market outlook december 2016

TRANSCRIPT

Market Outlook

December

2016

1

EQUITY

MARKETS

2

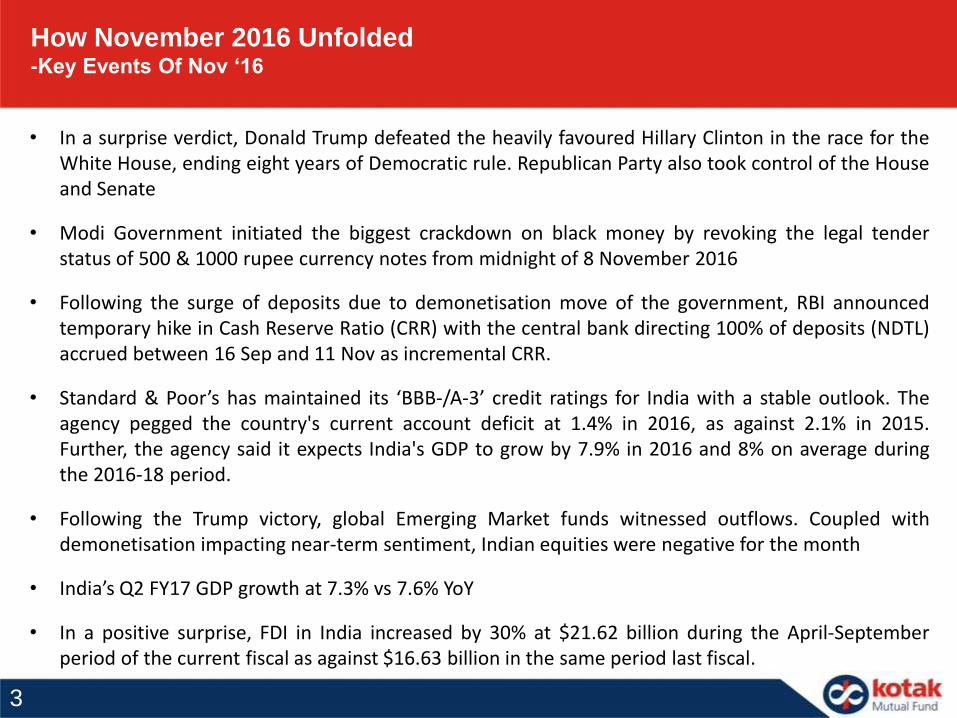

How November 2016 Unfolded -Key Events Of Nov ‘16

• In a surprise verdict, Donald Trump defeated the heavily favoured Hillary Clinton in the race for theWhite House, ending eight years of Democratic rule. Republican Party also took control of the Houseand Senate

• Modi Government initiated the biggest crackdown on black money by revoking the legal tenderstatus of 500 & 1000 rupee currency notes from midnight of 8 November 2016

• Following the surge of deposits due to demonetisation move of the government, RBI announcedtemporary hike in Cash Reserve Ratio (CRR) with the central bank directing 100% of deposits (NDTL)accrued between 16 Sep and 11 Nov as incremental CRR.

• Standard & Poor’s has maintained its ‘BBB-/A-3’ credit ratings for India with a stable outlook. Theagency pegged the country's current account deficit at 1.4% in 2016, as against 2.1% in 2015.Further, the agency said it expects India's GDP to grow by 7.9% in 2016 and 8% on average duringthe 2016-18 period.

• Following the Trump victory, global Emerging Market funds witnessed outflows. Coupled withdemonetisation impacting near-term sentiment, Indian equities were negative for the month

• India’s Q2 FY17 GDP growth at 7.3% vs 7.6% YoY

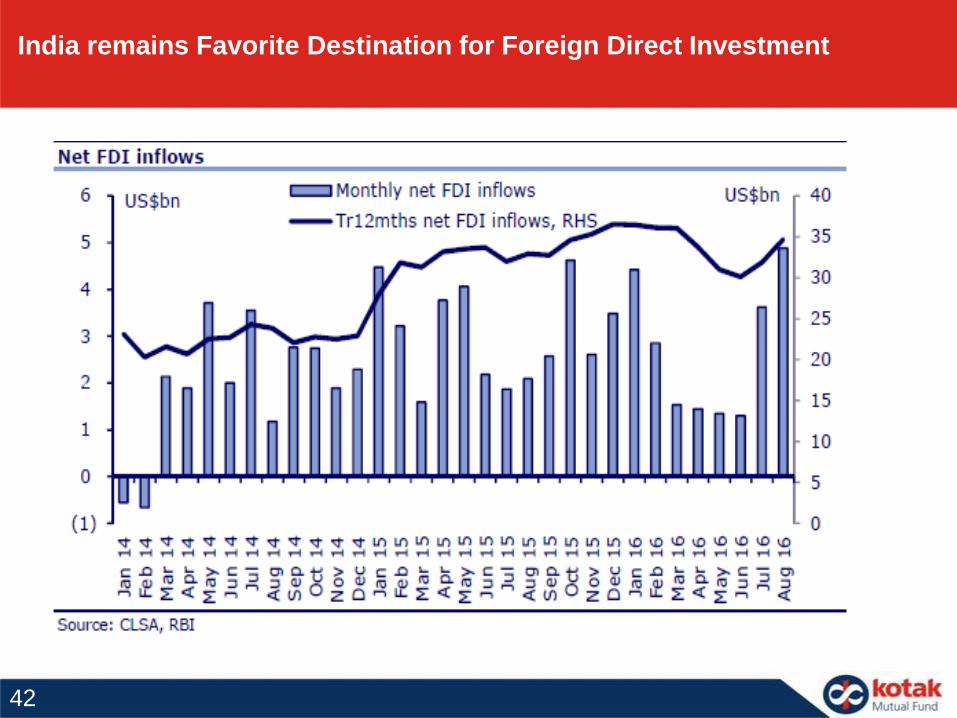

• In a positive surprise, FDI in India increased by 30% at $21.62 billion during the April-Septemberperiod of the current fiscal as against $16.63 billion in the same period last fiscal.

3

Why Was Demonetization Done?

Total Bank notes in circulation rose

by 40% in last 5 years

Shadow economy for India >23% of

GDP which corrodes

economy and stokes Inflation

Circulation of Rs. 500 rose by 76% and Rs. 1000 by

109%

Source: World Bank 2007 estimate, Ministry of Finance Press release 4

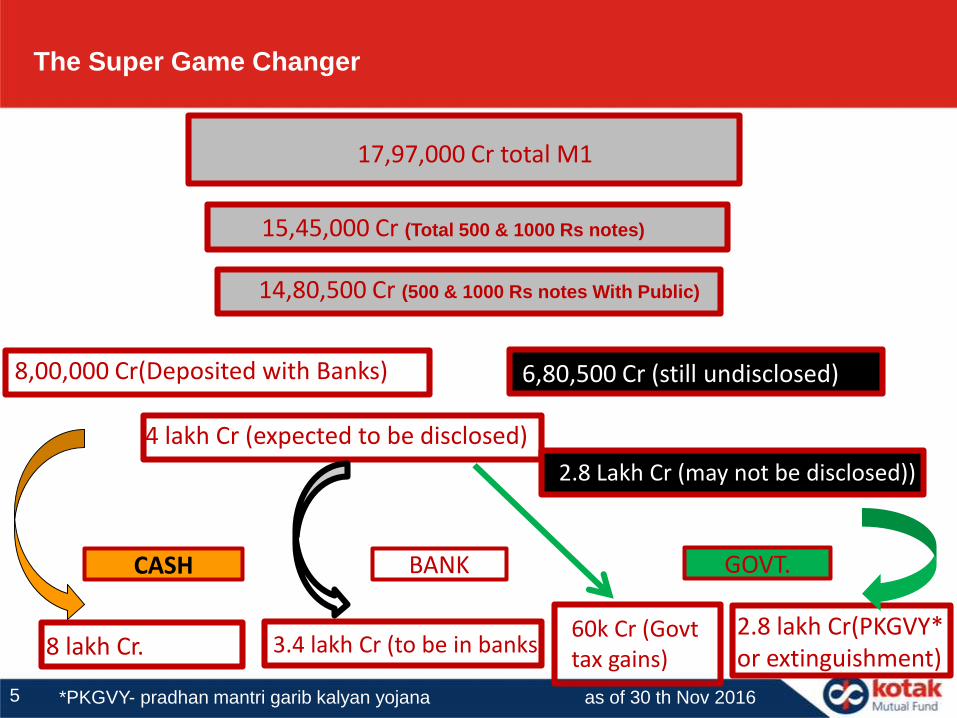

The Super Game Changer

17,97,000 Cr total M1

15,45,000 Cr (Total 500 & 1000 Rs notes)

14,80,500 Cr (500 & 1000 Rs notes With Public)

8,00,000 Cr(Deposited with Banks) 6,80,500 Cr (still undisclosed)

4 lakh Cr (expected to be disclosed)

2.8 Lakh Cr (may not be disclosed))

CASH BANK GOVT.

8 lakh Cr. 60k Cr (Govttax gains)

3.4 lakh Cr (to be in banks 2.8 lakh Cr(PKGVY* or extinguishment)

5 *PKGVY- pradhan mantri garib kalyan yojana as of 30 th Nov 2016

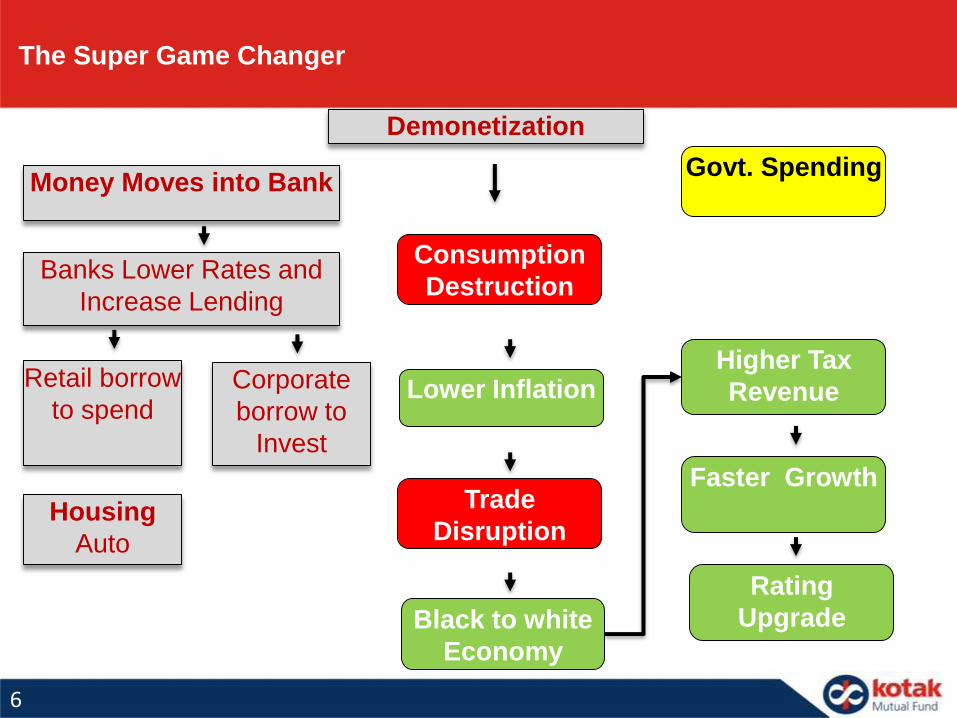

Demonetization

Money Moves into Bank

Banks Lower Rates and

Increase Lending

Retail borrow

to spend

Housing

Auto

Corporate

borrow to

Invest

Consumption

Destruction

Lower Inflation

Black to white

Economy

Trade

Disruption

Higher Tax

Revenue

Faster Growth

Rating

Upgrade

Govt. Spending

The Super Game Changer

6

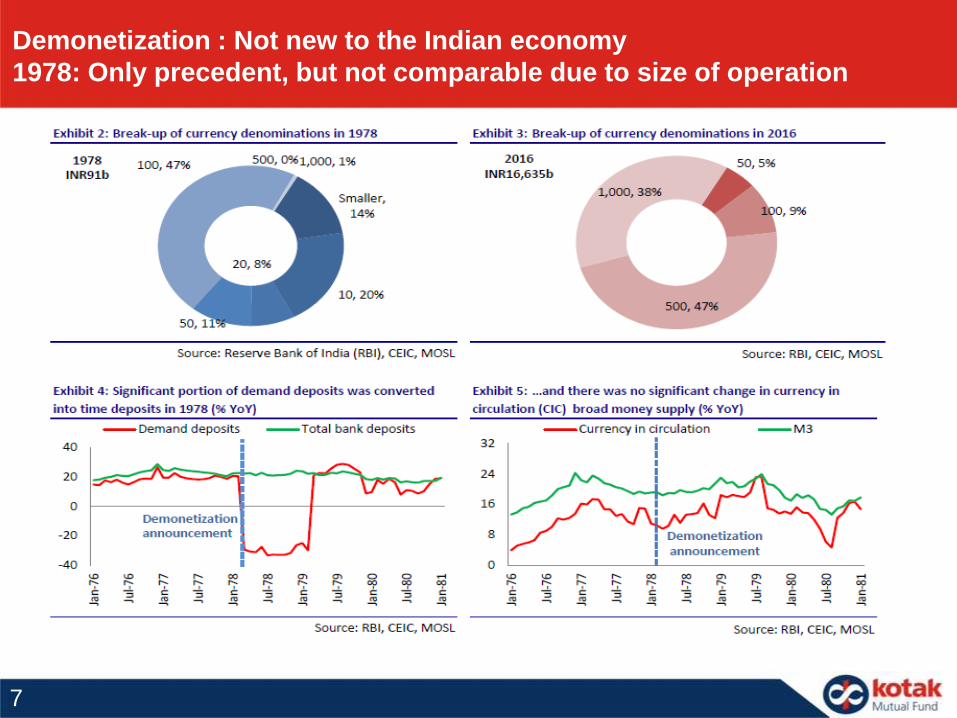

Demonetization : Not new to the Indian economy

1978: Only precedent, but not comparable due to size of operation

7

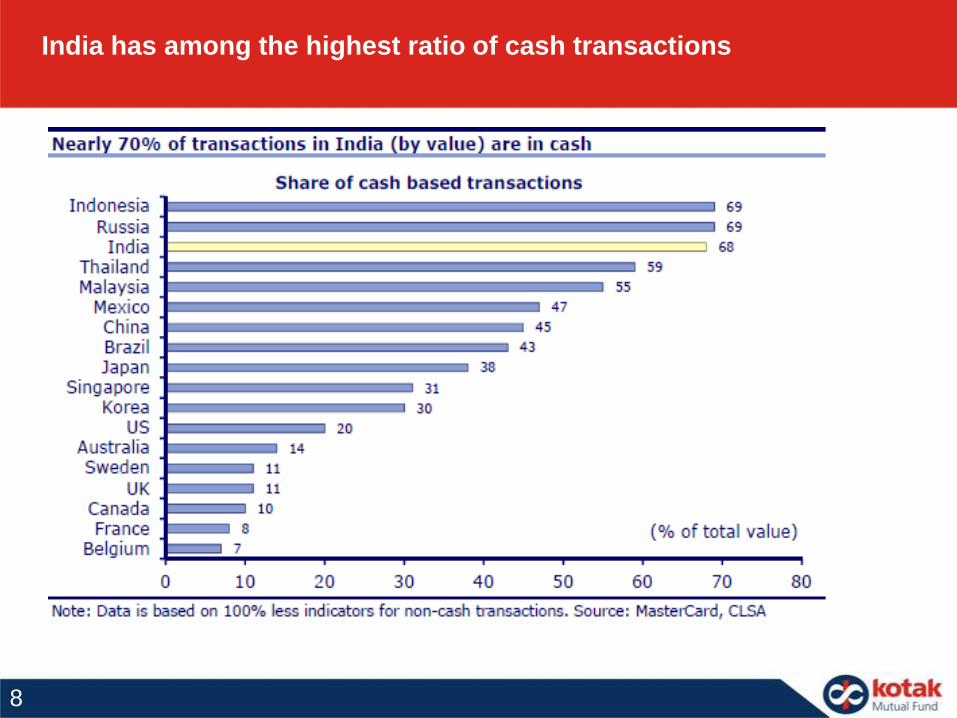

India has among the highest ratio of cash transactions

8

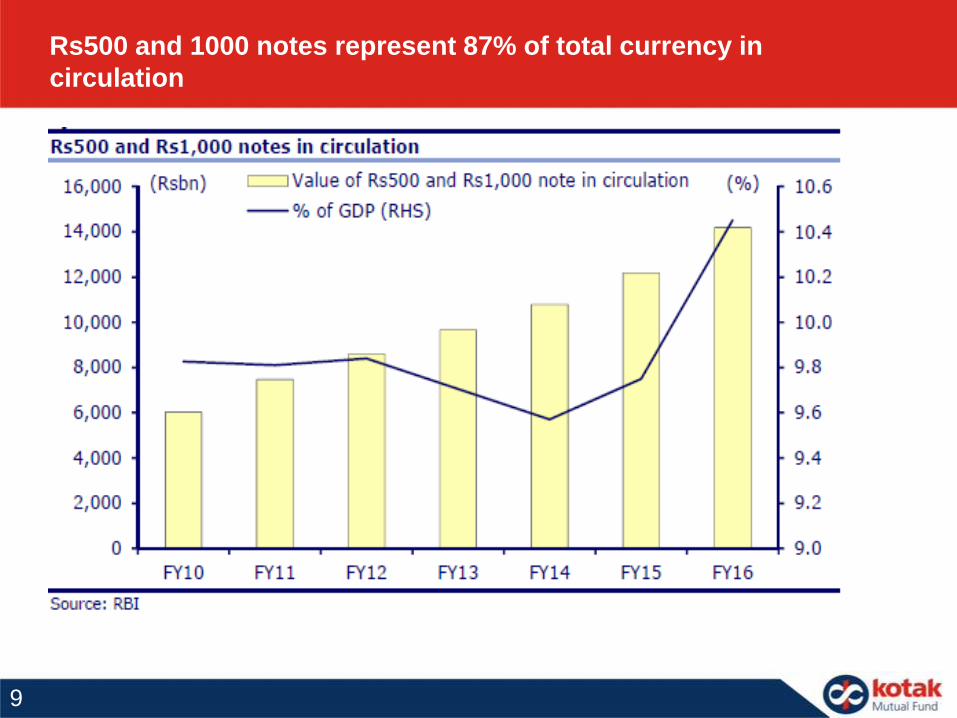

Rs500 and 1000 notes represent 87% of total currency in

circulation

9

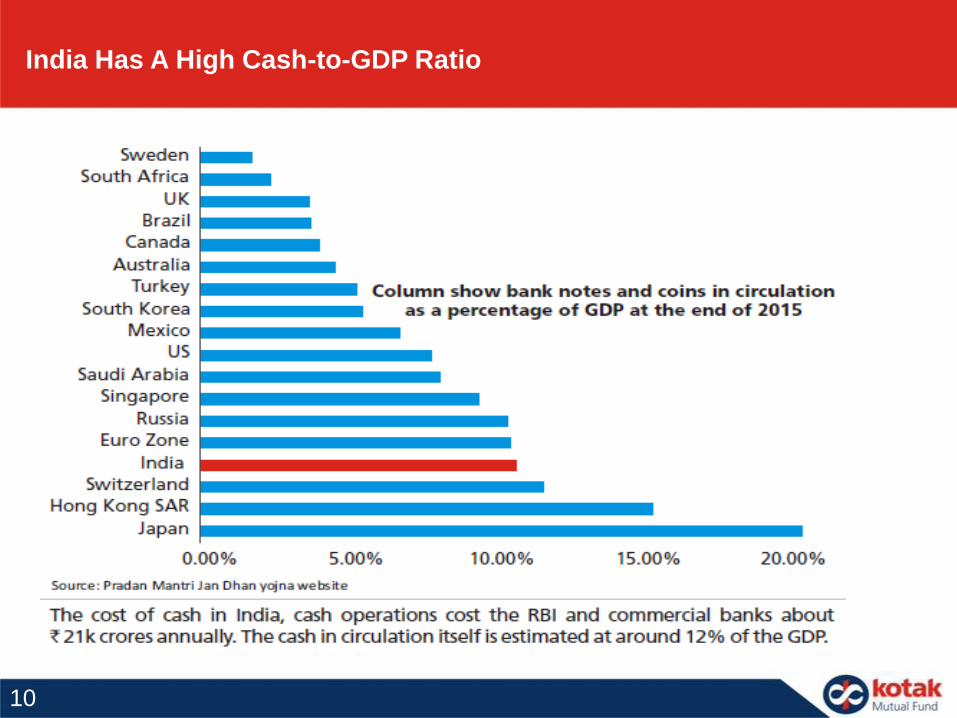

India Has A High Cash-to-GDP Ratio

10

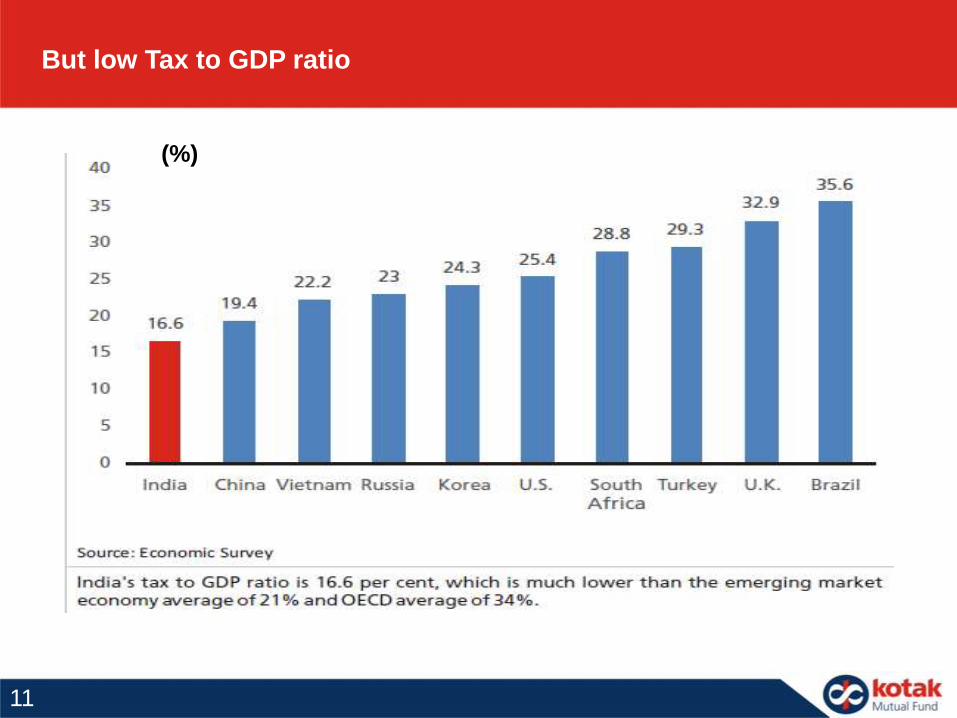

But low Tax to GDP ratio

(%)

