middle east transport and logistics 2010 - bussanbud€¦ · no part of this publication may be...

TRANSCRIPT

Middle East Transport and Logistics 2010

A comprehensive analysis and in-depth examination of the

Middle East air, sea, road and rail markets and profiles of

the leading players

December 2009

Report Code: TIMETL0912

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 2

About Transport Intelligence Headquartered in the UK, Ti is one of the world’s leading providers of expert research and analysis dedicated to the global logistics industry. Utilising the expertise of professionals with many years experience in the mail, express and logistics industry, Transport Intelligence has developed a range of market leading web-based products, reports, profiles and services used by all the world’s leading logistics suppliers, consultancies and banks as well as many users of logistics services.

Transport Intelligence products and services include:

• Ti's news and analysis briefing service, Logistics Briefing

• Exclusive access to Ti’s extensive research output through the ground breaking Global Supply Chain Intelligence portal www.gscintell.com

• Dedicated research through Ti Consulting

• Market and competitor monitoring

• Industry leading research reports including trend analysis, market sizing, market share, forecasting and ranking across global logistics markets

• In-depth intelligence on the world's leading logistics providers through Supply Chain Leaders Intelligence

• Ti Conferences and seminars – www.ticonferences.com

All rights reserved. No part of this publication may be reproduced in any material form including photocopying or storing it by electronic means without the written permission of the copyright owner, Transport Intelligence Limited.

This report is based upon factual information obtained from a number of sources. Whilst every effort is made to ensure that the information is accurate, Transport Intelligence Limited accepts no responsibility for any loss or damage caused by reliance upon the information in this report.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 3

Contents Page

About Transport Intelligence.................................................................................................................2

Contents Page ........................................................................................................................................3

List of Tables and Figures.....................................................................................................................9

1.0 Introduction ...........................................................................................................................12

2.0 Freight transportation sectors.............................................................................................13

2.1 Sea Freight..............................................................................................................................13 2.2 Air Transport ...........................................................................................................................16 2.3 Rail Transport..........................................................................................................................17

2.3.1 Rail network overview ........................................................................................................18 2.3.2 United Arab Emirates Railway ...........................................................................................19 2.3.3 The Saudi Landbridge........................................................................................................19

2.4 Road Transport .......................................................................................................................20 2.4.1 Case Study: TNT’s Middle East Road Network (MERN)...................................................21 2.4.2 Middle East Road Transport: Overview .............................................................................23 2.4.3 Major Regional Road Transport Corridors.........................................................................24 2.4.4 Jordan road corridor...........................................................................................................25 2.4.5 Syrian road corridor ...........................................................................................................26 2.4.6 Saudi Arabia road corridor .................................................................................................27 2.4.7 Lebanon road corridor........................................................................................................27 2.4.8 Egypt road corridor ............................................................................................................27 2.4.9 Qatar road corridor.............................................................................................................28

3.0 Regional trade and political groupings ..............................................................................29

3.1.1 League of Arab States .......................................................................................................29 3.1.2 Council of Arab Economic Unity (CAEU)...........................................................................30 3.1.3 The Agadir Agreement.......................................................................................................31 3.1.4 Greater Arab Free Trade Area (GAFTA) ...........................................................................31 3.1.5 Europe-Mediterranean Free Trade Area (EU-MEFTA)......................................................32 3.1.6 Middle East Free Trade Area (MEFTA) .............................................................................32 3.1.7 Gulf Co-operation Council..................................................................................................33 3.1.8 Maghreb Union...................................................................................................................34

3.2 Economic Analysis ..................................................................................................................35 3.3 Trade.......................................................................................................................................37

3.3.1 Share of Merchandise Export Trade by Region.................................................................37 3.3.2 Share of Merchandise Import Trade by Region.................................................................38 3.3.3 Export Value of Merchandise Product Groups ..................................................................39 3.3.4 Import Value of Merchandise Product Groups...................................................................40 3.3.5 Leading Merchandise Exporters ........................................................................................41

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 4

3.3.6 Leading Merchandise Importers ........................................................................................42

4.0 Middle East – Logistics Markets - Size & Forecasts .........................................................43

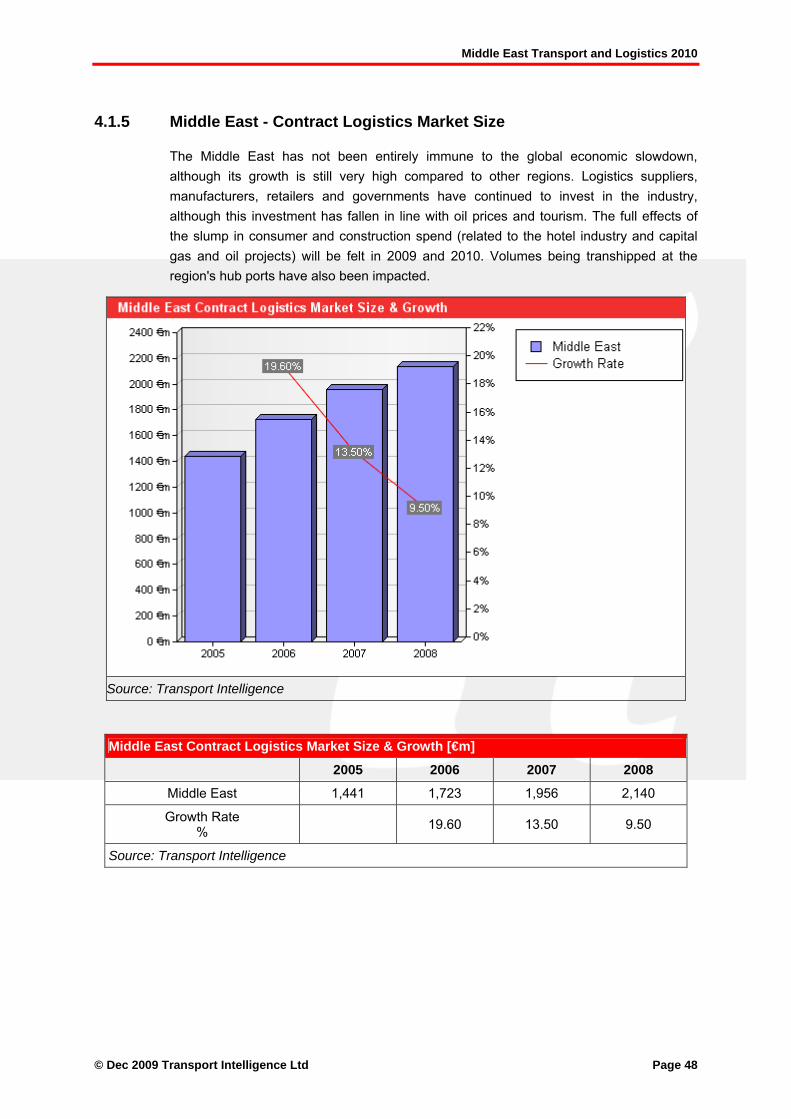

4.1 Contract Logistics....................................................................................................................43 4.1.1 Temperature controlled......................................................................................................44 4.1.2 Construction Logistics........................................................................................................44 4.1.3 Oil logistics .........................................................................................................................45 4.1.4 Automotive spare parts ......................................................................................................47 4.1.5 Middle East - Contract Logistics Market Size ....................................................................48 4.1.6 Middle East - Contract Logistics Market Forecast .............................................................49

4.2 Freight Forwarding ..................................................................................................................50 4.2.1 Middle East - Freight Forwarding Market Size...................................................................52 4.2.2 Middle East - Freight Forwarding Market Forecast............................................................53 4.2.3 Middle East – Air Freight Forwarding Market Size ............................................................54 4.2.4 Middle East – Air Freight Forwarding Market Forecast .....................................................55 4.2.5 Middle East – Sea Freight Forwarding Market Size ..........................................................56 4.2.6 Middle East – Sea Freight Forwarding Market Forecast ...................................................57

