na sales & production - s3.amazonaws.coms3.amazonaws.com/zanran_storage/ filena sales &...

TRANSCRIPT

NA SALES & PRODUCTION Taking Our Lumps Though Better For It

FACS Automotive ConferenceNAIASJanuary 12, 2008

Michael RobinetVice President, Global Vehicle Forecasts

2007 © CSM Worldwide

PRESENTATION OUTLINE

• United States Sales Outlook

• NA Production

• Fitting Into A Global Equation

• Summary

2007 © CSM Worldwide

Hmm ….. Never A Dull Moment

2007 © CSM Worldwide2007 © CSM Worldwide

$10

$20

$30

$40

$50

$60

$70

$80

$9019

93

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

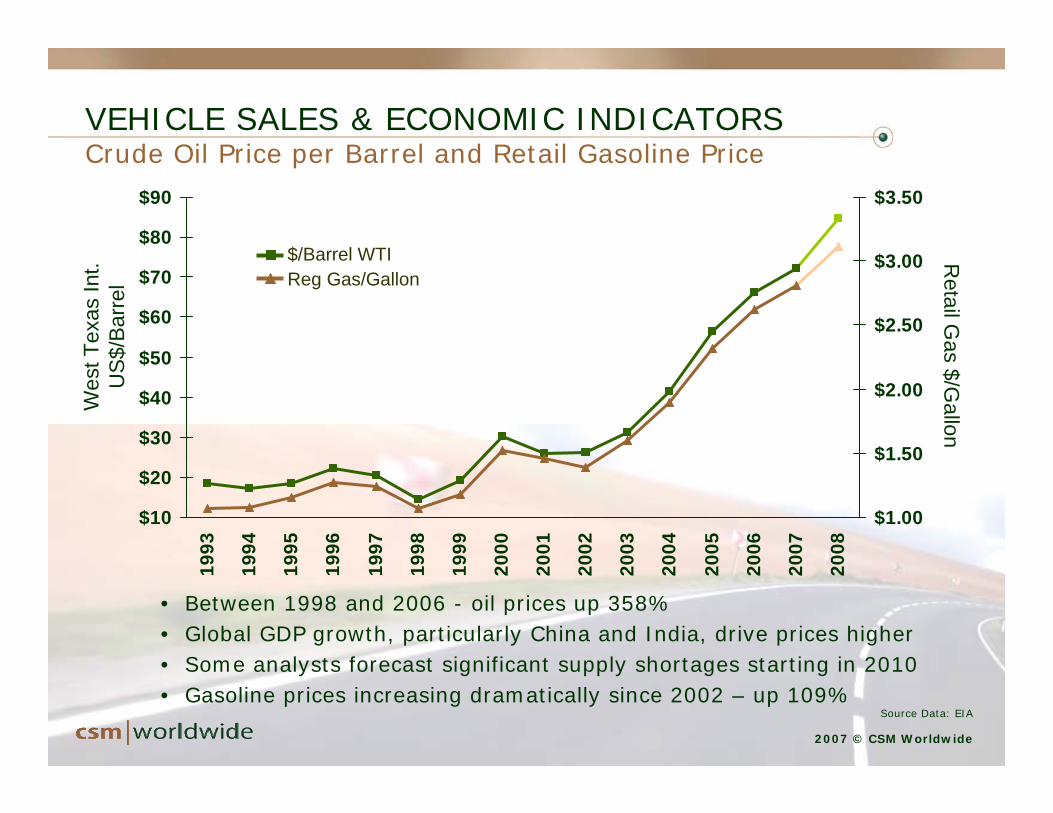

VEHICLE SALES & ECONOMIC INDICATORS Crude Oil Price per Barrel and Retail Gasoline Price

• Between 1998 and 2006 - oil prices up 358% • Global GDP growth, particularly China and India, drive prices higher• Some analysts forecast significant supply shortages starting in 2010• Gasoline prices increasing dramatically since 2002 – up 109%

