marketing science institute - how incentives shape strategy: the … · 2018-03-05 · 1 how...

TRANSCRIPT

1

How Incentives Shape Strategy:

The Role of CMO and CEO Equity

Compensation in Inducing Marketing Myopia

Martin Artz, Frankfurt School of Finance & Management

Natalie Mizik, University of Washington

February 2018

2

Do Managers Have Appropriate

Long-term Focus?

The Concern Over

Myopic Management:

• Managers may unduly emphasize current-

term financial performance

(i.e., have a discount rate higher than justified by the cost of capital

considerations)

3

Summary of Previous Myopic Research

• Wave 1: Econ Theory – Myopic Management is possible under certain conditions (Narayanan 1985, Stein

1989, Bizjak et al. 1993)

• Wave 2: Accounting Lit on Accruals Manipulation (AM) – Accrual Manipulation occurs and has negative consequences (Teoh, Welch and Wong

JFE 1998, Rangan JFE 1998, DuCharme, Malatesta and Sefcik JFE 2004)

• Wave 3: Acct and Mktg Lit on Real Activity Manipulation – Real Activity Manipulation (MM) occurs and has negative consequences that are more

severe than AM (Graham at al. 2005, Roychowdhury 2006, Mizik and Jacobson 2007, Cohen and Zarowin 2010, Kothari et al. 2016)

• Wave 4: Myopic Marketing Management

– MMM takes various forms (Chapman and Steenburgh 2011, Chakravarty and Grewal 2011, Moorman et al. 2012, Ahearne et al. 2016)

• Wave 5: What Drives Myopic Management ???

4

Study Objectives:

Assess whether the CMOs help reduce

the incidence and/or the severity of

Myopic Marketing Management

– does CMO presence affect incidence & severity of MMM?

– does CMO equity compensation affect incidence &

severity of MMM?

– do CMOs trade personal equity holding more actively

with incidence & severity of MMM?

5

Controversy around equity

compensation

“Pay-for-

performance“

theory

“Pay-without-

performance“

theory

Equity incentives align manager and owner

incentives; can increase firm value; stock options

reward making risky decisions

Event studies: positive abnormal returns for

announcements of stock-price based

compensation plans (e.g., DeFusco et al. 1990)

Top executives influence compensation

committees

Top executives manipulate the timing of equity /

option grants (Yermack, 1997)

Top executive manipulate stock prices by

announcements or manipulation of profits

6

CMO presence and MMM

Conflicting views on CMO effects and power:

1. CMOs are increasingly important. CMO’s role is to mitigate

marketing resource misallocation and to oversee the overall marketing

strategy (Aaker 2008, Jaworski 2011, Court 2007)

2. “The CMO Is Dead” (Forbes On Marketing, 10/03/2012, Webster et

al. 2005): CMOs are increasingly powerless and peripheral

Hypothesis 1: The mere presence of a CMO in an organization reduces or has no relation to the incidence and severity of MMM

7

Equity Compensation and MMM

Economics literature:

Under Perfect information tying managerial compensation to stock

prices leads to efficient managerial decision making

Imperfect information Incentive to manipulate earnings

e.g., Bizjak, Brickley, and Coles (1993) show that managers are more

likely to engage in MM the more managerial remuneration depends

on current stock price

Hypothesis 2: The more executive compensation

depends on equity, the greater the extent (incidence

and severity) of MMM

8

CMO compensation and MMM

1. Managers further down in the firm hierarchy can be more influential in

their domain than the CEOs (Jiang et. al 2010) and have “greater

opportunity to influence reported earnings in a manner that maximizes

these managers’ personal income” (Oberholzer-Gee and Wulf, ssrn 2012)

2. Currim et al. 2012, Luo et al. 2012: Equity-based compensation may curb

executive opportunism and reduce myopic management

Hypothesis 3: CMO equity incentives have a greater association with MMM than those of the CEO. The effect might be positive (increasing MMM, consistent with econ theory) or negative (decreasing MMM, consistent with mktg literature)