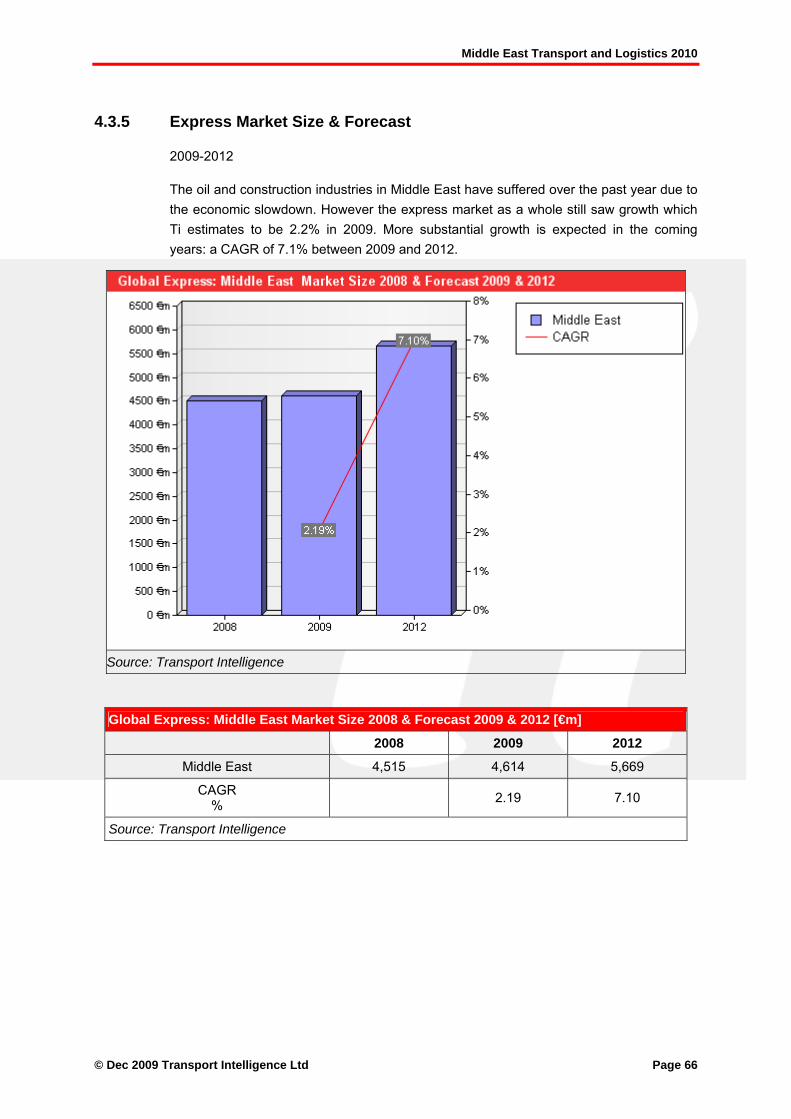

4.3 Express parcels.......................................................................................................................58 4.3.1 Overview ............................................................................................................................58 4.3.2 Profile: DHL Express..........................................................................................................60 4.3.3 Profile: FedEx Middle East.................................................................................................63 4.3.4 Profile: UPS........................................................................................................................65 4.3.5 Express Market Size & Forecast........................................................................................66 4.3.6 Interview with Aramex CEO...............................................................................................67

5.0 Bahrain...................................................................................................................................69

5.1 Economy .................................................................................................................................69 5.2 Trade.......................................................................................................................................69 5.3 Transport Infrastructure...........................................................................................................72

5.3.1 Road Network ....................................................................................................................75 5.3.2 Ports...................................................................................................................................76 5.3.3 Airports...............................................................................................................................77

5.4 Bahrain - Logistics Market.......................................................................................................78 5.4.1 Overview ............................................................................................................................78 5.4.2 Bahrain - Logistics Companies ..........................................................................................79

6.0 Egypt ......................................................................................................................................81

6.1 Economy .................................................................................................................................81 6.2 Trade.......................................................................................................................................81 6.3 Transport Infrastructure...........................................................................................................84

6.3.1 Road Network ....................................................................................................................86 6.3.2 Rail .....................................................................................................................................87 6.3.3 Ports...................................................................................................................................88 6.3.4 Airports...............................................................................................................................89

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 5

6.3.5 Inland Waterways ..............................................................................................................92 6.4 Egypt - Logistics Market..........................................................................................................95

6.4.1 Overview ............................................................................................................................95 6.4.2 Egypt - Logistics Companies .............................................................................................96

7.0 Iran....................................................................................................................................... 101

7.1 Economy .............................................................................................................................. 101 7.2 Trade.................................................................................................................................... 101 7.3 Transport Infrastructure........................................................................................................ 104

7.3.1 Road Network ................................................................................................................. 106 7.3.2 Railway Network ............................................................................................................. 107 7.3.3 Airports............................................................................................................................ 107 7.3.4 Ports................................................................................................................................ 108

7.4 Iran’s Logistics Market ......................................................................................................... 109 7.4.1 Overview ......................................................................................................................... 109 7.4.2 Iran - Logistics Companies ............................................................................................. 110

8.0 Iraq....................................................................................................................................... 111

8.1 Economy .............................................................................................................................. 111 8.2 Trade.................................................................................................................................... 111 8.3 Transport Infrastructure........................................................................................................ 114

8.3.1 Road Network ................................................................................................................. 115 8.3.2 Railway Network ............................................................................................................. 116 8.3.3 Airports............................................................................................................................ 116 8.3.4 Ports................................................................................................................................ 117

8.4 Iraq’s Logistics Market ......................................................................................................... 117 8.4.1 Overview ......................................................................................................................... 117 8.4.2 Iraq - Logistics Companies ............................................................................................. 118

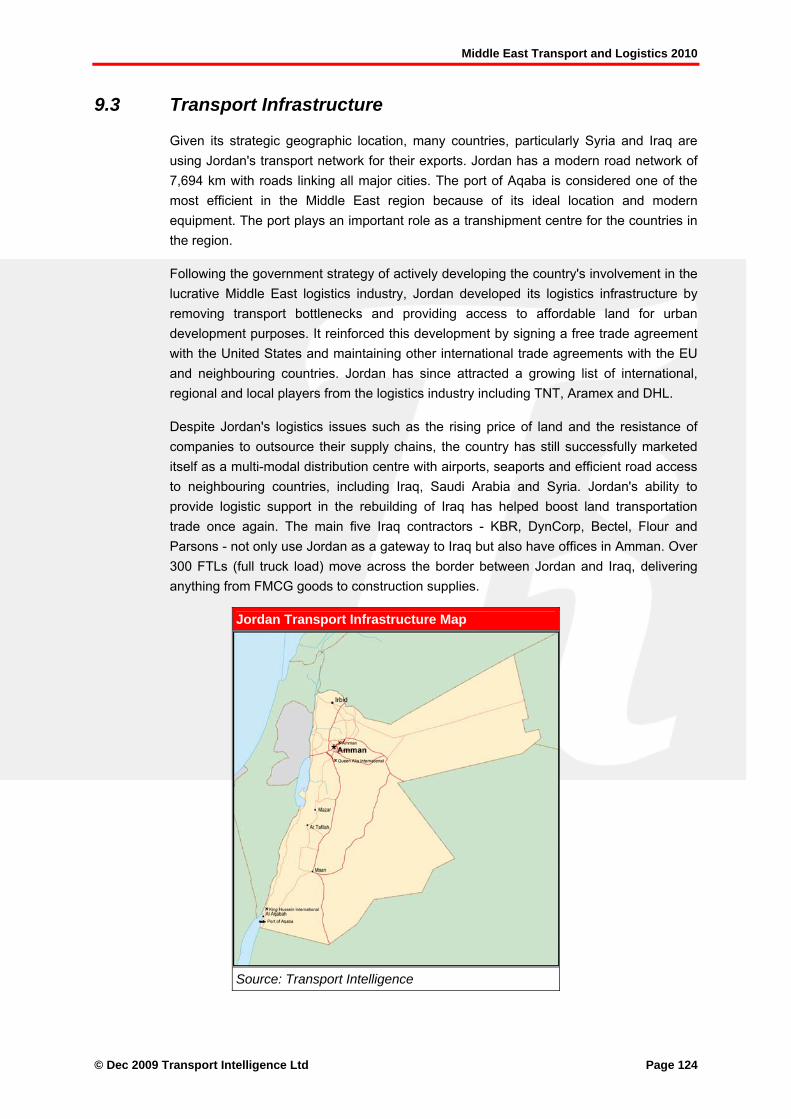

9.0 Jordan ................................................................................................................................. 120

