master thesis: bank capital requirements and …s3.amazonaws.com/zanran_storage/ thesis examines...

TRANSCRIPT

Master Thesis:

Bank Capital Requirements and Performance

Student:

Lilia Mukhlynina

Supervisor:

Prof. Kjell G. Nyborg

Department of Banking and Finance

University of Zurich

Januar 2012

AbstractThis thesis examines possible effects of stricter capital regulations on banks. Following

the history of Basel Accords, the focus of analysis lies on capital supervision and control.

An issue for controversial discussions among bankers and academics, Basel III is to be

implemented in the coming years as a response to the last financial crisis. Core element of

the new directive is the requirement to raise the proportion of equity in the bank capital

structure. The main reasoning is that equity is the loss-absorbing source of financing and

when increased, will help to reduce the probability and severity of systemic risks. This

initiative caused an intense opposition from the bankers’ side who claim, equity is too

expensive compared to debt. They argue that more equity will negatively affect bank

profits, lowering its lending abilities and eventually leading to a credit crunch. The thesis

analyses both stand points of the debate with the conclusion that equity funding is not

expensive per se. The justification of the opposite opinion can only be true under certain

conditions, which include tax deductibility of debt and government guarantees. In this case,

the paradoxical nature of government measures becomes obvious: strengthening the rules

on capital and, at the same time giving incentives for debt financing. Until the internal

contradictions are solved and the message of the authorities is clear, the probability that

financial institutions become risk-averse and stock up their capital reserves remains low.

Keywords: cost of capital, Miller-Modigliani proposition, Basel Accord, leverage, capital structure

Contents

Page

Abstract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

Table of Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

1 Evolution of Bank Regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.1 Birth of Capital Regulation . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.2 Capital Regulation Before Basel . . . . . . . . . . . . . . . . . . . . . . . 6

1.3 Basel I . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Definition of Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Risk Weights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Amendments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Evaluation of Basel I . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.4 Basel II . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Consultative Papers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Structure of the Accord . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Basel II: Pillar I in Detail . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Evaluation of Basel II . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.5 Basel III . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Features in Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Future of Basel III . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

2 Debt vs Equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

2.1 The Logic of Miller and Modigliani . . . . . . . . . . . . . . . . . . . . . . 32

Does M&M Apply to Banks? . . . . . . . . . . . . . . . . . . . . . . . . . 33

2.2 Market Distortions Due to Government Interventions . . . . . . . . . . . . 35

Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Bankruptcy, Bank Runs and Deposit Insurance . . . . . . . . . . . . . . . 38

2.3 Is Debt a Carrot or a Stick? . . . . . . . . . . . . . . . . . . . . . . . . . . 42

2.4 Banker’s Argument . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

3 Empirical Evidence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

3.1 Previous Studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

3.2 The Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Selection of Variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Relationship Expectations . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

ii

Data Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Regression Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

4 Evaluation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

4.1 Proposals to Capital Regulation . . . . . . . . . . . . . . . . . . . . . . . . 59

4.2 Is Debt Expensive? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Introduction

Motivation

A bank exists to facilitate the interaction between two parties. Being an intermediary insti-

tution, it plays a significant role in the financial system and society, who therefore depend

on its prudence and health. More than any other business entities, banks are extremely

interconnected with each other, which can lead to a domino effect in times of trouble.

Due to its high involvement in people’s lives, any malfunction becomes crucial, revealing

a considerable scale of adverse externalities. Such structural fragility also comes from the

bank-specific balance sheet that contains low portion of cash and capital reserves relative

to debt.

Banking is a spread business, which lives from the difference between receiving and pay-

ing interest on capital. To generate an income bank attempts to keep high interest rates

on its services while securing cheap access to the capital. Hence the price of financing

determines its structure. As equity predominantly perceived to be more expensive than

debt, it is plausible, that banks maintain high ratios of debt trying to lever up its earnings.

In this context it is also understandable why bank executives build an opposition against

strengthened capital requirements, which imply substantial raise in equity. Their claims

do not seem wrong, but the question is how they define expensiveness and at which cost

comes the “cheapness” of debt.

The problem of optimal capital structure is not new. The first thorough research on the

subject started with the article of M. Miller and F. Modigliani in the American Economic

Review: “The Cost of Capital, Corporation Finance and the Theory of Investment”. The

economists illuminated the fact, that whatever financial structure the firm might have, it

is completely irrelevant to its value, which depends only on the income from its assets.

This statement sounds contradictory to the managers’ behavior, who compose their bank

balance sheet according to the price for capital resources. That is however consistent with

the theory. The Miller and Modigliani Irrelevance Theorem (M&M henceforth) holds only

under certain assumptions, such as operating in perfect financial markets, with no transac-

tion or bankruptcy costs, no taxes, symmetric information or any other arbitrage allowing

frictions. As such ideal conditions are only theoretically possible, the proposition is better

used as a scale to measure market distortions. In other words, which of the prerequisites

2

may fail in order the capital structure to matter? Having an answer to this question and

modifying the corresponding parameters, it is possible to steer the form of funding. The

most common mechanisms that authorities apply to banks are taxes and deposit guaran-

tees. Under the current regulatory framework, debt has two major advantages over equity.

First, debt possesses the advantage of tax shield and second, it provides a safety net, as

the government gives subsidies and therefore is taking over a portion of risk. That allows

banks to pay investors less and thus to generate more income. Lacking such favorable char-

acteristics, equity is perceived to be more expensive. It is true, but cannot be generalized.

One has to distinguish between social and private costs. The same conditions do not have

the same implications for banking executives and for shareholders; the correlation of their

individual interests is often negative. It is also important to mention the time perspective.

In the short term, benefits of cheap financing may overweigh the risk concerns. But in

the long term, the probability of default will rise, making leveraged structure highly fragile

and expensive. Many economists point out, that the system designed today gives the man-

agement incentives to pile up debt and to shun equity, and thereby setting the economic

system on the brink of failure.

It is therefore very interesting to follow the evolution of capital regulation from the roots

to the modern concepts. Such analysis might help to see how particular rules formed the

structure and behavior of banking institutions and maybe it will help to identify the tools

that bring financial markets closer to the optimal functioning.

Structure

The thesis is organized in three parts. The first part is dedicated to the evolution of capital

regulation. The historical overview starts with the earliest attempts to set some rudimen-

tary capital rules the banking institutions should comply with. It continues with Basel

Accords, following the development of the directives from 1988 to the latest regulatory

initiatives. The purpose is not only to list the events in their chronological order, but also

to analyze the reasoning that lied behind the introduction of certain requirements, as well

as consequences and market response.

The second part is the core element of the paper. It contains the collection of arguments

from different market participants: academics and practitioners, “leverage defenders” and

those, who support an expansion of equity. To understand the rationale for particular

positions, it might be helpful to choose a starting point, which in this case would be M&M

Proposition. The first question which appears in the context is whether the Theorem holds

3

for banks. After having this point covered, we move to the extensive analysis of debt and

equity as building blocks of bank liabilities. This thesis examines the roles both types

of financing play privately and socially, the costs and benefits they create and how they

are perceived by the different kinds of discussion participants. The analysis is based on

the review of the advances in scientific literature, media contributions to the subject and

interviews with banking executives1.

