masters' thesis in mathematics - diva

TRANSCRIPT

Methods for Pricing Derivatives Written on a Large Number

of Underlying Assets

Daniel Pérez Wikmark

U.U.D.M. Project Report 2003:17

Examensarbete i matematik, 20 poäng

Handledare och examinator: Johan Tysk

November 2003

Department of Mathematics

Uppsala University

Methods for Pricing Derivatives Written on Abstract a Large Number of Underlying Assets

Abstract

The aim of this thesis is to examine methods for pricing derivatives written on a large number

of underlying assets. In order to develop these methods the thesis studies one particular

derivative product in detail. The studied derivative is the Podium Plus zero coupon equity-

linked note issued by Credit Suisse First Boston. The thesis is mainly concerned with finding

a “fair” issue price for the note but to some extent, the price at an arbitrary time point is also

dealt with. The payoff for this note is entirely determined by the performance of an

underlying basket of 50 stocks in a non-linear way. At the date of maturity, the payoff is the

greater of SEK 10.000 and SEK 18.000 – (500 × the number of stock losses in the reference

portfolio). A stock loss occurs when a stock has an end value less that ninety per cent of the

start value, defining the end value as the lowest official closing price of the stock in a period

of 20 banking days immediately prior to the date of maturity.

After an introduction to arbitrage theory, the quest for an analytical formula for a “fair” issue

price begins. This approach requires so many simplifying assumptions that it fails in giving us

a reliable answer. Therefore, computer simulations based on the CAPM theory and on general

arbitrage theory are conducted. The results suggest that the note is substantially overpriced.

Two conclusions are drawn. The main conclusion is that the issue price of the Podium Plus is

above the “fair” price and that the issuer could therefore, in theory, find a way to make risk

free profits. The second conclusion is that the only way one could possibly justify the

excessively high issue price is to make unrealistic assumptions on the volatility of the

underlying stocks.

2

Methods for Pricing Derivatives Written on Table of Contents a Large Number of Underlying Assets

Table of Contents

1 PREFACE........................................................................................................................................................... 5 1.1 OBJECTIVE .................................................................................................................................................... 5 1.2 THE PODIUM PLUS NOTE .............................................................................................................................. 6 1.3 METHOD ....................................................................................................................................................... 7 1.4 DELIMITATION .............................................................................................................................................. 8 1.5 DISPOSITION.................................................................................................................................................. 8

2 THEORY .......................................................................................................................................................... 10 2.1 THE ONE PERIOD BINOMIAL MODEL .......................................................................................................... 10

2.1.1 Arbitrage Pricing of an Option in the One Period Binomial Model................................................... 10 2.1.2 The Martingale Measure .................................................................................................................... 11

2.2 THE COX-ROSS-RUBINSTEIN MODEL.......................................................................................................... 14 2.2.1 Arbitrage Pricing in the CRR Model .................................................................................................. 14 2.2.2 Convergence of the CRR Model ......................................................................................................... 15

2.3 CONTINUOUS TIME ARBITRAGE PRICING...................................................................................................... 16 2.3.1 The Wiener Process ............................................................................................................................ 16 2.3.2 Diffusion Processes and the Itô Integral ............................................................................................ 16 2.3.3 Martingales ........................................................................................................................................ 18 2.3.4 The Itô Formula.................................................................................................................................. 19 2.3.5 Geometric Brownian Motion and the Black-Scholes Framework ...................................................... 19 2.3.6 Risk Neutral Valuation in the Black-Scholes Model........................................................................... 20 2.3.7 Arbitrage and Completeness .............................................................................................................. 22 2.3.8 Valuation of Derivatives on Dividend Paying Stocks ......................................................................... 23 2.3.9 The Capital Asset Pricing Model........................................................................................................ 24 2.3.10 The Traditional Model...................................................................................................................... 30

3 ANALYSIS ....................................................................................................................................................... 33 3.1 NOTATION................................................................................................................................................... 33 3.2 THE SIMPLE MODEL WITH NON-CORRELATED STOCKS .............................................................................. 34

3.2.1 Model.................................................................................................................................................. 34 3.2.2 Calculation of the Issue Price............................................................................................................. 34

3.3 THE EXTENDED MODEL WITH NON-CORRELATED STOCKS......................................................................... 36 3.3.1 Model.................................................................................................................................................. 36 3.3.2 Calculation of the Issue Price............................................................................................................. 36

3.4 GENERALIZATION OF THE MODEL WITH NON-CORRELATED STOCKS. ........................................................ 41 3.4.1 Model.................................................................................................................................................. 41 3.4.2 Valuation at Arbitrary Time Point Prior to Observation Period........................................................ 41

3

Methods for Pricing Derivatives Written on Table of Contents a Large Number of Underlying Assets

3.5 A SIMPLE MODEL WITH CORRELATED STOCKS........................................................................................... 48 3.5.1 Model.................................................................................................................................................. 48 3.5.2 Calculation of the issue price ............................................................................................................. 48 3.5.3 Further Modelling with Correlated Stocks and Conclusions ............................................................. 51

4 PRICING BY MONTE CARLO SIMULATION ......................................................................................... 53 4.1 SETTING UP THE SIMULATION ..................................................................................................................... 53 4.2 ISSUE PRICE ................................................................................................................................................ 55 4.3 PRICE AS OF 2003-08-18 ............................................................................................................................. 55 4.4 REMARKS AND CONCLUSIONS..................................................................................................................... 56

5 SENSITIVITY ANALYSIS............................................................................................................................. 57 5.1 INTEREST RATE SENSITIVITY ...................................................................................................................... 58 5.2 VOLATILITY SENSITIVITY ........................................................................................................................... 60

6 CONCLUSIONS .............................................................................................................................................. 63 7 DISCUSSION AND CONCLUDING REMARKS........................................................................................ 65

7.1 ON CHOSEN MODELS .................................................................................................................................. 65 7.2 ON THE FAIRNESS OF THE ARBITRAGE PRICE.............................................................................................. 66

REFERENCES.................................................................................................................................................... 68 APPENDIX A – STOCK BASKET ................................................................................................................... 69

4

Methods for Pricing Derivatives Written on 1. Preface a Large Number of Underlying Assets

1 Preface

Since the burst of the IT bubble investors have become increasingly reluctant to direct

investments on the stock market. Investors that have made risky investments in the past and

lost money have become more and more interested in limiting risk taking, without having to

abandon the stock market altogether. Private banking institutions are therefore facing a new

demand – a demand for stock-related securities with limited risk of losing money. These

structured derivatives range from simple packages of stock indices and put options to rather

sophisticated creations. While the former group of products easily can be valued by

decomposing them into, for instance, the underlying asset and options written on this asset,

the latter is harder to deal with. Clearly, this opens for the possibility that such securities trade

at prices that deviate substantially from the “fair” price.

1.1 Objective

The aim of this thesis is to examine methods for pricing derivatives written on a large number

of underlying securities. In order to explore the examined methods, the thesis estimates the

“fair” value of a sophisticated stock-related security. This price will be compared to the price

at which the issuing institution offers to sell the security (or offers to buy the security). Also,

the thesis will try to estimate parameters that are specified implicitly by a given price, in order

to judge whether this price is reasonable or not.

The security used in the thesis for exemplifying purposes is the Podium Plus note. The

Podium Plus is presented in more detail below.

5

Methods for Pricing Derivatives Written on 1. Preface a Large Number of Underlying Assets

1.2 The Podium Plus Note

The Podium Plus is a zero coupon note, issued by Credit Suisse First Boston (CSFB), whose

return is determined by the performance of an underlying basket of stocks. Appendix A

contains a list of the stocks that make up the reference portfolio. Under normal circumstances,

Hagströmer & Qviberg (H&Q) will provide a purchase price for the Podium Plus.

The face value of the Podium Plus is SEK 10,000 and its term of maturity is four years, 18

June 2003 to 18 June 2007. Podium Plus is sold and marketed in Sweden by several brokerage

firms, among them H&Q and Acta. Its issue price is 100 per cent, i.e. SEK 10,000.

On the date of expiry, the holder of the note is guaranteed to receive the face value but there is

also a possibility of getting an additional return of up to SEK 8,000 per note. The return is

determined by the performance of an underlying basket of both Swedish and foreign stocks.

The stocks that make up this reference portfolio are the 40 biggest corporations in the Dow

Jones Global Titans 50 Index and the 10 biggest stocks on the Stockholm Stock Exchange.

The final redemption amount to be received at the date of expiry, Φ, is calculated according to

the formula:

(1.1)

where n denotes the number of stock losses.

[ ]0),05.08.0(000,10max000,10 n⋅−⋅+=Φ

A stock loss occurs when the final price of a stock is strictly lower than 90 percent of the

official closing price of the stock at 18 June 2003. The final price of a stock is defined to be

the lowest official closing price of the stock during an observation period of 20 banking days

6

Methods for Pricing Derivatives Written on 1. Preface a Large Number of Underlying Assets

immediately prior to but excluding 19 June 2007. All possible values of the final redemption

amount are shown below in Figure 1.1.

0

2

4

6

8

10

12

14

16

18

20

0 5 10 15 20 25 30 35 40 45 50

Number of Losses

Fina

l Red

empt

ion

Am

ount

, kSE

K

Figure 1.1. Final redemption amount as a function of number of stock losses.

1.3 Method

The choice of the Podium Plus was made more or less at random among complex derivative

products available on the Swedish market and whose marketers provide second hand purchase

prices for the securities. The mathematical approach to the examination of the Podium Plus

will be arbitrage pricing, also known as martingale pricing. Some foundations of this theory

will be given in the theory section.

