market in minutes ireland retail q4 2016 - pdf repository |...

TRANSCRIPT

Market in MinutesIreland Retail Q4 2016

Savills Research Ireland Retail

ECONOMIC OVERVIEWIntroduction Consumer EconomyDespite increased political uncertainty across the world Ireland’s economy has continued to perform well since our last report. Total employment is rising by 2.9 percent per annum and the number of people at work has surpassed 2m for the first time since 2008. Because of reduced unemployment the public finances continue to improve. The deficit has shrunk from 1.9% of GDP in 2015 to an expected 0.9% this year, while the gross debt ratio has fallen from 78.6% of GDP to an expected 76.0%. Looking ahead, forecasting institutions have trimmed their growth projections for Ireland – mainly as a result of Brexit. Nonetheless, a simple average of GDP projections suggests that growth of around 4.3% will be attained this year, with continued expansion of 3.4% in 2017 and 3.1% in 2018. ■

Reduced unemployment has created competition in the labour market and, as a result, average earnings have been rising for the last two years. At the same time jobs growth has provided the fiscal space for tax reductions in three consecutive budgets. Individually these changes are modest but, taken together, they have led to a significant lift in real household disposable incomes. Adding to this, rising house prices and share values have increased households’ asset wealth - the net worth of Irish households has risen by 39.6% in the last four years.

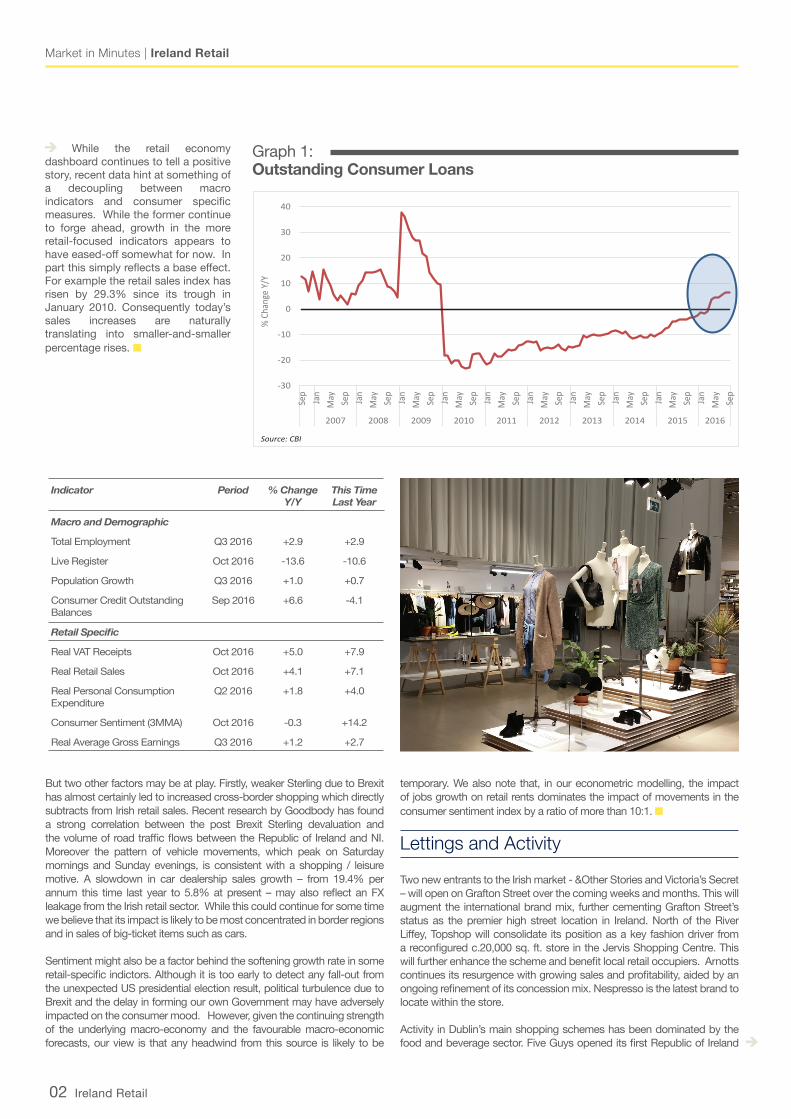

A further important development has been the pronounced rebound in consumer credit. For 75 consecutive months between the end of 2009 and March of this year,

households paid-off consumer debt more quickly than they drew down new loans, resulting in contracting credit balances. This changed dramatically from April and, since then, there has been a sustained and sharp growth in outstanding consumer debt (see graph 1). We believe this is significant for two reasons. Firstly, in practical terms, it adds to consumers’ spending power. Until this year the consumer recovery had been funded through jobs growth, modest increases in take home pay and reduced savings. But borrowing has now added another source of funding for consumer expenditure. In addition, credit expansion provides further evidence that the underlying confidence of consumers and banks has returned to a more normalised level. ■

