nepal fiscal restructuring and public resource management

TRANSCRIPT

Report No. 12281-NEP

NepalFiscal Restructuring and PublicResource Management in the Nineties(In Two Volumes)Volume II Review of Sector Expenditures, and Statistical Appendix

March 17, 1994

South Asia Country Department ICountry Operations, Industry and Finance Division

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FOR OFFICIAL USE ONLY

ABEBRVIATIONS AMD ACRONYNS

ADB - Asian Development Bank

ADB/N - Agricultural Development Bank of NepalAGO - Auditor General's OfficeAIC - Agricultural Inputs CorporationARC - Administrative Reform Commission

BAU - Business-As-UsualBOP - Balance of PaymentsBPE - Basic and Primary Education

BPEP - Basic and Primary Education Project

CBPASS - Commercial Bank Problem Analysis and Strategy Study

CEM - Country Economic Memorandum

CPR - Contraceptive Prevalence Rate

CTEVT - Council for Technical Education and Vocational Training

DANIDA - Danish International Development Agency

MDc - Dairy Development CorporationDOI - Department of IrrigationDOR - Department of Roads

DTOs - District Treasury Offices

DNPWC - Department of National Parks and Wildlife ConservationDSCWM - Department of Soil Conservation and Watershed ManagementDWSS - Department of Water Supply and Sanitation

BP - Eighth PlanBPI - Expanded Program for Immunization

ESAF - Enhanced Structural Adjustment Facility

FCGO - Financial Controller General's Office

FGF - Fully Government FundedFP/MCH - Family Planning and Maternity and Child Health

FY - Fiscal Year

GDP - Gross Domestic Product

HC - Health Centers

HFP - Health and Family Planning

HMG - His Majesty's GovernmentHPs - Health Posts

HPP - Health and Population Program

HRD - Human Resource DevelopmentHS - Higher Secondary

IDA - International Development Association

11si - International Irrigation Management Institute

ILC - Irrigation Line of CreditIMC - Irrigation Management Center

ISP - Irrigation Sector Project

This docmn bas a retricted distbuion and may be used by recipients only in te perfomnce of thdrofficial d rues Its contnts may not otherwise be tisclosed without World Bank auorizaton.

LRMP - Land Resources Mapping Project

MCH - Maternity and Child Health

MGA - Ministry of General AdministrationMOP - Ministry of Finance

MOH - Ministry of HealthMPE - Manufacturing Public EnterprisesMRCU - Maintenance and Rehabilitation Coordination Unit

NARC - Nepal Agricultural Research CouncilNBA - Nepal Electricity AuthorityNGO - Non-Governmental OrganizationNPC - National Planning CommissionNWSC - Nepal Water and Sewerage Corporation

OECD - Organization for Economic Cooperation and DevelopmentOGL - Open General LicenseO&M - Operations and Maintenance

PBPM - Program Budgeting and Project MonitoringPE - Public Enterprise

PEDP - Primary Education Development ProjectPEP - Primary Education ProjectPFP - Policy Framework Paper

PHC - Public Health CenterPME - Public Manufacturing EnterprisesPPAD - Perspective Plan for Agricultural Development

RNAC - Royal Nepal Airline CorporationROR - Rate of Returns

SAL - Structural Adjustment FacilitySFYP - Seventh Five Year PlanSMD - System Management DivisionSTW - Shallow Tubewells

TA/DA - Travel And Daily AllowanceT&D - Transmission and DistributionT&T - Trade and TransitTVE - Technical and Vocational Education

UNDP - United Nations Development ProgramUNICEF - United Nations Children's Education FundUPE - Universal Primary Education

VAT - Value-Added Tax

FISCAL RESTRUCTURING AND PBMLIC REBOURCEMANAGEMENT IN THE NINETIES

VOLUMM II: REVIEW OF SECTOR EXPENDITURES AND STATISTICAL APPMWDIX

C0NTBNT8

PRan

Chapter 5 SECTC-. EXPENDITURE PERFORMaNCE AND REFORMS

A. Agriculture .... . . . . . .. . . . . . . . . . 82e Introduction and Background . . . . . . . . . . 82* Irrigation .86e Irrigation Credit and Subsidies . . . . . . . . 92* Fertilizer .94

• Research and Extension . . . . . . . . . . . . . 98o Livestock ................... 100* Forestry .... . . . . . . . . . . . . . . . . 101o Conclusions ... . . . . . . . . . . . . . . . 107

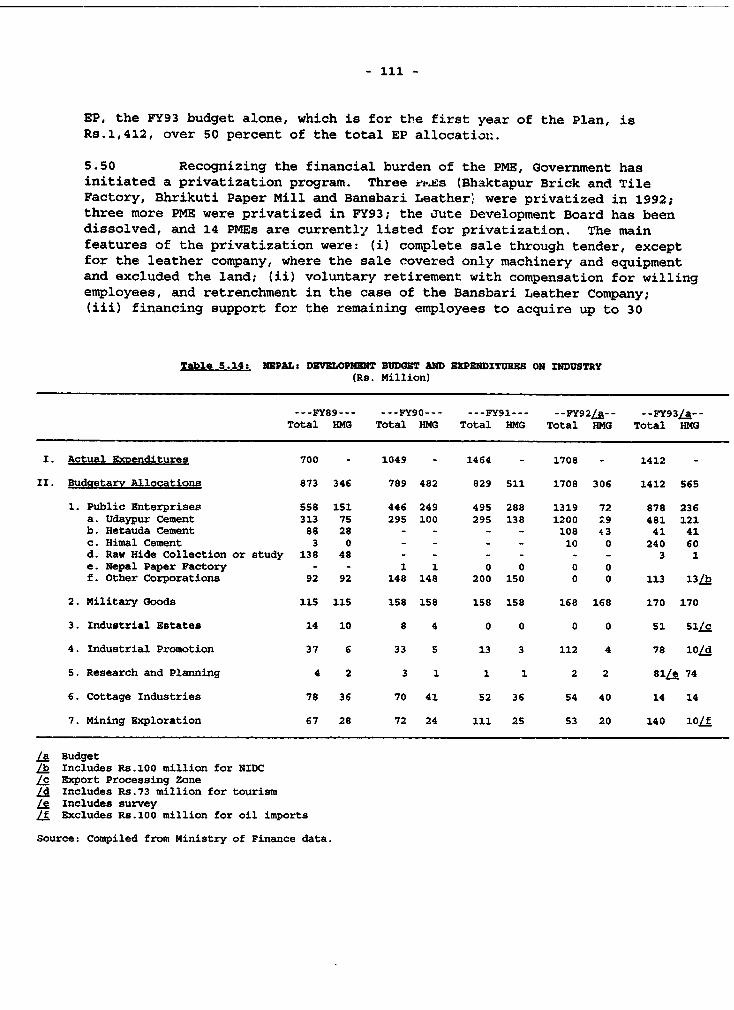

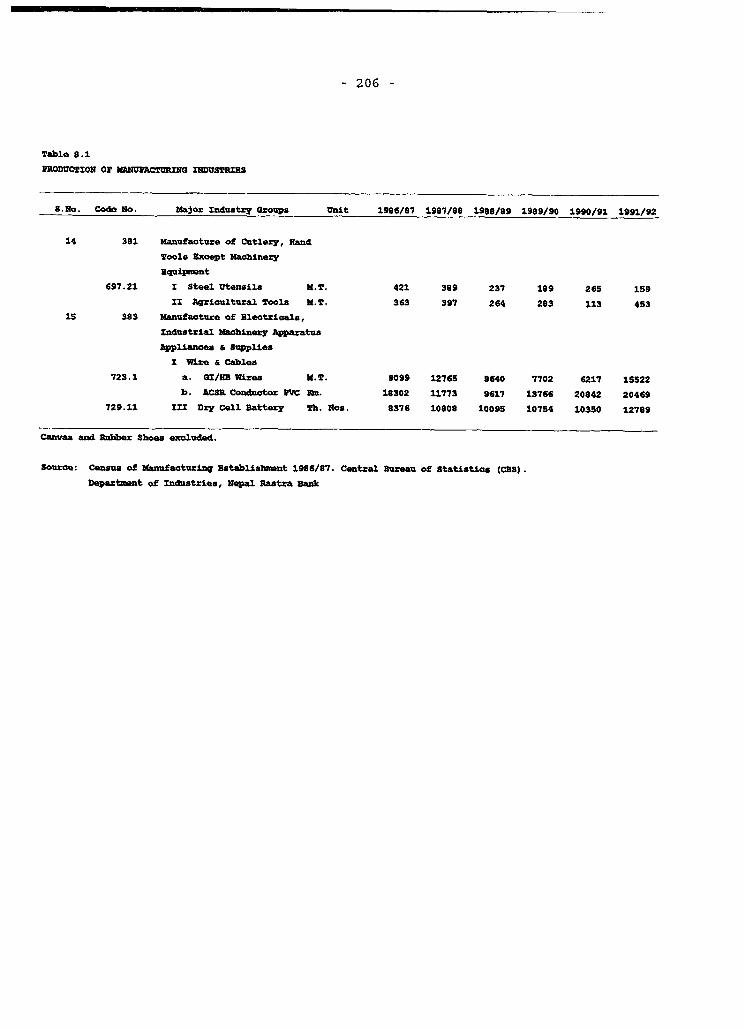

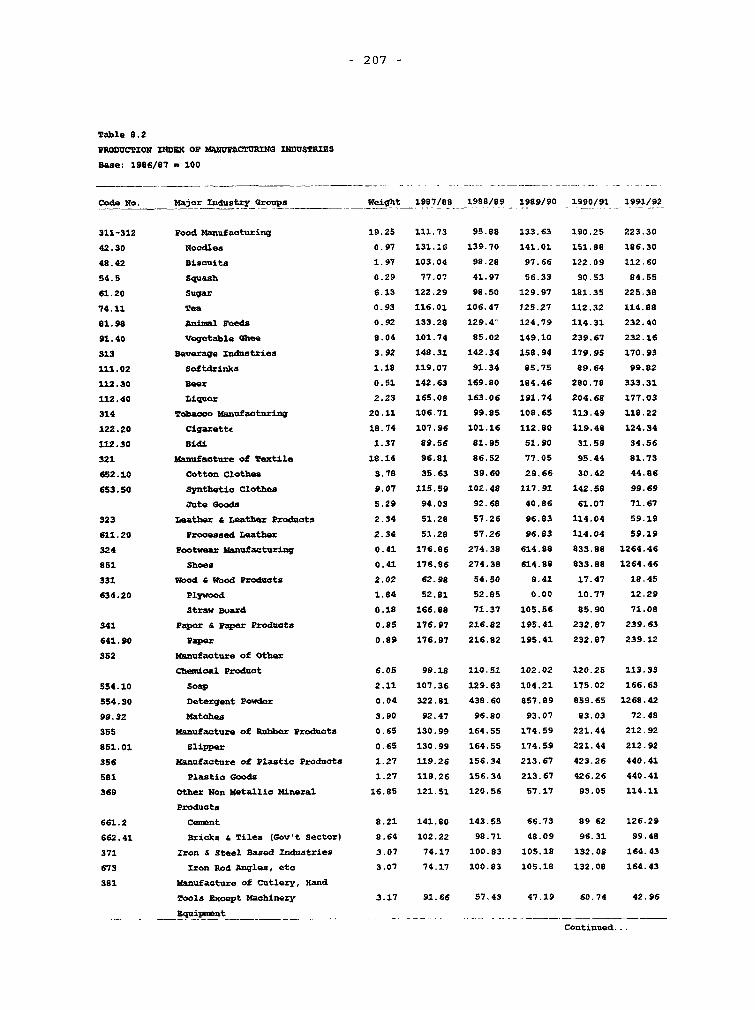

B. Industry ....................................... 109e Performance . . . . . . . . . . . . . . . . . . 109o Expenditure Priorities and Reforms ... . . . . 110

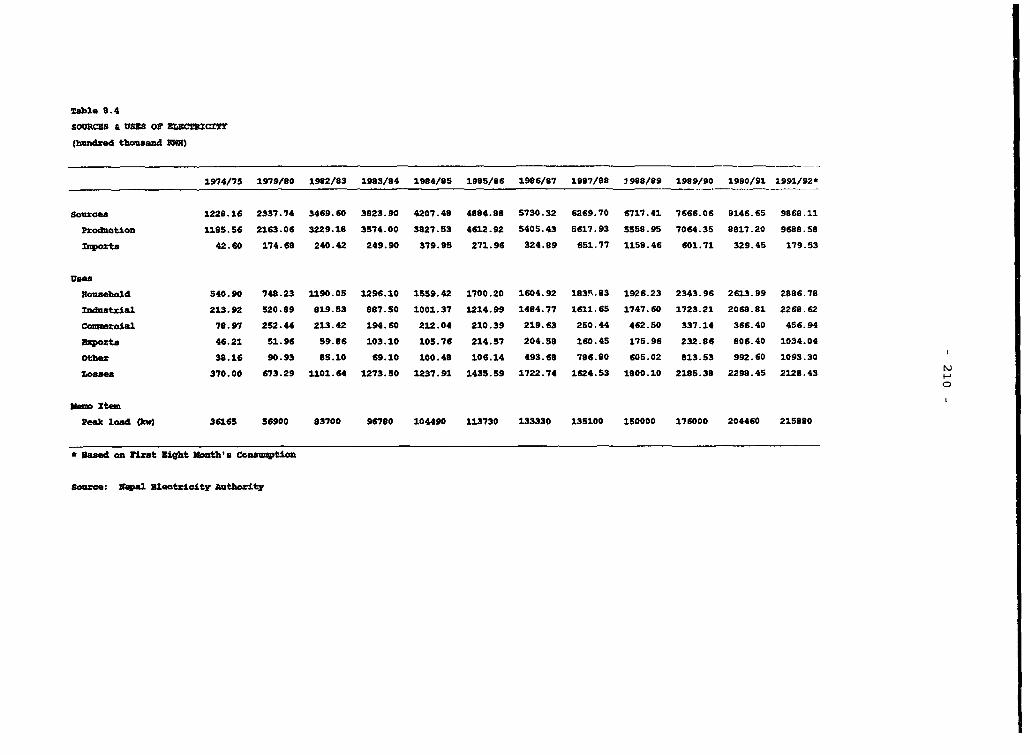

C. Power ................. . . . . . . . . . . 112* Performance and Overview of Issues ... . . . . 112* Sector Objectives and Strategy . . . . . . . . . 114e Priorities for Intermediate Power Supply . . . . 114o The Arun III Project . . . . . . . . . . . . . . 115* Commercialization of NEA . . . . . . . . . . . . 118* Rural Electrification Programs . . . . . . . . . 119* Summary and Conclusions . . . . . . . . . . . . 120

