUIDING QUESTIONS1. How do demand and supply affect prices?

2. How do prices help consumers and businesses make economic decisions?

Terms to Knowinteraction the effect of two or more things on each otherproducer a person or business who provides a good or a serviceconsumer a person who buys goods or servicesdemand the amount of a good or service that consumers are willing and able to buy over a range of pricessupply the amount of a good or service that producers are willing and able to sell over a range of prices

market a place where buyers and sellers come together competition struggle among sellers to attract buyersequilibrium price the price set for a good or service in the marketplace at which demand and supply are balancedsurplus a situation in which supply is greater than demandshortage a situation in which demand is greater than supplyadapt to change

What Do You Know?In the first column, answer the questions based on what you know before you study. After this lesson, complete the last column.

Now... Later...

How does supply and demand work?

Lesson 3: Demand and Supply in a Market Economy

Demand and Supply Make MarketsWhat makes prices go up and down? In a command economy, government officials set most prices. In a market economy prices are set by the interaction of demand and supply. Producers are the businesses that provide goods and services. Consumers are the people who buy them. Producers create supply and consumers create demand. In economics, demand is the amount of a good or service that people are willing and able to buy at a particular price.

Mark the Text 1. Circle the forces that

set prices in a market economy.

Introduction to Economics

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

206

206_210_BCCE_RESG_C16_L3_660008.indd Page 206 21/05/11 8:54 PM s-087206_210_BCCE_RESG_C16_L3_660008.indd Page 206 21/05/11 8:54 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME _______________________________________ DATE _______________ CLASS _________

Copy

righ

t © T

he M

cGra

w-H

ill C

ompa

nies

, Inc

.netw rks

Explaining2. What is the

relationship between price and supply?

Describing3. Study the charts.

What happens to the demand for oil as the price rises?

How does an increase in the price of oil affect the supply of oil?

Drawing Conclusions

4. What does the demand schedule tell you about the relationship between the price per barrel and the quantity demanded?

This definition of demand has four key parts:

1. Amount—Demand measures how much of something consumers will buy. This amount changes as prices change.

2. Willing to buy—Consumers must want to buy the good or service or there is no demand.

3. Able to buy—Consumers also must be able to buy. Wanting an item without having the money to pay for it does not count as demand.

4. Price—Demand is tied to price. The amount of an item people are willing and able to buy is linked to its price.

Supply is the amount of a good or service that producers are willing and able to sell at various prices during a set time period. As the price of a product goes up, producers are willing to supply more. As the price goes down, they supply less.

The amount of a good or service that is supplied and demanded at each price can be shown in a schedule. The schedules below show how much oil consumers demanded and producers supplied at certain prices.

$10 10

Price Per Barrel Quantity Supplied

Supply Schedule for Crude Oil

20

30

40

50

$20

$30

$40

$50

Quantity Demanded

$10 50

Price Per Barrel

Demand Schedule for Crude Oil

40

30

20

10

$20

$30

$40

$50

Economists use graphs to show how much of a good is supplied and demanded at each price. The data from schedules can be plotted on a graph. These graphs are called a demand curve and a supply curve. The graph on the next page shows the demand and supply curves for oil.

As you can see, the demand curve slopes down to the right. The supply curve slopes up to the right. They go in opposite directions. That is because as the price goes up, producers supply more, but consumers demand less. When prices are low, people demand more.

Introduction to Economics

Lesson 3: Demand and Supply in a Market Economy, Continued

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

207

206_210_BCCE_RESG_C16_L3_660008.indd Page 207 21/05/11 8:54 PM s-087206_210_BCCE_RESG_C16_L3_660008.indd Page 207 21/05/11 8:54 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME DATE CLASS

Copyright © The M

cGraw

-Hill Com

panies, Inc.

netw rks

Drawing Conclusions

5. Explain how increased competition affects prices and why.

Examining Details

6. What is the equilibrium price of oil according to the graph?

Contrasting 7. What is the

difference between a surplus and a shortage?

Describing8. How do prices

help determine for whom goods will be produced in a market economy?

Demand and supply curves together show a market. A market is anywhere buyers and sellers of the same good or service come together. Markets need many buyers and sellers to work well. This competition keeps prices down. Competition is the sellers’ struggle to attract buyers. If the market does not have enough sellers, prices may go too high. That is why U.S. laws ban monopolies.

$0

$10

$20

$30

$40

$50

$60

10 20 30 40BARRELS OF OIL (in tens of thousands)

PRIC

E PE

R BA

RREL

50

KEYSupplyDemandDS

Surplus

EquilibriumPrice

Shortage

Demand and Supply for Oil

Markets are important in many ways. One major way is that they set prices. Look again at the graph. Note that the lines on the graph cross at one point. This point is the price set by the market. At this price demand and supply balance. This is the equilibrium (EE•kwuh•LIH•bree•uhm) price. At this price, consumers want to buy just as much oil as producers want to sell.

