mena healthcare - arqaam capital · 2013-10-01 · arqaam capital research offshore s.a.l mena...

TRANSCRIPT

MENA HealthcareSector Report | 18 September, 2013

MENA HealthcareNo Better Time to be Overweight

S e c t o r C o v e r a g e

S e p t e m b e r 1 8 2 0 1 3

Mohammad Kamal [email protected] +9714 507 1743

Dahlia Sabaayon, CFA Arqaam Capital Research Offshore s.a.l

MENA Healthcare No better time to be overweight

Lifestyle-related diseases are highly prevalent in MENA, and particularly in KSA and the UAE: sedentary lifestyles and poor dietary habits linked to diabetes, cardiovascular diseases, and cancer have rendered KSA and UAE exposed to elevated incidence rates of key diseases. As a general data point, the obesity rate among Saudi adults, according to the WHO, is 3x the global rate, on par with the US (36%) and ahead of MENA (<30%). The UAE faces a similar situation, with 36% of the population classified as obese. Perhaps most striking is the incidence of diabetes among young (<39) residents in KSA, which stands at >2x the US rate at 32% of the overall diabetic population (14% US).

Chronic underinvestment and over-expenditure: The KSA bed/1,000 ratio of 2.2 (1.7 beds provided by the government, 0.5 by the private sector) is below the global average of 3.0, and far below the average of 5.5 in developed countries. The UAE is structurally similar, at 1.9 beds/1,000 in 2011. National spending on healthcare in KSA and UAE has been between 4.0% and 2.5% of GDP over the past 5 years, roughly in-line with the MENA average, but low by developed market standards (18% in the US, 11% in France and Germany, 8% in the UK). Conversely, the expenditure on medical treatments abroad for KSA and UAE nationals has cost both countries an average of USD 5bn in the past 10 years, as a consequence of insufficient domestic healthcare infrastructure and a shortage of qualified specialised doctors. Healthcare policy in both countries has stimulated private sector investment in capacity, while new regulation regarding insurance cover should prove a sizable catalyst. A combination of (i) reforms, (ii) public spending packages, and (iii) special lending terms targeting new medical facilities have spurred private sector participation. In the UAE, the introduction of mandatory health cover in Abu Dhabi in 2007 catalysed a 4x growth in inpatient claims, and 8x in outpatients. Dubai and the Northern Emirates are due to follow suit, releasing 50% in additional insured patients which to date have met treatment costs out-of-pocket. Discounted valuation despite superior quality: We are positive on NMC UH (Buy, GBp 440), MOUWASAT AB (Buy, SAR 103) and DALLAH AB (Buy, SAR 88). We find fundamentals priced in at current price for CARE AB (Hold, SAR 48) and ANH LN (Hold, GBp 840). KSA and UAE healthcare plays offer value in an EM context, as the sector trades at a 20% discount to EM peer fwd P/E, while generating stronger equity returns (1.5x), a 500bps EBITDA margin differential, and industry ROIC that is 6% higher on average. Risks: Geopolitics, sufficiency of government spending packages, and adoption of key regulation.

Bloomberg code MOUWASAT AB

Company name Al Mouwasat Medical Services Company Price target SAR 103

Rating 30% upside, Buy

Bloomberg code DALLAH AB Company name Dallah Healthcare Holding Company

Price target SAR 88

Rating 40% upside, Buy

Bloomberg code NMC LN Company name NMC Health

Price target GBp 440

Rating 40% upside, Buy

Bloomberg code CARE AB Company name National Medical Care Company

Price target SAR 48

Rating 12% downside, Hold

Bloomberg code ANH LN Company name Al Noor Hospitals Group

Price target GBp 840

Rating 0% upside, Hold

© Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice.

Summary of recommendations

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 2

Contents Summary of recommendations ....................................................................................... 3

Key Performance Indicators ............................................................................................ 4

Valuation: ........................................................................................................................ 5

KSA and UAE Healthcare ................................................................................................. 6

The healthcare opportunity in KSA ................................................................................. 7

Key private healthcare groups in KSA ........................................................................... 13

The healthcare opportunity in the UAE ........................................................................ 14

Key UAE healthcare indicators ...................................................................................... 20

Al Mouwasat Medical Services Co................................................................................. 21

Dallah Healthcare Holding Co........................................................................................ 30

NMC Health ................................................................................................................... 39

National Medical Care Co. ............................................................................................. 50

Al Noor Hospitals Group ................................................................................................ 59

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 3

Summary of recommendations

Exhibit 1: Summary of recommendations

Company Price target Rating Up (down) side ADTV, USDmn EV*, USDmn Index Free float

Dallah Healthcare SAR 88 Buy 40% 11.7 707.1 SASEIDX 37.9%

Mouwasat SAR 103 Buy 30% 3.4 1,099.4 SASEIDX 43.8%

National Medical Care SAR 48 Hold (12%) 12.5 607.4 SASEIDX 38.3%

NMC Health GBp 440 Buy 40% 0.6 983.4 ASX 33.0%

Al Noor Hospitals Group Plc GBp 840 Hold 0% 0.8 1,012.8 ASX 29.1%

Company EV/EBITDA FY 14e P/E FY 13e P/E FY 14e P/E FY 15e P/B FY 13e RoE Div yield

Dallah Healthcare 14.0x 26.0x 19.3x 15.7x 2.5x 10% 1.7%

Mouwasat 12.2x 18.1x 15.2x 14.2x 4.1x 23% 1.7%

National Medical Care 15.7x 24.8x 23.4x 20.9x 2.9x 12% 2.2%

NMC Health 9.8x 13.7x 12.7x 11.5x 2.4x 18% 1.5%

Al Noor Hospitals Group Plc 10.0x 23.5x 17.5x 17.2x 8.8x 37% 1.7%

Source: Company Data, Arqaam Capital Research *at recent market prices

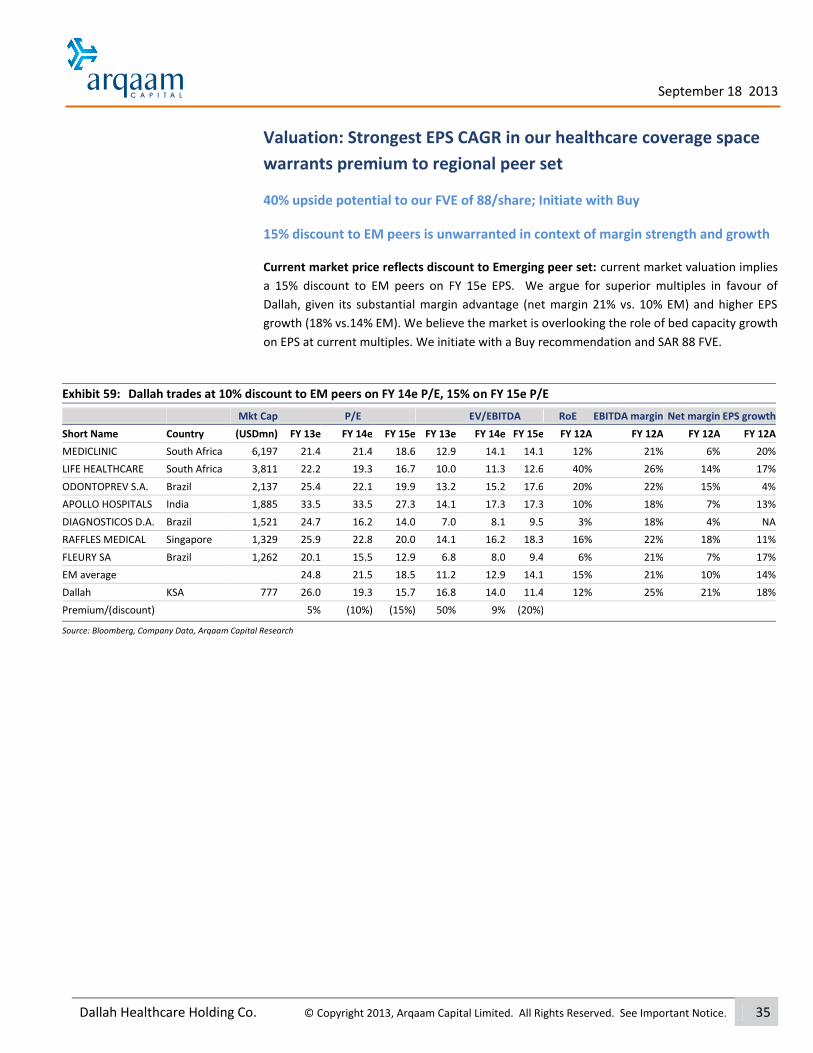

Dallah Healthcare (Buy, SAR 88): direct exposure to premium segment of KSA private healthcare sector. 2x expansion in bed capacity should translate into FY 13-18e EPS CAGR of 20%, which is further supported by double-digit growth in pharmaceuticals business (17% 5-yr revenue CAGR). Current market valuation implies 15% discount to EM peers on FY 14/15e EPS. We believe the market is overlooking the role of bed capacity growth on EPS at current multiples. We initiate with a Buy rating and SAR 88 FVE.

Mouwasat (Buy, SAR 103): unique positioning vis-a-vis KSA oil industry communities. Key growth catalysts overlooked at current valuation: 85% bed capacity increase over 5 years, roll out of facilities in dense, underserviced urban centers (Riyadh), and upward re-pricing of agreements with insurers. Mouwasat currently trades at 15.2x FY 14e EPS vs. 17.6x and 19.3x for regional and local peers, implying discounts of 15% and 20%, respectively. We believe the stock should re-rate and trade in-line with sector multiples, at the very least. We initiate with a Buy rating and SAR 103 FVE.

NMC Health (Buy, GBp 440): Well-positioned for mandatory health cover in Dubai & Northern Emirates, bed capacity in utilization should improve as a result. Bed capacity roll-out (+100%) should drive revenue CAGR of 16%. NMC holds the cheapest valuation profile within our healthcare coverage space (12.7x FY 14e EPS, 9.8x EV/EBITDA), despite superior healthcare EBITDA margins of 28% (vs. 25% regional peers, 20% EM). We value NMC at GBp 440/share, implying c. 40% in upside potential from current price, using DCF, and initiate with Buy.

