mbsl ar 2009

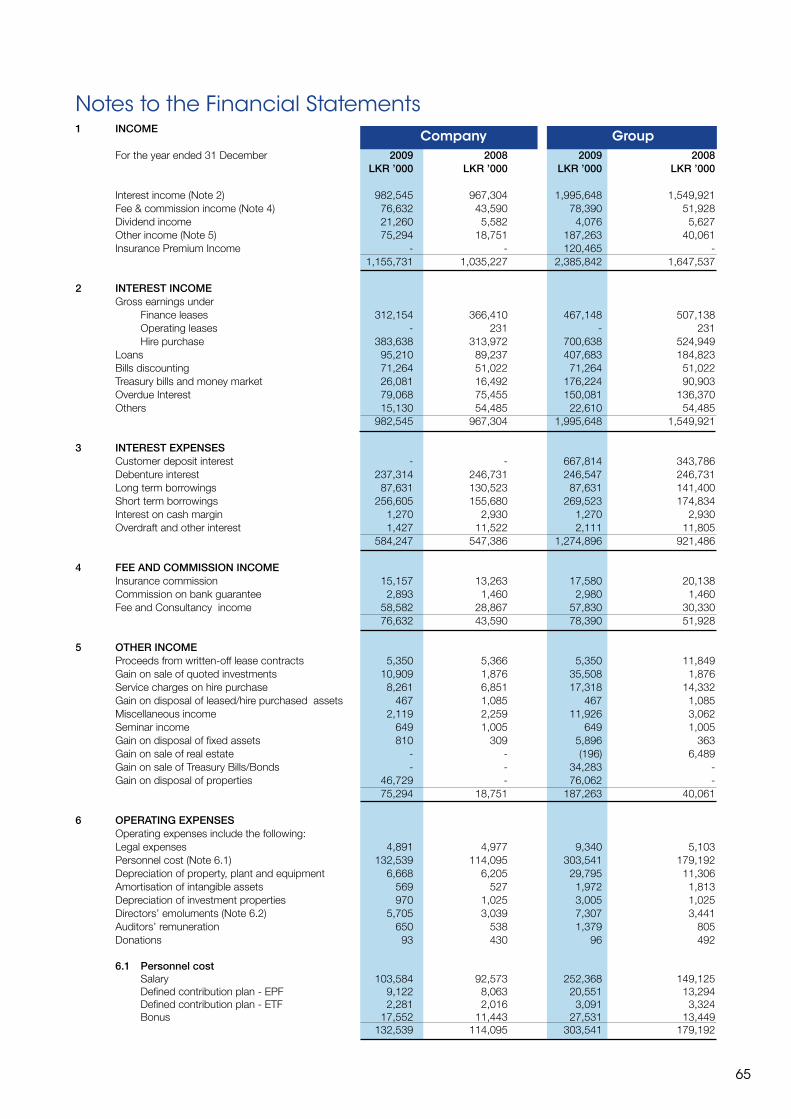

DESCRIPTION

MERCHANT BANK OF SRI LANKA - ANNUAL REPORT 2009.TRANSCRIPT

Restoring public con�dence by saving ailing businesses.

A N N U A L R E P O R T 2 0 0 9

Vision, Mission and Values 2

Financial Highlights 4

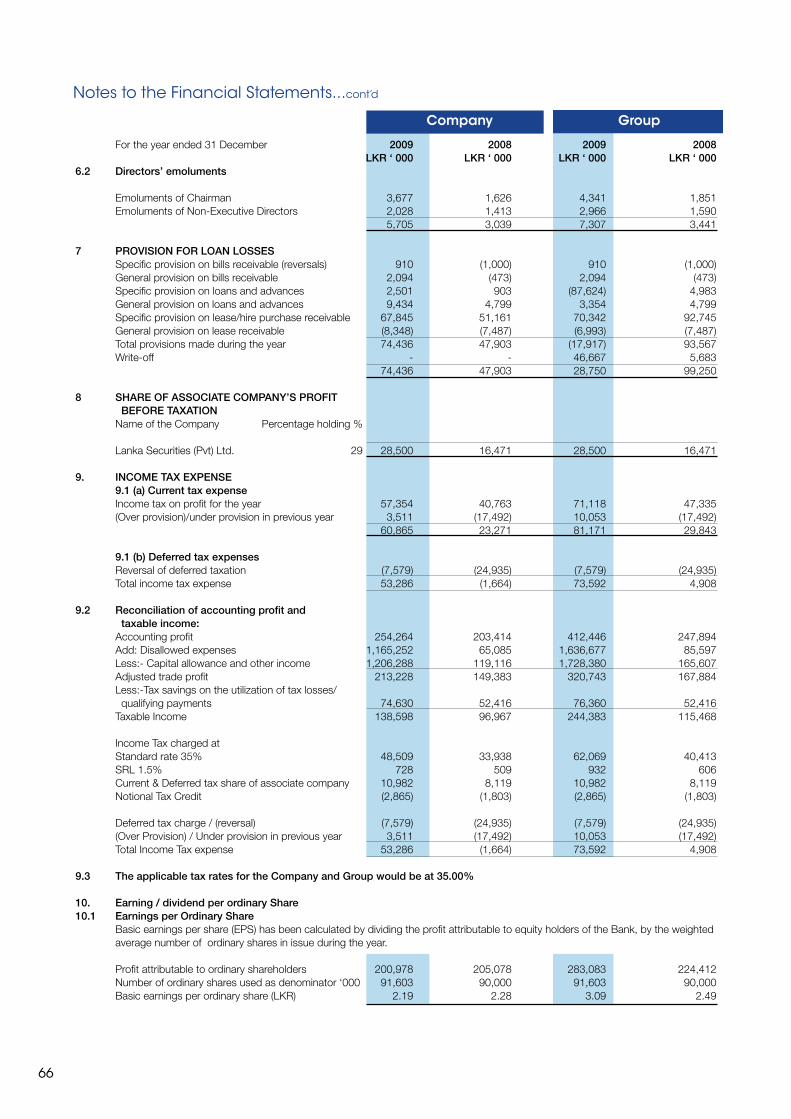

Board of Directors 6

Chairman’s Review 8

Senior Management 14

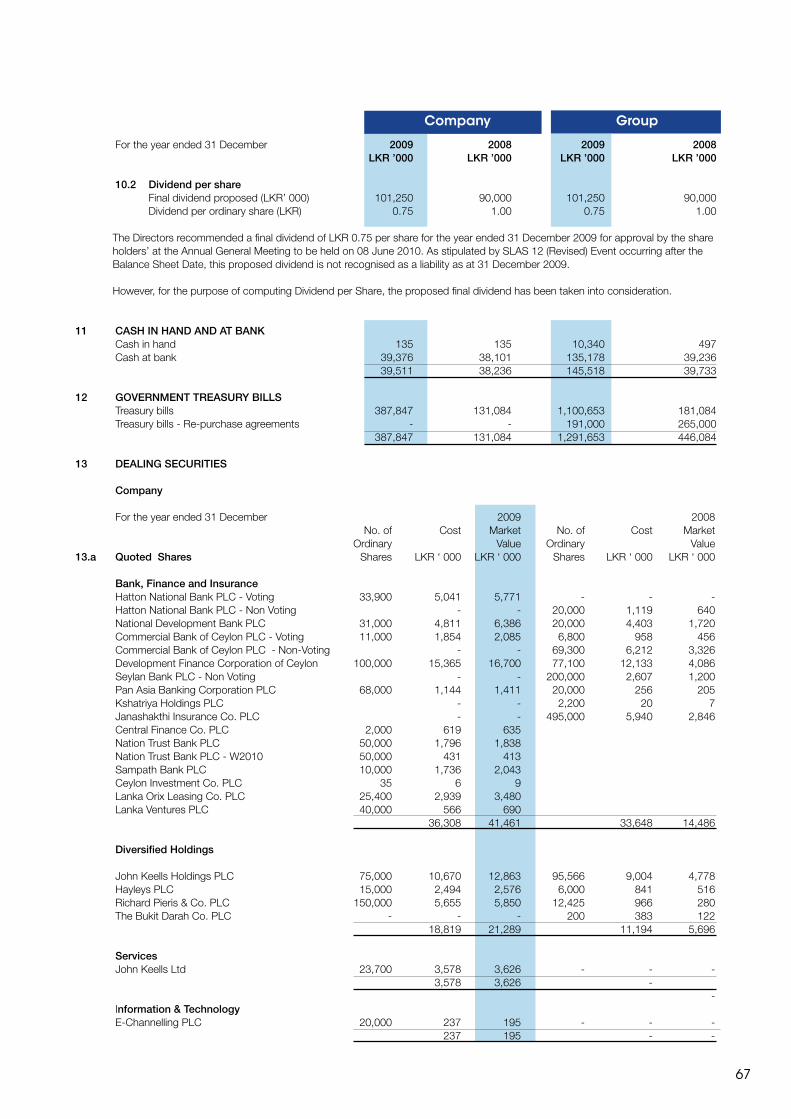

Chief Executive Of�cer’s Report 16

Management 21

Management Discussion & Analysis 24 Risk Management 30

Sustainability Report 34

Corporate Governance 42

Financial Information 44

Annual Report of the Board of Directors‘ on the Affairs of the Company 45 Directors’ Responsibilities 48

