moomba plant, cooper basin northern regional development board energy security forum gas supply –...

TRANSCRIPT

Moomba plant, Cooper Basin

Northern Regional Development Board Energy Security Forum

Gas supply – Opportunities and Challenges

17 August 2012

2

Eastern Australia has a significant resource base with geographic and geological diversity.

Eastern Australia gas reserves and resources

2 Source: AEMO Gas Statement of Opportunities 2012 (numbers rounded down)

1 Includes Clarence, Gloucester and Galilee

3 Source: ABARE Australian Gas Resource Assessment 2012; Facts Global Energy #57 2012

3

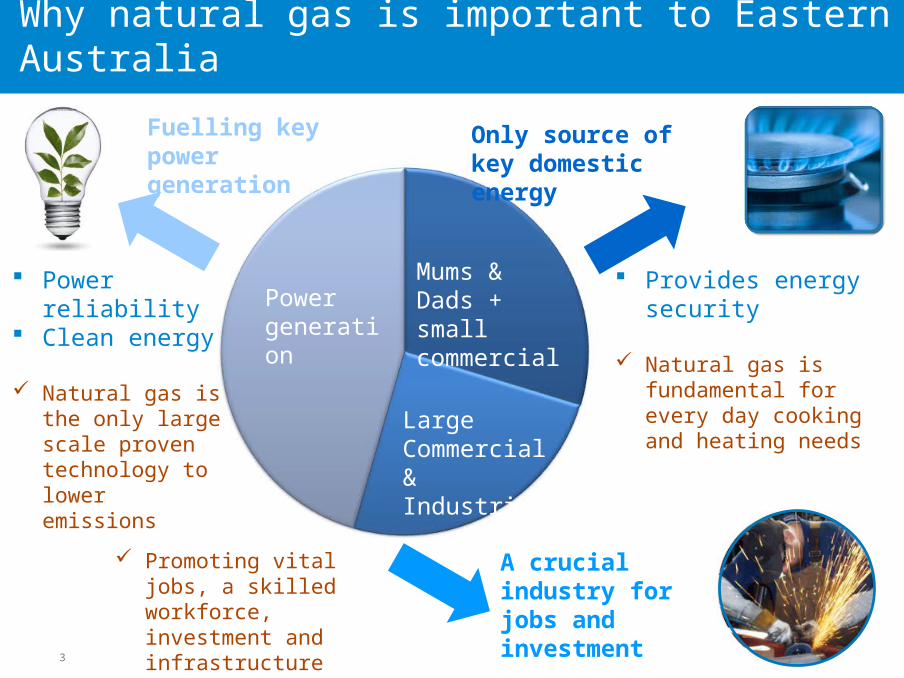

Mums & Dads + small commercial

Large Commercial & Industrial

Power generation

Power reliability

Clean energy

Natural gas is the only large scale proven technology to lower emissions

Fuelling key power generation

Provides energy security

Natural gas is fundamental for every day cooking and heating needs

Only source of key domestic energy

A crucial industry for jobs and investment

Promoting vital jobs, a skilled workforce, investment and infrastructure

Why natural gas is important to Eastern Australia

4

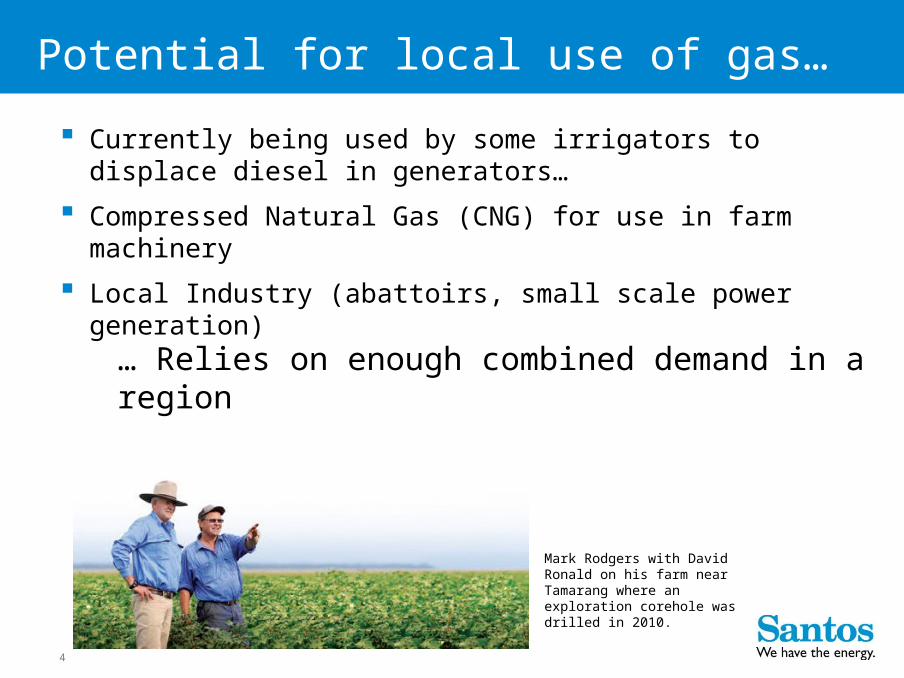

Currently being used by some irrigators to displace diesel in generators…

Compressed Natural Gas (CNG) for use in farm machinery

Local Industry (abattoirs, small scale power generation)