9.1 Economy .............................................................................................................................. 120 9.2 Trade.................................................................................................................................... 121 9.3 Transport Infrastructure........................................................................................................ 124

9.3.1 Road Network ................................................................................................................. 125 9.3.2 Railway Network ............................................................................................................. 125 9.3.3 Airports............................................................................................................................ 126 9.3.4 Ports................................................................................................................................ 126

9.4 Jordan’s Logistics Market..................................................................................................... 127 9.4.1 Overview ......................................................................................................................... 127 9.4.2 Jordan - Logistics Companies......................................................................................... 127

10.0 Kuwait.................................................................................................................................. 129

10.1 Economy .............................................................................................................................. 129 10.2 Trade.................................................................................................................................... 129

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 6

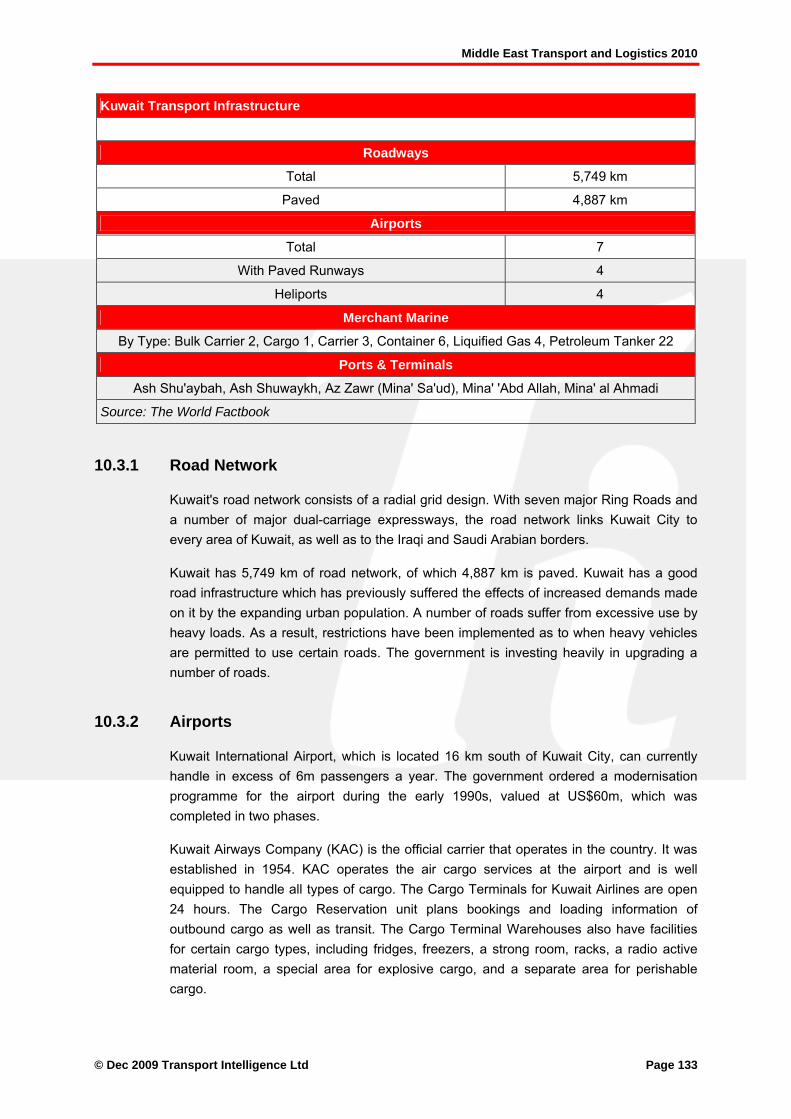

10.3 Transport Infrastructure........................................................................................................ 132 10.3.1 Road Network ................................................................................................................. 133 10.3.2 Airports............................................................................................................................ 133 10.3.3 Ports................................................................................................................................ 134

10.4 Kuwait’s Logistics Market..................................................................................................... 135 10.4.1 Overview ......................................................................................................................... 135 10.4.2 Kuwait - Logistics Companies......................................................................................... 135

11.0 Lebanon .............................................................................................................................. 137

11.1 Economy .............................................................................................................................. 137 11.2 Trade.................................................................................................................................... 137 11.3 Transport Infrastructure........................................................................................................ 140

11.3.1 Road Network ................................................................................................................. 141 11.3.2 Railway Network ............................................................................................................. 141 11.3.3 Airports............................................................................................................................ 142 11.3.4 Ports................................................................................................................................ 142

11.4 Lebanon’s Logistics Market ................................................................................................. 143 11.4.1 Overview ......................................................................................................................... 143 11.4.2 Lebanon - Logistics Companies...................................................................................... 143

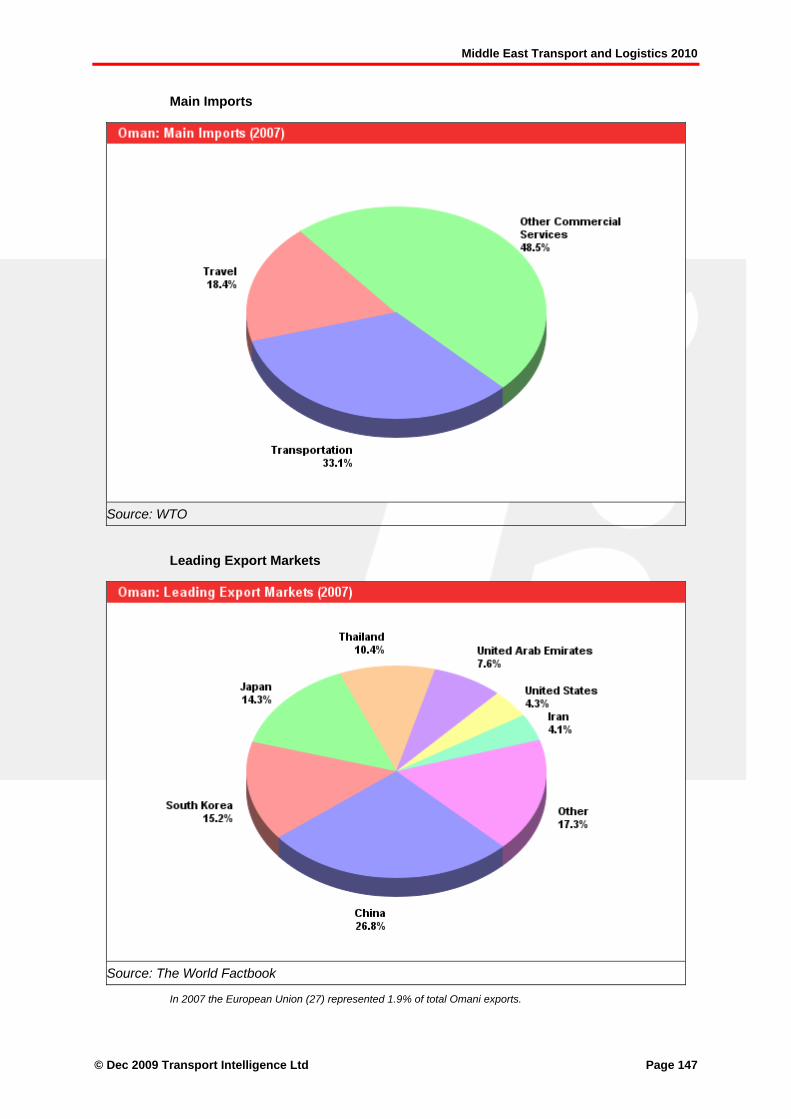

12.0 Oman ................................................................................................................................... 145

12.1 Economy .............................................................................................................................. 145 12.2 Trade.................................................................................................................................... 145 12.3 Transport Infrastructure........................................................................................................ 149

12.3.1 Road Network ................................................................................................................. 150 12.3.2 Airports............................................................................................................................ 150 12.3.3 Ports................................................................................................................................ 150

12.4 Oman’s Logistics Market...................................................................................................... 152 12.4.1 Overview ......................................................................................................................... 152 12.4.2 Oman – Logistics Companies ......................................................................................... 152

13.0 Qatar .................................................................................................................................... 154

