national policy on software products 2014 - ispirt · seen combinatorial innovation at work in the...

TRANSCRIPT

National Policy on Software Products 2014 Draft v1b

Preamble 1. Software product industry can be the growth engine for India. It has already

demonstrated its potential. Further, it is aligned with our national competitive advantage, and does not require prolonged “infant industry protection,” unsustainable subsidies or difficult to justify preferential treatment. It has the potential to generate substantial export earnings, and contribute positively to India’s current account deficit.

2. India possesses the following foundational blocks for a thriving software

product industry. It has well demonstrated skills in software. Indian software engineers, many working for MNC R&D Centers, are responsible for developing complex products for world’s largest product companies. Many of these talented engineers now aspire to be technology entrepreneurs. Unlike hardware products, where it is clear that India lacks essential elements of the ecosystem such as semiconductor fabrication and strong hardware R&D, the software product ecosystem is reasonably well developed. Further, mobile proliferation, commoditization of computing hardware and advent of cloud computing have made it possible to deliver software products across India. Finally, in the global market, thanks to success of Indians in Silicon Valley product startups, there is a relative absence of “liability of origin” effects. Indian companies like FusionCharts have already demonstrated that it is possible to sell products online from India without the liability of origin disadvantages that inhibit other industries (e.g. Tata has not added the Tata brand name to their global Jaguar and Land Rover brands for fear of these “liability of origin” effects).

3. For the first time in the history of the technology industry it possible for small entrepreneurial teams to develop complex software products quickly1. This is due the ‘Combinatorial Innovation’ (Varian, 2004) becoming possible with the rise of open source and web-services architecture. In India we have seen combinatorial innovation at work in the UID project. The core UID application was built by a very small but talented team of volunteer developers. They used many open-source components, built a few new ones,

1 The power of Combinatorial Innovation is well established and history is dotted with several of these periods. Back in 1898 it resulted in Wright brothers beating Langley to the creation of first powered flight despite Langley having a $70,000 grant from the US Government and the Smithsonian Institute. Later, combinatorial innovation was famously at work in Edison’s lab in the creation of a useable filament based light bulb. The electronics industry has used combinatorial innovation to turn hobbyists like Steve Jobs into computer makers of the world. More recently web-apps started being built using combinatorial innovation and these “mash-ups” resulted in rise of Yahoo and other internet players. Finally, and to India’s advantage, this power of combinatorial innovation has reached the world of business applications.

and then glued them all together in an innovative fashion to rapidly create the world’s largest identity management system.

4. Just like the mobile revolution where mobile penetration exploded

worldwide, a SaaS revolution is now underway. SaaS products are penetrating every small business. This is because they offer high functionality at a fraction of the cost of traditional enterprise software. The global market is estimated to be $600 billion dollar global opportunity (out of the total US $1.2 trillion dollar opportunity for software products). For the first time Indian SaaS product companies are part of this emerging market opportunity from the beginning and some early winners are starting to emerge2. It is vital that we build on this early momentum. In the software product industry the winners take most of the profits. Therefore timely intervention to nurture and amplify the Indian software product industry momentum is vital.

5. India is blessed with the world’s largest number of small businesses, primary and secondary schools, rural healthcare centers and farmers. As the mobile revolution unfolds, it has become possible to upgrade their functioning by use of software products (applications) at an affordable cost. Rather than rely on central design and control and a scale-out approach, it is possible to deploy software products using a “spread-out” model. This results in faster and smoother adoption as it relies on local aspirations and has a built-in mechanism for ensuring utility of the investment. Even today, Indian software product companies3 are impacting 3 million small businesses. With a policy impetus, this can grow to 30 million small enterprises. It is bring competitiveness to small businesses, teaching effectiveness to schools, productivity to healthcare centers and new skills to farmers.

6. A healthy software product industry is also pivotal to developing our defence,

aerospace and electronics industries. It is also necessary for creation as well as maintenance of strategic technologies that are critical to national security.

7. A strong software product industry is of strategic importance for India. In

addition to its direct impact on GDP, exports and balance of accounts, this industry also holds the potential to unleash social transformation, simultaneously addressing the economic growth and human development needs of India. Indian software product industry is in the maturation stage. The National Policy on Software Products provides the springboard for India to emerge as a global leader in this important industry.

8. The rise of software product industry in India is path dependent. This means

that small interventions will have disproportionately large effects in the

2 When ZenDesk, the SaaS market leader in customer service desk management products, did its roaring IPO earlier this year, it listed six key competitors in its S-1 SEC [US Securities and Exchange Commission] filing. Four of these - Kayako, Freshdesk, Supportbee and Tenmiles – are Indian! 3 Like Tally for accounting, Fordian for School ERP, Practo for doctors, Forus for eyecare, etc.

future. To leverage these effects it is essential to understand the stages of industry evolution that software product industry will go through. What is appropriate for one stage can even become counterproductive in the next stage. Therefore the National Policy on Software Products is built on the evolution framework of the software product industry4.

I Vision To drive the rise of India as a Software Product Nation and create in 10 years:

1,00,000 Product Startups in India Employment for 3.5 million technical people $500+ billion in Market Value, and New levels of performance for 30 million small enterprises.

II Mission 1. To capture 8-10% of the global software product market of US $1.2 trillion

USD by 2025 by enabling all sectors of the software product industry.

2. To build domestic market and grow penetration of software products to 30m SMEs in India thus raising their competitiveness, and emerge as Small Business Application Software (SBAS) hub for the world.

3. To create 3m technical operator jobs on the back of software product adoption in SMEs.

4. To promote Indian mid-market SaaS products across the world with desk selling and marketing, so that category leaders emerge in 12 segments.