Audit Committee Report 49

Auditors’ Report 50

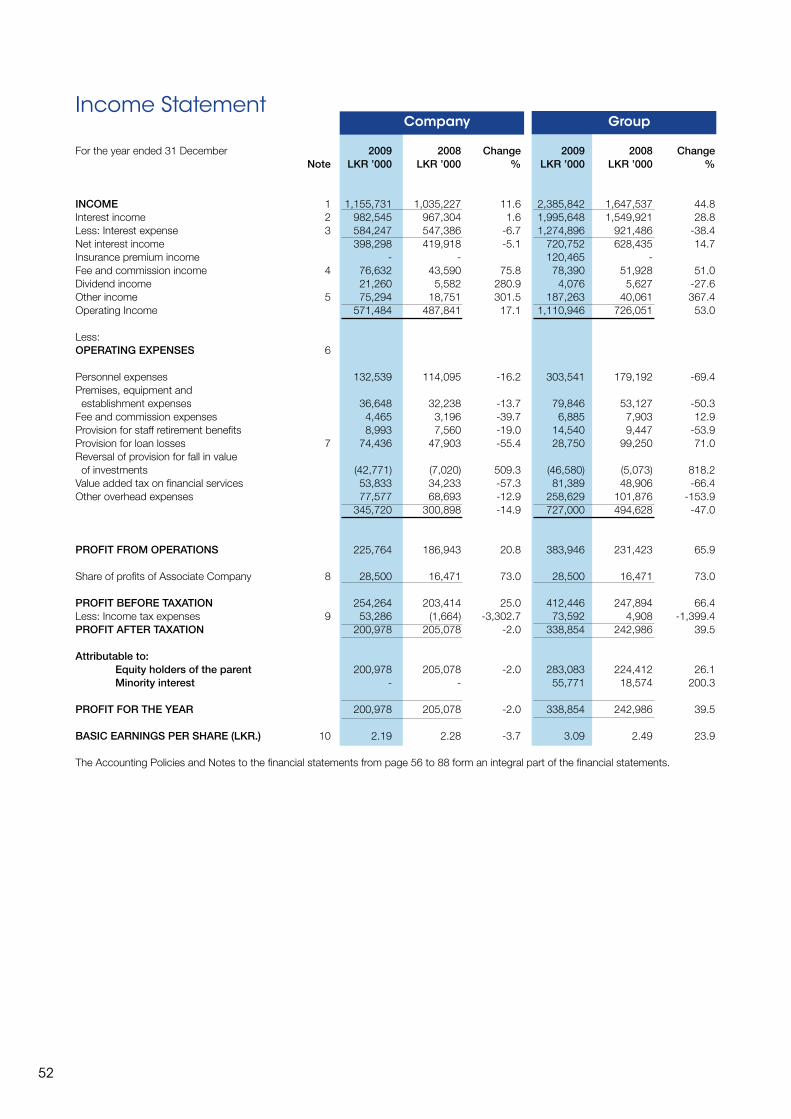

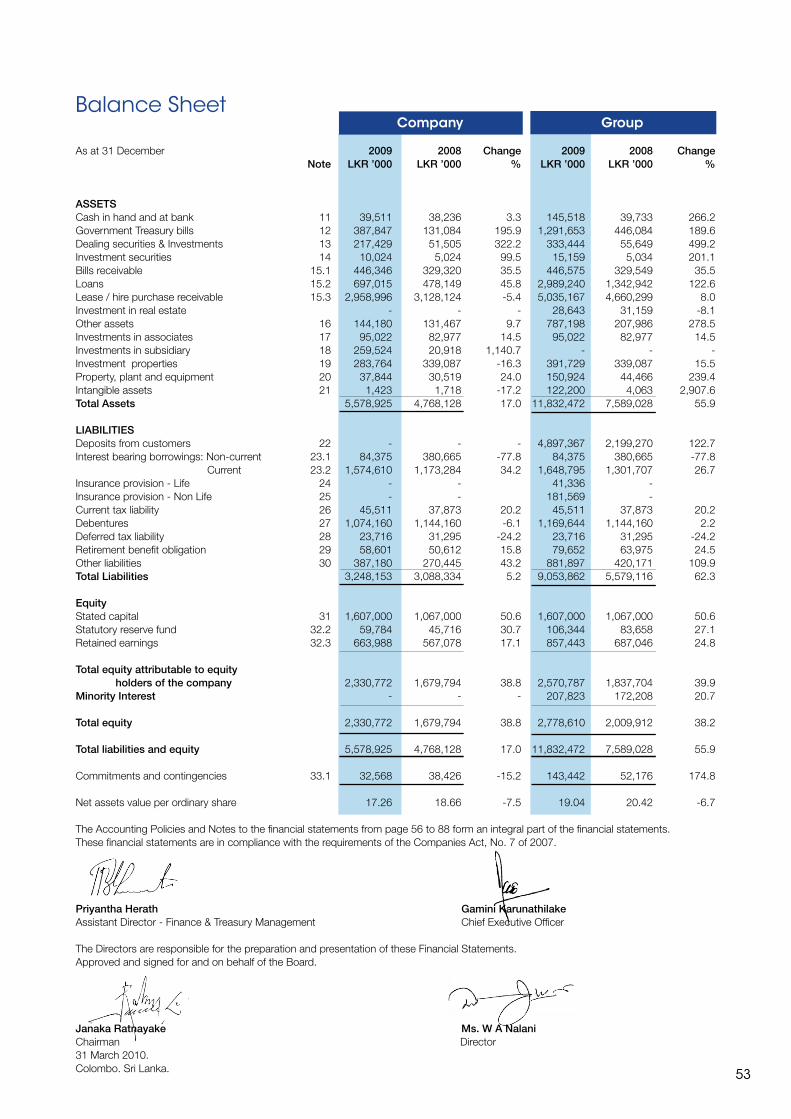

Income Statement 52

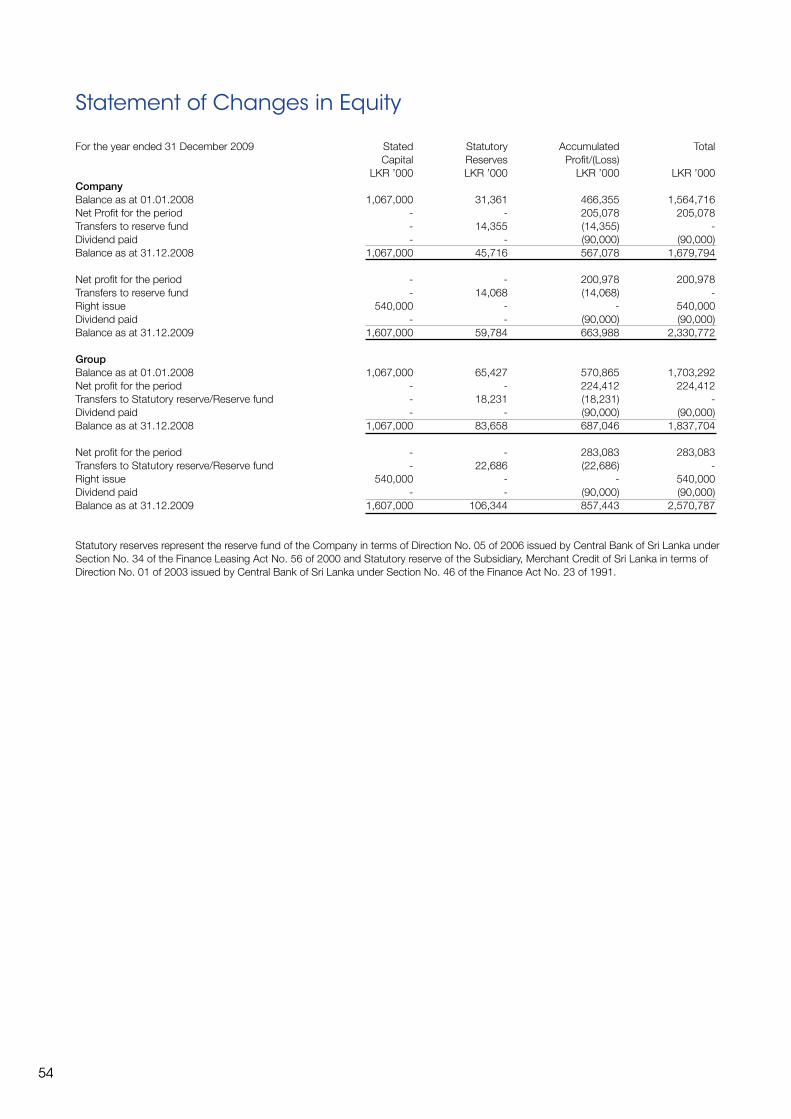

Balance Sheet 53 Statement of Changes in Equity 54

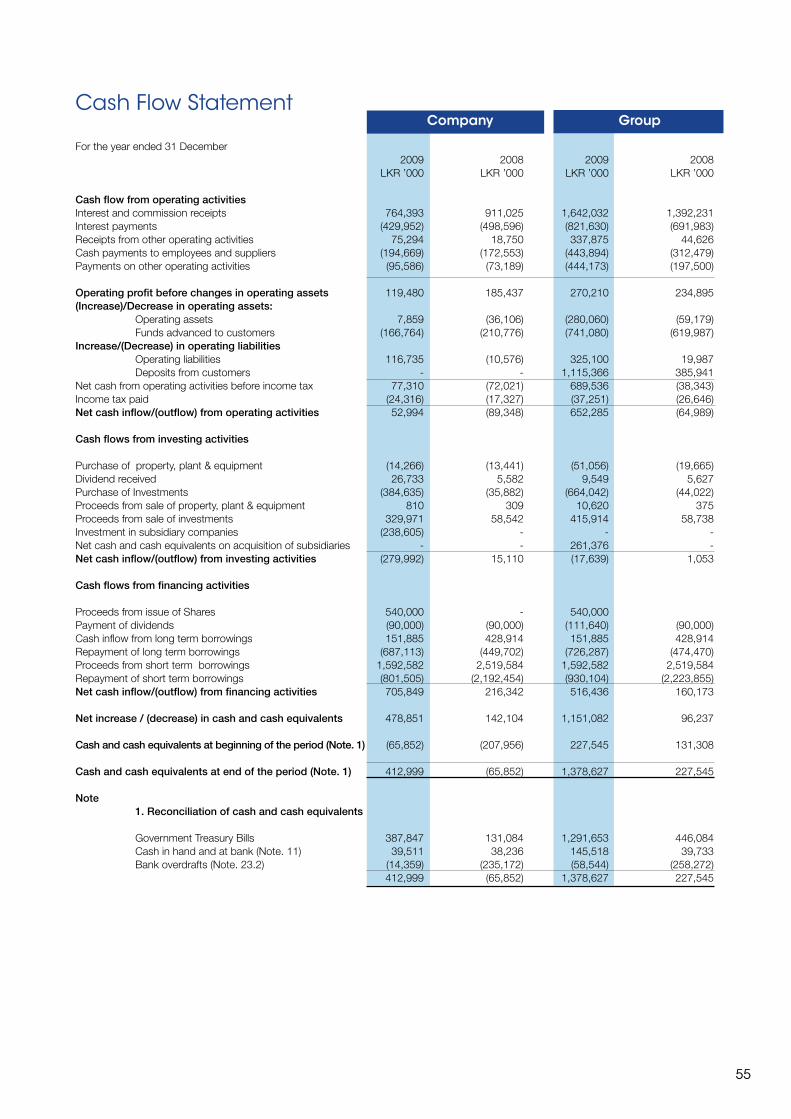

Cash Flow Statement 55

Accounting Policies 56

Notes to the Financial Statements 65

Share & Debenture Information 89

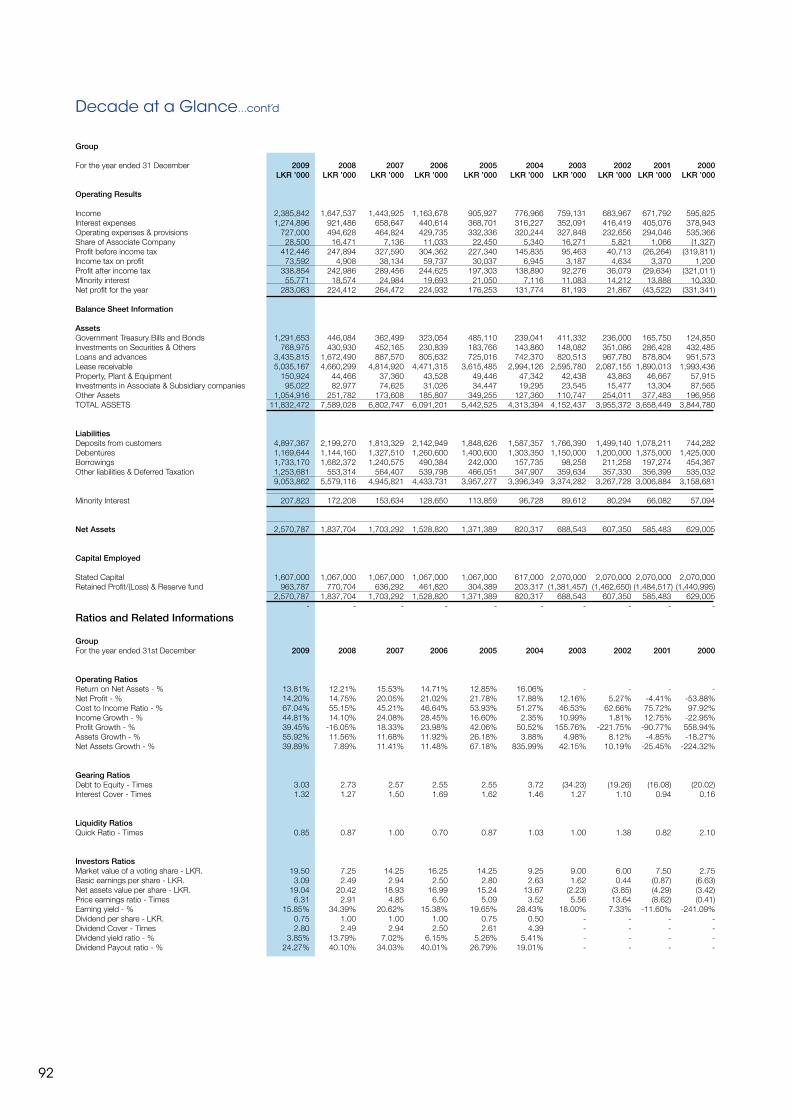

Decade at a Glance 91

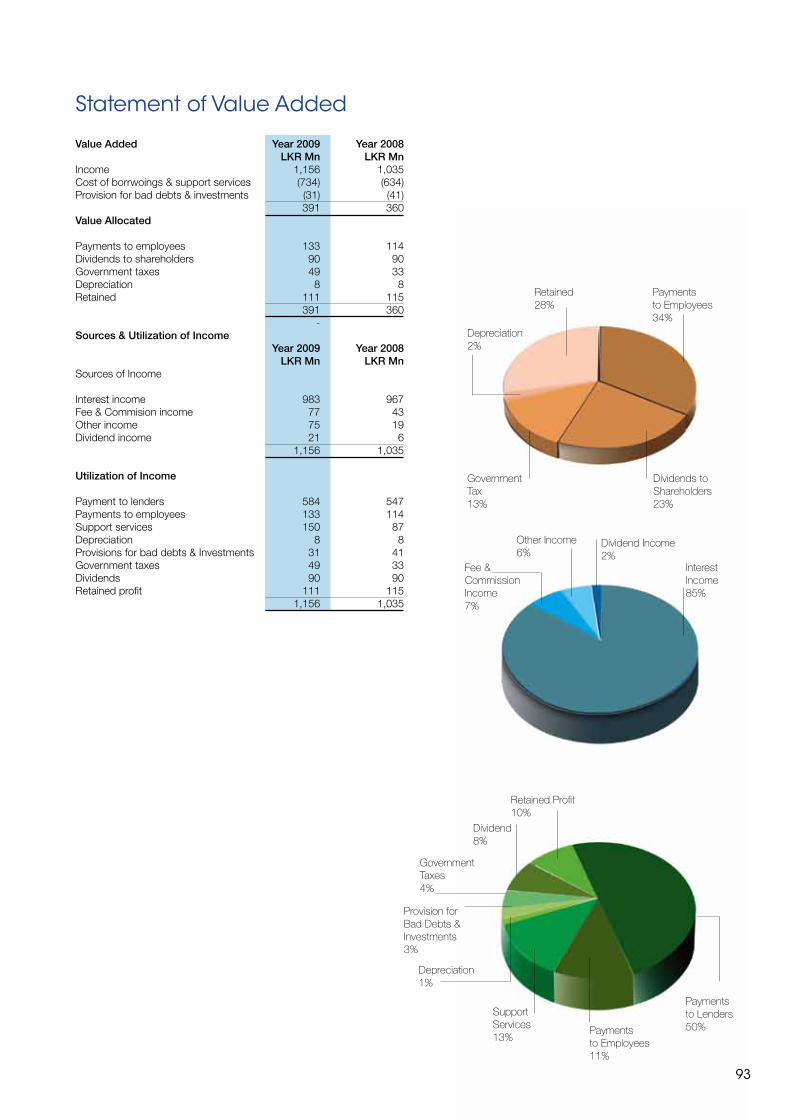

Statement of Value Added 93

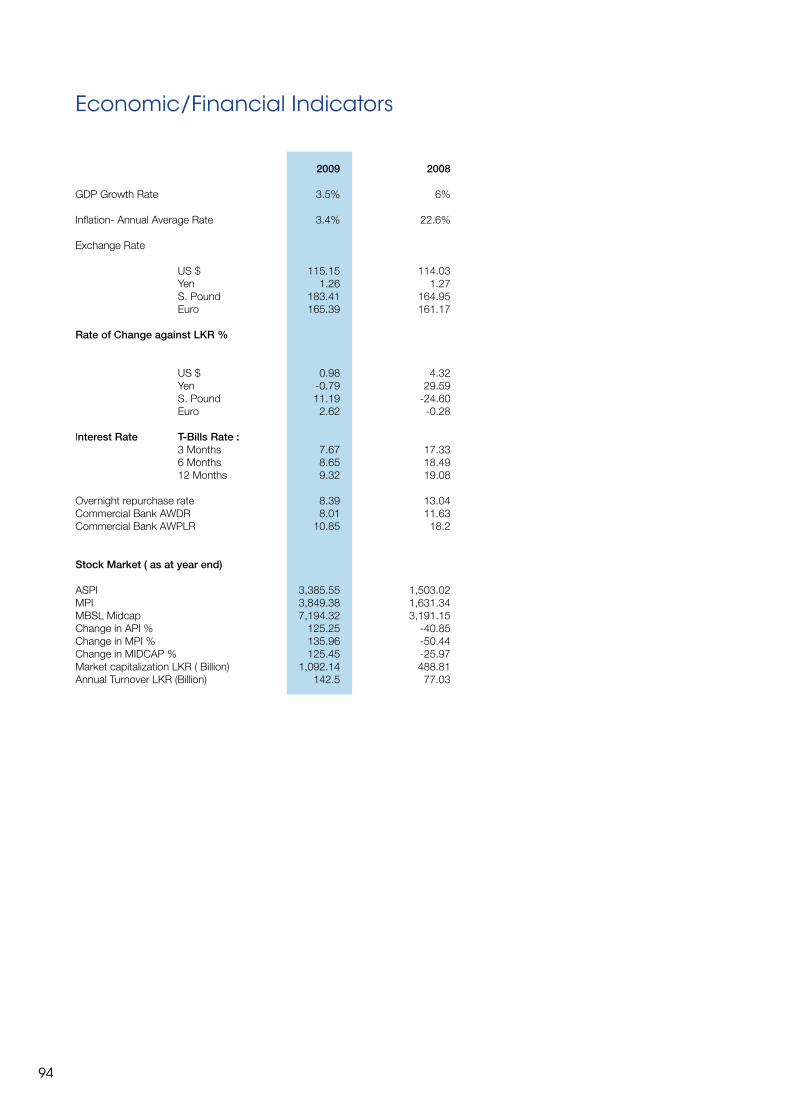

Economic/ Financial Indicators 94

Glossary of Financial Terms 95

Contact Information 96

Our Team 98

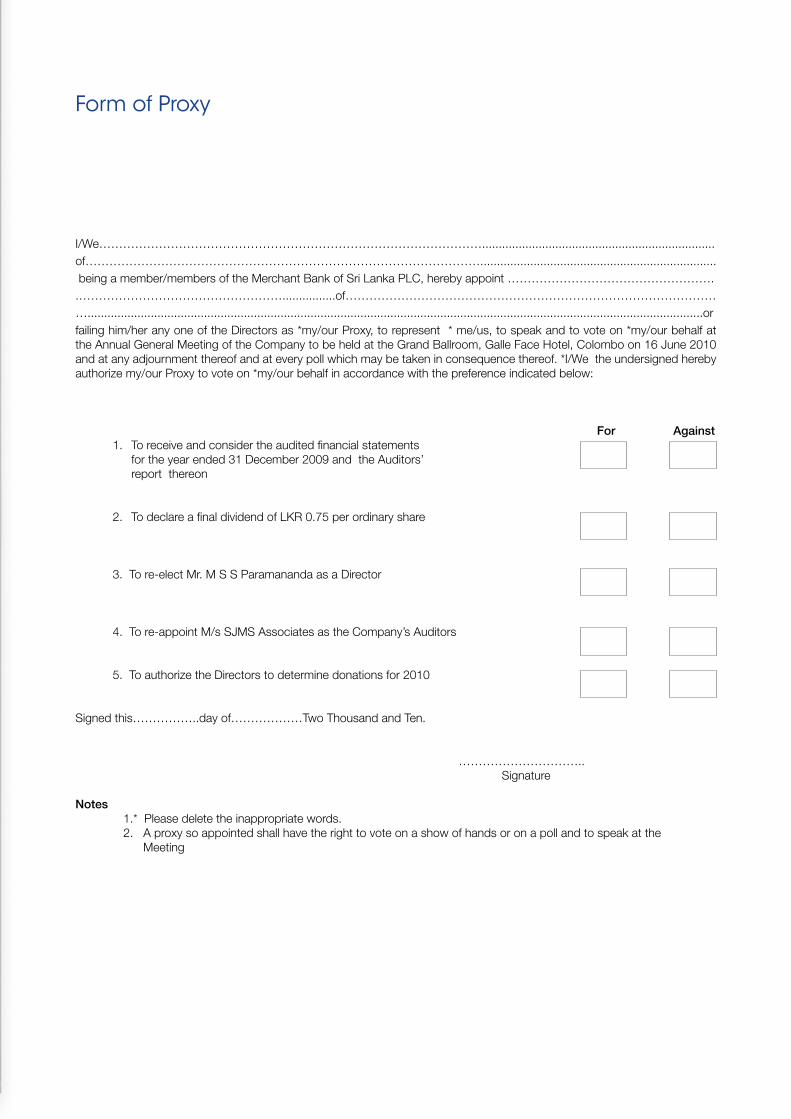

Notice of Meeting 102

Form of Proxy

Contents

i

We don’t make drama out of a crisis, but respond silently...

