minosity - maxlumans.com

TRANSCRIPT

MINOSITY

Luminosity Solutions Private Ltd.

LED Lights and Lighting Automation System

Company Name/firm Name Luminosity Solutions Pvt Ltd

Entity type

(Public Ltd/Private Ltd/Joint Venture/Sole Proprietorship)

Private Limited Company , Registered in Year 2015

Brand name LUMINOSITY LIGHTS

Websites(Group Company/Brand) www.Maxlumans.com

Industry Manufacturing – LED Lights And ancillary products

Authorized signatory/Designation/Contact Details Mr. Manoj Kumar - Director – 9899076648.

Top Management

(Key persons/Designations/Contact Details)

Mr. Manoj Kumar - Director – 9899076648.

Registered Address 101-A, Shiv Kutir, 2nd Floor, Hari Nagar, Ashram, New Delhi-110014

Principle place of business UPSIDC Industrial Area Salempur Hathras UP 204212

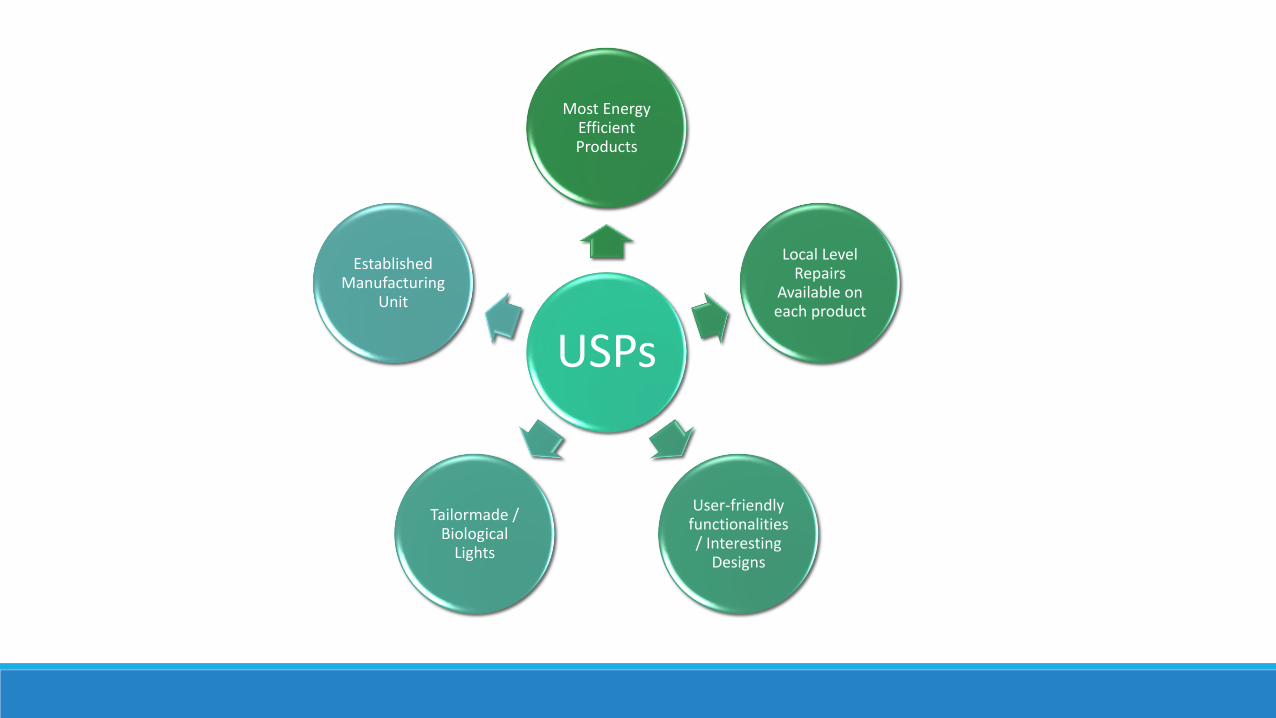

USPs

Most Energy Efficient Products

Local Level Repairs

Available on each product

User-friendly functionalities / Interesting

Designs

Tailormade / Biological

Lights

Established Manufacturing

Unit

Luminosity Solutions Pvt Ltd was established in 2015 with a vision to develop and provide high efficiency LED luminaries at most competitive prices.

Luminosity offers products for Indore Lighting/Outdoor Lighting/Decorative Lighting /Antique LightingFixtures and UVGI fixtures .Lighting and Control automation modules.

Luminosity offers maximum lumens per watt to save more energy aiming to offer more per watt by using less energy.

Luminosity offers wide of products Bulb/Tube lights/Downlighters/Panel lights/Flood lights/Street Lights/Solar Street Lights/Linear Lights/Highway Lights/Canopy Lights/Table lamps/Large Floor Lamps Chandeliers/Underwater Lights/Garden Lights/Gate Lights/Bollards/Well glass/Up-down Lights/Bulk Head /Post top Lanterns/Street Light Poles/Feeder Pillars/Junction Boxes/AC and DC Bulbs/Emergency Bulbs/Hanging Lights

MSME , Startup Unit with GOI. ISO 9001:2014 Unit

About US

CAPABILITIES AND PRODUCT DEVELOPMENT FACILITIES

DESIGN AND DEVELOPMENT DEPARTMENT

Experienced inhouse team and facility for design and development of products are equipped with latest technological advanced software’s and other tools for estimating the impact of various electro-mechanical/optical parameters to deliver products for longer use with less breakdowns,

Team using CAD/CAM technology and other helpful software’s .

PRINTED CIRCUIT BOARD MANUFACTURING UNIT:

• Inhouse design of PCB for faster development using latest software’s for schematic capture/Gerber editing or prototype development to match the latest industrial protocols and specification for personnel safety and environmental support.

• Full Turnkey capability in schematic design.

• CCL /CEM1-3/FR1-4 laminates with process capacity for 0.8 mm to 3.2 mm

• Metal Base PCB – Aluminium (1100, 3003, 5052, 6061).

• CNC Drilling/CNC routing machines offering best products with best finishing,

• In House quality control schedule for better products delivery gives confidence to customers for repetitive orders,

• Development of pcb length upto 1200 mm

• Latest technological equipment’s, plant and machinery for delivering quality products on time

• Our range of delivered products are being used extensively for LED lighting industry, Process control, switching devices circuits, AC/DC circuits, industrial applications as various R&D establishments.

• Many pre designed circuits boards, mounted or bare are available for SKD form of use .

