module 1_working capital

DESCRIPTION

Working capital notes for VTU MBA III sem AFMTRANSCRIPT

Advanced Financial Management

Module 1

Working Capital Management

Working capital management includes the following

- Principles of working capital management.- Receivables management and factoring.- Inventory management.- Cash management.- Working capital finance.

Working capital management is the functional area of finance that covers all the current assets accounts of the firm.

It is concerned with the management of the level of individual current assets as well as the management of total working capital.

Financial management: procurement of funds and effective utilization of these procured funds.

Procurement of funds is firstly concerned for financing working capital requirements of the firm and secondly for financing fixed assets.

Working capital refers to the funds invested in current assets. I.e. investment in stocks, sundry debtors, cash, Bank, short term marketable securities, Prepaid expenses, outstanding incomes, B/R, etc.

Current assets are essential to use fixed assets profitably.

Concept view of working capital

1. Gross working capital.2. Net working capital.

Gross working capital refers to the firm investment in all the current assets taken together.

- Cash, Bank, Stock, Debtors, Short term securities etc...

Net working capital refers to excess of total current assets over total current liabilities.

Current liabilities refers to the liabilities which are payable within an accounting period.

From the point of view of time

1. Permanent working capital (or) fixed working capital.2. Temporary working capital (or) Variable working capital.

Preethi MS Page 1

Advanced Financial Management

Permanent working capital refers to the hard core working capital. It is that minimum level of investment in the current assets that is carried by the business at all times to carry out minimum level of its activities.

Temporary working capital refers to that part of total working capital which is required by a business over and above permanent working capital.

Extra working capital needed to support the changing production and sales activities of the firm.

Importance of adequate working capital

- A concern needs funds for its day to day running.- Adequacy or inadequacy of these funds would determine the efficiency with which the daily business may

be carried on.- Management of working capital is the task of financial managers.- A firm is said to have over capitalization when it has large amount of working capital means it has idle

funds. - A firm is said to be Undercapitalization - when it has inadequate working capital.- When a firm is not able to meet liabilities it faces Risk of insolvency.

What is the optimum amount of working capital for a firm?

Current ratio along with acid test ratio – best indicator of the working capital situation.

Manufacturing companies --- CR = 2:1. } depending on the

ATR = 1:1.} Conversion cycle.

ATR = (Quick assets / current liabilities)

Quick assets = Cash, Bank, Debtors, Marketable securities.

Determination of level of working capital

Preethi MS Page 2

Amou

nt o

f w

orki

ng

capi

tal (

Rs)

Time

Temporary

or fluctuating

Permanent

Advanced Financial Management

1. Tradeoff between Profitability and Risk: An important consideration Profitability – profits after expenses Risk – the probability that a firm will become technically insolvent Technical solvency is measured by net working capital Greater the amount of net working capital – the less risk – prone the firm is or more liquid the firm is

and therefore the less likely it is to become technically insolvent and vice versa

Trade off:

If a firm wants to increase its profitability it must also increase its risk. If it is to decrease risk it must decrease its profitability.

The tradeoff between these variables is that regardless of how the firm increases its profitability through the manipulation of working capital, the consequence is a corresponding increase in risk as measured by the level of net working capital.

Assumptions

The assumptions in evaluating the profitability – risk trade off are:

- Those working capitals are dealing with a manufacturing firm.- That the current assets are less profitable than fixed assets.- That short term funds are less expensive than long term funds.

Effect of the level of current assets on the profitability – risk trade off

It can be shown using the ratio of current assets to total assets. This ratio indicates the percentage of total assets that are in the form of current assets. A change in the ratio will reflect a change in the amount of current assets.

An increase in the ratio: results in

Decrease in profitability, because current assets are assumed to be less profitable than fixed assets.

Decrease risk of technical in-solvency.

A decrease in the ratio: results in

Increase in profitability. Increase in risk. (Corresponding increase in fixed assets which generates higher

returns).

The above ratios are calculated keeping current liabilities constant.

Effect of change in current liabilities on profitability - Risk trade off

Preethi MS Page 3

Advanced Financial Management

Using the ratio of current liabilities to total assets:

- Indicates the percentage of total assets financed by current liabilities.- The effect of change :

a. Increase.b. Decrease

Effect of increase in the ratio:

Profitability will increase – because current liabilities or short term source of finance will increase where as long term source decrease, (short term finances are assumed to be less expensive).

Increases the risk – as any increase in current liabilities keeping current assets constant adversely affects the net working capital.

Effect of a decrease in the ratio:

Decrease in profitability. Decrease in risk.

(Use of long term source leads to increased cost.)

Policies for financing Current Assets

A firm can adopt different financing policies vis-à-vis current assets. Three types of financing may be distinguished:

a. Long – term financing: The sources of long – term financing include ordinary share capital, preference share capital, debentures, long – term borrowings from financial institutions and reserves and surplus (retained earnings).

b. Short – term financing: It is obtained for a period less than one year. It is arranged in advance from banks and other suppliers of short – term finance in the money market. Short – term finances include working capital funds from banks, public deposits, commercial paper, factoring of receivable etc.

c. Spontaneous financing: It refers to the automatic sources of short – term funds arising in the normal course of a business. Trade credit and outstanding expenses are examples of spontaneous financing. There is no explicit cost of spontaneous financing.

Financing mix

- Another ingredient of the theory of working capital management- The choice of sources of financing of current assets.- 2 sources for financing current assets:-

i. Short term sources (current liabilities).ii. Long term sources. - Share capital, long term borrowings, retained earnings, etc.

- What proportion of current assets should be financed by current liabilities and how much by long term resources – decisions will determine the financing mix.

