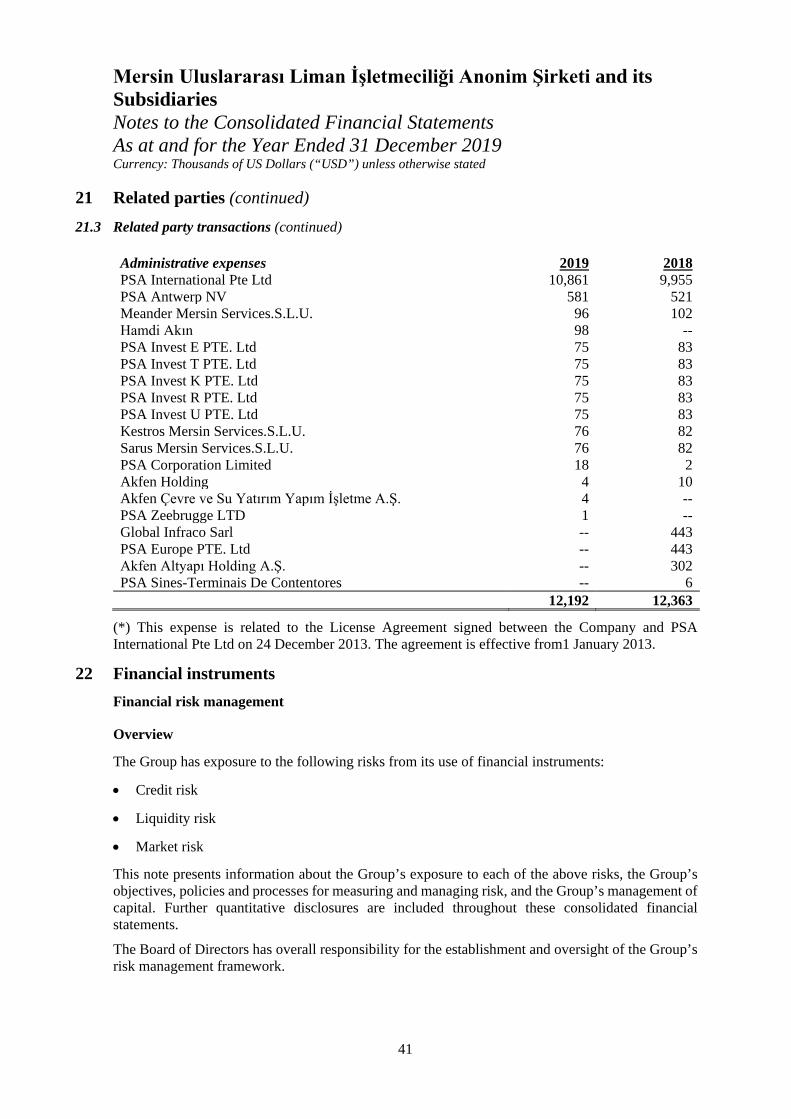

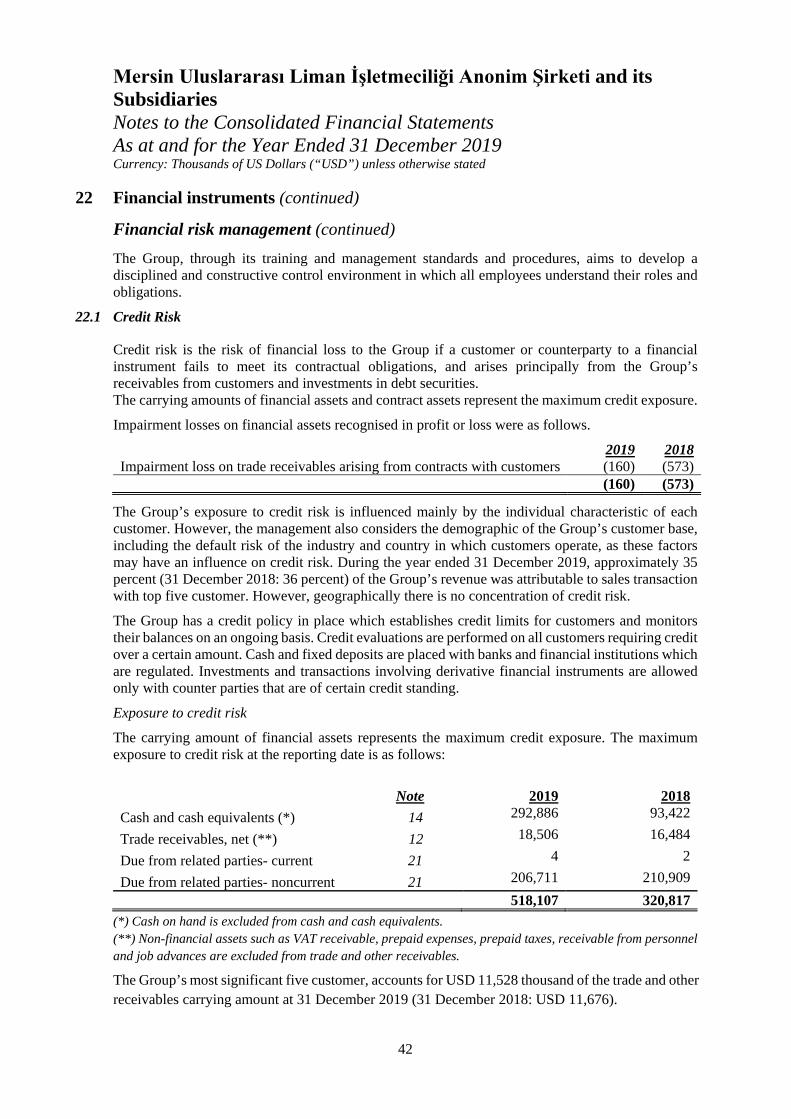

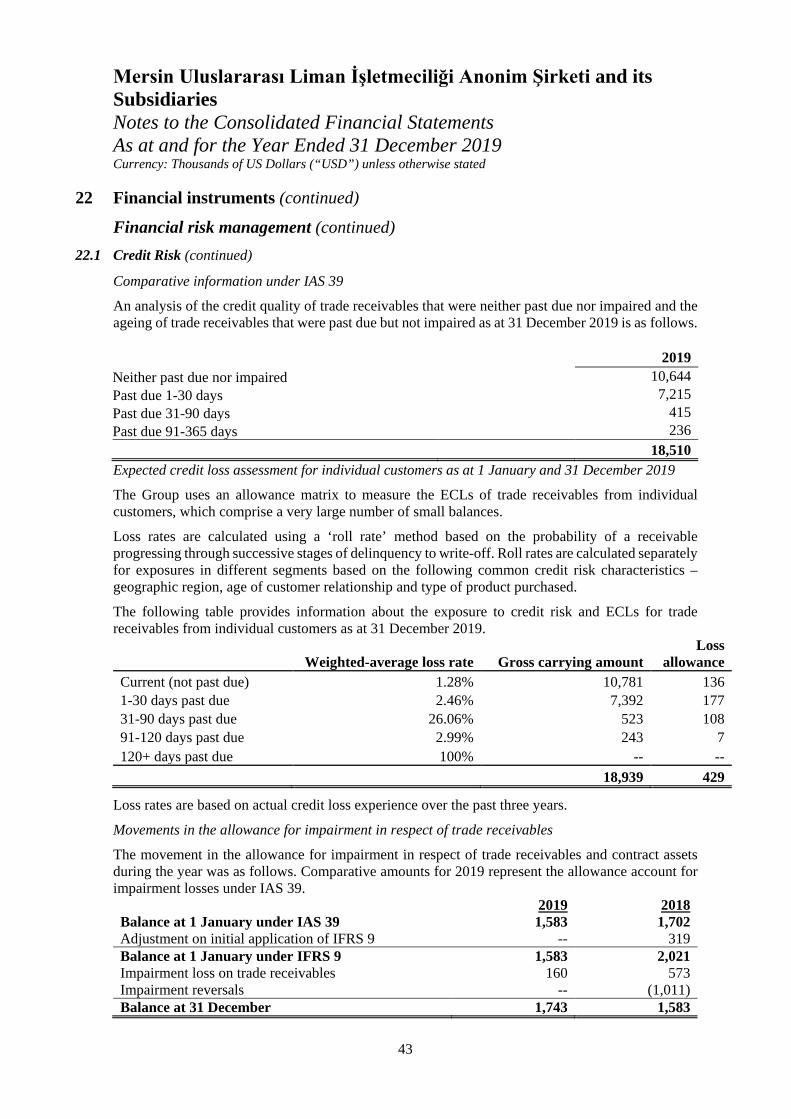

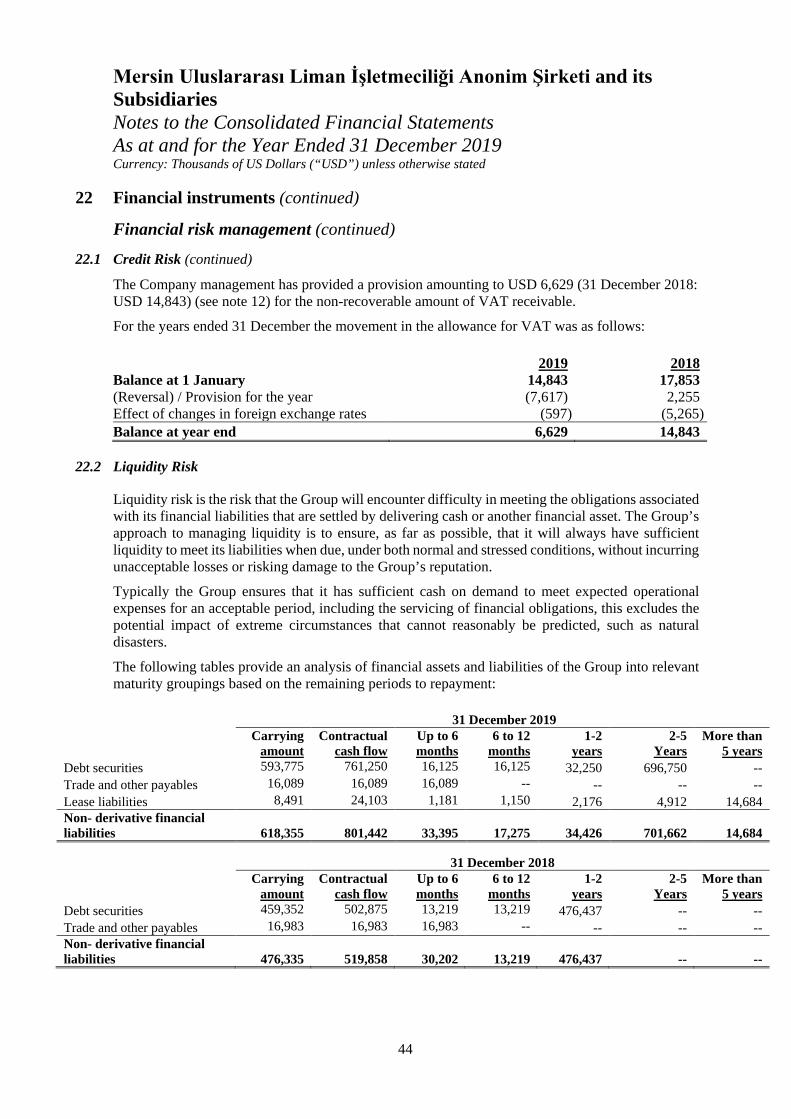

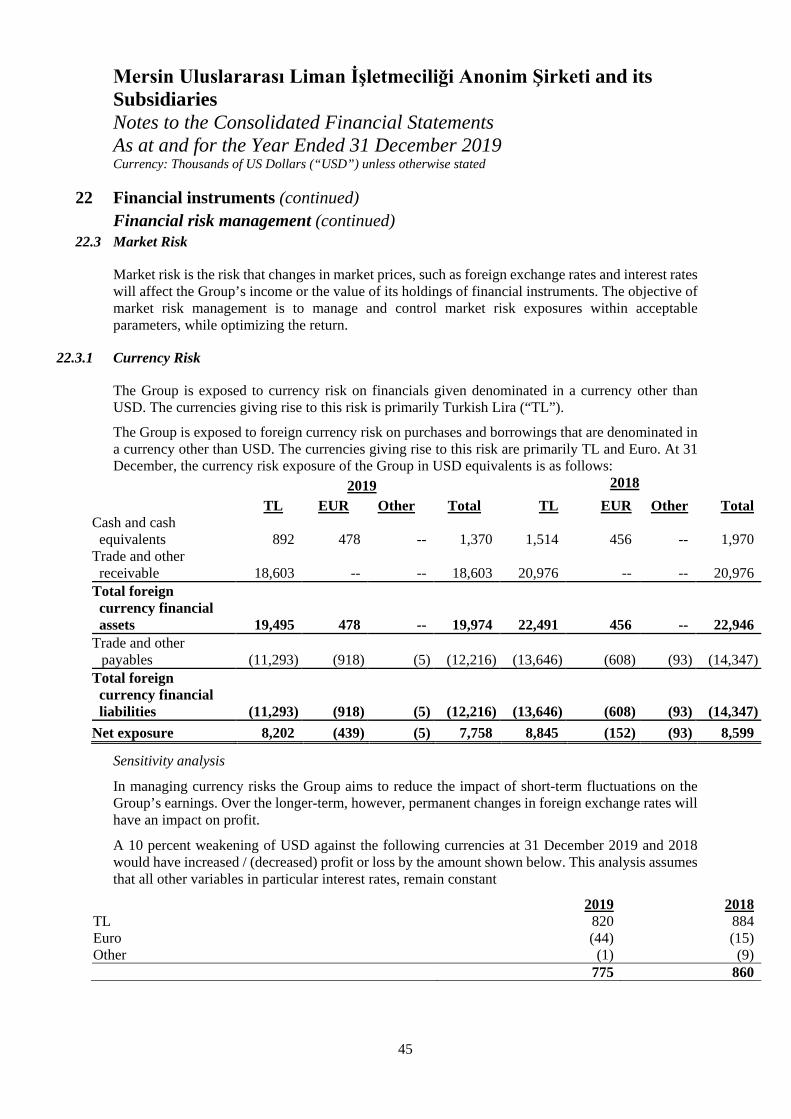

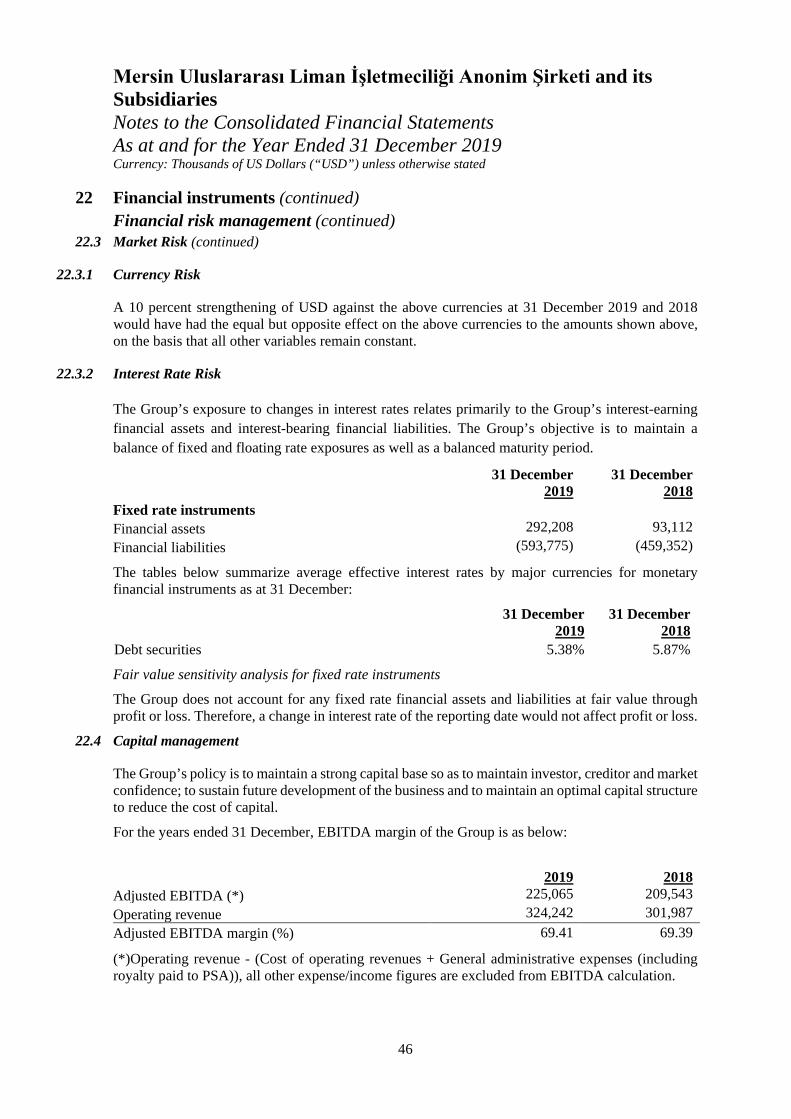

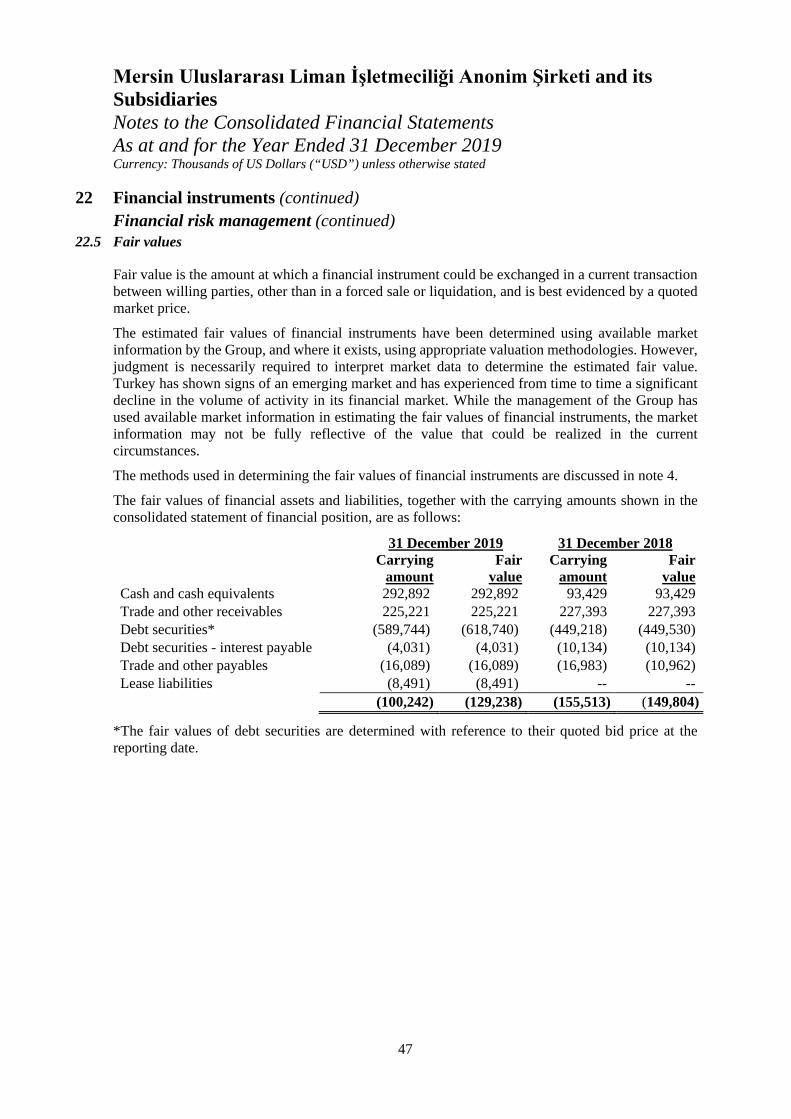

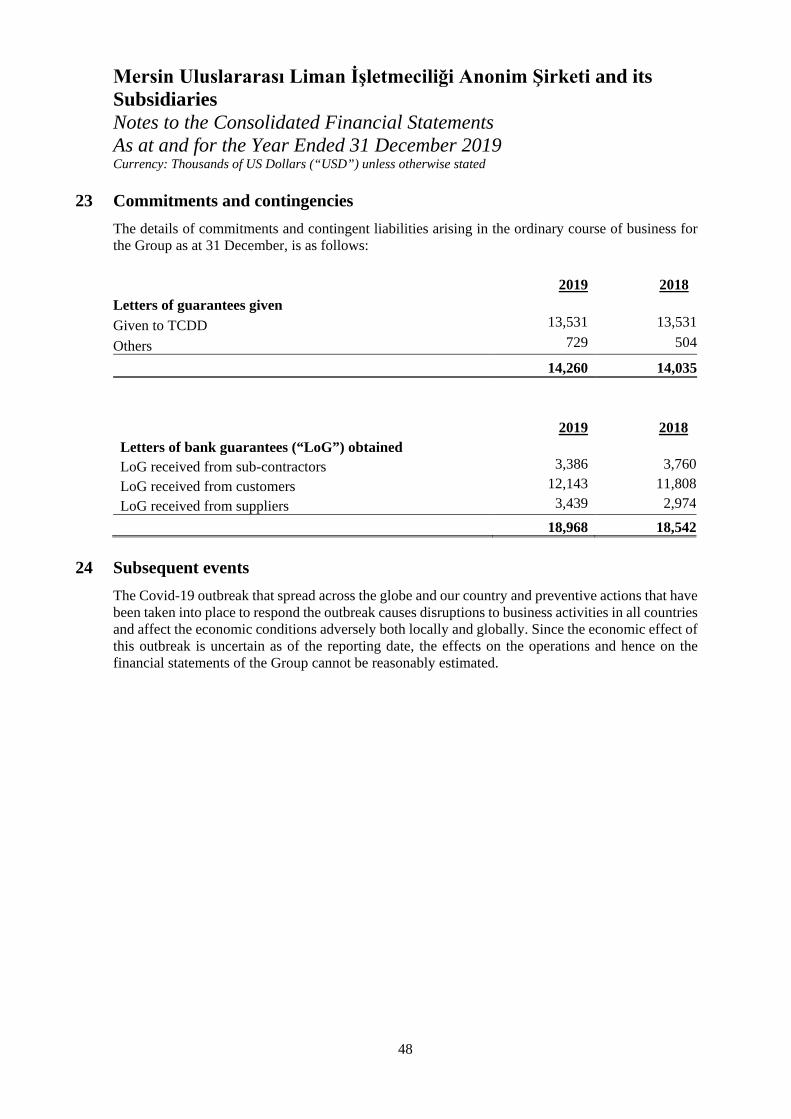

mersin uluslararası liman İşletmeciliği anonim Şirketi€¦ · mersin uluslararası liman...

TRANSCRIPT

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi

And its Subsidiaries Consolidated Financial Statements As at and for the Year Ended

31 December 2019 with Independent Auditors’ Report

31 March 2020 This report includes 4 pages of independent auditors’ report and 48 pages of consolidated financial statements together with their explanatory notes and supplementary information

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries

Table of Contents Independent Auditors’ Report Consolidated Statements of Financial Position

Consolidated Statements of Profit or Loss and Other Comprehensive Income

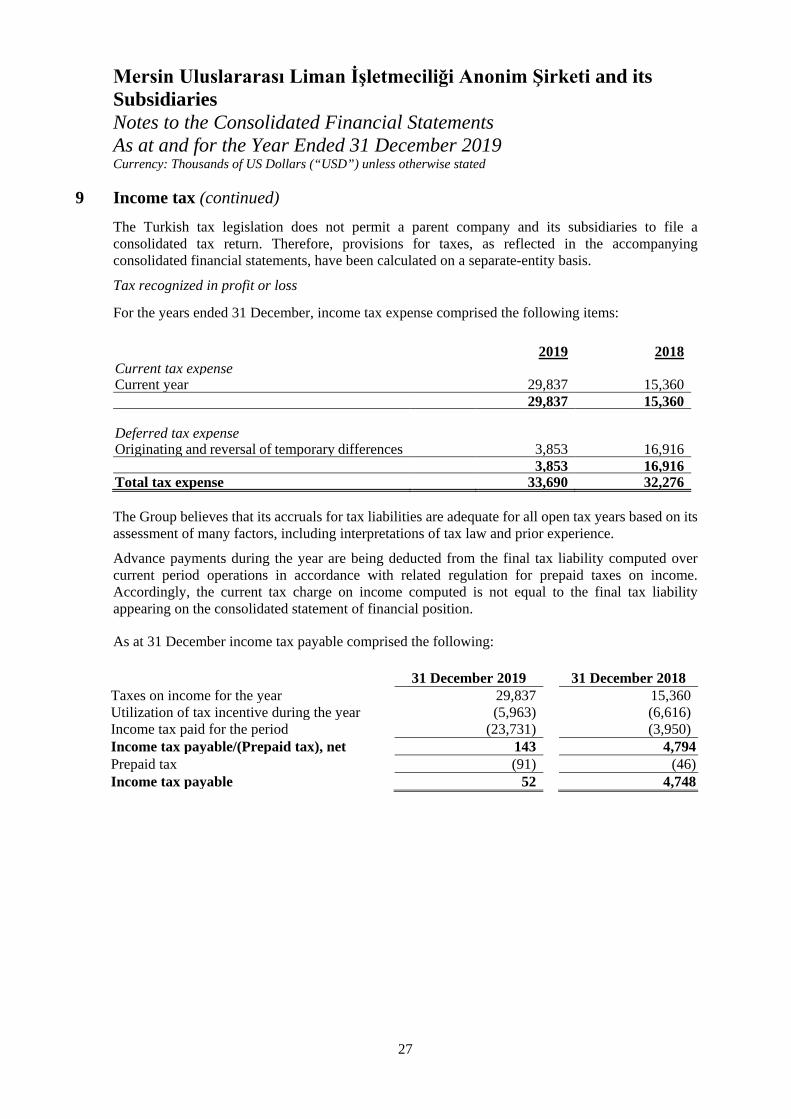

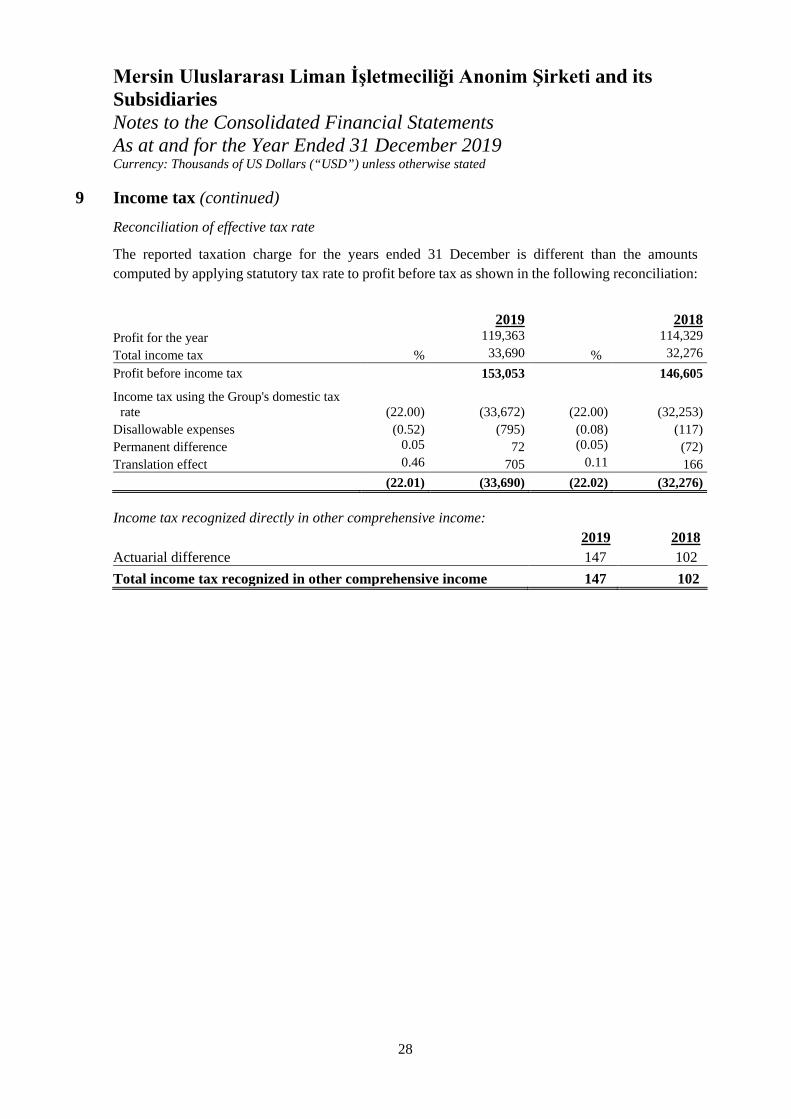

Consolidated Statements of Changes in Equity Consolidated Statements of Cash Flows Notes to the Consolidated Financial Statements

Independent Auditors’ Report

To the Board of Directors of Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi,

Audit of the Consolidated Financial Statements

Opinion

