model-independent option valuation dr. kurt smith

TRANSCRIPT

Model-Independent Option Valuation

Dr. Kurt Smith

Overview

• Introduction• Boundaries• Vertical Spread• Butterfly Spread• Calendar Spread• Conclusion

Model-Independent Option Valuation; Dr. Kurt Smith

Finance (Derivative Securities)

Finance (Derivative Securities)

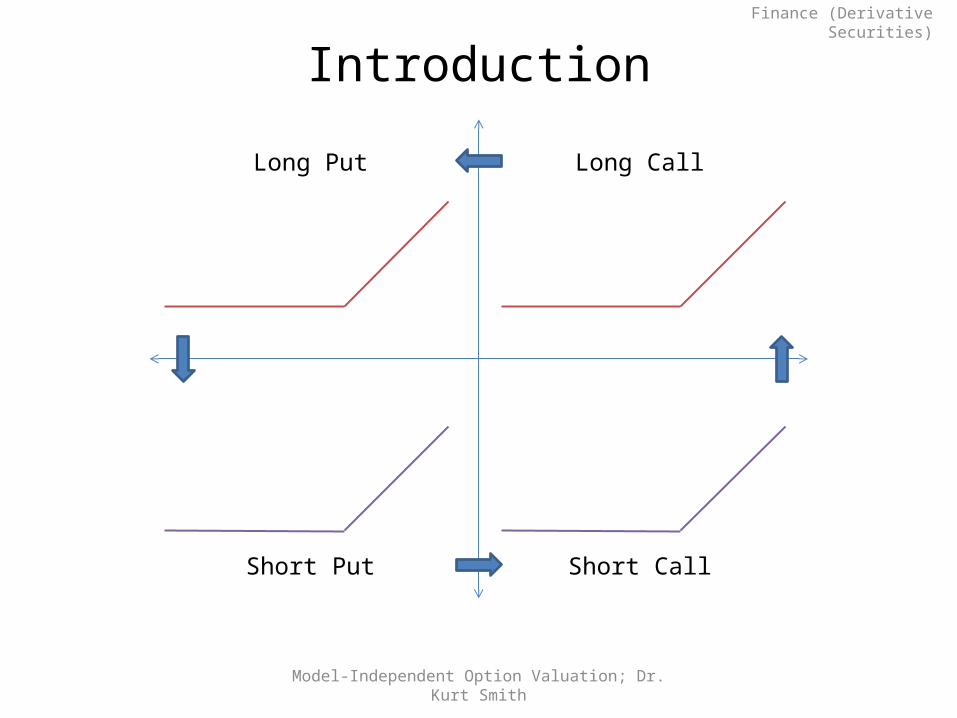

Introduction

Model-Independent Option Valuation; Dr. Kurt Smith

Finance (Derivative Securities)

Introduction

Model-independent means value relationships between different options on the same underlier that must hold to prevent arbitrage. These relationships must hold for every option pricing model.

The absence of vertical spread, butterfly spread and calendar spread arbitrages is sufficient to exclude all static arbitrages from a set of option price quotes across strikes and maturities on a single underlier.

Option buyers have the right, not the obligation, to exercise the option at expiry (European) or anytime up to and including expiry (American). Expiry payoff diagrams for options can be obtained via simple rotations about the x- and y-axis.

•

•

•

Model-Independent Option Valuation; Dr. Kurt Smith

The focus in this lecture is on a single underlier with zero intermediate cash flows (e.g., no dividends). For simplicity, interest rates are assumed to be zero unless stated otherwise.

•

Finance (Derivative Securities)

Introduction

Model-Independent Option Valuation; Dr. Kurt Smith

Expi

ry P

ayoff

STK

European Call

Expiry payoff = MAX(ST – K, 0)=(ST – K)+

100 12070

ST=120, K=100; then (ST – K)+=20

ST=70, K=100; then (ST – K)+=0

Examples:

Expi

ry P

ayoff

STK55 11030

European Put

Expiry payoff = MAX(K – ST, 0)=(K – ST)+

ST=110, K=55; then (K – ST)+=0

ST=30, K=55; then (K – ST )+=25

Examples:

Finance (Derivative Securities)

Introduction

Model-Independent Option Valuation; Dr. Kurt Smith

Long CallLong Put

Short Put Short Call

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

Contract maturity (Tj).

Strike price (Ki).

Spot price (S0).

American exercise.

