media insights from clearwater international spring 2016...

TRANSCRIPT

clearthoughtMedia Insights from Clearwater International Spring 2016

TV ProductionFurther consolidation, more investment in minority stakes, and the sale of digital media assets are on the horizon

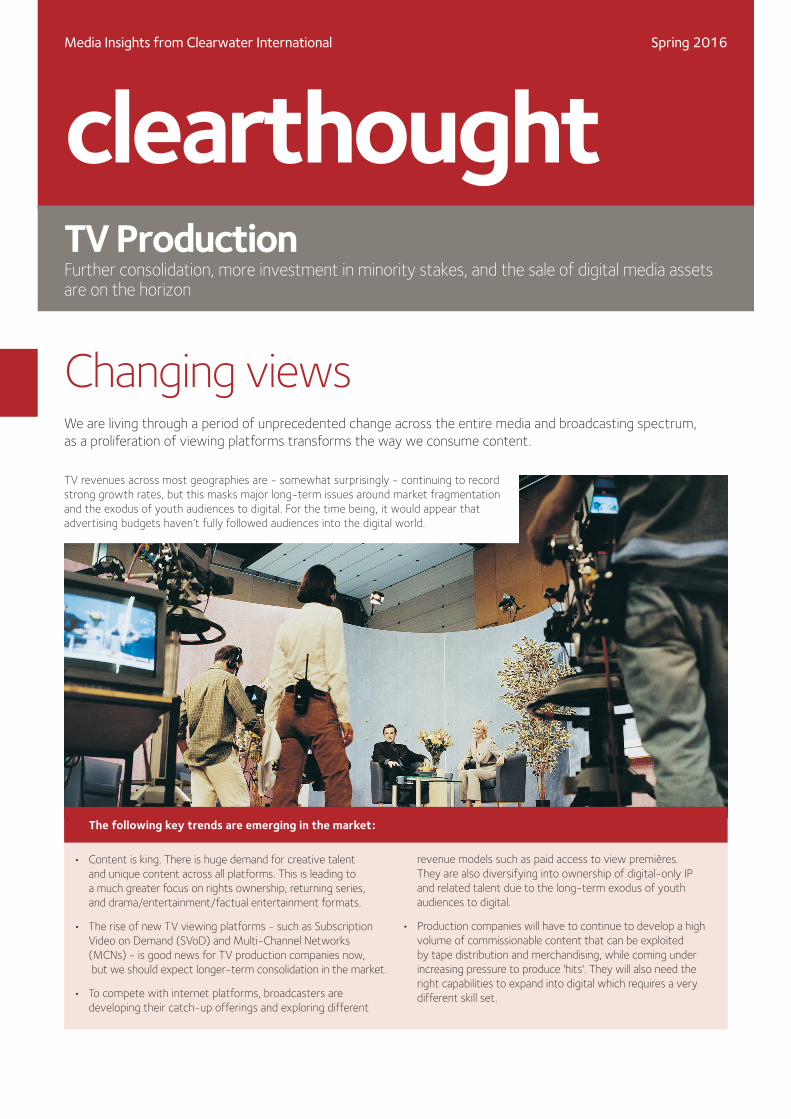

Changing viewsWe are living through a period of unprecedented change across the entire media and broadcasting spectrum, as a proliferation of viewing platforms transforms the way we consume content.

TV revenues across most geographies are - somewhat surprisingly - continuing to record strong growth rates, but this masks major long-term issues around market fragmentation and the exodus of youth audiences to digital. For the time being, it would appear that advertising budgets haven’t fully followed audiences into the digital world.

• Content is king. There is huge demand for creative talent and unique content across all platforms. This is leading to a much greater focus on rights ownership, returning series, and drama/entertainment/factual entertainment formats.

• The rise of new TV viewing platforms - such as Subscription Video on Demand (SVoD) and Multi-Channel Networks (MCNs) - is good news for TV production companies now, but we should expect longer-term consolidation in the market.

• To compete with internet platforms, broadcasters are developing their catch-up offerings and exploring different

revenue models such as paid access to view premières. They are also diversifying into ownership of digital-only IP and related talent due to the long-term exodus of youth audiences to digital.

• Production companies will have to continue to develop a high volume of commissionable content that can be exploited by tape distribution and merchandising, while coming under increasing pressure to produce 'hits'. They will also need the right capabilities to expand into digital which requires a very different skill set.

The following key trends are emerging in the market:

Media Insights from Clearwater International clearthought | Spring 2016

M&A activityConsolidation drive

Against the backdrop of these huge shifts in the market, there has been a wave of consolidation both within production companies (horizontal integration) and between production and broadcast firms (vertical integration).

