mondi groupmondi group results for the · pdf fileresults for the year ended 31 december...

TRANSCRIPT

MONDI GROUPMONDI GROUPRESULTS FOR THE YEAR ENDED31 DECEMBER 201131 DECEMBER 2011

23 February 2012

Agenda

Hi hli htHighlights

Financial overview

Operational review

Capital allocationCapital allocation

Summary

Appendices

Page 2

Highlights

€622m EBIT margin % Record financial performanceUnderlying operating profit up 36%

1

Underlying operating profit

H2€502m

€441m

€294m

€458m

10.8%

Underlying operating profit up 36%

Earnings per share – alternative measure up 57%

Return on capital employed of 15%

1

H1

8.0% 7.0%

5.6%

8.2% p p y

Excellent cash generationNet debt down 39% to €831 million

2007 2008 2009 2010 2011 Free cash flow of 72 cents per share, up 72%

Significant contribution from Syktyvkar & Ś i i i t t

Underlying earnings

H2€241m €206

€340m

71.8 Cents per share

Świecie investments

Successful demerger of Mpact

I d di i

1

1

H1

€172m

€95m

€206m

46.9

33.9

45.6

Investment grade credit ratings

Proposed full year dividend of 26 euro cents per ordinary share, up 30%

2007 2008 2009 2010 2011

18.7 per ordinary share, up 30%

Page 3

Record results on strong operational performance1 From continuing operations, therefore excluding Mpact.

Agenda

Hi hli htHighlights

Financial overview

Operational review

Capital allocationCapital allocation

Summary

Appendices

Page 4

Basis of preparation

Income statement

2010 comparative figures restated to reflect continuing operations

Mpact (including gain on disposal) reflected as a discontinued operation

Statement of financial position

Mpact is included in the 2010 figuresp g

Statement of cash flows

Incl des Mpact cash flo s ntil date of demergerIncludes Mpact cash flows until date of demerger

EPS alternative measure

Adjusted to exclude Mpact earnings

Number of shares adjusted for effect of share consolidation

Reflects business of continuing operations of Mondi Group on a like for like basis

Page 5

Operating financial highlights

€ millions 2010 2011 % Ch

H22010

H12011

H22011Change 2010 2011 2011

Group revenue 5,610 5,739 2% 2,858 2,942 2,797

EBITDA 798 964 21% 427 526 438 % Margin 14.2% 16.8% 14.9% 17.9% 15.7%

Underlying operating profit 458 622 36% 254 354 268

1

2Underlying operating profit 458 622 36% 254 354 268 % Margin 8.2% 10.8% 8.9% 12.0% 9.6%

Basic earnings per share (€ cents) - alternative measure 45.6 71.8 57% 25.4 41.7 30.1

Working capital cashflows (121) (68) 44% 20 (143) 75

Cash generated from operations 778 917 18% 509 403 514 g p

Net debt (1,364) (831) 39% (1,364) (1,200) (831)

Group ROCE 12 3% 15 0% 22% 12 3% 15 2% 15 0%3Group ROCE 12.3% 15.0% 22% 12.3% 15.2% 15.0%

Page 6

Record financial performance1 EBITDA is operating profit of subsidiaries and joint ventures before special items, depreciation and amortisation, excluding Mpact. 2 Underlying operating profit is operating profit from continuing operations before special items. 3 Group return on capital employed (ROCE) is an annualised measure based on underlying operating profit plus share of associates net earnings divided by average trading capital employed before impairments and adjusted for major capital projects not yet commissioned.

Divisional underlying operating profit1

Underlying operating profit

118

128

120

140

98

81

105

87

100 100

H1 2010

H2 2010

H1 2011

55

81

71

78 73

60

80

€millions

H1 2011

H2 2011

48 46

27

35 40

€

18

1 (5) (5) (13)0

20

(20)

Uncoated Fine Paper Corrugated Bags & Coatings South Africa division Newsprint

Page 7

All major European businesses contributing meaningfully1 Underlying operating profit is operating profit of subsidiaries and joint ventures before special items.

Input costs

4 500

Variable costs Recovered paper2

160

180

3 000

3 500

4 000

n 80

100

120

140

160

/ ton

ne

1 000

1 500

2 000

2 500

€m

illion

0

20

40

60

€

2007 2008 2009 2010 2011

500

1 000

2008 2009 2010 2011 700

Chemical prices3

2007 2008 2009 2010 2011

Wood Recovered paperEnergy Other variable costsVariable selling expenses PaperPulp Merchandise

1

400

500

600

/ ton

ne

Average fibre input costs increasedWood prices up around 10% on averageAverage recycled fibre prices up over 28%

200

300

€

Chlor-Alkaline Bleaching chemicals200920082007 2010 2011

Increased pulp self-sufficiency in Syktyvkar offset increased wood costs

Merchant volumes removed with disposal of Europapier in prior period

Chlor-Alkaline Bleaching chemicals

Page 8

Increased pulp self-sufficiency improves cost position1 Other variable costs consist mainly of 70% Chemical costs and 15% Packaging costs.2 Source - PIX statistics for "OCC 1.04 dd “ 3 Source - Harriman reports

