nbbl aml/cft& kyc policy

TRANSCRIPT

NBBL AML/CFT& KYC POLICY

Nepal Bangladesh Bank Ltd. Head Office, Kamaladi, Kathmandu, Nepal.

November 2021

(APPROVED BY THE 379TH MEETING OF BOARD OF DIRECTORS HELD ON 22

NOVEMBER 2021)

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

1

Contents

CHAPTER 1 ................................................................................................................................................. 3

1.1. Introduction .................................................................................................................................. 3

1.2. Broad Objective ............................................................................................................................ 3

1.3. Specific Objective ......................................................................................................................... 4

1.4. Title and Commencement: ............................................................................................................ 4

1.5. Definitions .................................................................................................................................... 4

1.6. Purpose ......................................................................................................................................... 8

1.7. Scope/Limitation .......................................................................................................................... 9

1.8. Description of Money Laundering and Financing of Terrorism ................................................. 10

1.9. Following mechanism shall be established by the bank to comply with the Sanction regime ... 13

1.10. Anti-Bribery and Corruption (ABC) .......................................................................................... 14

CHAPTER 2 ............................................................................................................................................... 15

2.1 International Initiatives ............................................................................................................... 15

2.2 National Legal and Regulatory Framework ............................................................................... 16

2.3 Obligations of Bank under ALPA .............................................................................................. 17

CHAPTER 3 ............................................................................................................................................... 19

3.1 Know Your Customer (KYC) ..................................................................................................... 19

3.2 Purpose of KYC .......................................................................................................................... 22

3.3 Mechanisms Deployed for KYC ................................................................................................ 22

3.4 Know your Employee (KYE) ..................................................................................................... 23

3.5 Due Diligence of vendors, service providers, consultants and business partners ....................... 23

3.6 Due diligence of correspondent banking relationships ............................................................... 24

3.7 Wire Transfer .............................................................................................................................. 24

3.8 Risk assessment .......................................................................................................................... 25

3.9 Suspicious and Large Value Transaction.................................................................................... 26

3.10 Account Review and Revision of Risk Level ............................................................................. 28

3.11 Ongoing Due Diligence ................................................................................................................ 29

3.12 Relationship with Walk in Customers: ......................................................................................... 29

3.13 Risk Based Approach to Customer Due Diligence: ....................................................................... 29

3.14 Automated Screening System: ........................................................................................................ 30

3.15 Sanctions Policy: ............................................................................................................................ 30

CHAPTER 4 ............................................................................................................................................... 31

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

2

Governance for AML & KYC .................................................................................................................... 31

4.1 Overview .................................................................................................................................... 31

4.2 Roles and Responsibility of Board of Directors (BOD) ............................................................. 31

4.3 Roles and Responsibility of Risk Management Committee (RMC) ........................................... 31

4.4 Roles and Responsibility of Assets (Money) Laundering Prevention Committee: .................... 31

4.5 Roles and Responsibility of Chief Executive Officer (CEO) ..................................................... 33

4.6 Roles and Responsibility of Chief Risk Officer (CRO) ............................................................. 33

4.7 Roles and Responsibility Chief Operating Officer (COO) ......................................................... 33

4.8 Roles and Responsibility of Head, Compliance Department...................................................... 34

4.9 Roles and Responsibility of Compliance Officer ....................................................................... 34

4.10 Roles and Responsibility ofProvincial Chief: ............................................................................. 35

4.11 Roles and Responsibility of Head, Information Technology Department: ................................. 35

4.12 Roles and Responsibility of Internal Audit: ............................................................................... 35

4.13 Roles and Responsibility of Human Resource Department:....................................................... 36

4.14 Roles and Responsibility of Branch In-Charge .......................................................................... 36

4.15 Roles and Responsibility of Branch Compliance Officer (BCO) ............................................... 36

4.16 Roles and Responsibility of Chief, Treasury Department .......................................................... 38

4.17 Roles and Responsibility of Individual Employees: ................................................................... 38

CHAPTER 5 ............................................................................................................................................... 39

Miscellaneous ............................................................................................................................................. 39

5.1 Retention of Records .................................................................................................................. 39

5.2 Awareness & Training: ............................................................................................................... 39

5.3 Amendment to the policy............................................................................................................ 39

5.4 Code of Conduct for Employee .................................................................................................... 39

5.5 Non-Compliance ......................................................................................................................... 40

5.6 Repeal and Save .......................................................................................................................... 40

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

3

CHAPTER 1

Introduction, Purpose and Scope and Limitation

1.1. Introduction

Money Laundering is a serious threat to financial system of all countries and it damages the

country’s economy including the country’s sovereignty and image. This has been widely

recognized at the international level. Throughout the world, banks have become a chief end of

money laundering operations and monetary crime because they are endowed with a range of

services and instruments that can be used to cover up the source of money. With their refined,

coherent and beguiling behavior, money launderers attempt to use banks as a vehicle for illegal

activity so as to accomplish their purpose.

Regulatory directives and the law of the land require the Banks & Financial Institutions to

institute, implement and exercise adequate measures so as to prevent the bank from being used,

intentionally or unintentionally, for Money Laundering (ML) and Terrorist Financing (TF)

activities. This policy has been accordingly introduced/ reviewed for ensuring compliance of

legal and regulatory statutes viz. Asset (Money) Laundering Prevention Act 2064 including

2nd Amendment2070 (ALPA), Asset (Money) Laundering Prevention Rule 2073 (ALPR),

Nepal Rastra Bank’s AML directive& circulars, NRB-FIU’s pertinent directives, circular and

guidelines including measures set forth by the relevant international bodies like FATF

(Financial Action Task Force), APG (Asia Pacific Group on ML) and for ensuring effective

compliance to the same.

The bank is determined:

▪ To safeguard its customers and other transacting entities, employees, from becoming a

victim or an unintentional accomplice of ML/TF activities.

▪ To meet the ML/TF related national and international regulatory obligations in

identification, treatment, rectification and management of ML/TF risk

▪ To protect the bank from reputational risk and to prevent breaches of AML/CFT&KYC

statute that may otherwise lead to serving fines and penalties

1.2. Broad Objective

To ensure that a system is established within which money laundering and terrorist financing

control is managed through stringent and appropriate procedures in order to discharge our legal

and moral duties. This policy, broadly is based on “Asset (Money) Laundering Prevention Act

2064(2nd amendment on 2070)”, Asset (Money) Laundering Prevention Rules 2073 and NRB

Unified Directive, Directive number 19. Also, this policy incorporates agreed international

rules and regulations and best practices, which directs Nepal Bangladesh Bank’s banking

activities to proactively comply with AML prudent practices among its stakeholders.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

4

1.3. Specific Objective

Apart from these broad objectives, the specific objectives are:

a) To make staff aware of legal obligations and national policy guideline in terms of AML &

CFT;

b) To focus on methods of prevention of money laundering and combating the financing of

terrorism;

c) To prevent the bank’s products or services from being used as a channel for money

laundering and financing of terrorism;

d) To prevent damage to the bank’s name and reputation by associating with money launderers

or terrorists’ financiers or proliferation financier of weapons of mass destruction;

e) To ensure that the bank complies with money laundering prevention and anti-terrorism

legislation/regulations;

f) To assist regulators/law enforcement agencies in their efforts to investigate and track money

launderers & terrorist financiers.

1.4. Title and Commencement:

This Policy shall be known as “NBBL AML/CFT &KYC Policy”

This policy and any changes to it shall come into force from the date of approval by the Board

of Directors (BOD) of the bank.

1.5. Definitions

a. Money Laundering

The conversion or transfer of funds, by any person who knows, should have known or suspects

that such funds are the proceeds of crime, for the purpose of concealing or disguising the illicit

origin of such funds or of assisting any person who is involved in the commission of the

predicate offence to evade the legal consequences of his actions.

b. Financing Terrorism

Financing Terrorism is an act committed by any person who, in any manner, directly or

indirectly, and willingly, provides or collects funds, support, or attempts to do so, in order to

use them or knowing that these funds will be used in whole or in part for the execution of a

terrorist act, or by a terrorist or terrorist organization.

c. Terrorist

Any natural person or organization who commits the following acts:

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

5

1. Commits or attempts to commit terrorist acts by any means, directly or indirectly, unlawfully

and willfully,

2. Participates as an accomplice in terrorist acts,

3. Organizes or directs others to commit terrorist acts, or

4. Contributes or cooperates to the group of persons acting with a common purpose of

commission of terrorist acts where such contribution or cooperation is made intentionally

and with the aim of furthering the terrorist act or with the knowledge or the intention of the

group to commit a terrorist act.

d. Transaction

Transaction means purchase, sale, distribution, transfer, investment, use/ occupancy or any

type of agreement or any of the following acts performed for any type of economic or business

activities:

• Establishment of business relation.

• Opening of an account.

• Deposits or collection of funds, payment, payment order, exchange or transfer of fund in

whatever currency, whether in cash or by cheque or other instruments through electronic

or any other means.

• The use of a safe deposit (Locker).

• Establishing any fiduciary relationship.

