monarques resources inc. (tsxv: mqr) – initiating - … 5, 2014 2014 ... of the richest mining...

TRANSCRIPT

Siddharth Rajeev, B.Tech, MBA, CFA Analyst

September 5, 2014

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com

PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

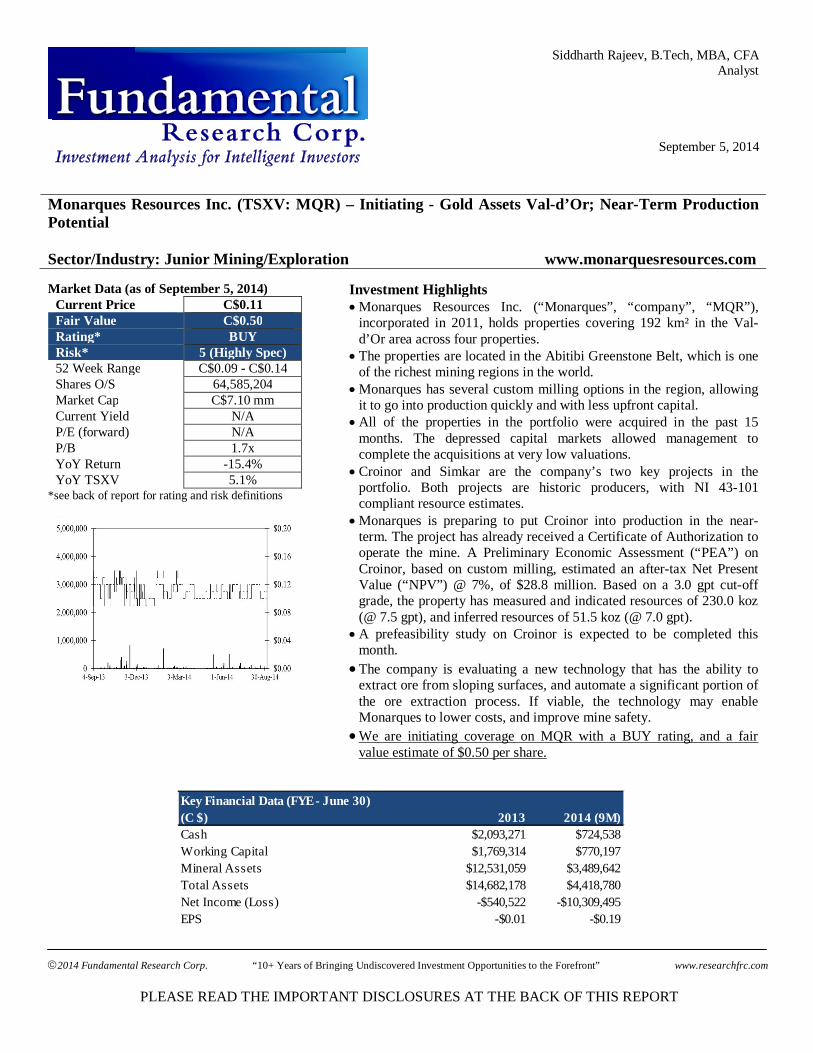

Monarques Resources Inc. (TSXV: MQR) – Initiating - Gold Assets Val-d’Or; Near-Term Production Potential Sector/Industry: Junior Mining/Exploration www.monarquesresources.com Market Data (as of September 5, 2014)

Current Price C$0.11 Fair Value C$0.50 Rating* BUY Risk* 5 (Highly Spec) 52 Week Range C$0.09 - C$0.14 Shares O/S 64,585,204 Market Cap C$7.10 mm Current Yield N/A P/E (forward) N/A P/B 1.7x YoY Return -15.4% YoY TSXV 5.1%

*see back of report for rating and risk definitions

Investment Highlights Monarques Resources Inc. (“Monarques”, “company”, “MQR”),

incorporated in 2011, holds properties covering 192 km² in the Val-d’Or area across four properties.

The properties are located in the Abitibi Greenstone Belt, which is one of the richest mining regions in the world.

Monarques has several custom milling options in the region, allowing it to go into production quickly and with less upfront capital.

All of the properties in the portfolio were acquired in the past 15 months. The depressed capital markets allowed management to complete the acquisitions at very low valuations.

Croinor and Simkar are the company’s two key projects in the portfolio. Both projects are historic producers, with NI 43-101 compliant resource estimates.

Monarques is preparing to put Croinor into production in the near-term. The project has already received a Certificate of Authorization to operate the mine. A Preliminary Economic Assessment (“PEA”) on Croinor, based on custom milling, estimated an after-tax Net Present Value (“NPV”) @ 7%, of $28.8 million. Based on a 3.0 gpt cut-off grade, the property has measured and indicated resources of 230.0 koz (@ 7.5 gpt), and inferred resources of 51.5 koz (@ 7.0 gpt).

A prefeasibility study on Croinor is expected to be completed this month.

The company is evaluating a new technology that has the ability to extract ore from sloping surfaces, and automate a significant portion of the ore extraction process. If viable, the technology may enable Monarques to lower costs, and improve mine safety.

We are initiating coverage on MQR with a BUY rating, and a fair value estimate of $0.50 per share.

Key Financial Data (FYE - June 30)(C $) 2013 2014 (9M)Cash $2,093,271 $724,538Working Capital $1,769,314 $770,197Mineral Assets $12,531,059 $3,489,642Total Assets $14,682,178 $4,418,780Net Income (Loss) -$540,522 -$10,309,495EPS -$0.01 -$0.19

Page 2

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Overview

Monarques Resources, incorporated in February 2011, is a junior gold exploration and development company focused on gold projects along the Cadillac trend in the Val-d’Or area of Quebec, Canada. The company went public through a spin out from Nemaska Lithium Inc. (TSX-V: NMX) in 2011. In exchange for Nemaska’s base metal and precious metal properties in the James Bay region of Quebec, Monarques granted 18.75 million shares @ $0.40 per share (valued at $7.50 million) to Nemaska. Nemaska continues to be the major shareholder of the company, holding 15.85 million shares, or 25% of the total outstanding shares. In late 2012, the company hired Jean-Marc Lacoste as the new Chief Executive Officer (“CEO”). His most recent success story was the sale of Golden Goose Resources Inc. (then public), to Prodigy Gold in 2010. Golden Goose’s primary asset was the past producing Magino mine in northern Ontario, which currently has an indicated resource of 6.25 Moz of gold. Prodigy Gold was subsequently acquired by Argonaut Gold (TSX: AR) in 2012 for $341 million. Through a series of acquisitions (13 properties) since he took over Monarques, Jean-Marc Lacoste changed the company’s focus to gold projects in Val-d’Or. In June 2014, the company consolidated the 13 properties into four properties. The following map shows the locations of the four projects that are currently in Monarques’ portfolio - Croinor Gold, Simkar Gold, Regcourt Gold, and Belcourt Gold. The region has multiple producers with excess mill capacity, offering Monarques several opportunities to go into production quickly, and with less upfront capital, using custom milling.