Wes

t Tex

as In

t.U

S$/B

arre

lR

etail Gas $/G

allon

Source Data: EIA

$/Barrel WTIReg Gas/Gallon

2007 © CSM Worldwide

UNITED STATES SALES OUTLOOK Lethargic Though It Could Have Been Worse

16.116.316.3

16.1 16.015.515.5

16.216.416.3

16.616.7

16.8

16.116.216.7

16.1

17.2

16.216.216.716.616.7

17.6

14

15

16

17

18

19

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2006

Uni

ts in

mill

ions

• Seasonally Adjusted Annualized Rate (SAAR) tracking at 16.1 million units

• Headwinds pose downside threat in 1Q & 2Q 2008

• Concerns include mounting consumer debt, stiffening credit practices and consumers uninspired by incentive programs

2007 © CSM Worldwide

• Sagging market demand to push sales to lowest level since 1998 • Sizable consumer debt, tightened lending guidelines and high gasoline

prices have diminished purchasing power• Depleted pent-up demand also hampering sales • Long-term, moderate growth stems from improved trends in housing, debt,

scrappage and off-lease prospects

UNITED STATES SALES OUTLOOK Remembering The Good Ole Days

17.3 17.1 16.8 16.6 16.9 16.9 16.6 16.1 15.8 16.1 16.5 16.9 17.3 17.6

0

4

8

12

16

20U

nits

in M

illio

ns

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2007 © CSM Worldwide

UNITED STATES SALES OUTLOOK 2007 Sales Forecast By Company

3.82

2.63

2.07

1.070.78

1.55

2.56

0

1

2

3

4

5

GM

Toyo

ta

Ford

Chr

ysle

r

Hon

da

Nis

san

Hyu

ndai

-15%

-10%

-5%

0%

5%

10%2007 ActualYOY % Change

Unit Sales

Uni

ts in

Mill

ions

Market Share

GM, 23.5%

Toyota, 16.2%

Ford, 15.8%

Chrysler, 12.9%

Honda, 9.6%

Nissan, 6.6%

Hyundai, 4.8%

2007 © CSM Worldwide

UNITED STATES SALES OUTLOOK 2008 Sales Forecast By Company

3.63

2.70

1.99

1.180.73

2.59

1.64

0

1

2

3

4

5

GM

Toyo

ta

Ford

Chr

ysle

r

Hon

da

Nis

san

Hyu

ndai

-10%

-5%

0%

5%

10%

15%2008 ForecastYOY % Change

GM2 3 . 7 %

Toy ot a16 . 2 %

For d15 . 8 %

Hy unda i4 . 8 %Ni ssa n

6 . 6 %

Chr y sl e r12 . 9 %

Honda9 . 6 %

Unit Sales

Uni

ts in

Mill

ions

Market Share

2007 © CSM Worldwide

PRESENTATION OUTLINE

• United States Sales Outlook

• NA Production

• Fitting Into A Global Equation

• Summary

2007 © CSM Worldwide

SHORT-TERM OUTLOOK Under Pressure – Short-Term Scenarios

2007 © CSM Worldwide

0

2

4

6

8

10

12

14

16

18

1985 1989 1993 1997 2001 2005 2009

Prod

uctio

n (M

illio

ns)

Detroit 3 New Domestics Total North America

• Negative production environment

• Structural upheaval continues in 2008

• Economic fears and uncertainty hurting demand

• New capacity online late in 2008

• 2009 provides best upside opportunity

• Exports are a positive factor

CAGR = -1.40%

CAGR = 0.40%

CAGR = 9.30%

2007 © CSM Worldwide

200814.4M

Demand

Imports

Capacity

Economics

2007 © CSM Worldwide

US demand weakening amid

growing uncertainty

Japanese imports expected to remain strong to fill supply

gaps

Plant closings and reduced labor

decreasing artificial, subsidized demand

Housing market, credit crunch, volatile fuel

prices adding to weakness

SHORT-TERM OUTLOOK Under Pressure – 2008

2007 © CSM Worldwide

DETROIT 3 VS. NEW DOMESTICSIt Isn’t Bad Everywhere ….

