media slant against foreign owners: downsizing guido friebel and

TRANSCRIPT

1

Media slant against foreign owners: Downsizing

Guido Friebel and Matthias Heinz1

July 2014

Abstract:

Using a unique data set from nationally distributed quality newspapers in Germany, we find

evidence for both quantitative and qualitative media slant against foreign firms. A downsizing

foreign firm receives almost twice as much attention as a domestic firm, and the tone of media

reports is more negative. Media slant is a measure for economic xenophobia directed against

foreign owners, which constitutes an obstacle to foreign direct investment.

Keywords: media economics, globalization, economic xenophobia, multi-national enterprises,

foreign direct investment

JEL Codes: L82, L33, L10

1 Friebel is at Goethe University Frankfurt and associated with CEPR and IZA. Heinz is at the University

of Cologne. Email: [email protected]; [email protected]. We thank the Editor,

Brian Knight, and two referees, Simon Anderson, Iwan Barankay, Sascha Becker, Stefan Bender, Paolo

Cox, Stefano DellaVigna, Klaus Desmet, Ruben Durante, Karolina Ekholm, Ruben Enikolopov, Lapo

Filistrucchi, Matthew Gentzkow, Lisa George, Fabrizio Germano, Maria Guadalupe, Sergei Guriev,

Peter Haan, Andrea Ichino, Niels Kemper, Joep Konings, Michael Kosfeld, Olga Kuzmina, Christian

Leuz, Alexander Lipponer, Marc-Andreas Muendler, Volker Nocke, Stefan Pasch, Maria Petrova,

Andrea Prat, Riccardo Puglisi, Ally Raith, Isabell Schnabel, Jana Schneider, Monika Schnitzer,

Antoinette Schoar, Andrei Shleifer, Eugene Soltes, David Strömberg, Jo Swinnen, James Tremewan,

Natalya Volchkova, Joel Waldfogel, Jörgen Weibull, Ekaterina Zhuravskaya and seminar participants

in Berlin (DIW), Cologne, Frankfurt, KU Leuven and Stockholm School of Economics for their

comments. We also thank conference audiences at the European Economic Association Meeting in Oslo

2011, the 9th Workshop on Media Economics in Moscow 2011 and the 3rd TILEC Workshop on Media

and Communication in Tilburg 2013.We are grateful to MediaTenor and YouGov for access to data, and

the DFG grant number GZ: FR 2822/1-1 that supported this research.

2

1. Introduction

Using a unique data set of nationally distributed quality newspapers in Germany, we establish

the existence of a strong media slant against foreign owners. On average, firms that are

controlled by foreign block-holders attract almost twice the media attention for each job shed

compared to domestic firms. More articles are written about downsizing when owners are

foreigners, and, in an average article, more of the words written concern downsizing rather than

other topics, such as firm performance, products, etc. Quantitative slant is accompanied by

qualitative slant; that is, newspapers report more negatively about downsizing in foreign-owned

firms.

Our estimates are likely to be a conservative measure of media slant against foreign

owners, because our sources are quality newspapers. Moreover, Germany is a leading export

country, and Germans tend to be very positive about globalization.2 Nonetheless, we find

evidence in line with Scheve and Slaughter’s (2006) observation that “people perceive an

asymmetric distribution of the benefits of globalization: more for consumers and corporations,

but less for workers”.

Media slant may affect foreign direct investment (FDI), because bad press creates a risk

of being penalized by consumers. In Section 2, we provide illustrative examples of consumer

reactions to downsizing news that were harmful for foreign firms. Foreign investors will price

in this risk, leading to FDI discounts, and lower investment in consumption good industries to

avoid visibility to consumers. Foreign investors may also refrain from buying firms that are

candidates for downsizing. Media slant may hence constitute a behavioral obstacle to FDI,

which according to some observers may potentially be equally important as the formal obstacles

dictated by governments (OECD, 2003).

2 On a level above that of the U.S., cf. Mayda and Rodrik (2005).

3

We use three data sets to establish and investigate the slant against foreign owners. Our

first data set is based on 5,394 articles from Germany’s newspaper Die Welt on a total of 651

downsizing events in Germany between December 2000 and September 2008.3 Following

Gentzkow and Shapiro’s (2006) definition of slant, we focus on the varying intensity of

reporting a fact, measured by the number of words written per job shed in instances of

downsizing by foreign-owned employers relative to domestic ones. A second data set from the

media consultancy Media Tenor measures the different qualitative evaluations involved. We

also collected a third data set that includes all articles on downsizing during five randomly

chosen months from all nationally distributed quality newspapers in Germany.

To build the first data set, we developed an algorithm aiming to reduce the probability

of making two types of errors: including “false” downsizing cases, and failing to include “real”

ones (see Section 3). The regressions (Section 4) show a strong media slant against foreign-

owned firms controlling for the magnitude of the downsizing event, the industry, and the size

of the firm measured in employment. The results are unchanged when more of the downsizing

event’s specificities are taken into account, like the downsizing magnitude relative to firm size,

establishment closures, regional unemployment, and the speed of downsizing. Propensity score

methods deal with foreign firms’ potential self-selection into specific regions and industries.

Investigating potential spurious correlations, our regressions show that the results are

robust to the inclusion of controls for the reason for downsizing and the type of ownership (see

Section 5). We also find no evidence that specific groups of countries4 drive the slant: rather,

the magnitude of the slant is quite similar across country groups. There is no tendency to report

3 We end with September 2008 because the collapse of Lehman Brothers triggered a wave of downsizing

and state interventions, and we are interested in normal, rather than special, times. 4 Distinctive features of such country groups could be cultural or linguistic distance to Germany, or

rather general perceptions of “free” market-based economic systems like those of the U.K. or the U.S.

compared to the continental European model of a “social” market economy.

4

more about foreign firms in general, or their job creation.5 Other omitted variables can be

controlled for to some extent. For a subset of large firms, we are able to match our data set with

financial and accounting information from the Amadeus data set (Bureau van Dijk, 2011).

Despite a smaller sample, the slant is statistically significant, while covariates such as assets,

employment costs per capita or return on equity before downsizing are not.

We also carried out a number of additional analyses to investigate what hypotheses

could explain the slant, some of which are briefly presented in Section 6. On the supply side,

we find no evidence that the bias6 of certain journalists can explain newspapers’ reports,7 or

that ownership changes affect the slant. Looking at other stakeholders, we do not find

significant advertiser influence. Political economy explanations like Besley and Prat’s (2006)

theory do not apply either, because in our period of observation, Germany was run by the

globalization-friendly Schröder and Merkel governments who had little to gain by influencing

the media against foreign owners. Inspired by Puglisi’s (2011) analysis of changes in the

agenda-setting behavior of the New York Times during presidential campaigns, we also

compared the coverage of downsizing events before German elections with no-campaign

periods and find no systematic differences (as shown in Table E in Web Appendix II).8

Our analysis is mainly based on a data set of reports from Die Welt, raising the question

of whether these results are specific to one newspaper. Although Die Welt is owned by the Axel

5 The slant is also unrelated to the impact of newspaper technology on the timing of the news, as in

Soltes (2009), and to the size of standard articles in different newspaper sections, as shown in Web

Appendix I. 6 We have so far used the term “slant” rather than “bias”, as the literature tends to associate bias with

behavior that is not in line with profit maximization (Gentzkow and Shapiro, 2010). Here, we prefer

using the word “bias”, as it describes individual behavior that is not necessarily in line with profit

maximization. 7 Baron (2006) argues that a newspaper may allow journalists to report in a biased way because this

makes it possible to retain the journalist and/or to cut wage costs. While we cannot exclude that all or

most journalists are biased against foreign owners, we have investigated whether the slant may be driven

by those journalists who are most actively writing on downsizing and have not found any supporting

evidence (see Tables C and D in Web Appendix II). 8 There is a noteworthy exception. The leader of the SPD, the German social democrats, conducted a

short campaign against what he called the “locusts”, foreign private equity investors. We do find a slight

increase in the slant during that period, but the slant is present across the entire period.

5

Springer Publishing House9 (a close ally of the business-friendly CDU party in government

since 2005), the readership of Die Welt is conservative, and conservatism may trigger some bias

against foreign owners. We therefore set up a third data set including five randomly drawn

months of reports from the six other leading national newspapers. We find that all newspapers

slant their reports in the same direction, with some indications of an increasing slant when

moving from right to left along the political spectrum.10 These results are consistent with the

presence of a general bias among the readership of all newspapers. Because the newspapers we

look at have a relatively well-educated readership compared to the main tabloids or the regional

newspapers (Jandura and Brosius, 2011), we would expect the slant in other media to be even

stronger.

We contribute to a growing empirical literature on media economics, which includes

studies about the ideological position of media (e.g. Ansolabehere et al., 2006; Durante and

Knight, 2012; Gentzkow and Shapiro, 2010; Groseclose and Milyo, 2005; Larcinese et al.,

2011; Puglisi and Snyder, 2011, forthcoming), and the impact of the media on voting turnout

(e.g. Gentzkow et al., 2011; Oberholzer-Gee and Waldfogel, 2009) and electoral outcomes (e.g.