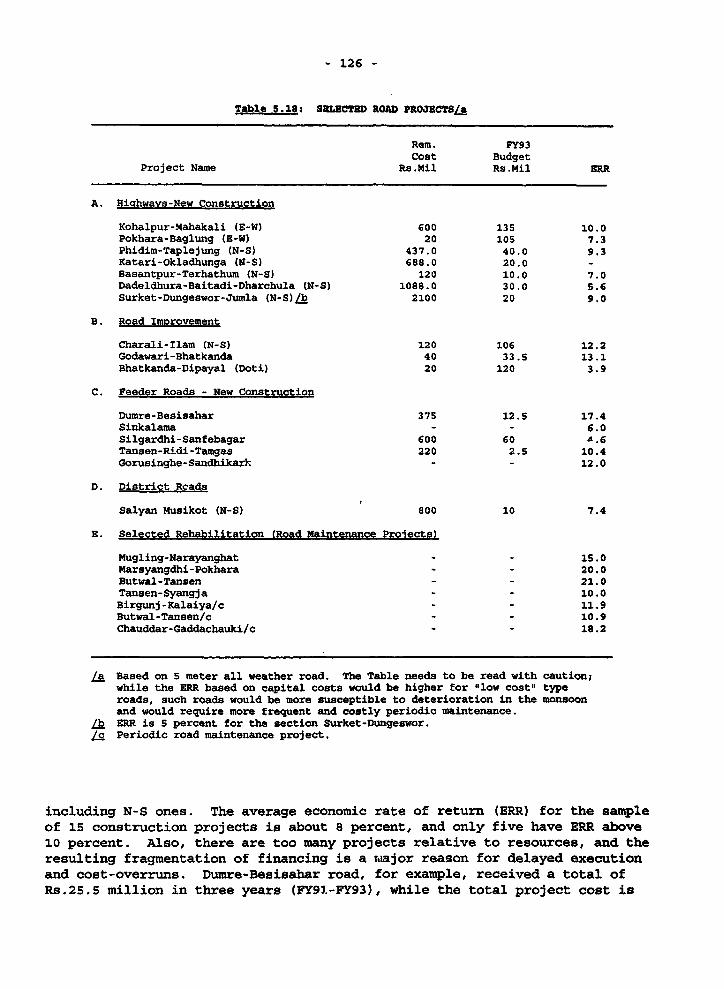

D. Transport . .................. . . . . . . . . . 120* Introduction and Background . . . . . . . . . . 120* Road Transport ... . . . . . . . . . . . . . . 123* The Trail System . . . . . . . . . . . . . . . . 129* Aviation .... . . . . . . . . . . . . . . . . 130* Conclusions ... . . . . . . . . . . . . . . . 132

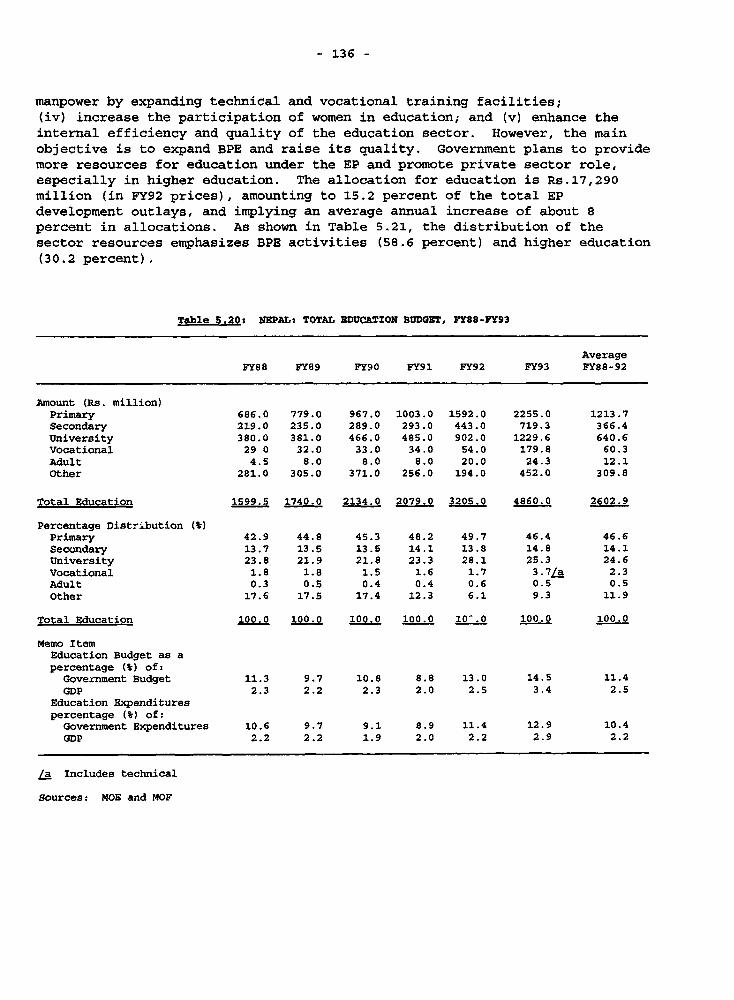

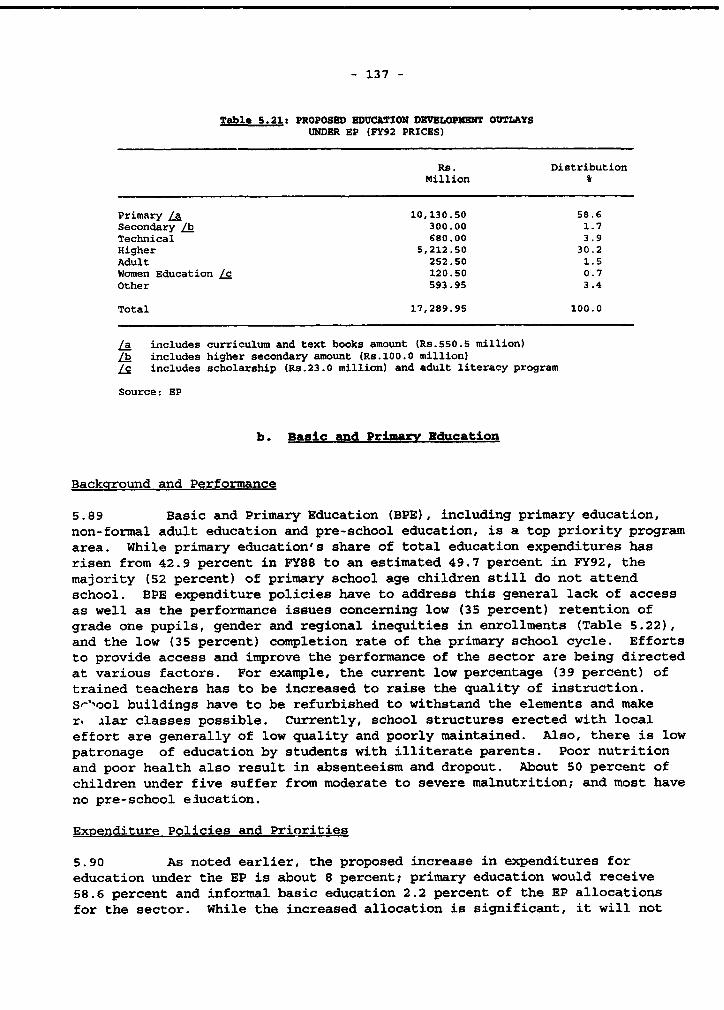

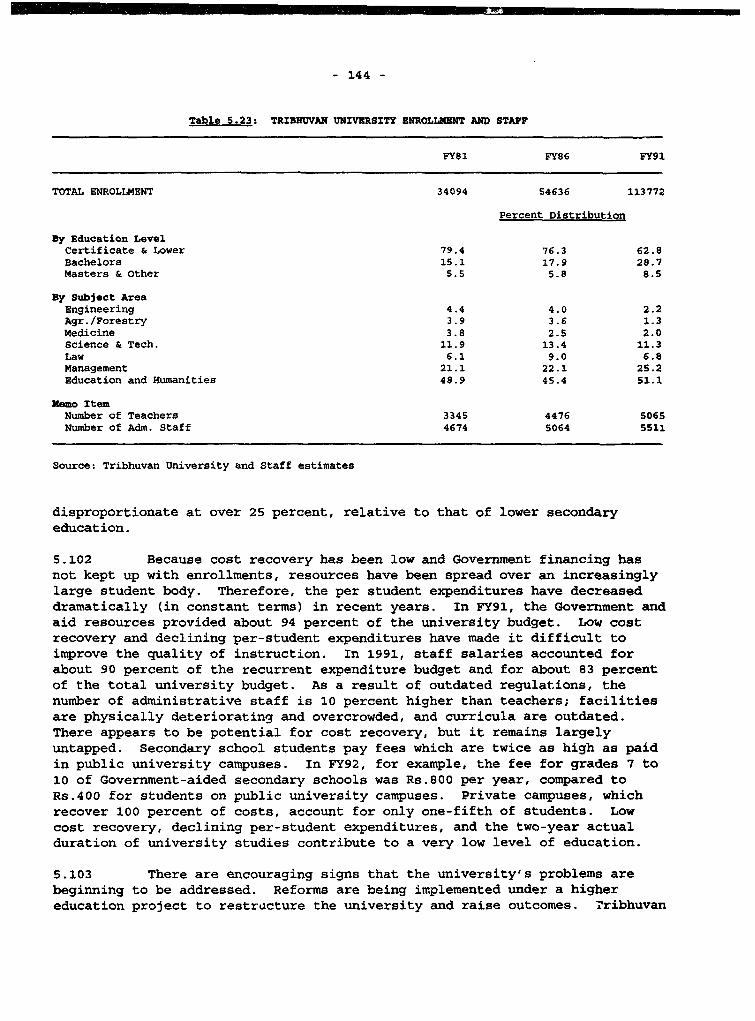

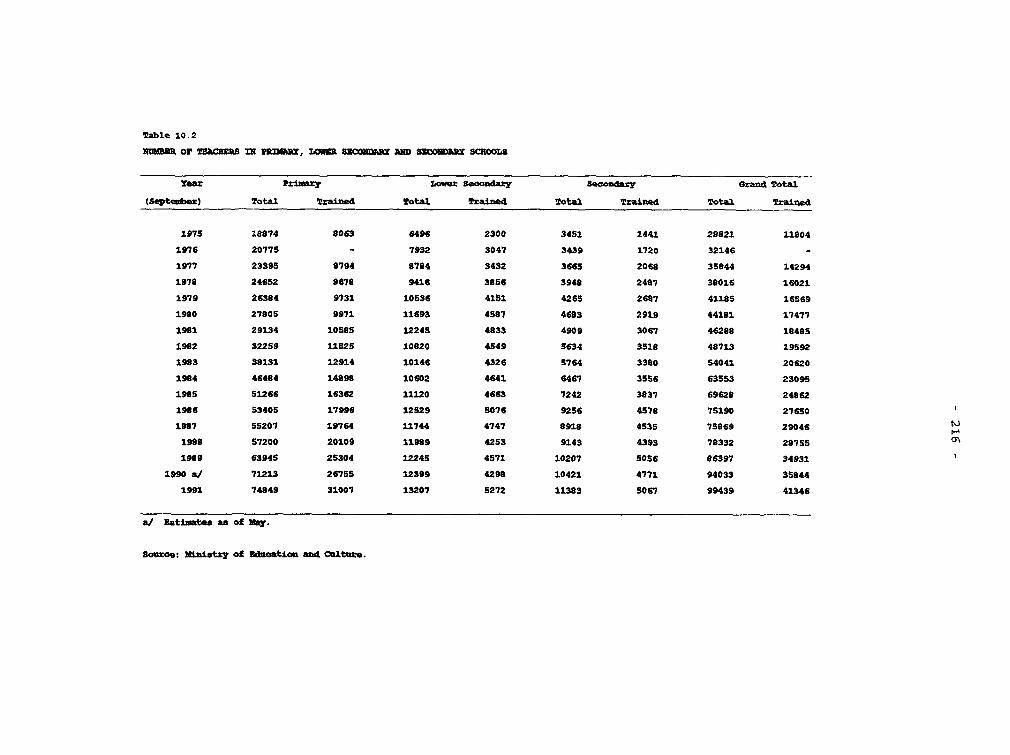

E. Education . .................. . . . . . . . . . 134* Background and Main Issues . . . . . . . . . . . 134• Basic and Primary Education . . . . . . . . . . 137* Secondary Education . . . . . . . . . . . . . . 140* Technical and Vocational Education . . . . . . . 141* Higher Education .143o Conclusion ................... 145

Contents

RFa

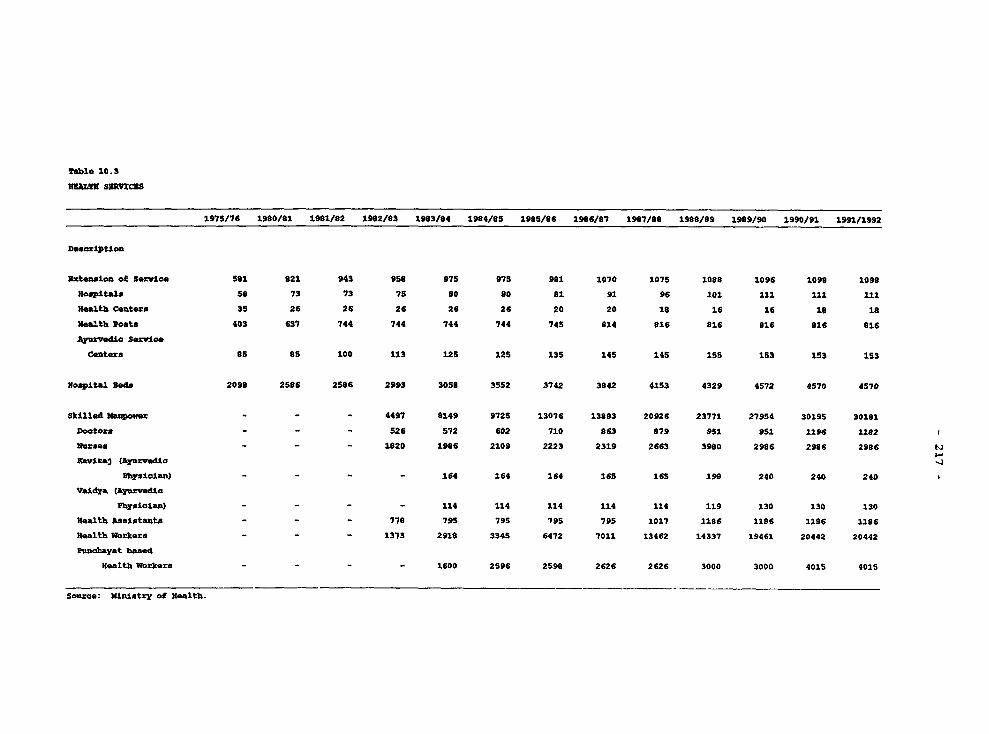

F. Health and Family Planning . . . . . . . . . . . . . 147• Introduction and Background . . . . . . . . . . 147o Health Service Institutions . . . . . . . . . . 150o Expanded Program for Immunication (EPI) . . . . 154

e Family Planning and Maternal and Child Health 155o Malaria Eradication Program . . . . . . . . . . 156o ronclusion . . . . . . . . . . . . . . . . . . . 156