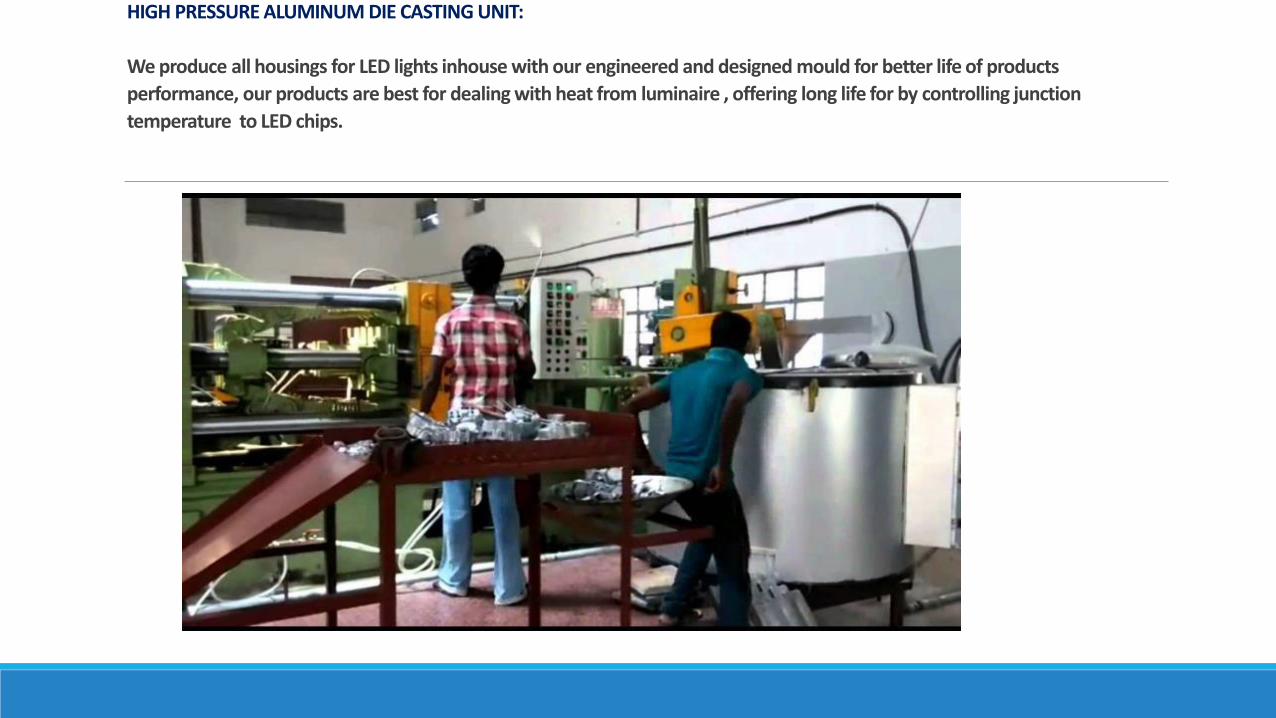

HIGH PRESSURE ALUMINUM DIE CASTING UNIT:

We produce all housings for LED lights inhouse with our engineered and designed mould for better life of products

performance, our products are best for dealing with heat from luminaire , offering long life for by controlling junction

temperature to LED chips.

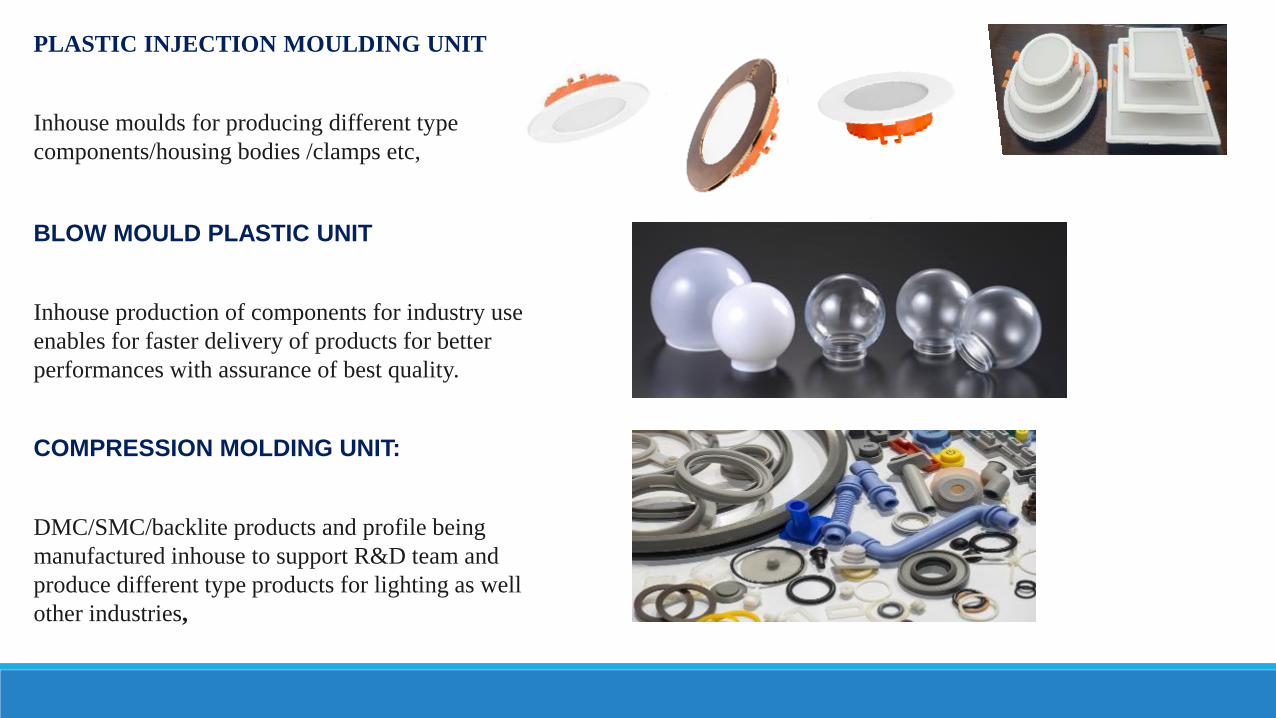

PLASTIC INJECTION MOULDING UNIT

Inhouse moulds for producing different type

components/housing bodies /clamps etc,

BLOW MOULD PLASTIC UNIT

Inhouse production of components for industry use

enables for faster delivery of products for better

performances with assurance of best quality.

COMPRESSION MOLDING UNIT:

DMC/SMC/backlite products and profile being

manufactured inhouse to support R&D team and

produce different type products for lighting as well

other industries,

SPINNING MACHINE UNIT:

Inhouse facility to produce light sheet metal gauge

housing/shapes for decorative lighting or bases of

light fixtures.

Any tailormade shape or design in round or cone or

other design proto can be produce within minimum

time and after design approvals mass production of

same will be offered to OEMs.

FABRICATION SHOP

Equipped with CNC machines for shearing/bending/punching /power presses machines for sheet metal fabrication of MS/SS/Aluminium cabinets and structures,

SURFACE TREATMENT SHOP

9 tank surface treatment plant for Ferrous metal treatment and 4 tank facility for non Ferrous metal products

PAINT SHOP

Semi-automated plant with conveyor belt /oven/2 paint booth system offers quality products for longer use within scheduled time .

