municipal – state and local issues - aglf.memberclicks.net · •civic federation roadmap report...

TRANSCRIPT

Municipal – State and Local Issues

Toi HutchinsonIllinois State Senator

Chair, Illinois Senate Revenue CommitteePresident-Elect, National Conference of State Legislatures

Director of Community Relations and Social Responsibility, Chapman and Cutler LLP

National perspective as President-Elect of National Conference of State Legislatures

• States as little laboratories of democracy• Beauty of convening legislators across the country in a setting

where they are not competing with one another but instead sharing ideas and analyzing results

• Party affiliation is secondary – it is primarily about the ideas and why the institution of the legislature is so critically important

Unique perspective as Chair of Illinois Senate Revenue Committee:• “You may be able to run the United States through a twitter feed but

it’s much harder to run Illinois government just trading headlines”• How to de-toxify politics in our two-party system• How to generate the political will and public support that’s necessary

to get solutions passed

Unique perspective as Chair of Illinois Senate Revenue Committee:• Untold stories of the sausage-making process - How the 2 year

budget impasse was overcome!• Democratic Chair of State Revenue Committee hiding 12

Republicans in her apartment • Breakthrough for impasse and 7 universities being downgraded in

one day • Facing crises together - relationships across party lines were

fostered by going to battle together• Be the Oprah of Politics – What can we all agree on?

Fiscal Issues: Challenges and Opportunities for Illinois and Chicago

Laurence Msall, PresidentThe Civic Federation

May 3, 2018

5-4-16

ABOUT THE CIVIC FEDERATION

• Members include major corporations and service firms

• Independent and nonpartisan

• Founded in 1894

• We promote:

• Sustainable tax and fiscal policies

• Responsible long-term financial planning

• High quality, efficient government services

Membership opportunities and more information at civicfed.org

www.civicfed.org

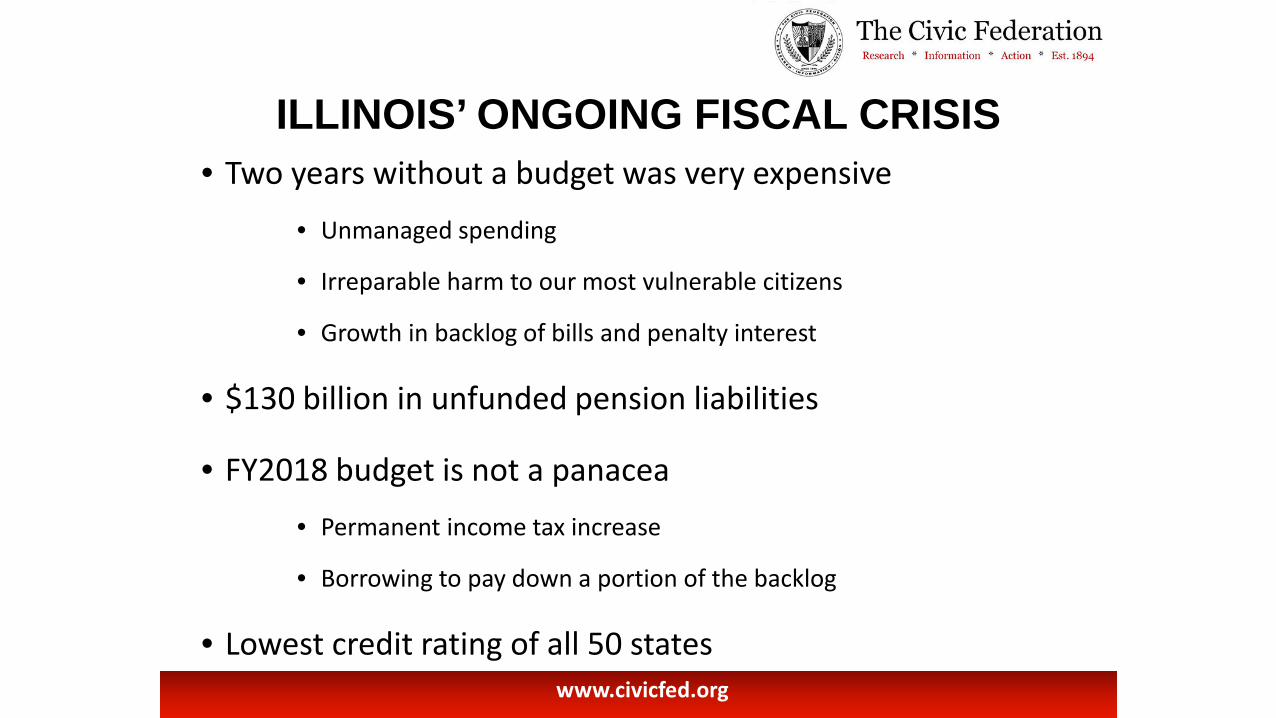

ILLINOIS’ ONGOING FISCAL CRISIS• Two years without a budget was very expensive

• Unmanaged spending

• Irreparable harm to our most vulnerable citizens

• Growth in backlog of bills and penalty interest

• $130 billion in unfunded pension liabilities

• FY2018 budget is not a panacea• Permanent income tax increase

• Borrowing to pay down a portion of the backlog

• Lowest credit rating of all 50 states www.civicfed.org

Aaa Credit (14 States)

