market entry and non-national suppliers: barriers to entry in uk public and utility procurement...

TRANSCRIPT

I•UTTERWORTH I ' I ~ E I N E M A N N

European Journal of Purchasing and Supply Management Vol 1, No 4, pp. 19%207, 1994 Copyright © 1995 Elsevier Science Ltd

Printed in Great Britain. All rights reserved 0%9-7012/94/$10.00 + 0.00

0969-7012(95)00008-9

Market entry and non-national suppliers

Barriers to entry in UK public and utility procurement markets

Andrew Cox The Contracts and Procurement Research Unit, Birmingham Business School, The University of Birmingham, Edgbaston, Birmingham B15 2TT, UK

This article outlines some of the major reasons why it is difficult for non-national suppli- ers to break into the UK public and utility procurement markets, despite recent changes in national and EC law, which seek to encourage more open and competitive market entry. The paper outlines the major changes in the national and EC law and then looks at some of the effective barriers to market entry. Finally, some suggestions about the possible strategies that non-national suppliers - especially SMEs - might use to overcome these obstacles are made.

Keywords: public procurement, EU regulations utilities

N a t i o n a l and E U regula tory rules against d i scr iminatory p r o c u r e m e n t practices in the U K

Both UK national and EC legislation have been developed since the 1980s to encourage more open and non-discriminatory procurement practices. A fundamental tenet of UK government policy since 1979 has been the introduction of competition and 'value for money' considerations in the delivery of goods, works and services. Policy approaches have included privatization (eg British Telecom), market testing (competition between public and private organizations for service delivery), contracting out (transfer of service provision from the public to the private sector), and hiving off (transfer of activities between central government organizations on efficiency grounds).

A more fundamental change since 1988, of course, has been the further development of EC Directives for public works, supplies and services contracts, and for similar contracts in the utilities sectors of transport, energy, water and telecommu- nications. These Directives have been essential in providing the legal framework that seeks to encour- age open, transparent and non-discriminatory public

and utility procurement practices across the 12 Member States of the EC (Cox, 1993).

One might expect, therefore, given that all contracts over certain threshold levels must now be open for competitive tendering, and that domestic legislation in the UK has reinforced this trend since 1979, that we would see a much greater incidence of foreign supply than in the past.

Reliable estimates are not available for the proportion of total procurement expenditure that has been contracted with private firms as a result of these changes, but there ought to be considerable scope for private firms - including SMEs - to enter UK public markets. These opportunities are indicated by the following information:

• Central government. Competition and the scope for private provision exist for the bulk of the central government's road building programme (valued at some £2 billion during 1990/91), and all departmental requirements for cleaning, laundry, catering, most security cover and some forms of maintenance. The majority of building construction and refurbishment (worth about £3.5 billion per annum) is also open to compet- itive tendering. Moreover, the government is not

199

A Cox

directly involved in industrial manufacture, and all supplies purchases are therefore obtained from private enterprises (figures in Table 1).

• The Ministry of Defence. Some 37.3% of the Ministry's expenditure is spent on equipment. In addition, contracts are placed for over £140 million worth of support service provision annually.

• Local government. Under domestic legislation, periodic competition is required by councils for construction work and for the provision of certain services (such as catering, refuse collec- tion, and sports centre management). These contracts are open to market entry by foreign firms under both EC and non-EC purchasing arrangements.

• National Health Service. All expenditure on construction and supplies is open to competition and market entry by firms. In addition, support activities including catering and management, valued at £140 million per annum, are subject to periodic competitive tender.

