mastery charter school clymer …...board of trustees mastery charter school ‐ clymer elementary...

TRANSCRIPT

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION

YEAR ENDED JUNE 30, 2013

(WITH COMPARATIVE TOTALS FOR JUNE 30, 2012)

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY TABLE OF CONTENTS

YEAR ENDED JUNE 30, 2013

INDEPENDENT AUDITORS’ REPORT 1 REQUIRED SUPPLEMENTARY INFORMATION MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED) 4 BASIC FINANCIAL STATEMENTS STATEMENT OF NET POSITION 7 STATEMENT OF ACTIVITIES 8 BALANCE SHEET – GOVERNMENTAL FUNDS 9 RECONCILIATION OF THE BALANCE SHEET OF GOVERNMENTAL FUNDS TO THE STATEMENT OF NET POSITION 10 STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCE – GOVERNMENTAL FUNDS 11 RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES 12 NOTES TO FINANCIAL STATEMENTS 13 SUPPLEMENTARY INFORMATION SCHEDULE OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCE – BUDGET AND ACTUAL – GENERAL FUND (UNAUDITED) 22 SINGLE AUDIT REQUIREMENTS SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS 23 NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS 24 INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENTAL AUDITING STANDARDS 25 INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE WITH REQUIREMENTS THAT COULD HAVE A DIRECT AND MATERIAL EFFECT ON EACH MAJOR PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A‐133 27 SCHEDULE OF FINDINGS AND QUESTIONED COSTS 29

(1)

CliftonLarsonAllen LLP www.cliftonlarsonallen.com

An independent member of Nexia International

INDEPENDENT AUDITORS’ REPORT Board of Trustees Mastery Charter School ‐ Clymer Elementary Philadelphia, Pennsylvania Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities and the general fund of Mastery Charter School – Clymer Elementary, as of and for the year ended June 30, 2013, the related notes to the financial statements, which collectively comprise the entity’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Board of Trustees Mastery Charter School ‐ Clymer Elementary

(2)

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities and general fund of Mastery Charter School – Clymer Elementary as of June 30, 2013, and the respective changes in financial position for the year then ended in accordance with accounting principles generally accepted in the United States of America Change in Accounting Principle

As discussed in Note 1 to the financial statements, Mastery Charter School – Clymer Elementary implemented the provisions of the Governmental Accounting Standards Board (GASB) Statements No. 63 –Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position for the year ended June 30, 2013, which represents a change in accounting principle. The adoption of this standard did not have any financial impact on the School’s financial statements. Our opinion is not modified with respect to this matter. Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis and the schedule of revenues, expenditures and changes in fund balance‐ budget and actual on pages 4 through 6 and page 23 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Report on Summarized Comparative Information

We have previously audited Mastery Charter School – Clymer Elementary’s 2012 financial statements, and we expressed an unmodified audit opinion on those audited financial statements of the governmental activities and general fund in our report dated November 14, 2012. In our opinion, the summarized comparative information presented herein as of and for the year ended June 30, 2012, is consistent, in all material respects, with the audited financial statements from which it has been derived. Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Mastery Charter School – Clymer Elementary’s basic financial statements. The schedule of expenditures of federal awards, as required by U.S. Office of Management and Budget Circular A‐133, Audits of States, Local Governments, and Non‐Profit Organizations is presented for purposes of additional analysis and is not a required part of the basic financial statements. The schedule of expenditures of federal awards is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional

Board of Trustees Mastery Charter School ‐ Clymer Elementary

(3)

procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the schedule of expenditures of federal awards is fairly stated, in all material respects, in relation to the basic financial statements as a whole. Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated December 10, 2013 on our consideration of Mastery Charter School – Clymer Elementary’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the result of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Mastery Charter School – Clymer Elementary’s internal control over financial reporting and compliance.

CliftonLarsonAllen LLP

Plymouth Meeting, Pennsylvania December 10, 2013

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

JUNE 30, 2013

(4)

The Board of Trustees of Mastery Charter School – Clymer Elementary (the School) offers readers of the School’s financial statements this narrative overview and analysis of the financial activities of the School for the fiscal year ended June 30, 2013. This is the School’s first year of operations. We encourage readers to consider the information presented here in conjunction with the School’s financial statements. Financial Highlights

Total revenues increased by $457,414 to $7,119,975 primarily due to an increase in the student subsidies for the year ended June 30, 2013.

At the close of the current fiscal year, the School reports an ending general fund balance of $541,263. The general fund balance increased from the previous year end general fund deficit as the result of a $548,736 excess of revenues over expenditures for the year ended June 30, 2013.

The School’s cash balance at June 30, 2013 was $719,351.

Overview of the Financial Statements

The discussion and analysis is intended to serve as an introduction to the School’s basic financial statements. The School’s basic financial statements as presented comprise four components: Management’s Discussion and Analysis (this section), the basic financial statements, required supplementary schedule and reporting requirements under Government Auditing Standards and OMB Circular A‐133. Government‐Wide Financial Statements

The government‐wide financial statements are designed to provide readers with a broad overview of the School’s finances, in a manner similar to a private‐sector business. The statement of net position presents information on all of the School’s assets and liabilities, with the difference between the two reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the School is improving or deteriorating. The statement of activities presents information showing how the School’s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. The government‐wide financial statements report on the function of the School that is principally supported by subsidies from school districts whose constituents attend the School. Fund Financial Statements

A fund is a group of related accounts that are used to maintain control over resources that have been segregated for specific activities or purposes. The School, like governmental type entities, utilizes fund accounting to ensure and demonstrate compliance with finance‐related legal requirements. The School has only one fund type, the governmental general fund. Notes to the Financial Statements

The notes provide additional information that is essential to a full understanding of the data provided in the government‐wide and fund financial statements.

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

JUNE 30, 2013

(5)

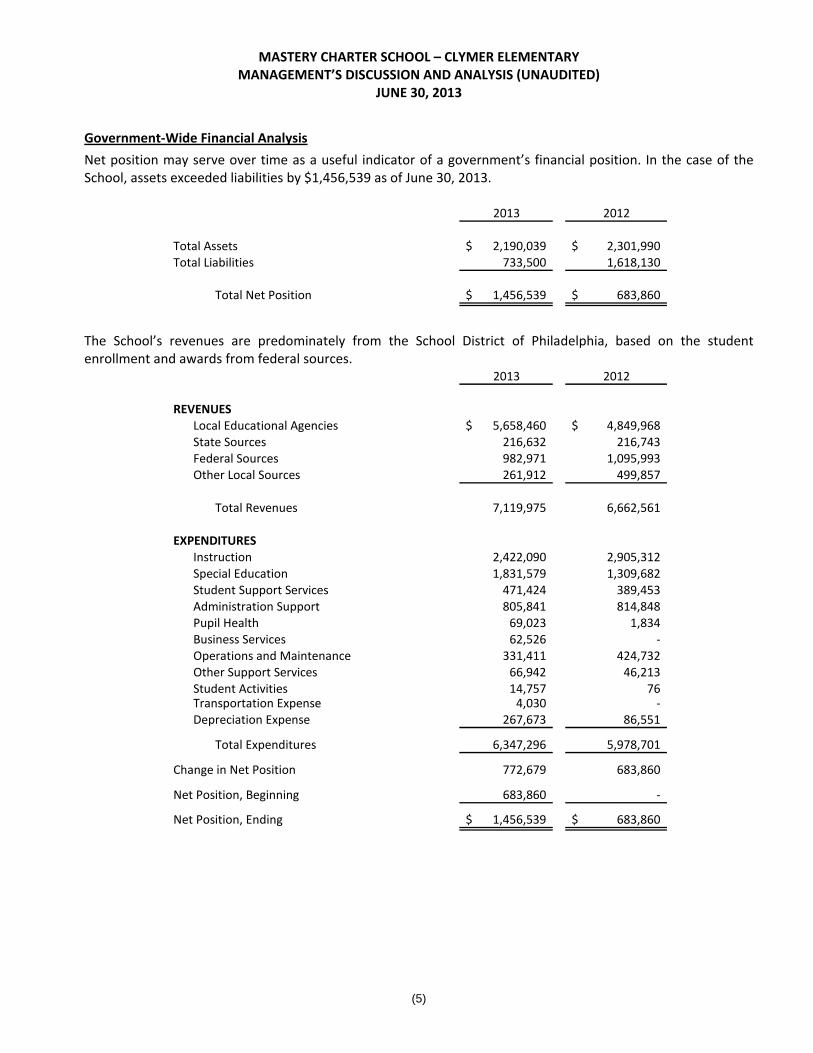

Government‐Wide Financial Analysis

Net position may serve over time as a useful indicator of a government’s financial position. In the case of the School, assets exceeded liabilities by $1,456,539 as of June 30, 2013.