7

Methods for Pricing Derivatives Written on 1. Preface a Large Number of Underlying Assets

1.4 Delimitation

The thesis will focus on transactions between the issuing institution and the holder of the

security. This means that the price at which H&Q initially issues the notes, and the price at

which they later offer to buy them back, will be examined. Calculations which require

numerical methods are outside the scope of this thesis. Therefore, assumptions that ease the

complexity of some calculations are required and made. Furthermore, the thesis is restricted to

analysis within the Black and Scholes framework, i.e. stock prices are modelled as geometric

Brownian motions.

1.5 Disposition

Section 2 is a brief exposition of the mathematical theory used in this thesis. This thesis is

only concerned with so called arbitrage pricing or martingale pricing. To highlight the basic

concepts behind this theory we begin examining the simplest possible discrete model of a

stock market. Then we expand the model to a continuous one which will be used in the

analysis of the Podium Plus. Arbitrage pricing in continuous time uses arguments similar to

those in the binomial models. The main difference is that it requires more advanced

mathematical tools. These will be introduced, but focus will lie on explaining fundamental

ideas behind arbitrage pricing. Rather than proving basic results readily available in a vast

quantity of texts on option pricing the texts points out similarities between intuitively

graspable concepts in discrete models and their counterparts in continuous time. An

introduction to the Capital Asset Pricing Model (CAPM) concludes the theory section. It will

be shown how a CAPM consistent single index model can be used to incorporate

interdependence between different stocks in a stock market. The more traditional way of

modelling stock markets with correlated stocks will also be presented briefly.

8

Methods for Pricing Derivatives Written on 1. Preface a Large Number of Underlying Assets

In Section 3, an analysis of the arbitrage free price of the Podium Plus is performed. In order

to explore our pricing problem in a more practical way we start our analysis of the Podium

Plus assuming an extremely simplified model and removing the most disturbing property of

the Podium Plus, the observation period. Then we gradually allow the model to grow more

and more realistic.

Having determined all necessary indata, evaluating the different expressions in Section 3 is

purely a matter of numerical analysis and falls outside the scope of this thesis. For the

practically inclined reader, Section 4 will give a rather precise estimate of the arbitrage free

issue price for the Podium Plus based on simulation.

Section 5 discusses the sensitivity of the price of the Podium Plus to changes in volatilities of

the underlying stocks and the risk free interest rate. Conclusions are collected in Section 6 and

a closing discussion on the findings of this thesis and the methods used to reach those will be

conducted in Section 7.

9

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

2 Theory

2.1 The One Period Binomial Model

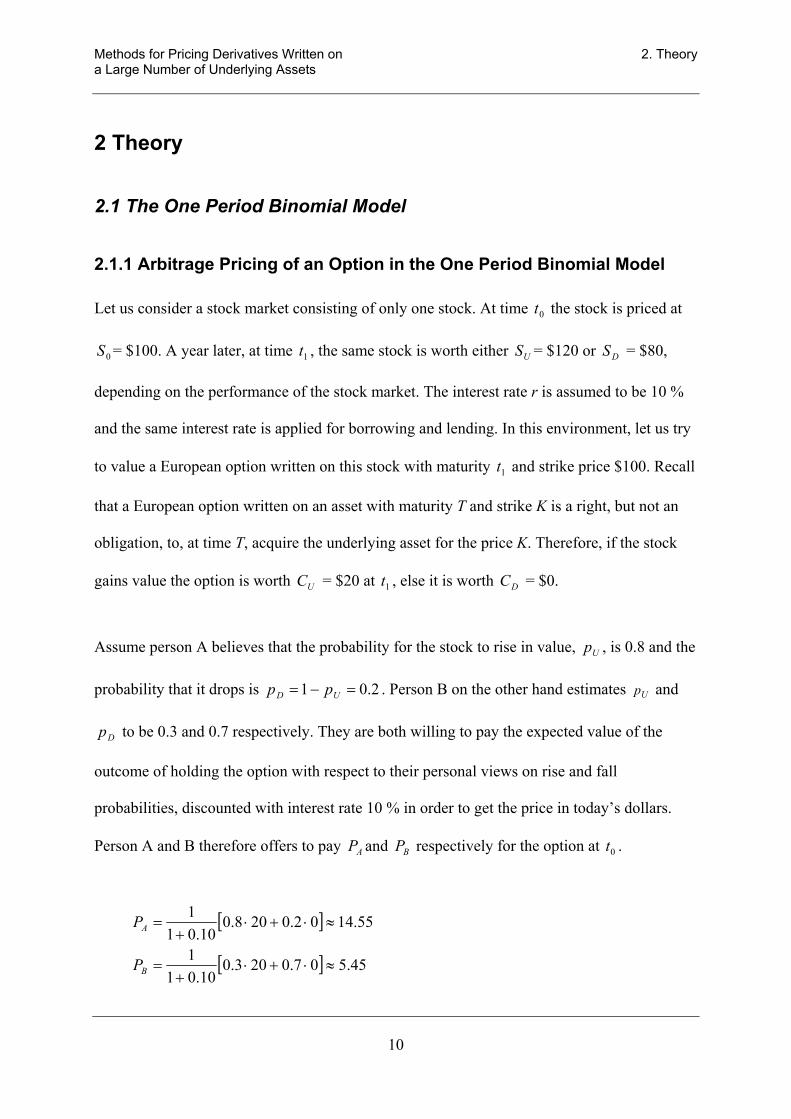

2.1.1 Arbitrage Pricing of an Option in the One Period Binomial Model

Let us consider a stock market consisting of only one stock. At time t the stock is priced at

= $100. A year later, at time t , the same stock is worth either = $120 or S = $80,

depending on the performance of the stock market. The interest rate r is assumed to be 10 %

and the same interest rate is applied for borrowing and lending. In this environment, let us try

to value a European option written on this stock with maturity and strike price $100. Recall

that a European option written on an asset with maturity T and strike K is a right, but not an

obligation, to, at time T, acquire the underlying asset for the price K. Therefore, if the stock

gains value the option is worth C = $20 at , else it is worth C = $0.

0

0S 1

U

US

D

D

1t

1t

Assume person A believes that the probability for the stock to rise in value, , is 0.8 and the

probability that it drops is

Up

2.01 =−= UD pp

AP

. Person B on the other hand estimates and

to be 0.3 and 0.7 respectively. They are both willing to pay the expected value of the

outcome of holding the option with respect to their personal views on rise and fall

probabilities, discounted with interest rate 10 % in order to get the price in today’s dollars.

Person A and B therefore offers to pay and respectively for the option at .

Up

Dp

BP 0t

[ ]

[ ] 45.507.0203.010.01

1

55.1402.0208.010.01

≈⋅+⋅+

=

≈⋅+⋅+

=

B

A

P

P 1

10

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

Obviously, person A and B cannot agree on a common price for the option. Now consider

instead person C. At , person C wants to buy a portfolio consisting of s shares and $ b in

cash with the property that at t , regardless of the movement on the stock market, the

portfolio has the same value as the option. This is called a replicating portfolio for the option.

Mathematically, this means that s and b solve the following system of linear equations.

0t

1

−≈

⇔ =+ borrowing) indicatessign (minus 36.36010.180 bbs

= =+ 5.02010.1120 sbs

At , this portfolio costs 0 = $13.64 dollars to acquire. Hence, in order to rule

out the possibility of a “money machine”, arbitrage, the option must be worth 13.64 at t .

0t 36.361005. −⋅

0

Proof: Consider two cases:

1. The option is traded at a higher price than 13.64 at t : At , person C buys the replicating portfolio

and sells an option. He keeps the difference. At , his portfolio is worth exactly what he owes the

holder of the option. By definition of this portfolio, he has taken absolutely no risk but has made money.

0 0t

1t

2. The option is traded at a lower price than 13.64 at : At t , the person C buys the option and sells the

replicating portfolio. He keeps the difference. At t , his option is worth exactly the amount of money

he needs to buy back the portfolio. By definition of this portfolio, person C has taken absolutely no risk

but has made money.

0t

1

0

2.1.2 The Martingale Measure

The previous subsection showed that if a portfolio replicates the option then the following

system of equations must hold (with notation from previous subsection).

11

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

−−

−+

=

−=

⇔

==

++++

DU

DUDD

DU

D

U

D

U

SSCCS

Cr

b

SSs

CC

brsSbrsS

)(1

1)1()1(

− DU CC

(2.1)

At , this portfolio is worth 0t

−

+−+

=+ DDU

UU

DU

D CSS

CSSr

bsS1

000

+−−+ rSSSrS )1()1(1 (2.2)

Thus, this is the value of the option. If

DU

DDU

U SSq

SSq

−=

−= and

−+ )1()1( 00 (2.3) UD rSSSrS +−

are interpreted as probabilities ( UDUDUD SrSSqqqq ≤+⋅≤≥−= )1( provided 0, and 1 0

0 0

)

belonging to a new probability measure Q then the value of the option at time t , C , is equal

to

, 110 TDDUU CE

rCqCq

rC

+=+

+=

T

(2.4)

where C is the value of the option at the end of the period.

[ ] [ ]11 Q

12

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

Under the measure Q,

, 110 TDDUU SE

rSqSq

rS

+=+

+= (2.5) [ ] [ ]11 Q

i.e. the price process for the stock, deflated by the discount factor, is a Q-martingale and Q is

called a martingale measure for the discounted stock price process. This is equivalent to

saying that S/B is a Q-martingale, where S denotes the price process for a stock and B denotes

the price process for the bank account. The economic interpretation of this is that S measured

in today’s currency is a martingale. A more formal definition of a martingale is given by

formula (2.11) in Subsection 2.3.3. The point in defining the new measure Q is the following.

For proof a proof we refer to [M&R, p 17].