Fixed costs

2 500€ million

Fixed costs as % of revenue Fixed costs composition

2 000

2 500

20%

25%

1 000

1 500

25.3% 26.1% 23.4% 22 1%

15%

500

1 000 22.1%

5%

10%

0 2008 2009 2010 2011

Personnel costs Maintenance and th i di t t

0%2008 2009 2010 2011

Fixed costs excl. depreciation

Continued focus on cost management

other indirect costsOther net operating expenses Depreciation and amortisation

Fixed costs excl. depreciation

Ongoing improvement in fixed cost recovery

Page 9

Focused cost management delivers further results

Financial review

€ millions 2010 2011 % Change

H22010

H12011

H22011

1Underlying operating profit 458 622 36% 254 354 268

Net finance costs (106) (111) (5%) (64) (60) (51)( ) ( ) ( ) ( ) ( ) ( )

Associate net earnings 2 1 (50%) - 2 (1)

Underlying profit before tax 354 512 45% 190 296 216Underlying profit before tax 354 512 45% 190 296 216

Tax before special items (88) (102) (16%) (42) (59) (43)

Total non-controlling interest (61) (70) (15%) (34) (42) (28)

Underlying earnings from continuing operations 205 340 66% 114 195 145

Special items (after tax and minorities) (15) (53) (>100%) (22) 4 (57)

Profit from discontinued operation - Mpact 34 43 26% 23 13 30

Reported profit after tax and minority interests for total operations

224 330 47% 115 212 118

Page 10

Record bottom line profit1 Underlying operating profit is operating profit from continuing operations before special items.

Finance charges

€ millions 2010 2011 % Change

H22010

H12011

H22011

Net debt (1,364) (831) 39% (1,364) (1,200) (831)

Total investment income (31) (30) (3%) (17) (15) (15)( ) ( ) ( ) ( ) ( ) ( )Total interest expense 152 141 7% 78 74 67 Interest expense, net of investment income 121 111 8% 61 59 52 Less: interest capitalised (8) - (100%) (1) (1) 1 Net debt finance charges and other financial 113 111 2% 60 58 53Net debt finance charges and other financial 113 111 2% 60 58 53 Foreign currency losses / (gains) (7) - (100%) 4 2 (2)Net finance costs 106 111 (5%) 64 60 51

Net finance charges upLower average net debt, offset by

Effective interest rate (before capitalised interest) 8.0% 8.6% 8.1% 8.3% 9.0%

Lower average net debt, offset byZero capitalised interestForeign exchange effectsMarginally higher effective net interest ratesa g a y g e e ec e e e es a es

85% of Group borrowings are at fixed interest ratesCash interest paid down 9% at €106 million

Page 11

Net finance charges marginally up

Taxation and non-controlling interests

Taxation Non-controlling interestsTaxation Non controlling interests€ millions 2010 2011 %

Change€ millions 2010 2011 %

Change

Underlying tax charge 88 102 (16%)

Tax on special items (6) (2) 67%

Taxation charge 82 100 (22%)

Non-controlling share before special items 62 70 (13%)

Non-controlling share of special items (1) - (100%)

g ( )

Underlying effective tax rate 25% 20%

Cash tax rate 12% 17%

Profit attributable to non-controlling interests 61 70 (15%)

Reduction in effective tax rate before special items to 20%

Strong results across most operations with non-controlling interests (notably Świecieand Ružomberok)

Cash tax rate 12% 17%

Increased profitability in regions with lower tax ratesBenefit from tax incentives mainly in Poland

and Ružomberok)

Page 12

Further reduction in effective tax rate

Special items

Operating items (€54 million loss): Non-operating items (€1 million loss):Operating items (€54 million loss):Uncoated fine paper (€2 million gain)

release of restructuring provisions no longer

Non operating items (€1 million loss):Corrugated (€3 million gain)

finalisation of sale of Frohnleiten and UK required

Bags & Coatings (€23 million loss)

reversal of restructuring provisions no longer

corrugated plants

Bags & Coatings (€4 million loss)

sale of Unterland flexible packagingreversal of restructuring provisions no longer required

Restructuring activities in Coatings & Consumer Packaging

sale of Unterland, flexible packaging business

Consumer Packaging

asset impairments in Kraft paper

Newsprint (€33 million loss)

impairment of Aylesford assets

Page 13

€55 million special items, of which €48 million non-cash

Cash flow

€ millions 2010 2011 % Change

H22010

H12011

H22011

EBITDA (including Mpact) 882 996 13% 477 562 434 Working capital movements (121) (68) 44% 20 (143) 75 Other operating cash flow items 17 (11) (>100) 12 (16) 5

1

Other operating cash flow items 17 (11) (>100) 12 (16) 5Cash generated from operations 778 917 18% 509 403 514 Dividends from financial investments and associates 3 2 (33%) 1 - 2 Taxes paid (47) (85) (81%) (11) (45) (40)Taxes paid (47) (85) (81%) (11) (45) (40)Net cash inflow from operating activities 734 834 14% 499 358 476 Capital expenditure, excl. major projects (234) (231) 1% (141) (109) (122)Investment in forestry assets (46) (42) 9% (25) (23) (19)Investment in forestry assets (46) (42) 9% (25) (23) (19)Proceeds on sale of fixed assets and other items 13 9 (31%) 6 12 (3)

467 570 22% 339 238 332Major expansionary projects' expenditure (160) (32) 80% (68) (18) (14)Major expansionary projects expenditure (160) (32) 80% (68) (18) (14)Acquisitions (2) (14) (>100) (13) (12) (2)Disposals 100 (21) (>100) 36 14 (35)N t h fl ft i ti ti iti 405 503 24% 294 222 281Net cash flow after investing activities 405 503 24% 294 222 281

Page 14

Significant cash generation1 EBITDA is operating profit before special items, depreciation and amortisation, including Mpact up to date of demerger.