13.1 Economy .............................................................................................................................. 154 13.2 Trade.................................................................................................................................... 154 13.3 Transport Infrastructure........................................................................................................ 157

13.3.1 Road Network ................................................................................................................. 158 13.3.2 Railway Network ............................................................................................................. 158 13.3.3 Airports............................................................................................................................ 160 13.3.4 Ports................................................................................................................................ 161

13.4 Qatar’s Logistics Market....................................................................................................... 163 13.4.1 Overview ......................................................................................................................... 163 13.4.2 Qatar - Logistics Companies........................................................................................... 163

14.0 Saudi Arabia ....................................................................................................................... 167

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 7

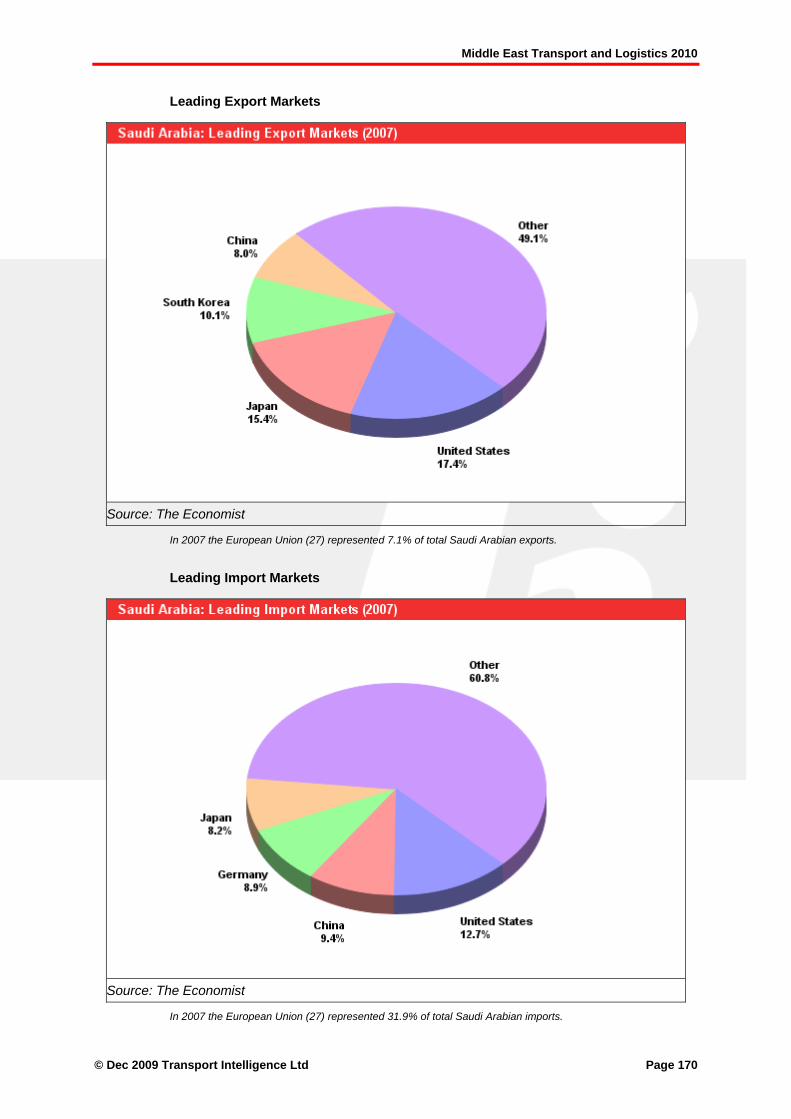

14.1 Economy .............................................................................................................................. 167 14.2 Trade.................................................................................................................................... 168 14.3 Transport Infrastructure........................................................................................................ 171

14.3.1 Road Network ................................................................................................................. 172 14.3.2 Railway Network ............................................................................................................. 174 14.3.3 Airports............................................................................................................................ 176 14.3.4 Ports................................................................................................................................ 177

14.4 Saudi Arabia’s Logistics Market........................................................................................... 179 14.4.1 Overview ......................................................................................................................... 179 14.4.2 Saudi Arabia - Logistics Companies............................................................................... 180

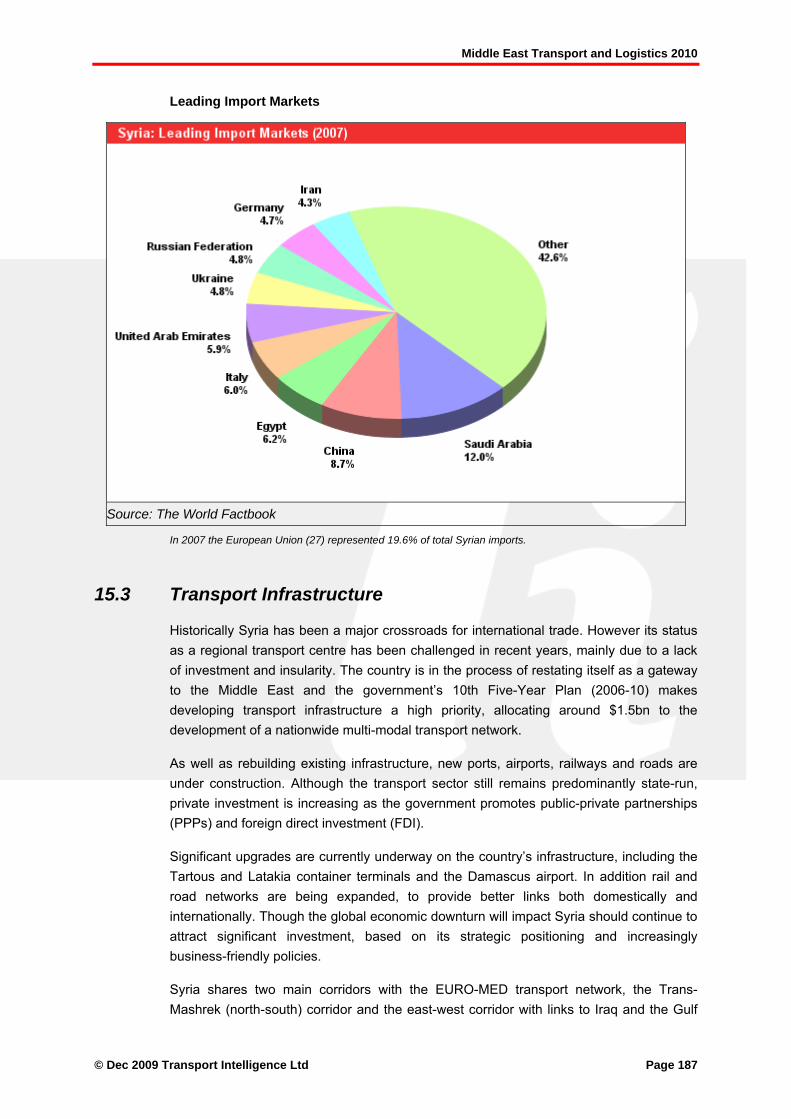

15.0 Syria..................................................................................................................................... 184

15.1 Economy .............................................................................................................................. 184 15.2 Trade.................................................................................................................................... 184 15.3 Transport Infrastructure........................................................................................................ 187

15.3.1 Road Network ................................................................................................................. 189 15.3.2 Railway Network ............................................................................................................. 190 15.3.3 Airports............................................................................................................................ 190 15.3.4 Ports................................................................................................................................ 190

15.4 Syria’s Logistics Market ....................................................................................................... 191 15.4.1 Overview ......................................................................................................................... 191 15.4.2 Syria - Logistics Companies ........................................................................................... 192

16.0 UAE...................................................................................................................................... 194

16.1 Economy .............................................................................................................................. 194 16.2 Trade.................................................................................................................................... 194

16.2.2 Free Trade Zones ........................................................................................................... 197 16.3 Transport Infrastructure........................................................................................................ 200

16.3.1 Road Network ................................................................................................................. 201 16.3.2 Railway Network ............................................................................................................. 202 16.3.3 Airports............................................................................................................................ 203 16.3.4 Ports................................................................................................................................ 207

16.4 UAE’s Logistics Market ........................................................................................................ 208 16.4.1 Overview ......................................................................................................................... 208 16.4.2 UAE - Logistics Companies ............................................................................................ 209

