mret case studies 5.16(2)-4

TRANSCRIPT

MICROSTRUCTURE RESEARCH & ENGINEERING TECHNOLOGIES, LLC

CASE STUDIESInnovative Solutions for Complex Quantitative Problems

44 Wall Street, 20th FloorNew York, NY 10005

contact@microstructure-research.comwww.microstructure-research.com

646.389.3856

MRET

CASE STUDY 1: Automated Market Maker Looking for Alpha

CASE STUDY 2: Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

CASE STUDY 3: Back-Office Automation & Infrastructure Products for a Broker-Dealer

CONFIDENTIAL

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Problem OverviewA designated market making firm that handles retail order flow aims to increase volume to 100 million shares per day and achieve net profits in excess of .004 cents per share.

What Can We Do for this Market Making Firm?

We provide a comprehensive, transparent quantitative research and statistical computing solution to help solve the automated dealer problem. Below is a flow chart illustrating our methodology in dealing with such a statistical computing problem.

MRET

CONFIDENTIAL

Research Dealer Problem

Code Factors in R/Create SQL Access Functions

Formulate Initial Hypotheses/Define Assumptions

Brainstorm Factors that Affect

Dealer PnL

Pseudo-Code Factors/Find Right Packages & Libs

Run Principal ComponentAnalysis (PCA) on Initial

Factor Dictionary

Fit the Data (Simple,Multiple, Non-Linear

RegressionConstruct Factor Dictionary

Prepare the Data/Acquire, Load/Clean...

Utilize Machine LearningAnd Artif. Intel. Techniques

Implement Regression and Logistic Tree Analysis

Create Model PnL Configure High Perf.Computing Environment

(8 Core, 16GHZ, GB Ram, Linux Servers)

Build Requisite Utilities

Classification and Sensitivity Analysis

Case Study 1 Automated Market Maker Looking for Alpha

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Define the Dealer Problem Formally

● Using an options pricing framework (Copeland and Galai, 1983) we can reduce the complex trade-off between

the spread that uninformed traders are willing to pay for liquidity versus the spread that aggressive informed

traders are willing to pay for liquidity to an optimal quoted price that represents the liquidity premium that the

dealer charges to traders for immediacy.

● To Solve the Dealer Problem, the dealer must beat Gambler’s Ruin by earning more from uninformed traders

than is lost to informed traders. This is done by earning a positive bid-ask spread, generating cash while

maintaining inventory.

● We want to first know what combination of factors related to the dealer’s order flow and market behavior

maximize the dealer’s risk adjusted return curve.

● The dealer must achieve a positive expectancy per share net of .004 cps in costs.

● How will the outcome be judged? The model will be judged by how accurately its output fits the market

maker’s ideal return curve.

Research the Dealer Problem

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Figure 1

Figure 1 illustrates the price of the demand for immediate liquidity in both efficient and inefficient markets. In efficient markets where information is distributed evenly and instantaneously across all market participants shares transact at the fundamental value given by Vt; however, in inefficient markets where information is asymmetrically distributed the monopolistic dealer has pure pricing power and trade prices given by K*(Q, λ) diverge from Vt and are a function of order quantity Q in relation to arrival rates of traders given by λ (Chacko, C., Jurek, J., Stafford, E., 2008).

Research the Dealer Problem

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

● The schedule of limit prices guaranteeing immediacy depends on the factors determining the value of

the dealer’s option such as arrival rate of opposing order flow λi(·) and limit order prices relative to the

fundamental value of the stock Vt.

● Stoikov and Avellaneda (2006) suggest that

● the optimal bid price may be given by:

● the optimal ask price may be given by:

● Liquidity price schedules can then be

estimated as a percentage immediacy

cost for sales and purchases given by:

Research the Dealer Problem

Compile Relevant Theoretical Papers

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

● Look at the data.

● Determine PnL/Share. Assume exit price after a fill is at VWAP.

● Plot each factor individually against PnL/Share.

● Plot all factors against PnL.

● Determine significant effects.

Collect data and examine them. What are the relevant factors? What are the relationships between the

relevant factors and the dependent variables?

Research the Dealer Problem -Compute PnL from Order Flow Data

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

H1: Liquidity is a function of a security’s fundamental value at a particular point in time and characteristics related to order flow. H2: Liquidity demand can be priced by using an options framework that characterizes concessions of traders seeking immediate liquidity for various transaction sizes.

H3: The most relevant factors affecting the price of liquidity are measurements of price, volatility, volume, and trading intensity.

H4: The liquidity premium that the dealer charges represents a large portion of the transaction costs incurred by traders/investors.

H5: Adverse selection cost when dealing to informed traders represents the dealer’s greatest expense.

H6: The dealer’s price setting power is a function of order arrival rates. The greater the demand for liquidity by uninformed traders, the more money the dealer makes.

H7: Widening Bid-Ask spreads are increasing functions of volatility.

H8: Widening Bid-Ask spreads are increasing functions of covariance in order flow.

H9: Subtle biases in price prior to order receipt may gauge adverse selection risk.

H10: Market impact is a non-linear concave function of transaction size.

H11: The price of liquidity is also a non-linear concave function of transaction size.

Formulate Initial Hypotheses and Assumptions

Initial Hypotheses

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

A5: Market is organized around a single market maker that acts as both an intermediary and an agent that trades

shares as a broker and from his own inventory as a dealer. If a traders wants to buy Q shares and there is an order

imbalance of q shares, the bid-ask spread is crossed for that quantity. The residual quantity is given by Q = Q-q.

A6: The probability of observing an order imbalance of Q shares in the next period is given by:

Accordingly, the estimated time for the completion of a Q share limit order to sell (buy) is distributed exponentially with mean:

Formulate Initial Hypotheses and Assumptions

Basic Assumptions

A1: Volatility increases the cost of transactions.

A2: Option maturities of the dealer’s quotes determine arrival rates.

A3: Order flows are stochastic.

A4: Markets are sometimes efficient and sometimes inefficient.