For European Call options Ci,j and European Put options Pi,j.

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

Contract maturity (Tj):

At expiry: , 0, i i j iK C S K

Before expiry:

0T

0T , 0, jrTi i j iK C S K e

•

•

At the limit:• T , 0, limi i jTK C S

t=0 T

S0 Ki

T=0

S0,Ki

t=0 T=∞

S0 Ki

Call

Pric

e

S0KijrT

iK e r

iK e

, 0i jC , 0i jC ,i jC

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

Strike price (Ki):

Zero: , 0 0, jrTj i j iT C S K e S

At the limit:

0K

K

•

• ,, lim 0j i jKT C

Call

Pric

e

S0Ki0K

, 0i jC 0, 0i jC S

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

Spot price (S0):

Zero: 0 0S •

Call

Pric

e

S0Ki0 0S

, 0, , 0jrTi j i j iK T C S K e

• At the limit: 0S , 0, , i j i jK T C S

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

American exercise (Amex.):

• ., ,, , 0Amex

i j i j i jK T C C

An American option has all of the features of a European option PLUS the ability to exercise early if it is in the buyer’s interest. Therefore, an American option cannot be worth less than a European option.

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

Why is the value of a Call option non-negative (Ci,j ≥ 0) whereas the value of a forward contract Ft can be negative?

A Call option expiry payoff (ST - Ki)+ ≥ 0. Since there is no possibility of loss at T, the option value at t Ci,j ≥ 0. In contrast, the expiry payoff of a forward contract (ST - ft;S,T) is positive, negative, or zero.

Expi

ry P

ayoff

STKi

Call Option

Expi

ry P

ayoff

ST

Forward Contract

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

European Put-Call parity for an underlier with no interim cash flows (e.g., no dividends): a forward contract and a synthetic forward contract created by options must have the same value.

Expi

ry P

ayoff

ST

f(t;S,T)=K

Buy at K thru long Call if ST > K

Buy at K thru short Put if ST < K , ,i j i jC P

0 0jrT

iF S K e , , 0

jrTi j i j iC P S K e

, , 0jrT

i j i j iP C S K e

Finance (Derivative Securities)

Boundaries

Model-Independent Option Valuation; Dr. Kurt Smith

Put options:

., ,, , 0Amex

i j i j i jK T P P

Maturity:

Strike:

0T

0T

•

•

Spot:•

T

, 0, i i j iK P K S

, 0, jrTi i j iK P K e S

,, lim 0i i jTK P

, 0, 0jrTj i j iT P K e S

0K

K ,, limj i jKT P K

0 0S , 0, , j jrT rT

i j i j i iK T P K e S K e

0S ,, , 0i j i jK T P

American:•Pu

t Pric

e

S0Ki

Ki

Finance (Derivative Securities)

Vertical Spread

Model-Independent Option Valuation; Dr. Kurt Smith

Finance (Derivative Securities)

