marketing assingment latest

TRANSCRIPT

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 1/15

1 | P a g e

ANALYSIS OF BANKING INDUSTRY USING

MICHAEL PORTERS FIVE FORCES MODEL

Marketing Management

ASSIGNMENT NO. 1

Submitted to: Prof. Komal Chopra

SYMBIOSIS INSTITUTE OF MANAGEMENT STUDIES

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 2/15

2 | P a g e

Industry Insights

Scheduled Commercial Banks (SCBs) comprises of 27 Public Sector Banks (PSBs), 22 Private

Sector Banks and 28 Foreign Banks.

For the purpose of the study I have considered all 77 SCBs profiled in the publication. The

data for the study was collated through responses received directly from banks, from

sources in public domain like RBI documents and annual reports of banks. I have examined

various parameters such as income growth and composition, business growth, asset quality

and market risk to gain insights on the profiled banks.

Total Assets

The total Assets of 77 SCBs rose by more than double to Rs 43,264.9 bn during FY09 , as

compared to the asset base of Rs 19740.2 bn in FY04. During FY09 , the total asset base of

the SCBs was equivalent to 91.8% of Indias GDP, as compared to 62.7% of GDP in FY04.

Public Sector Banks (PSBs) dominate the banking industry with a contribution of close to69.9% to total assets, followed by private sector banks which account for around 21.7% of

total assets.

Furthermore, based on the banks balance sheet size (total assets), Dun & Bradstreet has

classified that banks as large sized banks, medium sized banks and small sized banks using

the 80:15:5 principle.

The large sized banks are defined as banks with a balance sheet size of more than Rs600 bn,

medium sized from Rs 200 bn to Rs 600 bn and small sized banks are banks with a balance

sheet of up to Rs 200 bn.

In line with this principle there are 22 large sized ban ks with a balance sheet size of more

than Rs 600 bn together accounting for close to 80% of the total assets of SCBs. These

comprise of 16 PSBs, 3 private sector banks and 3 foreign banks.

The 18 medium sized banks account for the next 15% of the total ass ets, and include 11

PSBs, 5 private sector banks and 2 foreign banks. The small size banks at the lower end of

the spectrum account for 5% of the total assets and include 37 banks comprising of 23

foreign banks and 14 private sector banks.

