metrobank s.a. and subsidiaries...the information used for the present analysis includes the...

TRANSCRIPT

Translation

Equilibrium Calificadora de Riesgo, S.A.

Rating Report

Contact:

Fernando Arroyo

Hernán Regis

(507) 214-3790

The designation .pa reflects risks comparable only in Panama

METROBANK S.A. AND SUBSIDIARIES Panama City, Panama November 24th, 2016

Rating Category Definition of Rating

Entity A-.pa Reflects high capacity to pay principal and interest in the terms and conditions

agreed upon. The ability to pay is more susceptible to possible adverse changes

in the economic conditions than the higher categories.

Outlook (changed)

To Stable from Positive

“This rating is not a suggestion or recommendation to invest, nor an endorsement or guarantee of the issuance or the solvency of the rated entity”

--------------------------Millions of US$-------------------------

Dec.15 Jun.16 Dec.15 Jun.16

Assets: 1,159.9 1,245.0 Income: 12.5 6.3

Liabilities: 1,025.0 1,105.1 ROAA*: 1.1% 1.0% Equity: 134.9 139.9 ROAE*: 10.2% 9.4%

*As of June 30, 2016 the rates are presented annualized.

The information used for the present analysis includes the Metrobank, S.A. and Subsidiaries Audited Financial Statements as of December 31st,

2012, 2013, 2014, and 2015, as well as Unaudited Financial Statements as of June 30th, 2015 and 2016. Additional financial information furnished

by the Bank was also used. The rating is performed pursuant to what is established in Agreements 2-2010 and 6-2010, issued by the Superintendency of Banks of Panama (SBP).

Rationale: Equilibrium's Rating Committee affirms the

A-.pa rating to Metrobank, S.A. and Subsidiaries

(hereinafter, Metrobank or the Bank) after the evaluation

performed. Also, the outlook was changed to Stable from

Positive.

The rating assigned takes into account the sustained

growth of the Bank's earning assets throughout the last

periods evaluated. Likewise, the adequate technological

infrastructure Metrobank presents favorably contributes,

resulting in greater fee income, thus diversifying its

generation sources. The adequate liquidity ratios

maintained by the Bank are equally positive; the same are

reinforced with the available lines the Bank maintains

with first-rate correspondent banks. Additionally, the

performance of its main subsidiary, Financiera Govimar,

turns out favorable, contributing approximately 35% of

the consolidated net profit.

Notwithstanding the above, the decision to modify the

outlook takes into consideration the upward tendency of

the variation percentage of the Bank's delinquency during

the first semester of 2016, compared to previous periods;

even though said delinquency ratios are still below the

average of the National Banking System (NBS). The

above is also associated to the concentration that

Metrobank presents in its loan portfolio -typical of

corporate banking- where the Top 20 debtors represent

27.3% of the portfolio. Metrobank also has the challenge

to diversify its funding sources, where deposits are still

the main financing item of assets (80%), showing

concentration in its Top 20 depositors (22.5%). It is worth

indicating that, compared to the average of General

License banks in Panama, Metrobank presents a higher

funding cost (3.5% versus 2.0%). The contractual

mismatch between assets and liabilities the Bank shows

in the buckets under one year as a result of the

participation of deposits in these terms was also

considered. Notwithstanding the above, it should be noted

that the overall matching is positive and equivalent to

125.3% of capital funds.

Metrobank, which operates under a General License, is a

bank that is focused in the corporate segment, having

started operations in September 1991. Also, it is a wholly

owned subsidiary of Metro Holding Enterprises, Inc., and

in turn has five registered wholly owned subsidiaries,

among which there is Financiera Govimar S.A., which

core business is granting consumer loans mainly to

retirees and customers from the public sector.

As of June 30, 2016, Metrobank's gross loan portfolio

(consolidated) amounts to US$868.5 million, with a

participation of 69.8% of the Bank's total assets.

Compared to 2015, the portfolio shows a 7.1% increase,

both local and foreign, with 5.4% and 14.5% semester

growth, respectively. It is worth highlighting the greater

dynamism in the disbursements towards the foreign

sector; the same registers a 19.8% participation of the

total portfolio as of the analysis cut-off date (7.6% as of

the 2013 closing). It should be noted that the foreign

portfolio is distributed mainly in Guatemala, Mexico,

Ecuador, Trinidad and Tobago, and Costa Rica. Likewise,

in order to face the deceleration of the local economy, the

Bank's Management has the strategy to continue

increasing the disbursements abroad, the same are mainly

destined to companies dedicated to the industrial sector in

the mentioned countries. When analyzing the composition

of the portfolio by economic sector, it can be observed

that even if commercial maintains the first place with a

30.0% participation, the same has been decreasing

consistently throughout the last periods (48.4% as of the

closing of 2014) as a result of the problems in the Colon

Free Zone, which led the Bank to decide diminishing its

Rating History: Entity → BBB.pa (05.30.08), ↑ BBB+.pa

(10.19.09), ↑ A-.pa (10.31.14).

2

exposure in this market. It should be added that the

services and industries sectors are acquiring greater

importance within the Bank's portfolio, reaching

participations of 15.8% and 13.1%, respectively, at the

end of the first semester of 2016. Regarding the portfolio

concentration, the participation of the Top 20 debtors

goes from 22.8% to 27.3% of total gross loans throughout

the last four periods, while the average credit increases

from US$35,219 to US$51,500 in the same time span,

maintaining the growing tendency.

According to what was indicated above, during the first

semester of the period under evaluation, the

nonperforming and past-due balances ratio increases from

0.5% to 1.7%, as a result of the emergence of delays

between 30 and 90 days in some specific loans, in line

with the relative portfolio concentration. It should be

noted that during the first semester the Bank wrote off

US$0.7 million, therefore the real delinquency ratio is

equivalent to 2.2%. The coverage of the past-due and

nonperforming portfolio is 127.7% if we add up the

specific and the dynamic reserve, a level that, even

though it is above the 97.9% coverage observed in the

SBN, the same is below the 452.5% the Bank showed at

the end of 2015. Likewise, when analyzing the portfolio

classification, a decrease in the participation of credits

classified as Pass from 99.1% to 97.2% is observed, due

to the increase of the portfolio classified as Special

Mention from 0.1% to 2.2%. The latter, according to what

was indicated by the Bank's Management, can be

explained due to a requirement of the Superintendency of

Banks of Panama (SBP) to rate the Colon Free Zone

debtors showing profitability problems, without this

necessarily reflecting payment problems for the time

being.

The Bank's investments portfolio remains as the second

greatest earning asset, with a total of US$259.3 million as

of June 30, 2016, with a positive 14.7% variation during

the semester. It should be indicated that 49.9% of the

portfolio consist of local corporate bonds, out of which

33.2% has investment rating equal to or above A- local,

while the remaining balance is not rated. Also, 18.1% and

14.7% of the Bank's investment portfolio is invested in

Sovereign Debt and Treasury Notes issued by the

Government of Panama.

As to funding, deposits remain as the main source of

Metrobank, financing, as of the cut-off date, 79.7% of

total assets (81.2% as of the closing of 2015). Deposits

increased 5.3% during the period analyzed, an evolution

supported mainly by greater local customers' time

deposits. It should be added that out of total deposits,

76.6% corresponds to time deposits, 12.6% to savings

deposits, 9.1% to demand deposits, and 1.7% to interbank

deposits. Likewise, the upward trend in the concentration

in Top deposits is maintained, where the Top 20 support

22.5% of the total (20.7% as of the closing of 2015). On

the other hand, with the objective to migrate towards a

diversification in funding sources, Metrobank increased

borrowings received from third parties by US$40.9

million, which include the structured financing with the

participation of 4 Foreign Banks and Bladex. In this way,

the participation of borrowings within the funding sources

duplicated from 3.1% to 6.2%.

In terms of liquidity, Metrobank maintains adequate

ratios, reflected in a 64.9% Legal Liquidity Ratio, greater

than the 62.0% of 2015 and the 60.2% observed in

average in the NBS. Likewise, the ratio of available funds

over the more volatile deposits (demand and savings

deposits) changed from 168.0% to 174.5% between the

evaluated periods, higher than the 133.3% of the NBS.

However, it should be indicated that the Bank shows

mismatch gaps under contractual scenarios in the terms

under one year, the same represent 97.5% of the Bank's

capital funds, according to what is indicated at the

beginning of this rationale. This condition is partially

mitigated in case an orderly sale of investments was

simulated, that in the first place considers the realization

of titles related to the Government of Panama. In case this

premise is materialized, the 30 days mismatch gap would

represent 30.0% of the capital funds, a moderate

percentage, since the focus of the measuring of the

contractual mismatch is demanding, since the analysis

assumes that the demand and savings deposits are freely

demandable in the short term.

In terms of the Bank's solvency, even though a decrease

of the Capital Adequacy Ratio (CAR) from 15.6% to

14.4% between the periods evaluated is observed, the

ratio is still maintained at a level considered adequate to

sustain the Bank's assets growth. It should be indicated

that the decrease in the CAR is explained by the 9.8%

expansion in risk-weighted assets due to the portfolio

increase and its deterioration, while the capital funds

increased only by 1.1% reaching US$126.4 million.

In the interannual comparative with the first semester of

2015, Metrobank registers a deterioration in its average

profitability ratios on risk-weighted assets (ROARWA),

resulting mainly from the reduction in non-recurring

income, which include: (i) absence of income from sale

of securities, when a gain of US$1.4 million was

generated in the first semester of 2015, and, (ii) the

elimination of income for advisory services and

customers referred from Financiera Govimar that

represented income for US$0.5 million as of June 2015.