If the price of oil rises higher than the equilibrium price, producers will supply more. However, consumers will not buy more. This will result in a surplus of oil. A surplus occurs when supply is greater than demand. A surplus makes prices fall.

If the price of oil falls below the equilibrium price, the opposite will happen. There will be a shortage. A shortage occurs when there is not enough supply to meet demand. A shortage makes prices rise.

Introduction to Economics

Lesson 3: Demand and Supply in a Market Economy, Continued

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

208

206_210_BCCE_RESG_C16_L3_660008.indd Page 208 21/05/11 8:54 PM s-087206_210_BCCE_RESG_C16_L3_660008.indd Page 208 21/05/11 8:54 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME _______________________________________ DATE _______________ CLASS _________

Copy

righ

t © T

he M

cGra

w-H

ill C

ompa

nies

, Inc

.netw rks

Reading Check

9. What three changes will cause demand to rise?

Listing 10. List two factors

other than price that affect demand.

Paraphrasing11. Study the

information in the table. Then use your own words to write a short paragraph describing the factors that affect supply and demand.

Price is not the only thing that affects demand. Other factors that change the demand for a good or service are

• The number of consumers. More consumers mean more demand. Fewer consumers mean less demand.

• Consumer income. If people have more money to spend, they buy more. Demand goes up. If people have less money to spend, they buy less. The equilibrium price decreases.

• Consumer preferences. If people decide they like a product, demand for it goes up. Demand goes down if consumers do not like it.

Supply is also affected by factors other than price. Two key factors are

• The number of suppliers. When more suppliers enter the market for a product, the supply increases. If some producers leave the market, the supply decreases. When this happens, prices go up. Since consumers have fewer choices, producers can charge more.

• The costs of production. If the costs of making a product go up, producers make less profit. This leads them to produce less. Supply goes down. When producers find a cheaper way to make something, they make more profit. They will supply more of it at all prices. Supply goes up.

Introduction to Economics

Lesson 3: Demand and Supply in a Market Economy, Continued

Demand

• Prices

• Number of consumers

• Consumer income

• Consumer preferences

Supply

• Prices

• Number of suppliers

• Cost of production

Factors that Affect Demand and Supply

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

209

206_210_BCCE_RESG_C16_L3_660008.indd Page 209 21/05/11 8:54 PM s-087206_210_BCCE_RESG_C16_L3_660008.indd Page 209 21/05/11 8:54 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...

NAME DATE CLASS

Copyright © The M

cGraw

-Hill Com

panies, Inc.

netw rks

Check for UnderstandingWhat happens to demand as prices rise?

1.

How do prices help businesses decide what to produce?

2.

The Economic Role of Prices Prices play a key role in a market economy. First they help answer the three basic economic questions. These questions are what to produce, how to produce, and for whom to produce.

Businesses decide what to produce based on consumer demand. If a business cannot sell a product, the price falls. When the price falls, producers stop making the product. So prices determine what gets produced.

In the same way, prices determine how things are produced. Cars provide one example. Cars built by hand would cost too much. For this reason automakers use mass production to keep prices down. All businesses try to keep production costs down. This allows them to sell at prices consumers will pay.

Prices also answer the last question: for whom are goods produced? They are produced for those who have the money and desire to buy them at a given price.

In a market economy, prices also have other uses. They measure value. They send signals to producers and consumers about the value of a product or service. For producers the signals help them decide where to set prices. If consumers will not buy an item at a certain price, producers realize they should lower that price. For consumers prices signal what an item is worth. If no producer offers an item at the low price consumers want, then consumers must adapt. This means they must change their expectations about what they will have to pay.

Prices do not play the same role in a command economy. In this case government officials answer the three basic economic questions. Prices are not set by supply and demand. Instead, officials set prices based on their idea of the value of goods and services.

Introduction to Economics

Lesson 3: Demand and Supply in a Market Economy, Continued

Glu

e Fold

able h

ere

Reading Check

12. Are prices more changeable in a market economy or in a command economy? Why?

13. Place a Venn diagram Foldable along the line . Write the title The Role of Prices on the anchor tab. Label the top tab Demand, the middle tab Both, and the bottom tab Prices. On both sides of the tabs, write about each and what they have in common.

Program: RESG Component: Chapter 16PDF Pages

Vendor: APTARA Grade:

210

206_210_BCCE_RESG_C16_L3_660008.indd Page 210 21/05/11 8:54 PM s-087206_210_BCCE_RESG_C16_L3_660008.indd Page 210 21/05/11 8:54 PM s-087 /Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC.../Volumes/111/GO00792/BUILDING_CITIZENSHIP_CIVICS_AND_ECONOMICS_12/NATIONAL/ANC...