Working capital

Working capital cash flows2Working capital management1

17.2% 1,000.0

1,200.0

g pg p g

€248m

14.6%

11.9%

10.0% 10.0% 600.0

800.0

1,000.0

10%

12%€97m

9.9%

200.0

400.0

10%

€27m

2006 2007 2008 2009 2010 2011

-2006 2007 2008 2009 2010 2011

Working Capital

(€82m)(€121m)

(€68m)

g pWorking Capital % of Turnover

Working capital at lower end of target range of 10% to 12% of revenueDecreased demand and selling prices in second halfActive inventory management

Page 15

Working capital management an ongoing focus1 Excluding Mpact in 2011

2 Including Mpact

Capital expenditure

Capital expenditure Cash spend, excluding major

200%

350

400projects and Mpact was 63% of depreciation (2010: 63%)

13 135

189 150%

250

300

ions

25627

179

121 92

68

18 14

100%

150

200€m

illi

114

182 194

116 106 93 141

108 123

18

0%

50%

0

50

100

0%0H1

2007H2

2007H1

2008H2

2008H1

2009H2

2009H1

2010H2

2010H1

2011H2

2011

Capital expenditure, excl. Intangible assets, excl. major projectsMajor projectsDepreciation as % of CAPEX, excl. major projects

Page 16

Capital expenditure down as major projects completed

Debt facilities & net debt

€ millions 2010 2011 % Change

H22010

H12011

H22011

Net debt (1 364) (831) 39% (1 364) (1 200) (831)

Committed facilities 2 889 1 839 (36%) 2 889 1 897 1 839Committed facilities 2 889 1 839 (36%) 2 889 1 897 1 839 Of which undrawn 1 481 889 (40%) 1 481 781 889

Gearing (Net debt / Trading capital employed) 30% 22% 30% 27% 22%

Strong cash flow generation and Mpact demerger effect (€172 million) reduces net debt

Net debt / 12 month trailing EBITDA (times) 1.5 0.8 1.5 1.3 0.8

Strong cash flow generation and Mpact demerger effect (€172 million) reduces net debt

New €750 million 5 year syndicated revolving credit facility to refinance €1.55 billion “demerger” facilityg y

New facilities of €140 million from EIB1 & EBRD2

Average maturity of committed facilities is 4.3 years (2.6 years at 31 December 2010)Average maturity of committed facilities is 4.3 years (2.6 years at 31 December 2010)

Page 17

Robust financial structure1 European Investment Bank

2 European Bank for Reconstruction and Development

Dividends

Final dividend of 17.75 euro cents per Dividends per shareshare recommended (26 euro cents for the year)

Di id d f 2 8 ti26

25

30

p

Dividend cover of 2.8 times

Record date 13 April 2012

23

20 20

25

hare

Payment date 10 May 201215.7

16 5

17.75

12.7 15

r cen

ts p

er s

h

7.3 7.7 8.25

5.0

7.0

16.5 9.5

5

10 Eur

2.5 3.5

-

5

2007 2008 2009 2010 2011

Interim Dividend Final Dividend

Page 18

Full year dividend up 30%

Agenda

Hi hli htHighlights

Financial overview

Operational review

Capital allocationCapital allocation

Summary

Appendices

Page 19

Uncoated Fine Paper

Continued strong performanceP iti t di i t

Underlying operating profit

Positive trading environmentAnnual production records achievedLow cost baseH2€179m

€205m

14.3%

EBIT margin %

Benefiting from first full year contribution from Syktyvkar mill modernisation

I d t f d t l€99m

€126m €146m

8.1%

10.8% 11.8%

%

Industry fundamentalsDemand

Structural decline in Western Europe, continued h i E E

H15.9%

growth in Eastern Europe

SupplyIndustry rationalisation continuing

2007 2008 2009 2010 2011

Closures announced amounting to approximately 700kt (± 7% of European capacity)

Page 20

Delivering strongly

Uncoated Fine Paper –Performance vs IndustryPerformance vs Industry

Mondi and Industry sales volume growth in Mondi’s ROCE (%) Uncoated fine paperMondi and Industry sales volume growth in 2011 vs 2007 and 2010 (%)

2

11

Mondi’s ROCE (%), Uncoated fine paper price (EUR/tonne)

1%2%

11 vs 07 11 vs 10

H201

880

900 25%

€/tonne % ROCE

1%

-2%

8 2%

11.4%

14.5%16.9% 16.7%

780

800

820

840

860

10%

15%

20%

-11%

8.2%

700

720

740

760

0%

5%

2007 2008 2009 2010 2011Industry MondiMondiIndustry 2007 2008 2009 2010 2011

Annual ROCE A4 B-copy

Page 21Source: PIX – FOEX Indexes Ltd, Euro-Graph UFP deliveries to Europe and overseas, Pyrbelisk and Mondi estimates. Mondi UFP sales exclude SA and Hadera volumes and include Szolnok volumes.