We have audited the consolidated financial statements of Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its subsidiaries (“the Group”), which comprise the consolidated statement of financial position as at 31 December 2019, the consolidated statements of profit or loss and other comprehensive income, changes in equity and cash flows for the year then ended, and notes, comprising significant accounting policies and other explanatory information.

In our opinion, the accompanying consolidated financial statements give a true and fair view of the consolidated financial position of the Group as at 31 December 2019, and of its consolidated financial performance and its consolidated cash flows for the year then ended in accordance with International Financial Reporting Standards (“IFRS”).

Basis for Opinion

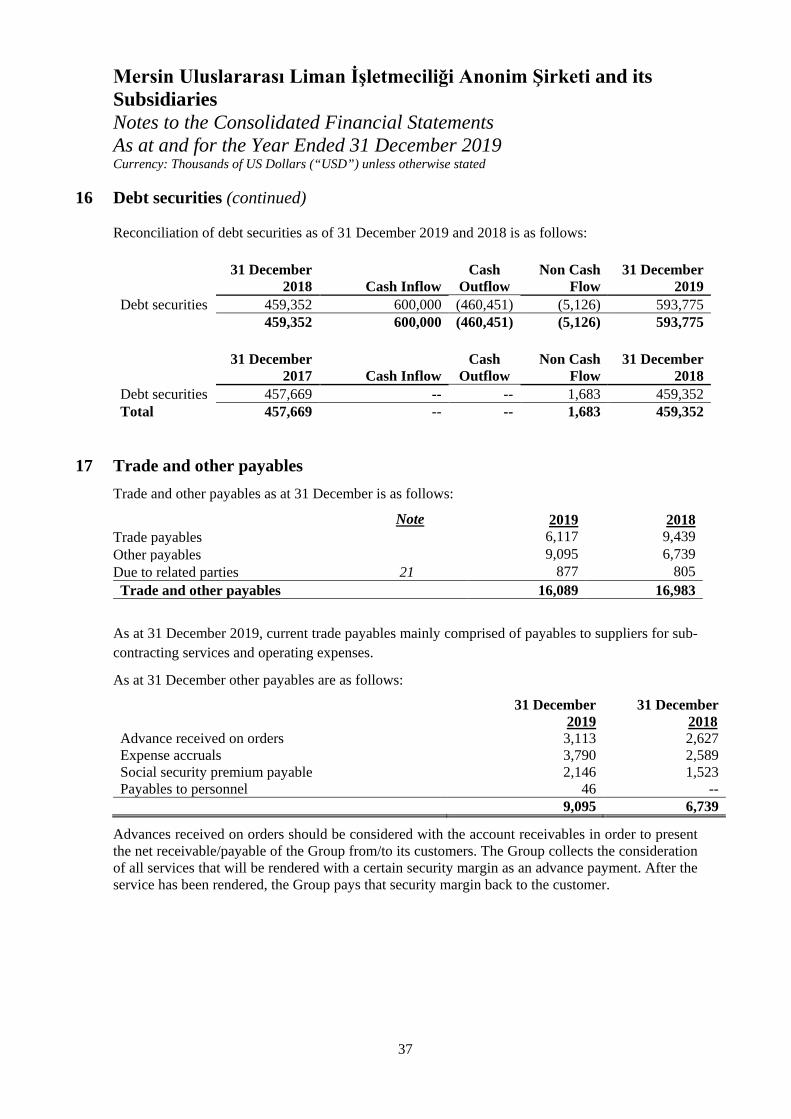

We conducted our audit in accordance with International Standards on Auditing (“ISAs”). Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are independent of the Group in accordance with the ethical requirements that are relevant to our audit of the consolidated financial statements in Turkey, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Emphasis of matter

The Covid-19 outbreak and taken precautions cause disruption on operations of organizations and affect the economic conditions negatively both globally and the countries in which the Group operates. We draw attention to Note 24 of the consolidated financial statements, which describes the possible effects of the outbreak. Our opinion is not modified in respect of this matter.

