media · surya citra media scma trading buy 3,870 47.5 47 29.6 25 12.6 10.7 ... tv companies’...

TRANSCRIPT

Analysts who prepared this report are registered as research analysts in Indonesia but not in any other jurisdiction. PLEASE SEE

ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Media

Prime time to overweight

We initiate our coverage on media companies MNC Nusantara Citra (MNCN/ Buy/ TP

IDR2,700) and Surya Citra Media (SCMA/ Buy/ TP IDR3,870). We like SCMA on the back

of its: 1) low gearing and high free cash flow (FCF), 2) robust dividend payout ratio, and

3) stellar ROE compared to peer. For MNCN, we favor the company due to 1) its strong

audience share, 2) top notch power ratio, 3) the fact that it is the only TV operator that

has integrated studio facilities located in one area in Kebon Jeruk, (MNC studio complex).

We also believe MNCN will benefit from the strengthening of the rupiah given its USD

debt exposures.

Indonesian media: appealing outlook ahead

We believe the media industry is well positioned to benefit from the continued

expansion of private consumption. Given the large population base (4th populous

country in the world) combined with stable income growth of consumers, we believe fast

moving consumer goods (FMCG) companies are likely to benefit from this favorable

macro backdrop. Furthermore, we expect FMCG companies to gear up their

advertisement spending to maximize their position in the market. Even though Indonesia

has exhibited high ad spend growth over the past couple of years (16% CAGR during

2011-2016F), we note that the average price for 30-second prime-time spot is relatively

inexpensive at only USD5,400/spot compared to peer countries such as Australia,

Singapore, Philippines (indicating ample room for growth). Furthermore, existing free-to-

air TV operators are likely to benefit from the natural entry barrier given broadcasting

license is limited by the regulators.

Expecting better revenue in2Q on the back of Ramadhan

We project revenue growth for both MNCN and SCTV will jump in 2Q, largely due to the

sahur (“pre-dawn meal” which refers to food consumed early in the morning) base effect.

As a quick reminder, Ramadhan was held during mid-June to July last year (vs. during the

early part of June in 2016). MNCN and SCMA feature popular religious dramas during

sahur in Ramadan.

We initiate coverage on SCMA with a buy recommendation and a target price of

IDR3,870, implying 34.7x 2016F P/E. We think the premium valuation on SCMA is

justified, given that SCMA has a strong track record and a solid balance sheet. Our

IDR3,870 target price is derived by using a blended calculation of target P/E at 35x and

Discounted Cash Flow (DCF) method with 10-year time span.

We initiate our coverage on MNCN with a trading buy rating and a target price of

IDR2,700, implying 27.5x 2016F P/E. Our target price of IDR2,700 was derived using a

blended calculation of target P/E at 28x and Discounted Cash Flow (DCF) method with

10-year time span.

Media companies covered in this report

Company name Ticker Rating TP

(IDR)

ROE (%) P/E(x) P/B(x)

2016F 2017F 2016F 2017F 2016F 2017F

Media Nusantara Citra MNCN Buy 2,700 14.2 16.6 22.4 17.8 3.1 2.9

Surya Citra Media SCMA Trading Buy 3,870 47.5 47 29.6 25 12.6 10.7

Source: Daewoo Securities Research

Overweight (Initiate)

Initiation

July 29, 2016

PT Daewoo Securities Indonesia

Trade

Christine Natasya

+62-21-515-1140

Media

2

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

C O N T E N T S

Investment summary 3

Indonesian media: appealing outlook ahead 3 Buy rating for SCMA (TP IDR3,870) and Trading buy for MNCN (TP IDR2,700) 4

Overview of the media industry 5

Private consumption is the backbone for advertisement demand 5 FMCG companies, especially cigarettes companies dominate the TV ad spend 9 TV companies’ biggest revenue comes from PT.Wira Pamungkas Pariwara 11 Ad supply: Limited for TV, yet huge potential for online advertisement 13 Biggest media TV competitor: Online advertisement 15

Surya Citra Media 18

Company Background 18 PT Indonesia Entertainment Group 20 Management team 21 Famous TV shows/drama currently played on SCTV 23 Famous TV shows/drama that is currently playing on Indosiar 24 SCMA investment in iflix 25 Analyzing the Sports content 26 Investment thesis on SCMA 28 Surya Citra Media (Valuations) 34 Surya Citra Media (Ticker SCMA IJ/ Buy/ TP: IDR3,870) 35

Media Nusantara Citra 39

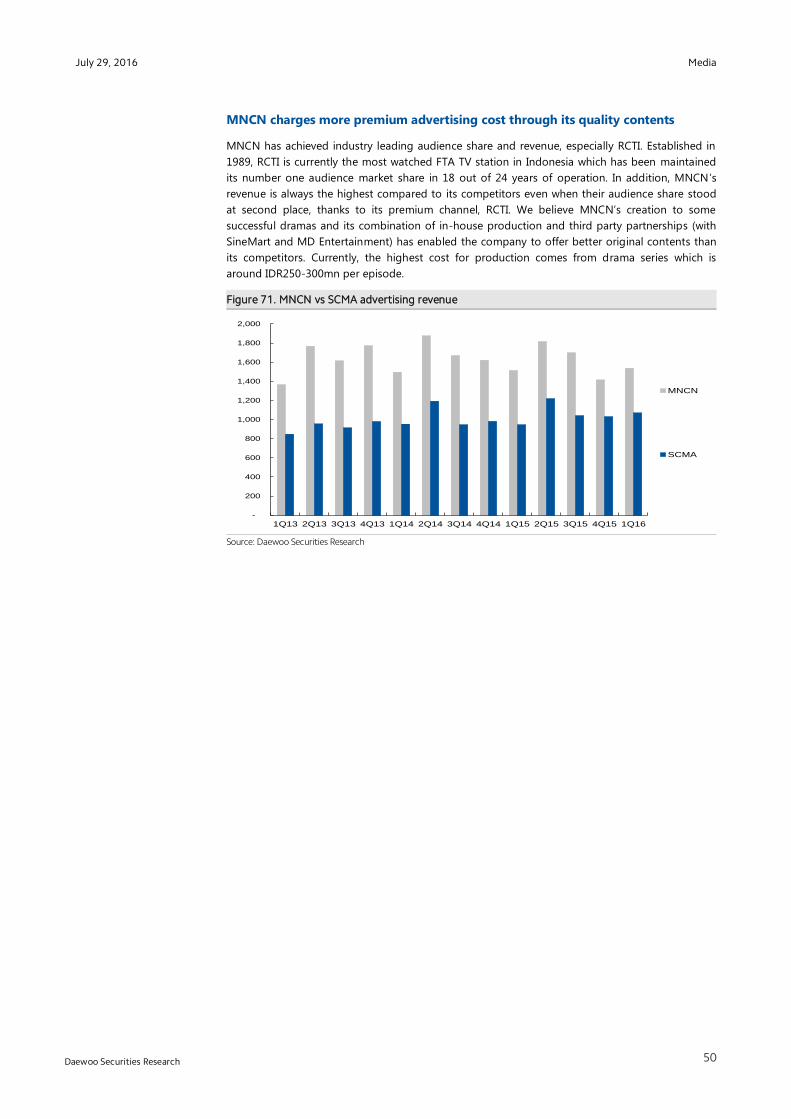

Company Background 39 MNCN’s local content 40 MNC Pictures 40 Talent management 41 MNC Channels 41 MNC’s FTA stations appeal to different audience segments 47 Famous dramas currently played on RCTI 47 Famous dramas that are currently played on GlobalTV 48 Famous dramas that are currently played on MNC TV 49 MNCN charges more premium advertising cost through its quality contents 50 Investment thesis on MNCN 51 Media Nusantara Citra (Valuations) 54 Media Nusantara Citra (Ticker MNCN IJ/ Trading buy/ TP: IDR2,700) 55

Risks to our call 58

Media

3

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Investment summary

Indonesian media: appealing outlook ahead

We believe Indonesia’s TV media industry is well poised to benefit from the continued private

consumption expansion. Given the large population base (Indonesia is the world’s 4th

largest

populous country) combined with stable income growth of consumers, we believe fast moving

consumer goods (FMCG) companies are likely to benefit from this favorable macro backdrop.

Furthermore, we expect FMCG companies to increase their advertisement expenses to maximize

their position in the market. Even though Indonesia has already exhibited high ad spend growth

over the past couple of years (16% CAGR during 2011-2016F), we note that the average price for

30-second prime-time spot is relatively inexpensive at only USD5,400/spot compared to peer

countries such as Australia, Singapore, Philippines (indicating ample room for growth).

Furthermore, existing free-to-air TV operators are likely to benefit from the natural entry barrier

given broadcasting license is limited by the regulators.

Figure 1. Indonesia ad spending has grown by 16% CAGR in 2011-2016F

Source: Media Partners Asia, Daewoo Securities Research

Figure 2. Average price for 30 seconds prime-time spot

Source: Media Partners Asia, Daewoo Securities Research

80,000

5,400

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Australia Singapore Philippines Thailand Vietnam Malaysia Indonesia

USD/spot

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Media

4

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 3. Prime time all demography (Free-to-air TV market share)

Source: Nielsen, Daewoo Securities Research

Buy rating for SCMA (TP IDR3,870) and Trading buy for MNCN (TP IDR2,700)

We like Surya Citra Media (SCMA) due to 1) its ability to maintain strong revenue growth despite

lower audience share compared to Media Nusantara Citra (MNCN), 2) better monetization of its

audience shares, and 3) high dividend payout ratio and strong cash position, as well as its stellar

EBITDA margin compared to peers.

MNCN, we favor the company due to 1) its strong audience share, 2) top notch power ratio, 3) the

fact that it is the only TV operator that has integrated studio facilities located in one area in Kebon

Jeruk, (MNC studio complex). We also believe MNCN will benefit from the strengthening of the

rupiah given its USD debt exposures.

Risks to our investment call

Risks to our call include 1) growing internet penetration which should prompt higher demand for

digital advertisement growth and pose threat to the conventional TV ad market, 2) government’s

regulation on cigarettes advertisement (as a quick reminder, cigarette companies command a

large portion of TV operators’ revenue), as well as 3) macroeconomic factors such as weaker-than-

expected Indonesian GDP (Daewoo forecast: 5.1% in 2016F, 5.3% in 2017F), commodity prices,

inflation rate, as well as the rupiah value against other countries.