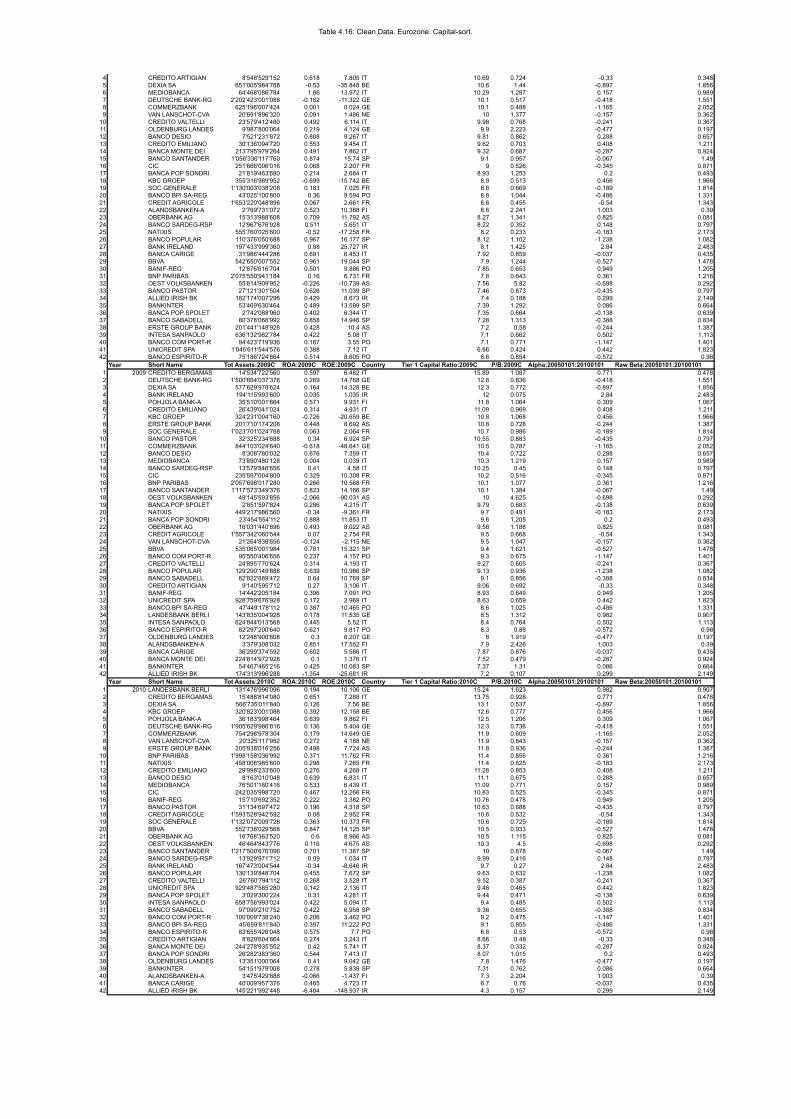

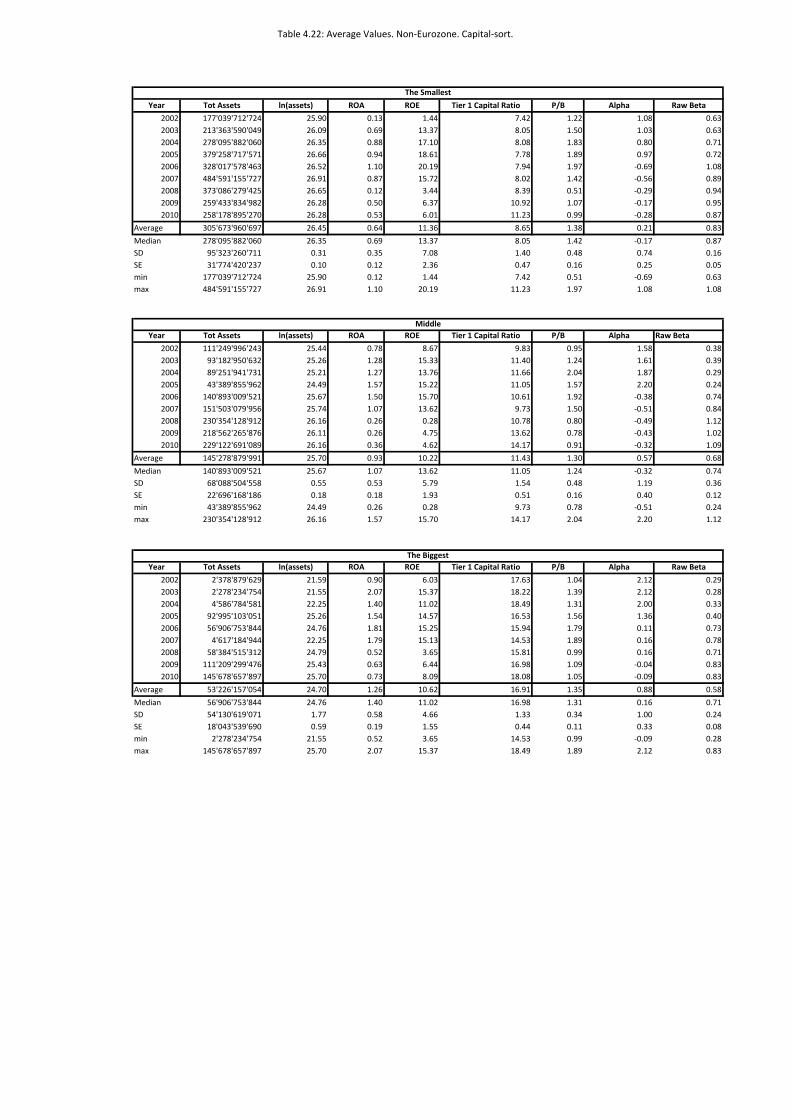

The last section covers empirical evidences to the subject. The sample of European banks

was used to evaluate the effect of leverage on a bank’s performance. Return on assets

and equity, residual returns and price-to-book ratio were chosen as a profitability measure,

whereas capital tier 1 ratio served as an indicator for leverage. The null-hypothesis is the

validity of M&M Proposition, meaning that the regression coefficients are not significantly

different from zero. Overview of the results is included in the part of data analysis and

tables.

The conclusion is dedicated to the current discussion of capital regulation and academic

proposals and summarizes the findings and thoughts of the thesis.

1Which could not be explicitely included in this thesis.

4

1

Evolution of Bank Regulations

1.1 Birth of Capital Regulation

Although there are a lot of arguments which justify control and supervision of banks,

the question whether and how far the sector has to be regulated remains controversial.

Economist Kevin Dowd (1996, [33]) compares this issue with generally desirable free trade

and asks why the laissez-faire approach could not be applicable for banks. Examining the

possibility of free financial system, he comes to the conclusion that, with no lender of last

resort or government guarantees, the market would be disciplined and punished by deposi-

tors themselves. In his theoretical model, the depositors, being aware of the risks, threaten

to close the accounts when the first signs of danger appear. That induces banks to pursue

conservative lending policy and transparency. Adequate level of capital therefore serves as

an insurance against potential losses to reassure investors. Dowd argues that additional

capitalization, being rather costly, makes a bank safer and more attractive to its depositors.

So the competition between banks would ensure the most appropriate to the customers’

demand degree of capitalization. The exact amount of capital would be determined by

market forces.

Representing the opposite point of view, Professor Sheila Dow (1996, [32]) brings two main

arguments for regulated financial system. She claims that, first, free banking is prone to

extreme cyclicality and second, central banking would automatically emerge in such a sys-

tem, so there is no point in laissez-faire (Dowd, 1996, [33]). Dow bases her position on “the

very special economic role of money and the uncertainty associated with it”. Unlike firms,

banks use their liabilities as money, so the purpose of the regulation is in this case “to

ensure that bank’s assets retain sufficient liquidity to meet any reduction in redeposit, and

to discourage such a reduction in the first place”. In her article “Why the Banking System

Should Be Regulated”, Dow reasons, that “regulation is warranted because the moneyness

of bank liabilities is a public good”. The state in turn “produces moneyness by inspiring

confidence in moneys capacity to retain value (Dow, 1996, [32]).

Following this line of argument, Santos (2000, [79]) derives the necessity to regulate banks

from the role they play in financial intermediation, providing liquidity, monitoring and in-

formation services. Such importance may increase the probability of a systemic crisis and

5

lead to substantial social costs. High interconnectedness and potential exposure to runs

make banks particularly vulnerable to any kind of actual or perceived failure. Thus, the

danger of a destructive chain reaction stimulates the idea of implementing bank insuring

mechanisms.

Another issue comes from the inability of depositors to monitor banking activities. Accord-

ing to the representation hypothesis of Dewatripont and Tirole (1994, [24]), the rationale

for banking regulation is based on agency problems and corporate governance. A bank

structure implies separation of ownership from management, what makes them susceptible

to moral hazard and adverse selection problems. Screening and monitoring, though neces-

sary, could be expensive for single depositors, especially for the small ones. That would also

lead to a free-riding effect. Therefore, the regulation could facilitate the communication

between two sides by taking over the control and supervision that depositors would exert

themselves under these certain conditions (Santos, 2000, [79]).

