namib i a u n ivers i tvexampapers.nust.na/greenstone3/sites/localsite/collect/exampape... ·...

TRANSCRIPT

nAmIB I A U n IVERS I TV OF SCIEnCE AnD TECHnOLOGY

FACULTY OF MANAGEMENT SCIENCES

DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE

QUALIFICATION: VARIOUS PROGRAMMES

QUALIFICATION CODE: VARIOUS LEVEL: 7

COURSE CODE: BAC1100 COURSE NAME: BUSINESS ACCOUNTING 1A

SESSION: JUNE 2016 PAPER: THEORY AND PRACTICAL

DURATION: 2 HOURS MARKS: 100

EXAMINER(S)

MODERATOR:

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

A. Ketjinganda, Wynand Dreyer, Alfred Makosa, Felix Mashoko, Helmut Namwandi, Andrew Simasiku, Dennis Fredericks, Salmi Kasita, Albertine Ngaruka, Benjamin Hendrickse, Tangeni Muleka and Gerhard Sheehama

Evans Mushonga

INSTRUCTIONS

1. This exam paper is made up of four (4) questions 2. Answer ALL the questions and in blue or black ink 3. Start each question on a new page in your answer booklet & show all

your workings 4. Questions relating to this test may be raised in the initial 30 minutes after

the start of the paper. Thereafter, candidates must use their initiative to deal with any perceived error or ambiguities & any assumption made by the candidate should be clearly stated.

PERMISSIBLE MATERIALS 1. Examination paper. 2. Examination script.

THIS QUESTION PAPER CONSISTS OF 6 PAGES (Excluding this front page)

Question 1 20 Marks

Part A (10 Marks)

In each of the following five (5) statements, you are required to indicate if the statements are True or False. If the statement is False, reasons for your answer must be provided.

1. Owners' equity is derived as the difference between money invested into the business by the owner less liabilities of the business. (2)

2. In terms of the financial conceptual framework transactions should be recorded on cash basis, thus when cash or cash equivalent are received or paid. (2)

3. From sales journal, transactions are then posted to creditors' ledger. (1)

4. The accounting principle that requires that information should be presented without bias in the selection and presentation of financial information is called neutrality. (1)

5. Pedex bought purchases amounting to N$91 200 inclusive of VAT. Assuming a VAT rate of 14%, thus VAT portion thus equals to N$12300? (2)

Part B (10 Marks)

1. Financial statements are prepared on the input of source documents of various transactions which are initially recorded in prime books and subsequently posted to ledgers, resulting in a trial balance. State the four components/types of reports contained in the financial statements. (4)

2. List any two examples of VAT zero rated items. (2)

3. The Cash book and bank statement often need to be reconciled. What is the purpose of the bank reconciliation statement? (2)

4. State any two enhancing qualitative characteristics of the financial statements. (2)

2

Question 2 25 Marks

On 1 January 2016, PreStar Entity commenced with activities and incurred the following transactions during January 2016:

1 On 2 January 2016, the owner provided the property to Prestar Entity for the exclusive use of the entity. The property was registered in the owner's name a few days before 2 January 2016. It was transferred into company's name on 3rd January 2016. The cost of the property was N$1 300 000 (N$300 000 for the land and N$1000 000 for the buildings).

2 On 3 January 2016, the owner opened a cheque account for the entity and deposited N$1 800 000 into the account.

3 On 5 January 2016, a delivery vehicle to the amount of N$225 000 was ordered. The supplier, Techxi, delivered the delivery vehicle to Prestar Entity's premises on 10 January 2016. On the same day, the local authority registered the vehicle in Prestar Entity's name. The invoice price is N$225 000 and it was agreed with the supplier, Techxi, to pay the outstanding amount on 30 January 2016.

4 Trade inventories to the amount of N$20 000 was ordered on 7 January 2016 from Pablo industries Ltd. On 25 January 2016, the supplier delivered the trade inventories to Prestar Entity's premises. The invoice price is N$20,000 and it was agreed with Pablo industries Ltd that the outstanding amount will be paid on 27 February 2016. (Prestar Entity uses the perpetual inventory system to account for trade inventories).

5 On 30 January 2016, the amount due to Techxi was paid.

Required:

a) For each transaction you are required to identify the source document, the book of original/prime entry and which account to be Debited and Credited.

NB: Provide the following format table in your answer book:

Source Book of prime Account to be Dr & Account to be Cr Date document entry N$ & N$

1.

