monetary models of exchange rates and exchange market pressure : some general limitations and an...

TRANSCRIPT

Monetary Models of Exchange Rates and Exchange

Market Pressure: Some General Limitations and an

Application to Sterling's Effective Rate

By

Graham Hacche and John C. Townend

C o n t e n t s : I . I n t r o d u c t i o n a n d S umma~-v . - - I I . S i m p l e M o n e t a r y M o d e l s o f E x c h a n g e R a t e s . - - I I I . T h e M e a s u r e m e n t a n d M o d e l l i n g o f P r e s s u r e . - - IV. R e s u l t s for S t e r l i n g ' s E f f e c t i v e R a t e . - - A p p e n d i x .

I. Introduction and Summary

R ecent interest in the apphcation of asset-market theory to the ex-

planation of currency movements has largely, in econometric work, taken the form of the estimation of simple monetary models repre-

senting the adaptation for flexible exchange-rate regimes of the monetary approach to the balance of payments 1. The monetary analysis of exchange rates has considerable advantages over more general asset theories in econometric tractability, and successful results have been obtained, for a number of bilateral rates, with simple equilibrium monetary models [Fren- kel, 1976; Bilson, 1978 ]. A particularly interesting variant of the mone- tary approach is the derivation by Girton and Roper [1977 ; hereafter GR] of an equation to explain exchange-market "pressure," a composite de- pendent variable which is defined for any currency such that its value in any period is a function of both the current change in its exchange rate and the current volume of official financing of the balance of payments (or intervention). The parameters of this function are determined unam- biguously a priori, and the equation describing the determinants of the composite variable is independent of intervention policy. The model thus suggests that the pressure on a currency - - a concept which has intuitive appeal as being apphcable in all exchange-rate regimes - - is measurable prior to estimation; that its determinants can be estimated from data timt span both fixed and floating exchange-rate periods; and tha t it can be forecast directly, leaving the authorities to choose tha t combination of exchange rate changes and intervention which optimises their objective

Remark: We are grateful to our colleagues at the Bank of England, especially R. N. Brown aad C. M. Miles, for helpful comments; the views expressed do not necessarily repre- sent those of the bank.

For surveys see, e.g., Dornbusch [x978]; Isard [x978].

Exchange Rates and Exchange Market Pressure 623

function. Another attractive feature of the approach is tha t it obviates the need for a structural model of the capital account in determining the balance of payments: for if intervention can be predicted in this way, then with the current or basic balance forecast using conventional equations, short-term capital flows, which have been notoriously difficult to forecast, are determined as a residual.

The purpose of this article is partly to draw attention to the restric- tiveness of the assumptions which enable GR to obtain a definition of pres- sure which allows it to be measured without estimation, and to show tha t on alternative assumptions which seem more valid, for the short run at least, the measurement of pressure becomes an empirical question even in the context of the simple monetary model (Section III). We have applied the model to sterling's effective exchange rate and the results reported in Section IV support the proposition that the GR model is best regarded as a model for the long run. In the short run, neither the GR model nor more general single-equation monetary models fit the data successfully. First, Section II reviews the formulation of simple monetary models of exchange rates.

H. Simple Monetary Models of Exchange Rates

What may be called the basic monetary model of exchange rates may be set out as follows. I t is assumed tha t there is in the domestic economy a stable aggregate demand for money function of the usual form in the price level P, real income Y, and interest rates i, and tha t there is mone- tary equilibrium so tha t this function describes the domestic money stock M in any period:

M ---- kPY ~ e -Bi (I)

Note, in particular, tha t the price-elasticity is assumed, following conven- tion, to be unity. Corresponding assumptions for the rest of the world give a similar equation for the foreign money stock: using F-subscripts for foreign variables and parameters, bu t assuming for simplicity, tha t the responsiveness to interest rates is internationally uniform,

MF = kF PF Y~F e -~iF (2)

I t is also assumed tha t the spot exchange rate S, defined as the price of a unit of domestic currency in terms of foreign exchange, is tethered by forces of international competition to the ratio between foreign and dom- estic price levels: purchasing power parity (PPP) holds 1 - -

t If PPP is interpreted as the equalisation of common-currency prices of traded goods rather than goods in general, k 'may be interpreted as measuring the relationship between

42*

6z4 G r a h a m H a c c h e ar~d J o h n C. T o w n e n d

S = k'PF/P (3)

On substitution, the following reduced-form equation for the exchange rate is obtained, the right-hand side variables being assumed exogenous:

InS = l n ( k k ' / k F ) - - l n M + l n M F + a l n Y

CtFln YF - - ~ (i--iF) (4)

The model thus implies strong a ~ io r i constraints on the coefficients of the money stock variables in this equation: the elasticities of S with re- spect to M and MF are --1 and -F1, respectively. This is a consequence of the assumptions of PPP and unit price-elasticity in the demand for money.