Benefiting from exposure to higher growth geographies

Corrugated

Continued improvement in performanceImproved trading conditions, although

€178m EBIT margin %

Underlying operating profit

Improved trading conditions, although slow down in demand in H2 2011Converting plants delivered pleasing margin improvement and improved

H2€133m

€119m8.2%

9.6% 12.8%

margin improvement and improved contributionRebuilt Syktyvkar VCB machine H1€49m

€119m 8.2%

3.2%

2.2% contributed stronglyIndustry fundamentals

Demand

€23m

2007 2008 2009 2010 2011Demand

Structural growth

Supply1.41.5

Selling prices - indexed

Announced recycled containerboard net capacity increases of 1.2 million tpa (excluding Russia)2 unchanged

N K ftli it0.9

11.11.21.31.4

No new Kraftliner capacity

0.50.60.70.8

Kraftliner - indexedWhite-top Kraftliner - indexedRCB / Recovered paper differential - indexed

2006 2007 2008 2009 2010 2011

11

1

Page 22

Well invested capital base delivers excellent returns1 Source: PIX – FOEX Indexes Ltd2 Mondi estimates

Corrugated –Performance vs IndustryPerformance vs Industry

VCB Mondi and Industry sales volume Mondi’s ROCE (%), kraftliner price and RB ygrowth in 2011 vs 2007 and 2010 (%) fluting – OCC price differential (EUR/tonne)

11 vs 07 11 vs 10

5%

15.1% 14.9%

18.5%H2

600

700

16%

18%

20%

€/tonne % ROCE

-2%

2%

0%

5 1% 3 6%300

400

500

6%

8%

10%

12%

14%

MondiIndustry

-4%

MondiIndustry

-4%

5.1% 3.6%

100

200

0%

2%

4%

2007 2008 2009 2010 2011yy

Industry incl. Russian market Industry excl. Russian market

Annual ROCE Kraftliner RB Fluting-OCC differential

Page 23Source: PIX – FOEX Indexes Ltd, Cepi VCB deliveries to Europe and overseas, RISI and Mondi estimates.

Benefiting from exposure to higher growth geographies

Bags & CoatingsKraft Paper

20% increase in average selling prices€228m EBIT margin %

Underlying operating profit

g g p

Strong sales volumes in 1st half

Significant downtime in 2nd half – ±10% of annual

H2€154m €159m

€133m Significant downtime in 2 half ±10% of annual capacity

Some price weakness going into 2012H1

€82m 7.6% 7.4%

4.5% 6.0%

9.2%

Industry fundamentals2007 2008 2009 2010 2011

Evidence of destocking coming to an end

No new capacity

Unbleached sack kraft prices

€/to

nne

average

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Page 24

Record financial performance, despite challenging 2nd halfSource : Mondi - Nominal prices.

Bags & Coatings (continued)

Industrial BagsM i i t

Sales revenue mix (%)Margin improvements

Selling price increases

More than offsetting higher paper input costsg g p p p

Restructuring following Smurfit Kappa acquisitions delivering positive returns

Coatings & Consumer Packaging61%

39%

Restructuring initiatives completed - delivering improved performance

Some new lines to start up in 2012Some new lines to start-up in 2012

Consumer packaging demand typically stable through down cycles. Strong structural growth.Kraft Paper & Industrial Bags

Coatings & Consumer packagingCoatings demand typically more cyclical, although still overall structural growth

Coatings & Consumer packaging

Page 25

Strong and stable earnings generators

Bags & Coatings –Performance vs IndustryPerformance vs Industry

Sack kraft paper Mondi and Industry sales Mondi’s ROCE (%), sack kraft paper prices

900 0

yvolume growth in 2011 vs 2007 and 2010 (%) (EUR/tonne) and indexed bags price (%)

19.0%

700 0750.0800.0850.0900.0

15.0%

20.0%0.4%

0.0%

-0.2%

11 vs 07 11 vs 10

11.4% 11.1%

7.5%

11.8%

500 0550.0600.0650.0700.0

0 0%

5.0%

10.0%

2011

2010

500.00.0%2007 2008 2009 2010 2011

Annual ROCE Unbleached sack Kraft (€/tonne)

-7.0%

2009

2008

2007

MondiIndustryMondiIndustry

2007

Page 26Source: Mondi nominal indexed prices, Eurokraft sack kraft paper deliveries to Europe and overseas.

