mpos - disruption or "only" evolution

TRANSCRIPT

1

Karl Illing, Product Management, ConCardis

Berlin, 04.11.2015

Conference³

WiWo

mPOS

Disruption or

„Only“ Evolution?

2

About ConCardis

German payment provider for cashles s payments with international reach

Principal Member of MasterCard and Visa

Acquirer for Diners, JCB, UP, Amex

Payment Institute as per Zahlungsdiensteaufsichtsgesetz (ZAG)

Headquartered in Eschborn near Frankfurt am Main

400.000 Points of acceptance

331 million transactions

€ 35 billion transaction volume

€ 450 million revenue

2

39 % Private Banken

39 % Sparkassen

Finanzgruppe

20 % Genossenschaftliche

Finanzgruppe

2 % Öffentliche

Banken

A shared enterprise of the German

banks

Stand 31.12.2014

3

From Acquirer to Payment Service Provider –

30 years of experience

PSP

Service

1982

1997

2003

2004

2009 2012 2013

2014

ConCardis

OptiPay

2015

Commercial

Network

Operator

Acquiring

Acquiring

E-Commerce POS-Terminals

mPOS

4

What is „mPOS“?

Basic definition of mPOS (mobile Point of Sale)

Merchant-side payment device connected to a smartphone or

tablet

Can vary in

Form factor (Dongle, Bluetooth reader, 2-in-1 device, …)

Platform (iOS, Android, ...)

Software Applications (Payment App only, cash register, …)

Not to be confused with

Mobile Payment in the narrow sense (involving buyer-side

mobile device)

Unterschiedliche mPOS-Formfaktoren

5

10 Mio. $

series B

67 Mio. $

series D

150 Mio. $

series E

The market dynamics are impressive...

Millions are invested in mPOS „start-

ups“…

60 Mio. $

series D

Selected rounds of financing in the last 12 months

… and new players enter the market every

month

Source: PYMNTS.com

6

…European market penetration lags behind

expectations

“46% of overall POS in 2019”

(ABI Research, May 2014)

“mPOS (mobile point of sale) usage by

small businesses (SMEs) in Europe will

take off dramatically in 2014.”

(VISA, May 2014)

High expectations… …and sober reality

Source: First Annapolis

7

Still: mPOS is a global phenomenon

First truly global payment innovation

mPOS players are active throughout the

world

The largest volume can be found outside of

Europe

Registrations in the Mastercard mPOS Program

Top 5 mPOS countries by volume

Source: Mastercard

8

Three target segments for mPOS with very

different characteristics and use cases

Micromerchants SME Enterprise

Re

ve

nu

e p

er

me

rch

an

t

Number of merchants (cumulative)

9

Micromerchants – accepting cards for the

first time

10

ConCardis OptiPay, launched 2014, has been

the first NFC mPOS solution in Germany

11

ConCardis OptiPay emphasizes maximum

simplicity and transparency

Transparent pricing model

Simple transaction fee

No running costs

No fixed contract duration

Payment app for iOS and Android

Mastercard, VISA, Maestro, VPay and Amex

Contactless payments (including Apple Pay and

Android Pay)

Radically simplifying the proposition „card acceptance“

12

The mPOS „package“ (device and pricing)

as long-tail solution vs traditional terminals

Light and mobile

Not as rigid

Low purchase price

No fixed contract period

Potentially higher transaction

feds

More than one device

(Smartphone/Tablet, Card

Reader, Drucker)

Robust, for heavy use

Limited mobility

High purchase price or rent

Multi-year contract period

Potentially lower transactions

fees

All-in-one

mPOS-Terminal TraditionalTerminal

13

Small businesses in Germany are more

skeptical than elsewhere

Results of an mPOS poll by VISA Europe in 2014

Source: VISA Europe

Likelihood of using

an mPOS solution

Definitely

Probably

Not sure

Probably not

Definitely not

Changing preconceptions (before and

after presenting the solution)

14

Example of a photographer

Photographer

Often on the road

Few, high-value

transactions

15

Example of a market seller

Market seller

Sales in a mobile setting

Only used on certain

days

16

Conclusion – mPOS for micromerchants

mPOS simplifies card acceptance regarding

hardware and pricing

There are clear pros and cons compared to

traditional terminals

Even though German micromerchants are

still relatively sceptical…

…mPOS for the first time renders card

acceptance economically viable for them

Disruptive potential

For merchants: medium

For providers: high

17

To be relevant for larger customers, mPOS

needs to go beyond pure payment

Micromerchants SME Enterprise

Um

sa

tz p

ro H

än

dle

r

Anzahl Händler

Card

acceptance as

a differentiator

Nice to

have

Should

have

Must

have

18

SME – integrated card payment and „big

retail“ functionality

19

Orderbird Payment by ConCardis: seamless

card acceptance with the orderbird POS

Card reader connected via BT /

Wifi to iPad / iPod

Fully integrated in the POS

(payment, refunds, invoice)

