mortgage protection - consolidated underwriters, inc. · mortgage protection insurance. ......

TRANSCRIPT

Mortgage ProtectionI N S U R A N C E

Mortgage Protection Sales Toolkitf o R P R o d U C E R S

This toolkit is a resource for you to use in your sales efforts in the area of mortgage protection.

To fully profit from it:

Have it handy after appointments so that you can add to it notes about how you closed the sale- or why you didn’t.

Keep it by your phone so that you can add to it notes on key words that you used to set the appointment.

This toolkit contains proven examples of what has worked for others, but it also contains space for you to add what works for you. Personalizing the toolkit and adding your own notes will aid you in the process of developing sales strategies to be successful yourself, and to develop and train a successful team. Good luck!

What’s Inside this Kit? Phone Sales Script Handling Objections Client Meeting Guide Prospecting Postcards Product Guides

For Questions, contact Consolidated Underwriters Inc. at 800-221-8011

A ToTAl PlATForM For SUCCeSS

Your Personal Mortgage Protection

Sales Toolkit

Mortgage ProtectionI N S U R A N C E

1. “Who is this?” I’m with the Mortgage Protection Department of {company name}. What we do {Client Name}, is provide the mortgage protection plan that will pay your loan off if you die, can give you money if you get sick, and can return all of your premiums if you live. It will only take about 20 minutes to go over all of your available benefits and answer all of your questions. I can meet with you at {give times again}. What time would work best for you?

2. “What is this?” {Mr./Mrs. Client}, this is the mortgage protection plan that will pay your loan off if you die, can give you money if you get sick, and can return all of your premiums if you live. It will only take about 20 minutes to go over all of your available benefits and answer all of your questions. {Agent Name} can meet with you at {give times again}. What time would work best for you?

3. “Are you with the Bank?” No, I am with the Mortgage Protection Department of {company name}. What we do is provide Mortgage Protection plans for all lenders. I will be in your area tomorrow and can answer all of your questions about your available benefits. Again, it only takes about 20 minutes. I have {repeat times again} available tomorrow. What time would work best for you?

4. “How much does this cost?” Well {Client Name}, I can’t quote you the price because there are plans available to fit just about any budget. I will be able to answer all of your questions as we review these options that best fit your needs. Once again, it only takes about 20 minutes. I have {repeat times again} available tomorrow. Does time {x or y} work best for you?

The assumptive sale works well in situations like this. Present your clients the opportunity to answer Yes/No questions and they will certainly say NO!

QUeSTIonS & AnSWerS

Here are some frequently asked questions your prospective clients may ask. Use this as a guide during your next call to help answer the questions standing between you and an actual appointment.

Mortgage ProtectionI N S U R A N C E

Mortgage ProtectionI N S U R A N C E

Client Meeting GuideMake sure to use the following steps to create a successful meeting and to close the deal.

Setting the Client at Ease

I Love You / Tie Down

Yourself / Your Company

Benefits/Features

Think About It

Cost / Filling Out the Application

Your demeanor should always be that of a mortgage protection specialist. Be sure that you are dressed appropriately…very sharp business casual (iron your shirt and pants so that they’re crispy). Greet the client with a warm and friendly greeting. Comment on anything that you can show sincere interest in…home, cars, neighborhood, pictures, furniture. Then, as soon as you can, say, “I’ve done my homework and have just what we talked about for your family. This will go quickly if we could sit at your kitchen table.”

Mrs. Smith, before we get started, I’d like to ask you to do something for me…but first, let me catch you up to speed on what your husband and I discussed on the phone. When I called him about the letter that he sent in for mortgage protection he told me that it was urgent and important to him because ___<whatever he said on the phone>____. Mr. Smith told me that if I could find a company that would protect his families specific needs, and fit it within his budget, he wanted to get it in place immediately so that you are protected right away. Is it fair to say that if Mr. Smith passes away that he won’t be able to spend any of this money? This is something that he does for you, his family, not for himself. Now, I know that men don’t always discuss their feelings as much as some women would like them to but, by making sure that you and your family are taken care of even after he’s gone, he’s telling you how much he loves you. Now, Mr. Smith, has anything changed since we spoke on the phone?

Take about 3 minutes to tell them something about yourself. Try to mirror them, their fears, and their concerns. Talk about how you feel and how your wife feels to know that you’re protected in the event of unexpected tragedy. Take about 3 minutes to tell them about the company that you’re showing them. Convey to them it’s financial strength, longevity, and commitment.

1. Choice of Beneficiary: With the plan that you choose, you decide who receives the proceeds from the program in the event of death. At such time, the beneficiary has several options. Three of which are:

Pay off the mortgage in one lump sum;

Invest the benefit and continue to make payments;

Use the proceeds to relocate to a different home.

2. Thirty Year Term: Imperative in order to protect your family for the full term of the mortgage. Many plans will only cover 20 years.

3. Portable: If you sell your home and buy another, or refinance your

I love You / Tie Down

Yourself/YourCompany

Benefits/Features

Setting the Client At-ease

Client Meeting GuideMortgage Protection

I N S U R A N C E

present home, this plan can simply move with you to continue to protect your next mortgage. This means regardless of how many times you move, you will never need to qualify for another plan or risk losing the one that you have.

4. Death Benefit Remains Level: The death benefit remains level for the length of your mortgage. With most plans, benefits decrease each year while the premium remains the same.

5. Unemployment: After one month of unemployment the premium will be paid each month for 6 months.

6. No medical exam required: In most cases, this company does not require a medical examination for healthy rates. Includes tobacco and non-tobacco.

7. Free Accidental Death Benefit Rider: The free ADB Rider benefit will pay an additional death benefit of up to 50% of the face amount in the event of certain accident-related deaths of the insured.

8. 24 Hour Coverage-Accident or Sickness: Unlike many mortgage protection plans, this program will pay benefits regardless of whether the death/disability occurs from accident or sickness

9. Money Back: You have the option of receiving a refund on all the premiums that were paid by you into this program if you live.

10. Disability: This feature will pay your mortgage payments if you become disabled for a period of 2 years after a 90-day elimination period. This protection covers disability under the “any occupation” definition.

11. Waiver of Premium: Another disability feature, this option will pay your premium, for as long as you are disabled, after six months of disability, with a refund for the premium payments for the first six months.

Now, Mr. and Mrs. Smith, I’ve gone over everything that I need to cover with you except for the numbers. Before we go through them I’d like for you to do one more thing for me…I’d like for you to promise me that you’re not going to tell me that you need to think about it…(pause and smile)…now let me tell you why. I’ve found that a “think about it” means one of two things…either you still have some questions about the benefits as I have explained them or the plan that you want doesn’t fit within your budget. So, rather than telling me that you need to think about it…ask me about any of the benefits that you have questions about or if we need to work out a cost issue. Does that sound fair enough?

Think About It

Client Meeting GuideMortgage Protection

I N S U R A N C E

Pull out the plans that you selected to meet their needs and explain each one to them. Immediately pull out the application while they are looking at the numbers and start filling it in. You should have their name and address on the lead card. Ask them for info to fill in the blanks while they pick a plan. If they haven’t chosen a plan by the time you reach that line on the app, just skip it and keep going. If they still haven’t chosen by the time you’ve completed the app just ask, “which of these plans best fits your needs?”

Client Meeting GuideMortgage Protection

I N S U R A N C E

Cost/Filling out the Application

Mortgage ProtectionI N S U R A N C E

Phone Sales ScriptMake sure you guide prospects in helping you to achieve three critical steps in the process of mortgage protection prospecting while on the phone.

Discovering the Importance/Urgency

Setting the Appointment

The Tie Down

Hello. _client_ ? This is __you__ calling in reference to your mortgage originated with _____________ for $_____________. Do you remember sending in a notice to us regarding mortgage protection on that loan? You filled in your name, birth date, height, weight, and phone numbers on it?

I’ve been assigned to assist you and your lender in getting this taken care of…I just need just a couple of minutes to confirm some of the information you filled in and get a couple more details from you so that I can process this request. Is this a good time?

