mergers, acquisitions and capital raising in mining and … · americas mining & metals...

TRANSCRIPT

Mergers, acquisitions and capital raising in mining and metals2013 trends2014 outlookChanging gear

About this study• The data is primarily sourced from ThomsonONE.com.• Unless otherwise stated, all values are in US dollars.

Mergers and acquisitions (M&A)• Only completed deals are included. Deals identifi ed as

incomplete, pending, partly incomplete, conditional or intended as of 31 December 2013 were excluded.

• The acquirer country is based on the ultimate owner’s geographic headquarters. The target country is determined by where the primary targeted asset or company is located.

• Country-based refers to domestic and inbound deals.

• A country’s acquisition refers to domestic and outbound deals.

• Commodity analysis is based on the company’s primary commodity focus.

• The value of M&A activity by commodity includes deals where the given commodity is the acquirer and/or target’s primary commodity. Commodity charts illustrate the value of deals where the given commodity is the target.

• The data does not capture the value of transactions where this information is not publicly available.

• “Megadeals” refer to all deals with a value equal to, or greater than, $1b.

Capital raisingThe primary source for this data is ThomsonONE. Certain details have been supplemented with information from company and stock exchange websites and major business press. Only completed transactions are included.

• Only original Initial Public Offerings (IPOs) — the fi rst time that a company issues equity to the public — are included in the IPO analysis. Proceeds are allocated to the primary exchange of listing.

• Equity issues are geographically categorized by the primary exchange where the issuer’s stock trades, except where stated. Where a company offers Global Depositary Receipts or American Depositary Receipts, the issue is allocated to the destination market of those shares.

• Loan data and proceeds include refi nancing and amendments to existing debt, and are as per ThomsonONE intelligence. Proceeds are allocated to the geography of the borrower.

• All credit rating references are to Standard & Poor’s long-term issuer ratings, unless otherwise stated.

Notes on the data:

Note: The data is primarily sourced from ThomsonONE, $ refers to US dollars.

This EY study examines transactions and fi nancing in the mining and metals sector in 2013, and discusses the outlook for 2014.

It provides an in-depth analysis of the major global mining and metals transactions, capital markets and resulting capital fl ows, by considering mergers and acquisitions (M&A), initial public offerings (IPOs), secondary equity offerings, bonds and loans. It also provides an analytical breakdown by commodity.

Mergers, acquisitions and capital raising in mining and metals — 2013 trends, 2014 outlook

This report was authored by:

And thank you to the EY Global Mining & Metals team for their support.

Lee DownhamGlobal Mining & MetalsTransactions LeaderTel: +44 20 7951 [email protected]

Robert StallAmericas Mining & Metals Transactions LeaderTel: +1 404 817 [email protected]

Jodie EldridgeM&A Analyst, Mining & Metals Tel +61 2 9248 4423 [email protected]

Mike ElliottGlobal Mining & Metals LeaderTel: +61 2 9248 [email protected]

Kunihiko TaniyamaJapan Mining & Metals Transactions LeaderTel: +81 3 4582 [email protected]

Nicky CrabtreeAssistant Director, Mining & MetalsTransactions Advisory ServicesTel: +44 20 7951 [email protected]

Emily ColborneStrategic Analyst, Mining & MetalsTel: +44 121 [email protected]

Celeste van der WaltSenior Researcher, Mining & MetalsTel +27 11 772 3219 [email protected]

Paul MurphyAsia-Pacifi c Mining & MetalsTransactions LeaderTel: +61 3 9288 [email protected]

Contents ThemesExecutive summary 6Spotlight: Alternative fi nancing 10Q&A with Silver Wheaton Corp. 14Spotlight: The window of opportunity 18Mergers & acquisitions 22Capital raising 32Outlook 40

Commodity analysisAluminium 44Coal 46Copper 48Gold 50Iron ore 52Nickel 54Potash/phosphate 56Silver/lead/zinc 58Steel 60Uranium 62

6 | Mergers, acquisitions and capital raising in mining and metals

2013: A year of calibration and repositioningWe look back at 2013 as an infl ection point, a year when management and investors fi nally came to terms with a new investing paradigm.

The extreme price volatility and rapid changes to the global economy that defi ned 2012 persisted through 2013.Year-end reporting announcements were littered with headlines of impairments and recriminations that forced changes in strategy and senior management across many of the industry’s participants during 2013.

As a result, we saw investing activity contract during 2013, where the risks were just too great given the moving base on which decisions needed to be made. Acquisition plans were not supportable and as a result, few deals were pursued. As the year progressed, even divestment plans were scaled back as it became clear that price expectations could not be met, and as balance sheets became less stressed due to refi nancing and stronger cash generation in the second half of the year.

2013 marks the tipping point for the sector, with many investors calling it the bottom of the market. This investment “inertia” is clear in the underlying deal volumes and values for the year,

which, excluding the all-share merger of Xstrata and Glencore International, were down 25% and 16% year-on-year (y-o-y) to 702 and $87.3b, respectively.

Capital raising followed a similar trend, with only a 9% increase in total proceeds to $272b, largely due to some exceptional loan refi nancings, and a 9% decrease in the total volume of issues to the lowest level seen since 2008. There were few new investments in the sector and the bulk of capital raised during 2013 is being used to refi nance existing facilities.

This pull-back in risk capital hit the junior sector hardest, with equity markets providing little support. Proceeds from secondary issues by juniors fell 43% y-o-y (from an already low base) with an inevitable tightening of global exploration spend. Investors are looking for low risk, near-term, high-yield opportunities, which the early-stage junior mining sector cannot offer at present. To bridge this gap, alternative capital raising options provided some reprieve but did not satisfy the level of capital being demanded across the sector.

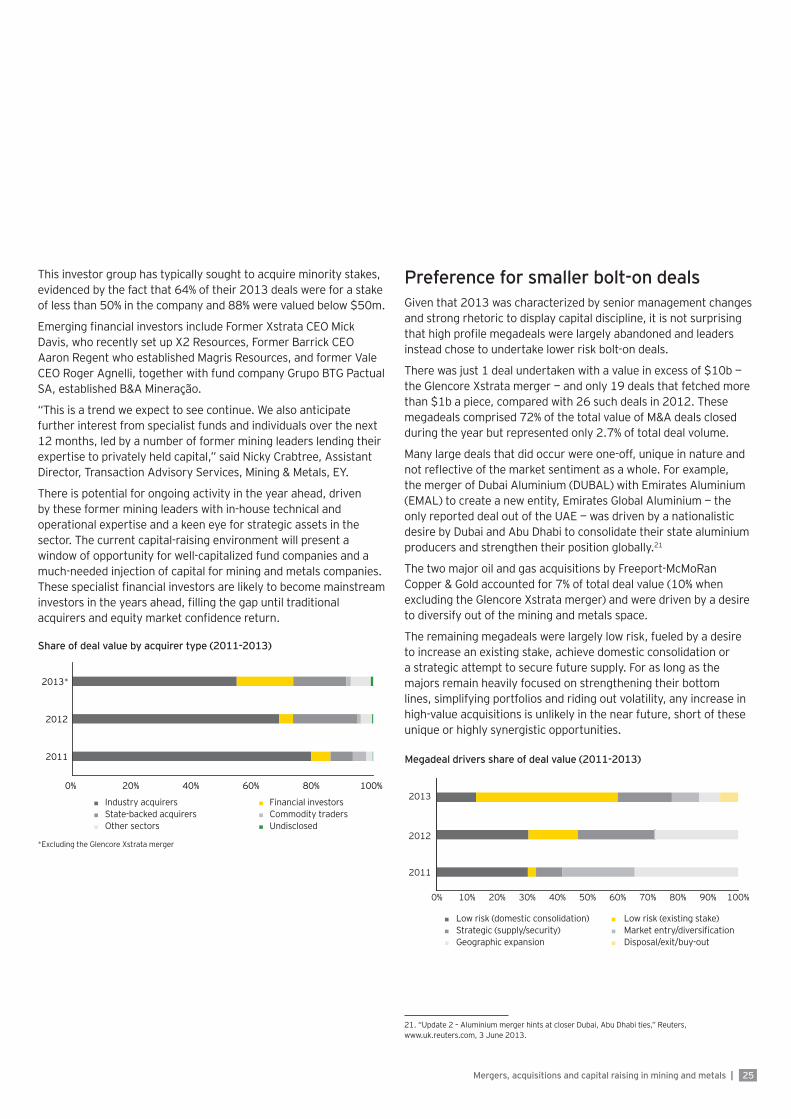

However, the continued rise of private capital in the sector, including the increased share of total M&A undertaken by fi nancial investors (by value) from 5% in 2012 to 19% in 2013, supports the view that 2013 marks the tipping point for the sector, with many of the providers of such capital calling the bottom of the market.