Market in Minutes | Ireland Retail

02 Ireland Retail

While the retail economy dashboard continues to tell a positive story, recent data hint at something of a decoupling between macro indicators and consumer specific measures. While the former continue to forge ahead, growth in the more retail-focused indicators appears to have eased-off somewhat for now. In part this simply reflects a base effect.For example the retail sales index has risen by 29.3% since its trough in January 2010. Consequently today’s sales increases are naturally translating into smaller-and-smaller percentage rises. ■

Graph 1: Outstanding Consumer Loans

-30

-20

-10

0

10

20

30

40

Sep

Jan

May Sep

Jan

May Sep

Jan

May Sep

Jan

May Sep

Jan

May Sep

Jan

May Sep

Jan

May Sep

Jan

May Sep

Jan

May Sep

Jan

May Sep

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

% C

hang

e Y/

Y

Source: CBI

But two other factors may be at play. Firstly, weaker Sterling due to Brexit has almost certainly led to increased cross-border shopping which directly subtracts from Irish retail sales. Recent research by Goodbody has found a strong correlation between the post Brexit Sterling devaluation and the volume of road traffic flows between the Republic of Ireland and NI. Moreover the pattern of vehicle movements, which peak on Saturday mornings and Sunday evenings, is consistent with a shopping / leisure motive. A slowdown in car dealership sales growth – from 19.4% per annum this time last year to 5.8% at present – may also reflect an FX leakage from the Irish retail sector. While this could continue for some time we believe that its impact is likely to be most concentrated in border regions and in sales of big-ticket items such as cars.

Sentiment might also be a factor behind the softening growth rate in some retail-specific indictors. Although it is too early to detect any fall-out from the unexpected US presidential election result, political turbulence due to Brexit and the delay in forming our own Government may have adversely impacted on the consumer mood. However, given the continuing strength of the underlying macro-economy and the favourable macro-economic forecasts, our view is that any headwind from this source is likely to be

temporary. We also note that, in our econometric modelling, the impact of jobs growth on retail rents dominates the impact of movements in the consumer sentiment index by a ratio of more than 10:1. ■

Lettings and Activity Two new entrants to the Irish market - &Other Stories and Victoria’s Secret – will open on Grafton Street over the coming weeks and months. This will augment the international brand mix, further cementing Grafton Street’s status as the premier high street location in Ireland. North of the River Liffey, Topshop will consolidate its position as a key fashion driver from a reconfigured c.20,000 sq. ft. store in the Jervis Shopping Centre. This will further enhance the scheme and benefit local retail occupiers. Arnotts continues its resurgence with growing sales and profitability, aided by an ongoing refinement of its concession mix. Nespresso is the latest brand to locate within the store.

Activity in Dublin’s main shopping schemes has been dominated by the food and beverage sector. Five Guys opened its first Republic of Ireland

Indicator Period % Change Y/Y

This Time Last Year

Macro and Demographic

Total Employment Q3 2016 +2.9 +2.9

Live Register Oct 2016 -13.6 -10.6

Population Growth Q3 2016 +1.0 +0.7

Consumer Credit Outstanding Balances

Sep 2016 +6.6 -4.1

Retail Specific

Real VAT Receipts Oct 2016 +5.0 +7.9

Real Retail Sales Oct 2016 +4.1 +7.1

Real Personal Consumption Expenditure

Q2 2016 +1.8 +4.0

Consumer Sentiment (3MMA) Oct 2016 -0.3 +14.2

Real Average Gross Earnings Q3 2016 +1.2 +2.7

Market in Minutes | Ireland Retail

Ireland Retail 03

store in Dundrum in September and was met by long queues and very positive reviews.This example demonstrates the growing synergy between fashion shopping and casual dining which has become something of a defensive mechanism for shopping malls against the ongoing threat from online retailers. Further evidence of the food and beverage offering becoming more deeply integrated into shopping centres’ core business model is provided by footfall data. While the overall number of shoppers is rising, footfall in the food court areas of some of the malls that are managed by Savills is rising at twice the overall rate.

Renewed letting activity is also a factor in the out-of-town and Retail Warehouse market with IKEA opening its “Click-and-Collect” store in The Park, Carrickmines.

While Ireland’s economy has been recovering strongly, jobs growth has not been evenly spread across the regions (see Graph 2). Therefore

retail activity outside Dublin continues to be confined to the main urban centres and cities. Crescent Shopping Centre in Limerick is undergoing an extension to its City Mall while UK retailer The Range is opening sizeable stores in both Limerick and Cork. Elsewhere in Cork the Patrick Street area has enjoyed a resurgence of activity with Sostrene Grene and Carluccios committing to new stores and H&M extending its Opera Lane outlet by some 11,000 sq. ft. The c. 40,000 sq. ft. Capitol retail development which fronts onto Patrick Street and Grand Parade is also now fully reserved.

