module 7 reporting and analyzing intercorporate investments

TRANSCRIPT

Module 7Module 7

Reporting and Reporting and Analyzing Analyzing

Intercorporate Intercorporate InvestmentsInvestments

InvestmentsInvestmentsA Corporation may own:

• *Part or all of another corporation• *Investments in bonds, notes, and other

securities• Part of a partnership or joint venture• Other non-operating assets, which are

treated as investment

*This module is about Intercorporate investments in stocks and bonds.

How Much Control do we How Much Control do we have?have?

Investment in voting shares may be• Passive—little influence over another

company—generally less than 20%• Trading—active buying and selling• Available-for-sale—could sell, but intend

to hold for gain• Significant influence—generally between

20% and 50%, but may be lower % for large corporations—depends on the actual circumstances.

• Control—Generally greater than 50% ownership

Intercorporate Intercorporate InvestmentsInvestments

Passive InvestmentsPassive Investments• Passive investments may be stocks, bonds, or

any marketable instrument including notes, futures contracts, commodities…

• Any dividends, interest, gains or losses on sale are recognized on the income statement

• Balance sheet investment account is kept at market value—this results in unrealized gains or losses. (Except for bonds “held to maturity” which are kept at amortized cost.)

Passive InvestmentsPassive Investments• Unrealized gains/losses:

• If “trading”, then income statement• If “available for sale,” then equity section

account “Accumulated Other Comprehensive Income”

• Under both U.S. GAAP and IFRS, companies classify passive instruments as trading, available-for-sale, or held-to-maturity, but under IFRS reclassifications are prohibited.

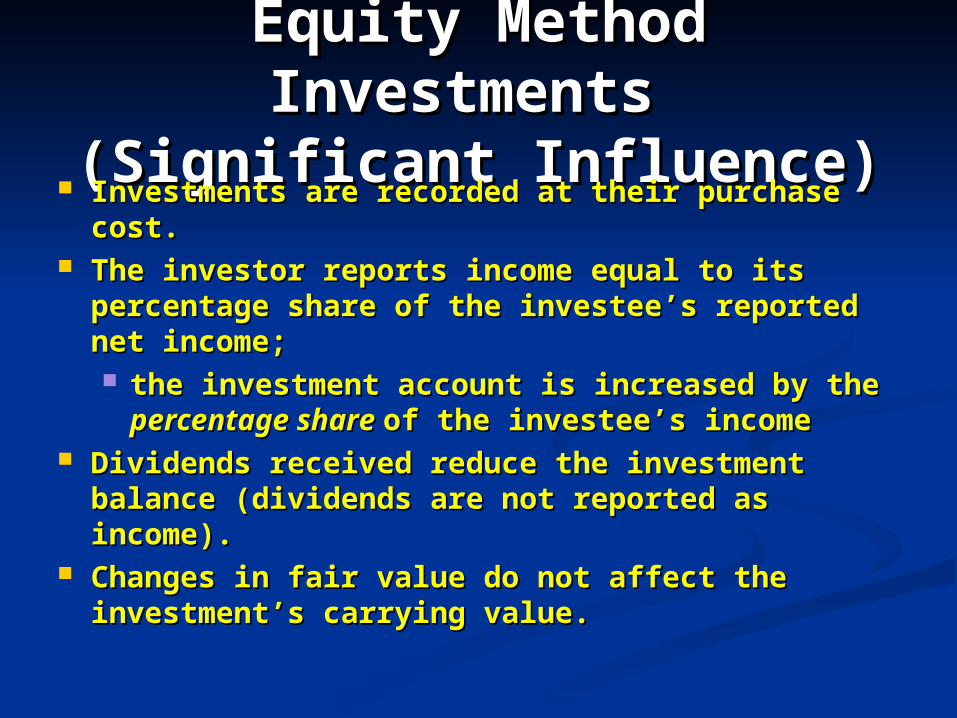

Equity Method Equity Method Investments Investments

(Significant Influence)(Significant Influence) Investments are recorded at their purchase cost.Investments are recorded at their purchase cost. The investor reports income equal to its percentage The investor reports income equal to its percentage

share of the investee’s reported net income; share of the investee’s reported net income; the investment account is increased by the the investment account is increased by the

percentage share percentage share of the investee’s incomeof the investee’s income Dividends received reduce the investment balance Dividends received reduce the investment balance

(dividends are not reported as income).(dividends are not reported as income). Changes in fair value do not affect the investment’s Changes in fair value do not affect the investment’s

carrying value.carrying value.