Executive summary

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*Volume 475 596 564 701 903 919 1,047 1,123 1,008 941 702Value ($m) 46,182 26,350 65,430 175,713 210,848 126,884 60,035 113,706 162,439 104,014 87,309 Average value ($m) 97 44 116 251 233 138 57 101 161 111 124Median value ($m) 4.4 3.1 4.8 6.2 7.2 6.0 3.2 5.2 5.6 5.0 3.8

Volume and value of deals (2003-2013)

*Excluding the merger between Glencore International and Xstrata (the “Glencore Xstrata merger”)

Mergers, acquisitions and capital raising in mining and metals |

Deal inertia drives M&A activity down2013 marked the third consecutive year of declining M&A activity in the mining and metals sector: deal volume dropped 25% y-o-y. While the value of deals increased by 20% to $124.7b, this increase was primarily due to the completion of the Glencore Xstrata merger. Excluding this deal, value decreased 16% to $87.3b, highlighting the contraction in investment spend across the sector during 2013.

Although there were notable exceptions, such as First Quantum Minerals’ acquisition of Inmet Mining, the majority of deals that completed in 2013 were largely smaller, low-risk acquisitions fueled by a desire to increase an existing stake, achieve domestic or inter-regional consolidation, or a strategic attempt to secure future supply.

As diversifi ed mining companies seek to optimize portfolios, many of the industry’s large producers announced signifi cant divestment progams. During 2013, the industry’s top fi ve diversifi ed mining majors completed $6.3b1 of divestments, while $5.5b of deals have been agreed and are expected to complete during 2014, with the Las Bambas divestment by Glencore Xstrata being the last major

1. This includes the $1.8b sale of Vale’s Norsk Hydro shares, which falls outside of the M&A data within this report.

7

divestment still in the process of fi nding a buyer. This activity, together with other rationalization measures and an upturn in iron ore prices toward the end of 2013, has taken the pressure off earnings and balance sheets, easing the pressure to divest.

Although the successful exit of many divested assets suggests deals are there to be done, there is strong evidence that a gap remained between the valuation expectations of buyers and sellers during 2013. Intensifi ed volatility in metals prices continues to drive a disparity in asset valuation expectations and, as a consequence, buyer and seller differing views on price remain a drag on M&A activity.

The opportunity for fi nancial investors continuesThe year in review proved to be of great opportunity for fi nancial investors who increased their share of total M&A value from 5% in 2012 to 19% in 2013. These investors can act counter-cyclically, attracted by the prospect of potentially strong returns driven by low asset valuations.

“2013 was a year of calibration and repositioning. Those mining companies who

had a change of leadership refreshed their strategies and focused on productivity and

capital optimization rather than pursuing M&A. Across the sector we saw the capital

raising environment tighten for those without an investment grade credit but,

looking forward, we expect to see a steady improvement in market conditions.”

Lee DownhamMining & Metals Global Transaction Advisory Services Partner

UKI

Capital raising by asset class - proceeds $b (2007-2013)

2007 2008 2009 2010 2011 2012 2013 ChangeIPOs 21,400 12,406 2,987 17,948 17,449 1,388 815 -41%Follow ons 66,802 48,751 73,806 49,705 49,745 25,950 26,233 1%Convertibles 12,865 12,238 14,431 5,477 2,365 3,537 7,738 119%Bonds 36,358 38,146 61,016 72,502 83,804 112,539 87,890 -22%Loans 110,787 171,691 62,420 183,875 187,059 105,981 148,881 40%Total 248,212 283,232 214,660 329,507 340,422 249,394 271,557 9%

8 | Mergers, acquisitions and capital raising in mining and metals

Financial investors (including sovereign wealth funds) undertook fi ve of the 19 megadeals (>$1b) in 2013: Lizarazu’s and Receza’s joint $3.6b investment in Polyus Gold International; investments in Uralkali by Onexim Group ($3.5b) and Chengdong Investment Corp ($2b); Samruk-Kazyna’s $1.7b investment in Kazzinc; and Crispian Investments’ $1.5b investment in Norilsk Nickel.

Other smaller deals of this nature included B&A Mineração, a venture headed by the former CEO of Vale Roger Agnelli, and Grupo BTG Pactual’s joint purchase of Rio Verde Minerals Development Corp for $36m. In addition, Mick Davis (Former Xstrata CEO) announced his intention to establish X2 Resources, while Aaron Regent (former CEO of Barrick Gold Corp) formed investment company Magris Resources, demonstrating the growing relevance of mining-focused private capital.

So, while 2013 will be known as the year in which this capital was raised, the infl ection we now see in the market is likely to mean that 2014 is the year when we start to see this capital being deployed.

Debt refi nancing driving an improvement in balance sheet strengthAlthough bank lending increased 40% y-o-y to $149b, this headline includes a large refi nancing of $17.3b by Glencore Xstrata — reportedly the largest corporate loan refi nancing in any sector in Europe for over fi ve years.

About half of the total loan proceeds were amendments, increases and extensions to existing credit agreements, with only $33b of lending coming in the form of new agreements for project fi nancing, acquisitions and capital expenditure.

A total of $74b of the refi nancing completed in the year was largely refi nancing on improved terms, which pushed out maturities and lowered yields to strengthen balance sheets. Average spreads on non-leveraged loans narrowed to 147bps in 2013 from 174bps in 2012. Intense competition among banks to secure relationships with industry heavy-weights meant that investment grade borrowers attracted greater fl exibility and, in some cases, better pricing, than corporate bonds could offer.

Syndicated project fi nance that closed in 2013 reached $13.4b, up from $5b in 2012. The largest fi nancings went to steel and aluminium projects in India and the Middle East, respectively. A small number of iron ore, gold and base metals mines in Africa, South America and Australia also attracted project fi nance on a smaller scale. Although this increase is well below 2011 levels, it is a move in the right direction. This positive indicator, coupled with greater competition from banks to fund the industry’s advanced and de-risked projects, supports a stronger appetite for lending going into 2014.

Convertible loans providing a rare source of capital for exploration and development companiesConvertible bond raisings experienced a 32% increase in volume and a massive 119% increase in proceeds, albeit from a low base in 2012.

Share of deal value by acquirer type (2011-2013)

Industry acquirersState-backed acquirersOther sectors

Financial investorsCommodity tradersUndisclosed

0% 20% 40% 60% 80% 100%

2011

2012

2013*

*Excluding the Glencore Xstrata merger

-2468

10121416

-20406080100120140160

Proceeds Number

Proc

eeds

($b)

Num

ber

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Convertibles became increasingly popular in 2013 as investors could secure coupon rates comparable with those of vanilla high-yield bonds, thereby effectively receiving free options as an inducement. This bucked the historical trend of issuers paying lower coupons to compensate for the potential equity dilution. The average coupon paid in 2013 was 9%, with one issue offering 22.5%. This partly refl ects the high proportion of early-stage,

9Mergers, acquisitions and capital raising in mining and metals |

unrated and therefore higher risk companies that are issuing convertibles, and in some cases are prepared to accept the highly dilutive equity valuations in the absence of many alternatives. As a result, any lack of confi dence in the upside potential of the share price is compensated for by the high yield that investors receive for the debt component.

Outlook - long term health in the balanceThe mining and metals sector is entering 2014 with a more positive outlook: confi dence in the global economy is improving, companies have taken action to deleverage balance sheets and the industry-wide focus on productivity and effi ciency should begin to yield results. As a result, we expect the gradual strengthening of mining and metals equity valuations to continue and the increased availability of capital.

However, continued economic volatility is also expected in 2014 due to Eurozone economics, Chinese economic rebalancing and US Federal Reserve policies regarding the tapering of quantitative easing. As supply and demand struggle to return to post-supercycle equilibrium, we expect further price volatility to occur for at least the next two years. This will see caution prevail: any uplift in M&A activity and improvement of capital raising conditions will be gradual and will require innovation in pricing to tame volatility.