These equations convey the essence of the monetary theory. They state, for a small open economy, tha t its exchange rate must be such that the domestic price level implied by PPP and foreign prices is such that the domestic demand for money, for given real output and interest rates, matches supply. But they describe a particularly strong version of the monetary theory, and at least for short-run analysis the equilibrium re- lationships (I)--(3) would usually be regarded as unrealistic, even within the monetary framework. Most empirical studies of the demand for money have shown lagged adjustment, and PPP is almost always considered to be a distinctly long-run phenomenon. Suppose, then, that there is partial adjustment to the desired money stocks and equilibrium exchange rate described by the above equations.

The short-run demand for money functions then become:

In M = v'ln k q- 7'ln P + ~"~ In Y - - "c'~i - - "l'ln M_I (5)

A In M F ---~ "r"ln k F -~- ~,"ln P F -~- "~"'~ In Y F

- - v " ~ i r - - ~ " ' l n M F 1 (6 )

where A is the first-difference operator, and (1--v') and (1--V") are the coefficients of adjustment in the domestic and foreign functions, respec- tively. Similarly, (3) is replaced by

A In S ~ 7 In (k'PF/PS_I) (7)

Finally, we allow for a trend in the equilibrium exchange rate by assuming

In (kk'/kF) = K + ~t (8)

where K is a constant and t a linear trend.

the relative price structure (ratio of price level of traded goods to general price level) in the domestic economy and the corresponding price structure in the rest of the world. Here we assume it to be constant.

Exchange Rates and Exchange Market Pressure 625

The amended, weaker version of the monetary theory thus comprises (5), (6), (7), and (8). Substitution yields the following equation in S:

A In S = yK + ySt - - (~/y') A In M - - y In (MS/My)_ 1

+ (y/y") h In My + y~ In Y - - Y~F In YF - - Y~ (i--iv) (9)

This may be compared with the stronger version, represented by (4). One difference, which is of some significance for the following section, is that the coefficient of In M is no longer - - 1 a priori but is dependent on the relationship between the speeds of adjustment in the exchange rate and the demand for money. The short-run elasticity of S with respect to M is numerically higher the larger is Y (the absolute value of the short-run elasticity of S with respect to P) and the smaller is 7' (the short-run price- elasticity of the domestic demand for money).

Equations of a form similar to (9) have been estimated by some writers 1. I t may be argued, however, tha t the role played by PPP in inter- national monetary theory would be better described by the lagged ad- justment of relative price levels to exchange rates which equilibrates money markets independently of variations in prices, than by the lagged adjust- ment of exchange rates to relative price levels. This transmission mecha- nism suggests an alternative model, obtained by replacing (7) with

A In (Pv/P) = "C In (SP_I/k'Pv_~) (io)

On substitution of prices from the demand for money functions the reduced-form equation for S has the following form, with coefficients given their a priori signs:

In S = In (kk'/kv) + axln Mr + a21n Mr 1 + aaln MF 2 - - a41n M

-- %ln M_I - - a.ln M z - - %In Yv + asln Yv_1 + as In Y

- - atoln Y-1 - - an (i iF) -J- al~ (i----iF)_ 1 (IX)

The signs show that although the dynamics of this equation are more complicated than in the case of equation (9), the impact effects all have the

E. g., Bilson [I978]. But although he refers to evidence of lagged adjus tment in the demand for money, his equation est imated for the/~/DM rate on mor~thly data (April 1970--- May z977) assumes partial adjus tment in the exchange rate ortly, with insta~taneons adjust- mertt ir~ money demand. Dornbusch [I978, p. IO9] derives an equation similar to (9) (but with equal speeds of ad jus tment assumed) and finds it more successful in explaining monthly variations in the $/DM rate (March x974--May x978) than an equation similar to our (4)- (The equation estimated by Frenkel [x976 ] for the ~/DM rate, February]x92x--August x923 assumes no lags and corresponds to our (4)-)

6z6 G r a h a m H a e c h e and J o h n C. T o w n e n d

same direction as in the former model; and this is true too of the long-term effects.

III. The Measurement and Modelling of Pressure

Before the appearance of the paper by Girton and Roper [i977] Whitman [x975, p. 519] observed: " In a world of managed floating, market pressures on a currency are reflected both in the net international flow of reserves and in movements in the effective exchange rate, although no one has yet developed a single composite unit to measure empirically the total pressure reflected through both these channels." GR claim to have discovered such a measure of exchange-market pressure and to have derived a monetary model in which it is the dependent variable. Their model may be set out, in simplified form, as follows.

With the money supply M separated into its domestic and external components, D (domestic credit) and R (foreign exchange reserves), re- spectively, the monetary equilibrium condition (I) may be rewritten as1:

M ~ D q- R ---- kPY ~ e -~i ( I2 )

Differentiation with respect to time s gives:

~I = (D/M) -{- (R/M) = P q- ~r __ ~i (~3)

with notation defined as follows for any variable x:

x ~ dx/dt and x ~ x/x ------- (d/dr) lnx

Subtraction from (r3) of the corresponding equation for the rest of the world 8 gives:

Up to this point the model assumes no more than the basic monetary model of the previous section. In fact it assumes less: (i4) is merely (4)

* Following CoRuolly and da Silveira [I979], we construct the model here in terms of an aggregate money stock, whereas GR's model is in terms of base money. For the United Kingdom, if IV[ is sterling M 3 and D is domestic credit, R defined as the level of foreign ex- chartge reserves does not strictly satisfy the money supply identity, which is best thought of a s an approximation in this context.

