milliman ul/iul survey results - association of insurance ... · milliman ul/iul survey results...

TRANSCRIPT

Milliman UL/IUL Survey Results

AICP New England Chapter

Sue Saip, FSA, MAAAMay 12, 2017

AICP New England Chapter

21st Annual Education Day

Session 4

Milliman UL/IUL Issues Survey

� Comprehensive survey covering:� ULSG, Cash Accumulation UL (AccumUL), Current Assumption UL (CAUL)

� IULSG, Cash Accumulation IUL (AccumIUL), Current Assumption IUL (CAIUL)

� Sales by UL/IUL Product Type � Profit Measures

• By Distribution Channel � Target Surplus

• By Issue Age Group � Reserves

2

• By Premium Type � Risk Management

• By Gender � Underwriting

• By Underwriting Class � Product Design

• By Death Benefit Option � Compensation

• By 7702 Option (CVAT/GPT) � Pricing

• With Chronic Illness Riders � Administration

• With LTC Riders � Illustrations

Milliman UL/IUL Issues Survey

� 32 Participants in the 2016/2017 survey

• Allianz • Global Atlantic • Principal

• American Family • John Hancock • Protective Life

• Americo • Kansas City Life • Sammons Financial Group

• Ameriprise • Lincoln Financial • Securian

• AXA • Modern Woodmen of America • State Farm

3

• Bankers Life • Mutual of Omaha • Symetra

• Cincinnati Life • Nationwide • Thrivent Financial

• Columbus Life • New York Life • TIAA-CREF

• Equitrust • Ohio National • Voya Financial

• Fidelity & Guaranty Life • Pan American • Washington National

• Foresters • Penn Mutual

UL/IUL Sales SummarySales Mix by Year

30%

40%

50%

60%

70%

66% 68%

62%64%

Per

cent

of T

otal

Indi

vidu

al U

L S

ales

Universal Life Sales Mix

30%40%50%60%70%80%90%

80%86% 86% 87%

Per

cent

of T

otal

Indi

vidu

al IU

L S

ales

Indexed UL Sales Mix

4

0%

10%

20%

2013 2014 2015 YTD 9/30/16

17% 18% 16% 15%17%

15%

22% 21%

Per

cent

of T

otal

Indi

vidu

al U

L S

ales

ULSG Cash Accumulation UL Current Assumption UL

0%10%20%30%

2013 2014 2015 YTD 9/30/166%

5% 5% 5%

14%8% 8% 8%

Per

cent

of T

otal

Indi

vidu

al IU

L S

ales

IULSG Cash Accumulation IUL Current Assumption IUL

ULSG dominates Cash Accumulation IUL dominates

UL/IUL Sales SummaryUL Average Amounts Per Policy

UL Weighted Average Premiums Per Policy UL Weighted Average Face Amount Per Policy

2

3

4

5

6

3.5 3.6 3.7 3.4

5.0 5.3

4.9

4.4 4.4 4.3

5.0 4.9

Ave

rage

Pre

miu

m P

er P

olic

y (1

000s

)

200

300

400

500

260 264 295 295

411 431

452 439

287 245

330

310

Ave

rage

Fac

e A

mou

nt P

er P

olic

y (1

000s

)

5

0

1

2

2013 2014 2015 YTD 9/30/16

1.4 1.5 1.6 1.5

Ave

rage

Pre

miu

m P

er P

olic

y (1

000s

)

Total Individual UL ULSG

Cash Accumulation UL Current Assumption UL

0

100

200

2013 2014 2015 YTD 9/30/16

78 85 90 90

Ave

rage

Fac

e A

mou

nt P

er P

olic

y (1

000s

)