• Any payment made or received in whole or in part based on any contractual or other legal

obligation;

• Any payment made or received in respect of a lottery, bet or other game of chance,

• Establishing or creating a legal entity or legal arrangement

• Such other act as may be designated by the Government of Nepal by publishing a notice in

the Nepal Gazette.

e. Customer

For the purpose of this policy, a customer will be defined as

• A person or entity that maintains an account and/or has a business relationship with the

Bank,

• One on whose behalf the account is maintained (i.e., the beneficial owner)

• Beneficiaries of transactions conducted by professional intermediaries such as Stock

Brokers, Chartered Accountants, Solicitors etc. as permitted under the law; and

• Any person or entity connected with a financial transaction, say a wire transfer or issue of

a high value demand draft etc. as a single transaction.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

6

f. Domestic Politically Exposed Persons (PEP)

The President, Vice-President, Prime Minister, Chief Justice, Speaker of Parliament,

Chairperson of National Assembly, Chief of Province, Minister of Government of Nepal,

Chief Minister of Provincial Government, Member of Federal Parliament of Nepal, head and

members of the constitutional bodies, Speaker of Provincial Parliament, Minister of Provincial

Government, officials in the special class or their senior of the Government of Nepal, judge

of the Appellate Court and apex court and their senior, senior politician, Deputy Speaker of

Provincial Parliament, member of Provincial Parliament, central member of national political

party or Chairperson/ Vice- Chairperson of district level committee, Mayor/ Deputy Mayor of

Municipality, Chairperson/ Vice- Chairperson of Rural Municipality or senior executives of

any institution partially or fully owned by the Government. Further, this definition may be

change if any amendment occurs in Assets (Money) Laundering Prevention Act 2064.

g. Foreign Politically Exposed Persons (PEP)

Politically exposed person who is or has been the Heads of State or of government, senior

politician, central member of national political party, senior government, judicial or military

official, senior executives of state-owned corporations of a foreign country.

h. Beneficial Owner

Natural person who, directly or indirectly, owns or controls or directs or influences a customer,

an account, or the person on whose behalf a transaction is conducted, or exercises effective

control over a legal person or legal arrangement or remains as an ultimate beneficiary or owner

of such activities. Beneficial owners are the individuals or entities who are owners of an

underlying company/entity and who ultimately control (either directly or indirectly) through

one or more shareholdings.

i. Customer Due Diligence (CDD)

Customer Due Diligence is the process of identifying and evaluating the customers and the

assessment of customer risk as part of know your customer (KYC) process, allowing banks to

better identify, manage, and mitigate the AML related risks.

1. Simplified Customer Due Diligence (SCDD): Simplified Customer Due Diligence is the

lowest level of due diligence that is conducted for the customer. Simplified CDD is the

information obtained for all customers to verify the identity of a customer and assess the

risk associated with that customer. Simplified Due Diligence will be applied where the

customer is considered to be at low level of risk having characteristics as specified by the

NRB directives [such as the total annual deposit or transactions remaining within the limit

of NPR 100,000, financial institutions supervised by NRB, customers whose identity is

controlled by the national system and others as specified by the regulator from time to time]

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

7

2. Normal Customer Due Diligence: Normal CDD is implied to the customers in general or

in medium risk or those who do not fall under high risk or low risk. This includes the

obtaining and analyzing the minimum documents as mentioned in directives and laws.

3. Enhanced Customer Due Diligence (ECDD): Enhanced Customer Due Diligence is the

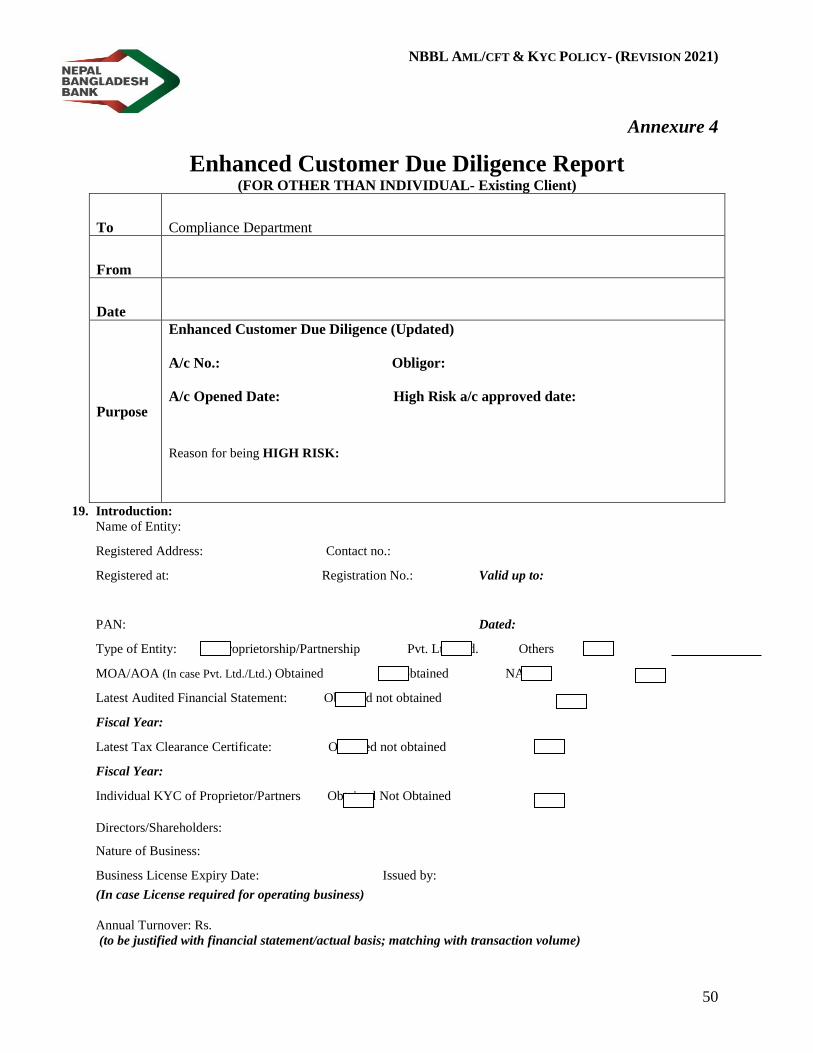

additional information collected from the customer to provide a deeper understanding of

the customer activity to mitigate associated risk. Enhanced Customer Due Diligence is

required where the customer and product/services combination are considered to be of high

risk. A high-risk situation is where there is an increased risk for money laundering and

terrorist financing and way of utilization of the products and services that are being offered

to the customer.