Source: Company

The properties are located in the Abitibi Greenstone Belt, which is a highly productive gold

Page 3

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Croinor Gold

and base-metal producing region. The Abitibi Greenstone Belt, which extends in an east-west direction for over 500 km from northeast Quebec to west of Timmins, Ontario, is one of the richest mining regions, and one of the largest greenstone belts in the world. Monarques’ properties currently cover 192 km² in Val-d’Or consisting of 593 claims. According to management, the properties have a total of $9.5 million in accumulated tax credits.

Source: Company

Croinor and Simkar are the two key projects in the portfolio. Monarques is expecting to put Croinor into production in the near-term. A 2011/2012 Preliminary Economic Assessment (“PEA”) conducted on Croinor, based on custom milling, showed robust economics. The PEA estimated an initial capital cost of $21 million. Based on a 3.0 gpt cut-off grade, the property has a NI 43-101 measured and indicated resource of 230.0 koz (@ 7.5 gpt), and inferred resource of 51.5 koz (@ 7.0 gpt). Considering that several existing mills in the region, operated by mid-size gold producers, are running out of ore, and are currently seeking custom milling options, we believe Monarques can position itself as a good acquisition candidate if it is able to prove up resources on its properties. Property Overview The 100% owned Croinor project covers 128 km² on 297 mineral claims, and a mining lease. The mining lease (BM 862) was registered in 2004, and expires in 2024. The project is comprised of four key properties - Croinor, Croinor-Pershing, Lac Tevernier and Bel-Rive properties. Monarques is currently primarily focused on the Croinor deposit. The properties, located approximately 70 km east of Val-d’Or, are accessible by all-weather roads through the year. Monarques acquired a 100% interest in the project in two stages.

Page 4

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

The first 50% was acquired in October 2013 through bankruptcy proceedings of Blue Note Mining Inc. (TSXV: BNT), and its wholly owned subsidiary, X-Ore Resources. Monarques acquired X-Ore Resources which owned a 50% interest in Croinor, for $110,000 in cash, and 1.46 million shares of Monarques, for a total valuation of $0.31 million. A 1.5% NSR is applicable on 44 claims and the mining lease. Blue Note Mining had acquired X-Ore Resources in 2009 for approximately $8 million. X-Ore shares were trading on the TSX Venture at that time. X-Ore (previous name - South-Malartic Exploration Inc.) has been holding the Croinor property since the late 1990s.

The other 50% was acquired in May 2014, from Critical Elements Corporation (TSXV: CRE) for 0.50 million Monarques shares (@ $0.15 per share), and eleven of Monarques’ James Bay properties to CEC. Critical Elements had originally optioned 50% of the property from X-Ore in 2007.

The following map shows the Croinor claims:

Claim map of the Croinor Property

Source: Technical Report (InnovExplo) Geology The Croinor property is underlain by two major lithological packages: the volcanic Assup Domain in the north, and the sedimentary Garden Island Domain in the south (see map below). The map also shows the location of Croinor, and the other key deposits in the

Page 5

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

region. Note that the resource estimates, and ownership information in the map, are not current.

Source: http://www.ditem.com/bruellpropertymap.pdf

The Croinor deposit is characterized by gold-rich lenses consisting of quartz-carbonate-tourmaline-pyrite veins, altered pyritic host rock material, and / or tectonic breccia. Two types of veins are observed on the property: shear veins, and subhorizontal tension veins. Gold is typically found as inclusions within pyrite grains or along its boundaries, or within fractures cutting pyrite.

The deposit is hosted by the synvolcanic Croinor sill. This dioritic sill is approximately 60-120 m thick, and hosted within volcanic rocks of the Assup Domain. Gold-hosting structures, within the sill, consist of a series of narrow breaks and reverse shears with dips of 25° to 60° to the north. According to InnovExplo’s technical report (dated April 4, 2012), “The lenses can generally be followed from one section to another (10-metre sections) over lateral distances varying from several tens of metres up to 600 metres.” Approximately 54 gold-rich lenses have so far been identified on the property. History Since the discovery of the project in 1940, approximately 1,219 holes, and 122,339 m of drilling have been conducted on the property. Several companies have conducted exploration and production on the property. The table below highlights past production from the project. A total of 138,441 tonnes were mined, at an average net grade of 3.3 gpt, for 14,750 recovered ounces.

Page 6

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Past Production on the Croinor Project

Source: Technical Report (InnovExplo)

The highest production period was 2003-2005, when approximately 75,752 tonnes @ 3.33 gpt (7,860 oz) was produced by X-Ore Resources (formerly Exploration Malartic-Sud Inc. / South-Malartic Exploration Inc.), primarily from the west and centre pits. The second best production period was 1996-1997, when Goldust Mines Ltd. produced 51,010 tonnes for 5,536 oz of recovered gold. Both production periods used surface mining and custom milling.

The Croinor deposit is serviced by a ramp measuring 300 m (long) by 4 m (high) by 4.5 m (wide), that extends to level 125 (38m), and by a three compartment shaft extending 195 m deep. As shown in the image below, development was completed on four levels: 496 m on level 125; 560 m on level 250; 233 m on level 375; and 730 m on level 500.

Existing Infrastructure

Source: Technical Report (InnovExplo)

The mine is currently flooded to the portal entrance. The cost to dewater the mine is estimated to be $1.25 million.

The following table shows the key drilling activities on the property since 1998.

Page 7

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Year Description1998 9 drill holes for 2,150 m2000 52 drill holes for 6,000 m2001 58 drill holes for 4,087 m

2002 - 2003 198 drill holes for 24,659 m2004 31 drill holes and 5 extensions (4,094 m)

2007-2008 16,481 m of drilling2010 19 drill holes for 2,789 m2011 42 drill holes for 13,046 m

Source: Technical Report (InnovExplo)

There has been no drilling on the project since the 2011 drill program.