If the regulation of banks is really crucial for the system, one has to ask why among

other parameters the regulation of bank capital seems to be particularly important. This

can be explained by the fact, that the bank has mainly two sources of financing at its

disposal. Using borrowed money, the bank has to fulfill its contractual liabilities, which, if

not satisfied, can lead to default. Financing its operations with the own funds (equity), the

bank does not expose itself to an immediate failure in case the value of the funds decreases.

Therefore, the bigger the proportion of own capital in the bank balance sheet, the greater

the probability that the institution will comply with its obligations even in difficult times

(FDIC, 2003, [37]).

1.2 Capital Regulation Before Basel

The history of banking regulation starts long before the Basel Accords and experiences a

series of changes from the strict policy to the phases of deregulation.

The earliest attempts to control bank capital can be traced back to 1863, when the new

class of “charter national banks” was created in the US1. Civil War was a heavy weight for

the economy, forcing government to look for funds. Thus, the new national banks were al-

lowed to issue their own currency, backed by the US securities. These were the first entities

to undergo capital requirements, which were based on the population in their service area.

1Before 1863 only state-regulated banks had existed in the US.

6

1913 is the birth year of the US Federal Reserve (FED) as the lender of last resort. That

helped banks to avoid losses by discounting assets instead of selling them at low prices

in case of liquidity problems. After the difficult year of 1929 and the beginning of the

Great Depression, the American Senate took several regulatory measures. On the proposal

of senator Steagall, the Federal Deposit Insurance Corporation (FDIC) was established in

1933. The purpose was to ensure the system from bank runs, providing creditors with gov-

ernment guarantees. At the same time, Senator Glass initiated the creation of a “Chinese

Wall” between investment banking, that issued securities, and commercial banking which

accepted deposits. These rules, known as Glass-Steagall Act, were introduced to protect

investors and to eliminate potential conflict of interest concerning granting and using of

credit by the same institution. Japan soon adopted a similar course of action, whereas

Europe kept its model of universal banking.

After the “golden 1960s” of economic prosperity, Europe experienced the Herstatt bankruptcy2,

when one of the biggest commercial banks in Germany with DM 2 million assets had gone

down. The bank was involved in the foreign exchange business, which after the collapse

of Bretton Woods in 1973 had become a risky activity under the floating exchange rates.

Responding to the consequences of the downfall, the G-10 countries3 formed a standing

committee at the Bank for International Settlements (BIS) in 1975, which later became

the birthplace of the Basel Accords (Balthazar, 2006, [7]).

The lack of consensus between supervisors from different countries at this moment made it

more difficult to work out a universal approach to capital regulation. There were numerous

developments that urged the authorities to turn their focus on capital (Tarullo, 2004, [86]).

In the late 1970s, the economic situation globally deteriorated. The combination of eco-

nomic stagnation and high inflation was named “stagflation”, characterizing the decade of

macroeconomic weakness (FDIC, 2003, [37]). Volatile foreign exchange and interest rates

caused the expansion of non-bank financial institutions (NBFIs), which became direct com-

petitors of banks. Together with rapid growth of capital markets, this effect led to the shift

in the clients’ behavior, who turned their attention from savings accounts to money mar-

ket funds. Losing on their gain margins, the banks began to look for alternative ways

2The Case of Herstatt was one of the largest failures in German banking history. The debacle received

much attention due to its regulatory implications and now is known in finance under the term “Herstatt

risk”, which comes from the time delivery lag between two currencies. The bank was closed in 1974 (BIS,

2004 [11]).3The Group of Ten includes eleven industrial countries: Belgium, Canada, France, Germany, Italy,

Japan, the Netherlands, Sweden, Switzerland, the United Kingdom and the United States. These countries

cooperate on economic, monetary and financial matters.

7

to secure their income, investing in real estate lending and loans to developing countries

(Balthazar, 2006, [7]). The downward trend in capital level, particularly at large banks,

became the point of concern. Looking for new sources of revenue, banks tried to increase

lending, putting their capital under pressure. They involved themselves in leasing and data

processing activities, but also sought for new ways within the traditional credit business.

One possibility to get higher returns fast was to attract borrowers with low credit history

or restricted access to public capital markets, who were ready to pay higher risk premi-

ums. Such a tendency proved to have disastrous consequences later on (Tarullo, 2004, [86]).

This situation of high competitiveness among banks was an unintended result of the partic-

ular macroeconomic strategy in the US, called “Regulation Q”. The Federal Reserve Board,

according to the Banking Act of 1933, prohibited the payment of interest on demand de-

posits and set a ceiling to the interest rates that banks paid for funds. The government

planned to restrain price competition in banking industry and to stabilize the system by

controlling credit flows in the economy. This implied that banks would lend more in their

local area instead of trying to keep pace with the big players. Regulation Q did not af-

fect the volume of total credit, but influenced its allocation. Restricted for the financial

intermediaries, the funds were available in the unregulated markets for a cheaper price.

The policy, complemented by the other restrictions concerning commercial and investment

business, put banks in a difficult position (Gilbert, 1986, [41]; Ruebling, 1970, [77]).

The US “Savings and Loans” institutions (S&L) soon were also in trouble. The 1980

marked the beginning of the S&L crises which took a decade to resolve. Growing fast after

the Great Depression, S&L offered long-term fixed-rate mortgage loans financed through

short-term deposits. Creditworthy borrowers and limited interest rates secured a comfort-

able economic environment. But the recession of the 1970s worsened funding conditions

considerably (Balthazar, 2006, [7]).

Responding to the poor economic development and problems in financial sector, the gov-

ernment started the deregulation campaign that lasted for the next 20 years. In 1980 the

limits on interest rates were abolished and the restrictions on banking activities were in

many ways loosened (Tarullo, 2004, [86]). To compensate for the higher costs of funding,

S&L began to look for riskier opportunities. This and the overall financial instability mo-

tivated the regulators to propose an explicit capital ratio requirement at the federal level.

The first standard was set by the leverage ratio on primary capital, which included equity

and loan loss reserves. Thus, the earliest capital adequacy ratio constituted a minimum of

6% for community banks and 5% for larger regional institutions.

8

In 1982 Mexico defaulted on its USD 80 billion debt, causing substantial write-offs of bad

loans during the next ten years. By 1983, twenty-seven countries had undergone debt re-

structuring processes, involving more than USD 230 billion. The same year the Rumasa

failure4 happened in Spain and one year later, Continental Illinois5 failed on its obligations

after the downgrading and followed bank run. In the US and Europe the government was

working on the uniform capital standards, emphasizing the growing necessity for interna-

tional convergence in bank regulation. As a result, the Congress passed the International

Lending and Supervision Act of 1983 (ILSA), responding to the international debt crisis

and its negative impact on the US. The common definition of regulatory capital and uni-

form capital requirements were finalized in 1985, changing the primary capital ratio for

large banks from 5% and for the community banks from 6% to equal 5.5% of adjusted total

assets. Holding less than 3% of primary-capital-to-total assets, banks were categorized as

“unsafe and unsound” and required to comply with corresponding corrective actions. By

1986 banks were expanding their activities, developing more innovative off-balance sheet

operations and at the same time were moving away from low-yield safe liquid assets. Reg-

ulators sensed the need to review the primary capital ratio as insufficient to differentiate

among newly appeared risks and were looking for ways to systematically consider risk pro-

files of individual banks (FDIC, 2003, [37]). Soon almost all Basel Committee countries

introduced capital ratio calculations, that were progressively based on a risk-weighting of

assets. However, there were substantial differences in the approach and details of capital

regulation among these countries (Tarullo, 2004, [86]).

1.3 Basel I

In July 1988, a working group of the Basel Committee published a set of minimal require-

ments for bank capital. The new Basel Accord mostly addressed to credit risk, leaving

4Rumasa was a diversified holding company with close government links and a conglomerate strategy.

