nagarjuna agrichem ltd detail reportbreport.myiris.com/firstcall/nagagric_20100714.pdf · the asset...

TRANSCRIPT

1

Stock Data

Sector Agrochemicals

Face Value(Rs) 10.00

52 wk. High/Low (Rs.) 385.90/113.70

Volume (2 wk. Avg.) 23000

BSE Code 524709

Market Cap(Rs in Mn) 5036.9

Financials (Rs in Mn) FY10A FY11E FY12E

Net Sales 6503 6828 7511

EBIDTA 1288 1391 1530

PAT 597 646 714

EPS 40.1 43.4 47.9

P/E 8.43 7.79 7.05

NAGARJUNA AGRICHEM LTD BUY F

I

R

S

T

C

A

L

L

R

E

S

E

A

R

C

H

SYNOPSIS

• NACL was established in 1994 for producing Monocrotophos Technical. NACL has since grown substantially and now manufactures a comprehensive range of pesticide technicals, formulations and custom manufactured fine chemicals.

• NACL has one of the largest Dealer Network spread across India, with marketing and sales offices in addition to an extensive Warehousing & Logistics Infrastructure to handle operations in 20 Indian States.

• The company operates at one of the most modern and comprehensive Technical Agrochemical manufacturing plants, situated in Srikakulam district of Andhra Pradesh, India.

• The revenue of the company for the year ended on March 31st increased 7.43% YoY while Profit increased 21.3% YoY.

• The topline & bottomline of the company are expected to grow at a CAGR of 7% & 13% over 2009A to 2012E respectively.

1 Year Comparative Graph

NAGARJUNA AGRICHE BSE SENSEX

V.S.R. Sastry

Equity Research Desk

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

C.M.P: Target Price: Rs.338.05 Rs.390.00

Share Holding Pattern

Date: 14 July 2010

2

Peer Group Comparison

Name of the company CMP(Rs.)

Market Cap.(Rs.Mn.) EPS(Rs.) P/E(x) P/Bv(x) Dividend (%)

Nagarjuna Agrichem

Ltd 338.05 5036.9 40.11 8.43 2.29 30

United Phosphorous 177.00 77802.8 4.12 42.9 3.89 75

Excel Crop Care 238.40 2623.7 34.01 7.01 1.55 125

Insecticides India 227.00 2879.0 22.25 10.20 2.23 20

Investment Highlights

FY10 Performance

Net profit of the company has increased at 21.3% yoy Rs.597.60mn from

Rs.492.60mn of same period of last year. Total revenue for the year stood at

Rs.6503.10 mn from Rs.6053.60 which is 7.43% increased than that of a year

ago. EPS for the year stood at Rs.40.11 per equity share of Rs.10.00 each.

Operating profit of the company stood at Rs.1288.60mn. OPM for the year stood at

20%. Expenditure of the company increased 8.3% YoY to Rs.5301.20 mn. Interest

expenses for the year stood at Rs.170.9mn.

3

Results Updates (Q4 FY10)

The bottomline of the company for the quarter increased at 16% yoy Rs.128.60mn

from Rs.110.90mn of same period of last year. Total revenue for the fourth quarter

stood at Rs.1400.20 mn from Rs.1436.80 which is 3% decreased than that of a

year ago.EPS for the quarter stood at Rs.8.63 per equity share of Rs.10.00 each.

Expenditure of the company decreased 4.4% YoY to Rs.1123.60mn from

Rs.1175.00mn of same period of last year. Interest expenses for the quarter stood

at Rs.50.1mn. OPM & NPM for the quarter stood at 21% and 9% respectively.

Quarterly Results - Standalone (Rs in mn)

As At Mar-10 Mar-09 %Change

Net sales 1400.20 1436.80 (3)

PAT 128.60 110.90 16

Basic EPS 8.63 7.44 16

Equity Capital 149.00 149.00

4

5

Board recommends Final Dividend

The Board of Directors of the Company have recommended a Final Dividend of

30% for the Financial Year 2009-10.