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

● Average Cost of Instantaneous Reversal-Estimates Fundamental Value

● Log Price Distributions and Patterns (Momentum/Reversal/Auto-Correlation)

● Log Volume Distributions

● Illiquidity Ratio and Measures

● Profitability of Limit Orders

● Log Range (Volatility)

● Bid-Ask Spread Estimates (Log)

● Estimated Order Arrival Rates (Buy/Sell)

Brainstorm Factors

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Construct Initial Factor Dictionary

1a. Log Returns

Log Returns are useful to analyze financial time series as they are easy to work with and more accurate in

describing actual distributions of asset prices as compared to simple returns.

Asynchronous data must be equally spaced.

Definition:

Factor 1: Distributions of Returns

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 1: Distributions of Returns

1b. Average Returns Over Various Evaluation Periods

Arithmetic averages can yield lower frequency return estimates. Moving averages can also be used to

estimate order book skewness which in turn could help estimate price sensitivity to market orders and

market depth.

Definition:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

1c. Volatility of Returns over Various Evaluation Periods

Variance of Simple and Log Returns:

Factor 1: Distributions of Returns

Definition:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

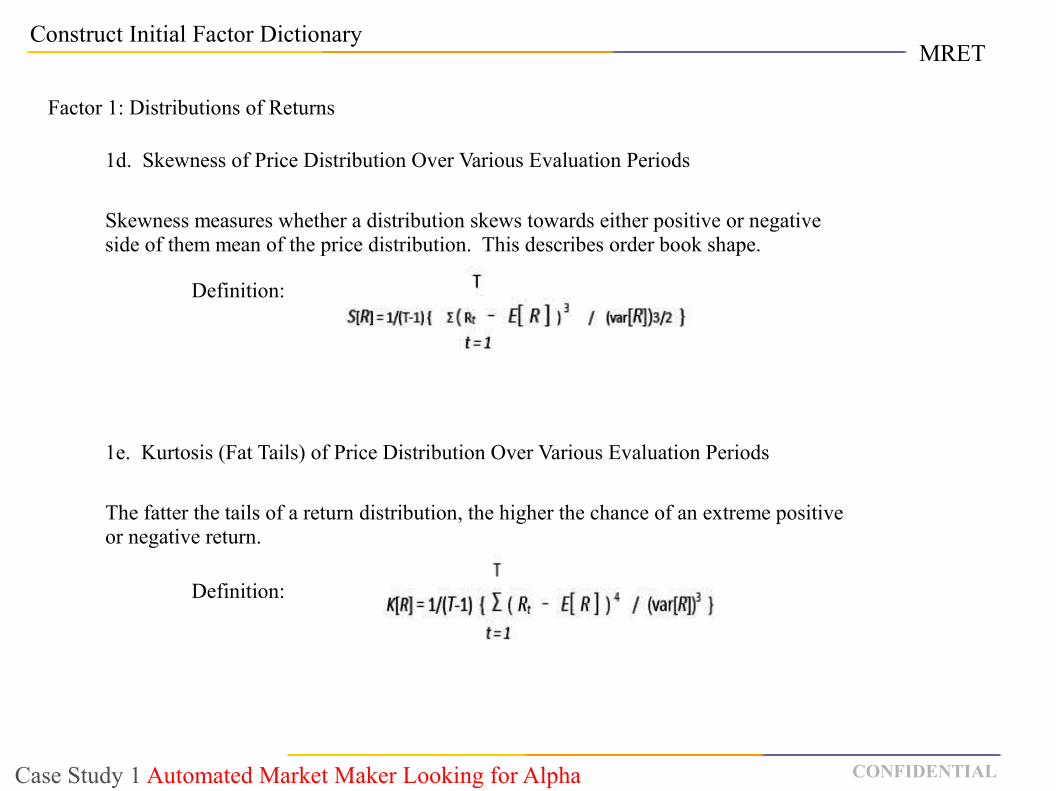

Factor 1: Distributions of Returns

1d. Skewness of Price Distribution Over Various Evaluation Periods

Skewness measures whether a distribution skews towards either positive or negative side of them mean of the price distribution. This describes order book shape.

Definition:

1e. Kurtosis (Fat Tails) of Price Distribution Over Various Evaluation Periods

The fatter the tails of a return distribution, the higher the chance of an extreme positive or negative return.

Definition:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 2: Auto-Correlation

Auto-correlation using log returns can indicate a persistent behavior in returns

and validate patterns of momentum or reversal over a particular evaluation

frequency. Auto-correlation p(p) of order p of a log return distribution can

range from -1 to 1. High auto-correlation >0.5 implies a positive relationship

between observations and lagged observations.

Definition:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 2: Auto-Correlation

Testing the statistical significance of the observed auto-correlation at a given lag:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