However, it was claimed that Rumasa did not have any real assets and used one company as a collateral

to buy another, building the whole empire in the pyramid fashion. At the time point of expropriation,

the group controlled over 700 companies, employing 65’000 people directly and 300’000 indirectly (Fight,

2004, ([38]).5Continental was the seventh largest bank in the US, which made its default consequential. Regulators,

worried about systemic implications, decided to rescue the bank, injecting USD 2bn. Other USD 5.3m were

granted by a consortium of the twenty-four major US banks and the FED managed its liquidity problems.

One of the first “too-big-to-fail” problems highlighted the concerns about control and possible failure of

large banks (Balthazar, 2006,[7]; FDIC, 1997, [36].

9

other kinds of risk to national regulators6. Targeting primarily on globally active banks,

the proposal outlined two major points: global reduction of competitive inequality among

banks and strengthening of the international banking system (Balthazar, 2006, [7]). To

resolve the first problem, the regulation increased current capital ratios, which seemed to

be too low in some countries. For the second purpose, it introduced a simpler approach to

credit risk, with regard to the risk-taking behavior of banks (van Roy, 2005, [76]).

The core of the initiative could be illustrated by the three steps of calculations. First,

each asset and off-balance sheet item held by the bank had to be assigned to one of the

five risk categories. Second, the capital required for each balance sheet item based on the

risk-weighting had to be determined. Third, these amounts had to be added together to

generate the total minimum capital the bank had to raise and to maintain (Tarullo, 2004,

[86]).

Definition of Capital

According to its quality, capital was divided into two major classes:

• core capital (basic equity): Tier 1

• supplementary capital: Tier 2

The first category contained stockholder equity7 and disclosed reserves8. The most impor-

tant element of capital, it defined bank competitiveness and profit margins. Common for

all banking systems it could be found in the published accounts of different countries where

market estimations of capital adequacy were made (BIS,1988, [9]).

Tier 2 contained undisclosed reserves9, asset revaluation reserves 10, general provisions11,

hybrid debt capital instruments12 and subordinated term debt.

6E.g. investment risk, interest rate risk, exchange rate risk and concentration risk.7Equity capital: common stock and non-cumulative perpetual preferred stock.8Disclosed reserves: e.g. share premiums, retained profit, general and legal reserves.9Undisclosed reserves (hidden reserves): usually unpublished, but considered in P&L account and ac-

cepted by bank supervisory authorities (BIS,1988, [9]).10Accounting standards in some countries allow to revalue assets to their current value rather than

historical costs (BIS,1988, [9]).11Also called general loan-loss reserves, usually built in anticipation of not-yet identified losses (BIS,1988,

[9]).12Capital instruments, which combain partly debt and partly equity characteristics (BIS,1988, [9]).

10

There were also certain deductions from both categories. Goodwill had to be eliminated

from Tier 1, due to its volatile and subjective character. Investments in not consolidated

subsidiaries had to be deduced against the total capital base in order to avoid several en-

tities using the same capital funds (Balthazar, 2006, [7]).

Besides, Tier 2 components had to be limited to a maximum of 100% and subordinated

debt to a maximum of 50% of the Tier 1 capital; general provisions were not allowed to be

more than 1.25 percentage points and asset revaluation reserves in form of latent gains or

unrealized securities were subject to a discount of 55% (Tarullo, 2004, [86]).

The first Basel Accord defined a minimum standard to apply for international banks. The

target ratio of capital to weighted risk assets had to be at least 8%, of which the core

capital had to be minimum 4%.

Risk Weights

After the capital was defined, the Committee worked on identifying factors to weigh the

balance sheet items, according to their risk characteristics. By doing that regulators aimed

to implement a novel approach, advantageous to the simple-ratio procedure. They wanted

to create a fairer international field and level basis for international comparison between

banks with various structures; to incorporate off-balance sheet exposure into the measure

and to stimulate banks to hold liquid or other low-risk assets. The method had to be as

simple as possible, using only five classes of weights: 0, 10, 20, 50 and 100% (Table 4.1).

The assignment of weights was based on the general characteristics of the borrower, rather

than borrower’s specific financial stand or credit history. That was the reason, for example,

to weigh all loans to non-banking entities at 100%, whether it was a blue-chip corporation

or a newly born startup.

There were several elements that deserved particular attention:

• categories of risk

It was emphasized that credit risk was the major issue for most banks, so the regu-

lation stressed the necessity to oversee the counterparty-relationships, especially the

risky ones.

• country transfer risk

11

The Committee defined a group of countries13 as a measure for different weight coef-

ficients. Any country rescheduling its external sovereign debt, precluded itself from

the group for five years.

• claims on non-central-government, public-sector entities

It did not seem adequate to set a single weight for all claims on domestic public-sector

entities, which would be below the level of central government. Thus, the Committee

granted the possibility to national authorities to apply the appropriate weighting

factors for public-sector within the country, according to certain guidelines.

• collateral and guarantees

The importance of collateral was recognized only to a limited extent, due to the

country differences in dealing with that issue. There was no initiative for a common

collateral weighting system. However, several specifications were composed in the

document.

• loans secured on residential property

Because of the rather low record of loss in the majority of countries, the regulation

assigned a 50% weight to loans fully secured by mortgages on residential property,

rented or occupied by the borrower.

• off-balance sheet engagements

Off-balance sheet exposures were divided into derivative instruments and obligations

similar to unfunded loans. The latter would be shifted to the on-balance sheet side

if a certain event occurred.

The Committee adopted a two-step approach to deal with this issue: first, a conver-

sion factor had to be used to transform the item into its on-balance sheet equivalent;

second, this equivalent had to be categorized into to the risk class, based on the

customer type, like a common asset would be. This conversion factor was basically a

discount which depended on the probability that the item became an asset, creating

credit exposure for the bank.

Treatment for the derivative exposures came later into action, in the 1995 Amend-

ment. (BIS,1988, [9]; Tarullo, 2004, [86])

Amendments

Several adjustments have been made until the full implementation of the Basel Accord in

1992. There were, for example, modifications in the handling of general provisions in the

13Members of the OECD or countries with special lending agreements with the IMF (BIS,1988, [9]).

12

aftermath of the Latin American debt crisis. The matter of loan-loss reserves gained con-

siderable attention and caused discussions about excluding country-risk provisions from the

Tier 2 category. Later some changes have been made in the characteristics of risk-weight

categories and netting possibilities for certain off-balance sheet exposures. These steps were

important to the banks with substantial activities in derivatives trading, but they were not

evolutionary important in the conceptual approach.

It was rather the 1996 Amendment, which incorporated market risk and included the

rules for calculation of capital charges for market risk, using internal Value-at-Risk models.

These additions moved the Proposal in the direction of the Basel II initiative, which had a

larger focus on banks internal risk management systems and models (Tarullo, 2004, [86]).

Evaluation of Basel I

One can evaluate the Basel I proposal in two ways. One way is to check if the arrangement

has been appropriately implemented and observed by single countries. The other way - to

assess if it was successful in achieving the stated goals.

The first Basel Accord was enacted in all G-10 countries by the end of 1990. In two years,

the countries outside the membership with developed banking systems also introduced the

arrangements for capital requirements. Such broad voluntarily implementation by non-

Basel countries was motivated by the fact that, by not complying with the new capital

rules banks would look less favorable compared with the ones that complied.

Despite many critical points, the Basel I initiative was to a large extent effective in its

implementation. By the end of the transition period in 1992, most Basel-countries had at

least 4% for Tier 1 and 8% for total capital14 (Tarullo, 2004, [86]).

Broadly speaking, the Basel Accord managed to establish an international set of rules for

more than hundred countries. The introduction of formal allowance for risk in computing

capital ratios was a major improvement in comparison with the situation until 1988, when

only some banks applied equity-to-assets or equity-to-deposits ratios. Moreover, the Pro-

posal included off-balance sheet exposures into consideration.

14The exceptions were Citicorp, which suffered from substantial losses in 1991 that reduced its Tier 1

capital to 3.64%; and some banks in Japan, which were in distressed financial situation (D.Tarullo, 2004,

[86]).