11

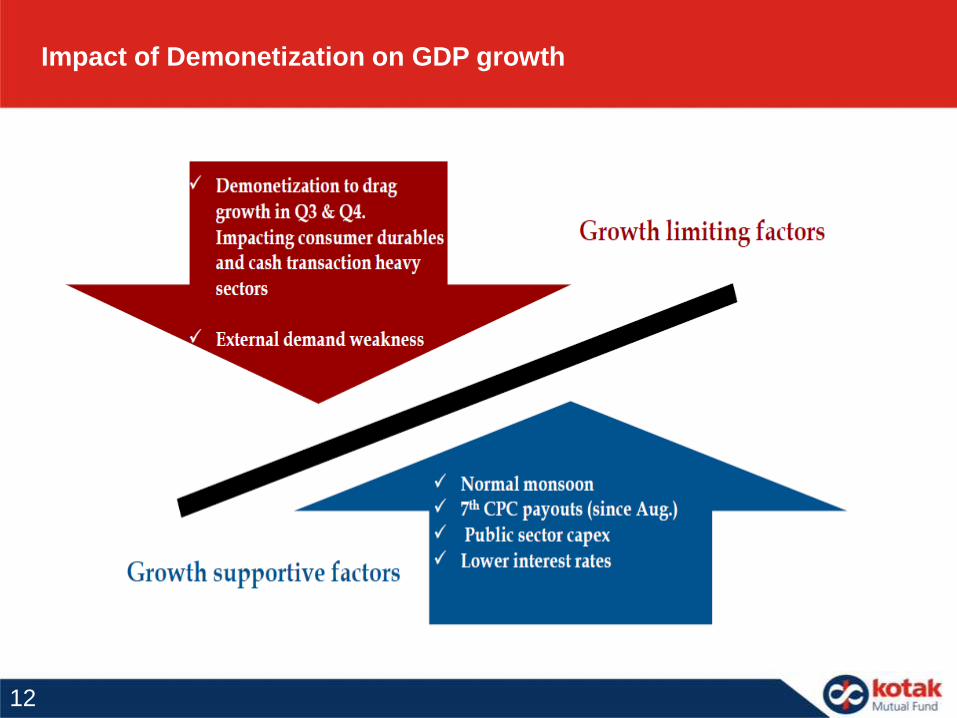

Impact of Demonetization on GDP growth

12

Immediate Economic Impact

• In the near term the economy could go through a period of transition on account of these measures together with the implementation of GST

• Property prices and gold may come down as most unaccounted wealth is invested in these

• In the short term there could be a negative impact on consumption demand; This could have a bearing on GDP growth in H2FY17

• Banks with higher branch presence would benefit with higher CASA / deposit growth

• With changing business models of SMEs and property prices going down asset quality pressures may mount in certain segments

• Upcoming state level elections may also get impacted as cash will no longer be king

In summary, since money supply would decline temporarily, we could see some deflationary tendencies lowering real demand

1313

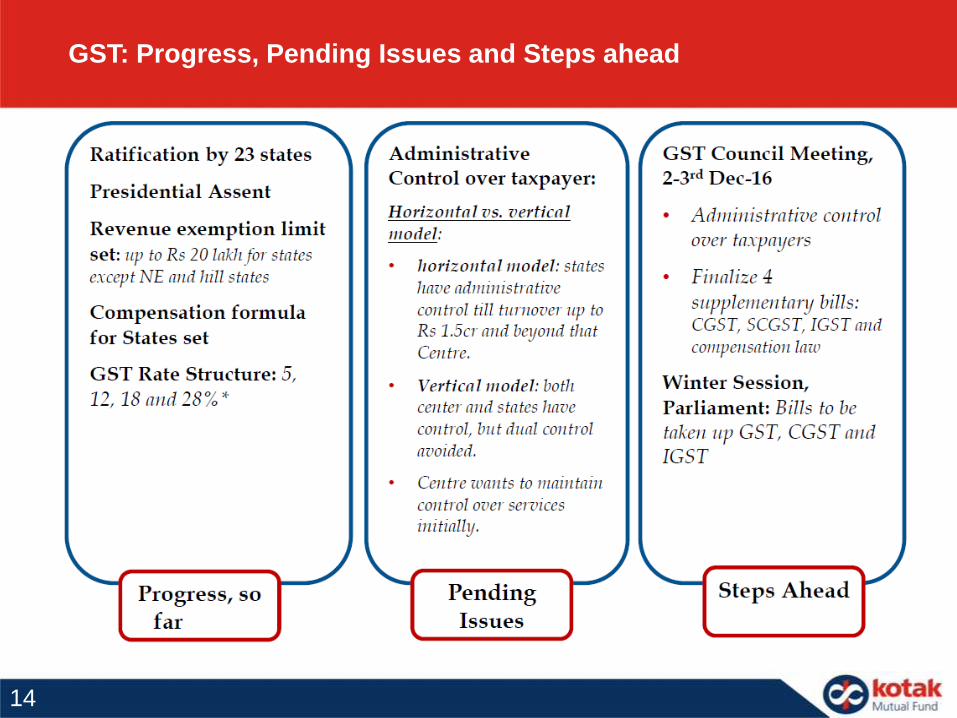

GST: Progress, Pending Issues and Steps ahead

14

• Winter Session of parliament commenced on 16th Nov and will continue until 16th December with a total of 22 sittings

• Additionally, it has been announced that the Government will present the Union Budget on 1st Feb-16

Winter Session Of Parliament

15

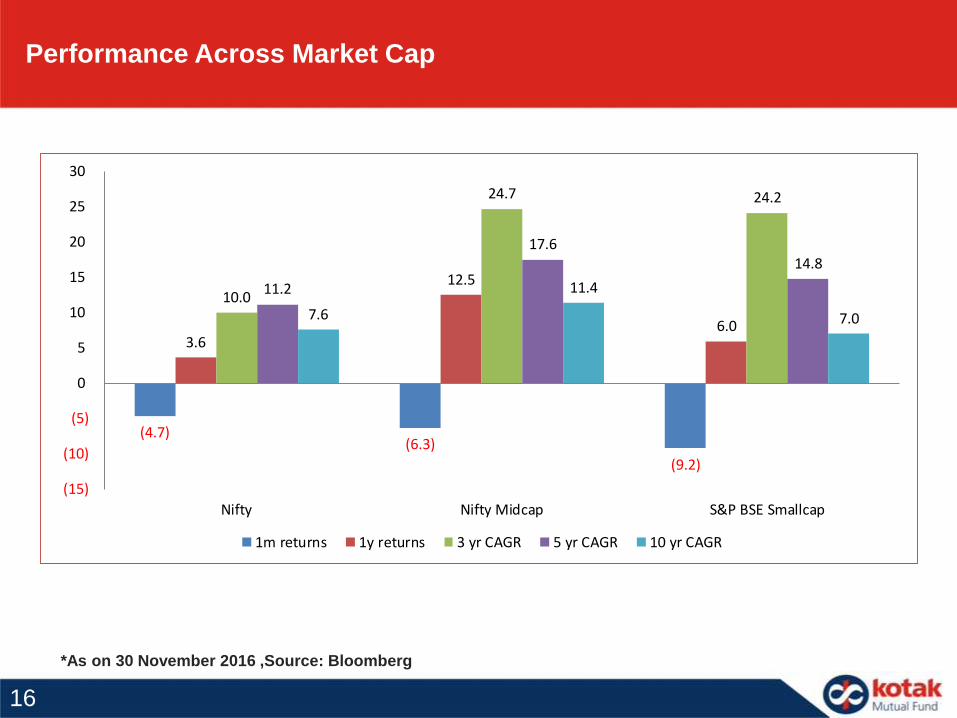

*As on 30 November 2016 ,Source: Bloomberg

Performance Across Market Cap

(4.7)(6.3)

(9.2)

3.6

12.5

6.0

10.0

24.7 24.2

11.2

17.6 14.8

7.6

11.4

7.0

(15)

(10)

(5)

0

5

10

15

20

25

30

Nifty Nifty Midcap S&P BSE Smallcap

1m returns 1y returns 3 yr CAGR 5 yr CAGR 10 yr CAGR

16

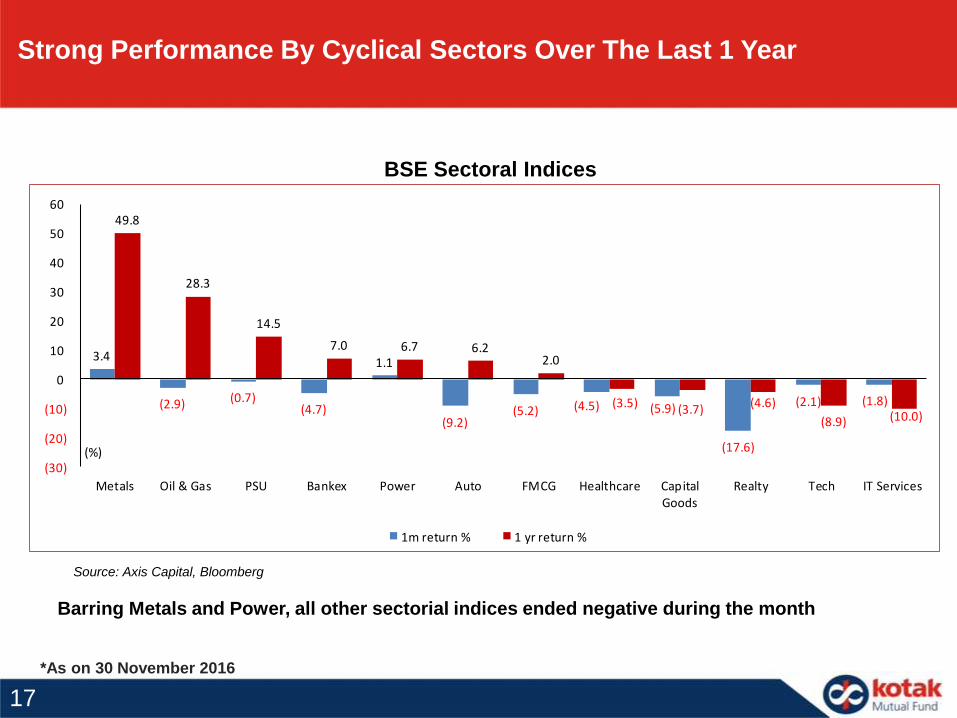

*As on 30 November 2016

Barring Metals and Power, all other sectorial indices ended negative during the month

Source: Axis Capital, Bloomberg

BSE Sectoral Indices

3.4

(2.9) (0.7)(4.7)

1.1

(9.2)(5.2) (4.5) (5.9)

(17.6)

(2.1) (1.8)

49.8

28.3

14.5

7.0 6.7 6.2 2.0

(3.5) (3.7) (4.6)

(8.9) (10.0)

(30)

(20)

(10)

0

10

20

30

40

50

60

Metals Oil & Gas PSU Bankex Power Auto FMCG Healthcare CapitalGoods

Realty Tech IT Services

(%)

1m return % 1 yr return %

Strong Performance By Cyclical Sectors Over The Last 1 Year

17

Volatility in Markets in the Short Term

Volatility may affect Equities, Debt, Real Estate etc. in the near term as

momentum swings from end to end

1918

0

10

20

30

40

50

60

70

Auto BFSI Engg FMCG IT Metals Oil Pharma Power Telecom Sensex

0

10

20

30

40

50

60

Auto BFSI Engg FMCG IT Services Metals Oil & Gas Pharma Power Telecom Sensex

-1 SD +1 SD Current Max Min

Top Quartile

Current

Lower Quartile

Min

Max

IT and Power are at lower end of valuations, other sectors have seen some moderation in

valuation

Source: Axis Capital, Bloomberg Note: * Since April-2005

Sensex sectoral long-term valuation snapshot: Forward PE*

Stock Picking Will Be Critical As Sectors Are At Higher End Of Fair Value

*As on 30 November 2016

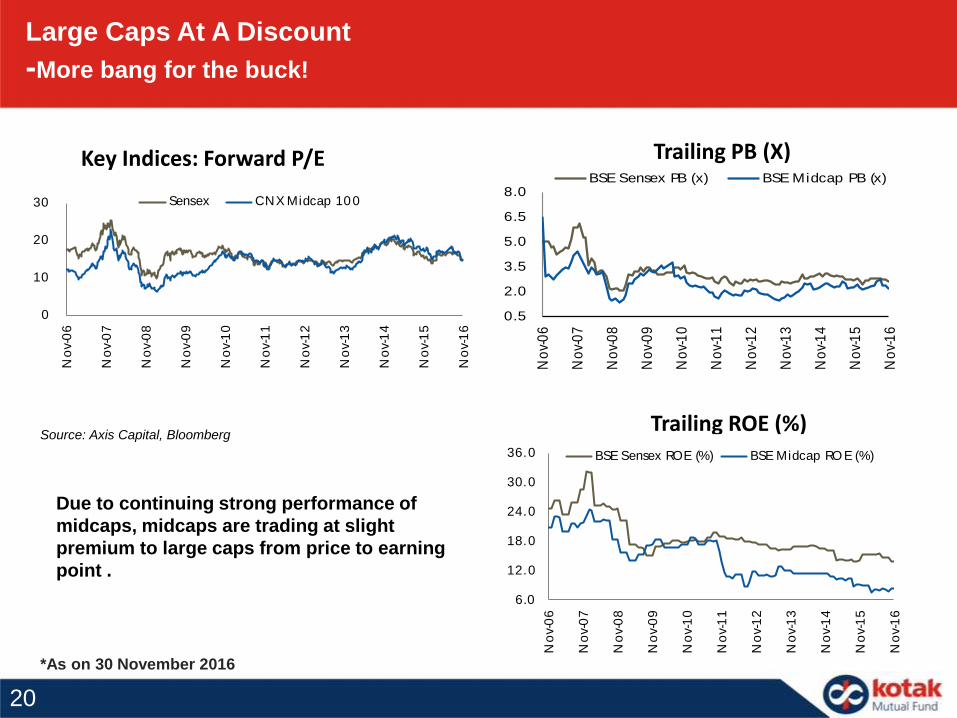

19

*As on 30 November 2016

Due to continuing strong performance of

midcaps, midcaps are trading at slight

premium to large caps from price to earning

point .

Source: Axis Capital, Bloomberg

Key Indices: Forward P/E

Large Caps At A Discount

-More bang for the buck!

Trailing ROE (%)

0.5

2.0

3.5

5.0

6.5

8.0

No

v-0

6

No

v-0

7

No

v-0

8

No

v-0

9

No

v-1

0

No

v-1

1

No

v-1

2

No

v-1

3

No

v-1

4

No

v-1

5

No

v-1

6

BSE Sensex PB (x) BSE Midcap PB (x)

6.0

12.0

18.0

24.0

30.0

36.0

No

v-0

6

No

v-0

7

No

v-0

8

No

v-0

9

No

v-1

0

No

v-1

1

No

v-1

2

No

v-1

3

No

v-1

4

No

v-1

5

No

v-1

6

BSE Sensex ROE (%) BSE Midcap RO E (%)

Trailing PB (X)

0

10

20

30

No

v-0

6

No

v-0

7

No

v-0

8

No

v-0

9

No

v-1

0

No

v-1

1

No

v-1

2

No

v-1

3

No

v-1

4

No

v-1

5

No

v-1

6

Sensex CNX Midcap 100

20

Indian Markets Middle Of Pack In Terms Of 1yr Return

Source: Bloomberg. Performance data

(13.3)

(12.8)

(8.2)

(7.3)

(6.7)

(3.2)

(0.4)

0.5

1.7

3.6

3.6

6.5

7.9

11.1

15.8

17.8

35.2

(0.6)

0.2

0.9

5.1

(0.4)

(3.2)

(1.2)

2.9

3.2

(0.6)

(4.7)

(2.6)

5.4

(0.5)

(5.0)

4.9

(6.1)

(20) (10) 0 10 20 30 40

EURO (Euro Stoxx 50)

Swiss (SMI)

France (CACS 40)

Japan (Nikkei 225)

Germany (DAX)

Malaysia (KLCI - FTSE)

Korea (Kospi)

China (HSCEI)

Singapore (Straits)

HK (HSI)

India (Nifty)

UK (FTSE 100)

US (Dow Jones)

Taiwan (TSWE)

Indonesia (JCI)

Russia (MICEX)

Brazil (IBOV)

1M 1Yr

21

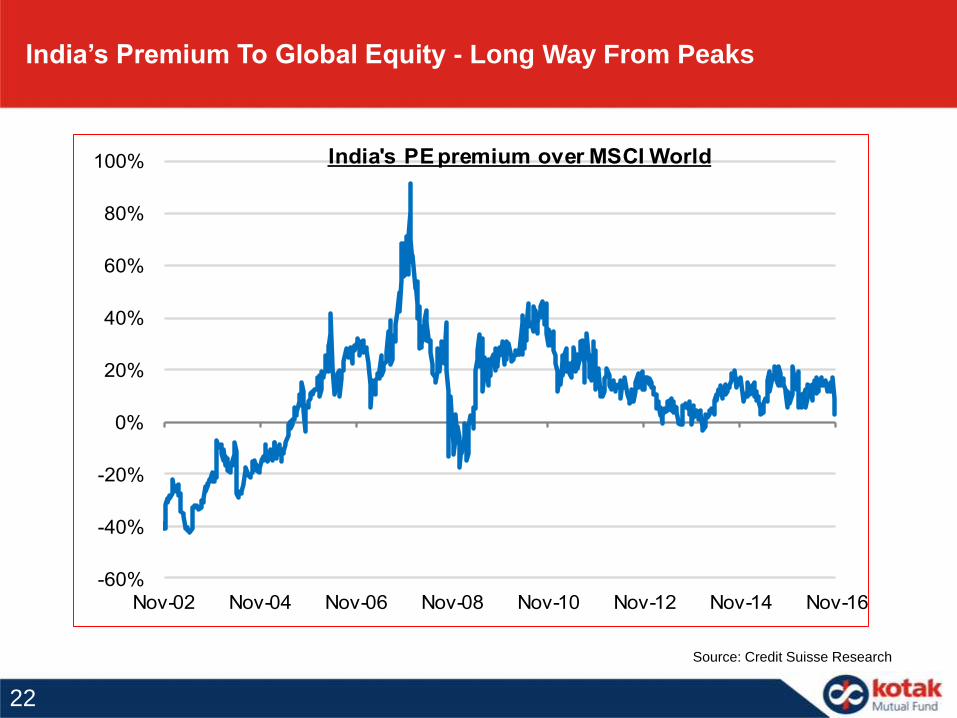

India’s Premium To Global Equity - Long Way From Peaks

Source: Credit Suisse Research

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Nov-02 Nov-04 Nov-06 Nov-08 Nov-10 Nov-12 Nov-14 Nov-16