Resource Estimate Based on historic drilling on the property, InnovExplo arrived at the following NI 43-101 resource estimate on Croinor: the technical report, published in April 2012, by InnovExplo, estimates measured and indicated resources of 960,700 tons @ 7.45 gpt for 230,000 oz, and inferred resources of 227,800 tons @ 7.03 gpt for 51,500 oz. This is based on a 3 gpt cut-off grade.

Source: Company

The estimate was based on 1,219 surface and underground diamond drill holes covering an east-west distance of 1,530 m. InnovExplo’s model was based on 1,560 m strike length, 230 m wide, and up to 500 m depth below surface. The following image shows a 3D isometric view of the deposit.

Page 8

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: Technical Report (InnovExplo)

The following image shows the influence of the resources.

Source: Technical Report (InnovExplo)

Metallurgical tests Various metallurgical tests have been conducted on the ore from Croinor. The following highlights the key results:

various bulk samples from the property from 1972 – 1997, indicated recovery rates of 87% - 97%

two samples from two different zones in 2001-2003, gave recovery rates of 94.9% - 97% for flotation, and 95.1% - 99.1% for cyanidation

milling from the Camflo mill for ore (2004 – 2005) produced an average recovery of 97% (discussed below)

Surrounding Mills There are several operating mills in the region that Monarques may use for custom milling

Page 9

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

ore from its properties. InnovExplo’s technical report highlights four such mills located within 120 km from Croinor.

Source: Company

The Beacon Gold (900 tpd capacity) was owned by North Star Mining. North Star

Mining went into bankruptcy in 2010. The mill is currently owned by a group of private investors.

The Aurbel Gold mill (1,200 tpd) is owned by QMX Gold Corporation (TSXV: QMX; formerly Alexis Minerals Corporation). QMX recently announced that they will seek custom milling options as they mine out their Lac Herbin mine. In the quarter ended March 2014, the Lac Herbin mine accounted for 600 – 650 tpd.

The Sigma-Lamaque Complex (2,200 tpd) was originally owned by Century Mining. Century Mining subsequently merged with White Tiger Gold Ltd. The combined entity was subsequently acquired in 2013. The mill is currently in care and maintenance. On September 4, 2014, Integra Gold Corp. (TSXV: ICG) announced that it has entered into an agreement to purchase the Sigma-Lamaque milling facility for $7.55 million.

Camflo mill (1,200 tpd): X-Ore had used this mill for custom milling ore from Croinor in 2003-2005. Approximately 75,752 tonnes @ 3.33 gpt was processed with an average recovery rate of 97.5%. The mill is owned by Richmont Mines (TSX: RIC), and is 105 km from Croinor. Currently, the mill processes ore from RIC’s Beaufor, W Zone and Monique mines. Richmont recently stated that they are seeking custom milling options starting 2015, as their Monique and W Zone mines are expected to run out of ore. Monique and W Zone accounted for 750 – 800 tpd in the first six months of 2014.

Management indicated to us that they are currently in discussions with various mills

Page 10

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

in the region to determine the optimal option for its projects. Preliminary Economic Assessment Results The PEA, completed in 2012, proposed an underground operation, of which, 80% of the tonnage comes from long- hole and sublevel development, and the remaining 20% from room-and-pillar mining. The following image outlines the proposed site infrastructure.

Proposed Site Infrastructure

Source: Technical Report (InnovExplo)

The PEA used 689,169 tonnes @ 6.72 gpt of resources for total contained gold of 148,790 oz. Based on a 425 tpd operation, ramping up to 750 tpd by year 4, the PEA estimates a total mine life of 6 years. The PEA assumed custom milling operations at the Camflo mill. Camflo uses a direct cyanidation circuit. The initial capital cost is estimated at $20.56 million, with sustaining capital of $19.10 million through the 6 year mine life. The initial capital cost estimate is approximately $18.26 million, excluding initial production revenues and production costs. Operating costs are estimated at $160/t, or $731/oz. The Croinor property does not have an electric power line that runs into the property. InnovExplo assumes electric power to the site will be supplied by a new 26.5 km 25 kV three-phase overhead power line. Based on an average gold price of US$1,495/oz (exchange rate of C$/US$:1.03), the PEA estimated an after-tax Net Present Value (“NPV”) @ 7% of $28.8 million, and an after-tax Internal Rate of Return (“IRR”) of 53%.

Page 11

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: Technical Report (InnovExplo)

The sensitivity of the after-tax NPV estimate to discount rates is shown in the table below:

Source: Technical Report (InnovExplo)

Development Plan On July 28, 2014, Monarques announced that they have commenced field work on Croinor to better evaluate the overall potential of the property. In the program, the company will revisit historical showings, and conduct a geological reconnaissance on geophysical anomalies. Monarques also recently announced that they have retained InnovExplo to conduct a prefeasibility on Croinor. For the study, the company will evaluate a new mining technology for narrow and inclined orebodies such as Croinor. The technology (S.A.M.S.™) was developed by Quebec based private company, Minrail. According to Minrail, their technology has the ability to:

extract ore at sloping surfaces between 10 and 45 degrees mechanize the vast majority of manual tasks that have historically been associated

with ore extraction The technology primarily uses an overhead double rail system shown on the next page.

Page 12

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Source: Minrail According to Minrail, the following are the primary benefits of their technology:

increase productivity of ore extraction reduce ore extraction costs to approximately $25 / ton compared to $75-$100 / ton

using conventional mining methods reduces operating costs by up to 40% reduce capital costs for infrastructure such as stopes, ramps and underground

access points by 50%. environmentally safe as it produces significantly less surface waste material than

conventional ore extraction methods; also, the technology does not use diesel provide a safer environment for miners

The technology has been in development since the early 2000s. The final product/service became commercially available this year. Both the Ontario and Quebec governments have approved the technology for ore extraction. Minrail has yet to attract a client. Monarques will be the first company to evaluate the technology in a prefeasibility study. Therefore, the long-term viability and efficiency of the technology is currently unproven. Near-Term Production Plan Management has indicated to us that they are currently gearing up for a mine testing program, wherein they will extract 30,000 tonnes of ore, and use custom milling for processing. The objective of the program is to test the long-term viability of the Minrail technology. Based on the average grade of 7.45 gpt for measured and indicated resources, the 30,000 tonne program, we estimate, could potentially produce 6,970 oz, and generate US$9.07 million in revenues (assumptions: gold price of US$1,300/oz; recovery rate of 97.5%). Management estimates the total upfront cost of the program at $5 million. The company has started seeking potential joint venture partners, or other sources of financing.