2013 2012

Total Assets 2,190,039$ 2,301,990$ Total Liabilities 733,500 1,618,130

Total Net Position 1,456,539$ 683,860$

The School’s revenues are predominately from the School District of Philadelphia, based on the student enrollment and awards from federal sources.

2013 2012

REVENUESLocal Educational Agencies 5,658,460$ 4,849,968$ State Sources 216,632 216,743 Federal Sources 982,971 1,095,993 Other Local Sources 261,912 499,857

Total Revenues 7,119,975 6,662,561

EXPENDITURESInstruction 2,422,090 2,905,312 Special Education 1,831,579 1,309,682 Student Support Services 471,424 389,453 Administration Support 805,841 814,848 Pupil Health 69,023 1,834 Business Services 62,526 ‐ Operations and Maintenance 331,411 424,732 Other Support Services 66,942 46,213 Student Activities 14,757 76 Transportation Expense 4,030 ‐ Depreciation Expense 267,673 86,551

Total Expenditures 6,347,296 5,978,701

Change in Net Position 772,679 683,860

Net Position, Beginning 683,860 ‐

Net Position, Ending 1,456,539$ 683,860$

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

JUNE 30, 2013

(6)

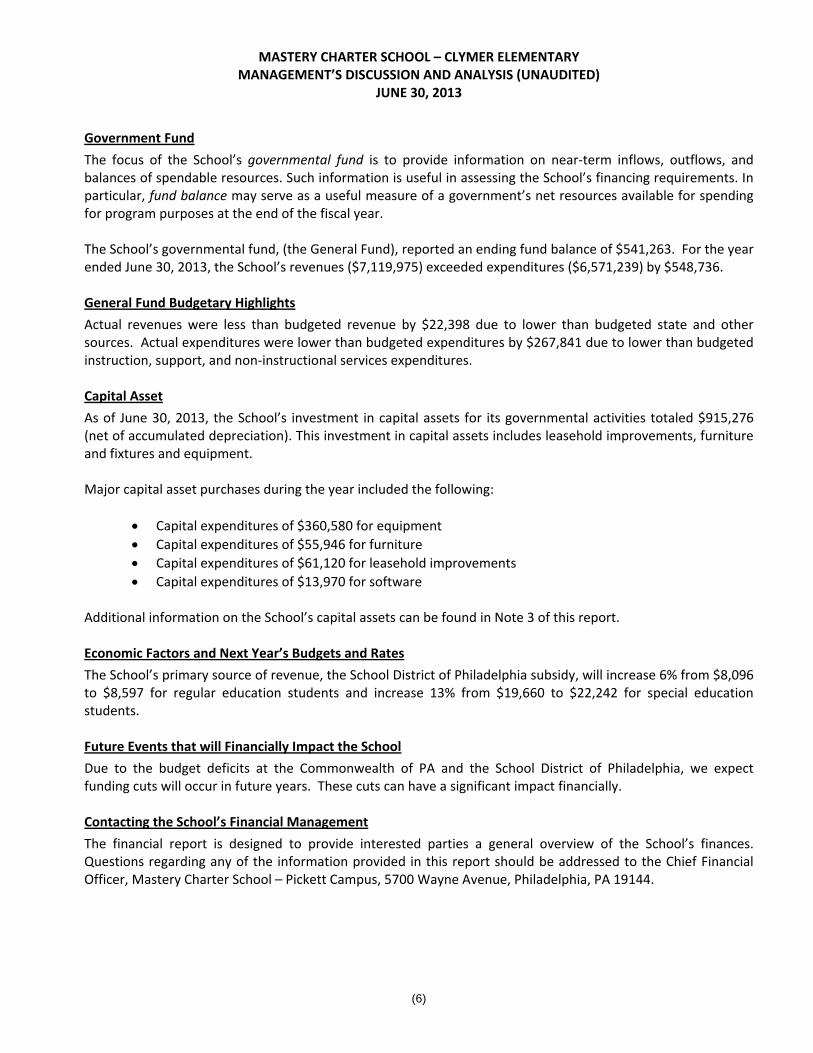

Government Fund

The focus of the School’s governmental fund is to provide information on near‐term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the School’s financing requirements. In particular, fund balance may serve as a useful measure of a government’s net resources available for spending for program purposes at the end of the fiscal year. The School’s governmental fund, (the General Fund), reported an ending fund balance of $541,263. For the year ended June 30, 2013, the School’s revenues ($7,119,975) exceeded expenditures ($6,571,239) by $548,736. General Fund Budgetary Highlights

Actual revenues were less than budgeted revenue by $22,398 due to lower than budgeted state and other sources. Actual expenditures were lower than budgeted expenditures by $267,841 due to lower than budgeted instruction, support, and non‐instructional services expenditures. Capital Asset

As of June 30, 2013, the School’s investment in capital assets for its governmental activities totaled $915,276 (net of accumulated depreciation). This investment in capital assets includes leasehold improvements, furniture and fixtures and equipment. Major capital asset purchases during the year included the following:

Capital expenditures of $360,580 for equipment

Capital expenditures of $55,946 for furniture

Capital expenditures of $61,120 for leasehold improvements

Capital expenditures of $13,970 for software

Additional information on the School’s capital assets can be found in Note 3 of this report. Economic Factors and Next Year’s Budgets and Rates

The School’s primary source of revenue, the School District of Philadelphia subsidy, will increase 6% from $8,096 to $8,597 for regular education students and increase 13% from $19,660 to $22,242 for special education students. Future Events that will Financially Impact the School

Due to the budget deficits at the Commonwealth of PA and the School District of Philadelphia, we expect funding cuts will occur in future years. These cuts can have a significant impact financially. Contacting the School’s Financial Management

The financial report is designed to provide interested parties a general overview of the School’s finances. Questions regarding any of the information provided in this report should be addressed to the Chief Financial Officer, Mastery Charter School – Pickett Campus, 5700 Wayne Avenue, Philadelphia, PA 19144.