India's PE premium over MSCI World

22

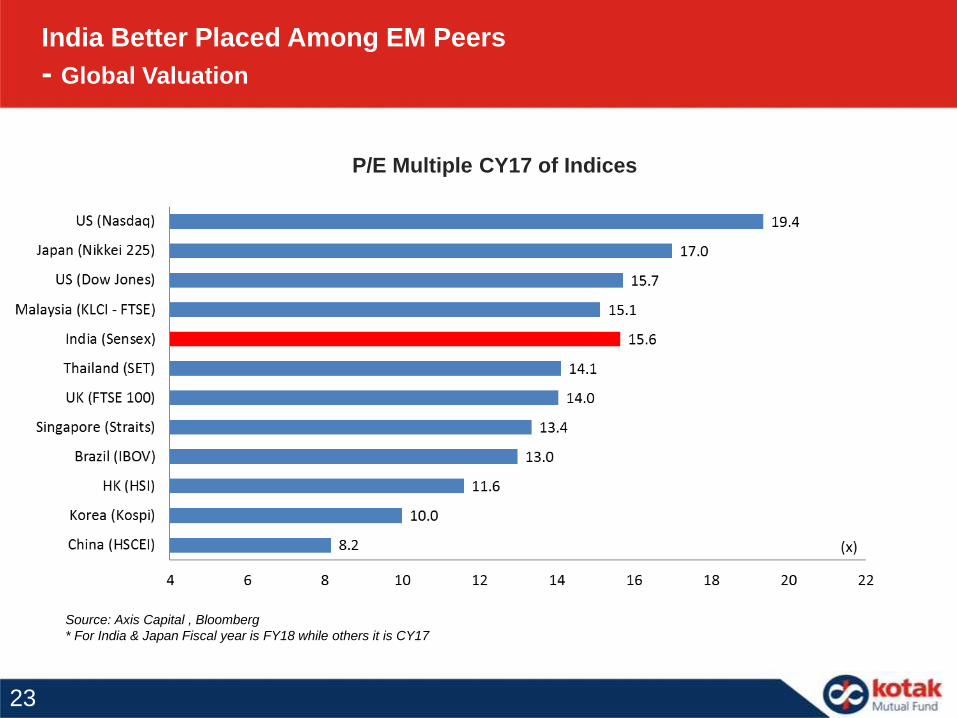

P/E Multiple CY17 of Indices

Source: Axis Capital , Bloomberg

* For India & Japan Fiscal year is FY18 while others it is CY17

India Better Placed Among EM Peers

- Global Valuation

23

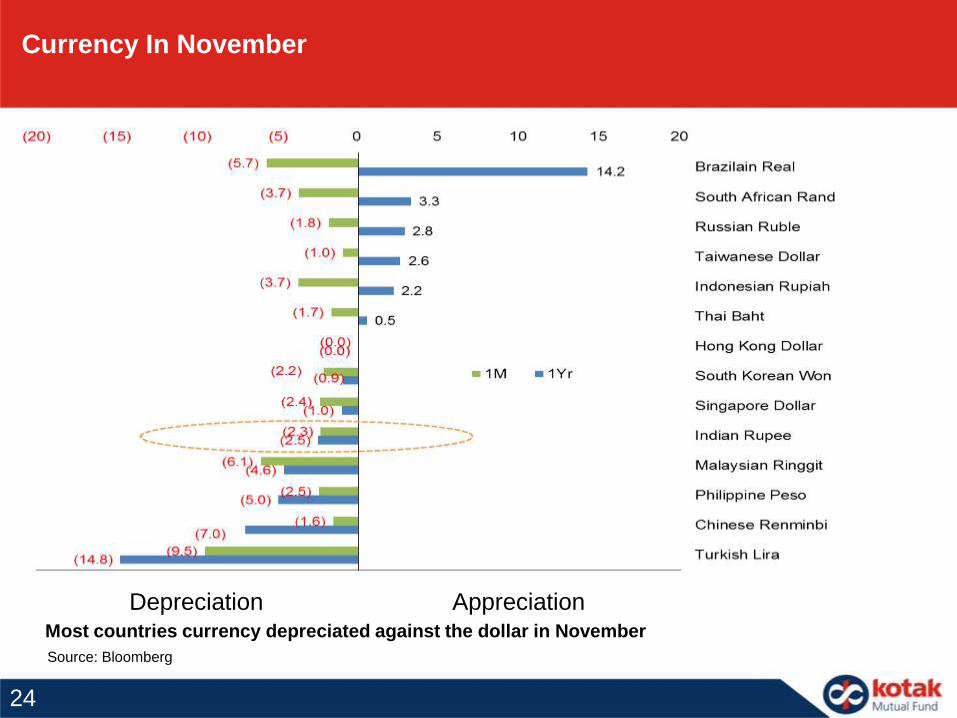

Currency In November

Most countries currency depreciated against the dollar in November

Source: Bloomberg

Depreciation Appreciation

24

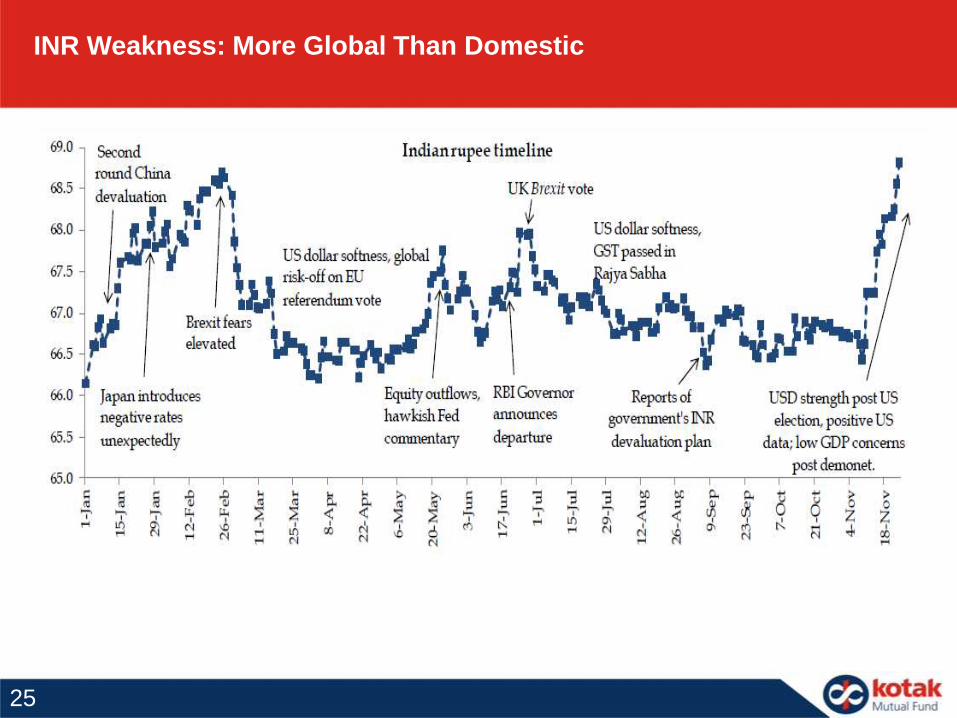

INR Weakness: More Global Than Domestic

25

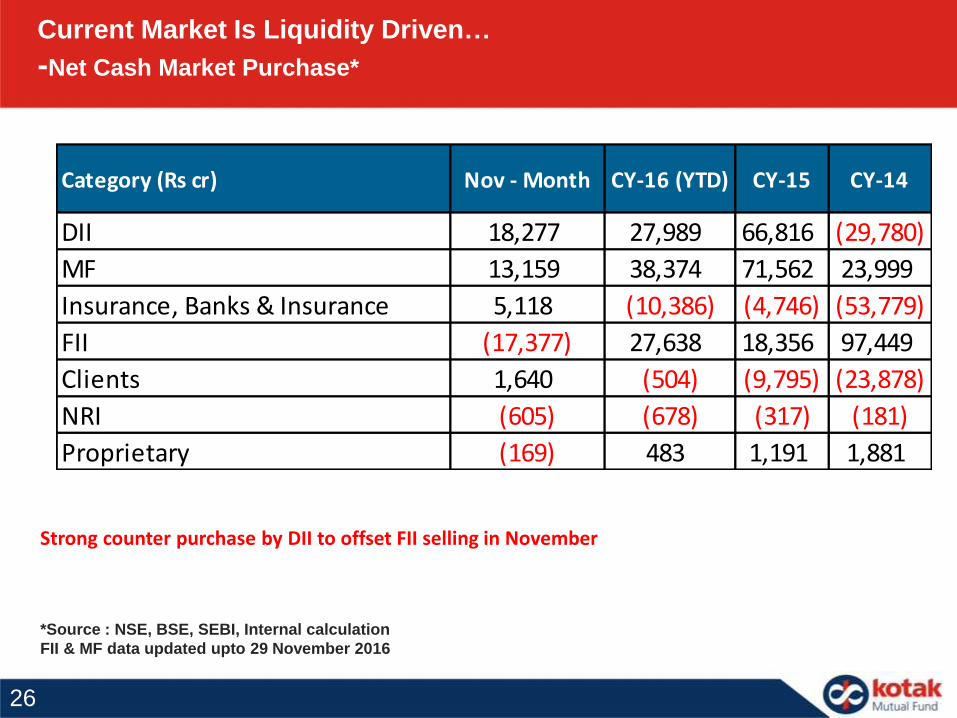

*Source : NSE, BSE, SEBI, Internal calculation

FII & MF data updated upto 29 November 2016

Strong counter purchase by DII to offset FII selling in November

Current Market Is Liquidity Driven…

-Net Cash Market Purchase*

Category (Rs cr) Nov - Month CY-16 (YTD) CY-15 CY-14

DII 18,277 27,989 66,816 (29,780)

MF 13,159 38,374 71,562 23,999

Insurance, Banks & Insurance 5,118 (10,386) (4,746) (53,779)

FII (17,377) 27,638 18,356 97,449

Clients 1,640 (504) (9,795) (23,878)

NRI (605) (678) (317) (181)

Proprietary (169) 483 1,191 1,881

26

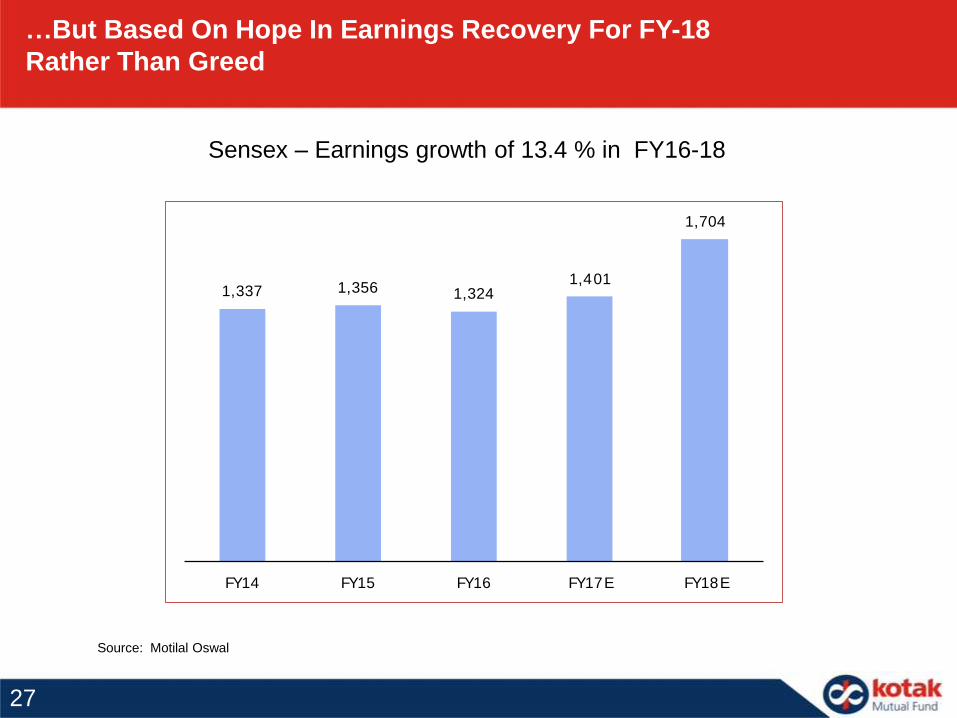

…But Based On Hope In Earnings Recovery For FY-18

Rather Than Greed

Sensex – Earnings growth of 13.4 % in FY16-18

Source: Motilal Oswal

1,337 1,356 1,3241,401

1,704

FY14 FY15 FY16 FY17E FY18E

27

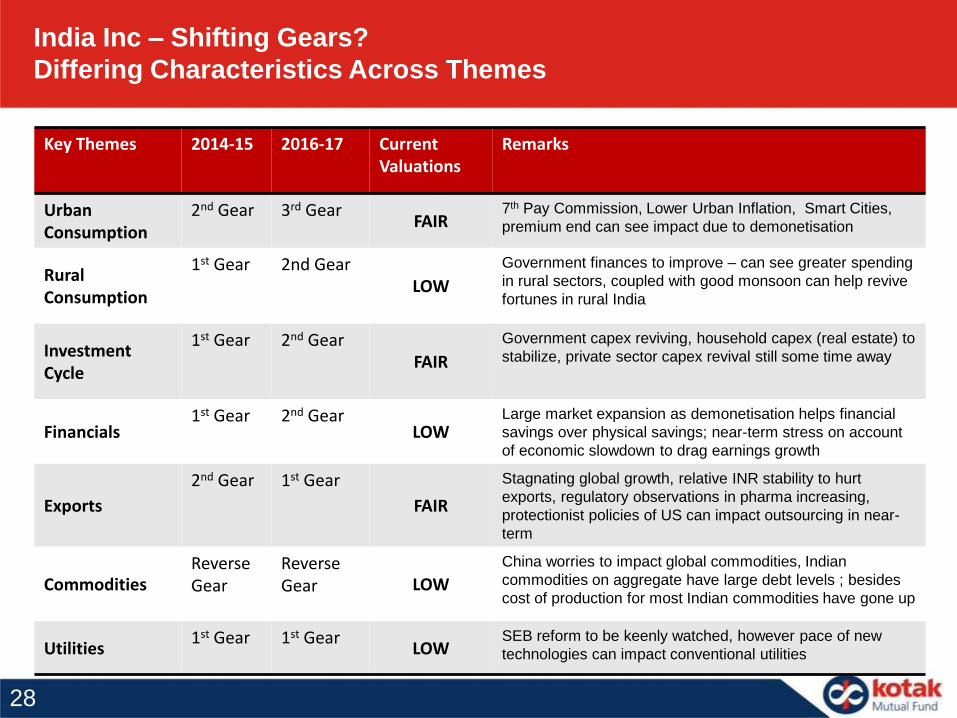

India Inc – Shifting Gears?

Differing Characteristics Across Themes

Key Themes 2014-15 2016-17 Current Valuations

Remarks

Urban Consumption

2nd Gear 3rd GearFAIR

7th Pay Commission, Lower Urban Inflation, Smart Cities,

premium end can see impact due to demonetisation

Rural Consumption

1st Gear 2nd GearLOW

Government finances to improve – can see greater spending

in rural sectors, coupled with good monsoon can help revive

fortunes in rural India

Investment Cycle

1st Gear 2nd GearFAIR

Government capex reviving, household capex (real estate) to

stabilize, private sector capex revival still some time away

Financials1st Gear 2nd Gear

LOWLarge market expansion as demonetisation helps financial

savings over physical savings; near-term stress on account

of economic slowdown to drag earnings growth

Exports

2nd Gear 1st Gear

FAIR

Stagnating global growth, relative INR stability to hurt

exports, regulatory observations in pharma increasing,

protectionist policies of US can impact outsourcing in near-

term

CommoditiesReverseGear

Reverse Gear LOW

China worries to impact global commodities, Indian

commodities on aggregate have large debt levels ; besides

cost of production for most Indian commodities have gone up

Utilities1st Gear 1st Gear

LOWSEB reform to be keenly watched, however pace of new

technologies can impact conventional utilities

28

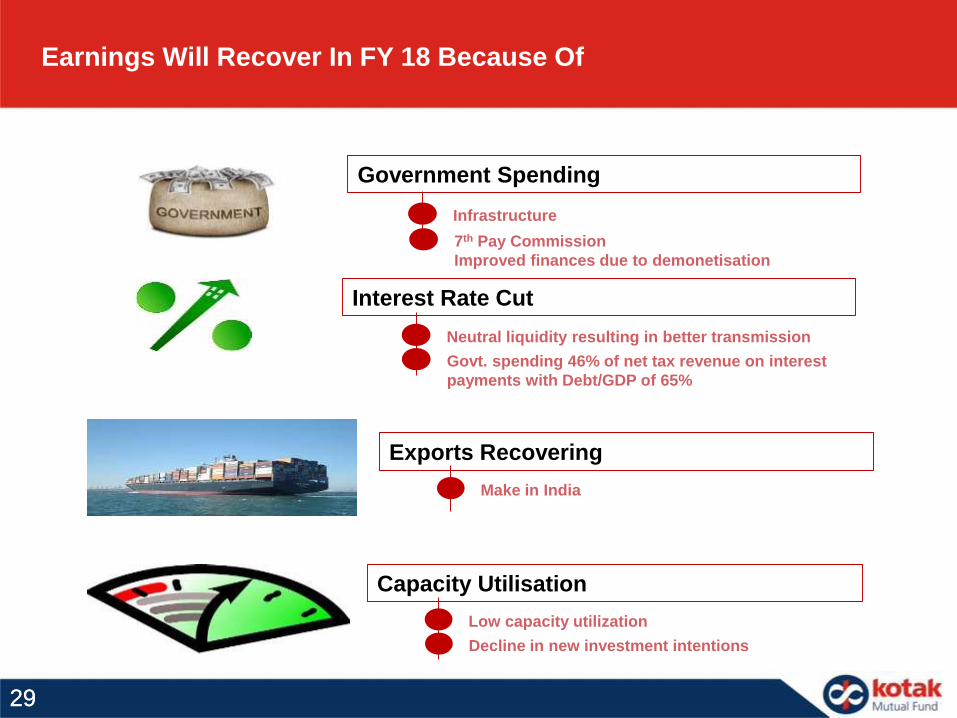

Earnings Will Recover In FY 18 Because Of

Interest Rate Cut

Neutral liquidity resulting in better transmission

Govt. spending 46% of net tax revenue on interest

payments with Debt/GDP of 65%

Capacity Utilisation

Low capacity utilization

Decline in new investment intentions

Exports Recovering

Make in India

Government Spending

Infrastructure

7th Pay Commission

Improved finances due to demonetisation

2929

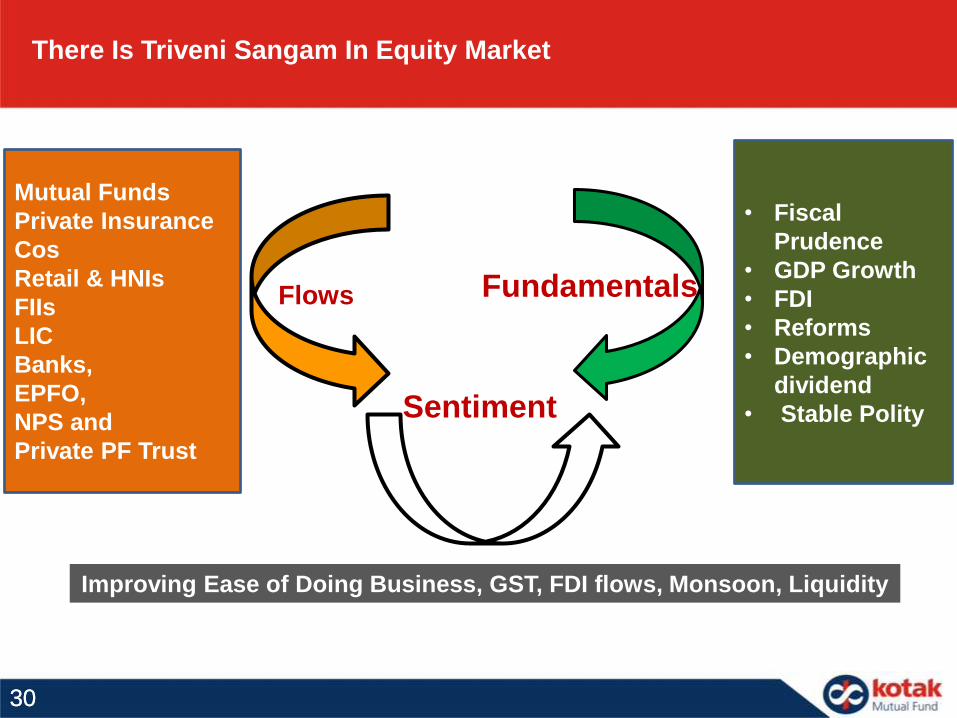

Flows

Sentiment

Fundamentals

There Is Triveni Sangam In Equity Market

Improving Ease of Doing Business, GST, FDI flows, Monsoon, Liquidity

Mutual Funds

Private Insurance

Cos

Retail & HNIs

FIIs

LIC

Banks,

EPFO,

NPS and

Private PF Trust

• Fiscal

Prudence

• GDP Growth

• FDI

• Reforms

• Demographic

dividend

• Stable Polity

3030

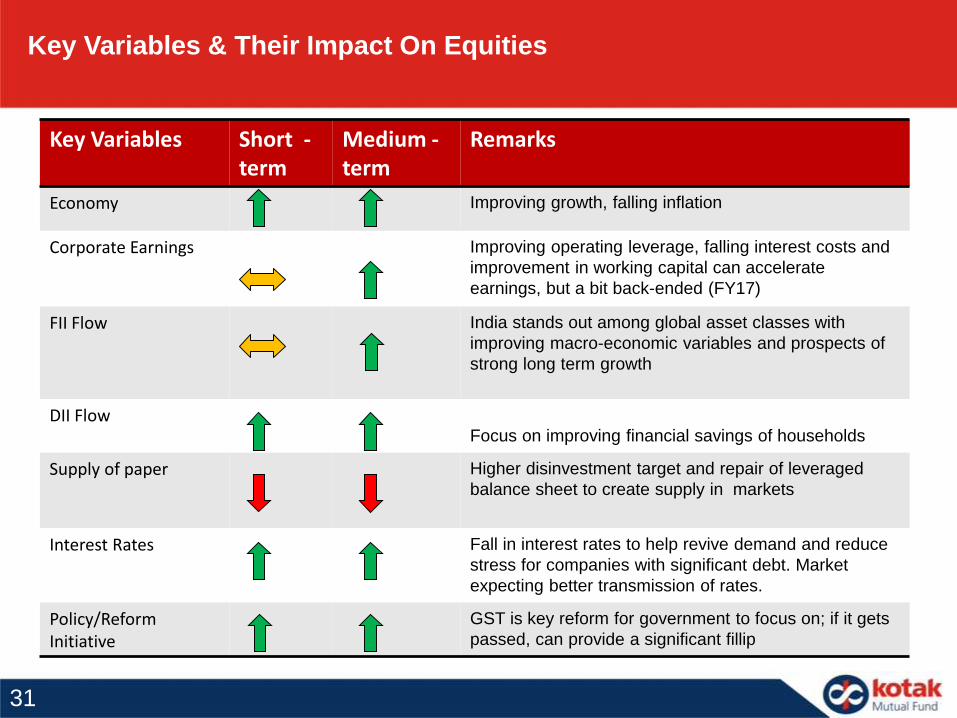

Key Variables & Their Impact On Equities

Key Variables Short -term

Medium -term

Remarks

Economy Improving growth, falling inflation

Corporate Earnings Improving operating leverage, falling interest costs and

improvement in working capital can accelerate

earnings, but a bit back-ended (FY17)

FII Flow India stands out among global asset classes with

improving macro-economic variables and prospects of

strong long term growth

DII FlowFocus on improving financial savings of households

Supply of paper Higher disinvestment target and repair of leveraged

balance sheet to create supply in markets

Interest Rates Fall in interest rates to help revive demand and reduce

stress for companies with significant debt. Market

expecting better transmission of rates.

Policy/Reform Initiative

GST is key reform for government to focus on; if it gets

passed, can provide a significant fillip

31

What Next?– Upcoming drivers and draggers

• GST Bill

• The Govt. is targeting GST roll out by April 1,2017. Most Corporates are not prepared from

infrastructure point view till Mid of FY 18. Will the roll out be deferred ?

• Demonitisation effects on following high frequency indicators

• Rabi crop sowing

• Wholesale prices of essential commodities

• Property registrations

• Consumption indicators like auto sales, durables sales etc

• 3QFY17 corporate earnings to be closely watched

3232

What Next?