The project has already received a Certificate of Authorization to operate the mine. The

Page 13

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Simkar Gold

company is required to attain the following permits for the development and operation of the Croinor mine:

Wood cutting Gravel pit Construction Explosive Fuel storage Beaver dam dismantling

Management believes they will be able to attain these permits in 3 - 5 months. Property Overview The Simkar property is located in the Louvicourt township, approximately 20km east of Val-d’Or, and approximately 50km from the Croinor property. The property is just 3.5 km from the Beacon mill shown in the map on page 9 of this report. The project consists of two contiguous mining concessions, and 21 claims totaling 5.29 km². As in Croinor’s case, Simkar is also a historic producer having produced approximately 51,915 oz of gold (surface mining). Like most other gold projects in the region, Simkar hosts a high-grade shear zone associated gold-quartz vein system. The project is also considered to host VMS type mineralization towards the northern portion of the property. Topography of the region is generally flat. The property can be accessed on a year round basis though the property is subject to snowfall during the winter months (November – March). Access can be obtained via a gravel road that branches off Highway 117 near the settlement of Colombiére situated between Val-d’Or and Louvicourt. According to a technical report published in November 2013 by MRB & Associates, power is available from a provincial hydro transformer located at the community of Louvicourt, approximately 20 km east of the property. There is ample local supply of water, both potable and for processing. Ownership Monarques acquired a 50% interest in the project in September 2013 from Eloro Resources Ltd (TSXV: ELO). In return, Monarques invested $120k through a private placement in Eloro at a price of $0.015 per share for 8 million shares. Monarques also had committed to $750k in exploration work on the property by June 2014 (completed). Subsequently, in June 2014, the company acquired the remaining 50% from Eloro, in return for a 1.5% NSR on Simkar, and a 0.5% NSR on Louvicourt, and a 1.5% NSR on Monarques’ Tex-Sol, Regcourt, and Plator I-V properties. Monarques has the option to reduce the NSR on all properties, with the exception of Louvicourt, from 1.5% to 1%, by making a payment of $1 million. Eloro had purchased the Simkar property from Megastar Development Corp. (TSXV: MDV) in March 2011, by issuing 70 million shares, worth $5.60 million at that time. In December 2011, Eloro acquired the Louvicourt project (adjacent to Simkar) from KWG Resources (TSXV: KWG), by issuing 3.08 million units (each unit had a common share

Page 14

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

and a warrant). Eloro reported the total acquisition price of Simkar and Louvicourt at $7.76 million on their financial statements. Work History The Simkar Property hosts the past producing Simkar Mine where 261,591 tons of ore was milled with production of 31,915 ounces of gold grading 4.62 gpt between 1947 and 1949, and an additional 71,068 tons grading at 8.42 g/t gold was produced between 1987 - 1993.

Source: Technical Report

Historically, the Simkar property has seen extensive exploration, development and small scale intermittent production. The discovery of gold at Simkar occurred in 1939, where it is reported that a high-grade vein was discovered and exposed on surface for 80 m. Drilling in 1939 included 9 drill holes, and a total of 4 holes are reported to have encountered significant gold values including 1.7 feet of 0.6 ounces per ton of gold. In the 1940’s, exploration at Simkar expanded, and an additional 12,000 m of drilling better defined the gold discovery, and identified additional zones of gold mineralization, the A and B zones. From 1945-1947, Louvicourt Goldfields Mine conducted underground development, which included the sinking of a shaft and erection of a mill with the capacity to process 750 tons of material per day. During this period, underground development reports 3,929 m of drifting, 2,346 m of raising, and 18,283 m of underground drilling was completed. Based on a 400 tpd operation, from 1947 till 1949, production at Simkar included 261,590 tons @ 0.123 opt for 31,915 ounces. The recovery rate was 94.71%. Production was suspended as costs exceeded revenues. It was subsequently estimated that the production rate of 400 tpd was too high for the property. Also, sufficient stope preparation had not been completed before production began, and mill tailing losses were excessive. Historic production from the property came from three main zones – the A Zone, B Zone, and C Zone. Though production was suspended, exploration in the area continued and an additional 6,100 meters of drilling in 1950 is reported, resulting in the discovery of the E zone. In the early 1990’s, with favourable gold prices, further underground development and bulk sampling occurred. Despite significant exploration expenditures in excess of $12 million, only a very modest gold resource had been outlined within the area of the old mine site. From 1988 to 1993, Ronrico Explorations Ltd. accessed the East Zone on levels 2 and 3, and extracted 71,068 metric tonnes at a grade of 8.42 g/t Au for 20,000 oz. In 1996, Megastar Development Corp. acquired the property. Drilling on the Simkar

Page 15

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Property by Megastar Development Corporation carried out most of the drilling and geophysical surveys from 1997, focusing on deeper targets (below 300 meters). No significant high grade results were obtained from the 1997 deeper drilling of the known gold-vein system, though one drill hole encountered a new area of interest identified on the northwestern portion of the property, outside of the known gold-vein system. The hole intersected a thick pyritic horizon within the felsic volcanics of the Val-d’Or formation. The horizon intersected by hole 97SKR – 07 encountered 64.4 m of chloritized tuff layers, containing up to 50 % pyrite in stringers ranging from 1 to 5 cm wide. Although no significant base metal values were obtained (maximum 390 ppm copper), interpretation by Megastar suggests the horizon may host massive sulphide mineralization along strike or down dip from the intersected horizon. The drill hole returned anomalous gold content of 0.59 g/t from a 4.5 m interval of sheared and altered zone intersected above the rhyolitic horizon. Subsequently, Megastar conducted a property wide IP survey in which a 900 m anomaly was identified to correlate with drill hole 97SKR – 07.

The map below shows the regional geology of the area.

Source: Megastar Development

Drilling in 2004 resulted in 4 holes to test the north portion of the Simkar property. Results from this program identified notable gold/copper mineralization over short intercepts including 7.43 g/t gold and 0.2% copper over 0.82 meters. In 2007, a 15 diamond drill hole totaling 4,340 m was completed. These programs

Page 16

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

identified three additional gold-bearing zones (Pillar Zone, F Zone, and Montana Zone), and identified a high-potential structure named the East Zone Shear.