* Following GR, we use continuous analysis to develop this model. Equivalent results may be obtained in terms of discrete time.

* GR construct their model for the two-country case to explain the exchange rate between the Canadian and U.S. dollar, but here, since our iaterest is in determining sterling's effective rate against a basket of currencies representing the U.K.'s trading partners, the appropriate "second country" is the rest of the world defined on this basis.

Exchange Rates and Exchange Market Pressure 627

differentiated and rearranged, with tile domestic money supply decom- posed by identity and the PPP assmnption removed. The procedure of the standard monetary approach would now be to invoke PPP and thereby replace the terms in (14) which represent the difference in inflation rates,

P--PF, by the rate of depreciation of the domestic currency, --S. Re-

arrangement would then give an equation in S which, apart from the decomposition of the domestic money stock growth rate, would be the same as the time-derivative of (4):

g = --(I)/M) - - (R/M) + l{lv + =Y - - ~-Y~. - - ,~ (i--iF) (I5)

GR, however, depart from the standard approach and claim more generality, as follows. Rejecting PPP, they introduce "for notational convenience only" [GR, 1977, p. 539, footnote II] a new variable 0, the rate of real appreciation of the domestic currency:

0 - - g - - - - b ) (16)

Substitution of (0--S) from this definition for (f~--i~r) in (14) then gives, on r e a l T a n g e m e n t ,

= 0 - - ( I ) /M) - - ( I~/M) + ~I,: + =5) - - = , , . ; f , : - ~(i-- i~.) ( i7 )

which differs from (15) only in the presence of 0, which measures the deviation of the movement of the exchange rate from the movement which would be implied by PPP. If PPP were assumed, 0 would of course dis- appear; but GR eliminate 0 not in this way but by supposing it to be a linear function of the normalised rate of domestic credit expansion and the growth rate of foreign money:

0 = 01 ( b / M ) - - 02f iF 01, % /> 0 (18)

The nature of this function is considered below. Its substitution into (17) g ives :

g = - - (1--01) (D/M) - - (R/M) + (1--08) l~I v + =Y

- - =F 5(F - - ~ ( i - - iF) (19)

This differs from the corresponding equation of tile basic monetary model,

(15), only in that the coefficients of l)[M and ~i F are no longer --1 and +1 a priori. But since 0 is not related to that part of the growth of the do-

628 G r a h a m H a c c h e and J o h n C. Townet~d

mestic money supply which is due to reserve changes, the coefficient of R/M is still --1, so tha t (19) may be rewritten as:

g + (l~/i) = - - (1--01) (filM) + (1--0,) MF + ='Z

- - ~ ~ - - ~ ( i ~ F ) (20)

The exchange-rate and balance of payments terms are now together on the left-hand side, with all other variables on the right; and in this way exchange-market pressure has emerged as an unambiguously defined vari- able which can be measured without estimation - - by the simple sum of the rate of appreciation and normahsed intervention - - and as the de- pendent variable in an equation derived from monetary theory. This is the novelty of the GR model.

GR go a step further than (2o), since they eliminate the interest-rate term by supposing tha t the rate of change of the uncovered differential, 8,

is, like 0, a linear function of D/M and ~I F :

- i - - iF = - - ~I (D/M) + ~ , ~ Sl, s 2 > 0 (21)

Equation (20) thus becomes

+ (R;M) = - - ( 1 - - ~ , - - 01) (b/M) + ( 1 - - ~ - - 0,) i F

+ ~Y - - ~F YF (22)

I t is this which corresponds to GR's estimating equation; but the distinc- tive innovation of the model remains the dependent variable, pressure.

Now an equation in pressure defined in the same way was always available from the basic monetary model since, partly owing to the

assumption of PPP, the coefficient of I~/M in (15) is ~ 1 a priori. GR do not

assume PPP; they obtain an equation in [S+R/M] "without relying on the small-country assumption" [GR, 1977, p. 537]- The assumption which they adopt instead and which allows them to derive their pressure equation is the 0 function (18). They in fact appear to assert tha t the function is unnecessary for this purpose x, but this seems incorrect because without

(18), S is present on the fight-hand side of (17) as part of 0 and so disap- pears from the equation. What then remains is nothing more than the stmunation of the equilibrium conditions for the domestic and foreign

a GR [x977, p. 54z] state tha t "Est imat ion of equation (6) iu its present form would serve the first purpose of explaining exchange market pressure." Their equation (6) corre- sponds to our equation (IF). (We consider in the following paragraph the other purpose to which GR refer.)