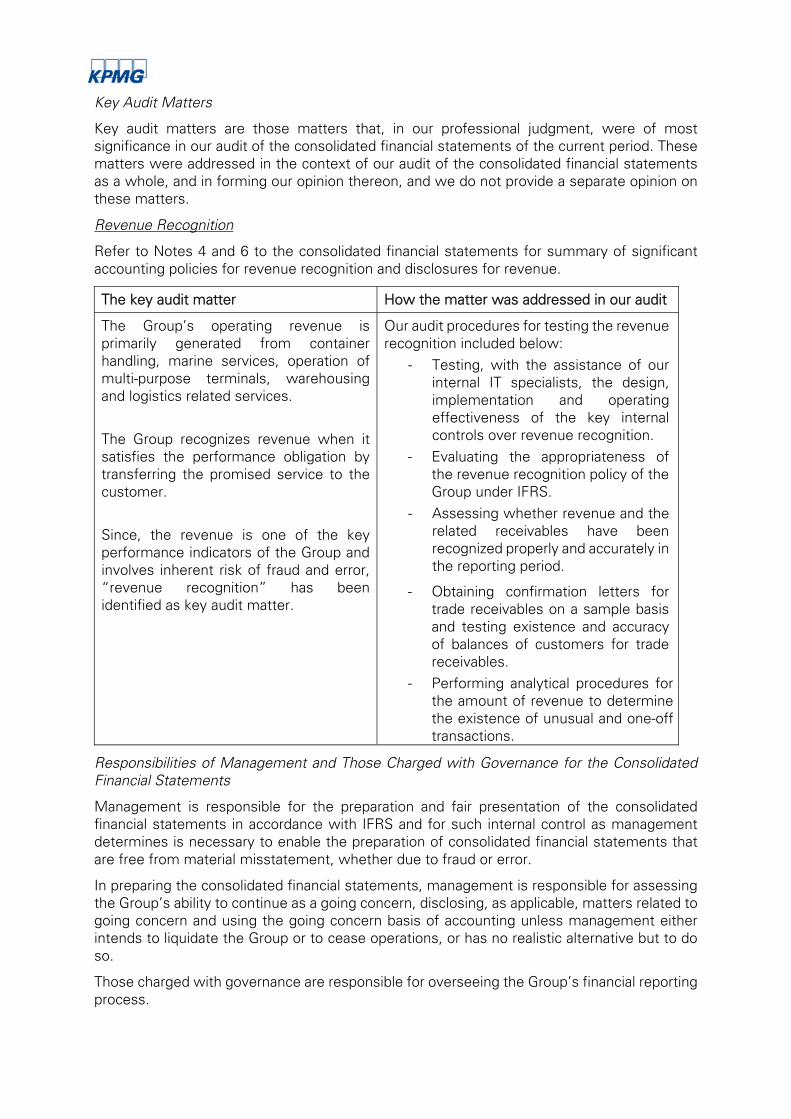

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Revenue Recognition

Refer to Notes 4 and 6 to the consolidated financial statements for summary of significant accounting policies for revenue recognition and disclosures for revenue.

The key audit matter How the matter was addressed in our audit

The Group’s operating revenue is primarily generated from container handling, marine services, operation of multi-purpose terminals, warehousing and logistics related services.

The Group recognizes revenue when it satisfies the performance obligation by transferring the promised service to the customer.

Since, the revenue is one of the key performance indicators of the Group and involves inherent risk of fraud and error, “revenue recognition” has been identified as key audit matter.

Our audit procedures for testing the revenue recognition included below:

- Testing, with the assistance of our internal IT specialists, the design, implementation and operating effectiveness of the key internal controls over revenue recognition.

- Evaluating the appropriateness of the revenue recognition policy of the Group under IFRS.

- Assessing whether revenue and the related receivables have been recognized properly and accurately in the reporting period.

- Obtaining confirmation letters for trade receivables on a sample basis and testing existence and accuracy of balances of customers for trade receivables.

- Performing analytical procedures for the amount of revenue to determine the existence of unusual and one-off transactions.

Responsibilities of Management and Those Charged with Governance for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with IFRS and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing the Group’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Group’s financial reporting process.

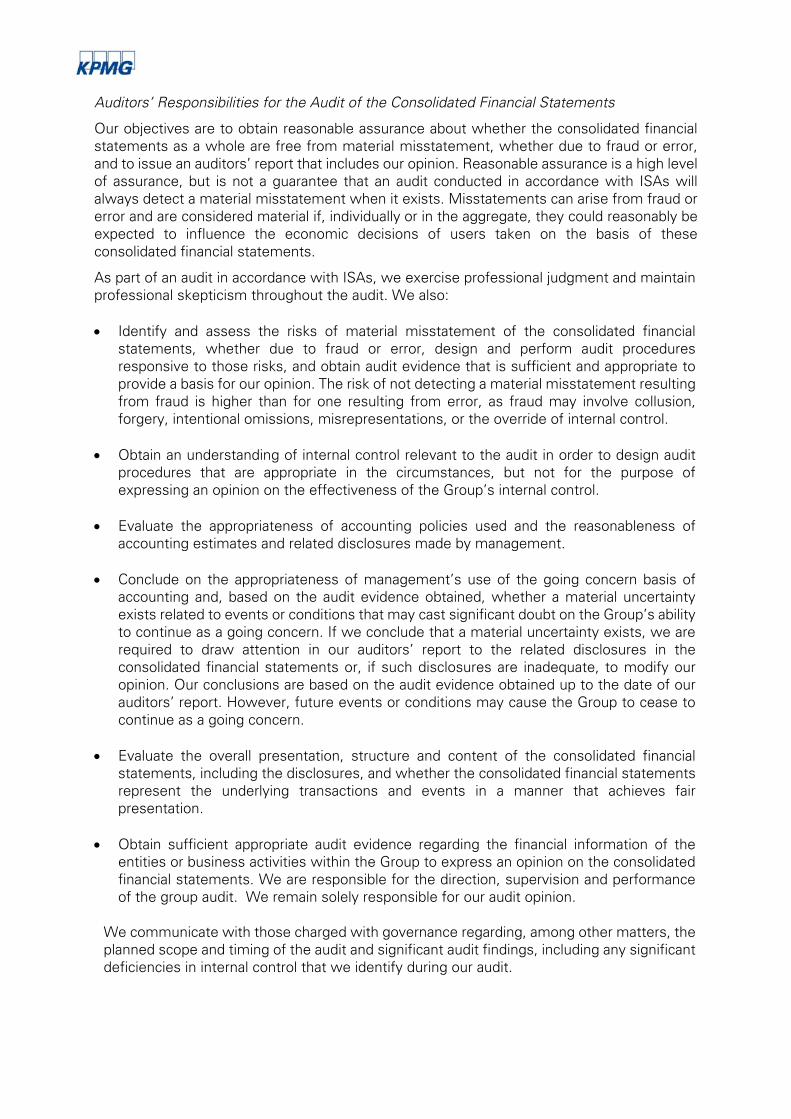

Auditors’ Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group’s internal control.

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditors’ report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors’ report. However, future events or conditions may cause the Group to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

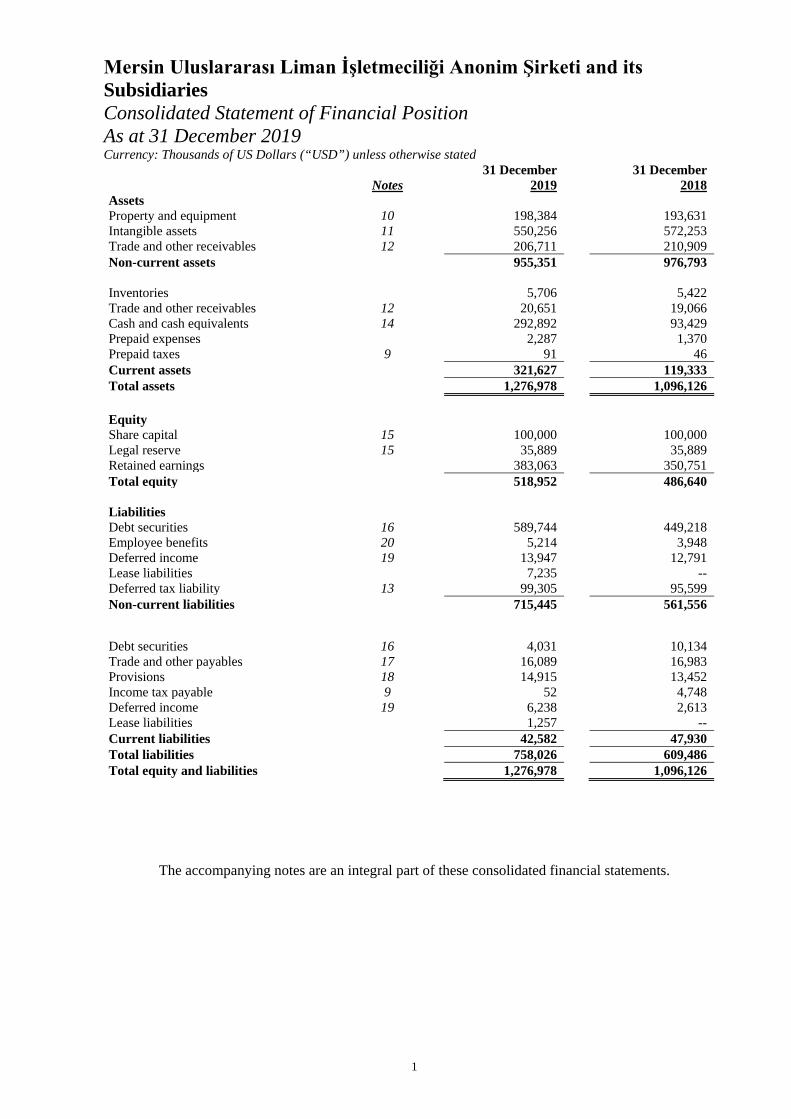

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Consolidated Statement of Financial Position As at 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

1

Notes

31 December 2019

31 December 2018

Assets Property and equipment 10 198,384 193,631 Intangible assets 11 550,256 572,253 Trade and other receivables 12 206,711 210,909 Non-current assets 955,351 976,793 Inventories 5,706 5,422 Trade and other receivables 12 20,651 19,066 Cash and cash equivalents 14 292,892 93,429 Prepaid expenses 2,287 1,370 Prepaid taxes 9 91 46 Current assets 321,627 119,333 Total assets 1,276,978 1,096,126 Equity Share capital 15 100,000 100,000 Legal reserve 15 35,889 35,889 Retained earnings 383,063 350,751 Total equity 518,952 486,640 Liabilities Debt securities 16 589,744 449,218 Employee benefits 20 5,214 3,948 Deferred income 19 13,947 12,791 Lease liabilities 7,235 -- Deferred tax liability 13 99,305 95,599 Non-current liabilities 715,445 561,556

Debt securities 16 4,031 10,134 Trade and other payables 17 16,089 16,983 Provisions 18 14,915 13,452 Income tax payable 9 52 4,748 Deferred income 19 6,238 2,613 Lease liabilities 1,257 -- Current liabilities 42,582 47,930 Total liabilities 758,026 609,486 Total equity and liabilities 1,276,978 1,096,126

The accompanying notes are an integral part of these consolidated financial statements.

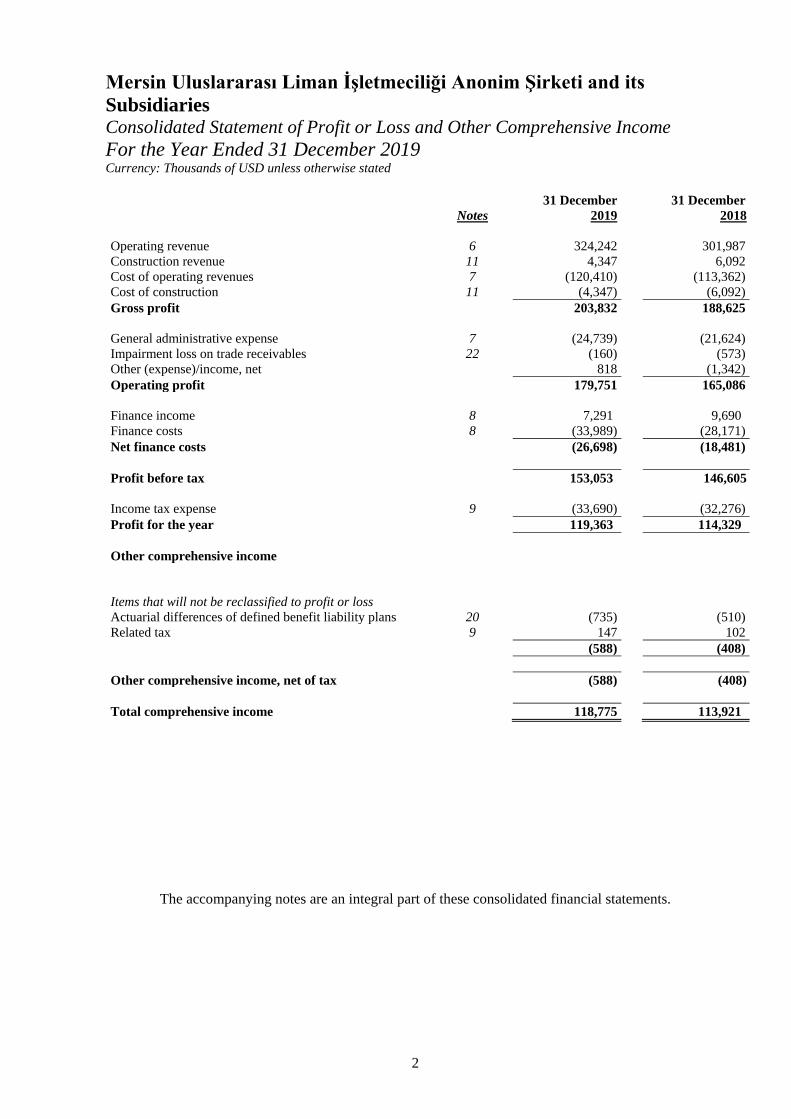

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Consolidated Statement of Profit or Loss and Other Comprehensive Income For the Year Ended 31 December 2019 Currency: Thousands of USD unless otherwise stated

2

Notes 31 December

2019 31 December

2018 Operating revenue 6 324,242

301,987

Construction revenue 11 4,347 6,092 Cost of operating revenues 7 (120,410) (113,362) Cost of construction 11 (4,347) (6,092) Gross profit 203,832 188,625 General administrative expense 7 (24,739) (21,624) Impairment loss on trade receivables 22 (160) (573) Other (expense)/income, net 818 (1,342) Operating profit 179,751 165,086 Finance income 8 7,291 9,690 Finance costs 8 (33,989) (28,171) Net finance costs (26,698) (18,481) Profit before tax 153,053 146,605 Income tax expense 9 (33,690) (32,276) Profit for the year 119,363 114,329 Other comprehensive income Items that will not be reclassified to profit or loss Actuarial differences of defined benefit liability plans 20 (735) (510) Related tax 9 147 102 (588) (408) Other comprehensive income, net of tax (588) (408) Total comprehensive income 118,775 113,921

The accompanying notes are an integral part of these consolidated financial statements.

