mo universal map fund family...the funds are managed with a long-term mind-set and the group...

TRANSCRIPT

BMO

Universal MAP Fund Family March 2020

2

© Defaqto Limited 2020. All rights reserved. No part of this publication may be reprinted, reproduced or used in any form or by any electronic, mechanical, or other means, now known or hereafter invented, including photocopying and recording, or in any information storage or retrieval system without the express written permission of Defaqto. This Fund Review is for the professional use of professional financial advisers only, and is solely made to and directed at such financial advisers. It is intended to be used by them only to inform them in the independent financial advice they give to their clients, and then only if those financial advisers are not acting as agents for their clients or, at least, will not be acting as agents for their clients in purchasing an interest in the investment or fund which is the subject of this Fund Review (Purchasing the Investment). This Fund Review is not for the use of, and is not made to, or directed at, the clients of professional financial advisers or anyone who may be considering purchasing the investment. No such clients or such other persons should rely on this Fund Review, and Defaqto shall not be liable in any respect whatsoever to such clients or other persons if they do so. This Fund Review was prepared by, and remains the copyright of, Defaqto.

Defaqto makes no warranties or representations regarding the accuracy or completeness of the information or views contained in this Fund Review. The views contained herein simply represent the views of Defaqto at the date of publication and both those views and the information set out herein may change without reference or notification to any recipient of this Fund Review. Defaqto does not offer investment advice or make recommendations regarding investments and nothing in this Fund Review constitutes, is intended to constitute, or should be taken as, a recommendation or advice that any investment activity be undertaken by any person. Readers of this Fund Review must make their own independent assessment of whether it is appropriate to purchase the investment. Defaqto is not acting as financial adviser or in any fiduciary capacity in relation to any transaction in any investment. Nothing in this Fund Review constitutes, is intended to constitute, or should be taken as, financial promotion, any incentive or any inducement to engage in any investment activity whatsoever, including to purchase the investment. It is not the purpose or intention of this Fund Review to persuade or incite anyone to engage in any such investment activities.

3

The Defaqto experts have created a range of ratings to help advisers find the best product or proposition for their clients.

An overall assessment of service – by advisers for

advisers.

Demonstrate the comprehensiveness of products

across a range of areas, from pensions to DFMs.

Defaqto have created a set of ten Risk Profiles, and four Income Risk Profiles with corresponding ratings to which funds are mapped using a robust process. This helps advisers to evidence suitability for their clients in both the accumulation and decumulation phase:

Show at a glance how a fund or fund family performs in

comparison to the rest of the market.

This document is designed to provide the reader with a quantitative overview of the fund/s reviewed. The review then goes on to examine information of a more qualitative nature, which has been obtained through an interview process with the fund manager/s. The qualitative information covers specific areas including the fund manager’s philosophy, their people, and the processes they employ. Additional information is also provided on their research capability, the resources they have at their disposal and how they manage risk. All of this information goes towards creating this comprehensive Fund Review.

Defaqto fund reviews

Defaqto Ratings Ratings to help advisers and their clients make better informed decisions

Suitability ratings to support compliant advice

4

BMO’s Universal MAP range launched with three funds in November 2017 and then added three further funds in October 2019. Five of the funds aim to provide CPI+ returns over the long-term within clearly targeted risk parameters i.e. predefined target volatility bands, while the Income fund aims for at least 4% of natural income. The funds provide differing risk/return profiles, with the Defensive fund being the lowest risk and the Adventurous the highest. The Income fund is designed to have a similar risk profile as the Balanced fund (8-10% target volatility on a rolling ten-year basis). The range’s declared USP is that the funds are actively managed but at passive-style cost, with the OCF capped at 0.29%.

Asset allocation - both strategic and tactical - is intended to be the main driver of returns, with both being the output of detailed internal processes that are initially quant driven but then qualitatively reassessed. Beyond that, this is essentially an actively managed fettered

product, made up of direct investments with some fund allocations; in terms of fund selection, the team can access the wide range of BMO specialist funds at favourable cost to populate the asset allocation. That said, investors should bear in mind that being fettered does constrain fund choices. Whilst the fund is actively managed at asset allocation level, investors should note that the funds may still use ETFs and index trackers where there are no appropriate actively managed vehicles available.

The multi-asset team of 28 responsible for this range has good average levels of experience and expertise, and is led by Paul Niven, whose own asset allocation and management expertise spans over 24 years.

The funds are managed with a long-term mind-set and the group emphasises that they are intended for investors with at least a five-year time horizon.

The Bank of Montreal Financial Group (BMO), established in Canada in 1817, is a diversified financial services provider based in North America and North America’s eighth largest bank by assets. It has over 45,000 employees, providing personal banking, commercial banking, wealth management and investment banking services to over 12 million customers.

The group’s asset management division, BMO Global Asset Management, has around £225bn AUM. Its asset management activity is focused in four major investment hubs - Canada (Toronto/Montreal), the US (Chicago/Miami), EMEA (London/Edinburgh) and Asia Pacific (Hong Kong) - and overall it has over 20 offices in 14 countries.