Products: General Lighting

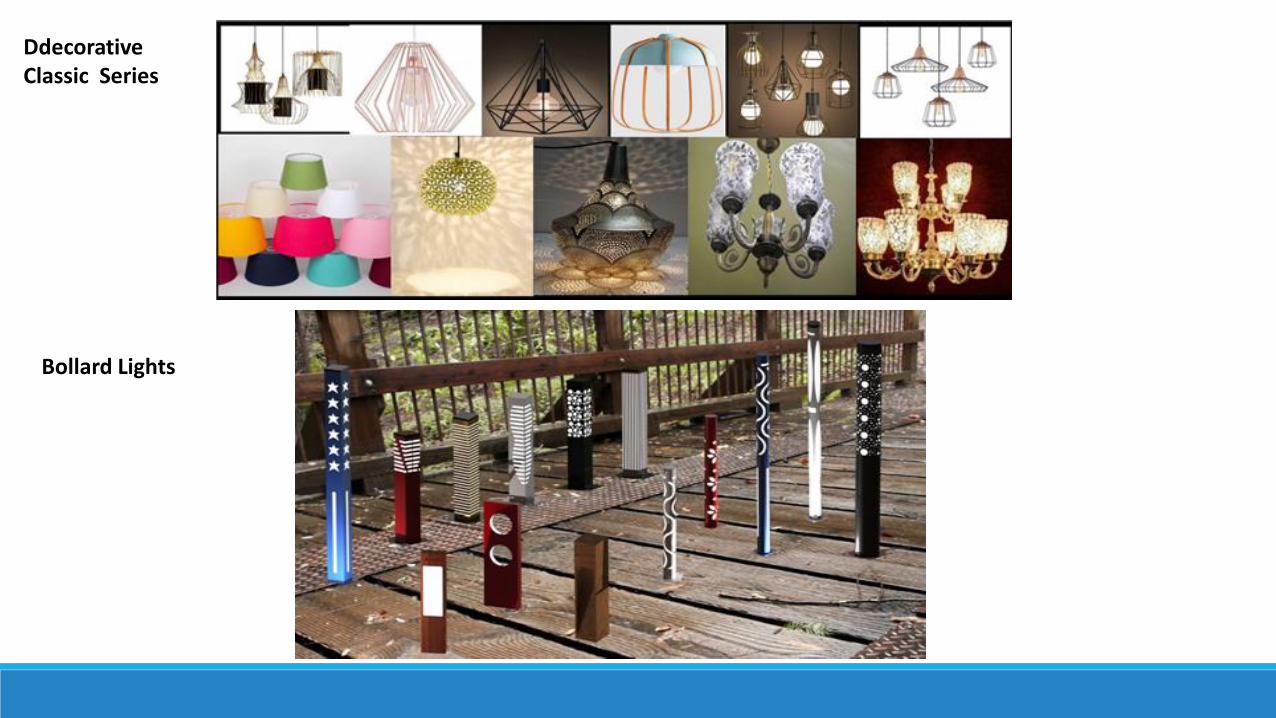

Ddecorative Innovative Series

Ddecorative Classic Series

Bollard Lights

JHOOMERSAntique , Brass Metal Hand make Series

Hanging Series Antique , Brass Metal Hand make Series

UVGI Lighting Fixtures best fit for use in Hospitals/Homes/offices for disinfection of SURFACES,AIR AND WATER

UVGI Lighting Fixtures For disinfection of Daily use cabinets, Large area movable UVC lights

Domestic and Global LED Lighting Market

Application

Indoor

Residential

Commercial

Industrial

Government

Outdoor

Architectural

Public Places

Highway and

Roadway

Product Type

Lamps

Luminaires

Distribution Channel

Direct Sales

Wholesale/Retail

Geography

Products applications and Business plan for different users

Government BidsBiological Lights

International

North America

Europe

Asia Pacific

Latin America

Domestic

North India

South India

East & North-

East

Mumbai Suburbs

& Western India

Middle East &

Africa

BUSINESS MODEL RECOMMENDATION TO APPOINT FRENCHISE , INVESTMENT

Tire-1 Cities: 100 lacs to 200 lacs

Tire-2 Cities: 50 lacs to 100 lacs

Tire-3 Cities: 20 lacs to 30 lacs

Return on Investment

LSPL will support by adding dealer distributor network to C&F for supply and services of products being sold to market, LSPL manage to share 7% profit on sale of products against investment made with us, 5 years lockout period for business with our products.

LSPL will support partner for 3 months with sales and marketing staff , after 3 months partner can retain same staff or can hire as per their business schedule , we can transfer this staff to their service on their payroll, LSPL will share 50% of staff cost of marketing for 1st 3 months, 90% amount stock will be stocked by partner , invoices shall be raised by partner, payment shall be transferred to LSPL.

LSPL will summaries business and share profit on quarterly basis,

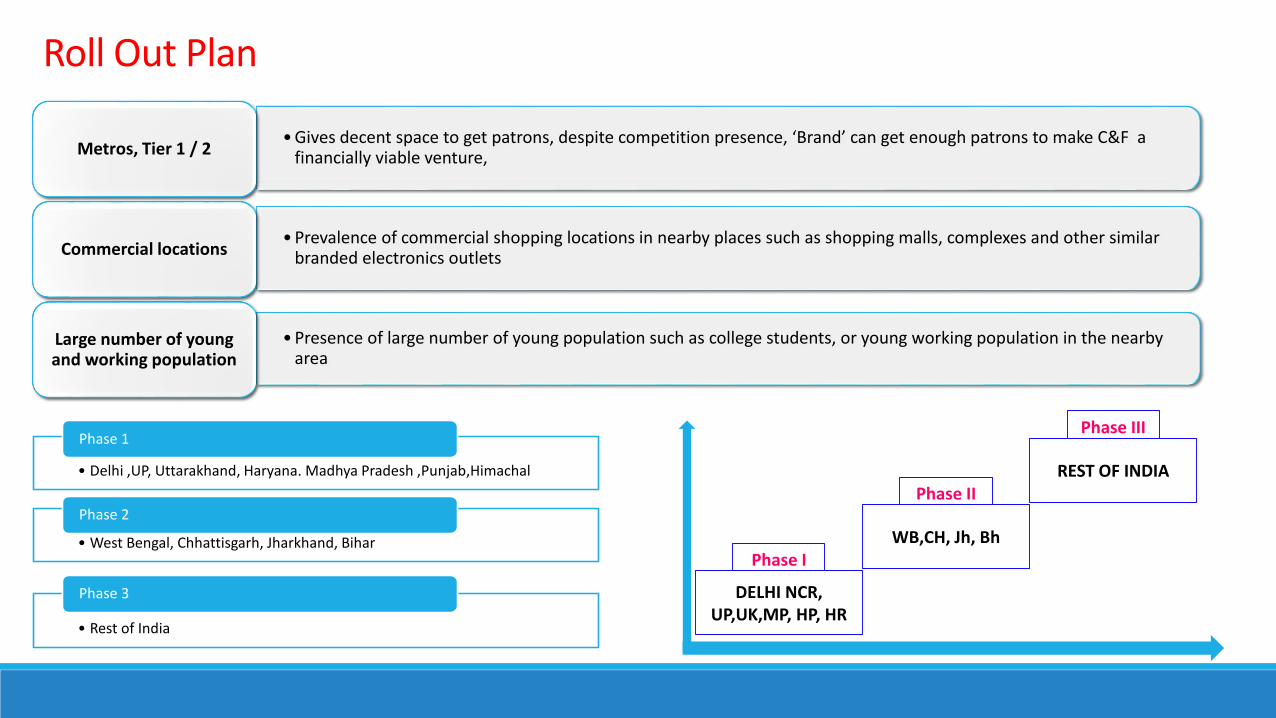

• Gives decent space to get patrons, despite competition presence, ‘Brand’ can get enough patrons to make C&F a financially viable venture, Metros, Tier 1 / 2