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY STATEMENT OF NET POSITION

JUNE 30, 2013 (WITH COMPARATIVE TOTALS AT JUNE 30, 2012)

See accompanying Notes to Financial Statements. (7)

2013 2012

ASSETS

CURRENT ASSETS Cash 719,351$ 620,540$ State Subsidies Receivable 53,436 161,368Federal Subsidies Receivable 306,984 564,242 Other Receivables 192,732 30,954 Prepaid Expenses 2,260 10,375 Due from Other Governmental Entities ‐ 223,178

Total Current Assets 1,274,763 1,610,657

CAPITAL ASSETS, NET 915,276 691,333

Total Assets 2,190,039 2,301,990

LIABILITIES

CURRENT LIABILITIESAccounts Payable 225,180 155,252 Accrued Expenses 485,651 492,218 Due to Other Governmental Entities 22,669 ‐ Due to Mastery Charter School Foundation ‐ 970,660

Total Current Liabilities 733,500 1,618,130

NET POSITION

Net Investment in Capital Assets 915,276 691,333 Unrestricted 541,263 (7,473)

Total Net Position 1,456,539$ 683,860$

Governmental Activities

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY STATEMENT OF ACTIVITIES YEAR ENDED JUNE 30, 2013

(WITH COMPARATIVE TOTALS FOR THE YEAR ENDED JUNE 30, 2012)

See accompanying Notes to Financial Statements. (8)

2013 2012

Net(Expense) Net(Expense)Revenue and Revenue and

Program Changes in Changes inRevenues Net Position Net PositionOperating Total Total Grants and Governmental Governmental

Functions Expenses Contributions Activities ActivitiesGovernmental Activities:Instruction 2,422,090$ 982,971$ (1,439,119)$ (1,809,319)$ Special Education 1,831,579 ‐ (1,831,579) (1,309,682) Student Support Services 471,424 ‐ (471,424) (389,453) Administration Support 805,841 ‐ (805,841) (814,848) Pupil Health 69,023 ‐ (69,023) (1,834) Business Services 62,526 ‐ (62,526) ‐ Operations and Maintenance 331,411 ‐ (331,411) (424,732) Other Support Services 66,942 ‐ (66,942) (46,213) Student Activities 14,757 ‐ (14,757) (76) Transportation Expense 4,030 ‐ (4,030) ‐ Depreciation Expense 267,673 ‐ (267,673) (86,551)

Total 6,347,296$ 982,971$ (5,364,325) (4,882,708)

General Revenues:Local Educational Agencies 5,658,460 4,849,968State Grants and Reimbursements 216,632 216,743Other Local Revenue 261,912 499,857

Total General Revenues 6,137,004 5,566,568

Change in Net Position 772,679 683,860

Net Position ‐ Beginning of Year 683,860 ‐

Net Position ‐ End of Year 1,456,539$ 683,860$

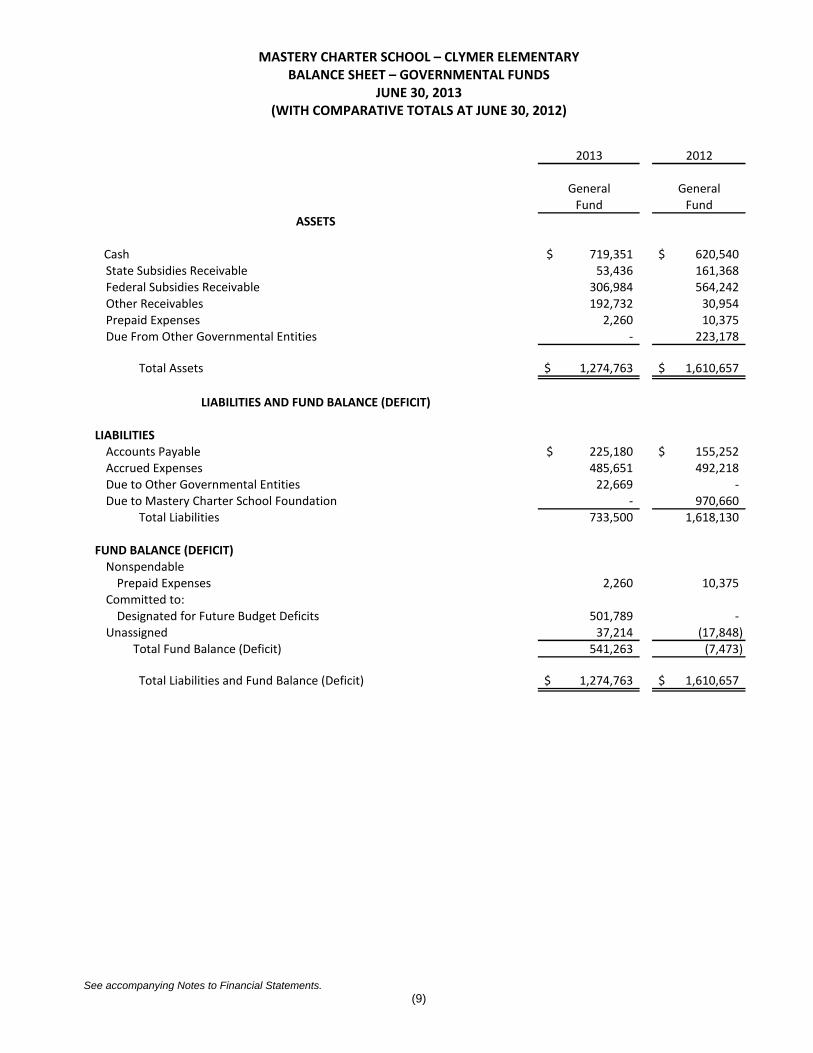

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY BALANCE SHEET – GOVERNMENTAL FUNDS

JUNE 30, 2013 (WITH COMPARATIVE TOTALS AT JUNE 30, 2012)

See accompanying Notes to Financial Statements. (9)

2013 2012

General GeneralFund Fund

ASSETS

Cash 719,351$ 620,540$ State Subsidies Receivable 53,436 161,368Federal Subsidies Receivable 306,984 564,242Other Receivables 192,732 30,954Prepaid Expenses 2,260 10,375Due From Other Governmental Entities ‐ 223,178

Total Assets 1,274,763$ 1,610,657$

LIABILITIES AND FUND BALANCE (DEFICIT)

LIABILITIESAccounts Payable 225,180$ 155,252$ Accrued Expenses 485,651 492,218 Due to Other Governmental Entities 22,669 ‐ Due to Mastery Charter School Foundation ‐ 970,660

Total Liabilities 733,500 1,618,130

FUND BALANCE (DEFICIT)NonspendablePrepaid Expenses 2,260 10,375

Committed to:Designated for Future Budget Deficits 501,789 ‐

Unassigned 37,214 (17,848) Total Fund Balance (Deficit) 541,263 (7,473)

Total Liabilities and Fund Balance (Deficit) 1,274,763$ 1,610,657$

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY RECONCILIATION OF THE BALANCE SHEET OF GOVERNMENTAL FUNDS

TO THE STATEMENT OF NET POSITION JUNE 30, 2013

See accompanying Notes to Financial Statements. (10)

Total Fund Balance for Governmental Funds 541,263$

Total net position reported for governmental activities in the statementof net position is different because:

Capital assets used in governmental funds are not financial resources and,therefore, are not reported in the funds. Those assets consist of:

Capital Assets, Net 915,276

Total Net Position of Governmental Activities 1,456,539$

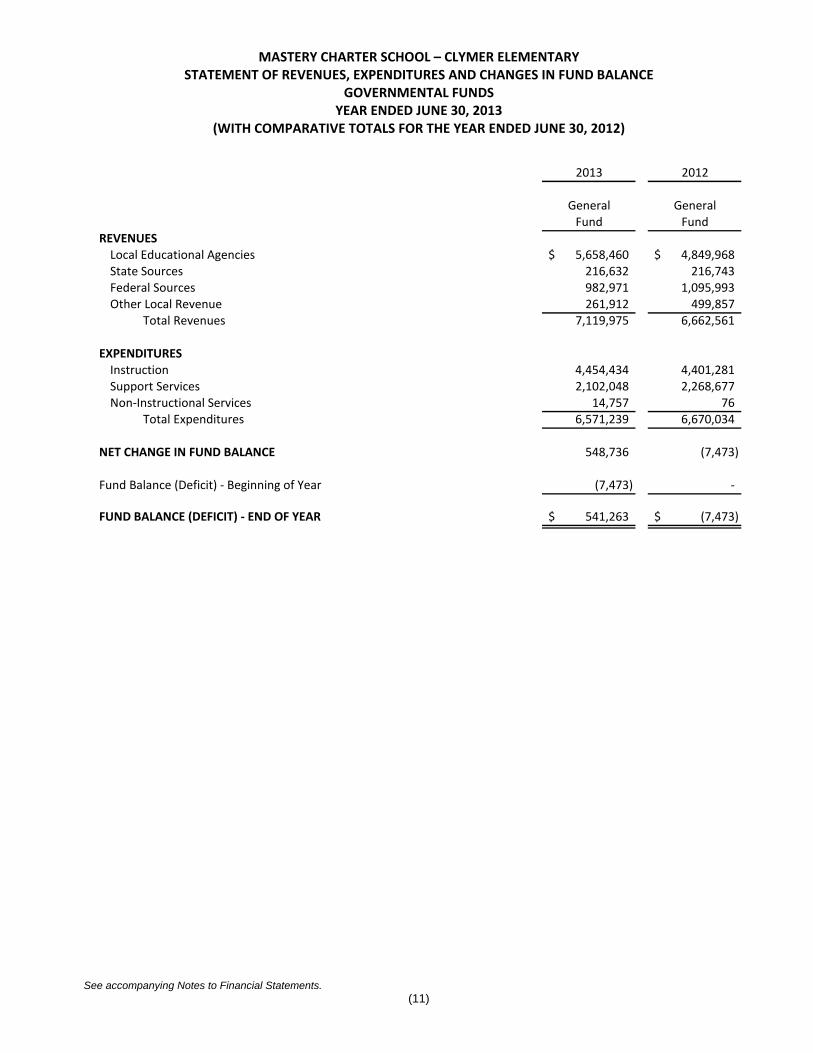

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCE

GOVERNMENTAL FUNDS YEAR ENDED JUNE 30, 2013

(WITH COMPARATIVE TOTALS FOR THE YEAR ENDED JUNE 30, 2012)

See accompanying Notes to Financial Statements. (11)

2013 2012

General GeneralFund Fund

REVENUESLocal Educational Agencies 5,658,460$ 4,849,968$ State Sources 216,632 216,743Federal Sources 982,971 1,095,993Other Local Revenue 261,912 499,857

Total Revenues 7,119,975 6,662,561

EXPENDITURESInstruction 4,454,434 4,401,281Support Services 2,102,048 2,268,677 Non‐Instructional Services 14,757 76

Total Expenditures 6,571,239 6,670,034

NET CHANGE IN FUND BALANCE 548,736 (7,473)

Fund Balance (Deficit) ‐ Beginning of Year (7,473) ‐

FUND BALANCE (DEFICIT) ‐ END OF YEAR 541,263$ (7,473)$

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES AND

CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES YEAR ENDED JUNE 30, 2013

See accompanying Notes to Financial Statements. (12)

Net Change in Fund Balance ‐ Total Governmental Funds 548,736$

Amounts reported for governmental activities in the statement of activities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of activities, assets are capitalized and the cost is allocated over their estimated useful lives and reported as depreciation expense. This is the amount by which capital outlays exceeded depreciation in the current period.

Capital Outlays 491,616 Depreciation Expense (267,673)

Change in Net Position of Governmental Activities 772,679$

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(13)

NOTE 1 BACKGROUND AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Background

Mastery Charter School – Clymer Elementary (School) was formed as a Pennsylvania nonprofit corporation to operate in accordance with Pennsylvania Act 22 of 1997. The initial charter was granted by the Commonwealth on April 27, 2011. The current charter is for a five‐year term from July 1, 2011 to June 30, 2016. During the year ended June 30, 2013, the School served approximately 515 students in grades kindergarten through eight.

Basis of Presentation

The financial statements of the School have been prepared in conformity with U.S. generally accepted accounting principles (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the accepted standard setting body for establishing government accounting and financial reporting principles. The GASB has issued a codification of governmental accounting and financial reporting standards.

Comparative Financial Information

The financial statements include certain prior year summarized comparative information in total. Such information does not include sufficient detail to constitute a presentation in conformity with generally accepted accounting principles. Accordingly, such information should be read in conjunction with the School’s financial statements for the year ended June 30, 2012 from which the summarized information was derived. Certain items in prior year financial statements have been reclassified to conform to current year presentation.

Government‐Wide and Fund Financial Statements

The government‐wide financial statements (the statement of net position and the statement of activities) report on the School as a whole. The statement of activities demonstrates the degree to which the direct expenses of the School’s function are offset by program revenues.

The fund financial statements (governmental fund balance sheet and statement of governmental

fund revenues, expenditures and changes in fund balance) report on the School’s General Fund. Measurement Focus, Basis of Accounting and Financial Statement Presentation

Government‐wide Financial Statements:

The statement of net position and the statement of activities are prepared using the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is incurred regardless of the timing of the related cash flows. Grants and similar items are recognized as soon as all eligibility requirements imposed by provider have been met.

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(14)

NOTE 1 BACKGROUND AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Measurement Focus, Basis of Accounting and Financial Statement Presentation (Continued)

Fund Financial Statements:

Governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, the School considers revenues to be available if they are collected within 60 days of the end of the current period. Expenditures generally are recorded when a liability is incurred, as under accrual accounting.

The government reports the following major governmental fund: General Fund – The General Fund is the operating fund of the School and accounts for all

revenues and expenditures of the School. Method of Accounting

Accounting standards requires a statement of net position, a statement of activities and changes in net position. It requires the classification of net position into three components – net investment in capital assets; restricted; and unrestricted. These calculations are defined as follows:

Net investment in capital assets – This component of net position consists of capital assets, including restricted capital assets, net of accumulated depreciation and reduced by the outstanding balances of any bonds, mortgages, notes, or other borrowings that are attributable to the acquisition, construction, or improvement of those assets. If there are significant unspent related debt proceeds at year‐end, the portion of the debt attributable to the unspent proceeds are not included in the calculation of net investment in capital assets. Rather, that portion of the debt is included in the same net position component as the unspent proceeds. The School presently has no debt related to the capital assets.

Restricted – This component of net position consists of constraints placed on net position use through external constraints imposed by creditors such as through debt covenants, grantors, contributors, or laws or regulations of other governments or constraints imposed by law through constitutional provisions or enabling legislation. The School presently has no restricted net position.

Unrestricted net position – This component of net position consists of net position that do not meet the definition of “restricted” or “net investment in capital assets.”

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(15)

NOTE 1 BACKGROUND AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Method of Accounting (Continued)

In the fund financial statements, governmental funds report nonspendable portions of fund balance related to prepaid expenses, long term receivables, and corpus on any permanent fund. Restricted funds are constrained from outside parties (statute, grantors, bond agreements, etc.). Committed fund balances represent amounts constrained for a specific purpose by a governmental entity using its highest level of decision‐making authority. Committed fund balances are established and modified by a resolution approved by the Board of Trustees. Assigned fund balances are intended by the School to be used for specific purposes, but are neither restricted nor committed. Unassigned fund balances are considered the remaining amounts. When expenditures are incurred for purposes for which both restricted and unrestricted fund balance are available, it is currently the School’s policy to use restricted first, then unrestricted fund balance. When expenditures are incurred for purposes for which committed, assigned, and unassigned amounts are available, it is currently the School’s policy to use committed first, then assigned, and finally unassigned amounts.

Budgets and Budgetary Accounting

Budgets are adopted on a basis consistent with U.S. generally accepted accounting principles. An annual budget is adopted for the General Fund.

The Budgetary Comparison Schedule should present both the original and the final appropriated

budgets for the reporting period. The School only has a general fund budget; an original budget was filed and accepted by the Labor, Education and Community Services Comptroller’s Office in June 2012. An amended budget was approved by the Board of Trustees in January 2013. The budget is required supplementary information.