The above was partially compensated by: (i) greater

interest earned on loans (+11.6%), allowing a 12.1%

interannual growth in financial income reaching US$32.5

million and, (ii) greater fees earned on loans that

increased from US$1.9 million to US$3.4 million. Thus,

the Bank's net income decreases 10.6% reaching US$6.3

million, with a 19.4% spread (24.4% as of June 2015),

even though it should be stressed out that the greatest

limiting factor to the results is related to the lower

generation of non-recurring income; since the financial

results before reserves1 increased at a greater pace than

the general and administrative expenses (12.0% vs.

5.8%), supporting said consideration.

Finally, Equilibrium will be watching closely the

evolution of Metrobank's portfolio quality, since the same

has been showing impairments resulting in delinquency

levels close to what is observed in the NBS average. This

event is relevant since the loan portfolio is the main

earning asset of the Bank, therefore a greater deterioration

would impact the earning levels. 1 Interest earned – Interest paid + Net fees.

3

Strengths

1. Growth of productive assets generates greater scale and allows the increasing generation of recurring income.

2. Robust technological infrastructure, a factor that has enabled it to generate higher fee income in the last periods.

3. Adequate liquidity ratios, which are complemented by available lines at correspondent banks.

Weaknesses

1. Relative concentration in deposits as liability funding source.

2. Relative concentration in the loan portfolio.

3. Negative contractual position in buckets below 1 year in the maturity matching, albeit the overall matching is positive and

equivalent to 125.3% of capital funds.

Opportunities

1. Technological and service infrastructure that would allow cross-selling.

2. Synergies between the Bank and its subsidiaries’ operations.

3. Gradual increase of geographic loan portfolio diversification.

4. Country’s economy with good medium-term growth projections.

Threats

1. Strong competition in local market exerts pressure on spreads and demands permanent renewal of comparative advantages

that will allow the reduction of interest rate risks.

2. Local and international credit and price variation risks.

3. At the banking sector level, the system as a whole has relative sensitivity in the presence of reputational risk events.

4

CORPORATE DESCRIPTION

Corporate Governance

Metrobank, S.A. and Subsidiaries, is a Panamanian capital

private entity operating in Panama since 1991 under a

General License granted by the Superintendency of Banks

of Panamá (SBP), which allows it to carry out banking

activities that take effect anywhere in the Republic of

Panamá or abroad.

Metrobank is owned 100% by Metro Holding Enterprises,

Inc., which does not have any other investment. In turn,

Metrobank maintains full control of 5 subsidiary

companies, which provide services that complement the

Bank's typical operation.

Metrobank's Economic Group Structure

Source: Metrobank / Prepared by: Equilibrium

Subsidiary Course of Business

Metroleasing, S.A. Leasing of equipment. It began operating

in April 1995.

Eurovalores, S.A

Financial intermediation, securities

brokerage and other related services. It began operating in August 2005.

Financiera Govimar,

S.A.

Personal loans, mainly under the

modality of direct discount. It is a subsidiary since April 2008.

Metrotrust, S.A. Trust Business. It began operating in

May 2013.

Metrofactoring, S.A. Purchase at a discount of invoices issued by third parties. It began operating in

January 2014.

As of the date of this report, the Board of Directors is

composed in the following manner:

Title Name

Director - President Eric Cohen Solis

Director - Vice-President Roy Katz Rabinovich

Director - Treasurer Eduardo Orillac Motta

Director - Secretary Juan Pablo Fábrega Polleri

Director - Deputy Treasurer Ernesto A. Boyd Sasso

Director - Deputy Secretary Orlando López Arosemena

Director Joseph Fidanque W.

Director Ramesh Chatlani

Director Óscar López Arosemena

Director Rafael Bárcenas P.

Director Abraham Assis

Independent Director Paul Smith Alegre

Independent Director Robert Boyd

Alternate Director Enrique Díaz López

Alternate Director Murad Moisés Harari Dabah Source: Metrobank / Prepared by: Equilibrium

The Board of Directors and management promote the

creation of the organization, processes and tools adequate

for the control and transparency of operations. Likewise,

Audit, Assets and Liabilities (ALCO), Risks, Compliance,

Credit, Human Resources, and Top Management

committees meetings are held, which promote the

strengthening of sound governance practices.

Business Strategy

Metrobank fosters a business strategy focused in

conducting financial transactions with, mostly, corporate

profile customers. Moreover, the products and services

offered by the Bank are geared, to a great extent, towards

the Corporate Banking and Private Banking segments,

while Financiera Govimar acts as the Consumer Banking

area, which constitutes a complement to the above-

mentioned strategy.

It should be noted that Metrobank has expanded its

operational infrastructure during the last years, which led to

greater asset volumes and income received, without

incurring in significant changes in the strategic focus. Bank

has made efforts to continue strengthening its lines of

business and stimulating products cross-selling, also

integrating services based on technology, in order to further

enhance its competitive advantages into the future.

One of the aspects that favor the Bank's operation is its

technological infrastructure, considered robust from the

point of view of controls, effectiveness, management

information, customer service and development of

products/services that generate fees and other income. Of

special interest, Metrobank has formalized relationships

with multiple prestigious companies nationwide, through

the offer of merchant acquisition and the Mobile Cash

services, which show a growing trend in recent years.

Regarding the administration of subsidiaries, Management

arranged for the homologation of Financiera Govimar to

the Bank with respect to: controls, processes, procedures

and policies, with the objective to integrate this subsidiary

at the operational (as the Consumer area of the Entity) and

corporate governance levels. In this way, Govimar remains

focused on granting personal loans using direct discount to

retirees and public sector officers or employees, thus, in

this sense, the strategy has remained consistent. On the

other hand, albeit the Eurovalores business holds a smaller

market share than other stock brokerage firms operating in

the local market, this company has shown a gradual growth

during the last years in terms of assets under administration

and traded transactions volume.

It should be noted that Financiera Govimar is the main

subsidiary of Metrobank, contributing 35.3% of the

consolidated net income as of June 30, 2016 (27.2% as of

June 30, 2015). Financiera Govimar's net income amounts

to US$2.2 million as of June 30, 2016, showing a 15.8%

interannual growth mainly as a result of greater loan fees

income and lower reserves expenses. It is important to

indicate that Govimar's gross loan portfolio was US$71.1

million as of June 30, 2016, with a 2.2% past-due and non-

performing ratio (US$68.7 million and 2.4% as of June 30,

2015, respectively).

5

65.9% 65.3%56.9%

68.6% 63.2%52.3%

30.1% 32.4%

32.8%

27.2%31.6%

35.3%

4.0% 2.3%10.4%

4.2% 5.2%12.4%

2012 2013 2014 Jun.15 2015 Jun.16

Contribution to Net Profit by Subsidiary

Other Subsidiaries

Govimar

Metrobank

Source: Metrobank / Prepared by: Equilibrium

ECONOMIC ANALYSIS

International Environment

In general, the main events happening in the world

economic sphere in recent periods define a mixed picture

for the different countries and regions during 2016.

In the first place, an economic recovery has been observed

in the United States (main trade partner of Latin America)

and a subsequent strengthening of the American Dollar.

The preceding, together with better expectations in the

unemployment and inflation on the part of the United

States, caused the Federal Reserve (FED) to increase

interest rates in December 2015 up to 0.50% from 0.25%.

FED does not expect to increase rates in the short-term,

although it does not rule out to increase interest rates in the

mid- and long-terms.

In contrast, should this scenario materialize, the outlook of

emerging countries worldwide could become more

aggravated, especially regarding the continuity in the

devaluation of their respective currencies, the rising cost of

their debt contracted in Dollars, and possible more

restrictive policies regarding their fiscal policies, all of

which would have repercussions in the payment capacity of

persons and companies located in said countries.

On the other hand, there are other unfavorable factors such

as the pressure suffered by commodities prices, the marked

downward trend experienced by oil prices and other

commodities, as well as the divergence in the application

of monetary policies applied by some advanced economies,

especially in the Euro Zone. Added to this, the exit of Great

Britain from the European Union during June resulted in

even more political and monetary uncertainty to the Old

Continent, added to the fact that the markets have reacted

adversely to said event.

Not less important are the adverse collateral effects on the

Latin-American emerging economies, such as smaller

growth of the primary and secondary sectors (especially

due to the ability to export goods and commodities), a

smaller leeway for Governments to face their fiscal

deficits, as well as greater restrictions for public and

private investment, especially in those economies that, in

addition, experience political imbalances. In particular, the

International Monetary Fund (IMF) has calculated that the

drop in commodities has fluctuated between 30% and 50%

depending on the country, which has had an impact in the

export volume income, especially in South American

countries.

Very much in line with the above, China continues

showing a deceleration in its economic growth; at the same

time that it also decreased its goods import and export

volumes during el 2015. Since China is currently the

second biggest trade partner of Latin America and an

important investment source for the region, it should be

mentioned that these elements influence, to a great extent,

the behavior of emerging countries. As long as a

weakening of the Chinese economy (together with the

Yuan) continues, it is probable that the Latin American

countries will need to diversify in order to adapt to this

environment.

For the time being, the IMF has projected a 3.2% growth of

the worldwide Gross Domestic Product (GDP) during 2016

(compared to the 3.1% during 2015), observing stable

growths in the Euro Zone, the United States, and other

advance economies; while, on the other hand, global

growth for Latin America would be -0.5%, mainly due to

the strong economic recession that Brazil is undergoing.

According to this international organization, the worldwide

economic growth would show a moderate trend again

starting in 2017, once the conditions of emergent

economies are normalized, together with more favorable

macroeconomic conditions regarding commodities.

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2010 2011 2012 2013 2014 2015 2016 (P) 2017 (P) 2018 (P)

Comparative GDP Annual Growth

United States China Euro Zone Brazil Latin America and The Caribbean World

Source: International Monetary Fund / Prepared by: Equilibrium

A positive aspect is that Brazil started to recover

economically and politically beginning in the second half

of 2016. Thus, it is expected that the Brazilian and Latin

American economic growth in general recover more

quickly that what was initially estimated. Also, investors

may experience partial relief in their fixed-rate securities

portfolios related to the Brazilian country.