Preethi MS Page 4

Advanced Financial Management

Approaches of financing mix

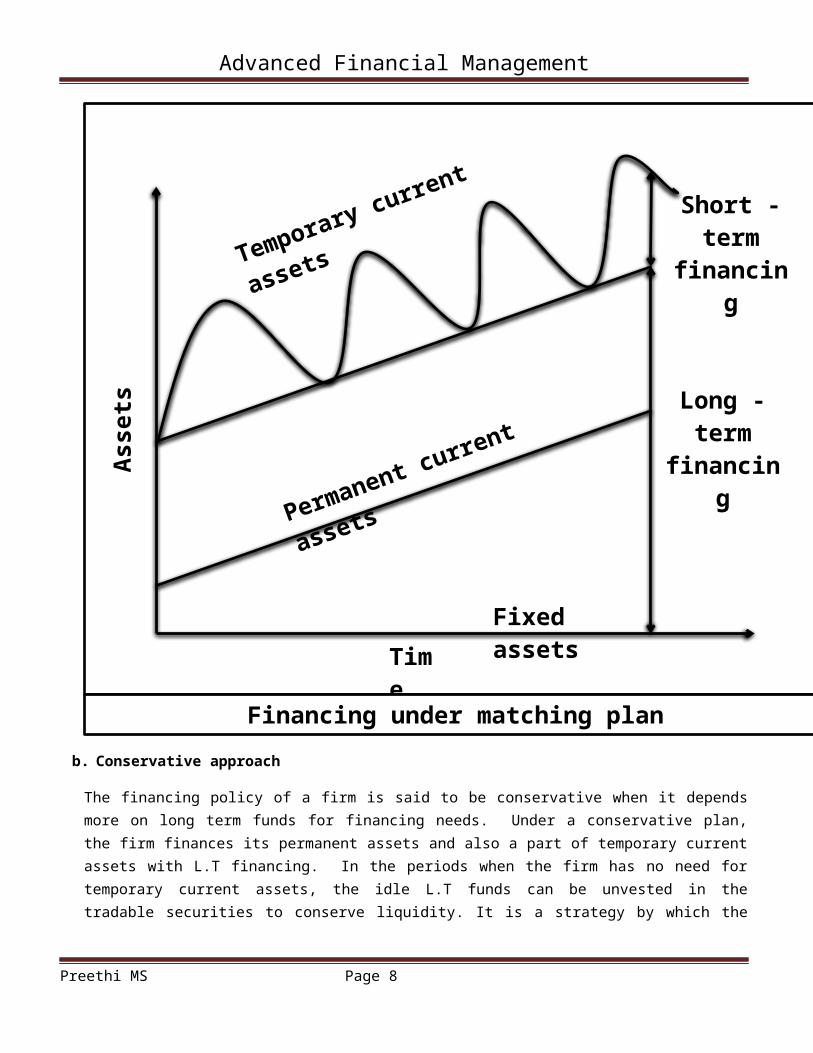

a. Hedging Approach (or) Matching Approach.b. Conservative Approach.c. Aggressive Approach. d. Trade-off between the above 2.

a. Hedging approach

It refers to the process of matching maturities of debt with maturities of financial needs. According to this approach, the maturity of the source of funds should match the nature of the assets to be financed.

The approach suggests that long term funds should be used to finance the fixed portion of current assets requirements. The purely temporary requirements, i.e. the seasonal variations over and above the permanent financing need should be appropriately financed with short term funds (current liabilities).

To sum up:

Permanent portion of funds – financed with long term funds

Seasonal portion of funds – financed with short term funds.

b. Conservative approach

The financing policy of a firm is said to be conservative when it depends more on long term funds for financing needs. Under a conservative plan, the firm finances its permanent assets and also a part of temporary current assets with L.T financing. In the periods when the firm has no need for temporary current assets, the idle L.T funds can be unvested in the tradable securities to conserve liquidity. It is a strategy by which the firm finances all funds requirements, with long term funds and uses short term funds for emergencies (or) unexpected outflows.