Use of Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Concentration of Credit Risk

Periodically, the School may maintain deposits in excess of the Federal Deposit Insurance Corporation’s limit of $250,000, with financial institutions. At times, cash in bank may exceed FDIC insurable limits.

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(16)

NOTE 1 BACKGROUND AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Significant Accounting Estimates—Self‐Insured Claims

As of July 1, 2011, the School entered into a self funded benefit payment plan (“plan”), which covers eligible employees/members and dependents of each of the Mastery Charter Schools and NST (“the Schools”), as defined in the agreement. The Mastery Charter High School (“MCHS”) is the plan sponsor of the plan. The Schools are primarily self‐insured, up to certain limits, for employee group health claims. The plan has purchased stop‐loss insurance, which will reimburse MCHS for individual claims in excess of $100,000 annually or aggregate claims exceeding $1,000,000 annually. During the year ended June 30, 2013, each school paid premiums to MCHS based on an 1) previous years claims and premiums experience, 2) actual claims for the year ended June 30, 2013 and 3) claims incurred but not reported. Such estimates were provided by the School’s benefits consultant. The self‐insured claims liability for all schools, which includes incurred but not reported losses, amounts to $1,396,931 as of June 30, 2013 and is reflected on the books of MCHS as an accrued liability. The total expense under the program was approximately $5,610,533, which includes the School’s portion of $279,010 for the year ended June 30, 2013.

The determination of such claims, premiums and expenses and the appropriateness of the related liability is continually reviewed and updated. It is reasonably possible that the accrued estimated liability for self‐insured claims may need to be revised in the near term.

Cash

The School’s cash is considered to be cash on hand and demand deposits. Accounts Receivable

Accounts receivable primarily consist of amounts due from the Pennsylvania Department of Education for federal, state and local subsidy programs. Accounts receivable are stated at the amount management expects to collect from outstanding balances. As of June 30, 2013, no allowance for doubtful accounts was deemed warranted based on historical experience.

Prepaid Expenses

Prepaid expenses include payments to vendors for services applicable to future accounting periods such as insurance premiums. Capital Assets

Capital assets, which include property and equipment, are reported in the government‐wide financial statements. All capital assets are capitalized at cost and updated for additions and retirements during the year. The School does not possess any infrastructure. Improvements are capitalized; the cost of normal maintenance and repairs that do not add to the value of the asset or materially extend an asset’s life are not. Capital assets of the School are depreciated using the straight‐line method over the estimated useful lives of the assets except for leasehold improvements which are limited to the shorter of the life of the School’s Charter or the estimated useful lives of the improvements. Software costs are depreciated over thirty‐six months using the straight‐line method.

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(17)

NOTE 1 BACKGROUND AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

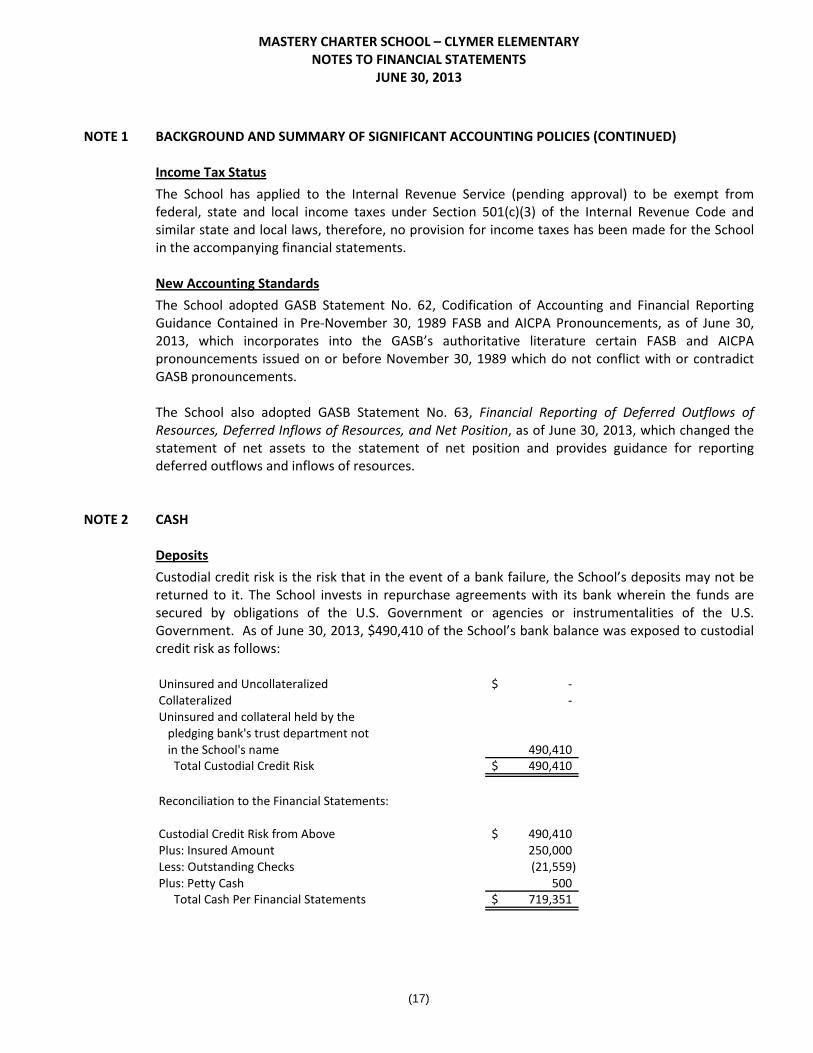

Income Tax Status

The School has applied to the Internal Revenue Service (pending approval) to be exempt from federal, state and local income taxes under Section 501(c)(3) of the Internal Revenue Code and similar state and local laws, therefore, no provision for income taxes has been made for the School in the accompanying financial statements. New Accounting Standards

The School adopted GASB Statement No. 62, Codification of Accounting and Financial Reporting Guidance Contained in Pre‐November 30, 1989 FASB and AICPA Pronouncements, as of June 30, 2013, which incorporates into the GASB’s authoritative literature certain FASB and AICPA pronouncements issued on or before November 30, 1989 which do not conflict with or contradict GASB pronouncements. The School also adopted GASB Statement No. 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position, as of June 30, 2013, which changed the statement of net assets to the statement of net position and provides guidance for reporting deferred outflows and inflows of resources.

NOTE 2 CASH Deposits

Custodial credit risk is the risk that in the event of a bank failure, the School’s deposits may not be returned to it. The School invests in repurchase agreements with its bank wherein the funds are secured by obligations of the U.S. Government or agencies or instrumentalities of the U.S. Government. As of June 30, 2013, $490,410 of the School’s bank balance was exposed to custodial credit risk as follows:

Uninsured and Uncollateralized ‐$ Collateralized ‐ Uninsured and collateral held by the pledging bank's trust department not in the School's name 490,410 Total Custodial Credit Risk 490,410$

Reconciliation to the Financial Statements:

Custodial Credit Risk from Above 490,410$ Plus: Insured Amount 250,000 Less: Outstanding Checks (21,559) Plus: Petty Cash 500 Total Cash Per Financial Statements 719,351$

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(18)

NOTE 3 CAPITAL ASSETS Capital assets are stated at cost. Depreciation has been calculated on such assets using the straight

line method over the following estimated lives:

Leasehold Improvements 5 YearsEquipment 5 YearsFurniture and Fixtures 7 YearsSoftware 3 Years

Capital asset activity for the year is summarized below:

Balance BalanceDescription July 01, 2012 Deletions Additions June 30, 2013

Equipment 11,075$ ‐$ 360,580$ 371,655$ Furniture and Fixtures 217,188 ‐ 55,946 273,134 Leasehold Improvements 541,040 ‐ 61,120 602,160 Software 8,581 ‐ 13,970 22,551

Total 777,884 ‐ 491,616 1,269,500 Less: Accumulated Depreciation 86,551 ‐ 267,673 354,224 Capital Assets, Net 691,333$ ‐$ 223,943$ 915,276$

NOTE 4 REVENUE Charter schools are funded by the local public school district in which each student resides. The rate

per student is determined annually and is based on the budgeted total expenditure per average daily membership of the prior school year for each school district. The majority of the students for the School reside in Philadelphia. For the year ended June 30, 2013, the rate for the School District of Philadelphia was $8,096 per year for regular education students plus additional funding for special education students and transportation. The annual rate is paid monthly by the School District of Philadelphia and is prorated if a student enters or leaves during the year. Total revenue from these sources was $5,658,460 for the year ended June 30, 2013.