In 2014, F & C became part of the BMO Financial Group. The majority of its products and services have been rebranded to BMO, as the group seeks to emphasise the global reach of its product range and investor solutions capability.

The multi-asset team responsible for this product numbers 28 and is led by Paul Niven; it is split across three of BMO’s investment hubs, with ten investment professionals in London, six in Chicago and twelve in Toronto. All told, the multi-asset team has over £30bn in AUM globally.

Fund review BMO

Universal MAP Fund Family

Executive summary

About BMO

Defaqto Ratings

Fund Family Diamond Rating Risk Rating Income Risk Rating

Universal MAP Defensive Fund

5

3 NA

Universal MAP Cautious Fund 4 NA

Universal MAP Balanced Fund 5 NA

Universal MAP Growth Fund 6 NA

Universal MAP Adventurous Fund 8 NA

Universal MAP Income Fund 5 NA

5

Five of the funds in the series specify a CPI+ annualised return expectation, with varying levels and ranges of volatility (Defensive being the lowest and Adventurous the highest) defined on a rolling ten-year basis. The sixth fund in the series, the Income fund, seeks to provide a steady natural income of at least 4% per annum within the same volatility band as the Balanced fund. All are aimed at investors with at least a five-year time horizon. They are, essentially, actively managed fettered

products, made up of direct investments with some fund allocations. They invest primarily in equities, fixed income and cash. Property is permitted but not considered as a separate asset class; any exposure is accessed via REITS as part of the equity mandate. Alternatives are not used. Derivatives may be used for risk management purposes and to execute tactical asset allocation decisions.

Quantitative review Investment objective All analysis using Morningstar data to 28 February 2020

Fund information

Fund classification

Fund Launch Date Fund Manager Domicile Assets Approach Type

Universal MAP Defensive Fund 07 Oct 2019 Paul Niven GBR Active Risk Targeted OEIC

Universal MAP Cautious Fund 10 Nov 2017 Paul Niven GBR Active Risk Targeted OEIC

Universal MAP Balanced Fund 10 Nov 2017 Paul Niven GBR Active Risk Targeted OEIC

Universal MAP Growth Fund 10 Nov 2017 Paul Niven GBR Active Risk Targeted OEIC

Universal MAP Adventurous Fund 07 Oct 2019 Paul Niven GBR Active Risk Targeted OEIC

Universal MAP Income Fund 07 Oct 2019 Paul Niven GBR Active Risk Targeted OEIC

Fund IA Sector Morningstar Category* Defaqto Diamond Rating Type

Diamond Rating

Universal MAP Defensive Fund Volatility Managed Moderately Cautious Allocation Not Rated NA

Universal MAP Cautious Fund Volatility Managed Moderate Allocation Not Rated NA

Universal MAP Balanced Fund Volatility Managed Moderate Allocation Not Rated NA

Universal MAP Growth Fund Volatility Managed Moderately Adventurous Allocation Not Rated NA

Universal MAP Adventurous Fund Volatility Managed Adventurous Allocation Not Rated NA

Universal MAP Income Fund Mixed Assets Moderate Allocation Not Rated

*Note: The Morningstar Category is used in all comparative analysis, over the following pages.