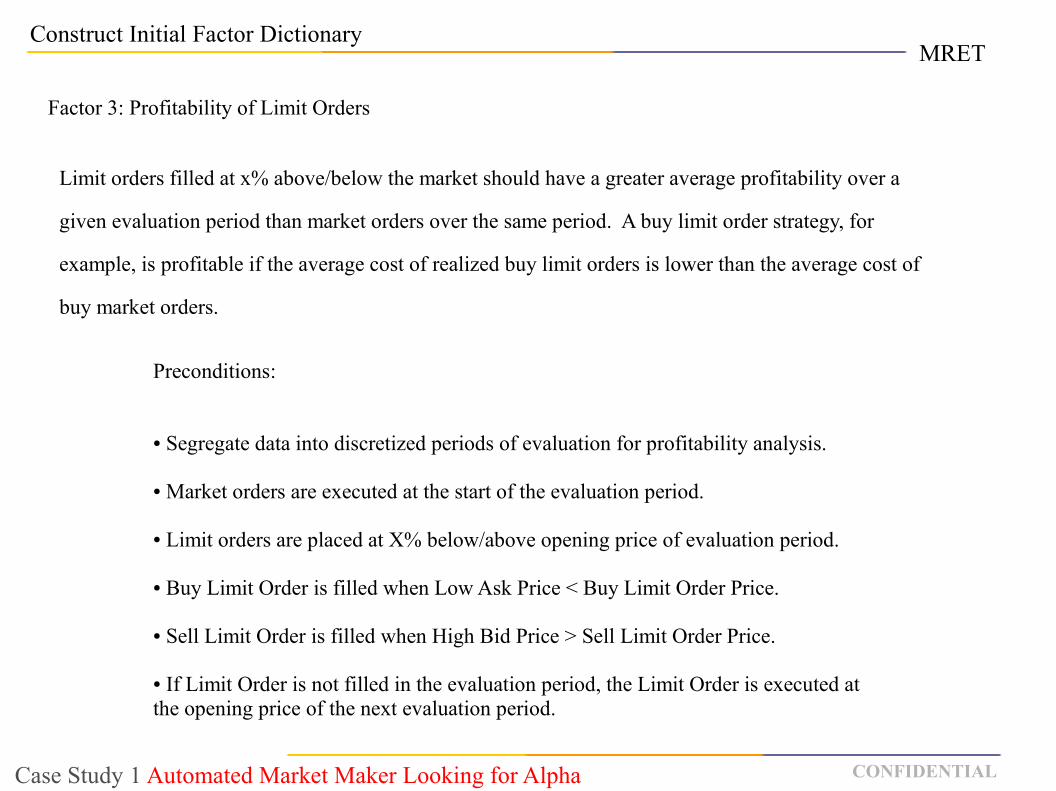

Limit orders filled at x% above/below the market should have a greater average profitability over a

given evaluation period than market orders over the same period. A buy limit order strategy, for

example, is profitable if the average cost of realized buy limit orders is lower than the average cost of

buy market orders.

Factor 3: Profitability of Limit Orders

Preconditions:

● Segregate data into discretized periods of evaluation for profitability analysis.

● Market orders are executed at the start of the evaluation period.

● Limit orders are placed at X% below/above opening price of evaluation period.

● Buy Limit Order is filled when Low Ask Price < Buy Limit Order Price.

● Sell Limit Order is filled when High Bid Price > Sell Limit Order Price.

● If Limit Order is not filled in the evaluation period, the Limit Order is executed at the opening price of the next evaluation period.

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 3: Profitability of Limit Orders

Definition:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Take evaluation period’s average price range divided by an evaluation

period’s standard deviation of average price range and adjust by square root of number of

observations in a year. Good strategies at the highest frequency have the highest risk

adjusted profitability and yield a double digit Sharpe Ratio. This can be used as a

comparative benchmark.

Factor 4: Market Opportunity (Maximum Possible Annualized Sharpe Ratio)

Compare maximum Sharpe Ratio of strategy with a strategy of perfect predictability over various evaluation periods. See next page. . .

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 4: Market Opportunity (Maximum Possible Annualized Sharpe Ratio)

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 5: Market Impact and Illiquidity Ratio

Higher illiquidity correlates to higher expected returns and greater market inefficiency. Below, λt is

proxy for market impact.

Definition:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 6: Price Sensitivity to Block Transactions

The smaller the sensitivity to transaction size, represented by λ, the larger the market’s capacity

to absorb market orders at the current market price.

Definition:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Cost of instantaneous reversal in price for a given order quantity relates to profitability of market orders

submitted by uninformed traders over a given evaluation period. This factor is estimated using a tightness

measure of the bid-ask spread. Limit orders tend to fare better in lower liquidity environments and this can be

assessed by the average cost of instantaneous reversal.

Factor 7: Average Cost of Instantaneous Reversal Over Various Evaluation Periods

Definition:

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Definition:

Factor 8: Market Inefficiency -Non-Parametric Runs (By Broker ID, Time of Day, Trade Size)

Sequential runs of trades with the same sign represent inefficiency and thus an alpha generation trading

opportunity. Based on factor 2, if the desired trading frequency (that dictates target Sharpe Ratio) is 1 second,

then a run is a consecutive set of price movements with the same sign that occurs at 1 second intervals. P4

would equate to the 4th run of positive sequential price movements, for example. N7 is the 7th run of negative

sequential price movements.

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 8: Market Inefficiency -Non-Parametric Runs (By Broker ID, Time of Day, Trade Size)

Definition Continued

Test for Randomness

Standard Deviation of Runs

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Runs at the specified evaluation interval are predictable with a 95% statistical

confidence if the number of runs is at least 1.654 standard deviations away from the

mean x bar.

The number of runs is not random if the two tailed test based on the Z score is

rejected.

_

Z = (|u – x| - 0.5)/s

Thus, the randomness of runs is rejected whenever the Z score is > 1.654.

Test for Statistical Non-Randomness

Definition Continued

Factor 8: Market Inefficiency -Non-Parametric Runs (By Broker ID, Time of Day, Trade Size)

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 8: Market Inefficiency -Non-Parametric Runs (By Broker ID, Time of Day, Trade Size)

Output Results Table Example

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 9: Bid-Ask Spread Estimates

Bid-Ask spreads vary according to intraday seasonality and volatility patterns and can be a

proxy for liquidity. Spreads widen during periods of market instability and contract when

markets are calm. Wider spreads represent decreased liquidity, increased volatility and

increased costs to traders and wider spreads decrease traders’ overall profitability. The

profitability of market orders should increase from the perspective of liquidity providing market

makers as increased volatility and decreased liquidity present an opportunity to profit from

uninformed participants. Spreads can be estimated by looking at the price of an asset at a given

time represented by pt that equals some fundamental value plus half of the bid ask spread, s.

The fundamental value is increased by s if the subsequent market order is a buy and the

fundamental value is decreased by s if the subsequent market order is a sell.