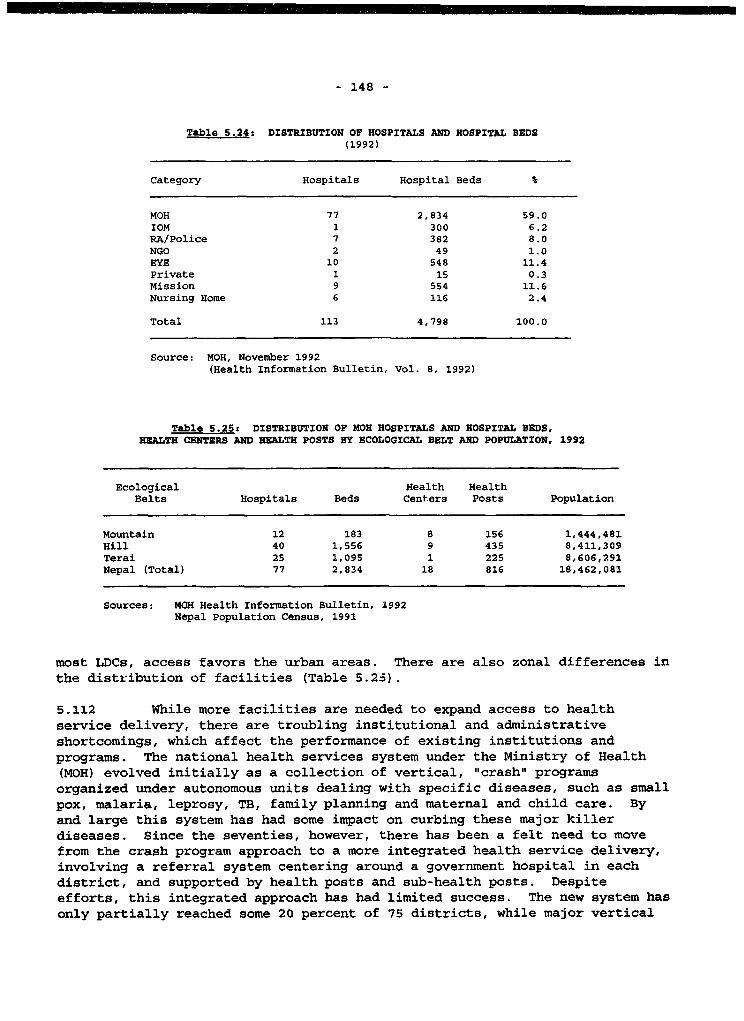

G. Water Supply and Sanitation . . . . . . . . . . . . 15So Background and Performance . . . . . . . . . . . 158o EP Expenditure Policies and Priorities . . . . . 160* Sustainability and Resource Mobilization . . . . 164

o Conclusion . . . . . . . . . . . . . . . . . . . 165

H. Expend-ture Reforms and Environmental Policy . . . . 166

STATISTZCAL APPNMDIX

MAP

TXT TABLES

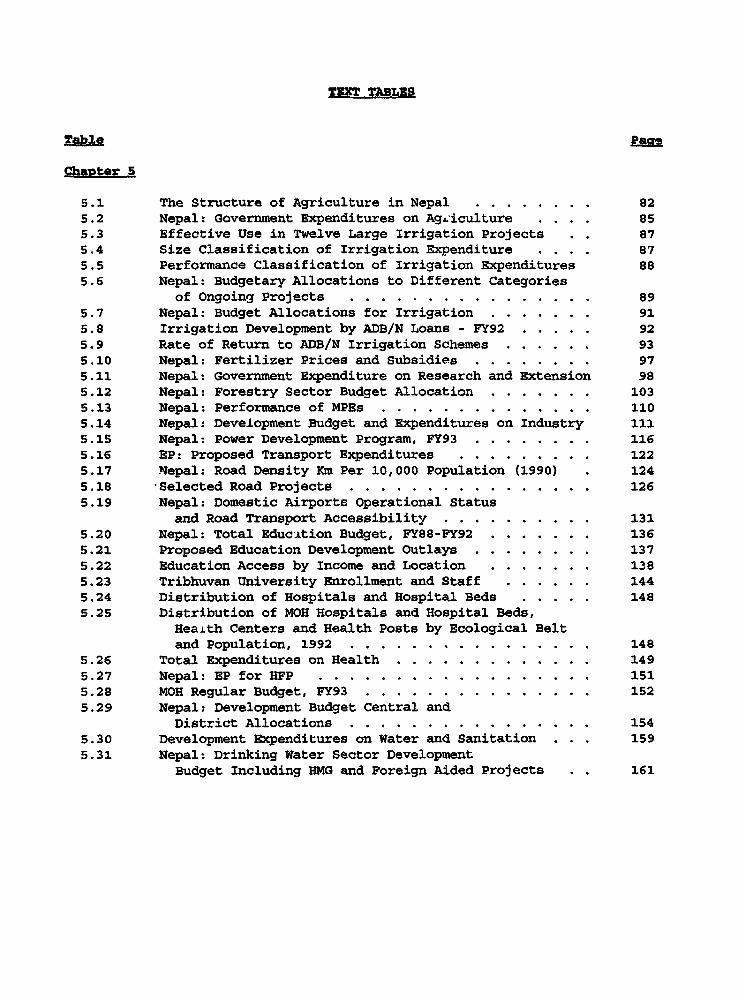

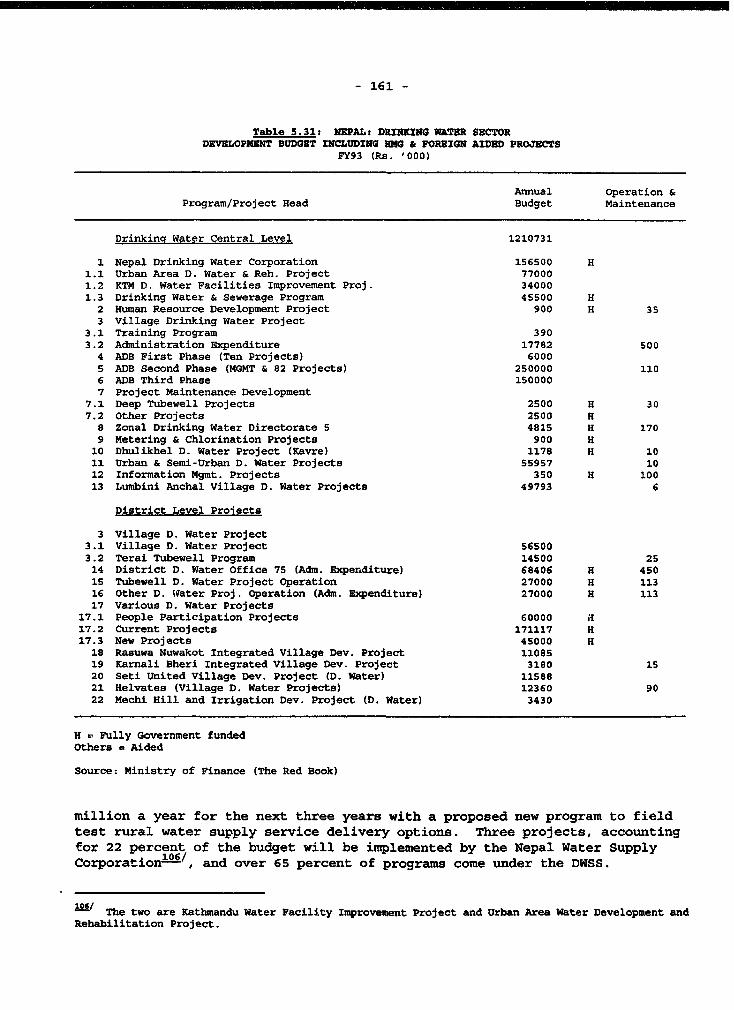

Table Pae

Chapter S

5.1 The Structure of Agriculture in Nepal . . . . . . . . 825.2 Nepal: Government Expenditures on Agriculture . . . 855.3 Effective Use in Twelve Large Irrigation Projects . . 875.4 Size Classification of Irrigation Expenditure . . . . 875.5 Performance Classification of Irrigation Expenditures 885.6 Nepal: Budgetary Allocations to Different Categories

of Ongoing Projects .895.7 Nepal: Budget Allocations for Irrigation . . . . . . . 91

5.8 Irrigation Development by ADB/N Loans - FY92 . . . . . 92

5.9 Rate of Return to ADB/N Irrigation Schemes . . . . . . 935.10 Nepal: Fertilizer Prices and Subsidies . . . . . . . . 97

5.11 Nepal: Government Expenditure on Research and Extension 985.12 Nepal: Forestry Sector Budget Allocation . . . . . . . 103

5.13 Nepal: Performance of MPEs . . . . . . . . . . . . . . 1105.14 Nepal: Development Budget and Expenditures on Industry 111

5.15 Nepal: Power Development Program, FY93 . . . . . . . . 1165.16 EP: Proposed Transport Expenditures . . . . . . . . . 122

5.17 Nepal: Road Density Km Per 10,000 Population (1990) 1245.18 Selected Road Projects .126

5.19 Nepal: Domestic Airports Operational Status

and Road Transport Accessibility . . . . . . . . . . 131

5.20 Nepal: Total Educltion Budget, FY88-PY92 . . . . . . . 1365.21 Proposed Education Development Outlays . . . . . . . . 137

5.22 Education Access by Income and Location . . . . . . . 1385.23 Tribhuvan University Enrollment and Staff . . . . . . 144

5.24 Distribution of Hospitals and Hospital Beds . . . . . 1485.25 Distribution of MOH Hospitals and Hospital Beds,

Health Centers and Health Posts by Ecological Belt

and Population, 1992 .1485.26 Total Expenditures on Health . . . . . . . . . . . . . 149

5.27 Nepal: EP for HFP .151

5.28 MOH Regular Budget, FY93 . . . . . . . . . . . . . . . 1525.29 Nepal: Development Budget Central and

District Allocations .1545.30 Development Expenditures on Water and Sanitation . . . 159

5.31 Nepal: Drinking Water Sector Development

Budget Including HMG and Foreign Aided Projects . 161

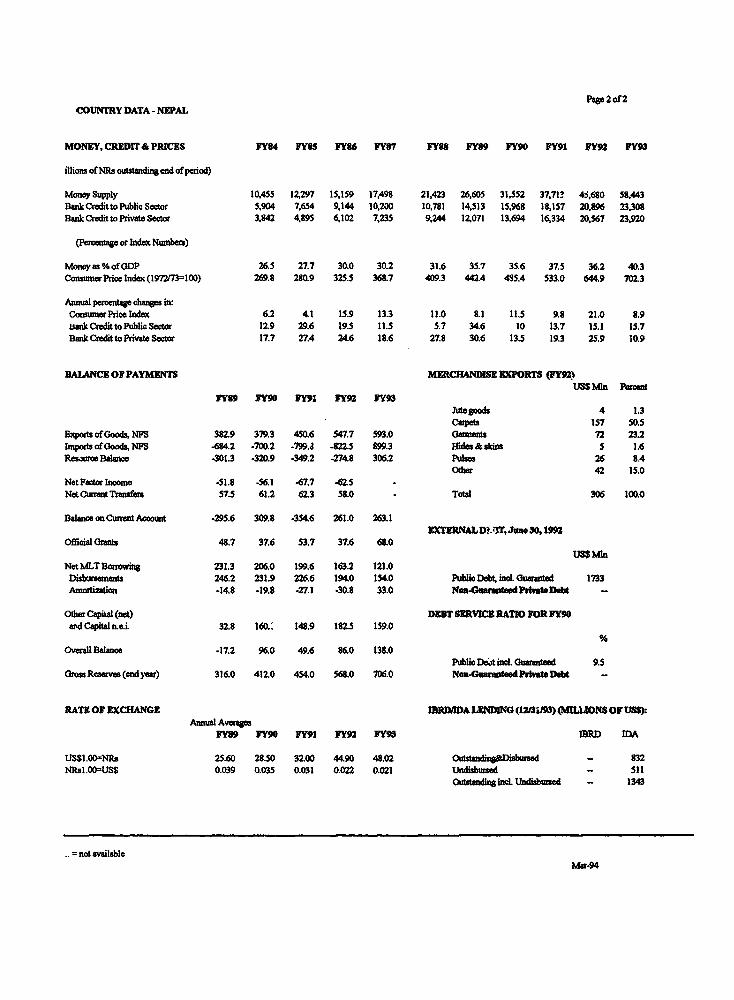

page lof 2

COUNTRY DATA - NEPAL

AREA POPULATION(1991) DEI (1991)147.181 km2 18.5 million 126 perkm2

Censusgrowthrate: 2.1%hA

POPULATION CHARACTURISTICS (1991) HEALTH (1992)Crude birth rate (per 1,000): 37.5 Populaion per physician: 15s,0Crude death a (per 1,000): 13.8 Population per hospital bed: 3,808Infant mortelity (per 1.000 live births): 102

INCOME DlSTRIBUTION DISTRIBUTION OF LANDOWNERSHIP% ofnational income, highest quintile: - % owned by top 10% of ownas:% of nation1 inconma, lowest quintile: - % owned by smallest 10% :

ACCESS TO SAFE WATER (1992) ACCESS TO ELECTRICITY% of population - urban: 62.0 % of populton - urban:% ofpopuation -rual: 380 % ofpopuation -rural:

NUTRITION(1986) EDUCATIONCalorie intake per peson: 2,078 Adult lltaay rate (% of population) (1991) 67Pea capita ptmein intake day): 53 Primary school enrlu nt - (% of

relevant apge goup -1988) 86

GNP PIR CAPITA IN 1992: US5170 lb

GROSS NATIONAL PRODUCT (FY93)uSSIn %

GNP at Market Prixs 2,891 100.0;hoss Domestic lnvestent 598 20.7Gas Naiona Saviwn 358 12.4Curet Accotmt Balance 263 8.9EWpt of Goods. NFS 593 20.2

Vnort ofoods. NFS 899 31.1

OUTfUT (FY92)Value Added

US$ Mln 3

Agriculture 1,408 48.7Induy 474 16.4Services 1.009 34.9

Total 2,891 100.0

GOVERNMENT FINACECenti Government

Rs Mln % ofGDPFY93 FY83 FY92 FY93

CurentReceipts 15,148 SA 10.7 10.4C etExpendtu 12,001 11.8 7.9 8.3CuentBance 3,147 .3A 2.8 2.1Capital Expeditures 20,405 8.7 13.1 14.1

la 1981-1991 intr censal gowth rate./b C tau in accordance with Atla5 methodoloy.- Not available.

Pae 2 of2COUNTRY DATA - NIPAL

MONEY, CREDIT& PRICES FY84 FY8S FY6 FY87 FY88 FY89 FY90 FY91 FY92 FY93

illion ofNRs outUndiend of piod)

Money Supply 10,455 12,297 15,159 17,498 21,423 26,605 31.552 37,71' 4J,680 58.443BamkCredittoPublicSector 5,904 7,654 9,144 10,200 10.781 14,513 15,968 18.157 20,896 23,308Bank Credit to Pivate Scaor 3,842 4,895 6,102 7,235 9,244 12,071 13,694 16,334 20,567 23,920

(Percenag or Index Number)

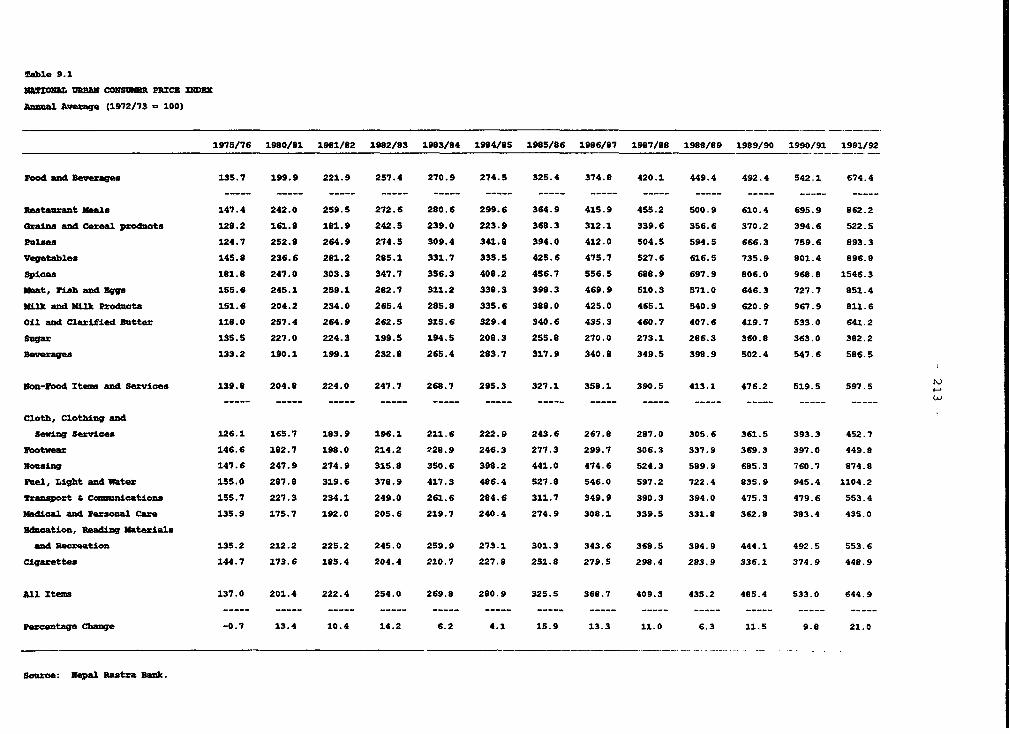

Monqas %ofODP 26.5 27.7 30.0 30.2 31.6 35.7 35.6 37.5 36.2 40.3Consuer Price Index(1972M=100) 269.8 280.9 325.5 368.7 409.3 442.4 4S5.4 533.0 644.9 702.3