– Upcoming drivers and draggers

• Global event

– Markets would be watching the US Fed rate hike signals closely

– Fiscal stimulus plans in Japan, Europe and US will provide cue to global liquidity

– Italian referendum which is expected to decide the fate of Euro zone and fate ofrecapitilisation of Italian banks

– OPEC meeting in November has advocated for production cuts, improving supply dynamicsfor crude

– Chinese currency continues to weaken, from its highs in end 2013, Chinese currency hasdepreciated by around 14%

– Formalising of plan for Britain’s exit from European Union

33

3333

SECTOR & THEMATIC

STANCE

34

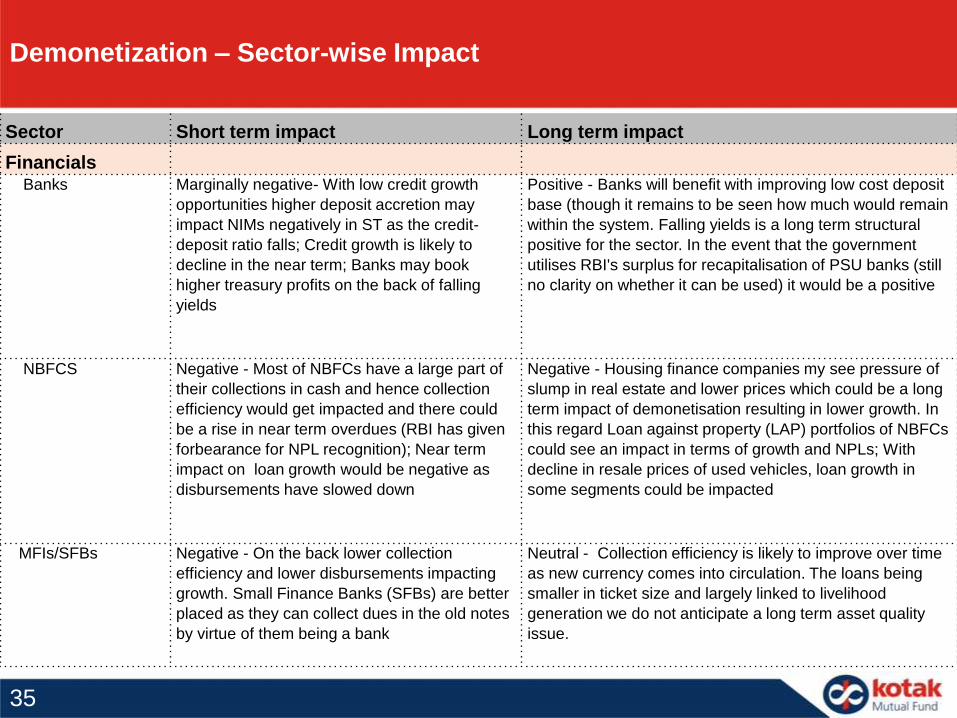

Demonetization – Sector-wise Impact

Sector Short term impact Long term impact

Financials Banks Marginally negative- With low credit growth

opportunities higher deposit accretion may

impact NIMs negatively in ST as the credit-

deposit ratio falls; Credit growth is likely to

decline in the near term; Banks may book

higher treasury profits on the back of falling

yields

Positive - Banks will benefit with improving low cost deposit

base (though it remains to be seen how much would remain

within the system. Falling yields is a long term structural

positive for the sector. In the event that the government

utilises RBI's surplus for recapitalisation of PSU banks (still

no clarity on whether it can be used) it would be a positive

NBFCS Negative - Most of NBFCs have a large part of

their collections in cash and hence collection

efficiency would get impacted and there could

be a rise in near term overdues (RBI has given

forbearance for NPL recognition); Near term

impact on loan growth would be negative as

disbursements have slowed down

Negative - Housing finance companies my see pressure of

slump in real estate and lower prices which could be a long

term impact of demonetisation resulting in lower growth. In

this regard Loan against property (LAP) portfolios of NBFCs

could see an impact in terms of growth and NPLs; With

decline in resale prices of used vehicles, loan growth in

some segments could be impacted

MFIs/SFBs Negative - On the back lower collection

efficiency and lower disbursements impacting

growth. Small Finance Banks (SFBs) are better

placed as they can collect dues in the old notes

by virtue of them being a bank

Neutral - Collection efficiency is likely to improve over time

as new currency comes into circulation. The loans being

smaller in ticket size and largely linked to livelihood

generation we do not anticipate a long term asset quality

issue.

35

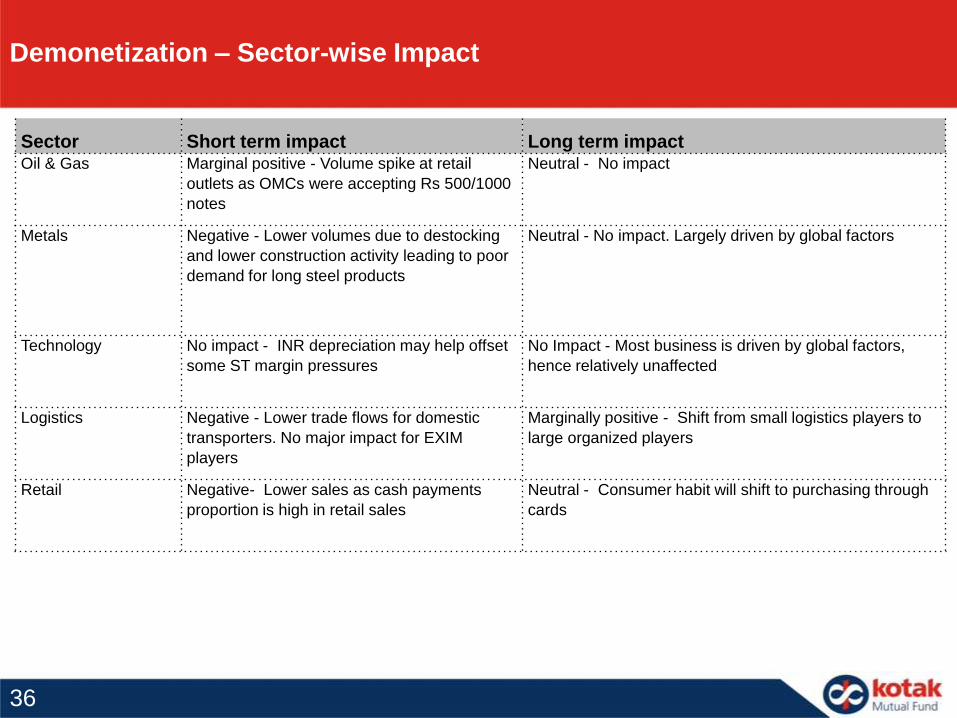

Demonetization – Sector-wise Impact

Sector Short term impact Long term impact Oil & Gas Marginal positive - Volume spike at retail

outlets as OMCs were accepting Rs 500/1000

notes

Neutral - No impact

Metals Negative - Lower volumes due to destocking

and lower construction activity leading to poor

demand for long steel products

Neutral - No impact. Largely driven by global factors

Technology No impact - INR depreciation may help offset

some ST margin pressures

No Impact - Most business is driven by global factors,

hence relatively unaffected

Logistics Negative - Lower trade flows for domestic

transporters. No major impact for EXIM

players

Marginally positive - Shift from small logistics players to

large organized players

Retail Negative- Lower sales as cash payments

proportion is high in retail sales

Neutral - Consumer habit will shift to purchasing through

cards

36

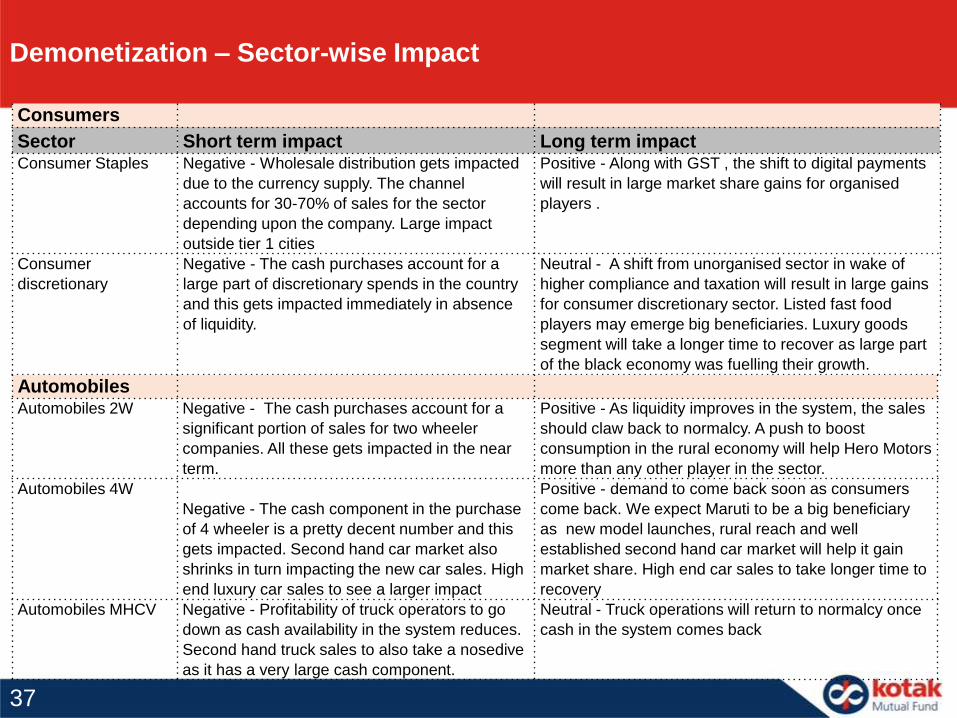

Demonetization – Sector-wise Impact

Consumers

Sector Short term impact Long term impact Consumer Staples Negative - Wholesale distribution gets impacted

due to the currency supply. The channel

accounts for 30-70% of sales for the sector

depending upon the company. Large impact

outside tier 1 cities

Positive - Along with GST , the shift to digital payments

will result in large market share gains for organised

players .

Consumer

discretionary

Negative - The cash purchases account for a

large part of discretionary spends in the country

and this gets impacted immediately in absence

of liquidity.

Neutral - A shift from unorganised sector in wake of

higher compliance and taxation will result in large gains

for consumer discretionary sector. Listed fast food

players may emerge big beneficiaries. Luxury goods

segment will take a longer time to recover as large part

of the black economy was fuelling their growth.

AutomobilesAutomobiles 2W Negative - The cash purchases account for a

significant portion of sales for two wheeler

companies. All these gets impacted in the near

term.

Positive - As liquidity improves in the system, the sales

should claw back to normalcy. A push to boost

consumption in the rural economy will help Hero Motors

more than any other player in the sector.

Automobiles 4W

Negative - The cash component in the purchase

of 4 wheeler is a pretty decent number and this

gets impacted. Second hand car market also

shrinks in turn impacting the new car sales. High

end luxury car sales to see a larger impact

Positive - demand to come back soon as consumers

come back. We expect Maruti to be a big beneficiary

as new model launches, rural reach and well

established second hand car market will help it gain

market share. High end car sales to take longer time to

recovery

Automobiles MHCV Negative - Profitability of truck operators to go

down as cash availability in the system reduces.

Second hand truck sales to also take a nosedive

as it has a very large cash component.

Neutral - Truck operations will return to normalcy once

cash in the system comes back

37

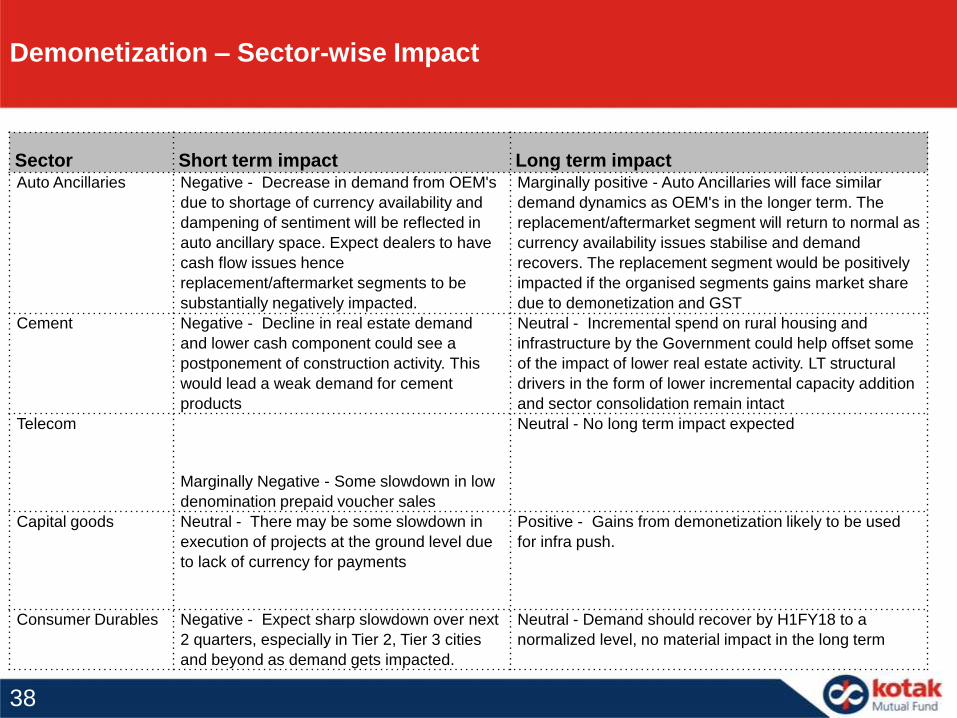

Demonetization – Sector-wise Impact

Sector Short term impact Long term impact Auto Ancillaries Negative - Decrease in demand from OEM's

due to shortage of currency availability and

dampening of sentiment will be reflected in

auto ancillary space. Expect dealers to have

cash flow issues hence

replacement/aftermarket segments to be

substantially negatively impacted.

Marginally positive - Auto Ancillaries will face similar

demand dynamics as OEM's in the longer term. The

replacement/aftermarket segment will return to normal as

currency availability issues stabilise and demand

recovers. The replacement segment would be positively

impacted if the organised segments gains market share

due to demonetization and GST

Cement Negative - Decline in real estate demand

and lower cash component could see a

postponement of construction activity. This

would lead a weak demand for cement

products

Neutral - Incremental spend on rural housing and

infrastructure by the Government could help offset some

of the impact of lower real estate activity. LT structural

drivers in the form of lower incremental capacity addition

and sector consolidation remain intact

Telecom

Marginally Negative - Some slowdown in low

denomination prepaid voucher sales

Neutral - No long term impact expected

Capital goods Neutral - There may be some slowdown in

execution of projects at the ground level due

to lack of currency for payments

Positive - Gains from demonetization likely to be used

for infra push.

Consumer Durables Negative - Expect sharp slowdown over next

2 quarters, especially in Tier 2, Tier 3 cities

and beyond as demand gets impacted.

Neutral - Demand should recover by H1FY18 to a

normalized level, no material impact in the long term

38

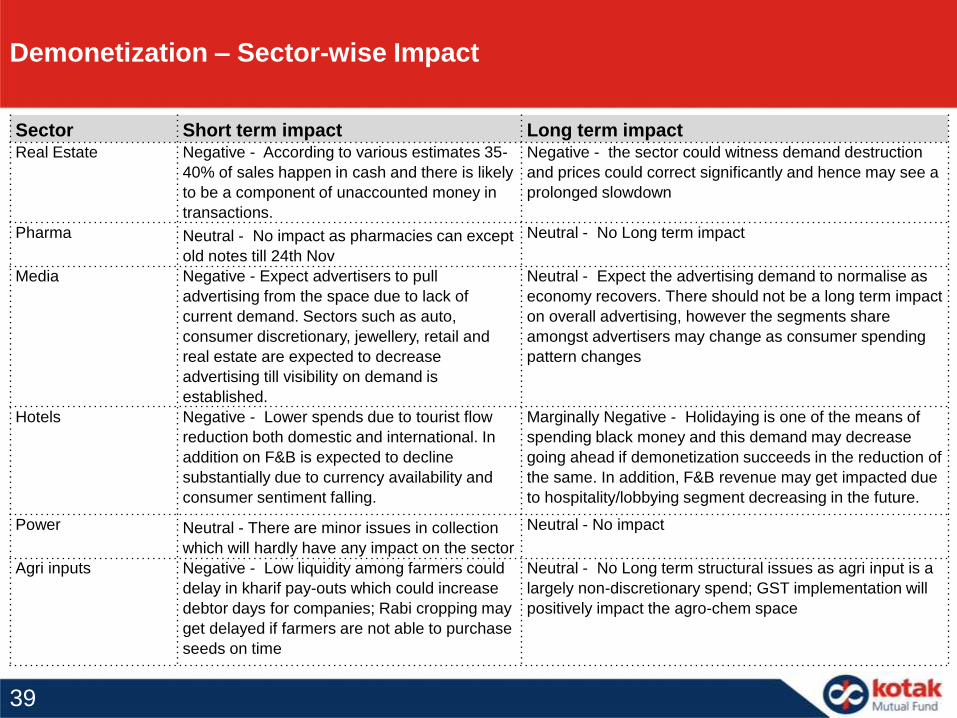

Demonetization – Sector-wise Impact

Sector Short term impact Long term impact Real Estate Negative - According to various estimates 35-

40% of sales happen in cash and there is likely

to be a component of unaccounted money in

transactions.

Negative - the sector could witness demand destruction

and prices could correct significantly and hence may see a

prolonged slowdown

Pharma Neutral - No impact as pharmacies can except

old notes till 24th Nov

Neutral - No Long term impact

Media Negative - Expect advertisers to pull

advertising from the space due to lack of

current demand. Sectors such as auto,

consumer discretionary, jewellery, retail and

real estate are expected to decrease

advertising till visibility on demand is

established.

Neutral - Expect the advertising demand to normalise as

economy recovers. There should not be a long term impact

on overall advertising, however the segments share

amongst advertisers may change as consumer spending

pattern changes

Hotels Negative - Lower spends due to tourist flow

reduction both domestic and international. In

addition on F&B is expected to decline

substantially due to currency availability and

consumer sentiment falling.

Marginally Negative - Holidaying is one of the means of

spending black money and this demand may decrease

going ahead if demonetization succeeds in the reduction of

the same. In addition, F&B revenue may get impacted due

to hospitality/lobbying segment decreasing in the future.

Power Neutral - There are minor issues in collection

which will hardly have any impact on the sector

Neutral - No impact

Agri inputs Negative - Low liquidity among farmers could

delay in kharif pay-outs which could increase

debtor days for companies; Rabi cropping may

get delayed if farmers are not able to purchase

seeds on time

Neutral - No Long term structural issues as agri input is a

largely non-discretionary spend; GST implementation will

positively impact the agro-chem space

39

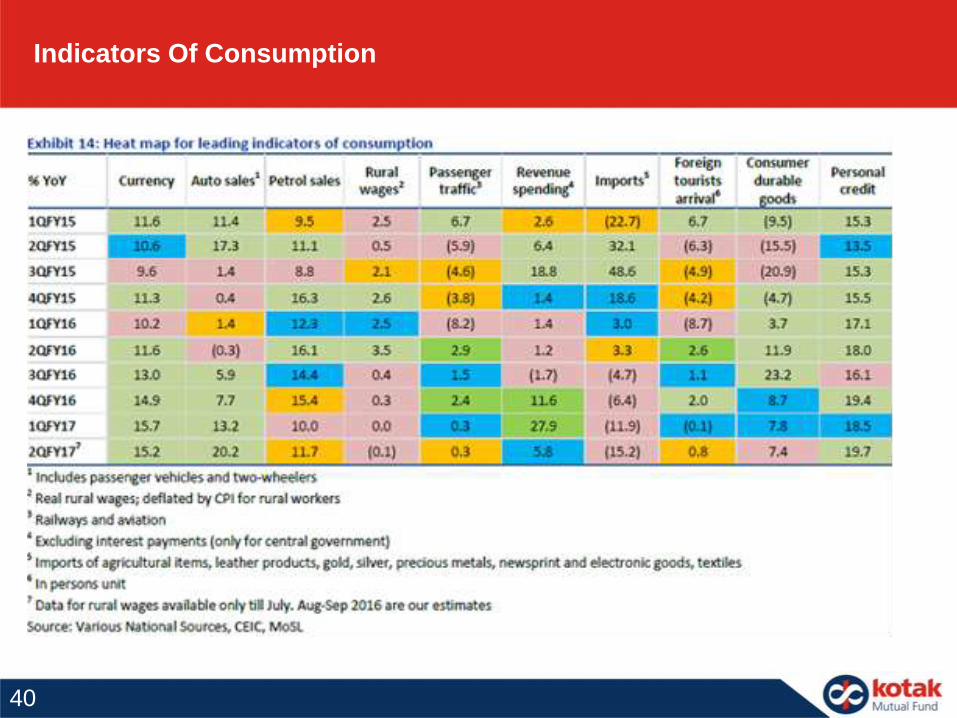

Indicators Of Consumption

40

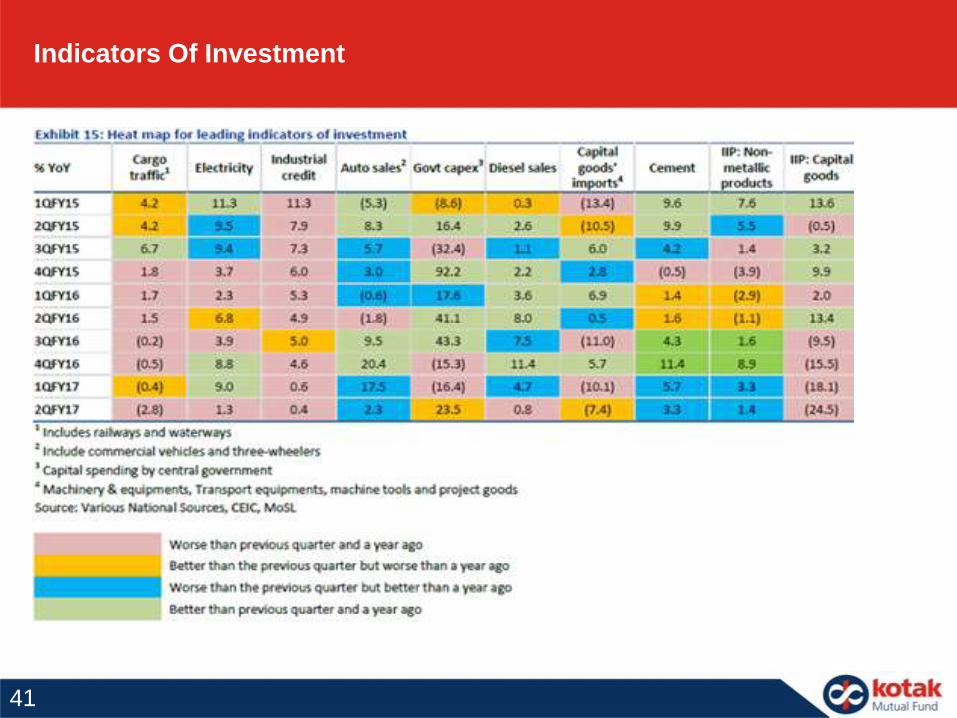

Indicators Of Investment

41

India remains Favorite Destination for Foreign Direct Investment

42

-10% -5% 0% 5% 10% 15% 20% 25%

Construction

Business Services

IT

Telecom

Trade

Transportation

Financials

Mining

Misc. Services

Education

Restaurants

Trading

Manufacturing

Share in Incremental $11bn FDI in FY16

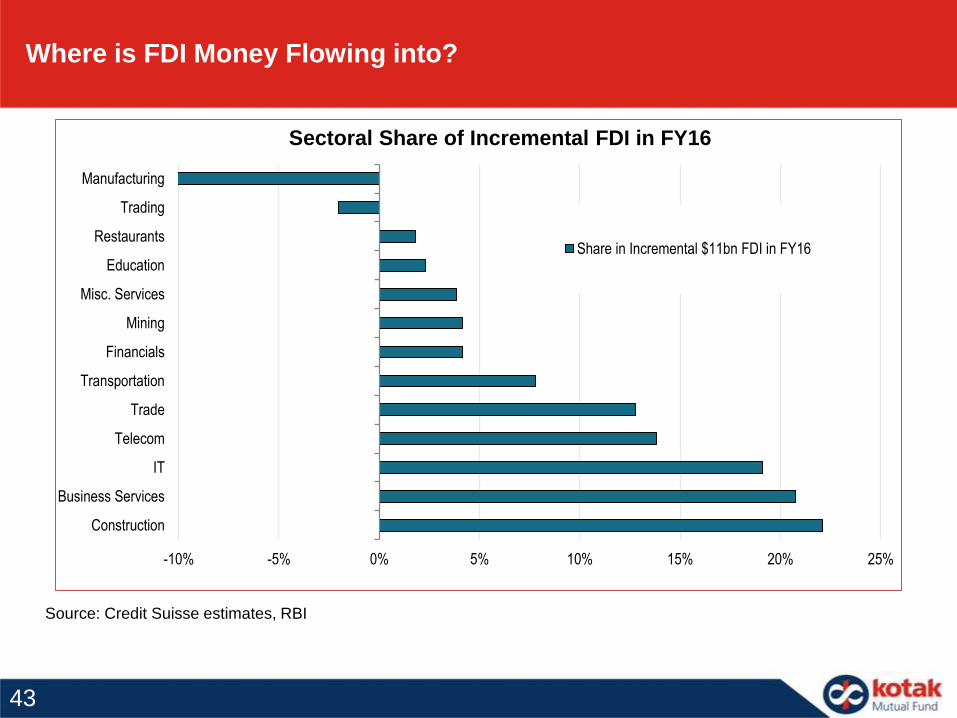

Sectoral Share of Incremental FDI in FY16

Where is FDI Money Flowing into?