13

As already mentioned, there were a lot of deficiencies in the initiative that led to a series of

further innovations and improvements. One problem was the rather crude classification of

credit-risk weightings. Quantification of economic capital was complicated in the absence

of precise estimates of risk and inner capital needs. In contrast to the regulatory capital,

economic capital is to be estimated by the bank itself, according to its risk-taking activities.

There is no problem if the internal models and risk parameters estimate economic capital

to be higher than regulatory limits. But as soon as the relation changes to the opposite,

the bank has to build a capital buffer in excess of its estimation what is sufficient. The

banks, expecting this mismatch to negatively influence the shareholder value, started to

look for prompt solutions.

Generally, in order to obey the Basel I capital requirements, banks had to choose one of the

following scenarios: increase their capital level, decrease their risk-weighted assets or sell

off the assets. This can be represented by the decomposition of the growth rate of capital

adequacy ratio of bank i into three growth rate terms:

∆(CARi, t)

CARi, t=

∆(Ki, t)

Ki, t− ∆(RISKi, t)

RISKi, t− ∆(Ai, t)

Ai, t(1.1)

where

CAR = K/RWA = capital adequacy ratio (tier 1 or total capital)

K = capital (tier 1 or total capital)

RISK = RWA/A = credit risk ratio

A = total assets

Source: P. Van Roy, 2005, [76]

One can see, that an obligatory increase in CAR does not hinder the bank from increasing

their capital level K and their credit risk ratio RWA/A15, at the same time. Such moral

hazard behavior was one of the negative responses from banking industry after the impo-

sition of the Basel Accord (Van Roy, 2004, [76]).

Interesting fact, that already back in 1980, Koehn and Santomero analyzed this kind of

argument, coming to the conclusion that ratio constraints for bank capital regulation do

not seem to be an adequate measure for controlling the riskiness of banks and probability

of failure. The economists first showed that the implementation of higher capital require-

ments induces banks to reshuffle the composition of its asset portfolio per unit of capital.

15Provided that the total amount of assets remains constant.

14

They evaluated the effect of changing required capital-asset ratio, assuming CRRA utility

function16and came to the conclusion that the composition of an equilibrium portfolio after

the mandatory ratio increase changed towards more risky assets17. Koehn and Santomero

pointed out that the level of reshuffling depends on the risk aversion coefficient of the bank

utility function. That implies that elasticity value of high risk assets for highly risk-averse

institutions is less than elasticity for the less risk averse ones. Thus, initially riskier agents

would tend to offset the capital restrictions to a greater degree than their conservative

counterparts, leading to the greater dispersion of risk taking across the whole banking in-

dustry (Koehn, Santomero, 1980, [57]).

Banks reacted to capital restrictions with various techniques to balance out the disad-

vantages and to exploit newly appeared opportunities. Expanding their capital arbitrage

strategies, they mutated the effect of the new rules, making them less efficient.

One way of using arbitrage was, as already mentioned, to invest in riskier assets. Purchas-

ing bonds of speculative classes with high compensation and the same capital requirements

as investment-grade bonds is an example of such a strategy (Balthazar, 2006, [7]).

Another, more sophisticated practice of outplaying a system was the integration of deriva-

tives in the daily business. Using securitization banks can transfer illiquid assets to a

self-created independent companies, named Special Purpose Vehicles (SPV). These entities

issued Asset Backed Securities (ABS) to finance themselves and buy loans from the bank,

liberating its balance-sheets by risk-chanelling. The result of the securitization mania was

vividly seen during the last financial crisis.

These arbitrage tactics can be harmless as well, allowing banks to correct the weaknesses

of the regulations, but it is hard to draw a line between correction and exploiting, making

it difficult to hold up. It is also worth mentioning that not all banks are able to use these

techniques, which leads to competitive disadvantages.

The reason why banks are motivated to perform capital arbitrage lies in the commonly

perceived expensiveness of equity compared to debt. Such factors as tax, asymmetric

information, agency costs and the safety net make equity look more costly. Therefore,

16CRRA: constant relative risk aversion, meaning the marginal rate of substitution remains unaffected

by the regulative changes.17For the utility function with decreasing relative risk aversion, the effect of substituting assets with

riskier alternatives is even larger.

15

when supervisory institutions demand capital standards higher than what the banks would

choose under the market discipline alone, these requirements could be viewed at as a form

of regulatory taxation (Donahoo, Shaffer, 2004, [31]). Thus, authorities encourage banks to

elaborate on methods to serve clients minimizing the taxation. Bank executives get them-

selves involved in capital arbitrage because they believe it is possible to enhance shareholder

value by replacing equity with debt in the capital structures of their banks (Jones, 2000,

[52]).

There have been some other critical issues raised in connection with Basel 1988 performance.

Lack of risk sensitivity granted a small company with high leverage an opportunity to get a

corporate loan with the same capital conditions as the AAA-rated large corporate company

would get. The list of recognized collateral was rather limited in comparison with that

effectively used by banks. Besides, Basel I focused only on credit risk and did not cover

other risk sources. The Amendment of 1996 partially filled this gap, but still some risk

types were not included in the requirements. Independent of the bank type, sophistication

and risk level, the rules were practically the same “one-size-fits-all approach”. The 8%

ratio was chosen arbitrarily, without any solvency targets outlined. Diversification of loans

through different sectors was not taken into account, letting the credit-risk requirements

have additive nature (Balthazar, 2006, [7]).

1.4 Basel II

Discussion about Basel II emerged in the need for improvements to the first set of capital

requirements. The purpose was to address the most important shortcomings of Basel I, that

were partly caused by the necessity to find an international compromise to set the capital

rules. Surprising was the speed with which the first international agreement was replaced

with the new version. There were two major trends that encouraged the review process.

On one hand, the fast-growing securitization activity of banks, on the other hand large

banking institutions were active in developing their internal models for risk assessment.

The difference between the Basel I approach and the advanced techniques for risk manage-

ment used by banks was thus increasing. Besides, the interbank competition became more

intense, arbitrage and securitization strategies more sophisticated (Tarullo, 2004, [86]).

The first Consultative Paper (CP1), containing the set of modifications of the 1988 Basel

Accord, was released in June 1999. CP2 came out in 2001 and included some adjustments

to the previous paper. In 2003 the Committee issued CP3 and in 2004 the Proposal was

16

finalized and published. This work lasted for more than six years and involved three

Quantitative Impact Studies (QIS)18(Balthazar, 2006, [7]).

Consultative Papers

CP1 was mostly an extensive version of Basel I. It revised some issues like capital charges

to operational risk and interest risk for the banks, whose exposure there was substantial.

The Committee introduced a “three-pillar” approach, where the first pillar contained the

capital rules, the second was about the supervision process and the third was dealing with

the market discipline. This framework allowed supervisors to ask banks to hold more cap-

ital, above the stated minimum. It was also possible for authorities to demand higher

transparency to better assess bank risk positions. The methodology was still in its raw

form, but the new outline was already visible. The most controversial innovation of the

concept was the suggestion to use external ratings from the credit assessment institutions

like Moodys and Standard&Poors. Their ratings would be used as a basis to categorize the

borrowers to a particular risk bucket. One additional risk bucket of 150% would be created,

compared to Basel I, but this new credit rating approach would allow risk differentiation

among corporate, sovereign and bank borrowers. The rest of the CP1 content were mainly

minor changes which addressed other deficiencies of the first Accord.

CP2 went a lot further, defining the character of the Basel Accords anew. It proposed the

internal ratings-based approach (IRB), introducing two IRB methodologies for small and

medium-sized institutions respectively. A-IRB19 implied that the banks could use their own

techniques to estimate the probability of default of their exposures. Once the values were

calculated, they would be converted into risk-weights, according to the regulative formulas.

However some minimum requirements relating to the internal rating, credit assessment,

and disclosure practices had to be fulfilled if the bank wanted to use the IRB approach.

For A-IRB there was a special set of rules, which concerned the calculation of exposure in

the event of default, possible loss, and maturity of the exposure.