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 9: Bid-Ask Spread Estimates

Definition (Roll, 1984):

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 10: Effective Bid-Ask Spread

Definition

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

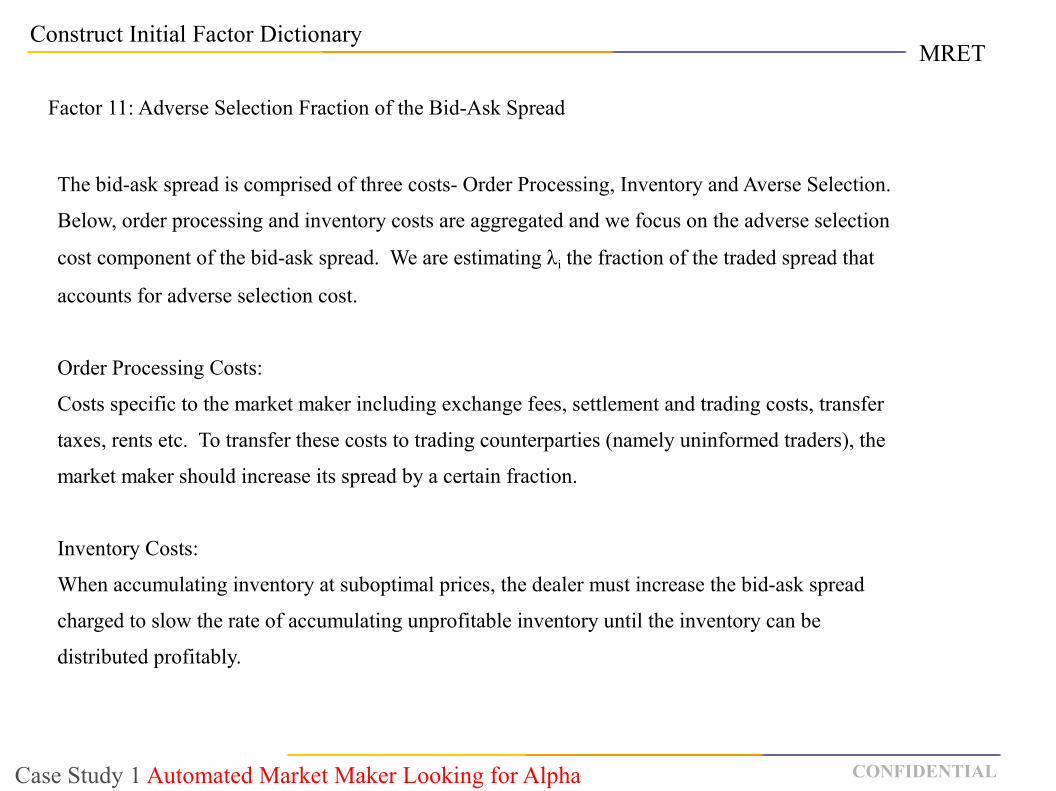

Factor 11: Adverse Selection Fraction of the Bid-Ask Spread

The bid-ask spread is comprised of three costs- Order Processing, Inventory and Averse Selection.

Below, order processing and inventory costs are aggregated and we focus on the adverse selection

cost component of the bid-ask spread. We are estimating λi the fraction of the traded spread that

accounts for adverse selection cost.

Order Processing Costs:

Costs specific to the market maker including exchange fees, settlement and trading costs, transfer

taxes, rents etc. To transfer these costs to trading counterparties (namely uninformed traders), the

market maker should increase its spread by a certain fraction.

Inventory Costs:

When accumulating inventory at suboptimal prices, the dealer must increase the bid-ask spread

charged to slow the rate of accumulating unprofitable inventory until the inventory can be

distributed profitably.

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Adverse Selection Cost:

The market maker always loses to better informed traders possessing asymmetric information. The dealer needs

to hedge out the risk associated with trading against informed traders by appropriately increasing the spread it

charges to all counter-parties so as to be compensated for incurring adverse selection risk as the primary cost of

providing liquidity. The primary tradeoff that the dealer faces that determines its profitability (beating

Gambler’s Ruin and achieving a net positive expectancy per share) is that it must earn more from uninformed

traders than it loses to informed traders.

Factor 11: Adverse Selection Fraction of the Bid-Ask Spread

Definition

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 12: Adverse Selection Fraction of the Bid-Ask Spread

The vector auto-regressive model measures presence of asymmetric information and estimates

information – based impact given by λ.

Definition

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Factor 13: Duration

Estimate the factors that affect the duration between sequential ticks as the interval between quote

arrivals contains valuable information. Analyze both quote and trade arrival patterns. Such arrivals

follow a Poisson process. Duration models suggest that the shorter the duration between trades the

higher the likelihood for pending good news. On the contrary, the longer the duration between trades,

the higher the likelihood for bad news. . .

Construct Initial Factor Dictionary

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Pseudo-Coding

Pseudo-Coding is a collaborative Process between MRET and the Client.

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Pseudo-Coding

Pseudo-Coding is a collaborative Process between MRET and the Client.