5. To promote Indian software product companies tin software infrastructure sector such that global leaders emerge to support explosion of data and video, usage of e-commerce, security of BYOD, availability of real-time social media, programmatic advertising5, etc.

6. To create novel business models and pathways for transformation of social enterprises like rural healthcare centers, primary schools, small family farms,

4 The evolution framework is described in the Appendix: Stages of Indian software product industry evolution. 5 There are potential leaders in each of these areas already. Druva, a Pune based startup is a global market leader for endpoint data security and governance infrastructure. Adsparx is an emerging leader for dynamic ad insertion infrastructure for mobile video. Unbxd is an emerging leader for e-commerce search infrastructure. i7 Networks and Uniken are emerging leaders for BYOD security infrastructure. Frrole and Qubole are emerging leaders for real-time social media analytics infrastructure. Inmobi is a global leader for mobile programmatic advertising infrastructure with Vizury, Pubmatic and others also doing well in related segments.

etc. so that new capacity is created to meet the unmet demand for public services.

7. To simplify rules for software products to prevent software product companies moving away from India.

8. To provide a level playing field to Indian software product companies,

particularly related to seed funding and public sector procurements, so that they can fully leverage the benefits of a large domestic market.

9. To refresh Brand India from the taint of being the back office of the world by highlighting India’s credentials as a land of technology, disruptive ideas, inventions and cutting-edge products.

III Objectives and Strategy 1. Ease of doing business. To publish an annual report on ease-of-doing

business for software product firms6. This will address SME listing and public listing norms7, M&A regulations8 that facilitate or hinder acquisitions, and investment regulations that facilitate or hinder VCs investing9 in Indian product startups. This will seek to arrest and reverse the movement of software product startups from India to US and Singapore jusrisdictions.

2. Tax. To bring clear demarcation in the tax regime between Software being

delivered as Service and Software as Product. A mechanism to notify a software product definition10 will be established so that there is homogenous understanding across Central and State govermnets, and across Direct and Indirect taxes. An new National Industrial Classification (NIC) code shall also be created for the software product industry11.

6 It covers ease of doing business for 5 facets of a software product startup: starting, running, giving stock options, M&A and going public. For instance, in the facet of starting, it benchmarks India against a goal of being able to start a software product company with a day of effort, online with less than Rs 5000 by interacting with a single site, and filling out a single form. 7 For instance, public listing norms require a minimum 3 years of profitability. This is pushing technology companies to list abroad. 8 Pernicious regulations related to payouts to investors prevent small M&As to happen in the software product industry. 9 Urgently needed are policy measures to allow VC and PE firms to directly invest in India rather than through foreign shell entities established in places like Mauritius. 10 Appendix lays out the “Principles for taxing software products”. 11 The Indian NIC code was last updated in 2008. This is when a new code (#72) was added for “all computer related activities” including activities “such as consultancy of hardware and software configurations, software supply, data processing and data base activities as well as repair and maintenance of (mostly smaller) computers and office machines.” This is clearly out of date and doesn’t reflect the state of the IT industry at all.

3. Buy Products, not Projects. To develop Model RFPs for buying software

products in place of custom projects for Government systems. Shifting Government buying from projects to software products will reduce cost of ownership dramatically12. A special effort will be made to incorporate domestic software products in the Defence sector. For PSUs and State Owned Enterprises, "Preference to Domestically manufactured Electronics products in Government Procurement" policy shall be extended domestic software products as well.

4. Defence and Cyber Security. To setup a Cyber Security Staging Lab (CSSL)

in an academic institution of repute to select cyber security products for accelerated trials in the defence and security institutions. This lab will be headed by an expert academic and will be supported by both public sector and private sector experts. CSSL will also organize ethical hacker meets with support of existing security communities13.

5. Rating Agency. To encourage the creation of a non-profit and independent

rating agency14 for software products in India. This would provide products and technology rating leading to expedited software product procurement decisions.

6. eGov Open APIs. To upgrade all eGov Services to Open APIs15. This will

empower ordinary citizens with responsive governance, driving greater public efficiency and satisfaction. It will bring tangible benefits for millions of people. Small Businesses will see greater efficiencies leading to increase in velocity of transactions, better collaboration, and corresponding growth.

7. MSME Competitiveness. To catalyze 5 million MSME’s into a fully cashless

era in 5 years by providing tax rebates to MSME's on cashless transactions. This would set in motion a virtuous cycle of technology upgrades leading to improved competitiveness of this important sector that contributes to employment and economic activity. A side benefit would reduce tax leaks and increase granularity of actual data leading to more informed planning decisions and interventions.

8. Employment. To create occupational standards along with an inexpensive

but modern training ecosystem for technical operators of software products

12 A recent survey by iSPIRT of 57 Mayors shows that each was using a custom developed solution for providing birth and death certificates. While this duplication of effort is good for the software services industry, it raises the costs for the country as a whole. 13 An example of an active Cyber Security community is the Null Open Security community. 14 iSPIRT PTR Council headed by Prof. Ashok Jhunjhunwala of IIT Madras is rating system called PTR that, if successful, could aid meeting this objective. 15 This requires participation by other Ministries. For example, APIs for GST require Ministry of Finance to be on board.

in the SME segment. Software adoption in 30 million SMEs is expected to create 3m technical operator jobs16.

9. Education and Talent. To fix the engineering curriculum such that it lays

emphasis on developing best-in-class products. To also support engineering colleges in leveraging the shift to achievement credentials17. This will improve the availability of skilled workforce suitable for software product companies.

10. Institute of Product Entrepreneurship. To create an Institute of Product

Entrepreneurship using a public-private partnership model. This Insitute would focus on prepare product entrepreneurs using Lean Startup methodology and Effectuation principles18.