While it is working against retailers in the Republic, cross border shopping should benefit the NI retail economy. North of the border Savills is reporting that Forestside – Belfast’s prime suburban mall – is now fully let. Elsewhere in NI retailers such as Swarovski and Smiggle have acquired stores in Folyeside, Derry, and Savills has brought ubiquitous British retailer Oak Furniture Land to these shores with its first Irish store at Shane Retail Park in Belfast. ■

VacancyWhile vacancy on Dublin’s high streets remains limited, some opportunities are arising either through active asset management or, in the case of Grafton Street, the failure of the American Apparel brand. Additionally, Topshop’s reconfiguration in the Jervis Shopping Centre will leave two units totalling c.10,000 sq. ft. to let at the beginning of 2017.

Graph 2: Percentage of Jobs Lost During the Crash Now Regained, by Region

0

10

20

30

40

50

60

70

80

90

Bord

er

Mid

land

Wes

t

Dubl

in

Mid

-Eas

t

Mid

-Wes

t

Sout

h-Ea

st

Sout

h-W

est

Stat

e

% R

egai

ned

Source: CSO, Savills Research

Market in Minutes | Ireland Retail

04 Ireland Retail

OUTLOOKEconomic and political uncertainty arising from Brexit and the US election result may drag somewhat on sentiment. In the immediate future this means we may see more volatility in short term indicators such as the consumer sentiment and retail sales indices. Additionally ongoing Sterling weakness may lead to further leakage of consumer demand from the Republic of Ireland. However our econometric

analysis, which is based on data going back to 2000, shows that employment has historically been by far the most important factor in determining the retail rents. With the latest CSO data showing continued very strong jobs growth in Q3 2016, and with consensus forecasts pointing to further robust employment gains, our view is that the fundamentals of the macro-economy should continue to support strong demand for retail property and further rental growth – albeit at more moderate rates than those that were experienced in the early recovery phase of the economy. ■

Retail Ireland and Research teams Please contact us for further information

Savills plcSavills is a leading global real estate service provider listed on the London Stock Exchange. The company established in 1855, has a rich heritage with unrivalled growth. It is a company that leads rather than follows, and now has over 200 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. All reference to floor size is approximate. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.

John McCartneyDirector Research+353 (0)1 618 [email protected]

David PotterDirector, Asset Management +353 (0)1 618 [email protected]

David EatonDivisional Director, Asset Management+353 (0)1 618 [email protected]

Colin KavanaghSurveyor, Retail+353 (0)1 618 [email protected]

Darragh CroninHead, High Street & Shopping Centre Retail+353 (0)1 618 [email protected]

Larry BrennanHead, Commercial Division+353 (0)1 618 [email protected]

Stephen McCarthyHead, General Retail Agency+353 (0)1 618 [email protected]

Tegan WhiteAssociate, Retail+353 (0)1 618 [email protected]

Anna GilmartinSurveyor, Retail+353 (0)1 618 [email protected]

Ciaran KellySurveyor, Retail+353 (0)1 618 [email protected]

Rents With the jobs market continuing to out-perform, retailer demand for occupational space should remain strong. Given the fact that large scale retail development is still some way off, rents are therefore likely to rise further. However, after three years of compounding rental growth, base effects are now beginning to dampen annual percentage increases. The growth of Grafton Street ERVs eased from 21.8% per annum in March to 19.2% in June. Our econometric model predicted that it would slow further to 14.1% in September and this forecast has subsequently proved to be very close to the actual 13.9% outcome. Looking further ahead the model predicts a further gradual moderation in the rate of Grafton Street rental growth as base effects continue to compound. Nonetheless rental growth of just under 10% is expected by Q2 2018. Across a broader mix of locations, including less prime markets, rental growth has been slower, with the MSCI overall retail rents index currently rising at 7.2% per annum. Our forecasting model predicts that this will ease somewhat over the next two years but further rental growth of about 7% is expected by mid-2018. ■

0

50

100

150

200

250

300

350

400

450

1996

Q1

1996

Q3

1997

Q1

1997

Q3

1998

Q1

1998

Q3

1999

Q1

1999

Q3

2000

Q1

2000

Q3

2001

Q1

2001

Q3

2002

Q1

2002

Q3

2003

Q1

2003

Q3

2004

Q1

2004

Q3

2005

Q1

2005

Q3

2006

Q1

2006

Q3

2007

Q1

2007

Q3

2008

Q1

2008

Q3

2009

Q1

2009

Q3

2010

Q1

2010

Q3

2011

Q1

2011

Q3

2012

Q1

2012

Q3

2013

Q1

2013

Q3

2014

Q1

2014

Q3

2015

Q1

2015

Q3

2016

Q1

2016

Q3(f)

2017

Q1(f)

2017

Q3(f)

2018

Q1(f)

Inde

x: D

ec 1

994

= 10

0

Source: Savills Research

Graph 3: Grafton St. Rents Forecast Q3 2016 - Q2 2018