Indiana(Aaa)

Iowa(Aaa)

Missouri(Aaa)

Texas(Aaa)

Aa Credit (32 States)

Kansas(Aa2)

Ohio(Aa1)

Wisconsin(Aa1)

Michigan(Aa1)

A Credit(2 States)

New Jersey(A3)

Connecticut(A1)

Baa3 Credit (1 State)

Illinois(Baa3)

CREDIT RATINGS OF SELECTED U.S. STATES

Source: Moody’s Investors Service

www.civicfed.org

CHICAGO’S FISCAL CHALLENGES

www.civicfed.org

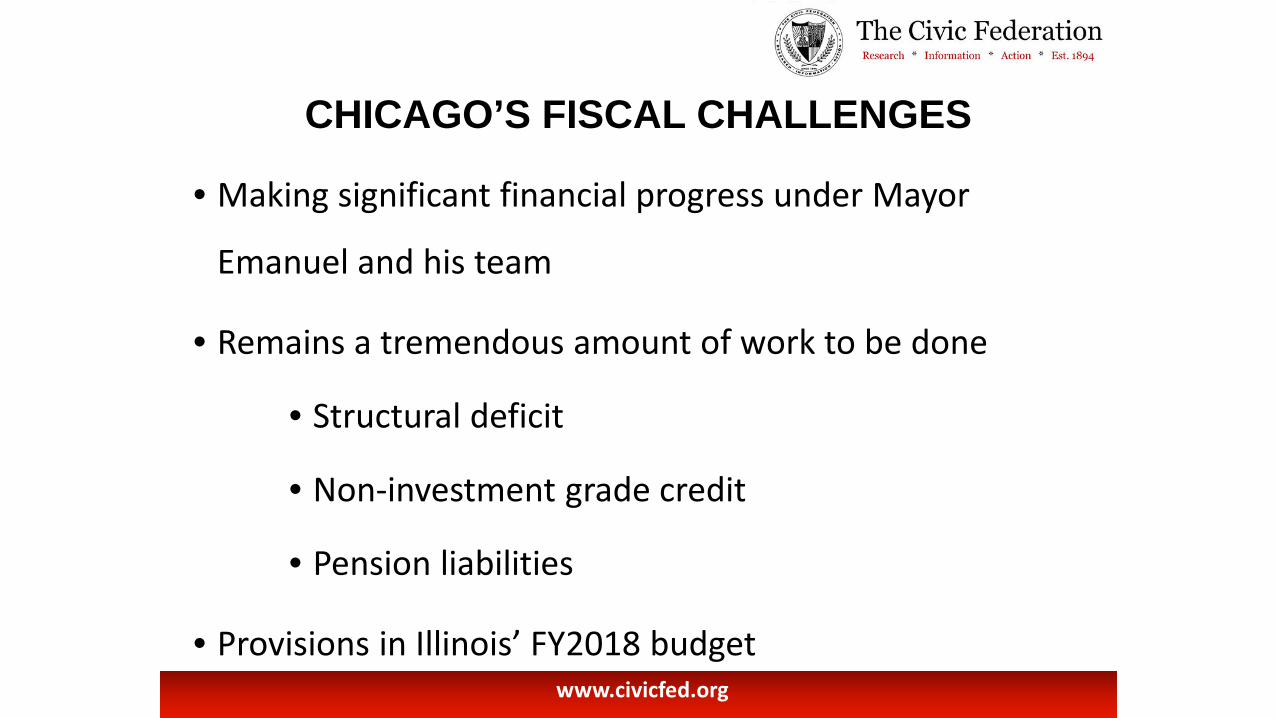

• Making significant financial progress under Mayor

Emanuel and his team

• Remains a tremendous amount of work to be done

• Structural deficit

• Non-investment grade credit

• Pension liabilities

• Provisions in Illinois’ FY2018 budget

CHICAGO PUBLIC SCHOOLS and SB 1947

www.civicfed.org

• P-12 funding contingent on evidence-based formula

• SB1947 passed, signed

• Hold harmless for all districts

• Pension levy increase for CPS

• Pilot program for donations to private school scholarships

• Ongoing challenges for CPS

WHAT’S NEXT?