The Board of Directors has also decided to raise further equity by way of QIP /

Public Issue / Rights Issue / Private Placement or any contribution thereof or

conversion of debt into equity not exceeding of Rs. 100 Crores by way of

conducting Postal Ballot pursuant to Sec. 192 A(2) of the Companies Act, 1956.

Company Profile

Nagarjuna Group is truly an enterprise on the move. The foundation of the Group was

laid over two decades ago by technocrat entrepreneur Shri. KVK Raju. He started with

an initial investment of US $ 1.2 million and sowed the seeds of what is now one of the

fastest growing industrial houses in India.

6

In addition to a growing presence in Agribusiness, the Group has made significant

investments in core sectors like Refining, Power generation and Life Sciences. Today,

the asset base of Nagarjuna Group is over US $ 2.5 billion.

The Agribusiness Division of Nagarjuna is committed to enhancing the availability of

quality food supply for the future by developing products and services that contribute

to increasing farm productivity.

The Agribusiness Division of the Nagarjuna Group consists of the following business

units:-

• Plant Nutrition

• Crop Protection

NACL was established in 1994 for producing Monocrotophos Technical. NACL has

since grown substantially and now manufactures a comprehensive range of pesticide

technical's, formulations and custom manufactured fine chemicals. All the

manufactured products conform to international quality standards and specifications.

The company have adequate capacities, state-of-the-art infrastructure, skilled

experienced manpower and technical absorption capabilities. In fact, Custom

Synthesis and manufacturing are one of NACL's inherent capabilities. The production

lines are designed for a quick change over. The company also have a Custom

Synthesis and Toll Manufacturing Division, which caters to the requirements of

reputed overseas customers.

NACL has one of the largest Dealer Network spread across India, with marketing and

sales offices in addition to an extensive Warehousing & Logistics Infrastructure to

handle operations in 20 Indian States. NACL has tie-ups with large Indian

Agrochemical Majors and MNC’s for the domestic and export markets. The Current

Gross Annual Sales of the Organization is apprx. US $ 145 million.

The company operate one of the most modern and comprehensive Technical

7

Agrochemical manufacturing plants, situated in Srikakulam district of Andhra

Pradesh, India.

NACL formulates its formulations in a modern Formulation Plant situated in the East

Godavari District of Andhra Pradesh. This location is situated in the scenic rice

growing area on India's East Coast. This Unit is one of the few to have in a single

location, integrated multi-line facilities capable of producing a variety of pesticide

formulations such as liquids, wettable powders and granules simultaneously. This

unit has the formulation technology to produce dry flowables and water based

emulsions.

The category wise annual capacities are:

• Liquid : 25,000 KL

• Granules : 15,000 MT

• Wettable Powder : 3,000 MT

NACL is setting up a New Green Field Project for Manufacturing Technical with an

initial investment of 30 Million US Dollars. The Project will be on stream by 2010.

NACL is also setting up a New Corporate R&D Centre in Hyderabad. In this Corporate

R&D Centre, in addition to in-house R&D projects, Contract Research will also be

undertaken.

NACL has an impressive range of branded formulations in the categories of

Insecticides, Fungicides and Herbicides. In addition to catering to the entire Indian

subcontinent, the company export both Technicals and Formulation grade pesticides

to some countries in Europe, Asia including the Middle East, Japan, USA, Australia

and Africa.