Despite this, while little systematic evidence has emerged on the extent to which foreign firms have bid for, or obtained, contracts advertised under the recently revised EC public purchasing regime, cross- sectional research based on 1992 data (Hartley and Uttley, 1994) indicates that fewer than 3% of bidding firms, and only 0.4% of successful tenders, were non- national. This would suggest that, despite the revisions to EC supplies legislation, foreign firms are adopting methods other than direct export to enter UK public markets. Hartley and Uttley indicate that the Post Office estimates that 27.5% of its procure- ment is imported. Similarly, British Rail estimates that imports represent approximately 25% of total procurement. These findings suggest that, despite a reluctance on the part of non-national firms to bid for UK public contracts directly, considerable market penetration is currently occurring, though not through direct cross-border contract bidding.

Other research indicates that SME participation in government contracting for the EC States as a whole represents approximately 25% of expendi- ture, despite estimates that SMEs account for some 65% of economic activity (SEMA, 1992). This suggests that SMEs have had limited success in obtaining UK public contracts directly. These figures do not, however, include SME participation in subcontracting, which may be significant. This implies that there may still be a problem of market opening, despite the recent legislative changes. The reasons for this are discussed below.

Barriers to market entry for n o n - n a t i o n a l suppl iers

Despite new national and EC regulatory rules, there are a host of barriers that persist for non-national

suppliers when they consider competing for contracts in the UK market. Obviously these barri- ers will vary in importance depending on the size of the company and the product or service that is being provided. Generally speaking, however, it can be argued that the smaller the company the greater the degree of difficulty it can expect to experience in overcoming these obstacles. This arises because most SMEs lack financial, cultural and personnel resources to deal with the most common barriers to entry. These are listed below.

Inadequate information on the demand for public services, goods and construction in the UK

One of the first difficulties that firms face in enter- ing the UK market is that it is difficult to assess the size of the UK public procurement market accurately. It is estimated that UK public expendi- ture on goods and services is large, accounting for approximately 20% of national GDP (OECD, 1992), or some 114 billion ECU during 1991 (current prices). On the basis of Irish Export Board estimates, the value of purchasing subject to contract has been approximately 7% of UK GDP between 1989 and 1990 (Irish Export Board, 1990).