National Medical Care- CARE (Hold, SAR 48): Pure play on the middle income segment of the Saudi healthcare sector. 48% bed capacity additions to bolster market share, going forward, and support 5-yr revenue CAGR of 9% on a rise in inpatient as well as outpatient visitation. Valuation: We initiate with a Hold recommendation and SAR 48 FVE. At 23.4x FY 14e EPS, CARE trades at 35% and 20% premiums to regional and local peers. Valuations are stretched but tolerable, given the business’s strong domestic positioning (16% Riyadh market share in FY 14e).

Al Noor Hospitals (Hold, GBp 840): Leading private healthcare provider in Abu Dhabi, dominant share of inpatient (39%) and outpatient (35%) market. Modest revenue growth outlook (5% CAGR 5-yr), medical staff costs to impact margins. Market valuation adequately captures fundamentals at c. 24x/18x FY 13e/14e P/E. We initiate coverage with Hold and GBp 840 FVE.

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 4

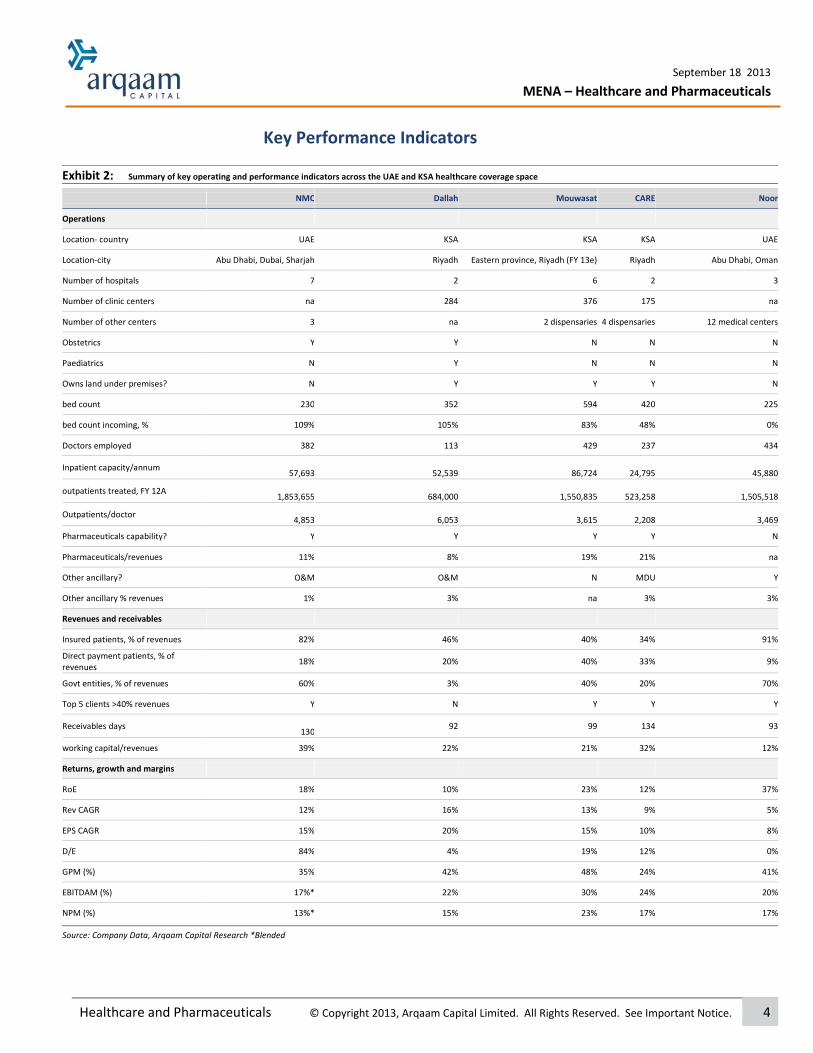

Key Performance Indicators

Exhibit 2: Summary of key operating and performance indicators across the UAE and KSA healthcare coverage space

NMC Dallah Mouwasat CARE Noor

Operations

Location- country UAE KSA KSA KSA UAE

Location-city Abu Dhabi, Dubai, Sharjah Riyadh Eastern province, Riyadh (FY 13e) Riyadh Abu Dhabi, Oman

Number of hospitals 7 2 6 2 3

Number of clinic centers na 284 376 175 na

Number of other centers 3 na 2 dispensaries 4 dispensaries 12 medical centers

Obstetrics Y Y N N N

Paediatrics N Y N N N

Owns land under premises? N Y Y Y N

bed count 230 352 594 420 225

bed count incoming, % 109% 105% 83% 48% 0%

Doctors employed 382 113 429 237 434

Inpatient capacity/annum

57,693

52,539

86,724

24,795

45,880

outpatients treated, FY 12A

1,853,655

684,000

1,550,835

523,258

1,505,518

Outpatients/doctor

4,853

6,053

3,615

2,208

3,469

Pharmaceuticals capability? Y Y Y Y N

Pharmaceuticals/revenues 11% 8% 19% 21% na

Other ancillary? O&M O&M N MDU Y

Other ancillary % revenues 1% 3% na 3% 3%

Revenues and receivables

Insured patients, % of revenues 82% 46% 40% 34% 91%

Direct payment patients, % of revenues

18% 20% 40% 33% 9%

Govt entities, % of revenues 60% 3% 40% 20% 70%

Top 5 clients >40% revenues Y N Y Y Y

Receivables days

130 92 99 134 93

working capital/revenues 39% 22% 21% 32% 12%

Returns, growth and margins

RoE 18% 10% 23% 12% 37%

Rev CAGR 12% 16% 13% 9% 5%

EPS CAGR 15% 20% 15% 10% 8%

D/E 84% 4% 19% 12% 0%

GPM (%) 35% 42% 48% 24% 41%

EBITDAM (%) 17%* 22% 30% 24% 20%

NPM (%) 13%* 15% 23% 17% 17%

Source: Company Data, Arqaam Capital Research *Blended

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 5

Valuation: sector valuation undemanding in EM context, catalysts

support 14% EPS CAGR and 20% average RoE, vs. 15% EM

Valuation across the UAE and KSA healthcare space is undemanding at 17.6x/15.9x FY 14e P/E,

12.3x/11.1x EV/EBITDA, as the sector continues to trade at a discount to EM comparables (21.5x/18.5x FY

14e/15e P/E, 12.9x/14.1x FY 14e/15e EV/EBITDA). This is despite (i) markedly better margin profiles on

aggregate (EBITDA margin 25% vs. 20%, net margins 20% vs. 15%), on a combination of higher operating

leverage and lower financial leverage, (ii) better RoE profiles (20% vs. 15%, and particularly in the UAE at

a 28% average) and (iii) regulatory catalysts in support of growth.

Exhibit 3: Performance and valuation summary

Rev CAGR EPS CAGR EBITDA margin

Net margin

RoE Div Yield P/E EV/EBITDA

BBG code Name Country FY 13-18e FY 13-18e FY 13e FY 13e FY 13e FY 13e FY 14e FY 15e FY 14e FY 15e

DALLAH AB Dallah Healthcare Holding Co SAUDI ARABIA 16% 20% 22% 15% 10% 1.7% 19.3 15.7 14.0 11.4

MOUWASAT AB Al Mouwasat Medical Services Co SAUDI ARABIA 13% 15% 30% 23% 23% 1.7% 15.2 14.2 12.2 11.9

CARE AB National Medical Care Co SAUDI ARABIA 9% 10% 24% 17% 12% 2.2% 23.4 20.9 15.7 13.9

NMC LN NMC Health PLC UAE 12% 15% 28% 25% 18% 1.5% 12.7 11.5 9.8 8.5

ANH LN Al Noor Hospitals Group Plc UAE 5% 8% 20% 17% 37% 1.7% 17.5 17.2 10.0 9.7

Average- coverage 11% 14% 25% 20% 20% 1.8% 17.6 15.9 12.3 11.1

DALLAH AB Dallah Healthcare Holding Co SAUDI ARABIA 16% 20% 22% 15% 10% 1.7% 19.3 15.7 14.0 11.4

MOUWASAT AB Al Mouwasat Medical Services Co SAUDI ARABIA 13% 15% 30% 23% 23% 1.7% 15.2 14.2 12.2 11.9

CARE AB National Medical Care Co SAUDI ARABIA 9% 10% 24% 17% 12% 2.2% 23.4 20.9 15.7 13.9

Average- KSA 13% 15% 25% 19% 15% 1.9% 19.3 16.9 14.0 12.4

NMC LN NMC Health PLC UAE 12% 15% 28% 25% 18% 1.5% 12.7 11.5 9.8 8.5

ANH LN Al Noor Hospitals Group Plc UAE 5% 8% 20% 17% 37% 1.7% 17.5 17.2 10.0 9.7

Average- UAE 8% 12% 24% 21% 28% 1.6% 15.1 14.4 9.9 9.1

MDC SJ Equity MEDICLINIC INTERNATIONAL LTD South Africa

20% 17% 15% 1.3% 21.4 18.6 14.1 14.1

LHC SJ Equity LIFE HEALTHCARE GROUP HOLDIN South Africa

24% 19% 37% 2.9% 19.3 16.7 11.3 12.6

ODPV3 BZ Equity ODONTOPREV S.A. Brazil

21% 15% 18% 3.5% 22.1 19.9 15.2 17.6

APHS IN Equity APOLLO HOSPITALS ENTERPRISE India

14% 10% 11% 0.7% 33.5 27.3 17.3 17.3

DASA3 BZ Equity DIAGNOSTICOS DA AMERICA SA Brazil

17% 12% 5% 0.6% 16.2 14.0 8.1 9.5

RFMD SP Equity RAFFLES MEDICAL GROUP LTD Singapore

23% 18% 15% 1.4% 22.8 20.0 16.2 18.3

FLRY3 BZ Equity FLEURY SA Brazil

20% 13% 6% 2.8% 15.5 12.9 8.0 9.4

Average- EM 20% 15% 15% 1.9% 21.5 18.5 12.9 14.1

Source: Bloomberg, Company Data, Arqaam Capital Research

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 6

KSA and UAE Healthcare

No better time to be overweight

Hereditary and lifestyle-related diseases are highly prevalent in MENA, and particularly in KSA

and UAE: The obesity rate among Saudi adults, according to the WHO, is 3x the global rate, on par

with the US (36%) and ahead of MENA (<30%). The UAE faces a similar situation, with 36% of the

population classified as obese. The incidence of diabetes is particularly high in both countries, at

c.1.5x the US rate and 1.7x the broader MENA rate. 12% (3.4mn) of the KSA population and 16% of

the UAE population are diabetic (0.9mn), vs. 10% and 9% in the US and broader MENA, according to

the WHO. Perhaps most striking is the incidence of diabetes among young (<39) residents in KSA,

which stands at >2x the US rate at 32% of the overall diabetic population (14% US).