Products

8

List of Technicals

TECHNICALS

Insecticides: . Purity

PROFENOFOS 91% / 95%

ACEPHATE 98%

DICHLOROVOS 98%

MONOCROTOPHOS 74%

TECHNICALS

Fungicides: Purity

PROPICONAZOLE 92%

MYCLOBUTANIL 97%

Herbicides: Purity

PRETILACHLOR 96%

List of Formulation Products

FORMULATIONS

FUNGICIDE . TRADE NAME Carbendazim 5% WP ZEN

Carbendazim 12% + Mancozeb 63% WP

NAGARJUNA COMBIPLUS

Cymoxanil 8% + Mancozeb 64% WP

FONT

Hexaconazole 5% EC NAGARJUNA MASS

Hexaconazole 5% SC NAGARJUNA MASS PLUS

Mancozeb 75% WP ZEB

Myclobutanil 10 % WP INDEX

Propiconazole 25 % EC RESULT

Tricyclazole 75% WP SIVIC

Thifluzamide 24% SC VISTA

Validamycin 3 % L RHIZOCIN

HERBICIDE . TRADE NAME

Atrazine 50% WP SURYA

Ammonium Salt of Glyphosate 71% SG

GLOBUS SG

Bensulfuron methyl 0.6% +Pretilachlor 6%

ERAZE STRONG

Clodinafop Propargyl 15 % WP

POINT

Glyphosate 41% SL GLOBUS SL

Metsulfuron Methyl 20% WP

DOT

Pretilachlor 50% EC ERAZE

Pretilachlor 30.7% w/w or 30% w/v

ERAZE-N

9

Paraquat Dichloride 24% SL

RHINO

INSECTICIDE . TRADE NAME

Acephate 75% SP PACE

Acetamiprid 20% SP NAGARJUNA ENNOVA

Buprofezin 25% SC BENJ

Carbofuran 3% CG FURY

Cartap Hydrochloride 4% G

SANVEX-4G

Cartap Hydro Chloride 50% SP

SANVEX SP

Chlorpyrifos 20% EC FORCE

Clothianidin 50 % WDG DANTOP

Chlorpyrifos 50% EC+ Cypermethrin 5% EC

CANON

Dichlorvos 76% EC DASH

Endosulfan 35% EC SPEED

Emamectin Benzoate 5% SG

NAGARJUNA TRUST

(BPMC) Fenobucarb 50% EC

MERLIN

Fipronil 0.3% GR TASK-GR

Fipronil 5% SC TASK

Imidacloprid 17.8% SL NAGARJUNA MIDA

Lambda Cyhalothrin 2.5% EC

WARRIOR

Lambda Cyhalothrin 5% EC

WARRIOR PLUS

Milbemectin 1 % EC MILBEKNOCK

Monocrotophos 36% SL MONOCROWN

Phorate 10%CG NAGARJUNA PHORATE

Profenofos 50% EC PROFEX

Profenofos 40% + Cypermethrin 4% EC

PROFEX SUPER

Spinosad 45% SC CONSERVE

Exports

Nagarjuna's growing global presence is reflected in its exports. Today Nagarjuna is

among the few companies in India exporting pesticide technicals and formulations to

as many as 24 countries including Australia, Bangladesh, Belgium, Brazil, Colombia,

Egypt, France, Germany, Indonesia, Italy, Ivorycoast, Japan, Malaysia, Netherlands,

10

Nigeria, Saudi Arabia, Singapore, Sri Lanka, Switzerland, Taiwan, Tanzania, Thailand,

USA and Yemen.

To meet the growing demand in the international markets and improve its export

business, the Group is constantly introducing new generics and formulations. To

strengthen this process, Nagarjuna has generated complete packages of Chemistry,

Toxicology, Residues and Bioefficacy data for all its manufactured techincals.

Manufacturing and R & D

NACL has adequate capacities, state-of-the-art infrastructure, skilled experienced

manpower and technology absorption capabilities. The production lines are designed

for quick change over to also undertake Toll manufacturing adhering to the highest

international standards and specifications.

The Technical Grade Pesticides manufactured are:

Insecticides Herbicides Fungicides

Profenophos Pretilachlor Propiconazole

Acephate

Tricyclozole

Dichlorovos . Myclobutanil

Research and Development plays a critical role in NACL. The R&D division carries out

work on process development of technical and intermediates, custom synthesis,

process improvement, application research and basic research.