East-west long section

Source: Technical Report

Eloro entered into an option agreement to acquire a 50% interest in the property in 2009. From 2009-2013, as the property operator, Eloro Resources completed 23,778 m of diamond drilling in 54 surface holes. Since Monarques took over as the operator in 2013, the company completed 19 holes totaling 8,055 m of drilling in 2013. The goal of the program was to extend the gold-bearing horizons previously identified as the A, B, C, D, East and South zones. The program identified large, near-surface mineralized zones, and confirmed the presence of silver.

To date, the property has had 590 surface and underground diamond-drill holes, comprising 79,590 total metres. Historical results from the property indicate its similarities to the Sigma-Lamaque deposit, located 10 km from the property. The Sigma and Lamaque mines have produced over 9 Moz of gold. The following image shows the depth to which Sigma was produced, and the potential of Simkar. Sigma has been mined up to 2,000 m compared to Simkar’s 250 m.

Page 17

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Regcourt Gold

Source: Company

Resource Estimate The most recent technical report on the property was completed in November 2013 by MRB & Associates. They estimated measured and indicated resources of 110,140 t @ 5.54 gpt (18,265 oz), and 321,210 t @ 4.76 gpt (57,325 oz) of inferred resources.

Source: Technical Report (MRB & Associates)

The technical report suggested that the recent work on Simkar has confirmed that the gold bearing structures on the project continue to show potential for hosting additional mineralization, and deserve additional exploration work. The report suggested additional diamond drilling to expand the resource estimate and also to upgrade the inferred resources, and initial metallurgical testing, totaling $5.69 million. Development Plan Monarques is currently developing a program which will consist of a geophysical survey to identify new drill targets, followed a drill campaign. The company’s first priority is Croinor at this moment. The scope of work at Simkar will be contingent on the results of the ongoing exploratory work at Croinor. This was the first property the company acquired in the Val-dO’r area. In May 2013, the company acquired a 100% interest (and an outstanding 2% NSR) in the Regcourt gold property, covering 26 km2, for $58,500. Subsequently, in June 2013, the company acquired another 192 claims for $25,000 (paid by 192,308 shares @ $0.l3), from Plato Gold Corp. Plato retains a 1% NSR, which can be purchased by the company for $1 million.

Page 18

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Belcourt Management

In total, the Regcourt project covers 270 claims across 57 km2. It is approximately 30 km east of Val-d’Or, and is accessible via Route 117. The project is a combination of six properties, including Regcourt and Plator I to V. As mentioned earlier, Eloro has a 1.5% NSR on Regcourt, and the Plator I-V properties. The company believes that Regcourt’s mineralization is similar to Richmont Mines’ Beaufor mine, which is located 10 km away. Gold was first discovered on the Regcourt property in 1944, when an outcrop area of the property was stripped, exposing a wide quartz vein, with a grade of 8.13 gpt gold, over a strike of 67 m, and width of 0.8 m. Monarques currently has no exploration plans for the property. The company is evaluating options to joint venture the project, and advance it along with Croinor and Simkar. This 100% owned property covers 10 claims covering 4.3 km2 . The property, located approximately 40 km northeast of Val-d’Or, was acquired in 2013, for less than $20k in cash.

Drilling by Placer Dome intersected gold with grades typically ranging from 1 to 3 gpt. A few intersections also showed values up to 32 gpt over widths ranging from 0.4 to 1.7 m. Most gold values are from veins and quartz veinlets in altered and sheared basalts.

As with Regcourt, the company has no exploration plans for the property at this time, and is evaluating joint venture options. Management and the board of directors own 2.9% of the outstanding shares of Monarques. The CEO, Jean-Marc Lacoste, owns 3.03 million shares, or 2.2% of the total outstanding, aligning management and investors’ interests. Brief biographies of the management team, as provided by the company, follow: Jean-Marc Lacoste - President and Chief Executive Officer - Mr. Jean-Marc Lacoste earned his bachelor’s degree in Economics from McGill University in Montreal. In 1993, Mr. Lacoste started a career in finance at the Montreal Stock Exchange where he worked for National Bank Financial and, subsequently, Merrill Lynch Canada Inc. In 2000 he left Montreal for Toronto to join Northland Power Inc., a wind power energy corporation, as Vice President of Acquisitions. He returned to Montreal in 2002 where he joined the boards of a few public and private companies. From 2004 to 2010, he took a major role in Golden Goose Resources Inc., a corporation principally engaged in mining exploration and acquisition, where he became President, Chief Executive Officer and Chairman of the Board. Since 2010, he is the President of Lacoste International Inc., a holding corporation specialized in the management of corporations. Steve Nadeau, CPA, CGA - Chief Financial Officer - Mr. Steve Nadeau is a certified general accountant and has been a member of the “Ordre des CPA, CGA du Québec” as well as a member of the certified general accountants’ association of Canada since October 1998. He completed a bachelor’s degree in business administration at Moncton University