www.civicfed.org

• FY2018 State of Illinois budget stops the bleeding; FY2019

budget deadline approaching

• Pensions continue to weigh on all levels of government

• Consolidation

• Constitutional amendment

• Bankruptcy? Better path: Local Government Protection Authority

• Civic Federation Roadmap report civicfed.org

THANK YOU

• Happy to answer questions

• Visit civicfed.org for more information

312-201-9066

www.civicfed.org

Ways for Returning to Championship FormA Case Study of Sales Tax Securitization Bonds

Issued for the City of Chicago

Juliet HuangPartner, Chapman and Cutler LLP

Perceived Bankruptcy Risk for State and Municipalities in Illinois:• The State of Illinois cannot file for federal bankruptcy protection • Municipalities in Illinois are not authorized to file for Chapter 9• The City of Chicago cannot file for Chapter 9 unless the law changes

The City of Chicago’s Economy

Highly Skilled Workforce

Destination for Corporations

TransportationHub

TouristDestination

The City has a concentration of talent in legal, engineering and financial services 35.6% of Chicagoans over 24 have bachelor’s degrees (a higher percentage

than New York City) Growing residential population in the City Center

34 Fortune 500 companies are headquartered in the Chicago region The City was named “Top Metro For Corporate Relocation” in 2014-2016 and

“Top Metro For Corporate Investment” in 2015 by Site Selection Chicago has been the #1 U.S. city for foreign direct investment for the last four

years, according to IBM Global Location Trends report

The City is a major hub for:– 6 of the 7 Class I railroads in the U.S.– 3 of the 4 largest airlines in the U.S.

O’Hare is the nation’s 2nd busiest airport by number of passengers

Investment downtown has revitalized cultural attractions for residents and tourists The City has:

– 56 museums, 125 art galleries and 20 neighborhood art centers– 8,100 acres of green space with 580 parks and 26 beaches

A record 54 million tourists visited the City in 2016

Chicago has one of the

most diverse

economies of any major

U.S. city

Key Statistics Regarding the City of Chicago’s Economy

A Case Study of

$743,735,000Sales Tax Securitization Corporation Sales Tax Securitization Bonds,

$172,065,000 Series 2017A$400,630,000 Taxable Series 2017B$171,040,000 Taxable Series 2017C

$680,280,000Sales Tax Securitization Corporation Sales Tax Securitization Bonds

$376,305,000, Series 2018A$303,975,000 Taxable Series 2018B

Statutory Framework of Securitization Statute• At the City of Chicago’s urging, state legislation (65 ILCS 5/8-13-5 et. seq)

(the “Authorizing Act”) was passed and became effective on July 6, 2017 which allows home rule units of government in Illinois to securitize revenues or taxes that flow through the State of Illinois.

• With the statutory framework in place, City of Chicago passed an ordinance establishing the new special purpose entity called the Sales Tax Securitization Corporation (“SPE” or “Corporation”).

• Chicago’s ordinance authorized up to $3 billion of borrowing under the new structure.

Securitization Statute is a Valuable Tool for Returning to Championship Form• Passage of this legislation by the State was a huge accomplishment for

the City as it:• Frees the transferred Sales Tax Revenues from any Perceived City

Credit Risk• Provides City with access to new investors• Lowers debt service• Preserves City access to residual Sales Tax Revenues after debt

service is paid • Provides City with financial flexibility

Significant Economic Benefit to Chicago$743,735,000 Series 2017 Sales Tax Securitization Bonds• Refunded $563,370,000 (i.e. all) of the City’s outstanding Sales Tax Revenue Bonds and

$165,960,000 of the City’s outstanding General Obligation Bonds• Attracted more than 70 traditional and non-traditional municipal investors• Five times oversubscribed• Generated ~ $34 million in premium$680,280,000 Series 2018 Sales Tax Securitization Bonds• Refunded $712,920,000 of City’s outstanding General Obligation Bonds• Attracted 42 investors• Two times oversubscribed• Generated present value savings of 6.3%• Priced approximately 275 basis points less than than similar maturities on the City's most recent

general obligation bonds from last year• Generated ~$45 million in premium.

Features of Securitization Program to Remove City Bankruptcy Risk• Similar in some ways to an intercept program, funds flow directly from the State

to the Bond Trustee. • Under this structure, the City's share of sales taxes that flow from the State ($660

million in 2016) goes directly from the State to the Bond Trustee and is no longer property of the City.