• Prevalence of commercial shopping locations in nearby places such as shopping malls, complexes and other similar branded electronics outletsCommercial locations

• Presence of large number of young population such as college students, or young working population in the nearby area

Large number of young and working population

• Delhi ,UP, Uttarakhand, Haryana. Madhya Pradesh ,Punjab,Himachal

Phase 1

• West Bengal, Chhattisgarh, Jharkhand, Bihar

Phase 2

• Rest of India

Phase 3 DELHI NCR, UP,UK,MP, HP, HR

WB,CH, Jh, Bh

REST OF INDIA

Phase I

Phase II

Phase III

Roll Out Plan

Roll out Plan with Timelines• Initiation with signing Letter of Intent followed with Agreement within 2 weeks with 20% payment of the Total

Project CostT -- ZERO

• Putting up the hoardings for the chosen location along with store finalizationT -- FOURTEEN

• Initiation of Hiring of Manpower and getting Leaflets, Flyer printed, etc to initiate the marketing campaignsT – FOURTEEN

• Finalizing the Interior as per the pre defined theme of the brand and other fit outs for the storeT -- TWENTY ONE

• Sharing Performa Invoice for the final payment with 2 weeks time for Stock movement from factory T – THIRTY

• Inauguration by Local Key Person along with Local Media Coverage for Grand InauguralT -- FORTY TWO

• LED lights are up to 80% more efficient than traditional lighting, such

as fluorescent and incandescent lights. 30% of the energy in LEDs is

converted into light and only 70% is wasted as heat, which is leading

consumers to opt for a more efficient form of lighting.

• By transitioning to energy-efficient LEDs, an estimated savings of

USD 18 billion in electricity costs can be achieved. Further, more

than 160 million tons of carbon dioxide emission can be avoided

every year.

• A wide variety of energy-saving LED bulbs in every shape and light

output level can already be found on the shelves of leading retailers

across the world. These bulbs are from well-known lighting

companies, such as Philips, GE, and Sylvania, as well as newer

companies that specialize in efficient lighting techniques, such as

Cree, TCP, Feit, and Maxlite.

• In the United States, all electrically controlled devices, including LED

light bulbs must meet minimum safety standards. The regulations

regarding these safety standards are covered in the United States by

laws, such as the Occupational Safety and Health Act (OSHA), Code

of Federal Regulations (CFR), and standards, such as the National

Electric Code (NEC).

MARKET OVERVIEW

Energy efficiency - LED lights use about 50% less electricity than traditional

incandescent, fluorescent, and halogen options, resulting in substantial

energy cost savings, especially for spaces with lights that are on for extended

periods.

Extended life - Unlike incandescent lighting, LEDs do not burn out or fail, they

merely dim over time. Quality LEDs have an expected lifespan of 30,000–

50,000 hours or even longer, depending on the quality of the lamp or fixture.

Durability - Without filaments or glass enclosures, LEDs are breakage

resistant and largely immune to vibrations and other impacts.

Controllability - It can take more than a few dollars to make commercial

fluorescent lighting systems dimmable, but LEDs, as semiconductor devices,

are inherently compatible with controls. Some LEDs can even be dimmed to 10

% of light output while most fluorescent lights only reach about 30 percent of

full brightness.

No IR or UV Emissions - Less than 10% of the power used by

incandescent lamps is actually converted to visible light. The majority of the

power is converted into infrared (IR) or radiated heat. Excessive heat and

ultraviolet radiation (UV) presents a burn hazard to people and materials.

LEDs emit virtually no IR or UV.

Advantages of LED Lighting

LED Lighting Market: Revenue in INR billion, 2017-2023

Year

2017 2018 2019 2020 2021 2022 2023

Revenue (

in I

NR

bill

ion)

INDIAN SCENERIO

• In Indian Market, nearly 80% of the total population resides in urban areas,

which is expected to rise during the forecast period. It is estimated that by

the end of 2045, urban dwellers might increase by two billion globally. In this

scenario, it becomes essential for the nations to use energy more efficiently.

• Buildings are the among the largest consumers of electricity worldwide.

However, estimates put that 80% of the energy efficiency potential of the

buildings is not utilized. Delhi NCR, for instance, consumes 60% more

energy for public lighting than that of the Chandigarh.

• India LED lighting market stood at $ 918.70 million in 2016, and is projected

to grow at a CAGR of 24.66%, in value terms, during 2016-2022, to reach $

3,758.74 million by 2022, on account of increasing government initiatives to

boost LED adoption and growing awareness regarding lower power

consumption of LED lighting

• LEDs are very energy efficient and serve a more extended period making it

more cost effective for the use for indoor as well as outdoor lighting. Smart

lighting and color changing capabilities that can be controlled by mobile

devices have added to the demand in commercial spaces across the region.

Indoor Lighting Products

Outdoor Lighting Products

SEGMENTATION - BY APPLICATION

SEGMENTATION - BYAPPLICATION

LED Lighting Market: Revenue Share (%), by Application, 2017

Indoor Outdoor

Application 2017 2018 2019 2020 2021 2022 2023 CAGR (%)

Indoor 85.00 82.00 78.00 74.00 70.00 70.00 70.00 21.66%

Outdoor 15.00 18.00 22.00 26.00 30.00 30.00 30.00 11.24%

Global LED Lighting Market : Revenue in INR billion, by Application, Global, 2017-2023

• Commercial

• Industrial

• Decorative

INDOOR LED LIGHTING PRODUCTS

• Residential

SEGMENTATION - BYAPPLICATION

Indoor 2017 2018 2019 2020 2021 2022 2023 CAGR (%)

Residential 20.00 22.00 24.00 26.00 27.00 27.00 27.00 28.00%

Commercial 29.00 28.00 28.00 27.00 26.00 26.00 26.00 22.00%

Industrial 26.00 26.00 26.00 25.00 25.00 25.00 25.00 26.00%

Decorative 25.00 24.00 22.00 22.00 22.00 22.00 22.00 24.00%

Global LED Lighting Market : Revenue in INR billion, by Application, Indoor, Global, 2017- 2023

Global LED Lighting Market: Revenue Share (%), by Application, 2017

Residential

Commercial

Industrial

Decorative

• Cree Inc.