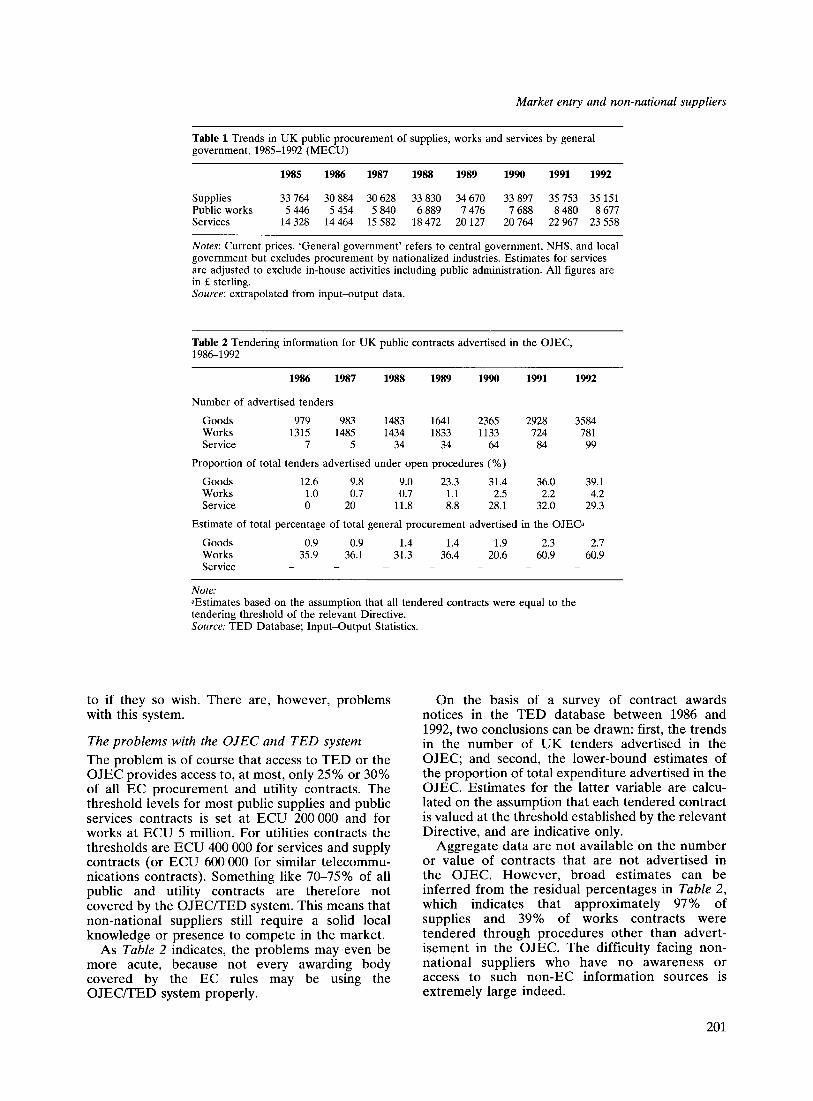

Time-series data are not published on an annual basis for the proportion of 'public sector' procure- ment of goods, works and services carried out under contract. This reflects the fact that many agencies (notably nationalized and recently privatized organizations) do not publish figures for their total purchases. However, estimates can be made of purchasing by 'general government' (central govern- ment, NHS and local authorities), which accounts for approximately 91% of total public sector procurement. Table 1 provides market trend figures extrapolated from input-output statistics for the period 1985-1992.

Despite the lack of consistent and reliable figures, these estimates indicate that supplies and services expenditure provides for the great bulk of public expenditure in the UK over the period 1985-1992. Furthermore, expenditure on services contracts has been increasing much more rapidly over the period - an almost twofold increase - when compared with supplies and works expenditure.

One might expect that the opportunities for non- national suppliers would be increasing at the same rate. The problem for such non-national suppliers, however, is that until recently there has been no ready access to reliable directories or databases on public or utility procurement contract opportunities. The Single Market rules, however, have attempted to overcome this problem by forcing all public and utility contract awarding bodies to publish their forthcoming tenders in the Official Journal of the Economic Community (OJEC). The intention here is to ensure that the data are available on line on a daily basis (the Tenders Electronic Daily (TED) system) for all potential contractors to have access

200

Market entry and non-national suppliers

Table 1 Trends in UK public procurement of supplies, works and services by general government, 1985-1992 (MECU)

1985 1986 1987 1988 1989 1990 1991 1992

Supplies 33 764 30 884 30 628 33 830 34 670 33 897 35 753 35 151 Public works 5 446 5 454 5 840 6 889 7 476 7 688 8 480 8 677 Services 14 328 14 464 15 582 18 472 20 127 20 764 22 967 23 558

Notes: Current prices. 'General government' refers to central government, NHS, and local government but excludes procurement by nationalized industries. Estimates for services are adjusted to exclude in-house activities including public administration. All figures are in £ sterling. Source: extrapolated from input-output data.

Table 2 Tendering information for UK public contracts advertised in the OJEC, 1986-1992

1986 1987 1988 1989 1990 1991 1992

Number of advertised tenders

Goods 979 983 1483 1641 2365 2928 3584 Works 1315 1485 1434 1833 1133 724 781 Service 7 5 34 34 64 84 99

Proportion of total tenders advertised under open procedures (%)

Goods 12.6 9.8 9.0 23.3 31.4 36.0 39.1 Works 1.0 0.7 0.7 1.1 2.5 2.2 4.2 Service 0 20 11.8 8.8 28.1 32.0 29.3

Estimate of total percentage of total general procurement advertised in the OJEC a

Goods 0.9 0.9 1.4 1.4 1.9 2.3 2.7 Works 35.9 36.1 31.3 36.4 20.6 60.9 60.9 Service . . . . . . .

Note." aEstimates based on the assumption that all tendered contracts were equal to the tendering threshold of the relevant Directive. Source: TED Database; Input-Output Statistics.

to if they so wish. There are, however, problems with this system.