Chiang and Knight, 2013; DellaVigna and Kaplan, 2007; Enikolopov et al., 2011). Other studies

analyze the impact of media on political outcomes (e.g. Besley and Burgess, 2002; Eisensee

9 The Springer family owned the majority of the publicly listed Axel Springer Publishing House

throughout the entire period. In the meanwhile the media entrepreneur Leo Kirch, the Deutsche Bank,

the private equity firm Hellman & Friedman hold larger minority stakes in the company. 10 Representative data about the political orientation of Die Welt’s or other nationally distributed

newspapers’ readership is not readily available. Jandura and Brosius (2011) provide some evidence for

the right-of-center orientation of Die Welt, and in Web Appendix I, we summarize the German political

science community’s perception about the newspapers’ orientation. Further support for these

perceptions is lent by a survey we carried out among students of Goethe University. A group of 102

participants in a lab experiment unrelated to the topic of this paper were asked about their political

orientation on a scale from 1 (left) to 10 (right). We also asked them how frequently they are reading

the national newspapers on a scale from 1 (never) to 10 (every day). Participants who are frequently

reading (with values of 8 or more) the Frankfurter Allgemeine Zeitung have an average political

orientation of 5.23 (s.d. 1.80; n = 39), Die Welt 4.93 (s.d. 1.68; n = 12), the Süddeutsche Zeitung 4.60

(s.d. 1.85; n = 20), the Frankfurter Rundschau 4.37 (s.d. 1.56; n = 30) and Die Tageszeitung 3.40 (s.d.

1.67; n = 5).

6

and Strömberg, 2007; Snyder and Strömberg, 2010; Strömberg, 2004) and household decisions

(e.g. Olken, 2009).

Our focus is on the functioning of media markets,11 and our results lend themselves to

the interpretation that the slant is demand-driven rather than the result of agenda-setting. The

empirical paper most closely related to ours is Gentzkow and Shapiro (2010) who find that

newspapers tailor their slant to the beliefs of their potential readers. We are also close to

Mullainathan and Shleifer (2005) who assume that newspapers receive an identical signal about

the truth, but can slant their stories by omitting some of the information. When readers have a

preference for news that is consistent with their initial beliefs, oligopolistic newspapers can

charge higher prices by differentiating themselves through slanted reports. Because we find

slant against foreign owners in all newspapers, and no slant in favor of foreign owners, it is

likely that the underlying beliefs of the population are biased in a homogeneous way (similar

to the beliefs about foreign policy, see Mullainathan and Shleifer, 2005). Gentzkow and Shapiro

(2006) generate slant in a theory in which consumers think that newspapers that share their

perspectives are more reliable. In their model, slant arises as a natural consequence of

newspapers’ desire to build a reputation for accuracy. Anderson and McLaren (2012) show that

similar mechanisms prevail when consumers are fully rational.

Our paper also contributes to a better understanding of the intricacies of corporate social

responsibility (CSR) and its significance for globally operating businesses. Kitzmueller and

Shimshack (2012) provide numerous examples of the scale and scope of CSR activities

including public statements, costly certifications and investments. Labor policies, in particular,

downsizing have great impact on a company's reputation (Karake, 1998), and media play a

particular role in channeling information that is CSR relevant (Couttenier and Hatte, 2013). Our

11 Related studies include Sweeting (2007, 2010) on product positioning in radio stations, George (2007)

on the effect of concentration on news variety, and Myers (2005) on racial diversity and discrimination

in competitive media markets.

7

paper adds to these insights by showing that the identity of a company (foreign vs. domestic) is

important for the differential impact of such activities on the company’s reputation. The

additional negative attention foreign firms attract in the media provides a concrete measure for

the concept of "liability of foreignness" in the management literature (Zaheer, 1995).

2. Case studies on media slant and FDI

To the extent that media slant may reinforce readers’ negative beliefs about foreign owners, it

may trigger or contribute to penalties imposed by consumers. Systematic evidence is hard to

generate due to a lack of data, but the following three cases are illustrative of what we have in

mind.

When the Finnish multinational Nokia announced the shutdown of its mobile-phone

plant in Bochum, Germany (a loss of 2,300 jobs) on January, 16th 2008, the decision attracted

overwhelmingly negative media attention. Nokia lost 8 percentage points in the German mobile

phone market in the subsequent six months, while in the rest of Europe, Nokia’s market share

remained constant. Meanwhile, Nokia’s global market share actually increased from 36 to 39

percentage points,12 suggesting that the loss in Germany cannot be explained by the entry of

new technologies like the iPhone. We estimate that Nokia lost 220 million Euro of sales after

the downsizing, based on the following back-of-the-envelope calculation. In 2007, Nokia sold

12 million mobile phones in Germany, representing a 44% market share. At an average price

of 110€ per mobile phone, a loss of 8 percentage points of market share (i.e. 2 million sales)

implies a fall in turnover of 220 million Euro in 2008.

TABLE 1 ABOUT HERE

12 Figures come from Gartner and GfK, market research institutes, and are documented in several

newspapers and magazines, e.g. New York Times (http://www.nytimes.com/2008/04/17/technology/17

iht-17nokia.12089585.html?_r=0).

8

As shown in Table 1, Nokia also suffered enormous reputational damage as documented

by the market research institute YouGov.13 Average quality ratings of Nokia mobile phones fell

from +50 two weeks before to +1 two weeks after the announcement (on a scale from +100 to

-100). The willingness to recommend Nokia products, and the perceived price-performance

ratio, also decreased. Nokia’s ratings recovered slightly in the following months, but nine

months after the announcement they had not reached half the pre-announcement level.14

The white-goods manufacturers Miele, Bosch Siemens HHG (both German) and

Swedish Electrolux provide a second illustrative case. In 2005, Miele announced the shedding

of 1,078 jobs in Germany, BSH 420, and Electrolux 1,750. Electrolux attracted four times more

articles as Miele and BSH. While Miele and BSH increased their joint market share in Germany

during 2006 by 5.2 percentage points, Electrolux lost 4 percentage points, moreover, its market

share was constant in the rest of Europe.15

A third case illustrates that consumer penalties may even differ across regions. Since

mid 2008, there has been an ongoing discussion about GM Opel’s plan to close its plant in

Bochum in 2014, attracting much interest and negative attention from the German media.

Between 2007 and 2012, Opel’s market share decreased by 41 percent (from 15.1 to 8.9

percentage points) in the Ruhr valley, while n the whole of Germany it “only” decreased by 26

percent (from 9.1 to 6.8 percentage points). The German BILD tabloid called the consumer

reaction a “message sent to the hard-hearted GM-management in Detroit”.16

3. Data

13 These data are not publicly available, but can be provided by the authors upon request. 14 In comparison, BMW shed 7,500 jobs at the same time, mainly in Leipzig, Eastern Germany, a much

larger job loss of an equally well-known brand, in a region plagued by a higher unemployment rate.

BMW, controlled by a German block-holder, received little media attention, the YouGov ratings

remained constant and BMW gained in 2008 the largest market share in their history. 15 These figures also come from GfK and are documented in several newspapers and magazines, e.g.

Nürnberger Nachrichten (http://www.nordbayern.de/nuernberger-nachrichten/wirtschaft/electrolux-

machte-mehr-gewinn-1.761846). 16 http://www.uni-due.de/~hk0378/publikationen/2013/20130330_WAZ.pdf

9

3.1 Identifying articles about downsizing

There are no data on downsizing in Germany, because the Labor Agency does not distinguish

announcements from actual downsizing decisions. We identify downsizing through LexisNexis

including only articles for which both firm identity and the actual number of jobs shed are

known.17

Our algorithm is described in detail in Web Appendix I. We first identified a list of

German synonyms for downsizing, ensuring inter-coder reliability for the synonyms through

the paid assistance of twenty students from different fields. An additional step was inspired by

Eisensee and Strömberg (2007): after identifying all articles in the data base in which synonyms

for downsizing appeared, we searched all articles on the 498 firms mentioned in these articles,

thus investigating 40,000 articles. All told, we found 5,394 articles on downsizing, with a total

of 42418 companies and 651 downsizing cases. Finally, another 24 students received packages

of articles either related or unrelated to downsizing. Their classifications were highly congruent

with ours.

We then counted the words in the paragraphs in which at least one synonym for

downsizing appeared. Sometimes, all paragraphs in an article are on downsizing, but there are

also articles in which the bulk of paragraphs refer to e.g. a new strategy or the CEO, and

downsizing only appears as a minor issue. The descriptive statistics show that the proportion of

an article, which is devoted to downsizing, constitutes an important distinction between the

reports on domestic versus foreign firms (see Section 3.2.2).

We only recorded articles on foreign firms’ downsizing when we could verify that

German locations were indeed affected by the downsizing of the company. In most downsizing

events, the total number of jobs shed are mentioned in Die Welt’s articles. For consistency, we

17 In Web Appendix III, we provide examples of articles that did and did not qualify to be included in

our data base. 18 For an additional 74 firms, we found reports of rumors, or announcements of downsizing, but no

information regarding the number of jobs shed. These cases were not entered into the data set.