Chronic underinvestment, reactive over-expenditure: The KSA bed/1,000 ratio of 2.2 (1.7 beds

provided by the government, 0.5 by the private sector) is below the global average of 3.0, and far

below the average of 5.5 in developed countries. The UAE is structurally similar, at 1.9 beds/1,000 in

2011. National spending on healthcare in KSA and UAE has been between 4.0% and 2.5% of GDP

over the past 5 years, roughly in-line with the MENA average, but low by developed market

standards (18% in the US, 11% in France and Germany, 8% in the UK). Governmental hospitals still

account for the bulk (65%) of bed capacity in KSA, and 50% in UAE. Conversely, the expenditure on

medical treatments abroad for KSA and UAE nationals has cost both countries an average of USD

5bn in the past 10 years, as a consequence of insufficient domestic healthcare infrastructure and a

shortage of qualified specialised doctors.

The policy response in both countries has stimulated private sector investment in healthcare

capacity, primarily via the phased introduction of mandatory health cover. In KSA, the

government introduced a series of (i) reforms, that have mandated insurance cover for public sector

employees (both Saudi and expatriate), working in the private sector since 2011. The next leg will

address public sector employees along with their dependants, which accounts for 10% of the KSA

workforce, and 22% of the population. (ii) Public spending packages, which focus on upgrading

healthcare infrastructure and domestic medical capability, and (iii) special lending terms targeting

new medical facilities. In the UAE, the introduction of mandatory health cover in Abu Dhabi in 2007

catalysed a 4x growth in inpatient claims, and 8x in outpatients. Dubai and the Northern Emirates

are due to follow suit, releasing 50% in additional insured patients which to date have either met

treatment costs out-of-pocket or via private cover.

This in our view is an industry game-changer that will add further pressure on existing bed

capacity in the UAE, and stimulate demand for qualified medical personnel. Mandatory insurance

cover should in our view lower real treatment costs to patients, raise the volume of health

premiums written substantially for insurers, and compromise margins for healthcare providers who

typically collect a smaller proportion of dues from insurers than from out-of-pocket patients (due to

negotiated agreements with insurers). The volume upside however, is more than sufficient to drive

earnings growth and largely override the compression in margins.

We initiate coverage of 5 key healthcare plays in KSA and UAE. We are positive on NMC UH (Buy,

GBp 440), MOUWASAT AB (Buy, SAR 103) and DALLAH AB (Buy, SAR 88). We find fundamentals

priced in at current price for CARE AB (Hold, SAR 48) and ANH LN (Hold, GBp 840). KSA and UAE

healthcare plays offer value in an EM context, as the sector trades at a 20% discount to EM peer

fwd P/E, while generating stronger equity returns (1.5x) and a 500bps EBITDA margin differential,

on average. Risks: Geopolitics, sufficiency of government spending packages, adoption of key

regulation.

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 7

The healthcare opportunity in KSA

Key drivers: demographics, disease incidence, reform and capacity additions

The KSA Government aims to raise the national bed/patient ratio to 3.3/1,000

residents from 2.2 in FY 08A, by adding 44k beds by FY 17e, via a mix of public

and private facilities

Expatriates are fully covered by mandatory employer-based health insurance.

Mandatory health cover for public sector employees is expected to be rolled out

starting 2014, and represents the next leg up for demand (we estimate +50%)

1-Demographic and epidemiological trends

(i) Population growth: The KSA population base has grown at an average of

3.3%/annum (CAGR FY 08-12e), expanding by c.3.2mn residents in total. Going

forward, the IMF forecasts an overall growth rate of 9% in FY 13-17e, well-ahead

of BRICS (4%), but behind neighboring GCC countries- Qatar (17%), Oman (13%),

and UAE (13%). The UAE and Qatar have generally been larger importers of

regional human capital than KSA in the past 10 years.

Exhibit 4: KSA GDP/capita growth in line with population

growth

Source: IMF

Exhibit 5: 30% of KSA population is <15 years of age, while 5%

is > 60

Source: UNDP

(ii) The proportion of residents > 60 is rising: While Saudi Arabia holds a relatively

young population base (39% below 18, 5% above 60), the portion of elderly

residents is growing, in absolute numbers. As the overall Saudi population base

grew at an average rate of 2.2% between 1990 and 2012, the 60+ age group

expanded by 0.8mn people (+10%) between 1990 and 2012.

Algeria

Bahrain

Jordan

Tunisia

Iraq

Egypt Kuwait LebanonLibya Morocco

Oman

Qatar

KSA

Sudan

Iran

UAE

(4%)

(2%)

--%

2%

4%

6%

8%

10%

12%

14%

(6%) (4%) (2%) --% 2% 4% 6% 8%

5-year population growth

5-year GDP/capita growth

27% 20%31%

43%

23%36%

27% 24%31% 27% 27%

14%30%

40%23%

14%

59% 72% 52%

48%

62%52% 65%

55%55% 55%

64%81%

65% 49%

56%85%

14% 8%17%

10% 16% 12% 8%21%

14% 17%9% 5% 5% 11%

21%

1%

0%

20%

40%

60%

80%

100%

Alg

eri

a

Bah

rain

Egyp

t

Iraq

Iran

Jord

an

Ku

wai

t

Leb

ano

n

Lib

ya

Mo

rocc

o

Om

an

Qat

ar

KSA

Sud

an

Tun

isia

UA

E

Population breakdown by age (FY 12)

< 15 years 15-60 years > 60 years

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 8

(iii) Lifestyle-related disease incidence: sedentary lifestyles, given regional weather

conditions that prohibit extensive outdoor activity, and poor dietary habits linked

to diabetes, cardiovascular diseases, and cancer have rendered KSA exposed to

elevated incidence rates of lifestyle-related diseases. As per data from the World

Health Organisation (WHO), the obesity rate among Saudi adults is 35% (vs. 11%

global, 36% US, <30% MENA), while around 37% of adults have elevated

cholesterol levels (vs. 39% global, 48% US, 40% MENA), and 12% or 3.4mn people

are diabetic (vs. 10% US, 9% MENA). The incidence rate of diabetes among young

(<39 year old) residents however, is particularly high, at 32% (vs. 14% US) of the

overall diabetic population.

Exhibit 6: The 60+ demographic is expected to reach 8% of the

KSA population base by FY 20e

Source: BMI

Exhibit 7: 12% of the KSA population is diabetic, well ahead of

MENA (9%) and the US (10%)

Source: WHO

Exhibit 8: 32% of diabetic patients are <39 years of age

Source: WHO

Exhibit 9: The KSA obesity rate of 35% is among the highest

globally (MENA 30%, global 11%)

Source: WHO

51% 51% 48% 43% 41% 39% 37% 37%

34% 33% 34%36% 39% 38% 38% 34%

11% 12% 13% 17% 16% 18% 19% 21%

0%

20%

40%

60%

80%

100%

120%

FY 90A FY 95A FY 00A FY 05A FY 10A FY 12A FY 15e FY 20e

KSA population breakdown by age

0-19 20-39 40-59 60-75+

16%

12% 12%

10% 9%

5%

9%10%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

UAE KSA Lebanon Kuwait Egypt Jordan MENA US

Diabetic incidence as a % of total population

23% 19%35%

11%

32%40%

14%

49%50%

52%

47%

51%

55%

44%

28% 31%

13%

42%

16%5%

42%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Egypt Jordan Kuwait Lebanon KSA UAE USA

Diabetes patients age structure

20-39 40-59 60-79

45%

36% 36% 35% 35% 34%

28%30%

11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Kuwait UAE US KSA Egypt Jordan Lebanon MENA Global

Obesity rates

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 9

2-Regulation and government spending as a supply–side catalyst

(i) Reform

Major structural changes have positively impacted the healthcare sector in Saudi Arabia over

the past decade. Healthcare reform has been focused on solutions that address rapidly

growing demand, while concurrently effecting improvements to the quality of healthcare

services provided by the public and private sectors. Key reform steps in the past 10 years have

been:

The enforcement of mandatory health insurance for expatriates and nationals

working in the private sector. Introduced a decade ago, this package of reforms

catalysed corporate/private sector demand for healthcare services.

Public spending packages on core healthcare needs: In 2012, the Saudi Government

allocated SAR 61bn (USD 16bn) towards health services and social development, up

from SAR 52bn a year earlier. This accounted for c. 70% of total healthcare

expenditure and constituted 9% of overall government spending. This has helped in:

(i) establishing medical universities and research facilities, (ii) increasing the breadth

and coverage of childhood vaccination programs, and (iii) improving the quality and

availability of care for pregnant mothers and newborns. Life expectancy in the country

has consequently risen to 74 years (vs. 64 in 1990) and infant mortality has dropped

significantly (17 per 1,000 from 26 previously), as of 2010.

Nevertheless, supply shortages remain massive. The KSA bed/patient ratio of 2.2 (1.7 beds

provided by the government, 0.5 by the private sector) is below the global the average of 3.0,

and far below the average of 5.5 in developed countries. As such, we believe that the

structural deficit in healthcare infrastructure prevalent in KSA will continue to (i) require

substantial budget allocations over the next 10 years, (ii) experience continued reform, and (iii)

experience a substantial upgrade in the quality and availability of healthcare services.

Exhibit 10: 2.2 beds per 1,000 patients is low vs. developed

markets

Source: World Bank

Exhibit 11: KSA healthcare per capita expenditure is well-below

global levels (-c.30%)

Source: BMI, OECD Health data

8.3

6.6

3.0 3.0

2.2 2.1 1.9

0

1

2

3

4

5

6

7

8

9

Germany France US UK KSA MENA UAE

Hospital beds per 1,000

3,537

2,373

1,640

1,030 758 709

209 99

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

US Europe UAE Global KSA Western Pacific Eastern Mediterranean

Africa

Healthcare expenditure per capita FY 11A (USD)

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 10

(ii) Mandatory health insurance cover for public sector employees

Phased introduction of mandatory health cover: Towards the end of the 1990s, the Saudi

government rolled out a health insurance system over 3 key phases. More than a decade

following the introduction of mandatory healthcare insurance, the first leg of a 3-phased

health insurance system was completed by 2011.

Phase 1: Covering expatriate workers and their dependents, in addition to Saudi

nationals working in the private sector

Phase 2: Covering public sector employees

Phase 3: Covering other groups, including pilgrims visiting the holy cities.