It has been a rough ride for financial businesses, the world over.

Besides driving the Company towards prosperity, we had to step in when some of the towering financial giants collapsed. A larger section of the nation, and may be some of you too, who had invested with them faced gloom when this misfortune befell.

The global economy itself had taken a severe pounding, and Sri Lanka too. Central Bank of Sri Lanka invited us to tug some these companies to safety. It was neither about profit nor safe strategies.

It was a considered risk that had to be taken...for if not, local financial crisis would have reached epic proportions.

It was a nation’s call...and for us at MBSL, ... the highest.

... we answered that call

Values

is to enhance our client’s wealth through optimal and sustainable solutions, to enhance shareholder value, to facilitate and motivate employees to give of their best,to foster mutually beneficial relationships with our business partners and to remain focused on our social responsibilities

at Merchant Bank, we uphold the accepted norms and ethics of the industry in all our endeavours. Our quest for innovation is guided by prudence and we also foster intrepreneurship amongst our employees and create an atmosphere where caring, sharing, openness and integrity is valued.

Our

VisionMission

Ouris to be the most innovative, dependable and diversified Merchant Bank

Our

2

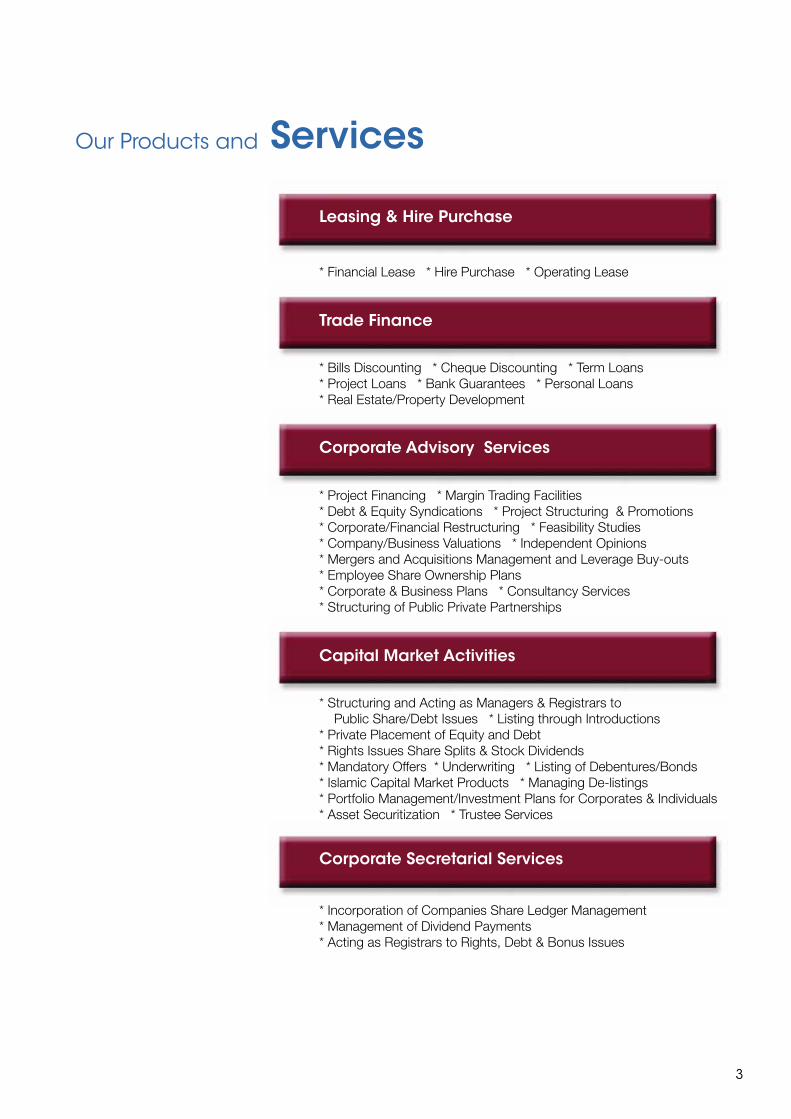

* Financial Lease * Hire Purchase * Operating Lease

* Bills Discounting * Cheque Discounting * Term Loans * Project Loans * Bank Guarantees * Personal Loans * Real Estate/Property Development

* Project Financing * Margin Trading Facilities * Debt & Equity Syndications * Project Structuring & Promotions* Corporate/Financial Restructuring * Feasibility Studies* Company/Business Valuations * Independent Opinions* Mergers and Acquisitions Management and Leverage Buy-outs * Employee Share Ownership Plans* Corporate & Business Plans * Consultancy Services * Structuring of Public Private Partnerships

* Structuring and Acting as Managers & Registrars to Public Share/Debt Issues * Listing through Introductions* Private Placement of Equity and Debt * Rights Issues Share Splits & Stock Dividends * Mandatory Offers * Underwriting * Listing of Debentures/Bonds* Islamic Capital Market Products * Managing De-listings* Portfolio Management/Investment Plans for Corporates & Individuals * Asset Securitization * Trustee Services

* Incorporation of Companies Share Ledger Management* Management of Dividend Payments* Acting as Registrars to Rights, Debt & Bonus Issues

Our Products and Services

3

Leasing & Hire Purchase

Trade Finance

Corporate Advisory Services

Capital Market Activities

Corporate Secretarial Services

4

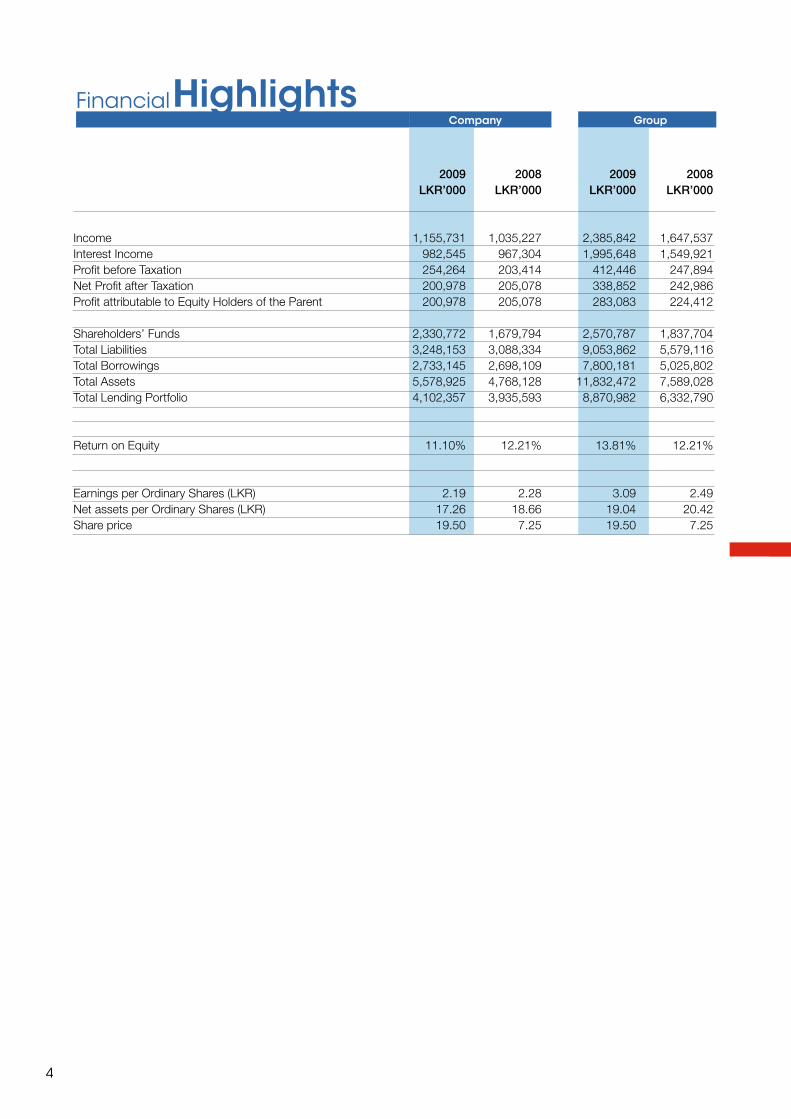

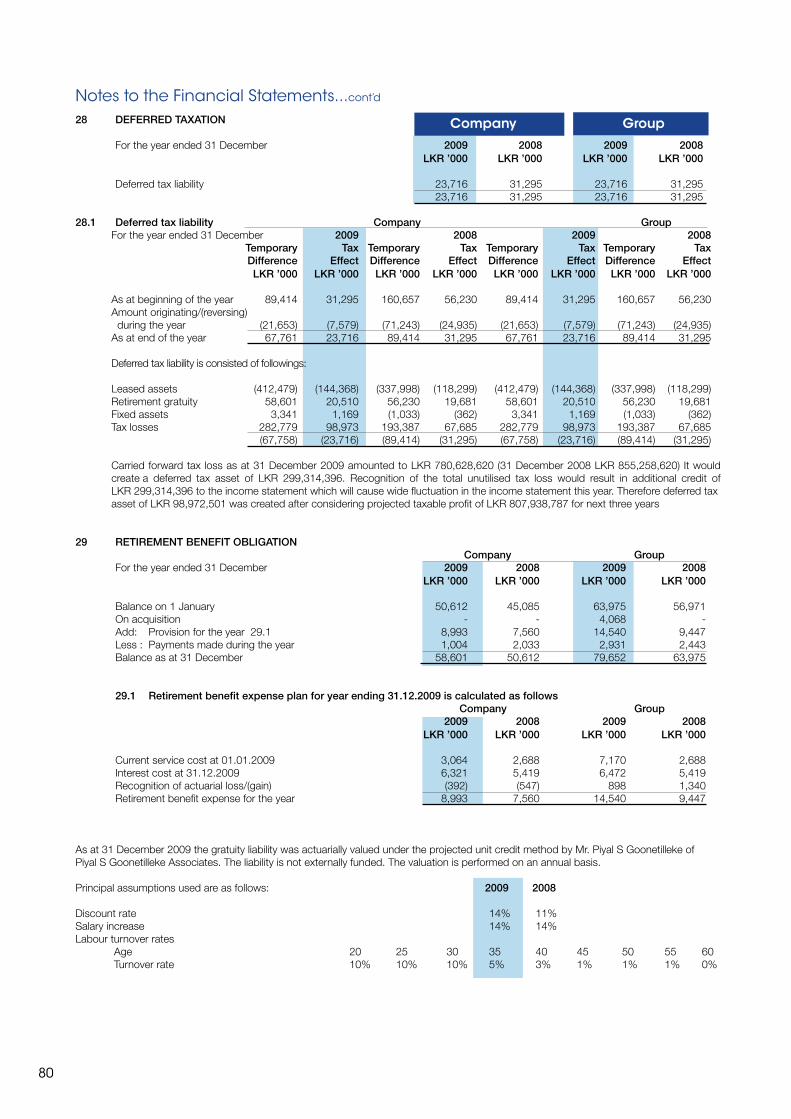

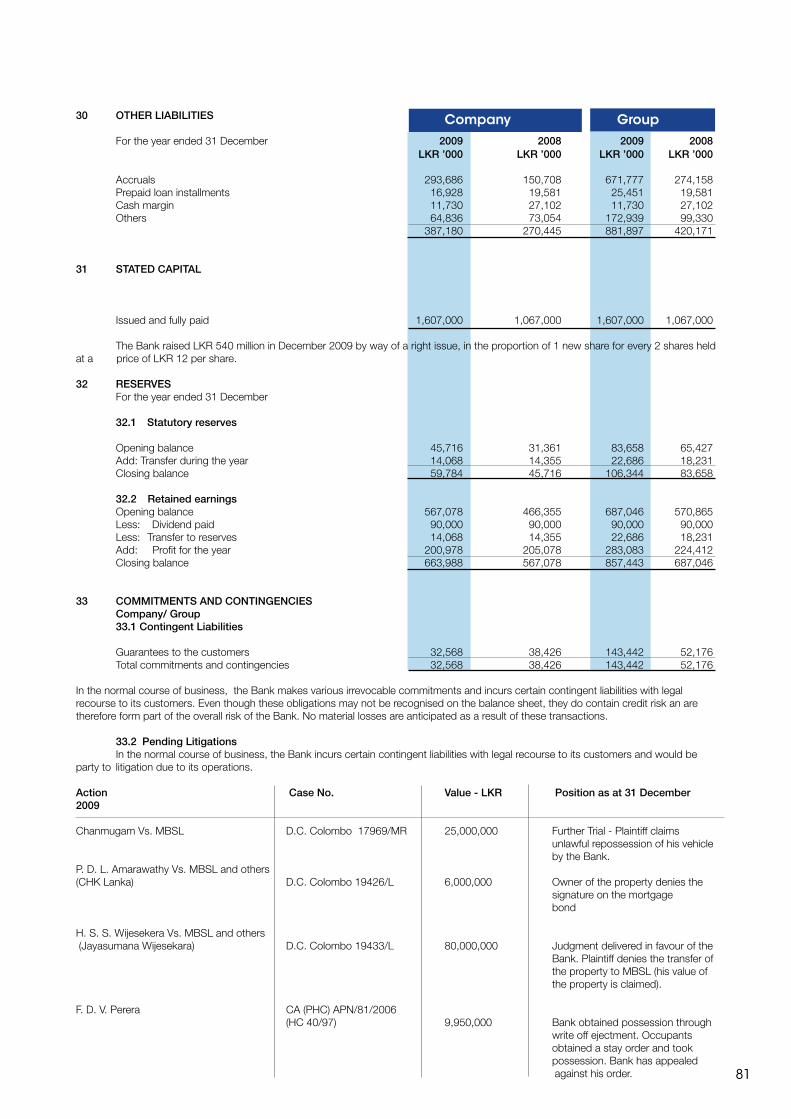

2009 2008 2009 2008 LKR’000 LKR’000 LKR’000 LKR’000

Income 1,155,731 1,035,227 2,385,842 1,647,537 Interest Income 982,545 967,304 1,995,648 1,549,921 Profit before Taxation 254,264 203,414 412,446 247,894 Net Profit after Taxation 200,978 205,078 338,852 242,986 Profit attributable to Equity Holders of the Parent 200,978 205,078 283,083 224,412 Shareholders’ Funds 2,330,772 1,679,794 2,570,787 1,837,704 Total Liabilities 3,248,153 3,088,334 9,053,862 5,579,116 Total Borrowings 2,733,145 2,698,109 7,800,181 5,025,802 Total Assets 5,578,925 4,768,128 11,832,472 7,589,028 Total Lending Portfolio 4,102,357 3,935,593 8,870,982 6,332,790 Return on Equity 11.10% 12.21% 13.81% 12.21% Earnings per Ordinary Shares (LKR) 2.19 2.28 3.09 2.49 Net assets per Ordinary Shares (LKR) 17.26 18.66 19.04 20.42 Share price 19.50 7.25 19.50 7.25