Now, this is a new style mortgage protection program that has the best living benefits in the industry such as making your mortgage payment for you if you become disabled or returning every penny of premium at the end of the term if you survive. Before I confirm the information you sent us I need to ask a few questions to qualify you…

Do both you and your spouse contribute to the monthly mortgage?

If one of you passed away would the other be able to maintain their standard of living and the mortgage payment without a struggle?

If one of you became disabled, could you keep your mortgage payment going?

Is the disability benefit or getting all your money back at the end of the term important to you?

__client__, some people have wanted this protection because they just lost a friend or loved one and they saw what the family went through after that, or they just feel a responsibility to make sure their family is taken care of, even when they’re gone.

Tell me, __client__, why is this important to you?

Now, _______ the reason I’ve asked you these questions is because we put programs together, we don’t use just one insurance company, we find out what you want and need and research the market to find the best program available to fit your specific situation.

Now I’ve got your birth date listed as …(verify info)

Are either of you on any kind of medication for any health conditions (Blood Pressure, Cholesterol or Diabetes)? What specifically are you taking and what dosage level?

Sample Phone Script

Phone Sales ScriptMortgage Protection

I N S U R A N C E

In the last 10 years, have either one of you had any major operations or diseases (Heart problems or cancer)? When was the operation? Still on medication?

Do either of you have any other major health challenges? Are you currently on disability? What is the nature of the disability? How long have you been on disability? What are you unable to do or perform as far as activities of daily living?

Have you or your spouse had any DUI convictions within the last 5 years?

Now for our disability option which pays your mortgage payment should you or your spouse become disabled: monthly mortgage payment in round numbers (including taxes and insurance, occupation, what company do you work for, how long have you been there, spouse?

Now our records show your mortgage amount to be (mortgage amount)

is that a 30 year loan? (Let them correct you as far as amount and length).

Is that a first mortgage? Are there any 2nd mortgages you want to cover?

_________, if we can find something out there that fits your budget and fits your needs are you ready to put something in place so you can be covered?

The reason that I’m asking is this, we service over a hundred families each week and it’s important to me to be able to spend as much time with you as you need, but I’ve found that it takes me about 17 minutes to go over with you and your spouse the options available to you, and about 15 more minutes to answer any questions you may have and get this taken care of for you, that’s 32 minutes all together. I’ll be in your area on _________, would afternoon, evening, or late evening be better for you? Verify address…

__________, between now and the time that we get together, I need you and your spouse to take a look at your budget and get a ballpark figure on what you can afford to set aside for this protection.

Now let me tell you what’s going to take place when I get there... I’m going to take a few minutes to get you familiar with my company and myself. Then I’m going to go over a few points which I think make us stand head and shoulders above everyone else out there.

Phone Sales ScriptMortgage Protection

I N S U R A N C E

Sample Phone Script

continued

Then, based on the info that you’ve just given me, I am going to explain to you the 3 or 4 best programs available out there to you. I’ll have everything from the Yugo to the Cadillac. I’ll help you select one that best fits your budget and your needs and when you’re comfortable with it price wise and coverage wise, I will fill out a Request for Coverage and we’ll submit that request with a check for the first months premium to get the program started. Is that fair enough?

If I can deliver a product that fits your needs and fits your budget, we’ll be able to do business Thursday night and you’ll be able to write a check for the first months premium?

Now ( Client ), this appointment is for your benefit, not mine. Can you see anything that might come up that would prevent us from meeting on Tuesday at 7:00 PM? Any school functions for the kids? Any games or practices? Any church meetings or classes that you have to attend?

I’ll have several appointments that evening so I may be there 30 minutes early or 30 minutes late, would that be ok?

Now _______, on a scale of 1 to 10 as far as accountability goes, I’m a 10, I’m good for my word. I will not cancel or just not show up. I know that none of us are promised tomorrow and I won’t let your family down.

Phone Sales ScriptMortgage Protection

I N S U R A N C E

Sample Phone Script

continued

Do both you and your spouse contribute to the monthly mortgage?

If one of you passed away would the other be able to maintain their standard of living and the mortgage payment without a struggle?

If one of you became disabled, could you keep your mortgage payment going?

Is the disability benefit or getting all your money back at the end of the term important to you?

__client__, some people have wanted this protection because they just lost a friend or loved one and they saw what the family went through after that, or they just feel a responsibility to make sure their family is taken care of, even when they’re gone.

Tell me, __client__, why is this important to you?

__client__, if we can find something out there that fits your budget and fits your needs are you ready to put something in place so you can be covered?

The reason that I’m asking is this, we service over a hundred families each week and it’s important to me to be able to spend as much time with you as you need, but I’ve found that it takes me about 17 minutes to go over with you and your spouse the options available to you, and about 15 more minutes to answer any questions you may have and get this taken care of for you, that’s 32 minutes all together. I’ll be in your area on _________, would evening, or late evening be better for you? Verify address.

Phone Sales ScriptMortgage Protection

I N S U R A N C E

#1 Discovering Importance/

Urgency

__________, between now and the time that we get together, I need you and your spouse to take a look at your budget and get a ballpark figure on what you can afford to set aside for this protection.

Now let me tell you what’s going to take place when I get there... I’m going to take a few minutes to get you familiar with my company and myself. Then I’m going to go over a few points which I think make us stand head and shoulders above everyone else out there.

Then, based on the info that you’ve just given me, I am going to explain to you the 3 or 4 best programs available out there to you. I’ll have everything from the Yugo to the Cadillac. I’ll help you select one that best fits your budget and your needs and when you’re comfortable with it price wise and coverage wise, I will fill out a Request for Coverage and we’ll submit that request with a check for the first months premium to get the program started. Is that fair enough?

If I can deliver a product that fits your needs and fits your budget, we’ll be able to do business Thursday night and you’ll be able to write a check for the first months premium?

Now ( Client ), this appointment is for your benefit, not mine. Can you see anything that might come up that would prevent us from meeting on Tuesday at 7:00 PM? Any school functions for the kids? Any games or practices? Any church meetings or classes that you have to attend?

I’ll have several appointments that evening so I may be there 30 minutes early or 30 minutes late, would that be ok?

Now _______, on a scale of 1 to 10 as far as accountability goes, I’m a 10, I’m good for my word. I will not cancel or just not show up. I know that none of us are promised tomorrow and I won’t let your family down.

Phone Sales ScriptMortgage Protection

I N S U R A N C E

#2 Tie Down

Mortgage ProtectionI N S U R A N C E

rebuttals to objections I Have Life Insurance At Work

I Already Have Life Insurance

Can You Mail Me the Information

I’m too Busy this Week

We Usually Sleep on It Before We Make Any Major Decisions

We Are Talking to Other Companies Right Now So We Can’t Commit

I Have life Insurance at

Work

I Already Have life Insurance

Can You Mail Me the Information?

I’m Too Busy This Week

I generally suggest that my clients take full advantage of their benefits at work, such as life insurance. That’s because it is usually either free or very inexpensive. However, there is a catch: When you leave, you don’t get to take it with you. Some companies say that you can, and even then, only at attained age. That means that you could be 65 when you leave. A 65 year-old’s rates are a lot higher than a 30 year old. That’s why it is smart to buy a policy independent of work.

That’s great that you already have life insurance, I think every family should. Life insurance is meant to replace the income of the person that is lost but it’s usually only about two to five times their income. That gives your family time to maintain their standard of living temporarily but it doesn’t let them keep the house or even one like it. In fact, without mortgage protection, most families are forced to leave their home in less than 15 months, even when they have life insurance.

To explain our process, part of our agreements with our referral mortgage companies is to meet with their clients face to face first, to visually verify you and your spouses health, and to visually verify the home that we will be protecting and finally to fully explain the program and all the options that you qualify for and the pricing.

I know how you feel, I felt the same way, but this is what I’ve found. We are all busy and truthfully, are you really going to be any less busy next week that you are this week? What if I told you that you won $100,000 and the only way to get the money is to meet with me this week for 32 minutes to fill out the paperwork, how would you accommodate your schedule to meet with me? Isn’t that what we are really doing with this mortgage protection? Can you guarantee your family that you will get up tomorrow morning?