The problems with the OJEC and TED system

The problem is of course that access to T E D or the OJEC provides access to, at most, only 25% or 30% of all EC procurement and utility contracts. The threshold levels for most public supplies and public services contracts is set at E C U 200 000 and for works at EC U 5 million. For utilities contracts the thresholds are ECU 400 000 for services and supply contracts (or ECU 600 000 for similar telecommu- nications contracts). Something like 70-75% of all public and utility contracts are therefore not covered by the OJEC/TED system. This means that non-national suppliers still require a solid local knowledge or presence to compete in the market.

As Table 2 indicates, the problems may even be more acute, because not every awarding body covered by the EC rules may be using the OJEC/TED system properly.

On the basis of a survey of contract awards notices in the T E D database between 1986 and 1992, two conclusions can be drawn: first, the trends in the number of UK tenders advertised in the OJEC; and second, the lower-bound estimates of the proport ion of total expenditure advertised in the OJEC. Estimates for the latter variable are calcu- lated on the assumption that each tendered contract is valued at the threshold established by the relevant Directive, and are indicative only.

Aggregate data are not available on the number or value of contracts that are not advert ised in the OJEC. However , broad estimates can be inferred f rom the residual percentages in Table 2, which indicates that approximately 97% of supplies and 39% of works contracts were t endered through procedures o ther than advert- isement in the OJEC. The difficulty facing non- national suppliers who have no awareness or access to such non-EC informat ion sources is extremely large indeed.

201

A Cox

The problem o f the structure o f the public and utility sectors in the UK

Another major obstacle facing non-national suppliers is a lack of knowledge of the structure of public and utility markets or their purchasing organizations. This has an impact on the availabil- ity of information, as well as on the size and number of contracts awarded. The basic structure in the UK and how this may affect market entry opportunities for non-national suppliers is described below.

Government in the United Kingdom is organized into a four-tier system. Central government ministries and departments have national responsi- bility for such areas as defence and health. The next three tiers are regional, and are made up of the local authorities at county, district and borough or parish councils levels. Major city areas have their own metropolitan district councils.

The key procurement agencies at governmental, regional and local levels are as follows:

• Central government department and agencies. Some 50 government departments procure goods and services, but 11 departments are responsible for 90% of procurement expenditure by central government. These are: Ministry of Defence; Foreign and Commonwealth Office; Ministry of Agriculture, Fisheries and Food; Department of Trade and Industry; Department of Employment; Department of Transport; Department of the Environment; Home Office and Lord Chancellor's Department; Department for Education; Department of Health; and the Department of Social Security.

• Local government. There are currently in England 47 non-metropolitan counties, 36 metropolitan districts, 334 non-metropolitan districts (outside London), and 32 London Boroughs and the City of London Corporation. In Scotland there are 9 regional, 3 island and 53 authorities. In Northern Ireland there are 9 regional boards and 26 district councils (for an overview see Watson, 1993, pp 91-103).

• The National Health Service (NHS). The admin- istration of the NHS is divided into 14 Regional Health Authorities in England, 15 Health Boards in Scotland, 9 District Health Authorities in Wales and 4 Boards in Northern Ireland.

• Nationalized industries. Despite extensive priva- tization during the 1980s a number of industries currently remain in public ownership: British Rail; the Post Office; and the Civil Aviation Authority. In addition, a number of privatized organizations are subject to EC public purchas- ing legislation under the Utilities Directive: British Telecom; British Gas and the water supply and treatment companies.

• Public agencies and corporations. This group comprises several hundred non-departmental

public bodies, including urban and rural devel- opment agencies, bodies concerned with the environment and housing, and property agencies. There are also now over 56 Next Step Agencies, which are independent hived-off bodies formerly under central government control.