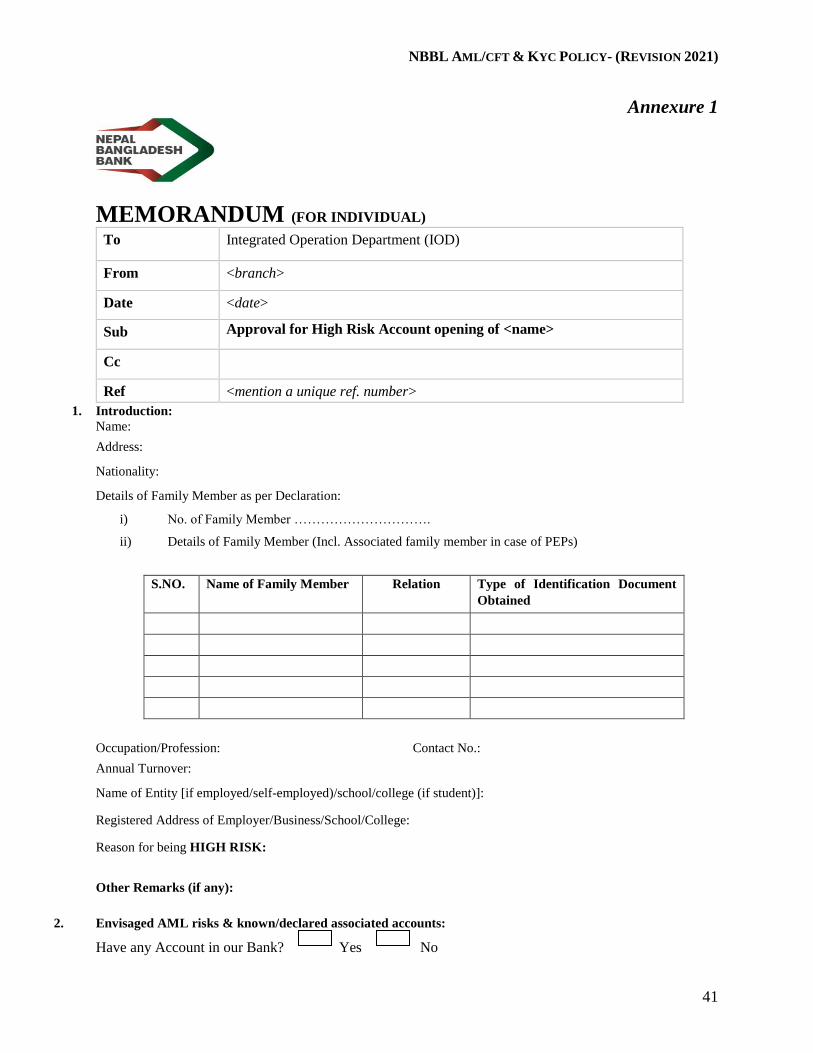

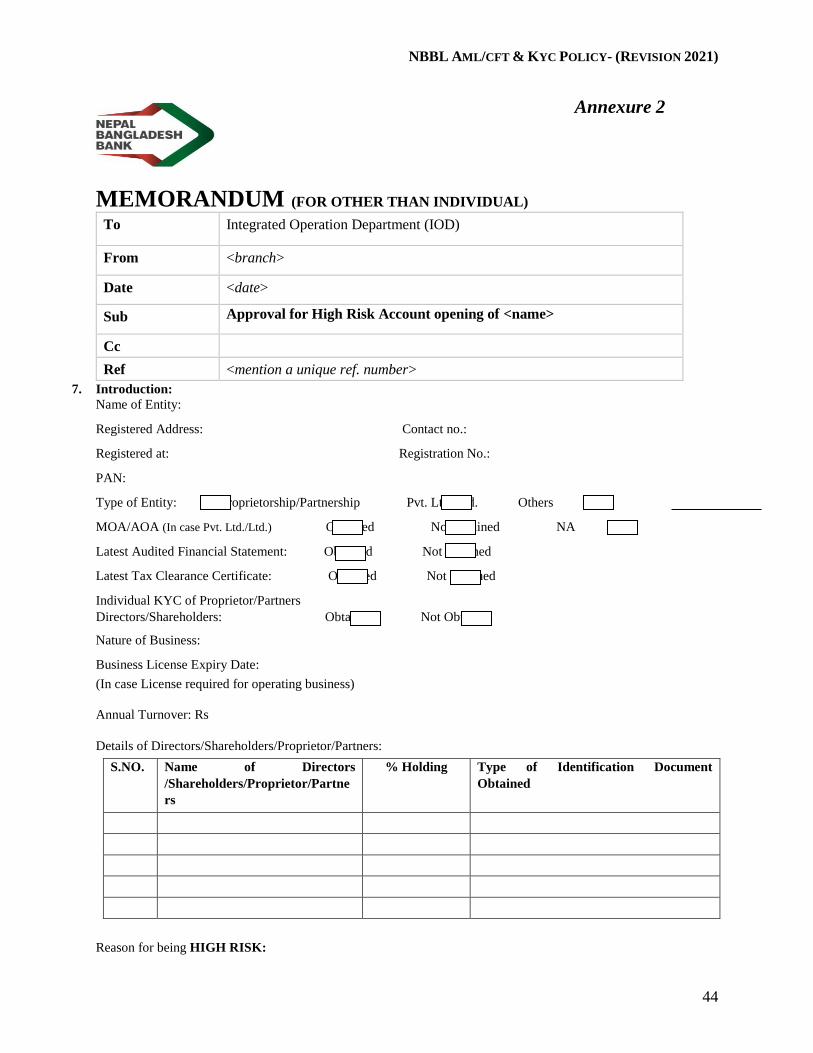

For Enhanced CDD measures, it shall include but not limited to the following:

• Obtaining additional information on the customer i.e. occupation, volume of assets,

information available through independent and reliable sources like public databases,

internet etc. and updating the identification data of customer and beneficial owner more

frequently.

• Obtaining additional information on the intended nature of the business relationship

• Obtaining information on the source of funds and purpose of account including fully

filled up transaction matrix of account opening form

• Obtaining information on the reasons for intended or performed transactions

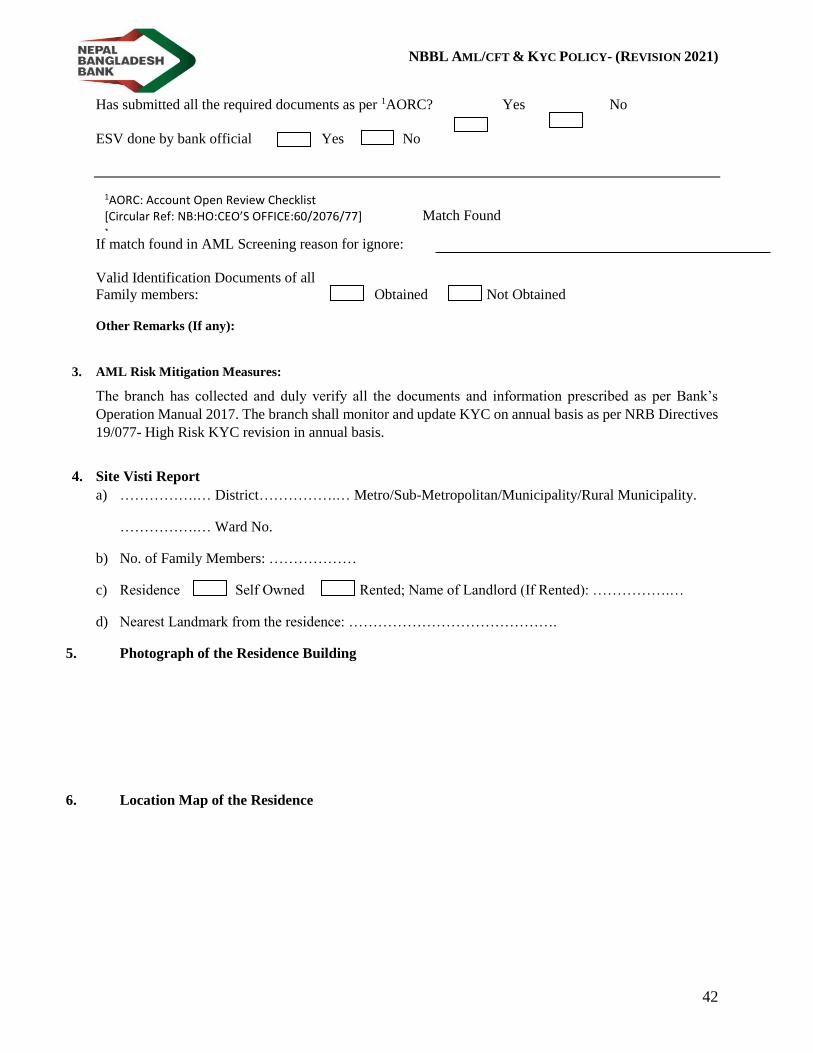

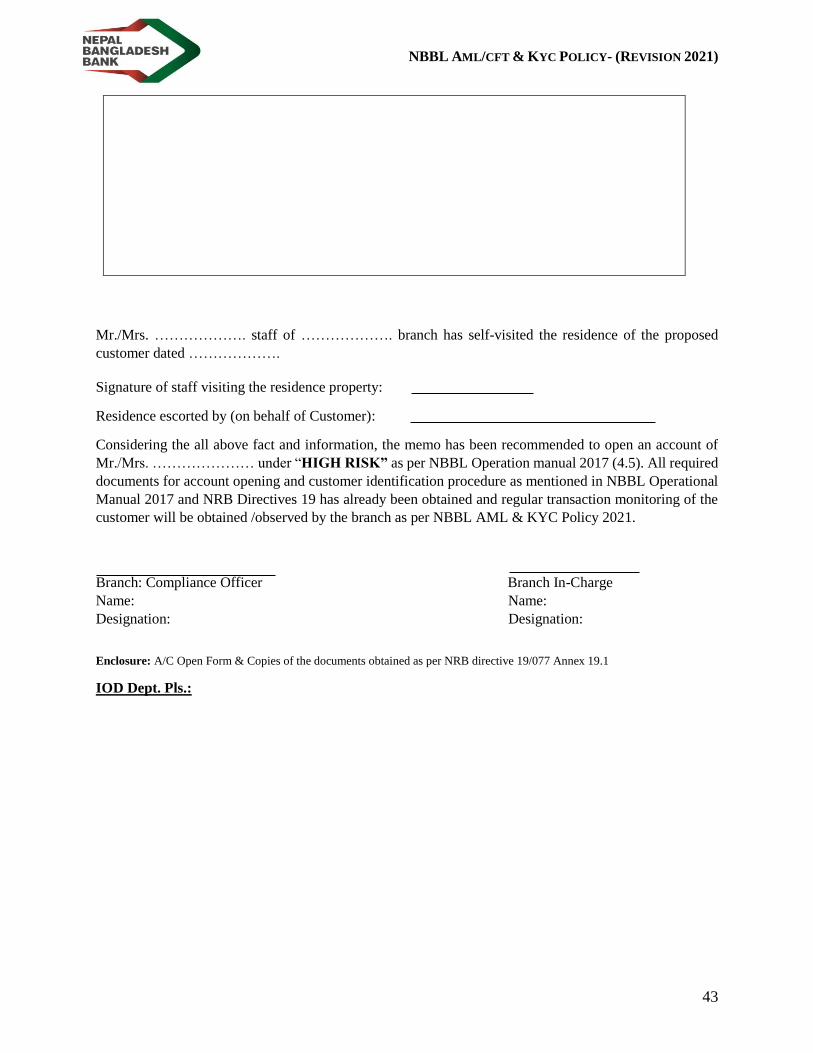

• Branch Compliance Officer or Branch In-Charge must visit the current residence in

case of natural person or registered office in case of legal person execute the ESVR

(ECDD Side Visit Report) and forward the ESVR in the prescribed format to

“IOD/HO” along with the Request for Consent for High Risk account Opening

accompanied by the customer’s KYC documents.