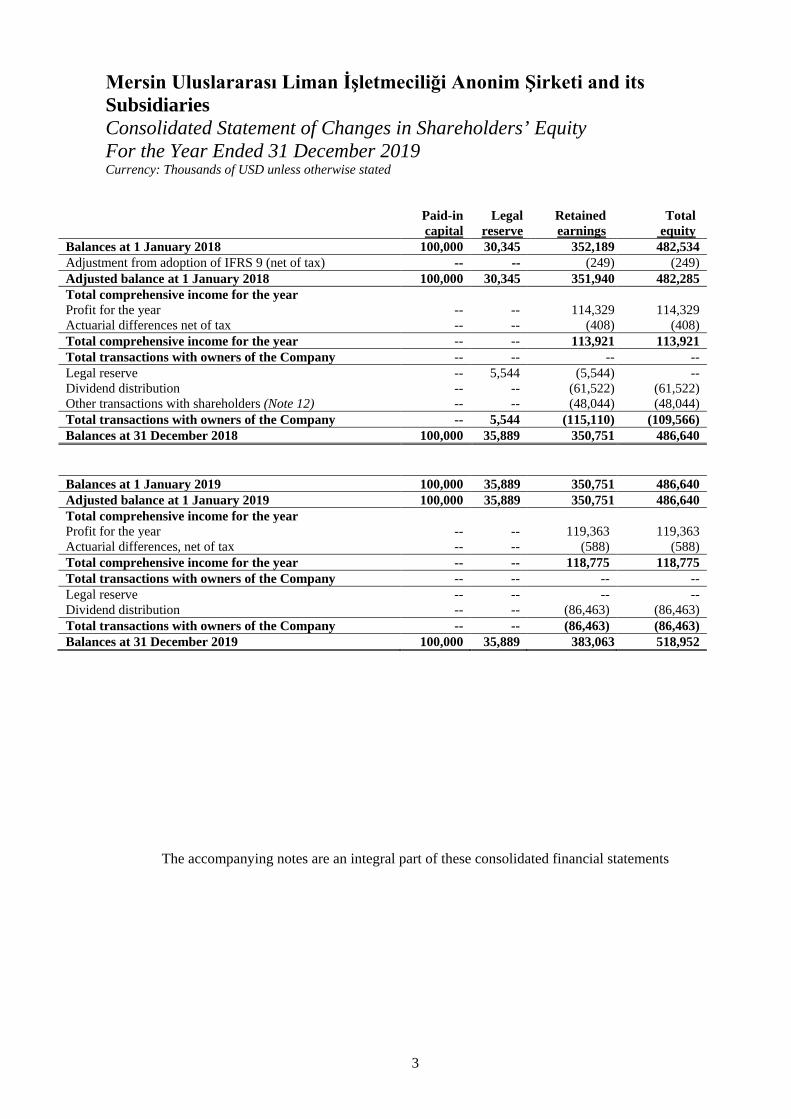

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Consolidated Statement of Changes in Shareholders’ Equity For the Year Ended 31 December 2019 Currency: Thousands of USD unless otherwise stated

3

Paid-in capital

Legal reserve

Retained earnings

Total equity

Balances at 1 January 2018 100,000 30,345 352,189 482,534 Adjustment from adoption of IFRS 9 (net of tax) -- -- (249) (249) Adjusted balance at 1 January 2018 100,000 30,345 351,940 482,285 Total comprehensive income for the year Profit for the year -- -- 114,329 114,329 Actuarial differences net of tax -- -- (408) (408) Total comprehensive income for the year -- -- 113,921 113,921 Total transactions with owners of the Company -- -- -- -- Legal reserve -- 5,544 (5,544) -- Dividend distribution -- -- (61,522) (61,522) Other transactions with shareholders (Note 12) -- -- (48,044) (48,044) Total transactions with owners of the Company -- 5,544 (115,110) (109,566) Balances at 31 December 2018 100,000 35,889 350,751 486,640 Balances at 1 January 2019 100,000 35,889 350,751 486,640 Adjusted balance at 1 January 2019 100,000 35,889 350,751 486,640 Total comprehensive income for the year Profit for the year -- -- 119,363 119,363 Actuarial differences, net of tax -- -- (588) (588) Total comprehensive income for the year -- -- 118,775 118,775 Total transactions with owners of the Company -- -- -- -- Legal reserve -- -- -- -- Dividend distribution -- -- (86,463) (86,463) Total transactions with owners of the Company -- -- (86,463) (86,463) Balances at 31 December 2019 100,000 35,889 383,063 518,952

The accompanying notes are an integral part of these consolidated financial statements

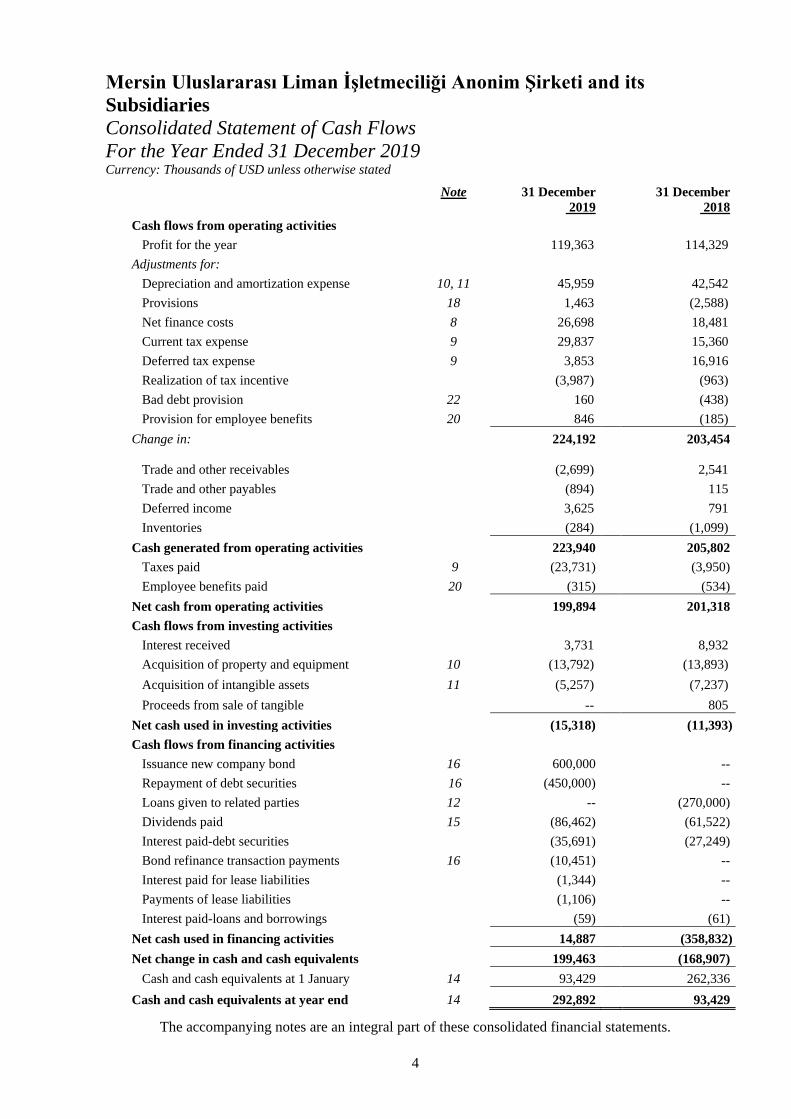

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Consolidated Statement of Cash Flows For the Year Ended 31 December 2019 Currency: Thousands of USD unless otherwise stated

4

The accompanying notes are an integral part of these consolidated financial statements.

Note 31 December

2019 31 December

2018 Cash flows from operating activities

Profit for the year 119,363 114,329 Adjustments for: Depreciation and amortization expense 10, 11 45,959 42,542 Provisions 18 1,463 (2,588) Net finance costs 8 26,698 18,481 Current tax expense 9 29,837 15,360 Deferred tax expense 9 3,853 16,916 Realization of tax incentive (3,987) (963) Bad debt provision 22 160 (438) Provision for employee benefits 20 846 (185) Change in: 224,192 203,454

Trade and other receivables

(2,699)

2,541 Trade and other payables (894) 115 Deferred income 3,625 791 Inventories (284) (1,099) Cash generated from operating activities 223,940 205,802 Taxes paid 9 (23,731) (3,950) Employee benefits paid 20 (315) (534) Net cash from operating activities 199,894 201,318 Cash flows from investing activities Interest received 3,731 8,932 Acquisition of property and equipment 10 (13,792) (13,893) Acquisition of intangible assets 11 (5,257) (7,237) Proceeds from sale of tangible -- 805 Net cash used in investing activities (15,318) (11,393) Cash flows from financing activities Issuance new company bond 16 600,000 -- Repayment of debt securities 16 (450,000) -- Loans given to related parties 12 -- (270,000) Dividends paid 15 (86,462) (61,522) Interest paid-debt securities (35,691) (27,249) Bond refinance transaction payments 16 (10,451) -- Interest paid for lease liabilities (1,344) -- Payments of lease liabilities (1,106) -- Interest paid-loans and borrowings (59) (61) Net cash used in financing activities 14,887 (358,832) Net change in cash and cash equivalents 199,463 (168,907) Cash and cash equivalents at 1 January 14 93,429 262,336 Cash and cash equivalents at year end 14 292,892 93,429

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

5

Notes Page 1 Reporting entity 6 2 Basis of accounting 7 3 Changes in significant accounting policies 8 4 Significant accounting policies 11 5 Measurement of fair values 24 6 Operating revenue 25 7 Expenses by nature 25 8 Net finance costs 26 9 Income tax 26 10 Property and equipment 29 11 Intangible assets 31 12 Trade and other receivables 33 13 Deferred tax assets and liabilities 34 14 Cash and cash equivalents 35 15 Capital and reserves 35 16 Debt securities 36 17 Trade and other payables 37 18 Provisions 38 19 Deferred income 38 20 Employee benefits 39 21 Related parties 40 22 Financial instruments 42 23 Commitments and contingencies 48 24 Subsequent events 48

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

6

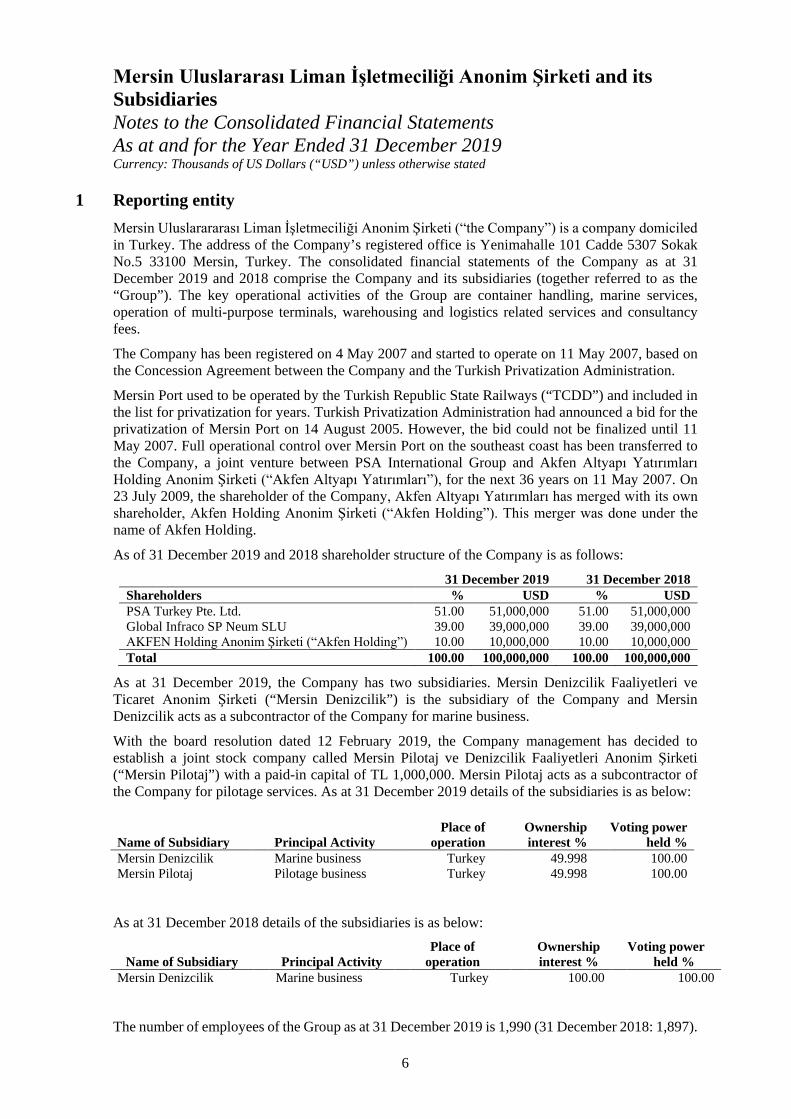

1 Reporting entity Mersin Uluslarararası Liman İşletmeciliği Anonim Şirketi (“the Company”) is a company domiciled in Turkey. The address of the Company’s registered office is Yenimahalle 101 Cadde 5307 Sokak No.5 33100 Mersin, Turkey. The consolidated financial statements of the Company as at 31 December 2019 and 2018 comprise the Company and its subsidiaries (together referred to as the “Group”). The key operational activities of the Group are container handling, marine services, operation of multi-purpose terminals, warehousing and logistics related services and consultancy fees.

The Company has been registered on 4 May 2007 and started to operate on 11 May 2007, based on the Concession Agreement between the Company and the Turkish Privatization Administration.

Mersin Port used to be operated by the Turkish Republic State Railways (“TCDD”) and included in the list for privatization for years. Turkish Privatization Administration had announced a bid for the privatization of Mersin Port on 14 August 2005. However, the bid could not be finalized until 11 May 2007. Full operational control over Mersin Port on the southeast coast has been transferred to the Company, a joint venture between PSA International Group and Akfen Altyapı Yatırımları Holding Anonim Şirketi (“Akfen Altyapı Yatırımları”), for the next 36 years on 11 May 2007. On 23 July 2009, the shareholder of the Company, Akfen Altyapı Yatırımları has merged with its own shareholder, Akfen Holding Anonim Şirketi (“Akfen Holding”). This merger was done under the name of Akfen Holding.

As of 31 December 2019 and 2018 shareholder structure of the Company is as follows:

31 December 2019 31 December 2018 Shareholders % USD % USD PSA Turkey Pte. Ltd. 51.00 51,000,000 51.00 51,000,000 Global Infraco SP Neum SLU 39.00 39,000,000 39.00 39,000,000 AKFEN Holding Anonim Şirketi (“Akfen Holding”) 10.00 10,000,000 10.00 10,000,000 Total 100.00 100,000,000 100.00 100,000,000

As at 31 December 2019, the Company has two subsidiaries. Mersin Denizcilik Faaliyetleri ve Ticaret Anonim Şirketi (“Mersin Denizcilik”) is the subsidiary of the Company and Mersin Denizcilik acts as a subcontractor of the Company for marine business.

With the board resolution dated 12 February 2019, the Company management has decided to establish a joint stock company called Mersin Pilotaj ve Denizcilik Faaliyetleri Anonim Şirketi (“Mersin Pilotaj”) with a paid-in capital of TL 1,000,000. Mersin Pilotaj acts as a subcontractor of the Company for pilotage services. As at 31 December 2019 details of the subsidiaries is as below:

Name of Subsidiary Principal Activity

Place of operation

Ownership interest %

Voting power held %

Mersin Denizcilik Marine business Turkey 49.998 100.00 Mersin Pilotaj Pilotage business Turkey 49.998 100.00

As at 31 December 2018 details of the subsidiaries is as below:

Name of Subsidiary

Principal Activity Place of

operation

Ownership interest %

Voting power held %

Mersin Denizcilik Marine business Turkey 100.00 100.00

The number of employees of the Group as at 31 December 2019 is 1,990 (31 December 2018: 1,897).