Risk neutral valuation in the one period binomial model (2.6)

The market consisting of a stock, a bank account and a derivative security is free

from arbitrage (and any derivative settled at T can be priced) if and only if there

exists a measure Q such that [BJÖ, pp 12-13]

[ ] [ DDUUTQ SqSq

rSE

rS +

+=

+=

11

11

0 ]. (2.6a)

In this case the price of any derivative χ settled at T, at t , 0 0χ , is given by

[ ] [ . 1

11

10 DDUUT

Q qqr

Er

χχχχ ++

=+

= ] (2.6b)

13

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

2.2 The Cox-Ross-Rubinstein Model

2.2.1 Arbitrage Pricing in the CRR Model

Let us now consider a model similar to the one in the previous subsection, but with several

time points, [0, 1,…, T], each at which the stock may move upwards or downwards. At each

of these time points we observe the stock prices , ,…, . Now define 0S 1S tS

.1 if and 1 if 1t11t1 <==>== ++++ δδδδ dS

uS t

tt

t11 ++ SS tt

Obviously )(1)( dPuP =−== δδ . Now,

.10= =ieSSt

ln∑t

iδ

We say that the price process for the stock follows an exponential random walk. In this model

let us try to value a path-independent derivative that settles at T.

1. At T – 1, we can use the replication strategy of the one period binomial model to get a

price for the derivative at T – 1 denoted by 1−Tχ .

2. At T – 2 we set up portfolios that replicate the behaviour of the derivative in [T – 2,

T – 1]. With the same method as above we now obtain a price at T – 2 denoted by

2−Tχ .

14

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

3. Continue backwards until t = 0 where the price of the derivative is 0χ . This price is

arbitrage free provided that d < 1 + r < u [M&R, p 35].

In this model, as in the one period model, the subjective probabilities are irrelevant when

pricing a derivative written on the stock. Even though they are not calculated here, there exist

martingale probabilities for the stock movements upwards and downwards that are determined

by the magnitude of the stock movements u and d, and the interest rate.

2.2.2 Convergence of the CRR Model

Although the CRR model yields more accurate estimates than the one period binomial model,

it is relevant in this thesis mainly because of its asymptotic behaviour. As we let the number

of periods in a given time interval tend to infinity, the behaviour of the stock price process

resembles more and more the geometric Brownian motion [M&R, p 41]. The reason for this is

that the probability of reaching the various end nodes in the CRR model is binomially

distributed. If the number of periods in the model is large enough, the binomial distribution

can be approximated by a normal distribution. The return from holding a stock can be written

as , where n is the number of periods in the model and k is the total number

of upward stock movements. This return is then normally distributed and therefore the stock

price is log-normally distributed, just as in the geometric Brownian motion case. In the limit,

the stock price process is governed by the dynamics of a geometric Brownian motion whose

parameters are specified entirely by u, d and the interest rate r.

dknuk ln)(ln −+

This allows us to model arbitrage free stock markets as geometric Brownian motions, and this

is the approach that will be used in this thesis.

15

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

2.3 Continuous time arbitrage pricing

2.3.1 The Wiener Process

A stochastic process W is a Wiener process (Brownian motion) if the following conditions all

hold.

1. W(0) = 0.

2. W has independent increments, i.e. if s ≤ t ≤ u ≤ v, W(t) – W(s) and W(v) – W(u) are

independent stochastic variables.

3. If s ≤ t, ( ) ),0()()( stNsWtW −∈− where ),0( stN − denotes the normal

distribution with mean 0 and standard deviation st − .

4. W has continuous trajectories.

2.3.2 Diffusion Processes and the Itô Integral

A diffusion process, X, is a stochastic process that is driven by a drift term, which is a

function of time and the current value of the process, and a stochastic diffusion term, which is

also a function of time and the current value of the process. It can be approximated by

stochastic difference equations of the type

, (2.7)

process Wiener a is and )()( where WtWttWW −∆+=∆

))(,())(,()()( WtXtttXttXttX ∆+∆=−∆+ σµ

16

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

Trying to solve this equation for X, perhaps we would divide by ∆t and led ∆t tend to zero.

We would then get, if X(0) = , 0x

=

+=

0)0(

))(,())(,(

xXdt

tXttXtdt

σµ )(tdWdX

(2.8)

However, dt

tdW )( is not defined (W is not differentiable anywhere). Therefore, let us keep the

stochastic differential of X,

(2.9) = 0)0( xX += )())(,())(,( tdWtXtdttXtdX σµ

tt

and interpret this as,

(2.10) .)())(,())(,()(00

0 ∫∫ ++= sdWsXsdssXsxtX σµ

This leaves us with a solution for X in terms of the new creature . This can

be interpreted as a so called Itô-integral. We will not go deeper into Itô-integrals here. Still, it

is important to mention that they are often difficult to calculate in any explicit way, but they

have interesting properties (f and g are functions and c is a constant) [ØKS, p 30],

∫t

sdWsXs0

)())(,(σ

1. ∫ ∫∫ +=T

S

T

U

U

S

tfdWtfdWtfdW )()()(

17

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

2. ∫ ∫∫ +=+T

S

T

S

T

S

tgdWtfdWctdWgcf )()()()(

3. 0)( =

∫T

S

tfdWE

4. is F∫T

S

tfdW )( T-measurable.

The third statement implies that Itô-integrals are martingales, i.e. they are stochastic processes

without systematic drift. This is a very important property and it makes Itô-integrals

convenient for financial modelling. Also the fourth statement needs explanation. FT can be

thought of as all information available at time T. If an expression is FT-measurable then it is

possible to determine the value of the expression given the information collected up to time T.

Statement four then says that it is possible to determine the value of the given integral at time

T.

2.3.3 Martingales

A martingale is a stochastic process X that does not explode, is FT-measurable and satisfies

(for all s ≤ t) [BJÖ, pp 33-34],

E[X(t) FS] = X(s). (2.11) ׀

18

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

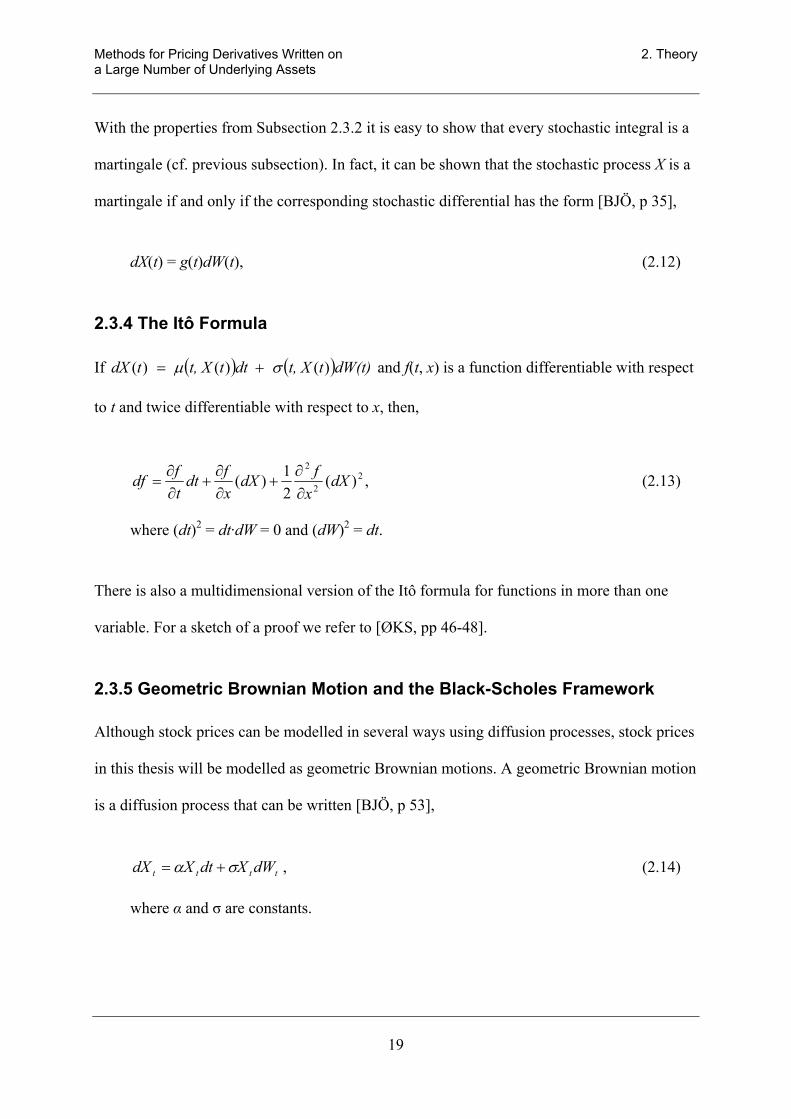

With the properties from Subsection 2.3.2 it is easy to show that every stochastic integral is a

martingale (cf. previous subsection). In fact, it can be shown that the stochastic process X is a

martingale if and only if the corresponding stochastic differential has the form [BJÖ, p 35],

dX(t) = g(t)dW(t), (2.12)

2.3.4 The Itô Formula

If ( ) ( )dW(t)tt, X dt tt, X tdX )()()( σµ += and f(t, x) is a function differentiable with respect

to t and twice differentiable with respect to x, then,

,)(2

)( 2 dX1 22

xfff ∂∂∂

tttt dWXdtXdX

dXx

dtt

df∂

+∂

+∂

= (2.13)

where (dt)2 = dt·dW = 0 and (dW)2 = dt.

There is also a multidimensional version of the Itô formula for functions in more than one

variable. For a sketch of a proof we refer to [ØKS, pp 46-48].