10

cross-checked other quality media, agency reports like Reuters and DPA, and information from

the company itself including annual reports and press releases. If there remained doubt about

the total number of jobs shed, we omitted the entire downsizing case. In our data set, one

observation is one downsizing event (or “case”) involving one firm.

3.2 Descriptive statistics

3.2.1 Firms, and downsizing events

Our classification of domestic versus foreign firms is based on the prescriptions of German law

that gives shareholders with 25% or more of the equity special control rights. In 426 cases,

foreign blockholders hold less than 25% of the equity of the firms, in 209 cases between 45%

and 100%. The first group of firms is treated as domestic, the second as foreign. For the

remaining 16 downsizing cases, classifying firms was less clear-cut. Excluding those cases from

our regressions, our final data set contains 5,172 articles from 412 companies and 635

downsizing cases. In Web Appendix I, we provide more information about the classifications,

the firms that we excluded, and a number of robustness checks to ensure the reliability of our

results.

In Web Appendix II (Table K) we also provide a summary of the downsizing cases

broken down by two-digit industry classification and by ownership (domestic versus foreign).19

Except for seven out of 39 industries, the data set contains at least one domestic and one foreign

firm in each industry.

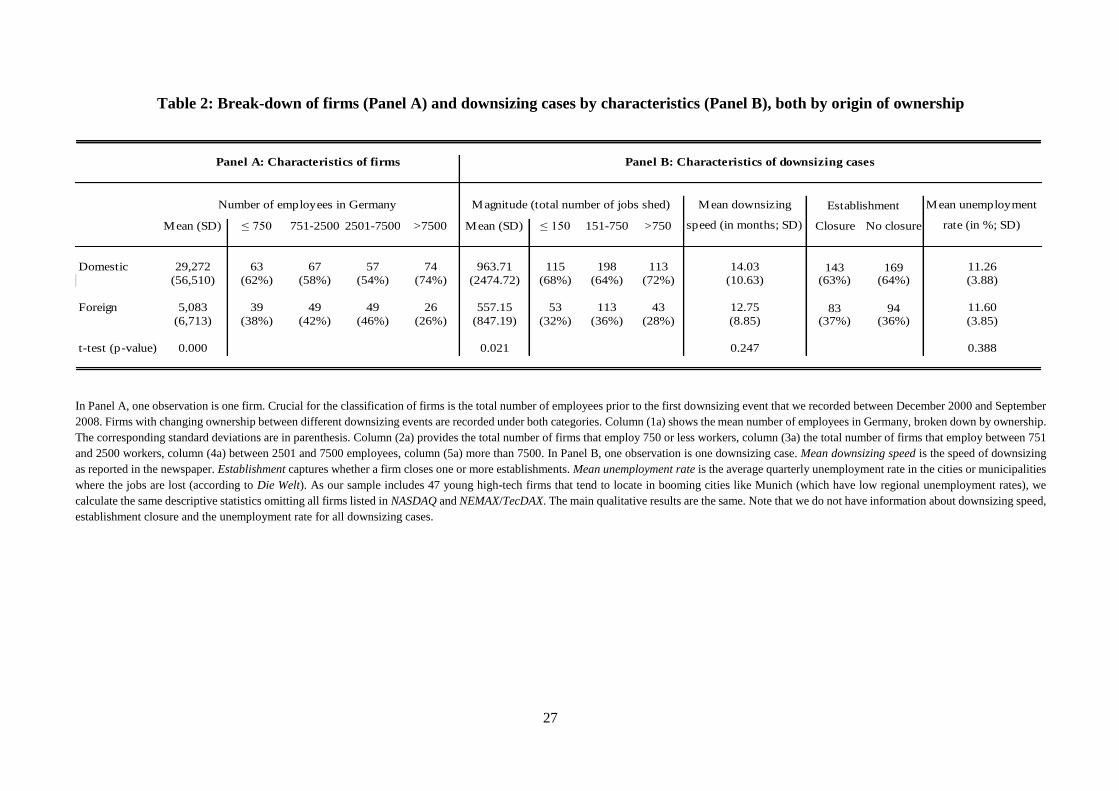

TABLES 2, 3 ABOUT HERE

Panel A of Table 2 provides an overview of the size of firms, measured by the number

of German employees before downsizing. Foreign firms are under-represented in the class of

19 Table L in Web Appendix II provides an overview using a one-digit industry classification. In all

regressions, we include sector dummies based on two-digit industry classifications. Using one-digit

industry dummies does not change the results (Web Appendix II, Table M).

11

very large firms. In all regressions, we control for size and industry, and we later use propensity

score techniques to control for self-selection into size, region and industry. Other covariates,

such as assets or employment costs per capita, might differ between domestic and foreign firms.

To control for those variables, we have matched a subset of large firms (80 domestic, 24

foreign) from our data set with financial and accounting information from the Amadeus data set

(Bureau van Dijk, 2011). Table 3 provides an overview of sales, assets, debt, employment costs

and profitability of domestic and foreign firms in 2001 (Panel B) and in the year before

downsizing (Panel C). Only for one variable (tangible fixed assets, in Panel B) do we find

statistically significant differences in a two-sided t-test, and controlling for it does not change

the main results (Section 5).

In Panel B of Table 2, we summarize several characteristics of the downsizing events:

the magnitude of downsizing, downsizing speed (in months), the number of cases with

establishment closures, and the quarterly local unemployment rate in the towns/districts where

the downsizing occurs. With the exception of fewer large downsizing events by foreign firms,

we do not find great differences between domestic and foreign firms’ downsizing events.20

3.2.2 Media slant: dependent variables

Our approach to measuring newspaper slant is similar to the method used by Eisensee and

Strömberg (2007), who compare the media coverage of natural disasters, depending on the

number of persons killed and the region in which it occurs. As dependent variables we use: (i)

the words per job lost (the total number of words about downsizing across all articles reporting

20 A concern could be that foreign and domestic multi-national enterprises (MNEs) may be downsizing

more or in different ways than domestic ones. The literature on FDI finds no evidence for this (see e.g.

Borrmann et al., 2003; Braconier and Ekholm, 2000; Buch and Lipponer, 2010; Konings and Murphy,

2006; Marin, 2004; Navaretti and Venables, 2004). A notable exception is Becker and Muendler (2010)

who document that German MNEs tend to adjust at the intensive margin at home, but at the extensive

margin abroad. Looking at the closure of establishments (the extensive margin), we find no descriptive

differences between foreign and domestic firms in our sample. In our regressions in Section 4.1 we find

no impact of closures on the media slant.

12

on a given downsizing case, divided by the number of jobs shed in this event); (ii) the number

of articles about downsizing for a given downsizing case, divided by the number of jobs shed

in this event, scaled down by 1/1,000.

TABLE 4 ABOUT HERE

Panel A in Table 4 compares the newspaper coverage per job shed of foreign versus

domestic firms’ downsizing. The coverage (in words per job shed) of foreign firms that

downsize is more than twice as large as that of domestic firms. Over 50% more downsizing

articles per job shed are written on foreign firms. Panel B compares the size of articles, and the

number of words devoted to downsizing (versus other news related to the firm). The size of the

typical article is the same for domestic and foreign firms (388.96 compared to 388.61 words),

but 19% more words are devoted to downsizing by foreign firms. Hence, media slant operates

through two channels: more articles are written on downsizing by foreign firms, and in each

article, more words are devoted to downsizing. The dependent variable words per job shed

incorporates both these channels, because it accounts for the total slant. Hence, we focus on the

total words written on a downsizing event, and report regressions with articles as the dependent

variable in the Web Appendix II. The coefficients are always positive, but not always

statistically significant.21

4. Empirical specification and basic results

4.1. Quantitative media slant against foreign firms

Our baseline OLS regression is as follows:

𝑦𝑖 = 𝛽0 + 𝛽1𝑓𝑜𝑟𝑒𝑖𝑔𝑛𝑖𝑡 + 𝛽2𝑋𝑖𝑡 + 𝜀𝑖,𝑡 (1)

21 An additional interesting observation relates to firms that change ownership from foreign to domestic

(or vice versa) and downsize under both owners. For the 13 such firms in our data set, the descriptive

statistics show that when owned by domestic owners, the newspaper prints 1.84 (s.d. 1.31) words per

job shed, and 15.41 (s.d. 13.10) articles per 1,000 jobs shed. If the same firm is owned by foreign

investors, media attention increases to 7.37 (s.d. 6.29), and 33.64 (s.d. 26.90) respectively.

13

with the dependent variable words per job shed. Ownership is captured by a foreign dummy

variable, and controls include industry and time22 dummies and employment. Standard errors

are robust, and clustering on the sector level does not change the results.