6

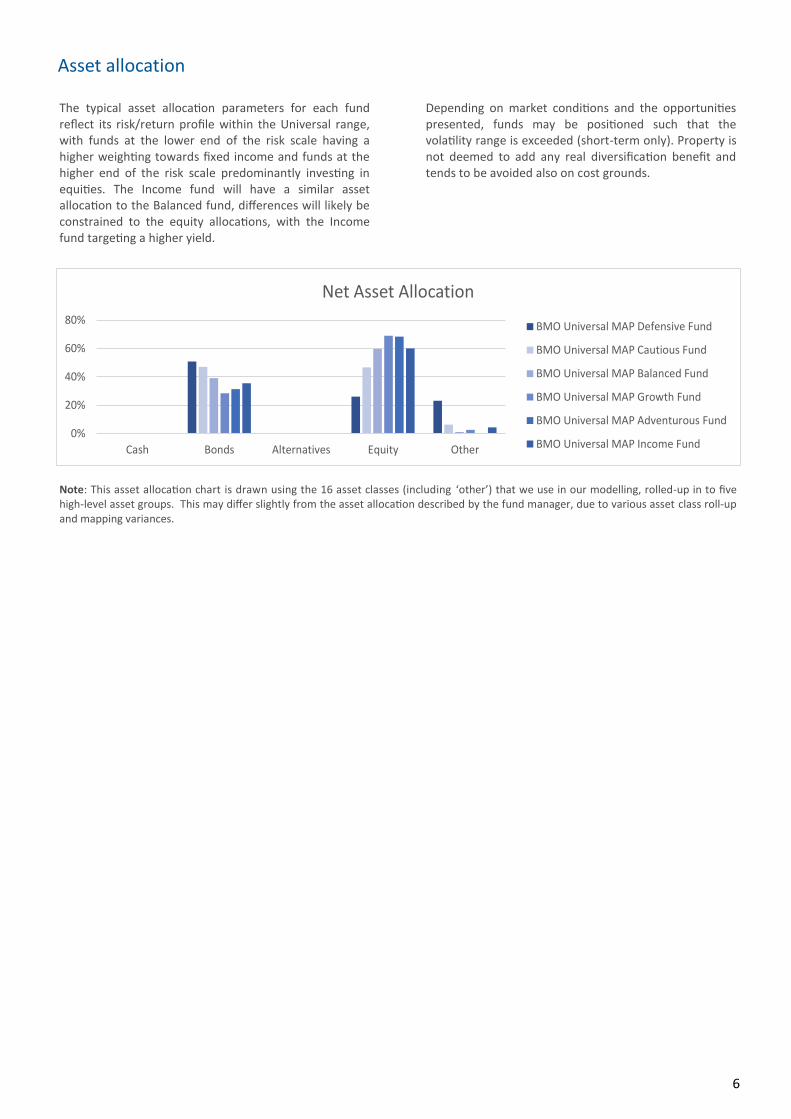

The typical asset allocation parameters for each fund reflect its risk/return profile within the Universal range, with funds at the lower end of the risk scale having a higher weighting towards fixed income and funds at the higher end of the risk scale predominantly investing in equities. The Income fund will have a similar asset allocation to the Balanced fund, differences will likely be constrained to the equity allocations, with the Income fund targeting a higher yield.

Depending on market conditions and the opportunities presented, funds may be positioned such that the volatility range is exceeded (short-term only). Property is not deemed to add any real diversification benefit and tends to be avoided also on cost grounds.

Asset allocation

Note: This asset allocation chart is drawn using the 16 asset classes (including ‘other’) that we use in our modelling, rolled-up in to five high-level asset groups. This may differ slightly from the asset allocation described by the fund manager, due to various asset class roll-up and mapping variances.

0%

20%

40%

60%

80%

Cash Bonds Alternatives Equity Other

Net Asset Allocation

BMO Universal MAP Defensive Fund

BMO Universal MAP Cautious Fund

BMO Universal MAP Balanced Fund

BMO Universal MAP Growth Fund

BMO Universal MAP Adventurous Fund

BMO Universal MAP Income Fund

7

The initial three funds (Cautious, Balanced and Growth) were launched in November 2017. Over the last year, leading up to February 2020, returns were as might be expected with the Growth fund having the highest volatility but also the highest return. Towards the end of February 2020, concerns about the coronavirus had a large negative impact across all equity markets. As a result, the Growth fund, which has a higher weighting to equities, suffered a larger drawdown.

However, it is worth highlighting that all 3 funds proved much more resilient than their category averages in 2018 and continued to outperform on the upside in 2019. As a result, since inception, all 3 funds are comfortably ahead of their category averages.

The remaining three funds (Defensive, Adventurous and Income) launched in October 2019. As such, we do not have enough performance data for these funds.

Interestingly, even considering the market turbulence of Q4 2018, the Growth fund fared better than the Cautious fund overall. This may reflect a stronger start to the year, which acted as a cushion for the impending market volatility.

In 2019, a bullish year, returns were as expected with the Growth fund outperforming due to its higher equity allocation. Consequently, the higher equity allocation has hindered performance during 2020 so far, as the equity markets were impacted by concerns of the coronavirus.

Performance - total returns

Performance - discrete returns

0%

2%

4%

6%

8%

10%

12%

14%

28/02/2019 29/02/2020

1 Year Total Return

BMO Universal MAPCautious Fund 1Yr TR

BMO Universal MAPBalanced Fund 1Yr TR

BMO Universal MAPGrowth Fund 1Yr TR

-10%

-5%

0%

5%

10%

15%

20%

Year 2016 Year 2017 Year 2018 Year 2019 Year 2020 todate

Discrete Returns

BMO Universal MAP Cautious Fund TR

BMO Universal MAP Balanced Fund TR

BMO Universal MAP Growth Fund TR

8

Given the large negative impact on equity markets, due to concerns around the coronavirus, it is not surprising that the Growth fund has been the worst affected. However, since the funds’ inception the return profiles are as expected with Cautious offering a slightly lower, more defensive return and Growth offering a slightly higher, but more volatile return.

However, it is worth highlighting that even given the recent increased volatilities, all 3 funds remain below their volatility targets.

As previously mentioned, we do not currently have enough performance data for the three newer funds. However, it is expected that Defensive will become the lowest volatility fund of the range, Adventurous will become the highest and the Income fund will have a similar volatility profile to the Balanced fund.

For the three older funds, positive months have exceeded negative months.

As expected, drawdowns have been sharper and more pronounced in the riskier fund.