Last month we spoke to a husband and father on the phone that had a need and said that this was important to him, he said that he was too busy to get this taken care of immediately and set an appointment for the next week. We spoke to him on Wednesday…that Friday he had a massive heart attack and passed away before we could protect his family. If he would have known the future he would have made time…it’s not a matter of being too busy, it’s a matter of what’s important to us. _________, you’ve already told me that this is important to you, is it important enough that we can find 32 minutes in the next couple of days to sit down with you and your spouse and get this taken care of?

rebuttals to objectionsMortgage Protection

I N S U R A N C E

We Usually Sleep on It Before We Make Any

Major Decisions

(On the phone call) You know, my wife and I feel the same way, and you’re right, this is a major decision. In fact, making sure that your family can keep the home is in many ways even more important than your decision to buy the home. I know that this has been on your heart lately or you wouldn’t have mailed in the notice…so why don’t you and your wife take some time tonight and take a look at your budget and get a ballpark figure on what you can afford to set aside for this protection and sleep on it. Let’s go ahead and set up a time to get together to give me time to do my part and deliver a program to you that fits your needs and fits your budget.

Great, I can understand wanting to get the best deal for your money. We are a broker company that can represent any number of a thousand different insurance companies’ products. We research constantly the cutting edge products on the market today to find the best products for our clients. You get to benefit from out research.

When you’ve done your shopping, have you found out the following:

Do they offer to return your premium payments after the term is over?

Do they offer a guaranteed premium that will never increase over the life of the term?

Can they offer you a low cost disability program that will pay your mortgage for you if you should become disabled for any reason?

Do they offer a level death benefit and not just the mortgage pay off when they pay the policy off?

Can they give you a choice of a lump sum payment of benefit or a guaranteed monthly income for a specific period of time?

Mrs. Smith, I have access to all of the companies that offer these benefits. Try to keep in mind that while your shopping, you are NOT covered. We find out what you are looking for and shop all of those company to find the one that best fits your needs and your budget. Now, isn’t that what you’re really looking for?

rebuttals to objectionsMortgage Protection

I N S U R A N C E

Mortgage ProtectionI N S U R A N C E

SOLD

What Every Homeowner Needs to Know About Their MortgageYou just bought a home, but is your mortgage protected? Finally, there’s a low-cost way to provide crucial insurance coverage in case something happens to you, or your spouse. Finally, there’s life insurance you can use while still living that will keep you in your house. LEARN MORE…

IMPORTA

NT

Keeping Your Home is Just as Important as

Buying ItBuying a home is a huge

decision, but protecting the mortgage can be just as important. In less than 5

minutes, a few questions, and no worrisome medical exams, you can apply and

qualify for a low-cost mortgage protection policy.

To Learn How You Can Stay in Your Home in case of a Financial

Emergency, call us for an instant quote and a free “Client Guide”

Agent Information

Mortgage ProtectionI N S U R A N C E

An EXCLUSIVE ONLINE TRAINING SERIES that will enable you to answer your clients’ BIGGEST Annuity Objections.

Be Mindful – You just Made an Important Life Changing Decision!

Now how can you be fully covered if something happens to you or your spouse, such as a lost job, illness, disability or death?

Let Me Help You to Select a Life Insurance Policy That’s Right for Your Family Today!

Just buy a home?

Your needs come first! The process is easy, no medical exams necessary.

We will help find the right product that best suits your current and future needs. Every situation is different, so call and schedule an appointment today. We will help you make an appropriate decision.

Making sure that your family can keep your home is in many ways even more important than your decision to buy the home.

Mortgage ProtectionI N S U R A N C E

Let Me Help You Select the Mortgage Protection That’s Right For Your Family Today!

Buying a Home Is an Important Life Changing Decision! Now, how can you be fully covered if something happens to you or your spouse, such as a lost job, illness, death or disability?

Your needs come first! The process is easy, no medical exams necessary.

We will help find the right product that best suits your current and future needs. Every situation is different, so call and schedule an appointment today. We will help you make an appropriate decision.

Making sure that your family can keep your home is in many ways even more important than your decision to buy the home.

Insurer: _____________________________Attn: ___________________________

Dept: _______________________________________________________________

Insured’s name: _______________________Address: ________________________

City: ________________________________State:_______ Zip: ________________

I authorize your company to release the requested information regarding the following policies:

_________________ _________________ ________________

_________________ _________________ ________________

Owner/trustee: _______________________________________________________

Signature: ___________________________ Date: __________________________

Please illustrate the following:

q Current crediting/interest rate w/current annual premium

q 1% below current crediting/interest rate w/current annual premium

q _____% Interest rate w/current annual premium for ____yrs.

q _____% Interest rate w/______ annual premium for ____yrs.

q No additional premiums paid into policy

q Total cost basis/premium paid information

q Current policy summary

q Minimum premium required to keep policy inforce to age ____

q Other _______________________________________________________________ _______________________________________________________________

Please forward illustrations to the Financial Consultant listed below by: q Mail q Fax q Email

c/o ___________________________

Address:____________________ City:________________ State:____

Zip:_______ Phone:_________________ Fax:__________________

Email: ___________________________________________________

How to Illustrate

owner / Trustee Authorization

In-Force IllustrationREQUEST FOR

Send To

Send By

Mortgage ProtectionI N S U R A N C E

Mortgage: non-Med Term: Americo – Home Mortgage Series Mutual of Omaha – Term Life Express Assurity – Non-Med 350 Fidelity – Rapid Decision Term

Fully Underwritten Term: Mutual of Omaha - Term Life Answers Genworth – Colony Term

Final expense: Americo – Ultra Protector Mutual of Omaha – Whole Life Express Foresters – Plan Right United Home Life – Total Protection Series III Monumental – Life Solutions American Amicable – Platinum Choice

ProDUCT ACCeSS – SUMMArY oF oFFerInGS

Mortgage ProtectionI N S U R A N C E

4

HomeMortgageSeries at aGlance

Face Amounts:

Minimum: $25,000

Maximum: $400,000

(HMS w/ADB has unique FaceAmounts. See Product Specificationson Page 5.)

Underwriting Classes:

Non-nicotine or NicotineNon-nicotine rates available if theapplicant has not smoked cigarettes,cigars, used nicotine patches orchewed tobacco or nicotine gum inthe last 12 months.

Underwriting:Accept/Reject through Table 6Non-medical through $400,000;saliva test $250,001 to $400,000.See Underwriting section for moreinformation.

Sex Rating duringinitial premium period:Unisex

Conversions:None

p.

Product Specifications

Policy Series 296 Policy Series 297

Policy Type Universal Life Universal Life

Maturity Date Age 100 Age 95

Cash Back Option(CBO)

At the end of the no-lapse guarantee period, the accumulation value of the policywill be at least as large as the total amount of premiums paid for the base policy,not including any premiums paid for riders.

Accidental DeathBenefit Rider

(Rider Series 2165)

An Accidental Death Benefit equal to25% of the base death benefit will bepaid, if death occurs prior to the endof the no lapse guarantee period and

is a result of an accident.

Not Available

An additional 25% of the base death benefit will be payable, if death

results from a bodily injury which isthe direct result of an accident, while riding as a fare-paying passenger on a

common carrier.

This rider terminates at the end of thelevel premium/no-lapse guarantee

period.

No Lapse Guarantee Periods

30, 25, 20, and 15 Years

Premium Modes Monthly EFT & Annual(No modal factors. The annual premium is simply divided by 12 to obtain monthly premium.)