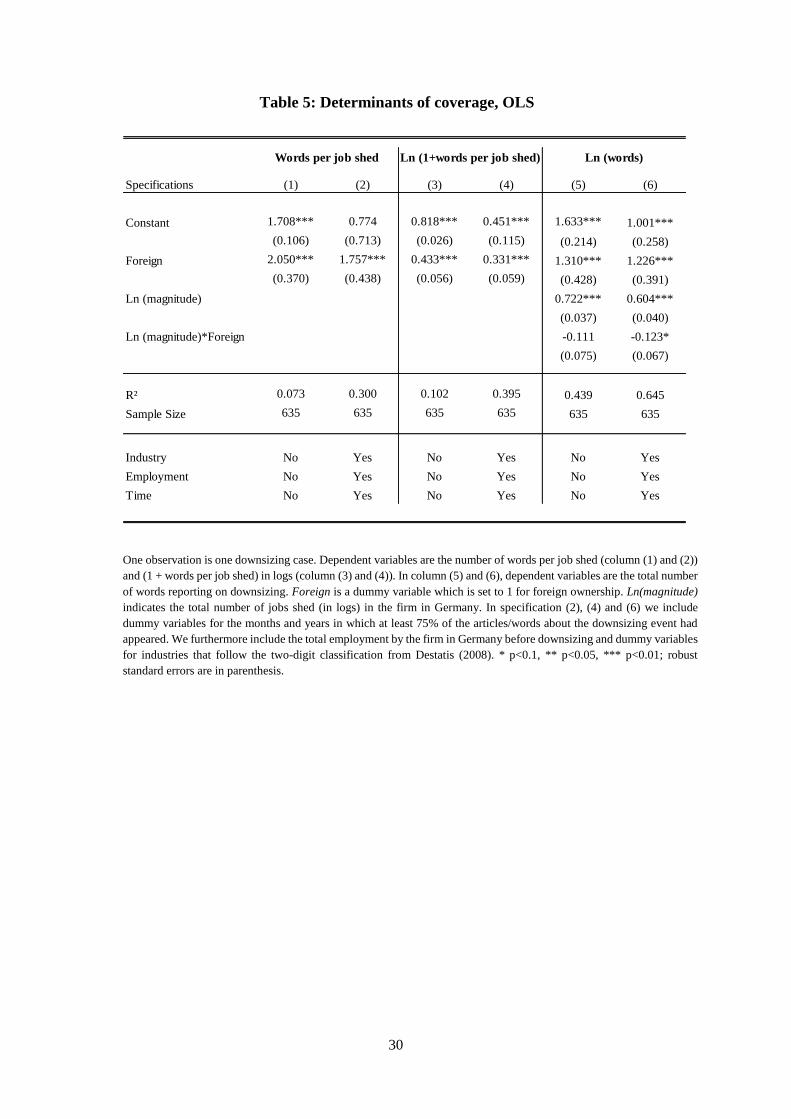

TABLE 5 ABOUT HERE

The first two specifications of Table 5 present the results with and without controls.

Media coverage of foreign firms is roughly two times higher. In specifications (3) and (4) we

use words per job shed (+1) in logs as dependent variable, finding a media slant against foreign

firms that is highly significant albeit of smaller size. Specifications (5) to (6) use the logs of the

raw numbers of words, and regress these in addition on the log of the magnitude of downsizing

to allow for non-linear effects, for instance, because there is a minimum size of an article. For

log of words, the size is similar to the ones in the baseline regressions. The coefficient of the

interaction term between foreign and magnitude indicates that the slant is larger for firms that

shed fewer jobs. Notice that specification (6) should be taken with a grain of salt because of the

multicollinearity of employment and magnitude of downsizing.23

TABLE 6 ABOUT HERE

Table 6 presents the results of an augmented regression that takes into account additional

characteristics of the downsizing event. We now include the magnitude of the downsizing, the

magnitude relative to firm size, whether or not there was an establishment closure, regional

22 There are several ways to control for seasonal differences in reporting and time trends, because

different articles on a downsizing event appear at different points of time. In most cases, the temporal

structure of news reports is as follows. First, one or a few articles refer to rumors and advance notices,

followed by an official announcement and background reports some days later. A final article or series

of articles appears when downsizing is completed, usually some months later. The bulk of articles on a

downsizing case appear in a short window of time: in 450 of the downsizing cases at least 75% of the

articles and words about downsizing appear in one month; in 120 cases in two, in 43 cases in three

months, and in 38 in four or more months. In the baseline regression, we include monthly and yearly

time dummies. The dummies are set to one for the months (years) during which at least 75% of the

words and articles have appeared, and zero otherwise. Other specifications (e.g. dummies set to one for

the month/year where the first article appears) do not affect the results in a qualitative way (see Table

N, Web Appendix II). 23 In Figure A in Web Appendix II we also present a scatterplot of words and the number of jobs lost

within domestic and foreign firms which shows that the functional forms looks quite linear.

14

unemployment, and, in a second specification, the speed of downsizing.24 The log of magnitude

is the only statistically significant variable, indicating that smaller downsizing events receive

relatively more attention. The foreign dummy remains stable. 25

Unemployment in the regional market does not seem to matter for media reports, which

is surprising as local labor markets have quite different degrees of unemployment that develop

differently over time. Also, German workers are relatively immobile compared to U.S. workers

(David et al., 2010). Hence, one should expect media attention for downsizing to depend on the

local unemployment rate.26

TABLE 7, FIGURE 1 ABOUT HERE

To look further into this issue, we split the sample of firms by quintiles of the

unemployment rate, see Table 7. We find that domestic and foreign firms are distributed

similarly across quintiles. This suggests that there is no self-selection of foreign or domestic

firms in regions plagued by high unemployment rates. Figure 1 offers an interesting

observation: while there is no pattern regarding the correlation of unemployment quintile and

media coverage per job shed for domestic firms, for foreign firms, when moving from the first

to the fifth quintile, media coverage per job shed increases from 3.07 to 4.63. Thus, there is a

higher media concern for unemployment when a foreign firm is the downsizing one.

To deal with potential problems of self-selection of foreign owners we use propensity

score methods (Becker and Ichino, 2002; Rosenbaum and Rubin, 1983).27 Foreign owners may

systematically select firms that are different from domestic ones; for instance, they may sort

24 We also run propensity score estimations using the same characteristics of the downsizing events as

covariates as in the OLS regression. The estimated coefficients of the average treatment on the treated

are similar to our OLS baseline regressions. Results are provided in Web Appendix II, Table P. 25 We also run our baseline regression including a dummy for firms which, according to the newspaper

reports, had received subsidies. However we only had 18 such cases and the results did not change much.

The inclusion of an interaction term between foreign and subsidies did not affect the results. 26 For example, Jacobson et al. (1993) have shown that workers’ costs of losing their jobs are higher

when the local unemployment rate is high, which would provide a rationale for the media to report more

about this. 27 Here we use the Nearest-Neighbor method as our matching procedure. The main results are the same

when using a Kernel method.

15

into different industries or different regions. If these characteristics attract more interest from

the media in general, they also do so when firms downsize, and our estimates would be biased.

Results of the propensity score regressions are shown in Web Appendix II, Table R. The

estimated coefficients of the average treatment on the treated are similar to our OLS baseline

regression.28 Given our controls, we find no evidence that foreign firms in our sample have

characteristics that systematically differ from domestic companies.

4.2. Qualitative media slant against foreign firms

To investigate whether Die Welt describes the downsizing of domestic and foreign firms in

different ways, one needs measures of qualitative aspects of reporting. While these are usually

hard to measure, we received access to data by Media Tenor, a Swiss media consulting

company.

FIGURE 2, 3 ABOUT HERE

Matching the data that Media Tenor recorded between August 2001 and September

2007 with our database, we have qualitative evaluations for 2,109 articles. Each article is

classified as positive (+1), neutral (0) or negative (-1).29 Figure 2 provides an overview of the

distribution of the articles, by ownership and evaluation. In total, the 1,346 articles reporting

about downsizing of domestic firms receive an average evaluation of -0.215 (s.d. 0.678).

However, the 763 downsizing articles reporting about foreign firms receive an average

28 Running estimations where we exclude all observations with a propensity score less than 0.1 or greater

than 0.9 (Table R, Panel B), as suggested by Crump et al. (2009), leads to similar results. 29 The company employs more than 120 employees who read several newspapers each day and record

all articles where first, the name of any company is mentioned, and second, five or more sentences report

about the company. The evaluation of each article is based on the following algorithm. First, the

adjectives used are recorded and whether these are positive or negative. Second, it is checked whether

the context of an article is consistent with the adjective-based evaluation. In case of contradiction, the

evaluation is based on the context. To make sure that all employees of Media Tenor evaluate the articles

in the same way, they receive three months of training. Once per month, Media Tenor’s management

randomly selects some articles and checks whether they have been coded in the right way. Employees’

wages are based on the result of this check.

16

evaluation of -0.307 (s.d. 0.644). This difference (roughly 50%) is significant according to a t-

test (two-sided, p-value: 0.001), and of a similar magnitude as the quantitative effects.