Total Individual UL ULSG

Cash Accumulation UL Current Assumption UL

Highest average => ULSG in 2013 & 2014 and Current Assumption UL in 2015 &

YTD 9/30/16

Highest average => ULSG in all periods

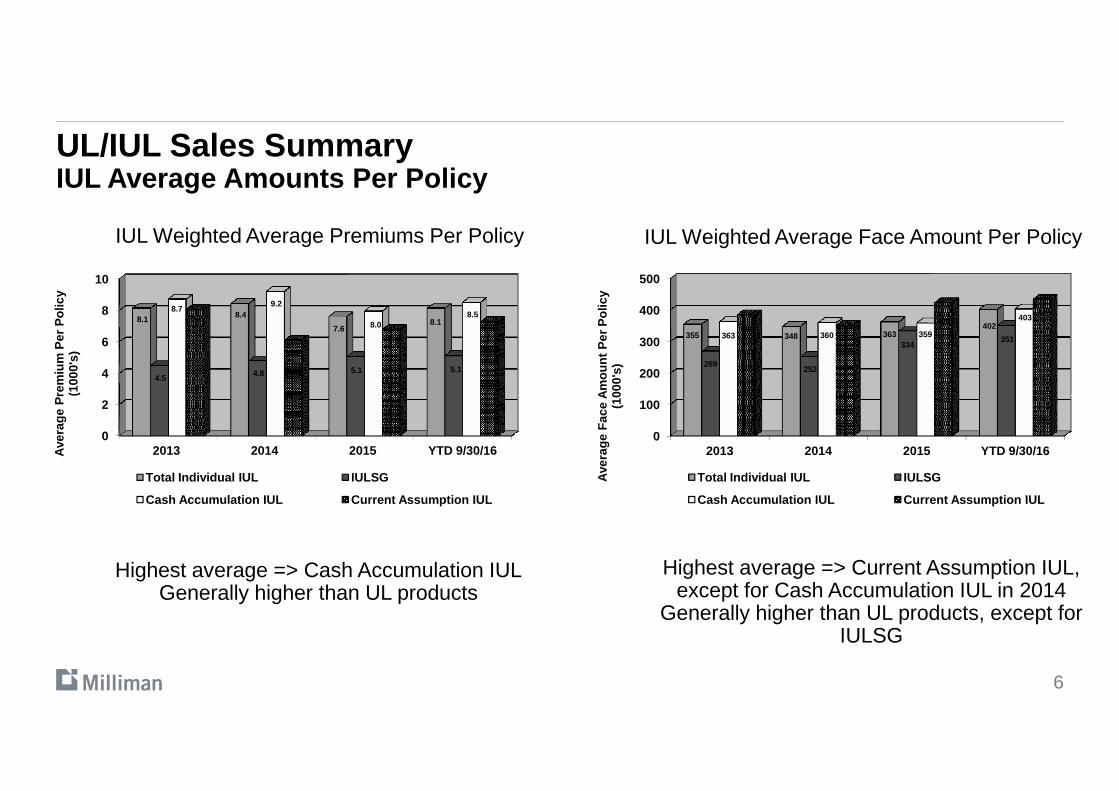

UL/IUL Sales SummaryIUL Average Amounts Per Policy

IUL Weighted Average Premiums Per Policy IUL Weighted Average Face Amount Per Policy

4

6

8

10

8.1 8.4

7.6 8.1

4.5 4.8 5.1 5.1

8.7 9.2

8.0 8.5 8.1

6.1 6.8

7.3

Ave

rage

Pre

miu

m P

er P

olic

y (1

000'

s)

200

300

400

500

355 348 363 402

269 252

334 351 363 360 359

403 385

352

423 434

Ave

rage

Fac

e A

mou

nt P

er P

olic

y (1

000'

s)

6

Highest average => Cash Accumulation IULGenerally higher than UL products

Highest average => Current Assumption IUL, except for Cash Accumulation IUL in 2014

Generally higher than UL products, except for IULSG

0

2

2013 2014 2015 YTD 9/30/16Ave

rage

Pre

miu

m P

er P

olic

y (1

000'

s)

Total Individual IUL IULSG

Cash Accumulation IUL Current Assumption IUL

0

100

2013 2014 2015 YTD 9/30/16

Ave

rage

Fac

e A

mou

nt P

er P

olic

y (1

000'

s)