11. Seed Funding. To promote a Software Product Development Fund to address the acute shortage of early stage capital for India software product startups19. Availability of angel and seed stage capital is a key driver in the growth of the software products industry. It will reduce mortality before the product-market fit stage.20 It also has number of multiplier effects. These range from follow-on innovations to deepening of the entrepreneur pool to creating winners by increasing speed of execution. The Software Product Development Fund will be setup as a fund-of-funds21.

16 Technical operator jobs are created when software products are implemented by SMEs. Tally trained accountants are well known. Use of Fordian, a school ERP, requires technical operators as well. Same is the case with Practo, a doctor ERP, or with Premise Management System for small hotels. 17 RSPCT.in is a new-age matching program for enlightened product companies that prefer to hire people with achievement credentials and those youngsters that have just acquired those credentials. t has an open architecture approach that encourages all Institutes to participate on a level-playing field basis. 18 Effectuation is a set of management principles that are very relevant to product entrepreneurship in India. These have been developed by Prof. Saras Sarasvathy, Isidore Horween Research Professor of Business Administration, Darden School of Business, University of Virginia. 19 This has been surfaced in Sep’12 Report titled “Creating a Vibrant Entrepreneurial Ecosystem in India” by Committee on Angel Investment and Early Stage Venture Capital, appointed by the Planning Commission, under the chairmanship of Shri Sunil Mitra, former Revenue Secretary, Government of India. 20 An iSPIRT survey has shown that currently 67% of the software product startups are pre-product-market fit stage. This is available as iSPIRT Product Industry Monitor report dated Feb’14. 21 Any new program should have three features. First and foremost, it should follow the funds-of-funds model and support many small angel and venture funds. Second, it should not try to pick winners. Third, it should foster relationships between Indian and International (Singapore, Israel and US) angel and seed investors.

12. Incubators. To foster competition amongst incubators and accelerators by

weeding out big players and poor performers after a 5 year period and replacing them with new players. The public good is served when incubators compete for startups attention based on their track records22.

13. Strategic Research. To create a Software Product Industry Research Program (SPIRP) that will focus on building strategic technologies at IISc/IITs/IIITs and providing privileged access to multiple startups at the same time. It will develop a symbiotic relationship between publicly funded research centers and multiple product companies to achieve the kind of benefits that DARPA and Cambridge have provided to their local product ecosystems23. The immediate focus areas will be on technologies, like Deep Packet Inspection (DPI), Finite Elements Analysis, Shock Analysis, Special Effects processors, which are strategic for India’s security infrastructure and might be on the US Export Control list.

In effect, we do not recommend an approach where there is a single venture fund. Given the diversity of the Software Product Industry this approach is unworkable. In terms of picking winners, governments and even venture capitalists themselves have a poor record of trying to guess which industries will grow the fastest over a 10-year horizon. The most successful investors in startups have therefore been those that remain flexible, able to adapt to unexpected innovations and the changing economic environment. Early-stage investing operates locally because only those embedded in the community have the information needed to place wise bets on unproven managers. Government has a important catalyst role to play in growing th pool of early stage investment managers. US did this with its SBIC Program in 1958 and Israel did the same with Yozma Program in 1993. Its time for India to replicate this in 2014. 22 Creating one mega incubator is not the answer. In fact, reducing competition is positively detrimental to the ecosystem. 23 SPIRP goes beyond creating and promoting research centers of excellence within IISc/IITs/IIITs. It provides a way to integrate these centers with multiple product companies on the other side. The current model of having partnerships with specific individual companies is not viable given the rapid technology evolution. The half-life of a technology startup is too short. This is why, it is important to have collaborations with multiple companies at the same time. There are two other alternatives hat were considered but both are not appropriate at this stage of the software product industry. First is the current system of providing write-offs of R&D expenses against future profits. This is not a practical solution. The Indian software product industry doesn’t (yet) have the wherewithal to fund core research in this technology. Second alternative is SEMATECH like consortium approach where Indian software product firms enter a consortium in search of R&D projects complementary to the ones that they have on hand. We do not favor this approach for two reasons. First, Indian software product firms are young and immature. Second, given that we are a low-trust society, operating a consortium is fraught with operational risks.

14. R&D Credit. To extend deferred tax credit to 7 years after the R&D

investment. The current write-offs of R&D expenses against profits do not work for most young product companies because they do not have profits at the initial stage when their R&D expenses are high.

15. R&D Grants. To extend DSIR’s PRISM program (formerly TePP) to software product industry. The potential for positive impact has been demonstrated in the biotechnology field.

16. Challenge Grants. To setup challenge grants for social transformation moon-

shots in Education, Healthcare, Sanitation, Agriculture and other sectors in collaboration with Science Parks24 and Think Tanks25. While our previous moon-shots in Space and Nuclear sectors could not leverage the private sector in this way, Challenge Grants are appropriate for the current plans to develop domestic technology in the Defence sector. Challenge Grants are a powerful tool to use26 at this stage of the industry evolution. They create valuable social results and drive the maturation of the industry.

17. Trade Promotion. To integrate Indian software products in India’s foreign

aid programs, and to develop trade promotion linkages with product nations like China, Korea, Taiwan, Israel and USA.

Government Structures. 18. DEITy to have a senior officer focused on the software product industry. A

separate division shall be created.

19. To setup a National Software Products Mission with industry participation to evolve programmes in pursuit of laid down policies and also to create institutional mechanisms to advance the implementation of various programmes aimed at achieving the objectives in this policy and to promote India as a Software Product Hub and brand India as a “Product Nation”.

20. To establish an Office of Technology, Innovation and Research to guide long range, horizon 3, strategic investments in technology, innovation and research. This Office will orchestrate the long-range roadmap for the industry with participation from Think Tanks.