Conditions in the bond markets are likely to tighten if global interest rates begin to rise should quantitative easing begin to taper. “We expect to see a greater proportion of the sector’s funding to come from equity through follow-on raisings, although a widespread return to equity will require a return of confi dence at the top of the industry along with some high profi le success stories among junior developers. If this occurs, it should translate into optimism and risk-taking at the bottom,” said Lee Downham, Mining and Metals Global Transaction Advisory Services Partner, UKI.

Similarly, we are seeing strong appetite from debt providers, with increased competition among banks likely to improve access to leveraged loans for quality mid-tier mining companies and developers. However, given the strict criteria applied by these investors, it is questionable if the availability of these funds will support industry needs in their entirety.

We expect growth in M&A activity during the fi rst half of the year to be driven by fi nancial investors and equity-backed alternative capital providers as outlined in our Spotlight section: Alternative fi nancing. This growth will not only be driven by anticipated longer term commodity price recovery but also by the application of in-house technical experience to drive operational, technical and

The Capital AgendaBased around four dimensions, the capital agenda helps mining and metals companies consider their issues and challenges and understand their options to make more informed capital decisions.

1. Preserving capital: reshaping the operational and capital base

2. Optimizing capital: driving cash and working capital and managing the portfolio of assets

3. Raising capital: assessing future capital requirements and assessing funding sources

4. Investing capital: strengthening investment appraisal and transaction execution

How organizations manage their capital agenda today will defi ne their competitive position tomorrow.

EY works with clients to help them make better and more informed decisions about managing capital and transactions strategically in a changing world. Whether you are preserving, optimizing, raising or investing capital, EY’s Transaction Advisory Services brings together a unique combination of skills, insight and experience to deliver tailored advice attuned to your needs — helping you drive competitive advantage and increased shareholder returns.

fi nancial infl uence. This has the potential to be the most exciting story of 2014. Will we see the deployment of capital so feverishly raised during 2013? And, if so, will it begin to drive new investment activity across producers?

With low levels of new capital and new investment, the mining sector may well be sowing the seeds for the next boom as supply falls short of demand. Will fi nancial investors, private capital and other counter-cyclical investors be able to fi ll this capital shortfall in 2014? It is EY’s view that a more patient form of capital creation is essential for the sector’s long-term health. This capital will be required to both replace the “hot money” that has been leaving the sector, as short-term returns fall from their record level, and provide capital for the next projects required to restore extinguishing supply or meet future demand growth.

10 | Mergers, acquisitions and capital raising in mining and metals

Alternative fi nancingThe majors found little diffi culty in securing funding through traditional means (primarily the debt markets) in 2013. But with equity markets increasingly taking a short-term view, juniors are necessarily looking for alternatives.

Spotlight

Lack of confi dence in the industry’s ability to yield satisfactory near-term returns has resulted in a dramatic pull back in public equity funding to the sector. Further, efforts by the majors to restore that confi dence, including through a focus on optimizing existing assets, have resulted in a slowdown of buying or investing on their part, particularly in long-lead exploration.

With much of the industry focused on optimization, it should be of little surprise that funding sources designed to achieve just that have seen an increase in demand. Streaming and royalty agreements aim to unlock incremental value through the monetization of non-core metals production; hence we are seeing the streaming model evolve and grow in tune with the current needs of the industry.

Further, a lack of clear consensus over the near-term direction of commodity prices – and more importantly, whether the bottom of the latest cycle has been reached – continues to inhibit the wholesale return of both public equity and industry-led M&A. But equally, this impasse has created exceptional opportunities for

capital providers with confi dence, patience and fi nancial capacity to take a long-term view on the sector, whether from an investment returns or supply security perspective.

Known brands, new vehiclesIn the private sphere, where arguably greater freedom exists to take such a view, veteran industry expertise is combining with private equity to inject capital into the sector through strategic acquisitions. Some examples include:

• X2 Resources, led by ex-Xstrata CEO Mick Davis and backed by TPG and Noble Group

• B&A Mineração, the venture of Roger Agnelli (ex CEO of Vale) and BTG Pactual

• QKR Corporation, the fund headed by ex-JP Morgan Chase banker Lloyd Pengilly, with Andre Liebenberg (former BHP Billiton), and backed by a consortium of investors including Qatar Holdings

• Magris Resouces, the fund set up by Aaron Regent (ex CEO of Barrick Gold Corp)

11Mergers, acquisitions and capital raising in mining and metals |

In addition, Resource Capital Funds, a mining-focused private equity (PE) fi rm, has $2.04b of committed capital in its latest fund to invest in the mining sector. This represents an estimated $4.6b of capital deployed – or waiting to be deployed - by this group alone.

The traditional private equity model has historically played a relatively small role in the upstream mining sector, but depressed valuations have increased speculation that this trend may change. However, while there may be discrete deals of this nature, with traditional PE looking at specifi c deals, our view is that “private capital” funds, of the type described above, are the ones that will be most active in the sector. These investors are deploying patient capital, adopting a longer-term investment horizon and seeking to establish a robust operational structure that supports margin-led growth, rather than pursuing the strategy of “growth for growth’s sake” which characterized industry growth over the previous decade. For mainstream PE, it is about backing the right management and funding an asset with short-term exit potential; those types of opportunities are few and far between. Strategic offtakers, such as state-backed entities and commodity traders, typically have greater private visibility over their particular near- and long-term demand picture through their customer base. This gives them the confi dence to invest now to secure future supply.

Exploration in crisisEarly-stage exploration companies have historically relied on public equity markets for funding. However, challenging market conditions mean that few institutional investors are prepared to take a risk on early stage investment and few companies are keen to issue further shares at such low valuations. As a result, explorers are left with few options: cancel exploration programs to preserve precious cash resources; or seek “last resort” fi nancing options that typically delay the dilution impact but of course come at a cost. Consequently, there has been both a dramatic decline in exploration expenditure over 2013,2 and an increase in the pursuit of equity-linked fi nancing options, such as standby-equity agreements and convertible instruments. Risk capital is unlikely to be available on a large scale in 2014, but there is an increasingly large pool of family offi ces, private equity providers and venture capitalists that provide early-stage seed funding, often linked to certain conditions and achievement of project milestones. However, access to this group of investors can be challenging, given the private and highly selective nature of their investments.

2. “SNL Metals Economics Group’s 24th Corporate Exploration Strategies estimates worldwide exploration budgets to fall 29% to $15.2b in 2013,” SNL Metals Economics Group press release, 24 October 2013.

“Alternative fi nance, while not a new phenomenon, has increasingly become mainstream in 2013. Unsupportive, “short-termist” equity markets have spawned a greater variety of funding structures and capital providers at a time of critical need among the industry’s advancing juniors.”

Michael ElliottGlobal Mining & Metals Leader

Australia

12 | Mergers, acquisitions and capital raising in mining and metals

Evolving landscapeDifferent fi nancing options are suited to particular stages of the development cycle and critically to the individual needs of the asset, each with their own risks and costs attached. Companies today typically require non-dilutive, committed, fl exible, value-accretive funding options where investor objectives are aligned with the long-term goals of management. Portfolio funding approaches are often adopted by advancing companies as a means of managing risks and costs.

Importantly, funding options are becoming increasingly fl exible and innovative in their structure, evolving to meet the changing demands of the industry. Streaming agreements form such an example: Vale’s landmark $1.9b agreement with Silver Wheaton Corp marked a step change in the scale and scope of streaming deals.3 For insights into Silver Wheaton Corp’s investment strategy, refer to the Q&A with Randy Smallwood, President & Chief Executive Offi cer, and Gary Brown, Senior Vice President & Chief Financial Offi cer, Silver Wheaton Corp.

Streaming represents a non-dilutive, non-controlling means of securing upfront capital and unlocking value, typically from non-core production. However, no form of fi nancing is without its costs and limitations. Streaming agreements limit the project owner’s future exposure to the streamed metal, and potentially impact a project’s margins once in production, through the loss of by-product credits. Further, Standard & Poor’s (S&P) has recently announced its decision to treat streaming agreements as debt (under prescribed circumstances), which may deter leveraged producers from undertaking streams. Other rating agencies, including Moody’s, have not followed suit, so the extent to which this move by S&P will inhibit the growth of streaming in 2014 remains to be seen.