Annual pactage changes in:ConaumerPricelndex 6.2 4.1 15.9 13.3 11.0 8.1 11.5 9.8 21.0 8.9bankCredittoPublicSctor 12.9 29.6 19.5 11.5 5.7 34.6 10 13.7 15.1 15.7BankkCreditto Privatector 17.7 27.4 24.6 18.6 27.8 30.6 13.5 19.3 25.9 10.9

BALANCE OF PAYMENTS MERCHAN EPORTS (FY92)USSMln Pecet

FY89 FY90 FY91 FY92 FY93JAtegoods 4 1.3Capet 157 50.5

lixpots ofGoods, NFS 382.9 379.3 450.6 547.7 593.0 Gannets 72 23.2Impoit ofGoods, NFS -684.2 -700.2 -799.J 822.5 899.3 Hides& sain 5 1.6Resatre Balence -301.3 -320.9 -349.2 -274.8 306.2 Palsae 26 SA

Otber 42 15.0NeotFstor noome -51.8 -56.1 -67.7 -65Net Current Trnafers 57.5 61.2 62.3 58.0 - Totl 306 100.0

Balance en Current Account -295.6 309.8 -354.6 261.0 263.1EXTERNAL DE 1T, June 30,1992

Official rants 48.7 37.6 53.7 37.6 68.0US$Mln

NetMLTBorrowing 231.3 206.0 199.6 163.2 121.0DisUXmnart 246.2 231.9 226.6 194.0 154.0 Pablc Det il uarantd 1733Amortization -14.8 -19.8 -27.1 -30.8 33.0 Nan-GuaratedPatDebt -

Other Capita (net) DEBT SlERVICE RATO FOR FY90wd Capitalnei. 32.8 160.: 148.9 182.5 159.0

Overall Balance -17.2 96.0 49.6 86.0 138.0Public Det ind. Guaanteed 9.5

Gro Resenw (end year) 316.0 412.0 454.0 568.0 706.0 Non-Guateed Privste Debt -

RATE OF EXCHANGE IDRDIIDA LEDG (12/31193) (IALUONS OF 11SS):Anual Averages

FY89 FY90 FY91 FY92 FY93 WIRD IMA

USSI.O=NRs 25.60 28.50 32.00 44.90 48.02 - 832NRsl.00=USS 0.039 0.035 0.031 0.022 0.021 Ussed - 511

O_utding ind Undisbrd - 1343

=not availableMsr-94

SE1CTOR EXPENDIZTRE PEMRFoANCE AND REWOR_M

A. AGRICULTURm

a. Introduction and Backaround

Overview of Aaricultural Performance

5.1 Agriculture/ is the largest sector in the economy of Nepal,accounting for over half of GDP, over 80 percent of employment and 15 percentof recorded exports. Ninety-five percent of the poor are in rural areas,dependent mainly on agriculture for their livelihood.33/ Nepal has adiverse agro-climat'c structure, with a corresponding diversity of croppingpatterns. The Terai contributes 48.0 percent of the sector's value-added,closely followed by the Hills with 44.1 percent, and with the mountainsproducing only 7.8 percent (Table 5.1). The Terai is more dominant in cropproduction, with 52.4 percent of the total, while the Hills

Table 5.1s: T STRUCTURE OF AQRIULTUR IN NPALtPercent of Agricultural GDP FY89)

Total of

gcological

Crops Livestock Forestry Fisheries Other Zone Nepal

mountain 56.3 32.3 9.8 0.0 1.6 100.0 7.8(7.4) (9.0) (8.2) (0.0) (7.4)

sill 54.s 34.1 9.9 0.0 1.6 100.0 44.1(40.2) (S3.3) (46.5) (1.4) (40.2)

Terai 6S.1 22.1 8.8 2.1 1.9 100.0 48.1(S2.4) (37.7) (4S.3) (98.6) (S2.4)

Total of Sub-

Sectors (100.0) (100.0) (100.0) ( .0) (100.0) - -

Nepal 59.7 28.2 9.3 1.0 1.7 - 100.0

Note: The entries not in parenthesis in the table are the percentages of the agro-ecological zone value-

added contribut^d by the sub-sector indicated by the column heading. The entries in parenthesis in

the table are the percentages of the sub-sectoral value-added produced in the agro-ecological zone

indicated by the rsw heading. The entries under the column labelled aNepala show the percentage of

total value-added for the sector produced in the relevant agro-ecological zone. The entries in the

row labelled "Nepal" show the percentage of total value-added foz the whole agricultural sector

produced by the relevant sub-sectors.

Source: NPC Special compilation, January 1993.

TU throughout this chapter, unless the content demands otherwise, the term agriculture is taken

to subsume the whole sector, including livestock, forestry, and irrigation.

-U World Bank, Nepal: Poverty and Incomes, A World Bank Country Study, Washington DC, 1991,

pp.13.

- 83 -

dominate livestock production (5?.3 percent). Almost 60 percent of value-added is generated by crop production (of which foodgrains account for about68 percent); about 28 percent by livestock, and forestry probably under-estimated at about 9 percent.

5.2 Agricultural performance has been disappointing, despiteGovernment efforts, and this poor performance has been obscured by poorstaiAstics. Official figures for the decade FY80 to FY90 indicate real annualaverage growth of agriculture GDP variously at 4.9 to 5.4 percent. A reviewof the national accounts by the NPC in July 1992 concluded that these growthrates were over-estimated._ The NPC has initiated a detailed study ofagricultural statistics. While not yet completed, the analysis to datesuggests that the source of the over-estimation was the revision, usuallyupwards, of district-level cropped area, following the availability of reviseddata from the cadastral survey and from the Land Resources Mapping Project(LRMP). It seems likely that revising the data will substantially reduce thepresent official growth rate, possibly to around 3.0 percent per annum.

5.3 Average crop yields are low, though there are significantdifferences between Terai and the Hills. Average yield increased slightly forpaddy (1.4 percent) and wheat (1.4 percent), but stagnated or declined forbarley, maize and millet in FY8O-FY90. While there are differences in yieldsbetween agricultural zones in Nepal, aver.ge level of cereal yields are almost35 percent below the average for Asia, about 30 percent below that inBangladesh, somewhat below India and much below Sri Lanka (36 percent).3/For the most part, the performance of programs in Government irrigation andagricultural research performed below expectation, while input supply schemesdid not succeed in producing results. The Government's approach toagricultural development in the past decades emphasized the role of the statein designing and implementing investments, operating irrigation systems,supplying inputs to farmers and in controlling prices. With the poor growthof agriculture, which is the main source of income for most of the ruralpopulation, not much, if any, progress has been made in reducing poverty.

5.4 There is recognition in the Government and among donors thatincreases in agricultural productivity are necessary for Nepal to make abroad-based impact on widespread low income levels. As reflected in recentinitiatives, such as Wtew Irrigation Policy and the launching of thePerspective Plan for Agricultural Development, Government has recognized theneed for a much-improved growth strategy for agriculture. Agricultural policyis now in a state of flux with new initiatives, such as in irrigation andresearch, but these have yet to be fully implemented. Reforms in fertilizermarketing and forestry have been introduced, and changes in structure andpersonnel have been effected in some of the key agricultural departments;however, an integrated strategy is yet to emerge.

S1/ See "Review of Data Sources and Methods of National Accounting of Nepal", pp 5-8, NationalPlanning Commission, July 1992.

35/Comparative cereal yields are reported in FAO Production Year Book, Volume 44, PAO/UN 1990.

- 84 -

Perspective Plan for Aqricultural Develonment (PPAD)

5.5 The PPAD is an HMG exercise coordinated by the NPC. While it willlook at the long-term development of the sector, its primary focus will be oni.dentifying a priority set of interventions to be implemented in the medium-term to accelerate growth. in outline, the priority set includes thefollowing.

Expansion of irrigation, which can permit intensive cropproduction. A major role for farmer groups is envisaged in allstages of design, construction, operation and maintenance. Thisapproach is consistent with the 1992 Irrigation Policy, whichcalls for shifting towards farmer-controlled schemes; its maindifference from the 1988 Irrigation Policy is the emphasis givento perennial irrigation and to increased cropping intensity.

Increased supplies of agricultural inputs, notably fertilizer, ina timely fashion, based on a dominant role for the private sector;this is consistent with recent announced policy changes, but whichstill falls short of full implementation.

e A research and extension effort focused on supporting rapidproduction increases. While this does not exclude research onrainfed land and Hill crops, which are emphasized in the BP, itgives priority to research directed at high yielding varietiesalong with controlled w'ter supplies and adequate fertilizer.

* Provision of supportive infrastructure in areas of high potentialfor production increases, emphasizing farm-to-market roads inthose areas of the Terai suitable for rapid expansion ofgroundwater irrigation and other irrigated farming.

5.6 This preliminary set of priorities will be tested and furtherelaborated by studies leading up to the PPAD. In addition to therecommendations for immediate action to accelerate growth in the medium-term,the PPAD will provide a long-term strategy for the development of both theTerai and the Hills, based upon the exploitation of ecological diversity andof comparative advantage.

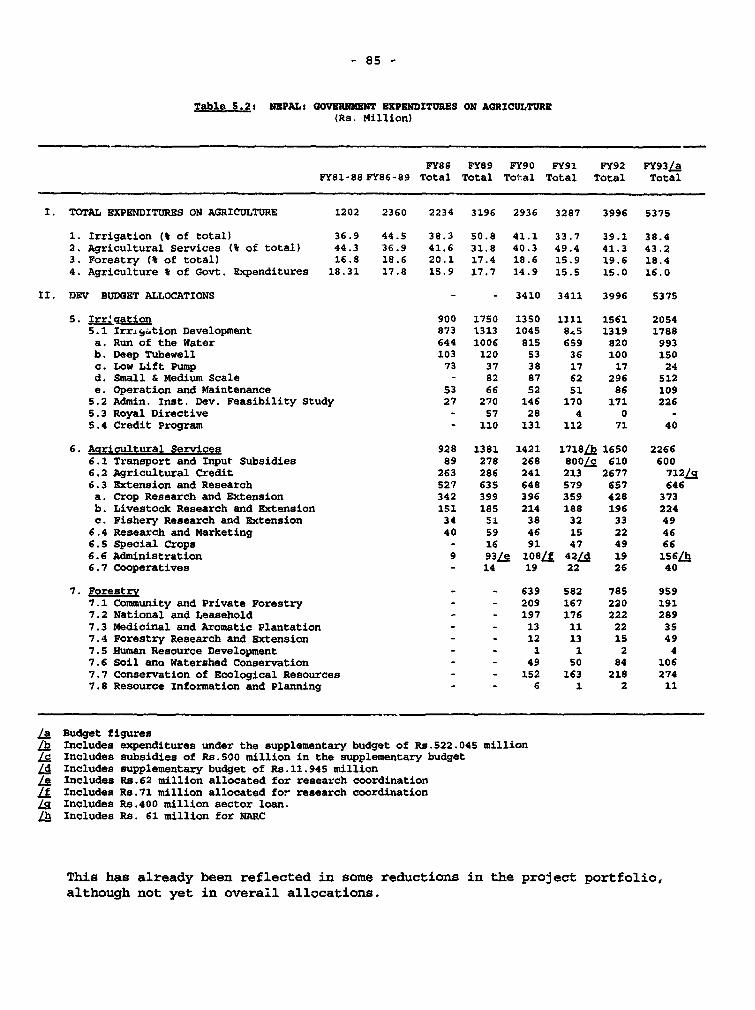

Total Government Expenditure: Aariculture

5.7 Because of its importance, agriculture has been a focus ofdevelopment efforts and expenditures, both on the part of Government and ofdonors. In the 1980s, the sector received 27 percent of developmentexpenditures, and 18 percent of total Government spending (Table 5.2).Nominal expenditures declined at the start of the nineties, due mainly tolower allocations for irrigation as projects were completed; but, totalexternal aid for agriculture has remained strong, accounting for 45-50 percentof financing. There have recently been indications, however, that some of themajor donors are concerned about the performance of projects in agriculture.

- 85 -

Table 5.2: NEPAL: GOVERUKNBT EXBPNDITUREt ON AGRICULTURE

(Rs. Million)

FY88 FY89 FY90 FY91 FY92 FY93LaFY81-88 FY86-89 Total Total Total Total Total Total

I. TOTAL EXPENDITU4RES ON AGRICULTURE 1202 2360 2234 3196 2936 3287 3996 5375

1. Irrigation (t of total) 36.9 44.5 38.3 50.8 41.1 33.7 39.1 38.4

2. Agricultural Services (t of total) 44.3 36.9 41.6 31.8 40.3 49.4 41.3 43.2

3. Forestry (% of total) 16.8 18.6 20.1 17.4 18.6 15.9 19.6 18.4

4. Agriculture & of Govt. Expenditures 18.31 17.8 15.9 17.7 14.9 15.5 15.0 16.0

II. DRV BUDGET ALLOCATIONS - - 3410 3411 3996 5375

S. Irr2aation 900 1750 1350 1311 1561 2054

5.1 Irr~.ytion Development 873 1313 1045 8.5 1319 1788

a. Run of the Water 644 1006 815 659 820 993

b. Deep Tubewell 103 120 53 36 100 150

c. Low Lift Pump 73 37 38 17 17 24

d. Small & Medium Scale - 82 87 62 296 512

e. operation and Maintenance 53 66 52 51 86 109

5.2 Admin. Inst. Dev. Feasibility Study 27 270 146 170 171 226

5.3 Royal Directive - 57 28 4 0 -

5.4 Credit Program - 110 131 112 71 40

6. Agricultural Services 928 1381 1421 1718/b 1650 2266

6.1 Transport and Input Subsidies 89 278 268 800ag 610 6006.2 Agricultural Credit 263 286 241 213 2677 712a

6.3 Extension and Research 527 635 648 579 657 646

a. Crop Research and Extension 342 399 396 359 428 373

b. Livestock Research and Extension 151 185 214 188 196 224

c. Fishery Research and Extension 34 5i 38 32 33 49

6.4 Research and Marketing 40 59 46 1S 22 46

6.5 Special Crops - 16 91 47 49 66

6.6 Administration 9 93/e 108/f 42Ld 19 1S6Lh

6.7 Cooperatives - 14 19 22 26 40

7. Forestry - - 639 582 785 959

7.1 Community and Private Forestry - - 209 167 220 191

7.2 National and Leasehold - - 197 176 222 289

7.3 Medicinal and Aromatic Plantation - - 13 11 22 35

7.4 Forestry Research and Extension - - 12 13 15 49

7.5 Human Resource Development - - 1 1 2 4

7.6 Soil ano Watershed Conservation - - 49 50 84 106

7.7 Conservation of Ecological Resources - - 152 163 218 274

7.8 Resource Information and Planning - - 6 1 2 11

/a Budget figures/b Includes expenditures under the supplementary budget of Rs.522.04S million

/c Includes subsidies of Rs.S00 million in the supplementary budget

/d Includes supplementary budget of Rs.11.945 million/e Includes Rs.62 million allocated for research coordination

/f Includes Rs.71 million allocated for research coordination

Lg Includes Rs.400 million sector loan.Lh Includes Rs. 61 million for NARC

This has already been reflected in some reductions in the project portfolio,although not yet in overall allocations.