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

7

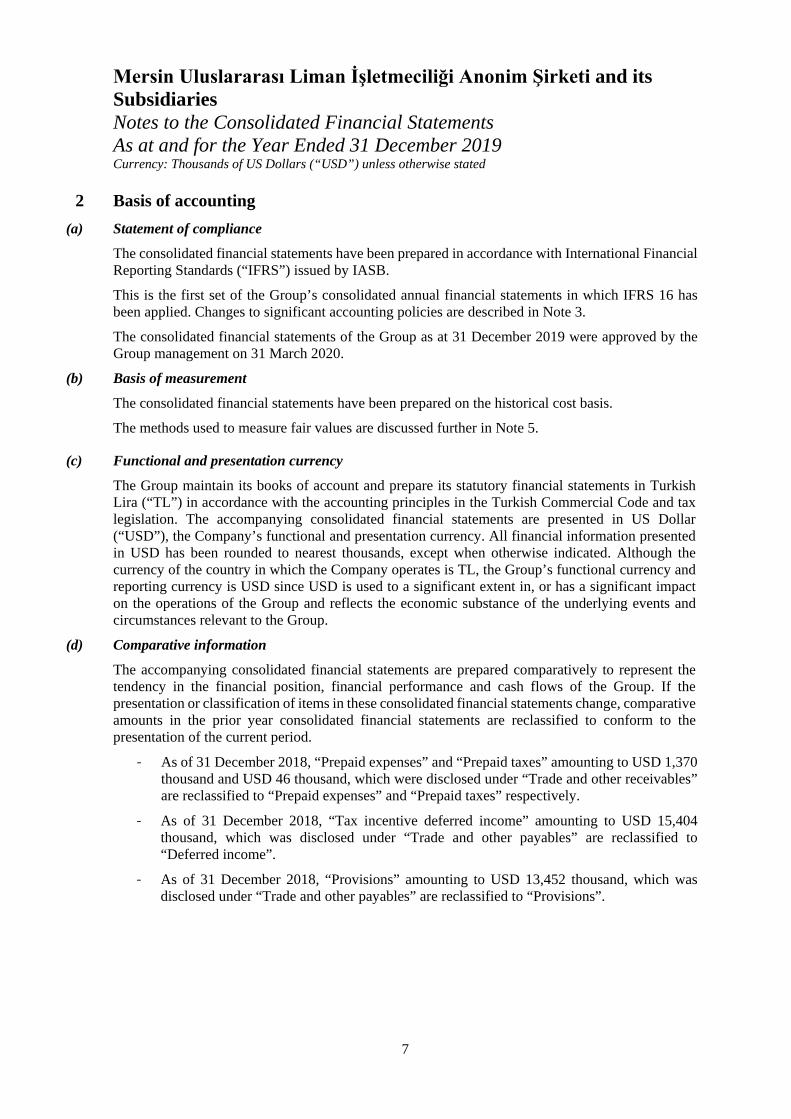

2 Basis of accounting (a) Statement of compliance

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by IASB.

This is the first set of the Group’s consolidated annual financial statements in which IFRS 16 has been applied. Changes to significant accounting policies are described in Note 3.

The consolidated financial statements of the Group as at 31 December 2019 were approved by the Group management on 31 March 2020.

(b) Basis of measurement

The consolidated financial statements have been prepared on the historical cost basis.

The methods used to measure fair values are discussed further in Note 5.

(c) Functional and presentation currency

The Group maintain its books of account and prepare its statutory financial statements in Turkish Lira (“TL”) in accordance with the accounting principles in the Turkish Commercial Code and tax legislation. The accompanying consolidated financial statements are presented in US Dollar (“USD”), the Company’s functional and presentation currency. All financial information presented in USD has been rounded to nearest thousands, except when otherwise indicated. Although the currency of the country in which the Company operates is TL, the Group’s functional currency and reporting currency is USD since USD is used to a significant extent in, or has a significant impact on the operations of the Group and reflects the economic substance of the underlying events and circumstances relevant to the Group.

(d) Comparative information

The accompanying consolidated financial statements are prepared comparatively to represent the tendency in the financial position, financial performance and cash flows of the Group. If the presentation or classification of items in these consolidated financial statements change, comparative amounts in the prior year consolidated financial statements are reclassified to conform to the presentation of the current period.

- As of 31 December 2018, “Prepaid expenses” and “Prepaid taxes” amounting to USD 1,370 thousand and USD 46 thousand, which were disclosed under “Trade and other receivables” are reclassified to “Prepaid expenses” and “Prepaid taxes” respectively.

- As of 31 December 2018, “Tax incentive deferred income” amounting to USD 15,404 thousand, which was disclosed under “Trade and other payables” are reclassified to “Deferred income”.

- As of 31 December 2018, “Provisions” amounting to USD 13,452 thousand, which was disclosed under “Trade and other payables” are reclassified to “Provisions”.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

8

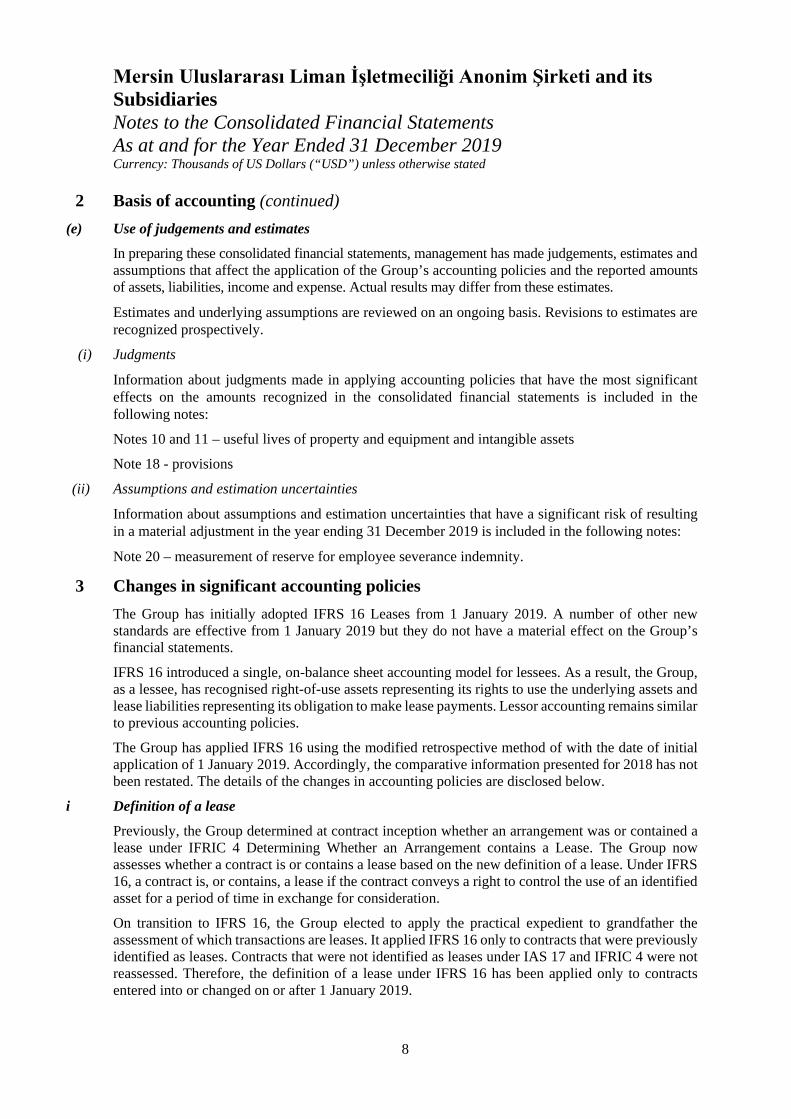

2 Basis of accounting (continued) (e) Use of judgements and estimates

In preparing these consolidated financial statements, management has made judgements, estimates and assumptions that affect the application of the Group’s accounting policies and the reported amounts of assets, liabilities, income and expense. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to estimates are recognized prospectively.

(i) Judgments

Information about judgments made in applying accounting policies that have the most significant effects on the amounts recognized in the consolidated financial statements is included in the following notes:

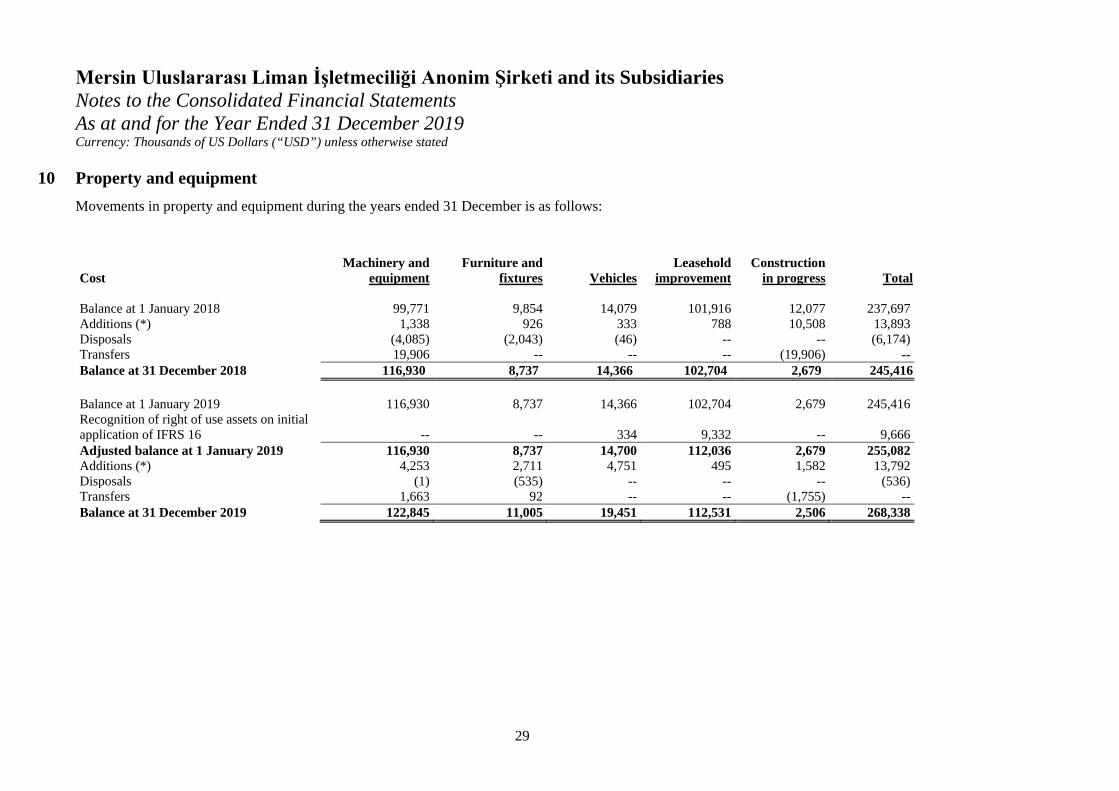

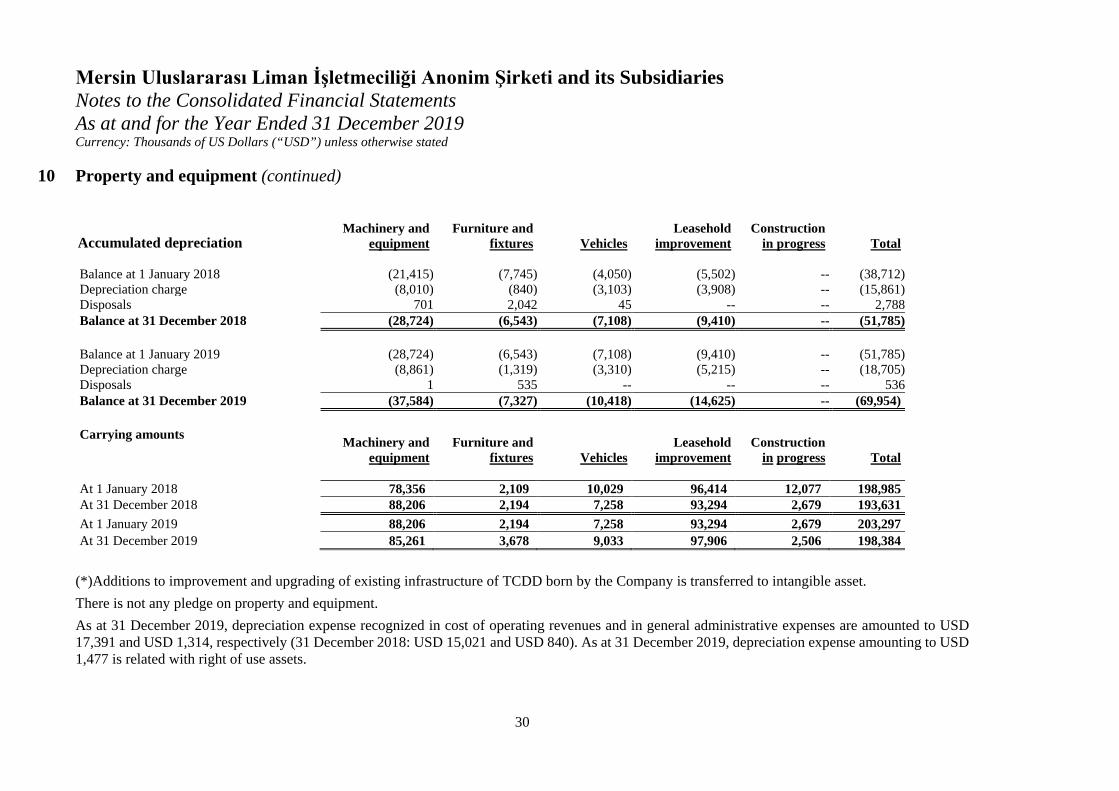

Notes 10 and 11 – useful lives of property and equipment and intangible assets

Note 18 - provisions

(ii) Assumptions and estimation uncertainties

Information about assumptions and estimation uncertainties that have a significant risk of resulting in a material adjustment in the year ending 31 December 2019 is included in the following notes:

Note 20 – measurement of reserve for employee severance indemnity.

3 Changes in significant accounting policies The Group has initially adopted IFRS 16 Leases from 1 January 2019. A number of other new standards are effective from 1 January 2019 but they do not have a material effect on the Group’s financial statements.

IFRS 16 introduced a single, on-balance sheet accounting model for lessees. As a result, the Group, as a lessee, has recognised right-of-use assets representing its rights to use the underlying assets and lease liabilities representing its obligation to make lease payments. Lessor accounting remains similar to previous accounting policies.

The Group has applied IFRS 16 using the modified retrospective method of with the date of initial application of 1 January 2019. Accordingly, the comparative information presented for 2018 has not been restated. The details of the changes in accounting policies are disclosed below.

i Definition of a lease

Previously, the Group determined at contract inception whether an arrangement was or contained a lease under IFRIC 4 Determining Whether an Arrangement contains a Lease. The Group now assesses whether a contract is or contains a lease based on the new definition of a lease. Under IFRS 16, a contract is, or contains, a lease if the contract conveys a right to control the use of an identified asset for a period of time in exchange for consideration.

On transition to IFRS 16, the Group elected to apply the practical expedient to grandfather the assessment of which transactions are leases. It applied IFRS 16 only to contracts that were previously identified as leases. Contracts that were not identified as leases under IAS 17 and IFRIC 4 were not reassessed. Therefore, the definition of a lease under IFRS 16 has been applied only to contracts entered into or changed on or after 1 January 2019.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

9

3 Changes in significant accounting policies (continued) i Definition of a lease (continued)

At inception or on reassessment of a contract that contains a lease component, the Group allocates the consideration in the contract to each lease and non-lease component on the basis of their relative stand-alone prices. However, for leases of properties in which it is a lessee, the Group has elected not to separate non-lease components and will instead account for the lease and non- lease components as a single lease component.

ii As a lessee

The Group leases many assets, including, properties and vehicles.