21. States would be actively encouraged to promote Software Products industry

24IKP Knowledge Park in partnership with USAID and the Bill & Melinda Gates Foundation has run the Grand Challenge on TB Control. 25 iSPIRT as a Think Tank is designing challenge grants under its iPrize initiative. 26 Challenge Grants have a chequered past. The oldest challenge grant is the British Government’s Longitude Prize established in 1714. More recently, the Ansari Space XPrize has been successful in fostering private space industry. Recently, Google Lunar Xprize Board is generating news with Team Indus, an Indian team, rising to the top three.

Draft for: Mr. Raj Kumar Goel, Joint Secretary, DEITy, Government of India,

V.1 Appendix. Principles for taxing software products Software Products need to reach out to the masses, and therefore, need a lubricated way to distribute and resell, whether for initial delivery and/or initial subscription, upkeep and/or renewals.. Today there are several anomolies in the what sales/service/excise tax is charged on software creation friction that is holding back the software product industry. By clarifying priciples for taxing software products, we hope to ensure that both Center and State Governments have a common vie about ‘when, and why, which tax is supposed to be applicable’. The source of confusion comes from the fact that software products are delivered in many ways, sometimes as a tradable license (packaged software), sometimes as non-tradable use (SaaS), and sometimes tradable ‘right to use/service’ (which is where SaaS is going).

Introduction This Software Industry in general, and the Software Product Industry, in particular, are amongst the new-age economic activities which have stressed traditional definitions of ‘goods’ and ‘services’, and therefore, associated legislative interventions. India, in particular, is peculiarly affected due to its dual legislative authorities of ‘center’ and ‘state’ – each having constitutional jurisdiction for taxation. To quote Peter Hill, from his paper titled “Tangibles, intangibles and services: a new taxonomy for the classification of output”, written just before he took a position with UN Economic Commission for Europe: “The distinction between goods and services has been traditionally interpreted by

economists as if it were equivalent to a distinction between physical commodities, or

tangible material products, on the one hand and immaterial, or intangible, products on the

other. The economics literature is full of statements to the effect that goods are material,

or tangible, whereas services are immaterial, or intangible. Such statements are casual

and conventional rather than scientific, as the nature of an immaterial product is not

explained. In practice, intangible products deserve more serious attention because they

play a major role in the ‘information economy.’ They are quite different from services.”

To understand the reasons why the new-age economic activities have created a problem, we should first examine the most common definitions of ‘good’ – and, again quoting Peter Hill: “Two characteristics of a good are the following:

A good is an entity that exists independently of its owner and preserves its identity through

time. If ownership rights can be established it follows that they can also be transferred

from one economic unit to another, which implies that goods must be exchangeable: i.e.,

tradable or vendible as emphasized by Smith and others.”

This fundamental property is inherently absent in a ‘service’ – since it can be ‘used or consumed’ but not ‘transferred’.

The transferability of a ‘good’ allows for an owner to reach out and deliver to far-flung customers of good through direct, distribution, and/or retail chains. In recent times, the concept of ‘right to service’ as a tradable instrument has stressed the definitions and distinctions of ‘good’ versus ‘service’. For example, a ‘concert ticket’ is tradable, and the value of the ticket is not the value of the ‘ticket material’, but the value of the ‘concert service’. However, the concept of the ‘ticket’ allowed for easier distribution and sale, and resale. The telecom industry aggravated the problem with Prepaid Cards – where again, a ‘right to service’ was sold through multi-tier distribution channels, challenging the traditional concepts of taxation. The Software Industry amplified this problem multi-fold – and software-enabled services set to magnify it even further, like electronic books and music. In the days ahead, we can anticipate fresh debates with 3D-printing changing the very fundamentals of even tangible goods, and how its associated commerce takes place. This Appendix provides a simple framework that can definitively resolve and lubricate the issues associated with the Software Product Industry, and potentially have a broader application to almost all new-age economic activities. The importance of doing this cannot be understated. The overall ability for massive inclusion of entities participating in economic growth requires that access to technology exists. Access to technology requires the ability to lubricate and promote the commerce associated with it.

Similarities and distinctions between ‘tangible goods’, ‘intangible goods’, ‘right to service’, and ‘service’ ‘Right to Service’ and ‘Intangible Goods’ have several of the same characteristics as ‘Tangible goods’. Borrowing from Peter Hill/Smith, each of these three: Can exist independently of the owner Preserve their identity through time Can be transferred from one economic unit to another Are exchangeable, that is, tradable or vendible Since they all have an associated ‘title’ or ‘ownership rights’ at a given moment in time, the process of transferring the title/rights is tantamount to ‘trade’, and within the state, liable for VAT, and across states, liable for CST. In contrast, a ‘service’ has none of the above characteristics. Quoting again from Peter Hill: “A hospital can hold stocks of medical goods and equipment ready for use but it cannot

hold stocks of appendectomies ready to meet an epidemic of appendicitises. The notion of a

stock of appendectomies that exists independently of both surgeons and patients is pure

nonsense”