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 3/15

3 | P a g e

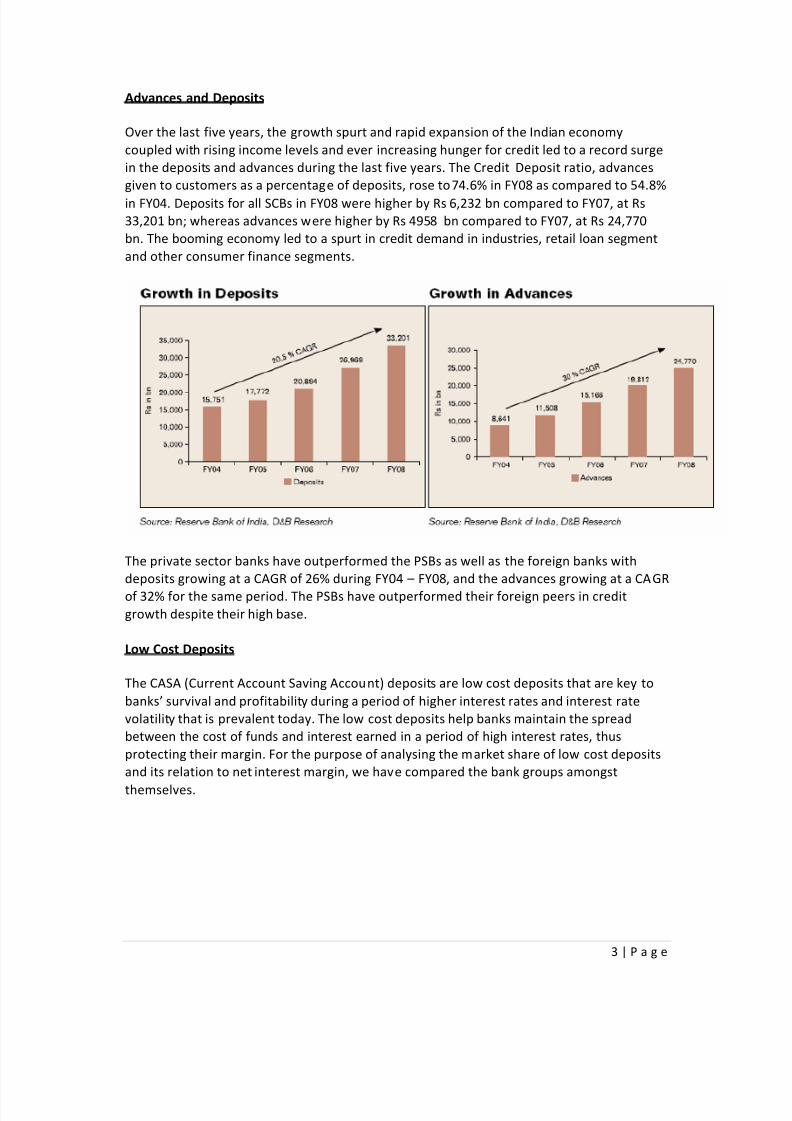

Advances and Deposits

Over the last five years, the growth spurt and rapid expansion of the Indian economy

coupled with rising income levels and ever increasing hunger for credit led to a record surge

in the deposits and advances during the last five years. The Credit Deposit ratio, advances

given to customers as a percentage of deposits, rose to74.6% in FY08 as compared to 54.8%

in FY04. Deposits for all SCBs in FY08 were higher by Rs 6,232 bn compared to FY07, at Rs

33,201 bn; whereas advances were higher by Rs 4958 bn compared to FY07, at Rs 24,770

bn. The booming economy led to a spurt in credit demand in industries, retail loan segment

and other consumer finance segments.

The private sector banks have outperformed the PSBs as well as the foreign banks with

deposits growing at a CAGR of 26% during FY04 FY08, and the advances growing at a CAGR

of 32% for the same period. The PSBs have outperformed their foreign peers in credit

growth despite their high base.

Low Cost Deposits

The CASA (Current Account Saving Account) deposits are low cost deposits that are key to

banks survival and profitability during a period of higher interest rates and interest rate

volatility that is prevalent today. The low cost deposits help banks maintain the spread

between the cost of funds and interest earned in a period of high interest rates, thus

protecting their margin. For the purpose of analysing the market share of low cost deposits

and its relation to net interest margin, we have compared the bank groups amongst

themselves.

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 4/15

4 | P a g e

Amongst foreign banks, the share of demand deposits and savings bank deposits rose to

44.7% of the banks total deposits in FY08 as compared to a 33.8% share of low cost

deposits in FY03; and amongst private banks the share of low cost deposits increased to

32.8% from a share of 23.8% of total deposits. The ratio of net interest income to total

assets increased to 3.8% and 2.4% in 2008 for foreign banks and private banks respectively.

However, for PSBs there is a slight decline in share of low cost deposits and a drop of 75

basis points in the ratio of net interest income to total assets.

Total Income

The total income of the SCBs doubled to Rs 3,688.9 bn in FY08 as compared to an income of

Rs 1,838.7 bn in FY04. The PSBs continue to dominate the Indian banki ng industry,

accounting for more than 66% share in total income; followed by 23.86% share of private

sector banks.

The total income of these banks comprises of interest income and noninterest income. The

interest income is the interest earned on loans and advances besides income from

investments; whereas the non interest income includes fee based income, income from

treasury operations, gain/loss on sale or revaluation of investments, gain/loss on sale of

banking and non-banking assets to name some.

Near-record loan growth lifts interest income

Accelerated economic growth in India over the last few years, coupled with heightenedindustrial activity and the subsequent robust credit growth lifted interest incomes, a major

constituent of the banks total income, by a level of 21% CAGR during FY04 FY08.

