mt briefing april15 - poundadayportfolio.com filepoliticians, markets, economists…. like children...

TRANSCRIPT

Politicians, markets, economists….Like children in a sweetshop.

As we move into the second quarter of 2015, three key issues are currently driving market sentiment; the timing of the next interest rate hike in the US, the future membership of Greece in the Eurozone and the outcome of the UK General Election. The outcome of each will impact markets one way or another over the course of the next few months.

The mere threat of higher interest rates in America has helped to stoke a remarkable rally in the dollar. Whilst noise from American news channels might suggest otherwise, the recent performance of US equities has actually been subdued. Measured in other currencies, however, the performance of US equities has been very good indeed. In fact, the key determinant of international portfolio performance over the last few quarters has been currency. In soggy euro terms, investors are delighted and even sterling shareholders are reasonably satisfied. Dollar investors, on the other hand, are generally disappointed at the mismatch between the newspaper headlines and reality. In global currency terms, there is no performance difference, yet the European investor feels greatly richer whilst the dollar investor feels short-changed.

Interest rates partly reflect inflationary expectations. In the US, the UK and Europe, inflation appears to have vanished altogether. In a zero inflation world, a pound is worth a pound and a dollar is worth a dollar. In parts of Europe, where no fewer than three central banks have set negative interest rates, you are being charged to lend them money. This weird situation cannot last indefinitely and the US Federal Reserve Bank is poised to hike interest rates at the first whiff of higher consumer prices. This would have happened sooner but, like an over anxious parent, the Fed is worried that economic growth is still too fragile to risk upsetting markets. Upset them it must, however, and the first hike in nearly 10 years will probably occur later this year. We expect the equity market’s reaction to be short, sharp, in a downwards direction and a buying opportunity. Longer term, markets are going up.

The second market concern is Greece. If Greece was a company employee, it would have been fired years ago. Unfortunately, the country is more akin to a delinquent family member whose parents blame each other for their failed prodigy. Whilst the Eurozone’s leaders have already bent the rules many times to accommodate the Greeks (who, of course, should never have been allowed to join the club in the first place), more rule bending will be needed to reinforce the delicate cord joining Greece to their regional partners.

Investment Management

Tel +44 (0) 1624 681250 Email [email protected] Web www.iomagroup.co.im

IOMA Fund and Investment Management Limited trading as IOMA Investment Management. Licensed by the Isle of Man Financial Supervision Commission.

Sugar Rush

They can’t pay their way, they blame others for their misfortune and they break their promises as well as possessing a comical finance minister. However, (German) irritation aside, Greece is small and shrinking. For all the wrong reasons, therefore, it will stay in situ. The consequences of a departure from the Eurozone are simply too great for the European Troika and the markets to contemplate.

Finally, the UK General Election campaign is under way. As Manx residents, we don’t qualify for a vote in this particular contest and so will watch events unfold with a degree of impartiality and/or indifference. The outcome will, however, have an impact on markets to some degree. A blue tinged coalition should theoretically be market friendly but the prospect of a referendum on whether the UK should leave the European Union or not provides uncertainty for businesses where the European market is key. A red tinged coalition, on the other hand, possibly tied up to the Scottish National Party and their questionable statistics will also fail to inspire the market and will rattle banks and property companies which, amongst others, represent relatively easy targets for higher taxes. The latest coalition budget was, however, well received and we think that this will help to tilt the balance in favour of the incumbent coalition. Either way, it all makes for an extremely interesting summer ahead.

Quarter 2 2015

Russell Collister Investment Director - April 2015

Zero Boundaries

www.iomagroup.co.im

On a journey between two US cities, I once saw a sign which said in bold letters: “America, bless God, so God can bless America”. It occurred to me that one might never see this statement declared (6 feet high and 20 feet off the ground) anywhere in the British Isles before it was razed to cinders by a scrum of politically correct local councillors, like a closing scene from “The Wicker Man”. As the former Archbishop of Canterbury, George Carey once suggested in his damning missive on the marginalisation of the Christian faith (“We Don’t Do God”), it would seem that, in the UK at least, Christianity is the new sacrilege, whereas in gun-toting Texas, it is still the norm.

Similarly, every now and again I wonder whether I have lost the run of logic in the world today or am suffering from myopia of conscience resulting from my Catholic upbringing. A case in point: A recent character defence suggested that a certain individual had “only” attended 12 sex parties in the past three years. If this had been some speedo-clad non-celebrity from the moronic TV series “Geordie Shore” or “Ex On The Beach”, I might have ignored it. Yet it referred to Dominique Strauss-Kahn, former French Minister for Economics, Finances and Industry, former head of the International Monetary Fund, economist, lawyer and erstwhile respected politician who fell from grace in 2011 following allegations of sexual assault. It was not so much his comment which floored me, but the fact that this “defence” was seemingly accepted by the media. To err is human, but to forgive is divine, so there must be an army of angels out there. I am clearly not one of them.