2007 © CSM Worldwide

-500

-400

-300

-200

-100

0

100

200

300

Uni

t Vol

ume

Cha

nge

(Tho

usan

ds) • North American

production to decline 2.0 million units

• New Domestics to grow by 2.0 million units

• Detroit 3 to decline 4.0 million units

• Mirror effect - less effective tool

2000 – 2009

2007 © CSM Worldwide

-500

-400

-300

-200

-100

0

100

200

300

Uni

t Vol

ume

Cha

nge

(Tho

usan

ds)

2007 © CSM Worldwide

14.7M200914.4M200815.1M2007

• Detroit 3 structural changes continue

• Shift in production continues

• New Domestics growth is product driven

• New Domestics continue to add local build and new capacity

• Nissan weakness follows difficult comparisons

SHORT-TERM OUTLOOK Under the Hood – Shifting Fortunes

2007 © CSM Worldwide

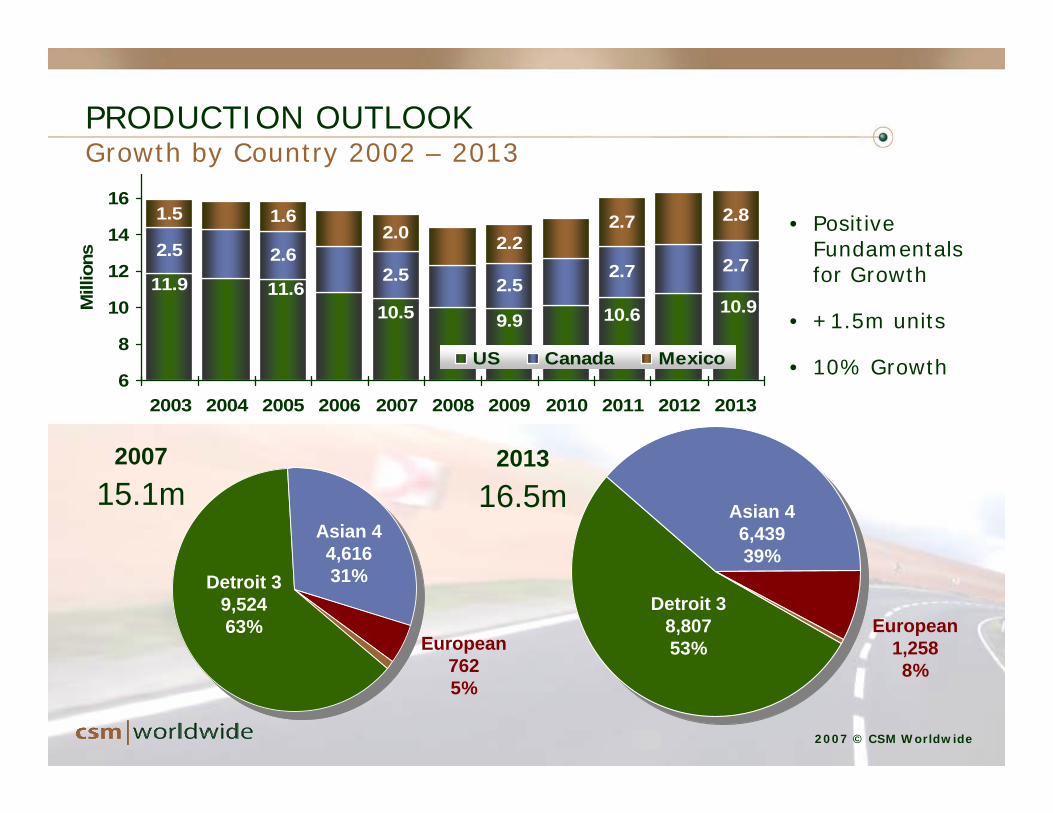

PRODUCTION OUTLOOKGrowth by Country 2002 – 2013

2.5 2.62.5 2.5

2.7 2.7

1.5 1.62.0 2.2

2.7 2.8

11.9 11.610.5 9.9 10.6 10.9

6

8

10

12

14

16

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Mill

ions

US Canada Mexico

200715.1m

Detroit 39,52463%

Asian 44,61631%

European7625%

Detroit 38,80753%

Asian 46,43939%

European1,2588%

2007 © CSM Worldwide

201316.5m

• Positive Fundamentals for Growth

• +1.5m units

• 10% Growth

2007 © CSM Worldwide

PRESENTATION OUTLINE

• United States Sales Outlook

• NA Production

• Fitting Into a Global Equation

• Summary

2007 © CSM Worldwide

GLOBAL LIGHT VEHICLE SALESEmphasis on New Markets

18.916.7

6.53.8 4.9

7.24.2

1.9

1.8

1.6

1.21.4

4.2

3.7

0.4

-5

0

5

10

15

20

25

N A

mer

ica

W E

urop

e

Japa

n/K

orea

S A

mer

ica

C/E

Eur

ope

Gtr

Chi

na

Sout

h A

sia

ME/

Afr

ica

Mill

ions

-2%

0%

2%

4%

6%

8%

10%

12%2007-13 Grth20072007-13 CAGR% (R-axis)