Equity Method Accounting Equity Method Accounting MechanicsMechanics

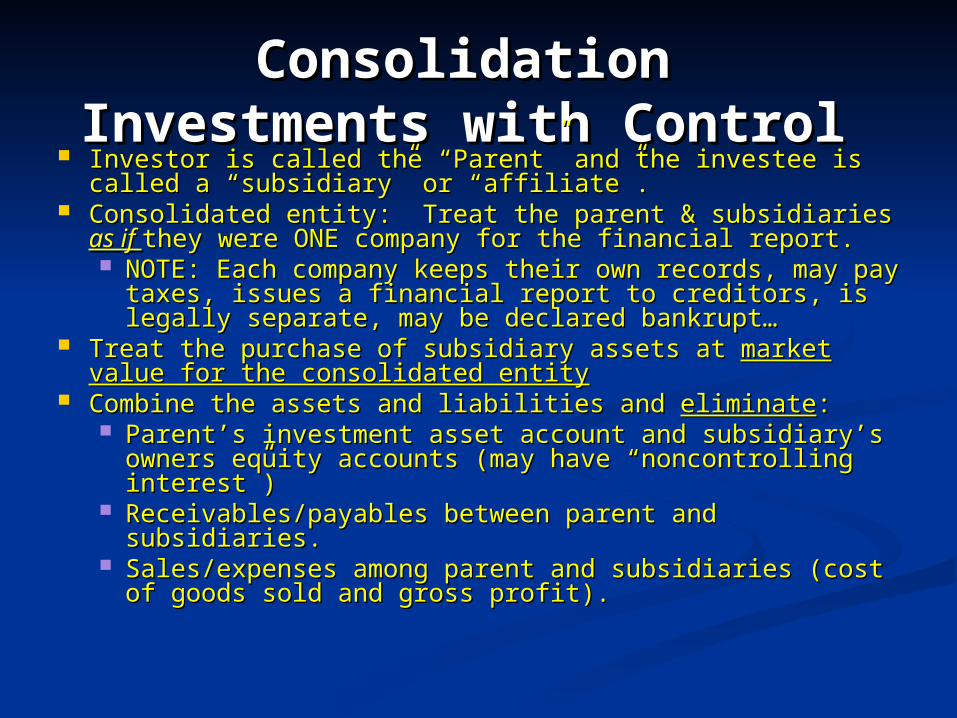

Consolidation Consolidation Investments with Control Investments with Control

Investor is called the “Parent” and the investee is called a Investor is called the “Parent” and the investee is called a “subsidiary” or “affiliate”.“subsidiary” or “affiliate”.

Consolidated entity: Treat the parent & subsidiaries Consolidated entity: Treat the parent & subsidiaries as if as if they they were ONE company for the financial report.were ONE company for the financial report. NOTE: Each company keeps their own records, may pay NOTE: Each company keeps their own records, may pay

taxes, issues a financial report to creditors, is legally taxes, issues a financial report to creditors, is legally separate, may be declared bankrupt…separate, may be declared bankrupt…

Treat the purchase of subsidiary assets at Treat the purchase of subsidiary assets at market value for market value for the consolidated entitythe consolidated entity

Combine the assets and liabilities and Combine the assets and liabilities and eliminateeliminate:: Parent’s investment asset account and subsidiary’s Parent’s investment asset account and subsidiary’s

owners equity accounts (may have “noncontrolling owners equity accounts (may have “noncontrolling interest”)interest”)

Receivables/payables between parent and subsidiaries.Receivables/payables between parent and subsidiaries. Sales/expenses among parent and subsidiaries (cost of Sales/expenses among parent and subsidiaries (cost of

goods sold and gross profit).goods sold and gross profit).

A Simple ConsolidationA Simple Consolidation

Notes: 1.Penman purchased 100% of Nissim stock with no revaluation of consolidated assets.2.The owners’ equity accounts of the parent company become the consolidated equity accounts.