Risk

Drawdown

Last 12 Months Max Drawdown Positive Months Negative Months Worst Month

Universal MAP Defensive Fund NA NA NA NA

Universal MAP Cautious Fund -5.3% 9 3 -3.5%

Universal MAP Balanced Fund -7.0% 8 4 -4.7%

Universal MAP Growth Fund -8.2% 7 5 -5.7%

Universal MAP Adventurous Fund NA NA NA NA

Universal MAP Income Fund NA NA NA NA

BMO Universal MAP Cautious Fund

BMO Universal MAP Balanced Fund

BMO Universal MAP Growth Fund

2%

3%

4%

5%

6%

5% 6% 7% 8% 9%

An

nu

alis

ed R

etu

rn

Annualised Volatility

1 Year Risk & Return

9

The original funds in the range have had recent strong inflows. The remaining funds are very new and therefore are below the threshold that Defaqto finds comfortable (£50m) for its Diamond Ratings. However, we believe that the group is fully committed to the product suite, as it deems that it fills a market gap i.e. offering actively managed portfolios at a passive cost.

The OCF is capped at 0.29%. This is achievable because, in fund selection, the product is fettered (i.e. confined to using in-house BMO products, with pricing much more

attractive than external fund vehicles). The managers may use ETFs and index trackers (when they deem it appropriate) to implement the desired asset allocation exposure. The fund is predominantly direct investments and clearly there will be transaction costs associated with buy/sell decisions.

Transaction expenses are currently higher than usual given the recent period of increased market volatilities and this figure is expected to fall over time.

Fund size and fees

Fund AUM OCF Estimated

OCF Actual Transaction Fee Actual

Performance Fee (Yes/No)

Performance Fee Actual

Universal MAP Defensive Fund £12.3M* 0.29% 0.29% NA No NA

Universal MAP Cautious Fund £122.1M* 0.29% 0.29% 0.30% No NA

Universal MAP Balanced Fund £181.5M* 0.29% 0.29% 0.35% No NA

Universal MAP Growth Fund £109.8M* 0.29% 0.28% 0.39% No NA

Universal MAP Adventurous Fund £8.4M* 0.29% 0.29% NA No NA

Universal MAP Income Fund £3.3M* 0.29% 0.29% NA No NA

*Source: BMO February 2020

10

The philosophy behind the Universal MAP product range is to provide investors with an actively managed, risk targeted suite of funds, with a graduated volatility risk profile to suit varying risk tolerances. The key point is that this active management should be available at a low cost i.e. comparable with passive vehicles. The investment horizon is long-term (a minimum of five years), and the volatility bands also applicable on a long-term rolling basis.

The team believes (and intends) that asset allocation should be the main driver of returns, and so strategic and tactical asset allocation is actively managed, without overt geographical, industry or sector constraints, except those deemed necessary by the managers to meet the portfolio’s target volatility bands. The managers may deviate from the volatility range (short-term) if market conditions, in their view, justify doing so. Asset allocation is emphatically not outsourced or decided with reference to externally sourced allocations, but derived from internal qualitative and quantitative analysis. The allocation output derived from the quantitative models can be

overridden by the fund manager and team. That said, the team is willing to ride out short-term market fluctuations as their stance is determined by longer-term considerations, with valuation metrics key.

Manager selection is made from the wide BMO specialist investment capabilities. If no appropriate active options are available, or no specific in-house expertise available, then the managers will use ETFs and trackers. However, the team characterises this as “not a dominant force” in the product. Nevertheless, the team looks for “best of breed” and spends time both analysing performance and monitoring style factors.

Direct investment ideas are typically drawn from underlying BMO fund managers and will be assessed individually for their contribution to the risk and return profile of the portfolio.