The focus of stream providers remains typically on producing and near-producing assets that present low political risk, and suffi cient operating margins and earnings stability to deliver throughout cycles. However, earlier stage options, such as the “early deposit” structure agreed upon by Silver Wheaton and Sandspring Resources in November 2013,4 are also emerging.

3. “Silver Wheaton acquires gold streams from Vale’s Salobo and Sudbury Mines,” Silver Wheaton Corp press release, 2 May 2013.4. “Silver Wheaton completes early deposit gold stream agreement with Sandspring Resources,” Silver Wheaton press release, 11 November 2013.

Streams have arguably been the story of 2013, although their contribution to the overall sector funding remains small: we estimate that about $2.4b of upfront capital was injected into the sector via streams in 2013. However, this is not to downplay its importance. While relatively small compared with traditional bank lending, project fi nance and equity, streaming as a form of alternative fi nance has become signifi cant, dwarfi ng the level of investment into the sector from standby equity distribution agreements (SEDAs) or royalties, for example.

Future of alternative fi nancingJust as many of the structures described above have been around for a long time, so they are likely to remain an important component of mining industry funding, going forward. The return of equity markets for early exploration should limit the need for higher cost alternatives, but we believe this may be some way off. If we are adapting to a “new normal” of steadier demand growth and increasing supply complexities, there will be an ongoing need for countercyclical, long-term investment approaches that sustain industry growth through inevitable periods of volatility.

Demand is only one side of the equation; supportive conditions would need to persist for fi nance providers to be able to secure and provide capital on attractive terms. Circumstances in 2013 have given rise to an environment of low confi dence among the many and high confi dence among the few – translating into the potential for opportunistic buying at depressed valuations.

We expect these circumstances to persist through 2014: the window of opportunity for private capital investment is clearly now and capital is ready and waiting to be deployed, albeit only to the best projects and teams. There are signals that juniors are adapting and responding to the changing funding environment - from better management of expectations, scaling back of project plans, and careful cost management, to better “storytelling.” As a result, in 2014, we expect to see continued strong growth in alternative fi nancing to the industry.

13Mergers, acquisitions and capital raising in mining and metals |

Note: Stages refer to exploration, development, construction, production.

Alternative fi nancing options utilized in 2013

Type Typical structure Benefits/drawbacks to company Example providersStage

E D C P

Standby equity agreements

Deferred equity and equity-backed loans. Option to issue shares to the provider over a multi-year period, at the issuer’s discretion.

Issuer is in control of timingDelayed dilution can adversely impact liquidity and share price

• YA Global• Darwin Strategic• Dutchess Opportunity Cayman Fund

Earn-in agreements

Partner (often a major) funds exploration activities over a specified time period, thereby earning the right to a pre-determined share of project ownership.

Ability to progress exploration projectsPotential exit optionExit risk – earn-in partner can elect notto continuePotential dilution

Development finance

Loans, strategic equity and convertibles. Banks may offer ancillary services (e.g., community engagement strategies, environment and social risk management).

Strong vote of confidence in the project and managementStringent environmental and social requirements; extensive diligence required

• International Finance Corporation• China Development Bank• European Bank for Reconstruction

and Development• International Development Corp of

South Africa

Offtake Terms vary but typically include exclusive right to percentage of future production. Can, but may not, include advance payment. Can be structured as take-or-pay.

Guaranteed source of demandOften a requirement for project financeCan include minimum stipulations – e.g., minimum price and volume, hedging

• Strategic state buyers• Private capital – e.g., Red Kite, Blackrock• Banks• Customers• Traders

Equipment/EPCM Equipment leasing agreements and project investment by equipment/service providers. Typically include operating leases, sale and lease-back, hire purchase, secured term loans, RCFs, asset-based inventory financing and equity investments.

Can reduce capital outlays at construction phaseSupply chain default risk - financial and legal due diligence required

• Equipment suppliers or EPCM• contractors – e.g.,• GE Capital• Macquarie Bank• Caterpillar Financial Services• Standard Bank

Royalties Upfront payment in return for a percentage of either future revenues or profits, or the value of the product produced

Long-term, passive investments – no dilutionNo interest costsPayments must be made – regardless of future profitabilityReduces future cash flows

• Royal Gold• Franco-Nevada• Premier Royalty• Anglo Pacific Group• Callinan Royalties• American Bullion Royalties• Royalco Resources• Gold Royalties Corp

Streams Upfront payment plus ongoing payments in return for a right to a percentage of production from an identified asset (usually life-of-mine). Typically precious metals by-product.

No equity dilution or interest costsRetain operational controlMonetization of non-core productionOngoing payments designed to cover cost of productionS&P treats as debt (fromNovember 2013)Terms need to be carefully negotiatedLoss of by-product credits

• Silver Wheaton• Franco-Nevada• Royal Gold• Sandstorm Gold• Sandstorm Metals + Energy

Alternative fi nancing options The table below outlines some of the options that are being adopted by mining and metals companies in the current environment. These options are explored in more detail in EY’s contributions to Mining Journal’s “Global Mining Finance Guide 2014.”

14 | Mergers, acquisitions and capital raising in mining and metals

Q&A

President & Chief Executive Offi cerRandy Smallwood

Senior Vice President & Chief Financial Offi cerGary Brown

Interview

With major producers under pressure from shareholders to pull back capital investment, combined with slow equity markets for developers, timing seems perfect for patient, counter cyclical investors such as Silver Wheaton. Do you agree, and how long do you see this “window of opportunity” being open for investors like Silver Wheaton?

“I think we’ve proven that this model works across the cycle. The current state of the industry in terms of reduced capital spending, lack of equity support and a challenging debt environment has made this market about as good as it can be for us and created all sorts of investment opportunities for us.

We always compete as a source of capital against debt and equity and in most markets we provide an attractive form of capital with one of the key characteristics being the unlocking of hidden value.

The feeling we get is that we are close to the bottom. We see fourth quartile producers hurting, and marginal projects cancelled or put on hold. In the precious metals space, we really feel that commodity prices cannot go down much further because it’s driving supply side pressure, so it’s only a matter of time before it starts moving up again.

On the demand side of the equation, there is a continued appetite for metals out there, which will apply upward pressure on commodity prices, so I am hopeful that by the end of this year we will start seeing a move back up off the low price environment that we are in right now.

I have been in the industry for close to 30 years now and it’s amazing how many times the experts can be wrong with respect to predicting commodity prices. You have to rely on your intuition to a certain extent, but more importantly, you need to focus on making good long term investments that are able to withstand the short term fl uctuations in commodity prices.” Randy Smallwood

Given the desire among many investors in major producers to reduce invested capital, do you see a greater opportunity for Silver Wheaton to come into some of these large assets through a streaming arrangement?

“I think that we have already touched upon the point that equity investors have defi nitely pulled back from this space, so the availability of capital from equity investors has defi nitely been reduced over the last 12 months. That in itself creates an opportunity for competing forms of capital like metal streaming. On the debt side, the companies that can attract debt are generally trying to reduce the fi nancial risk in their capital structures and that combination does create a more favorable environmental for metal streaming.

15Mergers, acquisitions and capital raising in mining and metals |

with Silver Wheaton Corp.the operating margins of the asset. We want mines that will deliver product to us through both the highs and the lows of the commodity price cycles. We have been in the industry long enough to know that commodity prices are cyclical and so the fi rst criteria that we look at is where the mining operation is expected to fall relative to the respective cost curve for the primary metal being mined. We are very focused on making investments in operations that lie in the bottom half of their respective cost curves.

To expand on that a little bit, if it is a copper mine that has silver or gold by-product production, we look at the copper cost curve and determine where this asset fi ts relative to all the other copper mines in the world, and we’ll be interested in the assets at the bottom half of the cost curve because those are the ones that will continue to operate and deliver through highs and more importantly through the lows of the commodity price cycle. It’s the fourth quartile and some third quartile producers that suffer and sometimes have to shut down during the lows of the commodity prices.

When we look at our existing portfolio, about 90% of our production comes from assets in the bottom half in the respective cost curves. With a portfolio that is comprised of 24 different assets, 19 in operation and 5 at various stages of development, to have that high a concentration in the bottom half of the cost curve, we would argue, it is one of the highest quality portfolios in the mining industry.” Randy Smallwood

And what about management, how important are good management teams to your investment decision?