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 5/15

5 | P a g e

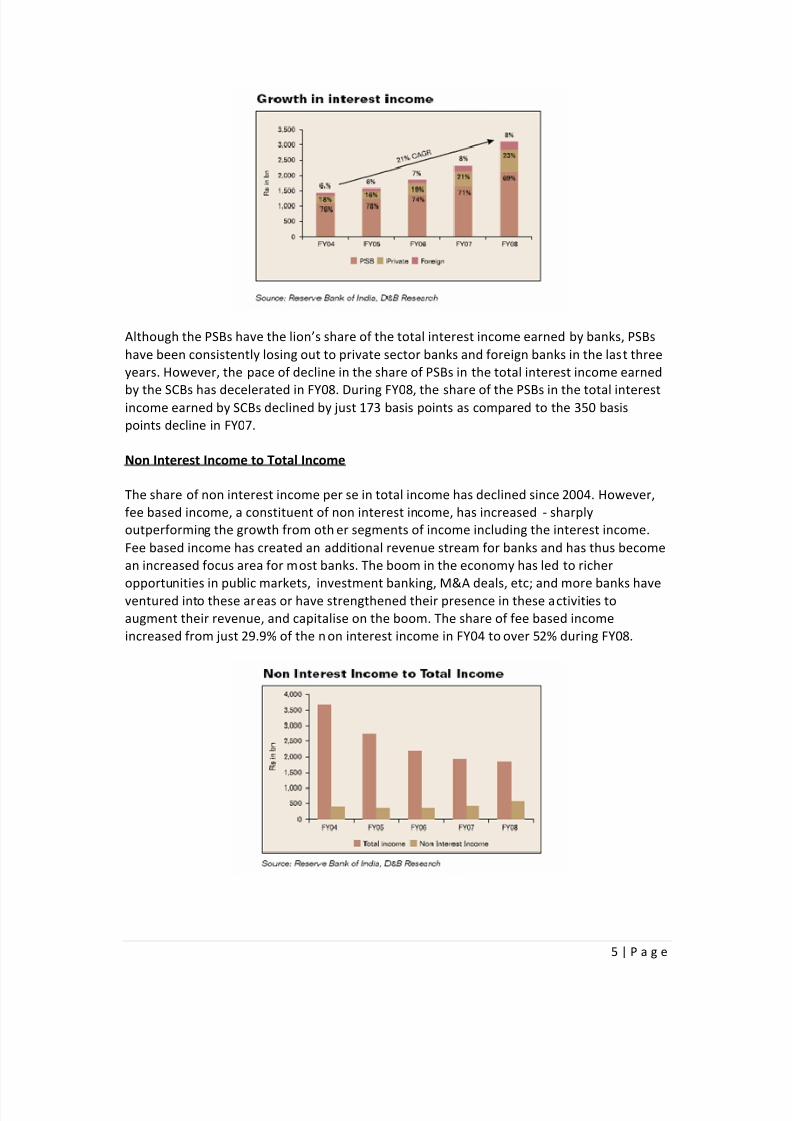

Although the PSBs have the lions share of the total interest income earned by banks, PSBs

have been consistently losing out to private sector banks and foreign banks in the last three

years. However, the pace of decline in the share of PSBs in the total interest income earned

by the SCBs has decelerated in FY08. During FY08, the share of the PSBs in the total interestincome earned by SCBs declined by just 173 basis points as compared to the 350 basis

points decline in FY07.

Non Interest Income to Total Income

The share of non interest income per se in total income has declined since 2004. However,

fee based income, a constituent of non interest income, has increased - sharply

outperforming the growth from oth er segments of income including the interest income.

Fee based income has created an additional revenue stream for banks and has thus become

an increased focus area for most banks. The boom in the economy has led to richer

opportunities in public markets, investment banking, M&A deals, etc; and more banks haveventured into these areas or have strengthened their presence in these activities to

augment their revenue, and capitalise on the boom. The share of fee based income

increased from just 29.9% of the n on interest income in FY04 to over 52% during FY08.

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 6/15

6 | P a g e

In 2008, the non interest income as a per cent of total income was higher for foreign banks

at over at 30%, followed by private sector banks at 19.1% and just 12.9% for PSBs.

In terms of the income share from fee based income, the PSBs have lost share to their

private sector and foreign peers in all four years, and have a much lesser share of fee

income, as compared to their dominance in interest income. The consolidated fee based

income for SCBs outstripped growth in interest income by growing at a CAGR of 27% during

FY04 FY08. For private sector banks, fee based income grew at a CAGR of 45% for the

same period, outperforming its foreign and public sector peers, whose fee based income

grew at a CAGR of 35% and 18% respectively. In 2008, fee based income accounted for close

to 12% of the total income of private sector bank; over 15% share in total income of foreign

banks and just 6% of the total income of PSBs.

Segment Wise Revenue Distribution

In accordance to RBI guidelines for SCBs on AS 17 (Segment Reporting) dated Apr 18,

2007; and effective Mar 31, 2008 the segment wise revenue of the banks are reported

under retail banking, corporate/wholesale banking, treasury, and other banking operation s.