Preethi MS Page 5

Asse

ts

Time

Long -

term financing

Short -

term financingFixed

assets

Financing under matching plan

Advanced Financial Management

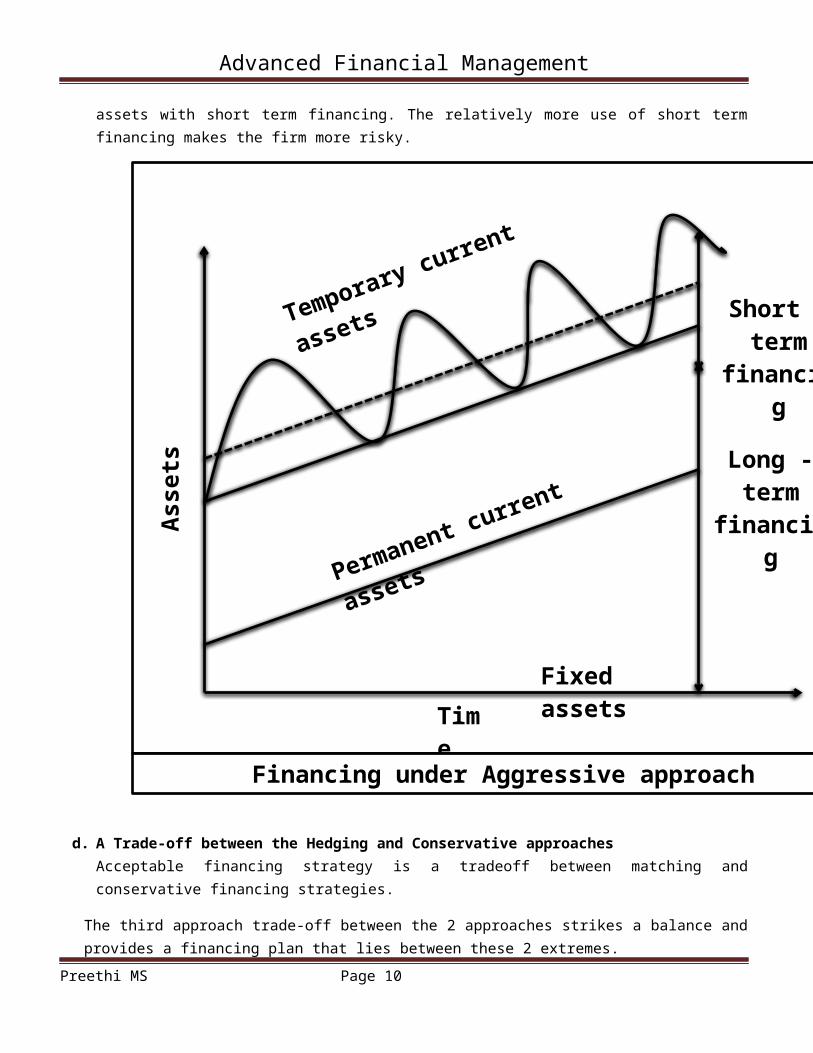

c. Aggressive approachA firm may be aggressive in financing its assets. An aggressive policy is said to be followed by the firm when it uses more short term financing than warranted by the matching plan. Under an aggressive policy, the firm finances a part of its permanent current assets with short term financing. Some extremely aggressive firms may even finance a part of their fixed assets with short term financing. The relatively more use of short term financing makes the firm more risky.

d. A Trade-off between the Hedging and Conservative approachesAcceptable financing strategy is a tradeoff between matching and conservative financing strategies.

The third approach trade-off between the 2 approaches strikes a balance and provides a financing plan that lies between these 2 extremes.

Operating cycle / Working capital cycle / cash cycle:

Preethi MS Page 6

Asse

ts

Time

Long -

term financing

Short -

term financingFixed

assets

Financing under Conservative approach

Asse

ts

Time

Long -

term financing

Short -

term financingFixed

assets

Financing under Aggressive approach

Advanced Financial Management

It is the time duration required to convert sale, after the conversion of resources into inventories, into cash. The operating cycle of a manufacturing company involves 3 phases:

a) Acquisition of resources - such as raw material, labor, power, fuel, etc.b) Manufacturing of raw material into work in progress into finished goods.c) Sale of the product – either for cash or on credit. Credit sales create account receivables for collection.

Operating cycle of a manufacturing firm

The length of the operating cycle of a manufacturing firm is the sum of:

i. Inventory conversion period.ii. Debtors/ receivables conversion period.

Typically it includes

i. Raw material conversion period.ii. Work in progress conversion period.

iii. Finished goods conversion period.

The debtor’s conversion period is the time required to collect the outstanding amount from the customers. The total of inventory conversion period and debtor’s conversion period is referred to as gross operating cycle.

The payables / creditors deferred period is the length of time the firm is able to defer payments on various resources purchases.

The difference between gross operating cycle and payables deferral period is net operating cycle.

Determinants of working capital

1. General nature of business

Preethi MS Page 7

Receivables c.p

Payable

Net operating cycle

purchases

Payment

Credit sale

Collection

Inventory C.PGross

operating cycle

Advanced Financial Management

Public utilities – low working capital requirements.Trading and financial enterprises – high.Manufacturing enterprises – fairly large amount of working capital varies from industry to industry.

2. Production cycle (or) Manufacturing cycle- Refers to the time involved in the manufacturing of goods.- Covers the time span between the procurement of raw material and the completion of the

manufacturing process leading to the production of finished goods.- Longer the time span – larger working capital and vice versa.

3. Business cycleBusiness fluctuations lead to cyclical and seasonal changes.

a. Upward phase – need for working capital is more.b. Downward phase – need for working capital will decline.

4. Production policy

5. Credit policyCredit policy relating to sales and purchases also affects the working capital in 2 ways:

i. Through credit terms granted by the firm to its customers/ buyers of goods.ii. Credit terms available to the firm from its creditors.

- Liberal credits terms – more credit sales and vice versa – more bad debts – more working capital.- Liberal credit terms form suppliers – less need for working capital.6. Growth and expansion

7. Vagaries in the availability of raw materialsWhen sources of raw materials are few/ irregular / scarcity.

8. Profit levelThe N/P is a source of working capital to the extent that it has been earned in cash.

Level of taxes: - determined by the prevailing tax regulations.

Preethi MS Page 8

For seasonal products

Confine production only to period of demandFollow a steady production policyPolicy of diversification

Advanced Financial Management

Dividend policy. Depreciation policy.

9. Price level changes rising prices – more working capital.

10. Operating efficiency Effective utilization of resources by eliminating waste, improving coordination and a fuller utilization of existing resources.

SOURCES OF FINANCING WORKING CAPITAL

I. Long - term Financing

Net current assets or working capital is supposed to be financed by long term sources of finance. It is raised for a period of above five years. It includes ordinary share capital, preference share capital, debentures, long term loans from Bankers and surplus (retained earnings)

II. Short - term Financing

Generally current assets should be financed by short term financial sources. It is obtained for a period of less than one year. The sources of short term finance are loans from banks, short term public deposits, commercial papers, factoring of receivables, bills discounting, retention of profit, etc.,..

III. Spontaneous Financing

It refers to the automatic sources of short term funds arising in the normal course of a business. The major sources of such financing are trade credit (creditors & B/p) and o/s expenses. It is available at cost free.