The implementation of Phase 1 in 2007-12 was instrumental in unlocking demand for

healthcare services in KSA. As insurance policy holders rose 4x to approximately 8.4mn (7mn

expats and 1.4mn Saudi nationals) in 2007-12, aggregate health insurance premiums spiked

from SAR c. 3.1bn in FY 07A to SAR 11.2bn in FY12A. The largest gainers in terms of market

share were Tawuniya 32% (Buy, SAR 37), and Medgulf 22% (Hold, SAR 26), and Bupa 20%

(Hold, SAR 34) which combined have emerged as leaders in the Saudi health insurance market.

Please refer to our coverage of GCC Insurers – Selection is Key, published July 4, 2013.

Phase 2 of the KSA health insurance regulatory system, which mandates cover for public

sector employees with their dependants by insurance providers, is in our view the next leg of

the KSA opportunity healthcare providers, as well as insurers. Public sector employees with

their dependants (10% of workforce, 22% population) have recourse to healthcare services via

the system of public hospitals in the Kingdom. But the opportunity, in our view, is also within

the network of private sector healthcare providers. Given new cover by private insurance

providers, demand for private healthcare in KSA should grow exponentially, albeit from a very

low base. As per SAMA data, the number of Saudi nationals employed in the public sector

stood at 1mn (with 5mn dependants) in FY 11A. Assuming an average health premium of SAR

1,000, the implementation of phase 2 would release c.SAR 6.0bn in new premiums written

(+55% growth vs. FY 12A). We expect this to translate into a 50% rise in the number of patients

seeking treatment within the private healthcare sector of Saudi Arabia.

(iii) Soft loans from the Ministry of Finance to fund private sector capacity roll out

Credit ceiling for soft loans raised in 2011: Given that the initial investment necessary to

acquire a land plot to build a hospital in the vicinity of a major city in KSA is sizable, the Saudi

Ministry of Finance raised the credit ceiling imposed on soft loans offered to the private

healthcare sector to SAR 200mn (vs. SAR 50mn previously), in 2011. Soft loans can be used to

finance up to 50% of the setup cost of a new hospital, covering construction, land acquisition,

medical equipment and maintenance. Soft loans are currently interest-free and typically

offered at 25-yr tenors and 5-yr grace periods. As per SAMA data, the KSA Ministry of Finance

has so far issued 143 loans towards healthcare projects, totalling SAR 2.5bn (USD 680mn) in FY

11A, ( 7% CAGR in FY 07-11A).

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 11

Sizing the impact- soft loans alone to produce 3k new beds (+5%): Assuming an average

development cost/bed of SAR 1.5mn, we believe a medium size hospital in a prime urban

location in KSA runs a development bill of c.SAR 300mn. As the lower of either SAR 200mn or

50% of the total cost of a facility can be financed through a soft loan from the MoF, we

estimate that if an equivalent (SAR 2.5bn) book of loans is issued over the next 5 years, this

should produce an additional 15 hospitals (3k beds) by 2017e, raising the bed/patient ratio to

2.3 (+5% vs. today’s 2.2).

Exhibit 12: Healthcare insurance premiums issued in KSA have

risen at a CAGR of c.30% since FY 07A, driven by

regulation stipulating mandatory health cover

Source: SAMA

Exhibit 13: Government funding of private health projects: 143

loans, SAR 2.5bn issued since 2007

Source: SAMA

3- A closer look at government spending on healthcare services

Government spending remains the primary source of industry capacity growth: National

spending on healthcare has varied between 3.0% and 4.0% (of GDP) over the past 5 years,

largely in line with the regional average, but low by developed market standards (18% in the

US, 11% in France and Germany, 8% in the UK). Though public spending on healthcare by the

government has fluctuated, it remains the main source of healthcare financing, accounting for

c. 70% of total expenditure in 2012. Governmental hospitals still constitute more than 65% of

total hospital beds in the Kingdom.

Exhibit 14: KSA government healthcare spend

Source: SAMA, IMF

Exhibit 15: Public healthcare spending vs. private

Source: SAMA

3.1

4.8

7.3

8.7

9.7

11.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FY 07A FY 08A FY 09A FY 10A FY 11A FY 12A

Medical Insurance Premiums in KSA (SAR bn)

1,962

2,195 2,358

2,536 2,536

-

20

40

60

80

100

120

140

160

-

500

1,000

1,500

2,000

2,500

3,000

FY 07A FY 08A FY 09A FY 10A FY 11A

(SAR mn)

Soft loans for health projects Number of loans

34.4

40.4

46.6

52.4

61.0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY 08A FY 09A FY 10A FY 11A FY 12A

(SAR bn)

Healthcare spending As a percentage of GDP

67% 66% 66% 69% 70%

33% 34% 34% 31% 30%

0%

20%

40%

60%

80%

100%

120%

FY 08A FY 09A FY 10A FY 11A FY 12A

Public spending Private spending

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 12

As per the KSA government’s 9th Development Plan for 2010-2014, KSA aims to raise the

hospital bed/patient ratio to 3.3 per 1,000 from 2.2 in FY 08A (vs. 3.0 US, 8.3 Germany, 2.1

MENA). With the country’s population expected to reach 30mn by next year, the initial plan

mandated the addition of 44k beds (34k government and 10K private) by 2014, reflecting an

80% growth in the total bed capacity of the country vs. 2008. We currently find the plan

ambitious and unlikely to be met by 2014, as 10k beds (or +20%) have been introduced over

the past 3-4 years, leaving a huge pipeline due over the next 18 months. The private sector’s

share of the industry has remained unchanged at c.22% since 2011, while we estimate its share

of new capacity at around 25%.

Exhibit 16: 52 hospital added since 2006, of which 9 are private

Source: CARE and MoH

Exhibit 17: 19% overall growth in bed count since 2008

Source: CARE and MoH

218 225 231 244 249 261

39 39 39 39 39 39

127 123 123 125 127136

0

50

100

150

200

250

300

350

400

450

500

FY 06A FY 07A FY 08A FY 09A FY 10A FY 11A

Hospitals by sector

Ministry of health hospitals Other Gov. Hospitals Private hospitals

31 31 32 33 34 38

10 11 11 11 11 12

13 11 11 12 13

14

-

10

20

30

40

50

60

70

FY 06A FY 07A FY 08A FY 09A FY 10A FY 11A

Beds by sector ('000)

Ministry of health hospitals Other Gov. Hospitals Private hospitals

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 13

Key private healthcare groups in KSA

Exhibit 18: KSA outpatient visits by sector

Source: CARE prospectus Arqaam Capital Research

Exhibit 19: KSA inpatient visits by sector

Source: CARE prospectus Arqaam Capital Research

Exhibit 20: Top 10 private hospitals in Riyadh

Hospitals No. of

beds Market

share Specialty

Dr. Sulaiman Al-Habib Medical Group

655

18% Pediatrics, obstetrics & gynecology, IVF, orthopaedics, ophthalmology, dermatology, plastic

surgery

National Medical Care Company

420 12% Pediatrics, obstetrics & gynecology, orthopaedics, ophthalmology, dermatology

Dallah Hospital

400 11% Pediatrics, obstetrics & gynecology, IVF, orthopaedics, ophthalmology, cardiology

Specialized Medical Center Hospital

400 11% Ophthalmology, pediatrics, cardiology, dermatology, dentistry, and internal medicine

Saudi German Hospital Riyadh

300 8% Cardiology, neurology & neurosurgery, opthalmology, orthopaedics and traumatology

Al Hammadi Hospital

275 8% Obstetrics & gynecology, cardiology, orthopaedics, dermatology, pediatrics

Kingdom Hospital Consulting Clinics

125 3% Surgical & medical obesity, anesthesiology, dentistry

Dr Abdul Rahman Al-Mishari Hospital

122

3% Nursery & neonatal intensive care, obstetrics & gynecology, pediatrics

Al-Mouwasat Hospital

120 3% Pediatrics, obstetrics & gynecology, IVF, orthopaedics, ophthalmology, cardiology

Obeid Specialized Hospital

120 3% Pediatrics, ophthalmology, cardiology, dermatology, gastroenterology, dentistry

Others

708 19%

Total

3,645 100%

Source: Company Data, Arqaam Capital Research

Private inpatient visits,

91%

Public inpatient visits, 9%

FY 10A

Private outpatient visits, 86%

Public outpatient visits, 14%

FY 10A

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 14

The healthcare opportunity in the UAE

Drivers: Demographics, sedentary lifestyles, rising health awareness, shortages in

specialised services, the introduction of mandatory health insurance

Healthcare indicators are generally good in the UAE, but there exists evidence of a rapid

increase in lifestyle diseases (diabetes and obesity) over the past 10 years. The UAE

Ministry of Health-MOH is due to expand health programmes and introduce new

measures aiming at reducing mortality rates

The MOH will address the need to expand healthcare infrastructure over the next 5

years. Shortages exist in (i) bed supply and clinics (UAE bed/patient ratio 1.9 vs 2.1

MENA, 3.0 US) and (ii) specialised doctors (physician/patient 1.9/1000). The UAE

Government has encouraged private participation through PPP programs

The Abu Dhabi population is fully covered by mandatory employer-based health

insurance. Dubai is expected to introduce a similar scheme by the end of 2013.

Mandatory health cover is expected to be rolled out across remaining emirates going

forward

Mandatory insurance cover will catalyse demand and prompt substantial new supply-

we estimate 40% growth in bed count by 2018. (including AD)

1-Demographics and epidemiological trends

Population growth: The UAE population will expand by an annual average of 3% over the

coming 5 years, reaching 6.4mn in FY 17e (an aggregate increase of 0.8 mn). Major age groups

(0-14 and 15-64 years) will expand markedly, whereas the 65+ segment will account for only

1.1% of total population by FY 17e. As opposed to KSA, we believe the UAE will face no

material pressure from an aging population, as expatriates (85% of the workforce) typically

leave the country upon retirement.

Rising incidence of lifestyle-related diseases: Lifestyles, environmental conditions and

dietary habits have been the major causes for diabetes, cardiovascular diseases, and cancer in

the UAE. 36% of the UAE population is obese, as per data from the WHO (vs. 11% global, 36%

US, 30% MENA), 27% of adults have elevated cholesterol levels (vs. 39% global, 48% US, 40%

MENA), and 16% or 0.9mn people are diabetic (vs. 10% US, 9% MENA).