The response of the banks regarding the IRB capital regulation was positive in the be-

ginning, while many academics were skeptical whether this approach was an appropriate

18QIS were conducted to collect the data for evaluation of the new capital requirements for different

types of banks. The regulators aimed to keep the level of capital in the banking sector as close as possible

to the current one (Balthazar, 2006, [7]).19Foundational internal ratings-based (F-IRB) approach was meant for wider range of banks, whereas

A-IRB was applicable only to some big banks, which could comply with the prerequisits (Tarullo, 2004,

[86]).

17

measure. There were also complaints that the banks would have to disclose proprietary in-

formation to be eligible for the use of internal estimates. But the most important comment

from the bankers side was the expected increase of regulatory capital under CP2 proposal.

As the first two papers contained a lot of disputable and incomplete features, the committee

decided to review the requirements for the third time. Based on the results of QIS-3, the

CP3 included, beside some modifications to the Pillar 1, major changes on retail exposures,

small business lending, operational and credit risk and asset securitization. That was the

last discussion paper before the final version of the second Basel Accord was released in

2004 (Tarullo, 2004, [86]).

Structure of the Accord

In the new Basel framework capital requirements were only part of the “three-pillars con-

cept, which aimed to secure banks robustness and health. Beside the capital regulation, the

committee empathized the necessity to consider supervisory approach as well as diclosure

practices in the Basel Accords.

Pillar 1 (reviewed later in detail) was dedicated to the minimum capital requirements,

updating the solvency ratio from 1988. The committee kept RWA as a main estimate to

control capital buffer and carried over the 4% and 8% minimum ratios from Basel I. But

the way to weigh assets was adjusted, introducing different versions of the IRB approach.

The values, rather than rough estimates as before, now were bound to the internal capital

estimates. Depending on the size and complexity the banks could choose the way to com-

pute their RWA for credit risk. The more sophisticated models consumed less capital but

required stricter prerequisites, motivating banks to improve their risk management.

Pillar 1 newly considered operational risk by setting explicit capital requirements for risks

of possible errors in internal processes, frauds, IT problems, etc. Here the banks could also

choose the most suitable approach according to its individual characteristics.

Pillar 2 based supervisory review on four main principles:

• The banks were required to adopt a process for assessing their capital requirements

relative to their individual risk profile

• This process would be evaluated by supervisors, eligible to take corrective actions

• The banks were expected to hold capital beyond the scope of the Pillar 1 minimum

and the regulators would be able to enforce this in case of non-compliance

18

• Supervisors were authoritized to intervene as soon as possible to prevent drastic

reduction of capital to ensure banks risk–resilience

Pillar 3 defined core and supplementary disclosures for banks and a set of disciplinary

measures for supervisors. Banks had to release publicly at least twice a year comprehensive

reports on their internal risk management and implementation of Basel II. The requirement

roused many discussions as the list of items to be published was rather extensive. (Jackson,

2001,[48]; Balthazar, 2006, [7]).

Basel II: Pillar I in Detail

Credit Risk: Unstructured Exposures

Under the standardized approach (SA) the banks calculated their RWA based not only

on the counterparty types, but also on the estimates of the external rating agencies. The

list of the recognized External Credit Assessment Institutions (ECAI) was provided by the

regulators, who examined the rating companies on their objectivity, resources, credibility

and other relevant parameters. Later these ratings were mapped on the S&P international

rating scale and converted into risk–weights. This simple application of the Accord was

created primarily for the smaller, less sophisticated banks. (Table 4.2)

The categories of risk for the RWA-calculation included: sovereign20, Public Sector Entities

(PSE)21, Multilateral Development Banks (MDB)22, banks23, corporate24, retail25, credits

secured by residential property26, credits secured by commercial real estate27, past due

loans28, other assets29, off-balance sheet items30.

20Exposures on countries were now considered according to their rating independently if they belong to

the OECD group.21The authorities could weigh non-central government PSE as banks or as sovereigns, depending on their

tax status.22Fulfilling certain criteria, these banks coild benefit from a 0% RWA, otherwise they fall in “banks”-

category.23Two possible options: to weight one risk-unit more than is given on their country or to use the banks’

rating. The category also includes security firms (except for RWA-calculation treated as “corporate”).24The category includes insurance companies.25The claim of a person or a small business, in the form of a retail product, not concentrated in the

portfolio and not more than EUR 1m.26Fully secured claims, where only borrower could use the property.27The Committee recommended to apply a risk-weight of minimum 100% with possible exceptions to

mature and well-developed markets.28Loans past due for longer than 90 days were risk-weighted according to their provisioning.29100% risk-weight.30Similar treatment as in Basel I.

19

Another issue covered by the Standardized Approach was the so-called Credit Risk Mit-

igation (CRM). This was designed as a set of techniques the bank can apply to reduce

its credit risk. That included collaterals, guarantees or hedging with credit derivatives.

There were also several methods to integrate collaterals into RWA calculation: simple and

comprehensive approaches. Thus the bank, depending on the collateral31, had either to

cover the exposure through the security with a minimum risk-weight of 20% or to apply

haircuts to take time value into account. For this purpose, the SA provided a formula for

computing the adjusted value of collateral:

AE = max(0; [E · (1 + (He)−Hc −Hfx)]) (1.2)

where

AE = Adjusted exposure

E = Original exposure

He = Haircut of the exposure

C = Collateral value

Hc = Haircut for collateral type

Hfx = Haircut for currency mismatch

Source: Balthazar, 2006 [7]

The bank could make the estimations using supervisory or its own haircuts. In the latter

case, it was necessary to comply with certain qualitative and quantitative criteria.

IRB Approaches32allowed banks to classify their assets based on the internal models for

credit risk. The regulators prescribed some key parameters33 that had to be used in the

formulas, whereas the others could be estimated internally. Exposure had to be assigned

to one of the six categories, which included corporate, sovereign, bank, retail, equity and

31Simple approach was applicable to cash on deposits, gold, debt securities with particular minimum

rating, some unrated debt securities, equities included in a main index, Undertakings for Collective In-

vestments in Transferable Securities (UCITS) and mutual funds under specified restrictions. Equities, not

included in a main index but from a recognized exhange, UCITS and mutual funds containing these equities

were the subject for the Comprehensive computation (Balthazar, 2006 [7], for more information see BIS,

2004, [11]32Include Foundation-IRB and Advanced-IRB approaches. The difference lied in the definition of the

input variables. Both models allow to use bank’s own PD parameters, but only under the A-IRB was

possible to estimate own LGD and EAD (Nomura, 2005, [70]).33Key inputs included: probability of default (PD), loss given default (LGD), exposure at default (EAD),

maturity (M), asset correlation (p) and confidence interval (CI) (Balthazar, 2006 [7].

20

purchased receivables exposures. The treatment was accordingly more comprehensive as

by the Standardized Approach, including specific risk-weighting functions and complex

computations. Under this approach, calculation of minimum capital was based on the

LGD-distribution in a portfolio of loans or similar instruments within one year. The confi-

dence level was chosen at 99.9% and only unexpected losses could be covered. (Balthazar,

2006,[7]; Nomura, 2005, [70]).

Credit Risk: Securitization

The regulators attempted to set stricter rules to the techniques close to capital arbitrage

in the second Accord. But the task was rather difficult due to the high complexity of the

securitization structures and the increasing sophistication of banks in using these tools. In

general, Basel II addressed both traditional34 and synthetic securitization35. Banks could

again make use of standardized or IRB approaches. In the first case, risk weights are based

on rating of the position. Unrated exposures had to be deducted from the capital with

several exceptions36. Banks using internal ratings had to comply with the following rules:

• for rated exposures risk weights must be based on ratings based approach (RBA)

• for unrated exposures - internal assessment (IA) possible if specified conditions met;

otherwise supervisory formula (SF), if inputs could be determined

• if exposures are unrated and earlier mentioned methods are unavailable, banks can

apply “look through” exceptional approach with regulatory approval and on tempo-

rary basis

• in other cases the exposure must be deducted from the capital

(Balthazar, 2006,[7]; GS, 2005, [78]).