2.3.5 Geometric Brownian Motion and the Black-Scholes Framework

Although stock prices can be modelled in several ways using diffusion processes, stock prices

in this thesis will be modelled as geometric Brownian motions. A geometric Brownian motion

is a diffusion process that can be written [BJÖ, p 53],

, (2.14)

where α and σ are constants.

σα +=

19

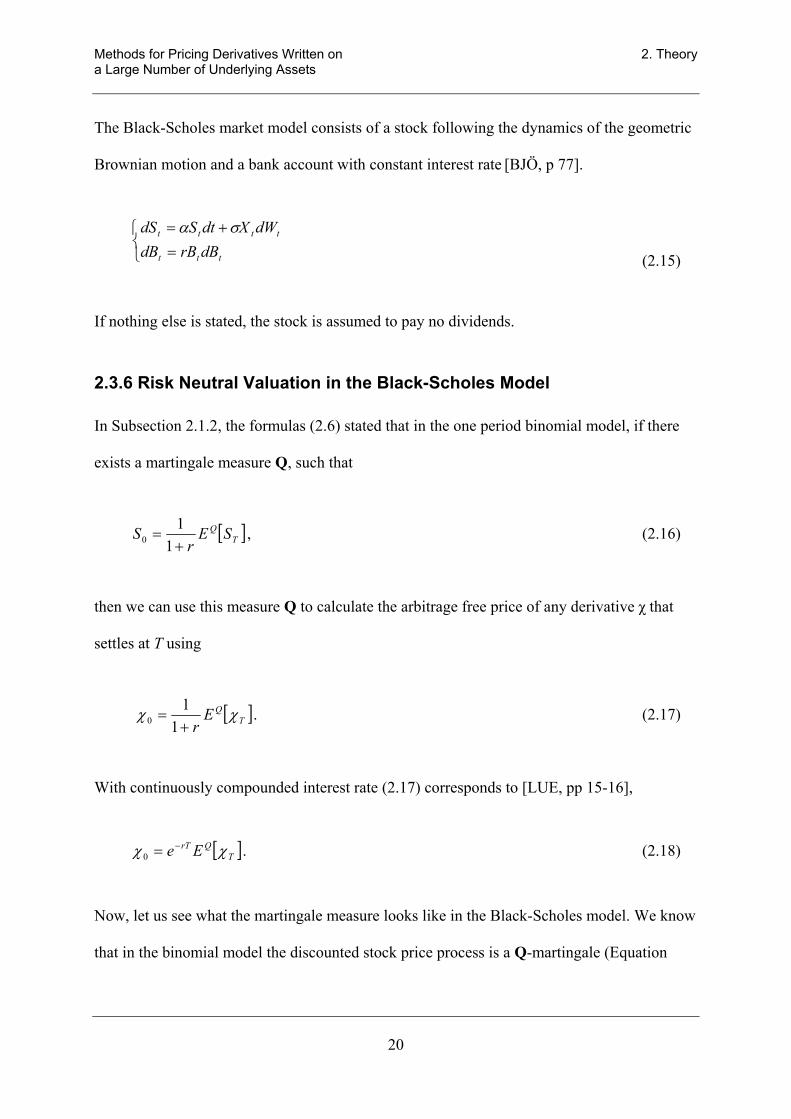

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

The Black-Scholes market model consists of a stock following the dynamics of the geometric

Brownian motion and a bank account with constant interest rate [BJÖ, p 77].

(2.15) = ttt dBrBdB += tttt dWXdtSdS σα

If nothing else is stated, the stock is assumed to pay no dividends.

2.3.6 Risk Neutral Valuation in the Black-Scholes Model

In Subsection 2.1.2, the formulas (2.6) stated that in the one period binomial model, if there

exists a martingale measure Q, such that

[ ]1 Q= , 10 TSE

rS

+ (2.16)

then we can use this measure Q to calculate the arbitrage free price of any derivative χ that

settles at T using

[ ]1 Q

[ ]. 0 TQrT Ee χχ −=

. 1 TE

rχ

+0χ = (2.17)

With continuously compounded interest rate (2.17) corresponds to [LUE, pp 15-16],

(2.18)

Now, let us see what the martingale measure looks like in the Black-Scholes model. We know

that in the binomial model the discounted stock price process is a Q-martingale (Equation

20

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

2.16). If we assume that this holds in the continuous time case as well, the following

relationship must hold,

(2.19) [ ] .0rt

TQ eSSE =

[ ] tt eSSE α

0=

tttt dWXdtrXdX

Furthermore, we can calculate the expected value of a process that follows the dynamics of

the geometric Brownian motion in Equation (2.14).

(2.20)

So, if we modify the process to

(2.21) σ+=

then (2.19) holds. Now we can think of the operation [ ]TQ SE as taking the expected value of

, but with the drift of S changed from α to r. TS

Having defined we state that Equation (2.18) holds in the continuous time case also for

a contract settled at T. This conclusion can also be reached using the Itô formula on the price

process of the derivative, arbitrage arguments and finally applying Feynman-Kac’s stochastic

representation formula on the result.

[ ]⋅QE

21

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

Risk neutral valuation in Black-Scholes model (2.22)

In the Black-Scholes model, the price of any derivative χ settled at T, at 0t , 0χ , is

given by

[ ], 0 TQrT Ee χχ −= (2.22a)

where, assuming the stock follows the dynamics of the geometric Brownian

motion, EQ[…] is equivalent to taking expected values but with the stock

following the Q-dynamic,

tttt dWXdtrXdX σ+= (2.22b)

If the price of the derivative depends on the price of several underlying assets,

then the expected value must be taken with respect to the respective Q-dynamic

for each of those assets.

2.3.7 Arbitrage and Completeness

When building stock market models for derivative arbitrage pricing purposes, one has to

consider two important properties of the model, absence of arbitrage and completeness. A

market model is said to be arbitrage free if there are no investment strategies that yield a

positive expected amount of money starting with $0, without risk of losing money [M&R, p

232]. If the market is arbitrage free then there are two possibilities. Either any derivative

written on the assets in the model can be replicated using the assets in the model or it cannot.

In the first case we say that the market model is complete, in the second case we say that the

22

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

market model is incomplete [BJÖ, p 99]. If a stock market model is arbitrage free and

complete then any derivative can be assigned a unique arbitrage free price consistent with the

prices of the underlying assets in the stock market model. In general, we have the following

result:

A stock market model with A traded underlying assets (not counting the risk free asset)

and R sources of randomness (for instance Wiener processes) is arbitrage free and

complete if and only if A = R [BJÖ, p 106]. (2.23)

2.3.8 Valuation of Derivatives on Dividend Paying Stocks

For a derivative that settles at T written on a stock that pays dividends at discrete time points,

the pricing formula (2.22a) has to be slightly modified. In addition to the previous setup, we

remove the no dividends constraint in Subsection 2.3.5 and assume that n dividends are paid

in (0, T]. We assume that a dividend paid at t , u

, (2.24)

where δ is a constant and u ∈ (0, T].

uu S⋅= δδ

We also assume that the stock at the moment of the payout of the dividend loses exactly the

dividend in value. Then [BJÖ, p 160],

))1(,(),( 0 stFstF n ⋅−= δδ , (2.25)

where is the price of the derivative on the dividend paying stock at time t and

is the price at time t of the same derivative on the same stock assuming that the

stock would pay no dividend in (0, T] and thus completely follow the previous setup.

),( stF δ

),(0 stF

23

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

From now on δ for a stock will be referred to as the dividend fraction.

2.3.9 The Capital Asset Pricing Model

Up until now, we have only discussed how to model the behaviour of one single stock. Of

course, the Black-Scholes framework of Subsection 2.3.5, and in particular (2.15), could be

used to model many stocks as well, but this setup would not take into account that stock

prices for different stocks often are correlated to one another. Therefore, the Black-Scholes

model needs some modifications before we can model correlated stock prices realistically.

Björk (1998) and Musiela & Rutkowski (1997), for instance, use this setup to model n

interdependent stocks.

nidWSdWSdWSdtSdS niiniiiiiii 1,...,for ...2211 =++++= σσσα (2.26)

This appears to be a standard way to model correlated stock prices in mathematical finance,

but it has two major drawbacks. It requires that a 50 50× correlation matrix is estimated

before we can even start working with the model and once we do, it is very cumbersome to

have 50 Wiener processes in the expression for each stock price process. We would wish for a

model with maximum two Wiener processes for each stock. Let us therefore abandon the

traditional model and glance at the Capital Asset Pricing Model (CAPM). Subsection 2.3.10

gives an idea of the calculations required when estimating the 2500 σ:s of the traditional

model.

The CAPM is a simple yet popular asset pricing model among economists. It can be used in

various contexts and will in this thesis form the basis for stock market models which

incorporate correlation between stocks in the Podium Plus stock basket. For more information

24

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

on the CAPM, refer to [BKM, pp 258-291]. For our use it is enough to know that every stock

is characterized by a real number β with the property that for a time interval, say [0, t], and

under P [LUE, pp 177-181],

( )

( ) ( )( ),)()()()( and )()()()()(

trtrEtrtrEttrtrtrtr

ms

ms

−⋅=−+−⋅=−

βεβ

(2.27)

where for any asset X,

=

0

ln)(XXt t

X

)(tr

)(t

r is the continuously compounded return

from holding the stock in [0, t], is the continuously compounded risk free

interest rate for the same period, ε is an error term, S is the stock and M is

the stock market portfolio. Note that the time dependence of returns and error

terms are suppressed below.