The trend has been typified by deals such as: the merger of Banijay Group and Zodiak Media; the tie-up between Endemol, Shine Group and Core Media Group (ESG); the acquisition of All3Media by Discovery and Liberty Global; and the buyout of Talpa Media by ITV. We expect this M&A activity to endure with the increasing demand for global content, while MCNs continue to emerge and grow.

Going global

The rush to acquire content shows no sign of abating as the largest TV production companies position themselves to grow their international content businesses.

Companies such as Vivendi and FremantleMedia have joined the ranks of Sky, ITV, ESG and Liberty in acquiring TV production companies across the world.

The UK has been a particular focus, with around 70% of independent production companies now owned by foreign businesses. There is also continued speculation that broadcasters such as Channel 4 and ITV could fall under foreign ownership.

• Production companies needing size and significant market share in top quality IP in order to have market power with broadcasters.

• Broadcasters squeezing overall production budgets as well as margins on commissions.

• Production houses increasingly needing financial strength to co-finance shows as broadcasters start to cut risk. They also need cash to invest in digital (both content creation and distribution) either organically and/or through M&A for a longer-term hedge against the likely decline in the TV market audience.

Key consolidation drivers include:

• Chinese conglomerate Dalian Wanda acquired production and finance company Legendary Entertainment for ¤3.2bn, the largest ever deal involving a Chinese company and Hollywood. Wanda previously acquired AMC Entertainment Holdings, one of the largest cinema chains in the US.

• French production group Banijay and Zodiak Media of the UK have merged to create one of the world’s biggest independent production and distribution companies, with a footprint in 18 countries.

• In autumn 2015, Vivendi made a trio of acquisitions as part of its ongoing content drive. It bought Can’t Stop Media, the UK formats creator and distributor which recently produced its first series Funnymals. It also acquired French talk show specialist Flab Lab, and La Parisienne d’Images which makes entertainment and drama programming. Vivendi has been pushing aggressively into content, building up its TV drama production and distribution operations via StudioCanal.

• FremantleMedia, the British TV production subsidiary of Bertelsmann’s RTL Group, completed a trio of deals as part of its strategy to invest in drama. It acquired French production firm Kwai, reality TV group No Pictures Please, and Italian TV and film production company Wildside.

• ITV has continued to be highly acquisitive, having purchased Talpa Media, the company behind TV productions such as The Voice, and Mammoth Screen, in which it has held a 25% stake since 2007. Other acquisitions include the purchase of Twofour Group from LDC in 2015 and a minority stake in MCN Channel Mum, in addition to taking a controlling stake in Leftfield Entertainment Group bought for ¤327m in 2014.

• All3Media acquired Neal Street Productions, the producer of Call The Midwife. It was the first deal for All3Media since it was acquired by Discovery Communications and Liberty Global in 2014. Neal Street, co-founded by Skyfall director Sam Mendes, also has a theatre arm responsible for musicals. In 2016, All3Media also acquired New Pictures, the producer of series such as The Missing and Indian Summers.

Recent deal highlights:

clearthought | Spring 2016 Media Insights from Clearwater International

Strong UK exports

Drama, entertainment, and factual entertainment content have become key drivers for British TV exports, all travelling well internationally and generating substantial distribution incomes for rights holders.

The UK’s independent television production sector is now worth more than £3bn (¤3.8bn), quadruple the sector’s value only nine years ago1, with international earnings now accounting for almost a third of the sector’s total value.

For instance the revenues of the UK's leading drama independent companies ('indies') soared last year, driven by global appetite for English language drama. However revenues across the wider indie sector were flat.

Commercial strength

UK commercial broadcasters have performed particularly strongly in recent years, to an extent masking the flatter perfomance of many indies. For instance ITV has grown through diversification, rapidly expanding its production arm and re-entering the pay TV market with ITV Encore. In 2015, it saw total revenues increase 15% to £2.97bn (¤3.86bn) with ITV Studios revenue up 33% to £1.24bn (¤1.61bn). Channel 5 has also performed strongly since being acquired by Viacom.

However, budgetary pressures on the BBC could have a knock-on impact on the rest of the TV industry as the BBC may have to reduce the amount it spends on producing original content. In spite of this, BBC Worldwide will continue to be a large contributor to the sector.

Scripted TV

Opportunities in scripted TV are also now attracting film industry talent. As Alison Owen, whose company Monumental Television recently sold a stake to ITV, says: “It’s not just that the wall between television and film has collapsed, it’s that the digital business has opened up a whole new space that is ready to house drama every bit as cinematic as movies, full of high-quality writing and just as attractive to A-list talent.”