Appendix 1: Logistics Provider Profiles ......................................................................................... 222

17.0 Egypt ................................................................................................................................... 222

17.1 3 A Logistics & Projects ....................................................................................................... 222 17.2 Egytrans ............................................................................................................................... 223

17.2.1 Finances.......................................................................................................................... 223 17.2.2 Operations....................................................................................................................... 224

17.3 El Wafaa Transport .............................................................................................................. 225

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 8

17.4 Mesco................................................................................................................................... 225 17.5 Nosco ................................................................................................................................... 227

18.0 Iraq....................................................................................................................................... 228

18.1 Middle East Shipping Services Ltd (MSS) ........................................................................... 228

19.0 Jordan ................................................................................................................................. 229

19.1 T. Gargour & Fils.................................................................................................................. 229

20.0 Kuwait.................................................................................................................................. 230

20.1 Agility.................................................................................................................................... 230 20.1.1 Finances.......................................................................................................................... 230 20.1.2 Operations....................................................................................................................... 236 20.1.3 Strategy........................................................................................................................... 237

20.2 Risco .................................................................................................................................... 239

21.0 United Arab Emirates......................................................................................................... 241

21.1 Ahmadah RAK International Logistics Services L.L.C......................................................... 241 21.2 Al-Futtaim Group.................................................................................................................. 243

21.2.1 Al_Futtaim Logistics........................................................................................................ 243 21.3 Aramex................................................................................................................................. 246

21.3.1 Finances.......................................................................................................................... 246 21.3.2 Operations....................................................................................................................... 250 21.3.3 Strategy........................................................................................................................... 251

21.4 DP World.............................................................................................................................. 253 21.4.1 Finances.......................................................................................................................... 253 21.4.2 Operations....................................................................................................................... 256 21.4.3 Strategy........................................................................................................................... 258

21.5 Empost ................................................................................................................................. 259 21.6 GAC...................................................................................................................................... 260

21.6.1 Operations....................................................................................................................... 260 21.6.2 Strategy........................................................................................................................... 261

21.7 Global Cargo System........................................................................................................... 263 21.8 Global Shipping & Logistics (GSL)....................................................................................... 264 21.9 Gulftainer Co. Ltd ................................................................................................................. 265

21.9.1 Operations....................................................................................................................... 265 21.9.2 Strategy........................................................................................................................... 266

21.10 RHS logistics................................................................................................................... 268

Contact Transport Intelligence ........................................................................................................ 269

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 9

List of Tables and Figures

About Transport Intelligence.................................................................................................................2

Contents Page ........................................................................................................................................3

List of Tables and Figures.....................................................................................................................9

1.0 Introduction ...........................................................................................................................12

2.0 Freight transportation sectors.............................................................................................13

Middle East Transport & Logistics Markets: Top 10 Middle East Ports [mTeu]................................13 Top 10 Middle East Ports ..................................................................................................................15 Table: Top Ten Cargo airports in Middle East ..................................................................................16 Top Ten Cargo airports in Middle East .............................................................................................17 Nine New Main Axes for Creation of Middle East Rail Network........................................................18 Saudi Arabia: potential new rail links ................................................................................................20 TNT: Middle East Route Network......................................................................................................21 TNT: Iran Route Network ..................................................................................................................23

3.0 Regional trade and political groupings ..............................................................................29

League of Arab States.......................................................................................................................29 Current Members and Observers of the Arab League......................................................................30 Greater Arab Free Trade Area (GAFTA)...........................................................................................31 GDP Figures by Country ...................................................................................................................35 Middle East Logistics 2009: Share of Merchandise Export Trade by Region [US$bn].....................37 Middle East Logistics 2009: Share of Merchandise Import Trade by Region [US$bn] .....................38 Middle East Logistics 2009: Export Value of Merchandise Product Groups [US$bn].......................39 Middle East Logistics 2009: Import Value of Merchandise Product Groups [US$bn].......................40 Middle East Logistics 2009: Leading Merchandise Exporters [US$bn] ............................................41 Middle East Logistics 2009: Leading Merchandise Importers [US$bn] ............................................42

4.0 Middle East – Logistics Markets - Size & Forecasts .........................................................43

Middle East Contract Logistics Market Size & Growth [€m]..............................................................48 Middle East Contract Logistics Market Size Forecast 2012 [€m]......................................................49 Major Forwarders Locations in the Middle East ................................................................................51 Middle East: Freight Forwarding Market Size & Growth [€m] ...........................................................52 Middle East: Freight Forwarding Market Forecast 2012 [€m] ...........................................................53 Middle East: Air Freight Forwarding Market Size & Growth [€m]......................................................54 Middle East: Air Freight Forwarding Market Forecast 2012 [€m]......................................................55 Middle East: Sea Freight Forwarding Market Size & Growth [€m]....................................................56 Middle East: Sea Freight Forwarding Market Forecast 2012 [€m]....................................................57 DHL Middle East Network .................................................................................................................60 Global Express: Middle East Market Size 2008 & Forecast 2009 & 2012 [€m]................................66

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 10

Global Express: Middle East International & Domestic Market Size % to Total [€m] .......................67

5.0 Bahrain...................................................................................................................................69

Bahrain Transport Infrastructure Map ...............................................................................................74 Bahrain Transport Infrastructure .......................................................................................................75

6.0 Egypt ......................................................................................................................................81

Egypt Transport Infrastructure Map ..................................................................................................85 Egypt Transport Infrastructure...........................................................................................................86 Trans African Highway Network........................................................................................................87 Suez Canal ........................................................................................................................................93 The Suez Canal.................................................................................................................................93 Distance Savings...............................................................................................................................94 Suez Canal versus The Cape of Good Hope....................................................................................94

7.0 Iran....................................................................................................................................... 101

Iran Transport Infrastructure Map................................................................................................... 105 Iran Transport Infrastructure........................................................................................................... 106

8.0 Iraq....................................................................................................................................... 111

Iraq Transport Infrastructure Map................................................................................................... 114 Iraq Transport Infrastructure........................................................................................................... 115

9.0 Jordan ................................................................................................................................. 120

Geographic Area (sq km) ............................................................................................................... 120 Jordan Transport Infrastructure Map.............................................................................................. 124 Jordan Transport Infrastructure...................................................................................................... 125

10.0 Kuwait.................................................................................................................................. 129

Kuwait Transport Infrastructure Map.............................................................................................. 132 Kuwait Transport Infrastructure...................................................................................................... 133

11.0 Lebanon .............................................................................................................................. 137

Lebanon Transport Infrastructure Map........................................................................................... 140 Lebanon Transport Infrastructure................................................................................................... 141

12.0 Oman ................................................................................................................................... 145

Oman Transport Infrastructure Map............................................................................................... 149 Oman Transport Infrastructure....................................................................................................... 149

13.0 Qatar .................................................................................................................................... 154

Qatar Transport Infrastructure Map................................................................................................ 157 Qatar Transport Infrastructure........................................................................................................ 158

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 11

14.0 Saudi Arabia ....................................................................................................................... 167

Saudi Arabia Transport Infrastructure Map .................................................................................... 171 Saudi Arabia Transport Infrastructure ............................................................................................ 172 Planned Extensions to the Saudi Arabian Rail Network ................................................................ 174

15.0 Syria..................................................................................................................................... 184

Syria Transport Infrastructure Map ................................................................................................ 188 Syria Transport Infrastructure......................................................................................................... 189 Syria: Strategic Location ................................................................................................................ 192

16.0 UAE...................................................................................................................................... 194

UAE Transport Infrastructure ......................................................................................................... 201

Appendix 1: Logistics Provider Profiles ......................................................................................... 222

17.0 Egypt ................................................................................................................................... 222

Egytrans Finances: Total [EGPm].................................................................................................. 223 Project Activities (2008) freight tons............................................................................................... 224

18.0 Iraq....................................................................................................................................... 228

19.0 Jordan ................................................................................................................................. 229

20.0 Kuwait.................................................................................................................................. 230

Agility Finances: Total [KWDm]...................................................................................................... 232 Agility Finances: Revenue by Reporting Segments % to Total [KWDm] ....................................... 233 Agility Finances: Revenue by Business Segment % to Total [KWDm].......................................... 235 Agility Finances: Revenue by Geographic Location % to Total [KWDm]....................................... 235 Agility Global Network .................................................................................................................... 236

21.0 United Arab Emirates......................................................................................................... 241

Aramex Finances: Total [AEDm].................................................................................................... 248 Aramex Finances: Revenue by Business Segment % to Total [AEDm] ........................................ 249 Aramex Finances: Revenue by Geographic Location % to Total [AEDm]..................................... 250 DP World Finances: Total [US$m] ................................................................................................. 255 DP World Finances: Revenue By Geographical Location % to Total [US$m] ............................... 256 Port Locations................................................................................................................................. 257

Contact Transport Intelligence ........................................................................................................ 269

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 12

1.0 Introduction In late 2009 news broke of what was an effective default on the debts of Dubai World, the state backed investment vehicle of the Dubai government. Up to this point it had seemed as if the Middle East had been largely immune from the global downturn which had proved so deleterious for the rest of the world. Oil and gas revenues over the previous years had filled the coffers of the resource-rich region, and although the oil price had fallen temporarily, there seemed no need for concern.