Note: The real choice of financing current assets lies between short- term and long – term sources

IV. Trade credit A source of short term finance for working capital refers to the credit extended by the

suppliers of goods and services in the normal course of business / transaction/ sale of the firm. Deferral of payment represents a source of finance for credit purchases. Appears in the books of accounts as sundry creditors / accounts payable.

Merits

1. Easily / automatically available.2. Flexible and spontaneous source.

Preethi MS Page 9

Advanced Financial Management

3. Availability and magnitude – size of operations.4. Free from the restrictions associated with formal / negotiated source of finance / credit.

Costs

1. No explicit interest charge.2. Implicit cost – depends on the credit terms offered by the supplier of goods.

V. Bank Finance for working Capital

It is a short term source where by banker decides to sanction short term loans for financing current assets or working capital requirements

Procedure for availing short term loan is:

a) Application and processingb) Sanction, terms and conditionsc) Modes of Bank financed) Securitye) Marginf) Maximum Permissible Bank Finance(MPBF)

a) Application and processingCustomer (firm) seeking short term finance shall submit an application form with the bank disclosing its name, address, nature of business, size of the firm, limit of finance, profitability of the business.

Bank shall process the application considering ability, integrity and experience of the borrower, the criteria considered shall include limit of sanction, interest payment, installment, security etc.,

b) Sanction terms and conditionsApplication once processed by the field investigators, the concerned authority, either, General Manager, Regional Manager or Branch Manager shall sanction the loan by keeping in mind the terms and condition.

Terms and conditions applicable are: Amount of loan ( Max. limit) Nature of advance Period for which the advance will be valid Rate of interest Security

Preethi MS Page 10

Advanced Financial Management

c) Modes of Bank FinanceDifferent types of bank finance includes

1. Direct form of financingi. Cash credit

ii. Short term loansiii. Discounting of bills

2. Indirect form of financingi. Letter of credit

1. Direct form of financing

i. Cash credit:A financial arrangement where amount is credited to the current account of the borrower as per

the predetermined limit. It is also said as overdraft. Interest is charged on the running balance i.e., the amount withdrawn by the borrower. Borrower has liberty to pay interest in installment as and when he desires.

ii. Short term loans:These are advances of fixed amounts which are credited to current account of borrower. Interest is charged on the whole amount but not on the amount withdrawn. Borrower has liberty to pay installment when he desires.

iii. Discounting or purchasing of bills:Bills arise out of the trade transaction. It is an arrangement by the banker in terms of buying and selling of goods. Buyer buys goods from the seller and seller prepares a bill and sends it to the buyer for acceptance. Once the buyer accepts bill, seller furnishes with the bank. Bank will pay or discount the bill on behalf of buyer and later collect the due from the buyer.

Bill may be clean or documentary. A bill which is documentary shall have enclosures in the form of railways receipt, loading or unloading charges fee receipt, bill of loading. A bill without this document is called clean bill. Bill may be paid on demand or with a default period of 90 days.

2. Indirect form of financingi. Letter of credit :

It is an arrangement whereby banker opens an account in the name of its client (customer) to facilitate the trade credit. Customer will be obligated to pay banker by availing a trade credit from the seller of goods.Eg: SBI opens letter of credit with a customer or a buyer i.e., ‘A” whereby, whenever ‘A’ purchases goods from seller ‘B’, banker will make immediate payment to the seller on behalf of its customer (buyer). Bank will charge a minimum cost for arranging this facility. Buyer will make payment to the banker after availing a trade credit a minimum transaction cost. It represents indirect mode of financing.

d) Security

Preethi MS Page 11

Advanced Financial Management

Customer while availing loan has to mortgage a security. It may be in the form of:

1. Hypothecation2. Pledge3. Lien4. Mortgage5. Charge

1. HypothecationIt is a security for availing loan by hypothecation of the moveable property (usually inventories). The hypothecator, who is the owner of the property shall hypothecate movable property with hypothecate (banker). The maintenance of a property during the agreement shall be with the owner. In default the banker shall have right to see the property of hypothecator to recover the debts.

2. PledgeThe owner of a property (pledgee) shall pledge immovable property (land & building) as a security with a banker for availing loan. As per the government banker shall maintain the immovable property and will have a right to sell off if the owner (pledgee) default in making payment as and when it is due.

3. LienRight of the lender to retain property belonging to the borrower until he repays credit. It can be either a particular lien or general lien. Particular lien is a right to retain property until the claim associated with the property is fully paid. General lien is applicable till all dues of the lender are paid. Banks generally enjoy general lien.

4. MortgageIt is the transfer of legal or equitable interest in a specific immovable property for the payment of a debt. The possession of the property may remain with the borrower, with the lender getting the full legal title. The transferor of interest (borrower) is called the mortgagor, the transferee (bank) is called the mortgagee, and the instrument of transfer is called the mortgage deed. The credit granted against immovable property has some difficulties like they are not self – liquidating and difficulties in ascertaining the title and assessing the value of the property. Without the court’s decree, the property cannot be sold.

5. ChargeWhere immovable property of one person is made the security for the payment of money to another by the act of parties / by the operations of law, then the latter person is said to have a charge on the property. All the provisions of simple mortgage will apply. Created by the parties or by operation of law.

e) Margin There is a limit for sanctioning loan to the customer usually banker follow “lower finance on raw- material & higher on account receivables”

Preethi MS Page 12

Advanced Financial Management

f) Maximum Permissible Bank Finance (MPBF)It is introduced by the Tandon Committee and it has suggested three methods for determining MPBF

Tandon committee recommendations

The recommendations of the Tandon committee are based on the following notions:

a. Operating planThe borrower should indicate the likely demand for credit. He should draw operating plan for the ensuing year and supply them to the banker. This procedure will facilitate credit planning at the banks’ level. It will also help the bankers in evaluating the borrower’s credit needs in a realistic manner and in the period follow up during the ensuing year.

b. Production based financingThe banker should finance only the genuine production needs of the borrower. The borrower should maintain reasonable levels of inventory and receivable; he should hold just enough to carry on his target production. Efficient management of resources should, therefore, be ensured to eliminate slow moving and flabby inventories.

c. Partial bank financingThe WC needs of the borrower cannot be entirely financed by the banker. The banker will finance only a reasonable part of it; of r the generated internally and externally.

