middle east and central asia regional economic outlook -- jacques charaoui, imf

TRANSCRIPT

Middle East and Central Asia

Regional Economic Outlook

December 2015

Jacques Charaoui

Roadmap

Regional Themes

MENAP Oil Exporters

MENAP Oil Importers

Oil and Conflicts Are the Key Factors Shaping the

Economic Outlook for MENAP

Conflicts Oil

3

4

The Slump in Oil Prices is Expected to Persist

0

20

40

60

80

100

120

140

160

2014 2015 2016 2017 2018 2019

95% confidence interval 86% confidence interval

68% confidence interval Brent spot price

Brent futures

Brent Crude Oil Price

(U.S. dollars per barrel)

WEO Baseline Average Oil Price

2015: $51.6

2016: $50.4

5

Conflicts Are Spreading and Deepening, Putting a Heavy

Toll on the Region and Spilling Across Borders

16 million refugees

and internally

displaced

Afghanistan 3.4

Iraq 2.4

Libya 0.1

Syria 9.6

Yemen 0.3

Refugees account for 25 percent of population in

Lebanon and 20 percent in Jordan

Roadmap

Regional Themes

MENAP Oil Exporters

MENAP Oil Importers

6

7

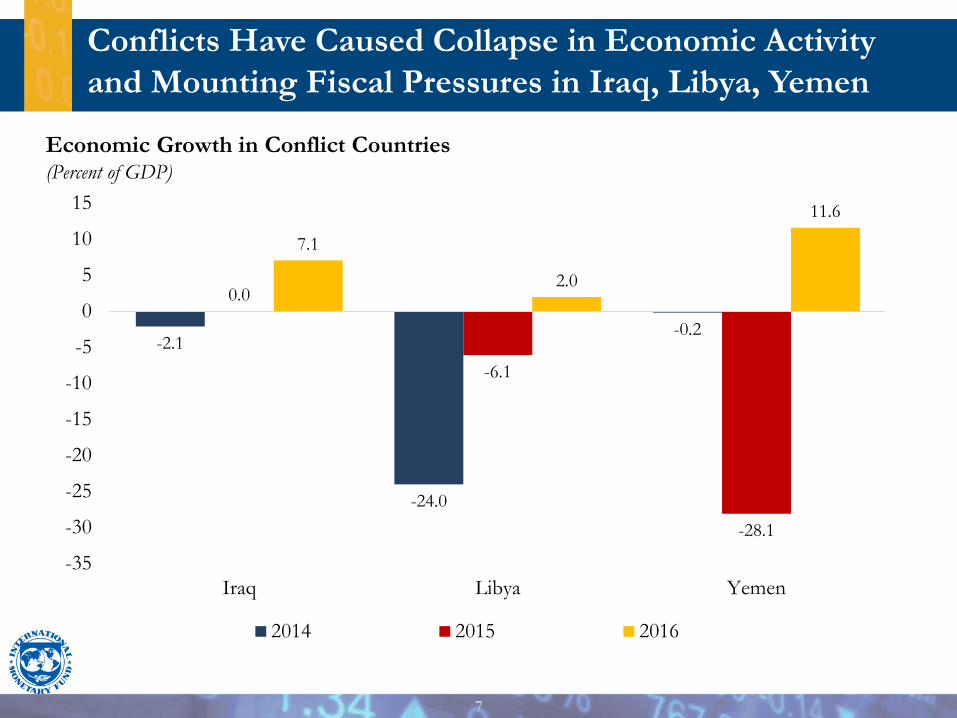

Conflicts Have Caused Collapse in Economic Activity

and Mounting Fiscal Pressures in Iraq, Libya, Yemen

-2.1

-24.0

-0.2

0.0

-6.1

-28.1

7.1

2.0

11.6

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

Iraq Libya Yemen

2014 2015 2016

Economic Growth in Conflict Countries (Percent of GDP)

8

Conflict Countries and Developments in Iran Drive

Changes in Oil Exporters’ Growth

Oil Exporters (Percent)

2.6

1.8

3.8

-1

0

1

2

3

4

5

2014 2015 2016

GCC and Algeria Iran Conflict countries MENAP oil exporters

9

-15

-10

-5

0

5

10

15

2012 2013 2014 2015 2016 2017 2018 2019 2020

GCC

Non-GCC

GCC, October 2014 REO

Non-GCC, October 2014 REO

Fiscal Balance, 2012–20 (Percent of GDP)

Low Oil Prices Lead to Persistent Fiscal Pressures for Oil

Exporters

10

0

5

10

15

20

25

30

0

20

40

60

80

100

120

QAT KWT UAE IRQ IRN OMN ALG SAU BHR

2015 Fiscal breakeven price (LHS) Fiscal buffers (RHS)

Fiscal Buffers and Breakeven Oil Prices, 2015 (Years and U.S. dollars per barrel)

2015

WEO oil price

Dwindling Fiscal Space Underscores Need for Fiscal

Action

Roadmap

Regional Themes

MENAP Oil Exporters

MENAP Oil Importers

11

12

Recovery is Gaining Momentum but Some Countries Still

Lagging

Real GDP Growth (Percent)

EGY PAK

MAR

SDN

TUN LBN

JOR AFG

MRT

DJI

0

1

2

3

4

5

6

7

8

9

0 1 2 3 4 5 6 7 8 9

2015-1

6 A

vera

ge

2010-13 Average

13

Recovery Driven by Improved External Environment

and…

MENAP Oil Importers:

External Gains from Lower Oil Prices (Percent of GDP, 2015–16 average)

-1

0

1

2

3

2013 2014 2015 2016

Euro area

Advanced economies excluding euro area

Advanced Economies:

Real GDP Growth (Percent)

-1

0

1

2

3

4

5

6

7

MRT LBN JOR MAR TUN PAK EGY SDN

Average External Gain

1¼ percent of GDP

14

…Subsidy Reforms Combined With Lower Oil Prices

Creating Space for Growth-Enhancing Spending

Change in Budget Expenditure Components (Percent of GDP)

Capital

Subsidies

Subsidies

-2

-1

0

1

2

3

Change 2010-13 Change 2013-16

Wages Subsidies and transfers Capital expenditures Other expenditures

15

Vulnerabilities Remain Significant Despite Lower Oil

Prices

Public Debt (Percent of GDP)

Remittances, 2014 (Percent of GDP)

0

20

40

60

80

100

120

140

1602010 2015

0

5

10

15

20

Egypt Jordan Lebanon Pakistan

Total From the GCC