naptha cracking

TRANSCRIPT

NAPHTHA CRACKINGCHANDRASEKAR

No. 2

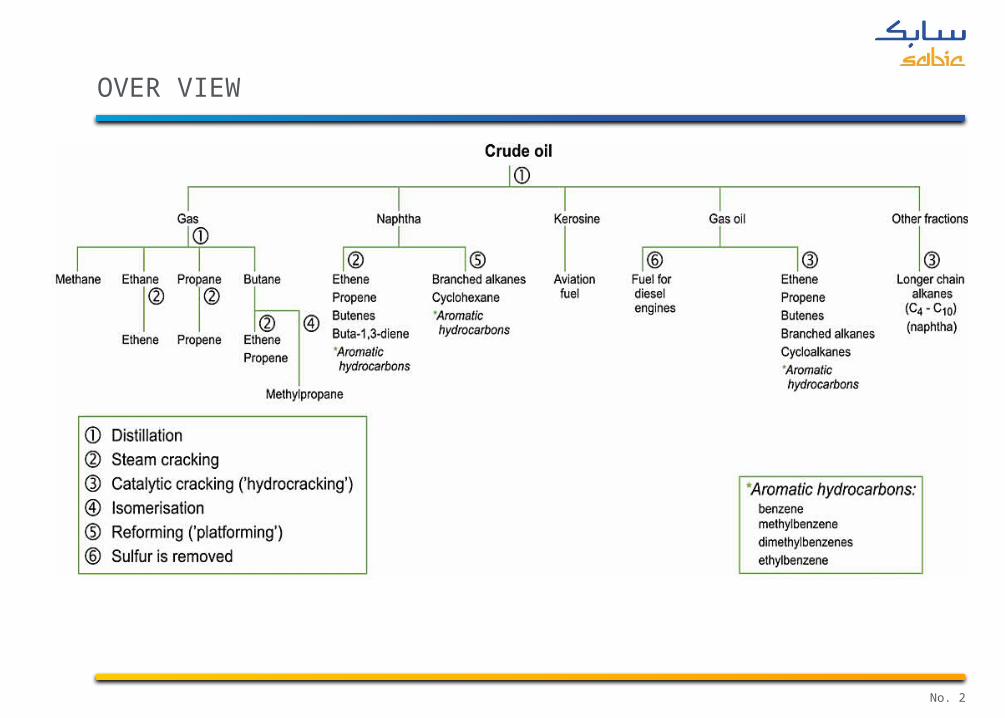

OVER VIEW

No. 3

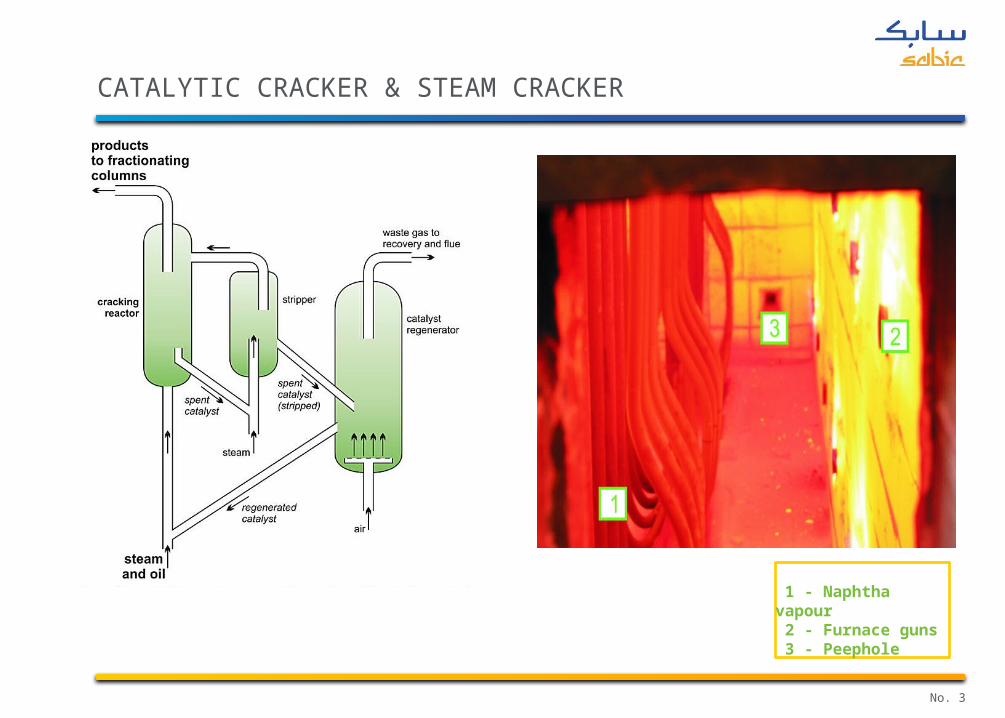

CATALYTIC CRACKER & STEAM CRACKER

1 - Naphtha vapour 2 - Furnace guns 3 - Peephole

No. 4

NAPHTHA CRACKER - SABIC EUROPE

1 - Debutaniser

2 - Depropaniser

3 - Deethaniser

4 - Demethaniser

5 - C3 splitter

6 - C2 splitter

SABIC Europe

No. 5

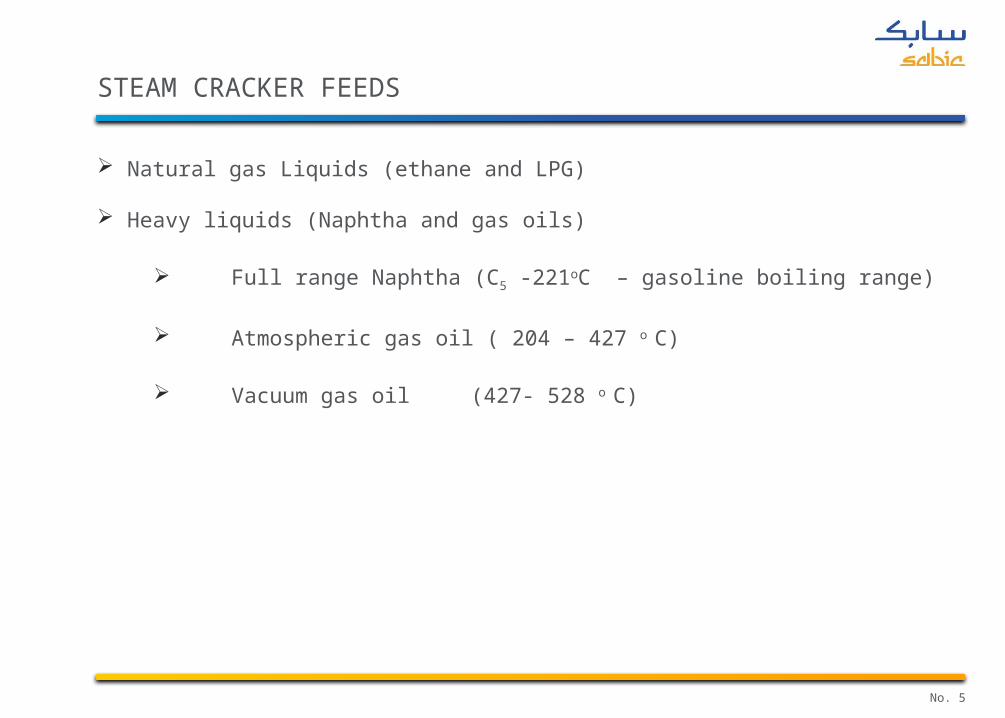

STEAM CRACKER FEEDS

Natural gas Liquids (ethane and LPG)

Heavy liquids (Naphtha and gas oils)

Full range Naphtha (C5 -221oC – gasoline boiling range)

Atmospheric gas oil ( 204 – 427 o C)

Vacuum gas oil (427- 528 o C)

No. 6

STEAM CRACKING LICENSORS

ABB Lummus Global

Kellogg Brown & Root ( exclusive for ExxonMobil for ethylene production)

Linde AG

Stone & Webster (S&W)

Technip- Coflexip

No. 7

ON-PURPOSE TECHNOLOGIES - PROPYLENE & BUTADIENE

New feed stock sources are emerging

Shale gas developments in North America. (NGLs have displaced naphtha at many steam crackers)

China has the largest shale gas reserves in the world, with 36.1 trillion cubic meters compared to

reserves of 24.4 trillion cubic meters in the U.S

3 to 5 mmtpa of new steam cracking capacity will actually come online in North America by 2020.