The following are the major recommendations of the Tandon committee:

i. Inventory and receivable norms Borrower should be allowed to hold only a reasonable level of current assets, particularly

inventory and receivable. Based on a production plan, lead time of supplies, economic ordering levels and reasonable

factor of safety, should be financed by the banker. Flabby, profit – making or excessive inventory should not be permitted under any

circumstance. The banker should finance should finance only those receivables which are in tune with the

practices of the borrower’s firm and industry. In its final report the Tandon committee suggested norms of r fifteen industries excluding

heavy engineering and highly seasonal industries, like sugar. The norms were applied to all industrial borrowers, including small scale industries, with

aggregate limit form the banking system in excess of Rs. 10lakh. The banks should deep in view ht purpose and sprit behind the norms when considering the

extension of credit facilities.

Preethi MS Page 13

Advanced Financial Management

The norms did not suggest entitlement to hold inventories and receivables up to the prescribed level.

If a borrower was efficient and could manage with less in the past, he should continue to do so.

The committee admitted that the norms cannot be followed rigidly. It allowed for flexibility in the application of norms when a major change on the environment justifies.

The committee visualized the circumstances, such as power cuts, strikes, transport delays etc., under which a deviation from norms could be permitted. Deviations should generally be allowed for short periods and should be agreed upon in advance between the borrower and the banker.

The committee also felt that the norms should be kept under constant review. If circumstances justified modification of the norms, it could be effected.

ii. Lending norms Another recommendation of the committee related to the approach to be followed by

commercial banks in lending credit to borrowers. The main function of a banker as a lender was to supplement the borrower’s resources to

carry an acceptable level of current assets. The level of current assets must be reasonable and based on norms. A part of the fund requirements for carrying current assets must be financed from

long term funds comprising owned funds and term borrowing including other noncurrent liabilities.

The banker was required to finance only a part of the working capital gap and the remaining the borrower was to be financed by long term sources.

Working capital cap is defined as current assets minus current liabilities excluding bank borrowings.

Current assets will consist of inventory and receivables, referred as chargeable current assets (CCA) and other current assets (OCA).

iii. Maximum permissible bank finance(MPBF)The committee suggested the following 3 methods of determining the permissible level of bank borrowings:-

First method: the borrower will contribute 25% of the working capital gap and the remaining 75% can be financed form borrowings. This method will give a minimum current ratio of 1:1.

Second method: the borrower will contribute 25% of the total current assets. The remaining the working capital gap can be bridged form the bank borrowings. This method will give a current ratio of 1.3:1.

Preethi MS Page 14

Advanced Financial Management

Third method: - borrower will contribute 100% of core assets, as defined and 25% of the balance of current assets. The remaining of the working capital gap can be met form the borrowings. This method will further strengthen the current ratio.

iv. Style of credit The committee recommended the bifurcation of total credit limit into fixes and fluctuating

parts. The fixed component was to be treated as a demand loan for the year representing the

minimum level of borrowing which the borrower expected to use throughout the year. The fluctuating component was to be taken care of by a demand cash credit. The cash credit portion could be partly used by way of bills. New cash credit limit should be placed on a quarterly budgeting – reporting system. It also recommended the interest differentials. It also recommended that interest rate on the loan component be charged lower the cash

credit account. The RBI stipulated the differential at 1%.

v. Information system It is related to the flow of the information from the borrower to the bank. The committee advocated for the greater flow of information both of operational purposes

and for the purpose of supervision and follow up credit. Information was sought to be provided into three loans: operating statement, quarterly

budget and funds flow statement. The main thrust of the Tandon committee’s recommendation regarding the information flow

was that the banker should be treated as a partner in the business with whom information was to be shared freely and frankly, so that he would be in constant touch with the operation of borrower to whom the bank credit has been allocated.

Advantage in implementing the Tandon committee is:

It brought about a perceptible change in the outlook and attitude of both the bankers and their customers.

It has helped in bringing a financial discipline through a balance and integrated scheme for bank lending.

Criticism

Bankers found difficulties in implementing.

Problems on MPBF

Preethi MS Page 15

Advanced Financial Management

Formulae:I method = 0.75(CA-CL)II Method = 0.75CA- CLIII Method= 0.75(CA- Core CA) – CLNote: Where, Core CA includes inventories

1) Consider the data for Amit and Co.,Current assets Rs. In lakhsInventories 700Debtors 600Cash 150

1450Current LiabilitesTrade Creditors 400Provisions 200

600What is the maximum permissible bank finance (MPBF) under Tandon method? Assume current core assets of the firm as Rs. 600 lakhs.

Solu: I method = 0.75(CA-CL)

= 0.75(1450- 600)

= Rs. 637.5 lakhs

II Method = 0.75CA- CL

= (0.75 * 1450) – 600

= Rs. 487.5 lakhs

III Method= 0.75(CA- Core CA) – CL

= 0.75(1450- 600) – 600

= Rs. 37.5 lakhs

Note: Crs, B/P, o/s expenses, provisions are CL

2) Consider the data for Ambux Company

Preethi MS Page 16

Current assets Amount Current Liabilities AmountRaw material 18 Trade creditors 12Work- in -progress 05 Other current liability 03Finished goods 10 Bank borrowing 25Receivable 15Other CA 02

50 40

Advanced Financial Management

Calculate MPBF for Ambux Company.