Total Individual IUL IULSG

Cash Accumulation IUL Current Assumption IUL

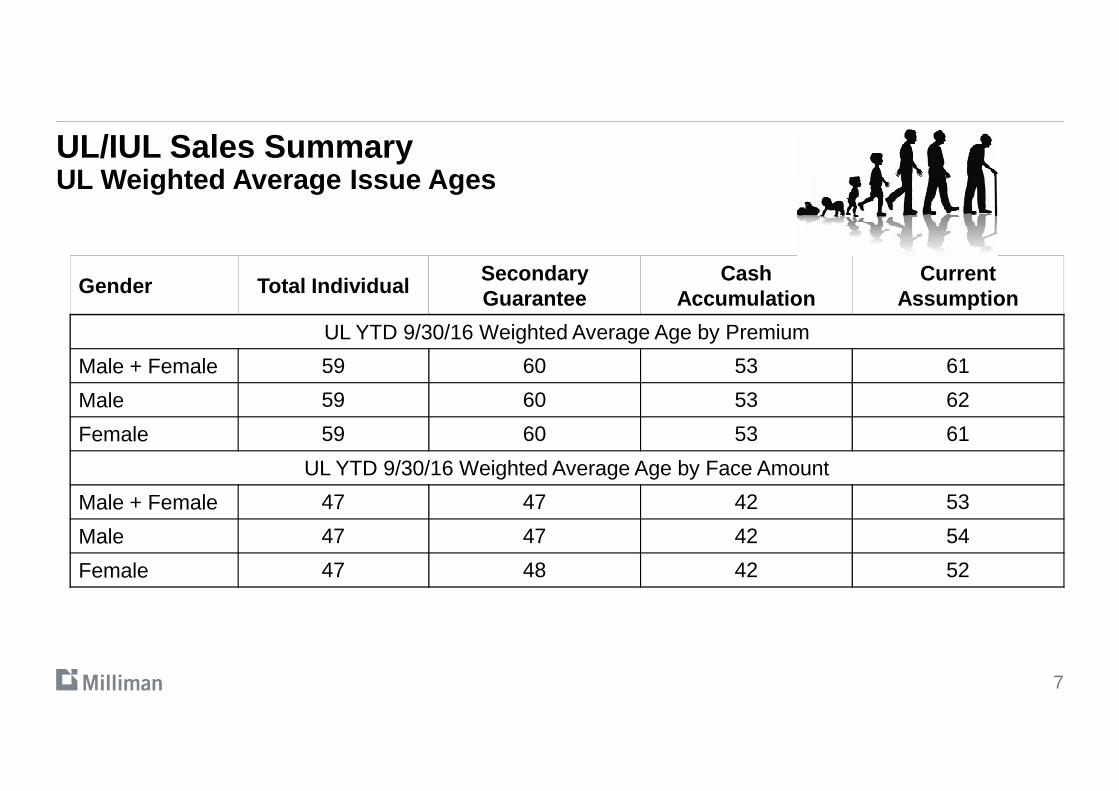

UL/IUL Sales SummaryUL Weighted Average Issue Ages

Gender Total IndividualSecondaryGuarantee

Cash Accumulation

CurrentAssumption

UL YTD 9/30/16 Weighted Average Age by Premium

Male + Female 59 60 53 61

Male 59 60 53 62

7

Male 59 60 53 62

Female 59 60 53 61

UL YTD 9/30/16 Weighted Average Age by Face Amount

Male + Female 47 47 42 53

Male 47 47 42 54

Female 47 48 42 52

UL/IUL Sales SummaryIUL Weighted Average Issue Ages

Gender Total IndividualSecondaryGuarantee

Cash Accumulation

CurrentAssumption

IUL YTD 9/30/16 Weighted Average Age by Premium

Male + Female 53 56 52 59

Male 53 57 53 59

8

Male 53 57 53 59

Female 53 55 52 59

IUL YTD 9/30/16 Weighted Average Age by Face Amount

Male + Female 46 50 45 53

Male 47 51 45 53

Female 45 49 44 52

UL/IUL Sales SummaryExpectations Regarding Future Mix of Business

Item ULSGCash

AccumulationCurrent

AssumptionIULSG

Cash Accumulation

IUL

Current Assumption

IUL

Mix of Business –Averages

Current (31) 28% 12% 9% 3% 42% 4%

9

Current (31) 28% 12% 9% 3% 42% 4%

Current (24) 17% 12% 2% 3% 61% 4%

2 Years (24) 11% 13% 3% 6% 62% 6%

5 Years (24) 9% 14% 3% 6% 62% 6%

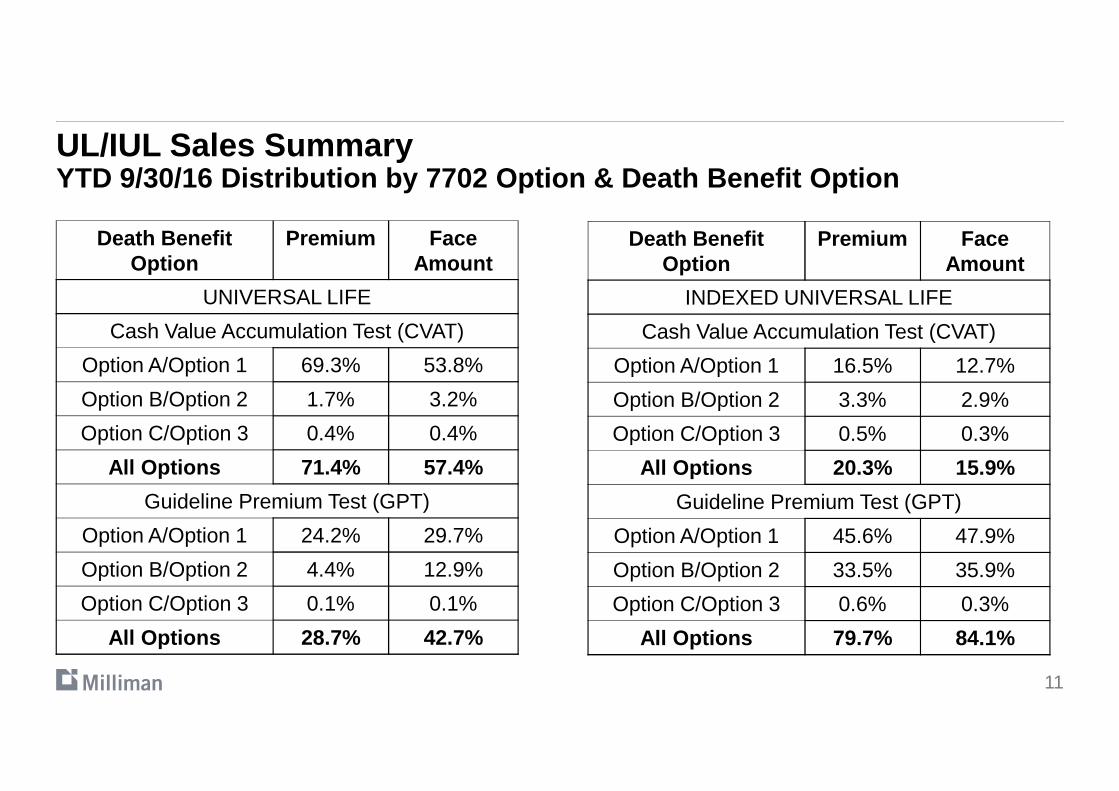

UL/IUL Sales Summary YTD 9/30/16 Distribution by Death Benefit Option

5.8%0.4% 0.9%

14.9%0.2%

UL by Face Amount

0.4%

IUL By Premium IUL by Face Amount UL by Premium

10

94.1%

61.0%

38.0%

84.7%

Option A/Option 1 Option B/Option 2 Option C/Option 3

60.8%

38.7%

UL/IUL Sales Summary YTD 9/30/16 Distribution by 7702 Option & Death Ben efit Option

Death Benefit Option

Premium Face Amount

UNIVERSAL LIFE

Cash Value Accumulation Test (CVAT)

Option A/Option 1 69.3% 53.8%

Option B/Option 2 1.7% 3.2%

Death Benefit Option

Premium Face Amount

INDEXED UNIVERSAL LIFE

Cash Value Accumulation Test (CVAT)

Option A/Option 1 16.5% 12.7%

Option B/Option 2 3.3% 2.9%

11

Option B/Option 2 1.7% 3.2%

Option C/Option 3 0.4% 0.4%

All Options 71.4% 57.4%

Guideline Premium Test (GPT)

Option A/Option 1 24.2% 29.7%

Option B/Option 2 4.4% 12.9%

Option C/Option 3 0.1% 0.1%

All Options 28.7% 42.7%

Option B/Option 2 3.3% 2.9%

Option C/Option 3 0.5% 0.3%

All Options 20.3% 15.9%

Guideline Premium Test (GPT)

Option A/Option 1 45.6% 47.9%

Option B/Option 2 33.5% 35.9%

Option C/Option 3 0.6% 0.3%

All Options 79.7% 84.1%

UL/IUL Sales SummaryChronic Illness Rider Sales

�Chronic Illness Rider Approaches

�Discounted death benefit approach (7 participants)

� Lien approach (5 participants)

�Dollar-for-dollar approach (5 participants)�Dollar-for-dollar approach (5 participants)