Minimum IssueAge

20; Age Last Birthdaay

Maximum IssueAges

Non-nicotine:30 Year No-Lapse Guarantee: 5525 Year No-Lapse Guarantee: 55

20 Year No-Lapse Guarantee: 6015 Year No-Lapse Guarantee: 55

Nicotine:30 Year No-Lapse Guarantee: 5025 Year No-Lapse Guarantee: 5020 Year No-Lapse Guarantee: 5515 Year No-Lapse Guarantee: 50

Age Last Birthday

Non-nicotine:30 Year No-Lapse Guarantee: 5525 Year No-Lapse Guarantee: 55

20 Year No-Lapse Guarantee: 6015 Year No-Lapse Guarantee: 60

Nicotine:30 Year No-Lapse Guarantee: 5025 Year No-Lapse Guarantee: 5020 Year No-Lapse Guarantee: 5515 Year No-Lapse Guarantee: 55

Age Last Birthday

Optional Benefit Riders

î Disability Income (Also available on Additional Insured Rider)

î Critical Illness Accelerated Benefit

î Additional Insured

î Waiver of Monthly Specified Premium

î Involuntary Unemployment Waiver of Premium

î Children’s Term (up to $15,000 per child)

Policy Fee $90, Fully Commissionable

11-149-1 (0911)_Agent Guide:layout 9/6/2011 2:18 PM Page 4

4

HomeMortgageSeries at aGlance

Face Amounts:

Minimum: $25,000

Maximum: $400,000

Underwriting Classes:

Non-nicotine or NicotineNon-nicotine rates available if theapplicant has not smoked cigarettes,cigars, used nicotine patches orchewed tobacco or nicotine gum inthe last 12 months.

Underwriting:Accept/Reject through Table 6Non-medical through $400,000;saliva test $250,001 to $400,000.See Underwriting section for moreinformation.

Sex Rating duringinitial premium period:Unisex

Conversions:None

p.

Product Specifications

Policy Series 295 300

Policy Type Universal Life Term Insurance

Maturity Date Age 105 Age 105

Cash Back Option(CBO)

At the end of the no-lapse guaranteeperiod, the accumulation value of thepolicy will be at least as large as thetotal amount of no-lapse guaranteepremiums paid for the base policy,not including any premiums paid forriders.

Not available

Accidental DeathBenefit Rider

(Rider Series 2165)

An Accidental Death Benefit equal to 50% of the base death benefit will be paid, if death occurs prior to the end of the level term period / no-lapse guarantee peri-

od and is a result of an accident.

An additional 50% of the base death benefit will be payable, if death results from a bodily injury which is the direct result of an accident, while riding as a

fare-paying passenger on a common carrier.

This rider terminates at the end of the level premium period/no-lapse guarantee period.

Level andGuaranteed

Premium Options

30, 25, 20, and 15 Year no lapse guarantee period

30, 25, 20, and 15-year guaranteed level premiums

or30, 25, 20, and 15 level premiums with

5-year guarantee

Premium Modes &Modal Factors

Monthly EFT(No modal factors. The annual premium

is simply divided by 12 to obtainmonthly premium.)

Monthly EFT: .095

Minimum IssueAge

20; Age Last Birthdaay

Maximum IssueAges

Non-nicotine:30 Year No-Lapse Guarantee: 5525 Year No-Lapse Guarantee: 55

20 Year No-Lapse Guarantee: 6015 Year No-Lapse Guarantee: 55

Nicotine:30 Year No-Lapse Guarantee: 50

(45 in FL and IL)

25 Year No-Lapse Guarantee: 5020 Year No-Lapse Guarantee: 5215 Year No-Lapse Guarantee: 47

Age Last Birthday

30-Year Term: 6025-Year Term: 6515-Year Term: 7015-Year Term: 75

Age Last Birthday

Optional Benefit Riders

î Disability Income (Also available on Additional Insured Rider)î Critical Illness Accelerated Benefit î Additional Insured î Waiver of Premium for Disability Rider (HMS150 only)î Waiver of Monthly Specified Premium (HMS150 CBO only)î Involuntary Unemployment Waiver of Premiumî Children’s Term (up to $15,000 per child)

Policy Fee $90, Fully Commissionable $80, Fully Commissionable

Not available in IN, MA or PA.

Over for more information

Policy Highlights

NonMed Term 350 Life InsuranceLifeScape®

Product Description A guaranteed-premium term life insurance policy. Uses a streamlined underwriting process requiring no medical exams; all cases are processed through Assurity’s automated underwriting system.

Term Periods 10, 15, 20, 30 yearsIssue Ages 10-year and 15-year level: ages 18 through 65

20-year level: ages 18 through 60 30-year level: ages 18 through 50, non-tobacco; ages 18 through 45, tobacco

Issue Amounts $50,000 to $350,000Underwriting Classes Select+ non-tobacco/tobacco; Select non-tobacco/tobacco; Standard non-tobacco/

tobaccoPremiums Level and guaranteed for the initial term period of 10, 15, 20 or 30 years. Annually

renewable after the initial term to age 95.Conversion Conversion period begins on issue date and ends on the earlier of:

one year prior to end of level term period for 10-year plan; or, two years prior to end of level term period on 15-, 20- and 30-year plans; or, policy anniversary after insured attains age 65.

Illustrations Not required, but software is available.Additional Benefi t Riders(no additional premium)

Accelerated Benefi ts Rider (Living Benefi t) - NOTE: not approved in all states.

Critical Illness Rider(additional premium)

Critical Illness Benefi t Rider pays a lump-sum benefi t if insured is diagnosed with a specifi ed critical illness. This innovative coverage has two unique features: 1) Benefi ts do not decrease the death benefi t but are paid in addition; 2) After fi rst-ever diagnosis, insured is still eligible for benefi ts from multiple CI categories if continuing to pay premiums. Available on other insured.

Other Riders(additional premium)

Disability Waiver of Premium Rider, Other Insured Rider, Monthly DI Rider, Accident Only DI Rider, Critical Illness Rider, Children’s Term Insurance RiderReturn of Premium Rider available on 20-year and 30-year plans (Base, Disability Waiver of Premium Rider and Return of Premium Rider only)

Payment Modes Annual, semi-annual, quarterly, list bill, monthly automatic bank withdrawal and credit card (recurring only)

Electronic Application E-app is available on AssureLINK (https://assurelink.assurity.com)Policy Fee $70, commissionable

PO Box 82533 • Lincoln, NE 68501-2533(800) 276-7619 • www.assurity.com

We’re all in.

Product and rider availability, rates and features may vary by state.Policy Form No. I L0760 and Rider Form Nos. R I0761, R I0762, R I0763, R I0764, R I0765, R I0766, R I0767, R I0825-T, R I0827-T, A-R M35.

15-250-01111 (Rev. 11/12)

For agent use only. Not for use with consumers.

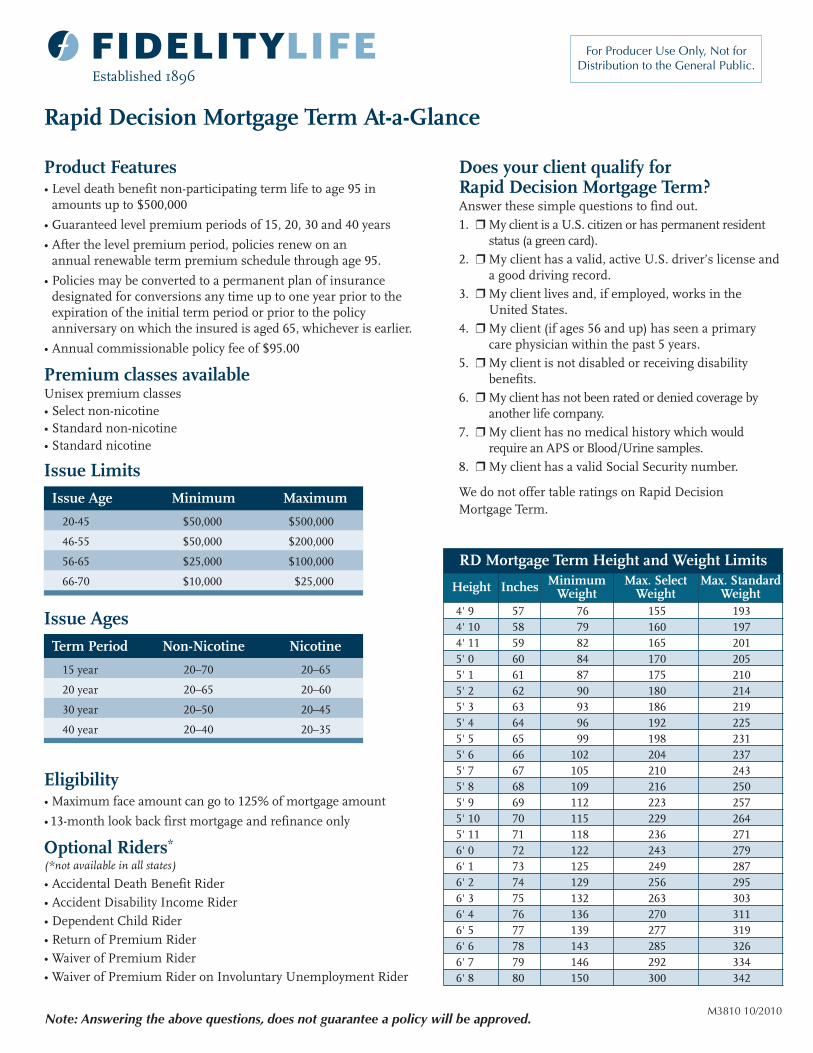

Rapid Decision Mortgage Term At-a-Glance

Product Features• Level death benefit non-participating term life to age 95 in

amounts up to $500,000

• Guaranteed level premium periods of 15, 20, 30 and 40 years

• After the level premium period, policies renew on an annual renewable term premium schedule through age 95.