Branch shall make High Risk Account operative only after obtaining needful consent

from “IOD/HO”.

• The branch must ensure for collecting of entire required documents from the customers

as per the existing provision and due diligence by ESVR (ECDD Site Visit Report)

measures however Branch Manager and Branch Compliance Officer may jointly agree

to recommend for consent to open high risk a/c based on the other authenticated

supervisory documents produced by the customers for confirmation of the site.

Furthermore, until the ESVR (ECDD Site Visit Report) is obtained by the branch; the

cash deposit transaction more than Rs. 100,000 shall not be allowed.

• Conducting regular monitoring of the business relationship

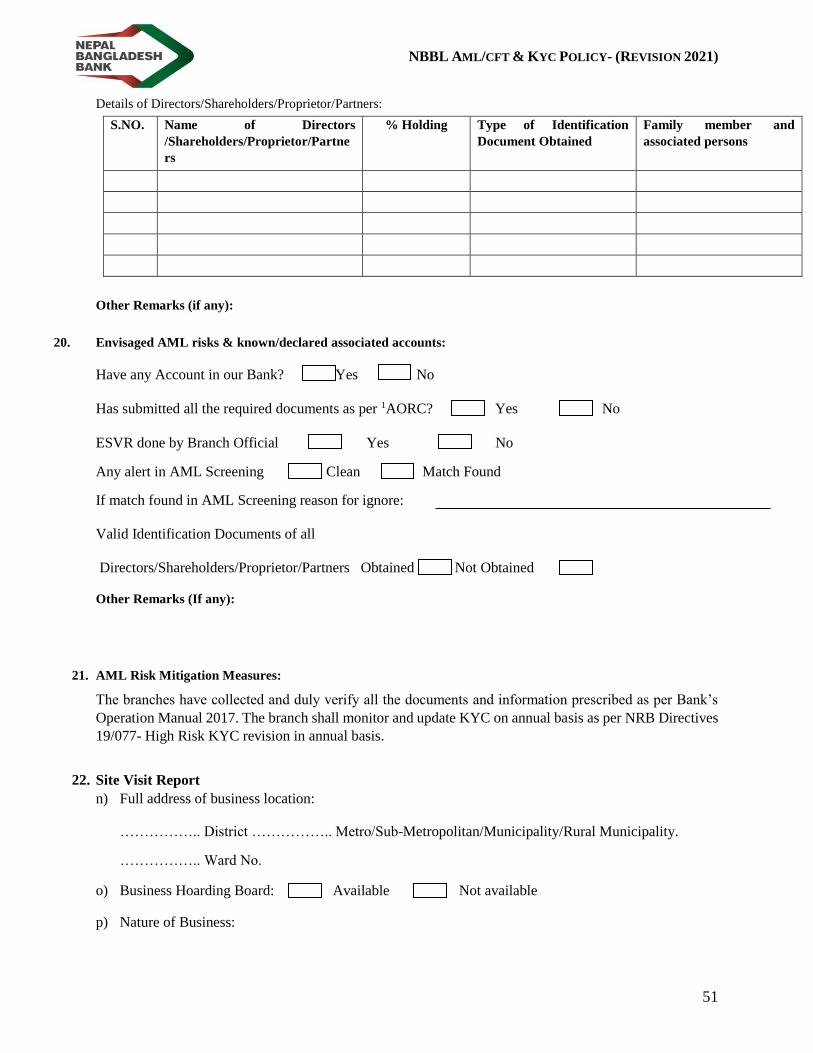

• Obtain all the documents and information as required by Account Open Review

Checklist (1AORC) as per Customer type mentioned in Annex 19.1 of NRB Directives

19.

• All the HIGH-RISK accounts should be TAGGED for categorically specifying the

reason for being classified as HIGH-RISK accounts.

(For Customer Due Diligence process, refer Chapter 4 of Operational Manual 2017 of the Bank

which is also annexed to this policy. ECDD must be carried out in the prescribed format as per

Annexure 1 & 2 attached herewith this policy.)

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

8

j. Asia/ Pacific Group on Money Laundering (APG)

Asia/Pacific Group on Money Laundering (APG) is an autonomous and collaborative

international organization founded in 1997 in Bangkok, Thailand consisting of 41

members and a number of international and regional observers. Nepal is a member of

APG.

APG members and observers are committed to the effective implementation and

enforcement of internationally accepted standards against money laundering and the

financing of terrorism, in particular the Forty Recommendations of FATF.

k. Financial Information Unit (FIU):

Financial Information Unit is Nepal's financial intelligence unit and it is the central,

national agency responsible for receiving, processing, analyzing and disseminating

financial information and intelligence on suspected money laundering and terrorist

financing activities to the Investigation Department, other relevant law enforcement

agencies and foreign FIUs.

l. Shell Entity:

Itis a legal person that exists in name only and are frequently used to shield identities and/or

to hide money. Nepal’s law prohibits the banks& financial institutions from

establishing/continuing transacting with the shell entities. The Bank will not establish any

business/ financial relations with shell entity.

m. Shell Bank

Shell Bank refers to Financial Institution or group of financial institutions that has no

physical existence in the country of incorporation or is not under any regime of effective

regulation and supervision. For the purpose of this clause, presence of local agent or junior

level staff does not constitute physical presence. The Bank will not establish any business/

financial relations with shell bank.

n. High Risk and Non-Cooperative Jurisdiction

High Risk and Non-Cooperative Jurisdiction are the Jurisdictions with strategic AML/CFT

deficiencies that have not made sufficient progress in addressing the deficiencies or have not

committed to an action plan given by FATF. The list can be accessed from the FATF websites.

1.6. Purpose

This policy is based ALPA, Nepal Rastra Bank & NRB-FIU’s directive, circulars and

guidelines, international rules and regulations, best practices which also directs Nepal

Bangladesh Bank Ltd.’s banking activities to proactively comply with the AML prudent

practices among its stakeholders.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

9

With the objective to safeguard the bank from being used as a component in the financial

system for money laundering, the purpose of the policy in the light of above is as follows:

a. To enable the bank to conduct clean, commercial business conforming to standards set by

the industry, laws and regulations of the country/governing authorities.

b. To follow the internationally accepted standards used for KYC compliance as far as

practical.

c. To report and take suitable actions upon detection of suspicious activity involving shades

of money laundering as directed by Nepal Rastra Bank, or any other laws formulated from

time to time.

d. To make the employees and customers aware about the seriousness of the impact of

occurrence of ML/TF activities.

e. To provide the knowledge to identify AML/CFT transactions

f. To make bank's staff aware of the AML/CFT policies and practices.

g. To comply with prevailing laws of the land regarding AML/CFT and adhere to the

standards accepted internationally by the financial world on the subjects, as far as practical.

h. To prevent the opening of anonymous, fictitious accounts or the accounts of the entities

sanctioned by bodies like UN, OFAC etc.

i. To verify the identity of prospective customers using reliable and independent

documentation before they are allowed to establish account relationship

j. To set-up needful administration process within the bank to implement the set AML

standards.

k. To train staff for updating on KYC, & AML practices, pertinent laws and their impacts.

l. To set-up independent administration process via bank’s compliance department to

implement the set AML standards.

m. To ensure the execution of required due diligence (ECDD or SCDD) as per the assigned

risk category.

1.7. Scope/Limitation

The four basic tenets of AML stated in this policy are as follows:

a. Know Your Customer (KYC)

b. Risk Assessment of Accounts

c. Accounts Review

d. Transaction/account monitoring for probable STR (Suspicious Transaction Reporting)

This policy is not a standalone document. AML functions are also guided by other factors such

as NRB directives, policy guidelines approved by the bank, periodic instructions issued by the

competent authority of bank based on the periodic review of the NBBL management policies

and instructions from time to time.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

10

There is a specific law ALPA prevailing for addressing ML/TF offences in the country and

NRB has also issued AML directive, NRB-FIU has issued guidelines on STR, TTR. Further,

FATF, APG have also issued various standards on ML/TF mitigating measures.

Further, the procedures and policies specified in this policy are the minimal compliance

requirements to be adhered to by the NBBL bank employees as such compliance of this policy

alone may not be considered as the complete discharge of their duties as compliance to all

prevailing factors governing the AML must be duly ensured.

1.8. Description of Money Laundering and Financing of Terrorism

a. Money Laundering (ML): ML is the process or series of processes designed to disguise

the nature/source of proceeds obtained from activities termed as predicate offence(s) under the

“Asset (Money) Laundering Prevention Act 2064(2nd amendment 2070) such as drug

trafficking, smuggling, kidnapping, gambling, robbery, counterfeiting, bogus invoicing, tax

evasion, misappropriation of public fund among others making it impossible to trace back the

origin of the fund.