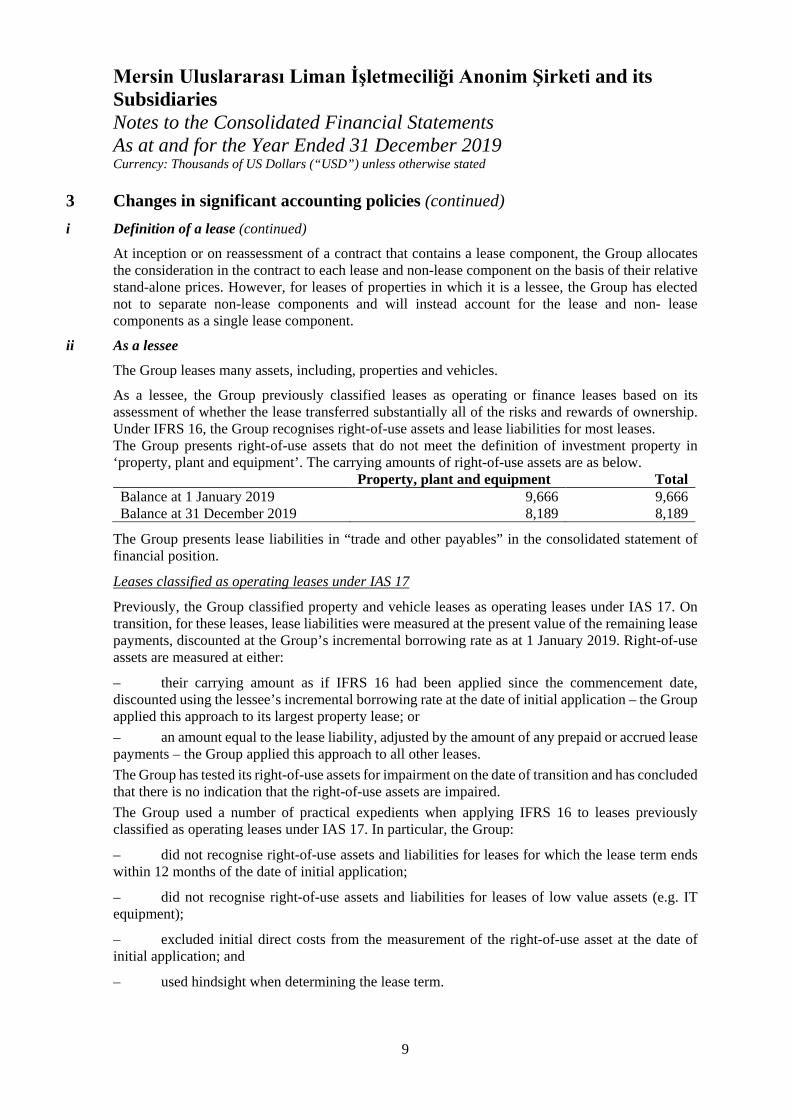

As a lessee, the Group previously classified leases as operating or finance leases based on its assessment of whether the lease transferred substantially all of the risks and rewards of ownership. Under IFRS 16, the Group recognises right-of-use assets and lease liabilities for most leases. The Group presents right-of-use assets that do not meet the definition of investment property in ‘property, plant and equipment’. The carrying amounts of right-of-use assets are as below.

Property, plant and equipment Total Balance at 1 January 2019 9,666 9,666 Balance at 31 December 2019 8,189 8,189

The Group presents lease liabilities in “trade and other payables” in the consolidated statement of financial position.

Leases classified as operating leases under IAS 17

Previously, the Group classified property and vehicle leases as operating leases under IAS 17. On transition, for these leases, lease liabilities were measured at the present value of the remaining lease payments, discounted at the Group’s incremental borrowing rate as at 1 January 2019. Right-of-use assets are measured at either:

– their carrying amount as if IFRS 16 had been applied since the commencement date, discounted using the lessee’s incremental borrowing rate at the date of initial application – the Group applied this approach to its largest property lease; or – an amount equal to the lease liability, adjusted by the amount of any prepaid or accrued lease payments – the Group applied this approach to all other leases. The Group has tested its right-of-use assets for impairment on the date of transition and has concluded that there is no indication that the right-of-use assets are impaired. The Group used a number of practical expedients when applying IFRS 16 to leases previously classified as operating leases under IAS 17. In particular, the Group:

– did not recognise right-of-use assets and liabilities for leases for which the lease term ends within 12 months of the date of initial application;

– did not recognise right-of-use assets and liabilities for leases of low value assets (e.g. IT equipment);

– excluded initial direct costs from the measurement of the right-of-use asset at the date of initial application; and

– used hindsight when determining the lease term.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

10

3 Changes in significant accounting policies (continued)

iii Impacts on consolidated financial statements

Impacts on transition

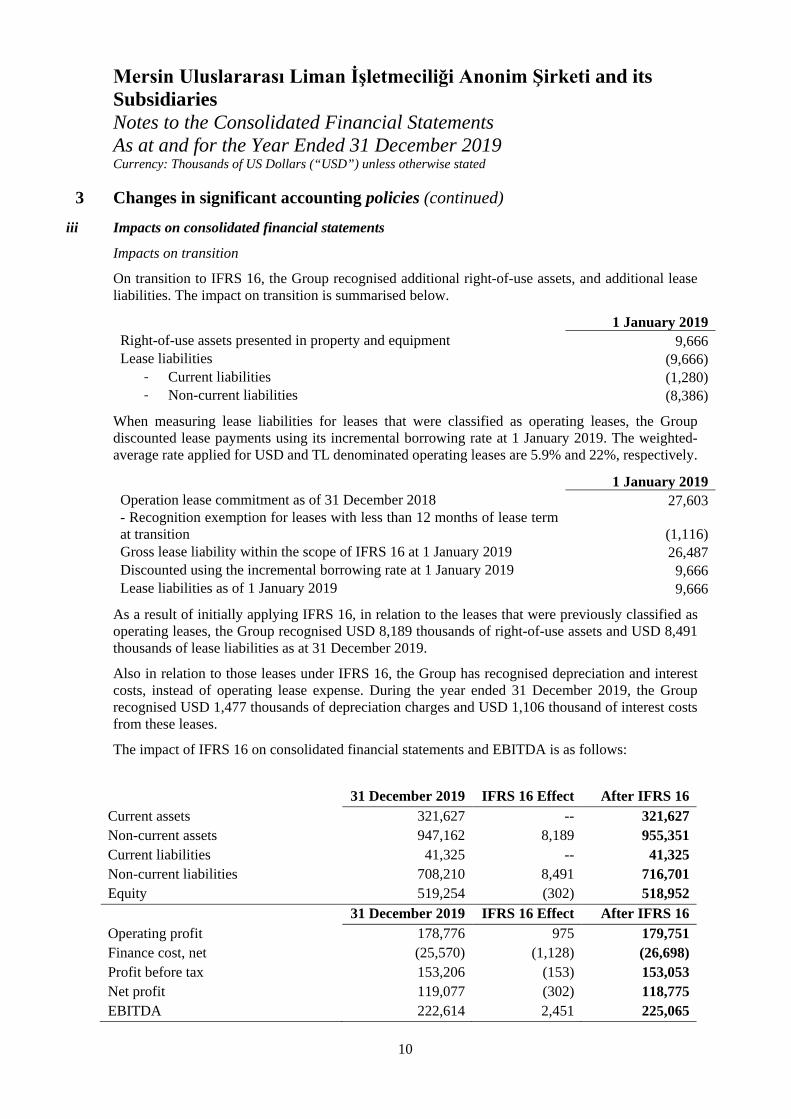

On transition to IFRS 16, the Group recognised additional right-of-use assets, and additional lease liabilities. The impact on transition is summarised below.

1 January 2019 Right-of-use assets presented in property and equipment 9,666 Lease liabilities (9,666)

- Current liabilities (1,280) - Non-current liabilities (8,386)

When measuring lease liabilities for leases that were classified as operating leases, the Group discounted lease payments using its incremental borrowing rate at 1 January 2019. The weighted- average rate applied for USD and TL denominated operating leases are 5.9% and 22%, respectively.

1 January 2019 Operation lease commitment as of 31 December 2018 27,603 - Recognition exemption for leases with less than 12 months of lease term at transition (1,116) Gross lease liability within the scope of IFRS 16 at 1 January 2019 26,487 Discounted using the incremental borrowing rate at 1 January 2019 9,666 Lease liabilities as of 1 January 2019 9,666

As a result of initially applying IFRS 16, in relation to the leases that were previously classified as operating leases, the Group recognised USD 8,189 thousands of right-of-use assets and USD 8,491 thousands of lease liabilities as at 31 December 2019.

Also in relation to those leases under IFRS 16, the Group has recognised depreciation and interest costs, instead of operating lease expense. During the year ended 31 December 2019, the Group recognised USD 1,477 thousands of depreciation charges and USD 1,106 thousand of interest costs from these leases.

The impact of IFRS 16 on consolidated financial statements and EBITDA is as follows:

31 December 2019 IFRS 16 Effect After IFRS 16 Current assets 321,627 -- 321,627 Non-current assets 947,162 8,189 955,351 Current liabilities 41,325 -- 41,325 Non-current liabilities 708,210 8,491 716,701 Equity 519,254 (302) 518,952

31 December 2019 IFRS 16 Effect After IFRS 16 Operating profit 178,776 975 179,751 Finance cost, net (25,570) (1,128) (26,698) Profit before tax 153,206 (153) 153,053 Net profit 119,077 (302) 118,775 EBITDA 222,614 2,451 225,065

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

11

4 Significant accounting policies Certain comparative amounts in the statement of financial position and profit or loss and other comprehensive income have been reclassified or represented, either as a result of correction of errors or change in classification to conform current year presentation.

The Group has consistently applied the following accounting policies to all periods presented in these consolidated financial statements, except the initial application of IFRS 16.

(a) Basis of consolidation

(i) Subsidiaries

Subsidiaries are entities controlled by the Group. The Group controls an entity when it is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. The financial statements of subsidiaries are included in the consolidated financial statements from the date on which control commences until the date on which control ceases.

(ii) Loss of control

When the Group loses control over a subsidiary, it derecognizes the assets and liabilities of the subsidiary, and any related non-controlling interests and other components of equity. Any resulting gain or loss is recognized in profit or loss. Any interest retained in the former subsidiary is measured at fair value when control is lost.

(iii) Transactions eliminated on consolidation

Intra-group balances and transactions, and any unrealized income and expenses arising from intra-group transactions, are eliminated.

(b) Foreign currency transactions

The consolidated financial statements of the Group are presented in the currency of the primary economic environment in which the Group operates (its functional currency). For the purpose of the financial statements, the results and financial position of the Group are expressed in USD, which is the functional and presentation currency of the Group.

In preparing the consolidated financial statements of the Group, transactions in foreign currencies other than USD (foreign currencies) are translated to USD at average monthly exchange rates. Monetary assets and liabilities denominated in foreign currencies are translated to the functional currency at the exchange rate at the reporting date.

Non-monetary items that are measured based on historical cost in a foreign currency are translated at the exchange rate at the date of the transaction.

Foreign currency differences are generally recognized in profit or loss.

(c) Financial instruments

(i) Recognition and initial measurement

Trade receivables are initially recognized when they are originated. All other financial assets and financial liabilities are initially recognized when the Group becomes a party to the contractual provisions of the instrument.

A financial asset (unless it is a trade receivable without a significant financing component) or financial liability is initially measured at fair value plus, for an item not at FVTPL, transaction costs that are directly attributable to its acquisition or issue. A trade receivable without a significant financing component is initially measured at the transaction price.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

12

4 Significant accounting policies (continued) (c) Financial instruments (continued)

(ii) Classification and subsequent measurement

Financial assets

On initial recognition, a financial asset is classified as measured at: amortised cost, FVOCI – equity investment, or FVTPL.

Financial assets are not reclassified subsequent to their initial recognition unless the Company changes its business model for managing financial assets in which case all affected financial assets are reclassified on the first day of the first reporting period following the change in the business model.

A financial asset is measured at amortised cost if it meets both of the following conditions and is not designated as at FVTPL:

- It is held within a business model whose objective is to hold assets to collect contractual cash flows; and

- Its contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

A debt investment is measured at FVOCI if it meets both of the following conditions and is not designated as at FVTPL:

– It is held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets; and

– Its contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

On initial recognition of an equity investment that is not held for trading, the Group may irrevocably elect to present subsequent changes in the investment’s fair value in other comprehensive income. This election is made on an investment-by-investment basis.

All financial assets not classified as measured at amortised cost or FVOCI as described above are measured at FVTPL. On initial recognition, the Group may irrevocably designate a financial asset that otherwise meets the requirements to be measured at amortised cost or at FVOCI as at FVTPL if doing so eliminates or significantly reduces an accounting mismatch that would otherwise arise.

Financial assets: Business model assessment

The Group makes an assessment of the objective of the business model in which a financial asset is held at a portfolio level because this best reflects the way the business is managed and information is provided to management. The information considered includes:

- The stated policies and objectives for the portfolio and the operation of those policies in practice. These include whether management’s strategy focuses on earning contractual interest income, maintaining a particular interest rate profile, matching the duration of the financial assets to the duration of any related liabilities or expected cash outflows or realizing cash flows through the sale of the assets;

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

13

4 Significant accounting policies (continued) (c) Financial instruments (continued) (ii) Classification and subsequent measurement (continued)

Financial assets: Business model assessment (continued)

- How the performance of the portfolio is evaluated and reported to the Group’s management; - The risks that affect the performance of the business model (and the financial assets held within that business model) and how those risks are managed; - How managers of the business are compensated – e.g. whether compensation is based on the fair value of the assets managed or the contractual cash flows collected; and - The frequency, volume and timing of sales of financial assets in prior periods, the reasons for such sales and expectations about future sales activity. Transfers of financial assets to third parties in transactions that do not qualify for derecognition are not considered sales for this purpose, consistent with the Group’s continuing recognition of the assets.

Financial assets that are managed and whose performance is evaluated on a fair value basis are measured at FVTPL.

Financial assets: Assessment whether contractual cash flows are solely payments of principal and interest

For the purposes of this assessment, ‘principal’ is defined as the fair value of the financial asset on initial recognition. ‘Interest’ is defined as consideration for the time value of money and for the credit risk associated with the principal amount outstanding during a particular period of time and for other basic lending risks and costs (e.g. liquidity risk and administrative costs), as well as a profit margin.

In assessing whether the contractual cash flows are solely payments of principal and interest, the Group considers the contractual terms of the instrument. This includes assessing whether the financial asset contains a contractual term that could change the timing or amount of contractual cash flows such that it would not meet this condition. In making this assessment, the Group considers:

- Contingent events that would change the amount or timing of cash flows;

- Terms that may adjust the contractual coupon rate, including variable-rate features;

- Prepayment and extension features; and

- Terms that limit the Group’s claim to cash flows from specified assets (e.g. non-recourse features).

A prepayment feature is consistent with the solely payments of principal and interest criterion if the prepayment amount substantially represents unpaid amounts of principal and interest on the principal amount outstanding, which may include reasonable additional compensation for early termination of the contract. Additionally, for a financial asset acquired at a significant discount or premium to its contractual par amount, a feature that permits or requires prepayment at an amount that substantially represents the contractual par amount plus accrued (but unpaid) contractual interest (which may also include reasonable additional compensation for early termination) is treated as consistent with this criterion if the fair value of the prepayment feature is insignificant at initial recognition.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

14

4 Significant accounting policies (continued) (c) Financial instruments (continued) (ii) Classification and subsequent measurement (continued)

Financial assets: Subsequent measurement and gains and losses

Financial assets at FVTPL

These assets are subsequently measured at fair value. Net gains and losses, including any interest or dividend income, are recognized in profit or loss.

Financial assets at amortised cost

Financial assets at amortised cost are comprised of cash and cash equivalents, trade receivables and other receivables. These assets are subsequently measured at amortised cost using the effective interest method. The amortised cost is reduced by impairment losses. Interest income, foreign exchange gains and losses and impairment are recognized in profit or loss. Any gain or loss on derecognition is recognized in profit or loss.