Perhaps I am being prudish? A more liberal reaction might be: “nice one DSK, way to go!” He’s only human after all. Perhaps, but it concerns me that reproachable political or financial actions should be greeted with such an enthusiastic high-five. Take, for example, the “necessary” trashing of savings income in the pursuit of (leveraged) growth. Instead of ZIRP (zero interest rate policy), behold, we now have NIRP (negative interest rate policy). Savers have suffered negative real returns for years but as inflation is pushed to the zero

Mary Tait Senior Investment Manager

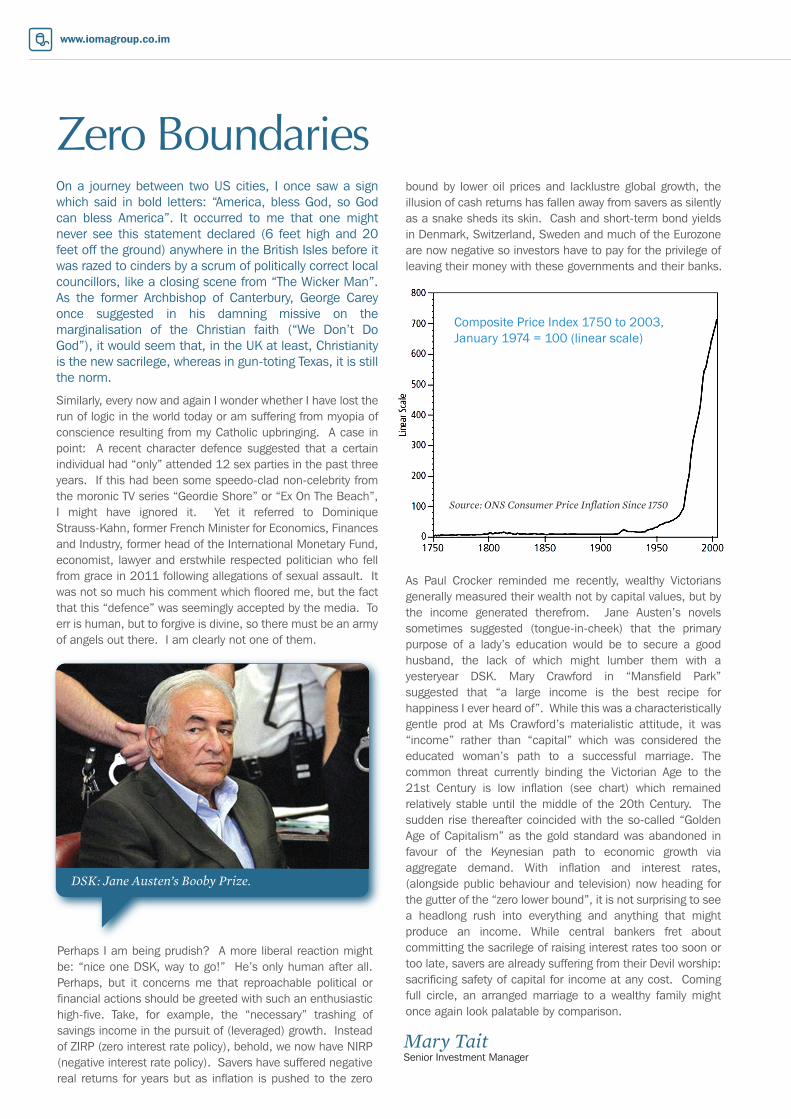

Source: ONS Consumer Price Inflation Since 1750

Composite Price Index 1750 to 2003,January 1974 = 100 (linear scale)

DSK: Jane Austen’s Booby Prize.

bound by lower oil prices and lacklustre global growth, the illusion of cash returns has fallen away from savers as silently as a snake sheds its skin. Cash and short-term bond yields in Denmark, Switzerland, Sweden and much of the Eurozone are now negative so investors have to pay for the privilege of leaving their money with these governments and their banks.