12

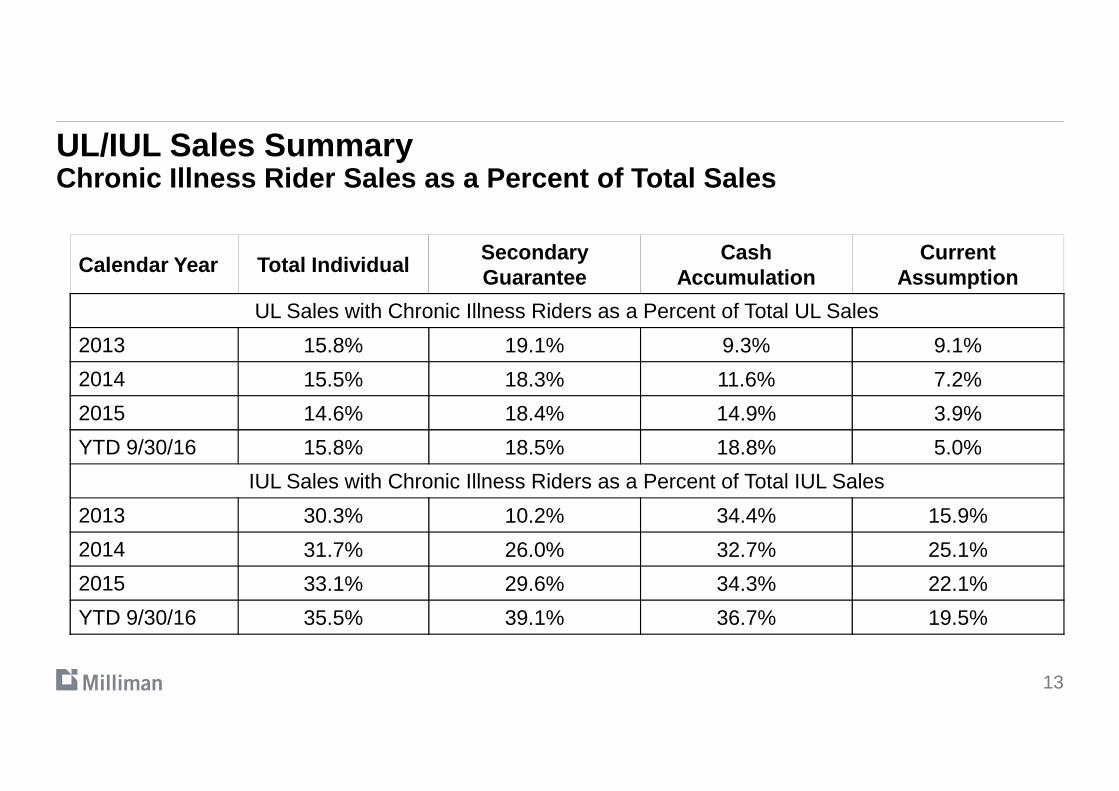

UL/IUL Sales SummaryChronic Illness Rider Sales as a Percent of Total S ales

Calendar Year Total IndividualSecondaryGuarantee

Cash Accumulation

CurrentAssumption

UL Sales with Chronic Illness Riders as a Percent of Total UL Sales

2013 15.8% 19.1% 9.3% 9.1%

2014 15.5% 18.3% 11.6% 7.2%

13

2015 14.6% 18.4% 14.9% 3.9%

YTD 9/30/16 15.8% 18.5% 18.8% 5.0%

IUL Sales with Chronic Illness Riders as a Percent of Total IUL Sales

2013 30.3% 10.2% 34.4% 15.9%

2014 31.7% 26.0% 32.7% 25.1%

2015 33.1% 29.6% 34.3% 22.1%

YTD 9/30/16 35.5% 39.1% 36.7% 19.5%

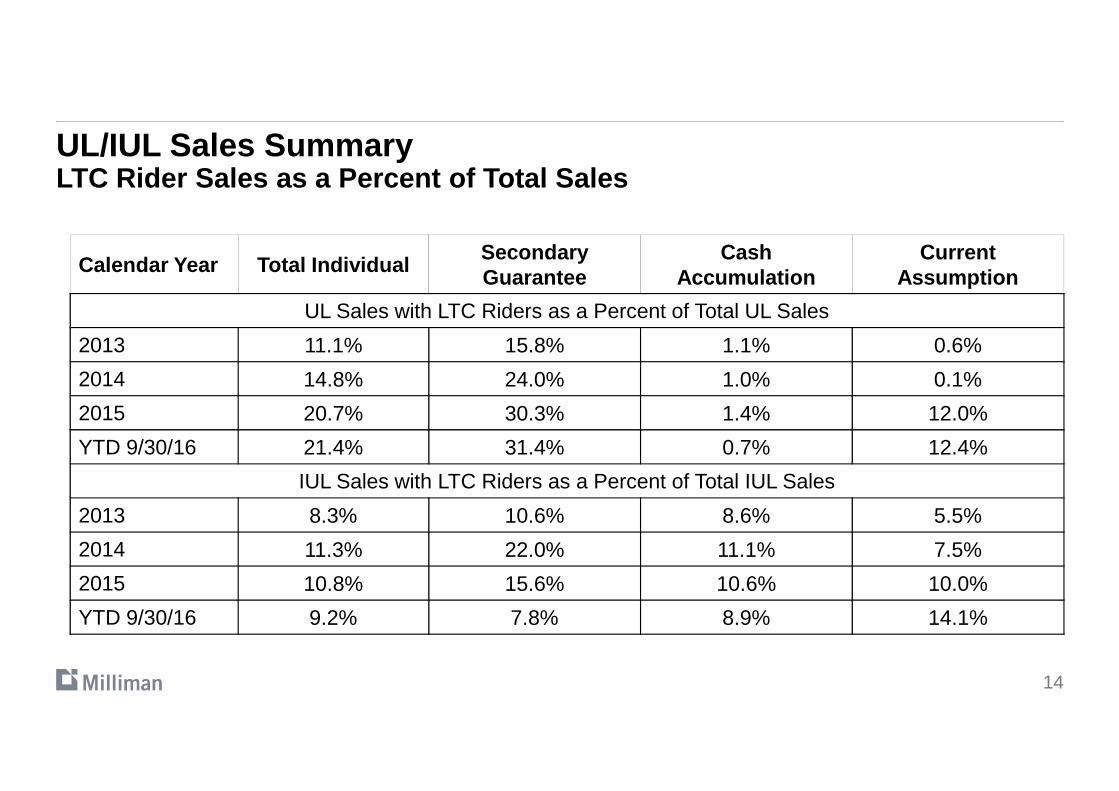

UL/IUL Sales SummaryLTC Rider Sales as a Percent of Total Sales

Calendar Year Total IndividualSecondaryGuarantee

Cash Accumulation

CurrentAssumption

UL Sales with LTC Riders as a Percent of Total UL Sales

2013 11.1% 15.8% 1.1% 0.6%

2014 14.8% 24.0% 1.0% 0.1%

14

2015 20.7% 30.3% 1.4% 12.0%

YTD 9/30/16 21.4% 31.4% 0.7% 12.4%

IUL Sales with LTC Riders as a Percent of Total IUL Sales

2013 8.3% 10.6% 8.6% 5.5%

2014 11.3% 22.0% 11.1% 7.5%

2015 10.8% 15.6% 10.6% 10.0%

YTD 9/30/16 9.2% 7.8% 8.9% 14.1%

Milliman UL/IUL Issues Survey

�Profit Measures

�Predominant measure is after-tax, after-capital statutory ROI/IRR

�Median ROI/IRR is 10% for all UL products, 9.8% for IULSG, 12.3% for AccumIUL, and 12.8% for CAIUL