FinancialHighlights Company Group

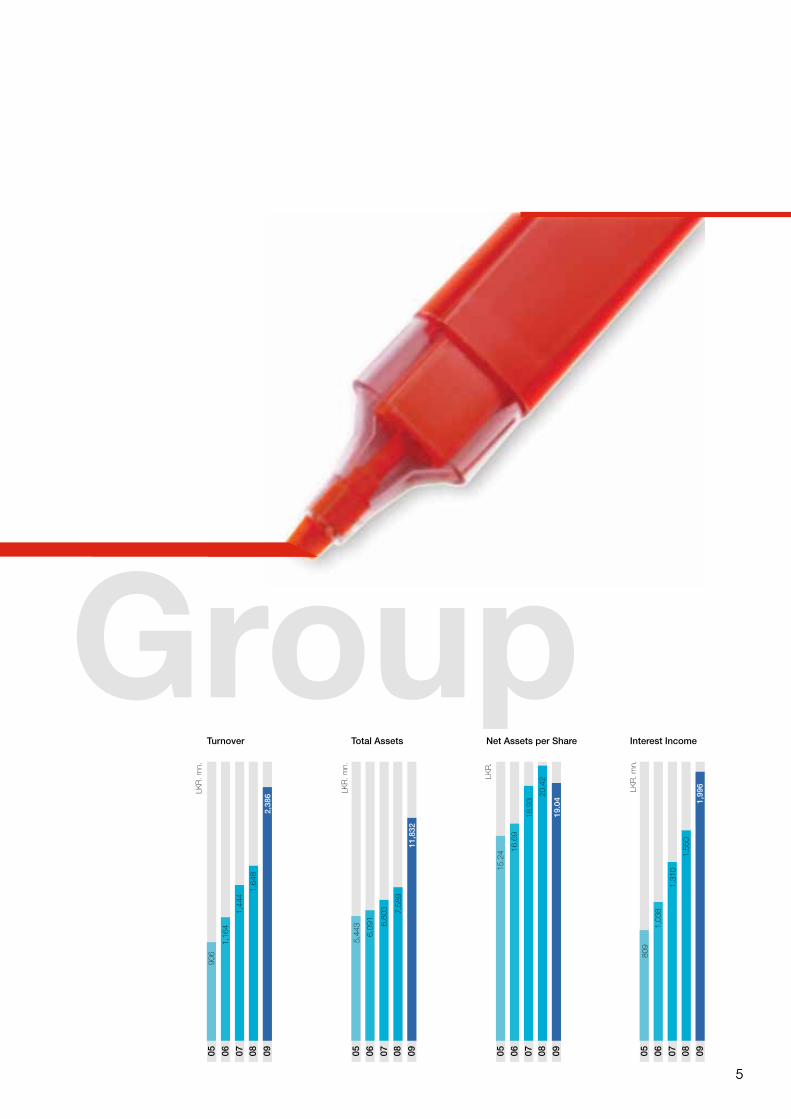

Total Assets

LKR

. mn.

05 06 07 08 09

5,44

3 6,80

3 7,58

9

11,8

32

6,09

1

Turnover

LKR

. mn.

05 06 07 08 09

906

1,44

4

1,64

8

2,38

6

1,16

4

Net Assets per Share

LKR

.

05 06 07 08 09

15.2

4

18.9

3

20.4

2

19.0

4

16.6

9

Interest Income

LKR

. mn.

05 06 07 08 09

809

1,31

0

1,55

0

1,99

6

1,03

8

5

Group

Janaka Ratnayake

- holds a BSc (Hon) Degree from University of Sri Jayawardenapura and a Post Graduate Diploma in International Business Relations from the University of Moscow, USSR.

He has an MBA from San José Uni-versity, California USA and a MastersDegree in Business Studies from the University of Colombo.

He is the Chairman of the MBSL Group, City Housing & Real Estate Co. PLC and Trillium Residencies Ltd. He is also the Chairman/ Managing Director of Computer Island Group. He was awarded the ‘Entrepreneur of the Year 2000’ by Federation of Chambers of Commerce and Industry of Sri Lanka (FCCISL).

Ms. W A Nalani

- is a Fellow of the Institute of Bankers (Sri Lanka).She also holds a Degree in Bachelor of Arts (Economics) and a Degree in Bachelor of Philosophy (Economics). She is presently the Senior Deputy General Manager (Corporate & Offshore Banking) of Bank of Ceylon ,with over 34 years of diversified banking experience, managing the largest strategic business segment including Corporate and Offshore Banking Units and the Trade Finance Unit.

She joined the Board of Merchant Bank of Sri Lanka on 28.04.2006.

She is also an Alternate Director on the Board of Credit Information Bureau of Sri Lanka, Institute of Bankers of Sri Lanka and BOC Travels (Pvt) Ltd.

Ms. Nalani was a co-winner of the “Zonta Award for Excellence” in the Banking category for the year 2009.

J G B P Tissera

- is a Fellow member of the Association of International Accountants UK, Fellow member of the Association of Company Accountants, UK. He holds an Executive Diploma in Business Administration from the University of Colombo and also holds a Masters in Business Studies from the University of Colombo.

He had a distinguished career in the financial sector and has over 30 years senior executive experience with a wide and varied knowledge both in the public and private sector organizations and has worked overseas for over 9 years with a reputed firm of Chartered Accountants. He was the Director Supervision at the Securities Exchange Commission for more than 13 years where heobtained training in the field of capital markets and represented the Commission at overseas conferences.

Mr. Tissera presently is a Management Consultant for a group of Companies.

V Kanagasabapathy

- is a Fellow Member of the Institute of Chartered Accountants of Sri Lanka. He holds a Masters Degree in Public Administration from the Harvard University. He is currently the Financial Management Advisor of the Ministry of Finance and Planning with over thirty five years of experience in the public service in several capacities.

He is the President of the Institute of Public Finance and Development Accountancy. He is also a member of the Governing Council of the Association of Accounting Technicians of Sri Lanka and Chairman of the Board of Directors of Distance Learning Centre.

He is on the directorate of several Public Enterprises and Government linked Companies such as Hotel Developers Lanka Ltd. and De La Rue Lanka Securities and Currency (Pvt) Ltd.

Board of Directors

6

M S S Paramananda

- Is an Accountant by profession having served the Sri Lankan government for over 25 years. Mr. Paramananda is a member of the Institute of Public Finance and Development Accountancy in Sri Lanka. He was responsible for the implementation and administration of the fiscal policy of the Government of Sri Lanka. He has specialised in foreign funding management and regulating financial policies of ministries and public enterprises.

His practical knowledge is enriched by hands - on engagements with ADB, JBIC funded development projects of the State.

P G Rupasinghe

- holds a Special Degree in Economics, a Post Graduate Diploma in Advanced Social Statistics from the University of Sri Jayawardenapura and a Masters Degree in Business Administration (MBA) from the Post Graduate Institute of Management (PIM).

Mr. Rupasinghe was a former Chairman of National Institute of the Business Management (NIBM) and a Consultant to the Industrial Development Authority of the Western Province. Mr. Rupasinghe has also functioned as a Senior Research Officer at DFCC Bank and has over 23 years experience in project appraisal, project monitoring, economic research, consultancy, planning & branch banking. He has 07 years of post graduate teaching experience in Economics, Accounting and Management at the Open University of Sri Lanka.

Mr. Rupasinghe is also a member of the Provincial Public Service Commission (WP). He is a Director & Trustee of the National Development Trust Fund under the Ministry of Finance and a member of the Na-tional Sports Council of Sri Lanka.

Lakshman Perera

- He is a Graduate of the University of Peradeniya and holds a Post Graduate Diploma in International Affairs and a Masters Degree in Business Administration. He played a pivotal role in partnering the progress and development of the Institute of Chartered Accountants of Sri Lanka as the Secretary and the CEO, for a period of over twodecades, to the position it holds today.

He also served the South Asian Federation of Accountants (SAFA) an apex body of SAARC, comprising of National Professional Accountancy Bodies in Bangladesh, Pakistan, India, Sri Lanka and Maldives as Executive Secretary for two terms and was responsible for networking the activities of SAFA during this period.

He was a Member of the Graduate Faculty Board of the University of Colombo and also functioned as a member of the Committee appointed by the Securities and Exchange Commission of Sri Lanka to formulate Corporate Governance Rules for listed companies.

He was a key player in establishing the Masters Degree Programme at the Institute of Chartered Accountants in collaboration with the University of Southern Queensland, Australia.

7

8

ReviewSince our inception, nearly 28 years ago, we considered external calamities as opportunities,viewing them as catalysts for internal adjustments.

Your Company has consistently demonstrated unique ability to remain flexible, yet strong, open to novelty whilst being in total control.

Once again, we managed to close a tough year quite successfully.

In fact, we look forward to more challenges in future as they bring the best in us, we never thought possessed...

Chairman’s

9

Dear shareholder,

It is with pleasure, that I write to you with the results of your Company for the year 2009.

Saddled between two diametrically opposite, but evenly negative environs: namely war and downturn, your Company not only performed successfully, but also enhanced brand visibility, adding more value to your stock.

As the global financial crisis started to reveal itself vividly, stock markets around the world began to fall, and large financial institutions collapsed. Governments of even the wealthiest nations had to come up with rescue packages to bail out their financial systems. The situation was so serious many nations whether wealthy and industrialised, or poor and developing, began sliding into recession.

With the end of civil conflict, Sri Lankan economy, which was gloomy, catapulted into one of the vibrant economies in Asia. The rejuvenated investor confidence from the world over augured well for the country as the much belated development programs got underway, heralding an era of rebuilding. The economic growth that slowed down in the first half of the year picked up in the second and inflation dwindled to a single digit.

The economy is expected to grow steadily in 2010 while imports and exports are expected to increase generating higher economic activity. Your Company will be able maximize gains from these opportunities for business development.

Rehabilitation of ailing companies:

Besides driving the Company towards prosperity, we had to step in when the catastrophes befell on others. But, I am glad that those events brought the best in us at a time when the odds were really against us.

We set out to restructure and rehabilitate ailing businesses to safeguard public depositors and also to secure hapless employees. Today, we are proud to have turned these, loss - making businesses around to be more viable entities recording profit, whilst managing liquidity issues successfully.

Calamity caused by these companies presented MBSL an opportunity to showcase its inherent strengths in restoring endangered businesses. This brought our core attributes to the fore to play the role of a Merchant Bank per se, to establish stability and help stabilise country’s financial system. Our timely commitment secured LKR 50 billion public deposits and over 5,000 employees who were destitute.

Despite the raging conflict during the early part of the year and the global economic melt-down which was beyond control, MBSL recorded it’s highest ever income of LKR 1.2 billion with a 11.6% increase over the past year and the Profit before Tax rose by 25%. Our subsidiary, MCSL also completed the year 2009 very successfully recording remarkable growth in all indicators. Revenue was increased by 34% to LKR 820 million, and the Deposit Base reached the LKR 3 billion mark, highlighting the customer confidence. MBSL Group collectively achieved substantial growth in revenue and profit.

Looking ahead…

Now that the country has settled down and on the mend, the entire world is looking towards us with envy. Sri Lankan Stock Exchange has become an attractive investment centre and all indices are showing growth and promise.

As a result, North and East have become the focal point of accelerated development and we foresee many opportunities. From macro to grass root level, investors will require funding for their enterprises, thus spells the business potential for MBSL in the near future: the most visible and respected merchant bank in the country. To make access easier to our potential customers, we have already started expansion of our branch network. We have already implemented our diversification plans.

10

Be it government sponsored or privately funded the need for cash infusion will be of paramount importance. Revival of north will require capital infusion, and MBSL with an extensive lending portfolio and expertise can be of immense assistance to the development drive of the nation.

We are also planning to actively promote our diversification plans to maximize future gains. As a pilot project of our diversification programme, we recently laid the foundation stone for a 3 star hotel project in the city of Nallur, in the Jaffna peninsula.

I am fully content that we have the right personnel, resources and the mechanisms to synergize the dynamics in a significant scale. I am optimistic that we will be able to post more sparking results this year, and look forward to meet you at our next general meeting.

Finally, I would like to thank my esteemed colleagues on the Board and Mr. Gamini Karunathilake CEO for their support, our staff for their diligence and especially our shareholders who kept their faith in us.

Janaka RatnayakeChairman

11

12

13

and respond with positive solutions...

CorporateManagementRanjith SiriwardenaDeputy DirectorStrategic Planning, & Risk Management.

- holds a B.Sc (Business Administration) Degree from the University of Sri Jayawar-denapura and is an Associate member of the Institute of Chartered Accountants of Sri Lanka. He has over 18 years experience in merchant bank-ing, strategic planning and risk management.

He also serves as a Director of Lanka Securities (Pvt) Limited and MBSL Savings Bank Limited.

Senaka UduwawelaAssistant Director - Leasing& Administration

- accounts for over 26 years of experience in the banking industry. His areas of speciality cover credit and branch opera-tions. He currently supervises collections and recoveries of the leasing division and branches.

A M A CaderDeputy DirectorCorporate Advisory & Capital Markets

- is a Fellow of the Chartered In-stitute of Management Accoun-tants FCMA,United Kingdom and holds two Post graduate Diplomas in Business Adminis-tration and Economics from the University of Colombo. He also holds a Post Graduate Diploma in Information Technology from CIMA and SLIIT. He has over 30 years experience in a wide range of Corporate Advisory/ Capital Market activities.

Gamini KarunathilakeChief Executive Officer

- is a professional banker with over 30 years of experience. He obtained a B.Com (Hon) Degree from the University of Sri Jayawar-denapura and MBA from the Post Graduate Institute of Management (PIM) of Sri Lanka. He is a fellow member of the Institute of Bankers of Sri Lanka, and was a visiting lecturer on ‘ Law and Practise of Banking’ for Bachelor of Com-merce and Economics Degree programmes and on ‘Banking and Finance’ for MSc. Management Programme at the University of Sri Jayawardenapura. He also served as a lecturer and Chief Examiner on ‘Law and Practice of Banking’ and ‘Practice of Banking’ at the Institute of Bankers of Sri Lanka. He is also a Director of Merchant Credit of Sri Lanka Ltd..

1

23

4

56

7

8

9

From left:1. A.M.A.Cader, 2. Gamini Karunathilake, 3. Ranjith Siriwardena, 4. Senaka Uduwawela,5. Marina Phillips, 6. Shyamalie Amaratunge, 7. Priyantha Herath, 8. Lakshman Kaluarachchi, 9. Amitha Samarasinghe.

14

Shyamalie AmaratungeDeputy DirectorTrade Finance

- holds a B.Com Special Degree and a Post Graduate Diploma on Modern Banking from the University of Sri Jayawardenapura and obtained an MBA from the Post Graduate Institute of Management of Sri Lanka. She also counts over 16 years experience in Trade Finance, Treasury Management, Strategic Planning, Balanced Score Card (BSC) Performance Management and accountancy.

Lakshman KaluarachchiDeputy DirectorLeasing

- is a holder of a B.Com Special Degree from the University of Kelaniya and has over 23 years experience in leasing and presently overlooks the marketing and branch operations.