Under Section 3 of Chapter 2 of ALPA “Offences of money laundering” has been defined as

under:

Assets shall be supposed to have been laundered if anyone commits any of the following acts:

i) Converting or transferring property by any means knowing or having reasonable grounds

to believe that it is proceeds of crime for the purpose of concealing or disguising the illicit

origin of property, or assisting any person involved in the offence for evading legal

consequences of offender.

ii) Concealing or disguising or changing the true nature, source, location, disposition,

movement or ownership of property or rights with respect to such property knowing or

having reasonable grounds to believe that it is proceeds of crimes.

iii) Acquiring, using, possessing any asset knowingly or having reasonable grounds to believe

that it is the proceeds of crime.

No person shall conspire, aid, abet, facilitate, counsel, attempt, associate with or participate in

the commission of the acts mentioned above.

b. Stages of ML: There are three stages of ML as follows:

1. Placement: The first and most vulnerable stage of laundering money is placement. The

goal is to introduce the unlawful proceeds are deposited into the financial system without

attracting the attention of financial institutions or law enforcement. Placement techniques

include structuring currency deposits in amounts to evade reporting requirement or

comingling funds from legal and illegal source.

2. Layering: It is the second stage of ML. At this stage, a complex web of financial

transactions is made with the sole purpose to wipe out the audit trail, disguise the origin,

and to maintain anonymity for actual people behind the transactions. e.g. fraudulent letters

of credit transactions, over-invoicing for goods transshipped from another country, raising

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

11

loans against illegal funds at different banks, using high value credit cards to pay for

goods/services and accounting for the credit card invoices with balances held in offshore

banks.

3. Integration: At this final stage, the laundered or cleaned up money is legitimately brought

back into financial system operated by end user and when it is safe and insulated from

enquiry by agency with a legitimate reason for querying the existence of money.

c. Money Laundering Areas

As money laundering is a necessary consequence of almost all profit generating crime, it can

occur practically anywhere in the world. Generally, money launderers tend to seek out areas

in which there is a low risk of detection due to weak or ineffective anti-money laundering

programs. Because the objectives of money laundering are to get the illegal funds back to the

individual who generated them, launderers usually prefer to move funds through areas with

stable financial systems. Therefore, Banks have been the targets for money launderer.

Money laundering activity may also be concentrated geographically according to the stage the

laundered funds have reached. At the placement stage, for example, the funds are usually

processed relatively close to the under-lying activity: often but not in every case, in the country

where the funds originate.

With the layering phase, the launderer might choose an offshore financial center, a large

regional business center, or a world banking center – any location that provides an adequate

financial or business infrastructure. At this stage, the laundered funds may also only transit

bank accounts at various locations where this can be done without leaving traces of their source

or ultimate destination.

Finally, at the integration phase, launderers might choose to invest laundered funds in still

other locations if they were generated in unstable economies or locations offering limited

investment opportunities

One of the latest trends in money laundering involves use of the new payment technologies

like Smart Cards, Online Banking and Electronic Cash etc. The Bank should be vigilant and

should administer the robust controlling, monitoring and reporting system to prevent money

laundering and financing of terrorism through such channels.

d. Terrorist Financing (TF)

It is the process of providing the financial support for the activities deemed as ‘terrorist

activities’ under ALPA and prevailing international standards.

Under Section-4, Chapter 2 of ALPA, provisions in regard to combating of financing of

terrorism has been stipulated under the point “Terrorist Activities not to be financed” as under:

i) No person shall, by any means, directly or indirectly, with unlawful intention and willfully,

provide or collect funds or assets, despite of having knowledge that such funds or assets

shall be used or may be used, in whole or in part, in order to carry out a terrorist act or by

a terrorist or a terrorist organization.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

12

ii) No person shall provide or conspire to provide material support or resources to any terrorist

or terrorist organization by any means, directly or indirectly, in order to carry out a terrorist

act.

iii) In relation to any of the acts mentioned above, no person shall commit any of the following

acts:

a) To participate as an accomplice in such act,

b) To organize or direct others to commit such act,

c) To contribute a group of persons which commits such act or has a common purpose of

committing such act or willfully promote such group of persons for furthering their

criminal activities or to achieve such purpose.

Even if any of the following circumstances exist in relation to any act mentioned above, it shall

be the offence of terrorist financing:

a) Terrorist act does not occur or is not attempted,

b) Assets or funds are not actually used to commit terrorist act or attempt thereof.

c) Assets or funds are linked or not linked to a specific terrorist act.

d) Terrorist act or intended terrorist act occurs or will occur in the country, state or territory

where such act was intended to occurs or somewhere else,

e) Individual terrorist or terrorist organization is located or not in country, state or territory

where the person committing such act resides or somewhere else.

f) Whether the assets or funds are collected or made available from legitimate or illegitimate,

any source or means.

If any person commits any of the activities as mentioned above, the same shall be offense of

financing terrorist activity.

Even if any act or offence mentioned above is committed in the foreign country or territory

provided that the act is treated as offence under the law of respective country, the same shall

be treated as the offense of Money laundering and Terrorist financing committed in Nepal.

There are two main sources of terrorist financing-

(1) Financial support from countries, organizations or individuals that may include criminal

activities.

(2) The second source, revenue-generating activities may involve drug trafficking, human

smuggling, theft, robbery and fraud to generate money. Funds raised to finance terrorism

usually are laundered and thus anti-money laundering processes in banks and other

reporting industries are important in the identification and tracking of terrorist financing

activities.

Bank shall build measures to monitor identity and report such funds received or sent using the

banks system. NBBL shall take caution while doing transaction, account opening, or carrying

banking activities if in any circumstances the name of any prohibited/sanctioned organization

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

13

or individual (involved in terrorist activities) appears as payee/endorsee/applicant and report

of such transaction as and when detected.

The bank shall endeavor to get list of such organization/individuals via the best possible means

or mechanisms.

e. Risks of money laundering and terrorist financing to the banks

Bank is exposed to several risks if it fails to prevent the Bank being used for M/L and F/T

activities.

➢ Reputational risk: The reputation of a business is usually at the core of its success. The

ability to attract good employees, customers, funding and business is dependent on

reputation. Even if a business is otherwise doing all the right things, if customers are

permitted to undertake illegal transactions through that business, its reputation could be

irreparably damaged. A strong policy helps to prevent a business from being used as a

vehicle for illegal activities.

➢ Operational risk: This is the risk of direct or indirect loss from faulty or failed internal

processes, management and systems. In today's competitive environment operational

excellence is critical for competitive advantage. If AML policy is faulty or poorly

implemented, then operational resources are wasted, there is an increased chance of being

used by criminals for illegal purposes, time and money is then spent on legal and

investigative actions and the business can be viewed as operationally unsound.

➢ Compliance Risk: Risk of loss due to failure of compliance with key regulations

governing the Bank’s operations.

➢ Legal risk: Risk of loss due to any of the above risk or combination thereof resulting into

the failure to comply with Law and having a negative legal impact on the Bank. The

specific types of negative legal impacts could arise by way of fines, confiscation of illegal

proceeds, criminal liability etc.

➢ Financial risk: Risk of loss due to any of the above risks or combination thereof resulting

into the negative financial impact on the Bank.

1.9. Following mechanism shall be established by the bank to comply with the Sanction

regime

a. Put in place a comprehensive policy approved by the Board of Directors;

b. Ensure all relevant sanctions lists are used electronically to detect the existence of

sanctioned individuals and entities

c. Conduct real-time transaction screening on all cross-border payments, SWIFT and other

modes of payment in relation to relevant list of named terrorist and sanctioned entities or

embargos

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

14

d. Freeze the accounts and relevant transactions in relation to relevant lists of named terrorist

and sanctioned entities or embargos immediately

e. Report to the detected incidents to FIU without delay

f. Keep record or audit trail for all sorts of monitoring mechanism

g. Take necessary training and awareness building arrangement

1.10. Anti-Bribery and Corruption (ABC)

Bribery may occur in a commercial arrangement or involve the misuse of public office or

public power for private gain in order to obtain, retain or direct business or to improperly secure

any other advantage in the conduct of business. Many national and international organizations

including the Organization for Economic Co-operation and Development (OECD) and the

United Nations (UN) are working to combat bribery and corruption in the public and private

sectors in countries around the world. The Bank has addressed ABC through following two

aspects:

a. Existence of control environment and corporate governance

b. Implementation of code of conduct for all officials of the Bank and promoting the highest

standards of integrity of employees and third parties performing certain services on our

behalf.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

15

CHAPTER 2

International Initiatives and National Legal and Regulatory Framework

2.1 International Initiatives

The international community has acted on many fronts to respond to the growing complexity

and the international nature of rapidly evolving ML/FT methods. The emphasis is on

promoting international cooperation and establishing a coordinated and effective international

AML/CFT regime. Many international agencies have helped countries develop a capacity to

prevent and counter ML. The following presents some of the main elements of the global and

regional initiatives.

i. The Financial Action Task Force (FATF) was established in 1989 by the G-7 countries to

respond more effectively to ML. The FATF Forty Recommendations require the

criminalization of ML. In addition, the recommendations call on countries to adopt

legislative and other measures in order to: freeze, seize and confiscate criminal proceeds;

waive bank secrecy laws to permit financial institutions to monitor and report suspicious

transactions; protect those reporting these transactions from civil and criminal liability;

establish financial investigation units; and, cooperate fully in international law

enforcement efforts to combat ML. The FATF Special Recommendations require countries

to criminalize the financing of terrorism, terrorist organizations and terrorist acts and to

designate these new offences as ML predicate offences. The FATF is also involved in

monitoring the progress of members in complying with its recommendations.