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Code Factors

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Code Factors

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Code Factors

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Code Factors

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Code Factors

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Code Factors

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

To-Dos

<Clean Sample Data> Completed

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

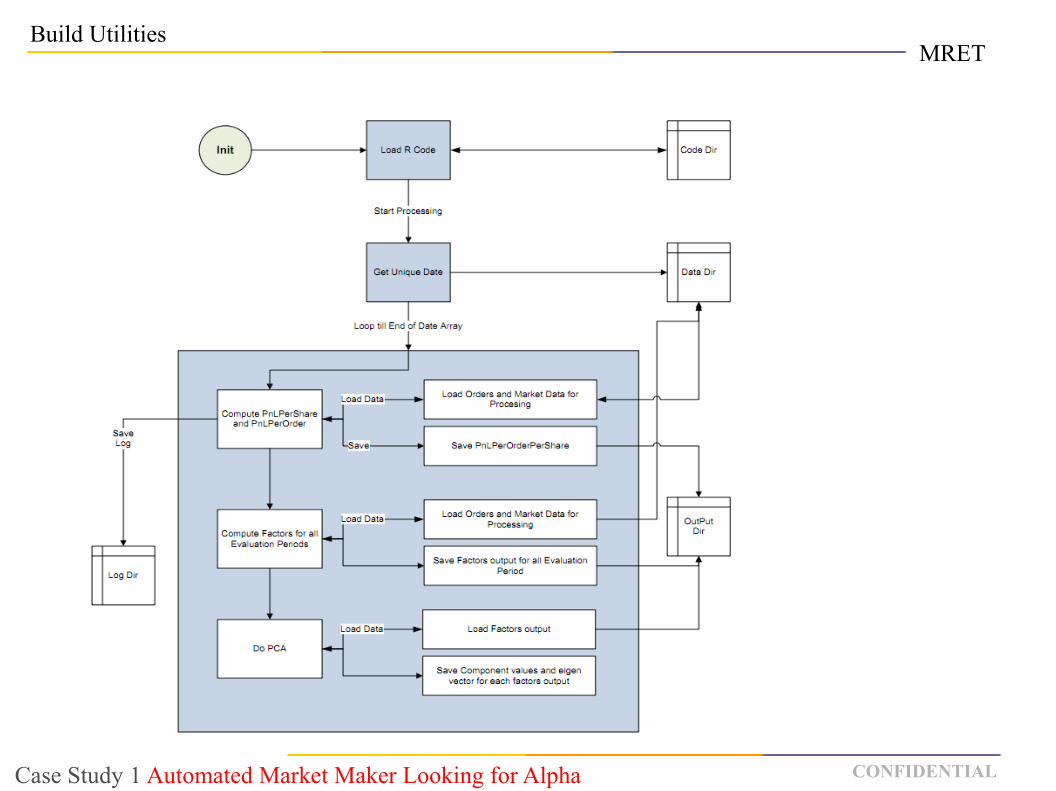

Build Utilities

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Output Sample Factor Values for Evaluation Period 10 Bars

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Run Principal Component Analysis (PCA)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Run Principal Component Analysis (PCA)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Run Principal Component Analysis (PCA)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report PCA Output for Factors (Sample for Evaluation Period 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Run Multi-Linear Regression

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report MLR Output for Principal Factors (Sample 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report MLR Output for Principal Factors (Sample 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report MLR Output for Principal Factors (Sample 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report MLR Output for Principal Factors (Sample 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report MLR Output for Principal Factors (Sample 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report MLR Output for Principal Factors (Sample 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report MLR Output for Principal Factors (Sample 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Report MLR Output for Principal Factors (Sample 10 Bars)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Data Fitting Update

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Status Updates Maintain Transparency & Proper Project Direction

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Classification (Sensitivity Analysis)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

Classification (Sensitivity Analysis)

MRET

CONFIDENTIALCase Study 1 Automated Market Maker Looking for Alpha

RESEARCH CONTINUES...

MRET

CONFIDENTIAL

CASE STUDY 1: Automated Market Maker Looking for Alpha

CASE STUDY 2: Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

CASE STUDY 3: Back-Office Automation & Diagnostic Tools

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

What can we do for this Hedge Fund?We will engineer an automated trading system according to the specifications of the client and provide ongoing support for the optimization of both the strategy and the automated trading system performance.

Problem OverviewAutomate an oil futures arbitrage strategy to generate entry and exit points and hedge orders across multiple exchanges.

MRET

CONFIDENTIAL

Research the Dealer Problem

Case Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Research Trading Concept

Code

Explore Client Objective& Gather Requirements

Create a Development Plan

Pseudo-Code

Implementation

Data Pre-Processing

Logging & Order Audit Trail

Provide PreliminarySchedule

Revise Code

Back Test

Probationary Testing

User Acceptance, Documentation

& Ongoing Work

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Explore Client Objectives & Requirements

Replace Manual Trading performed on the CME/NYMEX Exchanges.

Initial Requirements

● Exchange & Future Contract Information

● Offsetting Differential

● Margin Constraints

● Volume (Trade, Show)

● Technical (XTAPI, C#, .NET (Specified by Client in this Case))

● Noise Alerts

● User Documentation

● *C# Visual .NET for this initial strategy prototype as specified by Client.

●Organize the Manual Trading System's Rules●Automate Rules into Code●Execute Strategy

*MRET is Platform and Environment Neutral

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Create a Development Plan

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Create a Development Plan

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

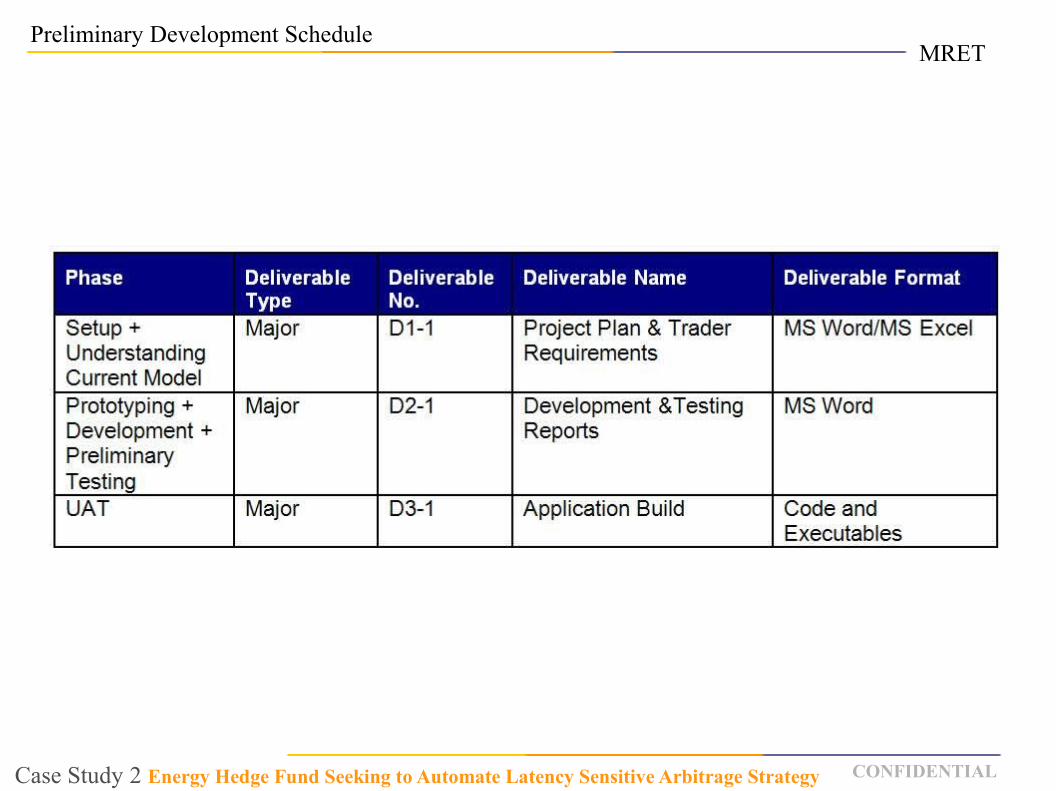

Preliminary Development Schedule

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

● A collaborative process

● Conceptualize and Formulate the Trading Strategy such that everyone is on the same page.