3

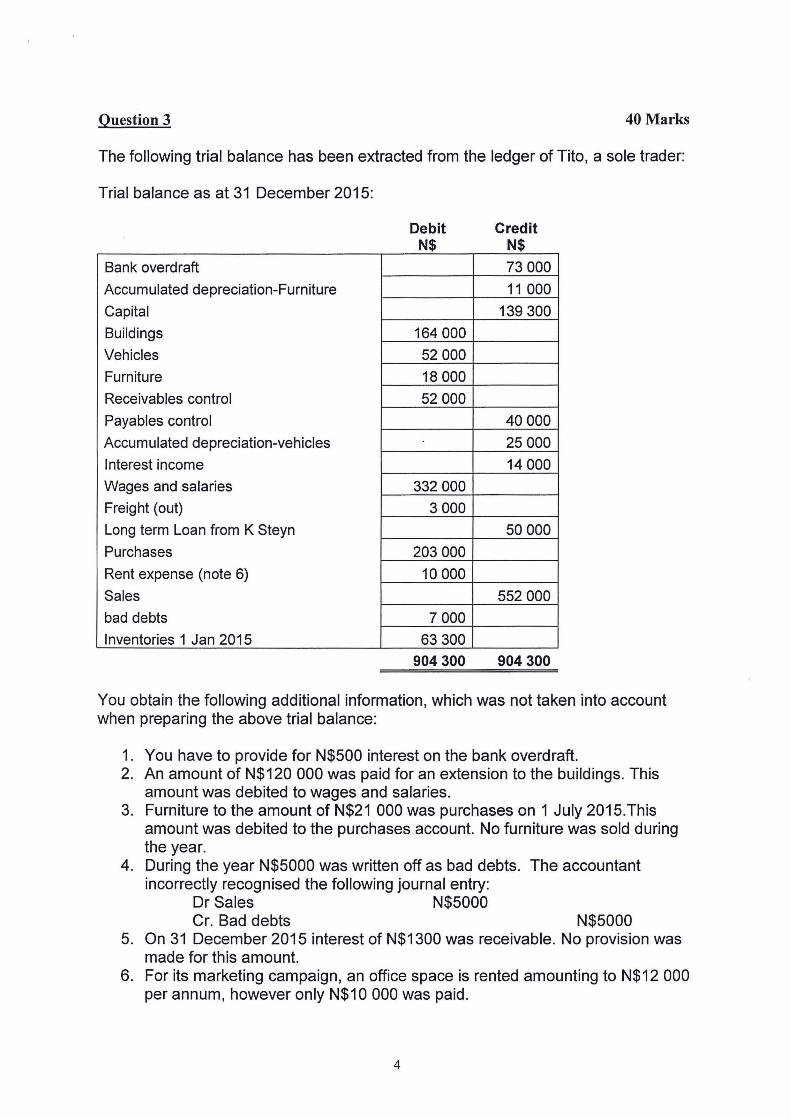

Question 3 40 Marks

The following trial balance has been extracted from the ledger of Tito, a sole trader:

Trial balance as at 31 December 2015:

Bank overdraft

Accumulated depreciation-Furniture

Capital

Buildings

Vehicles

Furniture

Receivables control

Payables control

Accumulated depreciation-vehicles

Interest income

Wages and salaries

Freight (out)

Long term Loan from K Steyn

Purchases

Rent expense (note 6)

Sales

bad debts

Inventories 1 Jan 2015

Debit N$

164 000

52 000

18 000

52 000

332 000

3 000

203 000

10 000

7 000

63 300

904 300

Credit N$

73 000

11 000

139 300

40 000

25 000

14 000

50 000

552 000

904 300

You obtain the following additional information, which was not taken into account when preparing the above trial balance:

1. You have to provide for N$500 interest on the bank overdraft. 2. An amount of N$120 000 was paid for an extension to the buildings. This

amount was debited to wages and salaries. 3. Furniture to the amount of N$21 000 was purchases on 1 July 2015.This

amount was debited to the purchases account. No furniture was sold during the year.

4. During the year N$5000 was written off as bad debts. The accountant incorrectly recognised the following journal entry:

Dr Sales N$5000 Cr. Bad debts N$5000

5. On 31 December 2015 interest of N$1300 was receivable. No provision was made for this amount.

6. For its marketing campaign, an office space is rented amounting to N$12 000 per annum, however only N$1 0 000 was paid.

4

Question 3 (continued)

7. Depreciation must be provided for 2015 as follows:

Required:

Furniture: 10% per annum on the straight line method Vehicles: 20% per annum on the diminishing balance

i) Prepare a statement of profit or loss of Apollus for the year ending 31 December 2015. (20 marks)

ii) Prepare the statement of financial position of Apollus as at 31 December 2015. (20 marks)

5

Question 4 15 Marks

The following information has been extracted from Mukela Supermarket, a company that specialises in Fast Moving Consumer Goods (FMCG).

Mukela Supermarket Statement of profit or loss for the year ending 31 December 2015

N$000 N$000 Revenue 1 845 Cost of sales (758) Gross profit 1 087 Distribution costs (136) Administrative costs ___(§j}

(197) Profit from operations 890 Finance cost (104)

786 Income tax expense (69) Profit for the period 717

Mukela Supermarket Statement of financial position as at 31 December 2015

Assets Noncurrent assets

Property, plant and equipment

Current assets Inventories Trade receivables Cash and cash equivalents Total assets

Equity and Liabilities Equity Issued share capital (N$ 1 shares) Retained earnings

Liabilities Noncurrent liabilities Interest bearing borrowings Deferred tax

Current liabilities Total Equity and Liabilities

N$000 N$000

42 180 113

600 1 132

2 022 __.ffli

6

4 002

335

4...3..31

1 732

2 313

Question 4 (continued)

The following information is also available:

1. All sales are made on credit. 2. Purchases made on credit during the year were N$527 000 and trade payables at 31 December

2015 were N$ 61 000.

Required:

From the information above, calculate: a) The gross profit margin b) Net profit margin c) Asset turnover d) Quick ratio e) Trade payables days

END OF EXAMINATION PAPER

7

(3 marks) (3 marks) (3 marks) (3 marks) (3 marks)