Iraq has set an oil production target of 13 million barrels per day by 2017.

Middle east companies adapted the shortage of natural gas.

Global propylene shortage will be 3 mmtpa by 2015 and 14 mmtpa by 2025.

Butadiene shortage could reach ~ 10 % of demand by 2015, and 25 % of demand by 2025.

©2012 Booz & Company Inc.

No. 8

CURRENT ON-PURPOSE TECHNOLOGIES FOR PROPYLENE

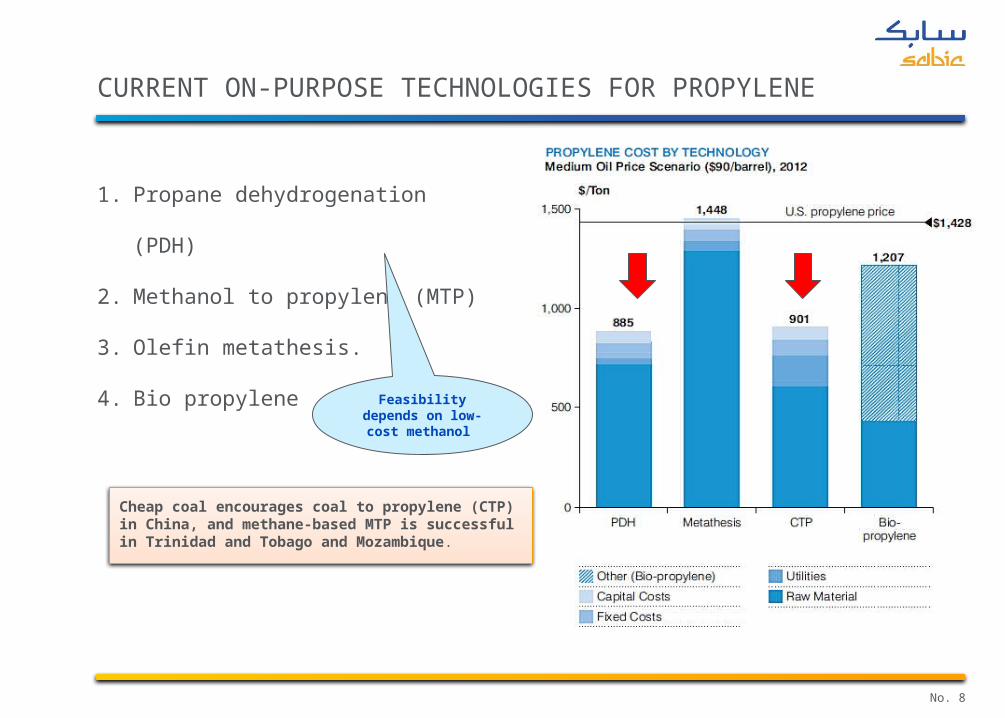

1. Propane dehydrogenation (PDH)

2. Methanol to propylene (MTP)

3. Olefin metathesis.

4. Bio propylene

Feasibility depends on low-cost methanol

Cheap coal encourages coal to propylene (CTP) in China, and methane-based MTP is successful in Trinidad and Tobago and Mozambique.