Benefiting from leading market position and forward integration

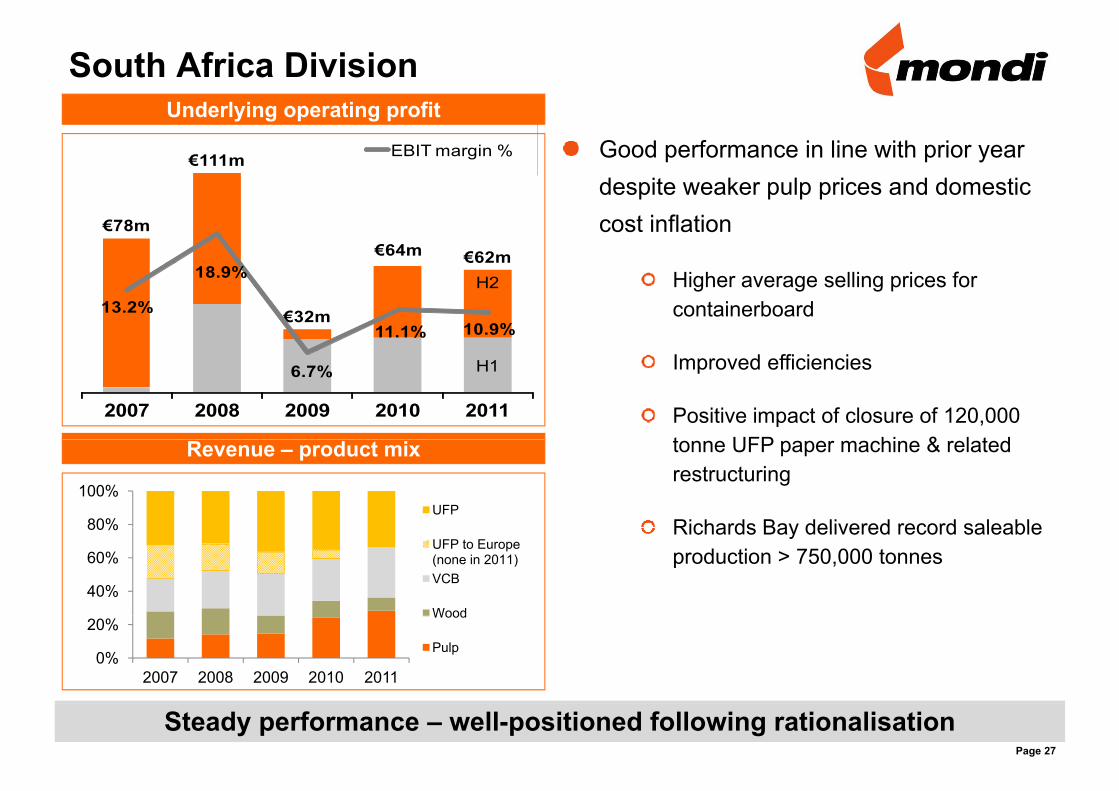

South Africa Division

Good performance in line with prior year €111m EBIT margin %

Underlying operating profit

despite weaker pulp prices and domestic cost inflation€78m

€64m €62m Higher average selling prices for containerboard

H2

€32m 13.2%

18.9%

11.1% 10.9%

Improved efficiencies

Positive impact of closure of 120,000 t UFP hi & l t d

H1

2007 2008 2009 2010 2011

6.7%

tonne UFP paper machine & related restructuring

Richards Bay delivered record saleable80%

100%UFP

Revenue – product mix

Richards Bay delivered record saleable production > 750,000 tonnes

40%

60%

80%UFP to Europe (none in 2011)VCB

Wood

0%

20%

2007 2008 2009 2010 2011

Wood

Pulp

Page 27

Steady performance – well-positioned following rationalisation

Agenda

Hi hli htHighlights

Financial overview

Operational review

Capital allocationCapital allocation

Summary

Appendices

Page 28

Free cash flow priorities

Maintain investment grade credit metrics

1 Selective capital investment opportunities, mainly

around cost optimisation

Support dividends

M&A, if appropriate

2 Increased shareholder distributions

Page 29

Continued disciplined cash flow allocation

Capital investment opportunities

Syktyvkar Bark Boiler & Pulp Dryer

Approved

Syktyvkar Bark Boiler & Pulp Dryer

Świecie Biomass DryerApproved± €170 million investment Stambolijski Steam Turbine & Recovery Boiler Economiser