Source: Credit Suisse estimates, RBI

43

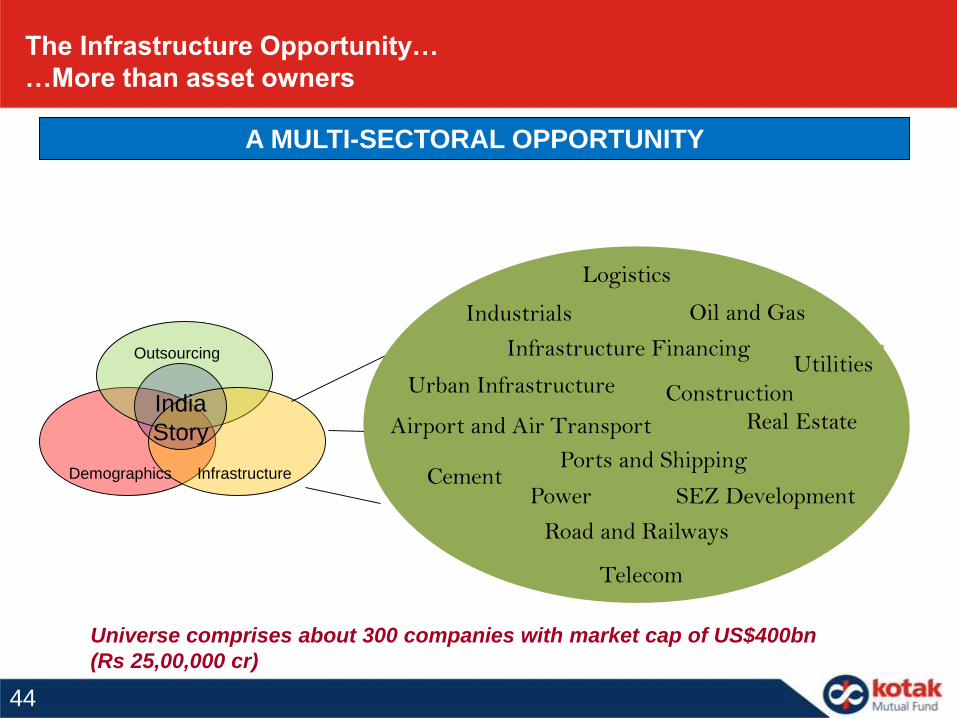

The Infrastructure Opportunity…

…More than asset owners

Demographics

Outsourcing

Infrastructure

India

Story

Universe comprises about 300 companies with market cap of US$400bn

(Rs 25,00,000 cr)

Airport and Air Transport

Cement

Industrials

Infrastructure Financing

Logistics

Oil and Gas

Ports and Shipping

Power

Real Estate

SEZ Development

Road and Railways

Telecom

UtilitiesUrban Infrastructure Construction

A MULTI-SECTORAL OPPORTUNITY

44

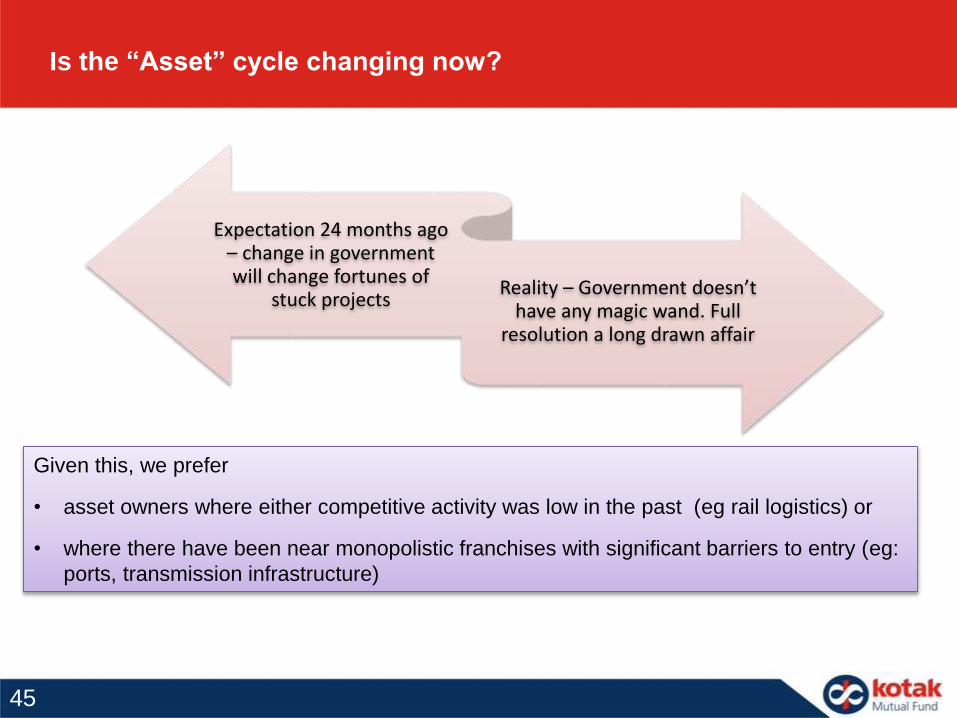

Is the “Asset” cycle changing now?

Expectation 24 months ago – change in governmentwill change fortunes of

stuck projectsReality – Government doesn’t

have any magic wand. Full resolution a long drawn affair

Given this, we prefer

• asset owners where either competitive activity was low in the past (eg rail logistics) or

• where there have been near monopolistic franchises with significant barriers to entry (eg:

ports, transmission infrastructure)

45

Better cost structure now

• Commodity costs – potentially account for 50-80% of any project

• with global commodities down 25-50%, theoretically government can

implement far more projects even with limited financial resources

• Interest costs – Fall in interest rates helps improve viability of new projects

Better fiscal health of government

Government focusing on reviving investment cycle

Comeback in rural housing can also provide support to overall investment cycle

Growth is already picking up and the evidence is visible in Roads, T&D, Railways, Defense, Power sector

“Going with the flow” – where all the action is

46

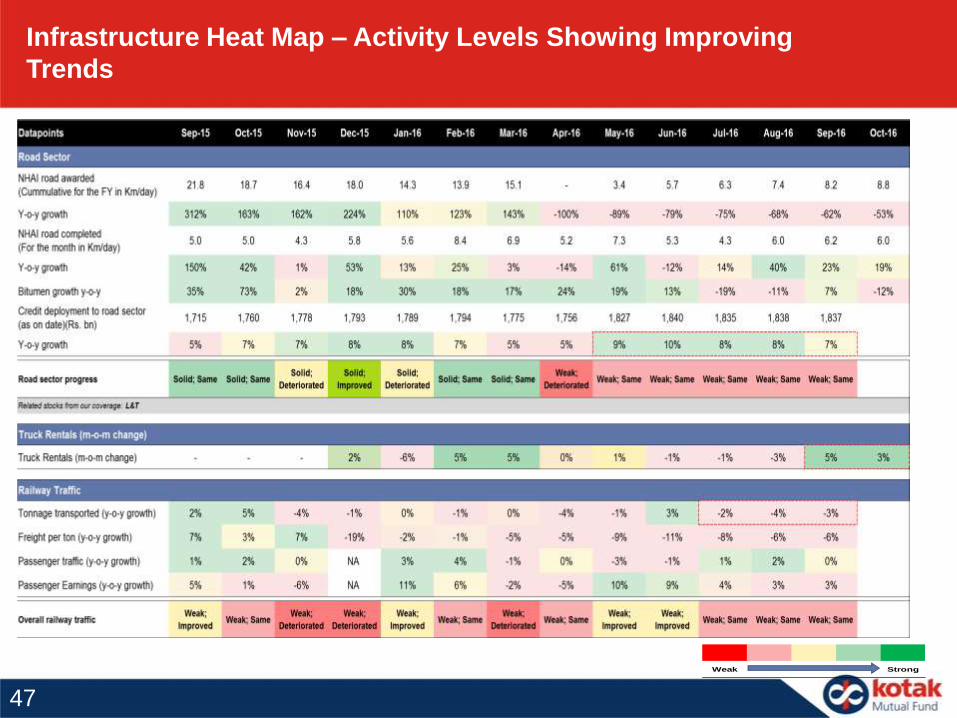

Infrastructure Heat Map – Activity Levels Showing Improving

Trends

Weak Strong

47

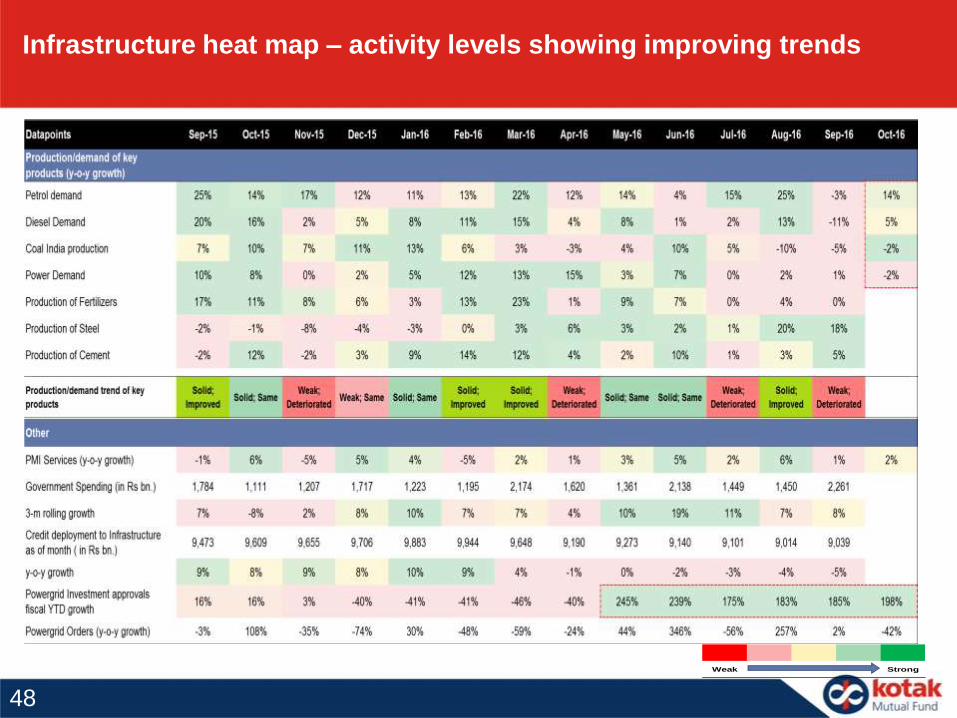

Infrastructure heat map – activity levels showing improving trends

Weak Strong

48

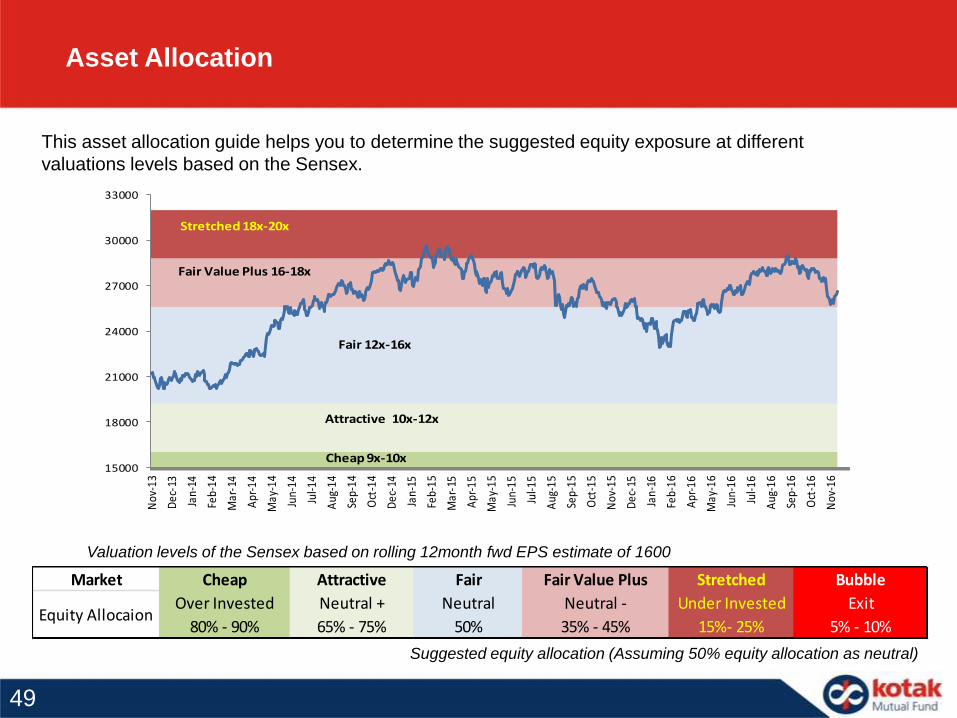

Asset Allocation

This asset allocation guide helps you to determine the suggested equity exposure at different

valuations levels based on the Sensex.

Valuation levels of the Sensex based on rolling 12month fwd EPS estimate of 1600

Suggested equity allocation (Assuming 50% equity allocation as neutral)

Market Cheap Attractive Fair Fair Value Plus Stretched Bubble

Over Invested Neutral + Neutral Neutral - Under Invested Exit

80% - 90% 65% - 75% 50% 35% - 45% 15%- 25% 5% - 10%Equity Allocaion

15000

18000

21000

24000

27000

30000

33000

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep-

14

Oct

-14

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct

-16

Nov

-16

Cheap 9x-10x

Attractive 10x-12x

Fair 12x-16x

Fair Value Plus 16-18x

Stretched 18x-20x

49

Strategy For Investment

• Assuming an agnostic perspective on risk, the following recommendations can be

prescribed:-

• Around half the money in SIP with 5 year horizon

• The rest of the corpus can be placed aside for event related volatility, such as:

• US fed raising interest rates

• India Quarterly Earnings

• UP Election Outcome

• European Banking Crisis

• China Slow down

• GST Roll Out

• In the absence of significant event risk, one can look at fresh issuance opportunities with

attractive valuations in

• IPO, OFS and FPO

• Any IPO in which NBFC are providing leveraged financing for applications might be

a good bet for retail application

50

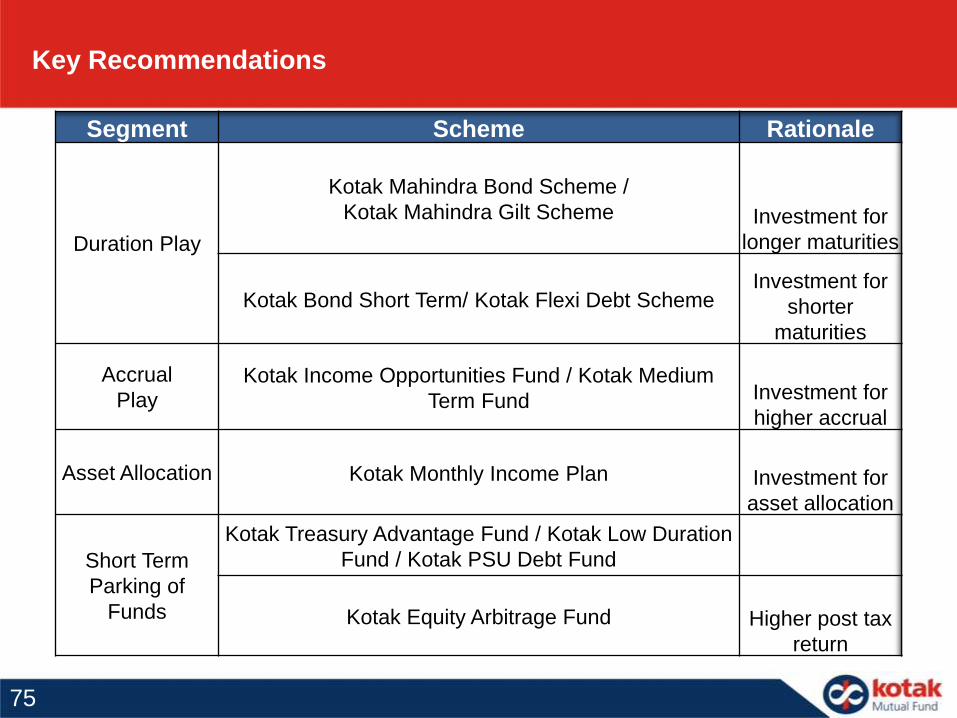

Key Recommendations

Key theme Remarks

Large Cap – play on buying sectoral leaders that

benefit from improving investment climate

Kotak50

Diversified/Multicap – focus on sectors that are

likely to benefit the most across market cap

Kotak Select Focus

Infrastructure revival – “True-to-label” fund –

recent thrust of government to revive the

infrastructure theme

Kotak Infrastructure &

Economic Reforms Fund

Through SIP in Midcap oriented scheme Kotak Emerging Equities Fund

Thematic opportunity through PMS Kotak Pharma PMS

We recommend investors to invest through SIP with a 5 years horizon.

51

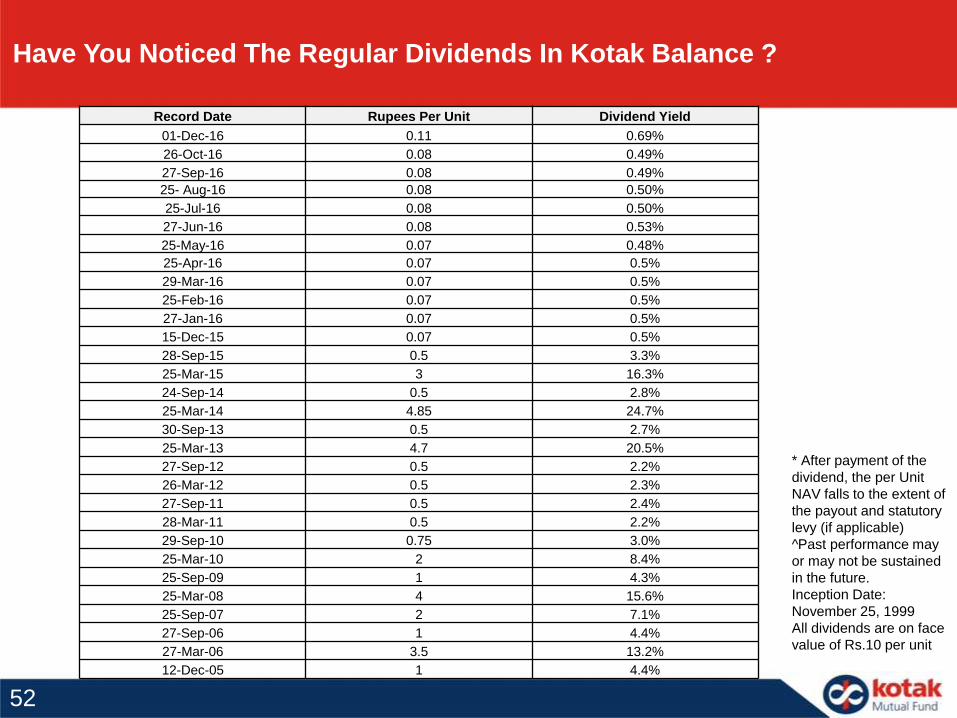

Record Date Rupees Per Unit Dividend Yield

01-Dec-16 0.11 0.69%

26-Oct-16 0.08 0.49%

27-Sep-16 0.08 0.49%

25- Aug-16 0.08 0.50%

25-Jul-16 0.08 0.50%

27-Jun-16 0.08 0.53%

25-May-16 0.07 0.48%

25-Apr-16 0.07 0.5%

29-Mar-16 0.07 0.5%

25-Feb-16 0.07 0.5%

27-Jan-16 0.07 0.5%

15-Dec-15 0.07 0.5%

28-Sep-15 0.5 3.3%

25-Mar-15 3 16.3%

24-Sep-14 0.5 2.8%

25-Mar-14 4.85 24.7%

30-Sep-13 0.5 2.7%

25-Mar-13 4.7 20.5%

27-Sep-12 0.5 2.2%

26-Mar-12 0.5 2.3%

27-Sep-11 0.5 2.4%

28-Mar-11 0.5 2.2%

29-Sep-10 0.75 3.0%

25-Mar-10 2 8.4%

25-Sep-09 1 4.3%

25-Mar-08 4 15.6%

25-Sep-07 2 7.1%

27-Sep-06 1 4.4%

27-Mar-06 3.5 13.2%

12-Dec-05 1 4.4%

Have You Noticed The Regular Dividends In Kotak Balance ?