Operational Risk

This was a new subject to Basel capital requirements. Three different approaches were

considered for the calculation of a bank capital ratio for operational risk:

34In traditional securitization the cash flows from an underlying pool service at least two different

tranches. In case of default, the lower tranches would absorb losses while the others were left untouched

(Balthazar, 2006, [7]).35The underlyings of this structure are not explicitly taken out of the balance sheet and only credit risk

is backed by funded or unfunded credit derivatives (Balthazar, 2006, [7]).36In case of: most senior exposure, second-loss position or better, liquidity facilities (GS, 2005, [78]).

21

• Basic Indicator Approach (BIA)

The simplest method, assuming that the amount of operational risk is proportional

to the size of banking activities. Thus the requirement was set at 15% of the bank

average gross annual income over the last three years.

• Standardized Approach (SA)

Here, bank’s three-year-average gross income was categorized into eight different busi-

ness lines: corporate finance, trading and sales, retail banking, commercial banking,

payment and settlement, agency services, asset management and retail brokerage.

The capital charge had to be calculated for each line by multiplying the correspond-

ing gross income by a factor assigned to that line by the Basel Committee. The total

capital requirement for operational risk would be the sum of the individual capital

requirements calculated for all business lines.

• Advanced Measurement Approach (AMA)

A more sophisticated method, which implied that banks would use their own opera-

tional risk management systems. These systems had to consider actual internal and

external loss data, scenario analysis and factors of the bank environment and internal

mechanisms.

(Balthazar, 2006,[7]; Nomura, 2005, [70]).

Evaluation of Basel II

The new Accord shifted the focus of banking executives on economic versus regulatory cap-

ital management, measuring their performance against risk factors instead of market share

or expected return. A change for a system based on bank internal risk models has a poten-

tial for enhancing bank safety and proper working. That is because under this regulatory

approach banks would develop greater risk sensitivity and would be able to manage their

capital according to the requirements and credit exposures much closer to the actual risks.

The IRB model was the major innovation in the Basel II Capital Accord, which received

a lot of praise as well as many critical comments. Several assumptions taken in Basel II

have been questioned by many academics and practitioners. For example the new concept

assumed that banks were in advantageous position compared to the supervisors concern-

ing the resources and expertise for the best possible risk assessment (Tarullo, 2004,[86];

KPMG, 2003, [58]). Being to a large extent true, this proposition increases the power of

banking institutions by decentralizing risk management process, which if exaggerated can

22

have rather negative consequences like the last financial crisis demonstrated.

There were also some problems related directly to Pillar 1. One of them Gordy (2003, [?])

calls “portfolio invariance”. A specified mathematical model, based on Merton’s Theory37,

represents the core of the risk-weighting formulas of the second Capital Accord. This model

is restricted with the assumption of an invariant portfolio, meaning that the required cap-

ital depends only on the risk of the loans it backs and not on the portfolio to which it is

added (Atkinson, 2010, [6]). In other words, “it is assumed that the bank‘s credit portfolio

is infinitely fine–grained in the sense that any single obligor represents a negligible share of

the portfolio‘s total exposure, and that a single, common systematic risk factor derives all

dependence across credit losses in the portfolio” (Gordy, 2004, [43]). Being a compromise

for the sake of easier global applicability, it has an important consequence on ignoring the

diversification effect which can influence the portfolio risk substantially. Thus the required

capital ratio is a linear function of the asset type it has to back, independent of the amount

of the exposure. Technically, the IRB approach and the model it uses, are based on the

asymptotic single-risk-factor (ASRF)38. This model has an important implication for credit

VaR39 of the portfolio as it allows to make calculations using only exposure–specific pa-

rameters, such as PD, LGD and a common factor, reducing computational complexity.

According to Gordy (2003, [?]), “each exposure’s contribution to VaR is portfolio invariant

only if: (a) dependence across exposures is driven by a single systemic risk factor - a global

risk factor [...] and (b) each exposure is small”. The last financial crisis proved that ex-

posures can be very large and emerge in the national (vs. global) market (Atkinson, 2010,

[6]).

In the context of securitization, the ASRF implies “capital neutrality”, meaning that ”the

sum of the economic charges for individual tranches of a securitization equals the economic

capital for the underlying collateral pool” (Gordy, 2004, [43]).

37The model to compute the correlation of default risk in the portfolio is based on one of the theories of

the Nobel Prize winner, Robert Meron. He specified certain default-generating processes and used them to

predict the defaults, adding such variables as estimation of asset’s returns and their volatility. Assuming

normal distribution, one can calculate the estimated probability of default (Balthazar, 2006,[7]).38Under the ASRF framework “correlations in realised losses across exposures are assumed to be driven

by a single systematic risk factor meant to capture the effects of unexpected changes in economic conditions.

It can be shown that given this dependence assumption the loss rate for a well- diversified credit portfolio

depends only on the systematic factor, and not on idiosyncratic risk factors associated with individual

exposures. Furthermore, the total economic resources (both capital and provisions) that a bank must

maintain in order to satisfy a portfolio-wide Value-at-Risk (VaR) target can be determined by estimating

the sum of the conditional expected losses (CEL) associated with each exposure in the portfolio” (BIS,

2004b, [10]).39Value-at-risk defines the maximum default loss with a given probability over a given horizon.

23

The ASRF model was heavily criticized for producing specification errors. The core of the

argument lied in the assumption that a single common factor could determine the system-

atic element of credit risk. The portfolio was taken as highly grained, diversifying away

all idiosyncratic risk components. Moreover, the model restrictions made it impossible to

consider any single exposure independently. However, to calibrate the model one needs the

information about the portfolio correlation structure or the common factor itself to esti-

mate the exposure-specific dependence on the common factor. When there is not enough

information, the model could be flawy calibrated leading to more errors in measuring port-

folio credit risk40 (Tarashev, 2008,[85]).

Another point of criticism relates to the risk-weighting approach which gives incentives to

concentration of low-weighted assets (sovereign debt, mortgages and interbank lending) in

the portfolio. Emerging at the same period of time as the Basel Rules, Credit Default

Swaps (CDS) made it possible to go short in credit contracts, a practice not allowed in the

past. The banks exploited the opportunity of risk-derivatives, transforming the basic idea

of capital weights.

Some argue that both Basel Accords did not pay enough attention to off-balance sheet

exposures and securitization issues, which subsequently led to huge counterparty risks and

global contagion.

A significant number of arguments points at the pro-cyclicality of the Basel capital reg-

ulations. The basic claim is that people tend to underestimate risks in good times and

overestimate them in bad times. As an example, the amount of debt held by banks usually

fluctuates with the market values and if the latter are not fairly priced, reflecting future

cash flows, the pro-cyclicality may result. Bank counterparty and risk management are

stricter in bad times, but looser when the economic conditions are getting better. Com-

pensation schemes are designed in the way that endorse short-term orientation, but is not

particularly suitable over the whole business cycle.

According to Kane (2006, [53]), the negotiations of Basel II were very complex due to

the multiple financial institutions and regulatory committees, which caused many sim-

plifications and compromise solutions to difficult issues. Banks looking for the loopholes

in the regulations could manipulate rather subjective risk inputs41 to reduce the amount

40Basel II ignores calibrationg problems, assuming that the level of PD can fully determine firm-specific

dependence on the single common factor (Tarashev, 2008,[85]).41For example, over-the-counter exposures are difficult to price and there is usually not enough historical

data on that kind of instruments (Atkinson, 2010, [6]).

24

of required capital. For that purpose Pillar 2 and Pillar 3 were introduced as a market-

controlling mechanism, but the problem was not resolved. The idea of bank fully disclosure

and transparency under the fear of punishment has its justification in efficient market hy-

pothesis, which assumes rational behavior of market participants. If the markets are not

efficient and suffer from information deficiency, the possibility of financial bubbles and sys-

temic pro-cyclicality is not unthinkable(Atkinson, 2010, [6]).