11

Financials Results

12 Months Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) FY09A FY10A FY11E FY12E

Description 12m 12m 12m 12m

Net Sales 6,053.60 6,503.10 6828.26 7511.08

Other Income 16.6 86.7 93.64 103.00

Total Income 6,070.20 6,589.80 6921.89 7614.08

Expenditure -4,892.80 -5,301.20 -5530.89 -6083.98

Operating Profit 1,177.40 1,288.60 1391.00 1530.10

Interest -191.1 -170.9 -179.45 -193.80

Gross profit 986.30 1,117.70 1211.56 1336.30

Depreciation -182.3 -205 -223.45 -245.8

Profit Before Tax 804.00 912.70 988.11 1090.51

Tax -311.4 -315.1 -341.13 -376.2

Net Profit 492.60 597.60 646.98 714.28

Equity capital 149 149 149.00 149.00

Reserves 1,449.60 2,047.20 2,694.18 3,408.46

EPS 33.06 40.11 43.42 47.94

12

Quarterly Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) Sep-09A Dec-09A Mar-10A June-10E

Description 3m 3m 3m 3m

Net sales 2,017.40 1,714.10 1,400.20 1358.19

Other income 19.1 31.5 24.3 25.52

Total Income 2,036.50 1,745.60 1,424.50 1383.71

Expenditure -1,672.50 -1,375.60 -1,123.60 -1093.35

Operating profit 364.00 370.00 300.90 290.36

Interest -40.3 -44 -50.1 -54.11

Gross profit 323.70 326.00 250.80 236.25

Depreciation -50.4 -53 -52.2 -53.24

Profit Before Tax 273.30 273.00 198.60 183.01

Tax -101.4 -89.8 -70 -58.56

Net Profit 171.90 183.20 128.60 124.45

Equity capital 149 149 149 149.00

EPS 11.54 12.30 8.63 8.35

13

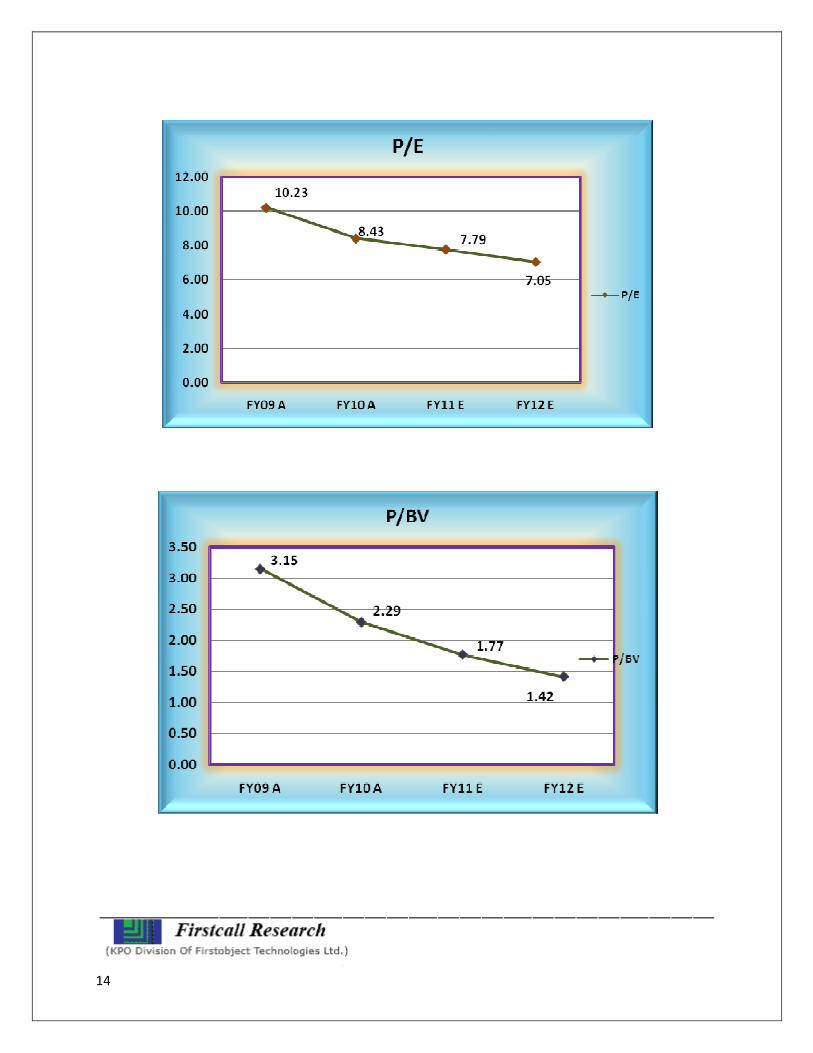

Key Ratio

Particulars FY09 A FY10 A FY11 E FY12 E

EBIDTA % 19% 20% 20% 20%

PAT % 8% 9% 9% 10%

P/E ratio (x) 10.23 8.43 7.79 7.05

ROCE - % 59% 47% 40% 35%

ROE - % 31% 27% 23% 20%

Price/Book Value 3.15 2.29 1.77 1.42

Debt Equity Ratio 0.05 0.04 0.03 0.03

Book Value (Rs.) 107.29 147.40 190.82 238.76

EV/EBIDITA (x) 4.28 3.91 3.98 3.95

Charts:

14

15

16

Outlook and Conclusion

• At the current market price of Rs.338.05. the stock trades at a P/E of 7.79x and

7.05x for FY11E and FY12E respectively. On the basis of EV/EBDITA, the stock

trades at 3.98x and 3.95x for FY11E and FY12E respectively.

• EPS of the company is expected to be at Rs.43.42 and Rs.47.94 for the earnings of

FY11E and FY12E respectively. Price to Book Value of the stock is expected to be

at 1.77 and 1.42 respectively for FY11E and FY12E.

• We recommend ‘BUY’ in this particular scrip with a target price of Rs.390.00 for

Medium to Long Term Gains.

Industry Overview

• Agrochemicals also known as Pesticides are substance or mixture of substances

that are used to avert, destroy or control any kind of pests or unwanted type of

plants or animals that cause harm to crops or hampers the normal growth

process of a crop. As per a Government of India estimate of 2002, value of crop