Priyantha HerathAssistant DirectorFinance & Treasury Management

- is an Associate member of the Institute of Chartered Accountants of Sri Lanka and an Associate member of the Certified Management Accountants of Sri Lanka.

He holds a B.Sc (Business Administration) Degree from the University of Sri Jayawardenapura, and MBA from the University of Colombo,Sri Lanka.

He counts over 10 years of experience in the field of finance. He also serves as a Director of MBSL Insurance Company Limited.

Amitha SamarasingheAssistant Director - Group Human Resources

- holds a Bachelor of Arts Degree from University of Peradeniya and a Diploma in Human Resources from the National Institute of Business Management. She is a member of the Institute of Personal Management.

She possesses over 25 years of experience in the field of Human Resource Manage-ment in diverse businesses such as manufacturing, service and banking.

Marina PhillipsAssistant DirectorCompany Secretary -MBSL Group

- is an Attorney -at -Law, Notary Public,with over 16 years of experience in all aspects of corporate secretarial practise.

She is also widely experienced in capital market operations.

15

16

MBSL mounted strong resilience to the deteriorating economic environment and weakening currency.

We tested our strengthsin the toughest of conditions,and emerged strong.

Strategic Brand realignment, service differentiation,geographic diversification...and most importantly our true corporate citizenship, brought us and the customer more and more closer... and that helpedincrease business volume.

Mn.

Mn.

Mn.

17

Chief Executive Officer’s

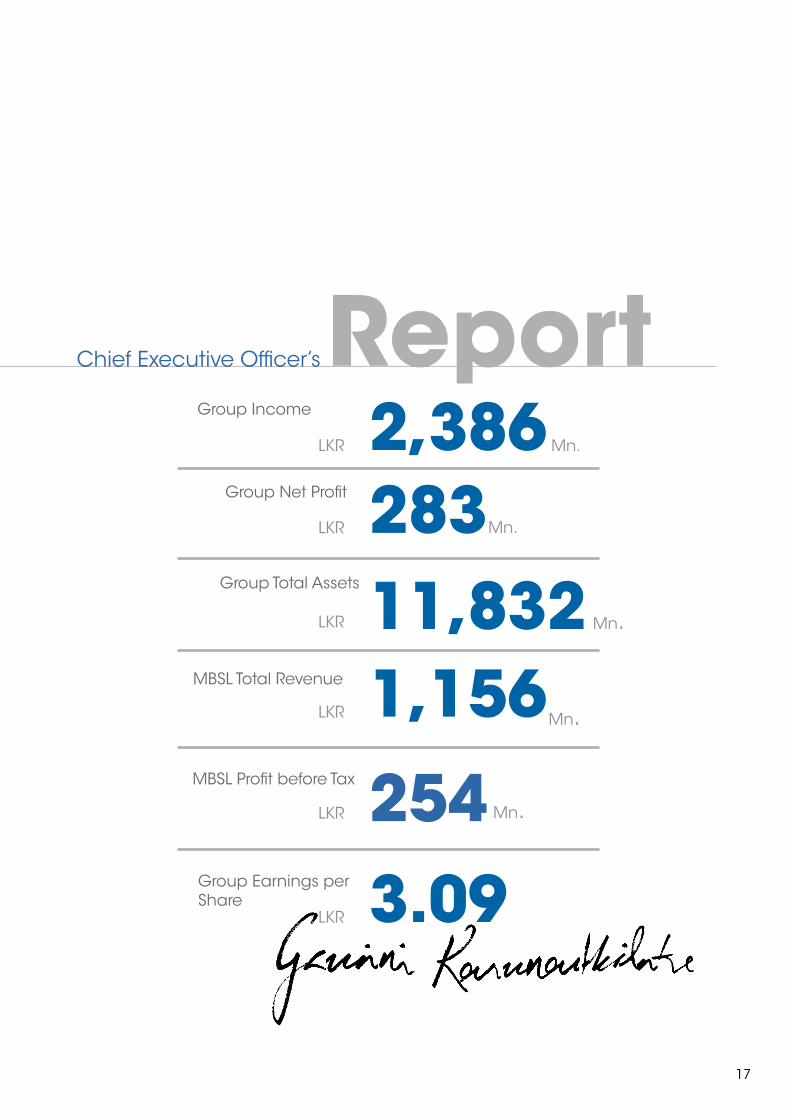

Group Income

Group Net Profit

MBSL Total Revenue

MBSL Profit before Tax

Group Earnings per Share

Group Total Assets

LKR

LKR

LKR

LKR

LKR

LKR

Mn.

Mn.

2,386283

1,156

2543.09

11,832

Report

Direct interaction -

Staff members actively promoting our products

and services...

18

It is with great pleasure that I meet you once again, to illustrate the performance details of your Company in the year 2009.

As you are aware that in the global scenario, year 2009 dawned with uncertainty. Ramifications of global meltdown were still unfolding and cohesive solutions were few and far apart. Though there were no direct effect on Sri Lankan financial industry the adverse impact on the economy was somewhat unsettling. Many top dollar earning businesses such as tea, garments, gems and non - traditional exporters suffered heavily, and the dollar influx dwindled considerably. Raging conflict in the northern zone reached a critical stage where inflation rose and reserves declined. Financial flows to the private sector diminished mainly due to the drying – up of credit lines in the aftermath of global slowdown.

Sri Lanka faced a historic opportunity to evolve from a lower-income country mired in conflict, to a middle-income country in lasting peace. Until now, Sri Lanka’s growth had been constrained by three decades of conflict despite the country’s highly educated population. The ending of the armed conflict in 2009 provided an opportunity for the country to embark on reforms and work with the private sector to establish a more dynamic and vibrant economy.

With the end of conflict, vast areas in the North and East of the country, neglected for nearly a quarter-century, stand to receive a considerable positive stimulus. Peace is widely expected to inject new life into the tourism sector, which until now could not reap its full potential. The country also stands to attract more Foreign Direct Investment especially from the burgeoning business process-outsourcing sector (BPO), which holds considerable promise. Sri Lanka is on track to achieve most Millennium Development Goals by 2015, but will need to focus on achieving quality, relevance and sustainability in key public services.

Also, 2009 was an extremely challenging year for banking industry and the preven-tive measures taken over the past few years by the regulator helped to deal with situation when it occurred. Sri Lanka’s banks had a capital adequacy ratio of over 14% that helped to negate the shock. The situation during first two quarters was so tense; not only businesses, but also even general public were intensely watching the unfolding events. The incensed battle, security restrictions on movement, credit squeeze, reduced exports and imports, high tariff added with high interest rates, low repayment capacity virtually brought the country to a stand still.

Saddled within these constrains, your Company managed to perform beyond expectations. The year 2009 also revealed the real Brand Strength of MBSL. The opportunity came with a rather sad occurrence. The flimflam of several miscreant financiers shook the very fundamentals of corporate governance, and if you will, common decency too.

Central Bank of Sri Lanka sought the assistance of MBSL to play the role of the managing agent to several crisis ridden financial institutions. Plans were formulated to support restoration programs which, were successfully implemented under the guidance and supervision of MBSL.

Our action staved off the collapse of financial industry that could otherwise have snowballed into a nasty economic tsunami. We successfully turned several companies around that were on the brink of an abyss, back to sound financial footing. The moral satisfaction, besides professional fulfillment makes us content that we have acted decisively, and decently as our profession propagate. While we indulge ourselves with fulfillment, we believe that the glory rests entirely with you, the stakeholders of MBSL. You are the core strength that gave us confidence to move forward.

This exercise brought our corporate citizenship out in a specific relief

The public perception on MBSL escalated to a level of admiration as a savior. Despite the ongoing conflict during the early part of the year and uncontrollable global economic downturn, your Company recorded it’s highest ever income of LKR 1.2 billion with an 11.6% increase over

Helping hand -

Scholarship to the children of deceased war heros...

19

the past year and the profit before tax rose by 25%. Total Equity Capital escalated by 39% to record LKR 2.3 billion and Total Assets swelled to LKR 5.6 billion, recording 17% growth over the previous year. The Group in its entirety achieved substantial growth in revenue and profit. The income grew to LKR 2.4 billion; a 45% surge and the profit grew by 26% to LKR 283 million. Total Assets stood at LKR 11.8 billion registering a 60% growth over the last year.

The significant expansion of Group turnover in the year 2009 was due to addition of two subsidiaries to the Group in line with strategic direction of the Strategic Plan for 2010 - 2015. Bank diversified its business activities to the insurance industry by acquiring ABC Insurance Ltd, which was an “Ailing Company” with a view of rehabilitating it. During the year 2009, we streamlined its policies, procedures and products and converted to a profitable entity. This company is now ready to take-off and more benefits are expected during this year.

Your Company also made a strategic investment in Ceylinco Savings Bank, now known as MBSL Savings Bank, which was the only private sector savings bank in Sri Lanka registered under Banking Act as a Licensed Specialized Bank. This institution too was severely affected by the liquidity crises that arose due to loss of reputation during the 1st quarter of year 2009.

As noted above, your Company was able to arrest the situation immediately, with the support of the regulator; the Bank was converted into a viable entity within a short span of time. The bank is now on the path for sustainable growth, consciously seeking to meet regulatory compliances. We are confident that the bank will become a strong private sector savings bank under the umbrella of the MBSL Group. Human Resource Development is the bedrock of your Company, and strives to create a healthy work environment where all employees have fair opportunity to maximize their professional and personal potential. We have defined the HR Vision and Objective, based on the pertinent factors to develop our human resource base and to elevate your Company to be a role model in human resource evolution, and deploy competent personnel into work environments where they are motivated to achieve the organisational goals, whilst expanding their personal frontiers. The year under reference witnessed a new resurgence in the two major areas of Human resource development and its utilization. With the improved financial performance, your Company was able to adopt and implement staff development programs on a continuous and meaningful basis. Both, as a motivational measure and as a skill development process, arrangements were also made for the staff to undergo Foreign training programs in addition to local training programs.Continuation of bi-annual Performance Appraisal System also enabled to develop the staff on a more consequential basis as well as to implement and monitor the progress of Bank’s major work plans. The signing of the collective agreement with the Bank’s Union for a ‘Per-formance based Annual Increment’ formula was a significant event during the year.

Sri Lanka has now entered a low inflation, low interest regime that provide growth prospects for the economy. Imports and exports are expected to grow in the year 2010, generating higher economic activities and income. The average growth in broad money supply is also expected at 14.5%, a level sufficient to facilitate smooth function-ing of economic activities.

Your Company plans to intensify capital market operations to maximize on opportunities in the present surge in the Stock Market. Fee based activities are expected to generate substantial income to the Company’s bottom line.

Consequent to cessation of hostilities in the north and eastern region, a dramatic boom is expected with the restoration programs that are forthcoming. Economy at all levels will expand when new industries; be it macro or micro commerce. Needs for capital infusion, leasing, corporate advisory and secretarial services in these ventures will be astounding, and your Company is comfortably placed to assist them in these spheres of business.

Year 2009 was a fulfilling year professionally and morally. Our team performed as usually expected and beyond. Your Company also changed its character from a merchant banker to a more varied service provider. The diversification has moved us into new areas i.e. insurance, savings banking and to hospitality industry. The first step in that direction was the laying of foundation for a three star hotel in Jaffna peninsula.

Our decisive intervention prevented the domino effect that could have snowballed into an economic avalanche...

20

We will continue to extend our provincial reach through the expansion of our branch network, the most recent additions being the branches opened in Trincomalee and Ambalantota.

Our achievements would not have been possible if not for the stewardship of the Chairman, Mr. Janaka Ratnayake and the astute support of the Board of Directors. I offer my sincerest thanks to them for their prudent counsel in chartering your Company’s progress, and especially our shareholders for their confidence in us and my sincere gratitude is extended to our loyal customers for giving us an opportunity to serve them.

Finally, my staff that wholeheartedly challenged the impossible to finish the year 2009 in an astounding success. Their commitment not only beat the odds, but also brought out several performers who are assuredly leadership material, whose contributions will augur well for your Company in the years to come.

Gamini KarunathilakeChief Executive Officer

21

Management

Amitha Mihirun Ratnasiri Keerthi Snr. Manager Snr. Manager Snr. Manager Snr. Manager Trade Finance Legal Galle Kandy

Pathirana Ananda Sarath Lalangi Manager Manager Manager Manager Leasing Legal Leasing Corporate Advisory

Sanjaya Fahima Chinthaka Asela Snr. Manager Manager Manager Manager Leasing Legal IT Finance & Treasury

Saman Janaka Manager Manager Kurunegala Maharagama

22

23

with carefully articulated solutions to restore ...

Management Discussion & Analysis

Profit(Group)

LKR

. Mn.

05 06 07 08 09

176

264

224

283

225

Turnover (Company)

LKR

. Mn.

05 06 07 08 09

539

873

1,03

5

1,15

6

704

24

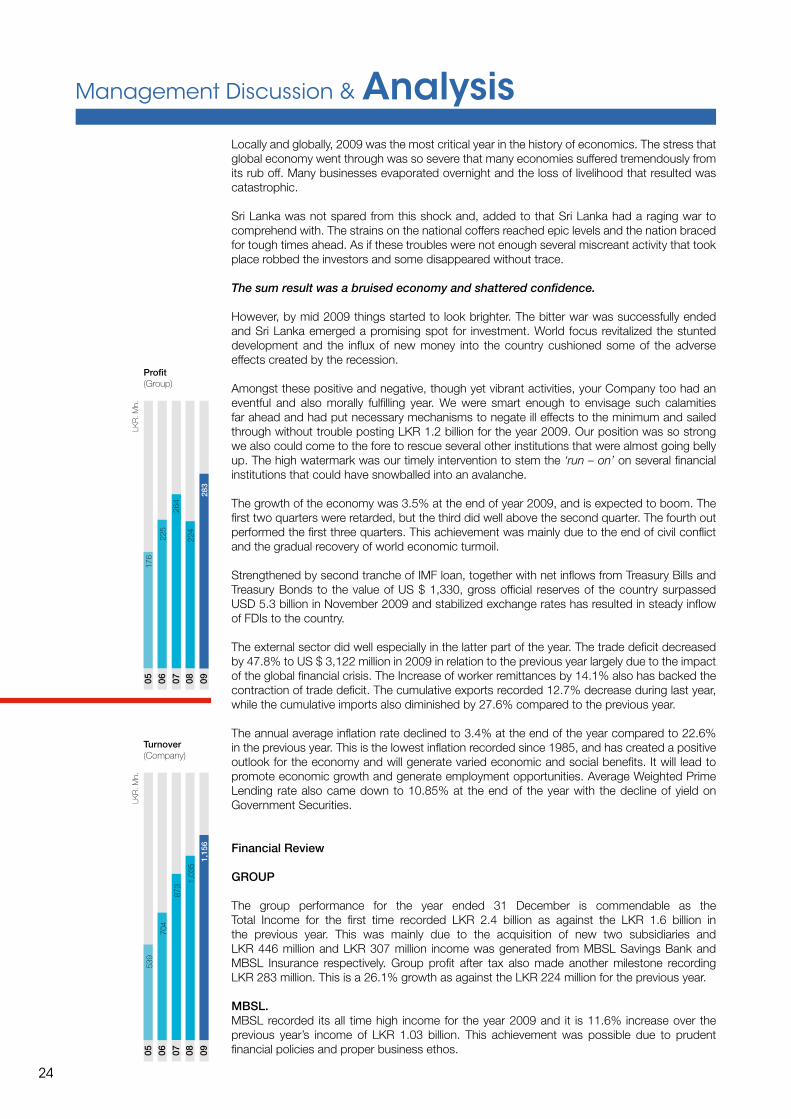

Locally and globally, 2009 was the most critical year in the history of economics. The stress that global economy went through was so severe that many economies suffered tremendously from its rub off. Many businesses evaporated overnight and the loss of livelihood that resulted was catastrophic.