* After payment of the

dividend, the per Unit

NAV falls to the extent of

the payout and statutory

levy (if applicable)

^Past performance may

or may not be sustained

in the future.

Inception Date:

November 25, 1999

All dividends are on face

value of Rs.10 per unit

52

DEBT

MARKETS

53

Market Outlook

December

2016

54

How November 2016 Unfolded-Key Events Of The Month

• GDP rose 7.3% in the quarter ended September, higher than the 7.1% in the previous one, as consumption

improved but investment slumped. The economy had expanded by 7.6% during the same period last year.

• India's fiscal deficit during the seven months, from April to October, was 79.3% of the budgeted target for the

financial year, compared to 74% last year.

• Taking the nation by surprise, PM Narendra Modi announced demonetisation of Rs 1000 and Rs 500 notes,

making these notes invalid in a major assault on black money, fake currency and corruption.

• The RBI has asked all banks to maintain 100% of incremental CRR on incremental NDTL from the week

starting 16th September to November 11. The move is aimed at absorbing part of surplus liquidity following the

demonetisation move

• The Organisation of the Petroleum Exporting Countries(OPEC) reached an agreement to cut their

production of oil at a meeting in Vienna in an effort to raise crude oil prices. The cartel will now cut production

by 1.2 million barrels per day, which accounts for nearly 1.3% of the entire world's daily oil production. Crude Oil

prices in November increased to $50.32/barrel (4.18% MoM)

• Retail inflation dipped to 4.2 % in October compared with 4.39 % in September, while wholesale inflation also

came down to 3.39 % in October as against 3.57 % in the previous month.

55

How November 2016 Unfolded-Key Events Of The Month

• India's eight core industries, which have a weight of 37.90 %in the Index of Industrial Production

(IIP), grew by 6.6 percent in October 2016 as compared to the same month of the previous year.

• Exports stood at $23.5 billion in October when compared to $21.4 billion in October 2015, aided by

an increase in two key categories — gems and jewellery and engineering goods. Imports grew 8.11 %

to $33.6 billion from $31.1 billion in the year-ago period, widening the trade deficit for October 2016 to

$10.1 billion from $9.69 billion, YoY

• Federal Reserve released minutes from its November meeting which showed that policy makers

agreed an interest-rate increase may be appropriate relatively soon

• Donald Trump stunned the world by defeating heavily favoured Hillary Clinton in the race for the

White House, ending eight years of Democratic rule

• As President-elect Donald Trump said that America will quit the Trans-Pacific Partnership (TPP) on

his first day in office, China which is opposed to the trade deal, began pushing for the proposed FTAAP

calling it critical to long-term prosperity of the region.

56

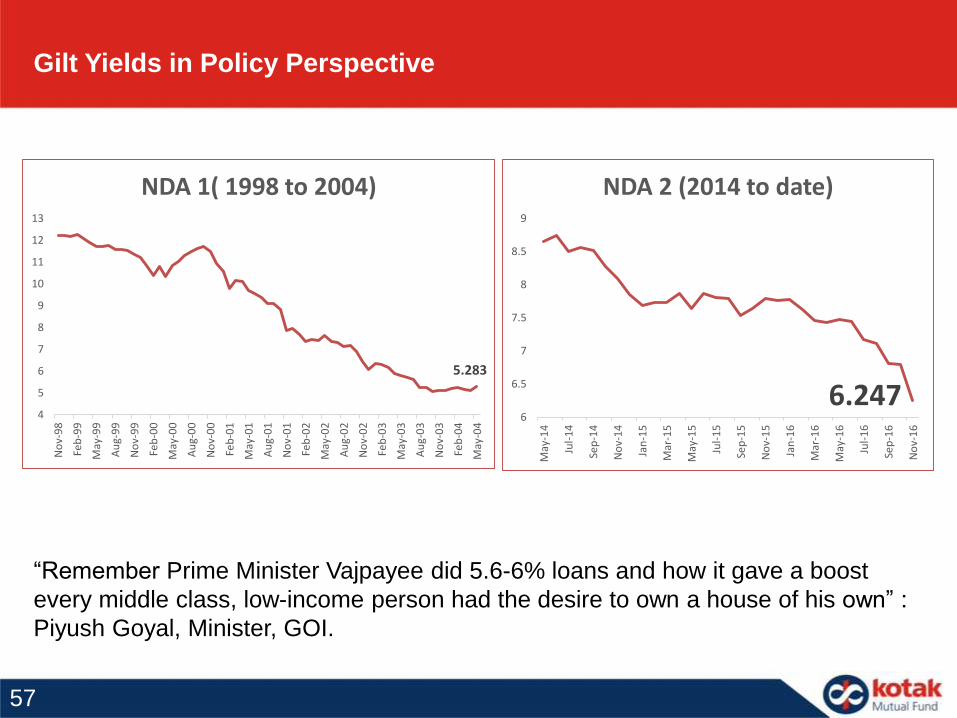

Gilt Yields in Policy Perspective

5.283

4

5

6

7

8

9

10

11

12

13

No

v-9

8

Feb

-99

May

-99

Au

g-9

9

No

v-9

9

Feb

-00

May

-00

Au

g-0

0

No

v-0

0

Feb

-01

May

-01

Au

g-0

1

No

v-0

1

Feb

-02

May

-02

Au

g-0

2

No

v-0

2

Feb

-03

May

-03

Au

g-0

3

No

v-0

3

Feb

-04

May

-04

NDA 1( 1998 to 2004)

6.2476

6.5

7

7.5

8

8.5

9

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-1

6

NDA 2 (2014 to date)

“Remember Prime Minister Vajpayee did 5.6-6% loans and how it gave a boost

every middle class, low-income person had the desire to own a house of his own” :

Piyush Goyal, Minister, GOI.

57

(In %)

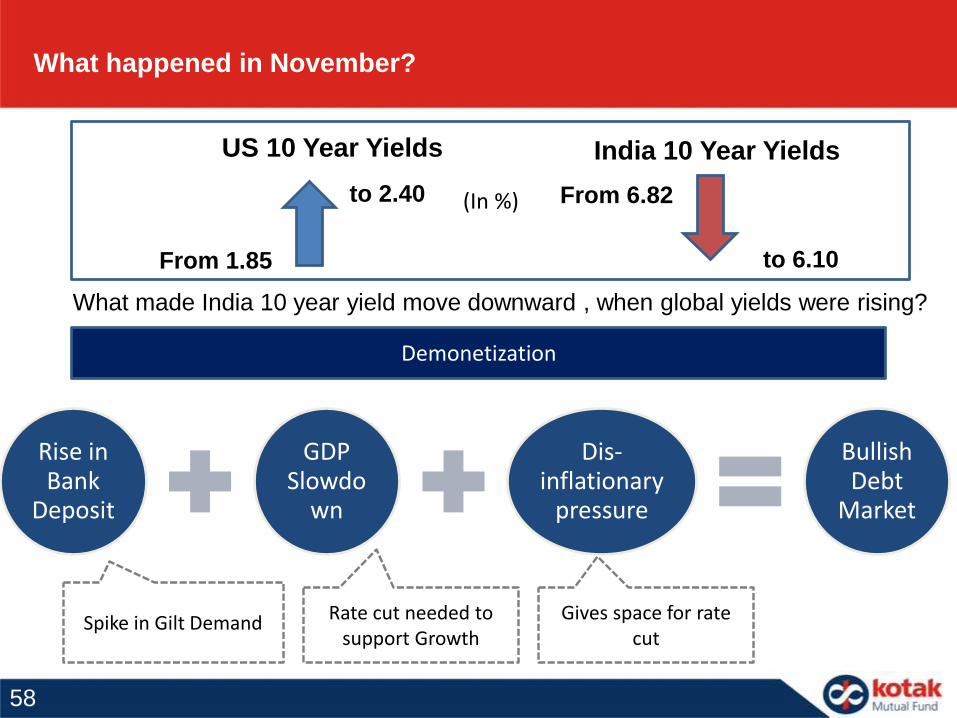

What happened in November?

US 10 Year Yields

From 1.85

to 2.40

India 10 Year Yields

From 6.82

to 6.10

What made India 10 year yield move downward , when global yields were rising?

Demonetization

Rise in Bank

Deposit

GDP Slowdo

wn

Dis-inflationary

pressure

Bullish Debt

Market

Spike in Gilt Demand Rate cut needed to support Growth

Gives space for rate cut

58

6.24

6

6.2

6.4

6.6

6.8

7

7.2

7.4

7.6

7.8

8

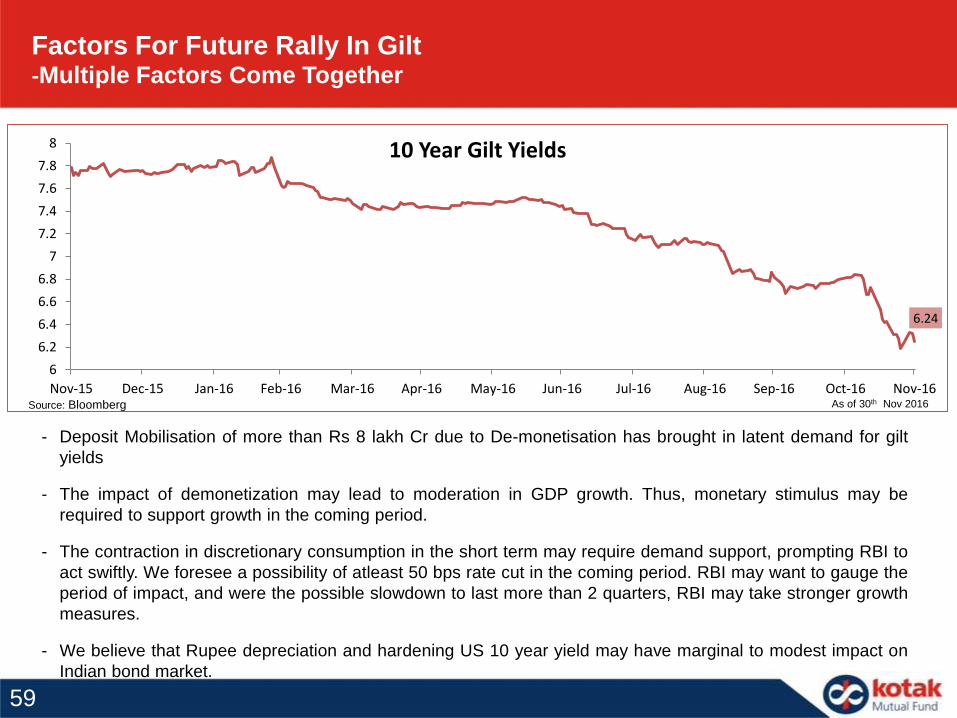

Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

10 Year Gilt Yields

- Deposit Mobilisation of more than Rs 8 lakh Cr due to De-monetisation has brought in latent demand for gilt

yields

- The impact of demonetization may lead to moderation in GDP growth. Thus, monetary stimulus may be

required to support growth in the coming period.

- The contraction in discretionary consumption in the short term may require demand support, prompting RBI to

act swiftly. We foresee a possibility of atleast 50 bps rate cut in the coming period. RBI may want to gauge the

period of impact, and were the possible slowdown to last more than 2 quarters, RBI may take stronger growth

measures.

- We believe that Rupee depreciation and hardening US 10 year yield may have marginal to modest impact on

Indian bond market.

Factors For Future Rally In Gilt-Multiple Factors Come Together

Source: Bloomberg As of 30th Nov 2016

59

Inflation Moderated

Source: MOSPI

• CPI inflation softened to a 14-month low 4.2% in October 2016 from the revised 4.4% in September 2016

benefitting from lower inflation for food & beverages, housing and fuel & light, which offset the impact of

higher prints for pan, tobacco & intoxicants, clothing & footwear and miscellaneous items.

• Core-CPI inflation rose mildly to 4.94% in October 2016, the highest print in eight months, from 4.88% in

September 2016 .As a result, the gap between core-CPI inflation and headline CPI inflation widened in the

just concluded month.

4.20%

4.94%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2D

ec-

12

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3M

ay-1

3

Jun

-13

Jul-

13

Au

g-1

3

Sep

-13

Oct

-13

No

v-1

3D

ec-

13

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4M

ay-1

4

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4D

ec-

14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5M

ay-1

5

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5D

ec-

15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6M

ay-1

6

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

CPI Core CPI

60

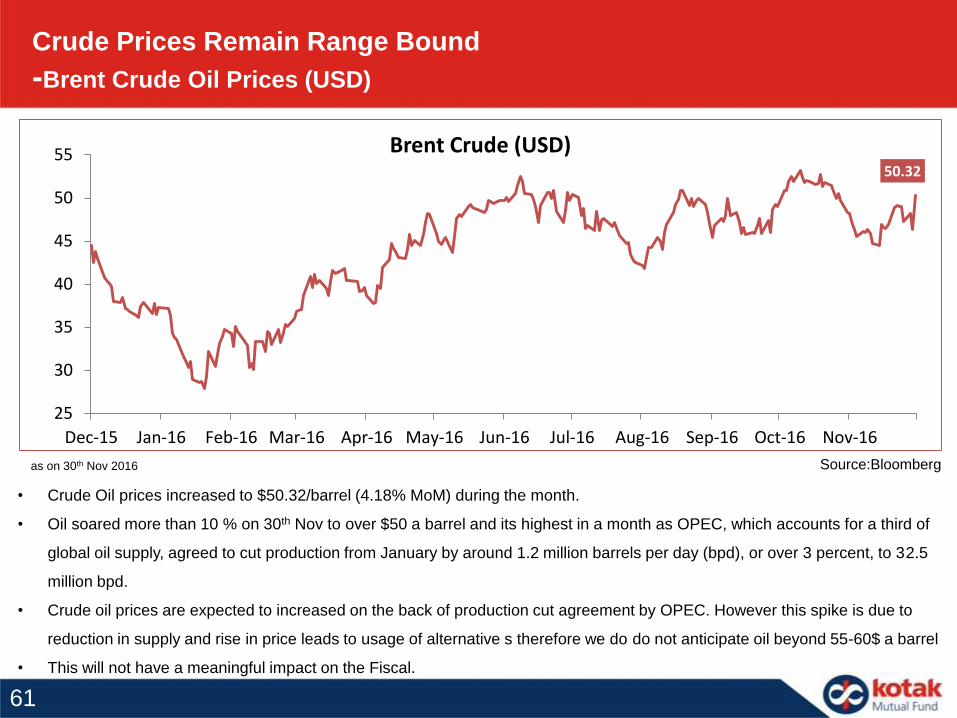

Crude Prices Remain Range Bound

-Brent Crude Oil Prices (USD)

Source:Bloombergas on 30th Nov 2016

• Crude Oil prices increased to $50.32/barrel (4.18% MoM) during the month.

• Oil soared more than 10 % on 30th Nov to over $50 a barrel and its highest in a month as OPEC, which accounts for a third of

global oil supply, agreed to cut production from January by around 1.2 million barrels per day (bpd), or over 3 percent, to 32.5

million bpd.

• Crude oil prices are expected to increased on the back of production cut agreement by OPEC. However this spike is due to

reduction in supply and rise in price leads to usage of alternative s therefore we do do not anticipate oil beyond 55-60$ a barrel

• This will not have a meaningful impact on the Fiscal.

50.32

25

30

35

40

45

50

55

Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

Brent Crude (USD)

61

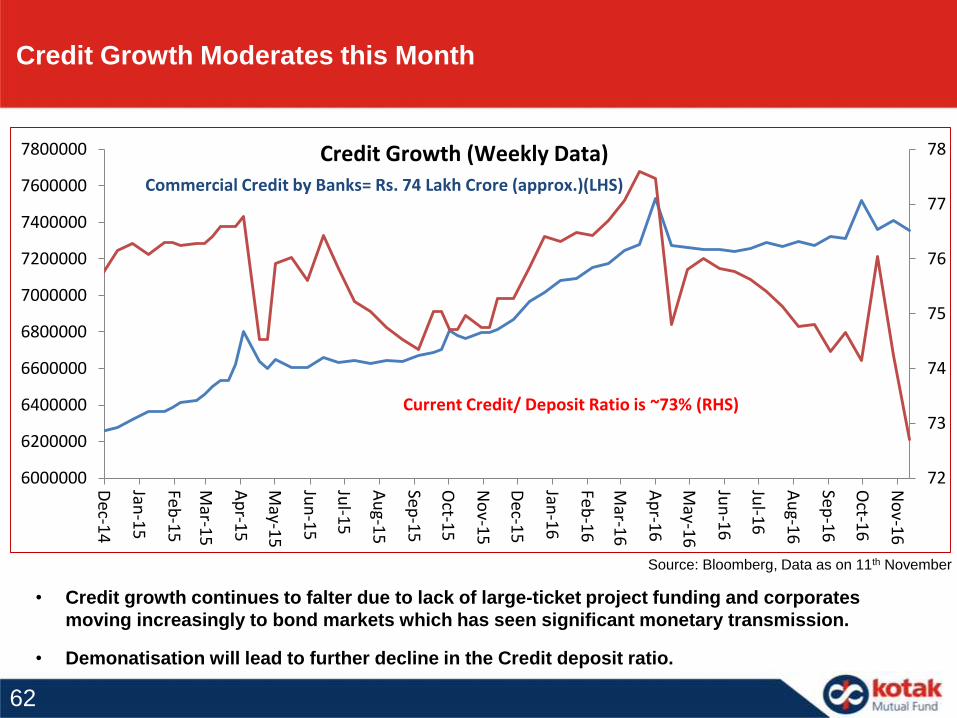

• Credit growth continues to falter due to lack of large-ticket project funding and corporates

moving increasingly to bond markets which has seen significant monetary transmission.

• Demonatisation will lead to further decline in the Credit deposit ratio.

Credit Growth Moderates this Month

Source: Bloomberg, Data as on 11th November

72

73

74

75

76

77

78

6000000

6200000

6400000

6600000

6800000

7000000

7200000

7400000

7600000

7800000

Dec-1

4

Jan-1

5

Feb-1

5

Mar-1

5

Ap

r-15

May-1

5

Jun

-15

Jul-1

5

Au

g-15

Sep-1

5

Oct-1

5

No

v-15

Dec-1

5

Jan-1

6

Feb-1

6

Mar-1

6

Ap

r-16

May-1

6

Jun

-16

Jul-1

6

Au

g-16

Sep-1

6

Oct-1

6

No

v-16

Credit Growth (Weekly Data)Commercial Credit by Banks= Rs. 74 Lakh Crore (approx.)(LHS)

Current Credit/ Deposit Ratio is ~73% (RHS)

62

• Resultant higher bank deposit growth

will lead to higher Gilt demand.