48%

23%

14%

11%

4%

MNC Group

SCMA

VIVA

Trans group

Others

Media

5

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Overview of the media industry

Private consumption is the backbone for advertisement demand

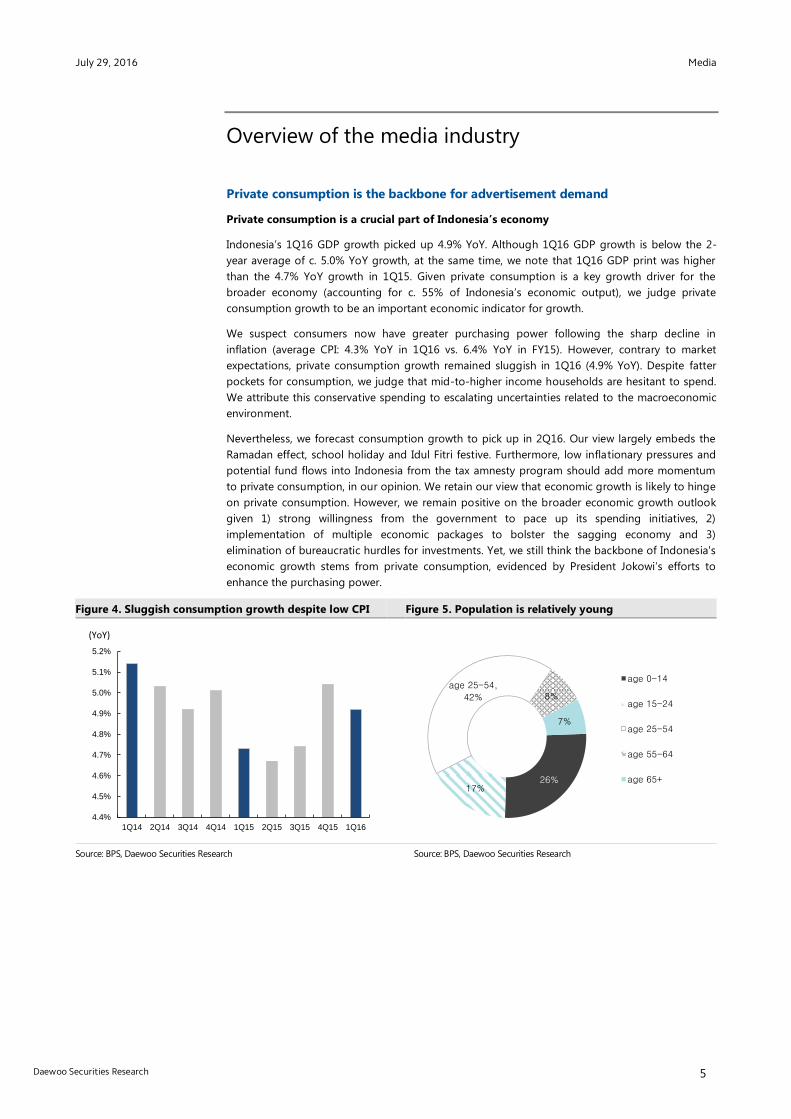

Private consumption is a crucial part of Indonesia’s economy

Indonesia’s 1Q16 GDP growth picked up 4.9% YoY. Although 1Q16 GDP growth is below the 2-

year average of c. 5.0% YoY growth, at the same time, we note that 1Q16 GDP print was higher

than the 4.7% YoY growth in 1Q15. Given private consumption is a key growth driver for the

broader economy (accounting for c. 55% of Indonesia’s economic output), we judge private

consumption growth to be an important economic indicator for growth.

We suspect consumers now have greater purchasing power following the sharp decline in

inflation (average CPI: 4.3% YoY in 1Q16 vs. 6.4% YoY in FY15). However, contrary to market

expectations, private consumption growth remained sluggish in 1Q16 (4.9% YoY). Despite fatter

pockets for consumption, we judge that mid-to-higher income households are hesitant to spend.

We attribute this conservative spending to escalating uncertainties related to the macroeconomic

environment.

Nevertheless, we forecast consumption growth to pick up in 2Q16. Our view largely embeds the

Ramadan effect, school holiday and Idul Fitri festive. Furthermore, low inflationary pressures and

potential fund flows into Indonesia from the tax amnesty program should add more momentum

to private consumption, in our opinion. We retain our view that economic growth is likely to hinge

on private consumption. However, we remain positive on the broader economic growth outlook

given 1) strong willingness from the government to pace up its spending initiatives, 2)

implementation of multiple economic packages to bolster the sagging economy and 3)

elimination of bureaucratic hurdles for investments. Yet, we still think the backbone of Indonesia's

economic growth stems from private consumption, evidenced by President Jokowi’s efforts to

enhance the purchasing power.

Figure 4. Sluggish consumption growth despite low CPI Figure 5. Population is relatively young

Source: BPS, Daewoo Securities Research

Source: BPS, Daewoo Securities Research

4.4%

4.5%

4.6%

4.7%

4.8%

4.9%

5.0%

5.1%

5.2%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

(YoY)

26%17%

age 25-54,

42% 8%

7%

age 0-14

age 15-24

age 25-54

age 55-64

age 65+

Media

6

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

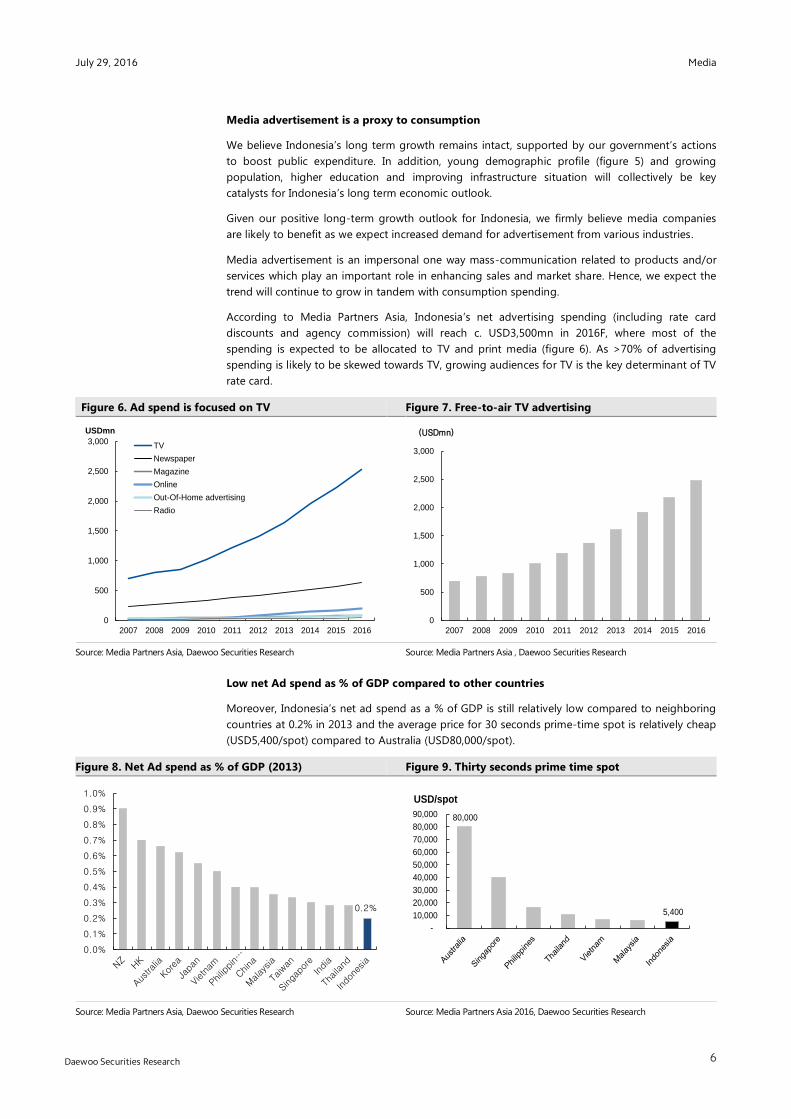

Media advertisement is a proxy to consumption

We believe Indonesia’s long term growth remains intact, supported by our government’s actions

to boost public expenditure. In addition, young demographic profile (figure 5) and growing

population, higher education and improving infrastructure situation will collectively be key

catalysts for Indonesia’s long term economic outlook.

Given our positive long-term growth outlook for Indonesia, we firmly believe media companies

are likely to benefit as we expect increased demand for advertisement from various industries.

Media advertisement is an impersonal one way mass-communication related to products and/or

services which play an important role in enhancing sales and market share. Hence, we expect the

trend will continue to grow in tandem with consumption spending.

According to Media Partners Asia, Indonesia’s net advertising spending (including rate card

discounts and agency commission) will reach c. USD3,500mn in 2016F, where most of the

spending is expected to be allocated to TV and print media (figure 6). As >70% of advertising

spending is likely to be skewed towards TV, growing audiences for TV is the key determinant of TV

rate card.

Figure 6. Ad spend is focused on TV Figure 7. Free-to-air TV advertising

Source: Media Partners Asia, Daewoo Securities Research

Source: Media Partners Asia , Daewoo Securities Research

Low net Ad spend as % of GDP compared to other countries

Moreover, Indonesia’s net ad spend as a % of GDP is still relatively low compared to neighboring

countries at 0.2% in 2013 and the average price for 30 seconds prime-time spot is relatively cheap

(USD5,400/spot) compared to Australia (USD80,000/spot).

Figure 8. Net Ad spend as % of GDP (2013) Figure 9. Thirty seconds prime time spot

Source: Media Partners Asia, Daewoo Securities Research

Source: Media Partners Asia 2016, Daewoo Securities Research

80,000

5,400

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

USD/spot

0

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USDmn

TV

Newspaper

Magazine

Online

Out-Of-Home advertising

Radio

0

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(USDmn)

0.2%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

Media

7

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Prime time show on TV

TV operators are regulated under the Law number 32 of 2002 on Broadcasting (Law 32/2002)

dividing broadcasters into 1) public broadcasters, 2) private broadcasters, 3) community

broadcaster and 4) subscription-based broadcasters.

In the area of broadcasting, there are several provisions concerning the minimum requirement to

air local contents. For example, broadcast content of private and public TV broadcasters must

contain at least 60% of domestic programs. Therefore, Indonesian TV stations have set up in-

house production facilities to produce local contents. Popular programs which are aired on TV

stations are locally produced dramas which are aired during prime time.

Prime time in Indonesia is considered to be from 18:30 to 22:00. It is imperative for TV

broadcasters to air the most popular movie or the highest rated drama during prime time since it

lifts up the all-time audience shares. In addition, prime time shows are highly profitable since

clients take advantage of the prime time shows to advertise. MNCN’s top TV channel namely, RCTI,

generates around USD6,000 gross rate per episode. The price of an advertising slot is mostly

determined by the number of viewers, with upper ratings leading to higher rates.

Following the prime time hours, “adult” programs are allowed to be broadcasted. In addition,

there is also a midnight prime time during sahur (“pre-dawn meal” which refers to food consumed

early in the morning) during the month of Ramadhan. It usually takes place from 02:30 and end at

the Fajr prayer call which varies from 04:30 to 05:00 in the early morning.