Debt investments at FVOCI

These assets are subsequently measured at fair value. Interest income calculated using the effective interest method, foreign exchange gains and losses and impairment are recognized in profit or loss. Other net gains and losses are recognized in OCI. On derecognition, gains and losses accumulated in OCI are reclassified to profit or loss.

Equity investments at FVOCI

These assets are subsequently measured at fair value. Dividends are recognized as income in profit or loss unless the dividend clearly represents a recovery of part of the cost of the investment. Other net gains and losses are recognized in OCI and are never reclassified to profit or loss.

(iii) Derecognition

Financial assets

The Group derecognises a financial asset when the contractual rights to the cash flows from the financial asset expire, or it transfers the rights to receive the contractual cash flows in a transaction in which substantially all of the risks and rewards of ownership of the financial asset are transferred or in which the Group neither transfers nor retains substantially all of the risks and rewards of ownership and it does not retain control of the financial asset.

The Group enters into transactions whereby it transfers assets recognised in its statement of financial position, but retains either all or substantially all of the risks and rewards of the transferred assets. In these cases, the transferred assets are not derecognised.

Financial liabilities

The Group derecognizes a financial liability when its contractual obligations are discharged or cancelled, or expire. The Group also derecognizes a financial liability when its terms are modified and the cash flows of the modified liability are substantially different, in which case a new financial liability based on the modified terms is recognized at fair value.

On derecognition of a financial liability, the difference between the carrying amount extinguished and the consideration paid (including any non-cash assets transferred or liabilities assumed) is recognized in profit or loss.

(iv) Offsetting

Financial assets and financial liabilities are offset and the net amount presented in the statement of financial position when, and only when, the Group currently has a legally enforceable right to set off the amounts and it intends either to settle them on a net basis or to realise the asset and settle the liability simultaneously.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

15

4 Significant accounting policies (continued) (d) Share capital

Ordinary shares

Incremental costs directly attributable to the issue of ordinary shares net of any tax effects are recognized as a deduction from equity.

(e) Impairment

(i) Non-derivative financial assets

Financial instruments and contract assets

The Group recognizes loss allowances for ECLs on:

– Financial assets measured at amortised cost;

– Debt investments measured at FVOCI; and

– Contract assets.

The Group measures loss allowances at an amount equal to lifetime ECLs, except for the following, which are measured as 12-month ECLs:

– Debt securities that are determined to have low credit risk at the reporting date; and

– Other debt securities and bank balances for which credit risk (i.e. the risk of default occurring over the expected life of the financial instrument) has not increased significantly since initial recognition.

Loss allowances for trade receivables are always measured at an amount equal to lifetime ECLs.

When determining whether the credit risk of a financial asset has increased significantly since initial recognition and when estimating ECLs, the Group considers reasonable and supportable information that is relevant and available without undue cost or effort. This includes both quantitative and qualitative information and analysis, based on the Group’s historical experience and informed credit assessment and including forward-looking information. The Group assumes that the credit risk on a financial asset has increased significantly if it is more than 30 days past due.

The Group considers a financial asset to be in default when:

- The borrower is unlikely to pay its credit obligations to the Group in full, without recourse by the Group to actions such as realising security (if any is held); or

- The financial asset is more than 120 days past due.

The maximum period considered when estimating ECLs is the maximum contractual period over which the Group is exposed to credit risk.

Measurement of ECLs

ECLs are a probability-weighted estimate of credit losses. Credit losses are measured as the present value of all cash shortfalls.

ECLs are discounted at the effective interest rate of the financial asset.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

16

4 Significant accounting policies (continued) (e) Impairment (continued)

(i) Non-derivative financial assets (continued)

Credit-impaired financial assets

At each reporting date, the Group assesses whether financial assets carried at amortised cost are credit-impaired. A financial asset is ‘credit-impaired’ when one or more events that have a detrimental impact on the estimated future cash flows of the financial asset have occurred.

Evidence that a financial asset is credit-impaired includes the following observable data:

– Significant financial difficulty of the borrower or issuer;

– A breach of contract such as a default or being more than 120 days past due;

– The restructuring of a loan or advance by the Group on terms that the Group would not consider otherwise;

– It is probable that the borrower will enter bankruptcy or other financial reorganisation; or

– The disappearance of an active market for a security because of financial difficulties.

Presentation of allowance for ECL in the statement of financial position

Loss allowances for financial assets measured at amortised cost are deducted from the gross carrying amount of the assets.

Write-off

The gross carrying amount of a financial asset is written off when the Group has no reasonable expectations of recovering a financial asset in its entirety or a portion thereof. For individual customers, the Group has a policy of writing off the gross carrying amount when the financial asset is 120 days past due based on historical experience of recoveries of similar assets. For corporate customers, the Group individually makes an assessment with respect to the timing and amount of write-off based on whether there is a reasonable expectation of recovery. The Group expects no significant recovery from the amount written off. However, financial assets that are written off could still be subject to enforcement activities in order to comply with the Group’s procedures for recovery of amounts due.

(f) Property and equipment

(i) Recognition and measurement

Items of property and equipment are measured at cost less accumulated depreciation and any accumulated impairment losses.

If significant parts of an item of property and equipment have different useful lives, then they are accounted for as separate items (major components) of property and equipment.

Any gain or loss on disposal of an item of property and equipment is recognized in profit or loss.

(ii) Subsequent expenditure

Subsequent expenditure is capitalized only if it is probable that the future economic benefits associated with the expenditure will flow to the Group.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

17

4 Significant accounting policies (continued) (f) Property and equipment (continued)

(iii) Depreciation

Depreciation is calculated to write off the cost of items of property and equipment less their estimated residual values using the straight-line method over their estimated useful lives, and is generally recognized in profit or loss.

The estimated useful lives for the current and comparative periods are as follows: Leasehold improvement Shorter of useful life and lease term Machinery and equipment 3-20 years Vehicles 4-5 years Furniture and fixtures 3-6 years

Depreciation methods, useful lives and residual values are reviewed at each reporting date and adjusted if appropriate.

(g) Intangible assets

Intangible assets that are acquired by the Group and have finite useful lives are measured at cost less accumulated amortization and impairment losses.

(i) Service concession agreements

Mersin International Port is bound by the terms of the concession Agreements made with TCDD. According to the concession agreement, the Company has received a right to charge users of Mersin International Port. The agreement covers a period of 36 years until May 2043.

The Company recognizes an intangible asset arising from a service concession arrangement when it has a right to charge for usage of the concession infrastructure. Intangible assets received as consideration for providing construction or upgrade services in a service concession arrangement are measured at fair value upon initial recognition. Subsequent to initial recognition the intangible asset is measured at cost less accumulated amortization and accumulated impairment losses.

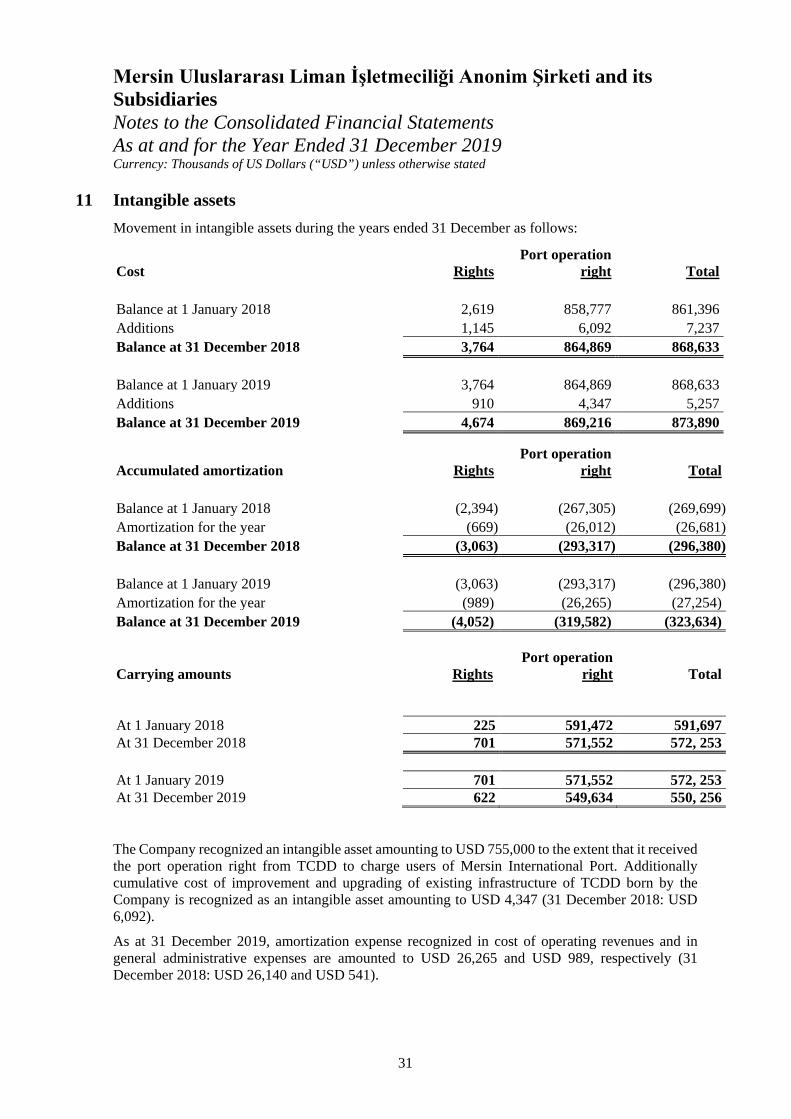

Under IFRIC 12 “Service Concession Arrangements” an operator recognizes an intangible asset or financial asset received as consideration for providing construction or upgrade or operation services or other items. The Company recognized an intangible asset amounting to USD 755,000 to the extent that it received the right from TCDD to charge users of Mersin International Port. Additionally cost of improvement of existing infrastructure of TCDD born by the Company is recognized at its fair value as an intangible asset amounting to USD 6,158 (31 December 2017: USD 3,448).

Fair value of the improvement of existing infrastructure of TCDD borne by the Company which is already recognized as an intangible asset also recognized as construction contract revenue and construction contract cost. Fair value of the improving existing infrastructure is assumed to be equal to its cost since this improvement service was given by third parties at fair value.

(ii) Other intangible assets

Other intangible assets that are acquired by the Group, which have finite useful lives, are measured at cost less accumulated amortization and accumulated impairment losses.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

18

4 Significant accounting policies (continued) (g) Intangible assets (continued)

(iii) Subsequent expenditure

Subsequent expenditure is capitalized only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is recognized in profit or loss as incurred.

(iv) Amortization

The extent that the Company received the right from TCDD, port operation right is amortized on a straight-line basis over the life of concession period. The cost of improvement of existing infrastructure of TCDD are amortized on a straight-line basis over the shorter of the life of concession period and their useful lives.

Amortization methods, useful lives and residual values are reviewed at each reporting date and adjusted if appropriate.

(h) Inventories

Inventories are measured at the lower of cost and net realizable value. The cost of inventories is based on first in first out method, and includes expenditure incurred in acquiring the inventories, and other costs incurred in bringing them to their existing location and condition.

(i) Employee benefits

Reserve for employee severance indemnity

In accordance with the existing social legislation in Turkey, the Group is required to make certain lump-sum payments to employees whose employment is terminated due to retirement or for reasons other than resignation or misconduct. Such payments are calculated on the basis of an agreed formula, are subject to certain upper limits and are recognized in the accompanying financial statements as accrued. The reserve has been calculated by estimating the present value of the future obligation of the Group that may arise from the retirement of the employees.

All actuarial differences are recognized in other comprehensive income in the period which they arise.

Vacation pay liability

In accordance with current labor law, the Group makes payments for unused vacations of employees. The liability is calculated by the remaining vacation days multiplied by one day’s pay.

(j) Provisions

A provision is recognized if, as a result of a past event, the Group has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability.

Contingent liabilities are reviewed to determine if there is a possibility that the outflow of economic benefits will be required to settle the obligation. Except for the economic benefit outflow possibility is remote such contingent liabilities are disclosed in the notes to the consolidated financial statements.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

19

4 Significant accounting policies (continued) (k) Revenue (i) Construction contracts

Revenue is recognised over time based on the cost-to-cost method. The related costs are recognised in profit or loss when they are incurred.

Advances received are included in contract liabilities.

(ii) Income from services

The Group’s operating revenue is primarily generated from container handling, marine services, operation of multi-purpose terminals, warehousing and logistics related services.

The Group recognizes operating revenue when it satisfies the performance obligation by transferring the promised service to the customer.

(l) Leases

The Group has applied IFRS 16 using the modified retrospective approach and therefore the comparative information has not been restated and continues to be reported under IAS 17 and IFRS Interpretation 4. The details of accounting policies under IAS 17 and IFRS Interpretation 4 are disclosed separately.

Policy applicable from 1 January 2019

At inception of a contract, the Group assesses whether a contract is, or contains, a lease. A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration. To assess whether a contract conveys the right to control the use of an identified asset, the Group uses the definition of a lease in IFRS 16. This policy is applied to contracts entered into, on or after 1 January 2019.

As a lessee

At commencement or on modification of a contract that contains a lease component, the Group allocates the consideration in the contract to each lease component on the basis of its relative stand-alone prices. However, for the leases of property the Group has elected not to separate non-lease components and account for the lease and non-lease components as a single lease component.

The Group recognises a right-of-use asset and a lease liability at the lease commencement date. The right-of-use asset is initially measured at cost, which comprises the initial amount of the lease liability adjusted for any lease payments made at or before the commencement date, plus any initial direct costs incurred and an estimate of costs to dismantle and remove the underlying asset or to restore the underlying asset or the site on which it is located, less any lease incentives received.

The right-of-use asset is subsequently depreciated using the straight-line method from the commencement date to the end of the lease term, unless the lease transfers ownership of the underlying asset to the Group by the end of the lease term or the cost of the right-of-use asset reflects that the Group will exercise a purchase option. In that case the right-of-use asset will be depreciated over the useful life of the underlying asset, which is determined on the same basis as those of property and equipment. In addition, the right-of-use asset is periodically reduced by impairment losses, if any, and adjusted for certain remeasurements of the lease liability.

The lease liability is initially measured at the present value of the lease payments that are not paid at the commencement date, discounted using the interest rate implicit in the lease or, if that rate cannot be readily determined, the Group’s incremental borrowing rate. Generally, the Group uses its incremental borrowing rate as the discount rate.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

20

4 Significant accounting policies (continued) (l) Leases (continued)

As a lessee (continued)

Policy applicable from 1 January 2019 (continued)

The Group determines its incremental borrowing rate by obtaining interest rates from various external financing sources and makes certain adjustments to reflect the terms of the lease and type of the asset leased.

Lease payments included in the measurement of the lease liability comprise the following:

– fixed payments, including in-substance fixed payments;

– amounts expected to be paid by the lessee under residual value commitments

The lease liability is measured at amortised cost using the effective interest method. It is remeasured when there is a change in future lease payments arising from a change in an index or rate, if there is a change in the Group’s estimate of the amount expected to be payable under a residual value guarantee, if the Group changes its assessment of whether it will exercise a purchase, extension or termination option or if there is a revised in-substance fixed lease payment.

When the lease liability is remeasured in this way, a corresponding adjustment is made to the carrying amount of the right-of-use asset, or is recorded in profit or loss if the carrying amount of the right-of-use asset has been reduced to zero.

The Group has elected not to recognise right-of-use assets and lease liabilities for leases of low-value assets. The Group recognises the lease payments associated with these leases as an expense on a straight-line basis over the lease term.

Policy applicable before 1 January 2019

For contracts entered into before 1 January 2019, the Group determined whether the arrangement was or contained a lease based on the assessment of whether: – fulfilment of the arrangement was dependent on the use of a specific asset or assets; and

– the arrangement had conveyed a right to use the asset. An arrangement conveyed the right to use the asset if one of the following was met:

‐ the purchaser had the ability or right to operate the asset while obtaining or controlling more than an insignificant amount of the output;

‐ the purchaser had the ability or right to control physical access to the asset while obtaining or controlling more than an insignificant amount of the output; or

‐ facts and circumstances indicated that it was remote that other parties would take more than an insignificant amount of the output, and the price per unit was neither fixed per unit of output nor equal to the current market price per unit of output.