Exchange Rates and Exchange Market Pressure 6z9

money markets differentiated with respect to time: the exchange rate does not appear because there is nothing to link it with the demand for supply of money. Hence there can be no equation in exchange market pressure. The 0 function is therefore crucial to the derivation of GR's equation in pressure, so tha t their contribution may be represented by the gain in generality obtained by its substitution for ppp1.

I t is therefore of some importance to consider the nature and appro- priateness of the 0 function. I t states, given the assumed bounds on the parameters 01 and 02, tha t the rate of real appreciation is an increasing function of domestic credit expansion and a decreasing function of for- eign monetary expansion. As a behavioural hypothesis, it would seem an unusual component of an international monetary model, since for the long run it conflicts with PPP (apart from the special case where 01 =0 z---0), while for the short run it runs counter to theories which explain the volatility of the exchange rate in terms of its tendency to "overshoot" its long-run equilibrium position when responding to monetary shocks. In fact, however, the assumption about the signs of 01 and 0 z which GR adopt is immaterial to the derivation of their pressure equation, so it may be argued that they are a mat ter for empirical investigation, to be revealed by the estimation of equation (20); both PPP and overshooting are then admitted as possibilities, and the pressure equation remains intact. The behaviour of the real exchange rate is, however, still being assumed to take a special form. There are, in particular, no adjustment lags allowed for in the 0 function, or for tha t matter in the rest of the model; we return to this point below. Furthermore, real economic variables which might be expected to influence real exchange rate movements are absent. So what is the justification for the particular 0 function chosen ? In fact, GR make little claim for the plausibility of the functions chosen for 0 or 8 as de- scriptions of the determination of exchange rates, prices and interest rates: they are introduced not so much for their intuitive appeal or empirical validity, but as "reduced form relations" [GR, i977, p. 542] which express hypotheses of monetary independence to be tested by the extent to which

the estimated coefficients of D/M and l~I F in (22) differ from --1 and +1. ~ This test is what GR consider to be the second purpose of their model. We

1 Connolly and da Silveira consider their work to be an application of the GR approach although they derive their pressure equation from the basic monetary model. GR may there- fore also be said to have inspired the novel manipulation of the conventional model which de- livers an equation in pressure.

s Thus the sentence quoted on p. 6z8, footnote i , continues: "but it would not provide a measure of monetary independence." The 0 and 8 functions are introduced in order "To develop an alternative to (6) that will allow one to measure the independence of monetary policy" [GR, x977, p. 542].

630 Graham Haccheand John C. Townend

are not so concerned with this issue, As far as the measurement and mod- elling of pressure are concerned, it seems tha t the 0 function, which is crucial to the derivation of GR's equation, was introduced for a different purpose.

I t is therefore important to examine how robust is the strong result which this equation constitutes. To do this, we restore tile partial adjust- ment hypothesis used in the previous section. In the GR model, not only does the 0 function exclude adjustment lags, but also money holdings are assumed to adjust instantaneously to incomes, prices and interest rates. This suggests t h a t the GR model is appropriate only for the long run. Even for estimation on annual data - - which GR used - - it may be inappropriate; for estimation on data of greater frequency evidence from the demand for money strongly suggests tha t it is so.

I t was shown above t ha t when there is partial adjustment in the de- mand for money and PPP, the resulting exchange rate equation (9) has a coefficient o n the domestic money term which depends on relative speeds of adjustment. If the money supply is decomposed into its domestic and external elements, the coefficient of each component will clearly also have this property: in particular, the coefficient of the external component representing official financing will need to be determined empirically, so t ha t pressure cannot be measured prior to estimation. Tile same result is easily derived in terms of continuous time. The continuous analogues of (5)--(8) are:

i~l - y'in k + 7 ' I n P + ";'~in Y - - ~"r#i - - ,v'ln M (5 a)

~'I r- ---- , / ' ln k F + ~,"ln Pv + Y"mF In YF - - ","'~lv ~" - - "~"ln My (6a)

= ~. In (k'Pr/PS) (7a)

In (kk'/kF) = K + ~ t (Sa)

On substitution, this model yields the following equation in S :

= vK + u - - (V/V') l~I - - V In (MS/MF) + (V/V") lVIF

+ -~ lnY - - "~vinYv - - "~ (i--iv) (9 a)

This corresponds to equation (9)- Then when M is decomposed:

= v K + vst - - (v / , / ) ( 6 / M ) - - (v/v' ) (P, /M)

- - y In (SM/MF) + (y/y") ~IF +V =InY - - WF in YF

- - y[~ ( i - - i F ) (23)

Exchange Rates and Exchange Market Pressure 631

The coefficient of I~/M is the ratio of the speeds of adjustment in the domestic demand for money and the exchange rate: the faster is the adjustment of the exchange rate to PPP in relation to the adjustment of the money stock to long-run demand, the larger, numerically, will be the coefficient. I ts a priori bounds (assuming stable adjustment) are 0 and - - oo. Its value will be --1 only if the speeds of adjustment happen to be equal, a special case of which would be instantaneous adjustment of both variables. The GR measure of pressure is therefore invalid when there is assumed to be partial adjustment 1, and apart from when there is perfect adjustment there is no a priori measure of pressure.