Figure 10. Screen use during the day

Source: Millward Brown, Daewoo Securities Research

0%

5%

10%

15%

20%

25%

30%

35%

40%

6 am-9 am 9 am-12 noon 12 noon- 3 pm 3 pm -6 pm 6 pm- 9 pm 9 pm-12midnight

12 midnight - 6am

TV Laptop Smartphone Tablet

Media

8

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

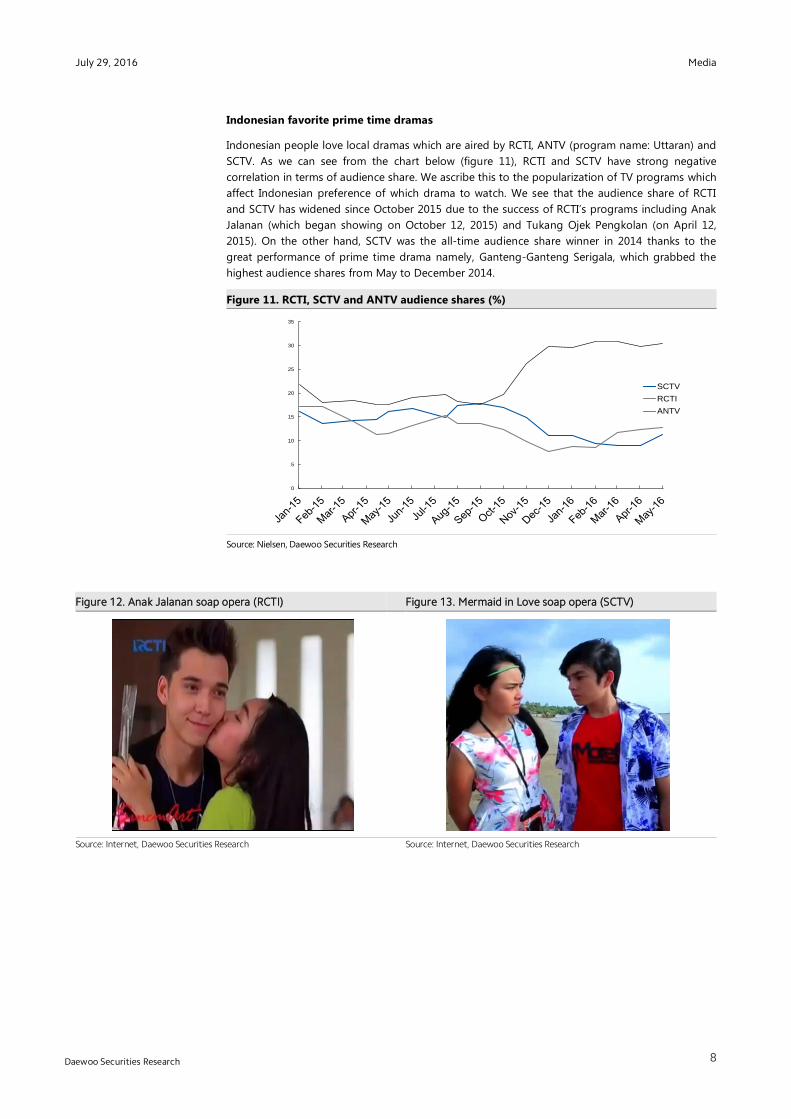

Indonesian favorite prime time dramas

Indonesian people love local dramas which are aired by RCTI, ANTV (program name: Uttaran) and

SCTV. As we can see from the chart below (figure 11), RCTI and SCTV have strong negative

correlation in terms of audience share. We ascribe this to the popularization of TV programs which

affect Indonesian preference of which drama to watch. We see that the audience share of RCTI

and SCTV has widened since October 2015 due to the success of RCTI’s programs including Anak

Jalanan (which began showing on October 12, 2015) and Tukang Ojek Pengkolan (on April 12,

2015). On the other hand, SCTV was the all-time audience share winner in 2014 thanks to the

great performance of prime time drama namely, Ganteng-Ganteng Serigala, which grabbed the

highest audience shares from May to December 2014.

Figure 11. RCTI, SCTV and ANTV audience shares (%)

Source: Nielsen, Daewoo Securities Research

Figure 12. Anak Jalanan soap opera (RCTI) Figure 13. Mermaid in Love soap opera (SCTV)

Source: Internet, Daewoo Securities Research

Source: Internet, Daewoo Securities Research

0

5

10

15

20

25

30

35

SCTV

RCTI

ANTV

Media

9

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

FMCG companies, especially cigarettes companies dominate the TV ad spend

According to Nielsen, cigarette companies such as Djarum (Not listed), HM Sampoerna

(HMSP/Hold/TP IDR4,260), Gudang Garam (GGRM/Buy/TP IDR81,200) are large spender of TV

advertising, with a total advertising value of IDR1,356bn, IDR1,228bn and IDR866bn, respectively,

as of FY2015. Second large spenders are Indomie, Traveloka, Tokopedia and Unilever products.

Figure 14. Top brands TV advertising spending (as of FY15)

Source: Nielsen, Company data, Daewoo Securities Research

IDR1,356bn

IDR225bn

IDR1,228bn IDR212bn

IDR866bn IDR592bn

IDR569bn

IDR938bn

IDR311bn

IDR685bn

IDR276bn

IDR431bn

IDR65bn IDR276bn

IDR467bn

IDR229bn

IDR460bn

IDR324bn

IDR254bn IDR407bn

IDR233bn

IDR367bn

IDR232bn

Media

10

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 15. Brands that do advertisement on TV

Source: Nielsen, Company data, Daewoo Securities Research

Given our expectations for improving economy this year, we expect higher advertising expenses

from FMCG companies in 2016. Indeed, we have witnessed higher ad spend in 1Q16. According to

Nielsen Indonesia, total ad spend growth jumped 33% YoY in 1Q16 reaching IDR31.5tr (77% of

total ad spend allocated to TV worth IDR24.2tr).

Media

11

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

TV companies’ biggest revenue comes from PT.Wira Pamungkas Pariwara

Revenues from customers which individually represent more than 10% of the total revenue largely

come from PT. Wira Pamungkas Pariwara (Not listed). PT Wira Pamungkas Pariwara is a local

subsidiary of Young & Rubicam Advertising which is one of the world’s largest consumer

advertising agencies. Young & Rubicam Advertising ranks as the world's 10th largest advertising

agency. The company is a subsidiary of WPP plc (Wire and Plastic Products) which is a British

multinational advertising and public relations company with its main office in London and its

executive office in Dublin. WPP plc is the world's largest advertising company by revenues and has

c. 3,000 offices across 112 countries with 190,000 employees. Both MNCN and SCMA generate

revenue mostly from PT Wira Pamungkas Pariwara. In FY15, MNCN received IDR1.65tr from WPP,

representing 25.64% of total revenues, while SCMA received IDR1.28tr or 30.38% of total revenue.

Figure 16. % of revenue that comes from PT. Wira Pamungkas Pariwara

Source: Company data, Daewoo Securities Research

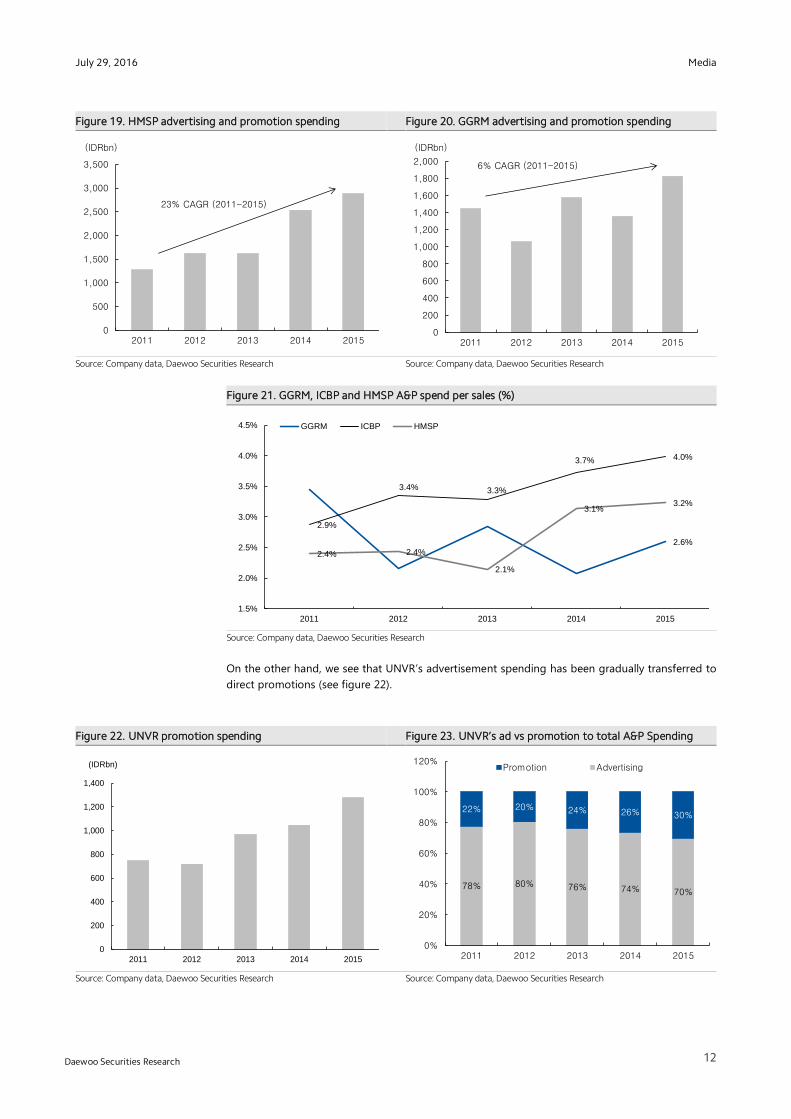

We consider media companies to be key beneficiaries of rising competition between FMCG

companies. Large cap FMCG names such as Gudang Garam (GGRM/Buy/TP IDR81,200), HM

Sampoerna (HMSP/Hold/TP IDR4,260) and Unilever Indonesia (UNVR/Buy/TP IDR52,000) have

begun to normalize their advertising spending since 2015, after being cost sensitive during the

presidential election year (2014). In particular, Indofood CBP Sukses Makmur (ICBP/Buy/TP

IDR9,200) and HMSP’s ad spending has demonstrated tremendous growth. ICBP’s advertisement

spending grew by 24% CAGR during 2011-2015 (figure 18), HMSP increased by 23% CAGR during

the same time frame (figure 19) – which were higher compared to that of GGRM at 6% CAGR

(figure 20) and UNVR’s 6% CAGR (figure 17). Furthermore, financial data from ICBP, GGRM, HMSP

further supports the appealing media outlook as their A&P spend per total sales is growing (see

figure 21).