There were also the debates regarding an increasing involvement of rating agencies. The

cornerstone is that non-rated entities could be uniformly charged at the conditions of the

old Accord and only the rated ones are the subject to improved capital allocation. Whereas

the US and European banks could use the IRB approach, banks in developing countries

would probably not. For the risky firm, rated BB– or below there was a clear incentive to

avoid the official rating procedure and to remain unrated, making use of lower risk weights

and so to reduce the cost of capital. The rating agencies even created such services as

preliminary rating without public disclosure (Danielsson et.al., 2001,[19]).

Summing up on Basel II, one can say that there are many critical opinions, the most

critical related to the sub-prime and the last systemic crisis. Most of the arguments contain

valuable inputs and suggestions, but those who ascribe all the failures of the last years to

the Capital Accords are certainly mistaken. There always has to be somebody to blame

and in this case it is Basel II, which stands out as one of the most influential regulatory

frameworks. But is it the rules, that are falsely composed or the underlying models or

the use of the models in these rules or the implementation of the rules altogether? There

is probably no answer to this question for the present system is of such an exponentially

increasing complexity, that it becomes impossible to single out some particular factor that

caused the damage. Every proposal in the regulation can be imagined as a vector that can

point either in one or in opposite direction and until we “open the box”, both destinations

are simultaneously reached. The metaphor from the quantum world can be a little bit

far-fetched but it also shows that it is not straightforward to predict the outcome of the

experiment 42. Unfortunately the costs of the “field research” here are too big to be ignored.

The quality and intensity of responsibility has to be much higher than in many other areas.

Thus the regulators should be committed to find the best staff, best instruments and best

control mechanisms to improve the system. That is probably the only thing they can do,

but this is a lot.

42Relates to the “Schrodinger’s cat” thought experiment and a concept of quantum superposition.

25

1.5 Basel III

At November 2010 Summit in Seoul, the Group of Twenty43 approved the new capital

adequacy framework, named “Basel III”. In December 2010 and January 2011 the latest

recommendations of the Basel Committee on Banking Supervision (BCBS) were published.

The revision of the existing capital rules was triggered by the financial crisis of 2008–200944,

which revealed many areas that needed further improvement and correction. Though the

Initiative is still in its developing phase45, the core principles have been already set.

The regulation attempts to increase the safety of the banking system by strengthening its

focus on capital, additionally turning its attention to the liquidity management. In general,

the new rules may be divided into 6 major statements:

1. increased quality of capital

2. increased quantity of capital

3. reduced leverage

4. increased short-term liquidity coverage

5. increased long-term balance sheet funding

6. strengthened risk capture, particularly counterparty risk

For the comparison overview between three Basel Accords see Table 4.3. For the timeline

of Basel III implementation - Table 4.4

Features in Review

1. “tighter numerator”

The deductions, earlier related to the total capital, now has to be imputed to the

common equity component of Tier 1. The higher subtraction percentage will apply

to equity stakes in other banks, insurance companies, financial companies and other

debt-like instruments if these stakes exceed 10% of the owner’s bank common equity

in aggregate. Under Basel II most of them were only 50% deductible. The elements

43G-20 countries include: Argentina, Australia, Brazil, Canada, China, France, Germany, India, Indone-

sia, Italy, Japan, Mexico, Russia, Saudi Arabia, South Africa, Republic of Korea, Turkey, the UK, the USA

and the EU as the 20th memeber.44The dates vary depending on the source.45Mostly related to the treatment of Systemically Important Financial Institutions (SIFIs), a.k.a. “too-

big-to-fail”.

26

of Tier 1 or Tier 2, not anymore eligible to belong to either category because of

their weak loss-absorbing capacity, will be eliminated by consecutive 10% tranches

annually from 2013 to 2023. Only Tier 1- “carve outs” are estimated to be around 25

- 40%. The amount of goodwill and deferred tax assets have to be carefully managed

by large banks being under the light of regulative attention. As the new requirements

are already discounted by markets, the banks would probably try to restructure their

balance sheets as soon as possible.

2. “more is better”

The last crisis exposed the fact, that the core capital was insufficient to absorb losses.

This led to the stricter definition of capital, meaning that “common equity Tier

1” (instead of “core Tier 1”) now comprises common shares and retained earnings

only. This is set to be 7% now, where 4.5% comes from minimum common equity

(2% under Basel II) and 2.5% from capital conservation buffer. The total capital

(including conservation buffer) has to be raised to 10.5% (vs. 8% under Basel II),

whereas Tier 1 has to constitute at least 6%. The capital conservation buffer should

help to prevent cyclicality by gaining additional slack through the periods of growth.

It is also possible that the banks, especially SIFIs may face total capital requirements

of 13 - 15% due to further revisions and BCBS add-ons.

3. “less greed”

The key message is that leverage can not exceed the limit of 3%, meaning that a bank

total assets (on- and off-balance sheet) should not be more than 33 times the bank

own capital. These ratios will be set in force in 2018 and starting from 2013, the

banks will be monitored on leverage data. The ratio has to be on a gross, unweighted

basis and not consider risks related to the assets. Taking into account the fact, that

the market or rating agencies can put pressure on banks to maintain a higher leverage

ratio than officially required, one can expect that the banks would look for riskier

return opportunities and to sell low margin assets (e.g. mortgages), driving the prices

down.

4. “take care of liquidity”

The Liquidity Coverage Ratio (LCR) was introduced to secure short-term resilience

to potential problems. Basically, banks have to sustain high-quality liquid assets

(HQLA) to cover 30 days’ net outflows following a short-term liquidity crisis. HQLA

have to amount to at least 100% of net outflows and are categorized into Level 1

and Level 2 assets. The first class contains cash, reserves held at the central bank

and sovereign bonds or items rated at least AA–. The second class includes sovereign

27

bonds or similar products rated between A– and A+, corporate and covered bonds

with the rating of minimum AA–. Beside that, Level 2 assets are restricted to 40%

of HQLA after a 15% haircut. As an implication for these measures, the risk of bank

run should be reduced, improving the stability in the markets. However for banks

this can mean lower profitability, as they have to hold more liquid, low-yield assets.

5. “healthy balance sheet, healthy spirit’

By adopting the Net Stable Funding Ratio (NSFR), the Basel Committee intended to

decrease bank dependency on short-term funding and protect them from the conse-

quences of a longer-term liquidity crisis. Basel III demands that weighted assets with

maturity longer than one year, as well as some off-balance sheet exposures, are 100%

covered by long-term stable funding. Generally, the weighting factors for assets vary

from 0% and 5% for cash and government bonds respectively, to 65% for mortgages,

85% for retail loans, and 100% for other assets. The liabilities for stable funding are

determined through weighting factors from 100% for Tier 1 capital to 90% for core

retail deposits and 50% for unsecured wholesale funding and ECB funding at 0%.

As a result, banks would probably rely less on their short-term funding and increasing

the stability of the funding mix. But they would need to pile up more of wholesale

and corporate deposits with maturities longer than one year and the demand for

term debt is rather limited right now. That can lead to higher funding costs. The

competition could be weakened because stronger banks with higher NSFR could try

to influence market prices for assets, the option weaker banks would not be able to use.

6. “beware of Lehman”

The Counterparty Credit Risk (CCR) management should be particularly taken care

of. The focus lies on the risk on derivative exposures and in order to deal with

this issue, the Committee introduced the concept of Credit Valuation Adjustments

(CVA) capital charge and a central counterparty for the treatment of market-to-

market counterparty risk. For the calibration of CCR-modeling some banks will be

permitted to use Internal Model Methods (IMM). These banks will need to integrate

the changes in the counterparty credit spreads in their calculations, which will result

in an additional capital charge.

According to the Standard&Poor’s research, this approach has several calibration

issues. Their calculations show that the banks can expect additional capital charge

of about 15%-20% of total regulatory Exposure-at-Default (EAD). Combined with

28

other requirements this would mean the total capital charge for counterparty risk at a

level between 20% and 25% of EAD (2.5% - 4% under Basel II), which is a big increase.

The researchers mention also other potential problems like incentives for banks to use

qualified clearing houses for OTC derivative transactions more frequently, as they are

not expected to make capital charges. This increased concentration at central clearing

houses under the risk-free assumption (zero capital charge) can expose the system to

further potential risks. There is also a possibility that banks would try to push OTC