Services cannot be traded, in the same way that a manufacturing activity (of tangible goods) is not a trading activity. Both these – services and manufacturing activity – for the most part fall under the legislature of the Center (with a few exceptions like Alcohol manufacture). And they attract Service Tax, or Excise Duty – as the case may be. Both these laws are constructed on the premise of non-tradability, and their associated rules inherently do not have a one-to-one correlation of ‘purchase’ and ‘sales’ – which is implicit in trading activities and associated laws (like VAT and CST). The problem that arose over time is the concept of a ‘tradable service’ – which concept is inherently paradoxical. Yet, it exists – though not as a ‘tradable service’, but as the ‘trading of a right to service’. The pitfalls of treating all tradable concepts – like Intangible Goods and Right-to-Service – in the same bracket as Tangible Goods also exist. Tangible Goods get ‘produced/manufactured’, and become economically relevant ‘inventory’ of the ‘producer/manufacturer’. This activity attracts Excise Duty – and confers a ‘title’/’ownership right’ of that inventory. Its sale now attracts VAT or CST. However, Intangible Goods and/or Right-to-Service do NOT have these same properties of ‘production/manufacture’, nor their coming into existence creates an economically relevant inventory for the owner. For example, if you walk into a music store, and buy a ‘coupon for Rs. 100’ which gives you ‘rights to download the soundtrack of a new movie’ – that ‘coupon’ has ‘ownership’ value only to the store which stocked it, and the person who purchased it, and has no value to the ‘producer’ of the coupon. Neither does the sale of the ‘coupon’ require the ‘producer’ to ‘reduce any inventory’ – even if the ‘soundtrack is downloaded’ – since there was ‘no tangible goods to produce’. However, the moment an ‘intangible good’ or ‘right to service’ moves to a distributor and/or retailer, it has ‘inventory’ value of the same characteristic as a ‘tangible good’. This overlap – of similarities between tangible goods, and distinction from tangible goods – has caused enough historical confusion in legislations, with corresponding aggravation of the legal system, as well as friction in the day-to-day commerce of new-age activities. In fact, the concept of ‘right-to-service’ and ‘intangible goods’ are almost identical – and we can treat ‘right-to-service’ as a special case of ‘intangible goods’. Taking all of the above, we attempt to craft an encompassing framework.

The framework, in some detail This framework covers the following methods of commercial activities for Software Products:

1. The ‘manufacture’ and subsequent distribution/sale of ‘packaged software’ (a dying breed, since almost all software has moved away from media-based sales)

2. The distribution/sale of ‘licenses’ – which allow the end-buyer to download and use the software.

3. The distribution/sale of ‘right-to-upgrades/AMCs/Service Contracts’ for a defined period – which allow the end-buyer services on top of their purchased ‘packaged software/license’

4. The online sale of the ‘license’ (point 2 above), or ‘upgrade/right-to-upgrade/AMC/Service Contract’ (point 3 above)

5. The use of the software over the internet – also called Software-as-a-Service (SaaS), which a buyer may buy online for a defined period

6. The distribution/sale of ‘right to SaaS’ – which allow the end-buyer to avail the required service for a defined period

Each of the above six transaction types have sub-types which is: end-buyer buys from company, end-buyer buys from intermediary.

Dealing with ‘Service Tax’. It rests on the premise that a ‘reseller of a right-to-service is selling a ‘good’, but not the ‘service’’. Therefore, the reseller should not be required to fulfill the norms of Service Tax. However, the original ‘producer of the right-to-service, and therefore, the service-provider’ must pay the required Service Tax. This Service Tax cannot be made available as ‘input credit’ to the Reseller – since the Reseller is not ‘using/consuming the service’. Now, in order to allow the buyer (if the buyer is not a consumer, but a company) the associated Service Tax credit, the producer should be allowed to provide a ‘pure service tax credit advice’ which can be used by the buyer to avail the relevant credit. In all cases, the Government is tax neutral, since the Service Tax has been fully paid for. If the buyer has directly purchased from the service provider, the invoice itself acts as the Service Tax credit. The above change will yield the following transaction flow (assume a ‘right-of-service’ as Rs. 1000, with reseller margin of Rs. 200): Company invoices to Reseller: Rs. 800 + Service Tax (12.36% on Rs. 1000),

but no VAT (since no ‘title’ got transferred). Reseller invoices to Customer: Rs. 1123.60 + VAT (say 5%) – cannot claim

Service Tax input credit, and needs to pay the output VAT. Customer: IF the customer is eligible for Service Tax input credit, can seek the

corresponding Service Tax Credit Advice from the Company. Else, the transaction closes.

In this chain, the Center has received the relevant Service Tax amount, and the State has received the relevant VAT for trading the ‘right to service’. In contrast, the current laws require the Reseller to both charge Service Tax, as well as take credit for it. However, the nature of the transaction is a trading activity and NOT a service. For example, if the reseller was unable to sell this ‘right

of service’, he/she could have done a ‘sales return’ to the company, and similarly, accepted a ‘sales return’ from the customer – in case the customer chose not to avail the service. Additionally, while the Company could directly sell to the Customer without any prior ‘purchase/manufacture’ step, the Reseller does NOT have such an ability – since the reseller is simply trading on something one has purchased, and is hence selling. Lastly, when the final invoice contains both Service Tax and VAT, it violates the constitutional principle of concurrency of legislature on tax – since no provision for concurrency exists for any area of tax. The simpler transaction flow, is of course, the Company directly selling to the Consumer – when the invoice would be Rs. 1000 + Service Tax.

Dealing with ‘Excise Duty’. The first, of course, is applicability of Excise Duty itself. This should be applicable only if a ‘tangible good’ is being produced – in the form of physical ‘packaged software’. Side note: if the previous concept of right-to-service is implemented in completeness, it may be more beneficial to the Government to treat all software, including packaged software, as attracting Service Duty uniformly, and the concept of ‘packaged software’ is simply a ‘right to service’ since it IS an ‘intangible goods sale’. Currently, due to the high friction of ‘trading a right to service’ as explained in italics above, it seems more ‘trade-friendly’ to have Excise Duty. The current abatement of Excise Duty at 15% of MRP, does not take the ground reality of software distribution costs into account. Most software, if sold through a distribution/reseller chain, have margins ranging from 25% to 50% - as the only viable means to counter the temptation and threat of piracy, and to encourage the eco-system to deal in legal software. The spirit of abatement, which is to tax the economic benefit arising to the manufacturer/producer is not met through an abatement of 15%. This should either become ad valorem – that is, the actual invoice value, or the abatement should become 35% at least. Making it at the actual invoice value has additional benefits of simplifying multi-seat licensing – which inevitably goes at significant discounts to the MRP. Once again, having the current concept of abatement does not take these new-age methods of commerce into account – where many of these problems were irrelevant in the traditional businesses.