Exhibit 21: UAE Population to grow at c. 3% annually

...............................

Source: World Bank, BMI

Exhibit 22: 1% of overall population is >60, but segment growth >10% 5-

yr CAGR

Source: BMI

5.1 5.2 5.4 5.5 5.7 5.9 6.0 6.2 6.4

2.0%

2.5%

3.0%

3.5%

4.0%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

FY 09A FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

mn

UAE population Population growth (RHS)

0-14, 14%

15-60, 85%

>60, 1%

UAE population breakdown by age group

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 15

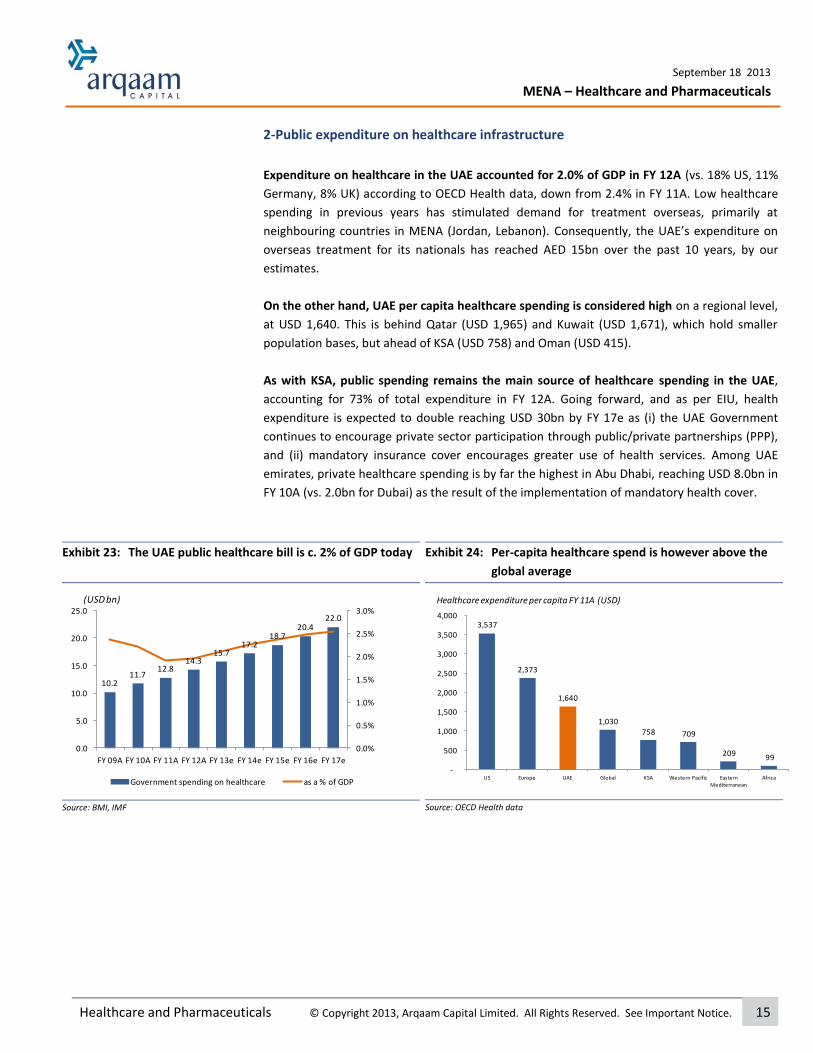

2-Public expenditure on healthcare infrastructure

Expenditure on healthcare in the UAE accounted for 2.0% of GDP in FY 12A (vs. 18% US, 11%

Germany, 8% UK) according to OECD Health data, down from 2.4% in FY 11A. Low healthcare

spending in previous years has stimulated demand for treatment overseas, primarily at

neighbouring countries in MENA (Jordan, Lebanon). Consequently, the UAE’s expenditure on

overseas treatment for its nationals has reached AED 15bn over the past 10 years, by our

estimates.

On the other hand, UAE per capita healthcare spending is considered high on a regional level,

at USD 1,640. This is behind Qatar (USD 1,965) and Kuwait (USD 1,671), which hold smaller

population bases, but ahead of KSA (USD 758) and Oman (USD 415).

As with KSA, public spending remains the main source of healthcare spending in the UAE,

accounting for 73% of total expenditure in FY 12A. Going forward, and as per EIU, health

expenditure is expected to double reaching USD 30bn by FY 17e as (i) the UAE Government

continues to encourage private sector participation through public/private partnerships (PPP),

and (ii) mandatory insurance cover encourages greater use of health services. Among UAE

emirates, private healthcare spending is by far the highest in Abu Dhabi, reaching USD 8.0bn in

FY 10A (vs. 2.0bn for Dubai) as the result of the implementation of mandatory health cover.

Exhibit 23: The UAE public healthcare bill is c. 2% of GDP today

…

Source: BMI, IMF

Exhibit 24: Per-capita healthcare spend is however above the

global average

Source: OECD Health data

10.211.7

12.814.3

15.717.2

18.720.4

22.0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0.0

5.0

10.0

15.0

20.0

25.0

FY 09A FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

(USD bn)

Government spending on healthcare as a % of GDP

3,537

2,373

1,640

1,030 758 709

209 99

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

US Europe UAE Global KSA Western Pacific Eastern Mediterranean

Africa

Healthcare expenditure per capita FY 11A (USD)

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 16

3-Healthcare policy

Healthcare policy in the UAE will focus on the expansion of infrastructure (new hospitals and

clinics), and the recruitment of specialised doctors, over the next 5 years. Health authorities

in Abu Dhabi estimate the demand for an additional 1,600 beds (vs. 4,700 beds currently) over

the period. This is underscored by the fact that only 2.0 physicians are currently available in

the emirates per 1,000 residents today, and severe shortages exists specifically in the

availability of specialists in emergency care, cardiology, critical and intensive care.

Exhibit 25: Physicians/1,000 residents: UAE remains behind global average, but ahead of KSA

Source: World Bank

Exhibit 26: 1.9 beds/1,000 residents: particularly low vs. developed markets and MENA average

Source: World Bank

4-Regulatory structure

The UAE Ministry of Health (MoH) is the regulator at the federal level, while public health

services are governed by different regulatory bodies at the emirate level. The UAE is

generally transitioning from a mono-regulatory system to a more decentralised structure in

which each emirate houses an autonomous health authority, supported by its own

infrastructure of institutions.

The Health Authority of Abu Dhabi (HAAD) was established in order to administer all

public healthcare institutions in Abu Dhabi, and to improve medical standards and

regulate policies. In addition, the Abu Dhabi Health Services Company (SEHA) was

established to act as the execution arm of HAAD policies and regulations. SEHA owns

and operates 12 hospital facilities and over 40 primary healthcare clinics in Abu Dhabi.

As the main health authority for the Emirate of Dubai, the Dubai Health Authority

(DHA) was created to regulate and deliver health services in Dubai, including free

zones. DHA owns and operates a network of hospitals and healthcare medical centers.

Mandated with the same objectives as HAAD and DHA, the Emirates Health Authority (EHA) is

responsible for the Northern emirates, including Ajman, Sharjah, Ras Al Khaima, Umm al

Quwain, and Fujairah.

4.3

3.73.4

2.8

2.4

1.91.7

0.9

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

Russia Germany France UK US UAE Turkey KSA

Physicians per 1,000

8.3

6.6

3.0 3.0

2.2 2.1 1.9

0

1

2

3

4

5

6

7

8

9

Germany France US UK KSA MENA UAE

Hospital beds per 1,000

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 17

5-Mandatory health cover: substantial demand catalyst to play out in 2014-15

Implemented in Abu Dhabi since 2007, mandatory health insurance cover is expected to be

rolled out across the remainder of the UAE by 2014. In the 3 year period between 2007 and

2010, the number of insurance claims processed in Abu Dhabi jumped 8x to 13.1mn in FY 10A

(98% CAGR). We expect private insurers to be the largest providers of new healthcare policies

going forward.

Exhibit 27: The number of inpatient claims expanded 4x as a result of mandatory health cover…

Source: HAAD

Exhibit 28: …similarly, outpatient claims grew 8x

Source: HAAD

The precedent: the Abu Dhabi health insurance system

Exhibit 29: Abu Dhabi insurance schemes by enrolment..

Source: HAAD

Exhibit 30: …and by claim value

Source: HAAD

There are 3 types of health insurance schemes in operation in Abu Dhabi. These address the

different social demographic groups that reside within the emirate:

Thiqa (UAE Nationals): All UAE nationals residing within the emirate are covered by a broad

scheme that administers a wide range of free treatments (including screening and dentistry),

at all private and public healthcare facilities in Abu Dhabi. It is provided by the National Health

Insurance Company (Daman). The number of UAE Nationals enrolled under Thiqa reached

588k in FY 11A. The program accounts for 16% of the enrolment base in Abu Dhabi in terms of

membership, but accounts for 48% of all claims processed.

42

166

-

20

40

60

80

100

120

140

160

180

FY 07A FY 10A

Inpatient Claims in AD ('000)

CAGR 58%

1.6

12.9

0

2

4

6

8

10

12

14

FY 07A FY 10A

Outpatient Claims in AD (mn)

CAGR 98%

Thiqa, 16%

Enhanced, 37%

Basic, 47%

(FY 11A)

Thiqa, 48%

Enhanced, 36%

Basic, 16%

(FY 11A)

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 18

Enhanced package (Expatriate residents): This is the insurance scheme offered to expatriates

that earn monthly salaries above AED 5k. It is an employer-based scheme offered by all

insurance companies, covering a spouse and 2 dependants with annual limits on payouts,

depending on the premium paid by employers. 37% of insured residents in Abu Dhabi fall

under the ‘Enhanced’ category, and account for a commensurate share of claims (36%).

Basic package (Expatriate residents): Expatriates who earn monthly salaries below AED 5k are

eligible for basic insurance cover. The scheme is employer-based and covers an annual benefit

limit of AED 250k, provided by Daman. It covers inpatient and outpatient care, maternity care

(in-patient maternity treatments subject to pre-approval), and emergency care. We note that

the package covers 47% of individuals enrolled in the program, but accounts for 16% of claims

processed in FY 11A.

The opportunity: Dubai and Northern Emirates

According to the Dubai Health Authority- DHA, 40% of the Dubai population (including 25%

of its expatriate residents) is covered by government and private health insurance schemes

today. That equates to 0.8mn residents, of which we estimate c.40% are UAE nationals, and

c.60% expatriates. We believe that at current, AED 1.32bn in insurance claims are collected in

Dubai, accounting for 30% of the UAE total.