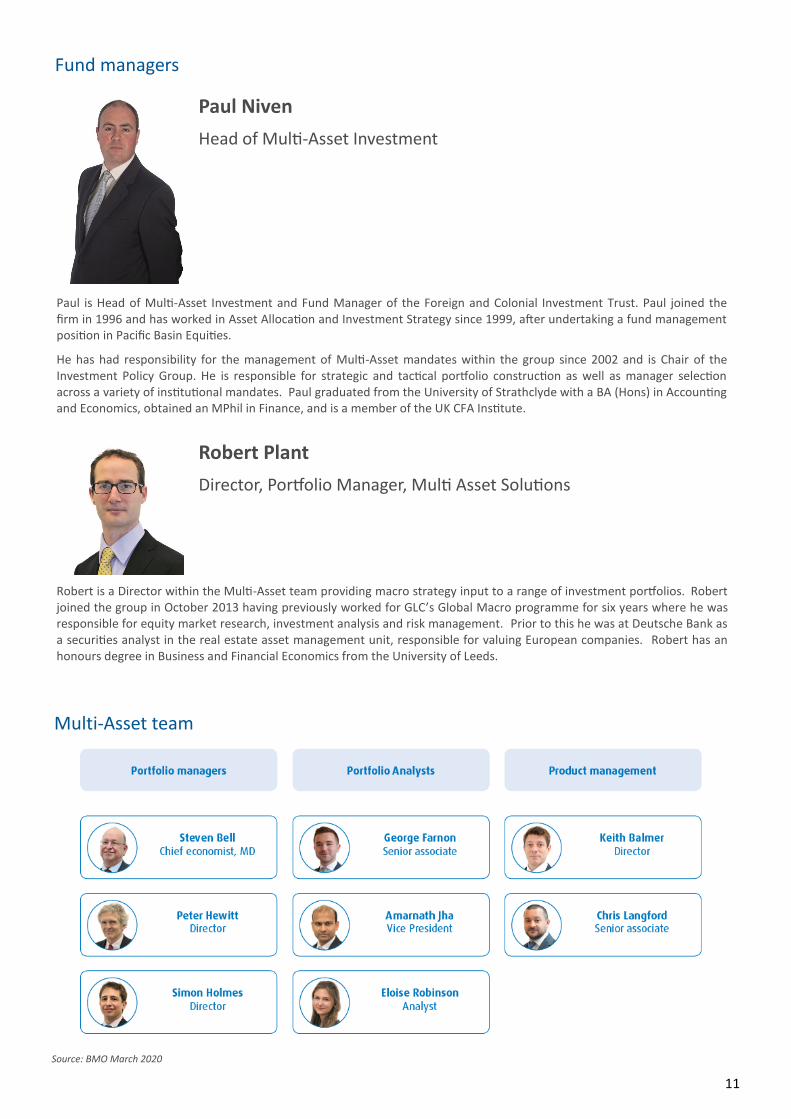

The 28-strong multi-asset team responsible for the Universal Fund range is led by Paul Niven. Niven joined BMO in 1996 and has specialised in asset allocation and investment strategy since 1999; he has been responsible for multi-asset mandates since 2002, and chairs the internal Investment Policy Group. He has over 24 years’ experience in the investment industry.

Niven is named manager on the Universal suite of funds; the team acts in a collaborative and collegial environment, but his is the final decision-making power. Team member Robert Plant is also a named manager on this fund. Plant joined BMO in 2013; his prior experience included 6 years on GLC‘s macro programme and a spell as a real estate analyst at Deutsche Bank. He has over 13 years’ experience.

The team is split between London (ten investment professionals), Chicago (six) and Toronto (twelve); its

geographical spread informs its macro economic analysis, and also facilitates contact with BMO specialist fund managers worldwide; the team emphasises that it makes use of BMO’s worldwide expertise. Overall, team members average 21 years’ experience in the financial industry. Recent recruits include a quants analyst (tasked with improving modelling reliability, a key function given the role of quantitative analysis in strategic asset allocation).

It should be noted that this team, in terms of philosophy and personnel, is quite distinct and separate from the multi-manager team led by Rob Burdett and Gary Potter, who run the well-known BMO Lifestyle and Navigator multi-manager product suites.

Qualitative review Defaqto met the BMO fund management team at their office in London in January 2019, October 2019 and February 2020, where much of the information for this review was obtained.

Philosophy

People

11

Source: BMO March 2020

Paul Niven

Head of Multi-Asset Investment

Paul is Head of Multi-Asset Investment and Fund Manager of the Foreign and Colonial Investment Trust. Paul joined the firm in 1996 and has worked in Asset Allocation and Investment Strategy since 1999, after undertaking a fund management position in Pacific Basin Equities.

He has had responsibility for the management of Multi-Asset mandates within the group since 2002 and is Chair of the Investment Policy Group. He is responsible for strategic and tactical portfolio construction as well as manager selection across a variety of institutional mandates. Paul graduated from the University of Strathclyde with a BA (Hons) in Accounting and Economics, obtained an MPhil in Finance, and is a member of the UK CFA Institute.

Robert Plant

Director, Portfolio Manager, Multi Asset Solutions

Robert is a Director within the Multi-Asset team providing macro strategy input to a range of investment portfolios. Robert joined the group in October 2013 having previously worked for GLC’s Global Macro programme for six years where he was responsible for equity market research, investment analysis and risk management. Prior to this he was at Deutsche Bank as a securities analyst in the real estate asset management unit, responsible for valuing European companies. Robert has an honours degree in Business and Financial Economics from the University of Leeds.