As Paul Crocker reminded me recently, wealthy Victorians generally measured their wealth not by capital values, but by the income generated therefrom. Jane Austen’s novels sometimes suggested (tongue-in-cheek) that the primary purpose of a lady’s education would be to secure a good husband, the lack of which might lumber them with a yesteryear DSK. Mary Crawford in “Mansfield Park” suggested that “a large income is the best recipe for happiness I ever heard of”. While this was a characteristically gentle prod at Ms Crawford’s materialistic attitude, it was “income” rather than “capital” which was considered the educated woman’s path to a successful marriage. The common threat currently binding the Victorian Age to the 21st Century is low inflation (see chart) which remained relatively stable until the middle of the 20th Century. The sudden rise thereafter coincided with the so-called “Golden Age of Capitalism” as the gold standard was abandoned in favour of the Keynesian path to economic growth via aggregate demand. With inflation and interest rates, (alongside public behaviour and television) now heading for the gutter of the “zero lower bound”, it is not surprising to see a headlong rush into everything and anything that might produce an income. While central bankers fret about committing the sacrilege of raising interest rates too soon or too late, savers are already suffering from their Devil worship: sacrificing safety of capital for income at any cost. Coming full circle, an arranged marriage to a wealthy family might once again look palatable by comparison.

Investment Management Briefing Quarter 2 2015

In another tale of marriage above her station, the above quote is attributable to the gentlewoman, Helena as she seeks to win the hand of Bertram, Count of Rousillon in a series of Machiavellian plots which threaten tragedy but end well (hence the title of the play). Ultimately, she gets her man, but not without considerable effort and risk. Shakespeare’s observations of human nature have stood the test of time and this tale is no exception, suggesting that only hard graft, ingenuity and other forms of self-help will achieve results.

In February, we saw the passing of the Italian entrepreneur, Michele Ferrero. If this name elicits a slightly comforting feeling, you would be right to assume that he was the founder of Ferrero SpA, Europe’s second largest confectionery company, renowned for its ambassadorial adverts for Ferrero Rocher, a sweet based predominantly on hazelnuts rather than cocoa, and the spread “Nutella”, which was recently the subject of a French court battle for parents to name their daughter after it (they lost, mercifully for the child). As a dedicated Catholic, perhaps Mr. Ferrero followed the Christian motto: God helps those who help themselves. His father (Pietro) made the post-war decision as a pastry cook in Alba to take advantage of an abundance of nuts in the surrounding Piedmont hills rather than using expensive, imported cocoa beans with unpredictable pricing. Nevertheless, it was his son, Michele who perfected the process, creating Nutella in 1964, now selling 365,000 tonnes per year (a generous portion of which fuels my teenage son by the spoonful). Along with Kinder and Tic Tac, the Ferrero business is one of Italy’s greatest successes, commanding an incredible 72% share of the global chocolate spreads market and employing 30,000 people in 14 different locations.

It may not have escaped investors’ notice that there is a sea-change taking place in the food industry today. We have seen many fads come and go (and return again) in the pursuit of a healthy, balanced diet (Atkins, Cambridge, 5:2, Paleo, Weight-Watchers, Slim-Fast, to name but a few) but there is significant academic momentum building to disprove (again) the findings of Ancel Keys’ “Seven Countries Study“ from the 1950s which still forms the basis of modern NHS dietary advice, laying the blame squarely on saturated (animal) fats as the key component of ill-health in the modern diet. Like the formulaic unmasking at the end of each episode of Scooby-Doo, it seems that sugar is actually the real villain (it would have gotten away with it too, if it weren’t for those meddling scientists!)

The vilification of sugar must strike silent horror into the core of big food groups like Kellogg, Coca-Cola, Pepsi and General Mills as well as fast-food chains like McDonald’s which have made healthy margins for decades from selling sugary, processed products. Some analysts suggest that this dietary “enlightenment” portends disaster for such companies and their strong record of shareholder returns from dividends and buybacks. The Stanford economist, Paul Romer once suggested “a crisis is a terrible thing to waste” and unlike the Ferrero family, there are significant accumulated profits as well as motivation for a range of “self-help” measures. There will be a few mis-fires along the way, like General Mills’ attempt to “protein-ise” its Cheerios, multiplying added sugars by a factor of approximately 16x to the equivalent of a Krispy Kreme glazed doughnut. Zero points for whoever came up with that concept. Perhaps a more successful approach has been to invest (e.g. Coke’s stake-build in Keurig Green Mountain) or disinvest (Procter & Gamble’s focus on higher-margin household products and Unilever’s proposed “sprexit”). Talk has circulated for some time that McDonald’s might buy out its smaller (successful) rival, Chipotle, while one or two UK companies must look sickly-sweet, with the dollar trading at $1.49 against the Pound. Who could forget the hostile bid for Cadbury’s by Kraft in 2010, which morphed into Mondelez International? As Unilever’s “Plan for Growth” strategy revealed in the 2000s, self-help will mean false-starts, over-ambitious targets and dead-ends, but with the financial fire power to affect change and a patient well-rewarded investor, all’s well that ends well.