Local Economy

The Panamanian economy is set to be the most dynamic

among the main Latin American countries, since its real

GDP growth result was 5.8% for 2015, above the figures

submitted by other countries from the region, including

those with international investment grade, even with the

real GDP showing a slight deceleration when compared to

previous years’ growth.

The sectors that have been the top contributors to this

dynamism were construction, commercial activity,

financial intermediation, real estate and rental activities, as

well as transportation, warehousing, and communications;

as has been during the last years, based on the national

6

macroeconomic model oriented towards the tertiary sector,

namely, Services.

According to the figures presented by the General

Comptroller's Office of the Republic, the real GDP growth

was 4.9% for the first semester of 2016, which could

indicate a growth below what was initially projected, albeit

it should be taken into account that it did not include the

recent opening of the Expanded Canal (inaugurated on

June 26, 2016), that may increase the economic activity

level within the national territory for the rest of the year.

Additionally, important infrastructure works are planned,

among which we have the construction of Line 2 of the

Subway (Metro), the expansion of the Tocumen

International Airport, the construction of new ports and

logistics parks, the expansion of the electrical transmission

infrastructure, among other future megaprojects; where the

construction of a fourth bridge over the Panama Canal,

together with the construction of a third line of the Subway

(Metro), are already contemplated for the end of the

present decade.

On the other hand, the Economy and Finance Ministry

(MEF, per its acronym in Spanish) has revealed that,

according to preliminary figures, the accumulated fiscal

deficit for 2015 represents 2.0% of the nominal GDP,

meaning an improvement in relation to the 3.4% seen the

previous year. The Government has made efforts to reduce

the weight of expenses from subsidies and encourage an

increase in taxpaying, and consequently the fiscal deficit

represented 0.2% of the nominal GDP as of the closing of

the first quarter of 2016, which is consistent with the 1.5%

limit set forth by the Social Fiscal Responsibility Law

(LRSF, per its acronym in Spanish).

An important aspect revolves around LRSF, since the

Government has promulgated amends with the intention of

maintaining a maximum deficit level for the different

periods. This deficit may be adjusted depending on the

contribution from income generated by the Panama Canal

to the nominal GDP. That is why the Panama Canal

Expansion has been a transcendental event for the country,

since with it there would also be an increase in the

contribution of the interoceanic way to almost 45% starting

in 2017, as well as a 40% increase in investments aimed at

the logistics sector in said period, according to the MEF

estimates.

In this context, the main challenge of the local economy is

centered in the public finance management and the

execution of the budget on the part of the current

Government Administration, without compromising the

public debt or the fiscal deficit, thus revenues collection, a

controlled indebtness, and an efficient use of public

expenses would allow maintaining Panama's soundness as

a country.

RISK MANAGEMENT

The Bank's Risks area is led by a Comprehensive Risks

Assistant Vice-President, which is supported by the differ-

ent units for each one of the different types of risk. At the

corporate governance level, the Bank holds Risk Commit-

tees every month, where eight directors participate in order

to maintain the Board of Directors informed about the

capacity of the Bank to face the different risks it could be

exposed to. Also, a Risks Committee corresponding to

Financiera Govimar is held with a bimonthly frequency. In

addition, the risks management carried out by the Entity is

focused in ensuring adherence to policies and parameters

defined by the Board of Directors by Management at all

times, in order to control risk exposures regarding net

stockholders' equity.

The Bank also has a Corporate Governance and Compli-

ance Vice-President as part of the strategies to strengthen

Metrobank's risk management and control framework and

work under the CRC (Corporate Governance, Risk, Com-

pliance) structure.

Credit Risk

The main evaluation criterion for this type of risk consists

of the exposure of the loan portfolio on the Bank's total

credit and on the net stockholders' equity. Therefore,

Metrobank analyzes the behavior of credit balances

according to product type, debtor economic activity,

geographic sector, among other criteria. Of particular

interest, the Board of Directors assigns global limits for

each country where it wants to participate, thus the Bank

places special emphasis on complying with said exposure

limits not only at loans' level, but also at the interbank

placings and financial investments, as a whole. The

countries chosen by the Board of Directors must meet a

series of requirements, with the main one being holding a

sovereign investment grade rating.

Additionally, the Bank monitors the concentration degree

exercised by its main economic groups, including their

credit balance and the different types of tangible collateral

supporting said facilities. The behavior of credit exposure

with related parties is also observed.

The risks area also monitors the Bank's nonperforming,

past-due and restructured loans, where measures to be

taken are evaluated for each one, as the case may be. This

includes assignment of specific reserves according to the

loans classified pursuant to Agreement 04-2013, review of

collaterals, and legal procedures to take on, in case the

need exists.

The Bank has implemented an internal scoring system for

the Corporate Banking loan portfolio, which objective is to

assign an internal rating based on specific qualitative and

quantitative criteria, according to its risk profile. This is

particularly useful when submitting credit proposals to the

different committees, as well as when following up the

credit behavior of each debtor.

It is worth mentioning that the Bank exercises a periodic

monitoring of the customers' files, both at the Head Office

and branches levels, as a quality control measure.

Market Risk

Market risk in Metrobank is focused in its investments

portfolio. Therefore, the Assistant Vice-President monitors

specific variables of the portfolio, such as average yield,

type of instrument, type of industry of the issuer, risk

rating, average duration, participation of investments on

total credits, proportion of securities issued abroad,

7

unrealized gain/loss amount, among other. Albeit foreign

securities (outside of Latin America) are managed by an

external custodian, the Bank monitors its positions in these

securities in the same manner as its local investments.

As an additional point, the Bank also oversees the

evolution of the VaR and CVaR (Conditional Value at

Risk), so that the maximum loss limits allowed regarding

net stockholders' equity are complied with.

Liquidity Risk

The risks area has prepared procedures for the activation of

the Contingency Plan, which has several levels depending

on the need for liquidity at a given time. The use of repos,

lines of credit, and the renewal of bank borrowings from

banks would be contemplated in case the legal liquidity

rate approaches the regulatory limit.

At the same time, the Board of Directors is kept informed

about the evolution of the concentration degree of Top

depositors, including the different types of deposits they

have in the Bank and those that are pledged as collateral of

the loan portfolio.

The Bank conducts a periodic review of liquidity levels it

maintains in the balance sheet, including the average legal

liquidity ratios (regulatory) and the immediate liquidity

ratio, which is an internal measure of the institution that

takes into consideration a more stringent deposits base.

This analysis is complemented through the monthly

monitoring of the liquidity matching position under

contractual and under renewal statistics scenarios, in turn

supported by overseeing the renewal percentages of time

deposits and the volatility ratios of the different types of

financial liabilities.

Operational Risk

The Assistant Vice-President has homologated the

incidents reporting system for both Metrobank and

Financiera Govimar, in order to monitor the operational

risk of both entities simultaneously.

The Entity has a software through which each area reports

operational risks events, in order to duly follow-up

afterwards with the help of a preventive actions matrix.

As part of its main objectives, the operational risks area has

been able to evaluate all the risks inherent to the identified

processes. The Bank presents its Board of Directors a

summary of these processes by credit product or

management area, as they are updated in the risk matrix.

This way, a constant update of the corresponding risk

matrixes is maintained, so that the areas owning the

processes, implement measures to control the possible risks

observed, supervised by the Comprehensive Risks area.

After considering the controls applied to the inherent

losses, the Bank obtains a residual loss figure, which is

compared to the limit assigned by the Board of Directors.

This allows showing a refined analysis of the main areas or

processes that should be reinforced, in order to reduce

future residual losses.

Metrobank continues developing the Business Impact

Analyses (BIA) for each one of the Bank's processes with

the objective to continue reinforcing its current Business

Continuity Plan to ensure operability in case of

technological failures or external events.

REGULATORY ASPECTS

Regulatory Framework for Capital Adequacy

On February 03 of 2015, the SBP issued Agreement 01-

2015, which sets forth new requirements for the

categorization of the capital funds computable for the

calculation of the Capital Adequacy Ratio (CAR). This

Agreement is applicable to the official banks, a General

License Banks, all International License Banks where the

SBP is the home country supervisor and to all the owners

of bank stock of banking groups that consolidate in

Panama and that the SBP is the home country supervisor.

The Agreement requires compliance with minimum

percentages of adequacy, according to the classification of

capital funds parameters. The components of each one of

the types of capital accepted by the regulation: ordinary

Tier 1 capital, additional Tier 1 capital, and Tier 2 capital

will be determined.

The minimum percentage of Capital Adequacy will

continue being 8%, as it is required under Agreement 05-

2008. However, the new Agreement establishes limits for

the Tier 1 capital, which will increase gradually, until the

adequation periods have elapsed.

The ordinary Tier 1 capital will consist of common shares,

retained and current period earnings, regulatory reserves,

and other elements included in the Agreement. The

calculation of Tier 1 capital according to the new

Agreement deducts Goodwill, in addition to other items or

regulatory adjustments that are not taken into account in

the current regulation. For example, the following are

mentioned:

Accumulated and current

period losses Other intangible assets

Shareholdings greater than

10% in the stockholders'

equity of financial entities

that do not consolidate to in

the Bank

Shareholdings in non-

financial entities included in

the financial consolidation

(greater than 10%)

Unrealized losses on

securities available for sale

Other adjustments

contemplated in the

Agreement

It is worth mentioning that retained and current period

earnings must be validated by the external auditors, in

order to ensure the deduction of every possible,

foreseeable expense, interest, or dividend from said profits.