Page 19

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Board of Directors

in May 1991. During his career, he mainly held management positions including, among other: since May 2008, he fulfills the role of Chief Financial Officer for Nemaska Lithium Inc., a corporation focused on becoming the next lithium compounds producer. From December 2007 to February 2011, Mr. Nadeau has been the controller of DAP Technologies Inc., a corporation specialized in the manufacturing of rugged electronic handheld and tablets. He also acted, from November 2005 to December 2007, as the financial controller of T-Rex Vehicles inc., a company specialized in the manufacturing of three-wheeled vehicles. Also, from January 2000 to November 2004 he has been the Controller of Stone Vogue International Inc. and subsidiaries, companies specialized in the commercialization, transformation and production of granite products as well as in the operation of granite quarries. From 1992 to December 1999, he began his career while working for Quebec Stevedoring Co. and subsidiaries, where he held several positions that led him to become the assistant to the controller from 1995 to 1999. Vincent Janelle - Vice President, Investor Relations - Mr. Vincent Janelle graduated from the HEC Montreal's Finance profile; he cumulates over 15 years of experience in management, finance and investor relations in the mining industry. He possesses extensive knowledge of financial markets and communication with various stakeholders. Prior to joining the Corporation, Mr. Janelle was Director, Investor Relations for MDN Inc., a junior gold and industrial metals exploration company with assets in Quebec and abroad. Previously, from 2006 to 2009, he served as Head of Business Development at BMO Nesbitt Burns for a private management of assets group. Guy Bourassa – Secretary - Mr. Guy Bourassa has graduated in law from the Université Laval, Québec, in 1983. He has been member of the Québec Bar from 1983 to October 2011. During his career as an attorney, he has mainly worked with Québec mining exploration businesses. He has been director and President of Radisson Mining Resources Inc. from November 1988 to June 1991. He has also been President and director of Dufresnoy Industrial Minerals Inc. from May 1994 to November 1996, and Corporate Secretary of Mazarin Mining Corporation from September 1991 to June 1994. He is secretary and director of Monarques, since February 2011 and has been President and Chief Executive Officer thereof from March 2011 to October 2012. From June 2004 to October 2007, he was President and Chief Executive Officer of T-Rex Vehicles Inc. From June 2002 to June 2004, he was Chief Executive Officer of Concepts Win Inc., a subsidiary of DEQ Systems Corp. From September 2000 to June 2002, he was corporate counsel with the firm LBJ Partners Inc., during which time he was also Chairman and Chief Executive Officer of TMI Éducaction.com Inc. From 1996 to 2000, he was an associate with the Québec law firm Flynn, Rivard, société en nom collectif avocats. Michel Baril, Eng. – Chairman - Mr. Michel Baril has been a member of the Ordre des Ingénieurs du Québec since June 1976. He graduated from Montreal’s École Polytechnique. Since 2003, Mr. Baril has served on several boards of directors. He was a director of The Hockey Co. from June 2003 to June 2004. He was also director of Groupe Laperrière & Verreault Inc., a corporation that specializes in the fields of pulp and paper and water treatment from September 2004 to August 2007. He has also been director of Raymor Industries Inc., a corporation specialized in the production of metallic powder and carbon nanotubes, from January 2005 to February 2009 and from June 2009 to February

Page 20

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

2010. Also, he has been a director of Komet Manufacturers Inc., a corporation specialized in the manufacturing of vanities and kitchen cabinets from June 2007 to September 2011. He is currently a director of Imaflex Inc., a corporation specialized in the manufacturing of polymer-based films, since April 2008 and of Nemaska Lithium Inc. since October 2008. These two corporations are listed on the TSX Venture Exchange Inc. He is also Chairman of the Board of Nemaska Lithium Inc. since October 2008. From June 1979 to November 2003, he held various administrative positions with Bombardier Inc. Jean Marc Lacoste – Director – see management bios Guy Bourassa – Director - see management bios Robert Ayotte – Director - Mr. Robert Ayotte is President of Gestion Somiray Inc., a holding corporation specialized in management of mining corporations and administrative services, since June 1995. He is Chairman of Brionor Resources Inc., a mining exploration corporation, since June 2011 and a Director since September 2009. He was President and director of Normabec Mining Resources Ltd., a mining exploration and development corporation, from December 1993 to November 2009 He is also a director of Cyprium Mining Corporation, a junior exploration mining company involved in Mexico. Mr. Ayotte has been the Chief Executive Officer of several public corporations since 1993. He served as a Vice President, Corporate Finance and Mining Analyst for two Canadian brokerage firms, namely McNeil, Mantha Inc. and Whalen, Béliveau & Associates Inc. He holds a Bachelors degree in Administration (Finance) of the Université du Québec à Trois-Rivières, which he received in 1975. Michel Bouchard – Director - Mr. Michel Bouchard, who has been involved in the exploration, development and production aspects of the mining sector for over 30 years, brings a wealth of knowledge and experience with him. He is actually the President and Chief Executive Officer of Clifton Star Resources Inc., since November, 2011. He has been a director and senior officer of several public companies in the mining sector. Mr. Bouchard holds a B.Sc and a M.Sc in Geology from University of Montreal and a M.B.A. from H.E.C. Montreal. René Lessard – Director - Mr. René Lessard held the position of sales manager at Campagna Motors Inc., a corporation specialized in vehicle manufacturing, from September 2008 to October 2009. From October 2004 to October 2007, he was sales manager of T-Rex Vehicles Inc.. From February 2001 to July 2004, he was sales manager of Distribution GLR. From March 1997 to October 2000, he was sales representative of Ray-Flammes Inc. He is a director of Nemaska, a mining exploration corporation, since September 2008. Christian Pichette – Director - Mr. Pichette holds a Bachelor of Engineering in Mining and a Master degree in Rock Mechanics from Ecole Polytechnique, Montreal. He has over 35 years of experience in the mining industry. Mr. Pichette has held managerial positions with many Canadian companies, including Placer Dome Inc., TVX Gold inc., Barrick Gold Corporation, Cambior Inc., and up to recently, he was holding the Executive Vice President and COO position at Richmont Mines Inc.

Page 21

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Financials

Our net rating on MQR’s management team is 3.75 out of 5.00 (see below).

We believe that the Board of Directors of a company should include independent or unrelated directors who are free of any relationships or business that could materially interfere with the director’s ability to act in the best interest of the company. An unrelated/independent director can be a shareholder. The following table shows our analysis on the strength of Monarques’ board.

Poor Average Good

Two out of seven directors are independent X

All the directors hold shares of the company X

The Audit committee is composed of three board members, all three are are independent X

A Compensation committee has yet to be formed. X

At the end of Q3-2014 (ended March 31, 2014) the company had cash and working capital of $0.72 million and $0.77 million, respectively. As a result of its decision to shift its focus to the newly acquired Val-d’Or properties, the company reported $10.34 million in impairment charges on its old properties. We estimate the company had a burn rate (cash spent on operating and investing activities) of $0.21 million per month in the nine month period. The following table summarizes the company’s liquidity position at the end of Q3-2014.

Page 22

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Stock Options and Warrants Valuation and Rating

(in C$) 2013 2014 (9M)Cash $2,093,271 $724,538Working Capital $1,769,314 $770,197Current Ratio 5.63 5.85 LT Debt/ Assets - - Monthly Burn Rate (incl. investing activities) (169,382) (213,177) Cash from Financing $2,723,141 $669,857

Subsequent to the quarter end, in June 2014, the company completed a $0.40 million financing by issuing 3.68 million units at a unit price of $0.11. Each unit consisted of a common share and share purchase warrant (exercise price – $0.14, maturity period – 2 years).