This is scarcely surprising. GR's pressure variable implicitly "provides a measure of the volume of intervention necessary to achieve any desired exchange rate target" [GR, 1977, p. 537]. It would be remarkable if the parameters of such a measure--the parameters of the "trade-off" between exchange rate changes and intervention - - were not a matter for empirical investigation on other than very special assumptions about behaviour. To be able to claim on theoretical grounds that there will be a regular, linear trade-off such that any I percent movement in the exchange rate may be avoided by intervention equivalent to I percent of the money stock, assumptions are required about the responsiveness of the demand for money and the behaviour of the exchange rate which are special, and of particularly doubtful validity for the short run.

IV. Results for Sterling's Effective Rate

This section describes the estimates obtained for the GR pressure equations (22) and (2o) and the partial-adjustment monetary exchange rate equation (23) on annual and quarterly data for sterhng's effective exchange rate over the period 1964--1978. The models estimated are the discrete-time analogues of those set out above: the data are defined in the appendix.

The first two equations in Table I show the estimates of the pressure model on annual data. GR's estimating equation (2z) is unsuccessful: the

overall fit is poor, and the coefficient of/)/M is the only one which is sign- ificant 2 (although the size of the parameter is outside its a priori bounds). There is considerable improvement with the inclusion of the interest differential, in (2o), but again here there are problems: the coefficients

1 This is true even when the part ial adjustment assumption is adopted only for the demand for money functions and the GR function (18) is used to describe the behaviour of the exchange rate.

t Significance statements refer to the 5 percent probabili ty level unless otherwise indi- cated.

6 3 2 G r a h a m H a c c h e and J o h n C. T o w n e n d

Period, no. of

equation

x964--x978 (22)

(20)

19631I-- z978IV

(22)

(20)

T a b l e I ~ Pressure Equations P

C o n s t a n t I)/M_ 1

I --.ox4 - - LO41

(.O92) (2.870)

--.212 --.629 (L634)

.444 (2-476)]

.024 i (2.2xo) I

Coefficients of

I

i 1.57o i 2.815 (L055) (LX56)

2.693 X.717 (2.512) (2-949) (L849)

i

--.991 -- .260 --.287 (4.242) ( L 9 X 9 ) (.8X9)

--.717 ~--.226 [ -- .53 ~ (3.676) (X.7X5) [ (L537)

] ~ . i ~rv i - - i v i

i [ , !

I - - 2.822 , (I.4771

- -2 .330 --.212 i (2.6r9) (i.634)

R2 Q

I i '327

i .780

-- . I98 (.362) i

S.E.

.IO 4 I i

.o6o

i

--.4o9 .4x4 .o35 i (2.312) '

!302!03, i --.314 ~1--.olo

(.625) I (3 .866) i

D.W. or P

L696

.705 (2.240)

[ .493 i (4.oo2) I .397 (3.i48)

Note: The dependent variable in all equation is S + I~/M _ 1. - - The numbers in parentheses are t-values. - - ~ l is the coefficient of determinat ion adjusted for degrees of freedom. - - S.E. is the s tandard error of the

equation - - D.W. and p refer to the problem of autocorrelation: D.W. is the Durbin-Watson statistic and ~ is the value of the first-order autocorrelation coefficient, with its t-value in parantheses, where found significant. - - The data used are defined in the appendix.

of the income terms may be considered large for real income elasticities in

the demand for money, and the fact tha t the coefficient of l~I F exceeds unity contradicts the assumed signs of 0 2 and 8,.

I t is argued by both GR and Connolly and da Silveirathat the validity of their definition of pressure may be tested by the introduction into the pressure equation of an independent variable Q constructed so as to

measure its composition between S and I~[M. The Q used by Connolly and da Silveira is

Q = (~--1) / [(filM) --1]

which has the desirable monotonic property of being greater the more the authorities allow pressure to be absorbed by the exchange rate rather than the reserves 1. In our estimates on annum data, this Q was found to be insignificant in both equations, and the results shown are those obtained without it. Since, however, there are infinitely many measures of compo- sition which satisfy the monotonic property*, each of which will produce different empirical results, this seems a very weak test of the validity of a measure of pressure. With no unique Q, the insignificance of any particular

would therefore seem to offer only limited support for the view that the GR measure of pressure combines its two components appropriately.

Turning to the quarterly estimates, we see a marked deterioration in the results which provides support for the argument of the previous section:

t T h e y p o i n t o u t t h a t t h e Q u s e d b y G R , S . ' - : i~]M, fa i l s to s a t i s f y t h i s c o n d i t i o n .

' S u c h as S - ( R / M ) , ( S - K ) ] [ I ~ / M - K ] w i t h v a l u e s of K o t h e r t h a n u n i t y .

Exchange Rates and Exchange Market Pressure 633

not only is Q significant in equation (22) , but the coefficients of I~IF and

are incorrectly signed in both equations, and the coefficient of 3( F is not significant. The only coefficients which are consistent with the GR model are those of domestic credit expansion and the interest differential.