After applying the corresponding regulatory adjustments,

the resulting ordinary Tier 1 capital must be greater than

4.5% of risk-weighted assets as of January 01, 2019, at the

same time that the total Tier 1 capital must be, as a

minimum, 6% on that date. The SBP will grant an

adequation period to the norm according to the following

table, in which the requirement dates are indicated, starting

July 01, 2016:

8

Type of

capital 07/01/16 07/01/17 01/01/18 01/01/19

Ordinary Tier 1 Capital

3.75% 4.00% 4.25% 4.50%

Total Tier 1

Capital 5.25% 5.50% 5.75% 6.00%

Total capital 8.00% 8.00% 8.00% 8.00%

Source: Superintendency of Banks of Panama

The additional Tier 1 capital will consist of equity

instruments with certain characteristics, among which the

non-cumulative preferred stock, without early redemption

clauses, perpetual, among other characteristics, will be

contemplated. The Bank can comply with the total Tier 1

capital requirement using these instruments, as long as it

complies with the ordinary Tier 1 capital percentage.

On the other hand, Tier 2 capital will continue consisting

of the subordinated bonds or other hybrid capital

instruments that do not meet the characteristics to be

considered additional Tier 1 capital. The Bank can reach

the minimum 8% adequacy using these instruments, as

long as it complies with the total Tier 1 capital levels

required.

The aforementioned will also apply for all the banks that

are subsidiaries of regulated banks, which home country

supervisor is the SBP. That is, the Bank not only has to

comply with the percentages on a consolidated basis, but

also individually, including all the banks that are a part of

the economic group.

The new Agreement will also establish compliance with a

Leverage Coefficient, which is calculated dividing the

ordinary Tier 1 capital by the sum of on- and off-balance

sheet non-weighted assets established by the SBP. The

minimum of this coefficient will be 3.00%. It should be

indicated that, according to information furnished by

Metrobank, the CAR would change from 14.4% to 14.1%

according to the partial parameters to be applied for the

new agreement as of the analysis cut-off.

FINANCIAL PERFORMANCE

METROBANK, S.A. AND SUBSIDIARIES

Assets and Credit Quality

Metrobank's consolidated assets as of June 30, 2016

amount to US$1,245.0 million, 7.3% higher than what it

showed as of the closing of 2015. The assets' growth is

associated to the expansion of the loan portfolio and the

increase in the investments portfolio balance. It should be

added that, interannually, both items mentioned also

support the 11.2% growth of total assets, thus Metrobank

registers a 12.5% average annual growth of assets during

the last four analyzed periods.

11.5% 12.4% 11.4% 10.0% 10.6% 9.3%

17.3% 17.7% 20.6% 20.7% 19.5% 20.8%

67.4% 66.8% 64.7% 66.1% 67.1% 67.2%

3.7% 3.2% 3.3% 3.2% 2.8% 2.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 Jun.15 2015 Jun.16

Assets Evolution and Composition

Other

Loans

Investments

Cash and duefrom banks

AssetsAnnualGrowth %

Source: Metrobank and SBP / Prepared by: Equilibrium

Regarding Metrobank's gross loans portfolio, it totals

US$868.5 millions, after a 7.1% expansion compared to the

balance registered as of the closing of 2015. Said growth

occurs both in the local and foreign portfolio, with 5.4%

and 14.5% increases, respectively. The greater dynamism

shown by the disbursements towards the foreign sector

should be highlighted, mainly in Central America,

throughout the last years evaluated, a situation that is also

associated to the Bank's strategy to face the deceleration of

the local economy. In this sense, the participation of

foreign loans reaches 19.8% as of June 30, 2016, from the

18.5% and 15.2% registered as of the closing of December

and June of 2015, respectively.

536.1 607.5 633.2 657.2 660.6 696.5

33.1 49.894.7 117.8 150.2

172.0

Dec.12 Dec.13 Dec.14 Jun.15 Dec.15 Jun.16

Evolution of the Loan Portfolio (in millions of USD)

Local credits Foreign credits

Source: Metrobank / Prepared by: Equilibrium

It should be indicated that the disbursements abroad are

distributed mainly in Guatemala (3.4%), Mexico (3.2%),

Ecuador (1.6%), Trinidad and Tobago (1.5%), and Costa

Rica (1.5%).

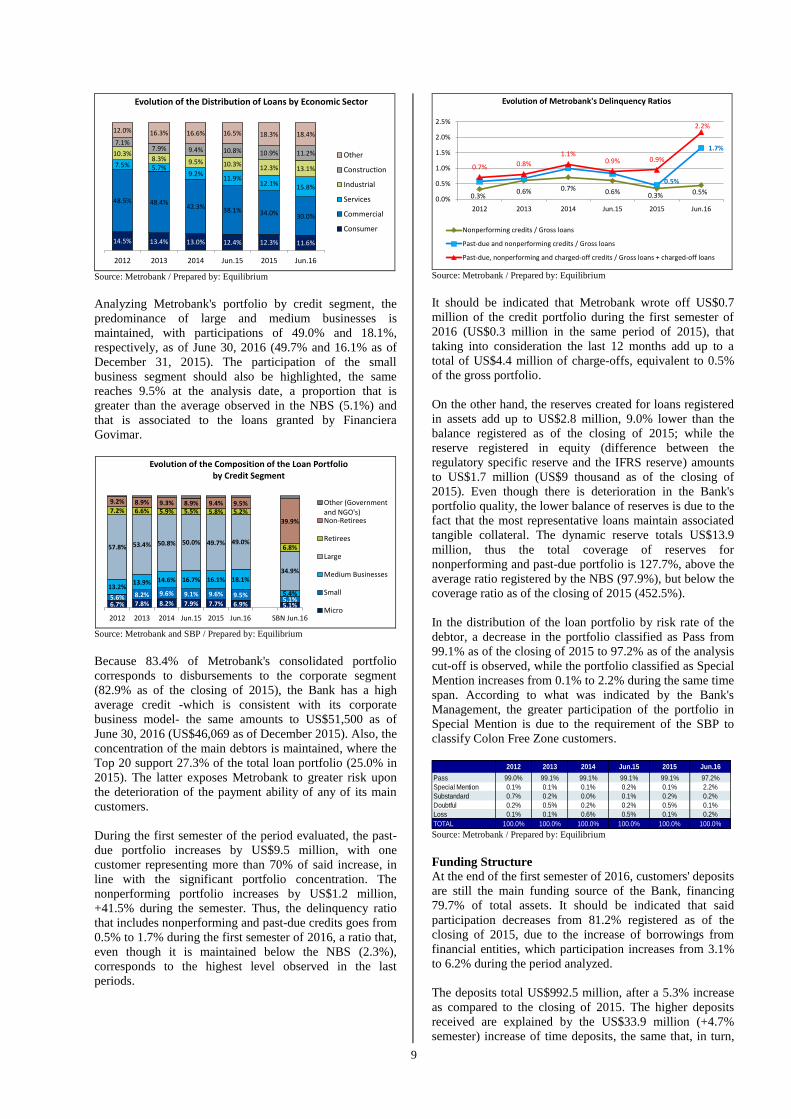

When analyzing the composition of the portfolio by

economic sector, the commercial sector remains in the first

position with 30.0%; however, its participation has

decreased gradually throughout the last periods evaluated,

as a result of greater dynamism in the disbursements to

other economic sectors and less financing of Colon Free

Zone companies. The sectors showing greater activity

within Metrobank's portfolio are services, industrial and

construction. It should be indicated that during the

evaluated semester the sector with greater growth was

services, since the disbursements increased by 39.1%,

placing it in second place in the portfolio composition with

a 15.8% participation.

9

14.5% 13.4% 13.0% 12.4% 12.3% 11.6%

48.5% 48.4%42.3% 38.1% 34.0% 30.0%

7.5% 5.7%9.2%

11.9%12.1% 15.8%

10.3%8.3% 9.5% 10.3%

12.3% 13.1%

7.1%7.9% 9.4% 10.8% 10.9% 11.2%

12.0% 16.3% 16.6% 16.5% 18.3% 18.4%

2012 2013 2014 Jun.15 2015 Jun.16

Evolution of the Distribution of Loans by Economic Sector

Other

Construction

Industrial

Services

Commercial

Consumer

Source: Metrobank / Prepared by: Equilibrium

Analyzing Metrobank's portfolio by credit segment, the

predominance of large and medium businesses is

maintained, with participations of 49.0% and 18.1%,

respectively, as of June 30, 2016 (49.7% and 16.1% as of

December 31, 2015). The participation of the small

business segment should also be highlighted, the same

reaches 9.5% at the analysis date, a proportion that is

greater than the average observed in the NBS (5.1%) and

that is associated to the loans granted by Financiera

Govimar.

6.7% 7.8% 8.2% 7.9% 7.7% 6.9% 5.1%5.6% 8.2% 9.6% 9.1% 9.6% 9.5%

5.1%

13.2%13.9% 14.6% 16.7% 16.1% 18.1%

5.4%

57.8% 53.4% 50.8% 50.0% 49.7% 49.0%

34.9%

7.2% 6.6% 5.9% 5.5% 5.8% 5.2%

6.8%

9.2% 8.9% 9.3% 8.9% 9.4% 9.5%

39.9%

2012 2013 2014 Jun.15 2015 Jun.16 SBN Jun.16

Evolution of the Composition of the Loan Portfolioby Credit Segment

Other (Governmentand NGO's)Non-Retirees

Retirees

Large

Medium Businesses

Small

Micro

Source: Metrobank and SBP / Prepared by: Equilibrium

Because 83.4% of Metrobank's consolidated portfolio

corresponds to disbursements to the corporate segment

(82.9% as of the closing of 2015), the Bank has a high

average credit -which is consistent with its corporate

business model- the same amounts to US$51,500 as of

June 30, 2016 (US$46,069 as of December 2015). Also, the

concentration of the main debtors is maintained, where the

Top 20 support 27.3% of the total loan portfolio (25.0% in

2015). The latter exposes Metrobank to greater risk upon

the deterioration of the payment ability of any of its main

customers.

During the first semester of the period evaluated, the past-

due portfolio increases by US$9.5 million, with one

customer representing more than 70% of said increase, in

line with the significant portfolio concentration. The

nonperforming portfolio increases by US$1.2 million,

+41.5% during the semester. Thus, the delinquency ratio

that includes nonperforming and past-due credits goes from

0.5% to 1.7% during the first semester of 2016, a ratio that,

even though it is maintained below the NBS (2.3%),

corresponds to the highest level observed in the last

periods.