• Dialight PLC

• Eaton Corporation

• General Electric Company

• OSRAM GmbH

• Samsung Group

• Sharp Corporation

• Signify Holding (Philips Lighting)

• Virtual Extension

• Zumtobel Group AG

COMPETITIVE INTELLIGENCE

(LIST NOT EXHAUSTIVE)

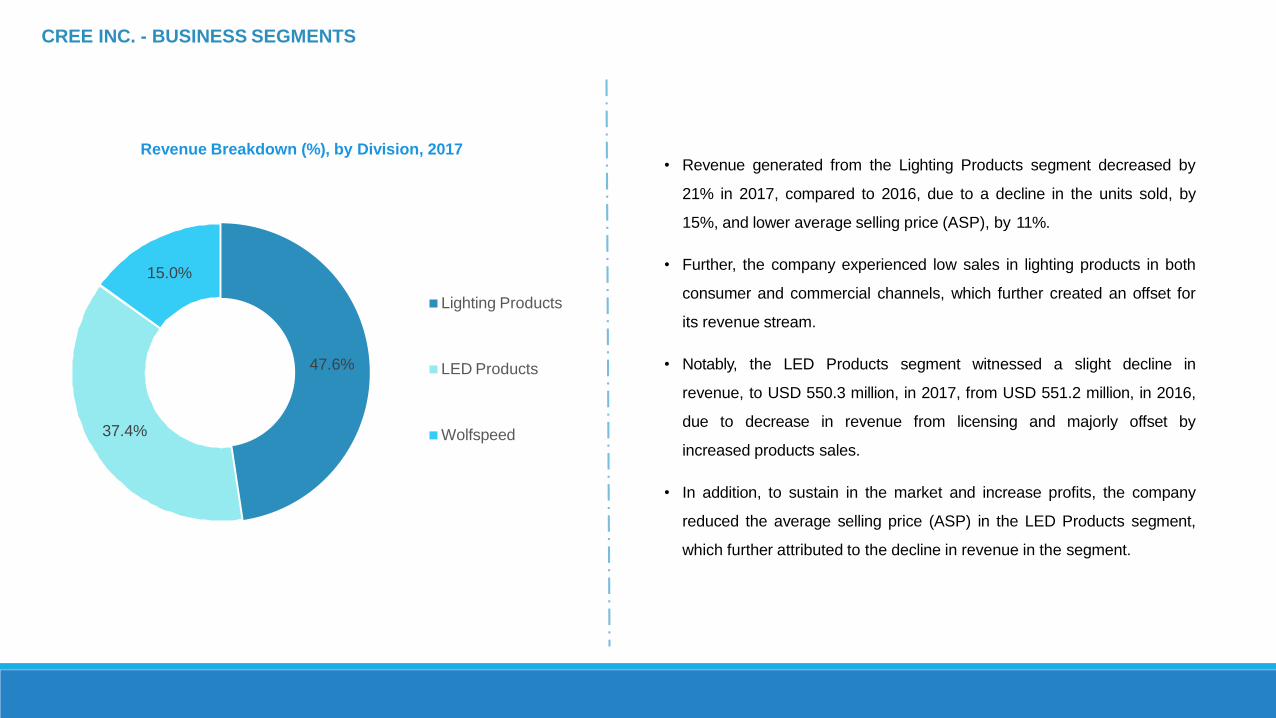

Revenue Breakdown (%), by Division, 2017

47.6%

37.4%

15.0%

Lighting Products

LED Products

Wolfspeed

• Revenue generated from the Lighting Products segment decreased by

21% in 2017, compared to 2016, due to a decline in the units sold, by

15%, and lower average selling price (ASP), by 11%.

• Further, the company experienced low sales in lighting products in both

consumer and commercial channels, which further created an offset for

its revenue stream.

• Notably, the LED Products segment witnessed a slight decline in

revenue, to USD 550.3 million, in 2017, from USD 551.2 million, in 2016,

due to decrease in revenue from licensing and majorly offset by

increased products sales.

• In addition, to sustain in the market and increase profits, the company

reduced the average selling price (ASP) in the LED Products segment,

which further attributed to the decline in revenue in the segment.

CREE INC. - BUSINESS SEGMENTS

Products and Services Strategies

• Indoor Lighting

• C-Lite™ Downlight

• CR-T Series

• DDS Series

• Essentia® Series Downlights

• KR Series

• ESA Series

• ESA Series Surface Cylinder

• C-Lite™ Flat Panel Troffer

• ZR Series

• CR Series

• Outdoor Lighting

• OSQ Series High Output

• C-Lite™ LED Area

• OSQ™ Series

• Cree Edge™ High Output

• XSP Series

• XSP High Output Series

• The company is trying to garner higher market share through strategic

approaches, such as mergers and acquisitions, partnerships, and joint

ventures.

• For instance, in early 2017, the company formed a joint venture, Cree Venture

LED Company Ltd, with San’an Optoelectronics Co. Ltd, to offer mid- power

lighting class LEDs to cater to the extended markets of Europe, Japan, and

North and South America.

• The company focuses on ascending infrastructure, such as schools and

universities, manufacturing, healthcare, airports, retails, and parking structure,

to target its products, wherein the chances of customer acquisition is high.

• Notably, the company has strong focus on R&D, which helps it position itself in

the market. Although, the company’s R&D expenditure reduced significantly

since 2015, due to reduced revenue, it is narrowing its focus on emerging

technologies and their application, so as to tap potential customers.

CREE INC. - PRODUCTS AND STRATEGIES

M I E P

Merger and

Acquisition

Product

InnovationExpansion Partnership

Cree expanded its SmartCast intelligence platform, including various

capabilities, such as wireless enabling smart building solutions

catering to the rising demand from internet of things (IoT). This is

likely to boost its presence and foster the financial growth.

May 2018

IThe company launched KBL LED High-Bay Series, a solution for various

As a result, it isapplications, such as retail, civic, and industrial.

projected to attract new and existing customers.

Nov 2017

E

The company introduced new innovative ZR-RK LED Troffer Retrofit

Kit, with reduced installation time and enhanced efficiency, which is

expected to have a positive impact on its growth.