9

CMO Equity Trading and MMM

If CMOs facilitate MMM (or have advanced insight into MMM’s future negative effects on valuation), they would take advantage of the opportunity and trade more actively in the years when MMM occurs to divest their personal equity holdings

Hypothesis 4: There is a greater equity selling activity in the years of MMM

10

Data: 1993-2014

• Annual COMPUSTAT for accounting data

• CRSP for stock returns

• Execucomp for executive compensation

• Thomson Reuters and US Insider Filing Feed for

executive trading

it

itit

Assets

Expense D)/Adv&R-D/(SGA&RIntensity /Mktg/AdvD&R

1

)(Accruals Total

tsTotalAsset

trtizDeprecAmmotrmDebttionLongTeCurrentPortbiltCurrentLiatCashtetsCurrentAss

it

it

itAssets

onDepreciati before Income OperatingROA

11

Measuring Exec Equity Incentives

• Identifying Executives (CEO, CMO, CFO, etc.): Execucomp database from 1993 to 2014

Identification of CMOs by job title (e.g., “CMO”, “Marketing”,

“Sales”)

• Equity Incentive: Sensitivity of exec’s annual

compensation to a 1% change in stock price

Equity Incentivei,t = Delta Stocksi,t + Delta Optionsi,t

(Salaryi,t + Bonusi,t + Delta Stocksi,t + Delta Optionsi,t)

Delta Stocksi,t = Sensitivity of stockholdings to stock price = .01 × Price𝑡 × Sharesi,t

Delta Optionsi,t = Sensitivity of optionholdings to stock price(Core and Guay 1999)

12

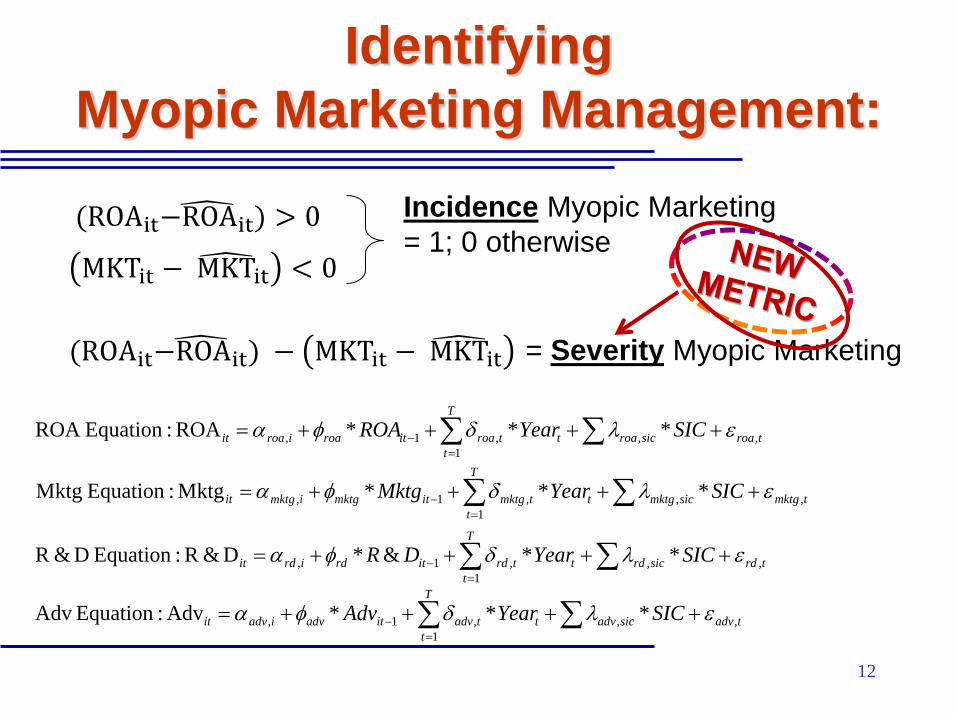

Identifying

Myopic Marketing Management:

T

t

trdsicrdttrditrdirdit SICYearDR1

,,,1, **&*D&R:Equation D&R

T

t

tmktgsicmktgttmktgitmktgimktgit SICYearMktg1

,,,1, ***Mktg:Equation Mktg

T

t

tadvsicadvttadvitadviadvit SICYearAdv1

,,,1, ***Adv:Equation Adv

T

t

troasicroattroaitroairoait SICYearROA1

,,,1, ***ROA:EquationROA

MKTit − MKT it < 0

(ROAit−ROAit ) > 0 Incidence Myopic Marketing

= 1; 0 otherwise

= Severity Myopic Marketing (ROAit−ROAit ) − MKTit − MKT it

13

Three Proxies of

Myopic Marketing Management

Incidence of Myopic 1. Management: ROA surprise>0, Mktg surprise <0, R&D surprise <0

2. Marketing: ROA surprise>0, Mktg surprise <0

3. Advertising: ROA surprise>0, Adv surprise <0

Severity of Myopic 1. Management: (ROA surprise - Mktg surprise - R&D surprise)

2. Marketing: (ROA surprise - Mktg surprise)

3. Advertising: (ROA surprise - Adv surprise)

14

Testing CMO Presence Effects:

no significant effects found

1. Basic Regressions may be subject to selection bias:

– Logit for Incidence, OLS for Severity

2. Treatment Effects, Selection on Observables:

– IPWRA

– Heckman

3. Treatment Effects, Relaxing Conditional Independence Assm:

– endogenous treatment effects models

4. Endogeneity tests

Incidence

Myopic

MKT_R&D

Incidence

Myopic

MKT

Incidence

Myopic

ADV

Severity

Myopic

MKT_R&D

Severity

Myopic

MKT

Severity

Myopic

ADV

CMO Presence (t) ATE 0.010 0.011 -.016 0.004 0.004 -0.0005

[0.011] [0.013] [0.018] [0.004] [0.003] [0.003]

Myopia Controls Included Included Included Included Included Included

Observations 11,330 11,330 5,000 11, 330 11, 330 5,000

Endogeneity test n/s n/s n/s n/s n/s n/s

15

Testing the Effect of Executive Equity

Incentives and Incidence of MMM

1. Instrumental Variables and Control Function approach to Address Potential Endogeneity

2. Treatment Effects models, Heckman

3. Differences-in-Differences (using FAS 123 adoption in 2005)

16

Executive Equity Incentives and Incidence of

MMM: no CEO effect, but CMO equity

increases MMM Incidence

Severity

Myopic

MKT_R&D

Severity

Myopic

MKT_R&D

Severity

Myopic

MKT

Severity

Myopic

MKT

Severity

Myopic

ADV

Severity

Myopic

ADV

CEO Equity Incentive (t-1) 0.172 0.033 -0.008 -0.148 0.084 -0.029

[0.160] [0.164] [0.147] [0.150] [0.200] [0.207]

CMO Equity Incentive (t-1) 1.639*** 1.721*** 1.422*

[0.561] [0.545] [0.765]

Abnormal Accruals (t) 5.141*** 5.158*** 5.462*** 5.470*** 3.900*** 3.883***

[0.458] [0.454] [0.418] [0.415] [0.605] [0.605]

Size (t-1) -0.084*** -0.100*** -0.043* -0.059** -0.040 -0.054

[0.030] [0.030] [0.025] [0.025] [0.035] [0.035]

Market-to-Book (t-1) 0.039*** 0.035*** 0.039*** 0.035*** 0.023** 0.019*

[0.008] [0.008] [0.008] [0.008] [0.010] [0.011]

Leverage (t-1) -1.203*** -1.165*** -0.947*** -0.912*** -0.802*** -0.772***

[0.227] [0.228] [0.189] [0.190] [0.298] [0.299]

Annual Stock Return (t-1) 0.263*** 0.252*** 0.240*** 0.229*** 0.281*** 0.269***

[0.048] [0.049] [0.047] [0.048] [0.070] [0.071]

Sales Volatility (t-1) -0.901*** -0.901*** 0.068 0.069 0.503** 0.502**

[0.275] [0.276] [0.162] [0.162] [0.248] [0.247]