“We are very focused on making sure that we invest into good partners, but one of the things we always have be sensitive to, is the fact that we do not select the management. So although these mines may have expert management right now, we do not know who is going to be operating these mines fi ve years from now. We do not have that control. Management is very important to us, and we work with strong partners but we also want assets that are able to withstand weak management and changes in management.

And so, again, that’s one of the objectives of being down on the bottom half of the cost curve, it gives it some capacity to withstand whatever gets thrown at these assets including political risks, tax changes, low commodity prices and poor management - we want to make sure that they are strong enough to withstand the impact of all of those.” Randy Smallwood

While there have been capital spending cuts, a lower commodity price environment results in less operating cash fl ow being generated by mining companies to fund capital projects that have not been cancelled. As a result, there is still signifi cant demand for capital in this space.” Gary Brown

And how about assets which are already in production, where a release of capital via a streaming agreement is being considered. Do you see an increase in those types of transactions?

“I think there is a bit of a paradigm shift happening in the mining industry in general. Historically mining companies have focused on growth without necessarily focusing on return on invested capital. And now I see there being a higher focus on generating returns on invested capital. With streaming’s ability to unlock value and reduce the mining company’s equity exposure to a particular project, I think that does open up additional opportunities to us.” Gary Brown

You have often been quoted as saying that a streaming arrangement creates shareholder value for both the streamer and the seller. Why do you think this is?

“There are two principal areas that highlight that value for shareholders:

Firstly, precious metal companies typically have a lower weighted average cost of capital than base metal companies and hence precious metals that are hidden within a base metal asset typically wind up getting valued with a higher weighted average cost of capital. So when you bring them into a precious metal company like Silver Wheaton, they have a lower weighted average cost of capital resulting in a higher net asset value.

In addition, precious metal companies tend to trade at higher market multiples than base metal companies, so when you take silver from a base metal company and bring it into a precious metals company, there is a creation of value there. This arbitrage was really the founding principle when we created Silver Wheaton back in 2004.

So those two characteristics haven’t changed through the commodity price cycles - precious metal companies continue to trade at better multiples and they have better access to capital than base metals companies.” Randy Smallwood

What are the key characteristics of an investment for Silver Wheaton, and is there anything that is absolutely critical for you to consider investing?

“In terms of us selecting a mine and making that investment into a mine, the key is the quality of the asset itself, specifi cally

16 | Mergers, acquisitions and capital raising in mining and metals

Risk aversion is driving many investors into safer, more developed mining districts. Do you see Silver Wheaton following this trend, or are emerging markets a key focus for you?

“Yes, we have always been and continue to be focused on assessing all the risks inherent in a potential investment opportunity, including assessing political risk.

When you look at our current portfolio, the majority of the assets are located in the Americas and Western Europe, which represent very safe jurisdictions from a political risk perspective, and we don’t see that changing. We don’t see ourselves expanding to areas that have a high level of political risk associated with them.

We are a precious metals streaming company, but we are focused on the silver side of things and when you look at where silver naturally occurs in the earth’s crust, that’s primarily North and South America. There is signifi cant amount of silver produced in China and Russia. However, those would be places that we would have a tough time consummating a silver stream transaction, unless we had a partner that could indemnify us against any of the political risks that we would be exposed to.

And then you look at Africa which has pockets of high political risks and there is really very little silver produced out of Africa, so there is very little chance that we’ll consummate a silver stream transaction relative to one of those areas. The bottom line is that we continue to see a lot of opportunity in politically stable jurisdictions and those are the opportunities that are at the top of our list.” Gary Brown

Silver Wheaton has 19 streams with operating assets and 5 with development assets. How does Silver Wheaton manage the increased risk associated with those in the development stage, where the ability to exercise operational control is limited?

“We consider all of our agreements as partnerships and we do our best to work with our partners in terms of supporting these projects going forward and when it comes to development assets, our primary security comes from the completion tests and corporate guarantees that are put in place when we close a transaction. These not only ensure that we are protected in terms of these assets getting to market, but also have penalty clauses to compensate us and encourage the asset to be built on time and on budget. Typically we fi nd this structure is adequate to protect us and the investor and to ensure everyone’s interests are aligned.” Randy Smallwood

“And I would just add to that for the development stage assets, we generally don’t advance a signifi cant amount of the upfront funds until permitting is in place, the mining company has secured all the fi nancing required to build the particular project, and construction has commenced.” Gary Brown

With whom do you see Silver Wheaton competing for investment opportunities over the next few years, and do you expect to see much consolidation across the industry in the near term?

“There are a couple of other companies that have adopted our metal streaming model, but they have generally applied it to the gold space. We are a precious metal company focused on the silver space, and so we don’t anticipate as much competition on the silver streaming transactions.

There have been murmurs that other purely fi nancial investors, private equity funds and pension funds have considered entering the metal streaming space, but as Randy alluded to earlier, the key component in making a good investment in metal streaming transactions is assessing the technical aspects associated with the mining operation and the resource itself. We have a world class team of geologists, mining engineers and metallurgists that we deploy in assessing those risks. It is very diffi cult for purely a fi nancial investor to assemble such a qualifi ed team that can focus on that space.

And with respect to the other players that are currently in the space, our key advantage is our size. We are the largest of the metal streaming companies out there. That provides us with the substantial cash fl ow which allows us to grow, it gives us excellent access to the capital markets both debt and equity, and with our highly diversifi ed portfolio, it gives us a little more latitude with respect to risk tolerance. I don’t see the landscape changing signifi cantly from a competitive perspective in the future and I see us as having a number of advantages over the current players.” Gary Brown

Finally, can you tell us a little more about Silver Wheaton as an investment itself? How do you feel the investment opportunity compares to investment into a pure-play silver producer or an ETF?

“Silver Wheaton provides shareholders with a much lower risk profi le than a traditional mining investment and yet still delivers most of the rewards that are traditionally related to a mining investment.

17Mergers, acquisitions and capital raising in mining and metals |

When I compare us to an ETF, the fi rst differentiating factor is that we provide a level of leverage to the precious metal exposure inherent in our portfolio. This leverage arises because we don’t pay fully for every ounce of silver or gold that we gain exposure to upfront. We defer a portion of the payment until the precious metal is actually delivered to us. This characteristic should result in us outperforming a straight investment in bullion which is supported by the fact that the returns we have generated for shareholders since the inception of the Company in 2004 are about three times that generated from an investment in bullion.

We also provide shareholders with exposure to the exploration and expansion upside that our portfolio has shown a propensity to deliver. As we have previously stated, our portfolio is comprised of very good mines and some of them are very young in their development and have all sorts of opportunity for continued growth through expansion and exploration success and we deliver that to our shareholders.

We also have the opportunity to make accretive acquisitions. We continue to grow and add value on a per share basis. One of the key stats that I have always admired is that the shareholders who acquired shares when this company was founded back in 2004 had about 1.5 silver equivalent ounces backing every share. We currently have about 6 silver equivalent ounces underlying each share in this company, highlighting just how accretive our acquisitions have been.

We also pay a dividend which is based on a percentage of operating cashfl ow. With the cost of every ounce of silver or gold being delivered to us being virtually fi xed contractually, basing the dividend on operating cashfl ows provides shareholders with direct participation in both our enviable organic growth profi le and increases in underlying commodity prices. ETFs and bullion investments obviously don’t pay dividends.

As a result of these characteristics, we believe that Silver Wheaton represents the best investment vehicle out there to gain precious metal exposure.” Randy Smallwood

“And I would just add that shareholders are gaining access to the expertise of the company that has not only demonstrated the ability to consummate highly accretive transactions but, has also shown that it has the discipline to avoid investing in assets that don’t deliver shareholder returns.” Gary Brown

18 | Mergers, acquisitions and capital raising in mining and metals

The window of opportunityOnly time will tell if we are witnessing a correction, a restructuring of the sector or just the start of the new normal. The capital decisions that companies make will be the key to their success.

What is certain is that this is a cyclical industry and one where the very factors contributing to the challenges will also force the solution: a lull in investment will eventually lead to a contraction in supply which will, once again, support higher commodity prices and investment.

Meanwhile, there is a window of opportunity for those with confi dence in the sector and access to longer-term, more patient capital. These investors are looking to capitalize on reduced competition for assets, lower valuations and a continued fl ow of divestments from the large cap producers.

This window of opportunity will remain open until equity markets for the sector recover fully and while large cap producers remain cautious about investing. Until then, those with access to patient private capital, including fi nancial investors, will have a free run to take advantage of the current market conditions.