�During YTD 9/30/16, 63% of participants were short of their profit goals for ULSG, and 78% of participants were at least meeting their profit goals for all other UL/IUL and 78% of participants were at least meeting their profit goals for all other UL/IUL products combined

�Primary reasons for not meeting goals were low interest earnings and expenses

�Target Surplus

�Majority set pricing assumptions as a percent of the NAIC company action level

�Ranged from 250% to 425%, with a median of 350% for most UL/IUL products, except 338% for AccumUL, and 388% for CAIUL

15

Milliman UL/IUL Issues Survey

�Reserves

�Principle-based reserves (PBR) implementation

�Timing

�94% over the 3-year phase-in period

�Rationale for timing – primarily based on resources issues, financial impact/cost/benefits, �Rationale for timing – primarily based on resources issues, financial impact/cost/benefits, impact on reserves and capital, the need for preparation and research, and competitive reasons

16

Milliman UL/IUL Issues Survey

�Reserves

�Pricing new UL products in a PBR environment

�8 of 29 participants did not know how they will reflect reserves in pricing in a PBR environment

�Remaining participants reported they will not change current approach, will reflect VM-20 reserves in pricing, will use a reduced subset of stochastic scenarios, and will use reserves in pricing, will use a reduced subset of stochastic scenarios, and will use approaches that estimate additional reserves

17

Milliman UL/IUL Issues Survey

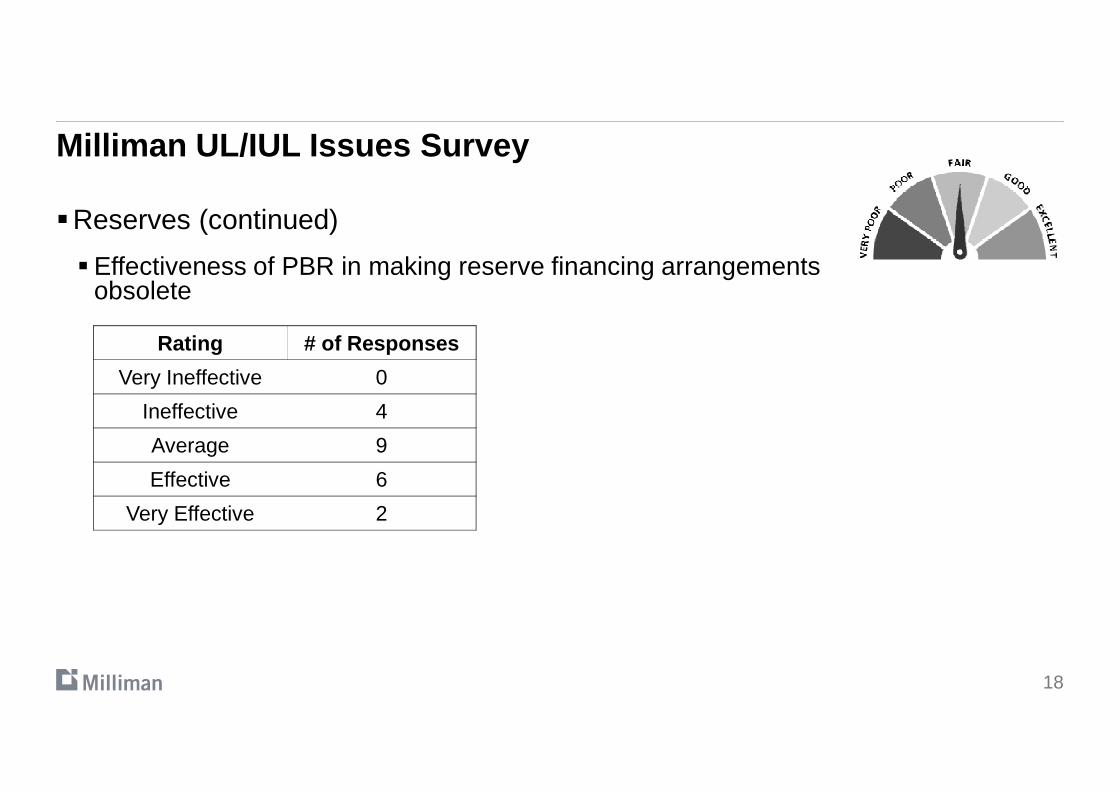

�Reserves (continued)