0.3%0.6% 0.7% 0.6% 0.3% 0.5%

0.5%

1.7%

0.7% 0.8%

1.1%0.9% 0.9%

2.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2012 2013 2014 Jun.15 2015 Jun.16

Evolution of Metrobank's Delinquency Ratios

Nonperforming credits / Gross loans

Past-due and nonperforming credits / Gross loans

Past-due, nonperforming and charged-off credits / Gross loans + charged-off loans

Source: Metrobank / Prepared by: Equilibrium

It should be indicated that Metrobank wrote off US$0.7

million of the credit portfolio during the first semester of

2016 (US$0.3 million in the same period of 2015), that

taking into consideration the last 12 months add up to a

total of US$4.4 million of charge-offs, equivalent to 0.5%

of the gross portfolio.

On the other hand, the reserves created for loans registered

in assets add up to US$2.8 million, 9.0% lower than the

balance registered as of the closing of 2015; while the

reserve registered in equity (difference between the

regulatory specific reserve and the IFRS reserve) amounts

to US$1.7 million (US$9 thousand as of the closing of

2015). Even though there is deterioration in the Bank's

portfolio quality, the lower balance of reserves is due to the

fact that the most representative loans maintain associated

tangible collateral. The dynamic reserve totals US$13.9

million, thus the total coverage of reserves for

nonperforming and past-due portfolio is 127.7%, above the

average ratio registered by the NBS (97.9%), but below the

coverage ratio as of the closing of 2015 (452.5%).

In the distribution of the loan portfolio by risk rate of the

debtor, a decrease in the portfolio classified as Pass from

99.1% as of the closing of 2015 to 97.2% as of the analysis

cut-off is observed, while the portfolio classified as Special

Mention increases from 0.1% to 2.2% during the same time

span. According to what was indicated by the Bank's

Management, the greater participation of the portfolio in

Special Mention is due to the requirement of the SBP to

classify Colon Free Zone customers.

2012 2013 2014 Jun.15 2015 Jun.16

Pass 99.0% 99.1% 99.1% 99.1% 99.1% 97.2%

Special Mention 0.1% 0.1% 0.1% 0.2% 0.1% 2.2%

Substandard 0.7% 0.2% 0.0% 0.1% 0.2% 0.2%

Doubtful 0.2% 0.5% 0.2% 0.2% 0.5% 0.1%

Loss 0.1% 0.1% 0.6% 0.5% 0.1% 0.2%

TOTAL 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% Source: Metrobank / Prepared by: Equilibrium

Funding Structure

At the end of the first semester of 2016, customers' deposits

are still the main funding source of the Bank, financing

79.7% of total assets. It should be indicated that said

participation decreases from 81.2% registered as of the

closing of 2015, due to the increase of borrowings from

financial entities, which participation increases from 3.1%

to 6.2% during the period analyzed.

The deposits total US$992.5 million, after a 5.3% increase

as compared to the closing of 2015. The higher deposits

received are explained by the US$33.9 million (+4.7%

semester) increase of time deposits, the same that, in turn,

10

represent 76.6% of the total takings of Metrobank. It

should be indicated that the increase of times deposits is

due mainly to local deposits, that represent 91.1% of the

total of this type of funding. Savings deposits advanced

5.3%, with a 12.6% participation of total deposits; while

demand deposits represent 9.1% of total deposits after

registering a 1.5% semester increase.

83.6 89.2 113.9 99.8 89.2 90.588.6 101.0

124.8 123.1 118.4 124.7

434.1540.6

636.2705.3

726.4 760.3

0%

5%

10%

15%

20%

25%

30%

0

200

400

600

800

1000

1200

2012 2013 2014 Jun.15 2015 Jun.16

Mill

on

s o

f U

S$

Evolution of Deposits

Interbank timedeposits

Customers'time deposits

Savingsdeposits

Demanddepostis

Total DepositsAnnualVariation %

Source: Metrobank and SBP / Prepared by: Equilibrium

On the other hand, the upward trend in the concentration of

Metrobank's Top depositors observed since 2014 is

maintained. In this sense, the Top 10 depositors represent

14.0% of total deposits, while the Top 20 represent 22.5%

of total takings as of the analysis cut-off date (12.5% and

20.7%, respectively, as of December 31, 2015). It should

be indicated that depositors concentration risk is partially

mitigated by the high renewal ratio of time deposits, with

81% at the evaluated date.

12.6%11.5% 11.0%

12.3% 12.5%14.0%

20.0%18.9% 18.1%

20.1% 20.7%22.5%

2012 2013 2014 Jun.15 2015 Jun.16

Evolution of the Concentration of Top Depositors

Top 10

Top 20

Source: Metrobank / Prepared by: Equilibrium

Regarding obligations with third parties, these increase

US$40.9 million during the first six months of the current

period, totaling US$77.4 million. The increase is due

mainly to a line taken with Bladex for US$40.0 million

(US$10.0 million as of the closing of 2015), the same that

expires in May 2019.

It should be indicated that Metrobank maintains repo lines

for US$15.0 million (US$27.5 million as of December 31,

2015), which expire in August 2016, which are secured

with securities available for sale registered in the Bank's

investments portfolio for US$21.0 million.

80.5% 81.4% 83.8% 84.4% 81.2% 79.7%

9.2% 10.3% 10.1% 9.9% 11.6% 11.2%

2012 2013 2014 Jun.15 2015 Jun.16

Evolution of Funding Sources

Other

Equity

Securities sold underrepurchase agreements

Borrowings

Deposits

Source: Metrobank and SBP / Prepared by: Equilibrium

Stockholders' equity remains in the second place in the

Bank's funding sources, with a 11.2% participation

equivalent to of total assets as of the analysis cut-off

(11.6% as of December 2015). Said item shows a 3.7%

increase in relation to the closing of the previous period,

due to the US$7.4 million increase of retained earnings.

Liquidity and Maturity Matching

As of June 30, 2016, Metrobank's available funds amount

to US$375.5 million, registering a 7.7% variation during

the first six months of the current period. Said evolution is

explained by the 14.7% expansion of the investments

portfolio, item that represents 69.1% of the Bank's total

funds available. Demand deposits due from banks represent

25.0% of total funds available, which dropped 4.6% when

compared to the closing of the previous period.

The increase of funds available at a faster rhythm than

deposits allowed that the coverage of the first on demand

and savings takings increase from 168.0% to 174.5%

during the evaluated period, a ratio above the 133.3%

observed in the NBS average. Also, if the coverage was

measured on total deposits, the ratio improves from 37.0%

to 37.8%; however, it still remains behind the 45.6%

observed in the NBS.

Metrobank's average Legal Liquidity Ratio was 64.9% as

of June 30, 2016 (62.0% as of December 31, 2015),

remaining higher than the average NBS (60.2%) ratio, a

situation associated with the funding type used by the

Bank.

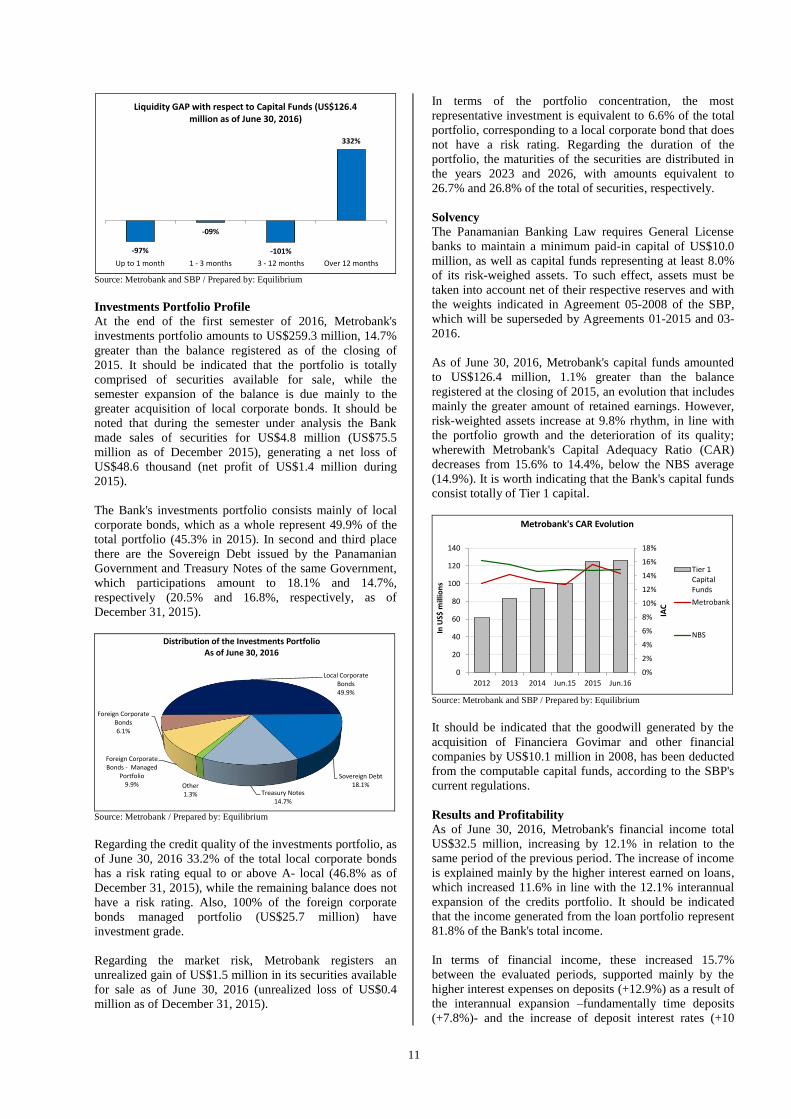

Regarding the liquidity contractual matching, at the end of

the first semester of 2016 Metrobank presents a deficit

position in all the buckets under one year, originated by the

maturity of deposits. In this sense, in the bucket under 30

days the deficit position is equivalent to 97.5% of capital

funds, while for the buckets from 01 to 03 months and

from 03 to 12 months, the mismatch is equivalent to 8.9%

and 100.6% of capital funds, respectively. On the other

hand, in the bucket over one year, the position is a surplus

and equivalent to 332.3% of the total capital funds, the

same is explained by the participation in the maturities of

the securities portfolio and of the loans portfolio in said

bucket. It should be noted that on an aggregate basis

Metrobank's contractual matching is positive and

equivalent to 125.3% of the total of capital funds.