losses caused due to non-usage of pesticides was around Rs 90,000 crore.

Thereon, assuming losses grew at an average 2%, total losses would have

amounted to Rs 101,355 crore in FY2009, a staggering 2.2% of India's GDP.

• Chemical Industry is one of the oldest industries in India, which contributes

significantly towards industrial and economic growth of the nation. It is highly

science based and provides valuable chemicals for various end products such

as textiles, paper, paints and varnishes, leather etc., which are required in

almost all walks of life. The Indian Chemical Industry forms the backbone of the

industrial and agricultural development of India and provides building blocks

for downstream industries.

17

• The chemical industry currently produces nearly 70,000 commercial products,

ranging from cosmetics and toiletries, to plastics and pesticides. The wide and

diverse spectrum of products can be broken down into a number of categories,

including inorganic and organic (commodity) chemicals, drugs and

pharmaceuticals, plastics and petrochemicals, dyes and pigments, fine and

specialty chemicals, pesticides and agrochemicals, and fertilizers.

• The Indian pesticide industry has advanced significantly in recent years,

producing more than 1,000 tons of pesticides annually. India is the 13th largest

exporter of pesticides and disinfectants in the world, and in terms of volume, is

the 12th largest producer of chemicals. The Indian agrochemical,

petrochemical, and pharmaceutical industries are some of the fastest growing

sectors in the economy. With an estimated worth of $28 billion, it accounts for

12.5 percent of the country's total industrial production and 16.2 percent of the

total exports from the Indian manufacturing sector.

• With a special focus on modernization, the Indian government takes an active

role in promoting and advancing the domestic chemical industry. The

Department of Chemicals and Petrochemicals, which has been part of the

Ministry of Chemicals and Fertilizers since 1991, is responsible for policy,

planning, development, and regulation of the industry. In the private sector,

numerous organizations, including the Indian Chemical Manufacturers

Association, the Chemicals and Petrochemicals Manufacturers Association, and

the Pesticides Manufacturers and Formulators Association of India, all work to

promote the growth of the industry and the export of Indian chemicals. The

Indian Chemical Manufacturers Association, for example, represents a large

number of Indian companies that produce and export a number of chemicals

that have legitimate commercial applications, but also could be used as

precursors and intermediates for chemical weapons production.