Table z thus shows a clear difference between the annual and quarterly results, and it is only the annual results which may be interpreted as providing any, limited, support for the GR model. This is not surprising in view of the argument of the previous section. But furthermore, even on annual data, the inclusion of the interest-differential term seems necessary for the GR model to have any explanatory power, and it is argued below that the coefficient on this variable is likely to be biassed because of the way the authorities have typically operated in the United Kingdom.

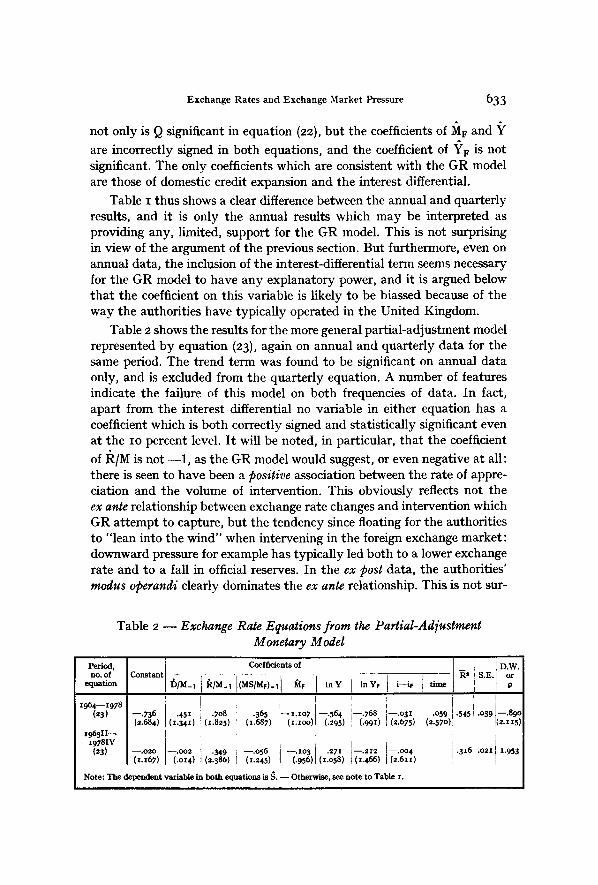

Table 2 shows the results for the more general partial-adjustment model represented by equation (23), again on annual and quarterly data for the same period. The trend term was found to be significant on annual data only, and is excluded from the quarterly equation. A number of features indicate the failure of this model on both frequencies of data. In fact, apart from the interest differential no variable in either equation has a coefficient which is both correctly signed and statistically significant even at the xo percent level. I t will be noted, in particular, that the coefficient

of I~[M is not - -1 , as the GR model would suggest, or even negative at all: there is seen to have been a positive association between the rate of appre- ciation and the volume of intervention. This obviously reflects not the ex ante relationship between exchange rate changes and intervention which GR attempt to capture, but the tendency since floating for the authorities to "lean into the wind" when intervening in the foreign exchange market: downward pressure for example has typically led both to a lower exchange rate and to a fall in official reserves. In the ex post data, the authorities' modus operandi clearly dominates the ex ante relationship. This is not sur-

Period, no. of

equation

x964--x978 (23)

x963II-- x978IV

(23)

Table 2 - - Exchange Rate Equations from the Partial-Adjustment Monetary Model

Constant Coefficients of DoorW.

DIM-1 R/M-11(MS/MF)-I I IVIF lnY lnYe i--iF time ~l S.E.

~ : I , ~ ! . o ~ 9 ! . 5 , 5 ~ q --.736 .45z .7off ~ .365 ]--x.zo7 --.564 --.768 --.o31 .o39 ---890 (2.684) (z.34z) (x.825) (L687) (Lxoo) (.295) i (.99x) , (2.675) (2.57o)i : !(2.zx5)

!

q i 4 k - o o 4 .o2x x9~3 --.020 --.OO2 .349 ---O56 --'IO3 i "271 --.212 i.3X6 (Z.X67) (2.586) i (x.245) (-956)] (I.O58) I (I"466) (2.6II)

Note: The dependent variable in both equations is S. - - Otherwise, see note to Table z.

634 G r a h a m H a c c h e and J o h n C. T o w n e n d

prising, and it may well be the case that the " t rue" coefficient of R/M can be estimated only by means of a two-stage model in which the authorities' reaction function is adequately specified.

The results in Table 2 thus show that the partial-adjustment modifi- cation does not succeed in correcting the failure of the GR model to ex- plain the quarterly data. But in addition, the annual results may be inter- preted as casting further doubt on the significance of the results obtained for the GR model on annual data, and on the appropriateness and validity more generally of such simple representations of the monetary approach.