● Specify trading rule.

Develop Pseudo-Code

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Code Snippets

Code

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Code Revision

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Data Pre-Processing & Logging

Data Pre-Processing

● Liquidity Test/Sufficient Market Depth.

● Liquidity Data Set.

● Requisite Order Flags.

Logging & Order Audit Trail

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Back Test Results

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Probationary Testing, Identify Errors, Debug and Re-Test

Overview

● Partial Fill.

Breakdown

● Fix the issue of totalQuantity and now strategy stops as soon as we reach total quantity.

● Unit testing of partialFill.

● Unit testing of totalQuantity.

Next Plan

● Unit Testing of Max Position.

● Questions.

● NaN.

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

Probationary Testing, Identify Errors, Debug and Re-Test

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

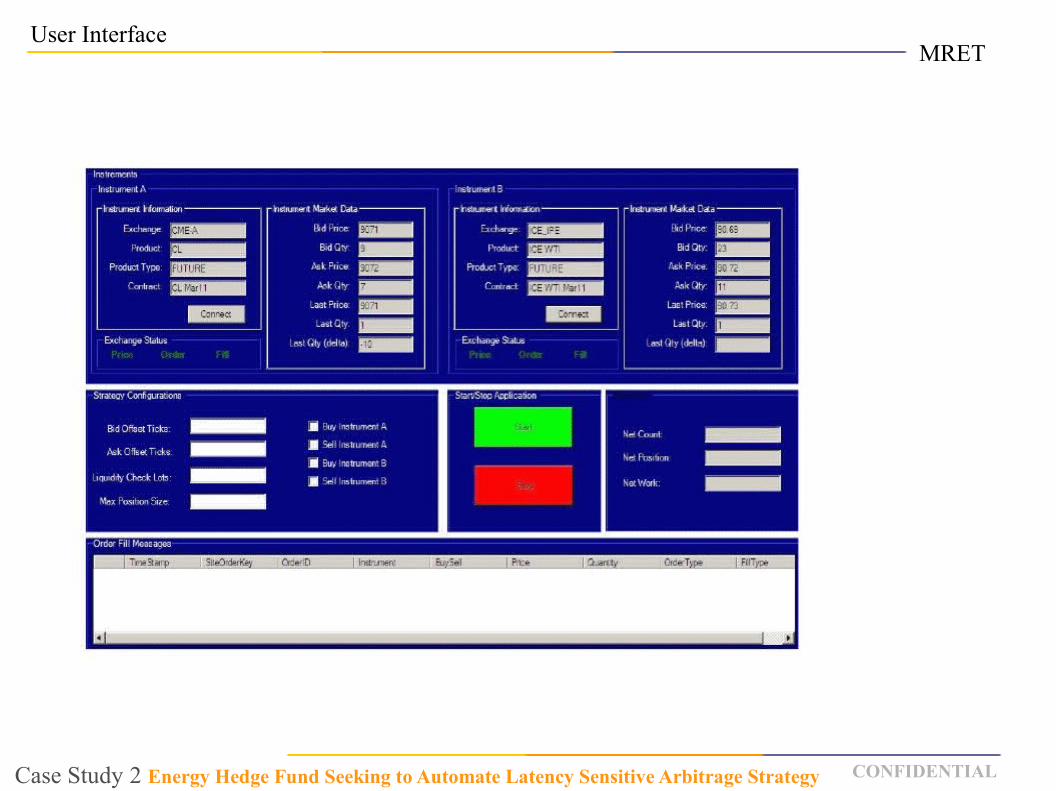

User Interface

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

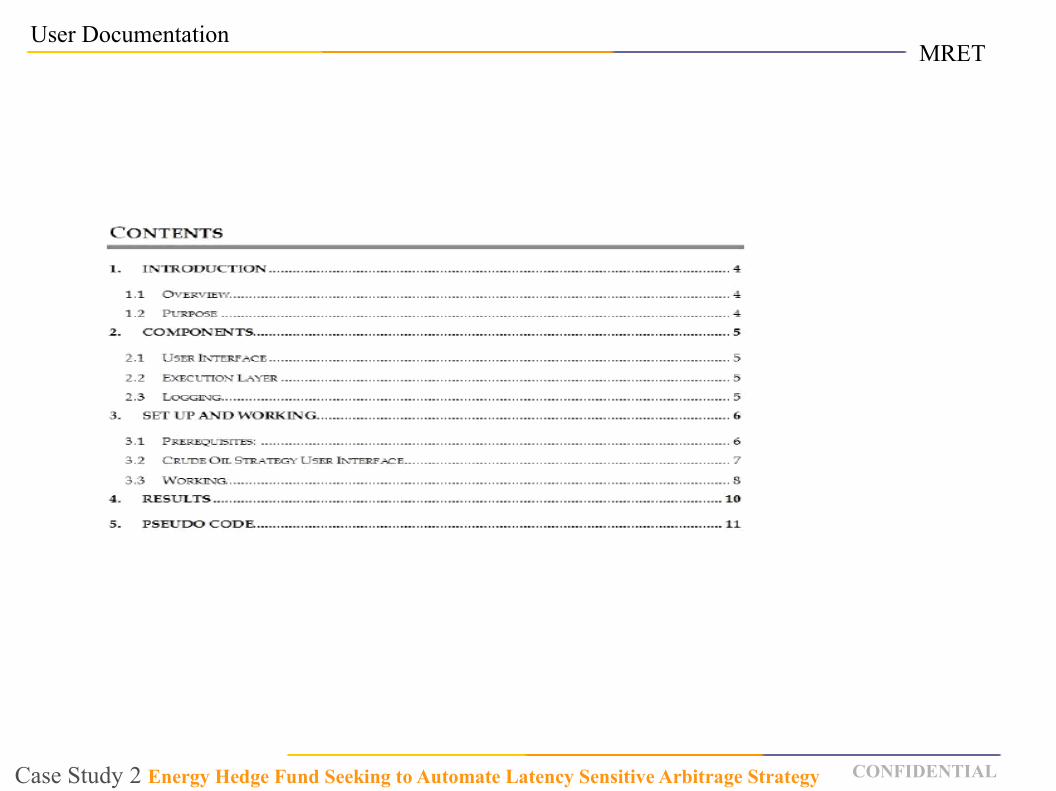

User Documentation

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

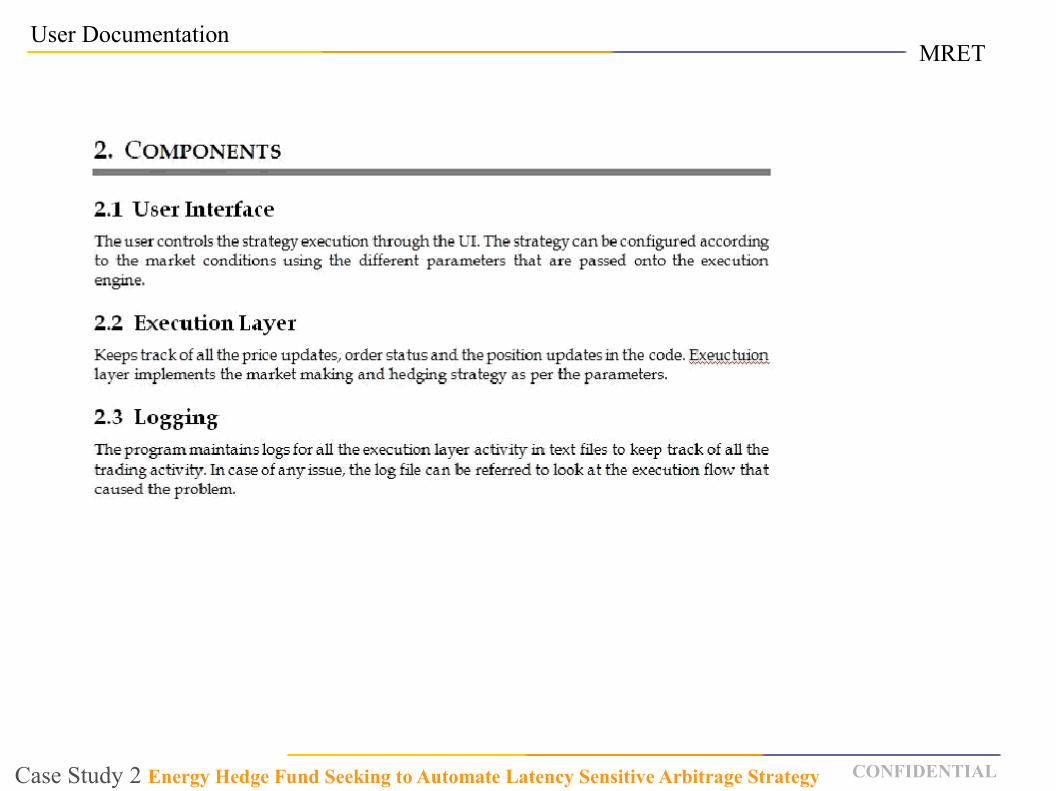

User Documentation

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

User Documentation

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

User Documentation

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

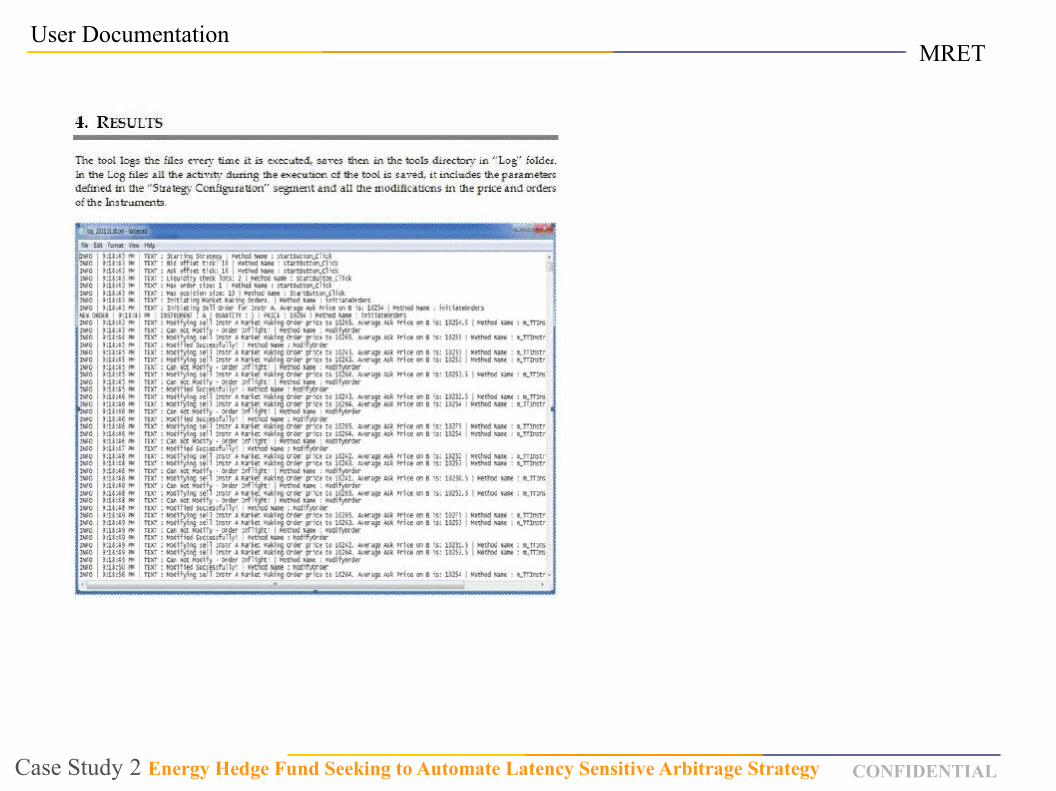

User Documentation

MRET

CONFIDENTIALCase Study 2 Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

User Acceptance Testing & Ongoing Work...