Vertical Spread

Model-Independent Option Valuation; Dr. Kurt Smith

1 2 0C K C K

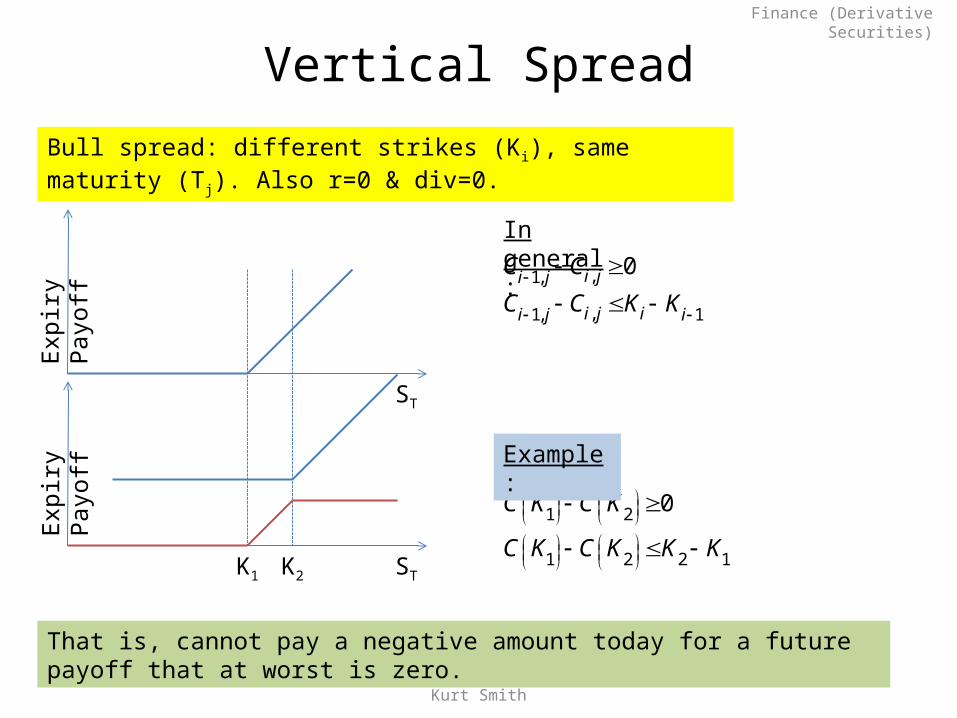

Bull spread: different strikes (Ki), same maturity (Tj). Also r=0 & div=0.

,1, 0i ji jC C

Expi

ry P

ayoff

Expi

ry P

ayoff

ST

STK1 K2

In general:

,1, 1i j ii j iC C K K

Example:

1 2 2 1C K C K K K

That is, cannot pay a negative amount today for a future payoff that at worst is zero.

Finance (Derivative Securities)

Vertical Spread

Model-Independent Option Valuation; Dr. Kurt Smith

How? Now t Payoff at Expiry T

Portfolio t ST < 50 50 ≤ ST ≤ 55 ST > 55

Buy K2 = 55 12 0 0 ST – 55

Sell K1 = 50 -18 0 -(ST – 50) -(ST – 50)

Sub-Total -6 0 50 – ST -5

Lend Cash 6 ≥ 6 ≥ 6 ≥ 6

Total 0 > 0 > 0 > 0

Therefore, pay zero today to get a guaranteed positive payoff in the future (Type 3 arbitrage violation). The trader will do this as many times as possible to pay a multiple of zero today to earn a multiple of a positive amount in the future.

Example: Let C(K1=50)=$18 and C(K2=55)=$12. Is there an arbitrage? If so, how would you exploit it?

,1, 1Since 18 12 6 5 55 50 : arbitrage.i j ii j iC C K K

Sell the bull spread. Why?

Finance (Derivative Securities)

Vertical Spread

Model-Independent Option Valuation; Dr. Kurt Smith

2 1 0P K P K

Bear spread: different strikes (Ki), same maturity (Tj). Also r=0 & div=0.

, 1, 0i j i jP P

Expi

ry P

ayoff

Expi

ry P

ayoff

ST

STK1 K2

In general:

, 1, 1i j ii j iP P K K

Example:

2 1 2 1P K P K K K

That is, cannot pay a negative amount today for a future payoff that at worst is zero.

Finance (Derivative Securities)

Butterfly Spread

Model-Independent Option Valuation; Dr. Kurt Smith

Finance (Derivative Securities)

Butterfly Spread

Model-Independent Option Valuation; Dr. Kurt Smith

1 1 1,1, 1,

1 10ii i i

i ji j i ji ii i

K K K KC C C

K K K K

Expi

ry P

ayoff

Expi

ry P

ayoff

ST

STK1 K2 K3

3 1 2 11 2 3

3 2 3 20

K K K KC K C K C K

K K K K

If K2 - K1 = K3 - K2 then C(K1) – 2C(K2) + C(K3) must have a value greater than zero.

In general:

Example:

Butterfly spread: different strikes (Ki), same maturity (Tj). Also r=0 & div=0.

That is, cannot pay a negative amount today for a future payoff that at worst is zero.

Finance (Derivative Securities)

Butterfly Spread

Model-Independent Option Valuation; Dr. Kurt Smith

0

0.5

1

1.5

2

2.5

50 70 90 110 130 150

Expi

ry P

ayoff

Expiry Spot

K=70, 72, 90

0

2

4

6

8

10

12

50 70 90 110 130 150

Expi

ry P

ayoff

Expiry Spot

K=70, 80, 90

02468

101214161820

50 70 90 110 130 150

Expi

ry P

ayoff

Expiry Spot

K=70, 88, 90

Asymmetric butterflies

Symmetric butterfly

C(K=70)-1.11C(K=72)+0.11C(K=90) C(K=70)-10C(K=88)+9C(K=90)

C(K=70)-2C(K=80)+C(K=90)

Finance (Derivative Securities)

Butterfly Spread

Model-Independent Option Valuation; Dr. Kurt Smith

Example: Let C(K=70)=$7, C(K=80)=$6 and C(K=90)=$4. Is there an arbitrage? If so, how would you exploit it?