Assume that the stock market (market portfolio) M, a stock S and the risk free asset B are

modelled

rBdtdB

SdWSdWSdtdSMdWMdtdM

MbSaS

MMM

=++=

+=σσα

σα (2.28)

Since the market portfolio is merely a weighted sum of stocks obeying geometric Brownian

motions it is strictly speaking a logical flaw to assume that the market portfolio also obeys a

geometric Brownian motion. The reason is that the sum of geometric Brownian motions is not

a geometric Brownian motion itself. However, this assumption is made for simplicity.

25

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

We will need expressions for Mt and St. M is a standard geometric Brownian motion, so

[BJÖ, p 56]

. 21exp 2

0

+

−= MMMMt WtMM σσα (2.29)

For St,

++

+−=

++

+−+=

++

+−

==++=

MbSabaSt

MbSabaSt

MbSabaS

MbSaS

WWtSS

WWtSS

dWdWdt

SdSdWSdWSdtdS

σσσσα

σσσσα

σσσσα

σσα

)(21exp

)(21lnln

)(21

2.3.4 Subsection of formula Itô The)(ln

220

220

22 (2.30)

Now let us calculate the distributions for r and . M Sr

+

+−∈

−∈

++

+−==

+

−==

ttNr

ttNr

WWtSSr

WtMMr

babaSS

MMMM

MbSabaSt

S

MMMMt

M

2222

2

22

0

2

0

,)(21

,21

)(21ln

21ln

σσσσα

σσα

σσσσα

σσα

(2.31)

26

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

We conclude that the market volatility is indeed Mσ and that the volatility of the stock

[BJÖ, p 93]

. 22baS σσσ += (2.32)

Furthermore

[ ] [ ] [ ]

( )( )[ ]

ttKKttKK

tKKWtKWWtKE

rErErrErrCov

MbSMMbSM

SMMMMMbSaS

MSMSMS

σσσσ

σσσ

=−+

=

=−+++

==−=

22

2

2.3.4section -Sub of rules

tionmultiplicanotation equivalent),(

(2.33)

Using standard linear regression [B&H, p 154],

. )(

),(M

b

M

MS

rVarrrCov

σσβ == (2.34)

Or equivalently,

. Mb βσσ = (2.35)

Since we already have the standard deviation of , i.e. the volatility of S denoted by Sr Sσ ,

0 assuming , 222

22222

≥−=

+=+=

aMSa

MabaS

σσβσσ

σβσσσσ (2.36)

27

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

Now we have determined aσ and bσ in terms of the market volatility and the stock volatility.

The last thing we need to calculate before we can write up our CAPM-consistent stock price

model is Sα . Recall from (2.27) that

( ) ( )

( ). )()(and

rrErrErrrr

ms

ms

−⋅=−−⋅−−=

ββε

(2.37)

We note that

−−

−+−∈ tttrtNt aMMSS σσαβσαβε ,

21

21)1()( 22 , (2.38)

or equivalently that aσ is the volatility which is not explained by the market index volatility.

This is clearly consistent with our setup (2.28). But (2.37) implies that E[ε] = 0. Then,

)1()(

21

021

21)1(

22

22

ββσσβαα

σαβσαβ

−+−+=

=

−−

−+−

r

ttrt

MSMS

MMSS

(2.39)

and,

[ tN aσε ,0∈ ]. (2.40)

We can now write down our CAPM-consistent model for the stock market. Having noted that

aσ is the variation is the stock’s price that cannot be explained by market variations, we will

refer to it as the firm specific volatility. On the other hand, bσ is the volatility in the stock

28

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

price due to fluctuations in the market index. It will therefore from now on be called the

systematic volatility.

rBdtdBidWSdWSdtSdS

MdWMdtdM

MibiiiaiiSii

MMM

==++=

+=1,...,50for σσα

σα (2.41)

where

Mσ is the volatility of the market portfolio,

iσ is the volatility of stock i,

)(),(

M

MSi rVar

rrCovi=β ,

)1()(21 22

iMiiMiSi r βσβσαβα −+−+= ,

Mibi σβσ = is the volatility explained by the stock’s beta value and

222Miiai σβσσ −= is the idiosyncratic volatility.

Under Q,

rBdtdB

idWSdWSrdtdSMdWrMdtdM

Mibiiiaii

MM

==++=

+=1,...,50for σσ

σ (2.42)

Note that CAPM is based on the relationship between a traded asset and the universe of all

traded assets. When we replace the universe of all traded assets with a specific market index,

we should really call our model a single index model. However, the single index model allows

for systematic return other than that explained by the β whereas the CAPM does not. Our

29

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

model is thus a hybrid. Hence it should rather be called a CAPM consistent model than a pure

CAPM model.

2.3.10 The Traditional Model

Let’s assume that n stocks on a stock market are governed by

nidWSdWSdWSdtSdS niiniiiiiii 1,...,for ...2211 =++++= σσσα

Then

niniii

niniiniii

ii

niniiniiii

niniiniiii

niniiniii

WWtKr

WWtS

tSr

WWtStS

WWtStS

dWdWdtSd

σσ

σσσσα

σσσσα

σσσσα

σσσσα

+++=

+++

++−==

++++

++−=

++++

++−+=

+++

++−==

...

...)...(21

)0()(

ln

...)...(21exp)0()(

...)...(21)0(ln)(ln

...)...(21formula Itô)(ln

11

1122

1

1122

1

1122

1

1122

1

Now,

[ ][ ] ttKKtttKKE

tKKWWtKWWtKE

rErErrErrCov

BnAnBABABnAnBABA

BAnBnBBnAnAA

BABABA

)...(...

)...)(...(

)()()(),(

112

112

21111

σσσσσσσσ

σσσσ

++=−+++

=−++++++

=−=

30

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

If we view the σ:s corresponding to one stock as a row vector we get

product)inner thedenotes (where ...

),...,(

11

1

••=++=

BABnAnBA

inii

σσσσσσσσσ

Assuming that we drop t and adjust our estimated covariances correspondingly, we can now

collect all the σ:s in a matrix. Recall that the covariance of a random variable with itself is the

variance of the random variable.

CSS

SSSS

SSSS

T

nnn

nT

nnn

n

nnn

n

=

=

),cov(...),cov(.........

),cov(...),cov(

............

...

............

...

1

111

1

111

1

111

σσ

σσ

σσ

σσ

Since Cov(X, Y) = Cov(Y, X) we only have as many restrictions on the σ:s as there are

elements in an upper triangular matrix of the same size as S and C. Therefore, we are able to

determine the same number of σ:s in terms of the others. An excellent way of using our

degrees of freedom would be to state that S is symmetrical. In effect this is to say that we keep

as many unknowns as there are elements in an upper triangular matrix, or equivalently, as

there are restrictions. Now we have that

CS =2

Theoretically this equation is easily solved. Since C is symmetric, it can be written as 1−PDP ,

where D is a diagonal matrix and P is an invertible matrix [LAY, p 446]. This is done by

computing the eigenvalues and eigenvectors for C. Recall that we are only interested in one

solution for S with positive numbers on the diagonal corresponding to the stock volatilities.

31

Methods for Pricing Derivatives Written on 2. Theory a Large Number of Underlying Assets

Now set , where E is the diagonal matrix whose non-zero elements are the positive

square roots of the corresponding elements in D. Now

1−= PEPS

PEP−1 S =2 CPDPPPEEPPPPEPEP ==== −−−−− 112111 ))()(())((

Thus, this is a perfectly valid solution for S.

Note that the covariance matrix C must be positive definite to rule out the possibility of

portfolios with negative variances [BKM, p 293]. Since we have to estimate C based on past

data, we cannot guarantee that this will always be the case. This is another argument for not

using the traditional model in our analysis.

32

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

3 Analysis

3.1 Notation

Throughout the thesis indices and arguments will be used synonymously depending on the

context. For instance, )0( and 0 ππ mean the same thing. Throughout this section, we will

adhere to the following notation, unless otherwise stated:

tπ Price of contract at t.

Payoff function of the Podium Plus, where is to be regarded as a vector.

Probability under Q.

Bin[n, p] The binomial distribution.

N[µ, σ] The normal distribution.

Re[a, b] The rectangular distribution with evenly distributed probability mass from a to b.

The cumulative normal distribution at x.

T Time to maturity.

)TS

)

)x

(Φ

(⋅Q

(N

TS

Other variables are explained as they appear.

33

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

3.2 The Simple Model with Non-Correlated Stocks

3.2.1 Model

Assumptions: The fifty stocks in the reference portfolio are uncorrelated and have the same

volatilities σ. Final price for each stock is the closing price at 18 June 2007 (i.e. no

observation period).

(3.1) dttrBtdB

idWtSdttStdS iiiii

)()(1,...,50 (t))()()(

==+= σα

3.2.2 Calculation of the Issue Price

The arbitrage pricing formula (2.22a) directly gives

[ ]

[ ] ).16(000.10)15(500.10...)0(000.18)(

where

,)(0

≥⋅+=⋅++=⋅=Φ

Φ= −

nQnQnQSE

SEe

TQ

TQTrπ

(3.2)

Since the probability that a stock loss occurs in a stock is independent from stock losses in

other stocks in this model, n ∈ Bin[50, p] where p is the probability for a stock loss to occur.

For any stock S under Q [B&S, p 114]

+−= tt WtrsS σσ )2

(exp2

0 . (3.3)

34

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

Now, Property 3 in Subsection 2.3.1 yields,

−∈= TTrN

sS

X T σσ ,)2

(ln2

0

. (3.4)

Thus

−−

=<=<=T

TrNXQsSQp T σ

σ )2

(9.0ln)9.0ln()9.0(

2

0 . (3.5)

Recalling that if then , we can easily

calculate the arbitrage price for the Podium Plus using expression (3.2).