Other banking operations may include hire purchase and leasing operations, gain/loss on

sale of banking and non-banking assets and other items not attributable to the other three

segments.

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 7/15

7 | P a g e

Retail banking is a high volume business which constitutes a majority of the total revenuefor both public and private sector banks. When compared to the private sector, PSBs which

are perceived to be risk averse, have higher exposure to the retail banking segment, and

lesser exposure to treasury operations.

Among the PSBs, SBI alone accounts for more than one fourth of the income pie from retail

banking operations. In fact, out of SBIs total revenue close to half is contributed from its

retail banking operations. The higher share of the PSBs in retail banking can be attributed to

their unmatched rural reach which keeps them far ahead of their private sector and foreign

peers in terms of their presence in rural areas. The PSBs account for 94.7% of the total

branches in rural areas.

Treasury operations rule the business of foreign banks

Of the total 28 foreign banks, segment wise revenue was unavailable for six foreign banks

due to non availability of their annual reports. On an aggregate level, for the 22 banks for

which segment wise revenue was available, treasury operations ruled their top line with a

contribution of 34% to the segment revenue, followed by a 31% contribution by retail

banking operations and a 28% contribution by corporate banking operations.

Within 22 banks, only 12 banks had exposure to retail bankin g. These 12 banks show that

retail banking operations form a major chunk accounting for 36% of their revenue; followed

by treasury operations and corporate banking. The 10 foreign banks that did not have any

exposure to retail banking had a majority of the ir revenue from either corporate banking or

treasury operations. Unlike their public sector and private sector peers, almost all the

foreign banks are very active in treasury operations in India.

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 8/15

8 | P a g e

MAJOR MARKET PLAYERS IN INDIAN BANKING INDUSTRY

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 9/15

9 | P a g e

MARKET SHARE OF TOP PLAYERS IN INDIAN BANKING INDUSTRY

GROWTH OF INDIAN BANKING INDUSTRY

The growth in the Indian Banking Industry has been more qualitative than quantitative and

it is expected to remain the same in the coming years. Based on the projec tions made in the

"India Vision 2020" prepared by the Planning Commission and the Draft 10th Plan, the

report forecasts that the pace of expansion in the balance -sheets of banks is likely to

decelerate. The total assets of all scheduled commercial banks by end-March2010 is

estimated at Rs 40,90,000 crores. That will comprise about 65 per cent of GDP at current

market prices as compared to 67 per cent in 2002 -03. Bank assets are expected to grow at

an annual composite rate of 13.4 per cent during the rest o f the decade as against the

growth rate of 16.7 per cent that existed between 1994 -95 and 2002-03. It is expected that

there will be large additions to the capital base and reserves on the liability side.

The Indian Banking Industry can be categorized into non -scheduled banks and scheduled

banks. Scheduled banks constitute of commercial banks and co -operative banks. There are

about 67,000 branches of Scheduled banks spread across India. As far as the presen t

scenario is concerned the Banking Industry in India is going through a transitional phase.

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 10/15

10 | P a g e

The Public Sector Banks(PSBs), which are the base of the Banking sector in India account for

more than 78 per cent of the total banking industry assets. Unfortun ately they are burdened

with excessive Non Performing assets (NPAs), massive manpower and lack of modern

technology. On the other hand the Private Sector Banks are making tremendous progress.

They are leaders in Internet banking, mobile banking, phone bank ing, ATMs. As far as

foreign banks are concerned they are likely to succeed in the Indian Banking Industry.

PORTERS FIVE FORCES MODEL OF COMPETITION

The nature of competition in the industry in large part determines the content of strategy,especially business level strategy .based it is on the fundamental economics of the industry, the very

profit potential of an industry is determine by competition interaction. Where these interactions are

intense, profit tends to be whittled away by the activities of competing.