�Effectiveness of PBR in making reserve financing arrangements obsolete

Rating # of Responses

Very Ineffective 0

18

Ineffective 4

Average 9

Effective 6

Very Effective 2

Milliman UL/IUL Issues Survey

�Reserves (continued)

� 2017 CSO Mortality Table (new valuation mortality table)

�No participants anticipated implementing immediately

�69% anticipate implementing over the 3-year phase-in period

�31% implementation is product dependent�31% implementation is product dependent

� 2017 CSO and PBR

�Implementation at the same time 28%

�Implement 2017 CSO, then PBR at a later date 16%

�Implementation is product dependent 47%

�Other (PBR, then 2017 CSO, 2017 CSO only, TBD) 9%

19

Milliman UL/IUL Issues Survey

�Underwriting

� Table-shaving programs are used by 7 of the 32 participants

� 13 of the participants use a credit program or other type of program that improves ratings for favorable risk factors

�Use of scoring models relative to life underwriting�Use of scoring models relative to life underwriting

�11 participants use; 8 use for fullly underwritten UL/IUL business; 1 uses for simplified issue business; 2 use for both fully underwritten and simplified issue business

�8 of the 11 use scoring models with automated rules

�Scoring models used include lab scoring models, credit scoring models, scoring models relative to motor vehicle records

� Ten participants reported utilizing fluid-less underwriting programs

20

Milliman UL/IUL Issues Survey

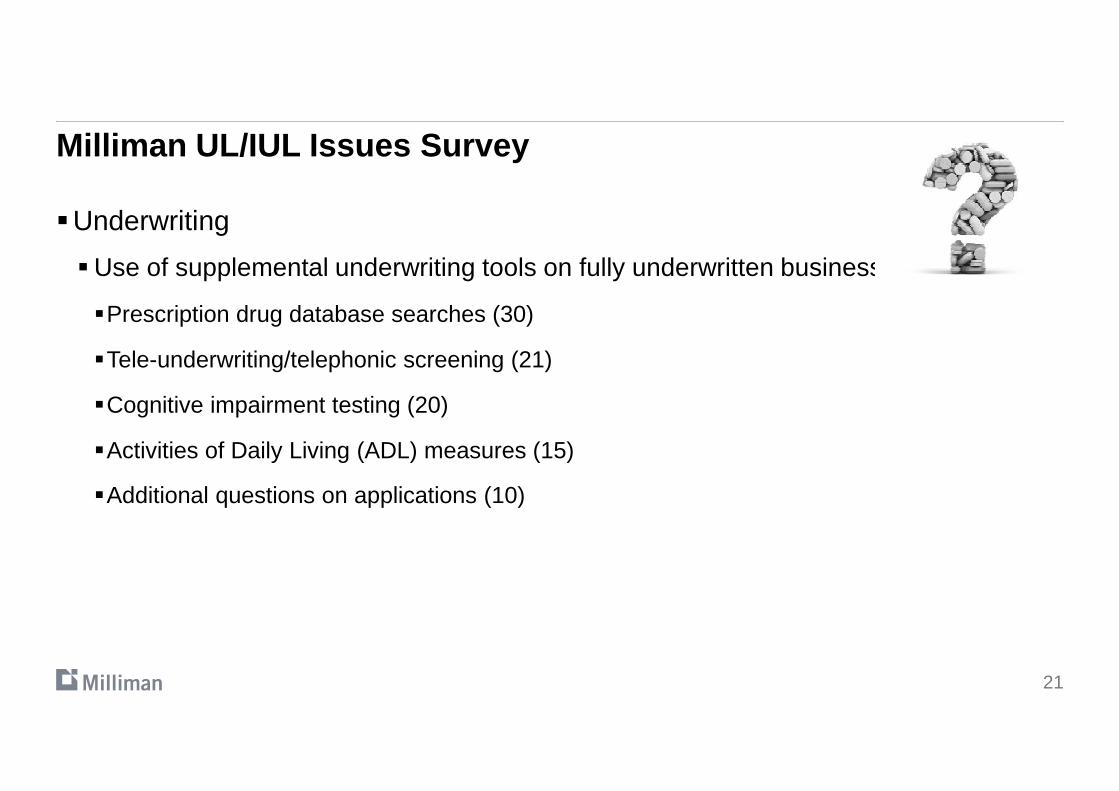

�Underwriting

�Use of supplemental underwriting tools on fully underwritten business:

�Prescription drug database searches (30)

�Tele-underwriting/telephonic screening (21)

�Cognitive impairment testing (20)�Cognitive impairment testing (20)

�Activities of Daily Living (ADL) measures (15)

�Additional questions on applications (10)

21

Milliman UL/IUL Issues Survey

�Underwriting

�Simplified issue underwritten UL/IUL

�17 of the 32 participants offer

�Top markets where offered => individual middle/upper income market and low/middle income marketincome market

�Most popular channel where offered => brokerage channel with 14 of the 17 offering products here

�Most common underwriting tools used are: a) Medical Information Bureau (MIB) Group reports (15), b) Prescription drug database searches (15), and c) Motor vehicle reports (13)

�Knock-out underwriting is used by 22 of 31 responding participants for preferred UL/IUL products

�Debit/credit underwriting by 6; and a combination of knock-out & debit/credit by 3