� The Indian fertilizer industry has succeeded in meeting almost fully the demand

of all chemical fertilizers except for MOP. The industry had a very humble

18

beginning in 1906, when the first manufacturing unit of Single Super

Phosphate (SSP) was set up in Ranipet near Chennai with an annual capacity of

6000 MT. The Fertilizer & Chemicals Travancore of India Ltd. (FACT) at Cochin

in Kerala and the Fertilizers Corporation of India (FCI) in Sindri in Bihar were

the first large sized -fertilizer plants set up in the forties and fifties with a view

to establish an industrial base to achieve self-sufficiency in food grains.

Subsequently, green revolution in the late sixties gave an impetus to the growth

of fertilizer industry in India. The seventies and eighties then witnessed a

significant addition to the fertilizer production capacity.

� Fertilizer sector is a very crucial for Indian economy because it provides a very

important input to agriculture. The fertilizer industry in India has played a

pivotal role in achieving self – sufficiency in food grains as well as in rapid and

sustained agriculture growth. India is the third largest producer and consumer

of fertilizers in the world after China and the United States. The growth of the

Indian fertilizer industry has been largely determined by the policies pursued by

the government. The government exercised extensive controls on the pricing,

distribution and movement of fertilizers. The industry is capital intensive and

the production process energy intensive with the combined cost of feedstock

and fuel accounting for anywhere between 55 and 80 per cent of cost of

production, depending on the type of fertilizers.

Key opportunities and challenges for industry

• Low penetration of pesticides:

Estimated size of the Indian economy is US $1 trillion of which Agriculture

accounts for 18%. The Agrochemical industry's size is estimated at US$1bn (Rs

5,000 crore) i.e. 0.1% of the country's total GDP and 0.6% of Agriculture GDP.

Meanwhile, the subsidy burden of urea for FY2009 is estimated at US$21.2

billion or 2% of the total GDP and 12% of agriculture GDP. We believe this

19

demonstrate the gross under penetration of agrochemical and the opportunity

that is available to the companies in the Sector.

• Biotech seeds threat to agrochemicals:

Scientific research has come up with seeds that have self-immunity towards

natural adversaries. This can be a potential threat to the business of

agrochemicals. Best example of such an introduction in the Indian market is

"Bt Cotton", which resulted in a decline in the consumption of agrochemicals by

cotton crop. However, off late there have been few reports of Bt Cotton unable to

develop immunity towards new type of pests.

• Patent expiry of molecules:

Agrochemicals are protected by patents to encourage innovation similar to the

Pharmaceutical industry. Going ahead, many molecules are likely to go off

patent throwing the market open for generic players. As per estimates, total

likely available opportunity through patent expiry stands at US

Determinants of Fertilize Demand

• Rainfall and irrigation facilities

• Relative prices of fertilizers

• Cropping pattern

• Government policies

Rising demand for fertilizers

20

� There has been significant growth in the consumption of fertilizers in last three

years due to overall good monsoon. The growth in NPK consumption was 9.50%

in 2004-05, 10.60 % in 2005-06 and 8.40% per cent in 2006-07.Against the

robust growth in consumption, domestic fertilizer production has remained

range – bound in the last decades. The surge in fertilizers demand and stagnant

to modest increase in production has widened the gap between consumption

and production causing larger dependence on imports. Therefore, the rising

demand for fertilizers is providing ample scope for the companies in this sector

to increase their production capacity and volumes thereby, driving the growth

of fertilizer sector.

� The installed capacity as on 30.01.2003 has reached a level of 121.10 lakh MT

of nitrogen (inclusive of an installed capacity of 208.42 lakh MT of urea after

reassessment of capacity) and 53.60 lakh MT of phosphatic nutrient, making

India the 3rd largest fertilizer producer in the world. The rapid build-up of

fertilizer production capacity in the country has been achieved as a result of a

favorable policy environment facilitating large investments in the public, co-

operative and private sectors. Presently, there are 57 large sized fertilizer plants

in the country manufacturing a wide range of nitrogenous, phosphatic and

complex fertilizers. Out of these, 29 unit produce urea, 20 units produce DAP

and complex fertilizers 13 plants manufacture Ammonium Sulphate (AS),

Calcium Ammonium Nitrate (CAN) and other low analysis nitrogenous

fertilizers. Besides, there are about 64 medium and small-scale units in

operation producing SSP

� The Indian fertilizer industry has come a long way since its early days post

independence. India today is one of the largest producer and consumer of

Fertilizers in the world. India’s production in terms of nutrients (N & P) reached

a level of 155 lakh MT in 2005-06 from 0.39 lakh MT in 1951-52. Similarly,

consumption of fertilizers in terms of nutrients (NPK) has also grown from

about 0.66 lakh MT in 1951-52 to nearly 184 lakh MT in 2004-05.