Sri Lanka was not spared from this shock and, added to that Sri Lanka had a raging war to comprehend with. The strains on the national coffers reached epic levels and the nation braced for tough times ahead. As if these troubles were not enough several miscreant activity that took place robbed the investors and some disappeared without trace.

The sum result was a bruised economy and shattered confidence.

However, by mid 2009 things started to look brighter. The bitter war was successfully ended and Sri Lanka emerged a promising spot for investment. World focus revitalized the stunted development and the influx of new money into the country cushioned some of the adverse effects created by the recession.

Amongst these positive and negative, though yet vibrant activities, your Company too had an eventful and also morally fulfilling year. We were smart enough to envisage such calamities far ahead and had put necessary mechanisms to negate ill effects to the minimum and sailed through without trouble posting LKR 1.2 billion for the year 2009. Our position was so strong we also could come to the fore to rescue several other institutions that were almost going belly up. The high watermark was our timely intervention to stem the ‘run – on’ on several financial institutions that could have snowballed into an avalanche.

The growth of the economy was 3.5% at the end of year 2009, and is expected to boom. The first two quarters were retarded, but the third did well above the second quarter. The fourth out performed the first three quarters. This achievement was mainly due to the end of civil conflict and the gradual recovery of world economic turmoil.

Strengthened by second tranche of IMF loan, together with net inflows from Treasury Bills and Treasury Bonds to the value of US $ 1,330, gross official reserves of the country surpassed USD 5.3 billion in November 2009 and stabilized exchange rates has resulted in steady inflow of FDIs to the country.

The external sector did well especially in the latter part of the year. The trade deficit decreased by 47.8% to US $ 3,122 million in 2009 in relation to the previous year largely due to the impact of the global financial crisis. The Increase of worker remittances by 14.1% also has backed the contraction of trade deficit. The cumulative exports recorded 12.7% decrease during last year, while the cumulative imports also diminished by 27.6% compared to the previous year.

The annual average inflation rate declined to 3.4% at the end of the year compared to 22.6% in the previous year. This is the lowest inflation recorded since 1985, and has created a positive outlook for the economy and will generate varied economic and social benefits. It will lead to promote economic growth and generate employment opportunities. Average Weighted Prime Lending rate also came down to 10.85% at the end of the year with the decline of yield on Government Securities.

Financial Review

GROUP

The group performance for the year ended 31 December is commendable as the Total Income for the first time recorded LKR 2.4 billion as against the LKR 1.6 billion in the previous year. This was mainly due to the acquisition of new two subsidiaries and LKR 446 million and LKR 307 million income was generated from MBSL Savings Bank and MBSL Insurance respectively. Group profit after tax also made another milestone recording LKR 283 million. This is a 26.1% growth as against the LKR 224 million for the previous year.

MBSL.MBSL recorded its all time high income for the year 2009 and it is 11.6% increase over the previous year’s income of LKR 1.03 billion. This achievement was possible due to prudent financial policies and proper business ethos.

Profitbefore Tax(Company)

LKR

. Mn.

05 06 07 08 09

187

273

203

25426

9

GroupEarnings per Share

LKR

.

05 06 07 08 09

2.80 2.

94

2.49

3.09

2.50

25

During the year, the company earned LKR 33 million from the business rehabilitation activities carried out by the Business Rehabilitation Unit. Having noticed the expertise displayed by the MBSL in managing F & G group, the Central Bank of Sri Lanka offered us the management of several ailing companies. Within less than twelve months of the undertaking, we were able to turn these companies around from dire straits.

Interest income of LKR 982 million represents 85% of the company’s total income and it is slightly above the previous year’s LKR 967 million.

Profit before tax indicate a 25% increase over the previous year even though the profit after tax recorded a marginal decrease of 2% over the previous year due to high income tax burden that prevailed in the country.

Earnings per Share The Earnings per Share (EPS) for the year is LKR 2.19, which is a decrease of 3.7% compared to the previous year. This is due to issue of 1 for 2 rights issue that was concluded in December 2009 and the time left was insufficient to generate an additional return for the increased capital. However, the Group Earnings per Share increased to LKR 3.09 from LKR 2.49 in 2009.

Net Interest Income Net interest income was LKR 398 million for the year, compared to LKR 420 million previous year. The marginal decrease of 5% compared to the previous year was primarily due to the increase in borrowing costs, as a result of strategic investments made during the year.

Operating Expenses As against previous year, the operating expenses excluding provisioning for loan losses increased marginally 7.2 % in 2009. The main contributory factors for this increase were increase of value added tax on financial services and provision for retirement benefit obligation. Personnel costs also have increased due to the ongoing processes adopted for consolidating current human resource. Increase in other expenses is in line with the increase income of the company. However, your Company reviews and carefully adopts cost optimization mechanisms in line with its revenue.

Provision for Bad and Doubtful DebtsDuring last year MBSL changed its provisioning policy of leasing to comply with the Central Banks direction No. 2 of 2006, and there were no significant impact to the brought forward provisions. In addition to the provisions required by the Central Bank, a general provision of .5% is provided annually until it reaches 2.5% of the net portfolio to meet the future contingencies, which might arise due to the market uncertainties.

Your Company’s main policy is to increase its disbursements while maintaining a healthy portfolio. During the year the lending portfolio increased by 4.2%, representing 73.5% of the total assets. The total provision as at the end of 2009 stood at 6.5% of the total portfolio compared to 8% of the previous year.

TaxationThe Bank’s corporate tax expense for the year was LKR 53 million against the marginal reversal in the previous year. Main reason for this was decrease in leasing disbursements compared to hire purchase disbursements.

Shareholder Equity and ReturnsTotal equity of the Shareholders increased by 38.8% to LKR 2.33 billion as a result of 1 for 2 rights issue offered during the year. The Company’s Return on Equity decreased to 11.1 % compared with 12.21 % in 2008 and Directors have recommended LKR 0.75 as dividends for the year ended 31 December 2009. Price earnings ratio at the end of year was 8.89 adding a substantial value to the shareholders’ investments.

Dividend DistributionDirectors have recommended LKR 0.75 per share first and final dividend for the year 2009. The dividend payout as a percentage of the Company’s own profit after tax is 50.4%. The Directors have recommended this dividend taking into consideration the sustained profitability and liquidity of the Company.

ShareholdersFund (Company)

LKR

. Mn.

05 06 07 08 09

1,27

4

1,56

5

1,68

0

2,33

1

1,41

6

Total Assets(Company)

LKR

. mn.

05 06 07 08 09

3.,2

73

4,40

4 4,76

8

5,57

9

3,50

4

26

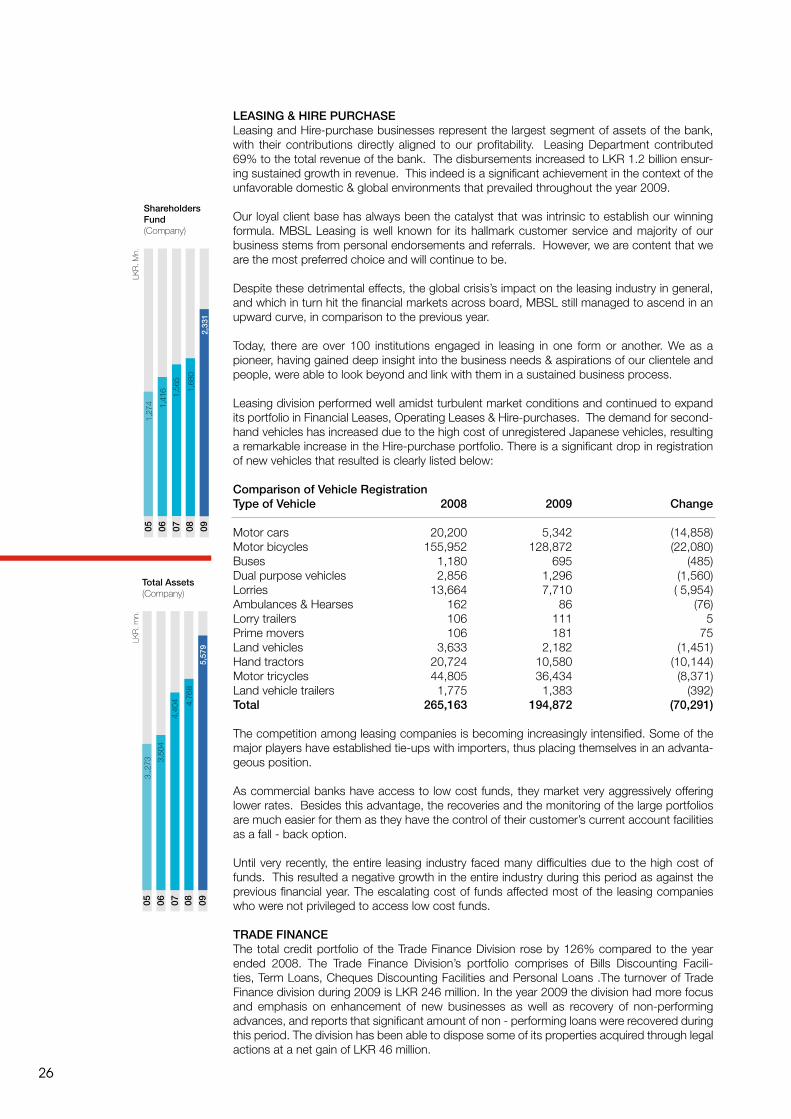

LEASING & HIRE PURCHASELeasing and Hire-purchase businesses represent the largest segment of assets of the bank, with their contributions directly aligned to our profitability. Leasing Department contributed 69% to the total revenue of the bank. The disbursements increased to LKR 1.2 billion ensur-ing sustained growth in revenue. This indeed is a significant achievement in the context of the unfavorable domestic & global environments that prevailed throughout the year 2009.

Our loyal client base has always been the catalyst that was intrinsic to establish our winning formula. MBSL Leasing is well known for its hallmark customer service and majority of our business stems from personal endorsements and referrals. However, we are content that we are the most preferred choice and will continue to be. Despite these detrimental effects, the global crisis’s impact on the leasing industry in general, and which in turn hit the financial markets across board, MBSL still managed to ascend in an upward curve, in comparison to the previous year.

Today, there are over 100 institutions engaged in leasing in one form or another. We as a pioneer, having gained deep insight into the business needs & aspirations of our clientele and people, were able to look beyond and link with them in a sustained business process.

Leasing division performed well amidst turbulent market conditions and continued to expand its portfolio in Financial Leases, Operating Leases & Hire-purchases. The demand for second-hand vehicles has increased due to the high cost of unregistered Japanese vehicles, resulting a remarkable increase in the Hire-purchase portfolio. There is a significant drop in registration of new vehicles that resulted is clearly listed below:

Comparison of Vehicle RegistrationType of Vehicle 2008 2009 Change

Motor cars 20,200 5,342 (14,858)Motor bicycles 155,952 128,872 (22,080)Buses 1,180 695 (485)Dual purpose vehicles 2,856 1,296 (1,560)Lorries 13,664 7,710 ( 5,954)Ambulances & Hearses 162 86 (76)Lorry trailers 106 111 5Prime movers 106 181 75Land vehicles 3,633 2,182 (1,451)Hand tractors 20,724 10,580 (10,144)Motor tricycles 44,805 36,434 (8,371)Land vehicle trailers 1,775 1,383 (392)Total 265,163 194,872 (70,291) The competition among leasing companies is becoming increasingly intensified. Some of the major players have established tie-ups with importers, thus placing themselves in an advanta-geous position.

As commercial banks have access to low cost funds, they market very aggressively offering lower rates. Besides this advantage, the recoveries and the monitoring of the large portfolios are much easier for them as they have the control of their customer’s current account facilities as a fall - back option.

Until very recently, the entire leasing industry faced many difficulties due to the high cost of funds. This resulted a negative growth in the entire industry during this period as against the previous financial year. The escalating cost of funds affected most of the leasing companies who were not privileged to access low cost funds.

TRADE FINANCEThe total credit portfolio of the Trade Finance Division rose by 126% compared to the year ended 2008. The Trade Finance Division’s portfolio comprises of Bills Discounting Facili-ties, Term Loans, Cheques Discounting Facilities and Personal Loans .The turnover of Trade Finance division during 2009 is LKR 246 million. In the year 2009 the division had more focus and emphasis on enhancement of new businesses as well as recovery of non-performing advances, and reports that significant amount of non - performing loans were recovered during this period. The division has been able to dispose some of its properties acquired through legal actions at a net gain of LKR 46 million.

27

The Trade Finance Division continues to make significant contributions towards the profitability of your Company and to develop the Trade Finance portfolio with strict evaluation guidelines. In addition to these measures, prudent provisioning has been the focus on all on-going businesses. The division is expected to bring more results in the coming year owing to enhancement of credit portfolio, recovery of balance non-performing loans and on realization of investment in properties.

CORPORATE ADVISORY & CAPITAL MARKETThough the Corporate Advisory & Capital Markets Division (CA&CM) is functioning in a very dynamic environment in its core activities, the division recorded impressive results during the year 2009 recording a total revenue of LKR 44 million with a profit growth of 100 percent in keep-ing with the right balance between the division’s fee based and fund based activities.

Among the key projects concluded during the year by the division, the Initial Public Offering of Renuka Agri Foods Ltd, “a local global success story” was oversubscribed by more than 12 times which was the first ever IPO after eighteen months lapse of IPOs in the Colombo bourse. Investor categories ranged from high-net-worth investors with strategic interest and retailers with a capital gain motive.

A Business plan consultancy was carried out for a local budget airline to develop turnaround strategies and to provide a future direction for the senior management of the Airline. At present the division is carrying out another Business Plan for a public utility entity for a time span of five years. With the upturn in the capital market and deal flows improving, the division was able to conclude two independent advisory reports and a mandatory offer successfully. The CA&CM continued to conduct several awareness programs on diverse topics of interest on rehabilitation of ailing businesses, ethics and governance and cost management strategies. Many participants from different segments of the Corporate to general public attended the seminars.