11

-97%

-09%

-101%

332%

Up to 1 month 1 - 3 months 3 - 12 months Over 12 months

Liquidity GAP with respect to Capital Funds (US$126.4 million as of June 30, 2016)

Source: Metrobank and SBP / Prepared by: Equilibrium

Investments Portfolio Profile

At the end of the first semester of 2016, Metrobank's

investments portfolio amounts to US$259.3 million, 14.7%

greater than the balance registered as of the closing of

2015. It should be indicated that the portfolio is totally

comprised of securities available for sale, while the

semester expansion of the balance is due mainly to the

greater acquisition of local corporate bonds. It should be

noted that during the semester under analysis the Bank

made sales of securities for US$4.8 million (US$75.5

million as of December 2015), generating a net loss of

US$48.6 thousand (net profit of US$1.4 million during

2015).

The Bank's investments portfolio consists mainly of local

corporate bonds, which as a whole represent 49.9% of the

total portfolio (45.3% in 2015). In second and third place

there are the Sovereign Debt issued by the Panamanian

Government and Treasury Notes of the same Government,

which participations amount to 18.1% and 14.7%,

respectively (20.5% and 16.8%, respectively, as of

December 31, 2015).

Foreign Corporate Bonds - Managed

Portfolio9.9%

Foreign Corporate Bonds6.1%

Local Corporate Bonds49.9%

Sovereign Debt18.1%

Treasury Notes14.7%

Other1.3%

Distribution of the Investments Portfolio As of June 30, 2016

Source: Metrobank / Prepared by: Equilibrium

Regarding the credit quality of the investments portfolio, as

of June 30, 2016 33.2% of the total local corporate bonds

has a risk rating equal to or above A- local (46.8% as of

December 31, 2015), while the remaining balance does not

have a risk rating. Also, 100% of the foreign corporate

bonds managed portfolio (US$25.7 million) have

investment grade.

Regarding the market risk, Metrobank registers an

unrealized gain of US$1.5 million in its securities available

for sale as of June 30, 2016 (unrealized loss of US$0.4

million as of December 31, 2015).

In terms of the portfolio concentration, the most

representative investment is equivalent to 6.6% of the total

portfolio, corresponding to a local corporate bond that does

not have a risk rating. Regarding the duration of the

portfolio, the maturities of the securities are distributed in

the years 2023 and 2026, with amounts equivalent to

26.7% and 26.8% of the total of securities, respectively.

Solvency

The Panamanian Banking Law requires General License

banks to maintain a minimum paid-in capital of US$10.0

million, as well as capital funds representing at least 8.0%

of its risk-weighed assets. To such effect, assets must be

taken into account net of their respective reserves and with

the weights indicated in Agreement 05-2008 of the SBP,

which will be superseded by Agreements 01-2015 and 03-

2016.

As of June 30, 2016, Metrobank's capital funds amounted

to US$126.4 million, 1.1% greater than the balance

registered at the closing of 2015, an evolution that includes

mainly the greater amount of retained earnings. However,

risk-weighted assets increase at 9.8% rhythm, in line with

the portfolio growth and the deterioration of its quality;

wherewith Metrobank's Capital Adequacy Ratio (CAR)

decreases from 15.6% to 14.4%, below the NBS average

(14.9%). It is worth indicating that the Bank's capital funds

consist totally of Tier 1 capital.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

20

40

60

80

100

120

140

2012 2013 2014 Jun.15 2015 Jun.16

IAC

In U

S$ m

illio

ns

Metrobank's CAR Evolution

Tier 1CapitalFunds

Metrobank

NBS

Source: Metrobank and SBP / Prepared by: Equilibrium

It should be indicated that the goodwill generated by the

acquisition of Financiera Govimar and other financial

companies by US$10.1 million in 2008, has been deducted

from the computable capital funds, according to the SBP's

current regulations.

Results and Profitability

As of June 30, 2016, Metrobank's financial income total

US$32.5 million, increasing by 12.1% in relation to the

same period of the previous period. The increase of income

is explained mainly by the higher interest earned on loans,

which increased 11.6% in line with the 12.1% interannual

expansion of the credits portfolio. It should be indicated

that the income generated from the loan portfolio represent

81.8% of the Bank's total income.

In terms of financial income, these increased 15.7%

between the evaluated periods, supported mainly by the

higher interest expenses on deposits (+12.9%) as a result of

the interannual expansion –fundamentally time deposits

(+7.8%)- and the increase of deposit interest rates (+10

12

basis points during the first six months of the current

period).

As a result of higher relative variation of expenses

compared to income, Metrobank's gross financial margin

drops from 44.1% to 42.3%; however, in absolute terms,

said margin shows a 7.4% interannual growth. On the other

hand, Metrobank registers higher fees on loans, which

increase by 79.1% reaching US$3.4 million. This latter,

together with lower reserves expense (-57.0%), allowed the

Bank's net financial margin to improve going from 53.9%

to 55.3% between the periods evaluated (+15.1% in

absolute terms).

0%

1%

2%

3%

4%

5%

6%

7%

-

10.0

20.0

30.0

40.0

50.0

60.0

2012 2013 2014 2015 Jun.15Jun.16

Spre

ad

In U

S$ m

illio

ns

Spread

Financialexpenses

Interest on duefrom banks

Interest oninvestments

Interest on loans

Average yield onearning assets*

Average fundingcost

*Does not include fees on loans. Source: Metrobank / Prepared by: Equilibrium

It should be indicated that Metrobank's average yield on

earning assets -not including fees- is 5.7% as of the closing

of the first semester of 2016, while the average funding

cost is 3.5% (3.4% as of June 2015), thus the financial

spread is 2.2% (2.3% as of June 2015), below the NBS

average (2.6%). However, when including fees on loans,

Metrobank's average yield on loans increases to 6.3%

(6.2% as of June 2015), thus the financial spread increases

to 2.8%.

On the other hand, other operating income drops 63.6%

and reaches US$1.3 million. Said evolution is due in the

first place too the result of the sale of securities, since as of

June 30, 2016 there is a loss of US$49 thousand (non

material amount regarding the investments portfolio),

while for the same period of the previous period the result

was a gain of US$1.4 million. It should be indicated that

the result is in line with the decision to make the invest-

ments in advance due to the expectation of the rise of

interest rates that could negatively impact the yields of the

portfolio securities. Another factor that explains the drop

of other income is because in the period evaluated

Metrobank does not register income from advisory ser-

vices and referred customers associated to the operation of

Financiera Govimar, while for the first semester of the

previous period income US$0.5 million was registered for

this concept.

Regarding general and administrative expenses, these

register a 5.8% growth, explained mainly by greater

employees and compensation expenses (+9.1%). Thus, the

result before taxes amounts to US$7.4 million, 7.3% below

than the result achieved in the same period of the previous

year.

As of June 30, 2016, net profits drop by 10.6% resulting in

US$6.3 million, registering in turn a net margin of 19.4%

(24.4% as of June 30, 2015). As a result of the lower result,

the ROAE drops from 13.0% to 9.4% between the periods

evaluated.

13

METROBANK, S.A. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEET

in thousands of dollars

ASSETS:

Cash and cash items 5,565 0.7% 5,970 0.6% 6,862 0.6% 5,165 0.5% 11,480 1.0% 4,188 0.3% -63.5% -18.9%

Demand deposits due from banks 44,945 5.7% 72,360 7.8% 76,172 7.1% 75,361 6.7% 98,214 8.5% 93,677 7.5% -4.6% 24.3%

Time deposits due from banks 40,645 5.1% 37,336 4.0% 39,804 3.7% 31,901 2.8% 12,988 1.1% 18,300 1.5% 40.9% -42.6%

Total Cash and due from Banks 91,155 11.5% 115,666 12.4% 122,838 11.4% 112,427 10.0% 122,682 10.6% 116,164 9.3% -5.3% 3.3%

Investments in securities available for sale 137,040 17.3% 165,092 17.7% 220,975 20.6% 231,324 20.7% 226,033 19.5% 259,288 20.8% 14.7% 12.1%

Total Investments 137,040 17.3% 165,092 17.7% 220,975 20.6% 231,324 20.7% 226,033 19.5% 259,288 20.8% 14.7% 12.1%

Total Funds Available 228,195 28.9% 280,757 30.1% 343,813 32.0% 343,751 30.7% 348,714 30.1% 375,452 30.2% 7.7% 9.2%

Loans 569,145 72.0% 657,277 70.4% 727,951 67.8% 774,554 69.2% 810,856 69.9% 868,492 69.8% 7.1% 12.1%

Internal sector 536,059 67.8% 607,513 65.1% 633,234 59.0% 657,284 58.7% 660,616 57.0% 696,462 55.9% 5.4% 6.0%

External sector 33,085 4.2% 49,763 5.3% 94,718 8.8% 117,270 10.5% 150,240 13.0% 172,030 13.8% 14.5% 46.7%

Current credits 565,876 71.6% 652,926 70.0% 720,670 67.2% 768,172 68.6% 807,144 69.6% 854,094 68.6% 5.8% 11.2%

Nonperforming and past-due credits 3,269 0.4% 4,351 0.5% 7,281 0.7% 6,382 0.6% 3,713 0.3% 14,398 1.2% 287.8% 125.6%