May 2017

CREE INC. - RECENT DEVELOPMENTS

I

Study Deliverables

Study Assumptions

Analysis Methodology

Research Phases

RESEARCH METHODOLOGY

FORECAST PERIOD COMPANIES ANALYZEDBASE YEAR

GEOGRAPHICAL SCOPE SEGMENTS COVERED

AIM AND OBJECTIVE OF THE STUDY

To gain a fundamental understanding of the global and regional market by analysing key market dynamics and profiling key vendors to structure the competitive

landscape

2018- 2023 2017 10

DRIVERS, RESTRAINTS, AND OPPORTUNITIES

PORTER’S FIVE FORCESANALYSIS

SEGMENT AND SUB-SEGMENTANALYSIS

KEY PLAYERS

COMPETITIVE LANDSCAPE

STUDY DELIVERABLES

SECONDARY

RESEARCH

DISCUSSION

GUIDE

PRIMARY

RESEARCH

ECONOMETRIC

MODELLING

EXPERT

VALIDATION

DATA

TRIANGULATION

REPORT

WRITING

• Company Annual Reports

• Journals

• Government Publications

• LED Light Vendors

• LED Lighting suppliers

and Distributors

• Industry Experts

• Consultants

• Subject-matter Experts

• In-house Experts

• Company Related Queries

• Market Related Queries

• Company Financials

• Forecasting Model

• Revalidation of Numbers derived from Secondary

through Primaries

• Combination of Top-down and Bottom-up

Approaches

Garnering Insights from Data

and Forecast, which are then

Compiled into One Report

RESEARCH PHASES

• Financial Journals

• Annual Reports

• Market Research Reports

• Industry Websites

• Industry-related Databases

• Thought Leader Briefings

Secondary Research

Primary Research2. Interview

Participants

1. Secondary Data

Analysis

3. Analyze and

Collate Different

Perspectives

Define Objective and Scope

Suppliers,

OEMs, Raw Material Suppliers, and

Customers’Perspective

Identify and Assess Top Companies

and their Best Practices

Outcome—Top performing Companies,

based on Revenue Generated

Overall Understanding of the Market,

Industry Trends, and Events

Research Methodology Research Process

• CEOs/CFOs

• Board Members

• Research Heads

• Strategic Decision-makers

• Financial Advisors

• Investors

Research Process

Industry Experts,

Consultants,

Managers,

Strategists, etc.

ANALYSIS METHODOLOGY

Weaknesses

• The company has been marketing and selling its products to

a relatively small array of consumers through targeted selling,

promotions, selected advertising, and attendance at trade

shows. However, the company needs to make significant

investments to expand its sales, marketing, and distribution

capabilities.

Strengths

• The company offers a wide range of products catering to several

markets across India. This helps it acquire more consumers, thereby

having a positive impact on the company’s growth.

• Luminosity invests significant resources in R&D activities. It operates

R&D facilities in Hathras, UP.

Threats

• As the company is a manufacturer of LED lighting solutions, it

is subject to strong competition in the market located in Delhi

NCR, and aspired markets. The industry is characterized by

rapid technological change, regular introduction of new

products, alterations in end-user and customer requirements,

and a competitive pricing environment.

SWOT ANALYSIS

Opportunities

• The launch of innovative and new products is expected to drive the

growth of the company and support it in enhancing its profitability.

The company constantly extends its market leadership in LED

lighting, with the launch of higher performance Lamp LEDs and

lighting products.

• Additionally, the increasing demand for energy efficient products

creates new avenue and generates an immense opportunity to

tap new and retain existing consumers.

PORTOR’S 5 FORCES

Supplier Power. This is determined by how easy it is for your suppliers to increase their prices. How many potential suppliers do you have? How unique is the

product or service that they provide, and how expensive would it be to switch from one supplier to another?

Low as most are inhouse supply parts or components

Competitive Rivalry. This looks at the number and strength of your competitors. How many rivals do you have? Who are they, and how does the quality of their

products and services compare with yours?

HIGH

Threat of New Entry. Your position can be affected by people's ability to enter your market. So, think about how easily this could be done. How easy is it to get

a foothold in your industry or market? How much would it cost, and how tightly is your sector regulated?

MODERATE

Threat of Substitution. This refers to the likelihood of your customers finding a different way of doing what you do. For example, if you supply a unique

software product that automates an important process, people may substitute it by doing the process manually or by outsourcing it. A substitution that is easy

and cheap to make can weaken your position and threaten your profitability.

LOW

Buyer Power. Here, you ask yourself how easy it is for buyers to drive your prices down. How many buyers are there, and how big are their orders? How much

would it cost them to switch from your products and services to those of a rival? Are your buyers strong enough to dictate terms to you?

HIGH

FRANCHISEE ENVIRONMENT

Why Franchising?

Operational Efficiency

Raise Capital

Risk mitigation

Management focus on core competencies

Deeper Penetration

Reasons why companies franchise?

Strategy Leadership R &D / New

Launches Roll out “On the job

roles” Marketing and

brand building

Enabler

FRANCHISEE

Operational focus

Strategic focus

Cu

sto

mer

m

anag

emen

t

Sto

re t

o s

tore

Leve

l bu

sin

ess

man

agem

ent

“In

th

e jo

b

Ro

le”

FRANCHISOR

Comparing Company Owned outlets with Franchise Owned

1. Pilot company owned stores are great for learning

and setting up benchmarks

2. One can handpick the staff, be very selective on

recruitment ; Incompetency can be replaced

3. 100% compliance on operations manual

4. Definitely, larger margins due to no middle men in

between

1. Own Investment – higher cost of capital

2. Linear Growth; limited roll out possible

3. Both the backend and front end lies on the company;large man power requirement

4. The onus of entire supply chain lies on the company

5. High Operational challenges for running a localdriven business

1. Franchise to invest – transfer the risk of investment to athird party

2. Exponential growth with multiple outlets

3. Company can Invest time on strategy development

4. With vested interest, the franchise will be self motivated;therefore brings in 7 -10% efficiency in the overall storeperformance

5. Lesser operational challenges due to local knowledge

1. One cannot replace incompetent franchise; has tocontinue through the term of contract

2. Franchisor – Franchise relationship critical

3. Performance of one outlet can hamper image of theentire chain

Company Owned outlets Franchisee Outlets

Market opportunity exists but needs to control critical points

The consumer is not particularly keen on travelling out too far

Location strategy should ensure easy accessibility and provision of wide range of options

Consumer looking for easy of visibility Product display should help customers to

look at the products easily

Consumers seeking out exclusivity Ensure availability of wide range of

creative and trendy designs

Customers looking for high quality products and at affordable prices

Maintaining high quality products and affordable prices

Consistent launch of new designs and products

Understanding about customers and market and development of new products as per market needs

CRM holds the key: High impact loyalty programs

Across numerous industries, merchant loyalty programs have shown success both in participation and return-on-investment sales.

Customer Loyalty Program helps to track customer purchase history and giving bonus points as per the sales history

Additionally, 90% said loyalty programs give them a competitive edge.

Higher dependence onfranchise model:

•It's hard to keep marketingmessages consistent acrossthe board.

The disparate point of saleenvironment within theindustry.

•The fast, efficient customerservice expected at theseoutlets may be compromisedby any program that addscomplexity to customerinteractions

A CENTRALIZED LOYALTY PROCESSING SYSTEM.

A centralized server can connect all franchisees to the same transactionprocessing network. Data can efficiently be entered regardless of POS system,which eliminates the need for franchisees to add or change equipment.

By offering reward points on every purchase, the customers can gain significantdiscounts or special offers on selected products, monthly list of updated or newarrival stock of preferred product categories

How it is done

What should be the loyalty program

Subscribe to a “surprise and delight” mentality, as opposed to a big, “lottery-sized” offer.

Location: High foot-fall

No location is bad and every location can be made to work in favor of the brand.

Its always a trade-off between the sales potential to support the cost of operations and also offer decent RoI.

Ideal locations for mobile accessories retail would be any location with high footfall of target audience and near areas such as high street, malls, Semi-residential areas.