ii. The United Nations Convention on Illicit Trafficking in Narcotic Drugs and Psychotropic

Substances (Vienna Convention), the UN Convention against Transnational Organized

Crime (Palermo Convention), the UN Convention against Corruption and the International

Convention for the Suppression of the Financing of Terrorism all contain provisions

relating to the tracing, freezing, seizing and confiscation of instrumentalities and proceeds

of crime.

iii. Financial regulation standards are also set by the Basel Committee on Banking

Supervision. In 1988, the Basel Committee put forward some basic principles as part of its

Statement for the Prevention of Criminal Use of the Banking System for the Purpose of

Money Laundering. It has also issued a paper a “sound management of risks related to

money laundering and financing of terrorism in 2014”.

iv. Wolfsberg Group, which is non- governmental organization of 13 large commercial banks

founded in AD 2000, develop and publishes financial industry standards for Anti-money

laundering (AML), Know Your Customer (KYC) and Counter Terrorist Financing (CTF)

policies. Its work is similar to what the Financial Action Task Force on Money Laundering

(FATF) does on a government level.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

16

v. Many countries have established financial intelligence units (FIUs) as a focal point for the

AML efforts and a point at which information is exchanged between financial institutions

and law enforcement. Since 1995, a number of these units have begun to work closely

together, to exchange information and to coordinate their AML efforts. They formed the

Egmont Group which facilitates international exchanges and cooperation among FIUs in

relation to both ML and FT.

vi. Multi-lateral organizations like World Bank, International Monetary Fund, Asian

Development Bank also work on preventing ML/FT risks. They also provide financial and

technical assistance to countries wishing to implement the FATF 40+9 recommendations.

They have also published several papers on the theme of preventing ML/FT risks for the

financial industry.

vii. Asia Pacific Group on Money Laundering (APG) is an autonomous and collaborative

international organization founded in 1997 in Bangkok, Thailand consisting of 41

members. APG members are committed to the effective implementation and enforcement

of internationally accepted standards against money laundering and the financing of

terrorism. Nepal became the member of APG Group in June 2002.

2.2 National Legal and Regulatory Framework

The bank is obliged to comply with the requirements of the following laws, rules and

regulations of the homeland. In addition, Nepal has to follow standards prescribed by FATF

as an obligation of member country of Asia Pacific Group on Money Laundering.

a. Legal Obligations: The bank is obligated to comply with the requirements of the following

laws and rules:

1. Asset (Money) Laundering Prevention Act, 2064 (Including second amendment)

(ALPA)

2. Asset (Money) Laundering Prevention Rules, 2073 (ALPR)

3. Asset (Money) Laundering Prevention (Freezing Asset or Fund of listed individual,

group or organization) Rules, 2070

b. Regulatory Obligations:

1. Unified Directives No. 19 issued by Nepal Rastra Bank:

2. Directives/Guidelines issued by FIU-Nepal (AML/CFT Directives to Financial

Institutions, Directives to implement UNSCR (United Nations Security Council

Resolutions) 1267 & 1373, Threshold Transaction Reporting Guidelines, Suspicious

Transaction Reporting Guidelines)

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

17

2.3 Obligations of Bank under ALPA

Section 7(Ta) and 7(Da) of ALPA has stipulated following obligations of the Bank, in addition

to others:

i. The Bank shall develop and implement AML/CFT Policy and Procedures compatible with

its nation, territory, working area, size of business, customer, transaction and risk for the

prevention of money laundering and financing of terrorism for the compliance of the

provisions stipulated under ALPA, ALPR and directives thereunder. The policy and

procedures so developed should include following components:

a. Internal policies, procedures and control arrangement relating to customer

identification, business relation, monitoring, transaction information/reporting, record

keeping and other obligations.

b. Arrangement for ongoing due diligence.

c. Arrangement to implement obligations as per ALPA, its rules and directives

thereunder.

d. Adequate procedural arrangement for ensuring high standard of employees, inter alia,

during selection and appointment.

e. Arrangement for ongoing training and refreshment to employees,

f. Effective arrangement for independent monitoring, review and audit of the activities

and updating the records.

g. Measures for detection and reporting of suspicious transaction,

h. Other measures required for fulfilling the obligations as per ALPA, ALPR and NRB

Directives and other arrangement required for evaluation of effectiveness of the same.

i. Other measures as prescribed by the Regulator,

ii. Bank shall have to appoint compliance officer of managerial level to comply the obligation

pursuant to the provision of ALPA or rules and directives thereunder. The Bank shall have

to ensure following function, rights and duties of the compliance officer and required

resources for the same:

a. Have access to any of the required records, books of accounts and related documents

in the course of delivering his/her responsibility.

b. Seek for and obtain data, information, details or documents from concerned employee

of the Bank.

c. Perform other necessary functions for implementation of ALPA, its rules and directives

thereunder.

d. Perform other functions as prescribed by the regulator

iii. The Bank shall maintain records, as under, accurately and securely for minimum five years

after the termination of business relationship or from the date of transaction or from the

date of occasional transaction:

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

18

a. All documents and records related to identification and verification of customer and

beneficial owner,

b. All documents, records and conclusion of the analysis of customer or beneficial owner

and transaction,

c. All documents, details and records related to accounting and business relation of the

Bank

d. All documents, details and records relating to domestic and foreign transactions,

e. All documents, details and records of attempted transactions,

f. All other documents, details and records as prescribed by regulators.

iv. The Bank shall maintain documents, details and records as mentioned above in such a way

that each of the transactions is clearly visible and sufficient to be produced in the course of

legal action as evidence.

v. The Bank shall have to maintain the report of suspicious transaction for the period of five

years.

As per the provision stipulated under Section 7(Pha) of ALPA, regulator may impose stipulated

action/actions and punishment if the Bank does not comply with the order, direction or

prescribed standard issued as per ALPA, rule or directives issued thereunder.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

19

CHAPTER 3

NBBL’s Policy on prevention of Money Laundering and Financing of Terrorism

3.1 Know Your Customer (KYC)

The Bank has a statutory obligation to know its customers and to understand the nature of the

business that is being conducted with us. This applies to every type of customer regardless of

who they are, their personal status, or the type of account or service that they require. Knowing

your customer means:

▪ Seeking evidence of identity and address and independently confirming that evidence at

the start of a business relationship with the Bank

▪ Seeking information regarding the nature of the business that the customers expects to

conduct with the Bank, establishing sources of income and expected patterns of

transactions, and keeping that information up to date, to show what might be regarded as

normal activity for that customer

Know Your Customer, KYC thus provides for a set of guidelines aimed at preventing banks

from being used intentionally or unintentionally by criminal elements for committing financial

frauds, transferring or deposits of funds derived from criminal activity or for financing

terrorism. KYC procedure also allow banks to be familiar with/understand their customers and

their monetary dealings better, which in turn help them administer their menaces carefully.

This policy aims for proper identification of an account holder/customer and for

scrutiny/monitoring of large value cash transaction or transaction of a suspicious nature.

The KYC procedures would be based on the following principles:

a. Customer Identification Procedure (CIP): Customer Identification Procedure is a critical

part of the Customer Due Diligence process. It is essential to establish the true identity of the

customers and be assured that the customers are not involved in any kind of money laundering

and terrorist activities.

In line with provision of Asset (Money) Laundering Prevention Act, 2064 (Including second

amendment), the customer identification procedures are to be carried out at the following steps;

a. While establishing a banking relationship

b. During opening of account

c. Carrying out FCY transaction equivalent or above NPR 1 lakhs with non-accountholder

customer. However, it is encouraged to concerned branches/ staffs to conduct CIP of non-

accountholder customer on every transaction irrespective of currency and amount.

d. Person who is not the operator of account and depositing above NPR 1 lakhs in that account

e. Wire transfer

f. When the bank has a doubt that authenticity/veracity or adequacy of the previously

obtained customer identification data

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

20

g. When the bank has a doubt on the activity related to money laundering or terrorism

financing

h. Every transaction of customer categorized under high risk or PEP

i. Any other activity prescribed by the regulatory body

j. Details of ultimate beneficial ownership (in person) who have multiple layers of ownership

shall compulsorily be identified and incorporate the details in account opening form and

CBS while on boarding new accounts.

k. IOD/HO the concerned branch should store all the account opening forms, documents and

details obtained during on boarding and after establishing the relationship with bank related

to accounts (KYC, signature update, etc.) in electronic form.

While identifying the natural person or legal person, the bank shall obtain the documents, data

and information as prescribed in the Operational Manual 2017 of the Bank and should also

refer to NRB directives/ Head Office Circular if any changes/ additional documents are

required in this regard. All the documents and information pertaining to the identification of

the natural and legal person should be retained in a legible manner and in managed way

The bank shall take all reasonable steps to verify the identity of customers, including the

beneficial owners of corporate entities and individuals as well, and the principles behind

customers who are acting as agents. The Bank will take all reasonable steps to ensure that

“Customer Due Diligence” information is collected and kept up-to-date.