• While federal law governs bankruptcy procedure, state law governs the ownership and conveyance of property. So federal bankruptcy courts must follow state law in determining ownership of property. In Chapter 9, a bankruptcy court is prohibited from confirming a plan that would violate state law.

• The absolute conveyance under the Authorizing Act means that the transferred sales taxes will become the property of the Corporation/SPE.

• Therefore in the event of a City bankruptcy, a plan of adjustment that contradicts this right and determination by the State would violate state law and thus should not be confirmable.

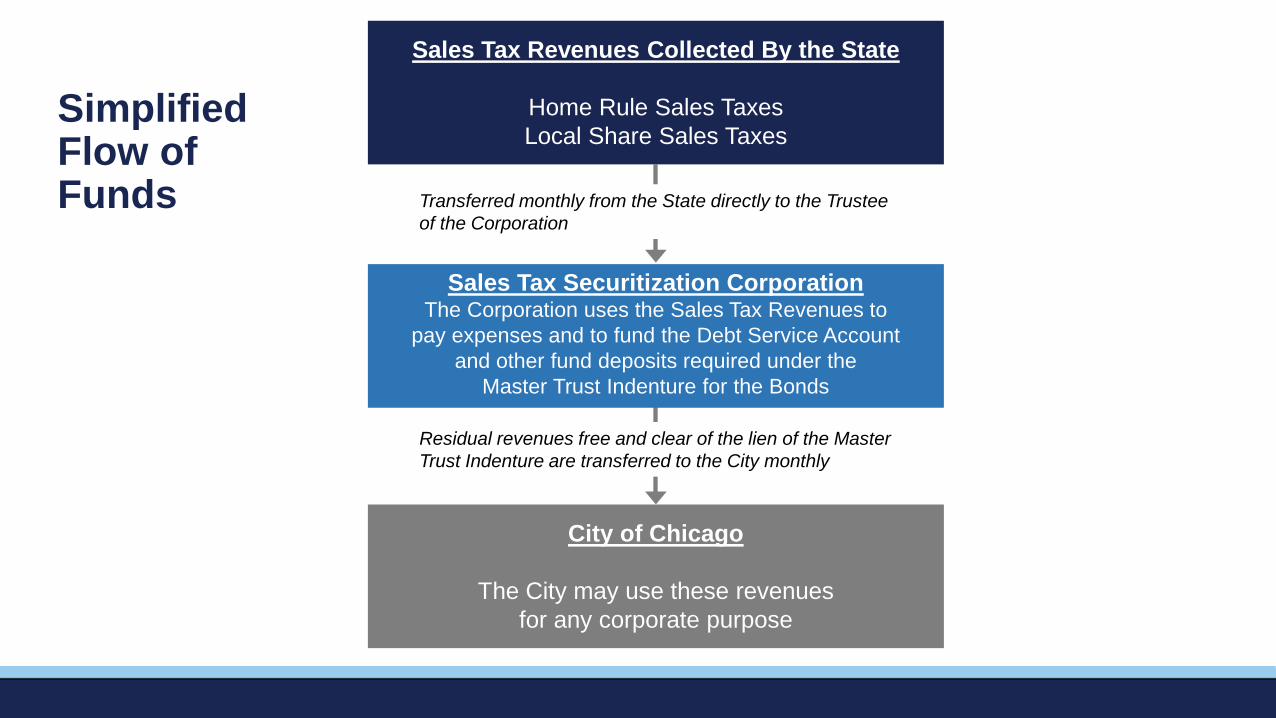

Simplified Flow of Funds

Sales Tax Revenues Collected By the State

Home Rule Sales TaxesLocal Share Sales Taxes

City of Chicago

The City may use these revenuesfor any corporate purpose

Sales Tax Securitization CorporationThe Corporation uses the Sales Tax Revenues to

pay expenses and to fund the Debt Service Account and other fund deposits required under the

Master Trust Indenture for the Bonds

Transferred monthly from the State directly to the Trustee of the Corporation

Residual revenues free and clear of the lien of the Master Trust Indenture are transferred to the City monthly

Features of the Corporation• The Corporation is formed as a nonprofit organization under the State of Illinois’

General Not For Profit Corporation Act of 1986• The City is authorized to enter into the Sale Agreement with the Corporation

and sell the Sales Tax Revenues in consideration for the proceeds of the bonds issued by the Corporation and a Residual Certificate

• The Corporation does not have any power to pledge the full faith and credit of the City nor shall any Corporation Obligation be an obligation, general or special, of the City

• Legal Analysis – True Sale and Non-Consolidation opinions rendered by Nixon Peabody which opinions are standard in securitization market.