We define ideal location as one which is not exactly the best location (with high rent! ) but a location which is close to this location (with lower rent !); This will still attract the same target group.

Preferred Locations for Distributors:

o Malls;

o Commercial Centres;

o Near Entertainment Centres;

o Within shopping hubs or high streets;

oResidential Areas.

Mo

nth

ly s

ales

p

ote

nti

al

High

Low

Low

High

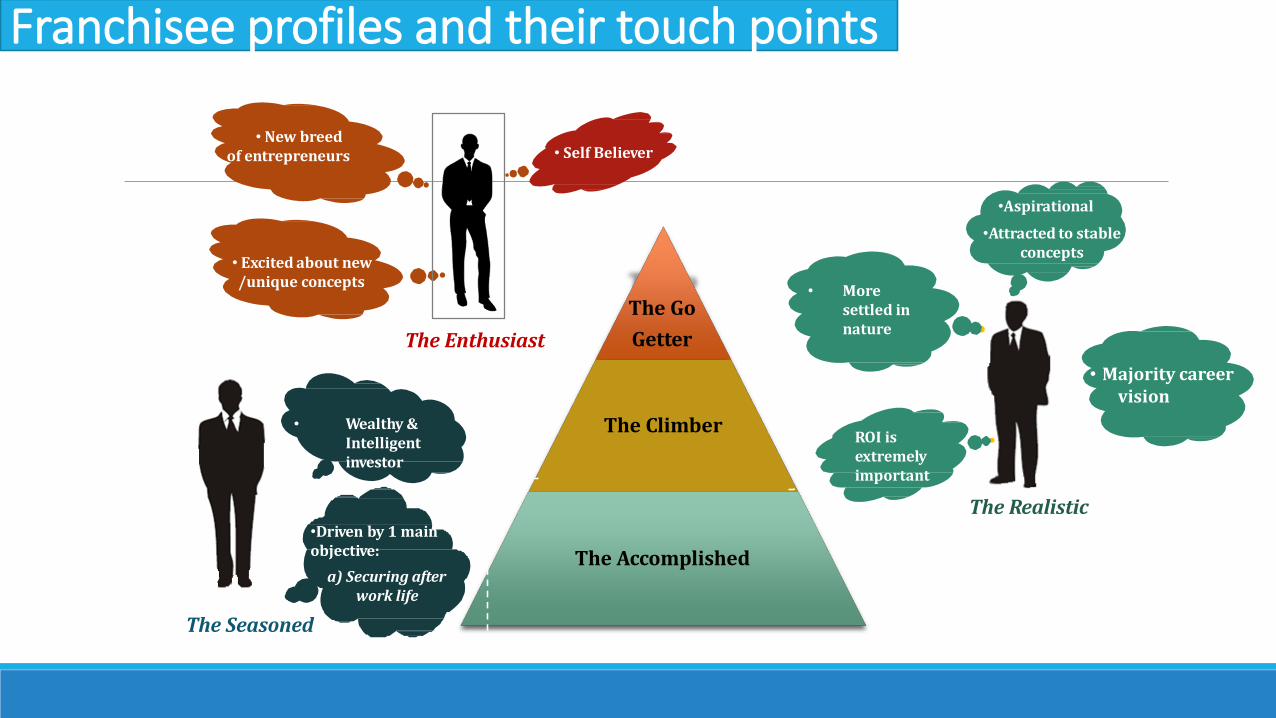

FRANCHISEE PROFILE

Franchisee profiles and their touch points

The Go

Getter

The Climber

The Accomplished

• New breedof entrepreneurs

The Enthusiast

• Self Believer

• Mentally strong

The Realistic

•Aspirational

•Attracted to stable concepts

• ROI isextremelyimportant

• Wealthy &Intelligent investor

• Moresettled innature

•Driven by 1 mainobjective:

a) Securing afterwork life

The Seasoned

• Majority careervision

• Excited about new/unique concepts

Advantages Of Franchising

• Through more touch points (reachability/approachability) of centres it’s easier topenetrate the market

Market Penetration

• Would help in brand recall and brand building

Brand recognition

• Economies of scale would ensure bettersourcing strategies and better utilization ofback end man power

Economies of scale

• Diversification of competencies to include otherproduct categories in the near future

Diversification

Product/

ServiceDiversification

Economies of Scale

Brand recognition

Market Penetration

Franchising

Franchising would help penetrating the market byoutsourcing non core functions, building the brand,generating revenues and building economies of scale.

Identifying the right Franchise Profile (1/2)

S. No Evaluating Parameters Rating Criteria MarksStrategic Parameters

1 City/Area population <18-20 L - 1; between 20 -40 L- 2 ; > 40L - 3

2 Socio economic profile of the location Med - 1; High - 2

3 Availability of the strategic location Low -1; Med - 2; High - 3

4 Presence of competition around the location Low -1; Med - 2; High - 3

5 Degree of competition in the neighborhood Low -1; Med - 2; High - 3

6 Keenness in Immediate roll out Undecided - 1; Within 3-6 months - 2; Immediately - 3;

7 Ease in getting a location Low -1; Med - 2; High - 3

Operational Parameters

1 Managerial bandwidth Low -1; Med - 2; High - 3

2 Overall experience in the retail business Nil -1; Med - 2; High - 3

3 Willingness to comply with franchisor guidelines Low -1; Med - 2; High - 3

4 Participation in the day to day business of the centre Low -1; Med - 2; High - 3

5 Local network and goodwill in the market Low -1; Med - 2; High - 3

6 Interpersonal skills Low -1; Med - 2; High – 3

Weightage: 30%

Weightage: 20%

Identifying the right Franchise Profile (2/2)

S. No Evaluating Parameters Rating Criteria Marks

Financial Parameters

1 Turnover potential of the franchisee centre location Low -1; Med - 2; High - 3

2 Funds availability Low -1; Med - 2; High - 3

3 Anticipated ROI from venture within the proposed plan Low -1; Med - 2; High - 3

4 Ownership of the propertyPremium rentals -1; Average rentals -2; Investorown property -3

Marketing skills

1 Local network and good will in the market Low -1; Med - 2; High – 3

2 Interpersonal skills Low -1; Med - 2; High – 3

• It is recommended that the cut off marks for shortlisting a franchisee should be 60% of the max marks

• This will ensure that the franchisee does not get selected based on any particular parameter