Figure 17. UNVR advertising and promotion spending Figure 18. ICBP advertising and promotion spending

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

35% 34%

25%

30%

25%26%

23%

26%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2012 2013 2014 2015

SCMA

MNCN

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2011 2012 2013 2014 2015

6% CAGR (2011-2015F)

(IDRbn)

0

100

200

300

400

500

600

700

800

900

1,000

2011 2012 2013 2014 2015

24% CAGR (2011-2015)

(IDRbn)

Media

12

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 19. HMSP advertising and promotion spending Figure 20. GGRM advertising and promotion spending

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

Figure 21. GGRM, ICBP and HMSP A&P spend per sales (%)

Source: Company data, Daewoo Securities Research

On the other hand, we see that UNVR’s advertisement spending has been gradually transferred to

direct promotions (see figure 22).

Figure 22. UNVR promotion spending Figure 23. UNVR’s ad vs promotion to total A&P Spending

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2011 2012 2013 2014 2015

6% CAGR (2011-2015)

(IDRbn)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012 2013 2014 2015

23% CAGR (2011-2015)

(IDRbn)

2.6%

2.9%

3.4% 3.3%

3.7% 4.0%

2.4% 2.4%

2.1%

3.1%3.2%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2011 2012 2013 2014 2015

GGRM ICBP HMSP

78% 80% 76% 74% 70%

22% 20% 24% 26% 30%

0%

20%

40%

60%

80%

100%

120%

2011 2012 2013 2014 2015

Promotion Advertising

0

200

400

600

800

1,000

1,200

1,400

2011 2012 2013 2014 2015

(IDRbn)

Media

13

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Ad supply: Limited for TV, yet huge potential for online advertisement

Free-to-air dominates TV ad

TV advertising – the main channel to reach both mass market and premium segments – is mostly

dominated by free-to-air TV rather than subscriber-based TV (figure 12). Free-to-air TV

advertisement market is expected to dominate more than 65% of the total ad market by 2019F,

whereby print media will have around 20% and online of c. 11% (see figure 25).

Figure 24. Free to Air TV dominates the TV ad spend Figure 25. The pie of advertising spending in 2019F

Source: Media Partners Asia, Daewoo Securities Research

Source: Media Partners Asia , Daewoo Securities Research

Limited supply for TV advertisement: Indonesia has only 11 FTA TV stations

In the past, there was only 1 state-owned TV channel, namely, TVRI which dominated the market

for over 25 years. This changed when the government allowed Rajawali Citra Televisi Indonesia

(RCTI) – a privately owned TV operator – to broadcast. However, when RCTI was introduced to the

market, viewers with satellite dish and a decoder were able to receive and watch the programs.

Began operating in 1989, RCTI is the first commercial TV station in Indonesia with a nationwide

coverage.

Currently, there are 11 private channels with nationwide coverage, such as Indosiar, SCTV, Global

TV (which initially offered programs from MTV Indonesia), MNC TV (formerly known as TPI), RCTI,

TV One, ANTV, Trans7, Trans TV, Metro TV and iNews TV.

While prime time slots in the private free-to-air TV are limited, there is growing demand for

advertisement. Given c. 65% of total advertisement is allocated to TV, while there are only 11 TV

channels available, we believe the potential for growth is huge and attractive. Moreover, since the

enactment of UU Penyiaran No. 32/2002 (Broadcasting Act No. 32/2002) TV operators what have

nationwide coverage must be affiliated with the local TV stations. We consider this regulation to

be positive given it creates a natural barrier to new local TV entrants.

0

500

1,000

1,500

2,000

2,500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USDmn

FTA

Pay Tv

Online/ mobile, 11%

Magazines, 2%

Newspapers, 18%

Out-Of-Home advertising,

2%

Radio, 1%

TV, 66%

Media

14

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 26. Prime time all demography (Free-to-air TV market share)

Source: Nielsen, Daewoo Securities Research

Broadcasting Act No. 32/2002

The Indonesian Broadcasting Commission (Komisi Penyiaran Indonesia or KPI) – an independent

body whose responsibility is to regulate and provide recommendations in the area of

broadcasting – was established under the Law 32/2002. It also recognizes broadcasting as a

subject to government regulation and a matter of public interest. In other words, private

broadcasting institutions (Lembaga Penyiaran Swasta or LPS) are commercial broadcasters in the

form of a limited liability company (Perseroan Terbatas or PT) where they are able to engage in

radio or television broadcasting services under the broadcasting license.

Regulation under the Minister of Communication and Information (MoCI) of the Republic of

Indonesia No.28 year 2008 (MoCI 28/2008) – which is the regulatory framework of the

Broadcasting Act 32/2002 – stipulates the provisions concerning the requirements to establishing

a private broadcasting company and the licenses required.

MoCI 28/2008 states that private broadcasting institutions shall obtain the Broadcasting License

(IPP) in order to conduct broadcasting activities. The Minister shall issue a Broadcasting Operation

License to the private broadcasting institutions after obtaining the recommendation from the

broadcasting evaluation team. The Broadcasting Operation License for radio shall be granted for 5

(five) years and 10 (ten) years for television broadcasting, while both licenses are extendable.

Indonesian government limits the number of broadcasting licenses due to inadequate frequency.

Therefore, we think this creates a natural barrier to entry for new local TV stations.

Currently, the Indonesian Broadcasting Commission (KPI) states that all 10 privately owned FTA TV

stations – Media Nusantara Citra’s (MNCN) RCTI, MNC TV and Global TV, Surya Citra Media’s

(SCMA) SCTV and Indosiar, Visi Media Asia’s (VIVA) ANTV and TV One, Trans Group’s Trans TV

and Trans 7, and Metro TV – are subject to the renewal process once their licenses expire (e.g.,

MNCN is expected to renew its license on October 2016). The KPI is currently conducting a factual

verification of the administrative, content and technical requirements of the 10 individual TV

stations.

We believe the licenses can be extended for another 10-year period if it is renewed by the KPI and

the Minister of Communications and Information (MoCI). We believe, MNCN and SCMA should be

able to get the approval for renewal for their TV stations without any major issues.

48%

23%

14%

11%

4%

MNC Group

SCMA

VIVA

Trans group

Others

Media

15

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Biggest media TV competitor: Online advertisement

Daytime screen use- Smartphone is the highest media screen used by Indonesian

According to Milward Brown research, Indonesian people spend nine hours or 540 minutes in

front of their screens (Television, laptop, smartphone, tablet, etc) each day. This is the highest view

time compared to peer countries (see figure 31) with smartphone being the most viewed screen

by Indonesian people (figure 27). Therefore, we think, over the next few years (albeit slow), a

gradual shift towards digital-based advertisement will take place, given the number of

smartphone users are increasing and mobile advertisements are getting more popular. While TV is

where most companies spend for advertisement, ironically, smartphone is the most widely used

device by Indonesians. Having said that, we judge TV broadcasters will eventually need to adapt

to the changing environment.

Figure 27. % of hours people spent on media (hours)

Source: Milward Brown research ,Daewoo Securities Research

Figure 28. Example of digital advertising on Youtube

Source: Internet, Daewoo Securities Research

24%

22%34%

20% TV

Laptop

Smartphone

Tablet

Media

16

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

However, the digital advertisement needs strong internet connection…

Indonesian internet penetration still remains low at c. 20.4%, and it is worth noting that the fourth

largest nation in the world (with population of more than 250mn). It is also the largest archipelago

in the world consisting five major islands that stretch from Sabang to Merauke. Given the natural

characteristics of Indonesia, we believe it is more convenient and effective for companies to

advertise their products through Television as it has wide coverage.

Figure 29. Indonesia large archipelago Figure 30. Indonesia is the fourth largest country

Source: Internet, Daewoo Securities Research

Source: Wikipedia, Daewoo Securities Research

Figure 31. Average daily screen use (hours) Figure 32. Indonesian internet users

Source: Millward Brown, Daewoo Securities Research

Source: Internet live stat, Daewoo Securities Research

0

200

400

600

800

1,000

1,200

1,400

1,600

mn pax

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

Indo

nesia

Ph

ilipp

ines

Ch

ina

Bra

zil

Vie

tna

mU

SA

Nig

eri

aC

olo

mbia

Th

aila

nd

Saudi

So

uth

Afr

ica

Szech

Ru

ssia

Arg

en

tina

UK

Ke

nya

Au

str

alia

Sp

ain

Tu

rke

yM

exic

oIn

dia

Po

lan

dS

outh

Ko

rea

Ge

rma

ny

Ca

nad

aS

lova

kia

Hu

nga

ryJap

an

Fra

nce

Italy

hours

6.9%

10.9%

12.3%

14.5%14.9%

17.1%

19.4%20.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014 2015F 2016F

(mn pax)

Internet users (L)

Penetration (R)

Media

17

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Surya Citra Media (SCMA IJ)

Grist to the mill

Surya Citra Media in brief

The company was first established under the name PT Cipta Aneka Selaras in 1999. The

company changed its name into PT Surya Citra Media (SCMA) in 2001. In 2002, the

company acquired 99.9% of shares of PT Surya Citra Televisi (SCTV) and then listed the

shares on the exchange with a ticker code, SCMA. In 2013, SCMA and IDKM merged

together to become the current SCMA.

Highest EBITDA margin compared to peers

SCMA has the highest EBITDA margin compared to peers. We believe its high margin is

supported by Indosiar’s prudency in replacing some of its expensive drama during prime

time with in-house produced talent, variety and entertainment shows. In-house production

shows bear significantly low cost base. Moreover, for SCTV’s locally produced dramas, 90%

of contents are produced in-house which is created under Screenplay production house (51%

owned by SCMA) which was bought from PT Elang Mahkota Teknologi, Tbk (EMTK) for

IDR242.25bn, and also PT Amanah Surga which is owned through PT IEG (IEG owns 70% of

the outstanding shares).

SCTV’s audience share started to recover

SCMA has launched several new dramas to fill in their prime time slots, such as Mermaid in

Love (began airing on May 2, 2016) and Surga yang ke 2 (started airing on April 18, 2016),

in an attempt to increase its audience shares. We expect the company to be successful in its

new drama releases, evidenced by its improvement in audience share in May 2016.

Initiate with a Trading Buy (TP: IDR3,870)

We initiate our coverage on SCMA with an overweight recommendation and present a

blended target price of IDR3,870, implying a 34.7x P/E to our 2016F EPS estimates. We think

the premium valuation on SCMA is justified, given SCMA has strong track record and

strong balance sheet. Our target price of IDR3,870 was derived by using a blended

calculation of target P/E of 35x and Discounted Cash Flow (DCF) method with 10-year time

span.

We like SCMA on the back of its 1) low gearing and high free cash flow (FCF), 2) high ROE,

preferably above market average, and 3) high EBITDA margin.