• Policies may be converted to a permanent plan of insurance designated for conversions any time up to one year prior to the expiration of the initial term period or prior to the policy anniversary on which the insured is aged 65, whichever is earlier.

• Annual commissionable policy fee of $95.00

Premium classes availableUnisex premium classes• Select non-nicotine• Standard non-nicotine• Standard nicotine

For Producer Use Only, Not for Distribution to the General Public.

M3810 10/2010Note: Answering the above questions, does not guarantee a policy will be approved.

Does your client qualify for Rapid Decision Mortgage Term? Answer these simple questions to find out.1. ❒ My client is a U.S. citizen or has permanent resident

status (a green card).2. ❒ My client has a valid, active U.S. driver’s license and

a good driving record.3. ❒ My client lives and, if employed, works in the

United States.4. ❒ My client (if ages 56 and up) has seen a primary

care physician within the past 5 years.5. ❒ My client is not disabled or receiving disability

benefits.6. ❒ My client has not been rated or denied coverage by

another life company.7. ❒ My client has no medical history which would

require an APS or Blood/Urine samples.8. ❒ My client has a valid Social Security number.

We do not offer table ratings on Rapid Decision Mortgage Term.

RD Mortgage Term Height and Weight Limits

Height Inches MinimumWeight

Max. SelectWeight

Max. StandardWeight

4' 9 57 76 155 1934' 10 58 79 160 1974' 11 59 82 165 2015' 0 60 84 170 2055' 1 61 87 175 2105' 2 62 90 180 2145' 3 63 93 186 2195' 4 64 96 192 2255' 5 65 99 198 2315' 6 66 102 204 2375' 7 67 105 210 2435' 8 68 109 216 2505' 9 69 112 223 2575' 10 70 115 229 2645' 11 71 118 236 2716' 0 72 122 243 2796' 1 73 125 249 2876' 2 74 129 256 2956' 3 75 132 263 3036' 4 76 136 270 3116' 5 77 139 277 3196' 6 78 143 285 3266' 7 79 146 292 3346' 8 80 150 300 342

20-45 $50,000 $500,000

46-55 $50,000 $200,000

56-65 $25,000 $100,000

66-70 $10,000 $25,000

Issue Age Minimum Maximum

Issue Limits

Eligibility• Maximum face amount can go to 125% of mortgage amount

• 13-month look back first mortgage and refinance only

Optional Riders*

(*not available in all states)

• Accidental Death Benefit Rider• Accident Disability Income Rider• Dependent Child Rider• Return of Premium Rider• Waiver of Premium Rider• Waiver of Premium Rider on Involuntary Unemployment Rider

15 year 20–70 20–65

20 year 20–65 20–60

30 year 20–50 20–45

40 year 20–40 20–35

Term Period Non-Nicotine Nicotine

Issue Ages

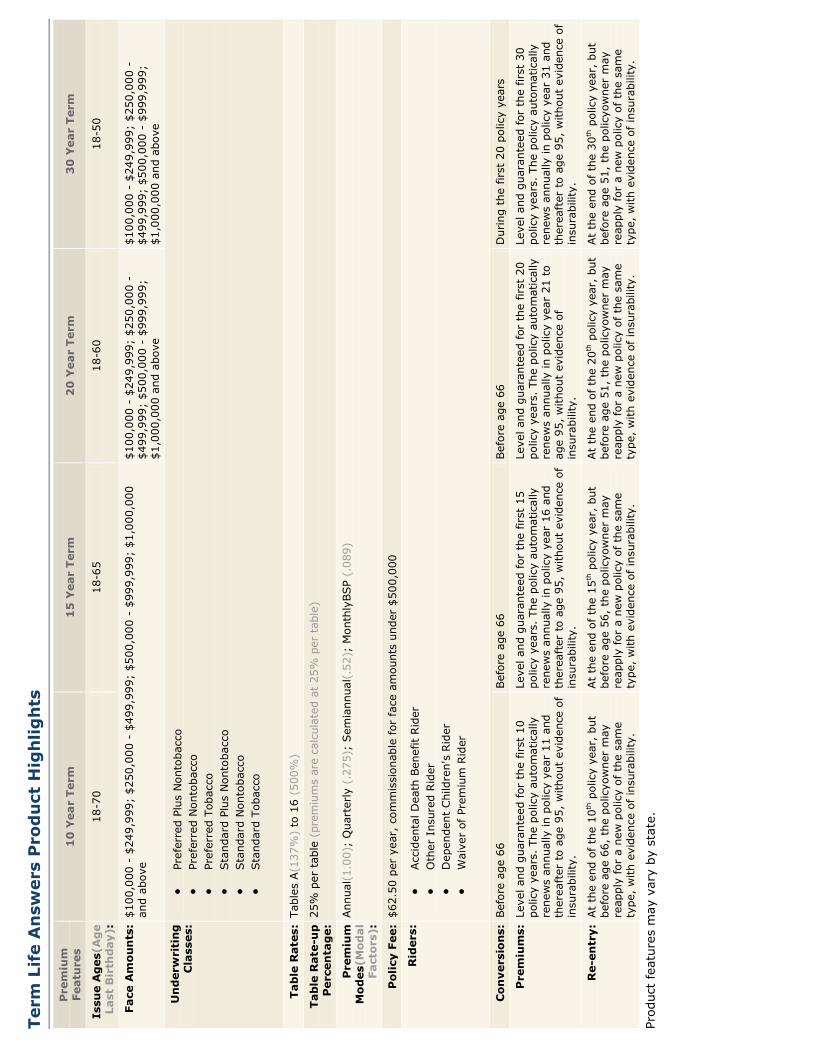

Term

Lif

e A

nsw

ers

Pro

du

ct H

igh

lig

hts

Pre

miu

m

Featu

res

10

Yea

r T

erm

15

Yea

r T

erm

20

Yea

r T

erm

30

Yea

r T

erm

Issu

e A

ges

(Ag

e La

st B

irth

day)

:18

-70

18-6

518

-60

18-5

0

Face

Am

ou

nts

:$1

00,0

00 -

$249

,999

; $2

50,0

00 -

$499

,999

; $5

00,0

00 -

$999

,999

; $1

,000

,000

an

d ab

ove

$100

,000

-$2

49,9

99;

$250

,000

-$4

99,9

99;

$500

,000

-$9

99,9

99;

$1,0

00,0

00 a

nd a

bove

$100

,000

-$2

49,9

99;

$250

,000

-$4

99,9

99;

$500

,000

-$9

99,9

99;

$1,0

00,0

00 a

nd a

bove

Un

der

wri

tin

g

Cla

sses

:•

Pref

erre

d Pl

us N

onto

bacc

o•

Pref

erre

d N

onto

bacc

o•

Pref

erre

d To

bacc

o•

Sta

ndar

d Pl

us N

onto

bacc

o•

Sta

ndar

d N

onto

bacc

o•

Sta

ndar

d To

bacc

o

Tab

le R

ate

s:Ta

bles

A(1

37%

)to

16

(500

%)

Tab

le R

ate

-up

P

erce

nta

ge:

25%

per

tab

le(p

rem

ium

s ar

e ca

lcul

ated

at

25%

per

tab

le)

Pre

miu

m

Mo

des

(Mo

dal

Fact

ors

):

Ann

ual(

1.00

); Q

uart

erly

(.27

5);

Sem

iann

ual(

.52)

; M

onth

lyBSP

(.08

9)

Po

licy

Fee

:$6

2.50

per

yea

r, c

omm

issi

onab

le for

fac

e am

ount

s un

der

$500

,000

Rid

ers:

•Acc

iden

tal D

eath

Ben

efit R

ider

•O

ther

Ins

ured

Rid

er•

Dep

ende

nt C

hild

ren'

s Rid

er•

Wai

ver

of P

rem

ium

Rid

er

Co

nve

rsio

ns:

Bef

ore

age

66Bef

ore

age

66Bef

ore

age

66D

urin

g th

e fir

st 2

0 po

licy

year

s

Pre

miu

ms:

Leve

l and

gua

rant

eed

for

the

first

10

polic

y ye

ars.