According to management, the company currently has approximately $0.8 million in working capital. The capital requirements for the next 12 months will be contingent on the prefeasibility study results (expected next month). The company currently has 3.69 million options outstanding (weighted average exercise price of $0.25) and 16.29 million warrants outstanding (weighted average exercise price of $0.23). At this time, none of the stock options or warrants are ‘in-the-money’. We used a Discounted Cash Flow (“DCF”) model to evaluate the Croinor and Simkar projects. We typically use a comparables valuation as well to evaluate junior resource companies, wherein we use the average Enterprise Value (“EV”) to resource ratio of comparable companies. However, unlike most junior resource projects, Croinor can be put into production quicker and cheaper (due to custom milling options in the region). Therefore, we do not believe it is appropriate to value Monarques based on the average EV to resource ratio of other gold focused juniors. Our DCF model is based on the following key assumptions:

Our long-term gold price forecast is US$1,200/oz (C$/US$ - 1.1) As with most junior resource projects, we have used 100% of the measured and

indicated, and 50% of the inferred resources. The production rate and cost estimates, used in the model, were based on Croinor’s

PEA results. Although a PEA has not been completed on Simkar, we have assigned an initial capital cost estimate of $12.50 million, and an operating cost estimate of $130/t.

Our model used a discount rate of 11.5%, which is our estimate of the expected return on junior gold projects.

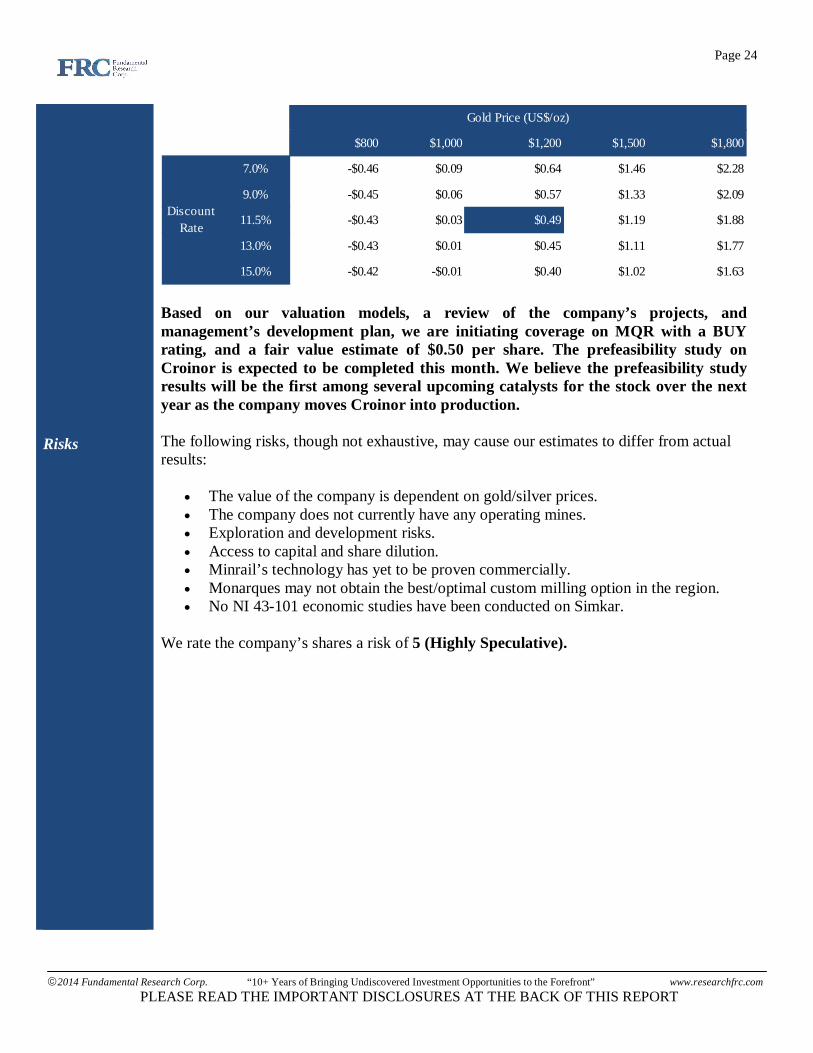

Our DCF valuation, based on the above assumptions, is $0.49 per share. The following table highlights all the assumptions.

Page 23

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

DCF Valuation

CroinorTonnage (M&I + 50% Inf) 1,074,600

Weighted Avg Grade (gpt) 7.41

Recovery 97.50%

Recovered Au (oz) 248,287

Production Rate 425 tpd in Year 1, ramping up to

750 tpd by Year 4

Mine Life (years) 5

Operating costs ($/t) - added a 10% premium to the PEA estimate $176

Initial Capital Cost (excl pre-production revenues and costs) - $, millions - added a 20% premium to the PEA estimate for conservatism $21.92

SimkarTonnage (M&I + 50% Inf) 270,745

Weighted Avg Grade (gpt) 5.42

Recovery 97.50%

Recovered Au (oz) 45,754

Production Rate 425 tpd

Mine Life (years) 2

Operating costs ($/t) $130

Initial Capital Cost - $, millions $12.50

Long-Term Gold Price (US$/oz) $1,200

Long-Term C$/US$ 1.10

Discount rate 11.5%Net Asset Value (C$) $31,079,064

Current Working Capital (estimate) $775,197

Fair Value of MQR $31,854,261

No. of Shares 64,585,204

Fair Value per Share ($) $0.49 The sensitivity of our valuation to gold prices and discount rates is shown below.

Page 24

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Risks

0 $800 $1,000 $1,200 $1,500 $1,800

7.0% -$0.46 $0.09 $0.64 $1.46 $2.28

9.0% -$0.45 $0.06 $0.57 $1.33 $2.09

11.5% -$0.43 $0.03 $0.49 $1.19 $1.88

13.0% -$0.43 $0.01 $0.45 $1.11 $1.77

15.0% -$0.42 -$0.01 $0.40 $1.02 $1.63

Discount Rate

Gold Price (US$/oz)

Based on our valuation models, a review of the company’s projects, and management’s development plan, we are initiating coverage on MQR with a BUY rating, and a fair value estimate of $0.50 per share. The prefeasibility study on Croinor is expected to be completed this month. We believe the prefeasibility study results will be the first among several upcoming catalysts for the stock over the next year as the company moves Croinor into production. The following risks, though not exhaustive, may cause our estimates to differ from actual results:

The value of the company is dependent on gold/silver prices. The company does not currently have any operating mines. Exploration and development risks. Access to capital and share dilution. Minrail’s technology has yet to be proven commercially. Monarques may not obtain the best/optimal custom milling option in the region. No NI 43-101 economic studies have been conducted on Simkar.