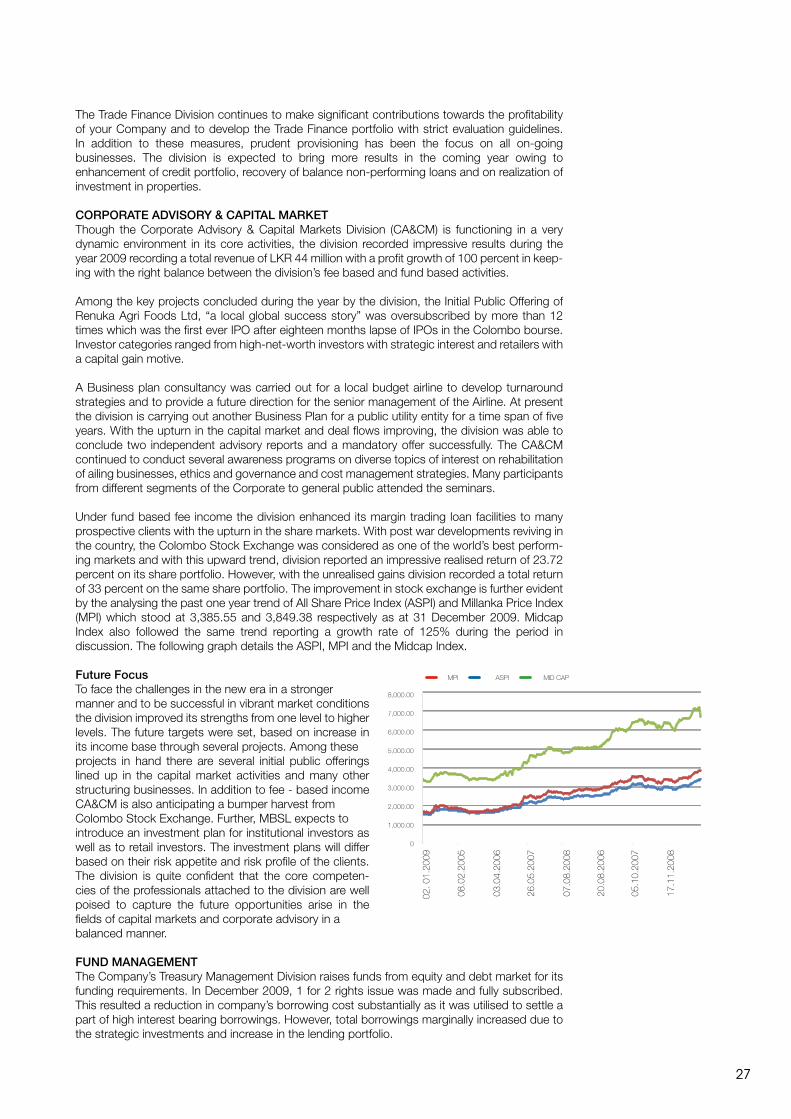

Under fund based fee income the division enhanced its margin trading loan facilities to many prospective clients with the upturn in the share markets. With post war developments reviving in the country, the Colombo Stock Exchange was considered as one of the world’s best perform-ing markets and with this upward trend, division reported an impressive realised return of 23.72 percent on its share portfolio. However, with the unrealised gains division recorded a total return of 33 percent on the same share portfolio. The improvement in stock exchange is further evident by the analysing the past one year trend of All Share Price Index (ASPI) and Millanka Price Index (MPI) which stood at 3,385.55 and 3,849.38 respectively as at 31 December 2009. Midcap Index also followed the same trend reporting a growth rate of 125% during the period in discussion. The following graph details the ASPI, MPI and the Midcap Index. Future FocusTo face the challenges in the new era in a stronger manner and to be successful in vibrant market conditions the division improved its strengths from one level to higher levels. The future targets were set, based on increase in its income base through several projects. Among these projects in hand there are several initial public offerings lined up in the capital market activities and many other structuring businesses. In addition to fee - based income CA&CM is also anticipating a bumper harvest from Colombo Stock Exchange. Further, MBSL expects to introduce an investment plan for institutional investors as well as to retail investors. The investment plans will differ based on their risk appetite and risk profile of the clients. The division is quite confident that the core competen-cies of the professionals attached to the division are well poised to capture the future opportunities arise in the fields of capital markets and corporate advisory in a balanced manner.

FUND MANAGEMENTThe Company’s Treasury Management Division raises funds from equity and debt market for its funding requirements. In December 2009, 1 for 2 rights issue was made and fully subscribed. This resulted a reduction in company’s borrowing cost substantially as it was utilised to settle a part of high interest bearing borrowings. However, total borrowings marginally increased due to the strategic investments and increase in the lending portfolio.

02. 0

1.20

09

08.0

2.20

05

03.0

4.20

06

20.0

8.20

06

26.0

5.20

07

05.1

0.20

07

07.0

8.20

08

17.1

1.20

08MPI ASPI MID CAP

8,000.00

7,000.00

6,000.00

5,000.00

4,000.00

3,000.00

2,000.00

1,000.00

0

28

During the year most of the high interest bearing borrowings was replaced with low interest borrowings and at the end of the year the debt equity ratio was 1.17 times.

CORPORATE SECRETARIALIn addition to providing secretarial services to the Company, the division also extends its services to the subsidiaries of Bank of Ceylon (BOC) and to those of MBSL including the recently acquired companies: MBSL Insurance Co. Ltd and MBSL Savings Bank Limited. The Division has also extended its services to many external clients during the year.

Amongst the more significant activities carried out by the Division during the year under review are; functioning as registrars and secretaries for the MBSL Rights Issue held in December, acting as registrars for BOC Debenture Issue of 2008/2013, management of share ledgers including the payment of dividends to shareholders of Merchant Bank of Sri Lanka PLC and Property Development PLC, to name a few.

Whilst actively striving to expand its clientele, the Division also intends to make use of opportu-nities created by the positive trends in the present Stock Market with the aim of increasing the overall revenue of the Company.

SUBSIDIARIES AND ASSOCIATESMerchant Credit of Sri Lanka LimitedThe company’s first subsidiary Merchant Credit of Sri Lanka, which is jointly owned by BOC and MBSL performed well during the year expanding its business activities in leasing & hire purchase, trade finance and real estate businesses. The total income grew by 33.9% to LKR 820 million from LKR 612 million in the previous year. MCSL has registered Profit after tax of LKR 70.8 million recording 86.9% increase over the previous year.

MBSL Savings Bank LimitedYour Company acquired 78% equity stake of Ceylinco Savings Bank in April 2009 at the time when it was experiencing great financial difficulties and was renamed MBSL Savings Bank. Hav-ing accepted the challenge, MBSL management turned the position of the company around and for the year ended 31 December 2009 recorded a net profit of LKR 40 million compared to the loss of LKR 371.9 million made in the previous year.

MBSL Insurance Company Limited ABC Insurance Company Limited was acquired in April 2009 and renamed as MBSL Insurance Company Limited. Customer base has increased significantly with the relaunch of new identity and, as a result number of insurance policies has increased significantly in both life and general insurance.

Lanka Securities (Pvt) LimitedMBSL holds 29% of its associate, Lanka Securities (Pvt) Limited, and the other investors i.e. BOC and First Capital Pakistan owns 20% and 51% respectively. It engages in stock brokering activates and their performance of the year is commendable as the stock market activities out performed during the latter part of the year. The income of the company grew by 35.5% to LKR 121 million while profit after tax recorded 117% growth over the last year reaching LKR 62.5 million.

Expansion of branch networkWe at MBSL are optimistic that we could expand our business by increasing the distribution network. Our initial plan was to increase branch network to 10 during the year. However, after a careful study of the prevailing market behaviour and macro economic conditions of the country, we opened our 7th Branch, the Colombo City Office in August last year to increase the speed and efficiency of our customer service. Opening of this new City branch has brought many busi-ness opportunities and increased easy accessibility for our customers. Negombo branch, which was opened in the latter part of the previous year also, was able to become profitable during the year. MBSL opened its latest, the Trincomalee branch in January 2010 and is expected to capitalise on post war opportunities.

Diversification into new areasAlthough 2009 was a very stressful year for most of the businesses, MBSL used this opportu-nity to venture into new areas such as insurance and retail banking through acquisition of ailing

Chairman, Mr. Janaka Ratnayake opening the City

Branch with CEO, Mr. Gamini Karunathilake...

29

companies. ABC Insurance Company was a registered insurance company to do both general and life insurance. This company was undergoing financial difficulties and MBSL acquired the same recognising the ability of reviewing its business with the existing merchant banking expertise and business opportunities available within the group.

Ceylinco Savings Bank was a licensed Specialized bank operating under the troubled Ceylinco group and this bank was about to be liquidated as a result of the demand for withdrawal of the entire deposit base due to loss of public confidence. MBSL acquired this bank opening a path to access public deposits. With these two acquisitions, MBSL subsidiaries expanded to three. Since acquisition, these companies have been turned around and have started making profits, yet again endorsing MBSL’s finest management practices.

Information TechnologyHaving understood the strength of Information Technology in business and overall context, we paid close attention on developing ICT contribution in both value addition as well as security aspects. In year 2009 ICT focus was mainly concentrated on high availability of system resources with the implementation of three new servers with virtualization capability.

The Objective was to fully utilise the unused hardware resources of modern server architecture in 64-bit computing environment. Simultaneously software systems were upgraded to respective latest versions available in the industry. The Data centre was restructured to accommodate new servers and environment was designed to support servers to run 24 by 7 operations.

As an improvement, information super highway links were upgraded to 4 MB links each. Further, internal branch communication links were upgraded wherever necessary. The core application was enriched with additional features to facilitate management to make decisions and to develop businesses in a competitive and real – time environment. In addition to that, several new satellite applications were developed to enhance businesses opportunities in capital market. All workstations were brought into a single compatible environment. The newly opened branches too were linked with core application system to provide each user to work on an identical business model.

Focus: 2010Having completed 2009 successfully, we are now focused on extending growth to 2010 and beyond. For that every member from the top management down is committed on a single - minded philosophy: Sustained growth.

In that endeavour, human and technical resources are inter - aligned to withstand any and every calamity that we may have to face. We are confident that our strength lies in our ingenuity to spot opportunities and threats, well in advance and to mobilise our forces in order to maximise gains.

Risk Management

30

OverviewRisk management is plays a pivotal role in our business planning process and is strongly supported by the Senior Manage-ment and the Board of Directors. The primary objectives of the risk management are to protect the Bank’s financial strength and reputation, while ensuring that capital is well deployed to support business activities and grow shareholder value. Fur-ther, the business mix of Leasing and Hire Purchase, Trade Finance, Investments and Corporate Advisory provides a certain amount of risk diversification. The Bank’s risk management framework is based on the following principles.

– Protection of financial strength – Protection of reputation – Risk transparency – Management accountability – Independent oversight

Risk Management OversightThe prudent taking of risk on business opportunities in line with our strategic priorities is fundamental to our business as the leading Merchant Bank. To meet the challenges in fast changing financial market with new players and innovative products, we established and continuously strengthen our risk function, which is independent of but closely interacts with, the sales and trading functions to ensure the appropriate flow of information.

Risks arise in all our business activities cannot be completely eliminated, but we work to effectively manage the risk in our internal control environment. Risk management oversight is performed at several levels of the Bank, in order to ensure that risks are managed within limits set in a transparent and timely manner. Key responsibilities to manage risk lies with following management bodies and committees:

– Board of Directors responsible to shareholders for the strategic direction, supervision and control of the Group and for defining the Bank’s overall tolerance for risk. – Audit Committee is responsible for assisting the Board of Directors of the Bank in fulfilling their oversight responsibilities by monitoring management’s approach with respect to financial reporting, internal controls, accounting, and regulatory compliance. Additionally, the Audit Committee is responsible for monitoring the independence and the performance of the internal and external auditors. – Internal auditors are responsible for assisting the Board of Directors, the Audit Committee and the Management by providing an objective and independent evaluation of the effectiveness of processes and controls and, compliance on operation activities. – Chief Executive Officer and Senior Management Committee is responsible for actively managing the Bank’s businesses and its risk profile to ensure that risk and return are balanced and appropriate with current market conditions.

Risk CategoriesThe Bank is exposed to many risks and identified them under the following seven major risk categories: – Market risk – the risk of loss arising from adverse changes in interest rates, equity prices and commodity prices etc. – Credit risk – the risk of loss arising from adverse changes in the creditworthiness of counterparties. – Expense risk – the risk that the businesses are not able to cover their ongoing expenses with ongoing income excluding expense and income items already captured by the other risk categories.

– Liquidity and funding risk – the risk that the Bank is unable to fund assets or meet obligations at a reasonable price in the case of extreme market disruptions. – Operational risk – the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. – Strategy risk – the risk that the business activities are not responsive to changes in industry trends. – Strategy and Reputational risk – the risk of outcome of strategic decisions or developments and the risk that the Bank’s market acceptability or damage to our standing in the market.

Market Risk The term market risk refers to the risk of potential loss arising from adverse effects on interest rates, foreign-currency exchange rates, equity prices, and other relevant market rates and prices. At MBSL, the primary market risk is the adverse change in the interest rates. The interest rate risk exposure is managed by matching the duration of the assets and liabilities enabling to minimize the risk exposure. The mismatch risk resulting from having assets and liabilities that mature at different intervals is managed through Gap analysis.

The scenario analyses are used to estimate the potential immediate loss after stressing market parameters. These changes are modeled on past extreme events and hypothetical scenarios.

31

Liquidity and Funding RiskLiquidity and funding risk is the risk of MBSL being unable to fund assets or meet obligations at a reasonable level, in case of extreme market disruption situations. This risk is managed at the Company level, in line with our general governance principles, which allow us to specifically, tailor the approach to the individual cash flow structure within the business units. The Bank monitors the identification and measurement of this risk and works in partnership with all business units to foster sound liquidity management practices.

Credit Risk Credit risk is the possible loss being incurred as the result of a borrower or counterparty failing to meet its financial obligations. In the event of a default, a bank generally incurs a loss equal to the amount owed by the debtors, less a recovery amount resulting from foreclosure, liquidation of collateral or restructuring of the company. The credit risks taken on by the Bank are mostly collateralised and primarily of an operational risk nature.

A system of individual credit limits is the traditional means of managing credit risk and preventing risk concentrations. A set of credit limits is in place to address concentration issues in the Portfolio. The next aspect of the credit risk management frame-work at MBSL is a healthy credit risk provisioning methodology.

The business units of Bank manage credit risks through a credit appraisal and approval process,ongoing client performance monitoring and a credit quality reviewing process. Credit appraisals are prepared by experienced credit officers, based on analysis and evaluation of debtors’ creditworthiness and the type of credit transaction. Credit decisions are taken on a trans-action-by-transaction basis by Credit Committee and Board of Directors at levels appropriate to the amount and complexity of the transactions, as well as to overall exposures to borrowers and their related entities.

Operational and Legal RiskOperational risk is the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. The primary aim of operational risk management is the early identification, prevention and mitigation of operational risks, as well as in timely and meaningful management reporting.

Responsibility for operational risk management essentially lies with the business units. Senior Managers meetings take place regularly to achieve this common understanding of priorities and to foster the dialogue between the management and the business units. Knowledge and experience is shared throughout the Company to ensure a coordinated approach. Development of specific operational risk management tools began with the common definition of risk indicators at all business units. Statistical and qualitative analyses show the relevance and usefulness of individual indicators as early warning signals. The analysis of internal and external audit reports indicates that most of the audit points are of operational nature. The Bank is therefore working on improving this indicator, allowing for judgment on the respective business units’ progress in the opera-tional area.

While each business units has its own self-sufficient and specialised Legal and compliance set-up, assistance of external counsel is obtained where necessary; to make sure the proper management of the legal risk arises from inadequate documentation, inability to meet regulations, insufficient authority of customers and uncertainty in the enforcement of contracts etc.

Strategy and Reputation RiskManagement risks are difficult to quantify. While management of strategy risk is at the Board of Directors and Senior Manage-ment levels, a process has been implemented to widely capture and manage reputational risk. Strategy risk is the risk deals with changing in the business activities and its options, based on a ‘what-if’ analysis. Strategy is doing the right thing at the right time with proper and timely implementation, compatible with statutory requirements and the industry trends.

Reputation risk is the aggregation of the outcome of all risks plus other internal and external factors based on market or service image. Reputation risk may arise from a variety of sources, including the nature or purpose of a proposed transaction or service, the identity or activity of a controversial potential client, the regulatory or political climate in which the business will be transacted or significant public attention surrounding the transaction itself. Where the presence of these or other factors gives rise to potential reputation risk, the relevant business proposal or service is required to be submitted through a review process, which involves a vetting of the proposal by senior management and the Board of Directors.

32

33

and help rise on their own and proceed ...with vigor.

Continuing sustainability of the organization.

Dear Stakeholder,Having seen the back of terrorism and destruction mid last year, I feel privileged to leave a note in our Sustainability Report, promising you more and more value in the future to your stake at MBSL. We are living in turbulent times and only decisive action will propel us forward. Your Company has engaged talented personnel to scout the fields well ahead before the perils occur and plan counter action to stay afloat. Last year we did just that and also ventured into salvage others who had perished due to ill informed decisions and malpractices.