The

pol

icy

auto

mat

ical

ly

rene

ws

annu

ally

in p

olic

y ye

ar 1

1 an

d th

erea

fter

to

age

95,

witho

ut e

vide

nce

of

insu

rabi

lity.

Leve

l and

gua

rant

eed

for

the

first

15

polic

y ye

ars.

The

pol

icy

auto

mat

ical

ly

rene

ws

annu

ally

in p

olic

y ye

ar 1

6 an

d th

erea

fter

to

age

95,

witho

ut e

vide

nce

of

insu

rabi

lity.

Leve

l and

gua

rant

eed

for

the

first

20

polic

y ye

ars.

The

pol

icy

auto

mat

ical

ly

rene

ws

annu

ally

inpo

licy

year

21

to

age

95, w

itho

ut e

vide

nce

of

insu

rabi

lity.

Leve

l and

gua

rant

eed

for

the

first

30

polic

y ye

ars.

The

pol

icy

auto

mat

ical

ly

rene

ws

annu

ally

in p

olic

y ye

ar 3

1 an

d th

erea

fter

to

age

95,

witho

ut e

vide

nce

of

insu

rabi

lity.

Re-

entr

y:At

the

end

ofth

e 10

thpo

licy

year

, bu

t be

fore

age

66,

the

pol

icyo

wne

r m

ay

reap

ply

for

a ne

w p

olic

y of

the

sam

e ty

pe, w

ith

evid

ence

of

insu

rabi

lity.

At

the

end

of t

he 1

5thpo

licy

year

, bu

t be

fore

age

56,

the

pol

icyo

wne

r m

ay

reap

ply

for

a ne

w p

olic

y of

the

sam

e ty

pe, w

ith

evid

ence

of

insu

rabi

lity.

At

the

end

of t

he 2

0thpo

licy

year

, bu

t be

fore

age

51,

the

pol

icyo

wne

r m

ay

reap

ply

for

a ne

w p

olic

y of

the

sam

e ty

pe, w

ith

evid

ence

of

insu

rabi

lity.

At

the

end

of t

he 3

0thpo

licy

year

, bu

t be

fore

age

51,

the

pol

icyo

wne

r m

ay

reap

ply

for

a ne

w p

olic

y of

the

sam

e ty

pe, w

ith

evid

ence

of

insu

rabi

lity.

Prod

uct

feat

ures

may

var

y by

sta

te.

Colony Term

Colony Term is term life insurance with level guaranteed premiums for the selected coverage period of 10, 15, or 20 years. After the level period, premiums are not guaranteed and increase annually.

Product Features

• Issue Ages - 10-year, 0-80; 15-year, 0-75; 20-year, 0-65 (state variations may apply)• Minimum issue age for nicotine use is age 16• Coverage Durations - 10, 15 or 20 years• Features - Guaranteed level premiums for selected coverage periods of 10, 15 or 20 years• Minimum Specified Amount - $50,000 at issue; $50,000 minimum in-force (after decrease)• Annual Policy Fee - $50 (non-commissionable)• Riders Available - Waiver of Premium, Children's Level Term Insurance, Accelerated Death Benefit

Premium Bands

Band 1: $50,000 - $99,999.99Band 2: $100,000 - $199,999.99Band 3: $200,000 - $499,999.99Band 4: $500,000 - $999,999.99Band 5: >= $1,000,000

Underwriting Classes

No Nicotine Use

Preferred Best No Nicotine Use

Preferred No Nicotine Use

Select No Nicotine Use

Standard No Nicotine Use

Nicotine Use

Preferred Nicotine Use

Standard Nicotine Use

Competitive Areas

• $150,000 and below face amounts• Select to Preferred Best No Nicotine Use underwriting classes

Conversion

Policyowners have the option to convert to a universal life insurance product. This option must be exercised before the end of the level-premium period.

Expiry Ages

• Policy expires at attained age 98• Maryland expires at attained age 95

p.5

Ultra Protector I Ultra Protector II Ultra Protector III

Minimum Face Amount* $2,000

Maximum Face Amount $30,000 $10,000

Issue Ages, age last birthday

Non-smoker: 50 – 85Smoker: 50 – 80

50 – 80 50 – 75

Death Benefit Level death benefit2-year graded death benefit

(Level death benefit in seven states,see below)

3-year graded death benefit

(2 years in four states, see below)

Death Benefit Descriptions

Full death benefit day one

Year 1: Death Benefit equals returnof premium plus 5%

Year 2: Death Benefit equals thegreater of return of premium plus 10%or 50% of the face amount

Year 3+: Death Benefit equals100% of the face amount

For Arkansas, Massachusetts,Minnesota, Missouri,Montana, New Jersey, NorthCarolina and West Virginia:

Full death benefit day one

Year 1: Death Benefit equals returnof premium plus 5%

Year 2: Death Benefit equals returnof premium plus10%

Year 3: Death Benefit equals 75% ofthe face amount

Year 4+: Death Benefit equals100% of the face amount

For Illinois, New Hampshire,New Jersey and West Virginia:

Year 1: Death Benefit equals returnof premium plus 5%

Year 2: Death Benefit equals returnof premium plus 10%

Year 3+: Death Benefit equals100% of the face amount

Available Riders and Additional Features

Accelerated Benefit PaymentRider included at no additional

cost. (Rider Series 2146)

Children’s Term Rider availablefor $11 per $1,000 annually.

(Rider Series 2147)

Accidental Death Benefit Provision:Full death benefit payable for accidental death

during graded death benefit period.

No riders available

Policy Fee $40 annual policy fee (commissionable)$40 annual policy fee (non-commissionable)

Underwriting Classes

Non-smoker/Smoker(Pipe & cigar smokers qualify for

non-smoker rates.)

Male/Female

Male/Female

Premium Modes Annual (1.00) and Monthly PAC (.095)

Application Application included in client brochure 10-170-2. State variations exist. Series 5099.

Policy DescriptionNonparticipating, level premium whole life product with premiums payable to age 100 and protection

provided until the insured’s attained age 120. The policy will endow at age 120(cash value will equal the face amount at age 120).

Ultra Protector SeriesThree products to fit individual situations

*Face amounts vary by issue age in WA. See page 6 for specific amounts.

10-170-1 (03-12):Layout 1 4/25/2012 9:30 AM Page 5

Whole Life Express Product Highlights

Issue Ages - (Age Last Birthday):

• 26-80• Age last birthday

Target Market:

• Individuals who want small face amounts of insurance protection for needs such as final expenses• Juveniles to guarantee future insurability and to build cash values.

Needs:

• Small face amount of permanent insurance• Fully guaranteed death benefit• Level premiums• Covers final expenses

Underwriting Classes:

• Tobacco• Non-Tobacco

Table Rate-Up Percentage:

N/A

Premuim Modes (Modal Factors)

• Annual (1.00)• Quarterly (.275)• Semi-Annual (.52)• Monthly BSP (.089)

Policy Fee

$36 Annual Policy Fee

Commissionable

Riders:

None: (Please refer to product guidelines for more details)

Guaranteed Interest Rate:

N/A

Low-Cost Loans

A 7.4% interest rate is payable in advance, 8% effective annual rate.

Partial Withdrawals:

None

Death Benefit Guarantees:

Policy is guaranteed to endow at age 100 as long as premium is paid.