Solu: I method = 0.75(CA-CL)

= 0.75(50-15)

= Rs. 26.25

II Method = 0.75CA- CL

= (0.75 * 50) – 15

= Rs. 22.50

III Method= 0.75(CA- Core CA) – CL

= 0.75(50-33) – 15

= Rs. -2.25

Note: i) Core CA = RM + WIP + FG

ii) Bank borrowing is not a part of CL

iii) Bank will not give any finance to the company if the MPBF value is negative

3) Consider the data for Duttreya Company

What is the MPBF under the three methods suggested by Tandon committee? Assume current core assets of the firm as Rs. 18 million.

Solu: I method = 0.75(CA-CL)

= 0.75(36-12)

= Rs. 18 million

II Method = 0.75CA- CL

Preethi MS Page 17

Current assets Amount(million)

Current Liabilities Amount(million)

Raw material 16 Trade creditors 10Work- in -progress 06 Other current liability 02Finished goods 12 Bank borrowing 18Other CA 02

36 30

Advanced Financial Management

= (0.75 * 36) – 12

= Rs. 15 million

III Method= 0.75(CA- Core CA) – CL

= 0.75(36-18) – 12

= Rs. 1.5 million

VI. Public Deposits

Represents unsecured short- term finance by the company with a general public. Cost of financing is in the form of interest (token) payment.

1 year 8 - 9% interest

2 years 9 - 10% interest

3 years 10 - 11% interest

Regulations

a) Maximum financing by public deposit is limited to 25% of share capital and reserves & surplus.b) The time limit for public deposit is maximum three years and five years in non banking finance corporation.c) Company as to disclose certain fact about its financial positiond) Company as to keep 10% of public deposits in the current year to repay the deposits along with the interest

in the next year.

Company’s advantage:

a) This represents unsecured deposits.b) Cost of raising funds is limited.c) Free tax cost is low.d) Progressing in raising fund is easy and simply or fair and simple.

Company’s dis-advantage:

a) Period of payment is limited to three yearsb) Interest payment is very costly

Depositor’s advantage:

a) Return is highb) Duration of length is low

Depositor’s dis - advantage:

a) It is unsecured and more risky for depositor

Preethi MS Page 18

Advanced Financial Management

b) Interest is not tax exemptc) Higher the return more the payment of tax

VII. Inter corporate Deposits

It deposits unsecured deposits between two or more than two companies which have a very good worthiness.

1. Call Deposits:It is also referred as on demand deposits, which mean deposit withdrawal by lender by giving one day’s notice. In practice one to three days would be extended for the repayment; interest rate is 10%.

2. Three month deposit:More popular in practice where the deposits are taken by the borrower to finance the short term requirements like tax payment, dividend payment, and unplanned capital expenditure. Even it is also used for inadequacy of short term cash in case of disruption in production, imports and duty payments. Interest rate is at 12%.

3. Six month deposit:Normally lending companies do not extend deposits beyond this time. Such deposits are usually made with high class borrowers. Interest payment is at 15%.

VIII. Short term loan by financial institutions

LIC & GIC of India provides short term loan to manufacturing companies with an excellent track record.

Regulations

A company to be eligible to receive short term loans should meet the following regulations:

a) Company should have declared not less than 6% dividends for the past five years.b) Debt equity ratio should be 2:1.c) Current ratio should be 1:1.d) Coverage ratio (interest) should be 2:1.

Features

a) These are unsecured and given on the strength of demand promissory note.b) Maximum time frame is one year and can be extended to the next consecutive year.c) Company has to wait for six months minimum for the next fresh loan.d) 18% is the rate of interest acceptable by the borrower and 1% is a discount for the prompt payment.

Commercial Paper

Represents unsecured promissory notes issued by highly credit worthy companies. Generally large companies with considerable financial strength will be able to issue the commercial paper. Maturity period of commercial paper is 90 days to 360 days. These are issued at discount and redeemed at par. It is issued to high borrowers who hold the instrument till the maturity. It does not have secondary market.

Preethi MS Page 19

Advanced Financial Management

Regulations:

Since these are unsecured, RBI regulates & imposes as a mandatory requirement for the company issuing commercial paper.

a) Company should have 60 million net worth.b) Company’s shares should have been listed in stock exchange.c) Companies should number one health code status.d) Current ratio should be 1.33:1e) Companies should be rated as P1 by CRISIL and P2 by ICRA.f) Face value of commercial paper issued by it does not exceed its working capital.g) Debt equity ratio should be 2:1.

Advantages

Simple instrument hardly involving any documentation. Flexible in terms of maturities. A well rated company can diversify its short term sources of finance. Investor get higher returns than banking systems. No limitations on the end use of funds raised through them They are unsecured. Negotiable instrument highly liquid. Regulated by RBI. Products ranging from 15 days to 1 year. Minimum subscription is Rs. 5lakhs, minimum issues is Rs. 25lakhs. Maximum limit of raising 100% of working capital of company.

IX. Factoring

It is system where factor is a financial institution, which renders services for financing & managing of debts arising out of credit sales. As per the mandatory requirement of RBI, leading financial institution across the country is rendering factoring services to their clients.

Western region – SBI factoring

Southern region – CAN bank factoring

Eastern region – Allahabad factoring

Northern region – Punjab National Bank factoring

Factoring means arrangements between a factor & his client which includes at least two of the following services to be provided by the factor. Finance, maintenance of accounts, collection of debts, protection against credit risk.