N Am, 12%

W EU, 11%

S Am, 8%

CE EU, 11%

China, 29%

S Asia, 26%

ME/Af, 3%

0%

100%

Contribution toGrowth 2007-

201377

% D

evel

opin

g M

arke

ts

2007 © CSM Worldwide

0

10

20

30

40

50

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Milli

ons

Japan/Korea W. Europe North America

GLOBAL PRODUCTION TRENDSGlobal Light Vehicle Production by Region

2007 © CSM Worldwide

0

10

20

30

40

Milli

ons M E/Africa S America C/E Europe

Gtr China SE Asia

43.2 45.4 45.547.9

45.58.9 10.4

22.1

36.8

2007-2013 Growth Rate 0.9%

2007-2013 Growth Rate 8.8%52

56

68

85

2007 © CSM Worldwide

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%19

97

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Glo

bal P

rodu

ctio

n Sh

are

By

Sale

s Pa

rent

%

GLOBAL PRODUCTION TRENDSGrowth of the Asian 4 by Sales Parent

2007 © CSM Worldwide2007 © CSM Worldwide

GLOBAL PRODUCTION TRENDSGlobal Production By Global Segment

10.610.5

9.3

18.5

16.5

10.5

9.9

5.6

10.5

12.5

9.5

4.1

5.7

10.6

13.9

4.9

10.1

5.9

6.3

12.6

19.2

13.2

6.9

23.2

0 5 10 15 20 25 30

A

B

C

D

E

FF

Millions

2013200720021997

0.0%

2.6%

4.6%

3.2%

5.8%

6.8%3.0

5.2

4.0

3.9

0.9

0.0

2007-13 Grow

th (Mil)

18%A

31%B

23%C

23%D

6%E

-1%FF

Share of Grow

th

Global Segm

ent

CAGR %2007-2013

2007 © CSM Worldwide

SEGMENT FOOTPRINT ANALYSISShare By Major Developed Region & Global Segment

• Europe and Japan/Korea focused on B- and C-segments, due to domestic market requirements and historical abilities

• Fewer space considerations and lower fuel costs drive North America toward C, D, E from Full-Frame

• Shifts reflective of domestic and export trends as production matures in developed markets

0%5%

10%15%20%25%30%35%40%

A

B

C

D

E

FF

EU-2007EU-2013JK-2007JK-2013NA-2007NA-2013

2007 © CSM Worldwide

SEGMENT FOOTPRINT ANALYSISNot Every Emerging Market Is The Same

• China matures –becoming more rationalized into the global framework

• China has similarities to Europe and Japan/Korea

• SE Asia driven by higher A & B segment volume in India, small car projects in Thailand – pickups suffer

• South America is the quintessential B-segment market –little change as the market expands