1 1 1,1, 1,

1 10ii i i

i ji j i ji ii i

K K K KC C C

K K K K

3 1 2 11 2 3

3 2 3 20

K K K KC K C K C K

K K K K

90 70 80 707 6 4 190 80 90 80

Hence, yes there is an arbitrage. Buy Call(K1=70), sell 2 Call(K2=80), buy Call(K3=90). The trader will receive $1 now [i.e., at t=0 will pay 7-2(6)+4=-$1 ]; and will have zero probability of loss in the future (refer to expiry payoff figure).

0

2

4

6

8

10

12

50 70 90 110 130 150

Expi

ry P

ayoff

Expiry Spot

K=70, 80, 90

Finance (Derivative Securities)

Calendar Spread

Model-Independent Option Valuation; Dr. Kurt Smith

Finance (Derivative Securities)

Calendar Spread

Model-Independent Option Valuation; Dr. Kurt Smith

,, 1 0; , 0i ji jC C i j

Expi

ry P

ayoff

ST

Call

Pric

e

S0

, 1i jC ,i jC

, 0i jC

Calendar spread: same strikes (Ki), different maturities (Tj). Also r=0 & div=0.

In general:

Example:

2 1 0C T C T

That is, cannot pay a negative amount today for a future payoff that at worst is zero.

Finance (Derivative Securities)

Calendar Spread

Model-Independent Option Valuation; Dr. Kurt Smith

Example: the price of a Call option expiring at T1 is $5 and T2 is $4, where T1 < T2. Is there an arbitrage? If so, how would you exploit it?

Expiry Payoff at T2

ST2 < K ST2

> K

Now Expiry Payoff at T1

Portfolio t ST1 < K ST1

> K ST1 < K ST1

> K

Sell C(T1) -5 0 -(ST2-K) 0 -(ST2

-K)

Buy C(T2) 4 0 0 ST2-K ST2

-K

Total -1 0 K-ST2ST2

-K 0The trader receives $1 today (t) for non-negative expiry payoffs at T2 . This is a Type 2 arbitrage violation. Sell near (T1) and buy far (T2) maturity to extract the arbitrage profit.

Finance (Derivative Securities)

Conclusion

Model-Independent Option Valuation; Dr. Kurt Smith

Finance (Derivative Securities)

Conclusion

Model-independent means value relationships between different options on the same underlier that must hold to prevent arbitrage. These relationships must hold for every option pricing model.

The absence of vertical spread, butterfly spread and calendar spread arbitrages is sufficient to exclude all static arbitrages from a set of option price quotes across strikes and maturities on a single underlier.

Option buyers have the right, not the obligation, to exercise the option at expiry (European) or anytime up to and including expiry (American). Expiry payoff diagrams for options can be obtained via simple rotations about the x- and y-axis.

•

•

•

Model-Independent Option Valuation; Dr. Kurt Smith

Vertical Spread: Butterfly Spread: Calendar Spread:

1 2 2 10 C K C K K K

3 1 2 11 2 3

3 2 3 20

K K K KC K C K C K

K K K K

2 1 0C T C T

Finance (Derivative Securities)

Conclusion

Model-Independent Option Valuation; Dr. Kurt Smith

Expi

ry P

ayoff

Expi

ry P

ayoff

ST

STK1 K2

Expi

ry P

ayoff

Expi

ry P

ayoff

ST

STK1 K2

Vertical Spread

Bull Spread Bear Spread

1 2 0C K C K

1 2 2 1C K C K K K

2 1 0P K P K

2 1 2 1P K P K K K

Finance (Derivative Securities)

Conclusion

Model-Independent Option Valuation; Dr. Kurt Smith

Expi

ry P

ayoff

Expi

ry P

ayoff

ST

STK1 K2 K3

3 1 2 11 2 3

3 2 3 20

K K K KC K C K C K

K K K K

Butterfly Spread

Finance (Derivative Securities)

Conclusion

Model-Independent Option Valuation; Dr. Kurt Smith

Call

Pric

e

S0

, 1i jC ,i jC

, 0i jC

2 1 0C T C T

Calendar Spread