Other Product Features:

• Simplified Underwriting• Small Face Amounts

No death benefit reductions in the early years

PlanRight Whole Life Insurance

PlanRight Whole Life Insurance

Level Graded Modified

Description Level, guaranteed premium whole life insurance. Three types of coverage – one that can immediately pay a full death benefit (Level) and two that provide a limited benefit (Graded and Modified) in the first two years, and can provide a full death benefit thereafter.

Death Benefit2,3 Based on4 100% of face amount in effect

For years 1 and 2 based on4, the greater of: 1. Return of Premium (ROP) plus 4.5% annual

interest5 or;2. In year 1 - 30% of the face amount in effect.

In year 2 - 70% of the face amount in effect. In year 3+ - full death benefit payable

Year 1: Based on4 Premium paid plus 10% annual interest5

Year 2: Based on4 Premium paid plus 10% annual interest5

Year 3+: Full Death Benefit

Riders Accidental Death Rider available (issue ages 50-80)

Common Carrier Accidental Death Rider included at no additional cost

Accidental Death Rider not available

Common Carrier Accidental Death Rider included at no additional cost

Accidental Death Rider not available

Common Carrier Accidental Death Rider included at no additional cost

Premiums Level, payable to age 121

Minimum Premiums $10/month

Issue Ages (age last birthday)

50-85 50-85 50-80

Minimum Face Amount $2,0006

Maximum Face Amounts

Ages 50-80: $35,000Ages 81-85: $15,000

Ages 50-80: $20,000Ages 81-85: $10,000

Ages 50-80: $15,000 Ages 81-85: N/A

Certificate Fee (commissionable)

$36 annually, subject to modal factors

Modal Factors Monthly: 0.0875, Quarterly: 0.26, Semi-Annually: 0.51, Annually: 1.00

Underwriting Classes7 Non-Tobacco & Tobacco

Cash Values Available (on full surrender only)

Loans4 Available

1 Foresters PlanRight whole life insurance and its riders may not be available or approved in all states, are subject to the terms and conditions of the applicable contract and state variations may apply. Refer to PlanRight Producer Guide for more detailed information.

2 For PlanRight – Graded and Modified, the Death Benefit is 100% of the face amount plus unearned premium minus debt in the event of accidental death during the first two years.

3 Each outstanding certificate loan amount will be deducted from the Death Benefit.4 Unearned premium will be added and debt subtracted from the applicable amount in calculating the death benefit.

Debt includes each outstanding certificate loan amount and unpaid premium owed during the grace period before lapse.5 Interest is compounded annually and is accrued on a daily basis to the date of death.6 Minimum face amount to qualify for certain non-contractual member benefits is $10,000, subject to benefit specific

eligibility requirements and limitations.7 Ratings do not apply on the PlanRight plans.8 Insurability depends on answers to questions in the applications and on the outcome of the underwriting review, based

on underwriting requirements and guidelines.

ForestersTM is the tradename and a trademark of The Independent Order of Foresters, a fraternal benefit society, 789 Don Mills Road, Toronto, Ontario, Canada M3C 1T9.

503294 US (07/12)PRODUCER USE ONLY.

• Face amounts range from $2,000 to $35,000• Plan eligibility determined at point of sale8

• No medical exam, no blood

• Personal Health Interviews (PHIs) available 7-days-a-week • Complete in the comfort of the client’s home

Sales Focus

Total Protection III is a Whole Life portfolio thatcombines three distinct products in one, easy-to-use application.

Key Features • Simplified application with a limited number of

health questions• No routine medical exams, blood work, urine

testing or physician’s statements• High Commissions • Level, guaranteed premiums

Express Issue Whole Life (Graded Benefit Whole Life Insurance)

• Ideal for clients with significant health issues – up to table 16. Previously declined applicants considered.

• Graded death benefit during the first two years:- Policy Year 1: Benefit payable equals refund of premium plus 12% interest*-Policy Year 2: Benefit payable equals refund of premium plus 24% interest*-Policy Year 3: Full death benefit payable

• Full death benefit is payable if death occurs due to accidental causes during the first two policy years

• Free identity theft benefit – premiums waived for three months

• Free extended hospital stay (20 consecutive days) – premiums waived for three months

• Free Common Carrier Accidental Death Benefit – death benefit payable is doubled if death is due to an accident while riding on public transportation.

• Issue ages 25 to 80 (45 to 80 in California)• Coverage amounts from $2,000 to $25,000Base plan and benefits may not be available in all states.

*In AR, KS, NV and PA: death benefit is 30% of initial death benefit in year 1, 60% of initial death benefit in year 2.

Express Issue Deluxe (Immediate Death Benefit Whole Life Insurance)

• Standard issue through Table 8 – ideal for clients with insulin dependent diabetes

• Full and immediate death benefit from first day of policy issue

• Issue ages 20 to 80• Coverage amounts from $5,000 to $50,000• Child Rider and Accidental Death Benefit available

Express Issue Premier (Immediate Death Benefit Whole Life Insurance)

• Standard issue through Table 4 – ideal for clients with minor health issues

• Full and immediate death benefit from first day of policy issue

• Issue ages 20 to 80• Coverage amounts from $5,000 to $100,000

through issue age 60; $50,000 for issue ages 61 to 80

• Child Rider and Accident Death Benefit Rider available

Base plan and benefits may not be available in all states.

Total Protection IIIWhole Life Insurance

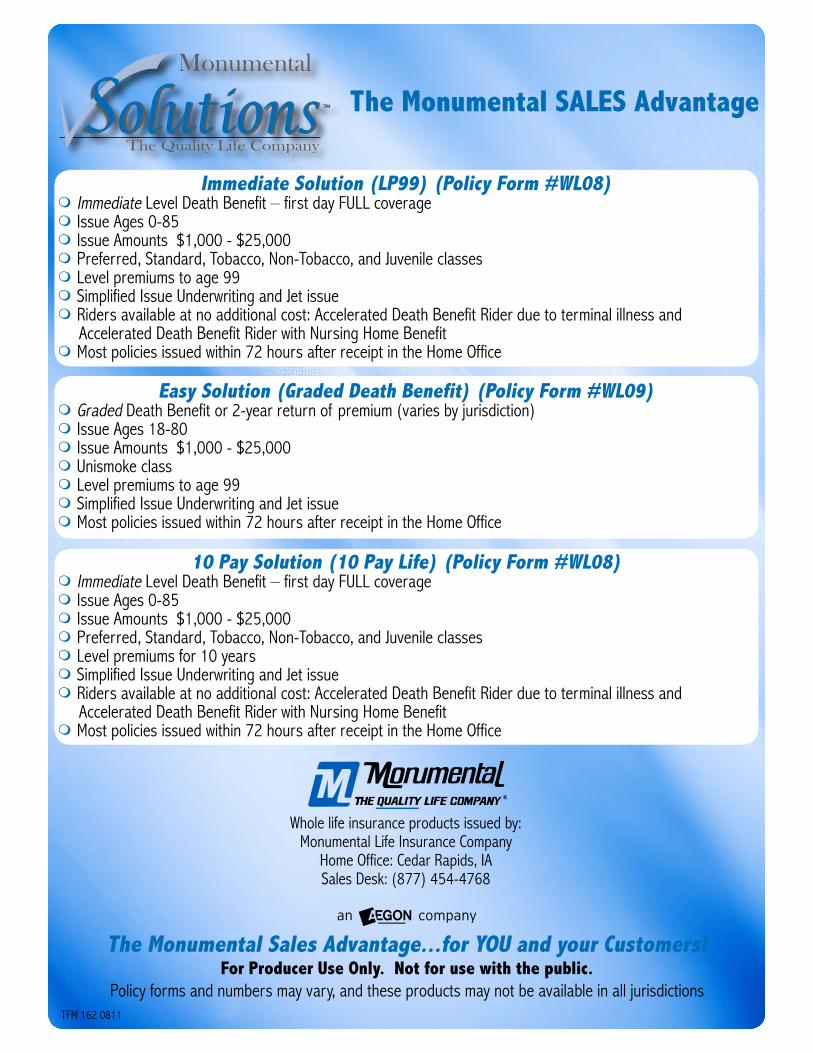

Immediate Solution (LP99) (Policy Form #WL08)m Immediate Level Death Benefit – first day FULL coveragem Issue Ages 0-85m Issue Amounts $1,000 - $25,000m Preferred, Standard, Tobacco, Non-Tobacco, and Juvenile classesm Level premiums to age 99m Simplified Issue Underwriting and Jet issuem Riders available at no additional cost: Accelerated Death Benefit Rider due to terminal illness and Accelerated Death Benefit Rider with Nursing Home Benefitm Most policies issued within 72 hours after receipt in the Home Office