0%

10%

20%

30%

40%

50%

60%

70%A

B

C

D

E

FF

China-2007China-2013SE Asia-2007SE Asia-2013S Am-2007S Am-2013

2007 © CSM Worldwide2007 © CSM Worldwide

0 1 2 3 4 5 6 7 8 9 10 11 12 13

Toyota

GM

Ren/Niss

Ford

VW

Hyundai

Honda

PSA

Fiat

Suzuki

Units in Millions

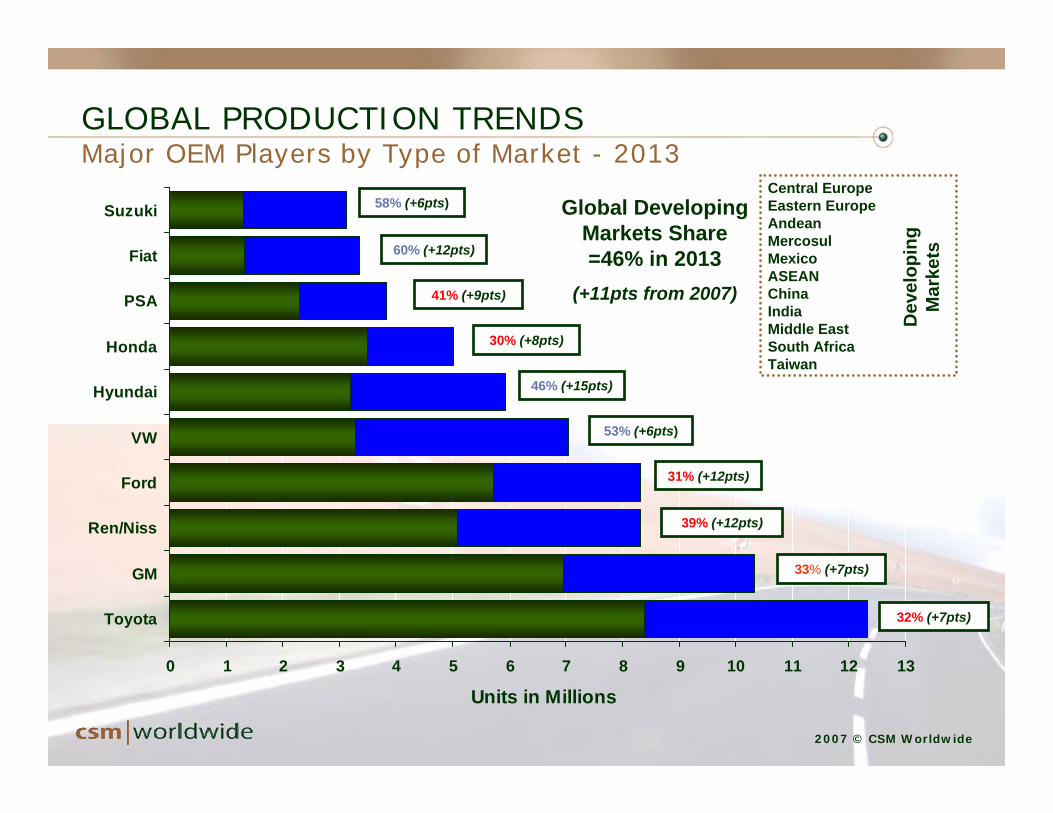

GLOBAL PRODUCTION TRENDSMajor OEM Players by Type of Market - 2013

Dev

elop

ing

Mar

kets

Global Developing Markets Share =46% in 2013

(+11pts from 2007)

Central EuropeEastern EuropeAndeanMercosulMexicoASEANChinaIndiaMiddle EastSouth AfricaTaiwan

39% (+12pts)

31% (+12pts)

53% (+6pts)

46% (+15pts)

30% (+8pts)

41% (+9pts)

60% (+12pts)

58% (+6pts)

32% (+7pts)

33% (+7pts)

2007 © CSM Worldwide2007 © CSM Worldwide

114

153

80

90

100

110

120

130

140

150

160

Th

ou

sa

nd

s

Vo

lum

e/P

lan

tLESS IS MORE AND MORE IS LESSIncreased Scale Affects Plants and Platforms

2007

192

168

155

160

165

170

175

180

185

190

195

Pla

tform

s O

ve

r 5

0K

2013

2005

2013

2005

Volume Per Plant Platforms over 50K/Year

2007 © CSM Worldwide

NOT MY GRANDFATHER’S INDUSTRY

• Style, Technology, Value & Scale• Tomorrow’s differentiators were yesterday’s

• Mastering The Fuel Economy Puzzle• No single solution – several options required• Don’t alienate suppliers – they may be needed

• An ever shrinking world still has its islands

• Little real trade liberalization from the BRICs

• Winners and Losers Will Be Determined by Those who Understand the Market and Those Flexible Enough to Adapt to It – Stick to the Basics

FACS Automotive Conference

2007 © CSM Worldwide

Michael RobinetVice President, Global Vehicle ForecastsCSM WorldwideNorthville, [email protected]