NOTE 5 GOVERNMENT GRANTS AND REIMBURSEMENT PROGRAMS The School participates in numerous state and federal grant and reimbursement programs, which

are governed by various rules and regulations of the grantor agencies. Costs charged to the respective grant programs and reimbursement programs for social security taxes, retirement expense, facility lease expense and health services are subject to audit and adjustment by the grantor agencies; therefore, to the extent that the School has not complied with the rules and regulations governing the grants and reimbursement programs, refunds of any money received may be required and the collectability of any related receivable at June 30, 2013 may be impaired. In the opinion of the School, there are no significant contingent liabilities relating to compliance with the rules and regulations governing the respective grants; therefore, no provision has been recorded in the accompanying financial statements for such contingencies.

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(19)

NOTE 6 PENSION PLAN Plan Description:

The School contributes to the Public School Employees’ Retirement System (the System), a governmental cost‐sharing multiple‐employer defined benefit pension plan. The plan provides retirement and disability benefits, legislatively mandated ad hoc cost‐of‐living adjustments, and healthcare insurance premium assistance to qualifying annuitants. The Public School Employees’ Retirement Code (Act No. 96 of October 2, 1975, as amended) (24 Pa.C.S. 8101‐8535) assigns the authority to establish and amend benefit provisions to the System. The System issues a comprehensive annual financial report that includes financial statements and required supplementary information for the plan. A copy of the report may be obtained by writing to Diane J. Wert, Office of Financial Management, Public School Employees’ Retirement System, P.O. Box 125, Harrisburg, Pennsylvania 17108‐0125. This publication is also available on the PSERS website at www.psers.state.pa.us/publications/cafr/index.htm. Funding Policy:

The contribution policy is established in the Public School Employees’ Retirement Code and requires contributions by active members, employers and the Commonwealth of Pennsylvania.

Member contributions are as follows:

‐ Active members who joined the System prior to July 22, 1983, contribute at 5.25%

(Membership Class T‐C) or at 6.5% (Membership Class T‐D) of the member’s qualifying compensation.

‐ Members who joined the System on or after July 22, 1983, and who were active or inactive as of July 1, 2001, contribute at 6.25% (Membership Class T‐C) or at 7.5% (Membership Class T‐D) of the member’s qualifying compensation.

‐ Members who joined the System after June 30, 2001, contribute at 7.5% (automatic Membership Class T‐D). For all new hires and for members who elected Class T‐D membership, the higher contribution rates began with service rendered on or after January 1, 2002.

‐ Members who joined the System after June 30, 2011 would become Class T‐E member or, alternatively, elect to become a class T‐F member. The base contribution rate for Class T‐E members is 7.50% of compensation. The base contribution rate for Class T‐F members is 10.30% of compensation. Class T‐E and Class T‐f members are subject to a “shared risk” employee contribution rate.

Employer contributions are based upon an actuarial valuation. For fiscal year ended June 30, 2013, the rate of employer’s contribution was 12.36% of covered payroll. The 12.36% rate is composed of a pension contribution rate of 11.50% for pension benefits and 0.86% for health care insurance premium assistance.

Payroll expense for employees covered by the System for the year ended June 30, 2013 was

approximately $3.1 million.

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(20)

NOTE 6 PENSION PLAN (CONTINUED) In accordance with Act 29 of 1994, the Commonwealth of Pennsylvania will pay school entities for

contributions made to the System based on the formula in Act 29 of 1994, but not less than one‐half of the school entities contributions. The School’s contributions to the Plan for the years ended June 30, 2013 and 2012 totaled $290,478 and $248,234, respectively.

Effective July 1, 2012, the School was part of the Mastery Charter School 403(b) Retirement Plan, a multiple employer defined contribution plan under Section 403(b) of the Internal Revenue Code, which employees of the School can elect to contribute. Employees, who do not participate in the PSERS retirement plan, can contribute up to 5% of their qualified compensation, with the School matching up to 5% of their qualified compensation. Employees who participate in the PSERS retirement plan can also participate in the 403b plan, but these 403b contributions are not matched by the School. The School’s contribution to the Plan for the year ended June 30, 2013 was $25,167.

NOTE 7 RISK MANAGEMENT The School is exposed to various risks of loss related to torts: theft of, damage to, and destruction of

assets; errors and omissions; injuries to employees; and natural disasters. The School carries commercial insurance for such risks. Settled claims resulting from these risks have not exceeded commercial insurance coverage.

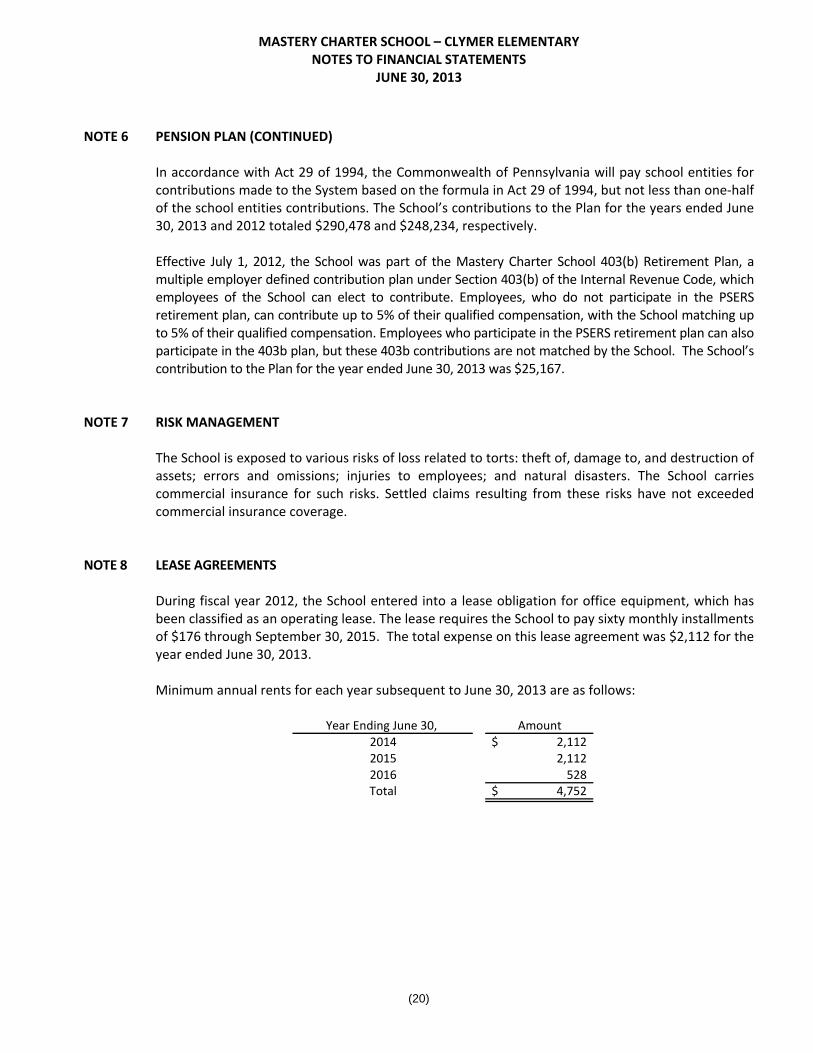

NOTE 8 LEASE AGREEMENTS

During fiscal year 2012, the School entered into a lease obligation for office equipment, which has been classified as an operating lease. The lease requires the School to pay sixty monthly installments of $176 through September 30, 2015. The total expense on this lease agreement was $2,112 for the year ended June 30, 2013.