Easy Solution (Graded Death Benefit) (Policy Form #WL09)m Graded Death Benefit or 2-year return of premium (varies by jurisdiction)m Issue Ages 18-80m Issue Amounts $1,000 - $25,000m Unismoke classm Level premiums to age 99m Simplified Issue Underwriting and Jet issuem Most policies issued within 72 hours after receipt in the Home Office

10 Pay Solution (10 Pay Life) (Policy Form #WL08)m Immediate Level Death Benefit – first day FULL coveragem Issue Ages 0-85m Issue Amounts $1,000 - $25,000m Preferred, Standard, Tobacco, Non-Tobacco, and Juvenile classesm Level premiums for 10 yearsm Simplified Issue Underwriting and Jet issuem Riders available at no additional cost: Accelerated Death Benefit Rider due to terminal illness and Accelerated Death Benefit Rider with Nursing Home Benefitm Most policies issued within 72 hours after receipt in the Home Office

The Monumental SALES Advantage

The Monumental Sales Advantage...for YOU and your Customers!For Producer Use Only. Not for use with the public.

Policy forms and numbers may vary, and these products may not be available in all jurisdictionsTFM 162 0811

Whole life insurance products issued by:Monumental Life Insurance Company

Home Office: Cedar Rapids, IASales Desk: (877) 454-4768

—3—

UNDERWRITING GUIDELINESOur new Platinum Choice life insurance plans target a broad spec-trum of the final expense insurance market. These policies and our application Form 9617(with state variations) of Form 9869 (in MD, NJ & SC) accommodate a simplified approach to purchasing life insurance. Platinum Choice "Immediate Death Benefit" policy is for those with no serious health history and can answer "NO" to all health ques-tions 1 through 9 on the application.Platinum Choice "Return of Premium Benefit" policy is for those who answer "NO" to questions 1 through 6, "YES" to any health questions 7 through 9.If health questions 1 through 6 are answered "YES" the applicant is not eligible for any of the Platinum Choice plans.The Platinum Choice application features simple "YES" or "NO" questions that enable you to quickly determine which plan of insur-ance the applicant may be eligible for.

Issue Ages: 0-49 (age last birthday)

Premium Paying Period: To age 110

Minimum Face Amount: $10,000

Maximum Immediate Death Benefit: Ages 0-49 - $35,000

Maximum Return of Premium Death Benefit: Ages 18-49 - $20,000

Policy Fee: $30 (Non-Commissionable)

Modal Factors: Semi-Annual: .519 Quarterly: .262 Monthly EFT: .088

Riders:20-Year Spouse Level Term RiderCIA—Children’s Insurance Agreement (not available on ROP Plan)ADB—Accidental Death Benefit (not available on ROP Plan)WP—Waiver of Premium (not available on ROP Plan)Terminal Illness Accelerated Benefit Rider*Accelerated Benefit Confined Care Rider* (not available on ROP Plan)

*Included at no additional premium, where available.

—3—

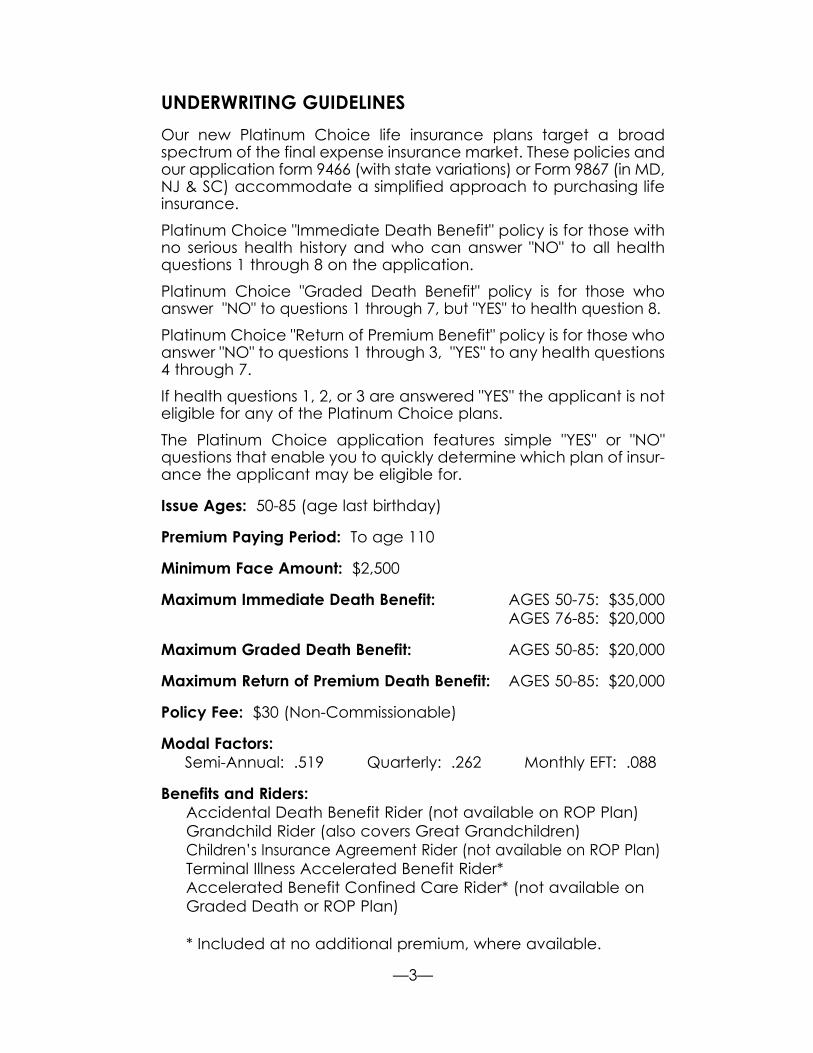

UNDERWRITING GUIDELINESOur new Platinum Choice life insurance plans target a broad spectrum of the final expense insurance market. These policies and our application form 9466 (with state variations) or Form 9867 (in MD, NJ & SC) accommodate a simplified approach to purchasing life insurance. Platinum Choice "Immediate Death Benefit" policy is for those with no serious health history and who can answer "NO" to all health questions 1 through 8 on the application.Platinum Choice "Graded Death Benefit" policy is for those who answer "NO" to questions 1 through 7, but "YES" to health question 8.Platinum Choice "Return of Premium Benefit" policy is for those who answer "NO" to questions 1 through 3, "YES" to any health questions 4 through 7.If health questions 1, 2, or 3 are answered "YES" the applicant is not eligible for any of the Platinum Choice plans.The Platinum Choice application features simple "YES" or "NO" questions that enable you to quickly determine which plan of insur-ance the applicant may be eligible for.

Issue Ages: 50-85 (age last birthday)

Premium Paying Period: To age 110

Minimum Face Amount: $2,500

Maximum Immediate Death Benefit: AGES 50-75: $35,000 AGES 76-85: $20,000

Maximum Graded Death Benefit: AGES 50-85: $20,000

Maximum Return of Premium Death Benefit: AGES 50-85: $20,000

Policy Fee: $30 (Non-Commissionable)

Modal Factors: Semi-Annual: .519 Quarterly: .262 Monthly EFT: .088

Benefits and Riders:Accidental Death Benefit Rider (not available on ROP Plan)Grandchild Rider (also covers Great Grandchildren)Children’s Insurance Agreement Rider (not available on ROP Plan)Terminal Illness Accelerated Benefit Rider*Accelerated Benefit Confined Care Rider* (not available on Graded Death or ROP Plan)

* Included at no additional premium, where available.