Indeed this argument still holds good, if Dubai’s problems can be contained. Dubai lacks the energy resources of its neighbours, such as Abu Dhabi, and instead has built its economy on tourism, construction and logistics. Of these, the global industries of tourism and real estate proved vulnerable to global weakness. However, whilst Dubai is struggling, other oil and gas rich GCC states are continuing to invest in their infrastructure.

What the Dubai crisis does prove is that it is impossible to look upon the region as in any way homogenous – there is a considerable disparity between neighbouring countries in terms of GDP per head. Impoverished and war torn nations, such as Iraq and Lebanon, are located next to those displaying conspicuous levels of wealth.

From a logistics point of view, efforts are being made to create cohesive cross-regional air and road networks. However attempting to integrate such a diverse range of economies is very challenging. Efforts at a governmental level are being made, especially in the GCC countries, to create a Single Market, in the mould of the European Union. However progress is slow for political reasons.

As in many parts of the developing world, logistics infrastructure in the Middle East is predominantly focused on ports and air freight due to the paucity of road and rail infrastructure. It also has the advantage of the Suez Canal, meaning that it has become a natural hub for sea freight. Its geographical location, triangulated by Europe, the Indian sub-continent and Africa, has meant that it is growing in importance as an air hub.

Consequently, Dubai and Abu Dhabi in particular have transformed themselves into major international logistics hubs, not just for the Middle East but also for much of the eastern hemisphere. Jebel Ali is the world's sixth largest container port by throughput and Dubai is attempting to position itself as a logistics hub for distribution between China, India and Europe.

Driven on by the development of a vast infrastructure, the GCC states have been described as the fulfilment of the notion, "build it and they will come". Despite the problems which Dubai is facing at the moment, there is no doubt that long term fundamentals are good and logistics companies are investing heavily in the market. A number of global and regional logistics providers with major operations in the Middle East, such as GAC Logistics (part of the diverse Gulf Agency Company group), Aramex, Agility, TNT, DHL and others, see major opportunities, and have announced major expansion plans, both within the region and in other parts of the world, particularly Asia.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 13

2.0 Freight transportation sectors

2.1 Sea Freight

The ports system in the Middle East region is dominated by the UAE, which accounts for around 50% of throughput. The bulk of these are trans-shipped from Asia Pacific destinations for onward distribution to Europe and North America.

Source: Transport Intelligence

Middle East Transport & Logistics Markets: Top 10 Middle East Ports [mTeu]

2008 Dubai, UAE 11.80 (+10.8%)

Jeddah, Saudi Arabia 3.33 (+8.4%)

Port Said, Egypt 3.26 (+14.7%)

Salalah, Oman 3.07 (+16.3%)

Sharjah, UAE 2.50 (+15.1%)

Bandar Abbas, Iran 2.00 (+16.1%)

Dammam, Saudi Arabia 1.25 (+14.7%)

Damietta, Egypt 1.24 (+23.8%)

Beirut, Lebanon 0.95 (-0.03%)

Aqaba, Jordan 0.59 (+42%)

Source: Transport Intelligence

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 14

With the global downturn, the historically buoyant sea freight volumes to and from the major logistics hub both in the Middle East region have come under threat. China in particular is a major market for Dubai's imports and exports, and this has fuelled the growing Middle East–Asia trade.

The biggest port operator in the region, DP World, has been badly affected, although not to the same extent as shipping lines. Its half year results 2009 saw container through–put fall by 1.3m TEU to 12.3m on a year–on–year basis. The falls in volumes experienced by DP World appear quite modest bearing in mind the collapse in trade seen on certain key trades. This seems to be due to DP World's market posture, with heavy exposure to the Gulf and other emerging markets and relatively under–weight in trans–pacific trades.

DP World's big investments in Dubai performed reasonably well with a 7% fall in containers comparing favourably with the rest of Europe.

In early 2009 the annual capacity at Dubai's extensive Jebel Ali container terminal was increased by 5m TEUs, up to 14m TEUs per year.

Located strategically between Europe and the Far East, UAE ports have been the preferred choice of location for a wide range of multinational companies. As the commercial and maritime centre of the Middle East region, UAE has been very proactive in recognising its strengths in the global market. The country has embarked on a programme of attracting investments into its free trade zones, particularly a wide range of manufacturing and service activities.

UAE now dominates the regional shipping industry with 61.3% of import activity and 103 berths for all types of cargoes and ships. Most of the maritime activity is now centred in two ports – Port Rashid and Jebel Ali, the largest man-made ports in the world. Jebel Ali primarily handles bulk cargo and industrial materials that are used in the Jebel Ali Industrial Zone. The port of Mina Zayed has emerged to be third-largest liquid bulk port in the UAE with 21 berths (12.5 percent of import activity), handling most of the UAE's own crude oil exports.

Sharjah is yet another major maritime hub in the region and is being developed as a maritime industrial city. It plans to set up a full-fledged maritime city in the Hamriya Free Zone for the exclusive use of shipbuilding and related maritime businesses. Details of this Maritime City that will cover one million square metres with facilities for dry docking, shipbuilding, ship design, warehousing and support services are still being worked out. Khor Fakkan Container Terminal (KCT), located closer to UAE’s eastern coast, is a dedicated container port. A modern road connects it with the commercial and industrial markets on the UAE's Gulf coast. KCT is the only natural deepwater port in the region.

The Port of Fujairah is also a leading multi-purpose port in the Middle East and is the third largest bunkering centre in the world after Rotterdam and Singapore.

Abu Dhabi is also pursuing a new ports strategy with the setting up of the Abu Dhabi Ports Company and Abu Dhabi Terminals Company which will centre on serving the new Khalifa Port & Industrial Zone, eventually Port Zayed operations will be transferred to the

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 15

new Khalifa Port. Abu Dhabi is seeking to diversify and drive economic growth by empowering the private sector to operate in the Khalifa Free Trade Zone.

Top 10 Middle East Ports

Source: Transport Intelligence

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 16

2.2 Air Transport

The Middle East has suffered the economic slowdown less than most other parts of the world in 2008. In the first ten months of the 2009 air cargo output in the region was down just 0.5% in terms of freight tonne kms. This compared with a fall of 15% in Asia Pacific and 19% in Europe. In the full year 2008, air cargo output grew by 6.3%.

Below is a guide to the top 10 Middle East Cargo hubs for 2008. The data is provided by GACA and Airports Council International.

Table: Top Ten Cargo airports in Middle East

1 Dubai International Airport (UAE)

2. Doha International Airport (Qatar)

3: Bahrain International Airport

4. Sharjah International Airport (UAE)

5. Abu Dhabi International Airport (UAE)

6. King Khalid International Airport – Riyadh (Saudi Arabia)

7. King Abdulaziz International Airport – Jeddah (Saudi Arabia)

8. Kuwait International Airport

9. Queen Alia International Airport (Jordan)

10. Beirut International Airport (Lebanon)

Source: ACI

A new airport, due for completion in 2010, will eventually dwarf Dubai International. Al Maktoum International Airport is located in Dubai World Central, an integrated logistics, residential and commercial centre 40km from the existing Dubai Airport, to which it will be linked by an express railway. The cargo centre will have an annual cargo capacity of 12 million tons. DWC-Al Maktoum International will be ten times larger than Dubai International Airport and Dubai Cargo Village combined.