- 86 -

b. Irriaation

5.8 Over one-third of cultivated land in Nepal is irrigated, althoughthere are differences between the Terai on the one hand (over one halfirrigated) and the Mountains and Hills on the other (less than one fifthirrigated) .361 Of the total area irrigated, no less than 71 percent isaccounted for by farmer-owned schemes, and the remaining 29 percent areDepartment of Irrigation (DOI) schemes. Farmer schemes cover about 94 percentof all irrigated area in the Mountains and Hills, but only 65 percent in theTerai. About 95 percent of DOI irrigated area is in the Terai, of which 89percent is included in surface water schemes. This reflects not only thedifference in the availability of irrigable land in the Terai and the Hills,but also the irrigation development potential of the Terai; 2.2 million ha orsome 80 percent of the country's total irrigable area is located in the Terai.

5.9 Irrigation absorbed 10-11 percent of development expenditures inthe eighties, with the bulk of these going to DOI surface and groundwaterschemes; and the planred allocation for the sector unler the EP remains muchthe same, at 10.5 percent. The performance of the irrigation sub-sector incontributing to increased output and farm incomes is mixed. First, since mostschemes are designed to augment monsoon rains for main season paddy, theyessentially provide some insurance against monsoon failure, rather thanleading to significant expansion of irrigated year-round production. Thus,while they are almost certainly highly cost-effective, many of them do notsustain high cropping intensities and high yields. Second, the performance oflarge-scale public irrigation schemes has generally been disappointing. Re-estimated ROR at project completion has most often been less than at appraisaland actual ROR even lower. Kankai irrigation project, for example, had 16percent ROR at appraisal and 5.2 percent at completion, and similarly forSunsari Morang I. Only three out of ten projects recently reviewed had RORabove 10 percent.17/ These low ROR reflect low effective use (area actuallysupplied with water) of large-scale irrigation projects. For example, 12large DOI projects reviewed by the Irrigation Master Plan!-, which togetherhad a planned net command area of about 221,000 ha, had an the average rate ofeffective use of only 57 percent even in the monsoon (Table 5.3).

L See Table 5.7

/ Master Plan for Irrigation Develooment in NeDal, February 1990, Annex Volume 3, Table D3-13.

3/ Master Plan for Irriaation Development in Nepal, February 1990, Annex Volume 2, Annex C2,Table C2-2.

- 87 -

Table 5.3s BFFBCTXVB VBO IN TWELVE LARGE ZRRaATION PROJECTS

Effective Use/aPlanned Net

rype Conumand Area Summer Winter spring

Monsoon- 113,133 0.49 0.13 0.06Irrigated

Year-Round 108,000 0.67 0.36 0.05

Total 221,133 0.57 0.23 0.05

/a "Bffective Use" is the proportion of Net Command Area that is effectively irrigated in theseason indicated.

Source: Table C2-2, Irriaation Master Plan on cit.

Even the year-round schemes achieved an effective use only of 36% and 5S inthe two dry seasons. Thus, the impact of such schemes must be anticipated tobe low. But there have been exceptions. Bhairawa-Lumbini, a large projectbased upon deep tubewells, and Mahakali Stage I, a command area developmentproject with year-round irrigation, have had some measure of success inraising production levels and farmers, incomes. Third, in response to the

problems noted above, increasing attention has been paid to developing small-

scale, farmer managed projects and to involving farmers in all stages ofproject identification, design, construction, operation and maintenance of DOI

schemes. These changes culminated in the new Irrigation Policy 1992, issuedby the Ministry of Water Resources. The preliminary indications are that the

newer style projects are most promising.

Irriaation Exnenditure Patterns

S.10 The Government's approach to irrigation in the past emphasized

large-scale projects. It has paid much less attention to smaller projects, to

managing and maintaining irrigation assets, and to providing training and

support to farmer groups. While the new Irrigation Policy of 1992 proposes to

change the Government's emphasis, the new directions are yet to be reflectedin budget or expenditure patterns, which continue to be dominated by the large

Table 5.4: SIZ8 CLASSIFICATION OF IRRIGATION EXPENITnuR(Re . I °°°)

FY91 FY92 Budget FY93

Expenditure on large projects 770,784 769,061 945,598

Total Bxpenditure 1,529,334 1,544,862 2,054,320

Share of large projects 50.4 49.8 46.0(percent)

* The six large projects are Mahakali, Bhairawa-Lumbini, Bagmati, Babai, Narayani, SunsariMorang.

Source: Table 5.6

- 88 -

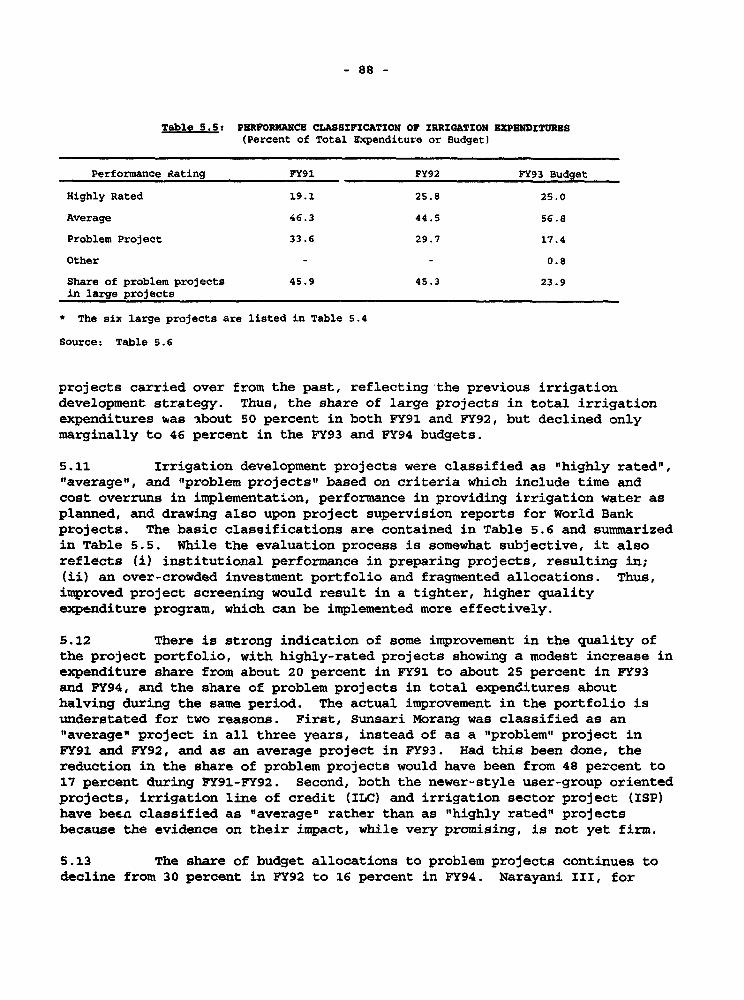

Table 5.5: PERFORMANCE CLASSIFICATION OF XRRI9ATION hXP8NDI$VRUS(Percent of Total Expenditure or Budget)

Performance Rating FY91 FY92 FY93 Budget

Highly Rated 19.1 25.8 25.0

Average 46.3 44.5 56.8

Problem Project 33.6 29.7 17.4

Other - - 0.8

Share of problem projects 45.9 45.3 23.9in large projects

* The six large projects are listed in Table 5.4

Source: Table 5.6

projects carried over from the past, reflecting the previous irrigationdevelopment strategy. Thus, the share of large projects in total irrigationexpenditures was -bout 50 percent in both FY91 and FY92, but declined onlymarginally to 46 percent in the FY93 and FY94 budgets.

5.11 Irrigation development projects were classified as "highly rated","average", and "problem projects" based on criteria which include time andcost overruns in implementation, performance in providing irrigation water asplanned, and drawing also upon project supervision reports for World Bankprojects. The basic classifications are contained in Table 5.6 and summarizedin Table 5.5. While the evaluation process is somewhat subjective, it alsoreflects ti) institutional performance in preparing projects, resulting in;(ii) an over-crowded investment portfolio and fragmented allocations. Thus,improved project screening would result in a tighter, higher qualityexpenditure program, which can be implemented more effectively.

5.12 There is strong indication of some improvement in the quality ofthe project portfolio, with highly-rated projects showing a modest increase inexpenditure share from about 20 percent in FY91 to about 25 percent in FY93and PY94, and the share of problem projects in total expenditures abouthalving during the same period. The actual improvement in the portfolio isunderstated for two reasons. First, Sunsari Morang was classified as an"average" project in all three years, instead of as a "problem" project inFY91 and FY92, and as an average project in FY93. Had this been done, thereduction in the share of problem projects would have been from 48 percent to17 percent during FY91-FY92. Second, both the newer-style user-group orientedprojects, irrigation line of credit (ILC) and irrigation sector project (ISP)have been classified as "average" rather than as "highly rated" projectsbecause the evidence on their impact, while very promising, is not yet firm.

5.13 The share of budget allocations to problem projects continues todecline from 30 percent in FY92 to 16 percent in FY94. Narayani III, for

- 89 -

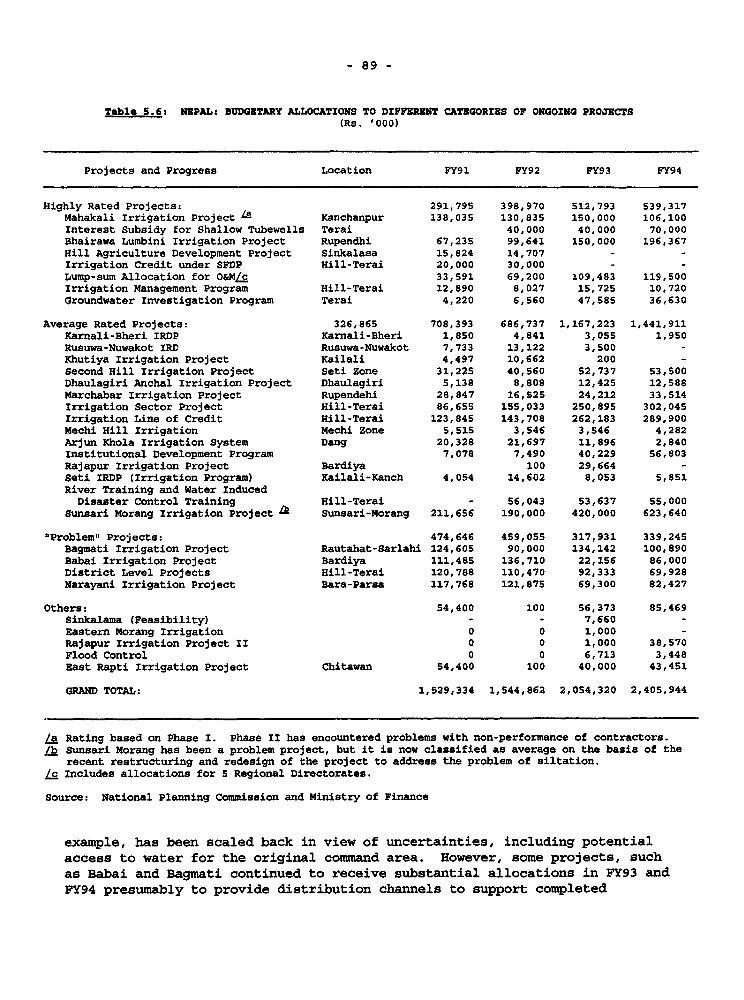

Table 5.6: NEPALs BUDGETARY ALLOCATIONS TO DIFFERENT CATEGORIES OF ONGOrNG PROJECTS(Rs. '000)

Projects and Progress Location FY91 FY92 FY93 FY94

Highly Rated Projects: 291,795 398,970 512,793 539,317Mahakali Irrigation Project l Kanchanpur 138,035 130,835 150,000 106,100Interest Subsidy for Shallow Tubewells Terai 40,000 40,000 70,000Bhairawa Lumbini Irrigation Project Rupendhi 67,235 99,641 150,000 196,367Hill Agriculture Development Project Sinkalasa 15,824 14,707 - -Irrigation Credit under SFDP Hill-Terai 20,000 30,000 - -

Lump-sum Allocation for O&MLc 33,591 69,200 109,483 119,500Irrigation Management Program Hill-Terai 12,890 8,027 15,725 10,720Groundwater Investigation Program Terai 4,220 6,560 47,585 36,630

Average Rated Projects: 326,865 708,393 686,737 1,167,223 1,441,911Karnali-Bheri IRDP Karnali-Bheri 1,850 4,841 3,055 1,950Rusuwa-Nuwakot IRD Rusuwa-Nuwakot 7,733 13,122 3,500 -Khutiya Irrigation Project Kailali 4,497 10,662 200 -

Second Hill Irrigation Project Seti Zone 31,225 40,560 52,737 53,500Dhaulagiri Anchal Irrigation Project Dhaulagiri 5,138 8,808 12,425 12,588Marchabar Irrigation Project Rupendehi 28,847 16,525 24,212 33,514Irrigation Sector Project Hill-Terai 86,655 155,033 250,895 302,045Irrigation Line of Credit Hill-Terai 123,845 143,708 262,183 289,900Mechi Hill Irrigation Mechi zone S,515 3,546 3,546 4,282Arjun Khola Irrigation System Dang 20,328 21,697 11,896 2,840Institutional Development Program 7,078 7,490 40,229 56,803Rajapur Irrigation Project Bardiya 100 29,664 -Seti IRDP (Irrigation Program) Kailali-Kanch 4,054 14,602 8,053 5,851River Training and Water InducedDisaster Control Training Hill-Terai - 56,043 53,637 55,000

Sunsari Morang Irrigation Project Z Sunsari-Morang 211,656 190,000 420,000 623,640

"Problem" Projects: 474,646 459,055 317,931 339,245Bagmati Irrigation Project Rautahat-Sarlahi 124,605 90,000 134,142 100,890Babai Irrigation Project Bardiya 111,485 136,710 22,156 86,000District Level Projects Hill-Terai 120,788 110,470 92,333 69,928Narayani Irrigation Project Bara-Parsa 117,768 121,875 69,300 82,427

Others: 54,400 100 56,373 85,469Sinkalama (Feasibility) - - 7,660 -Eastern Morang Irrigation 0 0 1,000 -

Rajapur Irrigation Project II 0 0 1,000 38,570Flood Control 0 0 6,713 3,448East Rapti Irrigation Project Chitawan 54,400 100 40,000 43,451

GRAND TOTAL: 1,529,334 1,544,862 2,054,320 2,405,944

/a Rating based on Phase I. Phase II has encountered problems with non-performance of contractors.lb Sunsari Morang has been a problem project, but it is now classified as average on the basis of the

recent restructuring and redesign of the project to address the problem of siltation./c Includes allocations for S Regional Directorates.