To ensure that we are capturing a slant against foreign firms that downsize, and not one

against foreign firms in general, we collected all articles on the 424 foreign and domestic firms

that downsized in our data set. Then, we checked Media Tenor’s qualitative evaluations of those

articles on the firms, which are not related to downsizing. In total there are 34,554 articles

reporting about our domestic firms and 10,351 articles about our foreign firms. Articles about

domestic firms receive an average evaluation of 0.012 (s.d. 0.572), foreign firms of 0.015 (s.d.

0.590). As indicated in Figure 3 this difference is not significant (two-sided t-test, p-value:

0.667). An interesting additional fact is that domestic firms receive more media attention in

general (by a factor of three). This makes our result that Die Welt publishes more articles about

foreign firms’ downsizing even more striking.30

We have identified an additional fact in line with our story on slant against foreign firms

that downsize. We examined all reports in LexisNexis on job creation, or “upsizing”,

distinguishing foreign versus domestic firms. Using a similar algorithm to that for downsizing,

we ended up with 451 articles about 76 companies and 100 upsizing events.31 A share of 67%

of the upsizing cases report on domestic firms. Comparing the number of words in the

paragraphs in which at least one synonym for upsizing appeared, we find no statistically

significant difference in reporting on foreign versus domestic firms (134.66 to 125.27, with a

two-sided t-test, p-value: 0.428). The average number of articles per upsizing case is higher for

domestic compared to foreign firms (5.34 to 2.85), but the difference is not significant (two

30 Using LexisNexis, we also counted all articles that mention the three leading domestic firms in each

sector in other contexts, such as strategy, new products, new management etc. We compared their media

coverage with that of the three leading foreign-owned competitors, for instance, Siemens versus Alstom,

VW versus Ford and found that 2.7 times more articles were written on the three largest German firms

in each sector than on their foreign counterparts (see Web Appendix II, Table T). 31 The upsizing company with the lowest share of a foreign block-holder is N3 Engine Overhaul

Services, a joint venture owned 50:50 by the German Lufthansa and the British Rolls-Royce.

17

sided t-test, p-value: 0.445). The number of words per new job created (1.29 to 1.49, two sided

t-test, p-value: 0.656) and articles per 1,000 new jobs created (10.82 to 10.43, two sided t-test,

p-value: 0.916) is roughly the same.32

5. Robustness checks

In this section, we primarily address potential omitted-variable biases. All regression tables for

this section are provided in Web Appendix II (Tables V-Z).

First, we classify foreign and domestic companies into five categories: publicly listed,

privately owned, private-equity, government owned and multiple/other owners. Interacting

these classifications with domestic and foreign ownership, we find that the respective

coefficients for most of the foreign, but for none of the domestic interaction terms are

significant. Hence, certain ownership forms receive more attention when the owner is foreign.

It is also possible that the slant is against owners from specific countries. For instance,

Anglo-Saxon countries are perceived to represent a “free market economy” which may have

negative connotations, compared to the “social” (or Rhineland) market economies of Germany

or France. Due to small sample sizes, we cannot control for each country separately. Rather, we

use the following regional variables: Continental Europe, U.K./Ireland, North America, Japan,

Others. The estimated coefficients in this regression are all positive, significant, and of similar

magnitude.

We also conduct a number of regressions where we include controls like sales, assets,

debt, employment costs and profitability for a subset of larger firms. The data are financial and

accounting data from the Amadeus data set (Bureau van Dijk, 2011). The foreign coefficient is

32 In OLS regressions similar to the ones used for downsizing, with the dependent variables words per

job created, and articles per 1,000 jobs created, the foreign dummy is far from significant in any

specification we tried (Web Appendix II, Table U).

18

in most specifications statistically significant, but smaller than in the baseline regressions for

large firms and, as discussed before, larger for smaller firms.

Foreign firms may tend to shed jobs for reasons that differ from those of domestic firms.

We augment our baseline model with the reasons given for downsizing in the media and press

releases of the company. The list includes state intervention, offshoring, insolvency, M&A,

other reasons, and multiple reasons. The regressions show a similar effect of foreign as before.

The coefficient on state intervention is positive and significant; none of the other variables are

statistically significant. Distinguishing M&A with acquiring firms that are headquartered in

Germany from the ones headquartered in foreign countries shows another interesting pattern.

M&A domestic is insignificant in the regression, but M&A foreign is positive and significant,

i.e. downsizing related to mergers and acquisitions attracts more media attention if the acquiring

firms are foreign owned.33

Foreign firms might not communicate their downsizing programs in the same way as

German firms do, in particular, they may use PR differently. To investigate this point, one can

compare domestic and foreign SMEs only, because SMEs tend not to invest a lot in PR, as

shown by Solomon (2012). Running our baseline regressions on firms employing 500 or less

workers in Germany we find that the foreign coefficient is positive, significant and substantially

larger than in the baseline regression with the full sample. If anything, foreign firms seem to

use PR to dampen media interest.

6. Channels of the slant

6.1 News process, perception

An event becomes news through the following stages: a firm’s downsizing action or press

release is received by the Deutsche Presse Agentur (DPA), the largest press agency in Germany,

33 Examples include the heated public discussions in Germany when British Vodafone Airtouch acquired

German Mannesmann in 2001, or when Spanish ACS acquired German Hochtief in 2011.

19

which then circulates the news to all journals. Thus, as argued by Gentzkow and Shapiro (2006)

and Mullainathan and Shleifer (2005), all newspapers observe the same signal delivered by

DPA, and then decide whether, how and how much to report. We checked for a subsample

DPA’s reports on 50 downsizing cases (sorted in descending alphabetical order) in our data set.

The agency writes 2.71 (s.d. 2.56) words per job shed when the firm is owned by a German

blockholder, and 1.95 (s.d. 2.40) for foreign-owned firms. DPA actually reports less on

downsizing by foreign firms, which makes the slant more significant.34

6.2 Advertiser influence

Ellman and Germano (2009), Gambaro and Puglisi (2010) and Reuter and Zitzewitz (2006)

argue that advertisers’ influence can cause slant. Domestic firms in our dataset could be placing

more advertising than foreign ones. As a result, domestic firms could put pressure on editors or

journalists to provide favorable coverage (e.g. write less about downsizing activities).35

However, as already shown, the media slant against foreign firms is even larger for SMEs.

Because neither domestic nor foreign SMEs invest a lot in advertising in main national

newspapers, this fact is not in line with a story that advertisers are the primary force explaining

the slant. As a second analysis, we randomly chose five months (November 2002, July 2005,

September 2006, May 2007, May 2008), and recorded all firms that placed advertisements in

Die Welt in this period (290 advertisers). During those five months, a total of 147 downsizing

cases are in our data set, with a total of 133 firms downsizing. 42 out of those firms were

advertisers in Die Welt. As shown in Table AB in Web Appendix II, neither the inclusion of a

34 To exclude the possibility that journalists write more about downsizing in Hamburg and Berlin

(headquarters of Die Welt and the Axel Springer Publishing House), as a large portion of them (and large

parts of the readership) might live there, we run our baseline including a dummy for jobs shed in the

two towns. As shown in Table AA in Web Appendix II, the main qualitative results are the same. 35 This is an argument similar to political economy explanations of media bias, where journalists report

favorably about certain policies, because they need to maintain a good relationship to politicians who

provide them with privileged material.

20

dummy capturing whether a downsizing firm is placing advertising nor an interaction term

between Advertiser and foreign/domestic affects the results.

6.3 Differentiation: Evidence from six other newspapers

A number of theoretical papers, in particular, Mullainathan and Shleifer (2005), and Anderson

and McLaren (2012) have argued that newspapers are catering to the beliefs of their readership,

and Gentzkow and Shapiro (2010) have presented empirical evidence. But, why would a

business-friendly newspaper like Die Welt slant reports about foreign owners? There are two

possible interpretations. One is that a conservative business-friendly readership may be

xenophobic for reasons beyond a simple economic cost-benefit appraisal. Another

interpretation is that in terms of beliefs about foreign owners everyone may be biased, and thus,

newspapers with otherwise quite different readerships may report in similar ways.

We look at six newspapers with a total of 1.56 million copies sold in 2008 who together

with Die Welt represent 90% of the national quality newspaper market in Germany:

Handelsblatt and Financial Times Deutschland (FTD), the Frankfurter Allgemeine Zeitung

(FAZ), Süddeutsche Zeitung (SZ), Frankfurter Rundschau (FR) and Die Tageszeitung (TAZ).

TABLE 8 ABOUT HERE

To investigate whether the slant found in Die Welt is idiosyncratic or may be a general

phenomenon of these quality newspapers in Germany, we randomly chose five months36 from

our period of observation and carried out the same algorithm as the one used for the initial data

set, allowing us to measure whether the average number of words on foreign versus domestic

firms shows patterns across newspapers.37 The descriptive results (see Panel B of Table 8) show

36 November 2002, July 2005, September 2006, May 2007, May 2008. 37 We cannot investigate whether during those five months, the newspapers published more articles,

because the five months are disjunct, and the publishing sequence of articles may differ between

newspapers.