• Demonetisation has accelerated

deposit growth in the banking sytem

• Large deposits will be withdrawn by

public and we expect that about 15-

20% will stay back and will keep

system flush with liquidity

Higher Gilt Demand Likely- Long Term

• Subdued Credit growth will also

favor higher Gilt demand

Source:RBI

8

9

10

11

12

13

14

15

16

17

FY 11 FY 12 FY 13 FY 14 FY 15 FY 16

Bank Credit Growth %

0

2

4

6

8

10

12

FY 11 FY 12 FY 13 FY 14 FY 15 FY 16

CPI % CAD (% GDP)

63

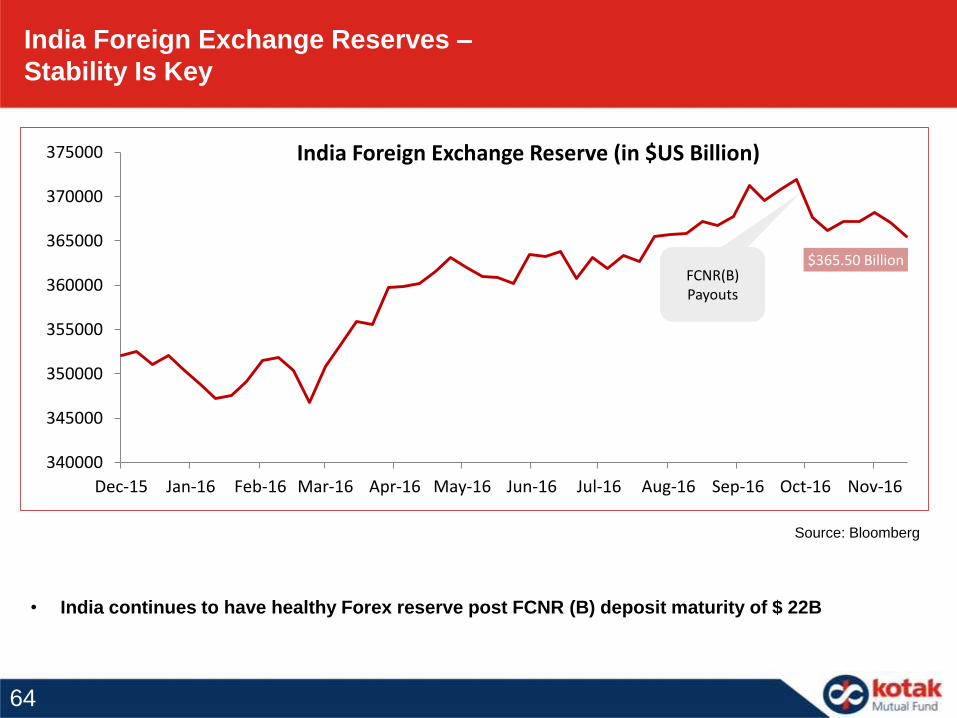

India Foreign Exchange Reserves –

Stability Is Key

• India continues to have healthy Forex reserve post FCNR (B) deposit maturity of $ 22B

Source: Bloomberg

$365.50 Billion

340000

345000

350000

355000

360000

365000

370000

375000

Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

India Foreign Exchange Reserve (in $US Billion)

FCNR(B) Payouts

64

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

6000

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

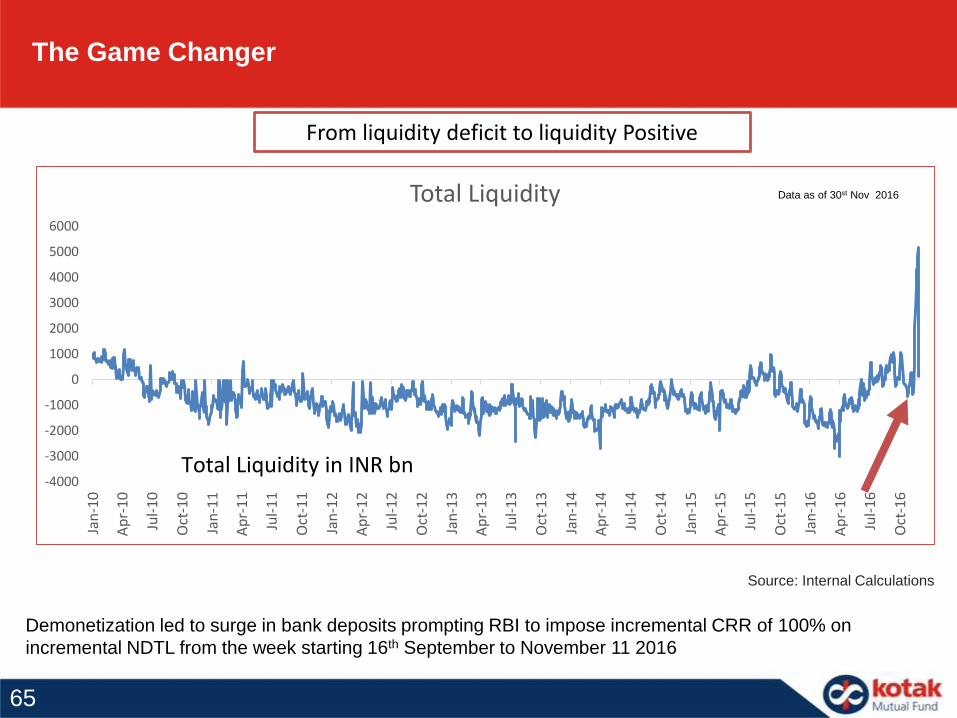

Total Liquidity

Total Liquidity in INR bn

The Game Changer

From liquidity deficit to liquidity Positive

Source: Internal Calculations

Demonetization led to surge in bank deposits prompting RBI to impose incremental CRR of 100% on

incremental NDTL from the week starting 16th September to November 11 2016

Data as of 30st Nov 2016

65

India-US 10 Yr Gilt

As foretold the spreads are compressing

66

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

Spread 10 year yield India - US Spread CPI India - US

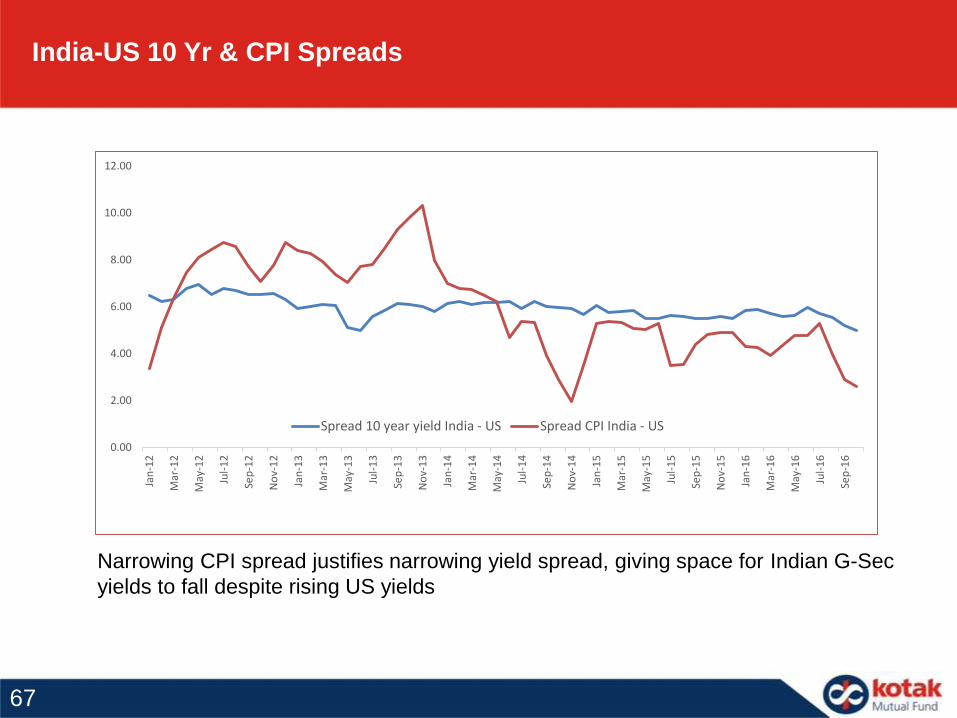

India-US 10 Yr & CPI Spreads

Narrowing CPI spread justifies narrowing yield spread, giving space for Indian G-Sec

yields to fall despite rising US yields

67

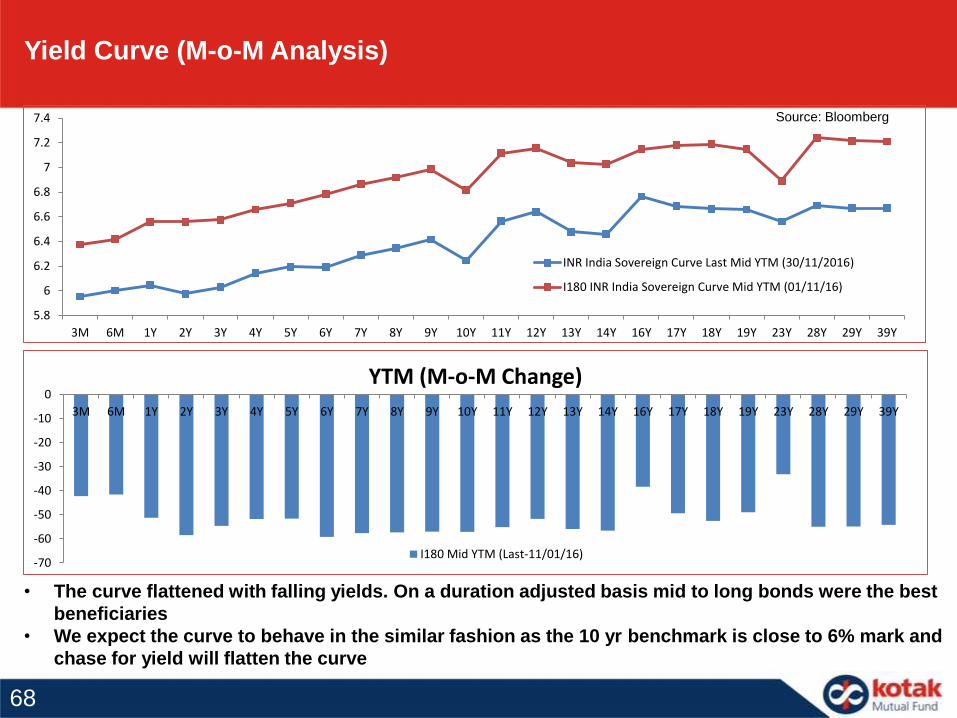

Yield Curve (M-o-M Analysis)

• The curve flattened with falling yields. On a duration adjusted basis mid to long bonds were the best

beneficiaries

• We expect the curve to behave in the similar fashion as the 10 yr benchmark is close to 6% mark and

chase for yield will flatten the curve

Source: Bloomberg

5.8

6

6.2

6.4

6.6

6.8

7

7.2

7.4

3M 6M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 11Y 12Y 13Y 14Y 16Y 17Y 18Y 19Y 23Y 28Y 29Y 39Y

INR India Sovereign Curve Last Mid YTM (30/11/2016)

I180 INR India Sovereign Curve Mid YTM (01/11/16)

-70

-60

-50

-40

-30

-20

-10

0

3M 6M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 11Y 12Y 13Y 14Y 16Y 17Y 18Y 19Y 23Y 28Y 29Y 39Y

YTM (M-o-M Change)

I180 Mid YTM (Last-11/01/16)

68

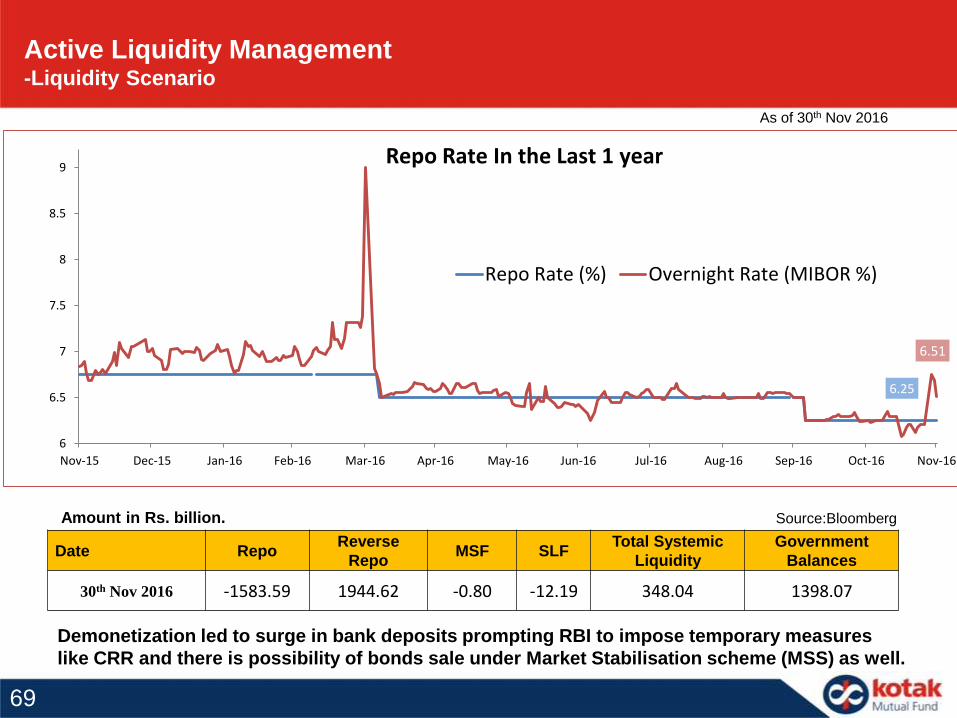

Demonetization led to surge in bank deposits prompting RBI to impose temporary measures

like CRR and there is possibility of bonds sale under Market Stabilisation scheme (MSS) as well.

Source:Bloomberg

Date RepoReverse

RepoMSF SLF

Total Systemic

Liquidity

Government

Balances

30th Nov 2016 -1583.59 1944.62 -0.80 -12.19 348.04 1398.07

Amount in Rs. billion.

Active Liquidity Management-Liquidity Scenario

As of 30th Nov 2016

6.25

6.51

6

6.5

7

7.5

8

8.5

9

Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

Repo Rate (%) Overnight Rate (MIBOR %)

Repo Rate In the Last 1 year

69

-0.5

0

0.5

1

1.5

2

2.5

3

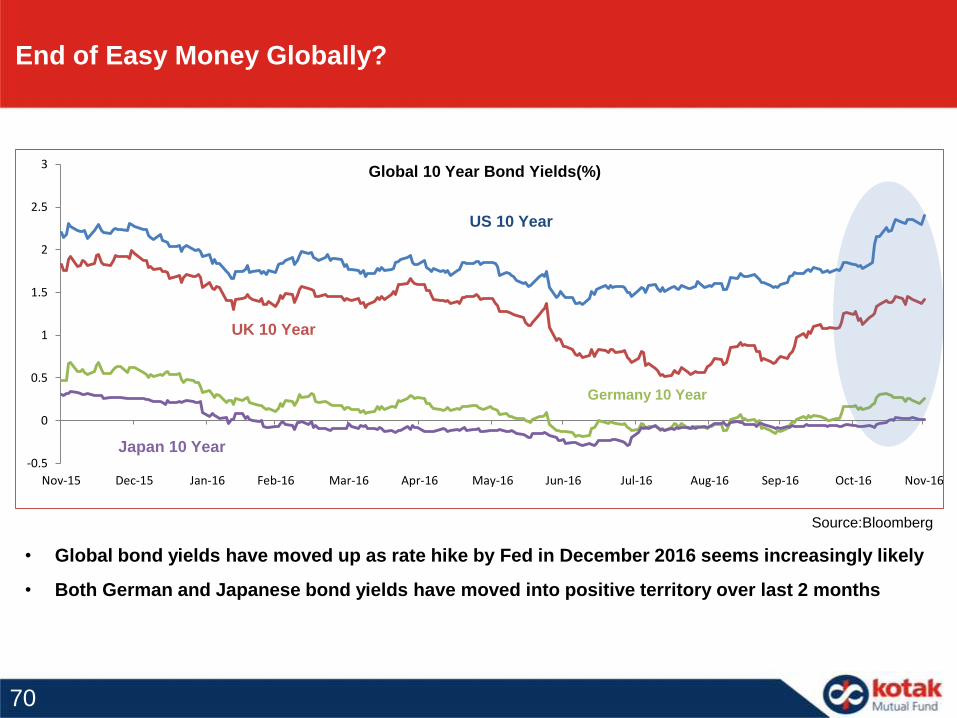

Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

US 10 Year

UK 10 Year

Germany 10 Year

Japan 10 Year

Global 10 Year Bond Yields(%)

Source:Bloomberg

End of Easy Money Globally?

• Global bond yields have moved up as rate hike by Fed in December 2016 seems increasingly likely

• Both German and Japanese bond yields have moved into positive territory over last 2 months

70

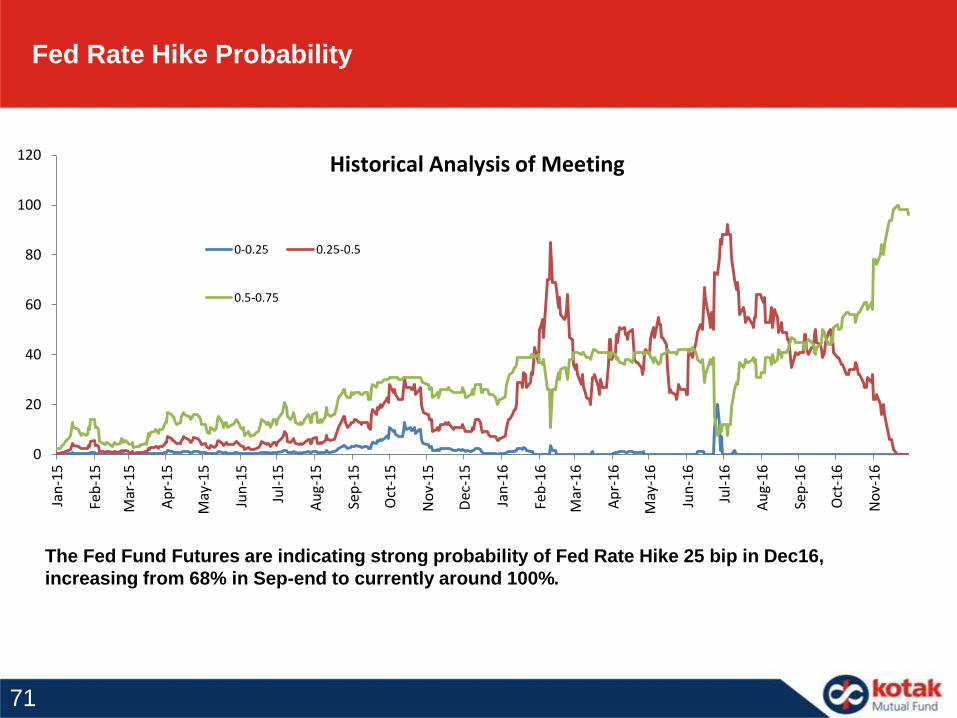

Fed Rate Hike Probability

The Fed Fund Futures are indicating strong probability of Fed Rate Hike 25 bip in Dec16,

increasing from 68% in Sep-end to currently around 100%.

0

20

40

60

80

100

120

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

0-0.25 0.25-0.5

0.5-0.75

Historical Analysis of Meeting

71

-2

0

2

4

6

8

10

12United states

Canada

Brazil

UK

France

Germany

Switzerland

Japan

Australia

South Korea

Thailand

China

India

Indonesia

Source: Bloomberg

Scope For More

-10 Year Gilt Yields Of Select Nations

As of 30th Nov, 2016.

Globally the yields are converging towards the centre while India remains one of the few

exceptions (amongst countries experiencing lower inflation) hovering around ~6.25% yield.

72

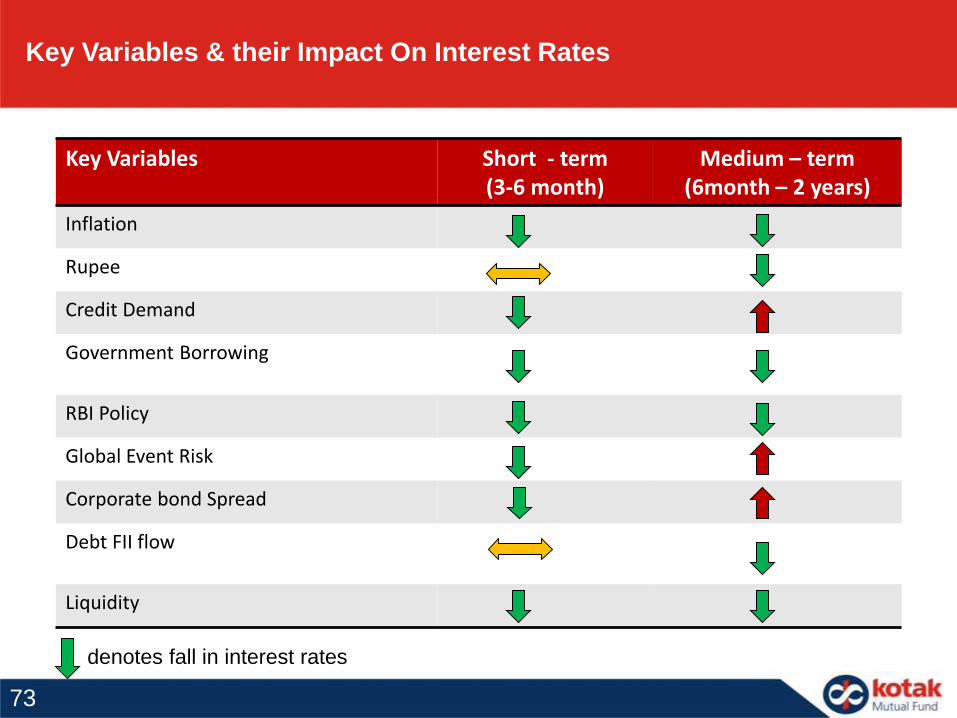

Key Variables & their Impact On Interest Rates

Key Variables Short - term (3-6 month)

Medium – term (6month – 2 years)

Inflation

Rupee

Credit Demand

Government Borrowing

RBI Policy

Global Event Risk

Corporate bond Spread

Debt FII flow

Liquidity

denotes fall in interest rates

73

Debt Outlook

• The avalanche of liquidity due to demonetisation has lead Deposit Mobilisation of more than Rs 8 lakh Cr

which has in turn created chase for assets leading for sharp fall in sovereign bond yields

• This chase of assets is likely to continue and will lead to spread compression

• The impact of demonetization may lead to moderation in GDP growth. Thus, monetary stimulus may be

required to support growth in the coming period

• We foresee a possibility of at least 50 bps rate cut in the coming period. RBI may want to gauge the

period of impact, and were the possible slowdown to last more than 2 quarters, RBI may take stronger

measures to boost growth ie up fronting the rate cut in the December policy

• We believe that Rupee depreciation and hardening US 10 year yield may have marginal to modest

impact on Indian bond market.

• We believe the new 10 year gilt to inch towards 5.9% mark by march 2017 and as said above if the

possibility of the GDP slowdown persists then it will trend lower

• Recent RBI action suggest that RBI intends to keep overnight rates near the Repo rate levels and

therefore the curve upt 12m has already discounted a cut of 25 bps, they may come down further in case

there is a cut of more than 25 bps

• The short tem rates (upto12m) may trend lower in case the RBI shifts the system to reverse repo by

making suitable adjustment in spreads (current spread of Repo and reverse repo rate in 50 bps)

74

Key Recommendations

Segment Scheme Rationale

Duration Play

Kotak Mahindra Bond Scheme /

Kotak Mahindra Gilt Scheme Investment for

longer maturities

Kotak Bond Short Term/ Kotak Flexi Debt SchemeInvestment for

shorter

maturities

Accrual

PlayKotak Income Opportunities Fund / Kotak Medium

Term Fund Investment for

higher accrual

Asset Allocation Kotak Monthly Income Plan Investment for

asset allocation

Short Term

Parking of

Funds

Kotak Treasury Advantage Fund / Kotak Low Duration

Fund / Kotak PSU Debt Fund

Kotak Equity Arbitrage Fund Higher post tax

return

75

Why Accrual Funds ?

• India is one of the fastest growing economy in the world and this will translate into revenue and profitability forIndia Inc. Commodity & oil price decline has reduced input cost and increased margin support

• RBI has slashed repo by 125 bps in 2015 and more cuts are expected in the next 12-18 months. Thoughtransmission has been slow, proposed calculation of base rate on marginal cost basis will ensure fastertransmission and lower base rates (and hence lower cost of capital for borrowers).

• Kotak AMC has strong fundamental processes in place to manage and mitigate credit risk

• Kotak AMC does not invest below A category rating. Our robust monitoring ensures that we do not take exposureeven in AA & A ratings from sensitive sectors

• AAA rate firms have never ever defaulted. The risk of default of AA is only 0.03% and of A is only 0.63%. NotJust that, the AAA continue to hold their rating 97% of times, AA around 92% of times, and A around 88% oftimes

• With efficiently managed credit risk, yields on accrual funds are attractive even on risk-adjustedbasis.

Ratings CRISIL AAA CRISIL AA CRISIL A CRISIL BBB CRISIL BB CRISIL B CRISIL C CRISIL D

CRISIL AAA 97.28% 2.72% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

CRISIL AA 1.41% 92.26% 4.78% 0.58% 0.19% 0.03% 0.02% 0.03%

CRISIL A 0.00% 3.31% 87.79% 5.95% 1.88% 0.15% 0.30% 0.63%

One year average transition rates : between 1988 and 2014

76

Story in Accruals

• Accruals generate performance by purchasing high yielding assets

• The market is currently tilted towards the buyers

• Corporates have alternative in NBFCs for funding. But such corporates would need to provide high

collateral in keeping with the RBI guidelines regarding loan against shares.