Source: National Planning Commission and Ministry of Finance

example, has been scaled back in view of uncertainties, including potentialaccess to water for the original command area. However, some projects, suchas Babai and Bagmati continued to receive substantial allocations in FY93 andFY94 presumably to provide distribution channels to support completed

- 90 -

headwork. Allocations for District level projects declined oteadily sinceFY91; these district have projects sufferred from fragmentation of financingamong too many sub-projects. In F':92, for example, over 75 percent of schemeswere allocated less than Rs.500,000, which was too small to support meaningfulconstruction. There is little documentation of their economic viability, andsome of the allocations represent routine administrative expenses which shouldbe classified appropriately as regular expenditures. The Government and somedonors have reviewed and scaled back selected irrigation projects. 3 9 /However, there is still some scope for shifts in resources away from lowquality projects. For example, the number of district level projects, exceptthose already close to completion, could be cut back; even redesigned projectssuch as Narayani should continue to be monitored for possible cancellation ifappropriate, and pending action should be taken on other projects consideredproblematic. Also, experience would warrant restrictions on new large-scalestate-managed project starts.

Institutional Development and Maintenance

5.14 Policy statements and sector studies have called for a shift inthe approach to irrigation development.-0/ Tl shift would: (i) emphasizesmall- and medium-scale farmer managed rather than large-scale schemes;(ii) change Government focus from physical investment expansion to irrigationmanagement; (iii) support private sector participation in irrigation schemes,including turnover of suitable publicly managed schemes to the private sector;and (iv) build institutional support for irrigation management and stressmaintenance of projects. There is awareness that the new priorities requiretransforming the role of Government agencies, and efforts to provide suchinstitutional reform are being made. The Irrigation Management ProjeoLstarted in 1985, for example, is concerned with supporting farmerorganizations and providing them with management training and improvingjresource mobilization, including cost recovery. The Irrigation Ma'iAgement and.ater Utilization Division of the Department of Irrigat.i.n was established inOctober 1991 (as a successor to the Ministry of Agriculture's FarmerIrrigation and Water Utilization Division), and this institutionalized theIrrigation Management Project. Initially, two agencies, namely, the SystemManagement Division (SMD) and Irrigation Management Center (IMC) wereestablished; but the fact that they were created outside the regulargovernment structure limited their acceptance as part of the normalorganizational set-up of the DOI. The merging of SMD and IMC and the officialestablishment of the Irrigation Management and Water Utilization Divisionwithin DOI provides it with the capacity and the opportunity to takeinitiative on the main issues, such as expenditure reforms, user fees,

-/This saved an estimated US$50 million, comprising US$8 million from Second Hill Project,US$21 million from East Rapti, and US$21 million from Irrigation Sector Loan.

40/ See, for example, "The Irrigation Management Project"; USAID, 1991. "Topics Paper on O0MStatus of Selected Large Scale Irrigation Projects", HMG, 1991. "Action Plan for ParticipatoryManagement Program", HMG, 1989. "Irrigation Directive", HMG, 1989. "The Role of ProgramBudgeting in the Development of the FY89 Irrigation Budget", HMG, 1988. "Irrigation Policy",1992, HMG, Ministry of Water Resources.

- 91 -

financing and monitoring of O&M activities, training farmers and expandingfarmer-managed schemes.

5.15 Given that Government currently has direct responsibility foroperating and maintaining large schemes covering over 250,000 hectares ofirrigation system, a strategy and program to support priority O&M needs to beadopted. Financing support for O&M activities increased in nominal terms asshown in Table 5.7; but the share of allocations for system utilization andmaintenance has been about 11.2 percent during FY88-92. Expenditures onroutine maintenance were 5.7 percent of recurrent expenditures during the sameperiod. Thus the financing of needed spare parts and materials has suffered,as personnel costs alone accounted for 48 percent of the O&M cost per ha inFY91 compared to 23 percent in FY89.4/ During the period FY88-FY92,budgetary allocations for system utilization averaged Rs. 126 per ha, under 25percent of estimated optimal requirements of Rs. 520 per ha. Moreover, theweak expenditure reporting system undermines the ability to monitor and ensurethat budgeted funds are utilized as envisaged.

Table 5.7: NEPAL: BUDGET ALLOCATIONS FOR IRRIGATION(Rs. Million)

FY88 FY89 FY90 FY91 FY92 FY93/a

Budgetary Allocations

1. Recurrent Budget Allocation 109 279 339 337 379(a) Administration 96 199 274 338 301 -

of which: Salary & Allowances 58 75 81 97 126 -(b) System Utilization & Maintenance 16 21 18 34 69 -

of which: Repair & Maintenance 11 13 11 8 31 -(c) Other Recurrent Budget 7 66 58 39 79 -

1(i) System Utilization & Maintenance (%) 1.8 1.2 1.3 2.1 4.4 -1(ii) Repair & Maintenance (%) 1.2 0.7 0.8 0.5 2.0

2. Capital Budget Allocation 790 1471 1025 1210 1192(a) Rehabilitation & Construction 730 1389 956 1185 1133(b) Purchase of Land Building 41 55 41 15 31(c) Equipment & Vehicles 19 27 28 10 28 -

3. Total Budget Allocation 899 1756 1364 1587 1571 2054

/a Budget

Source: Compiled from MOD data

-/ Based on a simple survey conducted by DOI on selected irrigation systems in the KathmanduValley.

- 92 -

c. Irriaation Credit and Subsidies

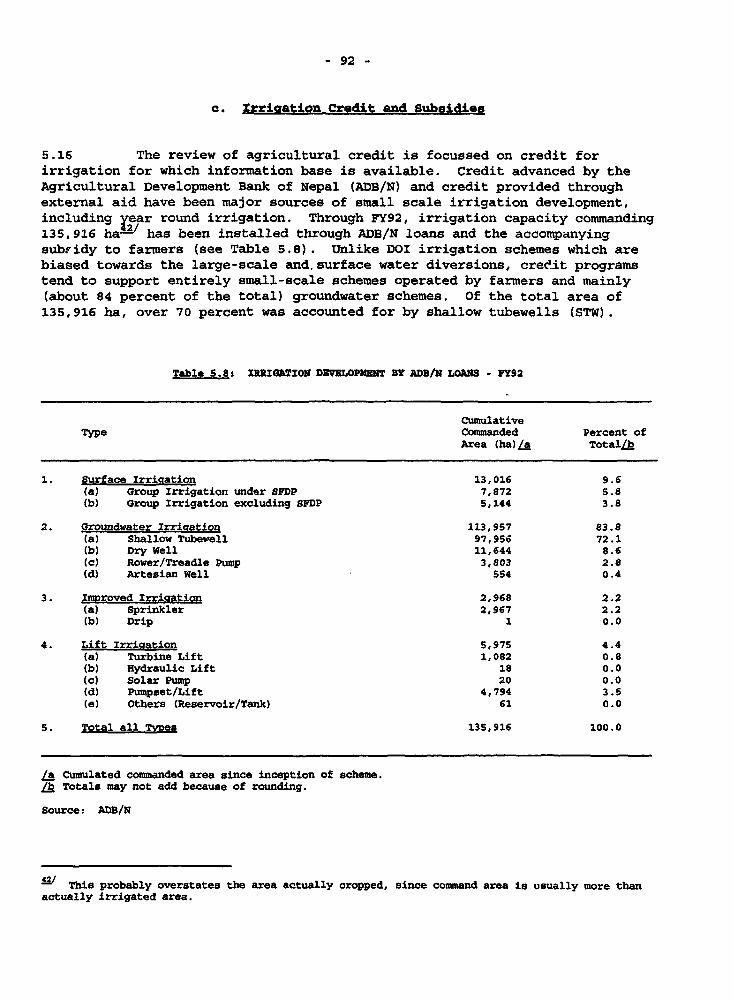

5.16 The review of agricultural credit is focussed on credit forirrigation for which information base is available. Credit advanced by theAgricultural Development Bank of Nepal (ADB/N) and credit provided throughexternal aid have been major sources of small scale irrigation development,including vear round irrigation. Through FY92, irrigation capacity commanding135,916 ha 2/ has been installed through ADB/N loans and the accompanyingsubridy to farmers (see Table 5.8). Unlike DOI irrigation schemes which arebiased towards the large-scale and,surface water diversions, creeit programstend to support entirely small-scale schemes operated by farmers and mainly(about 84 percent of the total) groundwater schemes. Of the total area of135,916 ha, over 70 percent was accounted for by shallow tubewells (STW).

Table 5.8s :RRIGATION DIVULOPUHET BY ADB/N LOANS - PY92

CumulativeType Commanded Percent of

Area (ha)la Total/b

1. Surface Irrication 13,016 9.6(a) Group Irrigation under SFDP 7,872 5.8(b) Group Irrigation excluding SFDP 5,144 3.8

2. Groundwater Irrication 113,957 83.8(a) Shallow Tubevell 97,956 72.1(b) Dry Well 11,644 8.6(c) Rower/Treadle Pump 3,803 2.8(d) Artesian Well 554 0.4

3. Imroved Irrigation 2,968 2.2(a) Sprinkler 2,967 2.2(b) Drip 1 0.0

4. Lift Irrigation 5,975 4.4(a) Turbine Lift 1,082 0.8(b) Hydraulic Lift 18 0.0(c) Solar Pump 20 0.0(d) Pumpset/Lift 4,794 3.5(e) Others (Reservoir/Tank) 61 0.0

5. Total all Tvyes 135,916 100.0

/a Cumulated commanded area since inception of scheme.lb Totals may not add because of rounding.

Source: ADB/N

iv This probably overstates the area actually cropped, since command area is usually more thanactually irrigated area.

- 93 -

Table 5.9s RATE OF RETURN TO ADB/N IRRIGATZON SCREU38jA(Percent)

Hill Terai Overall

Surface 26.q 67.6 47.2

STW - 40.6 40.6

La The IRR reported in the Table are the financial rates of returnwhich are lower than the economic rates of return calculated byIIMI (see Footnote 10). These IRR assume the opportunity costof farmer labor contributed to the construction of the surfaceschemes is half the minimum wage rate, and the investment costsare not reduced by the amount of the Government subsidy.

Source: Tables 5.6 and 5.9 in IIMI, Proces' and PerformanceEvaluation of ADB/N Sunnorted Irrigation Schemes, op cit

5.17 Evaluations conducted recently by The Internatiornal IrrigationManagement Institute (IIMI) on the economic performance of the irrigation sub-projects financed by ADB/N,43/ particularly the farmer-managed small surfaceirrigation schemes and the STW loans to farmers, indicate that the rates ofreturn (even without the government subsidies) are high, being about (i) 48percent for STW in the Terai; and (ii) 27 percent and 68 percent for surfaceschemes in the Hills and Terai respectively (see Table 5.9). Theseinvestments are profitable without subsidies. However, for surface schemes,the government provides over 70 percent of total construction costs, and 40percent (increased to 50 percent recently for a few months due to droughtconditions in FY93) for private STW.>1/ The subsidy rate is 8b percent forcommunity STW and 90 percent for new deep tubewells as well as for surface andgroundwater schemes constructed by government and turned over to water users'groups.

~/ The evaluation is more concerned with the sub-projects Per se, rather than with the lendingactivities of the ADB/N or of the SPDP. That is, it focuses mainly on the investment process,its impact upon agricultural output, and its economic and financial rates of return. Evaluatingthe lending activities, which would focus upon lending costs, loan servicing and other financialcriteria of a credit activity, was only partially undertaken. See Process and PerformanceEvaluation of ADB/N SuDvorted Irrication Schemes, Intarnational Irrigation Management Institute,Kathmandu, Nepal, 1991. It might be noted that, in calculating economic rates of return,international prices of commodities (which were about 1.7 times the financial prices) wereemployed. It can be argued that, because of the porous border with India, financial prices (whichreflect prices in India) are the appropriate border prices (in the sense of measuring opportunitycosts) for an economic evaluation in Nepal. For this reason, the financial rates of return(after netting out subsidies) which are also provided in the evaluation study are probably thebest indication of social or economic rates of return.

L/ These different subsidy rates on construction costs are intended to reflect to some extentthe very different operations and maintenance costs relative to construction costs of differentforms of irrigation. However, it is not clear that the actual subsidy formula employed is suchas effectively to equalize costs or shares or costs paid by farmers and government over differenttypes of irrigation. More generally, it is not clear that an appropriate formula should seek toequalize costs: there is a case for more expensive forms of irrigation, and for poorbeneficiaries paying less than richer.

- 94 -

5.18 Demand for new private STW, which has been about 3,000 units ayear in normal years and 6,000 in drought years, accelerated greatly in FY93with the increase in the subsidy to 50 percent for STW. ADB/N has receivedloan applications for more than double the number of STW which it can provideunder the constraint of the subsidy budget, and the subsidy fund was exhaustedduring the first six months. While the return on STW is high even without thesubsidy, farmers understandably prefer to wait to receive a loan with thesubsidy. But there is a ceiling on the subsidy fund, and it is not enough tosupport the implementation of the subsidy program.

5.19 The subsidy policy for STWs is not achieving its intendedobjectives, and it should be reviewed. Irrigation expansion under ADB/N withsmall-scale surface water schemes and STWs has high social and individualrates of return, but it is constrained by the subsidy policy and the limitedsubsidy budget. The whole subsidy scheme needs to be reviewed in order toadopt a consistent approach for all forms of irrigation. The subsidy levelsneed to take account of farmers' ability to pay; despite the high IRR, manylow income beneficiaries produce almost entirely for subsistence and,therefore, do not generate cash surpluses to service a loan on commercialterms. Finally, there is a need to emphasize expansion to community STWs.Given the small average size of holdings in the Terai and the fragmentation ofmost holdings, continued expansion of STWs will increasingly require thesharing of installations by user groups.

d. Fertilizer

Backaround

5.20 Fertilizer consumption has grown at an average annual rate of 11-13 percent over the past one and a half decades (FY75-FY90). In more recentyears, (FY90-FY92) this growth declined to 8.5 percent. Total fertilizersales amounted to 18S,422 metric tons in FY92 with urea accounting for 49.3percent of sales in the eighties, though has increased more recently to over70 percent. Complex (20:20:0) fertilizer accounts for 35.5 percent in theeighties; DAP 9.5 percent; and MOP and Ammonium Sulphate account for the rest.Currently, the Government is instituting a program to encourage farmers toshift from complex to DAP, which has higher nutrient content and, therefore,lower transportation costs per unit of nutrient. While fertilizer consumptionhas grown, Nepal has remained one of the lowest consumers of chemicalfertilizers. The application of fertilizer nutrient per ha is less than athird that of Bangladesh and about a fifth that of China.!J There are widedisparities in fertilizer consumption among regions. For example, fertilizersales in the Kathmandu Valley per ha of cropped land are 6.9 times thenational average; sales are equivalent to 1.2 times the national average in

-5/ Plant nutrient in Kg per ha is estimated at 23.2 for Nepal, 51.7 for India, 77 forBangladesh, 109.4 for Sri Lanka and 236.1 for China, batsed on data for FY87/88. See World Bank,World Development Renort. 199i, page 210. Data obtained from AIC sources.

- 95 -

the Terai, and half the national average in the Hills. 46t Fertilizerdistribution has been marked by shortages during the planting season in allparts of the country.

Fertilizer Issues

5.21 Fertilizer issues are well recognized as Government and donorshave sponsored detailed research on the subject. 47/ Options for reform havebeen debated extensively and some progress has been made in improving thedistribution system. For example, adjustments in fertilizer prices have beenused to control smuggling to India; subsidy levels were reduced, through theyare still high for urea; and most recently, the import and distribution offertilizer was opened in principle to the private sector. Despite the changesin declared policy, the fundamental difficulties of the fertilizerdistribution system have persisted. There is awareness that expanded accessto fertilizer, packaged appropriately with other necessary inputs andpolicies, offer substantial scope to increase agricultural productivity andgrowth. The main background factors causing the shortages, particularlyduring the planting season, and the low consumption were as follows.

e Until recently, all chemical fertilizers were imported by theGovernment or obtained through commodity aid. Aid accounts forabout 50 percent of supplies, and the scheduling of Government'sown imports often did not ensure delivery in time for the start ofthe planting season. The import and wholesale distribution offertilizer were controlled by a state monopoly, the AgriculturalInputs Corporation (AIC). Retail distribution was dominated bystate-sponsored cooperatives, many of which are inefficient, butare protected by preferential policies. The private sectorparticipated to a very minor extent in fertilizer retailing, butnot in imports or wholesale distribution. Subsequently, theprivate sector was permitted to compete with cooperatives inreceiving supplies from AIC, except if a shortage existed. Policymakers argued that private traders cannot be trusted to adhere tothe fixed retail price if supplies are short. Because shortageshave been the rule rather than the exception, little scope forprivate traders was left by this form of liberalization.