21

that all newspapers slant their news in the same direction.38 This observation is in line with

Mullainathan and Shleifer (2005) who argue that people have heterogeneous beliefs on some

and homogeneous beliefs on other topics. They argue that foreign policy is a good example of

the latter. Our data indicate that negative beliefs about foreign owners’ impact on employment

may be similarly homogeneous in the population.

The magnitude of the slant, however, is quite different. Business newspaper FTD spends

on average 1.07, and Handelsblatt 1.15 times, more words per article on foreign firms’

downsizing. The ratio of Die Welt is 1.15, consistent with the initial dataset. FAZ is considered

a right-of-center newspaper, and has a ratio of 1.17. SZ and FR, generally seen as left-of-center,

have ratios of 1.24 and 1.25, respectively. TAZ with its distinct left-wing orientation has the

strongest slant with a ratio of 1.27.

6.4 Owner influence

There is another possible explanation for the slant: newspaper owners could be biased (as

studied by Gentzkow and Shapiro (2010), who find no evidence, while Larcinese et al., (2011),

do). The newspapers we look at have different types of owners: foundations, cooperatives and

families. We can also use the fact that three newspapers changed their owners in our period of

observation, all because of severe financial difficulties. The FR was majority-owned by a

foundation until 05/2004 (Karl-Gerold-Stiftung), by the social-democratic party SPD until

07/2006, and afterwards by the DuMont Schauberg family. The SZ was owned by several

families, and in 03/2008 acquired by the entrepreneur Dieter Straub and several other families.

FTD initially was a 50-50 joint venture of Bertelsmann and the U.K. based Pearson Group; but

in January 2008 Bertelsmann acquired Pearson’s 50% share. We expand our dataset from the

previous section by randomly chosen months until we have at least three months of observations

38 The nature of this (third) data set does not lend itself to statistic tests or regressions and should hence

be taken with a grain of salt.

22

for each owner of each newspaper. Table AC in Web Appendix II shows that owner changes

have no substantial impact on any newspaper’s slant.

7. Concluding remarks

We have established a robust fact about media reports on downsizing by foreign owners. In

Germany, for any job shed, a foreign firm receives twice as much media attention when it

downsizes than a domestic one. Germany is a leading export country with a population inclined

to globalization, and the effect is both robust against the inclusion of relevant controls, and

against potential self-selection of foreign owners into regions or industries that could attract

negative attention. The slant is present in all national quality newspapers, indicating that there

may be homogenous, and biased beliefs in the respective readerships.

The media play an important role in transmitting news to people, and this news and the

information it contains shapes economic decisions. The slant we identify, may have severe

economic consequences and cause substantial obstacles to FDI. To the extent that a potentially

negative a-priori belief of the population about the costs of globalization is strengthened by the

media, foreign companies may fear punishment for activities that domestic firms would barely

be noticed for.

23

References

Anderson, Simon P. and John McLaren (2012), “Media Mergers and Media Bias with

Rational Consumers”, Journal of European Economic Association, Vol. 10, No. 4, pp. 831-

859.

Ansolabehere, Stephen, Rebecca Lessem and James M. Snyder, Jr. (2006), “The

Orientation of Newspaper Endorsement in U.S. Elections”, Quarterly Journal of Political

Science, Vol. 1, No.3, pp. 393-404.

Baron, David P. (2006), “Persistent Media Bias”, Journal of Public Economics, Vol. 90, No.

1-2, pp.1-36.

Becker, Sascha and Andrea Ichino (2002), “Estimation of Average Treatment Effects Based

on Propensity Score”, The Stata Journal, Vol. 2, No. 4, pp. 358-377.

Becker, Sascha and Marc-Andreas Muendler (2010), “Margins of Multinational Labor

Substitution”, American Economic Review, Vol. 100, No. 5, pp. 1999-2030.

Besley, Timothy and Robin S. L. Burgess (2002), “The Political Economy of Government

Responsiveness: Theory and Evidence from India”, Quarterly Journal of Economics, Vol. 117,

No. 4, pp. 1415-1451.

Besley, Timothy and Andrea Prat (2006), “Handcuffs of the Grabbing Hand? Media Capture

and Government Accountability”, American Economic Review, Vol. 96, No. 3, pp. 720-736.

Borrmann, Christine, Rolf Jungnickel and Dietmar Keller (2003), Auslandskontrollierte

Unternehmen – ein Gewinn für den nationalen Arbeitsmarkt?, Baden-Baden: Nomos Verlag.

Braconier, Henrik and Karolina Ekholm (2000), “Swedish Multinationals and Competition

from High- and Low-Wage Locations”, Review of International Economics, Vol. 8, No. 3, pp.

448-461.

Buch, Claudia M. and Alexander Lipponer (2010), “Volatile Multinationals? Evidence from

the Labor Demand of German Firms”, Labor Economics, Vol. 17, No. 2, pp. 345-353.

Bureau van Dijk (2011), “Amadeus. A Database of Comparable Financial Information for

Public and Private Companies across Europe”, Database.

Chiang, Chun-Fang and Brian Knight (2011), “Media Bias and Influence: Evidence from

Newspaper Endorsements”, Review of Economic Studies, Vol. 78, No. 3, pp. 795-820.

Couttenier, Mathieu and Sophie Hatte (2013), “Mass media effects on the production of

information: Evidence from Non-Governmental Organization (NGO) Reports”, Working

Paper.

Crump, Richard K., Joseph Hotz, Guido Imbens and Oscar A. Mitnik (2009), “Dealing

with limited overlap in estimation of average treatment effects”, Biometrika, Vol. 96, No.1, pp.

187-199.

David, Quentin, Alexandre Janiak and Etienne Wasmer (2010), “Local social capital and

geographical mobility”, Journal of Urban Economics, Vol. 68, No. 2, pp. 191-204.

DellaVigna, Stefano and Ethan Kaplan (2007), “The Fox News Effect: Media Bias and

Voting”, Quarterly Journal of Economics, Vol. 122, No. 3, pp. 1187-1234.

Durante, Ruben and Brian Knight (2012), “Partisan Control, Media Bias, and Viewer

Responses: Evidence from Berlusconi’s Italy”, Journal of European Economic Association,

Vol. 10, No. 3, pp. 451-481.

Eisensee, Thomas and David Strömberg (2007), “News Droughts, News Floods, and U.S.

Disaster Relief”, Quarterly Journal of Economics, Vol. 122, No. 2, pp. 693-728.

24

Ellman, Matthew and Fabrizio Germano (2009), “What Do the Papers Sell? A Model of

Advertising and Media Bias”, Economic Journal, Vol. 119, No. 537, pp. 680-704.

Enikolopov, Ruben, Maria Petrova and Ekaterina V. Zhuravskaya (2011), “Media and

Political Persuasion: Evidence from Russia”, American Economic Review, Vol. 101, No. 7, pp.

3253-3285.

Gambaro, Marco and Riccardo Puglisi (2010), “What do ads buy? Daily Coverage of Listed

Companies on the Italian Press”, Working paper.

Gentzkow, Matthew and Jesse M. Shapiro (2006), “Media Bias and Reputation”, Journal of

Political Economy, Vol. 114, No. 2, pp. 280-316.

Gentzkow, Matthew and Jesse M. Shapiro (2010), “What Drives Media Slant? Evidence

from U.S. Daily Newspaper”, Econometrica, Vol. 78, No. 1, pp. 35-71.

Gentzkow, Matthew, Jesse M. Shapiro and Michael Sinkinson (2011), “The Effect of

Newspaper Entry and Exit on Electoral Politics”, American Economic Review, Vol. 101, No. 7,

pp. 2980-3018.

George, Lisa (2007), “What’s fit to print: The effect of ownership concentration on product

variety in daily newspaper markets”, Information Economics and Policy, Vol. 19, No. 3-4, pp.

285-303.

Groseclose, Timonthy and Jeffrey Milyo (2005), “A Measure of Media Bias”, Quarterly

Journal of Economics, Vol. 120, No. 4, pp. 1191-1237.

Jandura, Olaf and Hans-Bernd Brosius (2011), “Wer liest sie (noch)? Das Publikum der

Qualitätszeitungen“, in Blum, Roger, Heinz Bonfadelli, Kurt Imhof and Otfried Jarren: Krise

der Leuchttürme öffentlicher Kommunikation, Wiesbaden: VS Verlag.

Jacobson, Louis S., Robert J. LaLonde and Daniel G. Sullivan (1993), “Earnings Losses of

Displaced Workers”, American Economic Review, Vol. 83, No. 4, pp. 685-709.

Karake, Zeina A. (1998), “An examination of the impact of organizational downsizing and

discrimination activities on corporate social responsibility as measured by a company’s

reputation index”, Management Decision, Vol. 36, No. 3, pp. 206-216.

Kitzmueller, Markus and Jay Shimshack (2012), “Economic perspective on corporate social

responsibility”, Journal of Economic Literature, Vol. 50, No. 1, pp. 51-84.