Fund managers

Multi-Asset team

12

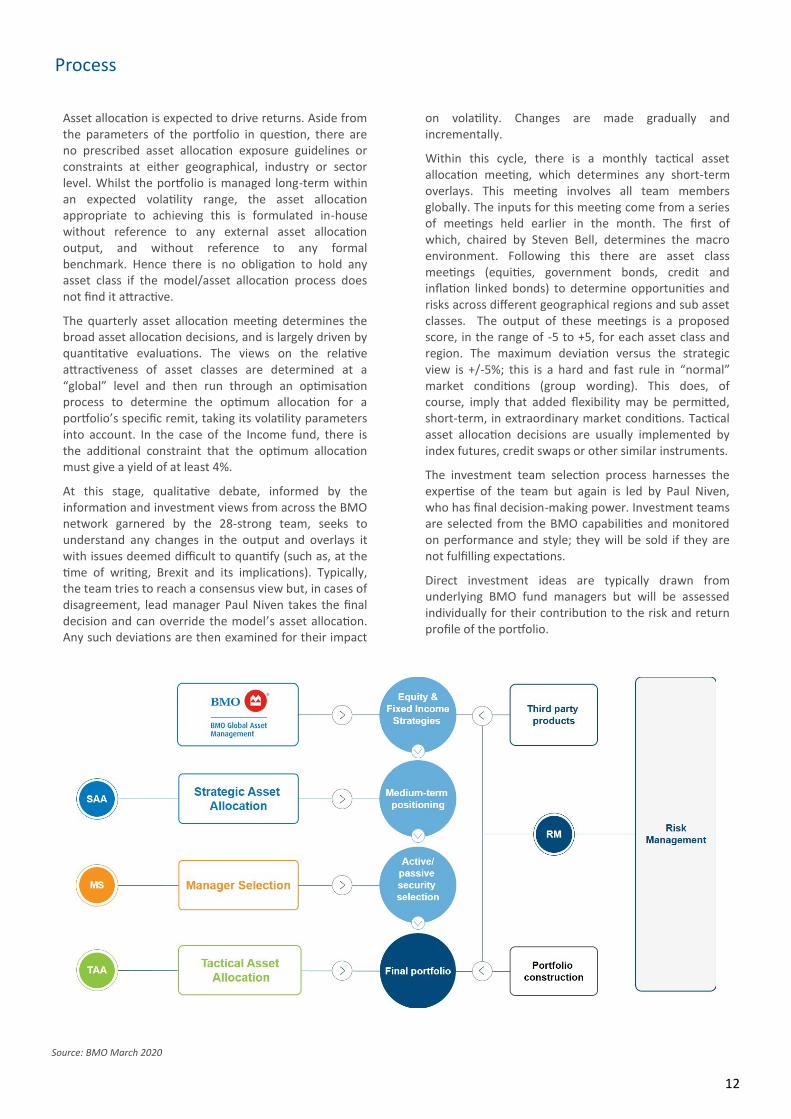

Asset allocation is expected to drive returns. Aside from the parameters of the portfolio in question, there are no prescribed asset allocation exposure guidelines or constraints at either geographical, industry or sector level. Whilst the portfolio is managed long-term within an expected volatility range, the asset allocation appropriate to achieving this is formulated in-house without reference to any external asset allocation output, and without reference to any formal benchmark. Hence there is no obligation to hold any asset class if the model/asset allocation process does not find it attractive.

The quarterly asset allocation meeting determines the broad asset allocation decisions, and is largely driven by quantitative evaluations. The views on the relative attractiveness of asset classes are determined at a “global” level and then run through an optimisation process to determine the optimum allocation for a portfolio’s specific remit, taking its volatility parameters into account. In the case of the Income fund, there is the additional constraint that the optimum allocation must give a yield of at least 4%.

At this stage, qualitative debate, informed by the information and investment views from across the BMO network garnered by the 28-strong team, seeks to understand any changes in the output and overlays it with issues deemed difficult to quantify (such as, at the time of writing, Brexit and its implications). Typically, the team tries to reach a consensus view but, in cases of disagreement, lead manager Paul Niven takes the final decision and can override the model’s asset allocation. Any such deviations are then examined for their impact

on volatility. Changes are made gradually and incrementally.

Within this cycle, there is a monthly tactical asset allocation meeting, which determines any short-term overlays. This meeting involves all team members globally. The inputs for this meeting come from a series of meetings held earlier in the month. The first of which, chaired by Steven Bell, determines the macro environment. Following this there are asset class meetings (equities, government bonds, credit and inflation linked bonds) to determine opportunities and risks across different geographical regions and sub asset classes. The output of these meetings is a proposed score, in the range of -5 to +5, for each asset class and region. The maximum deviation versus the strategic view is +/-5%; this is a hard and fast rule in “normal” market conditions (group wording). This does, of course, imply that added flexibility may be permitted, short-term, in extraordinary market conditions. Tactical asset allocation decisions are usually implemented by index futures, credit swaps or other similar instruments.

The investment team selection process harnesses the expertise of the team but again is led by Paul Niven, who has final decision-making power. Investment teams are selected from the BMO capabilities and monitored on performance and style; they will be sold if they are not fulfilling expectations.

Direct investment ideas are typically drawn from underlying BMO fund managers but will be assessed individually for their contribution to the risk and return profile of the portfolio.

Process

Source: BMO March 2020

13

Risk is managed at three levels.