Preethi MS Page 20

8. pays remaining 20% (with commission)7. Makes the full payment

6. Follow up5. Pays upto 80%

CLIENT

CLIENT

BUYER

CLIENT

FACTOR

CLIENT

1. Place an order

3. Deliver goods along with invoice & notice

2. Establish credit limit

Advanced Financial Management

“Factoring is an agreement in which receivables arising out of scale of goods/ services are sold by a firm (client ) to the ‘factor’ (a financial intermediary) as a result of which the title of the goods / services passes on to the factor.”

Function of a Factor

- Financing facility / trade debts.- Administration of sales ledger.- Collection of accounts receivables.- Assumption of credit risk.- Provision of advisory services.

Mechanism of Factoring

Features of Factoring

Factor selects the accounts of clients to advance debts arising out of credit sales.Factor assumes responsibility of collecting the debt from the buyer and making payment to the seller.To make pre payment of 80% of debt if it follows 90 days or the last day of credit which ever period is earlier.Factor charges interest for making payment to the seller which may be either equal to lending rates of financial institutions or more than that.Factor charges commission which may range from 1% to 2% of debt financed.Factoring may be an resource basis (where risk is assumed by the client i.e., if buyer becomes insolvent or default) & non- resource basis ( where risk is assumed by the factor)

Types of Factoring

1.Resource factoring2.Non- resource factoring3.Modified recourse factoring4.Undisclosed factoring

Preethi MS Page 21

4. Sends a copy of invoice

Advanced Financial Management

5.Notified factoring6.Bulk factoring7.Domestic factoring8. International factoring9.Export factoring10. Import factoring

1. Recourse factoring

Factor provides all types of facilities except debt protection. This type of factoring transaction allows the factor to go back to the seller if payment is not received (normally after a 90 days period). It is less expensive and less risk for client & factor respectively

2. Non- resource factoring

Factor offers all types of services – finance, sales ledger administration, collection, advisory services and debt protection. Here factor assumes 100% credit risk. Factor gives protection against bad debts to the client (seller).

3. Modified recourse factoring

Factor offers protection to the client if the customer fails to pay the invoice due to financial failure or bankruptcy. However, if the client refuses to pay the invoice from a dispute over quality, delivery or specifications. The factor has recourse back to the sellers other receivables.

4. Undisclosed factoring

Factor does not follow up or collect payment from the buyer. Here customer may not be aware of the factoring arrangement & pays the invoice directly to the client. The factor receives invoice through the client. It is also known as open account receivables.

5. Notified factoring

With notified factoring the buyer (debtor) is informed that the debt has been purchased & they are requested to pay the factor directly.

6. Bulk factoring

Client (seller) maintains and keeps sales ledger on behalf o factor. This arrangement is generally preferred by client where they have good credit management system, but needs finance. It is also known as in-house factoring or agencies factoring.

7. Domestic factoring

It is the factoring arrangement where all the three parties the factor, client and the buyer are domiciled in the same country, subject to the laws of country.

8. International factoring

Preethi MS Page 22

Advanced Financial Management

It is the factoring arrangement where the seller co-operation between two factoring companies, are in the seller’s country (export factor) and the other in the buyer’s country (import factor).

9. Export factoring

Export factoring arrangement in which domestic companies (exporters) use the factor’s services in same. Country- factor located in seller’s country.

In today’s business environment money businesses are selling millions of rupees worth goods or services to foreign customers. Factoring services are necessary for continuous flow of cash, reduced administration cost & credit protection.

10. Import factoring

Seller (exporter) use the factor’s services in other country. Factor is located in buyer country.

Advantages of factoring

Seller can have continuity of flow of funds. Seller can eliminate the collection debt.

Dis - advantages of factoring

Cost of financing through factoring is very high (interest & commission). It is perceived as seller is unable to collect the debts from the buyer.

X. Short- term loans by Insurance

To avail loan, a company should have declared 6% dividend for the past five years. Current ratio should be 1:1. Debt equity ratio should be 2:1.

Regulations - It is regulated by RBI that insurance company can change 18% of interest, with the following features:

Company can avail next short term loan after six months of clearing the previous loan. It is unsecured in nature. Maximum period of loan is one year.

Determination of Level of Current Assets

An important working capital policy decision is concerned with level of investment in current assets. There are two working capital policies:

1. Flexible policy 2. Restrictive policy

Flexible policy

Preethi MS Page 23

Advanced Financial Management

It is referred to as a conservative policy where the investment in current assets is high which means the firm maintains a huge balance of cash, marketable securities, carries large amount of inventories and grants generous credit terms which leads to high level of debtors.

Impact

a. Blockage of fundsb. Few production stoppagesc. It stimulates sales as credit terms are liberal

Restrictive policy

This means that current assets are low. Also referred to as aggressive policy. It means maintains a small amount of cash, marketable securities, manages with smaller amount of inventories, few debtors with strict credit terms.

Impact

a. It reduces sales as the credit terms are strict & stringentb. There is no blockage of fundsc. There will not be high cost in holding inventories

Note: A best policy is the one which balances between aggressive and conservative policies, which means an optimum level of inventory, current assets should be maintained.

Adequacy of Working Capital

Working capital should be adequate for following reasons:

1. It protects a business from the adverse effects of shrinkage in the values of current assets.2. It is possible to pay all the current obligations promptly and to take advantage of cash discounts.3. It ensures to a greater extent the maintenance of a company’s credit standing & provides for such

emergencies as strikes, floods, fires etc.,4. It permits the company of inventories at a level that would enable a business to serve satisfactorily the

needs of its customers.5. It enables a company to extend favorable credit terms to customers.6. It enables a company to operate its business more efficiently because there is no delay in obtaining

materials etc., because of credit difficulties.7. It enables a business to withstand periods of depression smoothly8. There may be operating losses or decreased retained earnings.9. There may be excessive non- operating or extra- ordinary losses10. Management may fail to obtain funds from other sources for purposes of expansion.11. There may be an unwise dividend policy.12. Current funds may be invested in non- current assets.