UAE is not the only country to invest heavily in its airport infrastructure. A new airport is being built in Doha (New Doha International Airport – NDIA) and Bahrain is being extended (due for completion 2010).

The largest indigenous air cargo carrier in the region is Emirates, although it is now being challenged by three or four other state backed rivals. These include:

• Gulf Air Cargo, owned by Kingdom of Bahrain and the Sultanate of Oman (50:50)

• Etihad, owned by Abu Dhabi (formerly held share in Gulf)

• Qatar Airways

In addition to the local players, all the major European airlines have strength in the region including Lufthansa and British Airways.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 17

Top Ten Cargo airports in Middle East

Source: Transport Intelligence

2.3 Rail Transport

The Middle East region could emerge as one of the world’s leading trans-continental railroad systems in the world. Despite many potential opportunities, the railroad systems in the Middle East have been so far limited to few countries including Iran, Egypt, Syria and Jordan. However, the region is witnessing renewed interest in railways with countries such as Saudi Arabia, United Arab Emirates (UAE), Iran looking to scale up railroad systems with several multi-billion dollar projects, including for national, intra-regional and trans-continental connectivity for passenger and cargo movement.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 18

2.3.1 Rail network overview

All Arab countries are now modernising their lines to the standard gauge, except in Sudan and Tunisia. Most lines are single track and very few electrified. The density is also very low compared to advanced countries. The diversity of track gauges further makes through movement of traffic, especially freight, difficult.

A study undertaken by the Arab Railway Union (ARU) on linking various Arab railways and subsequently adopted by the Council of Arab Transportation Ministers, highlights the importance of new railway projects in the Middle East.

Nine New Main Axes for Creation of Middle East Rail Network

1700 km connecting Syria with Iraq and Mediterranean Sea with Arab Gulf

1860 km connecting Iraq and Oman via Kuwait and Saudi Arabia

2560 km connecting Saudi Arabia and Jordan

1700 km connecting Syria and Saudi Arabia via Jordan

4000 km connecting Oman and Saudi Arabia via Yemen

2300 km connecting Egypt and Sudan

6200 km connecting Egypt and Mauritania via Libya, Tunisia, Algeria and Morocco.

3000 km connecting Algeria and Mauritania.

1500 km connecting Somalia and Djibouti and on to Yemen via Red Sea by ferry

Source: Arab Railway Union

The challenges in development of railways in the Middle East mainly centre on the following areas:

• Lack of government action, especially among those countries which have historically had limited or no railway networks and which lack strong economic incentive for investing in railways.

• The government emphasis on road and highway projects have, to an extent, led to neglect of rail, especially as the latter entails additional investments in rolling stock.

• Need for massive upfront capital investment. The huge interest payments on investments constitute a major budget difficulty.

• Difficulty of obtaining private financing for projects with slow rates of return. The World Bank has not financed railway projects in Arab countries but has instead contributed to highway construction, explaining why Arab governments focus on road development.

• Through-traffic problems due to specification/gauge differences. This also weakens the profitability of railways.

However a Middle East rail network, linking all major capitals across the region, could eventually become a reality. Plans for a high-speed inter-Gulf railway, linking all six Gulf

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 19

Co-operation Council states have already been proposed and Transport ministers of the Gulf Co-operation Council (GCC) states have approved a detailed feasibility study for the establishment of this multi-billion-dollar railway network. Saudi Arabia has been entrusted the responsibility for preparing a detailed technical study on GCC railway network connecting all six countries.

The preliminary study proposes construction of two lines, the first being 1,970 km long and stretching from Kuwait to Saudi Arabia, Bahrain and through a bridge to Qatar, and from there to the UAE and Oman. The second line would be 1,984-km long, running from Kuwait to Saudi Arabia and the UAE and ending in Oman. Connecting points will be in Bahrain and Qatar. This total network will comprise of 10 arteries and stretch from the Syrian/Turkish border in the north down to Aden (Yemen) and Salalah (Oman) in the south via Iraq and the UAE. A parallel line would run through Jordan and Saudi Arabia down to Yemen. A westward line would run across North Africa, linking in with the various national rail networks in the region, before terminating in Mauritania on the Atlantic. The plan is to link up the region’s highly fragmented rail networks, which includes separate systems in Syria, Iraq, Jordan and Saudi Arabia. The existing networks are under-developed though, as well as being sparsely utilised.

2.3.2 United Arab Emirates Railway

This proposed freight railway network extending between 700 and 1000 km in length will connect all seven of the emirates. The main trunk route will be Sharjah-Dubai-Abu Dhabi. The Emirates Rail project also potentially links up with a number of other rail projects across the region, which form the Arabian railway network.

In 2009 plans for this railway had progressed when Etihad (Union) Railways announced that the railway would comprise around 1100 km of track and would have an initial budget of AED 25-30 billion.

The railway will connect Ghuwaifat on the Saudi Arabian border with towns on the borders of Oman. The railway will be paid for by a combination of public and private money.

2.3.3 The Saudi Landbridge

Saudi Arabia is planning a rail $5bn project linking the East and the West of the country, known as the Saudi Landbridge railway. The freight expansion involves the construction of a new line from Eastern Province starting at Jubail Industrial City, passing through Dammam and Riyadh Dry Port on to the Jeddah Islamic Port. The Landbridge will be primarily a freight line for containers and general cargo.

When financing of the project from a private consortium fell through in 2009, the Saudi government decided to finance the Landbridge project itself, packaging parts to put up for tender.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 20

The Landbridge project, with an estimated cost of about SR4.875 billion (about $1.3bn) is expected to transform the existing rail network into a world-class freight and passenger rail link across the country, moving large quantities of cargo over long distances at competitive rates. The freight route expansion would integrate new lines from the Jeddah Islamic Port, King Abdul Aziz Port in Dammam, and the Riyadh Dry Port. Both the passenger and freight routes of the Landbridge would entail the opening of over 1,000 km of new railway track.

The project involves construction of 950 km new tracks between Riyadh and Jeddah and another 115-km line between Dammam and Jubail as well as upgrading of the existing rail link between Riyadh and Dammam.

Saudi Arabia: potential new rail links

Source: Saudi Railways Organisation

2.4 Road Transport

Road freight in the Middle East region is increasingly important, as infrastructure improves and the regulatory framework develops. It is believed that the number of licensed trucks on the roads between 2001 and 2007 almost doubled. This has meant that congestion in some areas is a major problem, as is the issue of overloaded vehicles which causes damage to roads as well as having safety implications.

The use of technology is also at a very early stage, meaning that efficiencies in the industry are low. Despite this the major global players, as well as national leaders, are building networks which span the region.

TNT Express has been at the forefront of extending and developing its road network in the Middle East. It reaches across the region and now includes the GCC countries, Lebanon, Jordan, Syria and Yemen. DHL has also developed a road network, connected to its European services.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 21

2.4.1 Case Study: TNT’s Middle East Road Network (MERN)

TNT Express is among one of the most expansive express players in the Middle East seeking to establish market leadership in ground based, rather than air express, distribution. In addition to air express services, it operates a Middle East Road Network (MERN), which offers Door to Door, Day Definite service throughout the region with its 'Day Definite' service guaranteeing customers the exact number of delivery days.

MERN also includes full track and trace technology, door-to-door delivery, one price for imports and exports, 24/7 customer service as well as GPS tracking. It covers 10 destinations including Dubai, Jebel Ali, Abu Dhabi, Doha, Bahrain, Kuwait, Dhahran, Riyadh, Jeddah and Muscat.

It has been steadily growing its vertical markets business by focusing on key Middle East sectors including oil and gas, telecoms, I.T, electronics, banking and retail. It claims it is able to achieve a day definite service through its knowledge and experience of all the preferred routes at specific times of the day and night. It also has relationships with authorities at border points and a good understanding of import-export regulations throughout the region. United Arab Emirates (UAE) to Kuwait has a transit time of two working days and UAE to Jeddah, three.

TNT: Middle East Route Network

Source: TNT

By 2009 TNT Express said the company had seen growth "ahead of management expectations", much of it due to outbound business from the UAE to Saudi Arabia, Qatar and Kuwait, without giving specific figures.