Minimum annual rents for each year subsequent to June 30, 2013 are as follows:

Year Ending June 30, Amount2014 2,112$ 2015 2,112 2016 528 Total 4,752$

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

(21)

NOTE 9 MANAGEMENT AGREEMENT The Mastery Charter Schools use a Network Support Team (NST) for their educational,

administrative and financial services. The NST is a separate department that is included in the operations of the Mastery Charter High School.

As of July 1, 2012, the School entered into a one year agreement with the Mastery Charter High

School to provide educational, administrative and financial services for the School by the NST. As a result of common usage of the NST, the Mastery Charter Schools are considered related parties (see Note 10). The NST management fee is 8.5% of local school funds plus reimbursement for any costs NST incurs in providing the educational, administrative and financial services. Unless specified notice is given, the agreement renews each year during the term of the School’s charter. The total fee was $408,824 for the fiscal year.

NOTE 10 RELATED PARTY TRANSACTIONS Mastery Charter High School, Mastery Charter School – Shoemaker Campus, Mastery Charter School

– Thomas Campus, Mastery Charter School – Pickett Campus, Mastery Charter School – Harrity Elementary, Mastery Charter School – Mann Elementary, Mastery Charter School – Smedley Elementary, Hardy Williams Academy Charter School, Grover Cleveland Mastery Charter School and Mastery Charter School – Gratz Campus are considered related parties as a result of common members of the boards and the management of the schools.

High Tech High Philadelphia Foundation (HTHPF) and Mastery Charter Schools Foundation (MCSF) are considered related parties due to the mission of each organization, which is to support the Mastery Charter Schools. The School received grants from the MCSF totaling $9,004 in the year ended June 30, 2013.

During the year end June 30, 2012, MCSF provided interest free advances totaling $970,660 for

start‐up costs during the year. The amount was included in the Due to Mastery Charter School Foundation balance at June 30, 2012. These advances were paid back to the Foundation during the year ended June 30, 2013.

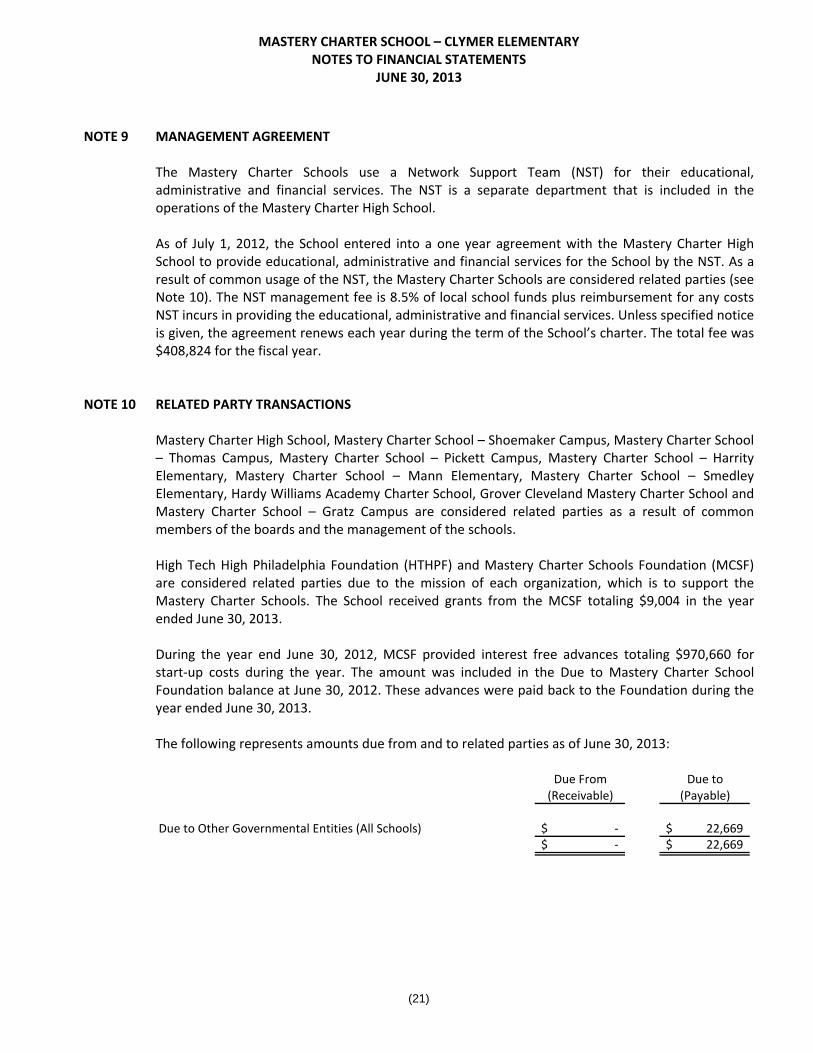

The following represents amounts due from and to related parties as of June 30, 2013:

Due From Due to(Receivable) (Payable)

Due to Other Governmental Entities (All Schools) ‐$ 22,669$ ‐$ 22,669$

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY SCHEDULE OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCE

BUDGET AND ACTUAL GENERAL FUND (UNAUDITED)

YEAR ENDED JUNE 30, 2013

(22)

Over(Under)

Actual FinalOriginal Final Amounts Budget

REVENUESLocal Sources 4,888,129$ 5,555,851$ 5,658,460$ 102,609$ State Sources 68,968 312,212 216,632 (95,580) Federal Sources 914,199 911,906 982,971 71,065 Other Revenue 326,000 362,404 261,912 (100,492)

Total Revenues 6,197,296 7,142,373 7,119,975 (22,398)

EXPENDITURESInstruction 3,692,813 4,474,970 4,454,434 (20,536) Support Services 2,185,188 2,337,110 2,102,048 (235,062) Non‐Instructional Services 27,000 27,000 14,757 (12,243)

Total Expenditures 5,905,001 6,839,080 6,571,239 (267,841)

NET CHANGE IN FUND BALANCE 292,295$ 303,293$ 548,736 245,443$

Fund Deficit ‐ Beginning of Year (7,473)

FUND BALANCE ‐ END OF YEAR 541,263$

Budgeted Amounts

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

YEAR ENDED JUNE 30, 2013

See accompanying Notes to Schedule of Expenditures of Federal Awards. (23)

Amount Accrued

Federal Grantor Federal Pass‐through Grant Period (Deferred) Total (Deferred)

Pass‐Through Grantor Source CFDA Grantor's Beginning/ Grant Revenue at Received Federal Revenue at

Program Title Code Number Number Ending Date Amount July 1, 2012 for the Year Expenditures June 30, 2013

U.S. Department of Education

Pass‐Through Pennsylvania Department of Education:

Title I ‐ Improving Basic Programs I 84.010 013‐121113 7/7/11‐9/30/12 315,513$ 210,342$ 210,342$ ‐$ ‐$

Title I ‐ Improving Basic Programs I 84.010 013‐131113 7/1/12‐9/30/13 339,711 ‐ 339,711 339,711 ‐

ARRA ‐ Title I School Improvement Grant 1003g I 84.388 139‐111113 8/31/11‐9/30/12 655,080 268,830 48,281 ‐ 220,549

ARRA ‐ Title I School Improvement Grant 1003g I 84.388 139‐123113 7/18/12‐9/30/13 448,402 ‐ 448,402 448,402 ‐