Mark Rodgers with David Ronald on his farm near Tamarang where an exploration corehole was drilled in 2010.

Potential for local use of gas…

… Relies on enough combined demand in a region

5

East Australian gas demand growth to 2020Strong LNG demand + Australia’s transition to a low carbon economy is driving unprecedented east coast gas demand growth.

Five LNG trains sanctioned

Gas-fired power generation to substantially increase by 2030

Source: Santos

PJ/a

2012 2014 2016 2018 2020 2022 2024 2026 2028 20300

500

1,000

1,500

2,000

2,500

3,000

3,500

Retail and C&I Power generation QCLNG (T1&2)

GLNG (T1&2) APLNG T1 APLNG T2

Shell (T1&2) QCLNG T3

Proposed

Sanctioned

6

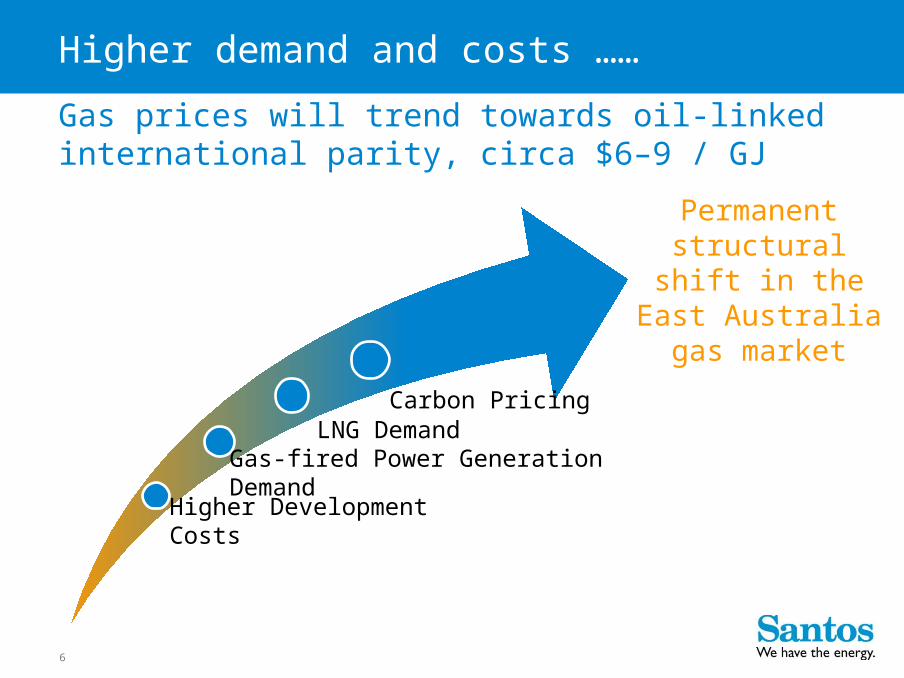

Higher Development Costs

Gas-fired Power Generation Demand

Carbon PricingLNG Demand

Permanent structural shift in the East Australia

gas market

Higher demand and costs ……

Gas prices will trend towards oil-linked international parity, circa $6–9 / GJ

7

Gas price increases are affordable

Historically east coast domestic gas prices have been relatively flat

Gas cost is a small percentage of end-user price of both gas and electricity – circa 20%

East coast gas prices are low compared to other markets (UK, Europe and Asia)

Expected higher domestic gas prices consistent with other energy and commodity price movements over the past decade.