Competition (t-1) 1.650 1.368 -0.116 -0.364 -1.792 -1.881

[1.595] [1.594] [1.532] [1.521] [2.339] [2.339]

Observations 5,135 5,135 5,135 5,135 2,625 2,625

Wald test, p-value

(Ho: γCMO= γCEO)

6.83

0.009

9.87

0.002

3.01

0.083

Hausman test of endogeneity n/s n/s n/s n/s n/s n/s

17

Executive Equity Incentives and Severity of

MMM: no CEO effect, but

CMO equity increases MMM Severity

Severity

Myopic

MKT_R&D

Severity

Myopic

MKT_R&D

Severity

Myopic

MKT

Severity

Myopic

MKT

Severity

Myopic

ADV

Severity

Myopic

ADV

CEO Equity Incentive (t-1) 0.017** 0.011 0.013* 0.008 0.006 0.003

[0.008] [0.008] [0.007] [0.007] [0.007] [0.007]

CMO Equity Incentive (t-1) 0.070** 0.059** 0.054**

[0.029] [0.026] [0.026]

Abnormal Accruals (t) 0.657*** 0.658*** 0.600*** 0.600*** 0.571*** 0.570***

[0.042] [0.042] [0.039] [0.039] [0.051] [0.051]

Size (t-1) 0.005*** 0.004*** 0.004*** 0.003** -0.001 -0.001

[0.001] [0.001] [0.001] [0.001] [0.001] [0.001]

Market-to-Book (t-1) 0.002*** 0.002*** 0.002*** 0.002*** 0.001 0.001

[0.001] [0.001] [0.001] [0.001] [0.001] [0.001]

Leverage (t-1) -0.055*** -0.054*** -0.044*** -0.043*** 0.006 0.007

[0.009] [0.009] [0.009] [0.009] [0.010] [0.011]

Annual Stock Return (t-1) 0.028*** 0.027*** 0.025*** 0.025*** 0.022*** 0.021***

[0.003] [0.003] [0.003] [0.003] [0.003] [0.003]

Sales Volatility (t-1) -0.015 -0.015 -0.008 -0.007 0.006 0.005

[0.014] [0.014] [0.013] [0.013] [0.019] [0.019]

Competition (t-1) 0.034 0.025 0.020 0.012 -0.050 -0.054

[0.069] [0.069] [0.067] [0.067] [0.068] [0.067]

Observations 5,135 5,135 5,135 5,135 2,625 2,625

Wald test, p-value

(Ho: γCMO= γCEO)