Non performing credits 1,844 0.2% 3,980 0.4% 5,122 0.5% 4,599 0.4% 2,791 0.2% 3,948 0.3% 41.5% -14.2%

Past-due credits 1,425 0.2% 371 0.0% 2,160 0.2% 1,783 0.2% 922 0.1% 10,449 0.8% 1033.2% 486.1%

Less: - -

Reserve for protection of portfolio 6,425 0.8% 3,343 0.4% 5,196 0.5% 5,707 0.5% 3,110 0.3% 2,829 0.2% -9.0% -50.4%

Discounted unearned Interest, fees and insurance 29,492 3.7% 31,042 3.3% 28,599 2.7% 28,651 2.6% 29,227 2.5% 29,567 2.4% 1.2% 3.2%

Net loans and discounts 533,228 67.4% 622,892 66.8% 694,156 64.7% 740,196 66.1% 778,520 67.1% 836,096 67.2% 7.4% 13.0%

Property, Furniture, Equipment and Improvements 6,503 0.8% 10,348 1.1% 10,759 1.0% 10,668 1.0% 9,842 0.8% 8,880 0.7% -9.8% -16.8%

Goodwill 10,134 1.3% 10,134 1.1% 10,134 0.9% 10,134 0.9% 10,134 0.9% 10,134 0.8% 0.0% 0.0%

Accrued interest receivable 2,639 0.3% 2,702 0.3% 3,586 0.3% 3,525 0.3% 3,957 0.3% 4,648 0.4% 17.5% 31.9%

Other assets 10,123 1.3% 6,288 0.7% 6,567 0.6% 7,342 0.7% 5,211 0.4% 6,725 0.5% 29.0% -8.4%

Assets held for sale 0 0.0% 0 0.0% 4,035 0.4% 4,035 0.4% 3,540 0.3% 3,115 0.3% -12.0% -22.8%

TOTAL ASSETS 790,822 100% 933,122 100% 1,073,052 100% 1,119,652 100.0% 1,159,918 100% 1,245,049 100% 7.3% 11.2%

LIABILITIES:

Local demand deposits 77,962 9.9% 83,042 8.9% 106,290 9.9% 93,809 8.4% 83,288 7.2% 84,880 6.8% 1.9% -9.5%

Foreign demand deposits 5,616 0.7% 6,205 0.7% 7,621 0.7% 5,944 0.5% 5,885 0.5% 5,589 0.4% -5.0% -6.0%

Demand deposits 83,578 10.6% 89,247 9.6% 113,910 10.6% 99,753 8.9% 89,173 7.7% 90,469 7.3% 1.5% -9.3%

Local savings deposits 81,415 8.7% 100,352 9.4% 98,303 8.8% 97,616 8.4% 106,020 8.5% 8.6% 7.8%

Foreign savings deposits 19,594 2.1% 24,431 2.3% 24,801 2.2% 20,800 1.8% 18,682 1.5% -10.2% -24.7%

Savings deposits 88,572 11.2% 101,009 10.8% 124,784 11.6% 123,104 11.0% 118,416 10.2% 124,701 10.0% 5.3% 1.3%

Local time deposits 378,539 47.9% 477,250 51.1% 576,274 53.7% 639,861 57.1% 659,876 56.9% 692,497 55.6% 4.9% 8.2%

Foreign time deposits 55,531 7.0% 63,385 6.8% 59,971 5.6% 65,471 5.8% 66,518 5.7% 67,805 5.4% 1.9% 3.6%

Customers' time deposits 434,069 54.9% 540,635 57.9% 636,245 59.3% 705,332 63.0% 726,394 62.6% 760,301 61.1% 4.7% 7.8%

Interbank demand deposits 1,129 0.1% 226 0.0% 210 0.0% 257 0.0% 208 0.0% 19 0.0% -90.9% -92.7%

Interbank time deposits 29,513 3.7% 28,787 3.1% 24,033 2.2% 16,502 1.5% 8,001 0.7% 17,013 1.4% 112.6% 3.1%

Interbank time deposits 30,642 3.9% 29,012 3.1% 24,243 2.3% 16,759 1.5% 8,209 0.7% 17,031 1.4% 107.5% 1.6%

Total deposits 636,862 80.5% 759,903 81.4% 899,182 83.8% 944,948 84.4% 942,192 81.2% 992,503 79.7% 5.3% 5.0%

Borrowings 28,058 3.5% 25,965 2.8% 17,517 1.6% 12,190 1.1% 36,481 3.1% 77,382 6.2% 112.1% 534.8%

Securities sold under repurchase agreements 37,199 4.7% 32,074 3.4% 27,500 2.6% 27,500 2.5% 27,500 2.4% 15,000 1.2% -45.5% -45.5%

Cashiers' checks and certified checks 3,833 0.5% 5,882 0.6% 4,525 0.4% 8,608 0.8% 2,560 0.2% 4,099 0.3% 60.1% -52.4%

Accrued interest payable 3,343 0.4% 3,596 0.4% 4,457 0.4% 4,934 0.4% 5,455 0.5% 6,675 0.5% 22.4% 35.3%

Pending acceptances 277 0.0% 0 0.0% 746 0.1% 24 0.0% 173 0.0% 0.0% -100.0% -100.0%

Other liabilities 8,621 1.1% 9,992 1.1% 10,879 1.0% 11,076 1.0% 10,639 0.9% 9,479 0.8% -10.9% -14.4%

TOTAL LIABILITIES 718,192 90.8% 837,411 89.7% 964,807 89.9% 1,009,280 90.1% 1,025,001 88.4% 1,105,137 88.8% 7.8% 9.5%

STOCKHOLDERS' EQUITY: - -

Common stock 50,000 6.3% 65,000 7.0% 65,000 6.1% 65,000 5.8% 85,000 7.3% 85,000 6.8% 0.0% 30.8%

Changes in securities available for sale 1,170 0.1% -1,182 -0.1% 2,649 0.2% 278 0.0% -363 0.0% 1,529 0.1% -521.4% 449.1%

Reserve for foreclosed assets 6 0.0% 0 0.0% 8 0.0% 4 0.0% 11 0.0% 11 0.0% 0.0% 200.0%

Regulatory reserve for assets under administration 0 0.0% 0 0.0% 91 0.0% 94 0.0% 113 0.0% 128 0.0% 13.2% 36.6%

Difference between regulatory specific reserve and IFRS reserve 0 0.0% 4,915 0.5% 358 0.0% 0 0.0% 9 0.0% 1,687 0.1% 18414.0% -

Dynamic reserve for loan losses 0 0.0% 0 0.0% 8,210 0.8% 11,867 1.1% 13,682 1.2% 13,872 1.1% 1.4% 16.9%

Net income for the period 6,873 0.9% 9,848 1.1% 11,226 1.0% 7,067 0.6% 12,457 1.1% 6,317 0.5% -49.3% -10.6%

Retained earnings 14,581 1.8% 17,129 1.8% 20,703 1.9% 26,062 2.3% 24,008 2.1% 31,368 2.5% 30.7% 20.4%

TOTAL STOCKHOLDERS' EQUITY 72,630 9.2% 95,711 10.3% 108,244 10.1% 110,372 9.9% 134,917 11.6% 139,912 11.2% 3.7% 26.8%

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY 790,822 100% 933,122 100% 1,073,052 100% 1,119,652 100.0% 1,159,918 100% 1,245,049 100% 7.3% 11.2%

%Jun.16/Dec.15

Var%

Jun.16/Jun.15

Var%% Jun.15 % Dec.15 % Jun.16% Dec.14Dec.13Dec.12 %

14

METROBANK, S.A. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF INCOME

(in thousands of dollars)

Financial Income 37,990 100.0% 45,649 100.0% 50,824 100.0% 29,017 100.0% 58,576 100.0% 32,522 100.0% 12.1% 15.3%

Interest earned on loans 32,677 86.0% 39,288 86.1% 41,764 82.2% 23,835 82.1% 48,000 81.9% 26,605 81.8% 11.6% 14.9%

Interest earned on due from banks 99 0.3% 82 0.2% 105 0.2% 93 0.3% 152 0.3% 67 0.2% -27.8% 44.1%

Interest earned on investment in securities 5,214 13.7% 6,279 13.8% 8,955 17.6% 5,090 17.5% 10,424 17.8% 5,850 18.0% 14.9% 16.4%

Financial Expenses 19,238 50.6% 23,847 52.2% 28,814 56.7% 16,212 55.9% 33,874 57.8% 18,765 57.7% 15.7% 17.6%

Interest expense on deposits 22,108 48.4% 27,601 54.3% 15,670 54.0% 32,661 55.8% 17,693 54.4% 12.9% 18.3%

Interest expense on borrowings 1,739 3.8% 1,214 2.4% 543 1.9% 1,214 2.1% 1,072 3.3% 97.5% 0.0%

Gross financial results 18,752 49.4% 21,802 47.8% 22,010 43.3% 12,805 44.1% 24,702 42.2% 13,758 42.3% 7.4% 12.2%

Fees earned 3,836 10.1% 5,436 11.9% 8,969 17.6% 4,182 14.4% 9,848 16.8% 5,170 15.9% 23.6% 9.8%

Loans 1,415 3.7% 2,193 4.8% 4,842 9.5% 1,898 6.5% 5,323 9.1% 3,398 10.4% 79.1% 9.9%

Letters of credit 118 0.3% 309 0.7% 310 0.6% 181 0.6% 347 0.6% 120 0.4% -33.7% 11.7%

Custody and administration of securities 331 0.9% 335 0.7% 295 0.6% 220 0.8% 386 0.7% 149 0.5% -32.6% 30.9%

Transfers, money orders cashiers' checks 910 2.4% 996 2.2% 1,071 2.1% 513 1.8% 1,006 1.7% 459 1.4% -10.5% -6.1%