Apart from the difficulties discussed above in defining pressure and estimating the coefficient on its reserve component, there are other reasons why single-equation monetary models of the exchange rate may be ex- pected to fail at least in the U.K. context. Two may be mentioned briefly. First, there appears to have been no success in finding a stable demand function for broad money in the U.K. on post - I97I data [e.g., I-[acche, I974; Hendry and Mizon, I978 ]. Second, there are good reasons to suppose tha t neither domestic credit expansion nor domestic interest rates can validly be assumed to be exogenous to the foreign exchange market, in the first case primarily because of interaction with behaviour in the market for government debt 1 and in the second case because of interaction with the authorities' monetary policy: in many instances over the period in question discretionary changes in domestic interest rates have been motivated by the authorities' concern for the balance of pay- ments. Biassed coefficients on these variables may be expected to result if these simultaneous relationships are not taken into account (and GR use OLS throughout).

Not only, therefore, is the failure of the single-equation monetary approach and of the special case of it represented by the GR pressure model, in the case of the U.K. effective rate, not surprising; but also, there are good reasons for believing that any single-equation approach which fails to take account of the simultaneity between the variables involved is unlikely to explain adequately the behaviour of this rate in recent years 2.

Appendix

D a t a D e f i n i t i o n s

Copies of the data used are obtainable from the authors. A dot (.) above A

a variable represents the first difference operator x --__- x - - x _ , ; a circum-

' This point is expanded on by Goodhart [x979].

9 Our attempts to take these important simultaneities into account are described in Hacche and Townend [x98x'].

Exchange Rates and Exchange Market Pressure 635

flex (" ) represents t he first difference of the na tu r a l logar i thm of t he var i-

able, i .e., i ts p ropor t iona l ra te of change, x ~ x /x_1 ; s. a. s t ands for seasonal ly ad jus ted .

U.K. Variables

S = U.K. effective exchange ra te index as defined b y I M F ; 1972 t r ade weights" value a t Smi tbson ian rea l ignment = 1"

I) = domest ic credi t ; I) represent domes t ic credi t expansion, s ran., s .a . , as defined b y t h e U.K. au thor i t i e s ;

R = U.K. foreign exchange reserves; R represents the ba lance for official f inancing, s ran;

M = (when used as a def la tor for D and t~) s M 3, s mn., s.a. (other-

wise) s M 3, s ran., s .a. , 1975 = 1"

Y = G D P a t 1975 fac tor cost, average es t imate , s .a. , 1975 = 1 ;

i = in teres t r a t e on t h r ee -mon th depos i t s wi th local author i t ies , average of da i ly rates .

Rest-of-World Variables

M F = weighted average of indices of money s tocks (M 2 as defined in International Financial Statistics) in U.S., Wes t Ge rmany , France , J a p a n , I t a l y , wi th weights der ived from I M F ' s MERM and normal i sed (weights are .4388, .I76O, .1554, .154o, and .0758, respect ively) , s. a., 1975 ----- 1;

YF = weigh ted average of indices of cons tan t price GDP, s. a., I975 = 1, wi th same coverage and weights as MF;

i F = in teres t r a te on th ree -month euro-dol la r depos i t s in London, average of da i ly rates .

References

Bilson, John F. 0., "The M~netary Approach to the Exchange Rate: Some Empirical Evidence". IMF, Staff Papers, Vol. z5, Washington, I978, pp. 48--75 .

Connolly, Michael, and Jos~ D. da Sflveira, "Exchange Market Pressure in Postwar Brazil: An Application of the Girton-Roper Monetary Model". The American Economic Review, Vol. 69, Menasha, x979, pp. 448--454 �9

Dornbuseh, Rudiger, "Monetary Policy under Exchange-Rate Flexibility". In: Managed Exchange Rate Flexibility. Federal Reserve Bank at Boston, Conference Series, No. 2o, Boston, i978, pp. 90---726.

Frenkel, Jacob A., "A Monetary Approach to the Exchange Rate: Doctrinal Aspects and Empirical Evidence". The Scandinavian Journal o/ Economics, Vol. 78. Stockholm, 1976, pp. 200---224.

636 Graham Hacche aud John C. Townend

Girton, Lance, and Don Roper, "A Monetary Model of Exchange Market Pressure Applied to the Postwar Canadian Experience". The American Economic Review, Vol. 67, Menasha, 1977, PP. 537--548.

Goodhart, C. A. E., "Money in an Open Economy". In : Economic Modelling. Current Issues and Problems in Macroeconomic Modelling in the UK and the US. London Graduate School of Business Studies, London, 1979, PP. x43--I67.

Hacche, Graham, "The Demand for Money in the United Kingdom: Experience since x97 I ' . Bank of England, Quarterly Bulletin, Vol. 14, London, 1974, PP. 284--3o5.

- - , and John C. Townend, "Exchange Rate and Monetary Policy: Modelling Ster- ling's Effective Exchange Rate, 1972--8o". In: W.A. Eltis and P. J. N. Sinclair, The Money Supply and the Exchange Rate.