[n,pX Bin∈ ] knkX pp

kn

kXPkp −−

=== )1()()(

[ ]

−−

=

−

+−

⋅+

+−

⋅+−

⋅

=≥⋅+=⋅++=⋅=

∑=

−

−

−

T

TrNp

ppi

pp

ppppe

nQnQnQe

i

ii

Tr

Tr

σ

σ

π

)2

(9.0ln where

)1(50

000.10)1(1550

500.10

...)1(150

500.17)1(0

50000.18

)10(000.10)17(500.10...)0(000.18

2

50

16

503515

491500

0

(3.6)

35

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

If we assume that the underlying stocks pay dividends n times during the term of maturity,

each in accordance with (2.24) and with the same constant rate δ, then p in formula (3.6) has

to be replaced by , δp

. )

2(

)1(9.0ln

))1(

9.0ln()9.0)1((

2

0

−−

−=

−<=<−=

T

TrNXQsSQp

n

nn

T σ

σδ

δδδ (3.7)

By statement (2.23) the market model is complete and arbitrage free and the arbitrage price

calculated here is thus unique.

3.3 The Extended Model with Non-Correlated Stocks

3.3.1 Model

Assumptions: The fifty stocks in the reference portfolio are uncorrelated and have the same

volatilities σ. Final price for each stock is min , where [a, T] is the observation period. [ ] uTau S,∈

(3.8) dttrBtdB

idWtSdttStdS iiiii

)()(1,...,50 (t))()()(

==+= σα

3.3.2 Calculation of the Issue Price

The only difference between this model and the model in Subsection 3.2 is that we now take

into account the observation period. This will change the parameter p in formula (3.6) but

leave the rest of the parameters unaffected. As in previous subsection we start with the

36

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

assumption that the underlying stocks pay no dividends. Then, if [a, T] is the observation

period and ms = , [ ] uTau S,min ∈

) . (3.9) 9.0( 0smQp s <=

Now we define a running minimum process ms as

. (3.10) [ ]

[ TatuStmtaus ,for )(min)(

,∈=

∈]

If the stock price process S under Q is at α at time a, i.e.

(3.11)

=+=

ασ

aSdWrdtdS

then the distribution function for ms is given by [BJÖ, p 183]

, )()(2exp)(

))(()(

2

)(

−

−+−⋅

−

⋅+

−

−−−

=<=

aTaTrxNxr

aTaTrxN

xTmQxF sTm

σα

σα

σα (3.12)

for x ≤ α and T > a.

Now p can be expressed as,

∫∞

⋅=<+<=

>⋅><+<=>∩<+<=

09.0)(00

0000

000

)()|9.0)(()9.0(

)9.0()9.0|9.0)(()9.0()9.09.0)(()9.0(

saSasa

aasa

asa

dfssTmQssQ

ssQsssTmQssQsssTmQssQp

ααα

(3.13)

37

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

The first factor under the integral sign is simply formula (3.12) using 0 as argument, 09. s

.

)(9.0)9.0(2exp

)(9.0

) |9.0)(Q(

0200

0

−

−+−⋅

−

⋅+

−

−−−

==<

aTaTrs

Nsr

aTaTrs

N

SsTm as

σα

σα

σα

α (3.14)

Also the second factor, fS(a)(α), can be calculated using (3.3).

∫

−−

∞−

−

=

−−

=<=

+−=

a

ars

t

aS

aa

dte

a

ars

NaSPF

WarsS

σ

σα

σ

σα

αα

σσ

)2

(ln

2

2

0)(

2

0

2

02

)2

(ln))(()(

)2

(exp

(3.15)

If F(t) is the primitive function of the integrand and g(α) is the upper limit of integration then

the last row of (3.15) equals,

. (3.16) ( )[ )()(lim)(lim)()(

)( rFgFdttfFr

g

rraS −==

∞→∞→ ∫ ααα

]

38

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

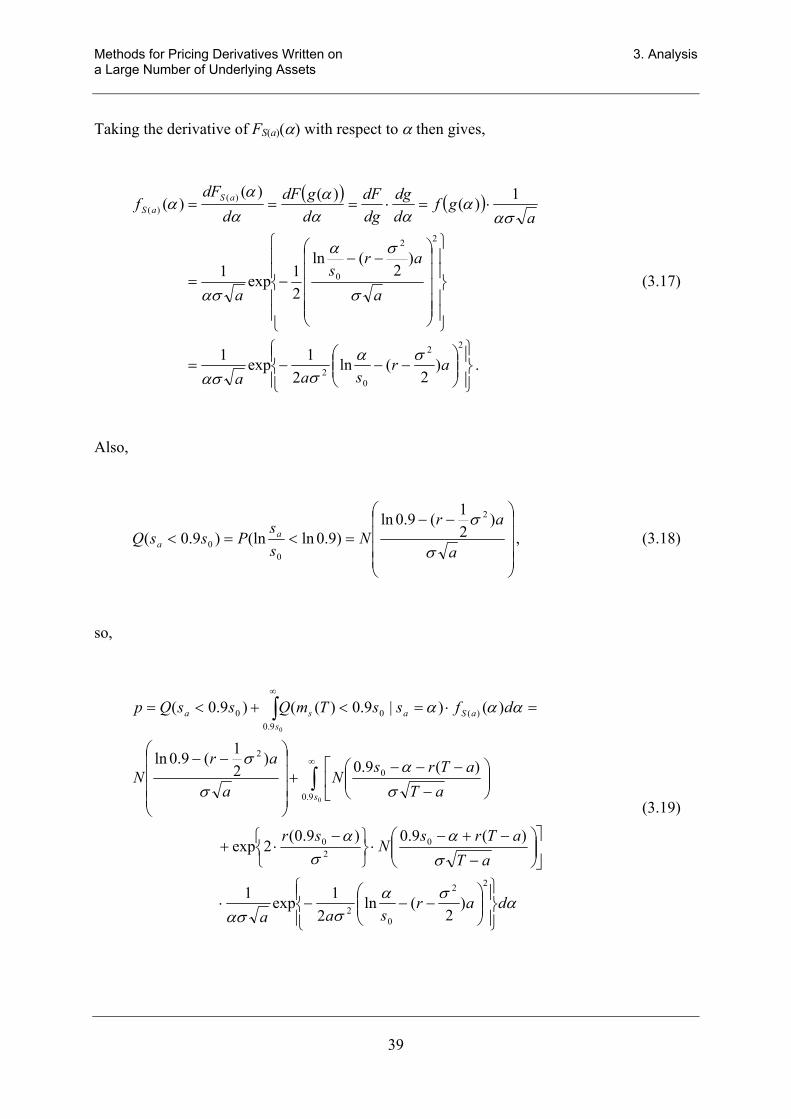

Taking the derivative of FS(a)(α) with respect to α then gives,

( ) ( )

. )2

(ln2

1exp1

)2

(ln

21exp1

1)()()()(

22

02

22

0

)()(

−−−=

−−

−=

⋅=⋅===

arsaa

a

ars

a

agf

ddg

dgdF

dgdF

ddF

f aSaS

σασασ

σ

σα

ασ

ασα

ααα

αα

α

(3.17)

Also,

−−=<=<

a

arN

ss

PssQ aa σ

σ )21(9.0ln

)9.0ln(ln)9.0(2

00 , (3.18)

so,

ασασασ

σα

σα

σα

σ

σ

ααα

darsaa

aTaTrs

Nsr

aTaTrs

Na

arN

dfssTmQssQp

s

saSasa

−−−⋅

−

−+−⋅

−

⋅+

−

−−−+

−−

=⋅=<+<=

∫

∫

∞

∞

22

02

020

9.0

0

2

9.0)(00

)2

(ln2

1exp1

)(9.0)9.0(2exp

)(9.0)21(9.0ln

)()|9.0)(()9.0(

0

0

(3.19)

39

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

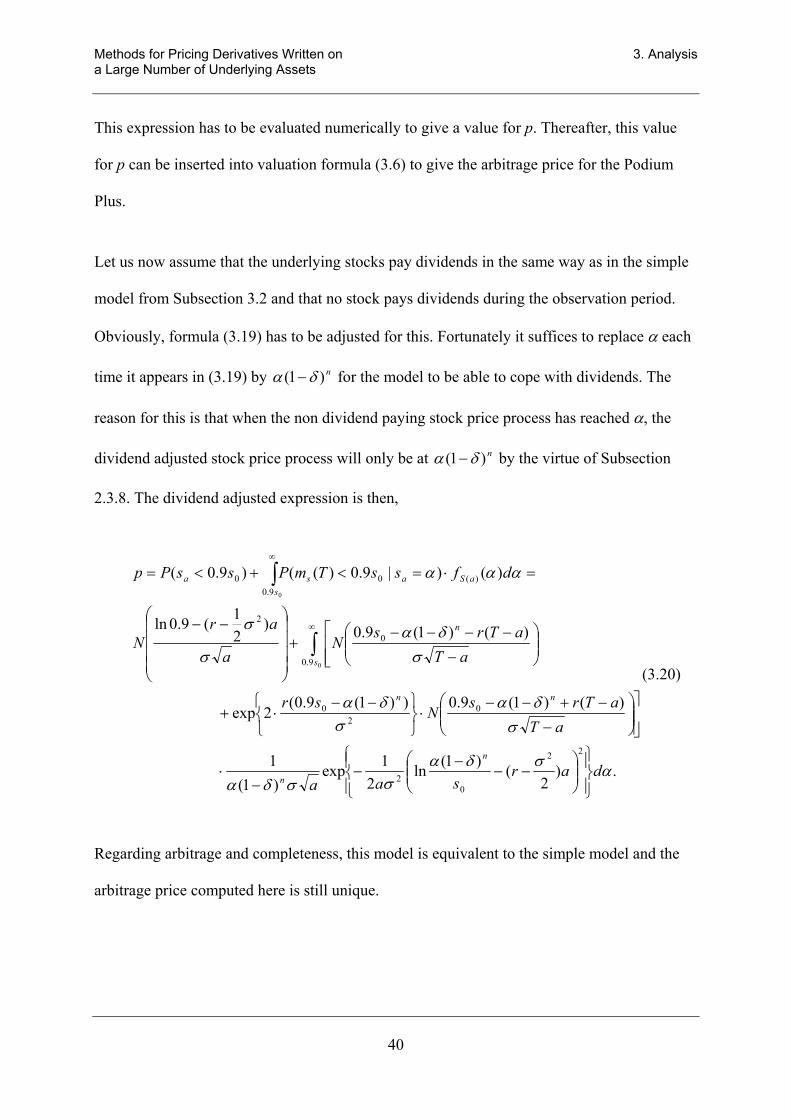

This expression has to be evaluated numerically to give a value for p. Thereafter, this value

for p can be inserted into valuation formula (3.6) to give the arbitrage price for the Podium

Plus.