Because of the process of privatization throughout the 1980s, and because many agencies do not publish annual figures for their total purchases of goods and services, it is difficult to compute the relative importance of procurement by organiza- tional type. However, approximations can be made on the basis of survey work conducted by the Irish Export Board during 1990 (see Table 3).

These figures pinpoint, immediately, one key problem area for non-national suppliers. Almost 20% of total procurement occurs through the Ministry of Defence, which is precluded under Article 223 of the Treaty of Rome from having to implement the non-discriminatory and transparent open procurement rules adopted under the Single Market initiative, when it purchases 'warlike' goods and services (Hartley and Cox, 1995). This is not to argue that non-national suppliers cannot enter the UK defence market; it simply underscores the fact that, notwithstanding recent national and EC legislative changes, national preference persists in many areas of UK procurement.

There is, however, one major advantage for non- national suppliers to the UK. If one considers the way in which procurement is actually organized in the UK it is clear that public purchasing is consid- erably more concentrated than in many of the other Member States of the European Community. This is illustrated by the number of contracting authori- ties: 700 contracting bodies in the UK compared with 1000 in Belgium, 50 000 in France and 20 000 each in Germany and Italy (European Community, 1988). The result is that the UK public contracts that are awarded by individual authorities are more likely to be above the thresholds set by the EC. Moreover, the number of awarding authorities in the UK suggests that, in principle at least, the task confronting SMEs in obtaining information on public contracts is more limited than in other

Table 3 Breakdown of UK public purchasing by organization

Organization Percentage of total public procurement

Ministry of Defence 19 Other central government 20 Central government agencies 4.6 Local government 265 NHS 11.5 Nationalized industries 8.1 Non-departmental public bodies 9.5

Source: calculated from Irish Export Board (1992)

202

Community public markets. Two trends are evident in the extent of purchas-

ing centralization in the UK since the early 1980s. On the one hand, government policy has empha- sized the devolution of purchasing and budgetary authority within organizations for low-value goods. For example, regional budget-holders in the Post Office have contracting authority for purchases under £50000. On the other hand, purchasing expertise has been centralized into professional units for higher-value contracts, including contracts let under the EC Public Procurement Directives. The high degree of purchasing concentration is illus- trated by the fact that local authorities have been developing centralized purchasing, either central- ized within individual authorities or through free- standing consortia owned by a number of authorities. This approach has been adopted to exploit the potential for scale economies and as a mechanism to rationalize procurement.

In the NHS a Procurement Directorate coordi- nates work by procurement units within the NHS regions, and individual contracts are placed by specialist contracting organizations at the regional level. The individual regions specialize and place contracts for the whole country in particular commodities and services. More recently, however, the development of hospital trusts has led to greater fragmentation. Finally, in the nationalized indus- tries, British Rail and British Coal established professional purchasing units. British Rail's procure- ment unit, for example, historically let approxi- mately 70% by value of all contracts. These trends have, however, been undermined by the recent pfivatization measures for these industries.

On the basis of this survey two observations emerge about the structure of purchasing as it relates to market opportunities for non-national suppliers. On the one hand, purchasing for high- value and core supplies, works and services tends to be centralized in the individual purchasing organi- zations making up the UK public sector. On the other hand, contracts for low-value goods and non- core equipment and works are delegated to regional or lower-level purchasing points within these organi- zations. Contracts opportunities for SMEs are likely to fall into this latter category, with only larger companies able to win large prime contracts and able to benefit from the more accessible information available through the OJEC/TED systems. This means that the more centralized nature of UK procurement may benefit only larger firms and not SMEs, whose natural contract size will be in smaller lots, which are below EC threshold levels.