Dealing with TDS An anomaly has been created in the commercial process of Software Products which needs correction. The concept of TDS was introduced to pre-tax incomes accruing to a given entity – and not to tax ‘turnover’ accruing to a given entity. This is the reason why TDS does not exist on any trading activity.

Except for Software Products, and ‘right to services’ – which are not ‘incomes’ for the distribution/retail chain, but are equal to ‘goods’. On one hand, this is fundamentally flawed – to apply TDS on a tradable good. From the Government point of view, it attempt to give some ‘relief’ to the industry by converting it to ‘single point’ – and requiring all further trading points to carry a declaration on their invoice that TDS has already been subjected to. From a trading community perspective, life is simpler to ‘not deal in software’ and require this ‘compliance’ – since any negligence would land up with their losing almost their entire potential income in terms of cash flow. On another hand, most (if not all) Software Product companies work with both negative cash flow, and negative profits in their inception years. Even with single point TDS (which is inherently flawed as mentioned above), this aggravates their cash flow to the point of non-viability. On a third hand, more and more of the commerce is shifting to online purchases – even when a Service is being purchased. It is almost impossible to have a workable method which allows TDS to be administered both from the buyer and seller side. TDS, as an instrument of early tax collection, works very well when there is regular commerce between buyer and seller, typically on credit. The obligations to pay the TDS and ensure that the TDS credit is available to the seller, happens smoothly in such situations. In situations where the seller is selling to hundreds of thousands of buyers – with whom no direct ‘contact’ can be established for completing a TDS denominated transaction – it is very evident that this frame is flawed. This is exactly the situation for all ‘goods’ – which is also why TDS is not applicable in any of those situations. For simple equivalence of treatment, and associated lubrication of commerce, TDS should be removed completely.

Summary The above framework has been tested against all the problems and issues raised in this document. The proposed framework will lubricate all the channels of commerce that have been discussed.

A compelling proposal The importance of the Software Product Industry comes far more from its Indirect Impact on the Economy, rather than its direct impact. It is a foundational enabler for upliftment of citizens and businesses alike, who will collectively contribute to the economy of the country. There is a compelling argument to say that software products, in all its forms, should be exempt from all taxes, for – say – a period of 5 years (till 2020), such that the entire economy gets a major shot in the arm.

Conclusion Software products are sold under a variety of business models, in much the same way that other industries do. A taxataion framework for software products has to recognize this fact. This framework provides elegant priciple for taxation while retaining the distinction of the various transactions types, and therefore, the various applicable taxes.

V.2. Appendix. Stages of Indian software product industry evolution The rise of software product industry in India is path dependent. This means that small interventions will have disproportionately large effects in the future. To leverage these effects it is essential to understand the stages of industry evolution that software product industry will go through. What is appropriate for one stage can even become counterproductive in the next stage. Indian Software Product Industry has five stages of evolution. The Indian is now entering Stage 3.

Stage 1: Underground Movement. 1999-2010 During the 11 years since 1999 Indian software product industry was an underground movement. Not many people, even in the IT Industry, were interested in this area. Yet, much was happening. The nascent industry was building confidence. During this stage, three success stories came to the fore that provided confidence to broader audience that software product industry can take root in India. In the Large Business Application Software (LBAS) segment, iFlex showed the way. Its acquisition for over $1 Billion dollars in 2005 by Oracle was a big boost to Indian software product industry. In the Small Business Application Software (SBAC), Tally sold to more than a million SMBs in India. This was a big milestone even by global standards. Tally joined a select club of software product companies in the world that have more than a million business customers. Finally, out of Kolkatta no less, FusionCharts sold its charting software to over ten thousand businesses outside India without having any sales office or sales presence in US. This

success galvanized the belief in India’s ability to be a player in the booming global SaaS market. Towards 2007, we saw industry leaders in Indian software product industry come together, first to celebrate success, then to create media awareness of the Industry and finally to create public goods necessary to take the industry forward.