The Ambassador’s Guide To Self-Help“Our remedies oft in ourselves do lie” William Shakespeare, All’s Well That Ends Well (c.1604)

“Upon this rock…..” (Matthew 16: 13-20)

Mary Tait Senior Investment Manager

Investment Management Briefing Editor: Mary Tait, Senior Investment Manager

IOMA House - Hope Street, Douglas, Isle of Man, IM1 1AP British Isles. Tel+44 (0) 1624 681250 Fax+44 (0) 1624 681392

www.iomagroup.co.im

Russell CollisterINVESTMENT DIRECTOREmail: [email protected] Tel: +44 1624 681354

Paul CrockerINVESTMENT DIRECTOREmail: [email protected] Tel: +44 1624 681307

Mary TaitSENIOR INVESTMENT MANAGEREmail: [email protected] Tel: +44 1624 681202

Michael CraineJUNIOR INVESTMENT MANAGEREmail: [email protected] Tel: +44 1624 681297

Barbara RhodesSENIOR INVESTMENT ADMINISTRATOREmail: [email protected] Tel: +44 1624 681303

Duelling

We sometimes look to the past with rose-tinted spectacles and I found some evidence suggesting that this has been happening for generations. In Siegfried Sassoon’s 1928 publication “Memoirs of a Fox-Hunting Man”, George Sherston reflects on the characters he knew in his youth at his hunt in the 1890s, saying: “As I remember them now they were desperately fine specimens of a genuine English traditional type which has become innocuous since the abolition of duelling”. It was not until the bottom of the next page that I fully appreciated what I had just read.

These elderly gents would have been middle-aged when duelling disappeared, and given their class, were exposed to this activity in their own youth. They would have been raised with an understanding of the consequences of reckless speech and the importance of knowing the facts, especially during a heated exchange. Their characters were shaped by such risks, contrasting widely with today’s overpaid celebrities, cheating footballers and politicians who have forgotten the meaning of “truth”. This had never crossed my mind before but perhaps explains why society is so different to that of 200 years ago. Nowadays, such a contest would be deemed barbaric but in a society where a man’s honour was central to his identity, reputations had to be maintained by any means necessary. Duels were common among the upper-classes and those who were, or aspired to be gentlemen. Despite a courageous front, few would have relished having to fight and risk killing or being killed. Most were fought to first blood (which could be death) but only 20% of duels ended in fatalities.

So what has this to do with markets? Like many readers I hold UK equities and have been pleased with returns. Unfortunately, if the media is to be believed, the forthcoming election is set to be more open and destructive than ever before. Those jockeying for roles in government are aligning their own interests ahead of the nation’s. The SNP care for nothing other than Scottish independence, Ed Miliband is desperate to be Prime Minister regardless of the consequences, thinking his disastrous policies in Wales will work better in England. Nigel Farage is pursuing a referendum on Europe to prove a point, while the Liberal Democrats appear deluded over what they have achieved in Government. The Conservatives need to “man-up” and confess to what they have got right, what has gone wrong and why. This is honesty, a rare commodity in the

Commons. In reality, this won’t happen and the electorate will be fed a series of half-truths. Imagine then, that we bring back duelling for the duration of the election campaign. Candidates would have to stand by their word and might well be more circumspect with their quips. Back in the 1800s, upper class twits who blurted out their thoughts, had poor eyesight and were lousy shots were selectively culled. That would thin out not only Conservative Party candidates but might scupper Boris Johnson to boot. Those who like a tipple would be vulnerable, both to loose words and a badly-timed fixture. The Scots would be limited to the Claymore, being true to their identity: either the steel or glass version (see above). Imagine Nigel Farage (UKiP) v Alex Salmond (SNP) or Danny Alexander (Lib Dem) v Alex Salmond on prime-time Saturday night viewing, rather than a Leaders debate. It’s a pity Charles Kennedy is out of the running as he may have stepped up to the challenge with a Claymore (glass and steel) in each hand. Duelling with Ed Balls or Ed Miliband (Labour) would probably be the most dangerous as they may forget how the argument started and just take it out on the audience. I don’t suppose Andrew Neil would wish to commentate either unless he was behind bullet proof glass. In times past, this would leave the ladies of the Commons running the country, but the modern age ushered in the Equal Opportunities Act, allowing Yvette Cooper (Labour), Nicola Sturgeon (SNP) and Teresa May (Conservatives) to take up arms as well. One thing is for certain, it would open up a new chapter of honesty in British politics.

Paul Crocker Investment Director

“Swords! What do you think this is, the middle ages? Only girls fight with swords these days. Stand by your gun sir…." (Blackadder the Third, “Duel and Duality”, 1987).

Question Time for Kennedy?