No. 9

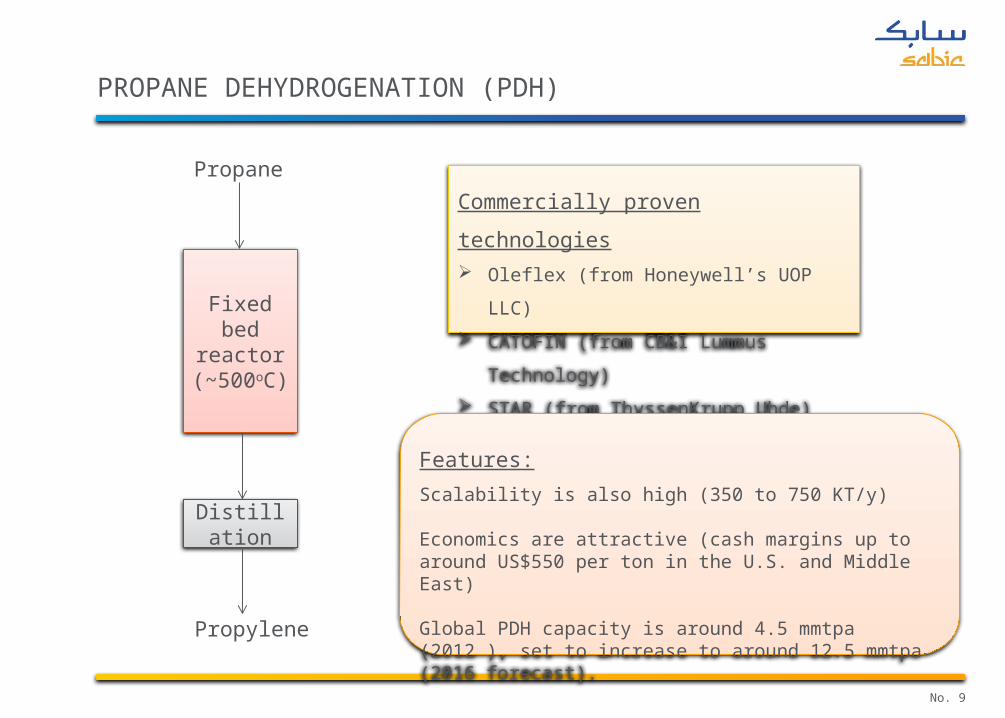

PROPANE DEHYDROGENATION (PDH)

Distillation

Fixed bed reactor

(~500oC)

Propane

Propylene

Commercially proven technologies

Oleflex (from Honeywell’s UOP LLC)

CATOFIN (from CB&I Lummus Technology)

STAR (from ThyssenKrupp Uhde)

Features:

Scalability is also high (350 to 750 KT/y)

Economics are attractive (cash margins up to around US$550 per ton in the U.S. and Middle East)

Global PDH capacity is around 4.5 mmtpa (2012 ), set to increase to around 12.5 mmtpa (2016 forecast).

No. 10

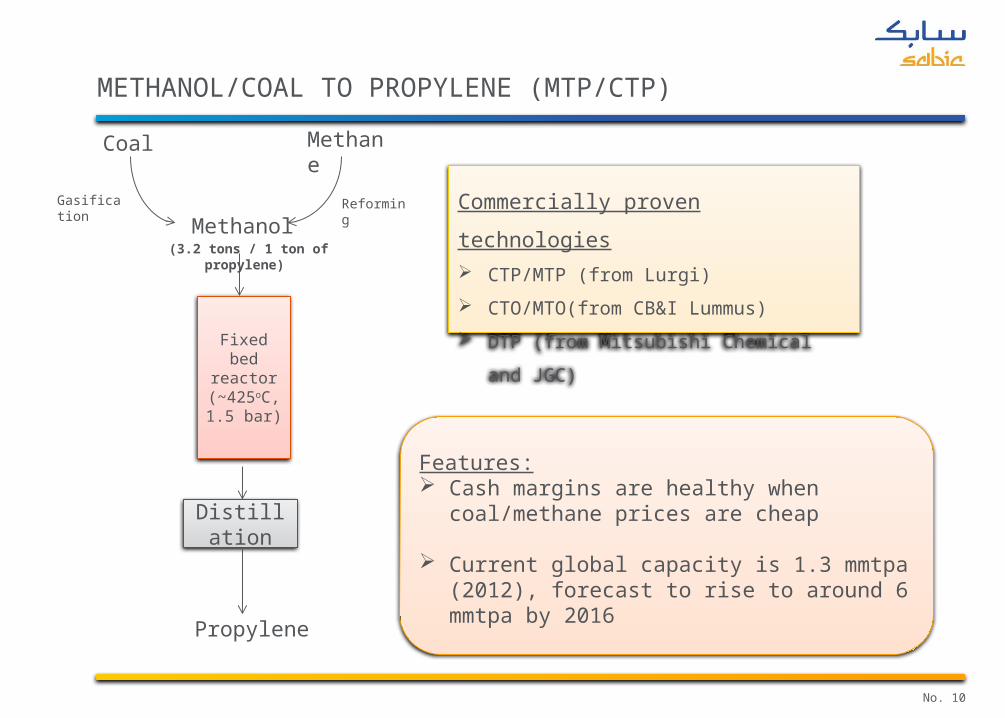

METHANOL/COAL TO PROPYLENE (MTP/CTP)