Porters model is based on the insight that a corporate strategy should meet the opportunities and

threats in the organizations external environment. Especially, competitive strategy should base on

and understanding of industry structures and the way they change. Porter has identified five

competitive forces that shape every industry and every market. These forces determine the intensity

of competition and hence the profitability and attractiveness of an industry. The objective of

corporate strategy should be to modify these competitive forces in a way that improves the position

of the organization. Porters model supports analysis of the driving forces in an industry. Based on

the information derived from the Five Forces Analysis, management can decide how to influence or

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 11/15

11 |

¡

¢

e

£

¤ e¥

¦ § ¤ ¨

£

¦ ¡ ©

£

̈ c § ¡ © c ¡ © ¡ c£

e © ̈ s£

̈ cs ¤

£

e ¨ © ¨ s£

© y

Ri

l

amon

Comp!

tin

Fi ms

" ̈v

¡ § © y

¡ # ¤

¢

c¤ # ¦

e£

̈

£

¤ © s ̈ s ve © y

̈ e © ce¨ $ ¨ ¡

B¡ % ¨

¢

$ s

£

© y

&

e se © v ̈ ces ' ¡ % s ¤

e© ̈

s# ¤ ©

e

¤

¤ # ¤

¢

e e¤

s(

̈c

# ¡ % es

£

e) ¤ # ¦ ¡

y£

¤ ¤

e ©

£

e s¡ #

e se © v ̈ ce ¡

£

¡ § ¤

(

e© © ¡

£

e¡

e ¡

£ £

e¨ ©

c¤ # ¦

e£

̈

£

¤ © # ¡ © % e

£

0

s s ¡ ©

e 1 ¡ © %

e£

§ ¡ ye © s se

¡ § § s

¤ ©

£

s ¤

¡

¢ ¢

© ess ̈ ve se § § ¨

¢

s£

© ¡

£

e¢

̈ es¡ ¡

c£

̈ v ̈

£

̈ es

© ¤ # ¨

£

e s ̈ ve¡

ve ©

£

̈ se # e

£

c¡ # ¦ ¡ ¨

¢

s£

¤ ¦ © ¤ # ¤

£

¨ ¤ ¡ § s

£

2 ve c

¤ s

# e © s

(

̈

£

c

© ¤ # ¤ e ' ¡ %

£

¤ ¡ ¤

£

e ©

3

̈

£

e © e ̈ s ¡

(

¨ e s

¦ © e

¡ ¨

£

e¨

£

e © es£

4 e ce

£

e¨

£

e s ̈

£

y ¤

© ̈v

¡ § © y ̈ s ve © y

̈

¢

&

e ¤

¤

¡ c£

¤ © s

¡ s c

¤

£

© ¨ '

£

e

£

¤ ¨ c © e ¡ se

© ̈v

¡ § © y

£

¤ se

¡ © e

1

5

§ ¡ ©

¢

e ¤ ¤

' ¡ % s

&

e © e ̈ s s¤ # ¡

y ' ¡ % s¡ ¤

¨ ¡ c

¨ ¡ § ¨ s

£

̈

£

£

¨ ¤

̈

¢

£

¨

¢

¤ © s

¡ # e

¦ ̈e3

(

̈c

¡ s

¨

£

e s ̈

̈ e

c¤ # ¦

e£

̈

£

¨ ¤ ?

2. High marke£

growth rate

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 12/15

12 | P a g e

India is seen as one of the biggest market place and growth rate in Indian banking industry is also

very high. This has ignited the competition.

3. Homogeneous product and services

The services banks offer is more of homogeneous which makes the company to offer the same

service at a lower rate and eat their competitor markets share.

4. Low switching cost

Costumers switching cost is very low, they can easily switch from one bank to another bank and very

little loyalty exist .

5. Undifferentiated services

Almost every bank provides similar services. Every bank tries to copy each other services and

technology which increase level of competition.

6. High fixed cost

7. High exit barriers

High exit barriers humiliate banks to earn profit and retain customers by providing world class

services.

8. Low government regulations

There are low regulations exist to start a new business due lpg policy adopted by India.

BARGAINING POWER OF SUPPLIERS

Banking industry is governed by Reserve Bank of India. Reserve Bank of India is the authority to takemonetary action which leads to direct impact on circulation of money in the Economy. The rules and

regulation lay down by RBI. Suppliers of banks are depositors .these are those people who have

excess money and prefer regular income and safety. In banking industry suppliers have low

bargaining power.

1.Nature of suppliers

Suppliers of banks are those people who prefer low risk and those who need regular income and

safety as well. Banks best place for them to deposits theirs surplus money.

2. Few alternatives

3. Rbi rules and regulations

Banks are subject to rbi rules and regulations .bank has to behave in a way that rbi wants. So rbi

takes all decisions related to interest rates . this reduces bargaining power of suppliers .

4. Suppliers not concentrated

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 13/15

13 | P a g e

Banking industry suppliers sure not concentrated. There are numerous with negligible portion of

offer .so this reduce their bargaining power .