* Quantitative restrictions were used in the management offertilizer distribution, despite some liberalization initiativesin the late eighties. AIC rationed available stock on the basis

In 1990, fertilizer sales per cropped area was estimated 438.5 Kg national average, 334 Kg inthe Kathmandu Valley, 60.3 Kg in the Terai; 28.8 Kg for the accessible areas in the Hills, and 15Kg in the remote areas.

-ii See, for example, "Nepal: Fertilizer Sector Management Studyu, April 1991; N.H. Dhakal,"Economics of Fertilizer Use, Allocative Error and Adoption in Nepal", May 1989. "Nepal:Fertilizer Distribution Issues", ASICO Working Paper, July 1988; "Fertilizer Distribution,Pricing and Subsidy", AID Planning Unit, March 1988; M.S. Wallace, "Fertilizer Price Policy inNepal:, USAID, November 1986; Gerald J. Gill and Davika Tamang, "The Present Situation withRespect to Private Sector Fertilizer Imports", Winrock International, Kathmandu, February 1993.

- 96 -

of targets and requests from zonal officials, and dealers wererestricted to distributing in designated zones.

Fertilizer prices were controlled and the administered pricescarried large subsidies, though existing studies suggest thataccess to fertilizer has to do less with price increases and morewith inadequate supply delivery on a timely basis. In FY91, forexample, the administered prices in Nepal were close to thecorzesponding Indian border prices; but because Indian prices weresubsidized below world market prices, Nepal's prices were alsosubsidized and were equivalent to 42 percent of actual costs forurea and 53 percent for complex, which together accounted for over80 percent of fertilizer sales. The direct subsidies allocated inthe Government budget for AIC to finance fertilizer purchases,excluding financial sector credit and unpaid bills, were Rs.733million in FY91, and Rs.610 million in FY92, equivalent to 37percent of the total development expenditure allocations foragricultural services; it declined to Rs.600 million in FY93.Under the pricing and subsidy policy which existed untilrecently,L- budgetary difficulties and limited Governmentcapacity to support the financing of the subsidy were majorconstraints on AIC's imports and on fertilizer supply. This ledto the paradoxical situation that the subsidies, which wereintended to increase fertilizer consumption by encouraging demand,actually acted as a brake on consumption by restricting supply.

Nepal's policies regarding fertilizer pricing are circumscribed toa large extent by policies in India, both at the central and stategovernment level. Under the policy which has been in effect fromthe late eighties, Nepal's fertilizer prices were to be adjustedto equal the corresponding prices at the border with India.However, because India's fertilizer is subsidized below worldprices, Nepal's existing policy of Indian border price paritystill involves substantial subsidies.

Recent Reforms and Future Action

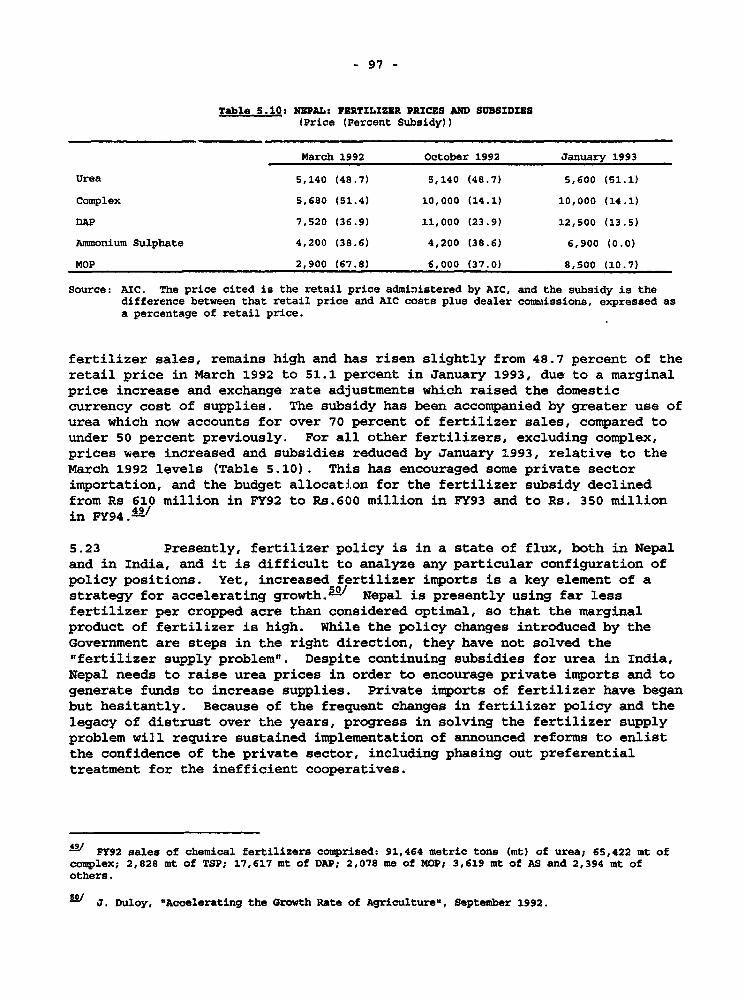

5.22 Government took some steps to liberalize Nepal's fertilizer marketin October 1992. Under these reforms: (i) the import of fertilizers would beon open general license; (ii) price controls would be abolished for allfertilizers, except urea and ammonium sulphate (which together account for 50percent of total sales); (iii) foreign exchange would be provided to theprivate sector at the official rate (equivalent to an implicit subsidy of 15percent relative to the free market exchange rate) for the import offertilizers; and (iv) the Government would phase out the remaining subsidiesgradually. As shown in Table 5.10 below, the reforms generally resulted inhigher prices and lower subsidies. The subsidy on urea, over 40 percent of

IV It is not yet clear whether or not recent policy changes will materially affect the situationdescribed in the text.

- 97 -

Table 5.10: NEPAL: FERTILIZER PRICES AND SUBSIDIES(Price (Percent Subsidy))

March 1992 October 1992 January 1993

Urea 5,140 (48.7) 5,140 (48.7) 5,600 (51.1)

Complex 5,680 (51.4) 10,000 (14.1) 10,000 (14.1)

DAP 7,520 (36.9) 11,000 (23.9) 12,500 (13.5)

Ammonium Sulphate 4,200 (38.6) 4,200 (38.6) 6,900 (0.0)

MOP 2,900 (67.8) 6,000 (37.0) 8,500 (10.7)

Source: AIC. The price cited is the retail price administered by AIC, and the subsidy is thedifference between that retail price and AIC costs plus dealer commissions, expressed asa percentage of retail price.

fertilizer sales, remains high and has risen slightly from 48.7 percent of theretail price in March 1992 to 51.1 percent in January 1993, due to a marginalprice increase and exchange rate adjustments which raised the domesticcurrency cost of supplies. The subsidy has been accompanied by greater use ofurea which now accounts for over 70 percent of fertilizer sales, compared tounder 50 percent previously. For all other fertilizers, excluding complex,prices were increased and subsidies reduced by January 1993, relative to theMarch 1992 levels (Table 5.10). This has encouraged some private sectorimportation, and the budget allocation for the fertilizer subsidy declinedfrom Rs 610 million in FY92 to Rs.600 million in FY93 and to Rs. 350 millionin FY94.9-/

5.23 Presently, fertilizer policy is in a state of flux, both in Nepaland in India, and it is difficult to analyze any particular configuration ofpolicy positions. Yet, increased fertilizer imports is a key element of astrategy for accelerating growth.'/ Nepal is presently using far lessfertilizer per cropped acre than considered optimal, so that the marginalproduct of fertilizer is high. While the policy changes introduced by theGovernment are steps in the right direction, they have not solved the"fertilizer supply problem". Despite continuing subsidies for urea in India,Nepal needs to raise urea prices in order to encourage private imports and togenerate funds to increase supplies. Private imports of fertilizer have beganbut hesitantly. Because of the frequent changes in fertilizer policy and thelegacy of distrust over the years, progress in solving the fertilizer supplyproblem will require sustained implementation of announced reforms to enlistthe confidence of the private sector, including phasing out preferentialtreatment for the inefficient cooperatives.

if/ FY92 sales of chemical fertilizers comprised: 91,464 metric tons (mt) of urea; 65,422 mt ofcomplex; 2,828 mt of TSP; 17,617 mt of DAP; 2,078 me of MOP; 3,619 mt of AS and 2,394 mt ofothers.

/ J. Duloy, "Accelerating the Growth Rate of Agriculture", September 1992.

- 98 -

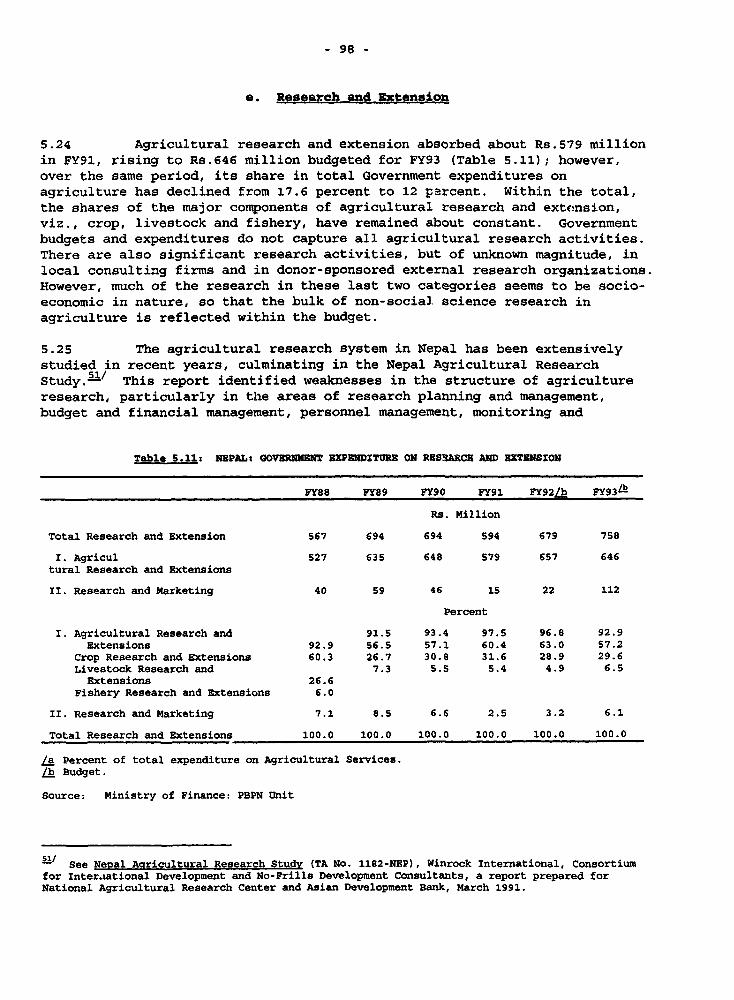

e. Research and Extension

5.24 Agricultural research and extension absorbed about Rs.579 millionin FY91, rising to Rs.646 million budgeted for FY93 (Table 5.11); however,over the same period, its share in total Government expenditures onagriculture has declined from 17.6 percent to 12 parcent. Within the total,the shares of the major components of agricultural research and extcnsion,viz., crop, livestock and fishery, have remained about constant. Governmentbudgets and expenditures do not capture all agricultural research activities.There are also significant research activities, but of unknown magnitude, inlocal consulting firms and in donor-sponsored external research organizations.However, much of the research in these last two categories seems to be socio-economic in nature, so that the bulk of non-social science research inagriculture is reflected within the budget.

5.25 The agricultural research system in Nepal has been extensivelystudied in recent years, culminating in the Nepal Agricultural ResearchStudy. 51 This report identified weaknesses in the structure of agricultureresearch, particularly in the areas of research planning and management,budget and financial management, personnel management, monitoring and

Table S.11: NEPAL: GOVERMNT EXENDITR ON RESa8CR AND XTESNSION

FY88 FY89 PY90 FY91 FY92/b FY93b

Rs. Million

Total Research and Extension 567 694 694 594 679 758

I. Agricul 527 635 648 579 657 646tural Research and Extensions

II. Research and Marketing 40 59 46 15 22 112

Percent

I. Agricultural Research and 91.5 93.4 97.5 96.8 92.9Extensions 92.9 56.5 57.1 60.4 63.0 57.2

Crop Research and Extensions 60.3 26.7 30.8 31.6 28.9 29.6Livestock Research and 7.3 5.S 5.4 4.9 6.5

Extensions 26.6Fishery Research and Extensions 6.0

II. Research and Marketing 7.1 8.5 6.6 2.5 3.2 6.1

Total Research and Extensions 100.0 100.0 100.0 100.0 100.0 100.0

/a Percent of total expenditure on Agricultural Services./b Budget.

Source: Ministry of Finance: PBPN Unit

-1/ See Nepal Agricultural Research Studv (TA No. 1182-NEP), Winrock International, Consortiumfor Inter.iational Development and No-Frills Development Consultants, a report prepared forNational Agricultural Research Center and Asian Development Bank, March 1991.

- 99 -

evaluation, and research outreach programs. The Government has accepted inprinciple the main recommendations of this report. The main thrusts of reformare to: (i) reconstitute the Nepal Agricultural Research Council (NARC) intoan autonomous organization with authorit-y to strengthen agricultural researchactivities; (ii) decentralize research programs to give more responsibilitiesto the divisions; (iii) provide regional and district research centers morescope to set research priorities in response to farmers' needs;(iv) strengthen NARC's capacity to evaluate, monitor and coordinate programs;(v) identify opportunities for the growth of private agro-enterprises anddevelop research programs to support them; and (vi) restructure and unifyextension services to complement reforms in agricultural research.L' TheGovernment has taken steps to implement proposed measures to enhance themanagerial autonomy of NARC. NARC needs to take full advantage of increasedautonomy to develop effective and well-justified research programs, and toreallocate its resources to achieve the objectives. This leadership isnecessary to warrant increased resources to agricultural research.

5.26 In the extension area, Government is taking steps to streamlinevarious activities and improve their performance. For example, extensionservices have now been reconstituted under a new department, and close to 30activities were consolidated in the FY94 budget in order to reduce duplicationand waste. Also, the share of allocation to fully Government funded programs,which have less supervision was reduced from 17 percent of the FY93 budget to14 percent in FY94. However, more expenditure management issues remain to beaddressed in order to enhance the performance of resources channelled toextension. First, state farms engaged in production and distributionactivities, such as in fisheries, seedlings and nurseries, which are alreadybeing undertaken by the private sector, need to be phased out in order to putmore resources into research and extension. In this regard, recent Governmentaction to lease out six state farms to the private sector is in the rightdirection. In addition, a privatization cell has been established in theMinistry of Agriculture to assess and imple;nent options for leasing out anddivesting state farms. In this connection steps could be taken to expand therole of the private sector in delivering suitable extension services, such asveterinary services. Second, many ac;.;vities are funded every year withouttermination. Some of them, including regional agricultural directorate,training centers and horticultural farms appear to be recurrent in nature.While these activities have been recently consolidated, it would makeallocations transparent, if they are appropriately classified under the"regular" budget. Third, more financing needs to be provided to supportoutreach programs for farmers. Facilities requiring more financing includeTA/DA and transportation. The need for new infrastructure for offices andstations requires to be reviewed in order to release resources to financethese support services for outreach programs.