Date Target Acquirer EV (¤m) EV/EBITDA Multiple

Mar-16 Renegade 83*(65%) Entertainment One 21 6.8x

Feb-16 Zodiak Media Banijay Entertainment 920 n.a

Jan-16 New Pictures All3Media n.d n.d

Sep-15 Astley Baker Davies (70%) Entertainment One 177 11.6x (estimated)

Jul-15 Blast! Films Sky n.d n.d

Jun-15 Twofour Group* (75%) ITV 117 9.0x (estimated)

Mar-15 Talpa Media ITV 449 8.2x

Mar-15 Neal Street Productions All3Media n.d n.d

Jan-15 Mark Gordon Company (51%) Entertainment One 218 8.7x

Oct-14 Endemol Core Entertainment Shine Group 21st Century Fox, Inc. and Apollo Global 783 n.a

Jul-14 Love Productions (50%) Sky n.d n.d

May-14 Leftfield Entertainment* (80%) ITV 327 9.5x

May-14 All3Media Discovery Communications/ Liberty Global 695 8.5x

* EV and multiples based on initial consideration

1 PACT Annual Report 2014

Media Insights from Clearwater International clearthought | Spring 2016

Minority deals

Large production companies, many from overseas, have also been taking minority stakes in small or start-up independents. The Channel 4 Growth Fund and BBC Worldwide have been particularly active in supporting new and emerging talent, while buy-and-build merchants such as Rare TV, Greenbird, Argonon and Red Arrow have taken stakes in newly formed production companies.

This is a sensible strategy as it is extremely difficult to create strong IP in-house due to the requirement for time, resources and fresh thinking. Large companies struggle to maintain all these requirements and therefore have to acquire IP and development teams via M&A.

Multi-Channel Networks

As broadcasters leverage their know-how into digital models, the market has seen a string of acquisitions of MCNs - companies which work with video platforms such as YouTube.

Technically, we consider MCNs to be predominantly YouTube only, aggregators of separately-owned YouTube channels and content creators rather than content owners.

The evolution of new digital content and MCNs is leading to the emergence of a wave of new creative talent and deals to increase sales to internet platforms. For example: ESG is creating content for DreamWorks-backed MCN AwesomenessTV's launch in the UK, France, Germany, Spain and Brazil.

Video producer and publisher Vice Media also recently launched VICELAND, its first linear TV channel, in the US. A partnership with A&E Networks, VICELAND features a 24-hour line-up of newly-produced original programming.

The only real revenue stream for MCNs is taking a commission from the YouTube ad sales that run across the channels in their network. However, AwesomenessTV is a good example of a YouTube MCN that has managed to create more of its own content.

Higher margins

Most MCNs have been slow to pivot their aggregation and YouTube ad revenue commission models in order to move into higher-margin opportunities such as:

owning IP; extending IP to other platforms such as TV; sourcing their own ad deals; and managing and nurturing talent in order to financially benefit from talent extensions into off-YouTube merchandise deals.

Such companies need to find ways of turning their huge audience numbers into profits, and to protect themselves against the fact that they don’t ‘own’ anything. They also need to be mindful of over-dependence on particular talent.

Deals to come

We expect all the major western YouTube MCNs to be acquired by traditional media strategic investors over the next year or so. This M&A is a hedge by TV companies against the long-term decline in young TV audiences. They are taking a very long-term bet that these audiences can eventually be monetised and introduced to new content that the TV companies already own.

• FremantleMedia has made a string of minority investments. It took a 25% stake in newly formed UK production company Naked Entertainment - run by Simon Andreae - as well as a stake in UK production company Full Fat TV. It has also taken a 25% stake in Corona TV and Justin Gorman's Man Alive Entertainment.

• Greenbird Media took a minority stake in Gobstopper Television, an independent launched by Desi Rascals executive Ross McCarthy. Amongst others, Greenbird has also taken a stake in Pi Productions which specialises in developing the next generation of features and factual entertainment formats. BBC Worldwide acquired a 30% stake in Greenbird in early 2016.

• BBC Worldwide took a 25% stake in Red Planet Pictures which recently made the 20-part Dickensian series for BBC1. The company is also producing a Motown musical drama Stop! In The Name Of Love and Hooten and The

Lady, a family adventure series for Sky 1. BBC Worldwide has also taken a stake in start-up Mighty Productions which aims to devise innovative series and formats for broadcasters globally.

• Channel 4 took a stake in Whisper Films which is co-owned by ex Formula 1 racing driver David Coulthard, BT presenter Jake Humphrey, and BBC Sports producer Sunil Patel. Channel 4 has since handed its Formula 1 TV production contract to Whisper which makes films for global brands within Formula 1 such as Red Bull, UBS, Shell, Casio and Hugo Boss. This is the latest investment to come from Channel 4’s Growth Fund which has taken stakes in Arrow Media, Eleven Film, Lightbox, Popkorn, Renowned Films, True North and Voltage TV.