In addition to above, following procedure needs to be carried out while Online Account

Opening

a. KYC application and required documents needs to be obtained digitally.

b. Such account should be categorized under High Risk and accordingly the transactions

monitoring should be carried out.

c. Account shall be debit restricted until the customer physically comes into the contact of

the Bank and produce the original documents.

d. Once the customer comes into physical contact with original documents, the risk grading

of that customer may be changed based on normal customer identification procedure.

e. Total deposit balance/ceiling of Rs. 1.00 Million till KYC updated or comprising in High

Risk Category. Deposit/balance above the mentioned ceiling can be maintained in such

accounts as per decision of management in case to case basis.

b. Customer Acceptance Policy:

The Customer Acceptance Policy ensures that only those clients whose identity and purpose

of opening accounts or performing transactions can be duly established and verified as

legitimate by conducting due diligence appropriate to their risk profile/services required would

be accepted. The bank shall have the option to Dr. Restrict/Dr. & Cr. restrict any account, if it

is not satisfied with the documentation /information/transaction of any customer.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

21

The bank must obtain thumb impression or Biometric of account holder and account operator

in case of natural person and of account operator in case of legal entity based on the associated

risk with the customer at the time of opening of account. But in case of minor thumb impression

or Biometric of only account operator may be obtained.

c. Identification of Politically Exposed Person (PEP):

Stakeholder/ Customer shall be categorized as PEP based on the definition provided in this

policy. The Bank shall obtain information or self-declaration from the customer and also

establish a risk management system to identify whether a customer, person seeking to be

customer or a beneficial owner of a customer or transaction is a politically exposed person.

Customer shall be categorized under PEP until span of 5year from the date of retirement or

release from his position related to PEP. Risk management and mitigation in relation to PEPs

are specifically described under section 4.13 of Operational Manual 2017 of the Bank.

d. Identification of Beneficial Owners: When establishing business relationship or

conducting transaction with the customer, the bank shall identify the beneficial owner; verify

the identity of the beneficial owner taking reasonable measures. The Bank shall also obtain

information or self-declaration from the customer. Identification of beneficial owner and the

steps to be taken in lack of such information shall be performed as per the procedure mentioned

under section 4.10 of Operational Manual 2017 of the Bank.

e. High Networth customer: Individual customer shall be considered as High Networth

customer if any of the following condition is met:

i) Annual declared income is Rs One Hundred Million or more by the customer during

account on boarding.

ii) If at any point of time credit balance of the customer reaches to Rs One Hundred Million

or above. [For this purpose, Fixed Deposit and balance on other saving/current account

if any must also be taken into consideration].

iii) Sum of annual credit turnover of the customer (sum of credit transaction) is Rs One

Hundred Million or above.

f. Customer profiling and Risk Grading: The bank shall prepare a profile for each customer

on risk categorization. The bank shall adopt three levels of KYC risk grading system in the

bank. They are: i. Low risk ii. Medium risk iii. High risk

All customer accounts and relationships shall be assigned a specific KYC risk grade. Risk

grading shall be carried out as per the procedure mentioned under section 4.3 of Operational

Manual 2017 of the Bank

g. Periodic review and update of Customer Due Diligence The bank shall view CDD as an

ongoing process and therefore, CDD information of the customers shall be regularly updated.

The frequency of reviews and update shall be determined by the level of risk associated with

the relationship.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

22

The timeframe for review shall be carried out as prescribed under section 4.3 of Operational

Manual 2017 of the Bank. Any shortcomings in CDD information detected in the review must

be regularized as soon as possible. Additional information should be taken from the existing

customers where it is apparent that the existing CDD information is out of dated or inadequate.

Any information on change in the ownership and/or change in persons controlling a

relationship or any other worthy/requiring information shall be taken as a trigger to update

CDD information. While updating KYC information and documents, only changed and

outdated information / documents are to be obtained instead of whole documents.

• The Branch need to main a separate list of account holders, the KYC of which could not

be updated even after regular follow up or where the customer is out of contact.

• Additional document needs to be obtained in case deposit transactions (single or

cumulative) does not match with the declared income during account on boarding and

similarly at the time of review of KYC/CDD and the Risk profile of the customers

h. Rejection or closure of customer relationship or transactions: Refuse and report any

transaction where, based on explanations offered by the customer or other information,

reasonable grounds exist to suspect that the funds may not source from a legitimate source or

are to be used for an illegal activity or as to be used for financing of terrorism or if

customer/applicant/beneficiary refuses or fails to submit required information/ documents.

3.2 Purpose of KYC

The purpose of KYC procedure is:

a. To avert banks from being used, deliberately or by accident, by criminal elements for

money laundering activities.

b. To establish procedures to verify the identification of individuals or corporate or other

institutional accounts to ensure that only legitimate and bona fide customers are accepted

c. To detect suspicious transaction.

d. To establish Process and Procedures to monitor high value and suspicious transactions.

e. To establish systems for conduction of due diligence and reporting of such activities.

f. To ensure that all relevant legal provision are adequately adhere.

3.3 Mechanisms Deployed for KYC

The bank shall use various mechanisms for Customers Due Diligence/ Know your Customers,

these activities shall be carried out at the time of account opening for all the types of accounts

opened by NBBL. Bank shall deploy all or the combination of any of the below mechanisms

for KYC/CDD.

a. Customer identification and profiling including screening of customer against Global

sanction list, PEP and adverse media/ enforcement and blacklisting.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

23

b. Risk Assessment

c. Documentary Evidence

d. Verification of Document as per original

e. Identification of Beneficial Owner

f. Identification or verification of Politically Exposed Person (PEP)

g. Restriction on Account Opening

h. Restriction on opening of multiple accounts (more than one) of same nature by natural

person while on boarding of new customer accounts.

3.4 Know your Employee (KYE)

NBBL shall have process in place that provides reasonable assurance of the identity, honesty

and integrity of prospective and existing employees. Employees are also emerging as the great

source of ML/FT risks for the bank. Therefore, the bank will arrange adequate screening

mechanism as an integral part of recruitment/hiring process of staffs. The Human Resource

Department of the bank shall conduct due diligence of employees before appointing as staff

and during service period on annual basis.

3.5 Due Diligence of vendors, service providers, consultants and business partners

Vendors, service providers, business partners, consultants, etc. also can pose significant

reputational risk to the bank if they are found involved in money laundering and terrorist

activities and/or use the relationship for money laundering or terrorist activities. The Bank

shall collect information about the potential business partners through direct contact, internet

searches and database checks, input or supervision from an independent business function of

the Bank and assistance from any reliable external sources if deemed necessary.

Therefore, the Bank shall not establish relationship with such parties if they are found involved

in money laundering or terrorist financing before establishing a relationship. In following

cases, but not limited to, the bank shall deny maintaining any kind of relationship with the third

party:

• The party is not able to prove its legitimacy

• The party present false, misleading or incorrect information to the Bank

• The party wants to work without a contract or with a vague contract that do not meet the

minimum standards as defined by the Bank

• The party refuses or is hesitant to provide any documentation required by the Bank

regarding the disclosure of identity, nature and scope of its business and its beneficial

owners

• The party requests for any indirect and unusual payment or billing procedure like payment

to anonymous bank account, payment through shell companies, payment through foreign

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

24

bank accounts other than the country where the services are being performed, payment in

high value cash or through bearer cheque, etc.

• The party in any way (directly or indirectly) is incorporated in a jurisdiction identified by

FATF to be a non-cooperative jurisdiction.

3.6 Due diligence of correspondent banking relationships

Correspondent banking is the provision of banking services by one bank (the correspondent

bank) to another bank (the respondent bank). Large international banks typically act as

correspondents for several other banks around the world. It would be the bank’s policy to

obtain sufficient information about correspondent banks to understand the nature of their

business & activities. When considering entering into a cross-border correspondent banking

relationship, the bank shall carry out due diligence measures i.e. ownership, Management

Structure, major business activities, customers, purpose of the Account, location, etc. In

addition, research will be conducted from publicly available information on the correspondent

bank's business activities, their reputation, and quality of supervision and whether the

institution has been subject to a money laundering or terrorist financing investigation or any

regulatory action.

NBBL shall implement risk based due diligence procedure that include, but not limited to, the

following

a. Understanding the nature of the correspondent’s business, its license to operate, the quality

of its management, ownership and effective control, its AML policies, external oversight

and prudential supervision including its AML & KYC regime.

b. Ongoing due diligence of correspondent accounts shall be performed on a regular basis or

when circumstances change. Bank policies also ensure that we do not offer ‘payable

through acounts’. All correspondent banking relationship is duly approved by competent

authority of the bank.

c. The bank shall ensure that it does not maintain any business relationship with the shell

entity.

3.7 Wire Transfer

Wire transfers are used as an expeditious method for transferring funds between bank accounts.

As wire transfer does not involve actual movement of currency, they are considered as a rapid

method for transferring value from one location to another. Prior to initiating wire transfers of

any amount in any currency, the bank shall obtain following information at minimum, with the

customer.