Despite that the first part of the year was not conducive for businesses due to the negative impact of world economic crisis and the intensified internal battle against terrorism, we did better throughout the year as we had adopted preemptive actions. After the end of battle in mid May 2009 our position was strengthened further, fueled by the gradual recovery of world economy.

We rejuvenated the fundamental principles our business’s of sustainability, optimizing our economic, social and environmental responsibilities through our business priorities while consolidating our vision ‘to be the most innovative, dependable and diversified merchant bank’. In this regard our prime aim is to satiate our customers by providing value added and innovative services. Even in tough economic conditions we are mind full to be profitable for our sharehold-ers while promising a sustainable future for our employees.

We, being a merchant bank always act as a responsible corporate citizen understanding the importance of securing and developing the economy and social wellbeing. We also have been able to secure interests of the stakeholders of troubled finance companies and banks by being the appointed managing agents by the Central Bank of Sri Lanka.

I take this opportunity to thank my team for their dedication to make MBSL a sustainable and socially responsible organization.

Gamini KarunathilakeChief Executive Officer

CEO, Mr. Gamini Karunathilake awarding the first lease to a customer at the new City Branch - Kolluptiya.

34

Sustainability Report

IntroductionOur corporate culture is based on a set of values that are intrinsic to good governance: Account-ability and transparency. Ours is an open book that conforms to Global Reporting Initiatives (GRI) Guidelines. And what follows is some of the performance activities we were engaged during year 2009.

Customer RelationsEmployee RelationsCommunity RelationsInvestor RelationsEnvironmental RelationsSupplier Relations

‘ If we hire people who are smarter than us, we will become a Company of giants... if not will become dwarfs.’

- David Ogilvy.

35

CUSTOMER RELATIONSEasy Access with new City BranchAs MBSL Head Office is situated inside the most high security zone in Colombo our visitors had to undergo countless difficulties such as security checks, and lack of parking space, if they tried to visit us. We were on the look out for a suitable place that is convenient for our customers and finally found one in Kollupitiya and opened our New City Branch in October 2009. The relief and appreciation by customers was amply demonstrated by the disbursement of LKR 52 million within the first three months of operations of this branch. 24 Hours serviceWe understand the urgent financial needs of our customers and are ready to provide them with a speedy service around the clock. To facilitate this commitment we have launched ‘24 hour customer service’ where a customer can obtain leasing or hire purchase facility within 24 hours in any of our branches. This was very well recognized by our long - standing customers and has helped to retain the customers within the company.

Insurance on behalf of customersTime is absolutely vital for customers especially for those who manage their own businesses. For them wasting time is anathema, as it is loss of business opportunity. Also customers find it is inconvenient to bear the insurance premium, which is mandated to be paid annually.

Having identified this issue, we launched a special product which has insurance ‘in – built’ to the leasing or hire purchase agreement, where the premium is paid by MBSL. No longer the customer is expected to seek an insurer. This feature has become very popular among customers especially those individuals and budding entrepreneurs.

Vehicle registration on behalf of customersWith the aim of ensuring a better customer satisfaction, the registration of vehicles under leasing or hire purchase are handled by us, minimizing the hassles that have to be faced by our customers.

EMPLOYEE RELATIONSIt is a fact that our success, depend on our service. The quality our service will propel the curve high in our performance chart. In order to achieve that, Human Resource Development is the most critical focal point within the Bank and the Bank seeks to create a healthy work environ-ment where all employees have the equal opportunity to maximize their personal potential. Therefore, we have defined our HR Vision and Objectives accordingly.

HR Vision:To create an environment in the Bank, with a view to develop ‘cutting – edge’ human resource base to elevate the Bank to be a role model in human resource development, management and utilization.

HR Objective:To deploy a group of competent personnel into a work environment in which they can expand their true potential to achieve organisational goals, as well as fulfilling their personal ambitions.

Human Capital Analysis

Age-wise 51-60 41-50 31-40 *Below 30 11 46 35 55 Senior Senior Junior Clerical & Others Management Executive Executive Allied Management Management

8 24 64 44 7

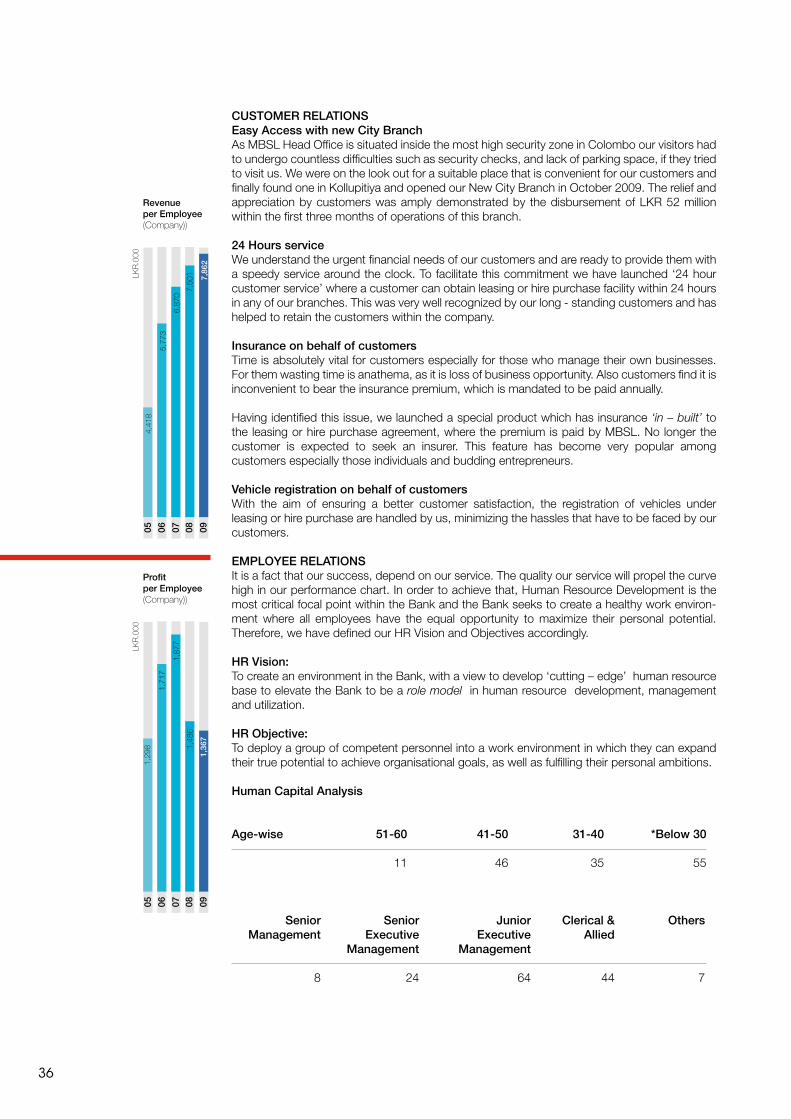

Revenue per Employee(Company))

LKR

.000

05 06 07 08 09

4,41

8

6,87

0

7,50

1 7,86

2

5,77

3

Profit per Employee(Company))

LKR

.000

05 06 07 08 09

1,29

8

1,87

7

1,48

6

1,36

7

1,71

7

36

Employee Productivity (LKR’ 000) 2008 2009

Revenue per employee 7,501 7,862 Net profit per employee 1,486 1,367Value added per employee 2,605 2,687Total Assets per employee 34,552 37,952Total Employees 138 147

Recruitment & Selection Since the performance of the employees is directly linked to profitability of the organisation, it is imperative that an organisation makes the correct decisions in talent scouting. With this in mind an exacting and meticulous Recruitment & Selection Process has been set in place with the aim of skimming off the cream of the job market.

The prospective candidates are subjected to a selection process consisting of interviews in several stages and in order to maintain unbiased fair play, we have introduced separate interview panels at each grade and stage of recruitment.

The Scheme of recruitment process, which is guided by the Recruitment & Selection Proce-dure, has clearly specified the Educational/Professional qualifications and experience required for each post in the Bank. This has helped the Bank to maintain consistency and transparency in the selection process.

Training & DevelopmentThe year under review witnessed a new resurgence in the two major areas of human resources development and utilization. With the improved financial performance, the Bank was able to adopt and implement staff development programs on a more continuous and meaningful basis. With Awareness Programs conducted on quality and productivity enhancement and organising several business improvement seminars/workshops were, major aspects of human resource development and utilization.

Both as a motivational measure and as a skills development process, arrangements were also made for the staff to attend cost-effective foreign training programs in addition to nominating them for local training sessions.

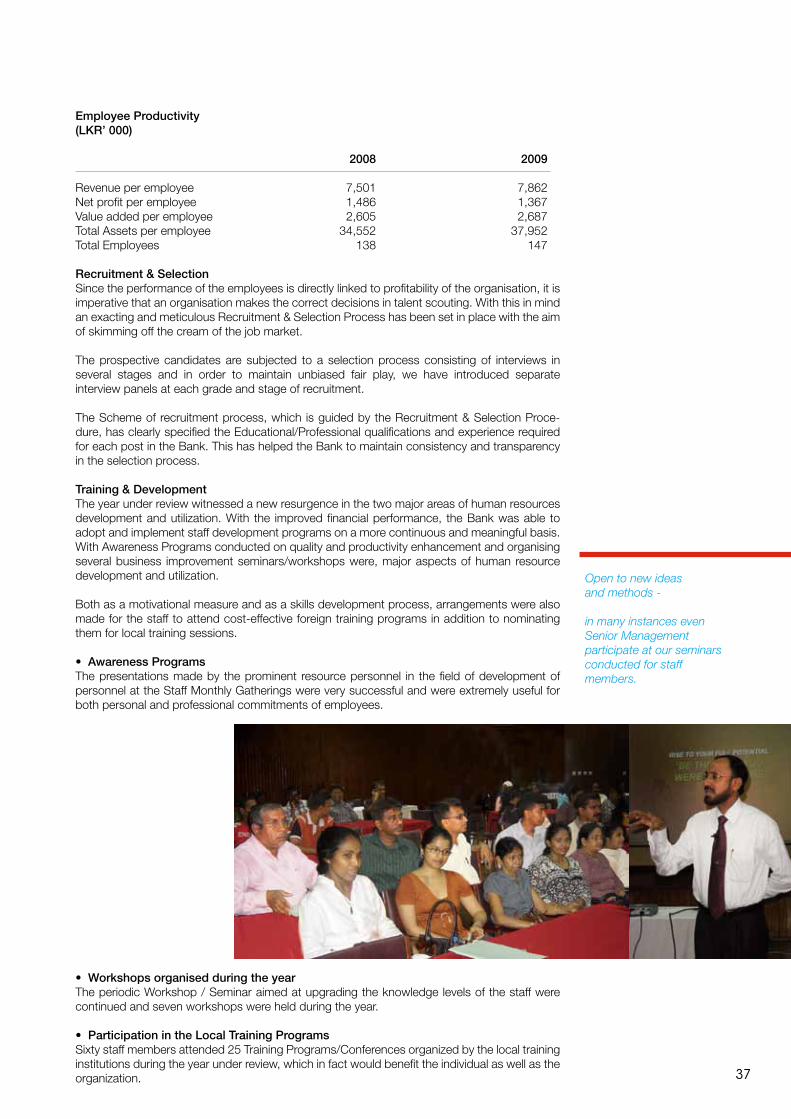

• Awareness ProgramsThe presentations made by the prominent resource personnel in the field of development of personnel at the Staff Monthly Gatherings were very successful and were extremely useful for both personal and professional commitments of employees.

• Workshops organised during the yearThe periodic Workshop / Seminar aimed at upgrading the knowledge levels of the staff were continued and seven workshops were held during the year.

• Participation in the Local Training Programs Sixty staff members attended 25 Training Programs/Conferences organized by the local training institutions during the year under review, which in fact would benefit the individual as well as the organization.

Open to new ideas and methods -

in many instances even Senior Management participate at our seminars conducted for staff members.

37

Overseas Training Programs Attended By The Staff - 2009 Duration Name Of The Workshop/Program Conducted By

25/02/2009 to 10/03/2009 Corporate Management AOTS, Nagoya, Japan for Sri Lanka

15/06/2009 - 19/06/2009 Lending Strategies to SMEs NIBM, India

22/06/2009 - 26/06/2009 Emotional Intelligence for NIBM, India Leadership Competence

25/11/2009 to 08/12/2009 Corporate Management AOTS, Nagoya, Japan for Sri Lanka

Performance oriented Culture and RewardsContinuation of Performance Appraisal System biannually also enabled to develop the staff on a more meaningful basis as well as to implement and monitor the Bank’s major work plans.

As per the Performance Based Annual Increment Scheme, Annual Increments of the staff are linked to the following factors: Performance of the Organisation, Divisional Performance, Individual Performance Cost of Living

The Bank continued with the staff incentive scheme, which has helped to enhance staff performance, to reach Bank’s business and administrative targets.

Building Relationship & EntertainingTo strengthen and build teamwork and promote closer staff interaction, an outing to “Cin-namon Lodge” (Habarana) was organised through the MBSL Welfare & Recreation Club. 90% of our staff members and their families participated in this event. The renewal of the Collective Agreement with the non-executive staff has assisted to maintain a closer rapport with the CBEU. For first time in the Bank’s history, the Bank entered into a Collective Agreement with the employees in the grades of Junior Executive, Executive, Assistant Manager and Deputy Manager.

On Thursday 4th March 2009, the Bank’s 27th Anniversary and the Monthly Gathering of March were held together. An employee with 20 years of service and eleven employees with 10 years of service were felicitated at this function. Short religious ceremonies, and worship services for all faiths followed the celebrations.

COMMUNITY RELATIONS

1. Honors to war heroes – scholarship for Ranawiru families

We hold the invaluable contributions and supreme sacrifices made by the armed forces to secure the sovereignty of the country and to bring the entire nation under single flag, very close to our hearts. As a tribute to our heroes a scholarship program was initiated by the MBSL to provide financial assistance to 30 children of deceased war heroes. This also will help to inculcate valuable future minds that can help to develop the economy of the country.

Under this scheme, a trust has been established from the contributions made by MBSL, MCSL and its staff who contributed their four days salaries. Each child will get LKR 1,000 per month until they finish their Advanced Level of schooling.

2. Securing future minds and employments- Ceylinco Sussex College The Ceylinco Sussex College is a privately owned premier international college. CSC faced a critical financial situation in 2009 consequent to the crisis at Ceylinco group. The recovery of the monies invested by The Finance Company, who were responsible for

Periodic family outings and Annual Get together have

helped to create harmony with meeting of minds...

Uninterrupted opportunities

- children participating at the Ranaviru Scholarship Awards

Ceremony

38

Watershed year -

MBSL diversifying into new ventures - Chairman,Mr. Janaka Ratnayake and CEO, Mr. Gamini Ka-runathilake meeting managements of newly acquired companies...

Seminar conducted by MBSL.

College Network development became doubtful. Further, MBSL wished to secure the future of over 5000 students scattered around the country. The school network was about to come to an end, and if allowed there was no viable option for these affected students as this was the only school that offered local curriculum in English medium. We have always recognized the importance of the education of younger generation and decided to undertake the manage-ment of this college. Also there were considerable academic/ non - academic staff at that time and their employment was at risk as the country was recoiling from the global economic shock. The decision taken by MBSL to manage this collage helped to secure not only the continu-ance of education for the students, but also employment of the staff and the well being of their families, whilst safeguarding the public depositors of TFC.