• Hat Trick Productions took a stake in Emporium Productions, the company launched by former ITN Productions executive Emma Read – its first indie investment in eight years.

Recent minority deal highlights:

clearthought | Spring 2016 Media Insights from Clearwater International

Private Equity

Just as we have seen a number of strategic minority deals across the industry, so Private Equity (PE) interest in the sector has been characterised more by exits than investments in recent times.

For example: Permira exited All3Media to Discovery/Liberty and LDC sold to ITV its stake in Twofour Group, the family of UK and US-based production companies behind shows including Educating Yorkshire, The Hotel Inspector, Posh Pawn and Animal Odd Couples.

Vitruvian pulled the sale of Tinopolis, the TV production company, after reported interest from Banijay as well as NBC, Entertainment One and Modern Times Group. Tinopolis

has since acquired Voxsports, an established media partner and content provider for Singapore sports, through its Sunset+Vine brand. The group previously acquired US-based Magical Elves in 2014.

Our view is that PE considers content-led companies too risky for investments right now, while it is very hard to deliver the required value upside in traditional media companies. There are very few remaining UK PE investments in traditional content businesses and, as such, we expect to see more PE and venture capital exits from digital media investments in the next 12 months with valuations probably at their peak.

• NBC Universal invested $200m (¤180m) each in BuzzFeed and Vox Media. Vox Media is home to digital media brands including SB Nation, video game site Polygon, and tech site The Verge.

• Disney acquired Maker Studios, a leader in short-form video which attracts more than 10 billion views every month and has more than 650 million subscribers. Maker has since acquired Instafluence, a start-up that helps match marketers with individuals who have built large followings on various social media applications such as Instagram, Snapchat and Twitter.

• FremantleMedia acquired a controlling stake in Divimove which has become a leading MCN in Europe with 900 million views per month. Its 1,700 partner channels attract 80 million subscribers and include the top YouTubers in Spain, Italy and the Netherlands.

• Vivendi acquired Dailymotion, one of the biggest video platforms behind YouTube, for ¤217m. The deal means Dailymotion can accelerate its growth and continue its international expansion with access to music and audio-visual content.

• The ¤800m acquisition of video-game streaming site Twitch puts Amazon in direct competition with Netflix and YouTube in this arena.

Recent MCN deal highlights:

Summary

The strategics’ thirst for international content, the tightening commissioning environment and the need to invest in digital (both content creation and distribution) will continue to drive consolidation in the TV production sector. The scarcity of top quality IP is fuelling higher multiples and will lead to further minority stakes being acquired by the large production companies in small or start-up UK indies.

However, it is the longer-term issues around market fragmentation and the exodus of youth audiences to digital that will extend M&A activity. The traditional strategics will place their bets on the major western YouTube MCNs and gamble on their ability to monetise their youth audiences.

Valuations of digital media are probably at or near their peak and with advertising revenues likely to go into a down-cycle at some point soon, we expect a raft of digital media exits over the coming year including Defy Media, Woven and Vox.

Media Insights from Clearwater International clearthought | Spring 2016

www.clearwaterinternational.com

Deal highlightsSome of our media deals Dominic Bolton

Senior Advisor +44 845 034 4775 [email protected]

Carl Houghton Partner +44 845 052 0344 [email protected]

Per Surland Partner +45 51 90 40 19 [email protected]

John Sheridan Partner +353 1 517 58 41 [email protected]

José Lemos Partner +351 917 529 764 [email protected]

Axel Oltmann Partner +49 611 360 39 22 [email protected]

Thomas Gaucher Partner +33 1 53 89 05 05 [email protected]

Emma Rodgers Director +44 845 052 0359 [email protected]

Kirsten Handley Associate – Analyst Team +44 845 052 0371 [email protected]

Meet the team

British digital studio

Dominic Bolton advised the European studio and production company on its sale of a minority stake to a sovereign fund

Imaginarium Studios

Emmy Award-winning US reality TV producer

Helen Lowe advised on the disposal of Magical Elves to Tinopolis Group (backed by Vitruvian)

Magical Elves

Multi media factual producer

Dominic Bolton advised on the US acquisition of the Agatha Christie Estate by Acorn Media

Agatha Christie Estate

Multi media factual producer

Dominic Bolton advised on the ¤8m refinancing

Ten Alps

Factual entertainment and reality TV producer

Helen Lowe advised on the disposal of Gurney Productions to ITV plc

Gurney Productions

US-based TV producer of reality, entertainment and drama series

Helen Lowe advised on the disposal of ThinkFactory Media to ITV plc

Thinkfactory Media

CHINA • DENMARK • FRANCE • GERMANY • IRELAND • PORTUGAL • SPAIN • UK • US