2000

2000

2000

2001

2001

2002

2002

2003

2003

2003

2004

2004

2005

2005

2005

2006

2006

2007

2007

2008

2008

2008

2009

2009

2010

2010

2010

20110

200

400

600

800

1,000

1,200

East coast gas Iron ore CopperSilver Coal

Gro

wth

in

dex (

Yr

20

00

= 1

00

)

Source: BMI

Commodity price indices

8

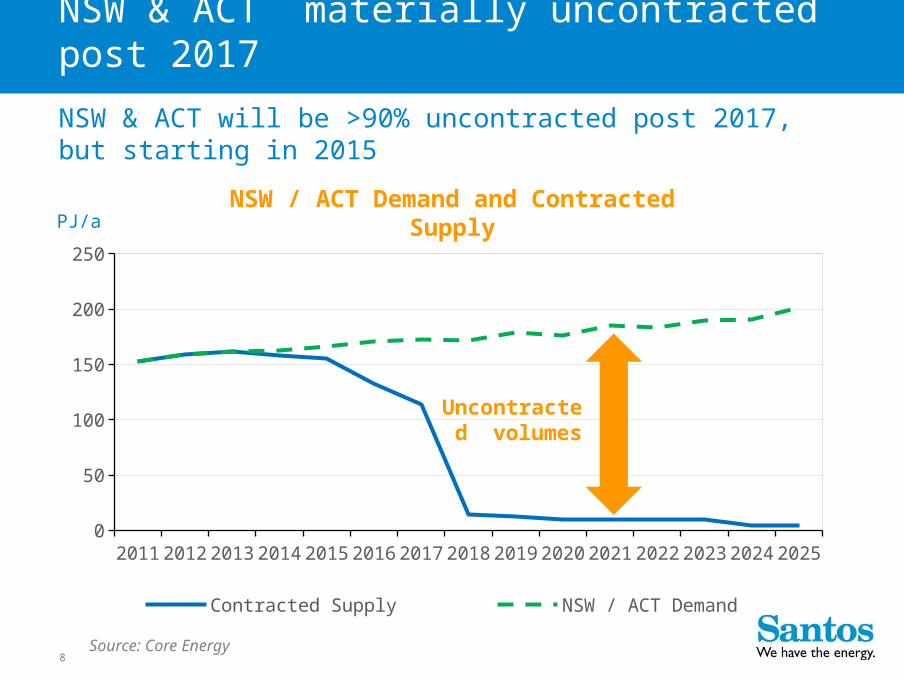

NSW & ACT materially uncontracted post 2017

NSW & ACT will be >90% uncontracted post 2017, but starting in 2015

NSW / ACT Demand and Contracted Supply

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

0

50

100

150

200

250

Contracted Supply NSW / ACT Demand

PJ/a

Uncontracted volumes

Source: Core Energy

9

2000

kilometres

Brisbane

CanberraSydney

Melbourne

Gladstone

Gunnedah Basin

NSW CSG – a world-class opportunityGunnedah Basin is world-class with appraisal program confirming confidence and known resources in excess of 12,000 PJ.

Exploration and Research

Development Planning

Environmental Impact

Assessment

Development

(construction)

Operations

Minimum 3 years

3-4 years

2018+

Development Process to Operations

The resources are available to meet the required 2017/18 development time frame, but we need to act now to achieve this.

NSW CSG industry

$1.5 billion already invested Over 1,000 potential new

jobs Significant local gas

production for the first time A low carbon alternative to

traditional dependence on coal

10

NSW jobs, investment and royaltiesGunnedah Basin offers NSW the possibility of significant growth between now and 2035.

2,900+ jobs created Investment of $16b+Incl. 200 ongoing full

time positions and 1800 during peak construction

Plus additional positions within Santos apprenticeship and indigenous employment programs

Employment

Investment

Royalties

NSW gross state product to increase by over $15b

Regional benefits around $450m pa

Substantial new regional infrastructure

Royalty payments of over $3bnPlus corporate tax receipts of ~$6.5bn

SOURCE: The Allen Consulting Group 2011