Distillation

Fixed bed reactor

(~425oC, 1.5 bar)

Methanol

Propylene

Commercially proven technologies

CTP/MTP (from Lurgi)

CTO/MTO(from CB&I Lummus)

DTP (from Mitsubishi Chemical and JGC)

Features: Cash margins are healthy when coal/methane

prices are cheap

Current global capacity is 1.3 mmtpa (2012), forecast to rise to around 6 mmtpa by 2016

Coal

Gasification

Methane

Reforming

(3.2 tons / 1 ton of propylene)

No. 11

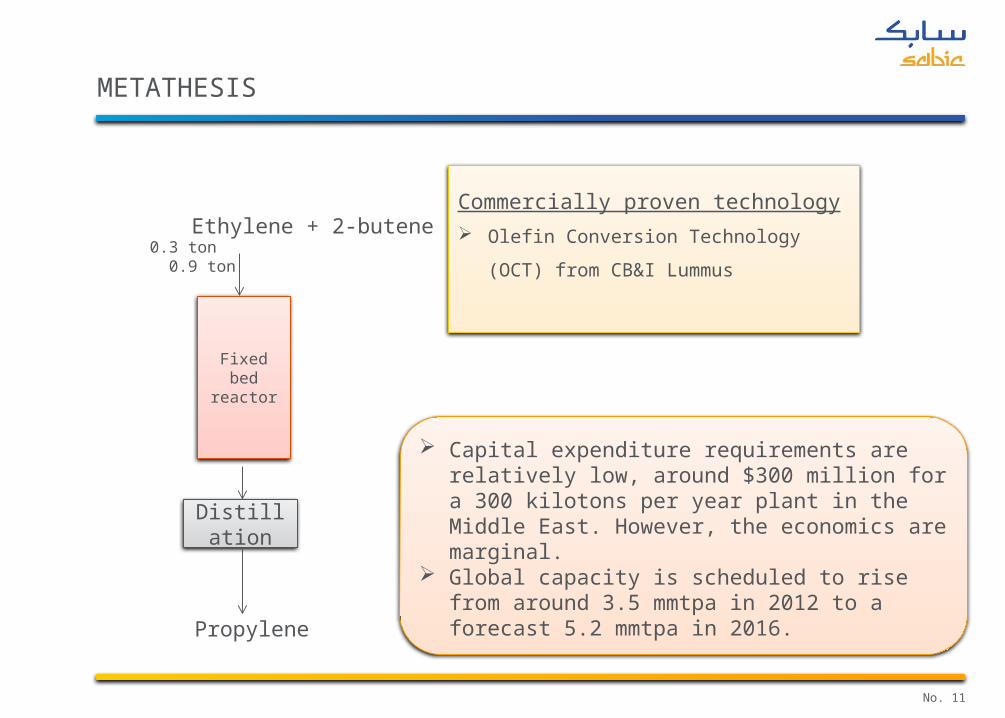

METATHESIS

Distillation

Fixed bed reactor

Ethylene + 2-butene

Propylene

Commercially proven technology

Olefin Conversion Technology (OCT) from

CB&I Lummus

Capital expenditure requirements are relatively low, around $300 million for a 300 kilotons per year plant in the Middle East. However, the economics are marginal.

Global capacity is scheduled to rise from around 3.5 mmtpa in 2012 to a forecast 5.2 mmtpa in 2016.

0.3 ton 0.9 ton

No. 12

BIOMASS TO PROPYLENE

Biochemical:

Fermentation of sugarcane/corn to ethanol followed by dehydration to ethylene, followed by dimerization (to produce 2-butene) and subsequent metathesis. Thermochemical:

Gasification of biomass to methanol followed by MTP.

Process maturity of both routes is quite low with no commercial scale plants.

Economics can be attractive with cash margins of around $100 to $150 per ton if ethanol is available at cost. This, however, requires backward integration into fermentation plants.