National preference schemes and partnership relationships in the UK

There is no direct evidence that procurement agencies in the UK employ policies that overtly favour domestic suppliers on the grounds of

Market entry and non-national suppliers

supporting regional or national employment. Whilst a number of authorities have operated like this in the past, value-for-money considerations appear to have replaced political and employment considera- tions in contractor selection in the 1980s and 1990s. The current policy throughout the public sector is summarized in a recent NHS document (NHS, 1993):

Fair and open competition between prospective suppliers for NHS contracts is a requirement of Standing Orders and of EC Directive on Public Purchasing for Works and Supplies. This means that:

* no private, public or voluntary organization or company which may bid for NHS business should be given any advantage over its competi- tors...

• each new contract should be awarded solely on merit, taking into account the requirements of the NHS and the ability of the contractors to fulfil them.

However, Government Contract Preference Schemes have allowed firms in Development Areas - special development zones or any part of Northern Ireland - to obtain preferential consideration, under certain circumstances, for contracts from govern- ment departments.

Despite the general theoretical evidence of market openness, in practice current trends in UK procurement are against adversarial, open and competitive supply chains in favour of a smaller supplier base and more long-term, partnership relationships. This trend has created a potential problem for new market entrants - especially non- nationals - because most professional purchasing officers are proactively seeking to reduce their supply base and to emphasize quality and life cycle over initial cost considerations.

Research therefore indicates differences in style between individual public sector organizations in their approach towards the supplier base. As a result, two general observations emerge:

* Procurement authorities have no specific policy about the length of contractual relations with suppliers for low-value goods and supplies that are not considered essential for the operation of the purchasing organization. In general, such procurement is conducted against value-for- money criteria, and is subject to periodic compe- tition. This approach affects the majority of purchases below the EC Directive thresholds. This may be the area in which non-national suppliers will have the greatest opportunity to compete in future, but the greatest difficulty in obtaining relevant information cheaply.

• A number of organizations, notably the nation- alized and private sector industries, indicate that they have adopted, or intend to adopt, the

203

A Cox

approach of maintaining stable and longer-term 'competitive partnerships' with the supplier base for core equipment (British Rail for rolling stock and signals equipment; the Post Office for high- value communications equipment). This strategy is based on periodic competition between a small number of prequalified suppliers, both domestic or foreign, using competition proce- dures compatible with the main provisions of the Utilities Directive.

Overall, however, despite these tendencies, the relationship between the public sector and its supplier base has not changed radically since the introduction of the new EC Directives. This reflects the fact that the basic tenets of EC competition policy have already been incorporated into domes- tic purchasing practices and legislation. For example, tendering and contracting procedures for local authority works and services under the 1980 Local Government Planning and Land Act and the 1988 Local Government Act include provisions broadly similar to the EC procurement regime. The EC regulations can thus be seen as an extension to purchasing practices already adopted extensively throughout the UK public sector.

The net result of all of this appears to be that UK public purchasing emphasizes the selection of the 'most economically advantageous', rather than necessarily the lowest-cost tender. These trends seem to reinforce preferred supplier relationships, rather than open tendering, for many of the contracts affected by EC threshold levels.

Vertical integration and in-house services A general entry barrier to obtaining public sector contracts is the degree of vertical integration within public sector and utility organizations. For example, many professional services that in principle could be undertaken by the private sector are conducted in house (eg accountancy, personnel recruitment). However, the processes of market testing and privatization have alleviated this problem as public sector activities have been contracted increasingly with the private sector. Market opportunities for the private sector are likely to be more extensive in the UK than in other Member States in the Community as a result. Despite this, there are a number of additional problems facing non-national suppliers.

Obtaining appropriate standards and technical specifications In the context of the purchasing criteria adopted by UK public purchasers, the achievement of defined standards is an essential prerequisite in bidding for contracts. The general standards currently adopted for tendering organizations are BS 5750, equivalent to the ISO 9000 series. Moreover, in addition to company accreditation, subcontracted products may

204

also be required to confirm to British technical standards or their European equivalent.