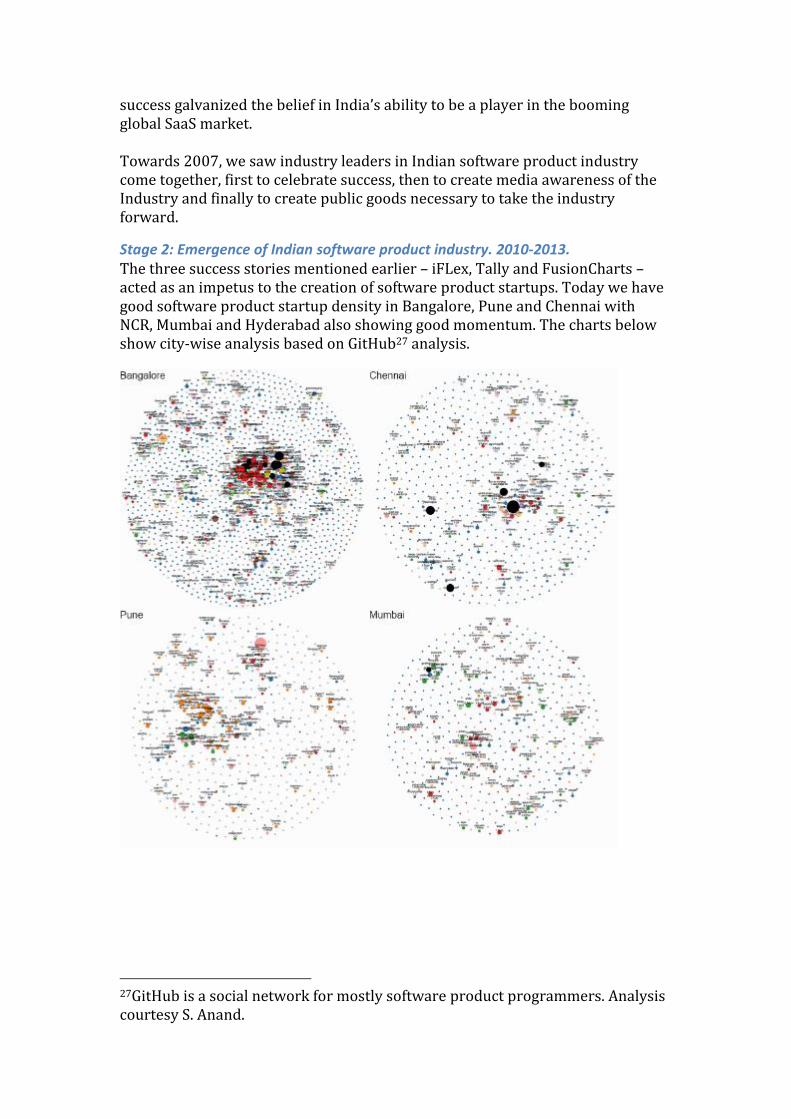

Stage 2: Emergence of Indian software product industry. 2010-2013. The three success stories mentioned earlier – iFLex, Tally and FusionCharts – acted as an impetus to the creation of software product startups. Today we have good software product startup density in Bangalore, Pune and Chennai with NCR, Mumbai and Hyderabad also showing good momentum. The charts below show city-wise analysis based on GitHub27 analysis.

27GitHub is a social network for mostly software product programmers. Analysis courtesy S. Anand.

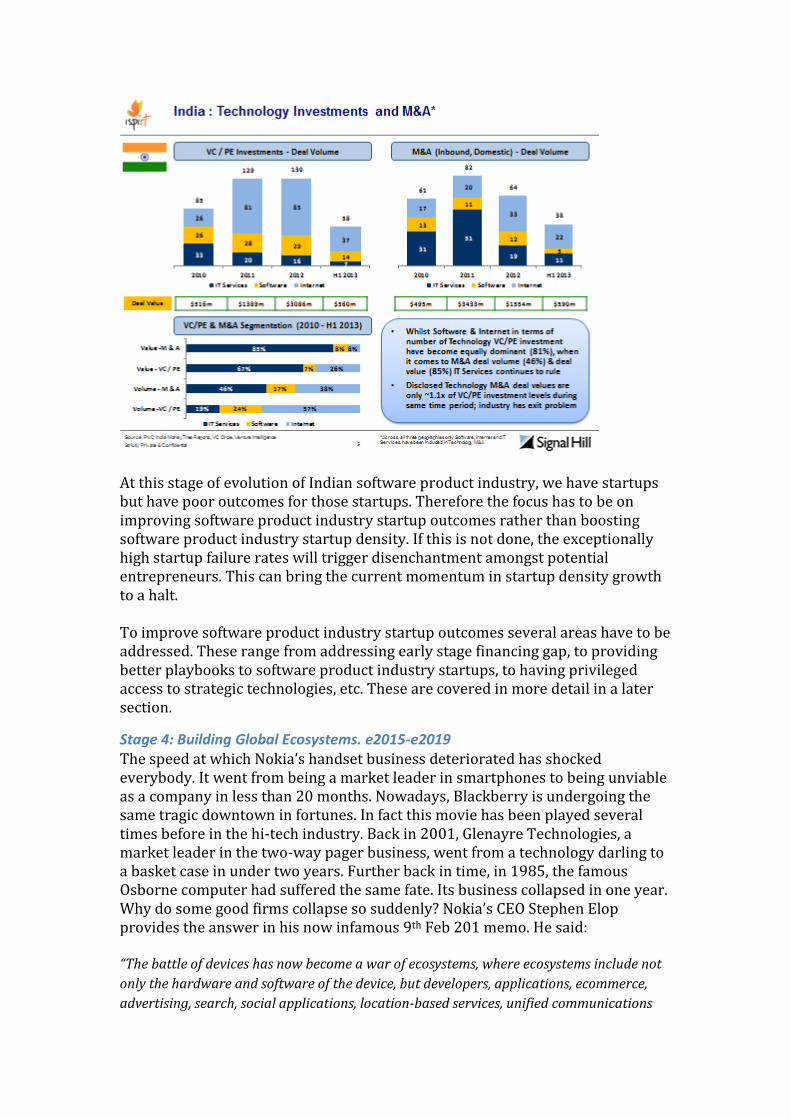

Software product startup density in India is now healthy. On Angel List28, India now 3.2 times more startups (2123 versus 651) than Israel, which is a shining example of hi-tech industry. Given these excellent numbers, we don’t need policies to boost software product startup rates. Instead we need policies and institutions to reduce software product startup failure rates and improve outcomes.

Stage 3: Maturation. 2014-e2017 This is the stage where the software product industry reaches a critical mass of companies needs to consolidate its position. This stage is typically characterized by a string of positive outcomes – substantial VC investments, M&As and IPOs – that give the industry much needed validation and a boost of confidence. Conventional wisdom, not just in India but across the world, holds that 2123 Indian software product industry startups listed on Angel List will have much poorer outcomes than the 651 Israeli software product industry startups. This belief is supported by data. An isoftware product industryRT and SignalHill analysis29 reveals that India has the worst multiple in terms of M&A exits. In Israel the M&A exit value was ~7X of the VC/PE investment during the same period. In US the multiple was ~5X. In India it was only 1.1X (and this too was inflated because it counted IT Services M&A exits as well).