A. Originator’s Name

B. Originator’s Account number or in case of non-account holder, a separate transaction

identification code

C. Originator’s address, birth date and birth place or citizenship number or national identity

card number

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

25

D. Beneficiary’s name and account number or in case of non-account holder, a separate

transaction identification code of the beneficiary

E. Any other information as specified by the regulatory authorities

Inter-bank transfers and settlements where both the originator and beneficiary are banks and

financial institutions would be exempted from the above documentation requirements.

The Bank is not compulsorily required to obtain the information mentioned in above point no.

C for the wire transfer of Rs seventy thousand or less.

The bank shall retain basic information about the originator of the wire transfers as stated above

and make available to the appropriate law enforcement and prosecutorial authorities when

asked for in order to assist them in detecting, investigating, prosecuting launderers and

criminals and tracing their assets.

The Bank shall obtain true identity of the beneficiary while making payment of the wire

transfers. All the wire transfer must be accompanied by accurate and meaningful originator

and beneficiary information. The bank shall retain all the information and document related to

wire transfers at least for 5 years from the date of transaction. Where the staff, initiating the

wire transfer has reason to believe that a customer is intentionally structuring the wire transfers

to below threshold limits to several or same beneficiaries in order to avoid documentation or

reporting requirement, the bank shall insist on complete originator and beneficiary

identification before effecting the transfer. Where the customer is not cooperative, the Bank

shall make necessary efforts to establish the identity and report suspicious transaction (STR)

to the Financial Information Unit.

3.8 Risk assessment

The Bank shall carry out risk assessment of threats and vulnerabilities related to money

laundering and terrorism financing as required by ALPA, ALPR and NRB Unified Directive.

The risk assessment helps to identify and assess threats and vulnerabilities in the Bank’s

operating environment pertaining to Money Laundering and Terrorism Financing and thereby

the risks the Bank is likely to encounter.

a. The bank shall identify and assess the money laundering or terrorist financing risks before

launch of new product, service, business practice, use of new technology and initiating non-

face to face customer services or transaction.

b. The risk assessment shall include risks coming out from following sources:

• Risks in customer

• Risks in Transactions

• Risks in products,

• Risks in services,

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

26

3.9 Suspicious and Large Value Transaction

a. Definition

This section of the document is intended to highlight about the suspicious transaction and large

value transaction. The Bank will refuse any transaction where based on explanation offered by

customer or other available information, existence of reasonable grounds to suspect that the

funds may not be form a legitimate source or are to be used for an illegal activity such as

terrorism, human trafficking etc. The bank shall use reasonable judgment in determining the

suspicious transactions.

The understanding of customers' identity via-a-vis their stated norms of dealings, services, etc

would also have a bearing on transaction before they are viewed as suspicious transactions

hence cautious approach in the process is very essential.

Under no circumstances, bank will alert a customer about his transactions being considered

suspicious or that reporting is underway. The bank will make prompt report of suspicious

transactions, or proposed transactions to Nepal Rastra Bank via Compliance Department, Head

Office.

The bank shall take necessary precautions for identification of suspicious transaction and

onward reporting in events of ST. Some of the indicators of suspicious transaction shall be:

i. Involvement of funds for illegal activity.

ii. Intending to disguise the origin of the assets derived from illegal activities.

iii. Intention to evade AML/CFT procedures.

iv. Customer has no business or apparent lawful purpose and has no linkage with such

business.

b. General Characteristics of Suspicious and Large Value Transactions.

i. Transactions having unclear economical and business target.

ii. Transactions conducted in relatively large amount cash and /or conducted repeatedly

and unnaturally.

iii. Transactions conducted differently from that of usually and normally conducted by the

relevant customer.

iv. Huge, complex and unusual transaction.

v. Transactions from or to the offshore banking locations

c. Elements of Suspicious and large value Transactions.

i. Transaction deviating from:

▪ The established profile;

▪ The characteristics; or

▪ The usual transaction pattern of the relevant customer.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

27

ii. Transaction reasonably suspected to have been conducted with the purpose of evading

the reporting that must be conducted by the relevant reporting entity.

iii. Financial transaction conducted using fund alleged to be attributable to predicate

offences stipulated in the prevailing laws.

d Detection of Suspicious and Large Value Transactions

Whilst all unusual or Threshold transactions are not automatically linked to ML, such

transactions become suspicious if they are considered inconsistent with a customer's legitimate

business, personal activities or with the nominal business for that type of account.

The Bank shall follow the guidelines issued by Nepal Rastra Bank regarding Suspicious

Transaction Reporting for detecting suspicious and large value transactions:

e. Reporting Related to Suspicious Transaction

Upon detection of suspicious transaction or having the reasonable grounds to suspect the

account transaction has derived from the illegal activity or in relation with money laundering,

Compliance Department must report to FIU confidentially. Accordingly, the reporting

modality will be as follows:

▪ The concerned branch staff should report the same immediately to the BCO to ensure that

there are no known facts, which would negate the suspicion

▪ If suspicion remains, the matter should be reported to the Head, Compliance Department,

who will review and investigate the entire case.

▪ The suspicion if well founded should be reported to the concerned authority.

▪ Upon finalization, the suspicion should also be reported to the FIU at Nepal Rastra Bank

in the prescribed Format.

f Account and Transaction Monitoring

Money Laundering risk and CDD does not end after a customer has opened an account. To

satisfy regulatory requirements and prevailing best practices as well as to safeguard the Bank,

the BMs/BCO must perform on-going monitoring of the customers’ accounts at their end.

BMs/BCO must ensure that the CDD documents, data or information retained are kept up-to

date and that the assessment of AML/CFT risk for the customer is appropriate.

Monitoring of transactions will be conducted taking into consideration the risk profile of the

account. Special attention will be paid to all complex, unusually large transactions and all

unusual patterns, which have no apparent economic or viable lawful purpose. Transactions that

involve large amounts of cash inconsistent with the normal and expected activity of the

customer must be subjected to detailed scrutiny.

After due diligence at the branch level in the Bank, suspicious transactions will be reported to

the Head Office Compliance Department. All STR should be duly preserved at branch level.

Head Office Compliance Department shall maintain the records of the STRs files to FIU.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

28

Bank shall deploy the below mechanisms for ongoing account monitoring of accounts based

on:

i. Threshold breach for both personal and non-personal accounts.

ii. Case Logged by AML system

iii. Change of account name

iv. Change of shareholders

v. Change of Signatories

vi. Change of Directors

vii. Activation of Dormant/Where About Unknown (WAUN) accounts.

viii. Account’s transaction reported as being suspicious

ix. The customer has becoming a PEP

x. Customer name has been altered through public media, regulatory authority,

Newspapers, Financial Information Unit (FIU), UN & other sanction lists, CIAA, Tax,

Revenue Investigation& other Nepal Government Authorities etc.

g Prohibited Customers: Anonymous or Fictitious Accounts

i. Shell Banks/Shell Companies

ii. Entities (including natural person, legal person, etc.) sanctioned by major sanction

authorities such as United Nations, Office of Foreign Assets Control (OFAC)-USA,

Her Majesty’s Treasury (HMT)-United Kingdom, European Union, Ministry of Home

Affairs, Nepal (MOHA), etc.

iii. Sanctioned Countries

iv. Offshore Banks

v. Customers from High Risk Non-Cooperative Jurisdiction according to the FATF

The above list of Prohibited Customers is indicative only and not exhaustive.

3.10 Account Review and Revision of Risk Level

Ongoing review of accounts is the process where the bank shall review all its accounts based

on risk grading..For this the bank shall review accounts risk grading as follows:

Risk Grade Review Frequency

High Risk accounts: one year and/or as deemed necessary.

Medium Risk accounts: five years /or as deemed necessary

Low Risk account: eight years/or as deemed necessary.

NBBL AML/CFT & KYC POLICY- (REVISION 2021)

29

Account Risk grading review must be carried out in afore stated frequency and the level of risk

must be upgraded to higher risk level as per the criteria set forth by Nepal Rastra Bank’s AML

Directive.

Account Risk level should be downgraded as follows:

a. In case of medium risk level accounts, cumulative balance is less than prescribed threshold

for both personal and Non-Personal A/Cs for last 2 year

b. Signatories/Directors/Head of the organization/Shareholders/Beneficial Owners are no

longer PEP

c. Resident /Operating Address is no longer under High Risk Countries

d. Nature of business is no longer fall under High Risk Business

Branch In-Charge must obtain approval from IOD/Head Office approval for downgrading of

risk level in all accounts.

3.11 Ongoing Due Diligence

Ongoing monitoring is an essential element of the effective CDD process. Customer

transactions shall be monitored automatically or manually whichever is feasible for the

Bank and as per the NRB Directives. Branch compliance officers can effectively control

and reduce the risks only if they understand normal and reasonable activities of a customer

so that they have the means to identify irregular patterns of transactions. However, the extent

of monitoring depends on the risk sensitivity of the account. Branch compliance officers

should pay special attention to all complex, unusually large-value and/or unusual patterns

of transactions that have no apparent economic or visible lawful purposes.

3.12 Relationship with Walk in Customers:

The Bank shall obtain the KYC Documents and identify the Walk in Customers in case of