• Thus, creditable and quality corporates has to shell out high rates to attract capital

• Retail Investors can consider accrual funds like Kotak Income Opportunities / Kotak Medium term to

gain from the potential high yields in the market.

77

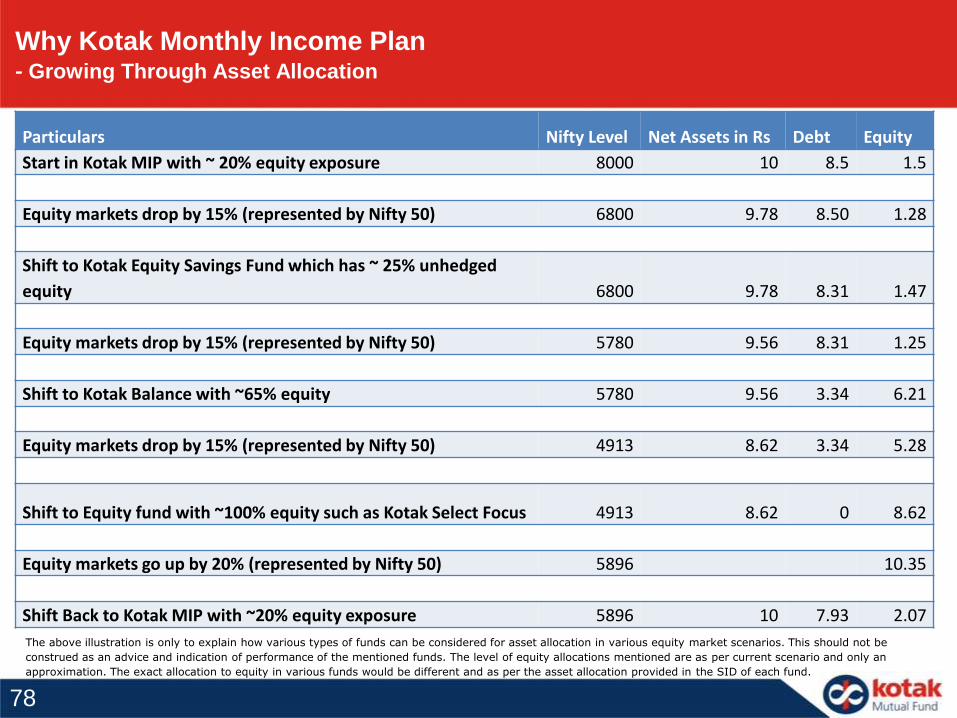

Particulars Nifty Level Net Assets in Rs Debt Equity

Start in Kotak MIP with ~ 20% equity exposure 8000 10 8.5 1.5

Equity markets drop by 15% (represented by Nifty 50) 6800 9.78 8.50 1.28

Shift to Kotak Equity Savings Fund which has ~ 25% unhedged

equity 6800 9.78 8.31 1.47

Equity markets drop by 15% (represented by Nifty 50) 5780 9.56 8.31 1.25

Shift to Kotak Balance with ~65% equity 5780 9.56 3.34 6.21

Equity markets drop by 15% (represented by Nifty 50) 4913 8.62 3.34 5.28

Shift to Equity fund with ~100% equity such as Kotak Select Focus 4913 8.62 0 8.62

Equity markets go up by 20% (represented by Nifty 50) 5896 10.35

Shift Back to Kotak MIP with ~20% equity exposure 5896 10 7.93 2.07

Why Kotak Monthly Income Plan- Growing Through Asset Allocation

The above illustration is only to explain how various types of funds can be considered for asset allocation in various equity market scenarios. This should not be

construed as an advice and indication of performance of the mentioned funds. The level of equity allocations mentioned are as per current scenario and only an

approximation. The exact allocation to equity in various funds would be different and as per the asset allocation provided in the SID of each fund.

78

Tactical Asset Allocation Through MIP- Growing Through Asset Allocation

Kotak Monthly Income Plan can be used as a de-risking strategy

o The scheme invests upto 20% in equity & equity related instruments & rest in

debt instruments

o Thus, an investor could consider Kotak MIP as a starting point for a moderate

exposure to equity and use it as de-risking strategy by shifting into funds with

higher equity allocations as valuations become attractive

o The same has been explained below with an illustration

Whom is the Fund Ideal for?

Investors seeking regular income over short term

Investors seeking income through fixed income securities and marginal gains

from equities

Investors with 1-3 year investment horizon

Those who are unwilling to assume the full equity risk

Those who have low appetite for credit risk

79

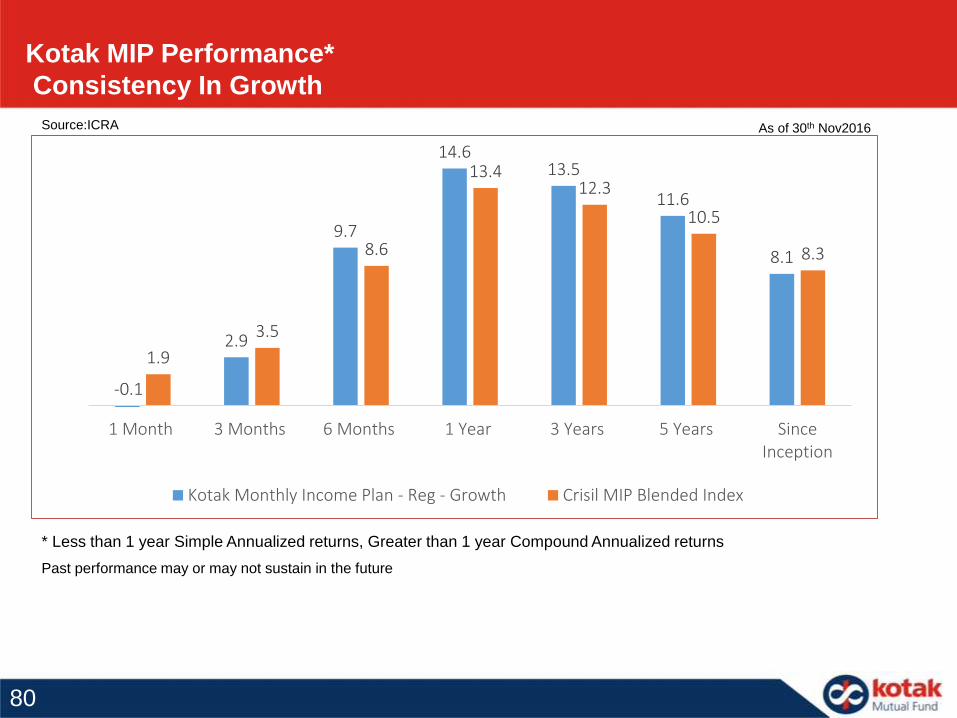

-0.1

2.9

9.7

14.613.5

11.6

8.1

1.9

3.5

8.6

13.412.3

10.5

8.3

1 Month 3 Months 6 Months 1 Year 3 Years 5 Years SinceInception

Kotak Monthly Income Plan - Reg - Growth Crisil MIP Blended Index

Kotak MIP Performance*

Consistency In Growth

As of 30th Nov2016Source:ICRA

* Less than 1 year Simple Annualized returns, Greater than 1 year Compound Annualized returns

Past performance may or may not sustain in the future

80

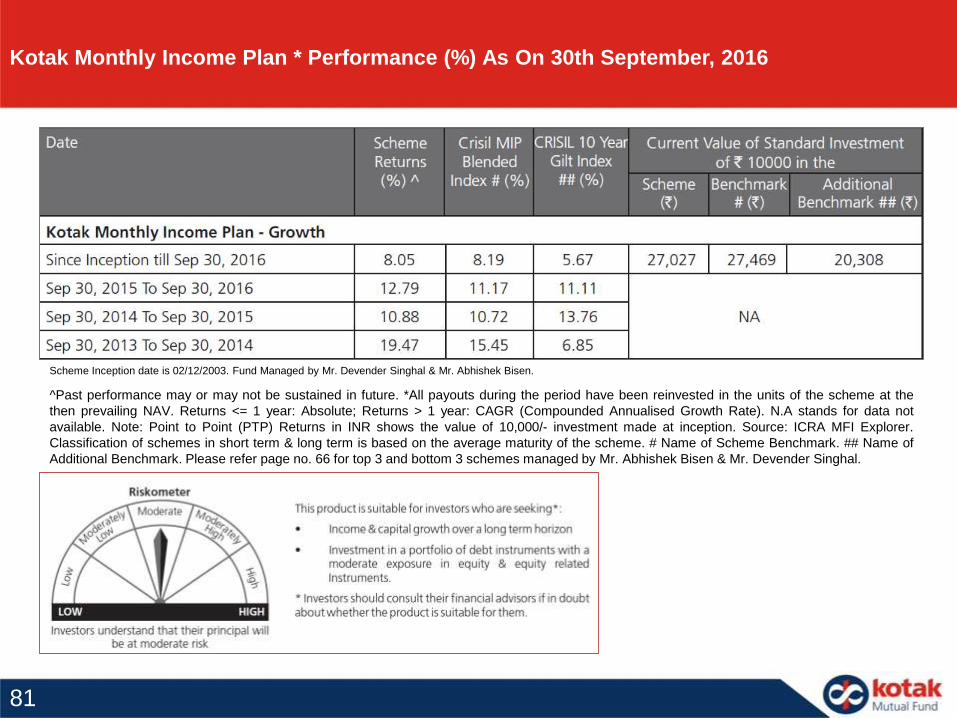

Scheme Inception date is 02/12/2003. Fund Managed by Mr. Devender Singhal & Mr. Abhishek Bisen.

^Past performance may or may not be sustained in future. *All payouts during the period have been reinvested in the units of the scheme at the

then prevailing NAV. Returns <= 1 year: Absolute; Returns > 1 year: CAGR (Compounded Annualised Growth Rate). N.A stands for data not

available. Note: Point to Point (PTP) Returns in INR shows the value of 10,000/- investment made at inception. Source: ICRA MFI Explorer.

Classification of schemes in short term & long term is based on the average maturity of the scheme. # Name of Scheme Benchmark. ## Name of

Additional Benchmark. Please refer page no. 66 for top 3 and bottom 3 schemes managed by Mr. Abhishek Bisen & Mr. Devender Singhal.

Kotak Monthly Income Plan * Performance (%) As On 30th September, 2016

81

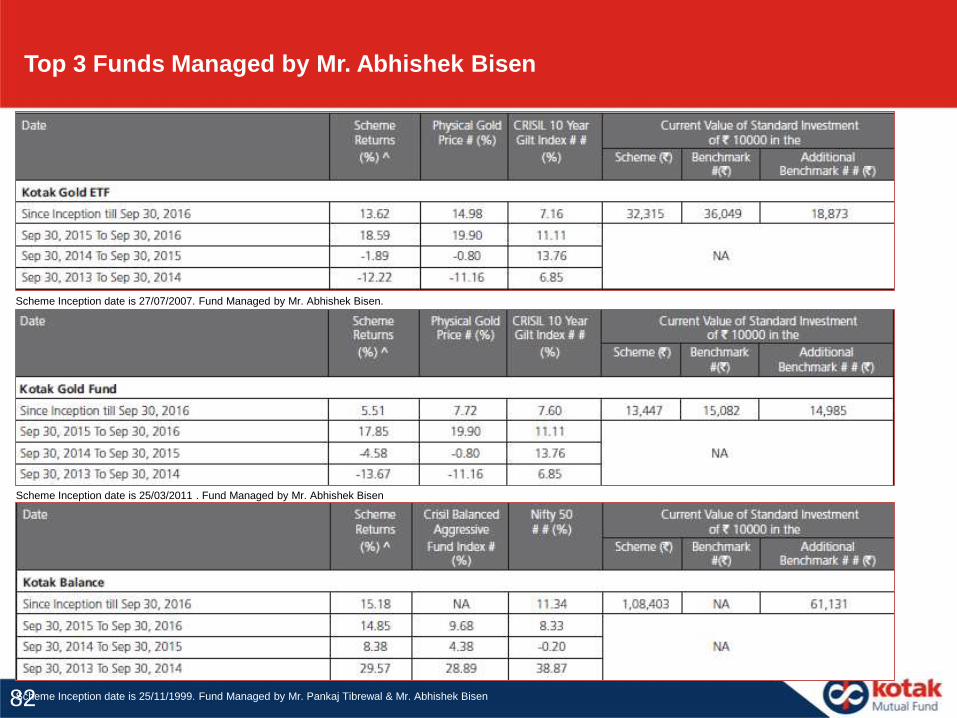

Top 3 Funds Managed by Mr. Abhishek Bisen

Scheme Inception date is 27/07/2007. Fund Managed by Mr. Abhishek Bisen.

Scheme Inception date is 25/03/2011 . Fund Managed by Mr. Abhishek Bisen

Scheme Inception date is 25/11/1999. Fund Managed by Mr. Pankaj Tibrewal & Mr. Abhishek Bisen82

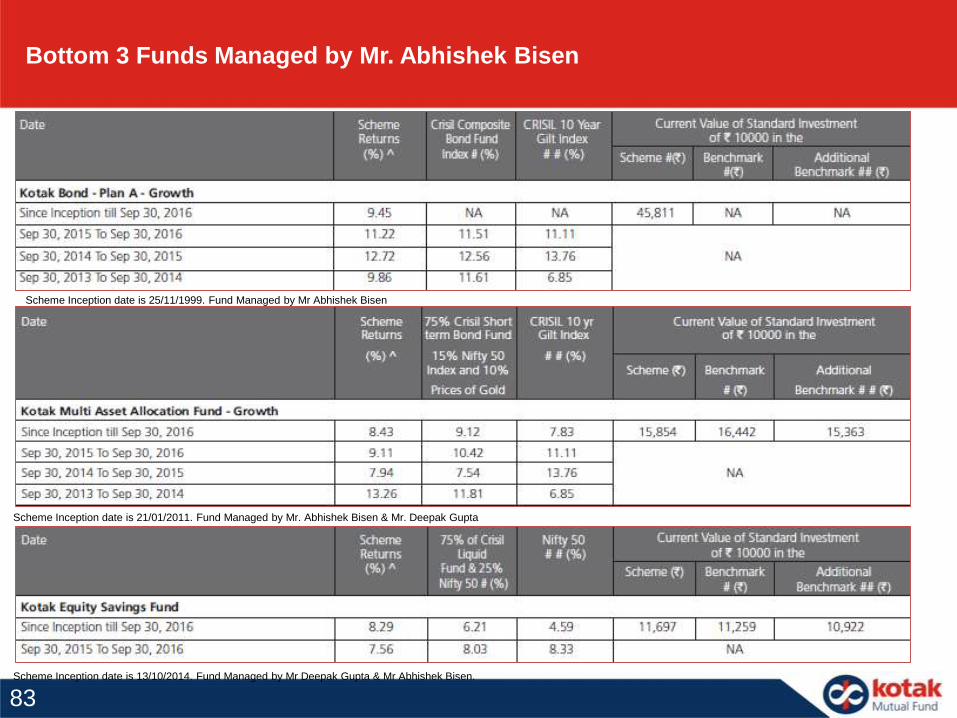

Bottom 3 Funds Managed by Mr. Abhishek Bisen

Scheme Inception date is 25/11/1999. Fund Managed by Mr Abhishek Bisen

Scheme Inception date is 21/01/2011. Fund Managed by Mr. Abhishek Bisen & Mr. Deepak Gupta

Scheme Inception date is 13/10/2014. Fund Managed by Mr Deepak Gupta & Mr Abhishek Bisen.

83

The information contained in this (document) is extracted from different public sources. Allreasonable care has been taken to ensure that the information contained herein is notmisleading or untrue at the time of publication. This is for the information of the person towhom it is provided without any liability whatsoever on the part of Kotak Mahindra AssetManagement Co Ltd or any associated companies or any employee thereof.We are notsoliciting any action based on this material and is for general information only. Mutual Fundinvestments are subject to market risks, read all scheme related documents carefully.

DISCLAIMERS & RISK FACTORS

About the scheme:

84

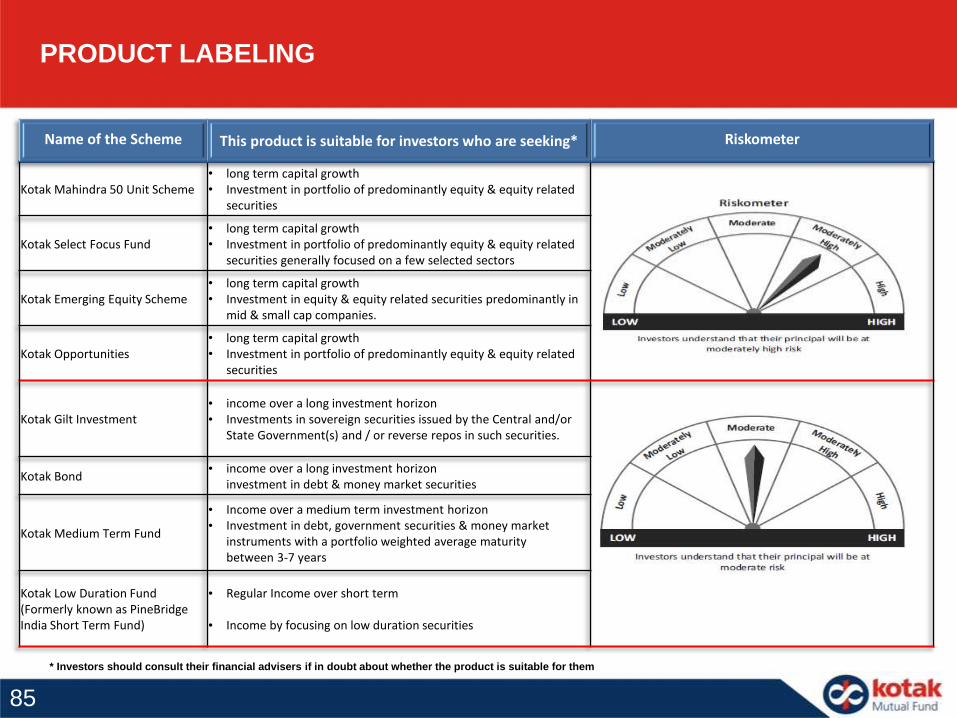

Name of the Scheme This product is suitable for investors who are seeking* Riskometer

Kotak Mahindra 50 Unit Scheme• long term capital growth• Investment in portfolio of predominantly equity & equity related

securities

Kotak Select Focus Fund • long term capital growth• Investment in portfolio of predominantly equity & equity related

securities generally focused on a few selected sectors

Kotak Emerging Equity Scheme• long term capital growth• Investment in equity & equity related securities predominantly in

mid & small cap companies.

Kotak Opportunities• long term capital growth• Investment in portfolio of predominantly equity & equity related

securities

Kotak Gilt Investment• income over a long investment horizon• Investments in sovereign securities issued by the Central and/or

State Government(s) and / or reverse repos in such securities.

Kotak Bond• income over a long investment horizon

investment in debt & money market securities

Kotak Medium Term Fund

• Income over a medium term investment horizon• Investment in debt, government securities & money market

instruments with a portfolio weighted average maturitybetween 3-7 years

Kotak Low Duration Fund (Formerly known as PineBridgeIndia Short Term Fund)

• Regular Income over short term

• Income by focusing on low duration securities

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them

PRODUCT LABELING

85

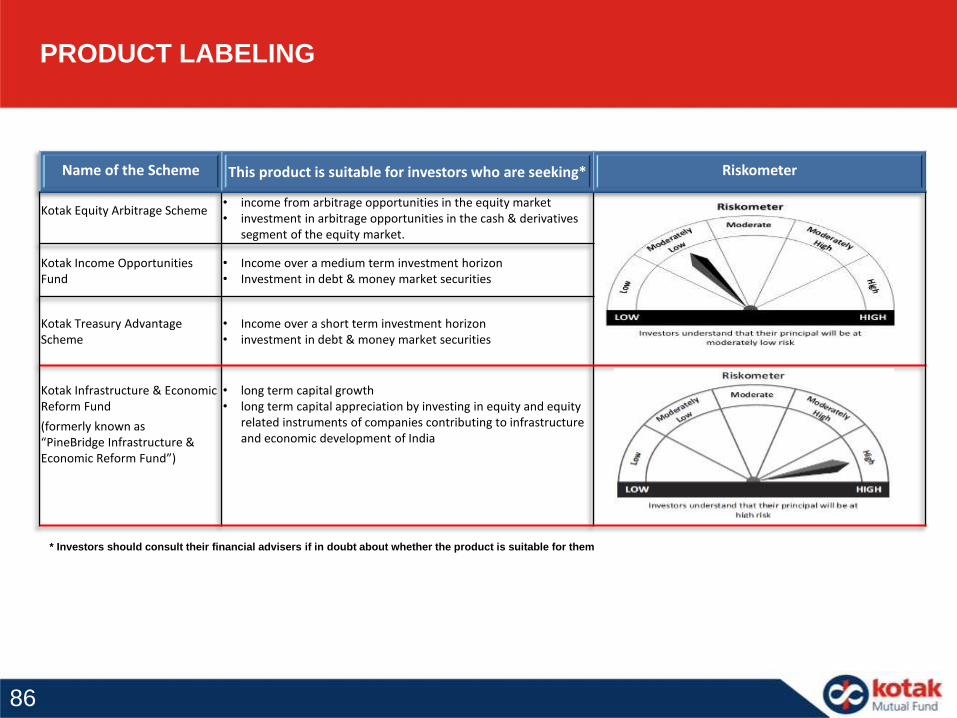

Name of the Scheme This product is suitable for investors who are seeking* Riskometer

Kotak Equity Arbitrage Scheme• income from arbitrage opportunities in the equity market• investment in arbitrage opportunities in the cash & derivatives

segment of the equity market.

Kotak Income Opportunities Fund

• Income over a medium term investment horizon• Investment in debt & money market securities

Kotak Treasury Advantage Scheme

• Income over a short term investment horizon• investment in debt & money market securities

Kotak Infrastructure & Economic Reform Fund

(formerly known as “PineBridge Infrastructure & Economic Reform Fund”)

• long term capital growth• long term capital appreciation by investing in equity and equity

related instruments of companies contributing to infrastructure and economic development of India

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them

PRODUCT LABELING

86