The onus, in the first instance, is on the managers to monitor and analyse risk at both portfolio level and individual holding level. A weekly meeting looks at all the fund components, their performance and contribution not only to that performance but the risk profile, with an ongoing emphasis on ensuring there is no meaningful style drift.

At the next level, a number of risk systems monitor portfolios’ compliance with risk limits. VAR analysis, leverage and risk exposure analysis is also key. Aggregated exposures to asset classes and fund management groups are also monitored on an ongoing basis. Underlying exposures in asset classes (on a look through basis, with cash excluded) are also monitored. This function also provides performance attribution.

At the third level, there is the independent risk management team, headed by Richard Wintle. Wintle, who joined BMO in February 2018, has over 18 years’ experience in risk management, principally at Newton Investment Management (2000-2016). As far as we are aware, there is no crossover in personnel between the investment and risk teams. Additionally and importantly, his reporting line is outside the investment function. The principle remit of this team is to discuss and evaluate risk exposures, and to “advise and warn” of any potential issues. We are given to understand that they do not have veto power but, should there be a fundamental disagreement, the risk team escalates the issue up to senior BMO management and, ultimately, to the risk supervision at senior BMO level, where oversight lies with COO Joan Mohammed.

Risk management

14

Asset allocation is expected to drive returns.

The quarterly asset allocation meeting determines the broad asset allocation decisions, and is largely driven by quantitative evaluations. The team is aware that quantitative systems repose on historic data and in their case backward-looking rolling five-year historical volatilities and correlations; the aim is to be more forward-looking, prioritising a deeper and more frequent review of data points, and more forward-looking data. In the case of the return assumptions, expected fixed income returns equal current yields while expected equity returns equal the current dividend yield plus the forecast dividend growth rate, with the latter being linked to GDP growth.

There is no restriction on assets by geography, sector or industry, but alternatives and property are excluded. Bonds are sub-divided into distinct categories for analysis (government, corporate, global high yield and global corporate). There are limitations on exposures at a sub asset class and aggregate level built into the asset allocation model. The team is cognisant that historic data e.g. in emerging markets or high yield may not capture risk wholly or appropriately and hence their potential maximum exposure is limited versus the other asset classes. An optimisation process determines the optimum allocation within the specific confines of a portfolio’s remit and defined volatility parameters. The output is subject to qualitative examination, upon which changes to the model output may be amended. The

resulting portfolio is then tested to ensure that it fits within stated investment objectives. This involves Monte Carlo-style detailed simulations and modelling of risk and return distributions, the impact of risk and uncertainty, and probable outcomes.

The monthly tactical asset allocation meeting looks at markets in depth. Equity and fixed income markets are scored on a scale of –5 to +5 (relative to the strategic allocation) within a framework of Economic, Policy, Valuation and Behavioural factors. After debate, if the variation is agreed, tactical tilts of up to +/-5% will be implemented, typically using equity index and bond futures.

Fund selection essentially focuses on finding the “best of breed” within the BMO range. Given that these funds are internal, data transparency should render analysis relatively straightforward. The team needs to understand individual managers’ approaches and styles, as they may vary materially.

As regards direct investments, the multi-asset team does not analyse these bottom-up, but relies on specialist investment teams to select individual companies using their own security selection processes. The multi-asset team’s focus is on how the overall investment impacts the risk/return profile of the fund, and whether it leads to any unexplained or unintended incremental risk biases.

Research process

The team has considerable resources available to it, in terms of personnel (the wider BMO teams) and also in terms of internally developed systems (in addition to

the standard portfolio and fund selection tools).

Resources available

15

Defaqto Family Diamond Rating A quality rating based upon a range of key attributes, including performance, consistency, risk spread, cost, size, and manager tenure, across the family.

Defaqto Risk Rating A suitability rating that applies to each solution within the family, which have been mapped and aligned to the ten Defaqto Risk Profiles.

Defaqto Income Risk Rating A suitability rating that applies to each solution within the family, which have been mapped and aligned to the four Defaqto Income Risk Profiles.

Launch Date The launch date for the share class being reviewed.

Assets Refers to the asset types that the fund managers uses, being either ‘active’ or ‘passive’.

Approach Refers to the management focus adopted by the manager.

Investment Association (IA) sector The Investment Association peer group that the fund/s are classified within. See www.investmentassociation.org for details.

Morningstar Category Funds are grouped into categories according to their actual investment style, not merely their stated investment objectives, nor their ability to generate a certain level of income. To ensure homogeneous groupings, Morningstar normally allocates funds to categories on the basis of their portfolio holdings. Several portfolios are taken into account to ensure that the fund´s real investment stance is taken into account. Source: Morningstar Inc.

Defaqto Diamond Rating Type Created by Defaqto to determine the Defaqto Diamond Ratings.

Defaqto Diamond Rating A suitability rating based upon a range of key attributes, including performance, cost, size, and manager tenure for each solution in the family.

Asset allocation chart Created using Defaqto’s 16 asset classes including ‘other’. The 16 asset classes have then been ‘rolled-up’ in to five high-level asset categories.