Spotlight

Source: S&P Capital IQ, EY analysis.

0.00.2

0.60.4

1.0

1.41.6

1.2

0.8

1.8Consensusforecast

-1,000

0

1,000500

-500

1,500

2,5002,000

3,0003,500

Net

Deb

t/EB

ITDA

Net Debt/EBITDA

2005

2006

2007

2008

2009

2010

2011

2012

2013

E

2014

E

2015

E

2016

E

Availability of capital to undertake M&ATop 14 globally diversifi ed mining companies leverage and cash fl ow summary

19Mergers, acquisitions and capital raising in mining and metals |

Free cash fl ows have been squeezed over the last 18 months due to low earnings and a record level of investment, which reached its peak during 2012. Across our sample of the top 14 globally diversifi ed mining and metals companies, each company allocated on average $6.3b5 to capital expenditure, primarily on large-scale, tier-one organic growth projects in an environment where costs escalated and initial budgets were exceeded. Leverage consequently soared as companies took advantage of the favorable lending conditions to fund growth.

The industry has quickly reacted to this scenario: major producers are focused on achieving cost-saving targets, productivity improvements, divestments and scaling back capital expenditure, while pursuing only the top-tier projects and doing so incrementally. As a result of these actions, consensus forecasts show improved cash fl ows, after capital investment, albeit modestly during 2013 and then dramatically after 2014 to levels more conduciveto investment, particularly as leverage begins to fall over the same period.

However, while conditions lend themselves to a return to investment, a complex capital allocation challenge exists where investment decisions are tougher than ever. Companies are challenged to identify a unique strategy that sets them apart from their peers in an uncertain economic and commodity price environment, where returns can be marginal.

5. Source: S&P Capital IQ, EY analysis.

In the immediate aftermath of recent market conditions and changes to management, we are witnessing a greater focus on yield. Dividends and share buybacks are being used to appease shareholders and compensate for a perceived under-delivery on capital returns. As the graph below shows, beyond 2014, the forecast ramp-up in dividends is highly affordable against the expected improved cash fl ows; a much lower percentage of cash is being paid out as dividends despite the relative level increasing signifi cantly.

So the question is: how does management achieve the right balance between short-term yield and long-term capital appreciation? The danger in seeking the former is that growth projects are snubbed at the detriment of long-term value. Encouragingly, analysis suggests the large cap producers, at least, should be able to satisfy both criteria, given expected improvements to cash fl ows.

“It’s an opportunistic time for those with access to longer-term capital and with confi dence in the sector to capitalize on attractive investment opportunities in the current market.”

Nicky CrabtreeMining & Metals Global Transaction

Advisory Services, Assistant Director EY UKI

Source: S&P Capital IQ, EY analysis.

Dividend

2005

2006

2007

2008

2009

2010

2011

2012

2013

f

2014

f

2015

f

2016

f

0%

20%

40%

60%

80%

100%

120%

0200400600800

1,0001,2001,4001,600

Divi

dend

/FCF

Divi

dend

($m

)

Top 14 globally diversifi ed mining companies dividend summary

20 | Mergers, acquisitions and capital raising in mining and metals

Investors are presently being offered a better yield with higher dividends set against depressed share prices. While this is yet to fl ow through to improved investor sentiment, we do expect this to happen over time. Once confi dence returns to the sector, companies will have more capacity to again focus on investing capital for growth.

This change in sentiment is not limited to the producers; development companies are preserving capital, optimizing project timetables and looking for a broader range of partners to de-risk the build-out. The manner in which these companies are approaching capital markets is also changing, where wider pools of capital providers are being considered and capital is being stretched further. As this group of companies is increasingly looking to attract private equity-type investment, they are beginning to approach investment in a more disciplined manner, setting out milestones, increasing accountability and adjusting rewards.

Return on investment time horizonMining companies invest for the future – that is, investments made are not expected to generate income immediately but at some point in the future. The graph opposite shows expected return on capital employed (ROCE), revealing that historical investments are unlikely to yield signifi cant uptick in ROCE until after 2016. This analysis is based on consensus forecasts, which some argue to be conservative and others realistic.

Based on these forecast returns, it will be diffi cult to justify a signifi cant increase in M&A activity outside of investments that present a unique or highly synergistic value proposition. This suggests that for those investors who are able to realize this upside, the window of opportunity will remain open for some time.

When is the timing right?While the best time to undertake M&A is at the bottom of the market, this has not historically proven to be the case. The graph below demonstrates little correlation between commodity price peaks (and possibly the timing of decisions) and when deals are completed.

Historical M&A value vs commodity price

Value of M&A LMEX base metals Iron oreGold Coal

0

50

100

150

200

250

0

10,000

20,000

30,000

40,000

50,000

5,000

15,000

25,000

35,000

45,000

Jan

08

May

08

Sep

08Ja

n 09

May

09

Sep

09Ja

n 10

May

10

Sep

10Ja

n 11

May

11

Sep

11Ja

n 12

May

12

Sep

12Ja

n 13

May

13

Sep

13

Com

mod

ity p

rices

(mon

thav

erag

es, r

ebas

ed)

Deal

val

ue, $

m

Source: EY analysis, ThomsonONE, Thomson Datastream

Source: S&P Capital IQ, EY analysis.

ROCE

2005

2006

2007

2008

2009

2010

2011

2012

2013

E

2014

E

2015

E

2016

E

02468

1012141618

ROCE

%

Consensusforecast

Top 14 globally diversifi ed mining companies - ROCE summary

21Mergers, acquisitions and capital raising in mining and metals |

As long as management’s primary focus is on cost optimization and driving up ROCE, in the absence of a signifi cant metals price jump, we are unlikely to see a return to large-scale M&A in the near-term. However, shareholder pressure may alleviate over time, resulting in a situation where expectations realign to more modest levels of ROCE, incentivized by the prospect of higher yields.

In the interim, the time for those with a longer-term investment horizon to undertake M&A is now, where favorable valuations and reduced competition support an attractive acquisition environment. However, the nature of this M&A is likely to differ from that historically, where capital is likely to be preserved for opportunities that support a robust operational structure and margin-led growth, rather than pure scale-led growth.

From a wider economic and commodity price environment, the sector requires some fi rm consensus on valuation before investment decisions free up more widely. Interestingly, it is those with a clear “in house view” of commodity prices and other key valuation input assumptions, including economic and commodity prices, such as commodity traders, which are most active in the M&A market right now.

The window will gradually close, not slamThere is no disputing that the mining and metals sector invests and reaps its return in cycles. The cyclical nature of the industry is one of the key determinants of how long the window of opportunity will remain open for patient capital. While forecasts are never conclusive, historical trends suggest larger producers will return to investments before long, although an imminent fi ght for assets with private capital looks unlikely.

Mergers & acquisitions

1.

Preference for smaller bolt-on deals

Valuation gap

Regional M&A trends

Financial investors

Cross border activity

Commodity overview

22 | Mergers, acquisitions and capital raising in mining and metals

23Mergers, acquisitions and capital raising in mining and metals |

Introspection and inertia characterized a year of subdued M&A activity in the mining and metals sector. During the last 12 months, there was a distinct shift away from external investing for growth toward internal capital optimization. Traditional buyers concentrated on capital discipline, improving balance sheet strength and maximizing return on capital. The majors continued to pursue divestment of non-core assets, while cash-strapped juniors struggled to raise fi nance. Such a climate presents deal opportunities. However, the sense of urgency to make them happen was missing.

The year 2013 marked the third consecutive year of declining M&A deal values and volume in the mining and metals sector. Deal volume dropped 25% y-o-y, while total deal value increased by 20% to $124.7b. However, this increase was misleading as it was primarily due to the completion of the merger between Glencore International and Xstrata. Excluding this, overall deal value decreased 16% to $87.3b, prolonging the downward trend of recent years.

The mining and metals industry continued to be plagued by volatility in commodity markets and the macroeconomic uncertainty that characterized the last fi ve years. With margins squeezed and returns from previous investments under scrutiny, companies are hesitant to part with capital. Faith has been shaken and investment sentiment in the industry is at an all-time low.