Let us now assume that the underlying stocks pay dividends in the same way as in the simple

model from Subsection 3.2 and that no stock pays dividends during the observation period.

Obviously, formula (3.19) has to be adjusted for this. Fortunately it suffices to replace α each

time it appears in (3.19) by for the model to be able to cope with dividends. The

reason for this is that when the non dividend paying stock price process has reached α, the

dividend adjusted stock price process will only be at by the virtue of Subsection

2.3.8. The dividend adjusted expression is then,

n)1( δα −

n)1( δα −

.)2

()1(ln2

1exp)1(

1

)()1(9.0))1(9.0(2exp

)()1(9.0)21(9.0ln

)()|9.0)(()9.0(

22

02

02

0

9.0

0

2

9.0)(00

0

0

ασδασσδα

σδα

σδα

σδα

σ

σ

ααα

darsaa

aTaTrs

Nsr

aTaTrs

Na

arN

dfssTmPssPp

n

n

nn

s

n

saSasa

−−

−−

−⋅

−

−+−−⋅

−−

⋅+

−

−−−−+

−−

=⋅=<+<=

∫

∫

∞

∞

(3.20)

Regarding arbitrage and completeness, this model is equivalent to the simple model and the

arbitrage price computed here is still unique.

40

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

3.4 Generalization of the Model with Non-Correlated Stocks.

3.4.1 Model

Assumptions: The fifty stocks in the reference portfolio are uncorrelated. They may have

different volatilities and/or pay different dividends. Final stock price is determined by the

performance of the stock basket in the observation period [a, T].

(3.21) dttrBtdB

idWtSdttStdS iiiiii

)()(1,...,50 (t))()()(

==+= σα

δi = dividend fraction for Si (3.22)

3.4.2 Valuation at Arbitrary Time Point Prior to Observation Period

3.4.2.1 The Pricing Formula

In this model it is clear that the probability that a stock causes a stock loss may be different

from the probability that another stock causes a stock loss. We therefore denote the

probability (under Q) that Si causes a stock loss, given that we are at time t, . This

probability is determined by the volatility of the stock, the risk free rate, dividends, today’s

price of the stock, and the remaining time to maturity. Moreover, we let the discrete

random variable K denote the number of stock losses (under Q). The probability distribution

for K is denoted

)(tpi

)(tSi

) at time are we|(),( tkKQktpK == . (3.23)

41

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

Since K no longer follows the assumptions for the binomial distribution our pricing formula

has to be rewritten. Using the arguments from Subsection 3.2.2 and our new probability

distribution for K we write,

. (3.24)

+⋅++⋅= ∑

=

−−50

16

)( ),(000.10)15,(500.10 ...)0,(000.18i

KKKrtT

t itptptpeπ

3.4.2.2 Determining the Probability Distribution

In order to evaluate formula (3.24) and actually price the Podium Plus we need the probability

distribution . It is easily constructed by the :s. This is by no means intellectually

challenging, but requires immense calculations, and therefore calls for computerized

evaluation. Nevertheless, let us describe how this distribution is computed in theory.

),( itpK )(tpi

First, for all stocks, the corresponding is calculated. This is described in Subsection

3.4.2.3. Then is calculated in this manner: (3.25)

)(tpi

),( itpK

1. The probability for no stock loss to occur is

))(1))...((1))((1()0,( 5021 tptptptpK −−−= .

2. The probability for one stock loss to occur is a sum of 50 probabilities, each of which is

the probability for one stock loss to occur in a specific way,

)())(1))...((1))((1(...))(1))...((1)(()0,( 5049215021 tptptptptptptptpK −−−++−−= .

42

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

3. The probability for i stock losses to occur is a sum of probabilities [BLO, p 43], each

of which is the probability for i stock losses to occur in a specific way.

i

50

Since we only need to calculate for i ∈ [0,15].

Still, is the sum of approximately 2.3·10

)15,(...)0,(1),(50

16tptpitp KK

iK −−−=∑

=

)15,(tpK

),( itpK

12 terms, each of which is a product of 50

factors out of which 35 require a subtraction. Even a computer may need a considerable

amount of time to perform these computations. Therefore an approximation procedure may be

useful. A very basic approximation procedure may look like this: (3.26)

1. Decide how many additions are reasonable for each , say for instance n = 20.000. ),( itpK

2. Calculate all p that require less than n additions exactly. In our case, this is only

for i ∈ [0, 3].

),( itK

),( itpK

3. For all other , select n combinations randomly out of the possible and add

the probabilities for these n outcomes. Make sure addition is performed by the computer

in such a way that few significant figures are lost.

),( itpK

i

50

4. A unbiased estimate for each is this sum multiplied by a factor ),( itpK ni

50

[B&H, p 60].

43

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

5. Normalize the estimations so that the sum of the estimated equals one minus the

sum of the exactly computed :s to get a new estimate:

),(* itpK

),( itpK

( )∑

∑−⋅=

),(1),(

),( *

***

itppitp

itpK

KKK

),(** itpK

),( it

These :s together with our first, exactly calculated values for , is our

estimate of the probability distribution for K for our purposes.

),( itpK

3.4.2.3 Determining Underlying Probabilities

Since we know how to price the Podium Plus given the values of the :s our final task is

to determine the values of these. We begin with the assumption that there is no observation

period and that the final prices are the stock prices at 19 June 2007. We assume that we

are standing at time t and that the stock prices are for i ∈ [1, 50]. The initial stock price

for each stock is . Stock prices and dividends are governed by (3.21) and (3.22). Now,

under Q,

)(tpi

)(TSi

)(tsi

)0(is

−+−−= ))()(())(2

(exp)()(2

tWTWtTrtsTS iiii

iii σσ

. (3.27)

=

−⋅

<−+−−

=

<−⋅

−+−−

=<−⋅=

nii

iiii

ii

in

iiiii

ii

in

iii

tss

tWTWtTrQ

stWTWtTrtsQ

sTsQtp

)1()()0(9.0

ln))()(())(2

(

)0(9.0)1())()(())(2

(exp)(

))0(9.0)1()(()(

2

2

δσ

σ

δσσ

δ

44

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

, ))(

2(

)1()()0(9.0

ln)(

2

−

−−−

−⋅

=tT

tTrts

s

Ntpi

iin

ii

i

i σ

σδ

)0(is

(3.28)

where T is the date of maturity, t is current time (before the observation period), is

today’s price for stock i, is the initial price for S

)(tsi

i, ri is the risk free interest rate for

the currency in which Si is quoted, σi is the volatility for Si and δi is the dividend fraction

for Si.

If, on the other hand, the observation period [a, T] is taken into account, we get analogous to

Subsection 3.3.2,

, )())(|)0(9.0)(())0(9.0)(()(09.0

)(∫∞

⋅=<+<=s

aSiisiii dfassTmQsasQtpii

ααα

where, from above

−

−−−

=<tT

tTrts

s

NsasQi

ii

i

i

ii σ

σ))(

2(

)()0(9.0

ln))0(9.0)((

2

and

45

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

−

−+−⋅

−

⋅+

−

−−−

==<

aTaTrs

Nsr

aTaTrs

N

aSsTm

i

iii

i

iii

i

iii

iiisi

σα

σα

σα

α

)()0(9.0))0(9.0(2exp

)()0(9.0

))( |)0(9.0)(Q(

2

(3.29)

We also get,

. ))(2

()(

ln)(2

1exp1)()(

))(2

()(

ln))(()(

)()(())(2

(exp)()(

22

2)(

)(

2

)(

2

−−−

−−

−==

−

−−−=<=

−+−−=

tartstatad

dFf

ta

tarts

NaSPF

tWaWtartsaS

ii

i

i

iii

aSaS

i

ii

i

i

iiiaS

iiii

iii

i

i

i

σασσαα

αα

σ

σα

αα

σσ

(3.30)

The expression for is therefore by formula (3.13), )(tpi

46

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

ασα

σσα

σα

σα

σα

σ

σ

ααα

dtartstata

aTaTrs

Nsr

aTaTrs

N

tT

tTrts

s

N

dfassTmQsasQtp

ii

i

i

iii

s i

iii

i

iii

i

iii

i

ii

i

i

saSiisiii ii

−−−

−−

−⋅

−

−+−⋅

−

⋅+

−

−−−

+

−

−−−

=⋅=<+<=

∫

∫

∞

∞

22

2

9.02

2

9.0)(

))(2

()(

ln)(2

1exp1

)()0(9.0))0(9.0(2exp

)()0(9.0

))(2

()(

)0(9.0ln

)())(|)0(9.0)(())0(9.0)(()(

0

0

(3.31)

Adjustment for dividends is made by replacing iα by wherever it appears in

formula (3.31),

nii )1( δα −

ασδα

σσδα

σδα

σδα

σδα

σ

σ

ααα

dtartstata

aTaTrs

Nsr

aTaTrs

N

tT

tTrts

s

N

dfassTmQsasQtp

ii

i

nii

iin

ii

i

in

iii

i

niiii

s i

in

iii

i

ii

i

i

saSiisiii ii

−−−

−−

−−−

⋅

−

−+−−⋅

−−

⋅+

−

−−−−

+

−

−−−

=⋅=<+<=

∫

∫

∞

∞

22

2

2

9.0

2

9.0)(

))(2

()(

)1(ln

)(21exp

)1(1

)()1()0(9.0))1()0(9.0(2exp

)()1()0(9.0

))(2

()(

)0(9.0ln

)())(|)0(9.0)(())0(9.0)(()(

0

0

(3.32)

47

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

Formula (3.32) now gives the distribution with the same notation as in (3.28), with a

being the beginning of the observation period and t < a.