MRET

CASE STUDY 1: Automated Market Maker Looking for Alpha

CASE STUDY 2: Energy Hedge Fund Seeking to Automate Latency Sensitive Arbitrage Strategy

CASE STUDY 3: Back-Office Automation & Infrastructure Products for a Broker-Dealer

CONFIDENTIAL

MRET

CONFIDENTIAL

Problem Overview1) Broker/Dealer needs to Stress Test Automated Trading Infrastructure.

2) A Broker/Dealer needs to build out its back-office compliance and risk management of its proprietary traders due to increased regulation.

What can we do for this Broker/Dealer?

We can build customized tools to stress test its automated trading system and develop products for its back-office compliance and risk management needs.

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIALCase Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

Product Research

Understanding Existing Back-Office Processes

Understanding Key Participants

Understanding How Components Interact

Develop Web Portal and/orDesktop Applications

Understanding SOR, OMS & Compliance Systems

END PRODUCTS

Implementation

Design Relational Schema

Compliance/Risk Tool Reconciliation Engine

Order Spammer

Draft Requirements

Reconciliation Tool

MRET

CONFIDENTIAL

● A Diagnostic Tool for Reconciling a Smart Order Routing System with an Order Management System.

● A Tool that Duplicates Order Flow in Real Time to Two Separate Processing Engines.

● A Component that Generates Log Files for Each Order Flow.

● An Output Compares Results to Identify Mismatches and Possible Erroneous Trades.

Reconciliation Engine

The Reconciliation Engine is part of an Infrastructure Ramp-Up for High Freq. Trading, including:

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Reconciliation Engine -Order Spammer

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Reconciliation Engine -Order Spammer Documentation

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Reconciliation Engine -Order Spammer Documentation

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Reconciliation Engine -Reconciliation Tool

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

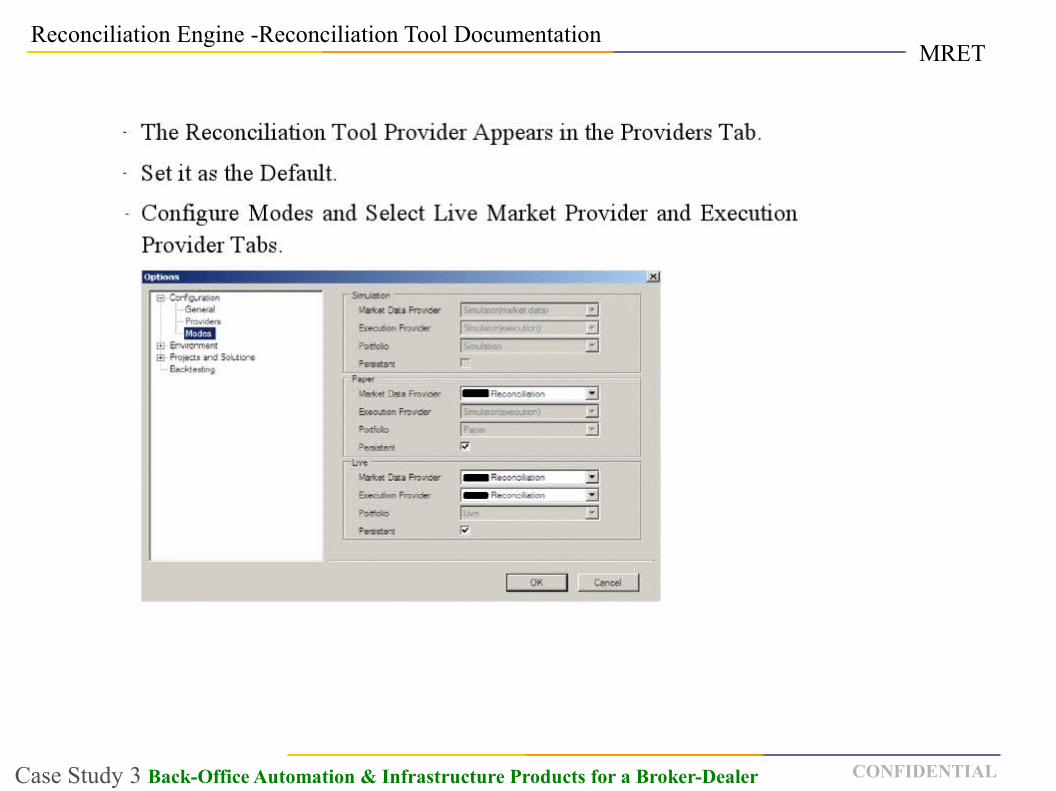

Reconciliation Engine -Reconciliation Tool Documentation

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Reconciliation Engine -Reconciliation Tool Documentation

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Reconciliation Engine -Reconciliation Tool Documentation

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Reconciliation Engine -Reconciliation Tool Documentation

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Reconciliation Engine -Reconciliation Tool Documentation

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Risk & Compliance UI

● Create Trader Profiles.

● Manage Buying Power.

● Manage Max Position Size.

● Manage Max Order Size.

● Set Thresholds and Alerts for Traders as Well as Firm-Wide.

● Manage Short-Sales and Hard to Borrow List.

● Manage Trader Fee & Rate Schedules.

Manage Trader Risk & Compliance Profile

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MRET

CONFIDENTIAL

Risk & Compliance UI

Case Study 3 Back-Office Automation & Infrastructure Products for a Broker-Dealer

MICROSTRUCTURE RESEARCH & ENGINEERING TECHNOLOGIES, LLC

CASE STUDIESInnovative Solutions for Complex Quantitative Problems

44 Wall Street, 20th FloorNew York, NY 10005

contact@microstructure-research.comwww.microstructure-research.com

646.389.3856