22

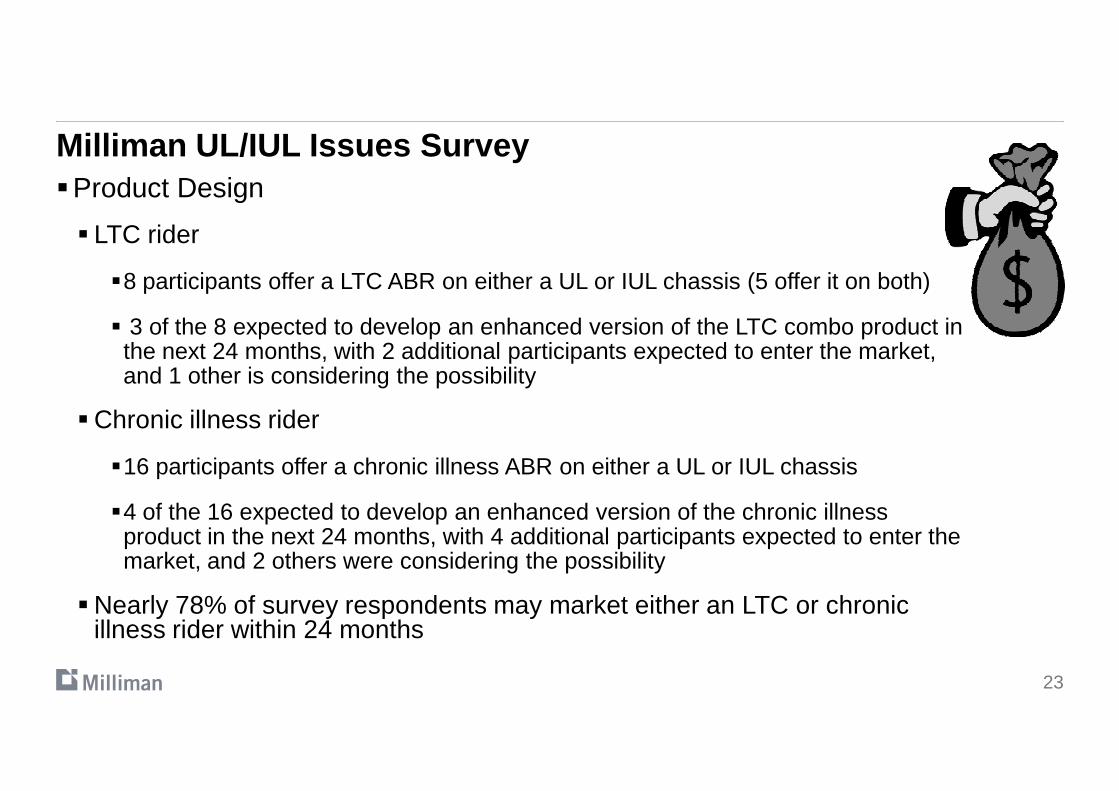

Milliman UL/IUL Issues Survey�Product Design

� LTC rider

�8 participants offer a LTC ABR on either a UL or IUL chassis (5 offer it on both)

� 3 of the 8 expected to develop an enhanced version of the LTC combo product in the next 24 months, with 2 additional participants expected to enter the market, and 1 other is considering the possibility

�Chronic illness rider

�16 participants offer a chronic illness ABR on either a UL or IUL chassis

�4 of the 16 expected to develop an enhanced version of the chronic illness product in the next 24 months, with 4 additional participants expected to enter the market, and 2 others were considering the possibility

�Nearly 78% of survey respondents may market either an LTC or chronic illness rider within 24 months

23

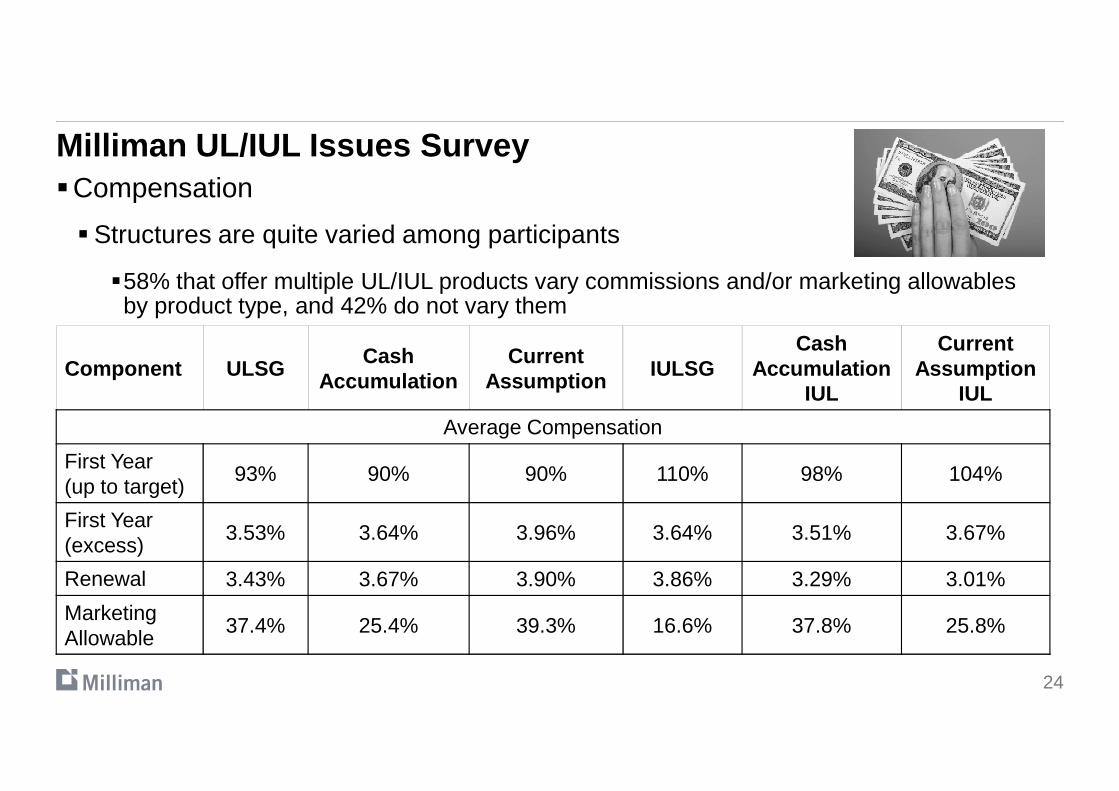

Milliman UL/IUL Issues Survey�Compensation

�Structures are quite varied among participants

�58% that offer multiple UL/IUL products vary commissions and/or marketing allowablesby product type, and 42% do not vary them