Hendry, David F., and Grayham E. Mizon, Simplification, Not a Nuisance: A Comment by the Bank of England". The Economic pp. 549---563 �9

Isard, Peter, Exchange-Rate Determination: A Models. Princeton Studies in International

Whitman, Marina v. N., "Global Monetarism Balance of Payments". Bvookings Papers x975, 3, PP. 49x--536.

Oxford, I981.

"Serial Correlation as a Convenient on a Study of the Demand for Money Journal, Vol. 88, Cambridge, i978,

Survey o/ Popular Views and Recent Finance, No. 4 z, Princeton, 1978.

and the Monetary Approach to the on Economic Activity, Washington,

Z u s a m m e n f a s s u n g : Monet~4.re Modelle fiir den Wechselkurs und den Druck auf dem Devisenmarkt. Einige generelle Beschrlinkungen und eine Anwendung auf den effektiven Kurs des Pfund Sterling. - - Das gegenw~rtige Interesse daran, die Kapitalmarkttheorie zur Erkl~rung von Devisenbewegungen zu benutzen, hat sich meistens in der Form ausgewirkt, dab einfache monettixe Modelle geschtktzt wurden, in denen der monet~re Ansatz zur Zahlungsbilanzerkltixung dem System flexibler Wechselkurse angepaBt wurde. Eine besonders interessante Variante des monetiixen Ansatzes lieferten Girton und Roper mit der Ableitung einer Gleichung, die den Druck auf dem Devisenmarkt erkHixt und deren Parameter sich im voraus eindeutig festlegen lassen. Der Zweck dieses Aufsatzes besteht zum Teil darin, die Aufmerksam- keit auf die restriktiven Annahmen zu lenken, die es Girton und Roper erm6glichen, den Drnck so zu defmieren, dab er ohne Sch~tzung gemessen werden kann. AuBerdem soll der Aufsatz zeigen, daB bei alternativen Annahmen, die zumindest auf kurze Sicht gllltiger zu sein scheinen, die Messung des Drucks auch in einem einfachen monetgren Modell ein empirisches Problem wird. Wit haben das Modell auf den effektiven Kurs des Pfund Sterling angewandt, und die Ergebnisse stittzen die An- sicht, dab das Modell yon Girton und Roper bestenfalls ein Modell ffir die lange Frist ist.

$

Rdsumd: Les mod6les mondtaires des taux de change et la pression sur le marchd des changes: Quelques limitations gdndrales et une application au taux effectif de sterling. -- L'application de la thdorie de marchd d'actifs pour l'explication des

Exchange Rates and Exchange Market Pressure 637

mouvements des monnaies se manifeste par les est imations des simples modules monfitaires qui reprdsentent l ' adapta t ion de l 'approche mon~taire de la balance des paiements au rfigime des t aux de change itexibles. Une var iante particuli~rement int&essante de l 'approche mon6taire est la d&ivat ion par Girton et Roper d 'une 6quation pour expliquer la pression sur le march~ des changes oi~ les param~tres sont ddtermin6s sans ambiguit~ ~ priori. Le but de cet article est, d 'une part, d 'a t t i rer l 'a t tent ion sur le caract~re restrictif des suppositions qui le rend possible pour Girton et Roper de d~finir la pression de telle sorte qu'elle peut ~tre mesur6e sans est imation et, d ' au t re part, de d6montrer que le mesurage de la pression devient une question empirique m~me en contexte du simple module monStaire et sous des hypotheses al ternat ives qui semblent 6tre plus valides, au moins ~. court terme. Nous avons appliqu~ le module au t aux effectif de change de sterling et les r6sultats suppor tent la proposition que le module de Girton]Roper peut 6tre r'egard6, dans le cas le plus favorable, comme rnodble de long terme.

R e s u m e n : Modelos monetarios de tipos de cambio y presiones de mercado cambiario: Algunas limitaciones y una aplicaci6n a la tasa efectiva del Sterling. - - E1 inter6s reciente en la aplicaci6n de la teoria de mercado de activos para la expli- caci6n de movimientos cambiarios, ha tornado ampl iamente la forma de la estimaci6n de modelos monetarios simples representando la adaptaci6n de regimenes de tipos de cambio flexibles al planteamiento monetario de la balanza de pagos. Una variante part icularmente interesante del planteamiento monetario es la derivaci6n de Girton y Roper de una ecuaci6n para explicar presiones det mercado cambiario cuyos parA- metros son determinados a priori sin ambigiiedades. E1 prop6sito de este artlculo es en parte l lamas la atenci6n sobre la restrict ividad de los supuestos que habil i tan a Girton y Roper obtener una definici6n de presi6n que permite ser medida sin estima- ci6n y mostrar, que sobre supuestos al ternativos que parecen ser mAs vAlidos, al menos para el corto plazo, la medici6n de presi6n se t ransforma en una pregunta emplrica, incluso en el contexto de un simple modelo monetario. Hemos aplicado e modelo al tipo de cambio efectivo del Sterling y los resultados apoyan la proposici6n que el modelo de Girton/Roper se considera mejor como un modelo de largo plazo

Wettwirtscl~tliches AEchiv Bd. CXVII. 43