In the comparative period, as a lessee the Group classified leases that transferred substantially all of the risks and rewards of ownership as finance leases. When this was the case, the leased assets were measured initially at an amount equal to the lower of their fair value and the present value of the minimum lease payments. Minimum lease payments were the payments over the lease term that the lessee was required to make, excluding any contingent rent. Subsequent to initial recognition, the assets were accounted for in accordance with the accounting policy applicable to that asset.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

21

4 Significant accounting policies (continued) (l) Leases (continued)

As a lessee (continued) Policy applicable before 1 January 2019 (continued)

Assets held under other leases were classified as operating leases and were not recognised in the Group’s statement of financial position. Payments made under operating leases were recognised in profit or loss on a straight-line basis over the term of the lease. Lease incentives received were recognised as an integral part of the total lease expense, over the term of the lease.

(m) Finance income and finance costs

The Group’s finance income and finance costs include:

– Interest income;

– Interest expense;

– The foreign currency gain or loss on financial assets and financial liabilities;

– Interest income or expense is recognised using the effective interest method.

The ‘effective interest rate’ is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument to:

– The gross carrying amount of the financial asset; or

– The amortised cost of the financial liability.

In calculating interest income and expense, the effective interest rate is applied to the gross carrying amount of the asset (when the asset is not credit-impaired) or to the amortised cost of the liability. However, for financial assets that have become credit-impaired subsequent to initial recognition, interest income is calculated by applying the effective interest rate to the amortised cost of the financial asset. If the asset is no longer credit-impaired, then the calculation of interest income reverts to the gross basis.

(n) Income tax Income tax expense comprises current and deferred tax. It is recognized in profit or loss except to the extent that it relates to a business combination, or items recognized directly in equity or in other comprehensive income.

(i) Current tax Current tax comprises the expected tax payable or receivable on the taxable income or loss for the period and any adjustment to tax payable or receivable in respect of previous years. It is measured using tax rates enacted or substantively enacted at the reporting date.

(ii) Deferred tax

Deferred tax is recognized in respect of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. Deferred tax is not recognized for:

• Temporary differences on the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit or loss,

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

22

4 Significant accounting policies (continued) (n) Income tax (continued) (ii) Deferred tax (continued)

• Temporary differences related to investments in subsidiary to the extent that the Company is able to control the timing of the reversal of the temporary differences and it is probable that they will not reverse in the foreseeable future.

Deferred tax assets are recognized for unused tax losses and deductible temporary differences to the extent that it is probable that future taxable profits will be available against which they can be used. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realized.

Deferred tax is measured at the tax rates that are expected to be applied to the temporary differences when they reverse, using tax rates enacted or substantively enacted at the reporting date.

The measurement of deferred tax reflects the tax consequences that would follow from the manner in which the Group expects, at the reporting date, to recover or settle the carrying amount of its assets and liabilities.

Deferred tax assets and liabilities are offset only if certain criteria are met. Prepaid corporation taxes and corporation tax liabilities are offset as they relate to income taxes levied by the same tax authority.

(n) Government grants and incentives

Government grants are not recognized until there is reasonable assurance that the Group will comply with the conditions attaching to them and that the grants will be received. Government grants are recognized in profit or loss on a systematic basis over the periods in which the Group recognizes as expenses the related costs for which the grants are intended to compensate.

Specifically, government grants whose primary condition is that the Group should purchase, construct or otherwise acquire non-current assets are recognized as deferred revenue in the consolidated statement of financial position and transferred to profit or loss on a systematic and rational basis over the useful lives of the related assets.

Government grants that are receivable as compensation for expenses or losses already incurred or for the purpose of giving immediate financial support to the Group with no future related costs are recognized in profit or loss in the period in which they become receivable.

(o) Standards issued but not yet effective and not early adopted

A number of new standards and amendments to existing standards are not effective at reporting date and earlier application is permitted; however the Group has not early adopted are as follows.

The revised Conceptual Framework (Version 2018)

The revised Conceptual Framework issued on 28 March 2018 by the IASB. The Conceptual Framework sets out the fundamental concepts for financial reporting that guide the Board in developing IFRS Standards. It helps to ensure that the Standards are conceptually consistent and that similar transactions are treated the same way, so as to provide useful information for investors, lenders and other creditors. The Conceptual Framework also assists companies in developing accounting policies when no IFRS Standard applies to a particular transaction, and more broadly, helps stakeholders to understand and interpret the Standards.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

23

4 Significant accounting policies (continued) (p) Standards issued but not yet effective and not early adopted (continued)

The revised Conceptual Framework (Version 2018) (continued)

The revised Framework is more comprehensive than the old one – its aim is to provide the Board with the full set of tools for standard setting. It covers all aspects of standard setting from the objective of financial reporting, to presentation and disclosures. For companies that use the Conceptual Framework to develop accounting policies when no IFRS Standard applies to a particular transaction, the revised Conceptual Framework is effective for annual reporting periods beginning on or after 1 January 2020, with earlier application permitted.

Amendments to IAS 1 and IAS 8 - Definition of Material

In October 2018, IASB issued Definition of Material (Amendments to IAS 1 and IAS 8). The amendments clarify and align the definition of ‘material’ and provide guidance to help improve consistency in the application of that concept whenever it is used in IFRS Standards. The amended “definition of material “was added to the important definition and it was stated that this expression could lead to similar results by not giving and giving misstating information. In addition, with this amendment, the terminology used in its definition of material has been aligned with the terminology used in the Conceptual Framework for Financial Reporting (Version 2018). Those amendments are prospectively effective for annual periods beginning on or after 1 January 2020 with earlier application permitted.

The Group does not expect that application of these amendments to IAS 1 and IAS 8 will have significant impact on its consolidated financial statements

Amendments to IFRS 3 - Definition of a Business

Determining whether a transaction results in an asset or a business acquisition has long been a challenging but important area of judgement. IASB has issued amendments to IFRS 3 Business Combinations to make it easier for companies to decide whether activities and assets they acquire are a business or merely a group of assets. With this amendments confirmed that a business must include inputs and a process, and clarified that the process shall be substantive and the inputs and process must together significantly contribute to creating outputs. It narrowed the definitions of a business by focusing the definition of outputs on goods and services provided to customers and other income from ordinary activities, rather than on providing dividends or other economic benefits directly to investors or lowering costs and added a concentration test that makes it easier to conclude that a company has acquired a group of assets, rather than a business, if the value of the assets acquired is substantially all concentrated in a single asset or group of similar assets.

This is a simplified assessment that results in an asset acquisition of substantially all of the fair value of the gross assets is concentrated in a single identifiable asset or a group of similar identifiable assets. If a preparer chooses not to apply the concentration test, or the test is failed, then the assessment focuses on the existence of a substantive process. The amendment applies to businesses acquired in annual reporting periods beginning on or after 1 January 2020; with earlier application permitted.

The Group does not expect that application of these amendments to IFRS 3 will have significant impact on its consolidated financial statements.

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

24

4 Significant accounting policies (continued) (p) Standards issued but not yet effective and not early adopted (continued)

Interest Rate Benchmark Reform (Amendments to IFRS 9, IAS 39 and IFRS 7)

Interest Rate Benchmark Reform, which amended IFRS 9, IAS 39 and IFRS 7 issued in September 2019, added Section 6.8 and amended paragraph 7.2.26. About this issue, IASB identified two groups of accounting issues that could affect financial reporting. These are:

• pre-replacement issues—issues affecting financial reporting in the period before the reform; and • replacement issues—issues that might affect financial reporting when an existing interest rate benchmark is either reformed or replaced. IASB considered the pre-replacement issues to be more urgent and decided to address the following hedge accounting requirements as a priority in the first phase of the project:

(a) The highly probable requirement; (b) Prospective assessments; (c) IAS 39 retrospective assessment; and (d) Separately identifiable risk components.

All other hedge accounting requirements remain unchanged. A company shall apply the exceptions to all hedging relationships directly affected by interest rate benchmark reform.

The Group shall apply these amendments for annual periods beginning on or after 1 January 2020 with earlier application permitted.

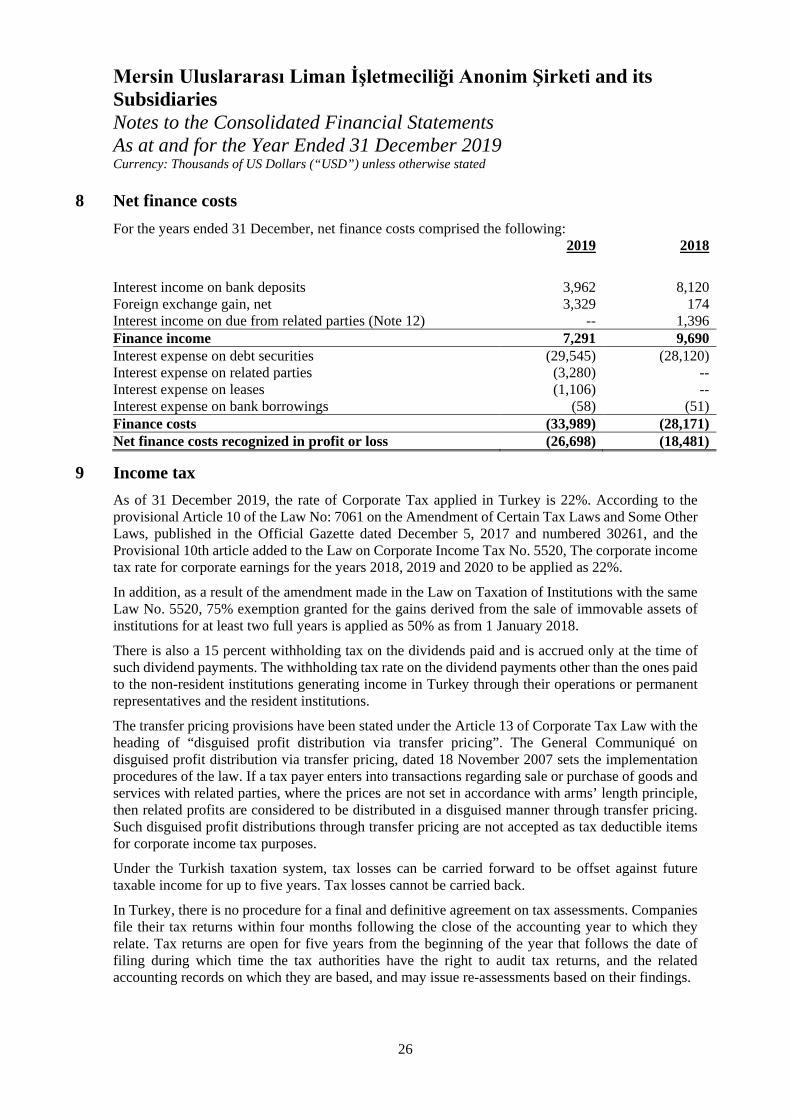

5 Measurement of fair values

A number of the Group’s accounting policies and disclosures require the measurement of fair values, for both financial and non-financial assets and liabilities. When applicable, further information about the assumptions made in determining fair values is disclosed in the notes specific to that asset or liability.

The Group management regularly reviews significant unobservable inputs and valuation adjustments. If third party information, such as broker quotes or pricing services, is used to measure fair values, then the valuation team assesses the evidence obtained from the third parties to support the conclusion that such valuations meet the requirements of IFRS, including the level in the fair value hierarchy in which such valuations should be classified.

Significant valuation issues are reported to the Group management.

When measuring the fair value of an asset or a liability, the Group uses market observable data as far as possible. Fair values are categorized into different levels in a fair value hierarchy based on the inputs used in the valuation techniques as follows.

• Level 1: quoted prices (unadjusted) in active markets for identical assets or liabilities.

• Level 2: inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices).

• Level 3: inputs for the asset or liability that are not based on observable market data (unobservable inputs).

Mersin Uluslararası Liman İşletmeciliği Anonim Şirketi and its Subsidiaries Notes to the Consolidated Financial Statements As at and for the Year Ended 31 December 2019 Currency: Thousands of US Dollars (“USD”) unless otherwise stated

25

5 Measurement of fair values (continued)

If the inputs used to measure the fair value of an asset or a liability might be categorized in different levels of the fair value hierarchy, then the fair value measurement is categorized in its entirety in the same level of the fair value hierarchy as the lowest level input that is significant to the entire measurement.

The Group recognizes transfers between levels of the fair value hierarchy at the end of the reporting period during which the change has occurred.

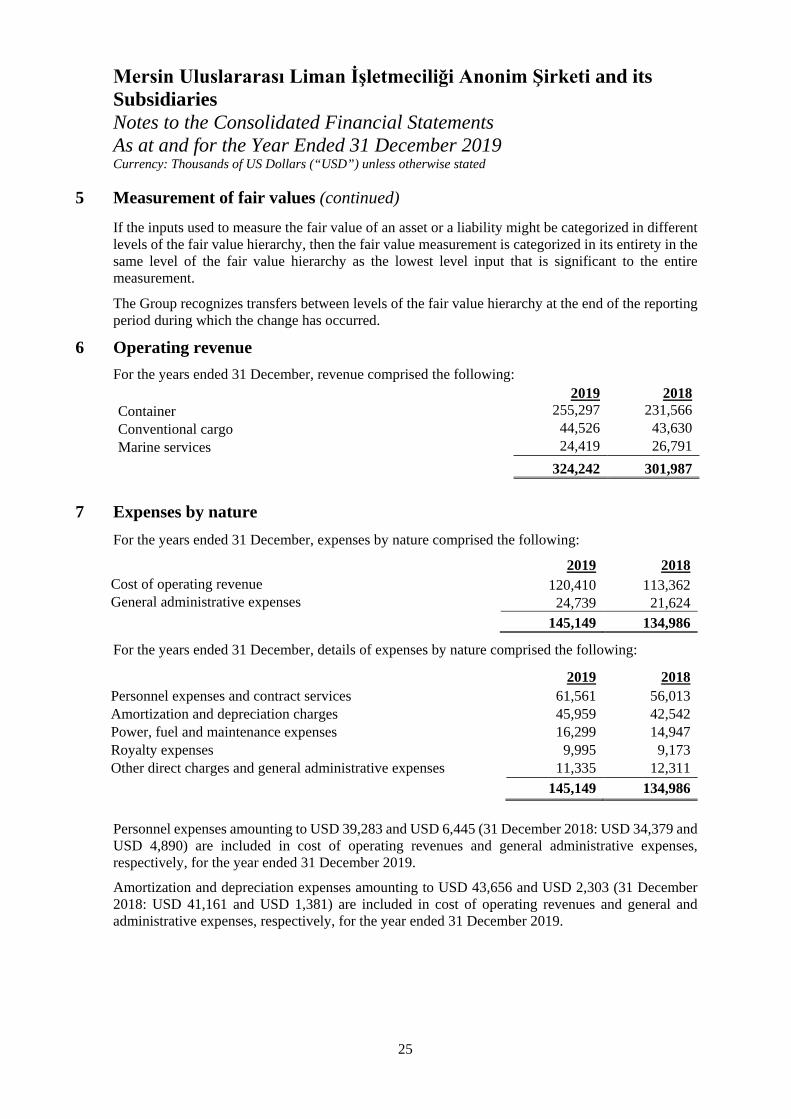

6 Operating revenue For the years ended 31 December, revenue comprised the following:

2019 2018 Container 255,297 231,566 Conventional cargo 44,526 43,630 Marine services 24,419 26,791

324,242 301,987

7 Expenses by nature For the years ended 31 December, expenses by nature comprised the following:

2019 2018 Cost of operating revenue 120,410 113,362 General administrative expenses 24,739 21,624 145,149 134,986

For the years ended 31 December, details of expenses by nature comprised the following:

2019 2018 Personnel expenses and contract services 61,561

56,013