We rate the company’s shares a risk of 5 (Highly Speculative).

Page 25

2014 Fundamental Research Corp. “10+ Years of Bringing Undiscovered Investment Opportunities to the Forefront” www.researchfrc.com PLEASE READ THE IMPORTANT DISCLOSURES AT THE BACK OF THIS REPORT

Fundamental Research Corp. Equity Rating Scale: Buy – Annual expected rate of return exceeds 12% or the expected return is commensurate with risk Hold – Annual expected rate of return is between 5% and 12% Sell – Annual expected rate of return is below 5% or the expected return is not commensurate with risk Suspended or Rating N/A— Coverage and ratings suspended until more information can be obtained from the company regarding recent events. Fundamental Research Corp. Risk Rating Scale: 1 (Low Risk) - The company operates in an industry where it has a strong position (for example a monopoly, high market share etc.) or operates in a regulated industry. The future outlook is stable or positive for the industry. The company generates positive free cash flow and has a history of profitability. The capital structure is conservative with little or no debt. 2 (Below Average Risk) - The company operates in an industry where the fundamentals and outlook are positive. The industry and company are relatively less sensitive to systematic risk than companies with a Risk Rating of 3. The company has a history of profitability and has demonstrated its ability to generate positive free cash flows (though current free cash flow may be negative due to capital investment). The company’s capital structure is conservative with little to modest use of debt. 3 (Average Risk) - The company operates in an industry that has average sensitivity to systematic risk. The industry may be cyclical. Profits and cash flow are sensitive to economic factors although the company has demonstrated its ability to generate positive earnings and cash flow. Debt use is in line with industry averages, and coverage ratios are sufficient. 4 (Speculative) - The company has little or no history of generating earnings or cash flow. Debt use is higher. These companies may be in start-up mode or in a turnaround situation. These companies should be considered speculative. 5 (Highly Speculative) - The company has no history of generating earnings or cash flow. They may operate in a new industry with new, and unproven products. Products may be at the development stage, testing, or seeking regulatory approval. These companies may run into liquidity issues, and may rely on external funding. These stocks are considered highly speculative. Disclaimers and Disclosure The opinions expressed in this report are the true opinions of the analyst about this company and industry. Any “forward looking statements” are our best estimates and opinions based upon information that is publicly available and that we believe to be correct, but we have not independently verified with respect to truth or correctness. There is no guarantee that our forecasts will materialize. Actual results will likely vary. The analyst and Fundamental Research Corp. “FRC” does not own any shares of the subject company, does not make a market or offer shares for sale of the subject company, and does not have any investment banking business with the subject company. Fees were paid by MQR to FRC. The purpose of the fee is to subsidize the high costs of research and monitoring. FRC takes steps to ensure independence including setting fees in advance and utilizing analysts who must abide by CFA Institute Code of Ethics and Standards of Professional Conduct. Additionally, analysts may not trade in any security under coverage. Our full editorial control of all research, timing of release of the reports, and release of liability for negative reports are protected contractually. To further ensure independence, MQR has agreed to a minimum coverage term including an initial report and three updates. Coverage cannot be unilaterally terminated. Distribution procedure: our reports are distributed first to our web-based subscribers on the date shown on this report then made available to delayed access users through various other channels for a limited time. The performance of FRC’s research is ranked by Investars. Full rankings and are available at www.investars.com. The distribution of FRC’s ratings are as follows: BUY (69%), HOLD (8%), SELL (5%), SUSPEND (18%). To subscribe for real-time access to research, visit http://www.researchfrc.com/subscribe.php for subscription options. This report contains "forward looking" statements. Forward-looking statements regarding the Company and/or stock’s performance inherently involve risks and uncertainties that could cause actual results to differ from such forward-looking statements. Factors that would cause or contribute to such differences include, but are not limited to, continued acceptance of the Company's products/services in the marketplace; acceptance in the marketplace of the Company's new product lines/services; competitive factors; new product/service introductions by others; technological changes; dependence on suppliers; systematic market risks and other risks discussed in the Company's periodic report filings, including interim reports, annual reports, and annual information forms filed with the various securities regulators. By making these forward looking statements, Fundamental Research Corp. and the analyst/author of this report undertakes no obligation to update these statements for revisions or changes after the date of this report. A report initiating coverage will most often be updated quarterly while a report issuing a rating may have no further or less frequent updates because the subject company is likely to be in earlier stages where nothing material may occur quarter to quarter. Fundamental Research Corp DOES NOT MAKE ANY WARRANTIES, EXPRESSED OR IMPLIED, AS TO RESULTS TO BE OBTAINED FROM USING THIS INFORMATION AND MAKES NO EXPRESS OR IMPLIED WARRANTIES OR FITNESS FOR A PARTICULAR USE. ANYONE USING THIS REPORT ASSUMES FULL RESPONSIBILITY FOR WHATEVER RESULTS THEY OBTAIN FROM WHATEVER USE THE INFORMATION WAS PUT TO. ALWAYS TALK TO YOUR FINANCIAL ADVISOR BEFORE YOU INVEST. WHETHER A STOCK SHOULD BE INCLUDED IN A PORTFOLIO DEPENDS ON ONE’S RISK TOLERANCE, OBJECTIVES, SITUATION, RETURN ON OTHER ASSETS, ETC. ONLY YOUR INVESTMENT ADVISOR WHO KNOWS YOUR UNIQUE CIRCUMSTANCES CAN MAKE A PROPER RECOMMENDATION AS TO THE MERIT OF ANY PARTICULAR SECURITY FOR INCLUSION IN YOUR PORTFOLIO. This REPORT is solely for informative purposes and is not a solicitation or an offer to buy or sell any security. It is not intended as being a complete description of the company, industry, securities or developments referred to in the material. Any forecasts contained in this report were independently prepared unless otherwise stated, and HAVE NOT BEEN endorsed by the Management of the company which is the subject of this report. Additional information is available upon request. THIS REPORT IS COPYRIGHT. YOU MAY NOT REDISTRIBUTE THIS REPORT WITHOUT OUR PERMISSION. Please give proper credit, including citing Fundamental Research Corp and/or the analyst, when quoting information from this report. The information contained in this report is intended to be viewed only in jurisdictions where it may be legally viewed and is not intended for use by any person or entity in any jurisdiction where such use would be contrary to local regulations or which would require any registration requirement within such jurisdiction.