Preethi MS Page 24

Advanced Financial Management

13. Management fails to accumulate funds necessary for meeting debentures on maturity.14. There may be increasing price necessitating bigger investments in inventories and fixed assets.

Inadequacy of Working Capital

1. It s not possible for it to utilize production facilities fully for the want of working capital.2. A company may not be able to take advantage of cash discount facilities.3. The credit worthiness of the company is likely to be jeopardize because of the lack of liquidity4. A company may not be able to take advantage of profitable business opportunities.5. The modernization of equipment and even routine repairs and maintenance facilities may be difficult to

administer.6. A company will not be able to pay its dividends because of the non- availability of funds.7. A company cannot afford to increase its cash sales and may have to restrict its activities to credit sales

only.8. A company may have to borrow funds at exorbitant rates of interest. 9. The low liquidity may lead to low profitability in the same way as low profitability results in low

liquidity.10. Low liquidity would positively threaten the solvency of the business. A company is considered illiquid

when it is not able to pay its debt on maturity.

Dangers of excessive working capital

Too much working capital is as dangerous as too little o it. Excessive working capital raises the following problems.

1. A company may be tempted to override & lose heavily.2. A company may keep very big inventories and tie up its funds unnecessarily.3. There may be an imbalance between liquidity & profitability4. A company may enjoy high liquidity and, at the same time, suffer from low profitability.5. High liquidity may induce a company to undertake greater production which may not have a matching

demand. It may find itself in an embracing position unless its marketing policies are properly adjusted to boost up the market for its goods.

6. A company may invest in its fixed equipment which may not be justified by actual sales or production. This may provide a fertile ground for later over capitalization.

7. Excessive working capital may be as unfavorable as inadequacy of working capital because of the large volume of funds not being used productively.

Working Capital Leverages

It refers to impact of level of current assets on company’s profitability or return on capital employed. It signifies the change in level of current assets brings change in the level of ROCE. It also measures the responsiveness of ROCE for changes in current assets.

Preethi MS Page 25

Advanced Financial Management

The working capital leverage reflects the sensitivity of return on capital employed to changes in level of current assets. Working capital leverage would be less in the case of capital intensive capital employed is same working capital leverage expresses the relation of efficiency of working capital management with the profitability of the company.

Impact on ROCE

1. Higher investment in current assets than required actually means increase in the cost of interest on short term loans and working capital finance raised from banks & insurance companies. This reduces the profitability in the long run.

2. To improve the profitability, the productivity should be increased. An optimum level of investment in current assets leads to increase in productivity & thereby increasing sales & generating revenues.

3. This concept improves the profitability position or ROCE.

Problems on Working capital leverages

Formulae: Working capital leverage (WCL) = _____current assets____________

Total assets – change in current assets

WCL = __CA___

(TA - ∆ CA)

1) Following is the information relating to ABC Ltd., and XYZ Ltd.,

You are required to compute the working capital leverage with a 20% increase & reduction in current assets.

Solu: Calculation of working capital leverage

WCL = __CA___

(TA ± ∆ CA)

Particulars ABC Ltd., XYZ Ltd.,

(i ) Increase in CAWCL = CA/TA +∆ CA 200/280+40 80/280+16

= 62.5% = 27%(ii ) Decrease in CA

Preethi MS Page 26

Description ABC Ltd., (million) XYZ Ltd., (million)Current assets 200 80Net fixed assets 80 200Total assets 280 280EBIT 700 700ROI 25% 25%

Advanced Financial Management

WCL = CA/TA-∆ CA 200/280-40 80/280-16

= 83.33% = 30.30%

Inference: Sensitivity of ROCE is more in ABC Ltd., than in XYZ Ltd.,

2) Following information is available for 2 companies:

Particulars Arun Ltd.,(Million) Ajay Ltd (Million)Current assets 150 50Net fixed assets 50 150Total current assets 200 200EBIT 30 30ROI 15% 15%

Calculate WCL at 20% decline or increase in CA.

Solu:

Particulars Arun Ltd., Ajay Ltd.,

(i) Increase in CA(20%)WCL = CA/TA +∆ CA 150/200+30 50/200+10

= 65.22% =23.81%(ii) Decrease in CA(20%)WCL = CA/TA-∆ CA 150/200-30 50/200-10

= 88.24% = 26.32%

Inference: Sensitivity of change in ROCE is more due to change in level of CA in Arun Ltd., than in Ajay Ltd.,

3) From the following information calculate WCL for MNC & ABC:

Description MNC ABCNet fixed assets 60 200Total assets 200 250

Assume a 10% increase or decrease in the level of current assets

Solu: Current assets = Total assets – fixed assets

MNC; CA = 200-160 = 140

ABC; CA = 250-200 = 50

Particulars MNC Ltd., ABC Ltd.,

(i ) Increase in CA (10%)WCL = CA/TA +∆ CA 140/200+14 50/250+5

= 65.42% =19.61%(ii ) Decrease in CA (10%)WCL = CA/TA-∆ CA 140/200-14 50/250-5

= 75.27% = 20.41%

Preethi MS Page 27

Advanced Financial Management

Inference: Sensitivity of change in ROCE is more due to change in level of CA in MNC Ltd., than in ABC Ltd.,

Preethi MS Page 28