Konings, Jozef and Alan Patrick Murphy (2006), “Do Multinational Enterprises Relocate

Employment to Low-Wage Regions? Evidence from European Multinationals”, Review of

World Economics, Vol. 142, No. 2, pp. 267-286.

Larcinese, Valentino, Riccardo Puglisi and James M. Snyder, Jr. (2011), “Partisan Bias in

Economic News: Evidence on the Agenda-Setting Behavior of U.S. Newspapers”, Journal of

Public Economics, Vol. 95, No. 9-10, pp. 1178-1189.

Marin, Dalia (2004), “’A Nation of Poets and Thinkers’ – Less so with Eastern Enlargement?

Austria and Germany”, CEPR Discussion Paper 4358.

Mayda, Anna-Maria and Dani Rodrik (2005), “Why are some people (and countries) more

protectionist than others?”, European Economic Review, Vol. 49, No. 6, pp. 1393-1430.

Mullainathan, Sendhil and Andrei Shleifer (2005), “The Market for News”, American

Economic Review, Vol. 95, No. 4, pp. 1031-1053.

Myers, Caitlin Knowles (2005), “Discrimination as a Competitive Device: The Case of Local

Television News”, IZA Discussion Paper No. 1802.

25

Navaretti, Giorgio Barba and Anthony J. Venables (2004), Multinational Firms in the World

Economy, Princeton and Oxford: Princeton University Press.

Oberholzer-Gee, Felix and Joel Waldfogel (2009), “Media Markets and Localism: Does

Local News en Espanol Boots Hispanic Voter Turnout?”, American Economic Review, Vol. 99,

No. 5, pp. 2120-2128.

OECD (2003), VII. Foreign Direct Investment Restrictions in OECD Countries, Paris

Olken, Benjamin A. (2009), “Do Television and Radio Destroy Social Capital? Evidence from

Indonesian Villages”, American Economic Journal: Applied Economics, Vol. 1, No. 4, 2009,

1-33.

Puglisi, Riccardo (2011), “Being The New York Times: the Political Behaviour of a

Newspaper”, The B.E. Journal of Economic Analysis & Policy, Vol. 11, No. 1, pp. 1-20.

Puglisi, Riccardo and James M. Snyder, Jr. (2011), “Newspaper Coverage of Political

Scandals”, Journal of Politics, Vol. 73, No. 3, pp. 1-20.

Puglisi, Riccardo and James M. Snyder, Jr. (forthcoming), “The Balanced U.S. Press”,

forthcoming, Journal of the European Economic Association.

Reuter, Jonathan and Eric Zitzewitz (2006), “Do Ads Influence Editors? Advertising and

Bias in the Financial Media”, Quarterly Journal of Economics, Vol. 121, No. 1, pp. 197-227.

Rosenbaum, Paul R. and Donald B. Rubin (1983), “The Central Role of Propensity Score in

Observational Studies for Causal Effects”, Biometrika, Vol. 70, No. 1, pp. 41-55.

Scheve, Kenneth F. and Matthew J. Slaughter (2006), “Public Opinion, International

Economic Integration, and the Welfare State”, pp.217-260 in Bardhan, Pranab, Samuel Bowles

and Michael Wallerstein (eds.), Globalization and Egalitarian Redistribution. New York:

Russell Sage Foundation.

Solomon, David (2012), “Selective Publicity and Stock Prices”, Journal of Finance, Vol. 67,

No. 2, pp. 599-638.

Soltes, Eugene (2009), “News Dissemination and the Impact of the Business Press.” Ph.D.

diss., The University of Chicago Graduate School of Business.

Snyder, James M. and David Strömberg (2010), “Press Coverage and Political

Accountability”, Journal of Political Economy, Vol. 118, No. 2, pp. 355-408.

Strömberg, David (2004), “Radio’s Impact on Public Spending”, Quarterly Journal of

Economics, Vol. 119, No. 1, pp. 189-221.

Sweeting, Andrew (2007), “Dynamic Product Repositioning in Differentiated Product

Markets: The Case of Format Switching in the Commercial Radio Industry”, NBER Working

Paper 13522.

Sweeting, Andrew (2010), “The effects of mergers on product positioning: evidence from the

music radio industry”, RAND Journal of Economics, Vol. 41, No. 2, pp. 372-397.

Zaheer, Srilata (1995), “Overcoming the Liability of Foreignness”, Academy of Management

Journal, Vol. 38, No. 2, pp. 341-363.

26

Appendix

Table 1: Average rating of Nokia products by consumers around the downsizing

announcement date

Quality of products +50 +1 +14 +19

Willingness to recommend products +42 -15 +4 +11

Perceived price-performance ratio +31 -6 +2 +9

September 2008January 03-15,

2008

January 16-28,

2008June 2008

27

Table 2: Break-down of firms (Panel A) and downsizing cases by characteristics (Panel B), both by origin of ownership

In Panel A, one observation is one firm. Crucial for the classification of firms is the total number of employees prior to the first downsizing event that we recorded between December 2000 and September

2008. Firms with changing ownership between different downsizing events are recorded under both categories. Column (1a) shows the mean number of employees in Germany, broken down by ownership.

The corresponding standard deviations are in parenthesis. Column (2a) provides the total number of firms that employ 750 or less workers, column (3a) the total number of firms that employ between 751

and 2500 workers, column (4a) between 2501 and 7500 employees, column (5a) more than 7500. In Panel B, one observation is one downsizing case. Mean downsizing speed is the speed of downsizing

as reported in the newspaper. Establishment captures whether a firm closes one or more establishments. Mean unemployment rate is the average quarterly unemployment rate in the cities or municipalities

where the jobs are lost (according to Die Welt). As our sample includes 47 young high-tech firms that tend to locate in booming cities like Munich (which have low regional unemployment rates), we

calculate the same descriptive statistics omitting all firms listed in NASDAQ and NEMAX/TecDAX. The main qualitative results are the same. Note that we do not have information about downsizing speed,

establishment closure and the unemployment rate for all downsizing cases.

Mean (SD) ≤ 750 751-2500 2501-7500 >7500 Mean (SD) ≤ 150 151-750 >750 Closure No closure

Domestic 29,272 63 67 57 74 963.71 115 198 113 143 169 11.26

(56,510) (62%) (58%) (54%) (74%) (2474.72) (68%) (64%) (72%) (63%) (64%) (3.88)

Foreign 5,083 39 49 49 26 557.15 53 113 43 83 94 11.60

(6,713) (38%) (42%) (46%) (26%) (847.19) (32%) (36%) (28%) (37%) (36%) (3.85)

t-test (p-value) 0.000 0.021 0.388

Establishment Number of employees in Germany Magnitude (total number of jobs shed)

Panel B: Characteristics of downsizing casesPanel A: Characteristics of firms

Mean unemployment

rate (in %; SD)

Mean downsizing

speed (in months; SD)

14.03

(10.63)

12.75

(8.85)

0.247

28

Table 3: Characteristics of the largest domestic and foreign downsizing firms

We selected the 500 largest German firms (based on turnover) and matched our data with firm-level financial and

accounting information from the Amadeus data set (Bureau van Dijk, 2011). Panel A provides an overview on the total

number of firms and downsizing cases, and the media coverage of those cases for our subset of firms, broken down by

ownership. Data are from 2001-2007. Panel B shows the mean sales, mean tangible fixed assets, mean long term debt,

mean total employment costs, mean employment costs per capita, mean return on equity, mean return on assets and

mean EBITDA margin of the firms in the year 2001. The corresponding standard deviations are in parenthesis. Panel

C provides the statistics for the year before the firm first sheds some jobs in our period of observation. Output and

capital variables are deflated using deflators obtained from EU-KLEMS database. Note that we lose some observations

in each row as we do not have the information for all downsizing firms. In column (5) we present the p-values of two-

sided t-tests.

t-test (p-values)

Total number of firms

Total number of downsizing cases

Words per job shed (mean, SD) 0.014

t-test

Obs. Mean (SD) Obs. Mean (SD) (p-values)

Employees 63 8,421 (25,418) 11 4,198 (9,456) 0.590

Ln (Sales) 60 20.37 (1.97) 17 20.18 (1.36) 0.707

Ln (Tangible fixed assets) 75 20.05 (2.03) 19 18.74 (2.06) 0.014

Ln (Intangible fixed assets) 64 15.19 (2.72) 18 14.94 (3.36) 0.738

Ln (Long term debt) 74 19.77 (1.93) 19 19.22 (1.66) 0.253

Ln (Total employment costs) 70 18.31 (1.91) 16 17.98 (1.56) 0.521

Ln (Employment costs per capita) 60 11.21 (0.971) 9 11.25 (0.51) 0.909

Return on equity 73 25.77 (7.50) 19 18.15 (6.05) 0.614

Return on assets 76 6.48 (9.73) 19 5.34 (9.14) 0.645

EBITDA margin 61 6.18 (3.21) 14 10.31 (10.85) 0.549

Employees 42 6,050 (23,726) 10 1,380 (2,157) 0.540

Ln (Sales) 39 19.75 (2.24) 9 20.10 (1.18) 0.661

Ln (Tangible fixed assets) 47 19.84 (1.91) 12 18.84 (1.99) 0.113

Ln (Intangible fixed assets) 43 15.26 (2.05) 11 15.00 (3.15) 0.742

Ln (Long term debt) 47 19.26 (2.00) 13 19.11 (2.32) 0.818

Ln (Total employment costs) 44 17.65 (1.98) 10 17.55 (1.36) 0.886

Ln (Employment costs per capita) 41 11.31 (0.69) 8 11.42 (0.57) 0.660

Return on equity 45 10.00 (24.52) 11 21.44 (51.25) 0.281

Return on assets 47 3.51 (11.24) 12 6.83 (10.94) 0.364

EBITDA margin 39 7.38 (26.10) 9 7.71 (9.77) 0.515

163

1.52 (1.90)