Title II ‐ Improving Teacher Quality I 84.367 020‐121113 7/7/11‐9/30/12 30,990 20,660 20,660 ‐ ‐

Title II ‐ Improving Teacher Quality I 84.367 020‐131113 7/1/12‐9/30/13 31,364 ‐ 31,016 31,364 348

Total U.S. Department of Education 499,832 1,098,412 819,477 220,897

Pass‐Through School District of Philadelphia

Individuals w/Disabilities Education Act‐ Part B I 84.027 N/A 7/1/12‐6/30/13 133,805 ‐ 66,903 133,806 66,903

Total U.S. Department of Education ‐ 66,903 133,806 66,903

U.S. Department of Health and Human Services

Pass‐Through Pennsylvania Department of Public Welfare

Medical Assistance I 93.778 044‐007674 7/1/11 ‐ 6/30/12 94,410 64,410 64,410 ‐ ‐

Medical Assistance I 93.778 044‐007674 7/1/12 ‐ 6/30/13 27,338 ‐ 10,504 27,338 16,834

Total U.S. Department of Health and Human Services 64,410 74,914 27,338 16,834

Total Expenditures of Federal Awards 564,242$ 1,240,229$ 980,621$ 304,634$

D ‐ Direct Funding

I ‐ Indirect Funding

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

YEAR ENDED JUNE 30, 2013

(24)

NOTE 1 GENERAL INFORMATION The accompanying Schedule of Expenditures of Federal Awards presents the activities of the federal

financial assistance programs of Mastery Charter School – Clymer Elementary (the School). Financial awards received directly from federal agencies, as well as financial assistance passed through other governmental agencies or non‐profit organizations, are included in the schedule.

NOTE 2 BASIS OF PRESENTATION The accompanying Schedule of Expenditures of Federal Awards includes the federal grant activity of

the School and is presented on the accrual basis of accounting. The information in this schedule is presented in accordance with the requirements of OMB Circular A‐133, Audits of States, Local Governments, and Non‐Profit Organizations.

NOTE 3 RELATIONSHIP TO FINANCIAL STATEMENTS The Schedule of Expenditures of Federal Awards presents only a selected portion of the activities of

the School. It is not intended to, nor does it, present either the balance sheet, revenue, expenditures, or changes in fund balances of governmental funds. The financial activity for the aforementioned awards is reported in the School’s statement of activities and statement of revenue, expenditures, and changes in fund balance – governmental funds.

(25)

CliftonLarsonAllen LLP www.cliftonlarsonallen.com

An independent member of Nexia International

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN

ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

Board of Trustees Mastery Charter School – Clymer Elementary Philadelphia, Pennsylvania We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the governmental activities and the general fund of Mastery Charter School – Clymer Elementary, as of and for the year ended June 30, 2013, and the related notes to the financial statements, which collectively comprise Mastery Charter School – Clymer Elementary’s basic financial statements, and have issued our report thereon dated December 10, 2013. Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we considered Mastery Charter School – Clymer Elementary’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of Mastery Charter School – Clymer Elementary’s internal control. Accordingly, we do not express an opinion on the effectiveness of Mastery Charter School – Clymer Elementary’s internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

Board of Trustees Mastery Charter School ‐ Clymer Elementary

(26)

Compliance and Other Matters

As part of obtaining reasonable assurance about whether Mastery Charter School – Clymer Elementary’s financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the result of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

CliftonLarsonAllen LLP

Plymouth Meeting, Pennsylvania December 10, 2013

(27)

CliftonLarsonAllen LLP www.cliftonlarsonallen.com

An independent member of Nexia International

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE WITH REQUIREMENTS THAT COULD HAVE A DIRECT AND MATERIAL EFFECT ON EACH MAJOR PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE IN

ACCORDANCE WITH OMB CIRCULAR A‐133

Board of Trustees Mastery Charter School – Clymer Elementary Philadelphia, Pennsylvania Report on Compliance for Each Major Federal Program

We have audited Mastery Charter School – Clymer Elementary’s compliance with the types of compliance requirements described in the OMB Circular A‐133 Compliance Supplement that could have a direct and material effect on each of Mastery Charter School – Clymer Elementary’s major federal programs for the year ended June 30, 2013. Mastery Charter School – Clymer Elementary’s major federal programs are identified in the summary of auditors’ results section of the accompanying schedule of findings and questioned costs. Management’s Responsibility

Management is responsible for compliance with the requirements of laws, regulations, contracts, and grants applicable to its federal programs. Auditors’ Responsibility

Our responsibility is to express an opinion on compliance for each of Mastery Charter School – Clymer Elementary’s major federal programs based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and OMB Circular A‐133, Audits of States, Local Governments, and Non‐Profit Organizations. Those standards and OMB Circular A‐133 require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about Mastery Charter School – Clymer Elementary’s compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion on compliance for each major federal program. However, our audit does not provide a legal determination of Mastery Charter School – Clymer Elementary’s compliance. Opinion on Each Major Federal Program

In our opinion, Mastery Charter School – Clymer Elementary complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs for the year ended June 30, 2013.

Board of Trustees Mastery Charter School ‐ Clymer Elementary

(28)

Report on Internal Control Over Compliance

Management of Mastery Charter School – Clymer Elementary is responsible for establishing and maintaining effective internal control over compliance with the types of compliance requirements referred to above. In planning and performing our audit of compliance, we Mastery Charter School – Clymer Elementary’s internal control over compliance with the types of requirements that could have a direct and material effect on each major federal program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for each major federal program and to test and report on internal control over compliance in accordance with OMB Circular A‐133, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of Mastery Charter School – Clymer Elementary’s internal control over compliance. A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the result of that testing based on the requirements of OMB Circular A‐133. Accordingly, this report is not suitable for any other purpose.

CliftonLarsonAllen LLP

Plymouth Meeting, Pennsylvania December 10, 2013

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY SCHEDULE OF FINDINGS AND QUESTIONED COSTS

YEAR ENDED JUNE 30, 2013

(29)

Section I – Summary of Auditors’ Results

Financial Statements

1. Type of auditors’ report issued: Unmodified

2. Internal control over financial reporting:

Material weakness(es) identified? yes X no

Significant deficiency(ies) identified that are not considered to be material weakness(es)? yes X none reported

3. Noncompliance material to financial

statements noted? yes X no

Federal Awards

1. Internal control over major federal programs:

Material weakness(es) identified? yes X no Significant deficiency(ies) identified that are not considered to be material weakness(es)? yes X none reported

2. Type of auditor’s report issued on

compliance for major federal programs: Unmodified

3. Any audit findings disclosed that are required to be reported in accordance with section 510(a) of Circular A‐133? yes X no

Identification of Major Federal Programs CFDA Number(s) Name of Federal Program or Cluster 84.010 Pass‐Through Pennsylvania Department of Education

– Title I Improving Basic Programs 84.388 Pass‐Through Pennsylvania Department of Education

– ARRA – Title I School Improvement Grant Dollar threshold used to distinguish between Type A or Type B programs was: $ 300,000 Auditee qualified as low‐risk auditee pursuant to

OMB Circular A‐133? yes X no

MASTERY CHARTER SCHOOL – CLYMER ELEMENTARY SCHEDULE OF FINDINGS AND QUESTIONED COSTS

YEAR ENDED JUNE 30, 2013

(30)

Section II – Financial Statement Findings

Our audit did not disclose any matters required to be reported in accordance with Government Auditing Standards.

Section III – Findings and Questioned Costs – Major Federal Programs

Our audit did not disclose any matters required to be reported in accordance with Section 510(a) of OMB Circular A‐133.

Section IV – Prior Audit Findings

There were no prior year findings required to be reported under the Federal Single Audit Act.