Taking precedent from the growth in insurance claims processed in Abu Dhabi, in the 3 years

following the implementation of mandatory health cover in 2007 (4.0x), we calculate that

patient claims in Dubai should follow suit and reach AED 4.8bn (3.6x FY 11A) by FY 16e

(corresponding to the 3-year period during which the scheme is scheduled to be rolled out).

The jump in UAE claims is in our view a function of (i) higher health insurance premiums

(+150%) and (ii) a rise in claims per patient (+45% over the past 4 years in the UAE).

Accordingly, we expect healthcare demand in Dubai to pressure bed capacity, which will need

to grow by at least 50% (1,700 beds) in the coming 5 years to absorb incoming patients on

aggregate.

Exhibit 31: UAE health insurance premiums grew 2.7x over the past 4 years…

Source: National Bureau of statistics

Exhibit 32: …while claims expanded by 4x

Source: National Bureau of statistics

1.1

2.1

3.1

4.1

5.0

5.6

-

1.0

2.0

3.0

4.0

5.0

6.0

FY 06A FY 07A FY 08A FY 09A FY 10A FY 11A

UAE written premiums (AED bn)

0.5

1.1

1.6

2.5

3.6

4.4

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

FY 06A FY 07A FY 08A FY 09A FY 10A FY 11A

UAE claims paid (AED bn)

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 19

Medical tourism flows can reverse course as bed capacity and service quality improve The UAE aims to transition towards becoming a recipient, rather than a supplier, of medical

tourism flows in MENA. As an initial step, Dubai has introduced a 3-month visa (extendable to

9) designed for foreign visitors seeking medical treatment in the emirate. Though the

necessary infrastructure is gradually being installed, we believe inbound medical tourism will

remain muted in the near term, as shortage in bed capacity and the availability of specialised

doctors remain in place. It is worth noting that according to the Abu Dhabi Health Authority,

outbound patients seeking treatment abroad have retracted by 50% as of 2011, to reach 1,451

Emirati nationals (equivalent 3.4 per 1000).

September 18 2013

MENA – Healthcare and Pharmaceuticals

Healthcare and Pharmaceuticals © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 20

Key UAE healthcare indicators

Exhibit 33: Healthcare indicators in Dubai and Abu Dhabi

Dubai Abu Dhabi

Private hospitals 19 17

Public hospitals 5 18

Total hospitals 24 35

Public beds 2,006 1,765

Private beds 1,238 2,984

Total bed capacity 3,244 4,749

Beds/1,000 people 1.9 2.1

Physicians/1,000 people 2.9 2.0

Source: HAAD, DHA, WHO

Exhibit 34: Abu Dhabi inpatients by sector

Source: HAAD

Exhibit 35: Abu Dhabi outpatients by sector

Source: HAAD

Exhibit 36: Abu Dhabi hospitals by sector

Source: HAAD, company data

Exhibit 37: Dubai hospitals by sector

Source: DHA, company data

Exhibit 38: Abu Dhabi hospital beds by sector

Source: HAAD, company data

Exhibit 39: Dubai hospital beds by sector

Source: DHA, company data

Public, 65%

Private, 35%

FY 11A

Public, 40%

Private, 60%

FY 11A

Private hospitals, 49%Public

hospitals, 51%

FY 11A

Private hospitals, 79%

Public hospitals, 21%

FY 11A

Private hospital beds, 2,984 ,

63%

Public hospital beds, 1,765 ,

37%

FY 11A

Private hospital beds, 1,238 ,

38%Public hospital beds, 2,006 ,

62%

FY 11A

I n i t i a t i o n R e p o r t

S e p t e m b e r 1 8 2 0 1 3

Mohammad Kamal [email protected] +9714 507 1743

Dahlia Sabaayon, CFA Arqaam Capital Research Offshore s.a.l

Saudi Arabia – Healthcare and Pharmaceuticals Al Mouwasat Medical Services Co.

BUY

Healthcare and Pharmaceuticals / Saudi Arabia Bloomberg code MOUWASAT AB

Market index SASEIDX

Price target (local) 103

Upside (%) 30.9

Market data 12/09/2013

Last closing price 79.00

52 Week range 48.2-85.0

Market cap (SARmn) 3,950

Market cap (USDmn) 1,053

Average daily traded value (SARmn) 12.6

Average daily traded value (USDmn) 3.4

Year-end (local mn) 2012 2013e 2014e 2015e

Revenues 796.5 943.7 1,114.6 1,199.1

EBITDA 224.7 280.6 337.7 345.9

Net income 171.6 217.7 260.5 279.1

EPS 3.43 4.35 5.21 5.58

P/E (current price) 23.0 18.1 15.2 14.2

BVPS 16.3 19.3 22.7 26.2

P/B (current price) 4.9 4.1 3.5 3.0

EV/EBITDA (current price) 18.3 14.7 12.2 11.9

Div. yield (%) 1.9 1.7 2.2 2.6

FCF margin (%) (1.2) 2.7 2.1 9.4

Net debt/EBITDA (x) 0.4 0.4 0.6 0.5

Net debt/Capital (%) 7.6 10.8 13.7 11.7

Interest cover (x) 164.5 95.8 76.3 58.5

RoAA (%) 15.6 17.2 18.1 16.8

RoAE (%) 22.5 24.5 24.8 22.8

RoIC (%) 18.2 21.7 21.4 20.1

Core growth drivers are in an even blend of volume (bed capacity +85%) and pricing elements (re-pricing of insurance contracts +20%) Cheap in peer context: 23%+ RoE at 15.2x FY 14e P/E, 15% discount to peers. Initiate with Buy, SAR 103 FVE

Mouwasat Medical Services is a broad play on the Saudi healthcare

sector. We believe Mouwasat is trading at an unwarranted 15% discount

to regional peer set multiple of 17.6x/15.9x, given its (i) superior returns

(23% FY 13e RoE vs. 15% for local peers, (ii) EPS outlook at 15% CAGR, and

(iii) unique growth catalysts. We value Mouwasat at SAR 103/share,

implying 30% in upside from current market price, using DCF. We initiate

with a Buy rating and a FVE of SAR 103.

The business enjoys 3 key growth catalysts that in our view are currently

foregone in current share price: (i) Bed capacity expansion to 1,089 beds

(c. 85% growth) by FY 18e, translating into an 5-yr revenue CAGR of 13%,

(ii) A departure from its core market towards the urban center of Riyadh,

through the roll out of an additional 175 beds (23% of total bed capacity)

by the end of FY 13e. Both volume elements above should produce a 75%

growth in revenues over the next 5 years. (iii) Agreements with insurers

regarding the collection of patient claims, which constitute 40% of

revenues, have recently been re-priced upwards by an average of 20%.

This is a negotiated process that adjusts the collection ratios applied on

inpatient and outpatient services administered to patients that enjoy

health insurance cover. Contract prices have not been reset since 1994,

and we model for a 2% increase in FY 14e onwards. This should translate

into 8% incremental revenues, and consequently a 160bps expansion in

blended margins. Both volume and price elements combined will in our

view drive 13% revenue CAGR.

Revenue visibility is strong on corporate client base: 40% of revenues

derive from corporate clients (Aramco, GOSI and other large corporates).

The company’s broad presence in the eastern province has resulted in a

disproportionately large share of the healthcare industry in the region, at

28% (inpatients) and 16% (outpatients).

Cheap in peer context: Mouwasat currently trades at 15.2x FY 14e EPS vs.

17.6x and 19.3x for regional and local peers, implying a discount of 15%

and 20%, respectively. We believe the stock should re-rate and trade in-

line with sector multiples, at the very least. Risks: Delays, Saudisation

laws.

SAR 103

© Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice.

Price Performance

81

99

117

135

153

171

Sep-12 Dec-12 Mar-13 Jun-13

MOUWASAT AB SASEIDX

September 18 2013

Al Mouwasat Medical Services Co. © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 22

Abacus Arqaam Capital Fundamental Data

Profitability

Growth

Gearing

Valuation

0%

20%

40%

2012 2013e 2014e 2015e 2016e

EBITDA Margin Net Margin

0%

10%

20%

30%

2012 2013e 2014e 2015e 2016e

Revenues Assets

0%

5%

10%

15%

0.0

0.2

0.4

0.6

2012 2013e 2014e 2015e 2016e

Net Debt/Capital Net Debt/EBITDA

0

10

20

30

2012 2013e 2014e 2015e 2016e

P/E P/E Sector

Al Mouwasat Medical Services Co.

Year-end 2011 2012 2013e 2014e 2015e 2016e

Financial summary

Reported EPS 2.96 3.43 4.35 5.21 5.58 6.08

Diluted EPS 2.96 3.43 4.35 5.21 5.58 6.08

DPS 1.00 1.50 1.37 1.74 2.08 2.23

BVPS 14.22 16.27 19.25 22.72 26.22 30.07

Weighted average shares 50.00 50.00 50.00 50.00 50.00 50.00

Average market cap 2,239.00 2,617.50 3,865.00 3,865.00 3,865.00 3,865.00

Year-end 2011 2012 2013e 2014e 2015e 2016e

Valuation metrics

P/E (x) (current price) 26.7 23.0 18.1 15.2 14.2 13.0

P/E (x) (target price) 34.9 30.1 23.7 19.8 18.5 17.0

P/BV (x) (target price) 7.3 6.4 5.4 4.5 3.9 3.4

EV/EBITDA (x) (target price) 25.8 23.6 18.9 15.7 15.3 13.5

EV/FCF (x) 41.5 (534.3) 207.3 221.6 46.8 24.3

EV/Invested capital (x) 6.4 5.4 5.0 4.1 3.6 3.2

Dividend yield (%) 1.3 1.9 1.7 2.2 2.6 2.8

Year-end 2011 2012 2013e 2014e 2015e 2016e

Growth (%)

Revenues 15.5 17.4 18.5 18.1 7.6 15.1

EBITDA 16.7 9.4 24.9 20.3 2.4 13.5

EBIT 18.5 9.9 28.7 19.5 7.3 8.8

Net income 24.9 15.9 26.9 19.7 7.2 8.9

Year-end 2011 2012 2013e 2014e 2015e 2016e

Margins (%)

EBITDA 30.3 28.2 29.7 30.3 28.8 28.4

EBIT 24.9 23.4 25.4 25.7 25.6 24.2

Net 21.8 21.5 23.1 23.4 23.3 22.0

Year-end 2011 2012 2013e 2014e 2015e 2016e

Returns (%)

RoAA 15.8 15.6 17.2 18.1 16.8 16.3

RoAE 22.5 22.5 24.5 24.8 22.8 21.6

RoIC 18.6 18.2 21.7 21.4 20.1 19.3

FCF margin 18.8 (1.2) 2.7 2.1 9.4 15.8

Year-end 2011 2012 2013e 2014e 2015e 2016e

Gearing (%)

Net debt/Capital (6.4) 7.6 10.8 13.7 11.7 4.2

Net debt/Equity (7.6) 10.0 12.9 16.5 13.7 4.8

Interest cover (x) 79.2 164.5 95.8 76.3 58.5 60.8

Net debt/EBITDA (x) (0.3) 0.4 0.4 0.6 0.5 0.2

September 18 2013

Al Mouwasat Medical Services Co. © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 23

Abacus Arqaam Capital Fundamental Data

Company overview

Established in 1974, Mouwasat Hospital owns and operates 4 hospitals and 2 dispensaries in the eastern province of KSA with a total bed capacity of 594 beds and 227 clinics as of FY 12A. The company is also in the process of launching a new hospital in Riyadh at a total bed capacity of 175 beds. SABIC and Saudi Aramco are the company’s two largest clients, generating 40% of its healthcare revenues.