Two to three years to completion Frantschach Recovery Boiler

ROCE > 40%Richards Bay Steam Turbine

Under consideration Various

Three to four years to completion

Up to ±€250 million

Page 30

Focus on high return energy and de-bottlenecking opportunities

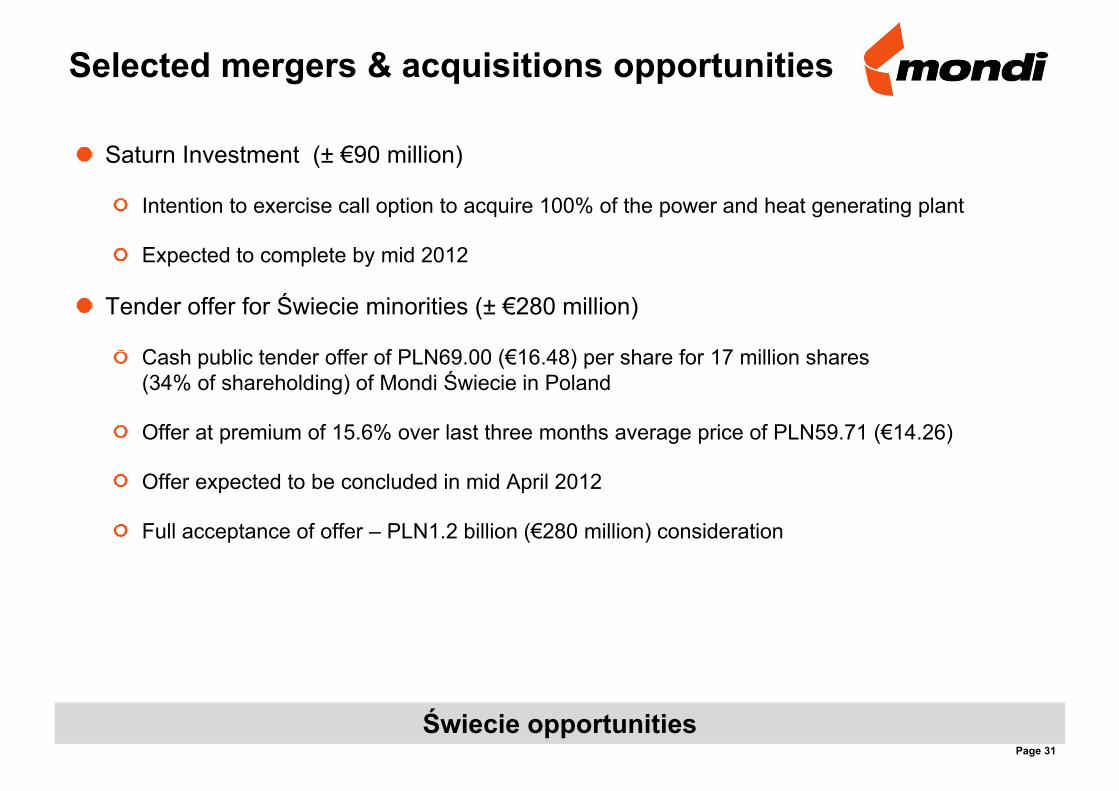

Selected mergers & acquisitions opportunities

Saturn Investment (± €90 million)

Intention to exercise call option to acquire 100% of the power and heat generating plant

Expected to complete by mid 2012p p y

Tender offer for Świecie minorities (± €280 million)

C h bli t d ff f PLN69 00 (€16 48) h f 17 illi hCash public tender offer of PLN69.00 (€16.48) per share for 17 million shares (34% of shareholding) of Mondi Świecie in Poland

Offer at premium of 15.6% over last three months average price of PLN59.71 (€14.26)Offer at premium of 15.6% over last three months average price of PLN59.71 (€14.26)

Offer expected to be concluded in mid April 2012

F ll acceptance of offer PLN1 2 billion (€280 million) considerationFull acceptance of offer – PLN1.2 billion (€280 million) consideration

Page 31

Świecie opportunities

Agenda

Hi hli htHighlights

Financial overview

Operational review

Capital allocationCapital allocation

Summary

Appendices

Page 32

Summary

Very strong performance – delivering ROCE of 15%

Strong operational performance

Investment grade credit ratings

Successful demerger of Mpact leading to a further refined portfolio

Cash utilised toStrengthen balance sheet

Invest in selected high return projects

Grow dividendGrow dividend

OutlookMacroeconomic risks remainMacroeconomic risks remain

Order books improved & prices stabilised

Price increases announced in certain grades

Supply side fundamentals remain good

Page 33

Continuing to deliver

Agenda

Hi hli htHighlights

Financial overview

Operational review

Capital allocationCapital allocation

Summary

Appendices

Page 34

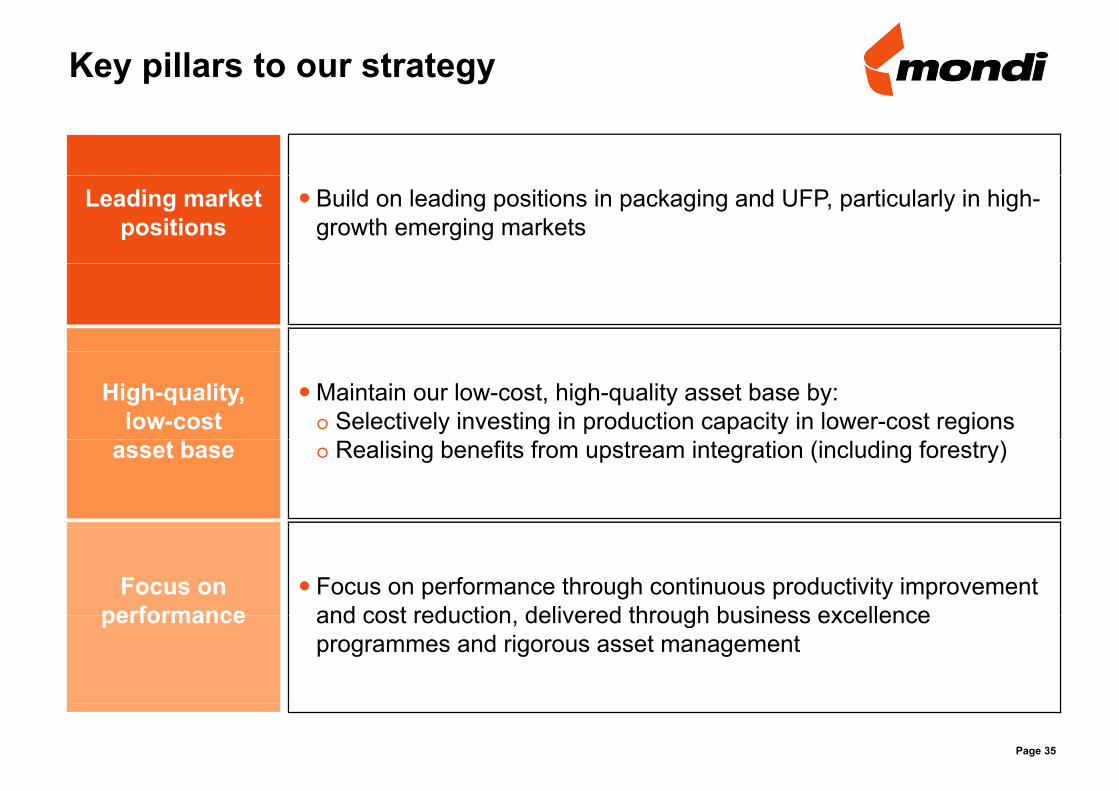

Key pillars to our strategy

Leading market positions

Build on leading positions in packaging and UFP, particularly in high-growth emerging markets