Merchants' acquisition and points of sales 0 0.0% 661 1.4% 858 1.7% 745 2.6% 1,497 2.6% 270 0.8% -63.8% 74.6%

Advisory fees 254 0.7% 191 0.4% 697 1.4% 112 0.4% 334 0.6% 282 0.9% 151.2% -52.2%

Other 807 2.1% 751 1.6% 895 1.8% 512 1.8% 955 1.6% 493 1.5% -3.8% 6.7%

Fees expenses 879 2.3% 1,146 2.5% 1,470 2.9% 661 2.3% 1,498 2.6% 638 2.0% -3.5% 1.9%

Net fees 2,958 7.8% 4,289 9.4% 7,498 14.8% 3,520 12.1% 8,350 14.3% 4,532 13.9% 28.8% 11.4%

Financial results before reserves 21,710 57.1% 26,092 57.2% 29,508 58.1% 16,325 56.3% 33,052 56.4% 18,290 56.2% 12.0% 12.0%

Loan loss reserve 1,339 3.5% 1,652 3.6% 2,588 5.1% 689 2.4% 1,676 2.9% 296 0.9% -57.0% -35.2%

Reserve for impairment losses on investment in securities 204 0.5% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 0.0% - -

Financial results after reserves 20,167 53.1% 24,440 53.5% 26,920 53.0% 15,636 53.9% 31,375 53.6% 17,994 55.3% 15.1% 16.5%

Dividends income 4 0.0% 4 0.0% 5 0.0% 2 0.0% 3 0.0% 4 0.0% 125.8% -44.2%

Gain on sale of securities 1,045 2.7% 932 2.0% 676 1.3% 1,448 5.0% 1,413 2.4% (49) -0.1% -103.4% 108.9%

Other 1,480 3.9% 2,564 5.6% 5,299 10.4% 2,138 7.4% 3,560 6.1% 1,350 4.2% -36.8% -32.8%

Other income (expenses) 2,529 6.7% 3,500 7.7% 5,980 11.8% 3,588 12.4% 4,976 8.5% 1,305 4.0% -63.6% -16.8%

Total operating income, net 22,695 59.7% 27,940 61.2% 32,900 64.7% 19,224 66.2% 36,351 62.1% 19,300 59.3% 0.4% 10.5%

General and administrative expenses 14,488 38.1% 17,013 37.3% 20,661 40.7% 11,239 38.7% 22,334 38.1% 11,896 36.6% 5.8% 8.1%

General operating expenses 6,450 17.0% 6,438 14.1% 8,384 16.5% 4,743 16.3% 9,761 16.7% 4,943 15.2% 4.2% 16.4%

Employee expenses and other compensations 7,541 19.8% 9,085 19.9% 10,622 20.9% 5,625 19.4% 10,860 18.5% 6,139 18.9% 9.1% 2.2%

Depreciation and amortization 497 1.3% 1,490 3.3% 1,654 3.3% 871 3.0% 1,713 2.9% 814 2.5% -6.6% 3.5%

Profits before income taxes 8,208 21.6% 10,927 23.9% 12,239 24.1% 7,984 27.5% 14,017 23.9% 7,404 22.8% -7.3% 14.5%

Income taxes 1,335 3.5% 1,079 2.4% 1,013 2.0% 917 3.2% 1,560 2.7% 1,087 3.3% 18.5% 54.0%

NET INCOME 6,873 18.1% 9,848 21.6% 11,226 22.1% 7,067 24.4% 12,457 21.3% 6,317 19.4% -10.6% 11.0%

Dec.12 % % Dec.14Dec.13 %Var%

Jun.16/Jun.15

Var%

Dic.15/Dic.14% Jun.15 % Dec.15 % Jun.16

15

LIQUIDITY

Investments / Liquid assets 60.1% 58.8% 64.3% 67.3% 64.8% 69.1% 97.9%

Net loans / Deposits 83.7% 82.0% 77.2% 78.3% 82.6% 84.2% 85.6%

(Cash + Due from banks) / Demand and savings deposits 53.0% 60.8% 51.5% 50.4% 59.1% 54.0% 67.4%

(Cash + Due from banks) / Total deposits 14.3% 15.2% 13.7% 11.9% 13.0% 11.7% 23.1%

(Cash + Due from banks) / Total liabilities 12.7% 13.8% 12.7% 11.1% 12.0% 10.5% 19.0%

(Cash + Due from banks + Investments) / Demand and savings deposits 132.6% 147.6% 144.0% 154.2% 168.0% 174.5% 133.3%

(Cash + Due from banks + Investments) / Total deposits 35.8% 36.9% 38.2% 36.4% 37.0% 37.8% 45.6%

(Cash + Due from banks + Investments) / Total liabilities 31.8% 33.5% 35.6% 34.1% 34.0% 34.0% 37.6%

Top 20 depositors / Total deposits 20.0% 18.9% 18.1% 20.1% 20.7% 22.5% N.D.

(Liquid assets + Investments) / Top 20 depositors 1.9 2.0 2.2 1.9 1.8 1.7 N.D.

Legal Liquidity Ratio (average) 58.9% 47.8% 55.6% 64.5% 62.0% 64.9% 60.2%

SOLVENCY

Liabilities / Equity (in number of times) 9.9 8.7 8.9 9.1 7.6 7.9 8.5

Equity / Assets 9.2% 10.3% 10.1% 9.9% 11.6% 11.2% 10.6%

Equity / Gross Loans 12.8% 14.6% 14.9% 14.2% 16.6% 16.1% 16.6%

Fixed assets / Equity 9.0% 10.8% 9.9% 9.7% 7.3% 6.3% N.D.

Financial debt / Liabilities 9.1% 6.9% 4.7% 3.9% 6.2% 8.4% 14.7%

Deposits / Liabilities 88.7% 90.7% 93.2% 93.6% 91.9% 89.8% 82.5%

Time deposits / Deposits 73.0% 75.0% 73.5% 76.4% 78.0% 78.3% 52.2%

Capital Adequacy Ratio9

12.8% 14.2% 13.2% 12.8% 15.6% 14.4% 14.9%

ASSET QUALITY

Nonperforming credits / Gross loans 0.3% 0.6% 0.7% 0.6% 0.3% 0.5% 1.1%

Nonperforming and past-due credits / Gross loans 0.6% 0.7% 1.0% 0.8% 0.5% 1.7% 2.3%

Nonperforming, past-due and charged-off credits / Gross loans + charged-off credits 0.7% 0.8% 1.1% 0.9% 0.9% 2.2% N.D.

Loan loss reserves / Nonperforming credits 348.4% 207.5% 108.4% 124.1% 111.8% 114.4% 85.1%

Loan loss reserves / Nonperforming and past-due credits 196.5% 189.8% 76.3% 89.4% 84.0% 31.4% 39.2%

(Loan loss reserves + dynamic reserve) / (Nonperforming and past-due credits) 196.5% 189.8% 189.0% 275.3% 452.5% 127.7% 97.9%

(Nonperforming credits - Asset reserves) / Equity -6.3% -4.5% -0.4% -1.0% -0.2% -0.4% 1.0%

(Nonperforming + past-due credits - Loan loss reserves - Dynamic Reserve) / Equity -4.3% -4.1% -6.0% -10.1% -9.7% -2.9% 0.3%

Top 20 debtors / Gross loans 22.8% 23.0% 24.6% 24.2% 25.0% 27.3% N.D.

PROFITABILITY

ROAA1

1.0% 1.1% 1.1% 1.3% 1.1% 1.0% 1.4%

ROAE2

10.0% 11.7% 11.0% 13.0% 10.2% 9.4% 13.2%

ROARWA3

1.6% 1.9% 1.7% 1.9% 1.6% 1.4% 1.9%

Average yield on loans (only interest) 6.4% 6.4% 6.0% 6.2% 6.2% 6.2% 5.6%

Average yield on investments (only interest) 4.3% 4.2% 4.6% 4.7% 4.7% 4.6% 2.8%

Average yield on earning assets4 (only interest) 5.7% 5.7% 5.5% 5.7% 5.7% 5.7% 4.5%

Average funding cost5

3.1% 3.1% 3.3% 3.4% 3.5% 3.5% 2.0%

Financial spread (only interest) 2.6% 2.5% 2.2% 2.3% 2.3% 2.2% 2.6%

Average yield on loans (including fees on loans) 6.7% 6.8% 6.7% 6.9% 6.9% 7.0% 6.9%

Average yield on earning assets, incl. fees on loans 6.0% 6.0% 6.0% 6.2% 6.3% 6.3% 5.4%

Financial spread, incl. fees on loans 2.9% 2.8% 2.8% 2.9% 2.8% 2.8% 1.5%

Financial spread7 (only interest) 49.4% 47.8% 43.3% 44.1% 42.2% 42.3% 58.4%

Extraordinary component in net profit 36.8% 35.5% 53.3% 50.8% 39.9% 20.7% 83.4%

EFFICIENCY

Operating expenses / Financial income 38.1% 37.3% 40.7% 38.7% 38.1% 36.6% 59.2%

Operating expenses / Gross margin 77.3% 78.0% 93.9% 87.8% 90.4% 86.5% 101.4%

Employees expenses / Financial income 19.8% 19.9% 20.9% 19.4% 18.5% 18.9% 27.8%

Employees expenses / Gross loans 1.3% 1.4% 1.5% 1.4% 1.3% 1.3% 1.8%

General and administrative expenses / Average total assets 2.1% 2.0% 2.1% 2.1% 2.0% 1.9% 2.5%

Operational efficiency8

59.8% 57.5% 58.2% 56.4% 58.7% 60.7% 59.7%

ADDITIONAL INFORMATION

Annualized intermediation income (US$ thousands) 40,948 49,939 58,322 63,382 66,926 71,443 4,605,759

Annualized intermediation costs (US$ thousands) 19,238 23,847 28,814 31,236 33,874 36,426 1,659,172