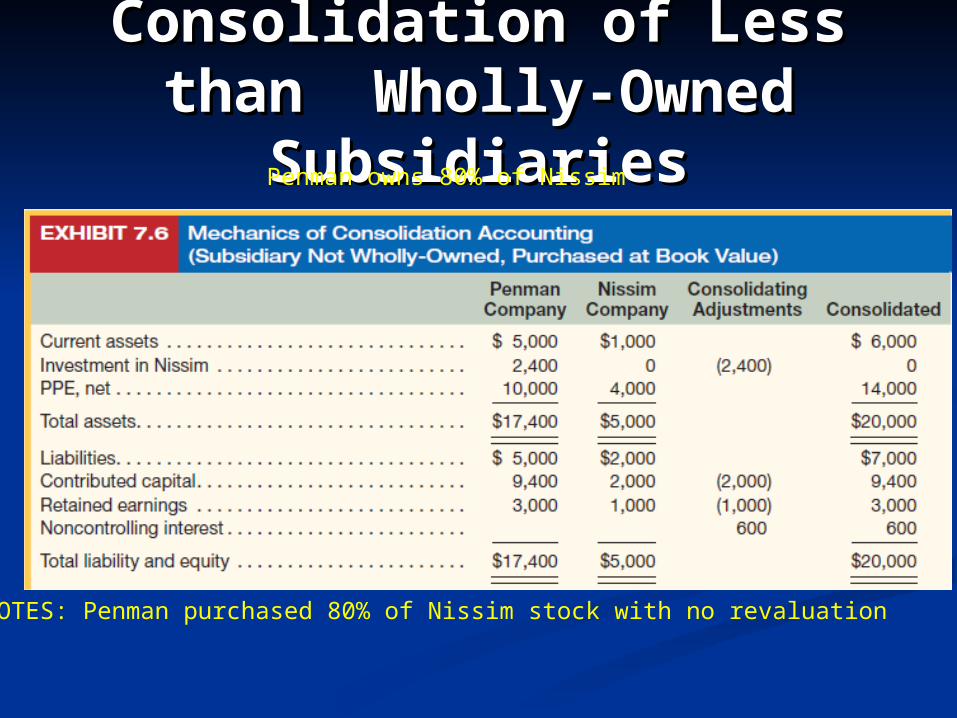

Consolidation of Less Consolidation of Less than Wholly-Owned than Wholly-Owned

SubsidiariesSubsidiariesPenman owns 80% of Nissim

NOTES: Penman purchased 80% of Nissim stock with no revaluation

Consolidation When Purchase Consolidation When Purchase Price Exceeds Book Value of Price Exceeds Book Value of

Stockholders’ EquityStockholders’ Equity

Notes:1.Penman purchased 100% of Nissim, paying $4,000, which is $1,000 more than book equity value.2.PPE, net book value is revalued in the acquisition.

Acquired Intangible Acquired Intangible AssetsAssets

The purchase price is allocated to acquired The purchase price is allocated to acquired identifiable identifiable intangibleintangible assets, which include assets, which include the following:the following: Marketing-related assetsMarketing-related assets like trademarks like trademarks

and internet domain namesand internet domain names Customer-related assetsCustomer-related assets like customer lists, like customer lists,

production backlog, and customer contractsproduction backlog, and customer contracts Artistic-related assetsArtistic-related assets like plays, books, and like plays, books, and

videovideo Contract-based assetsContract-based assets like licensing and like licensing and

royalty agreements, lease agreements, royalty agreements, lease agreements, franchise agreements, and servicing franchise agreements, and servicing contractscontracts

Technology-based assetsTechnology-based assets like patents, like patents, computer software, databases and trade computer software, databases and trade secretssecrets