Total returns chart Displays the percentage return, over the specified period, comparing the solutions within the family, with gross income reinvested.

Discrete returns chart Based on 5 discrete 12 month periods (if available), working backwards from the stated month-end. Displays the percentage return, comparing the solutions within the family, with gross income reinvested.

Risk-return chart Displays the annualised standard deviation of daily log returns and the annualised percentage returns, of the solutions within the family.

Drawdown and positive/negative months table

Displays the maximum peak to trough loss, within the period stated, using daily pricing data, together with the number of positive and negative months of performance, and the percentage fall in value in the worst month, for the solutions within the family.

Fund size and fees Displays assets under management (AUM), for the solutions within the family, together with a range of MIFID II compliant fees. It should be noted that, for technical reasons, negative transaction fees can occur. Its also possible that negative performance fees can be displayed and these represent fee rebates.

Historic income chart If displayed, shows the net distribution history declared by the solutions within the family, on a £ per unit basis.

Yield table If displayed, shows the current income yield, calculated on a trailing percentage basis, together with the distribution frequency, for the solutions within the family.

Glossary

Data source: Morningstar Inc. Please note that some solutions may have simulated/extended track records, in accordance with Morningstar’s Extended Performance Methodology paper.

Version 1.3 2019

16

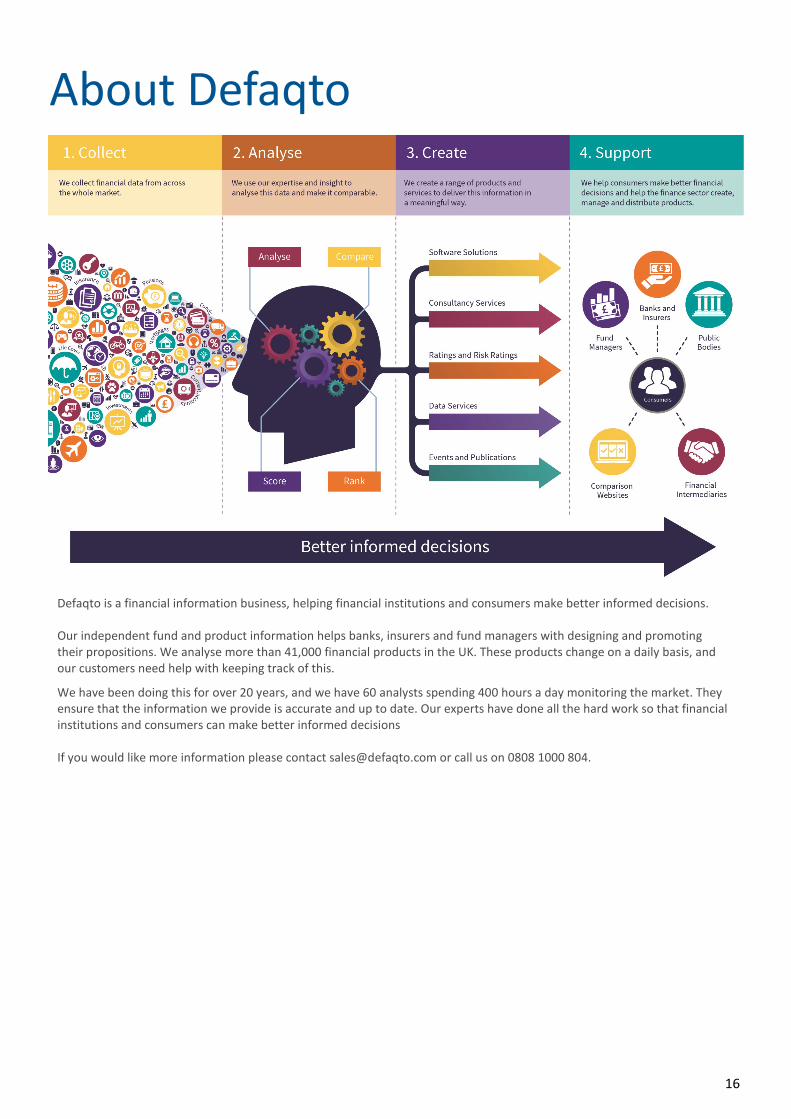

Defaqto is a financial information business, helping financial institutions and consumers make better informed decisions. Our independent fund and product information helps banks, insurers and fund managers with designing and promoting their propositions. We analyse more than 41,000 financial products in the UK. These products change on a daily basis, and our customers need help with keeping track of this.

We have been doing this for over 20 years, and we have 60 analysts spending 400 hours a day monitoring the market. They ensure that the information we provide is accurate and up to date. Our experts have done all the hard work so that financial institutions and consumers can make better informed decisions If you would like more information please contact [email protected] or call us on 0808 1000 804.

About Defaqto

17

Please contact your Defaqto Account Manager or call us on 0808 1000 804

defaqto.com/advisers