But, for the large cap producers at least, there is very little distress and balance sheets are looking increasingly healthy. As diversifi ed mining and metals companies seek to optimize portfolios with a focus on increasing overall margins, many of the industry’s majors have announced high-value divestment programs. During 2013, the industry’s top fi ve diversifi ed mining majors completed $6.3b6

of divestitures, while $5.5b of deals have been agreed and are expected to complete during 2014. As it stands, the Las Bambas divestment by Glencore Xstrata appears to be the last major divestment across the top fi ve major producers that is still in the process of fi nding a buyer. Other examples of divestments made in 2013 include the following:

• BHP Billiton divested its Pinto Valley mining operation and associated San Manuel Arizona Railroad Company ($650m)7,interests in the EKATI Diamond Mine and Diamonds Marketing operations ($553m),8 and the East and West Browse joint venture ($1.63b).9

• Vale sold its shares in Norsk Hydro for $1.82b,10 and announced the sale of its Araucaria fertilizer plant for $234m11 and its stake in the Brazilian BM-ES-22A oil and gas concession for $40m.12

• Rio Tinto sold its 80% interest in Northparkes ($820m);13

agreed the sale of its Eagle project to Lundin (c.$325m);14 and completed the sale of its 57.7% effective interest in Palabora Mining Company ($373m);15 the North American portion of its Alcan Cable business ($151m) in 2012;16 and 50% stake in the Clermont mine ($1b).17

6. Including Vale’s $1.8b sale of its Norsk Hydro shares, which falls outside of the M&A data within this report.7. “BHP Billiton completes sale of Pinto Valley to Capstone Mining Corp,” BHP Billiton press release, 11 October 2013.8. “BHP Billiton completes diamond business to Dominion Diamond Corporation,” BHP Billiton press release, 10 April 2013.9. “BHP Billiton completes the sale of interest in East and West Browse joint venture,” BHP Billiton press release, 7 June 2013.10. “Vale sells all of its shares in Norsk Hydro with the exercise of the over-allotment option,” Vale press release, 14 November 2013.11. “Vale to sell fertilizers asset,” Vale press release, 18 December 2012.12. “Vale to sell stake in oil and gas concession,” Vale press release, 26 December 2012.13. “Rio Tinto agrees to sell of interests in Northparkes,” Rio Tinto press release, 28 July 2013.14. “Rio Tinto agrees sale of Eagle project,” Rio Tinto press release, 12 June 2013.15. “Rio Tinto agrees sale of shareholding in Palabora,” Rio Tinto press release, 11 December 2012.16. “Rio Tinto completes sale of Alcan Cable’s North American business,” Rio Tinto press release, 5 September 2012.17. “Rio Tinto agrees sale of interest in Clermont mine,” Rio Tinto press release, 25 October 2013.

“2013 was a tough year for M&A across the sector. There was a lack of desire to pursue acquisitive growth and for those with multiple assets there was insuffi cient distress to force divestment. The most signifi cant deal of the year, the merger of Glencore International and Xstrata, was unique in nature, was all equity and represented 30% of deal value for the year.”

Lee DownhamGlobal Mining & Metals Transactions

Leader, EY

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*Volume 475 596 564 701 903 919 1,047 1,123 1,008 941 702Value ($m) 46,182 26,350 65,430 175,713 210,848 126,884 60,035 113,706 162,439 104,014 87,309 Average value ($m) 97 44 116 251 233 138 57 101 161 111 124Median value ($m) 4.4 3.1 4.8 6.2 7.2 6.0 3.2 5.2 5.6 5.0 3.8

Volume and value of deals (2003-2013)

*Excluding Glencore Xstrata merger

24 | Mergers, acquisitions and capital raising in mining and metals

Additionally, most of the majors focused their strength on achieving cost saving targets and scaling back capital expenditure while pursuing only the top tier projects and doing so incrementally. For instance:

• Rio Tinto reduced operating costs by $2b by the end of 2013 and is scaling back capital expenditure 20% y-o-y for the next two years.18

• Anglo American will deliver about $1.3b annually by cutting overhead costs, reducing its project pipeline and generating more value from product sales.19

• AngloGold Ashanti plans cuts of $460m from corporate and exploration costs and $500m from operating cost savings.20

This activity, together with other rationalization measures and an uptick in iron ore prices during the back end of 2013, has strengthened cash fl ows and balance sheets and eased the pressure to divest non-core or underperforming assets.

As such, investing activities remained subdued in 2013 and any expectation of rock-bottom asset sales seems off the mark. These conditions collectively point toward deal inertia. With buyers looking for bargains and sellers in no mood to let assets go cheaply, it’s a stalemate.

Valuation gap – increasingly diffi cult to bridgeHowever, the gap between buyers’ and sellers’ valuation expectations is not only the preserve of the large cap producers. A total of 74% of the respondents to EY’s Capital Confi dence Barometer Survey for Mining and Metals, released in October 2013, believe that a valuation gap of 10% -30% currently exists. Further, the expectation of the majority of respondents is that the gap is going to remain or even increase.

A disparity in analysts’ forecast for metal prices, fueled by differing expectations for world economic growth, is producing a broad range of asset valuations. This is only serving to widen the gap between buyer and seller expectations on price and hinder deal completion. While some believe that current equity valuations are wildly undervalued, others consider this to be a much-needed market correction. From any vantage point, it is a challenging

18. “Rio Tinto is delivering on its commitment to create greater value for shareholders,” Rio Tinto Investor Presentation, 3 December 2013.19. “Anglo American chief plans $1.3bn cash uplift in shake-up,” The Telegraph, 26 July 2013.“Half year fi nancial report for the six months ended 30 June 2013,” Anglo American report, 26 July 2013.20. “AngloGold Q3 earnings jump on 12% output gain, 10% cost decline,” AngloGold Ashanti press release, 6 November 2013.

backdrop against which to make investment decisions. With price volatility expected to continue for a few more years as the supply and demand balance struggles to achieve equilibrium, both buyers and sellers will need to be innovative in their approach to valuations.

2004

2003

2005

2006

2007

2008

2009

2010

2011

2012

2013

<$200m

>$1b

Between $200m and $1b

Volume

Deal

val

ue ($

b)

Deal

vol

ume

-50

100150200250

02004006008001,0001,200

Volume and value of deals by size (2003-2013)

Financial investors embrace opportunitiesDespite challenging market conditions, the sector’s new entrants appear to be fi nding a way to successfully navigate the M&A landscape. During the last 12 months, fi nancial investors increased their share of total M&A undertaken by value from 5% in 2012 to 19% in 2013. This stands to reason given that many fi nancial investors are countercyclical, attracted by the prospect of potentially strong returns driven by low asset valuations.

In 2013, 5 of the 19 megadeals (>$1b) were undertaken by fi nancial investors:

1. The $3.6b joint investment by Lizarazu and Receza in Polyus Gold International

2. Onexim Group’s $3.5b investment in Uralkali

3. Chengdong Investment Corp’s $2b (12.5%) stake in Uralkali

4. Samruk-Kazyna’s $1.7b investment in Kazzinc

5. Crispian Investments’ $1.5b investment in Norilsk Nickel

These deals highlight the disparity between market valuations and the underlying value that a strategic and more patient investor can attribute. In most part, these megadeals demonstrated a belief by the fi nancial investor that the market was being too risk averse.

25Mergers, acquisitions and capital raising in mining and metals |

This investor group has typically sought to acquire minority stakes, evidenced by the fact that 64% of their 2013 deals were for a stake of less than 50% in the company and 88% were valued below $50m.

Emerging fi nancial investors include Former Xstrata CEO Mick Davis, who recently set up X2 Resources, Former Barrick CEO Aaron Regent who established Magris Resources, and former Vale CEO Roger Agnelli, together with fund company Grupo BTG Pactual SA, established B&A Mineração.

“This is a trend we expect to see continue. We also anticipate further interest from specialist funds and individuals over the next 12 months, led by a number of former mining leaders lending their expertise to privately held capital,” said Nicky Crabtree, Assistant Director, Transaction Advisory Services, Mining & Metals, EY.