The Government has recently announced an intention to pilot-test other approaches toextension, particularly through the private sector. See Garesh B. Thapa and Tek B. Thapa, oncit.

- 100 -

f. Liveotock

5.27 Officially, livestock account for almost 30 percent ofagricultural sector GDP, 15 percent of total GDP, and is dominated by milk andmilk products (54 percent) and meat (26 percent). Exports of live animals,hides and skin accounted for over 10 percent of merchandise exports.Agricultural activity, especially in the Hills, is linked closely withlivestock which are important for transport, producing manure to maintain thefertility of the land, meat, dairy and clothing. The most high valuedlivestock are cattle (over 6 million), buffalo (over 3 million), goat (over 5million) and sheep (under 1 million). Officially, average growth of livestockvalue added was estimated at 4-5 percent during FY81-FY90, originating mainlyfr.... poultry and eggs. The growth of the total animal population has remainedunchanged or declined since the mid-eighties at -0.2 percent for cattle, 1.1percent for buffalo and 1.7-2.5 percent for goats and sheep. Diminishingfodder supply and malnourishment are the main causes of low growth. Openaccess to communal land has contributed to over-grazing, and small farm sizeslimit the scope for allocating more individual holding for livestockexpansion. 53

Expenditure Priorities

5.28 Concerns about land degradation and the limited scope forproviding more land for livestock expansion have renewed debate on asustainable livestock development strategy and the role of Governmentexpenditure programs in that regard. Current thinking in Nepal stresseslimiting increases in the livestock population, while promoting increases inlivestock productivity through research and reforms.-/ Reform policiescall for consolidating major livestock research work under the NARC,restructuring the Dairy Development Corporation (DDC) to improve itsperformance and promoting private sector expenditures on livestock activitiesthrough deregulation. Measures to promote livestock development are toemphasize (i) preventive health, focusing on animal nutrition and foddersupply; (ii) breeding and curative health care; and (iii) livestockmanagement.

5.29 The share of livestock from the agricultural research budget hasremained more or less at 30 percent since FY90, but it declined in real terms(based on GDP deflator) at an average rate of 8 percent during FY90-93.W'Less than 5 percent of the livestock research and extension budget wasallocated to pasture development in only ten districts in recent years,

_/ Typical farm size is 2-3 ha in the Terai and 0.5 ha in the Hills, an estimated 40% of Hillfarms are o.s ha.

-/ Current policies are discussed in detail in Master Plan for Livestock Development 1992; DairyDevelopment Master Plan, 1991; Livestock Research Under NARC, in Nepal Agricultural Researchstudy, 1991.

Sf/ FY93 deflator is based on expected inflation of 10%.

- 101 -

despite the importance attached to fodder development. Livestock wouldreceive the equivalence of 13 percent of allocations for agricultural servicesunder the EP; this is virtually unchanged from the ratio of 13.5 percentduring FY88-FY92. Increased allocations would require a research program inthe priority area of fodder supply. Measures to expand the role of theprivate sector in livestock development need to be developed and adopted. Onearea is in the delivery of veterinary services. Measures proposed under theTen-Year Dairy Development Plan to commercialize the Dairy DevelopmentCorporation and expand the supply of dairy products need to be implementedwithout creating new public enterprises in the manufactrring sector. Therecord of poor performance of public manufacturing enterprises andprivatization measures already underway, would suggest that new publicinvestments in manufacturing be limited and new projects be promoted forprivate sector investment and management control.

g. Forestrv

Introduction and Backcrround

5.30 Forestry is the source of at least 11 percent of agricultural GDP.It provides about 74 percent of national energy use, and is a source of foddersupply for livestock, which accounts for over 40 percent of farm income in theMid-Hills and High-Hills. Over the past decades Nepal has faced problems offorestry degradation related to limited energy alternatives and a pressingdemand for fuelwood, growing pressure on agricultural land from populationgrowth as well as from increased livestock numbers on grazing lands, illegalfelling of timber and lack of forest resource management. There is greaterpressure on accessible forests, as close to 50 percent of forest cover isestimated to be in the remote middle Hills. An estimated 19 percent of forestcover was lost in the Terai with economic expansion in the seventies andeighties, and nation-wide deforestation was then estimated at about 4 percent,one of the highest in South Asia.1/ Though Government proposed variousforest plans since the start of the sixties, it was not until the earlyeighties that forestry development began to receive some attention.

Sector Obiectives and Stratec*v

5.31 The broad objectives of the Forestry Master Plan (1989) and themore recent EP (1993-1997) are to:

Meet the basic needs of the people for forest products in asustained fashion;

O other countries which have experienced serious deforestation problems include Sri Lanka (3.5percent) and Thailand (1.6 percent). See World Bank, "Strategy For Forest Sector Development inAsia", 1992; pages. 2-5.

- 102 -

O Classify forests under different management for production and forprotection to foster efficient forest resource utilization whileimproving environmental quality;

* Increase the supply of industrial raw materials throughagro-forestry and industrial forestry, and increaseincomes and employment of the rural poor;

* Protect watersheds from environmental damage andprotect forest resources from destruction and overuse by peopleand livestock.

Within this framework, the approach to forestry development under the EPinvolves a variety of institutional arrangements. These include broadbasedparticipation through community and user group management, private leaseholds,improved market-oriented management of state forests and improved statemanagement of protected areas.

5.32 The increased attention being paid to forestry development isreflected in rising resource allocations to the sector. There have been some125 projects so far, sponsored jointly by HMG, 28 major donors and 40 otheragencies, including NGOs. In FY93, for example, HMG and foreign allocationstotalled US$10 million each, representing a 50 percent increase in the last 4years. Overall Government expenditures on the sector have risen from 2.7percent of total Government expenditures in FY80 to 3.2 percent by the end ofthe decade, and forestry was allocated 4.7 percent of development resourcesunder the EP. The expenditure pattern of Table 5.12 conveys the main emphasisof forestry development. Three program areas, namely, Community Forestry (29percent), National and Leasehold Forestry (30 percent), and Conservation ofEcosystems and Genetic Resources (26 percent), accounted for 80 percent ofsector allocations during FY90-FY93. While initially, Community programs wereexpected to absorb over 45 percent of sector allocations under the EP, thefirst year (FY93) allocation shows a lower share of 19 percent, as humanresource development needs and the needs of resource information and planningsupport for forestry programs received increased attention, particularly fromexternal funding sources.

Sector Performance, Priorities and Adiustments

5.33 It is difficult to assess quantitatively the performance offorestry projects and programs, (i) in the absence of systematic evaluation ofthe impact on the environment, forest productivity and other sectorobjectives; (ii) lack o effective monitoring of the imiplementation ofprojects; and (iii) poor project accounts. However, there are preliminaryindications that while intra-sectoral expenditures conform broadly to sectorstrategy and objectives, performance has generally been below expectation invarious respects. Thus, new policies for developing the sector were just madeunder the Forestry Act of 1993, and the By-Laws which will guide sectoractivities and programs are now under preparation.

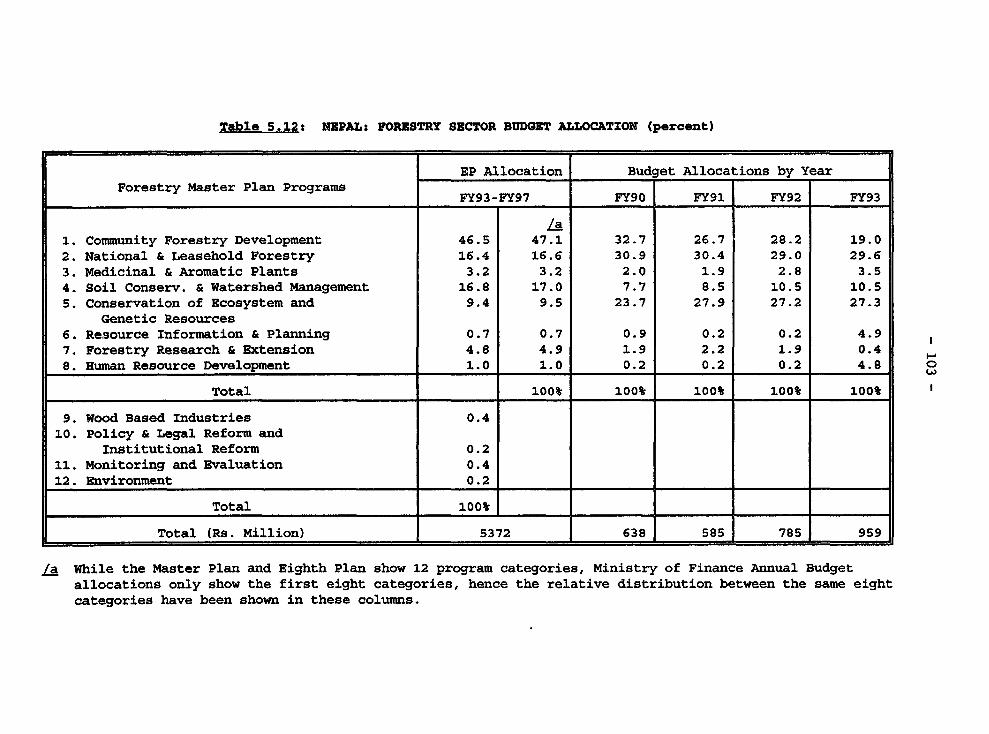

Table 5.12s NEPAL: FORESTRY SECTOR BtDGET ALLOCATXON (percent)

EP Allocation Budget Allocations by Year

Forestry Master Plan Programs FY93-FY97 FY90 FY91 FY92 FY93

/a1. Community Forestry Development 46.5 47.1 32.7 26.7 28.2 19.0

2. National & Leasehold Forestry 16.4 16.6 30.9 30.4 29.0 29.6

3. Medicinal & Aromatic Plants 3.2 3.2 2.0 1.9 2.8 3.5

4. Soil Conserv. & Watershed Management 16.8 17.0 7.7 8.5 10.5 10.5

S. Conservation of Ecosystem and 9.4 9.5 23.7 27.9 27.2 27.3

Genetic Resources6. Resource Information & Planning 0.7 0.7 0.9 0.2 0.2 4.9

7. Forestry Research & Extension 4.8 4.9 1.9 2.2 1.9 0.4

8. Human Resource Development 1.0 1.0 0.2 0.2 0.2 4.8 0

Total t100% 100 100% 100% 100%

9. Wood Based Industries 0.4

10. Policy & Legal Reform andInstitutional Reform 0.2

11. Monitoring and Evaluation 0.4

12. Environment 0.2

Total 100%_

Total (Rs. Million) 5372 638 585 785 959

ja While the Master Plan and Eighth Plan show 12 program categories, Ministry of Finance Annual Budget

allocations only show the first eight categories, hence the relative distribution between the same eight

categories have been shown in these columns.

- 104 -

5.34 The major problem is weak implementation and low resourceabsorption. For example, only 65 percent of the sector budget was utilized inFY92, and preliminary estimates indicate a similar situation for FY93 as someprojects, including the second tranche of the ADB-supported Forestry Programloan were cancelled. Some of the poor implementation relate to lack oftechnical skills and adequate operational guidelines to design and translatethe Master Plan into feasible projects. Also, administrative practices favorbureaucratic control, especially over nationalized forests at the expense ofpromoting efficient use and regenerating forest resources. Until recently,clear guidelines for transferring resources to Community and User groups werelacking; and poor management of project finances and weak monitoring adverselyaffected fund release for programs. In the absence of functioning local levelorganizations, O&M support was inadequate and completed programs could not besustained. Often, such activities were operated at much diminished levels,and project staff laid off. This has been so even for most of therevenue-generating programs which were to be self-sustaining, but tended tofold up at the end of external support. Training and other opportunitiesprovided by externally-funded projects were often not well utilized.

5.35 Despite the generally poor implementation performance, there areindications of differences in progress across sub-sectoral programs. The restof this section will examine performance in the major program areas, startingwith Community Forestry.

5.36 The top priority program area is Community Forestry, which appliesmainly in the Hills. It is the largest single program area envisaged underthe Master Plan, and it accounted for 28-30 percent of forestry sectorallocations in FY90-FY92. Its main activity is to transfer management rightsand responsibilities over assigned forest land from the Fcrest Department toUser Groups, and for the Forest Department to provide technical services tohelp User Groups achieve efficient and sustained utilization as described insimple operational plans. To date some l90O User Groups are reportedly atdifferent stages of formation, and 500 Operational Plans have been approved.As awareness of the program spreads, the Forest Department's role would haveto shift gradually from handing over forest land to User Groups to providingthem with technical and extension advice for managing community forest landsfor multiple uses, responding to the rural economy. Anecdotal evidencesuggests that the program may be starting to mitigate deforestation, with aslow but gradual forest regeneration in some parts of the Hills. The programis entering a consolidation phase, as local communities are getting more awareof the benefits of participation. The program has the potential to reduceGovernment expenditures on forestry development, with increased communityparticipation in forest management; lead to the withdrawal of subsidies forforest watchers; increase user group contributions of which 50-75 percent havebeen recorded; and emphasize regeneration through protection rather thanplantation. It is estimated that Government allocations to the program couldbe reduced by about a third without adversely affecting program performance.Core activities that have to be retained include trained technical staff withadequate budget and facilities to support user groups with advice on extensionand on the technical options for harvesting and regeneration.

- 105 -

5.37 Another important program area is private forestry, which mainlyinvolves supplying free seedlings to private landowners to grow trees. Thedemonstrated success of lucrative tree crops has given impetus to the rapidestablishment of private nurseries, primarily in the Terai. With this privatesector expansion, the commercial production of seedlings by the ForestDepartment needs to be sharply reduced and the Department's efforts refocussedon research and provision of new technology and improved seeds. The singlemost important impediment to this program has been restrictions on cuttingtrees on private land, which is considered to be providing a cover for illegalfelling in the nationalized forests. The new Forest Act has removed theserestrictions.

5.38 Another major program area undergoing reform is productionforestry. Unlike in the past, the emerging policy is to manage nationalforests as productive concerns. The new Forest Act implicitly (i) requiresthe line Ministry to assess and allocate national forests for sustainable usein line with social, economic and environmental goals; and (ii) providesalternatives to Government management of forests by making provisions forleasehold (concession) forestry. The emerging policy calls for Government toestablish clear goals for managing national forestry to:

Identify ecologically sensitive, severely degraded or fragileareas, (such as parts of the Siwaliks) that require protection.These areas are to be retained under the territorial functions ofthe District Forest Officers.

Identify potential production forests; that is, areas which havegood growth and regeneration potential and would be economicallyviable. These are to be managed through concessions or by theGovernment. Excluding the parks and reserves, middle mountainsand the fragile Siwalik range, some 400,000 ha have beenidentified for producing forest products, mainly logs andfirewood. From these, an annual sustainable production has beenestimated conservatively at Rs.6,450 million ($130 million) instumpage value alone, a sizeable revenue compared to the Rs.5,372million envisaged under the EP for the entire forestry sector.

e Remove all restrictions on the distribution and pricing of forestproducts by adopting a market responsive supply system, includingabolishing the virtual monopoly of the Timber Corporation andother agencies and making them financially autonomous. Removeopen-ended subsidies; target the socially desirable ones andreplace them with explicit budgetary allocations. Collect feesand royalties systematically as part of forest resource managementinstead of the present ad hoc subsidies to a variety of users.

Strengthen the capacity of Government tc manage and monitorproduction forests; develop research capacity, especially inforest regeneration; establish transparency and accountability andscope to enforce environmental codes.

- 106 -