3.45

0.063

3.26

0.071

3.37

0.067

Hausman test of endogeneity n/s n/s n/s n/s n/s n/s

18

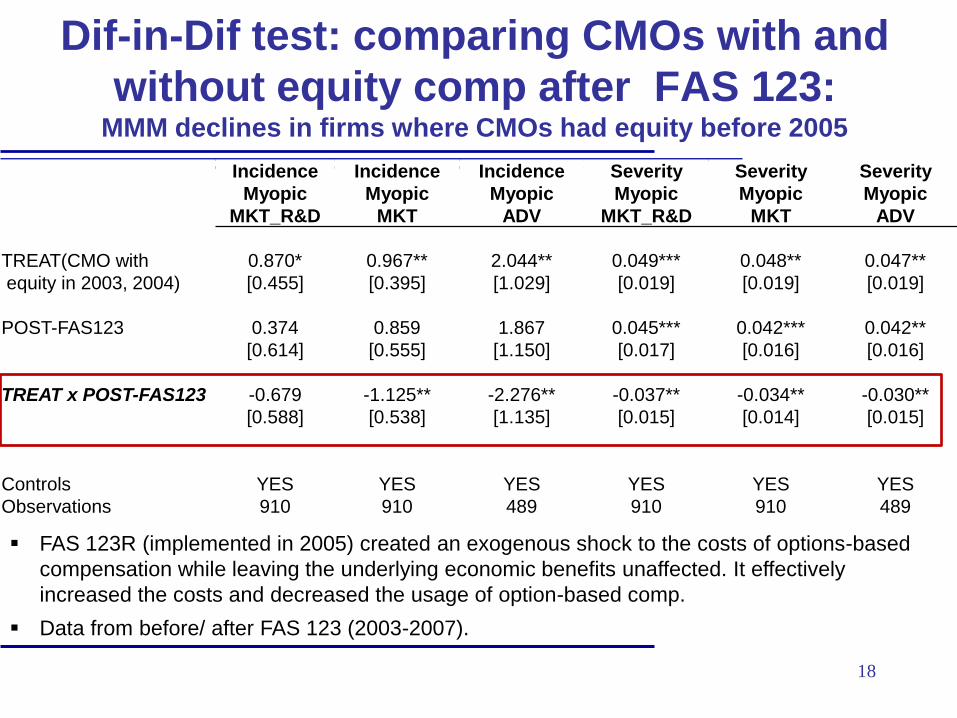

Incidence

Myopic

MKT_R&D

Incidence

Myopic

MKT

Incidence

Myopic

ADV

Severity

Myopic

MKT_R&D

Severity

Myopic

MKT

Severity

Myopic

ADV

TREAT(CMO with 0.870* 0.967** 2.044** 0.049*** 0.048** 0.047**

equity in 2003, 2004)

[0.455] [0.395] [1.029] [0.019] [0.019] [0.019]

POST-FAS123 0.374 0.859 1.867 0.045*** 0.042*** 0.042**

[0.614] [0.555] [1.150] [0.017] [0.016] [0.016]

TREAT x POST-FAS123 -0.679 -1.125** -2.276** -0.037** -0.034** -0.030**

[0.588] [0.538] [1.135] [0.015] [0.014] [0.015]

Controls YES YES YES YES YES YES

Observations 910 910 489 910 910 489

Dif-in-Dif test: comparing CMOs with and

without equity comp after FAS 123: MMM declines in firms where CMOs had equity before 2005

FAS 123R (implemented in 2005) created an exogenous shock to the costs of options-based

compensation while leaving the underlying economic benefits unaffected. It effectively

increased the costs and decreased the usage of option-based comp.

Data from before/ after FAS 123 (2003-2007).

19

Incidence

Myopic

MKT_R&D

Incidence

Myopic

MKT

Incidence

Myopic

ADV

Severity

Myopic

MKT_R&D

Severity

Myopic

MKT

Severity

Myopic

ADV

TREAT(CEO with high -0.057 0.246 0.135 0.026 0.021 -0.002

equity in 2003, 2004)

[0.419] [0.401] [0.847] [0.019] [0.018] [0.017]

POST-FAS123 -0.336 0.616 0.279 0.018 0.019 0.017

[0.487] [0.470] [1.010] [0.023] [0.021] [0.018]

TREAT x POST-FAS123 0.196 -0.529 0.686 -0.030 -0.026 0.012

[0.553] [0.512] [1.081] [0.022] [0.020] [0.018]

Controls YES YES YES YES YES YES

Observations 423 423 209 423 423 209

Dif-in-Dif test: comparing CEOs with high vs.

low equity comp in no-CMO firms: no significant effect on MMM

FAS 123R (implemented in 2005) created an exogenous shock to the costs of options-based

compensation while leaving the underlying economic benefits unaffected. It effectively increased

the costs and decreased the usage of option-based comp.

Data from before/ after FAS 123 (2003-2007) for firms that did not have a CMO.