Media

(Initiate) Trading Buy

Target Price (12M, IDR) 3,870

Share Price (7/28/16, IDR) 3,300

Expected Return 17.2%

OP (16F, IDRbn) 2,191

Consensus OP (16F, IDRbn) 2,226

EPS Growth (16F, %) 6.7

Market EPS Growth (16F, %) 9.6

P/E (16F, x) 29.6

Market P/E (16F, x) 28.9

JCI (7/28/2016) 5,299.2

Market Cap (IDRbn) 48,251.3

Shares Outstanding (mn) 14,621.6

Free Float (%) 39.8

Foreign Ownership (%) 6.56

Beta (5Y) 0.90

52-Week Low (IDR) 2,285

52-Week High (IDR) 3,550

(%) 1M 6M 12M

Absolute 2.17 13.4 14.58

Relative -6.37 1.44 2.19

FY (Dec.) 12/13 12/14 12/15 12/16F 12/17F

Revenue (IDRbn) 3,695 4,075 4,238 4,663 5,417

Gross profit (IDRbn) 2,313 2,591 2,712 2,951 3,428

Operating profit (IDRbn) 1,759 1,928 2,015 2,191 2,545

NP (IDRbn) 1,286 1,458 1,522 1,630 1,934

EPS (IDR) 88 100 104 111 132

BPS (IDR) 186.41 236.34 215.19 254.04 308.72

P/E (x) 37.5 33.1 31.7 29.6 25.0

ROE (%) 48.6% 47.2% 46.1% 47.5% 47.0%

ROA (%) 32.9% 33.2% 32.7% 32.4% 32.4%

Note: NP refers to net profit attributable to controlling interests

Source: Company data, Daewoo Securities Indonesia Research estimates

Media

18

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Surya Citra Media

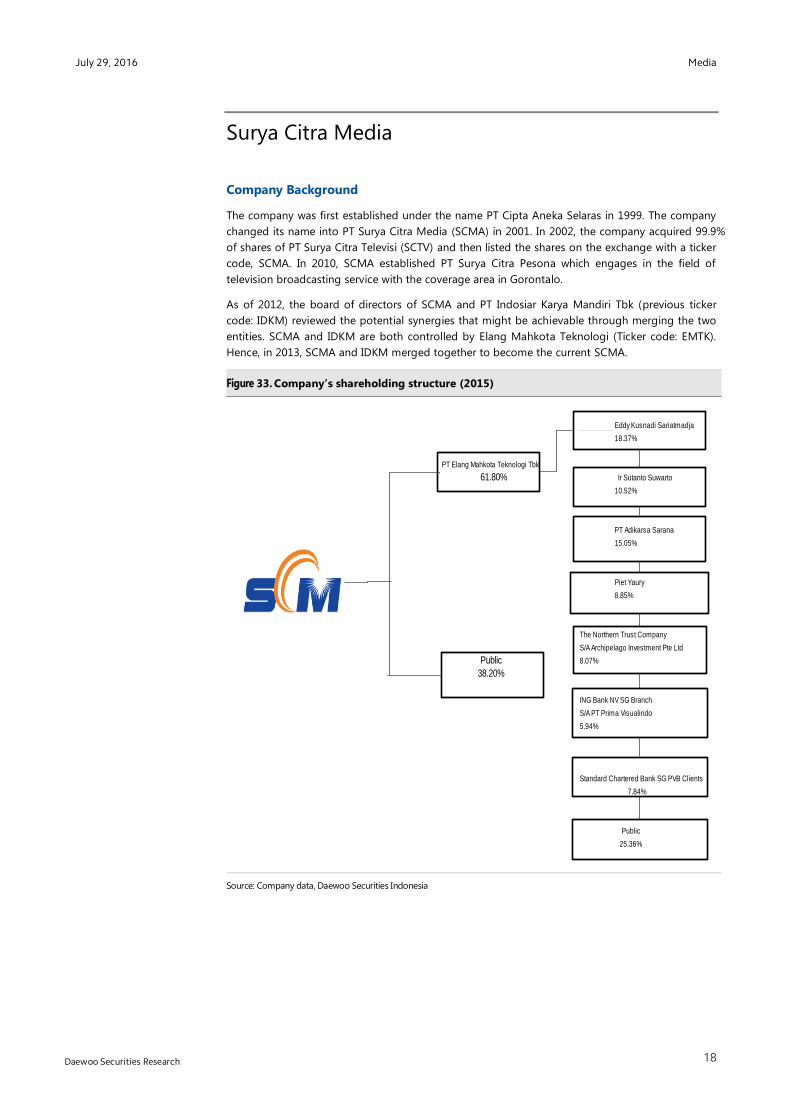

Company Background

The company was first established under the name PT Cipta Aneka Selaras in 1999. The company

changed its name into PT Surya Citra Media (SCMA) in 2001. In 2002, the company acquired 99.9%

of shares of PT Surya Citra Televisi (SCTV) and then listed the shares on the exchange with a ticker

code, SCMA. In 2010, SCMA established PT Surya Citra Pesona which engages in the field of

television broadcasting service with the coverage area in Gorontalo.

As of 2012, the board of directors of SCMA and PT Indosiar Karya Mandiri Tbk (previous ticker

code: IDKM) reviewed the potential synergies that might be achievable through merging the two

entities. SCMA and IDKM are both controlled by Elang Mahkota Teknologi (Ticker code: EMTK).

Hence, in 2013, SCMA and IDKM merged together to become the current SCMA.

Figure 33. Company’s shareholding structure (2015)

Source: Company data, Daewoo Securities Indonesia

Eddy Kusnadi Sariatmadja

18.37%

PT Elang Mahkota Teknologi Tbk

61.80% Ir Sutanto Suwarto

10.52%

PT Adikarsa Sarana

15.05%

Piet Yaury

8.85%

The Northern Trust Company

S/A Archipelago Investment Pte Ltd

Public 8.07%

38.20%

ING Bank NV SG Branch

S/A PT Prima Visualindo

5.94%

Standard Chartered Bank SG PVB Clients

7.84%

Public

25.36%

Media

19

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 34. SCMA’s business line structure (2015)

Source: Company data, Daewoo Securities Indonesia

PT Surya Citra Televisi

Broadcasting PT Indosiar Visual Mandiri

PT Bangka Tele Vision

PT Surya Citra Pesona

PT Screenplay Produksi

PT Indonesia Entertainmen

Group

PT Indonesia

Entertainmen Studio

PT Indonesia

Entertainmen

Production

Content

PT Amanah Surga

Produksi

PT Animasi Kartun

Indonesia

Supporting

and others PT Screenplay

Sinema Film

PT Surya Trioptima Multikreasi

PT Surya Citra Gelora

Media

20

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

PT Indonesia Entertainment Group

PT Indonesia Entertainmen Group (IEG) was set up in July 2015 to recognize the content

businesses of SCM and Emtek in order to 1) consolidate content resources and capabilities to

expand production and maximize utilization and efficiency, 2) create contents business that can

service multiple media distribution platforms, and 3) create new revenues which can provide

diversification from FTA TV revenues.

Figure 35. IEC’s business line of structure (2015)

Source: Company data, Daewoo Securities Indonesia

51% PT Screenplay Produksi

72% 70%

PT Amanah Surga Productions

50.10%

PT Animasi Kartun Indonesia

PT Indonesia Entertainmen grup

(IEG)

99.90% PT. Indonesia Entertainmen Produksi

PT Elang Mahkota Teknologi Tbk

28%

99.90% PT Indonesia Entertainmen Studio

Media

21

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Management team

Board of Commissioners

President Commissioner (Independent): Raden Soeyono

Mr Raden Soeyono was born in 1943 in Malang, East Java. He has been serving as the President

Commissioner of the Company since 2005. His academic background includes the National

Military Academy in Magelang in 1965 and the National Defense Agency regular course class XXII.

He obtained his Bachelor’s Degree in Economics from Universitas Terbuka. His career path ranged

from Aide de Camp to President Soeharto, Vice Assistant of Security to the Head Staff of Military,

Vice Commander to the Centre of Infantry Arms, Commander of Regional Military IV/ Diponegoro,

Head of Staff of the Armed Forces, Secretary to the Bureau of Aid Coordination to National

Stability, and Secretary General of the Defense and Security Department.

Vice President Commissioner: Suryani Zaini

Mrs Suryani Zaini is an Indonesian citizen who was born in 1962 in Jambi. She graduated from the

Department of Economic Laws and Notarial Program of the University of Indonesia. In 2011, she

joined PT Indosiar Karya Media (IDKM) and held the position of President Commissioner and

Independent Commissioner of IDKM and Indosiar. She has been the Company’s Vice President

Commissioner and Independent Commissioner since April 2013. Aside from holding the position

of Vice President Commissioner, she actively participated in various social and educational

programs in the community.

Independent Commissioner: Glenn M Surya Yusuf

Mr Glenn M Surya Yusuf is an Indonesian citizen who was born in 1955 in Jakarta. He obtained his

Bachelor of Arts Degree in Economics from University of the Philippines, Manila, the Philippines,

and a Master’s Degree in Business from the Asian Institute of Management, Makati, Philippines.

He commenced as the Company’s Independent Commissioner since May 24, 2012. In addition, he

is also chairman of the Audit Committee since October 2012. He has had important roles as the

President Director and Director in several companies in Indonesia since 1991. Currently, his title

includes Non-Executive Independent Director of CIMB Group Holdings Berhad, in Malaysia, since

2010, and Vice President Commissioner of PT Bank CIMB Niaga Tbk. Several governmental roles

previously assumed includes: Chairman of the Assistance Team to the Minister of Finance for the

Financial Sector Restructuring during the period of October 2001 - October 2002, Chairman of the

Indonesian Bank Restructuring Agency (IBRA) for the period of June 1998- January 2000, and

Director General for Finance Institutions, Ministry of Finance for the period of April-June 1998.

Commissioner: Alvin W. Sariaatmadja

Mr Alvin W Sariaatmadja is an Indonesian citizen who was born in 1983 in Sydney, Australia. He

graduated from University of New South Wales, Australia, with a bachelor’s degree in law and

finance. He has been serving as the Company’s Commissioner since 2015. Previously, he served as

a Director of the Company from 2013 to 2015. Previously, he served as a Director of PT Indosiar

Karya Media Tbk and PT Indosiar Visual Mandiri from 2011 to 2013.

Commissioner: Jay Geoffrey Wacher

Mr Jay Geoffrey Wacher is an Australian citizen, born on September 16, 1967. He was appointed as

Commissioner since April 2013. He has over 26 years’ experience in finance, private equity,

mergers and acquisitions, direct investment, business development and strategy. He is also a

Commissioner of PT Elang Mahkota Teknologi Tbk (EMTK IJ), Plan B Media Public Co. Ltd

(Thailand) and Property Guru Pte Ltd (Singapore). Previously, he served as a Financial Director of

PT PP London Sumatra Indonesia Tbk from 2004 to 2007 and Investment Director of Carnegie

Wylie & Company, Sydney, Australia, from 2000 to 2006. He held various other corporate finance

and investment roles in Australia from 1993 to 2000 and started his career as a Lawyer of Blake

Dawson Waldron, Sydney, Australia, from 1992 to 1993. He completed his studies at the University

of New South Wales, Sydney, Australia in 1991, earning a Bachelor of Law and Commerce degree

as well as becoming an Associate of the Australia Securities Institute in 1996.