Ownership and management

Shareholders

Mohammed Sultan Hammad Al Subaie 17.5%

Nasser Sultan Fahad Al Subaie 17.5%

Suleiman Mohammed Suleiman Al Saleem 17.5%

Public 47.5%

Source: Zawya

Board of Directors

Mr. Mohammed Sultan Hammad Al Subaie Chairman

Mr. Nasser Sultan Fahad Al Subaie Director

Mr. Mohammed Bin Suleiman Al Saleem Director

Mr. Khaled Bin Suleiman Al Saleem Director

Mr. Ibrahim Hamad Al Babtain Director

Mr. David Anthony Price Director

Mr. Abdulaziz Saad Al Mangoor Director

Source: Company data

Al Mouwasat Medical Services Co.

Year-end 2011 2012 2013e 2014e 2015e 2016e

Income statement (SAR mn)

Sales revenue 678.4 796.5 943.7 1,114.6 1,199.1 1,380.3

Gross profit 324.0 372.7 456.5 542.5 582.9 651.6

SG&A (154.7) (186.7) (217.1) (256.4) (275.8) (317.5)

EBITDA 205.5 224.7 280.6 337.7 345.9 392.5

Depreciation & Amortisation (36.2) (38.7) (41.2) (51.6) (38.8) (58.3)

EBIT 169.3 186.0 239.4 286.1 307.1 334.1

Net interest income(expense) (2.1) (1.1) (2.5) (3.8) (5.3) (5.5)

Associates/affiliates — — — — — —

Exceptionals/extraordinaries — — — — — —

Other pre-tax income/(expense) 8.5 8.7 8.7 8.7 8.7 8.7

Profit before tax 175.6 193.6 245.6 291.0 310.5 337.3

Zakat (16.0) (8.6) (10.8) (12.9) (13.7) (14.9)

Minorities (11.5) (13.4) (17.0) (17.7) (17.7) (18.5)

Other post-tax income/(expense) — — — — — —

Net profit 148.1 171.6 217.7 260.5 279.1 303.9

Arqaam adjustments (including dilution) — — — — — —

Arqaam Net profit 148.1 171.6 217.7 260.5 279.1 303.9

Year-end 2011 2012 2013e 2014e 2015e 2016e

Balance sheet (SAR mn)

Cash and equivalents 192.7 177.7 63.0 44.6 45.5 153.2

Receivables 183.5 215.7 255.6 301.9 324.8 373.9

Inventories 58.6 62.6 72.0 84.5 91.1 107.7

Tangible fixed assets 525.6 688.0 852.9 1,059.3 1,214.4 1,272.8

Other assets including goodwill 24.5 75.1 75.1 75.1 75.1 75.1

Total assets 984.8 1,219.2 1,318.6 1,565.4 1,750.9 1,982.6

Payables 108.3 115.2 132.5 155.6 167.5 198.1

Interest bearing debt 138.5 259.1 187.6 232.3 224.5 225.9

Other liabilities 27.2 31.2 35.9 41.5 47.9 55.3

Total liabilities 274.0 405.6 355.9 429.4 439.9 479.3

Shareholders equity 710.9 813.6 962.7 1,136.1 1,311.0 1,503.3

Minorities — — — — — —

Total liabilities & shareholders equity 984.8 1,219.2 1,318.6 1,565.4 1,750.9 1,982.6

Year-end 2011 2012 2013e 2014e 2015e 2016e

Cash flow (SAR mn)

Cashflow from operations 221.9 192.8 231.6 281.9 306.9 334.5

Net capex (94.2) (202.7) (206.1) (258.0) (193.9) (116.6)

Free cash flow 127.7 (9.9) 25.5 23.9 113.0 217.9

Equity raised/(bought back) — — — — — —

Dividends paid (50.0) (75.0) (68.6) (87.1) (104.2) (111.6)

Net inc/(dec) in borrowings (28.2) 120.6 (71.6) 44.8 (7.9) 1.4

Other investing/financing cash flows 6.1 (50.7) — — — —

Net cash flow 55.5 (15.0) (114.7) (18.4) 0.9 107.6

Change in working capital 21.6 (27.1) (32.0) (35.7) (17.4) (35.1)

Mohammad Kamal Dahlia Sabaayon, CFA [email protected] Arqaam Capital Research Offshore s.a.l +9714 507 1743

September 18 2013

Al Mouwasat Medical Services Co. © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 24

Bed capacity expansion (+85%) and the re-pricing of insurance

contracts (+20%) drive 15% EPS CAGR

Cheap in peer context: 15.2x FY 14e EPS 15% discount to comparables. Initiate with

Buy, SAR 103 FVE

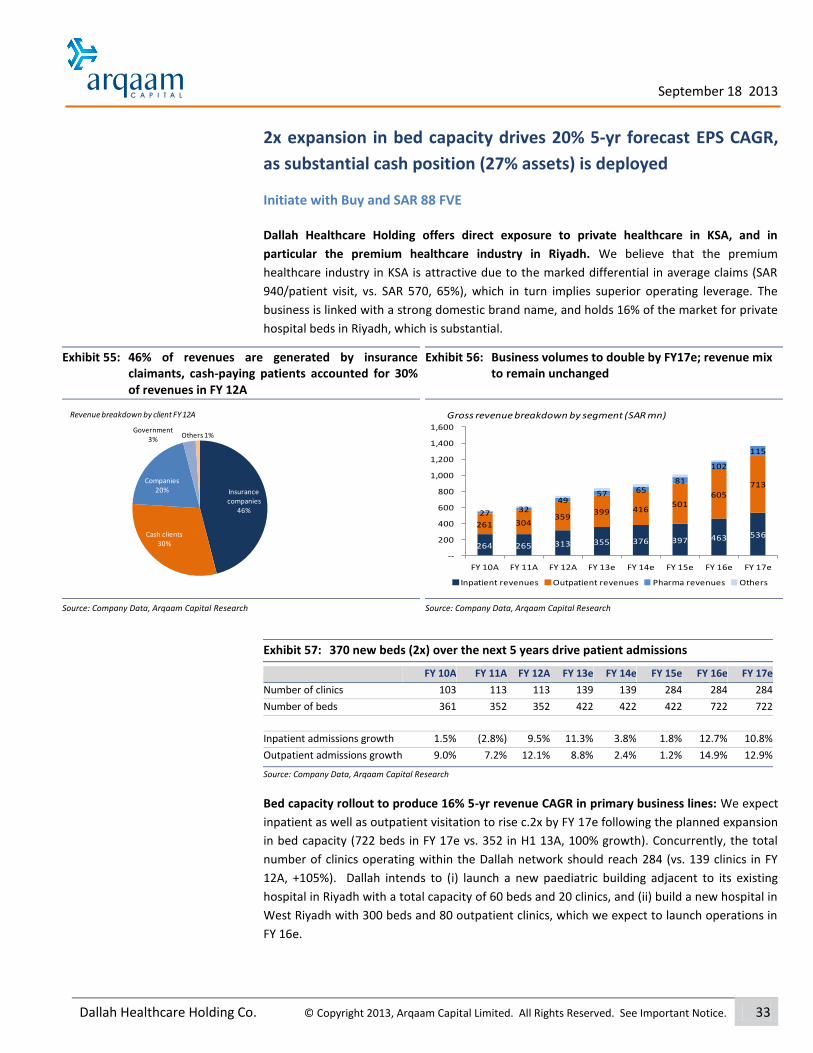

Al Mouwasat is a medical services provider that operates 6 facilities in the Eastern province

of KSA (Dammam, Jubail, Qatif, and Madina). We believe that the company is very well

positioned to capitalise on (i) its geographical presence in the Eastern Province (largest oil

industry community in the Kingdom; population of 4.3mn) and its strategic relationships with

insurance companies and direct corporate clients, which offer medium-term visibility on

revenue growth, (ii) the recent re-pricing of contracts with insurance companies, which should

support revenues from insurance (40% in FY 12A) by 20%+, (iii) expansion plans to raise its bed

capacity to 1,089 beds (c. 90% growth) by FY 18e, translating into a 5-yr revenue CAGR of 13%,

and (iv) future plans to expand to Riyadh by operating 175 beds (23%) by the end of FY 13e.

We initiate coverage on Mouwasat with a Buy recommendation and a fair value estimate of

SAR 103, offering 30% in upside potential vs. current market price.

Exhibit 40: KSA beds by sector

Source: Company Data, Arqaam Capital Research

Exhibit 41: Mouwasat market share (based on inpatient admissions)

Source: Company Data, Arqaam Capital Research

Riyadh Hospital to expand foothold in the Saudi Capital: The company is currently

establishing 2 new hospitals in Riyadh (which houses 26% of the Saudi population) and Khobar

(4%) in a step intended to expend into a relatively underpenetrated, highly concentrated urban

(2.6x bed per 1,000 residents (vs. 2.1 MENA, 3.0 US, 5 mn residents). Additionally, Mouwasat

intends to raise total bed capacity to 1,089 beds by FY 18e (+85%, vs. 594 beds in FY 12A) by

expanding its existing 4 hospitals in the Eastern Province (Dammam, Jubail, Qatif and Madina).