Component ULSGCash

AccumulationCurrent

AssumptionIULSG

Cash Accumulation

IUL

Current Assumption

IUL

24

IUL IUL

Average Compensation

First Year(up to target)

93% 90% 90% 110% 98% 104%

First Year (excess)

3.53% 3.64% 3.96% 3.64% 3.51% 3.67%

Renewal 3.43% 3.67% 3.90% 3.86% 3.29% 3.01%

Marketing Allowable

37.4% 25.4% 39.3% 16.6% 37.8% 25.8%

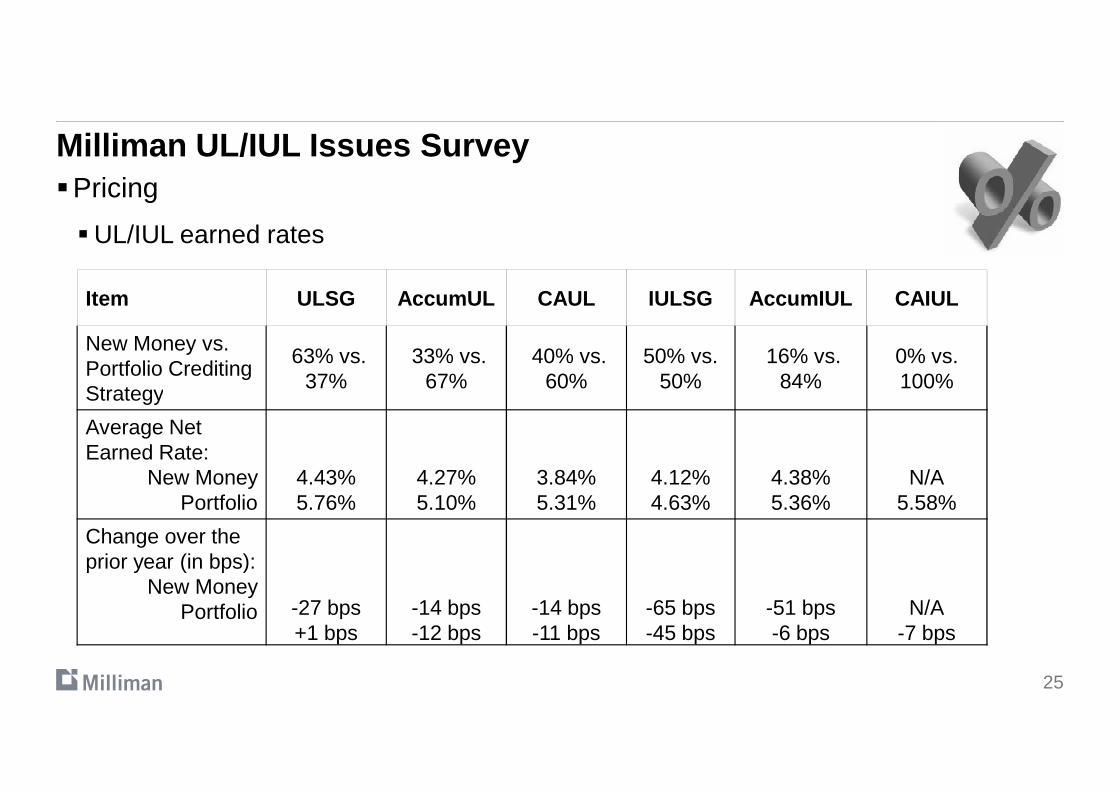

Milliman UL/IUL Issues Survey�Pricing

�UL/IUL earned rates

Item ULSG AccumUL CAUL IULSG AccumIUL CAIUL

New Money vs.Portfolio Crediting Strategy

63% vs. 37%

33% vs. 67%

40% vs. 60%

50% vs. 50%

16% vs. 84%

0% vs. 100%

25

Strategy

Average Net Earned Rate:

New MoneyPortfolio

4.43%5.76%

4.27%5.10%

3.84%5.31%

4.12%4.63%

4.38%5.36%

N/A5.58%

Change over the prior year (in bps):

New MoneyPortfolio -27 bps

+1 bps-14 bps-12 bps

-14 bps-11 bps

-65 bps-45 bps

-51 bps-6 bps

N/A-7 bps

Milliman UL/IUL Issues Survey

�Pricing (continued)

� 2017 CSO Mortality Table impact on pricing

�None have repriced/redesigned UL/IUL products under this table

�Impact on UL/IUL product development relative to guideline premium policies to be sold

�Development of more CVAT products?�Development of more CVAT products?

26

Milliman UL/IUL Issues Survey

� Illustrations

�Actuarial Guideline 49

�Benchmark Index Account rate

�Rates range from 5.29% to 7.92%, with an average of 6.79%

�The average maximum illustrated rates pre-AG 49 ranged from 5.60% to 8.50%, with an �The average maximum illustrated rates pre-AG 49 ranged from 5.60% to 8.50%, with an average of 7.38%

�The average maximum illustrated rate post-AG 49 ranged from 5.02% to 7.75%, with an average of 6.69%

27

Milliman UL/IUL Issues Survey

�Available reports

� If your company name was listed as a participant, you can receive the full report (including individual company responses on an anonymous basis)

�Alternatively, go to http://www.milliman.com and search “Universal Life”, and select the 2016 surveythe 2016 survey

�Download the complimentary Executive Summary; or

�Download the order form for the Detailed Report (similar to the full report, but without the individual company responses) – available on a subscription basis

�Contact me if you have any questions at [email protected]

28