Media

22

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Directors

President Director: Sutanto Hartono

Mr Sutanto Hartono was born in 1967 in Yogyakarta. He was appointed as the Company’s

President Director in 2013. Prior to his appointment, from 2011 to 2013 he served as the President

Director of SCTV, a role for which he was re-appointed in 2015. Previously, he was the Country

General Manager/President Director of PT Microsoft Indonesia and the CEO of Rajawali Citr

Televisi (RCTI) since 2008. He served as a Managing Director since 2003 and, at the same time, the

Director of Media Nusantara Citra (MNC). Prior to this, Sutanto started his career in Sony Music

Entertainment as the Senior Vice President to the South East Asia Divis ion, and a Senior Associate

at Booz Allen & Hamilton, Southeast Asia.

He obtained his Bachelor’s Degree in Chemical Engineering from the University of Notre Dame,

Indiana, and obtained his Master of Business Administration Degree from University of California,

Berkeley, US.

Director: Harsiwi Achmad

Mrs Harsiwi Achmad was born in 1966 in Karanganyar, Central Java. She was the best graduate of

Gadjah Mada University in 1990, and in 1992, she secured a scholarship from AIDAB Australia to

study for a Master’s Degree at Monash University.

Mrs Harsiwi Achmad has been serving as the Company’s Director since 2013. Previously, she held

the position of Programming Director of PT Surya Citra Televisi (SCTV) in 2010-2013, Director at PT

Rajawali Citra Televisi (RCTI) in 2006-2010 and General Manager of PT CTPI in 2004-2005. She

started her career in SCTV in various positions in programming division in 1997-2004.

Director: Imam Sudjarwo

Mr Imam Sudjarwo was born in 1955 in Kendal, Central Java. He has been serving as the

Company’s Director since 2015. Previously, he served as the President Director of PT Indosiar

Visual Mandiri in 2014. In December 2013, he held the position of Inspector of General

Supervision in the National Police (Inspektur Pengawasan Umum Polri), previously he was the

Head of Security Intelligence of the National Police (Kepala Badan Intelijen Keamanan Polri), Head

of National Police Security (Badan Pemeliharaan Keamanan Polri – Kabaharkam Polri), Head of

National Police Educational Institution (Lembaga Pendidikan Polri ), Head of Mobile Brigade Corps

of National Police (Kepala Korps Brimob Polri) and Chief of Regional Police of Bangka Belitung

Islands. He obtained his Bachelor’s Degree from Perguruan Tinggi Ilmu Kepolisian (PTIK) and his

Master of Science Degree from the University of Indonesia.

Director: Rusmiyati Djajaseputra

Mrs Rusmiyati Djajaseputra was born in 1978 in Jakarta. She has been serving as the Company’s

Director since 2015. Previously, she served as the Finance Director of PT Surya Citra Televisi (SCTV)

and PT Indosiar Visual Mandiri (Indosiar). She started her career as an auditor at Public Accounting

Firm of Prasetio Utomo & Co in 2000, before joining Public Accounting Firm of Prasetio, Sarwoko

& Sandjaja (Ernst & Young) in 2002. In 2005, she continued her career at Public Accounting Firm of

Haryanto Sahari & Rekan (PricewaterhouseCoopers). In 2006, she continued her career at PT

Johnson Home Hygiene Products (member of SC Johnson Group). She graduated from

Tarumanagara University with a Bachelor’s Degree in Accounting and owned CPA Indonesia

certificate.

Media

23

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Famous TV shows/drama currently played on SCTV

Super Puber: Indonesian locally made drama that tells a story about Joned, an 8th

grade teenager

who is in his puberty.

D’Hijabers: Indonesian locally produced drama that tells a story about Kantini, a solehah Muslim

woman who is always terrorized by her mother to get married but always avoids her whenever the

question came. This drama airs every day at 18.00.

Romeo and Juminten: Indonesian locally made drama that tells a love story of Romeo and

Juminten who happens to know each other from their parents’ relationship. This drama airs

Monday to Friday at 19:00.

Mermaid in love: Indonesian locally produced drama that tells a story about two mermaids who

fell in love after meeting two handsome guys at the beach. The program airs every Monday-

Friday at 20:15.

Surga yang ke 2 (or ‘The second paradise’ in English): Indonesian drama that tells a story about

three comrades who are trapped in a love triangle, airs every day at 21:15.

Figure 36. D’Hijabers Figure 37. Mermaid in love

Source: Internet, Daewoo Securities Research

Source: Internet, Daewoo Securities Research

Figure 38. SCTV’s audience share began to rebound due to Mermaid in Love

Source: Nielsen, Daewoo Securities Research

0

5

10

15

20

25

30

35

1/15 2/15 3/15 4/15 5/15 6/15 7/15 8/15 9/15 10/15 11/15 12/15 1/16 2/16 3/16 4/16 5/16 6/16

SCTV RCTI IVM TPI/ MNCTV TRANS7 GTV ANTV(%)

Media

24

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Famous TV shows/drama that is currently playing on Indosiar

SCMA has changed its strategy in the prime time program by moving out of drama series and into

variety and entertainment shows. SCMA’s audience share improved after the D’Academy- a reality

show or the first largest dangdut singer talent show in Indonesia. This event first began on

Monday, February 3, 2014 for the first season. The second season started on February 8, 2015,

which was followed by the third season which aired on January 24, 2016. In addition, Indosiar also

launched D’Academy Asia which was aired in November and December of 2015, bringing together

contestants from Singapore, Malaysia, Brunei and Indonesia. D’Academy was nominated by

Panasonic Gobal Awards for Talent and Best Reality Show in 2015. Indosiar ranked first spot in

prime time in Feb-May 2015, bringing its audience share as number 2 in 2015’s prime time.

Figure 39. SCMA GPM always peak in 2nd

quarter due to Indosiar’s great seasonality

performance

Source: Company data, Daewoo Securities Research

Going forward, we believe that due to its strong performance in talent shows, Indosiar will be able

to gain higher margins since its talent shows are studio based which do not require higher

programing costs (e.g., hiring actors/actresses and filming outside of the studio). We also

highlight that Indosiar achieved 67.8% of gross margins in 1Q16 compared to SCTV’s 57.0%.

Figure 40. Indosiar’s audience share peaked on April 2015 due to D’Academy

Source: Nielsen, Daewoo Securities Research

18.920.5

21.9

18.1

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

SCTV

RCTI

Indosiar

60.7%

70.9%

57.9%

62.9%

59.5%

65.8%

61.8%

68.1%

63.8%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

Media

25

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

SCMA investment in iflix

SCMA has investments in iflix amounting to IDR98.6bn in 1Q16, which is SCMA’s first technology

related investment.

iflix is Southeast Asia’s version of Netflix, which is Southeast Asia’s leading Internet TV service or a

subscription video on demand (SVOD) platform based in Kuala Lumpur. The company owns library

of the world’s top TV shows and movies in the region, with over tens of thousands of hours of

popular comedies, drama, K-drama and cartoons plus movies from Hollywood, UK, Asia and more.

iflix was founded by Patrick Grove (CEO of Malaysia based Catcha Group), Mark Britt and Evolution

Media Capital (EMC), a merchant bank focused on the media, sports, and entertainment industries.

iflix (available in Malaysia, Thailand, and the Philippines) will use the funds for expansion into new

markets on the back of strong demand for the service. Rupert Murdoch’s, European broadcaster

Sky has also invested USD45mn into iflix.

We believe SCMA’s investment into iflix is positive for SCMA as the company can monetize its

content library which is produced under IEG. Moreover, this investment should benefit SCMA in

the longer term on the back of Indonesia’s expansive internet penetration.

We also think that this SVOD (subscription video on demand) business is very attractive, as people

can be more flexible in downloading movies instead of following the given movie schedules. If we

benchmark the service to Netflix users in the United States, there were several reasons why Netflix

subscribers in the USA subscribed to Netflix (as of January 2015). According to our findings, 82%

of respondents signed up for Netlfix due to the convenience of on-demand streaming, 67% said it

was cost effective, and around 23% said they subscribed to watch Netflix’s original programs.

Having said that, we believe the prospect of SVOD business is bright for Indonesia. The digital

subscription video-on-demand viewer penetration in the U.S. is expected to grow from 23.5

percent in 2015 to 30.1 percent in 2020. Rentals or subscription-based services (SVoD) such as

Netflix, Hulu and Amazon Prime Instant Video are expected to account for 30 percent of this total,

with forecasted revenue of around USD15bn by 2020. About half of this total revenue is projected

to be generated in the US, one of the biggest SVoD markets in the world.

Figure 41. iflix layout Figure 42. SVoD penetration in USA

Source: Internet, Daewoo Securities Research

Source: Statista, Daewoo Securities Research

30%

15%

17%

19%

21%

23%

25%

27%

29%

31%

2014 2015 2016 2017 2018 2019 2020

Media

26

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Analyzing the Sports content

SCMA aired the Champions League for the last three seasons (usual schedule: August to May)

from 2012~ 2013 season, 2013~ 2014 season and 2014~ 2015 season, after it bought the rights

from Orange TV for a limited Free-to-Air rights (limited meaning only 3 matches per weekend).

Moreover, SCMA also aired the Barclays Premier League (also called Premier League and English

Premier League) in 2013~ 2014, 2014~ 2015, and 2015~ 2016 seasons (usual schedule: August to

May). Currently, the contract has been expired.

Observing SCMA’s historical gross profit margin during 2013~ 2015, we notice that the trough of

the cycle was at 4Q13. We suspect that the decline was mainly due to the introduction of more

soccer programs that include the Barclays Premier League (BPL) since 3Q13, whereby the expenses

were USD-denominated and thus was negatively impacted by a weaker rupiah. SCMA’s gross

profit margin recovered to 68.1% in 4Q15 due to the expiry of the Champions League Football

contract in June 2015.

SCMA is looking to buy BPL (Barclays Premier League) from BEIN (Aljazeera Qatar news channel),

however, SCMA is mulling at the price tag, which we suspect is quite expensive (and denominated

in USD). Furthermore, the matches are usually aired after midnight.

Figure 43. SCMA historical GPM

Source: Company data, Daewoo Securities Research

Currently, both SCTV and Indosiar take turns to air the Indonesian Torabika Soccer Championship

(rupiah denominated expense), which began since April 29, 2016 (it has 2 matches every Friday,

Saturday and Sunday).