Riyadh hospital is expected to constitute 15% of the company’s total revenues by FY 18e.

Overall CAPEX in relation to both the new hospitals and bed capacity expansions amounts to

SAR 770mn, and will be financed through (i) SAR 240mn from the company’s operation (net

cash as of H1 13A is 240mn), (ii) a soft loan from the Ministry of Finance (SAR 200mn), (iii) and

the remaining 330mn from conventional loans.

Private hospital beds, 23%

Public hospital beds, 77%

22.9%24.1%

25.8%26.7% 27.5%

14.4% 14.5% 14.9%16.5%

19.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

FY 08A FY 09A FY 10A FY 11A FY 12A

East region Madinah

September 18 2013

Al Mouwasat Medical Services Co. © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 25

Exhibit 42: 495 new beds over the next five years drive patient admissions

FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

Number of clinics 188 188 188 253 253 253 376 376

Number of beds 594 594 594 769 869 869 1,089 1,089

Inpatient admissions (000') 37 39 42 44 59 66 72 78

Outpatient admissions (000') 1,316 1,341 1,454 1,402 1,525 1,550 1,912 2,121

Source: Company Data, Arqaam Capital Research

Revenue visibility is high, given corporate client base: As 40% of revenues are driven by

corporate clients (Aramco, GOSI and other large corporations), Mouwasat enjoys a degree of

revenue visibility absent among comparable healthcare providers. The company’s broad

presence in the Eastern Province has resulted in strong relationships with direct corporate

clients. There exists a direct correlation between the proportion of corporate clientele

contributing to revenues (40%), and the degree of exposure to insurance-based patient

visitation (40%), as mandatory health cover in KSA since 2007 has mandated insurance cover

for all residents employed in the private sector.

Exhibit 43: Revenue visibility is high given corporate client base

Source: Company Data, Arqaam Capital Research

Exhibit 44: 1,089 bed capacity by FY 17e

Source: Company Data, Arqaam Capital Research

Re-pricing continues to drive revenue in FY 13e: The business posted robust revenue growth

in the past 3 years (FY 10-12A CAGR 17%), mainly due to (i) higher healthcare charges imposed

on cash business (20% in FY 12A) , and (ii) rising patient visitation (+11%), as a result of a ramp

up in utilisation rates (53% in FY 12A) across facilities. In FY 11, the business received approval

from the Ministry of Health to raise its charges on medical services by 25%, and in April of this

year announced a 20-25% increase on insurance premiums, effective January 2013. The

increase in premiums will be passed on to all insured clients, with the exception for Medgulf,

which had its charges revised in 2011 (as Mouwasat’s SABIC account became insurance-based,

and covered by Medgulf). The account was previously a direct corporate client of Mouwasat’s).

We expect average claims/patient to grow by 8% in FY 13e, and to subsequently settle at an

average growth of 2% thereafter. We expect Mouwasat to register revenue CAGR of c.12%

over the next 3 years via (i) a ramp up in utilisation rates within existing hospitals, (and ii) the

launch of 2 new hospitals by 2016 (driving c.10% of revenue growth by 2016).

Insurance companies, 40%

Corporates (inlcuding

Aramco) , 40%

Cash business, 20%

Revenue breakdown by client FY 12A

188 188 188 253 253 253

376 376

594 594 594

769

869 869

1,089 1,089

--

200

400

600

800

1,000

1,200

FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

Number of clinics Number of beds

September 18 2013

Al Mouwasat Medical Services Co. © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 26

Valuation: trades at 15% discount to lower-margin peer set, RoE

superiority should command premium

30% in potential upside on DCF-based price target of SAR 103; initiate with Buy

Cheap in peer context: Mouwasat currently trades at 15.2x FY 14e EPS vs. 17.6x and 19.3x for

regional and local peers, implying a discount of 15% and 20%, respectively. We believe

Mouwasat should re-rate to trade to trade in-line with domestic peers at the very least, given

its (i) stronger growth (5-yr EPS CAGR of 15%, vs. 14% peers), (ii) leading position in the Saudi

healthcare market (28% and 16% in the eastern region in terms of inpatients and outpatients

respectively, in FY 12A), (iii) superior profitability (23% FY 14e RoE vs. 15% for local peers).

Exhibit 45: Unwarranted 15% discount to regional peers

P/E EV/EBITDA

At market price FY 13e FY 14e FY 15e FY 13e FY 14e FY 15e

Dallah Healthcare 26.0 19.3 15.7 16.8 14.0 11.4

Mouwasat 18.1 15.2 14.2 14.7 12.2 11.9

National Medical Care 24.8 23.4 20.9 17.1 15.4 13.6

NMC Health 13.8 12.7 11.5 10.7 9.8 8.5

Al Noor Hospitals Group 23.1 17.5 17.2 12.5 10.0 9.7

Average regional peers 21.2 17.6 15.9 14.3 12.3 11.1

Premium/ (discount) -14% -14% -11% 2% -1% 7%

Source: Company Data, Arqaam Capital Research

Exhibit 46: Attractively priced despite RoE differential…

Source: Company Data, Arqaam Capital Research

Exhibit 47: …And EPS growth (5-yr forward CAGR)

Source: Company Data, Arqaam Capital Research

DALLAH

MOUWASAT

CARE

NMC

Al Noor

10

12

14

16

18

20

22

24

26

0% 10% 20% 30% 40%

FY 14e RoE (%)

PE 14e

DALLAH

MOUWASAT

CARE

NMC

Al Noor

10

12

14

16

18

20

22

24

26

0% 5% 10% 15% 20%

5-yr EPS CAGR

P/E 14e

September 18 2013

Al Mouwasat Medical Services Co. © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 27

We value Mouwasat at SAR 103/share, implying 30% in upside potential from current market

price, using DCF. We apply a WACC of 9.5% (11.0% Re, 0.85 Beta, 5% Rd) and a terminal growth

rate of 4%. We believe current market valuation (At 15.2x/14.2x FY 14e/15e P/E) does not

reflect business fundamentals, catalysts in the coming 12 months, growth (13% FY 13-18e

revenue CAGR) and comparatively superior returns (+23% RoE).

Exhibit 48: DCF summary

Source: Company Data, Arqaam Capital Research *FCF calculation based on adjusted EBIT rather than net income

Risks

Delays in the launch of facilities in Riyadh and Madina could be material to growth forecasts.

Saudisation requirements may become more demanding, and this is material to margins. We

estimate that for every 5% increase in staff costs, a 130bps compression in EBITDA margins is

likely. This on aggregate cam cut our FVE by 7%.

DCF summary

SARmn unless otherwise stated FY 13e FY 14e FY 15e FY 16e FY 17e FY 18e FY 19e FY 20e

EBIT (1-τ) 229 273 294 319 385 454 470 479

Depreciation & Amortization 41 52 39 58 54 61 63 64

EBITDA 270 325 332 378 439 514 532 543

Working Capital Changes (32) (36) (11) (28) (29) (31) (1) 6

Operating Cash Flow 238 289 321 350 410 484 532 549

Purchase of PPE (206) (258) (194) (117) (108) (121) (125) (128)

Free Cash Flow to Firm 32 31 127 233 301 362 406 421

Discount Factor using WACC at 9.5% 0.97 0.89 0.81 0.74 0.68 0.62 0.56 0.51

PV of Visible FCFF 10 28 103 173 204 224 229 217

Terminal Value 7,958

Equity Valuation WACC parameters

PV of Visible FCFF 1,186 22% Rf 4.2%

PV of Terminal Value 4,094 78% EMRP 8.0%

Enterprise Value 5,280 Adjusted Beta 0.85

Cost of Equity 11.0%

Cash & Cash Equivalents 178

Less: Net (Debt) Funds (259) Marginal tax rate 2.50%

Investments in associates 8

NCI (50) Cost of Debt 5.00%

D/C (market) 25.00%

Equity Value 5,156 WACC 9.50%

NOSH 50 Perpetual grow th 4.00%

Equity Value per Share 103

Implied multiples

EV/EBITDA 19.6 16.2 15.9 14.0 12.0 10.3 9.9 9.7

P/E 23.7 19.8 18.5 17.0 14.0 11.8 11.4 11.2

P/B 5.4 4.5 3.9 3.4 2.9 2.5 2.2 2.0

September 18 2013

Al Mouwasat Medical Services Co. © Copyright 2013, Arqaam Capital Limited. All Rights Reserved. See Important Notice. 28

Business Trends

Exhibit 49: Uniform growth across business lines (13% CAGR)

Source: Company Data, Arqaam Capital Research

Exhibit 50: Patient visitation to double by FY 17e

Source: Company Data, Arqaam Capital Research

Exhibit 51: Margin expansion in FY 13e on a re-pricing of insurance contracts

Source: Company Data, Arqaam Capital Research

Exhibit 52: Improvements to filter through to net margins

Source: Company Data, Arqaam Capital Research

Exhibit 53: RoE among the highest in healthcare coverage space

Source: Company Data, Arqaam Capital Research

Exhibit 54: Positive free cash flows throughout forecast period …….

Source: Company Data, Arqaam Capital Research

192 229 275 312 422 480 538 594 257 301

358 450

492 500

604 697

137 148

164 182

201 219

238

257

--

200

400

600

800

1,000

1,200

1,400

1,600

1,800

FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

Revenue breakdown by segment (SAR mn)

Inpatient revenues Outpatient revenues Pharma revenues

--

500

1,000

1,500

2,000

2,500

3,000

--

10

20

30

40

50

60

70

80

90

FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

Total number of patients (000')

Number of inpatient visitors Number of outpatient visitors

176 205

225

281

338 346

392

457

--

50

100

150

200

250

300

350

400

450

500

--%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

(SAR mn)

EBITDA EBITDA margin

119 148

172

218

260 279

304

368

--

50

100

150

200

250

300

350

400

--%

5.0%

10.0%

15.0%

20.0%

25.0%

FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

(SAR mn)

Net income Net margin

--

50

100

150

200

250

300

FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

Capex vs. borrowings (SAR mn)

Capex Debt

167 190 216 270

325 332 378 439

(84)(94)

(203)

(206) (258) (194)(117) (108)

(400)

(300)

(200)

(100)

--

100

200

300

400

500

FY 10A FY 11A FY 12A FY 13e FY 14e FY 15e FY 16e FY 17e

FCF composition (SAR mn)

NOPLAT Working capital changes Capex