High-quality, low-cost

Maintain our low-cost, high-quality asset base by: Selectively investing in production capacity in lower-cost regions

asset base Realising benefits from upstream integration (including forestry)

Focus on performance

Focus on performance through continuous productivity improvement and cost reduction delivered through business excellenceperformance and cost reduction, delivered through business excellence programmes and rigorous asset management

Page 35

Mondi at a glanceSouth Africa NewsprintUFP

€1 4B €0 6B €0 2B

gBags & Coatings

€2 5B€1 4B

Corrugated

24%

41%

9%3%

2011Sales 1

€1.4B €0.6B €0.2B€2.5B€1.4B

23%41%

2011 EBIT %

14.3% 9.2%12.8% 10.9% (11.1)%

P d tProducts

Positions in relevant

No. 1 in Newsprint in South Africa2

No. 1 in Office Paper and UFP in Europe 3

Europe South Africa Europe/SA No. 1 in Kraft Paper in

Europe2 No. 2 Virgin

containerboard i E 2

No. 1 in Office Paper in SA 2

in relevant markets(2011)

Europe 3 No. 1 in Industrial Bags in Europe3

No. 1 in Commercial release liner in Europe3

in Europe 2

No. 1 Recycled containerboard in Emerging Europe2

No. 1 Corrugated Packaging in Emerging

No. 1 in White Top Kraftliner in SA 2

Page 361 Segment revenues, including inter-segment revenues. EBIT % is before special items. 2 Based on production capacity. 3 Based on sales volume. 4 Based on production.Sources: RISI, Pöyry Forest Industry Consulting, Freedonia, BMI Foodpack, PAMSA, Mondi.

Packaging in Emerging Europe 4

Focus on Packaging and UFP in emerging markets1emerging markets1

Revenue by destination Revenue by origin Net operating assets

29%44%

71%56%

44%50%50%

Mature marketsEmerging markets

Mature marketsEmerging markets

Mature marketsEmerging markets

14%

Virgin-based production Revenue by product

24%

23%

15%

14%

81%

19% Corrugated productsUncoated fine paper

Kraft paper & industrial bags

Coatings & consumer packaging23%24%

Mature marketsEmerging markets

Other

Page 37

Competitive cost base1 Mondi 2011 data, excluding Mpact.

Emerging market asset base leads to low cost positions across the group’s main grades…

+

Leading market positions

Grade 1st Quartile 2nd Quartile 3rd Quartile 4th Quartile

Percentage of Mondi's capacity in overall cost curve at Q3 2011 1

+High quality, low cost asset base

Unbleached Sack Paper 40% - 35% 26%NSSC Fluting 100% - - -Unbleached Kraftliner 100%

Low cost asset base

Unbleached Kraftliner 100% - - -White Top Kraftliner 100% - - -BHKP (Pulp)2 - 100% - -Recycled Fluting 75% - 25% -UFP 61% 10% 21%3 8%3

1 Delivered to Frankfurt except where notedDelivered to Frankfurt except where noted2 Delivered to Rotterdam3 Includes specialities

Page 38Source: RISI and Mondi estimates.