Post the suspension of the Indonesian Super Leagued (ISL) by Minister for Youth and Sports

Affairs, Imam Nahrawi, on April 17, 2015, FIFA then froze the membership of the PSSI, resulting in

the suspension of the Indonesian Football Association. The 2015~ 2016 season of the Indonesia

Super League (ISL) was originally scheduled to begin from October 25, 2015 and end in August

2016. However, various constraints have thwarted the plan, including the use of the name

‘Indonesia Super League’ which was the property of PSSI. Finally PT Liga and Indonesian football

clubs agreed not to use the ISL name for the upcoming long-term tournament.

The Indonesia Soccer Championship or more widely known as Torabika Soccer Championship

(which is a professional soccer competition in Indonesia) replaced the temporarily-suspended

Indonesia Super League (ISL). As such, we are projecting flat number of GPM throughout the

coming years. Over the past 2~ 3 years, there has been no domestic league (Indonesia Super

League - ISL) aired by SCMA. SCMA hopes that there will be another next year, once PSSI is

reformed and FIFA once again accredits Indonesian soccer (currently banned by FIFA). Under such

conditions, we see the likelihood of SCMA bidding for the deal.

51.5%

57.9%

68.1%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

Media

27

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 44. Torabika Soccer Championship 2016

Source: Internet, Daewoo Securities Research

Media

28

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Investment thesis on SCMA

Highest EBITDA margin compared to peers

SCMA has the highest EBITDA margin compared to peers. We believe its high margin is supported

by Indosiar’s prudency in replacing some of its expensive drama during prime time with in-house

produced talent, variety and entertainment shows. In-house production shows bear significantly

low cost base. Moreover, for SCTV’s locally produced dramas, 90% of contents are produced in-

house which is created under Screenplay production house (51% owned by SCMA) which was

bought from PT Elang Mahkota Teknologi, Tbk (EMTK) for IDR242.25bn, and also PT Amanah

Surga which is owned through PT IEG (IEG owns 70% of the outstanding shares).

Figure 45. EBITDA margin (as of 1Q16)

Source: Company data, Daewoo Securities Research

Through SCMA’s in-house production joint venture, SCTV has been able to produce some of the

great high-rating drama series, for instance, Ganteng- Ganteng Serigala which was the top ranking

show back in 2014. We believe Screenplay has been supporting SCMA’s great performance given

much lower cost and good quality dramas. Screenplay and Amanah Surga (for SCTV) film on

location, while PT IEP (99% owned by IEG) and PT IES (90% owned by IEG) film inside studios (for

Indosiar).

Consistently pay large dividend amount

SCMA has maintained its high dividend payout ratio (an average of 87% in the past 3 years), which

enables the company to sustain its top-notch ROE (average of 47% through the years). We model

in a dividend payout ratio of 70% going forward as we believe SCMA 1) has solid balance sheet

(net cash position), 2) is consistently generating positive operating cash flow of above IDR1tr, and

3) has moderately low capital expenditure (c. 5% of revenue).

0%

10%

20%

30%

40%

50%

60%

TV18 IN ABS PM BMTR IJ ENIL IN MNCN IJ BEC TB SCMA IJ

Media

29

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 46. SCMA has the highest ROE among peers

Source: Company data, Daewoo Securities Research

SCTV’s audience share started to recover

SCMA has launched several new dramas to fill in their prime time slots, such as Mermaid in Love

(began airing on May 2, 2016) and Surga yang ke 2 (started airing on April 18, 2016), in an

attempt to increase its audience shares. We expect the company to be successful in its new drama

releases, evidenced by its improvement in audience share in May 2016.

Figure 47. SCTV’s audience share started to improve since May 2016

Source: Company data, Daewoo Securities Research

-5

0

5

10

15

20

25

30

35

40

45

50

SXL AU 511 HK 2008 HK 4676 JP 9409 JP TV18 IN 037560 KS 9404 JP 9413 JP 000665 CH ABS PM SKT NZ ENIL IN MNCN IJ 053210 KS MDIA IJ BEC TB SCMA IJ

7

8

9

10

11

12

13

14

15

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

Media

30

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

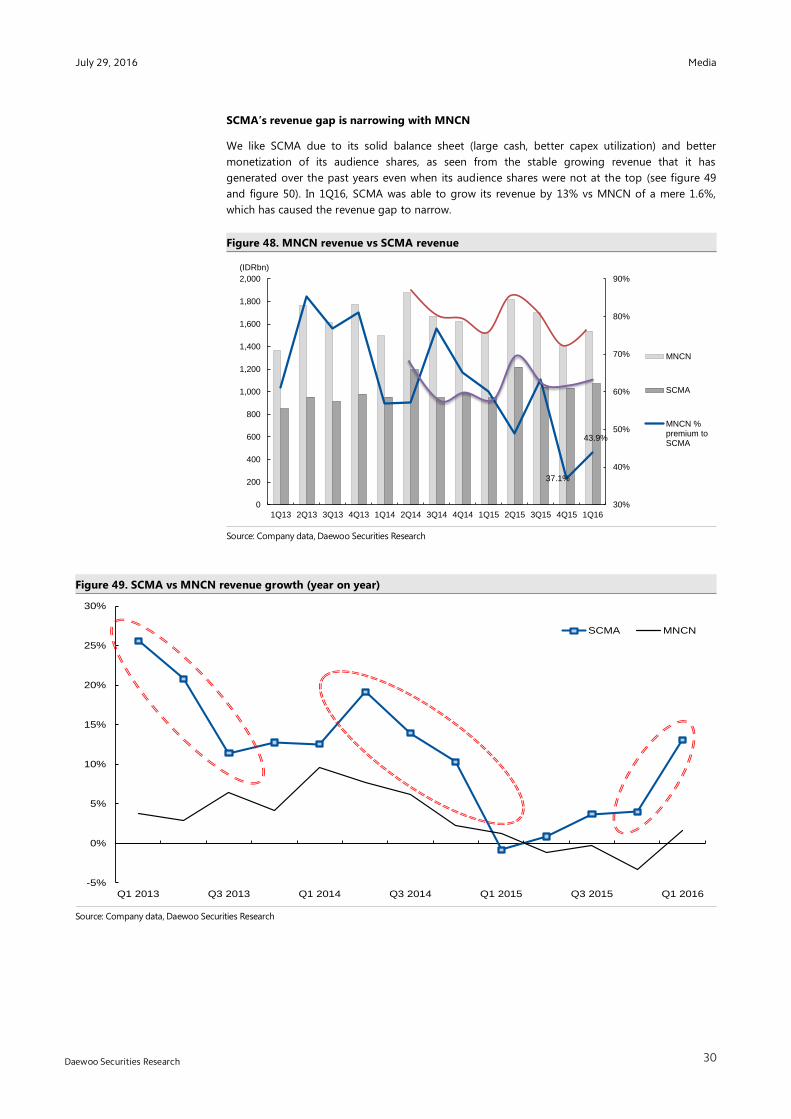

SCMA’s revenue gap is narrowing with MNCN

We like SCMA due to its solid balance sheet (large cash, better capex utilization) and better

monetization of its audience shares, as seen from the stable growing revenue that it has

generated over the past years even when its audience shares were not at the top (see figure 49

and figure 50). In 1Q16, SCMA was able to grow its revenue by 13% vs MNCN of a mere 1.6%,

which has caused the revenue gap to narrow.

Figure 48. MNCN revenue vs SCMA revenue

Source: Company data, Daewoo Securities Research

Figure 49. SCMA vs MNCN revenue growth (year on year)

Source: Company data, Daewoo Securities Research

37.1%

43.9%

30%

40%

50%

60%

70%

80%

90%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

MNCN

SCMA

MNCN %premium toSCMA

(IDRbn)

-5%

0%

5%

10%

15%

20%

25%

30%

Q1 2013 Q3 2013 Q1 2014 Q3 2014 Q1 2015 Q3 2015 Q1 2016

SCMA MNCN

Media

31

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 50. SCTV vs RCTI prime time audience share

Source: Company data, Daewoo Securities Research

Better working capital management

We believe SCMA has higher turnover since SCMA’s days of inventory in stock stood at an

average of 92 days over the past 5 years, comparable to MNCN’s which stood at an average of

162 days. Moreover, SCMA’s average receivable days stood at an average of 102 days during the

same time frame, while MNCN recorded an average of 150 days. However, both MNCN and SCMA

were able to maintain its payable days low at a similar level. SCMA’s average of payable

outstanding was 62 days, while MNCN’s was 63 days over the past 5 years. SCMA has a lower

average of cash conversion cycle of 132 days compared to MNCN’s 250 days.

Figure 51. Days of inventory Figure 52. Days of receivables

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

0

5

10

15

20

25

30

35

Q1 2010 Q3 2010 Q1 2011 Q3 2011 Q1 2012 Q3 2012 Q1 2013 Q3 2013 Q1 2014 Q3 2014 Q1 2015 Q3 2015 Q1 2016

SCTV RCTI

(%)

60

80

100

120

140

160

180

2009 2010 2011 2012 2013 2014 2015

MNCN Days ofsales outstanding

SCMA Days ofsales outstanding

(days)

0

50

100

150

200

250

2009 2010 2011 2012 2013 2014 2015

MNCN Days ofinventory on hand

SCMA Days ofinventory on hand

(days)

Media

32

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 53. Days of payables Figure 54. Cash conversion cycle

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

SCMA invests for the future

We think that SCMA is ready for the development of online advertising since it has made

investments in iflix. We believe iflix is going to fuel one of the most talked-about global media

trend – especially among millennial consumers. Bear in mind that due to the rising internet

connectivity and advancement of technology, consumers’ media screening habits have radically

evolved – especially in terms of how they access traditional home entertainment media, including

TV, print, and radio. Currently, we think some of the challenges of iflix are:

Lack of/limited live video streaming, such as live streaming of sports matches

Internet speed issues

Unavailability of certain movies

Payment method - Low penetration of credit card usage

In addition, the Screenplay production contents are also sold to websites and cinemas. These

websites are www.vidio.com, www.bintang.com, www.bola.com, www.liputan.com (all owned by

EMTK). On the other hand, name of the movies in cinemas produced by Screenplay are Magic

Hour (aired in 3Q15), London Loves Story (aired in 1Q16), ILY from 38.000 ft (aired in 2Q16).

Figure 55. Magic Hour movie

Source: Internet, Daewoo Securities Research

35

45

55

65

75

85

95

105

115

2009 2010 2011 2012 2013 2014 2015

MNCN Days ofpayables payment

SCMA Days ofpayables payment

(days)

-

50

100

150

200

250

300

350

2009 2010 2011 2012 2013 2014 2015

MNCN CashConversionCycle

SCMA CashConversionCycle

(days)

Media

33

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Figure 56. London Love Story movie Figure 57. ILY from 38.000 ft movie

Source: Internet, Daewoo Securities Research

Source: Internet, Daewoo Securities Research

Media

34

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Surya Citra Media (Valuations)

We initiate our coverage on SCMA with an overweight recommendation and present a blended

target price of IDR3,870, implying a 34.7x P/E to our 2016F EPS estimates. We think the premium

valuation on SCMA is justified, given SCMA has strong track record and strong balance sheet. Our

target price of IDR3,870 was derived by using a blended calculation of target P/E of 35x and

Discounted Cash Flow (DCF) method with 10-year time span.