Integrated payment leads to a

much higher share of orderbird

merchants accepting cards

We showed the first Apple Pay

transaction in Germany using an

integrated payment system

20

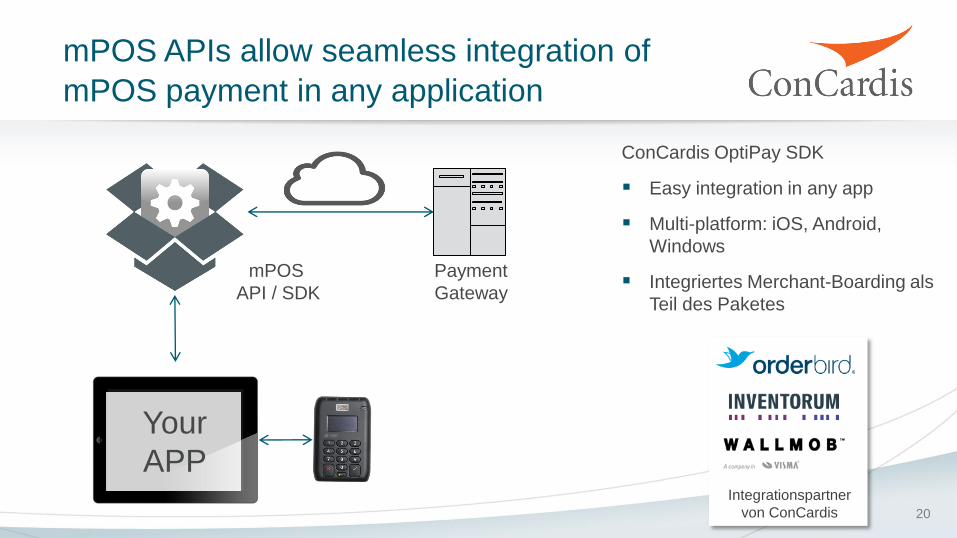

mPOS APIs allow seamless integration of

mPOS payment in any application

ConCardis OptiPay SDK

Easy integration in any app

Multi-platform: iOS, Android,

Windows

Integriertes Merchant-Boarding als

Teil des Paketes

mPOS

API / SDK

Payment

Gateway

Your

APP Integrationspartner

von ConCardis

21

„mPOS“ as a scalable hub for POS services,

backend processes, and business intelligence

In Store

Cloud

APIs

Inventory management

E-Commerce

Loyalty

…

Payment

Mobile POS Devices

SaaS-Server

Additional services

WWW

Shopper-WiFi

22

Conclusion – mPOS for SME

mPOS as stand-alone payment lacks

relevance for SMEs

True value comes from integrated

payment as part of mobile POS systems

Mobile/tablet POS systems such as

orderbird give SMEs access to „big retail“

functionalities, greatly improving

processes and giving a new level of

control over their business

Disruptive potential

High for both merchants and

providers

23

Enterprise – from replacement terminal to

omnichannel system

24

Value added of mPOS terminal stem from

various „small“ use cases

Use cases of mPOS terminals in „Big Retail“:

However, the complete use case (not only the payment part) needs to be

considered

Queue Busting Pop-up Stores

Replacement

Terminal

Assisted

Shopping

Street Sale

25

mPOS as omnichannel enabler – example

of a sports retailer in Denmark

Implementation of the Wallmob iPad POS

Omnichannel

Seamless integration of POS and e-commerce

In-store payment – even for online deliveries

Mobile card acceptance

Queue busting

Street sale

Pop-up shop

Improved shopping experience

Assisted shopping

Quelle: Wallmob

26

Conclusion – mPOS for enterprise

mPOS terminals can add value for large

retailers through various use cases

When implementing mPOS, the end-to-end

customer experience needs to be considered

Holistic implementations can change the way

of doing business, e.g. through omnichannel

commerce

Disruptive potential

Low for stand-alone payment

High for holistic solutions

27

Summary

mPOS market dynamics are high, the volume seems to be lagging

Micromerchants: mPOS makes card acceptance possible for

everyone

Small and medium businesses: It‘s about more than payment –

scalable platforms and „big retail“ functionality

Enterprise: Depeding on the implementation mPOS can add value

on a small level or change the entire business

“There will always be a need for traditional POS solutions

driven by large fixed lane checkout applications, but equally

there will be merchants looking at simpler cost-effective

solutions with added value services.”

(ABI Research, 2014)

28

www.concardis.com www.concardis.com

ConCardis GmbH

Karl Illing

Helfmann-Park 7

65760 Eschborn

Thank you for your attention!