BARGAINING POWER OF CONSUMERS

In today world, Customer is the King. Banks offers different services According to clients

need and requirement. They offer loans at Prime Lending Rate (PLR) to their trust worthyclients and higher rate to others clients.

Customers of banks are those who take loans and uses services of banks. Customers have

high bargaining power. These are:

1.Large no of alternatives

Customers have large no of alternatives, there are so many banks, which fight for same pie. There

are many non financial institutions like icici, hdfc, and ifci, etc. which has also jump into these

business .there are foreign banks , privet banks, co-operative banks and development banks

together with specialized financial companies that provides finance to customers .these all increase

preference for customers.

2. Low switching cost

Cost of switching from one bank to another is low. Banks are also providing zero balance account

and other types of facilities. They are free to select any banks service. Switching cost are becoming

lower with internet banking gaining momentum and a result customers loyalties are harder to

retain.

3. Undiffenciated service

Bank provide merely similar service there are no much diffracted in service provides by differentbanks so, bargaining power of customers increase. They cannot be charged for differentiation.

4. Full information about the market

Customers have full information about the market due to globalization and digitalization

Consumers have become advance and sophisticated .they are aware with each market

condition so banks have to be more competetive and customer friendly to serve them.

For good creditworthy borrowers bargaining power is high due to theavailability of large number of banks

POTENTIAL ENTRY OF NEW COMPETITORS

Reserve Bank of India has laid out a stagnant rules and regulation for new entrant in Banking

Industry. We expect merger and acquisition in the banking industry in near future. Hence,

the industry is less porn of new com petitor.

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 14/15

14 | P a g e

Barriers to an entry in banking industry no longer exist. So lots of privet and foreign banks

are entering in the market. Competitors can come from an industry to disinter mediate

bank product differentiation is very difficult for banks and exit is difficult. So every bank

strives to survive in highly competitive market so we see intense competitive can mergers

and acquisitions. Government policies are supportive to start new bank. There is less

statutory requirement needed to start a new venture6 Every bank to tries to achieve

economies of scale through use of technology and selecting and training manpower .

There are public sector banks, private sector and foreign banks along with

non banking finance companies competing in similar business se gments.

POTENTIAL DEVELOPMENT OF SUBSTITUTE PRODUCTS

Every day there is one or the other new product in financial sector. Banks are not limited to

tradition banking which just offers deposit and lending. In addition, today banks offers loans

for all products, derivatives, ForEx, Insurance, Mutual Fund, Demit account to name a few.

The wide range of choices and needs give a sufficient room for new product developmentand product enhancement.

Substitute products or services are those, which are different but satisfy the same set of

customers. In private banking industry following are the substitutes:

NBFC: Non-banking financial Institutions play an important role in giving

financial assistance. Mobilization of financial resources outside the tradition al banking

system has witnessed a tremendous growth in recent years in the India. NBFC is a close

substitute of banking in respect of raising funds.

Borrower can easily raise funds from NBFC because it requires less formal

procedure for getting funds compare to private banks.

y Post Office Products: Post office is also providing some service like fixed

deposit facility, saving account, recurring account etc. The interest rate of saving account is

higher than private banks. It is fully secured by the government so people who do not want

to take risk for them post office saving is good substitute.

y Government Bond: Govt. Bond also attracts savings from the general

public. It is less risky and more secured as compare to savings in private

banks.y Mutual Funds: Mutual funds are also now proving as good substitutes for

banks. They assure for providing high return with less time in comparison of banks. The

administrative expenses are also very low as compared to banks. Investment in Mutual

funds is more flexible than investment in banks.

y Stock Market: People who are ready to bear risk and wants a high return on

8/8/2019 Marketing Assingment Latest

http://slidepdf.com/reader/full/marketing-assingment-latest 15/15

15 | P a g e

their investment, stock market is a good substitute for them. Day by day investors are

moving towards stock market as interest rate in banks are decreasing. So now stock market

has proved as a big competitor for baking sector.

y Debentures: Debentures is also proved as a good substitute of banks fixed

deposit as return on debenture is fixed and high. There are different types of

debentures, which attract various classes of investors.

y Other Investment Alternatives: Now common peoples attraction is shifting

from banks to other various alternatives such as gold, precious metals, land, small savings

etc. As we can see the growing trend in these alternatives in comparison of decreasing

interest rates in banks.