There is potential for ongoing activity in the year ahead, driven by these former mining leaders with in-house technical and operational expertise and a keen eye for strategic assets in the sector. The current capital-raising environment will present a window of opportunity for well-capitalized fund companies and a much-needed injection of capital for mining and metals companies. These specialist fi nancial investors are likely to become mainstream investors in the years ahead, fi lling the gap until traditional acquirers and equity market confi dence return.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2013

2012

2011

Low risk (domestic consolidation)Strategic (supply/security)Geographic expansion

Low risk (existing stake)

Disposal/exit/buy-out

Megadeal drivers share of deal value (2011-2013)

Preference for smaller bolt-on dealsGiven that 2013 was characterized by senior management changes and strong rhetoric to display capital discipline, it is not surprising that high profi le megadeals were largely abandoned and leaders instead chose to undertake lower risk bolt-on deals.

There was just 1 deal undertaken with a value in excess of $10b — the Glencore Xstrata merger — and only 19 deals that fetched more than $1b a piece, compared with 26 such deals in 2012. These megadeals comprised 72% of the total value of M&A deals closed during the year but represented only 2.7% of total deal volume.

Many large deals that did occur were one-off, unique in nature and not refl ective of the market sentiment as a whole. For example, the merger of Dubai Aluminium (DUBAL) with Emirates Aluminium (EMAL) to create a new entity, Emirates Global Aluminium — the only reported deal out of the UAE — was driven by a nationalistic desire by Dubai and Abu Dhabi to consolidate their state aluminium producers and strengthen their position globally.21

The two major oil and gas acquisitions by Freeport-McMoRan Copper & Gold accounted for 7% of total deal value (10% when excluding the Glencore Xstrata merger) and were driven by a desire to diversify out of the mining and metals space.

The remaining megadeals were largely low risk, fueled by a desire to increase an existing stake, achieve domestic consolidation or a strategic attempt to secure future supply. For as long as the majors remain heavily focused on strengthening their bottom lines, simplifying portfolios and riding out volatility, any increase in high-value acquisitions is unlikely in the near future, short of these unique or highly synergistic opportunities.

21. “Update 2 – Aluminium merger hints at closer Dubai, Abu Dhabi ties,” Reuters, www.uk.reuters.com, 3 June 2013.

Share of deal value by acquirer type (2011-2013)

Industry acquirersState-backed acquirersOther sectors

Financial investorsCommodity tradersUndisclosed

0% 20% 40% 60% 80% 100%

2011

2012

2013*

*Excluding the Glencore Xstrata merger

26 | Mergers, acquisitions and capital raising in mining and metals

Rank Value ($m)

Type Target name Target country

Target commodity

Acquirer Acquirer country

Acquirer commodity

Share (%)

1 37,439 Domestic Xstrata Switzerland Diversifi ed Glencore International Switzerland Trading company 65.9

2 7,500 Domestic DUBAL (Dubai Aluminium Company Limited)

United Arab Emirates

Aluminium Emirates Aluminium Co United Arab Emirates

Aluminium 100.0

3 6,450 Domestic Plains Exploration & Production Co

US Oil & gas Freeport-McMoRan Copper & Gold US Copper 100.0

4 5,058 Domestic Inmet Mining Corp Canada Copper First Quantum Minerals Canada Copper 94.0

5 3,911 Domestic Sterlite Industries (India) India Diversifi ed Sesa Goa India Iron Ore 100.0

6 3,620 Domestic Polyus Gold International Russia Gold Lizarazu and Receza Russia Financial investor 37.8

7 3,543 Domestic Uralkali Russia Potash/phosphate

Onexim Group Russia Financial investor 21.8

8 3,462 Domestic Consolidation Coal US Coal Murray Energy Corp US Coal 100.0

9 2,616 Domestic Hyundai Hysco - Steel milling business

South Korea

Steel Hyundai Steel South Korea Steel 100.0

10 2,611 Domestic Titanium Metals Corp US Titanium Precision Castparts Corp US Aircraft components

90.4

11 2,218 Cross border

Eurasian Natural Resources UK Diversifi ed Eurasian Resources Group Luxembourg Consortium 55.4

12 2,100 Domestic McMoRan Exploration Co US Oil & gas Freeport-McMoRan Copper & Gold US Copper 64.0

13 2,000 Cross border

Uralkali Russia Potash/phosphate

Chengdong Investment Corp China Sovereign wealth fund

12.5

14 1,650 Domestic Kazzinc Kazakhstan Silver/lead/zinc Samruk-Kazyna Kazakhstan Sovereign wealth fund

29.8

15 1,487 Domestic GMK Noril'skiy Nikel' (Norilsk Nickel)

Russia Nickel Crispian Investments Russia Financial investor 5.9

16 1,347 Cross border

Uranium One Kazakhstan Uranium ARMZ Russia Uranium 48.4

17 1,109 Cross border

ArcelorMittal Mines Canada Canada Iron ore POSCO; China Steel; EQ-Partners South Korea Steel 15.0

18 1,105 Cross border

CGA Mining Philippines Gold B2Gold Corp Canada Gold 100.0

19 1,077 Domestic Henan Dayou Energy Co China Coal Investor Group China Coal 26.3

Megadeals (2013)

The table above includes deals that are reported as mergers of equals. However, targets and acquirers are assigned for the purposes of analysis per ThomsonONE classifi cations.

27Mergers, acquisitions and capital raising in mining and metals |

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Cross-borderDomestic

65% 65%60% 59%

43%

67%

55%52%

48%

58%

35% 35%40% 41%

57%

33% 45%48%

52%

42%

Share of cross-border and domestic deals, by volume (2004-2013)

Cross-border activity – declining popularityThe year 2013 saw the fi rst fall in the proportion of cross-border deal activity since the global fi nancial crisis (GFC) in 2008. Outbound activity, as a proportion of the total M&A volume, fell from 52% to 42% y-o-y, with only 18% of the total deal value for the year targeting cross-border assets.

The fl ow-on effect was a signifi cant increase in the value of domestic deal activity, which rose from $43.3b in 2012 to $65.1b in 2013 (excluding the Glencore Xstrata merger), accounting for 75% of the entire deal value for the year. All of the top 10 deals were domestic targets, while two of the largest deals — the merger of DUBAL with EMAL and the merger of Sterlite Industries into Sesa Goa — were driven by nationalistic consolidation. The remaining megadeals were largely low risk, fueled by a desire to increase an existing stake, achieve domestic consolidation or a strategic attempt to secure supply.

Target region 2008 2009 2010 2011 2012 2013* Y-o-Y change*North America 48,520 15,420 22,200 54,187 13,306 26,923 102%Asia Pacifi c 29,611 20,505 38,955 38,297 41,055 25,365 -38%CIS 3,553 3,836 3,718 23,894 5,418 17,939 231%Middle East - - 1,605 131 - 7,500 -Europe 26,432 4,608 6,613 3,564 10,424 3,863 -63%Latin America 16,924 12,139 23,957 22,084 13,872 2,792 -80%Africa 1,844 3,285 16,657 20,282 19,940 2,927 -85%Total 126,884 60,035 113,706 162,439 104,014 87,309 -16%

Value of deals by target region ($m)

*Excluding the Glencore Xstrata merger

“Cross-border statistics point to a very cautious sector, one that is holding back from high-risk cross-border investments that are diffi cult to value and justify. It is not surprising that 2013 M&A activity was largely focused on creating value in familiar territories.”

Jodie EldridgeM&A Analyst, Mining & Metals, EY

Australia

Regional M&A trendsIn 2013, Europe was both the most targeted and the most acquisitive region by deal value due to the Glencore Xstrata deal. Excluding this deal, North America was the most targeted region with 31% of deal value, narrowly leading Asia Pacifi c (29%). North America and the Asia-Pacifi c region tied as the most acquisitive regions by deal value, each with 33%.

At a country level, excluding Switzerland’s Glencore Xstrata merger, the US was the most targeted by value ($18b or 21%) and Canada was the most targeted by volume (153 or 22%). Similarly, the US was the most acquisitive country by value (21%) and Canada by volume (30%). The value of US domestic deals rose from $2b in 2012 to $16.6b in 2013, and Canada from $2.2b to $6.8b. Within these countries, buyers mostly targeted assets within their existing commodity focus and looked to strategically create growth and effi ciencies locally.

The unusually high deal value targeting the Middle East is attributable exclusively to the DUBAL-EMAL merger completed in 2013, rather than an overall surge in activity from this region. Similarly, the CIS more than trebled its value of deal investment on a fl urry of large domestic private investor activity in the gold and coal sectors plus the $5.5b worth of investment into potash producer, Uralkali, by Onexim Group and Chengdong Investment Group.

28 | Mergers, acquisitions and capital raising in mining and metals