21

� The Indian Fertilizer industry, given its strategic importance in ensuring self–

sufficiency of food grain production in the country, has for decades, been under

Government control. The Government has over the years, provided subsidies/

concessions through the fertilizer companies to farmers and the manufacturers

have been compensated through various schemes. Though the Government

control helped in meeting the objective of ensuring creation of capacities and

ultimately achieving self-sufficiency in food grain production, it did not

encourage improving efficiencies in the sector.

� Burgeoning subsidy bill and the need to focus on fiscal prudence, Government

polices in recent times are aimed at encouraging efficiencies in the sector. Policy

measures like the new pricing scheme have made the operations of less efficient

players unviable. The Government polices today are oriented towards achieving

the stated objective of total deregulation in the sector. However, the uncertainty

over exact policy parameters and absence of a comprehensive long term policy

has not augured well for the industry. The financial year 2006-07 began with

practically no clarity on the policy parameters for both nitrogenous and

phosphatic fertilizers.

� Another important issue confronting the sector is with respect to the feedstock.

Natural gas which is the main feedstock for production of nitrogenous fertilizers

is available in limited quantities and the industry competes with the power

sector for its share. With the Government policy favoring conversion to gas

based units, the demand for gas is only expected to go up in the future, which

may in turn lead to further shortages.

� The Indian fertilizer industry has come a long way since its early days post

independence. India today is one of the largest producer and consumer of

Fertilisers in the world. India’s production in terms of nutrients (N & P) reached

a level of 155 lakh MT in 2005-06 from 0.39 lakh MT in 1951-52. Similarly,

consumption of fertilizers in terms of nutrients (NPK) has also grown from

about 0.66 lakh MT in 1951-52 to nearly 184 lakh MT in 2004-05. The Indian

22

Fertilizer industry, given its strategic importance in ensuring self– sufficiency of

food grain production in the country, has for decades, been under Government

control.

� The Government has over the years, provided subsidies/concessions through

the fertilizer companies to farmers and the manufacturers have been

compensated through various schemes. Though the Government control helped

in meeting the objective of ensuring creation of capacities and ultimately

achieving self-sufficiency in food grain production, it did not encourage

improving efficiencies in the sector. With the burgeoning subsidy bill and the

need to focus on fiscal prudence, Government polices in recent times are aimed

at encouraging efficiencies in the sector. Policy measures like the new pricing

scheme have made the operations of less efficient players unviable. The

Government polices today are oriented towards achieving the stated objective of

total deregulation in the sector. However, the uncertainty over exact policy

parameters and absence of a comprehensive long term policy has not augured

well for the industry. For instance, the financial year 2006-07 began with

practically no clarity on the policy parameters for both nitrogenous and

phosphatic fertilizers.

� Another important issue confronting the sector is with respect to the feedstock.

Natural gas which is the main feedstock for production of nitrogenous fertilizers

is available in limited quantities and the industry competes with the power

sector for its share. With the Government policy favouring conversion to gas

based units, the demand for gas is only expected to go up in the future, which

may in turn lead to further shortages. Similarly, in the case of phosphates, on

account of the limited availability of phosphoric acid and rock phosphate in the

country, domestic units are dependent to a large extent on imports. In view of

the limited availability of the main feedstock within the country, fertiliser

companies today are exploring the possibility of setting up joint ventures

abroad to tie up their feedstock requirements. Though a few joint venture

agreements have been signed with respect to supply of phosphoric acid, only a

23

couple of joint ventures have been established with respect to urea. Domestic

players have also not been able to enter into long term gas supply agreements

primarily due to differences over pricing.

24

_____________ ____ _________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

25

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Auto

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com