Well-Established Structure to use Bankruptcy Remote SPEs in Securitization MarketThe Corporation is a special purpose entity (“SPE”) organized for the limited purpose of purchasing the Sales Tax Revenues from the City and issuing bonds, notes, certificates, contract rights or other obligations for the benefit of the City:• Proceeds of the Corporation’s issuances are for the sole benefit of the City, including the

refunding of any existing obligations of the CityThe affairs of the Corporation are managed by a Board of Directors comprised of:• Five permanent members, including the Chief Financial Officer, Budget Director, Comptroller,

Chair of the Finance Committee of the City Council, and Chair of the Committee on Budget of the City Council. The Chairs of the Finance and Budget Committees may appoint designees.

• In addition, one Independent Director will be appointed by the Mayor and approved by City Council in the event of a “Specified Vote,” defined as any vote to take actions that could be adverse to bondholders (e.g., consolidate, liquidate, etc.)

• The Board Members have a fiduciary duty to the Corporation• A “Specified Vote” requires the affirmative vote of all six members of the Board of Directors

(including the Independent Director)

The Independent Director cannot:i. be a City Elected Official, a State Elected Official or a member of the governing board of any

Affiliated Local Government or of any Affiliated Corporate Entityii. have a Familial Relationship with any City Elected Official, any State Elected Official or any

member of the governing board of any Affiliated Local Government or of any Affiliated Corporate Entity

iii. have a Familial Relationship with any person who is an employee of the City, any Affiliated Local Government, any Affiliated Corporate Entity or the State

iv. be an employee of the City, any Affiliated Local Government, any Affiliated Corporate Entity or the State; and will not have been such an employee within the five years preceding the date of appointment; or

v. be Doing Business or seeking to Do Business with the City, any Affiliated Local Government, any Affiliated Corporate Entity or the State and will not, within the five years preceding the date of appointment, have Done Business with the City, any Affiliated Local Government, any Affiliated Corporate Entity or the State.

Red Herring - COFINA Concerns Do Not Extend to STSC bondsCOFINA (Corporación del Fondo de Interés Apremiante)• Aka: Puerto Rico Sales Tax Financing Corporation• A government-owned subsidiary of the Government Development Bank for

Puerto Rico or GDB. • COFINA receives a portion of the sales and use taxes collected in Puerto

Rico and was designed to use those revenues to pay debt service on sales tax revenue bonds

Unique COFINA Dispute (has been brewing since before Chicago’s STSC bonds)

• Puerto Rico Constitution essentially requires that ALL “Available Resources” be used to pay General Obligation Debt

• Congress enacted bankruptcy-like legislation for Puerto Rico (PROMESA) and thereby created a venue to challenge COFINA

• General Obligation holders assert that COFINA structure is unconstitutional and that Revenues must be paid to General Obligation holders

How Chicago’s Securitization Bonds differ from COFINA• The power to control the imposition of a sales tax is reserved to the State under

the Illinois Constitution. The State of Illinois is acting within its constitutional authority to direct the treatment of these sales tax revenues.

• The Authorizing Act allows a home rule municipality in Illinois to enter into an assignment agreement with the SPE for the absolute conveyance of revenues or taxes.

• The State has exercised its constitutional right to control the disposition of the Sales Tax Revenues and determined that the Sales Tax Revenues, once sold, are no longer property of the City.

• Illinois' constitutional authority to define the powers of its municipalities is not subject to dispute.

• (The Authorizing Act also provides that a statutory lien (11 U.S.C. 101 (53)) attaches automatically to the Sales Tax Revenues without further action.)

Legal Differences• No analogous “Available Resources” provision in Illinois Constitution

• Hierarchy of laws: A statute (i.e. the COFINA statute) cannot amend, change or overcome a constitutional requirement

• In Illinois the State has constitutional authority to impose and control sales tax

• No means for State-level bankruptcy proceeding like PROMESA because of State sovereignty

o Illinois cannot file for bankruptcy and Congress cannot enact PROMESA-like legislation for states

Legal Differences (cont’d)• Non impairment claim - failure of the State to remit taxes to STSC would likely

violate the federal and states Contracts Clause

• City bankruptcy is irrelevant because Sales Tax Revenues have been sold pursuant to state statute and there is no means to claw back revenues

o No practical way for the City to Intercept revenues since taxes are collected by the State and remitted to STSC

o City has no claim to “Sales Tax Revenues” but only to residual funds of STSC after debt service

• CONFINA, the dispute also involves the bankruptcy of a quasi-State, not a city

• Practical Differences–Illinois is Not Puerto Rico (Not equivalent financial distress)