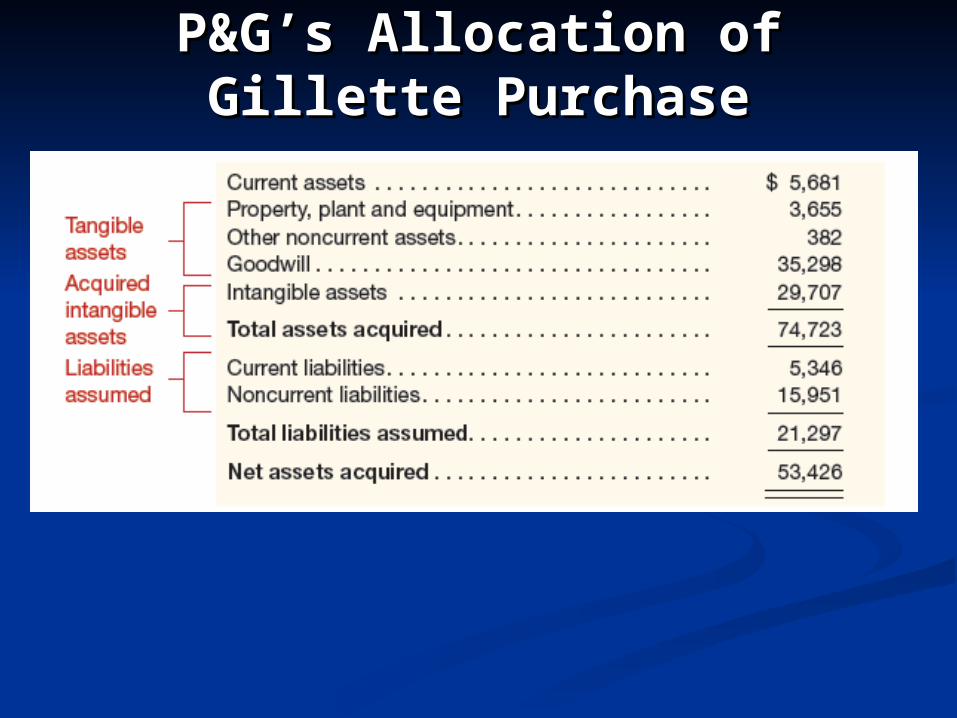

P&G’s Allocation of Gillette P&G’s Allocation of Gillette PurchasePurchase

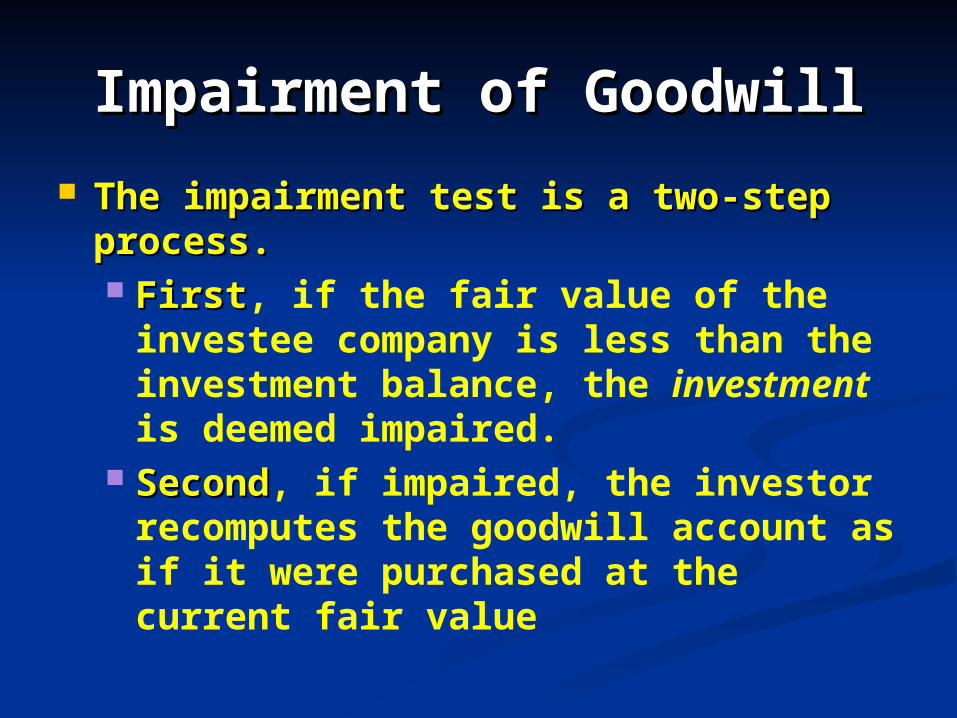

Impairment of GoodwillImpairment of Goodwill

The impairment test is a two-step The impairment test is a two-step process.process. FirstFirst, if the fair value of the investee

company is less than the investment balance, the investment is deemed impaired.