High quality, low cost, well invested asset base

Integrated value chain 2011

+

Leading market positions

Pulp Virgin Containerboard

+High quality, low cost asset base

Low cost asset base

Upstream production cost advantages

Kraft Paper Recycled Containerboard

g

Page 39Source: Mondi – 2011, excluding Mpact

Exploiting benefits of upstream integration

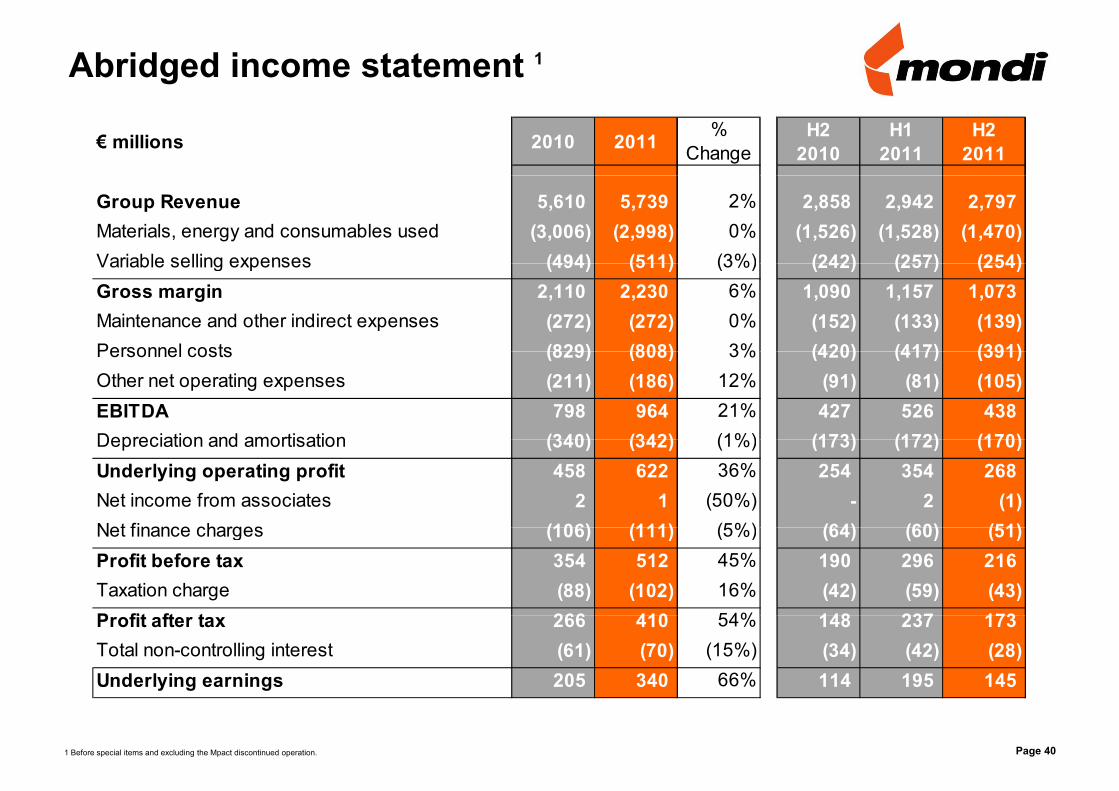

Abridged income statement 1

€ millions 2010 2011 % Change

H22010

H12011

H22011

Group Revenue 5,610 5,739 2% 2,858 2,942 2,797 Materials, energy and consumables used (3,006) (2,998) 0% (1,526) (1,528) (1,470)Variable selling expenses (494) (511) (3%) (242) (257) (254)Variable selling expenses (494) (511) (3%) (242) (257) (254)Gross margin 2,110 2,230 6% 1,090 1,157 1,073 Maintenance and other indirect expenses (272) (272) 0% (152) (133) (139)Personnel costs (829) (808) 3% (420) (417) (391)Personnel costs (829) (808) 3% (420) (417) (391)Other net operating expenses (211) (186) 12% (91) (81) (105)EBITDA 798 964 21% 427 526 438 Depreciation and amortisation (340) (342) (1%) (173) (172) (170)Depreciation and amortisation (340) (342) (1%) (173) (172) (170)Underlying operating profit 458 622 36% 254 354 268 Net income from associates 2 1 (50%) - 2 (1)Net finance charges (106) (111) (5%) (64) (60) (51)Net finance charges (106) (111) (5%) (64) (60) (51)Profit before tax 354 512 45% 190 296 216Taxation charge (88) (102) 16% (42) (59) (43)P fit ft t 266 410 54% 148 237 173Profit after tax 266 410 54% 148 237 173Total non-controlling interest (61) (70) (15%) (34) (42) (28)Underlying earnings 205 340 66% 114 195 145

Page 401 Before special items and excluding the Mpact discontinued operation.

Exchange rates

2010 2011 % Change

H22010

H12011

H22011

Closing rates against the euro

South African rand 8.86 10.48 18% 8.86 9.86 10.48 Pounds sterling 0.86 0.84 (3%) 0.86 0.90 0.84 Polish zloty 3.97 4.46 12% 3.97 3.99 4.46 Russian rouble 40.82 41.77 2% 40.82 40.40 41.77 US dollar 1.34 1.29 (3%) 1.34 1.45 1.29 Czech koruna 25.06 25.79 3% 25.06 24.34 25.79 Turkish lire 2.07 2.44 18% 2.07 2.35 2.44

Average rates for the period against the euro

South African rand 9.70 10.10 4% 9.42 9.69 10.51 Pounds sterling 0.86 0.87 1% 0.85 0.87 0.87 Polish zloty 3.99 4.12 3% 3.99 3.95 4.29 Russian rouble 40.27 40.88 2% 40.66 40.14 41.62 US dollar 1.33 1.39 5% 1.33 1.40 1.38 Czech koruna 25.29 24.59 (3%) 24.85 24.35 24.84

Page 41

Turkish lire 2.00 2.34 17% 2.00 2.21 2.34

Production volumes

€ millions 2010 2011 % Change

H22010

H12011

H22011

Europe & InternationalUncoated fine paper Tonnes 1 524 225 1 400 991 (8%) 733 477 712 886 688 105 Containerboard Tonnes 1 939 935 2 009 984 4% 931 630 991 970 1 018 014 Kraft paper Tonnes 984 607 955 741 (3%) 518 451 535 238 420 503 Corrugated board and boxes m m² 1 308 1 213 (7%) 595 609 604 Industrial bags m units 3 850 3 958 3% 1 992 2 050 1 908 Coating and release liners m m² 3 187 3 357 5% 1 586 1 797 1 560 gNewsprint Tonnes 197 601 199 337 1% 99 550 97 931 101 406

South Africa Uncoated fine paper Tonnes 276 957 233 837 (16%) 124 294 114 686 119 151Uncoated fine paper Tonnes 276 957 233 837 (16%) 124 294 114 686 119 151 Containerboard Tonnes 259 785 257 680 (1%) 130 955 126 516 131 164 Wood chips (bone dry) Tonnes 280 154 206 150 (26%) 150 638 101 454 104 696 External hardwood pulp Tonnes 223 016 320 817 44% 98 384 128 882 191 935

Newsprint JVs (attributable share)Aylesford Tonnes 187 971 188 536 0% 95 396 95 955 92 581 Mondi Shanduka Newsprint Tonnes 126 530 124 914 (1%) 61 554 61 548 63 366 p ( )

Page 42