28 Angel List is the leading platform for technology startups looking for early-stage funding. Data as of 3rd Nov 2013. 29 This is dated 10th Oct 2013.

At this stage of evolution of Indian software product industry, we have startups but have poor outcomes for those startups. Therefore the focus has to be on improving software product industry startup outcomes rather than boosting software product industry startup density. If this is not done, the exceptionally high startup failure rates will trigger disenchantment amongst potential entrepreneurs. This can bring the current momentum in startup density growth to a halt. To improve software product industry startup outcomes several areas have to be addressed. These range from addressing early stage financing gap, to providing better playbooks to software product industry startups, to having privileged access to strategic technologies, etc. These are covered in more detail in a later section.

Stage 4: Building Global Ecosystems. e2015-e2019 The speed at which Nokia’s handset business deteriorated has shocked everybody. It went from being a market leader in smartphones to being unviable as a company in less than 20 months. Nowadays, Blackberry is undergoing the same tragic downtown in fortunes. In fact this movie has been played several times before in the hi-tech industry. Back in 2001, Glenayre Technologies, a market leader in the two-way pager business, went from a technology darling to a basket case in under two years. Further back in time, in 1985, the famous Osborne computer had suffered the same fate. Its business collapsed in one year. Why do some good firms collapse so suddenly? Nokia’s CEO Stephen Elop provides the answer in his now infamous 9th Feb 201 memo. He said: “The battle of devices has now become a war of ecosystems, where ecosystems include not

only the hardware and software of the device, but developers, applications, ecommerce,

advertising, search, social applications, location-based services, unified communications

and many other things. Our competitors aren't taking our market share with devices; they

are taking our market share with an entire ecosystem. This means we're going to have to

decide how we either build, catalyse or join an ecosystem.”

In many cases, the very success of a product firm results in a competitive response where the battle of products becomes the war of ecosystems. If a firm has not planned for this new kind of competition, it quickly loses its market position and fades away. We expect that there will be about five software products companies with a billion dollar market cap (e.g. InMobi, Zoho, QuickHeal, Pubmatic) in the coming years. Of these, at least one of them will have to engage in this war of ecosystems in the coming years. We know that losing this ecosystem war has delirious consequences. In contrast, winning the war of ecosystems has big benefits. By turning a product franchise into a developer ecosystem, a company becomes less vulnerable and has better financials. There are other benefits as well. Microsoft claims an employment of 15m in its ecosystem30. SAP, Google and OpenSource ecosystems also report similar benefits. There are significant challenges in creating developer ecosystems. These relate to three areas. First, there are no clear guidelines for performing correct and insightful modeling of developer ecosystems. Second, conducting an ongoing health analysis of an ecosystem is still a daunting data-mining task: what are the indicators to look at? How can data be found on the revenues of our partners? How many new developers join the ecosystem every year? And how much do these really contribute? Third, relates to the issue of Governance. This addresses the issue of how to govern developer ecosystems to gain measurable success in terms of staying power, profit, usage and participation. India has not yet built a software ecosystem though one local ecosystem building project is underway. UIDAI is trying to build a developer ecosystem around its offerings. This is a good for India to strengthen its ecosystem building muscles. In time, we are confident that at least one Indian software product industry firm will be successful in building an ecosystem around its products. Only when this happens, will it signify that the “next Google” or the “next Microsoft” has been born from India. Getting to this stage is something that (even) the Israeli hi-tech industry has not been able to do. What is working in India’s favor is the presence of a big domestic market in India.

Stage 5: Outward Investment. e2019 onwards. This stage is characterized by outward investments to deal with transformative technologies and strengthening of the moat around the India software product industry ecosystems. It is only at this stage that a truly sustainable India software product industry would be created.

30http://www.informationweek.com/microsoft-says-its-software-ecosystem-em/202404791

V.3. Appendix. Principles for interventions in software product industry A set of principles guides our specific interventions in the software product industry. These principles are non-protectionist and avoid infant industry protection. We are not recommending plan-oriented economy type interventions as they wouldn’t work in this fast paced industry. We refute the traditional approach that involves identification of a R&D trend, setting goals, providing grants to private sector for R&D and reviewing achievements. We do not believe in this approach and have seen this fail numerous times, most recently, in US, Malaysia and Japan. We also do not expect the Government to guide the market towards planned structural change. Instead of favoring an “optimal” degree of openness and “optimal” degree of outside competition, we subscribe to “maximum” openness and “perfect” competition. There are 8 key principles behind our interventions are: 1. Our belief is that the primary focus of policy should be to provide social, legal

and economic infrastructure so that private enterprise can flourish. 2. We believe that software product start-up communities are networks —

glorious in all their messiness and chaos. Yet they aren't simply organic phenomena. They need careful nurturing and support.

3. We believe that market interventions should be simple, transparent and subject to rules rather than official discretion.

4. We believe that Government should not create a software ecosystem for a specific product. It should restrict its role to being a market maker or to making public platforms (e.g. UID, GST) that have open access.

5. We believe that co-evolution of institutions will be critical to success given the path dependent nature of software product industry evolution. This co-evolution of institution can only be achieved within the framework of public-private governance of these institutions.

6. We believe that urgency is important. There are favorable international market conditions right now and quick action on policy and institution front can recreate the East Asian miracle for India in software products.

7. We believe that greater degree of cluster integration of the Indian software product industry with Silicon Valley and Israel startup clusters is desirable.

8. We believe that we should not pick technology winners. Not withstanding any specific mention of technologies, if a better technology emerges thats better in total cost, time, ease of use or effeciency for similar purpose; it should be treated on par and may supersede the preferences mentioned in the policy.