Weightage: 30%

Weightage: 20%

FRANCHISEE ACQUISITION

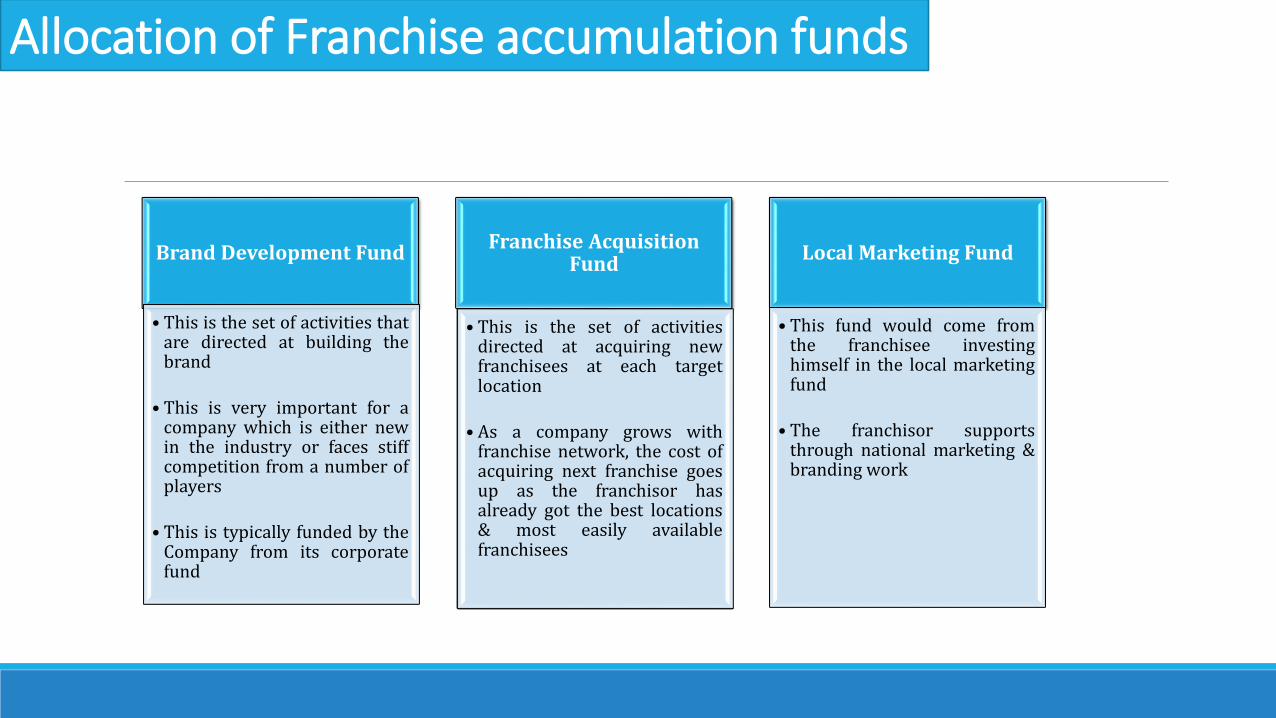

Allocation of Franchise accumulation funds

Brand Development Fund

• This is the set of activities thatare directed at building thebrand

• This is very important for acompany which is either newin the industry or faces stiffcompetition from a number ofplayers

• This is typically funded by theCompany from its corporatefund

Franchise Acquisition Fund

• This is the set of activitiesdirected at acquiring newfranchisees at each targetlocation

• As a company grows withfranchise network, the cost ofacquiring next franchise goesup as the franchisor hasalready got the best locations& most easily availablefranchisees

Local Marketing Fund

• This fund would come fromthe franchisee investinghimself in the local marketingfund

• The franchisor supportsthrough national marketing &branding work

Steps in Franchisee Acquisition

Presenting the business financial model to investors along with marketing kit

Understanding the investors requirements and feedback about the business financial model

In case the investor wants any changes in financial model, the same will be incorporated and presented again to the investors

Finalizing the location and property and signing the LOI

LUMINOSITY should provide adequate support to franchisees which is the critical success factor for expansion

Based on every investor interaction, LUMINOSITY should look at support system and modify it as per the investor needs

Expansion Budget Flux

35% 30% 35%

60% 30% 10%

• As LUMINOSITY launches its franchise program in a territory, it needs to create brand awareness.• Also, since no referrals or conversion of franchises can be expected, hence no significant BTL activities are required

at this stage.• At this stage, NO existing franchisee means NO expenditure towards additional customer acquisition.

50% 30% 20%

• Post initial set of marketing activities, LUMINOSITY gets referrals & follows up referrals of previous stage (1) whichare potential franchisees.

• This means expenditure on Brand development & Franchise acquisition can be relatively lowered.• LUMINOSITY signs up initial set of Franchisees. Hence, for additional customer acquisition, LUMINOSITY will require

higher centralized marketing & support for the franchisee.

• At this stage the brand becomes established & renowned in the city.• It starts getting significant referrals for Franchisee conversions and enjoys a higher customer base.• The overall spend on marketing can be considerably reduced now, which continues for subsequent years.

Brand development fund Franchise Acquisition fund Customer Awareness fund

Tim

eli

ne

for

Fra

nch

ise

Acq

uis

itio

n

1.

2.

3.

Franchise Acquisition Process

Franchise Application signed.Agreement Process initiated.Rollout Plan.

Franchise meetings, further scrutiny of the prospect.

Email Blasts to prospects.Advertisements in The Franchising World & website.Franchise Exhibition.Franchise kits & Communication design.

Basic Information provided to all Inquiries.Expression of Interest generated.Site details would be discussed as per client requirement.Weekly progress sheet submitted to client.Test & measure marketing activity- to identify gaps.

Lead ManagementMarketing Lead Generation Recruitment

Marketing

Business Partner

application

Review of business partner

application

Review Financial Capabilities

Interview with Business partner

Understanding of the business &

conviction

Approval of the business partner

Signing the agreement

Awarding the business partner

Franchisee contract

Typically a LOI is signedwhen a franchisee comes onboard with a token amount.This is followed by thefranchise fee and signingagreement after the locationis finalized

Factory Area: 8050 Sqmtr for B12 and B13 UPSIDC Industrial Area Flatted Factory Constructed Area

Basement : 22000 Sqftused for

PCB manufacturing Unit

R&D

Material loading and unloading Bay

Ageing and assembly lines ,

3 stores for : raw material/semi finished goods/Finished Good

Ground Floor: 22000 Sqft used for

Office

utilities

Solar Module manufacturing

Raw Material

Packing and stacking raw material.

First Floor : 12000 Sqft used for

Hand Sanitizer unit

Guest House

Material loading and unloading Bay

Ageing and assembly lines ,

stores for : raw material/semi finished goods/Finished Good

Shade Factory Section A

Constructed Area

22000 Sqft used for

Sheet Metal Fabrication

Plastic injection/Blow mold machine

Aluminium Die casting Unit

9 tank powder Coating Unit

Shade Factory Section B

Constructed Area 12000 Sqft

Preparation area for Powder coating unit

Compression Molding machine area

Raw material Staorefor rubber/plastic/dmc/smc

Stock yard for MS angle/channels/Pipes/poles

Location : District Hathras Utter Pradesh India

Address: Luminosity Solutions Private Limited

Plot No B13, UPSIDC Industrial Area Salempur Hathras UP

Connectivity : By Road travel

From Agra: 71 Km

Mathura:63 Km

Aligarh : 43 Km

Khurja DFC E&W Jn Station:90 km

New Delhi:177 KM

Nearest Railway Station:

Hathras Junction

Agra:

Mathura

Aligarh

Thanks

For More details.

Please Visit us

www.maxlumans.com