)(tpi

3.5 A Simple Model with Correlated Stocks

3.5.1 Model

Assumptions: The fifty stocks in the reference portfolio are correlated. They may have

different volatilities and/or pay different dividends. Final price for each stock is the closing

price at 18 June 2007 (i.e. no observation period). Stock price processes are described by

(2.41).

3.5.2 Calculation of the issue price

When working with this setup the appropriate pricing formula is (3.24) and the appropriate

expression for the issue price is

(3.33)

where K is the random variable for the number of stock losses and is the

probability, at time 0 and under Q, for i stock losses to occur.

+⋅++⋅= ∑

=

−50

160 )(000.10)15(500.10 ...)0(000.18

iKKK

Tr ipppeπ

)(ipK

What we need to be able to evaluate (3.33) is the probability distribution for K. Let us first

assume that the underlying stocks pay no dividends. We already know that given our model,

the risk neutral dynamics for a given stock is

48

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

rBdtdB

iSdWSdWrdtdSMdWrMdtdM

MSSI

MM

==++=

+=1,...,50for σσ

σ (3.34)

Recall from (2.30) that

++

+−= )()()(

21exp)0()( 22 tWtWtStS MSSISIS σσσσα . (3.35)

This is the same as saying

+

+−⋅⋅= )()(

21exp)0()( 22)( tWteStS SISIS

tWMS σσσασ , (3.36)

or equivalently, if we know the value of W at the date of maturity, we can easily calculate

the distribution for the stock price at the same time point. Using the technique of Subsection

3.3.2,

M

, (3.37)

where (f is the value of the density function for W at value s.

( ) ( )∫∞

⋅=<=<0

)( )()( |)0(9.0)()0(9.0)( dssfsTWSTSPSTSP TWM M

)() sTWM M

Since ( )TNTM ,0)( ∈W the density function for W is given by [BLO, p 169] )(TM

−=

Ts

TsTWM 2

exp21)(

2

) πf ( . (3.38)

Now is easily obtained from (3.36), ( sTWSTSP M =< )( |)0(9.0)( )

49

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

( )

( ) , )(

219.0ln

)( |)0(9.0)(

9.0ln)()(21

)( |9.0)0()()( |)0(9.0)(

)()(21exp)0()(

22

22

22)(

+

+−−

==<

=

<++

+−

=

=<==<

+

+−⋅⋅=

T

sTNsTWSTSP

TWsTP

sTWS

TSPsTWSTSP

TWTeSTS

I

SSIS

M

SISSIS

MM

SISISTWMS

σ

σσσα

σσσσα

σσσασ

(3.39)

and so, the probability for a stock loss to occur in stock i, , is ip

( )

.2

exp21

)(219.0ln

)()( |)0(9.0)(

0

222

0)(

∫

∫

∞

∞

−⋅

+

+−−

=⋅=<=

dsT

sTT

sTN

dssfsTWSTSPp

Ii

SiSiIiSi

TWMiii M

πσ

σσσα (3.40)

If the stock pays dividends consistently with previous dividend modelling and with a dividend

fraction of δ,

, (3.41) (∫∞

⋅=<−⋅=0

)( )()( |)0(9.0)1()( dssfsTWSTSPp TWMin

iii Mδ )

and,

50

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

( )

, )(

21

)1(9.0ln

)1(9.0ln)()(

21

)( |)1(

9.0)0()()( |)0(9.0)1()(

22

22

+

+−−

−

=

−

<++

+−

=

=

−<==<−⋅

T

sTN

TWsTP

sTWS

TSPsTWSTSP

Ii

SiSiIiSini

ni

iIiSiSiIiSi

Mnii

iMi

nii

σ

σσσαδ

δσσσσα

δδ

(3.42)

so,

∫∞

−⋅

+

+−−

−=

0

222

2exp

21

)(21

)1(9.0ln

dsT

sTT

sTNp

Ii

SiSiIiSini

i πσ

σσσαδ

. (3.43)

Now that we have the :s we can calculate, or estimate using methods of Subsection 3.4.2.2,

the :s and thereafter evaluate formula (3.33) to get the arbitrage price for the Podium

Plus. Since we have 51 sources of randomness and 51 traded assets, this price will be both

arbitrage free and unique by statement (2.23).

ip

)(ipK

3.5.3 Further Modelling with Correlated Stocks and Conclusions

It is possible to ease some of the assumptions made in Subsection 3.5.2 and still get analytical

formulas for the arbitrage price of the Podium Plus. We could for instance assume the CAPM

consistent model up until the start of the observation period and thereafter assume

independence. The reason this will not be done here is two-fold. First of all such calculation

will add nothing conceptually new. All calculations could be done with ideas from previous

subsections. The main reason it is not done, is that such formulas would be so extremely

51

Methods for Pricing Derivatives Written on 3. Analysis a Large Number of Underlying Assets

complex that their practical use would be close to zero. The main conclusion drawn from our

attempt to price the Podium Plus by mathematical analysis is that this tool is not particularly

well suited for the task.

In order to get an arbitrage price for the Podium Plus with a minimum of simplifying

assumptions (i.e. no other than the CAPM correlation model) we shift our focus towards

simulations.

52

Methods for Pricing Derivatives Written on 4. Pricing by Monte Carlo Simulation a Large Number of Underlying Assets

4 Pricing by Monte Carlo Simulation

In real life, the theoretical price of a complex financial derivative is often found using

simulations. This is particularly true when evaluating path dependent derivatives or

derivatives written on several underlying assets [WIL, p 934]. In our case, analytical tools

could hardly take us further than does Subsection 3.5.2, and even if had access to the immense

computer power needed to evaluate some of the expressions in that and prior subsections,

simplifying assumptions have been made that distort the result of the computations. Thus,

simulation appears to be a helpful tool when evaluating the Podium Plus note. We will

perform two sets of simulations, one where we determine a “fair” issue price and one where

we compare the price at which H&Q offers to buy back the note at a given date to a

theoretical price. This section roughly follows the procedures outlined in [HUL, pp 410-414]

4.1 Setting up the Simulation

Betas and volatilities for the 50 stocks were estimated using two years of weekly data,

adjusted for dividends. The estimation procedure is explained in Subsection 2.3.9. The market

with respect to which the stocks were modelled is the S&P 500-index.

Stock prices were modelled under Q and in accordance with the CAPM model outlined in

Subsection 2.3.9. Each simulation trial then consisted of the following steps:

1. and the W :s at the first time point of the observation period were constructed

using random numbers from Re[0,1] and the normal inverse function. Thereby, stock

prices and the stand of the market at this time point could be constructed using

formulas (2.29) and (2.30)

MW i

53

Methods for Pricing Derivatives Written on 4. Pricing by Monte Carlo Simulation a Large Number of Underlying Assets

2. For each trial, the observation period consisted of 21 time points, corresponding to the

beginning of the observation period and the 20 days that make it up, at which we

could observe the stock price. The stock prices, and the market stand, were

constructed in analogy with point one.

3. For each trial and each stock, the lowest stock price was picked and compared to the

initial value of that stock to determine the number of stock losses and thus the payoff

of the Podium Plus.

4. At the end of the simulation the average payoff ( x ) and the sample standard deviation,

s, of this quantity were calculated. Using the fact that any average of independent

identically distributed stochastic variables are approximately normally distributed

[BLO, p 181] a confidence interval for the payoff could be constructed using the

formula [B&H, p 97]

⋅−+⋅−−=

nsntx

nsntxI m )1(,)1( 2/2/ αα

)1(2/

, (4.1)

where n is the number of trials and −ntα is an appropriate quantile for the t-

distribution.

5. Having done this, the confidence interval for the arbitrage price was calculated by

discounting the limits of the abovementioned confidence interval.

54

Methods for Pricing Derivatives Written on 4. Pricing by Monte Carlo Simulation a Large Number of Underlying Assets

4.2 Issue Price

The parameter inputs and the results of the issue price simulation are presented in Table 4.1.

Table 4.1. Parameters and results for issue price simulation.

Volatilities and betas: Refer to Appendix A Continuously compounded risk free rate: 3.25 per cent Yearly dividends: 1 per cent of stock price at date of payment Number of trials: 10.000 95 % confidence interval, SEK: [9083, 9118]

4.3 Price as of 2003-08-18

The price at which H&Q offered to buy back the Podium Plus notes at August 18 2003 was

99 per cent, i.e. SEK 9.900. The performance of the stock basket up to this date is tabled in

Appendix A. For instance, a growth factor of 1.05 means that the stock price had increased by

5 percent from June 18, 2003. At this date, an equally weighted portfolio of the stocks in the

stock basket had gained 0.43 per cent in value since the issue day and the number of stocks

traded at prices below 90 per cent of their start values was 5. Parameter inputs and results of