Our WACC assumption of 11.2% is derived by our assumptions on risk free (Rf) rate of 7%, market

risk premium (MRP) of 5%, terminal growth rate of 3% and equity beta of 0.9x. We believe the

reduction in cost of capital tracks the decline in Indonesian bond yields which further supports our

DCF target price.

We like SCMA on the back of its 1) low gearing and high free cash flow (FCF), 2) high ROE,

preferably above market average, and 3) high EBITDA margin.

Table 1. DFC assumption table

Item Details

Cost of Equity 12%

Risk free rate 7.0%

Beta 0.90

Equity risk premium 5%

WACC 11.2%

Terminal growth rate 3%

After tax Cost of Debt 6.67%

Total PV of FCF 23,371

PV of TV 31,556

Total PV of FCF and TV 54,927

Cash 2013 1,596

Debt 2013 434

Equity value (in bn) 56,088

Equity value/share 3,836

Source: Daewoo Securities Research

Figure 58. SCMA Forward P/E Band

Source: Daewoo Securities Research

-1 Std Dev

Avg PER

+1 Std Dev

-2 Std Dev

+2 Std Dev

10

15

20

25

30

35

40

45

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

( x )

Media

35

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Surya Citra Media (Ticker SCMA IJ/ Buy/ TP: IDR3,870)

Table 2. Forecast and valuations

2014 2015 2016F 2017F

Revenue (IDRbn) 4,075 4,238 4,663 5,417

EBITDA (IDRbn) 2,029 2,135 2,323 2,699

Net profit (IDRbn) 1,458 1,522 1,630 1,934

EPS (IDR/share) 100 104 111 132

DPS (IDR/share) 51 125 73 78

ROE (%) 42.2% 48.4% 43.9% 42.8%

Dividend yield (%) 1.5% 3.8% 2.2% 2.4%

P/E ratio (x) 33.1 31.7 29.6 25.0

P/BV ratio (x) 14.0 15.3 13.0 10.7

EV/EBITDA (x) 23.2 22.1 20.3 17.4

Source: Daewoo Securities Research

Table 3. Income Statement projection

IDRbn 2014 2015 2016F 2017F

Revenue 4,075 4,238 4,663 5,417

Broadcasting expenses (1,484) (1,526) (1,711) (1,988)

Gross Profit 2,591 2,712 2,951 3,428

Opex (672) (711) (776) (901)

Operating Profit 1,928 2,015 2,191 2,545

Other income/(expenses) 10 14 16 18

Profit before income tax 1,927 2,038 2,178 2,585

Income tax expenses (469) (513) (549) (651)

Minority interest - - - -

Net profit 1,458 1,522 1,630 1,934

EBITDA 2,029 2,135 2,323 2,699

Source: Daewoo Securities Research

Media

36

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Table 4. Balance sheet projection

IDR bn 2014 2015 2016F 2017F

Assets

Cash and equivalents 1,249 686 1,596 2,044

Receivables 1,292 1,412 1,339 1,557

Inventories 464 533 446 518

Others 201 213 220 261

Total current assets 3,205 2,843 3,600 4,380

Fixed assets - net 764 962 1,059 1,194

Long term investments 24 24 24 24

Others 757 736 800 853

Total non-current assets 1,545 1,722 1,883 2,072

Total assets 4,749 4,566 5,484 6,452

Liabilities and equity

Short-term bank loans and current

maturities

102 150 116 155

Trade payables 333 260 447 453

Others current liabilities 384 451 494 570

Total current liabilities 818 860 1,058 1,178

Long term debt 350 207 318 319

Others 94 85 108 102

Total non-current liabilities 444 292 426 421

Total liabilities 1,262 1,152 1,484 1,599

Minority interests 32 267 286 339

Shareholders' equity 3,456 3,146 3,714 4,514

Source: Daewoo Securities Research

Media

37

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Table 5. Cash flow statement projection

IDRbn 2014 2015 2016F 2017F

CF from operation

Net profit 1,458 1,522 1,630 1,934

Depreciation/amortization 55 12 64 51

Change in working capitals (328) (252) 326 (297)

Others (40) 45 58 47

CF from operation 1,145 1,327 2,077 1,735

CF from Investments

Net capex (96) (199) (182) (190)

Others (41) 9 (42) (50)

CF from investments (137) (190) (224) (240)

CF from financing activity

Increase/(decrease) in debt (55) (95) 78 41

Increase/(decrease) in equity - (4) - -

Dividend payments (746) (1,828) (1,065) (1,141)

Others (1) 225 45 53

CF from financing activity (802) (1,701) (942) (1,047)

Net changes in cash 205 (565) 910 448

Source: Daewoo Securities Research

Table 6. Key Ratio

2014 2015 2016F 2017F

Growth (%)

Revenue 10.3% 4.0% 10.0% 16.2%

EBITDA 9.0% 5.2% 8.8% 16.2%

Net profit 13.4% 4.4% 7.1% 18.7%

Profitability (%)

Gross margin 63.6% 64.0% 63.3% 63.3%

Operating margin 47.3% 47.5% 47.0% 47.0%

EBITDA margin 49.8% 50.4% 49.8% 49.8%

Net margin 35.8% 35.9% 34.9% 35.7%

ROE 47.2% 46.1% 47.5% 47.0%

ROA 33.2% 32.7% 32.4% 32.4%

Leverage (X)

Current ratio 3.9 3.3 3.4 3.7

Quick ratio 3.4 2.7 3.0 3.3

Debt to equity 0.03 0.05 0.03 0.03

Net debt to equity net cash net cash net cash net cash

Interest coverage 28.3 46.8 41.8 44.4

Source: Daewoo Securities Research

Media

38

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Media Nusantara Citra (MNCN IJ)

Waiting for the real stars to show

Company Background

PT Media Nusantara Citra Tbk was established in June 1997. It currently operates four out of

Indonesia’s total eleven free-to-air (FTA) TV stations. The company was listed since June 2007

with ticker code MNCN. Not only does MNCN own FTA-TV stations such as RCTI, MNCTV,

GlobalTV, and iNewsTV, but also owns 22 pay-tv channels. The company is diversified into

additional businesses in television contents production and delivery. MNCN has been able to

maintain its top ranking in audience shares.

MNCN has integrated studio facilities

MNCN is the only TV operator that has integrated studio facilities located in one area (Kebon

Jeruk, namely MNC studio complex). The construction began in 2014 where MNCN utilized

USD250mn loans to build the four buildings. The new MNC studio complex started

functioning in July 2016, which means it is at the end of its large 3 year-capex period. MNCN

is guiding its 2016F capex for buildings and maintenance of USD60-70mn, and 2017F of

USD10-20mn. The integrated new studio complex which has four new buildings with a total of

28 new studios and also equipped with HD rating equipment is believed to enhance the on-

screen quality (better lightning, audio sharpness, etc.) and have more production capacity.

MNCN expects new studios will help actors and actresses to with easier shooting with close

proximity compared to scattered studios.

Initiate with a BUY (TP IDR2,700)

We initiate our coverage on MNCN with a trading buy rating and a target price of IDR2,700,

implying 27.5x 2016F P/E. Our target price of IDR2,700 was derived using a blended

calculation of target P/E at 28x and Discounted Cash Flow (DCF) method with 10-year time

span.

Our WACC assumption of 10.5% is derived from our estimates on risk free rate (Rf) of 7%,

market risk premium (MRP) of 5%, a terminal growth rate of 3% and equity beta of 1.0x. We

believe the reduction in cost of capital tracks the decline in Indonesian bond yields which

further support our DCF target price.

Media

(Initiate) Buy

Target Price (12M,

IDR) 2,700

Share Price (7/28/16, IDR) 2,200

Expected Return 22.7%

OP (16F, IDRbn) 2,465

Consensus OP (16F, IDRbn) 2,628

EPS Growth (16F, %) 18.1

Market EPS Growth

(16F, %) 24.7

P/E (16F, x) 22.4

Market P/E (16F, x) 17.7

JCI (7/28/2016) 5,299.2

Market Cap (IDRbn) 31,407.4

Shares Outstanding

(mn) 14,276

Free Float (%) 25.3

Foreign Ownership (%) 12.78

Beta (5Y) 1

52-Week Low (IDR) 1,185

52-Week High (IDR) 2,415

(%) 1M 6M 12M

Absolute 2.33 15.79 7.32

Relative -6.22 3.83 -5.08

FY (Dec.) 12/13 12/14 12/15 12/16F 12/17F

Revenue (IDRbn) 6,522 6,666 6,445 7,015 7,925

Gross profit (IDRbn) 3,672 3,853 3,584 3,978 4,494

Operating profit (IDRbn) 2,560 2,602 2,194 2,465 2,785

NP (IDRbn) 1,691 1,761 1,186 1,401 1,760

EPS (IDR) 120 123 83 98 123

BPS (IDR) 524.11 632.34 635.90 701.94 751.53

P/E (x) 18.3 17.8 26.5 22.4 17.8

ROE (%) 22.9% 19.7% 13.2% 14.2% 16.6%

ROA (%) 17.6% 12.9% 8.2% 8.9% 10.5%

Note: NP refers to net profit attributable to controlling interests

Source: Company data, Daewoo Securities Indonesia Research estimates

Media

39

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

Media Nusantara Citra

Company Background

PT Media Nusantara Citra Tbk was established in June 1997 and currently operates four out of

Indonesia’s total eleven free-to-air (FTA) TV stations. The company was listed since June 2007 with

ticker code MNCN. Not only does MNCN own FTA-TV stations such as RCTI, MNCTV, GlobalTV,

and iNewsTV, but also owns 22 pay-tv channels. The company is diversified into additional

businesses in television contents production and delivery.

MNCN has been able to maintain its top ranking in audience shares. Moreover, MNCN also owns

radio, print media, talent management and TV production companies which support MNC’s core

business areas.

Figure 59. Company’s business line structure (2015)

Source: Company data, Daewoo Securities Indonesia

Figure 60. Integrated end-to-end programing strategy

Source: Company data, Daewoo Securities Indonesia

Media

40

July 29, 2016

Daewoo Securities Research

Daewoo Securities Research

MNCN’s local content

MNC produces over 15,000 hours of in-house contents every year or 41 hours/ day. Currently,

MNCN has a library of 270,000 hours of local contents which makes up 40% of the total contents

available in Indonesia.

MNCN purchases some external contents other production houses in Indonesia such as SineMart

and MD Entertainment to produce superior dramas. Quality contents provided by external

production houses enable the company to reach large audiences as broadcasting high-quality

programs continue to be the core pillar of MNCN.

In addition, through in-house production facilities such as MNC Pictures, as well as MNC’s talent