20

CMO Exercise More Options when

MMM Occurs and is More Severe

Myopic Management Proxy

Incidence

Myopic

MKT_R&D

Incidence

Myopic MKT

Incidence

Myopic ADV

Severity

Myopic

MKT_R&D

Severity

Myopic MKT

Severity

Myopic ADV

Myopic Management Proxy (t) 0.042*** 0.028*** 0.036** 0.127*** 0.134*** 0.070

[0.012] [0.011] [0.017] [0.041] [0.045] [0.069]

CEO Share Options Ex. (t) 0.426*** 0.426*** 0.429*** 0.424*** 0.424*** 0.430***

[0.028] [0.028] [0.036] [0.028] [0.028] [0.037]

Abnormal Accruals (t) -0.007 -0.002 -0.096 -0.059 -0.058 -0.115

[0.053] [0.054] [0.078] [0.060] [0.061] [0.090]

Annual Stock Return (t-1) 0.065*** 0.066*** 0.073*** 0.064*** 0.064*** 0.074***

[0.008] [0.008] [0.012] [0.008] [0.008] [0.012]

Stock Return Volatility (t-1) -0.186** -0.179** -0.248** -0.168** -0.161** -0.238**

[0.078] [0.079] [0.107] [0.078] [0.078] [0.108]

Market to Book (t-1) 0.004*** 0.004*** 0.004*** 0.004*** 0.004*** 0.004***

[0.001] [0.001] [0.001] [0.001] [0.001] [0.001]

R&D Expenses (t-1) -0.142** -0.127** -0.068 -0.131** -0.139** -0.079

[0.062] [0.063] [0.085] [0.062] [0.063] [0.085]

Market Value (t-1) 0.108 0.116 -0.412 0.091 0.101 -0.443

[0.315] [0.315] [0.324] [0.314] [0.314] [0.324]

CMO Equity Holdings (t-1) -0.009 -0.015 -0.075 -0.013 -0.013 -0.069

[0.041] [0.042] [0.047] [0.042] [0.042] [0.047]

Observations 3,303 3,303 1,773 3,303 3,303 1,773

21

CMO Reduce Equity Holdings when

MMM Occurs and is More Severe

Myopic Management Proxy

Incidence

Myopic

MKT_R&D

Incidence

Myopic MKT

Incidence

Myopic ADV

Severity

Myopic

MKT_R&D

Severity

Myopic MKT

Severity

Myopic ADV

Myopic Management Proxy (t) -0.008 -0.012*** -0.014** -0.036*** -0.037** -0.042*

[0.005] [0.004] [0.007] [0.014] [0.015] [0.022]

CEO Share Options Ex. (t) 0.014** 0.014** 0.010** 0.014** 0.014** 0.010**

[0.006] [0.006] [0.005] [0.006] [0.006] [0.005]

Abnormal Accruals (t) -0.077** -0.070** -0.053** -0.060 -0.061 -0.039

[0.035] [0.033] [0.024] [0.037] [0.037] [0.028]

Annual Stock Return (t-1) -0.009*** -0.008*** -0.009** -0.008*** -0.008*** -0.009*

[0.003] [0.003] [0.004] [0.003] [0.003] [0.005]

Stock Return Volatility (t-1) -0.003 -0.001 -0.037 -0.005 -0.006 -0.038

[0.030] [0.030] [0.028] [0.030] [0.030] [0.028]

Market to Book (t-1) -0.024 -0.028 0.004 -0.027 -0.024 0.010

[0.025] [0.026] [0.028] [0.025] [0.026] [0.029]

R&D Expenses (t-1) 0.507*** 0.494*** 0.396*** 0.510*** 0.507*** 0.407***

[0.068] [0.067] [0.062] [0.068] [0.068] [0.063]

Market Value (t-1) -0.001* -0.001 -0.000 -0.001 -0.001 -0.000

[0.000] [0.000] [0.000] [0.000] [0.000] [0.000]

CMO Equity Holdings (t-1) -0.006** -0.006** -0.004** -0.006** -0.006** -0.004**

[0.003] [0.003] [0.002] [0.003] [0.003] [0.002]

Observations 1,913 1,913 1,073 1,913 1,913 1,073

22

Conclusion

The mere presence of a CMO does not reduce either the Incidence or the Severity of MMM

CMO equity compensation increases the incidence and severity of MMM

In the years when MMM occurs, CMOs trade more shares and exercise more options

Results in contrast to dominant views in the marketing literature but in support of recent comparable work in accounting and financial economics