24

40

Panel A: Descriptive statistics for subsample of firms

Domestic Foreign

80

2.33 (1.67)

Panel B: Firm characteristics (year 2001)

Panel C: Firm characteristics (year before first downsizing)

Domestic Foreign

29

Table 4: Coverage per job shed (Panel A), mean number of words in the entire articles and the downsizing parts of the articles (Panel B), by

origin of ownership

Ownership Observations Ownership Observations

All cases 635 2.38 (3.58) All firms 5,172 388.83 (295.97) 148.45 (128.37)

Domestic 426 1.71 (2.19) Domestic 3,288 388.96 (287.87) 137.75 (114.48)

Foreign 209 3.76 (5.13) Foreign 1,884 388.61 (309.67) 167.12 (147.75)

Mean number of words in

the whole article

Mean number of words reporting on

downsizing per article

Panel A: Coverage per job shed

23.55 (28.14)

18.10 (22.23)

15.43 (18.11)

Mean number of words per

job shed

Mean number of articles per

1,000 jobs shed

Panel B: Coverage per article

In Panel A, one observation is one downsizing case. Column (2a) provides the mean number of words per job shed in all downsizing cases, broken down by origin of ownership, that is, we have summed

up all words in the downsizing parts of articles of a given downsizing case and divided the number of words by the number of jobs shed. Column (3a) is the mean number of articles per 1,000 jobs shed

in Germany in each downsizing case. The corresponding standard deviations are in parenthesis. In Panel B, one article about downsizing is one observation. Column (1b) is the number of observations,

broken down by ownership. Column (2b) is the mean number of words in the entire article, while column (3b) is the mean number of words reporting on downsizing per article, again broken down by

origin of ownership. The corresponding standard deviations are in parenthesis.

30

Table 5: Determinants of coverage, OLS

Specifications (1) (2) (3) (4) (5) (6)

Constant 1.708*** 0.774 0.818*** 0.451*** 1.633*** 1.001***

(0.106) (0.713) (0.026) (0.115) (0.214) (0.258)

Foreign 2.050*** 1.757*** 0.433*** 0.331*** 1.310*** 1.226***

(0.370) (0.438) (0.056) (0.059) (0.428) (0.391)

Ln (magnitude) 0.722*** 0.604***

(0.037) (0.040)

Ln (magnitude)*Foreign -0.111 -0.123*

(0.075) (0.067)

R² 0.073 0.300 0.102 0.395 0.439 0.645

Sample Size 635 635 635 635 635 635

Industry No Yes No Yes No Yes

Employment No Yes No Yes No Yes

Time No Yes No Yes No Yes

Ln (words)Words per job shed Ln (1+words per job shed)

One observation is one downsizing case. Dependent variables are the number of words per job shed (column (1) and (2))

and (1 + words per job shed) in logs (column (3) and (4)). In column (5) and (6), dependent variables are the total number

of words reporting on downsizing. Foreign is a dummy variable which is set to 1 for foreign ownership. Ln(magnitude)

indicates the total number of jobs shed (in logs) in the firm in Germany. In specification (2), (4) and (6) we include

dummy variables for the months and years in which at least 75% of the articles/words about the downsizing event had

appeared. We furthermore include the total employment by the firm in Germany before downsizing and dummy variables

for industries that follow the two-digit classification from Destatis (2008). * p<0.1, ** p<0.05, *** p<0.01; robust

standard errors are in parenthesis.

31

Table 6: Regression results, controlling

for characteristics of the downsizing

event, OLS

Relative magnitude indicates the number of jobs

shed divided by the total number of workers

employed by the firm in Germany before

downsizing. Establishment closure is a dummy set

to one if the firm closes an establishment,

Unemployment the average quarterly

unemployment rate in the cities/municipalities

where the jobs are lost. Downsizing speed is the

speed of downsizing as reported in the newspaper.

Note that we lose some observations as we do not

know whether an establishment gets closed, the

regions where the jobs are lost and the downsizing

speed for all downsizing cases. * p<0.1, ** p<0.05,

*** p<0.01; robust standard errors are in

parenthesis.

Specifications (1) (2)

Constant 5.760*** 7.782***

(1.377) (2.005)

Foreign 1.455*** 1.347**

(0.386) (0.564)

Ln(magnitude) -1.190*** -1.146***

(0.193) (0.265)

Relative magnitude -1.422 0.144

(0.928) (1.174)

Establishment closure 0.036 0.308

(0.455) (0.600)

Unemployment 0.036 -0.008

(0.455) (0.069)

Downsizing speed -0.026

(0.031)

R² 0.482 0.558

Sample Size 364 207

Industry Yes Yes

Time Yes Yes

Employment Yes Yes

Words per job shed

32

Table 7: Coverage per job shed, by quintiles of the mean unemployment rate

The table shows the mean number of words per job shed by quintiles of the mean local unemployment rate. Mean

local unemployment rate is the average quarterly unemployment rate in the cities or municipalities where the jobs

are getting lost (according to Die Welt). Standard deviations are in parenthesis. Note that we lose some

observations as we do not know the regions where the jobs are lost for all downsizing cases. As our sample

includes 47 young high-tech firms that tend to locate in booming cities like Munich (which have low regional

unemployment rates), we calculate the same descriptive statistics omitting all firms listed in NASDAQ and

NEMAX/TecDAX. The main qualitative results are the same.

33

54 29

51 32

2.29 (3.24) 3.07 (2.68)

2.08 (2.71) 3.31 (2.44)

1.31 (1.21) 3.53 (4.09)

Quintile

3.8 - 7.9%1

2 7.94 - 10.1%

Domestic Foreign Domestic

ObservationsMean local

unemployment

rate

Mean number of words per job shed

Foreign

3 10.1 - 11.7%

4 11.7 - 14.21% 46

50

37 1.34 (1.08) 4.22 (5.80)

4.63 (4.21)5 14.29 - 22% 51 32 2.18 (2.73)

33

Table 8: Downsizing reports in the seven leading national newspapers for five

randomly selected months, by origin of owner

Panel A reports the total number of articles reporting about downsizing in November 2002, July 2005, September 2006,

May 2007 and May 2008 for the TAZ, SZ, FAZ, Die Welt, Handelsblatt and FTD, broken down by ownership. Panel B

reports the mean number of words reporting on downsizing per articles for TAZ, SZ, FAZ, Die Welt, Handelsblatt and FTD.

Standard deviations are in parenthesis. Panel A and B also report the same data for FR, but only for July 2005, September

2006, May 2007 and May 2008 as the data for November 2002 were not available in LexisNexis.

Figure 1: Mean number of words per job shed

across unemployment rate quintiles, lowest (1) to

highest (5), by ownership

Taz FR SZ FAZ Die Welt Handelsblatt FTD

(left) (left-center) (left-center) (right-center) (right-center) (business) (business)

All firms 86 129 143 150 351 192 209

Domestic 63 84 100 112 246 128 138

Foreign 23 45 43 38 105 64 71

All firms 201.7 126.0 185.3 217.8 141.6 308.2 124.8

(217.3) (84.6) (145.7) (145.9) (105.7) (240.1) (88.8)

Domestic 188.2 116.0 172.7 208.6 135.5 293.8 121.7

(222.7) (75.4) (121.9) (138.6) (101.1) (250.2) (77.1)

Foreign 238.7 144.5 214.8 244.7 155.9 336.9 130.8

(201.9) (97.8) (188.2) (164.4) (155.2) (217.4) (108.3)

Panel B: Mean number of words in the downsizing part of the articles

Panel A: Total number of articles about downsizing

01

23

45

1 2 3 4 5 1 2 3 4 5

Domestic Foreign

Me

an

num

ber

of w

ord

s p

er

job s

he

d

Graphs by var6

34

Figure 2: Distribution of the articles about

downsizing, by ownership and evaluation

Figure 3: Distribution of the articles not related

to downsizing, by ownership and evaluation

0.1

.2.3

.4.5

-1 0 1 -1 0 1

Domestic ForeignD

en

sity

Evaluations (articles about downsizing)Graphs by Owner

0.2

.4.6

.8

-1 0 1 -1 0 1

Domestic Foreign

Den

sity

Evaluations (articles not related to downsizing)Graphs by Owner