SecondSecond, if impaired, the investor recomputes the goodwill account as if it were purchased at the current fair value

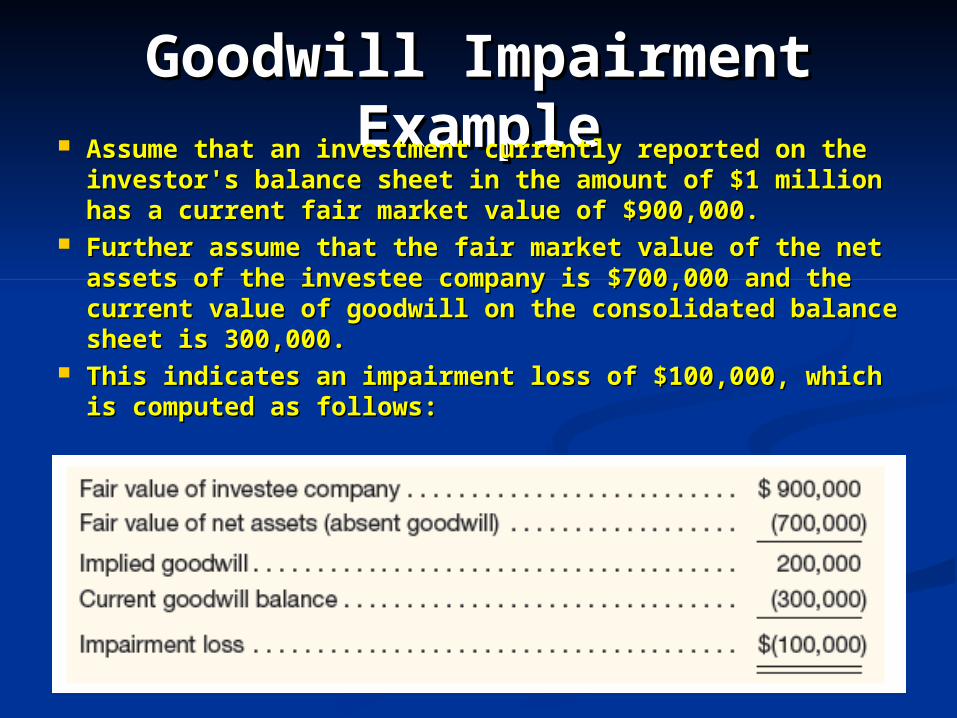

Goodwill Impairment Goodwill Impairment ExampleExample Assume that an investment currently reported on Assume that an investment currently reported on

the investor's balance sheet in the amount of $1 the investor's balance sheet in the amount of $1 million has a current fair market value of $900,000. million has a current fair market value of $900,000.

Further assume that the fair market value of the net Further assume that the fair market value of the net assets of the investee company is $700,000 and the assets of the investee company is $700,000 and the current value of goodwill on the consolidated current value of goodwill on the consolidated balance sheet is 300,000. balance sheet is 300,000.

This indicates an impairment loss of $100,000, This indicates an impairment loss of $100,000, which is computed as follows:which is computed as follows:

Sales of Subsidiaries – Sales of Subsidiaries – Discontinued OperationsDiscontinued Operations

Limitations of Consolidated Limitations of Consolidated Financial StatementsFinancial Statements

Consolidated statements do Consolidated statements do notnot imply that:imply that: The cash of foreign subsidiaries is in or The cash of foreign subsidiaries is in or

can be brought to the USA. can be brought to the USA. The consolidated earnings or cash flow The consolidated earnings or cash flow

from operations can be invested in the from operations can be invested in the USA.USA.

Companies with financial Companies with financial subsidiaries may be difficult to subsidiaries may be difficult to analyze.analyze.

Global Accounting: Global Accounting: ConsolidationConsolidation

Consolidation accounting standards were Consolidation accounting standards were developed jointly by the FASB and the IASB. developed jointly by the FASB and the IASB.

Yet, a few differences remain:Yet, a few differences remain: Contrary to US GAAP, under IFRS, parent Contrary to US GAAP, under IFRS, parent

and subsidiaries’ accounting policies and subsidiaries’ accounting policies must must conformconform..

Contrary to US GAAP, under IFRS, fair-value Contrary to US GAAP, under IFRS, fair-value impairments for intangible assets, excluding impairments for intangible assets, excluding goodwill, goodwill, can be later reversed can be later reversed (that is, written (that is, written back up after being written down).back up after being written down).