MERN - UAE

Much of TNT's regional strength comes from the UAE which acts as a shipping, storage and redistribution hub for major corporate clients, including Daimler and Volvo. TNT Express in the UAE was recently awarded a two year contract worth over AED6m per year by Volvo Middle East to provide express road and air distribution across the region.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 22

TNT has invested more than Dh10m in the United Arab Emirates to expand the network and increase its geographical presence. The company has been building a Dh4m warehousing and distribution facility in Dubai Airport Free Zone in addition to its Middle East road network hub in the south of Jebel Ali Free Zone. TNT's planned expansion was expected to increase its UAE workforce by 20%. TNT has also been establishing new facilities in Abu Dhabi and Al Ain with investment commitment totalling Dh3m. A new 1,000 sq m road express operations centre at Al Mina Port, an office in Mussafah and a walk-in express high street facility in Al Ain are among the facilities that are part of the expansion plan. In 2006 TNT opened new road hubs in the United Arab Emirates, Bahrain and in 2007 in Saudi Arabia, as well as an additional trucking facility in Kuwait, further strengthening the MERN.

MERN - Bahrain

TNT's strategy in Bahrain has been to increase infrastructure investment with plans to target a 40% increase in business. TNT's immediate plan was to invest in an additional 1,500 sq m of warehousing and office space to accommodate growth, both in its Middle East Road Network and the anticipated increase in business out of Bahrain.

MERN - Saudi Arabia

In Saudi Arabia, TNT/SAB Express, TNT's JV, has undergone major expansion. The company has opened a new warehouse and office in Dhahran. Although TNT entered the Saudi Arabia market relatively late, the operator has still managed to find opportunities in the country.

“Since TNT enjoys a smaller market share, we can offer a more personal and engaging service to our customers,” explains TNT. “We operate a number of depots and warehouses in the three provinces and have more than 50 retail access points across the Kingdom to support the requirement of customers.”

MERN - Iran

In 2005 TNT Express launched the Middle East's first UAE-Iran road express as part of the consolidation of its ground distribution networks in the region. The thrice-weekly Sharjah-Bandar Abbas route was part of the company's plan to double its Middle East Road Network (MERN) revenues during the following three years. Iran is a top 10 destination for TNT UAE and currently represents around 5% of total revenue.

It expects its Iranian business to at least double in the future. The new road express route will include a door-to-door service. The 12-hour journey to the southern Iran port city of Bandar Abbas will run every 3 days. Air freight is very expensive compared to the road haulage, which is around 40% cheaper with a transit time of an additional two to three days.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 23

TNT: Iran Route Network

Source: TNT

Lebanon

In 2008 TNT extended its Middle East Road Network (MERN) into Lebanon, through a partnership with Net Holding.

Lebanon is key to the Levant region development as it is strategically placed as both a European gateway and a natural extension to the Middle East Road Network.

Through this partnership TNT now offers a range of services to customers in Lebanon, including 9:00 Express, 12:00 Express, Global Express, Economy Express, Receiver Pays, Airfreight services and Road Haulage.

2.4.2 Middle East Road Transport: Overview

With its vast land area, harsh terrain, extremes of climate and low density of population, the construction and maintenance of an adequate modern transport networks has always been difficult and challenging task in the Middle East.

The road transportation sector has grown rapidly in Arab countries due to the relatively fast development of the road networks as well as the underdevelopment of other surface transport modes such as the railways. A combination of factors such as rapid population growth, increasing consumer demand for products and surplus incomes owing to high oil prices further means that there has been a strong market for the road transport sector. At the same time, many parts of this region (countries like Iraq, Lebanon, Yemen, etc) are re-emerging after long periods of war and political isolation. These countries want not only the consumer products but also are eager to diversify their economy in the non-oil sector and for rapid reconstruction of assets lost during periods of war. In addition large scale investment, emerging political stability and open economic policies have turned the Arabian Gulf into the logistical hub for large scale trans-continental trade.

The road transport industry in the Middle East is, as in many other parts of developing world, fragmented with many trucking companies. Few companies have been able to build scale and size into their operations.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 24

The major drawbacks of the industry consist in overcoming following challenges:

• inefficient trucking and transport services

• low outbound export volume leading to long shipping times and the need for costly inventory accumulation

• inefficient customs authorities and procedures

• low and inconsistent product quality,

• an underdeveloped transport intermediary sector

• inefficient cross-border transit procedures

There are a few large government owned trucking companies that are engaged in cross-border movement of goods, such as between Jordan and Syria but domestic trucking companies have struggled in scaling up their business models to fully capture the emerging market opportunities or improve the quality of services. There has however, been a marked consolidation trend in this industry, with entry of large overseas players into road express services. Conventional players who have been able to consolidate their positions now enjoy a competitive advantage, as it is harder for new entrants to penetrate the market and build an effective operational and terminal network.

The supply/demand equation in the “less than truck load” (LTL) industry has been tightening and some market players have been able to capitalise on their operating leverage through better usage of previously unutilised networks, resulting in better performances. However, the main risk lies in these LTLs maintaining defensive pricing strategies against aggressive inroads adopted by large integrators seeking to increase their express offerings.

2.4.3 Major Regional Road Transport Corridors

At present, there are seven main “port-to-hinterland” road corridors used for moving commercial cargos in the region.

• Jordan corridor using the Port of Aqaba as point of origin extends through to the Karama/Trebil border

• Syrian corridor is served by its own ports as well as Lebanese ports

• Iraq's road corridors connect to ports of Umm Qasr and Umm Zubayr on the Arabian Gulf

• Turkish corridor uses several Mediterranean ports as well as the overland route from Europe and Black Sea trade through the port of Samsun

• Kuwait, with Shuwaikh Port and Shuaiba Port

• Iran is connected through Bandar Khomeini

• Saudi Arabia's Ar'ar border crossing point.

Traffic through Iran into Iraq is negligible with Saudi Arabia emerging as an entry point. Most trade from Saudi Arabia passes through Kuwait, as evidenced by the large number of Saudi transit trucks in Kuwait.

Middle East Transport and Logistics 2010

© Dec 2009 Transport Intelligence Ltd Page 25

2.4.4 Jordan road corridor

Jordan’s trucking industry primarily transports goods to and from Aqaba as well as transit goods to neighbouring Arab countries, especially Syria. During the 1980s, transit goods represented a major portion of freight traffic, but with the Gulf War and competition from other ports in the region, the trucking industry experienced a downturn. Since then the industry has deteriorated and is currently characterised by the following features:

• Oversupply in the market along with stagnant demand has led to the decrease in rates. Jordan’s total truck fleet reached 13,000 trucks, while the market demand does not exceed 5,000 trucks.

• Transport rates set by the Ministry have been decreasing over the past couple of years but the rates have not yet reached a level that allow Jordanian trucks to compete with neighbouring countries.

• Ninety percent of trucks are 20 years or older and need to be replaced. But the industry is in poor financial condition and does not have the capability to modernise.

The trucking industry in the trans-Jordan region (covering Lebanon, Iraq and Syria) are dominated by three companies, two of which are state-owned on a joint basis between Jordan government and Syria while the third is a government-run cartel.

These comprise:

1. Jordan-Syria Land Transport Company, owned by the Jordanian and Syrian governments operates with a fleet of 392 trucks and 700 drivers. The company transports goods between Port of Aqaba and various locations in Jordan, phosphate from mines to Aqaba, and transit goods from Syria and Lebanon.

2. Iraqi-Jordanian Road Transport Company, established jointly in 1980 by the Jordanian and Iraqi governments for the purpose of transporting oil from Iraq to Jordan moves transit cargo from Aqaba to Baghdad and phosphate from mines to the Port of Aqaba. The company has a fleet of 300 trucks operated by about 500 drivers.

3. Unified Company Land Transport Company is a cartel that owns no trucks but which was established by government for the purpose of organising private sector trucking by assigning loads for trucks operating in the Aqaba and Zarqa Free Zones. As to the private operators, the largest company is Odeh Naber Transportation Company with a fleet of 350 trucks and 450 employees.

Further development of road transport system in the region requires concerted government actions to address:

• defining a national and regional transport policy

• overhauling the regulatory regime for the trucking sector