Many public purchasers also maintain lists of approved firms that have achieved the necessary standard, and inclusion on the list may be a pre- requisite for bidding. A number of supply-side organizations indicate that market entry is expen- sive for non-national SMEs because of the need for annual accreditation in particular. As part of the selection criteria, public organizations also require details concerning the financial viability of compa- nies. This factor may also have the effect of discrim- inating against SMEs. It must also be recognized that tendering for UK public contracts imposes a number of costs on potential suppliers. These include costs of certification, the costs of purchasing tender documentation, and the costs of formulating bids. These transaction costs have been estimated to be 10% of total contract value. The cost and risks of an unsuccessful bid must clearly have acted as deterrents for many non-national firms seeking business with the UK public sector.

Sunk costs and equipment compatibility As the Costs of Non-Europe research demonstrated, public procurement expenditure has been concen- trated on a number of specific industries and product groups. In many of these industries, for example railway equipment, the technical charac- teristics of existing equipment act as a potential barrier to firms operating from a home country with differing standards (Atkins, 1988).

Repair and servicing arrangement UK purchasing authorities emphasize equipment reliability and maintenance in procurement decisions. In this context the availability and speed with which equipment is maintained may be of paramount importance. Consequently, contractors based in other states may be unsuccessful in tender- ing for certain contracts on the grounds of potential response times.

Foreign exchange risk and cost The extent to which these factors constitute a barrier to foreign firms will vary on a contract-by- contract basis. However, some authorities indicate that the possible effects of exchange rates, particu- larly on longer-term contracts, may militate against firms based in other states.

Quality, qualifications and safety standards While in the UK international standards have been adopted in accordance with EC public procurement legislation, the standards adopted in other states in some industries has been identified as a potential barrier to market entry for foreign firms. In the case of railway equipment, for example, specific British safety standards (which are not in force in other

states) may have the effect of ruling out bids for certain categories of equipment. The Association of British Pharmaceutical Industries has indicated that UK certification requirements for drugs are a poten- tial barrier to non-national firms. In addition, in the process of gaining accreditation, foreign firms are likely to incur greater costs than domestic firms in obtaining information on standards specific to the UK public market.

Ease o f legal recourse to the supplier

The fact that non-national firms may operate outside the UK legal framework, and would thus be more difficult to pursue in respect of inadequate performance, may also be a possible barrier to market entry for non-national suppliers.

Shortage o f language skills, particularly in technical areas

The need to translate technical standards from English to other languages often causes confusion and inaccuracy. In addition foreign firms, particu- larly SMEs, are likely to encounter problems in tendering if they do not have in-house personnel with the necessary language skills.

What can be done to assist market entry for non-national firms?

The analysis above suggests that, despite the intro- duction of new EC and national legislation, a number of barriers may still limit the ability of non- national firms to obtain UK public sector and utility contracts. Whilst formal barriers have been removed, problems in gaining market information and meeting the required technical standards may still result in barriers for non-national firms, and SMEs in particular. This raises the question of what can be done to alleviate these problems because, if foreign firms are experiencing problems entering the UK market, UK firms will be facing similar problems in other EC markets. Possible strategies to overcome these barriers are discussed below.

Two main methods of direct exporting exist for foreign firms to enter UK public and utility markets. First, non-national firms can compete for contracts tendered through the OJEC and under EC public purchasing legislation. Second, opportunities exist for submitting tenders for contracts that are advert- ised by UK authorities but which are not regulated by the EC Directives. Under the existing Directive thresholds it is likely that SMEs will have to consider both approaches to obtain UK public contracts.

The analysis presented here suggests that three basic preconditions should be met by foreign firms wishing to enter the UK market:

• First, the firms must have obtained the requisite British Standard (BS 5750) or the international equivalent (ISO 9000).

Market entry and non-national suppliers

• Second, particularly for contracts tendered under restricted procedures, the firm should have obtained inclusion on select tendering lists.

• Third, for contracts tendered under open proce- dures, non-national suppliers will be required to provide detailed financial information about their company.

In addition to responses to advertisements in the OJEC, a number of 'direct' and 'indirect' methods exist for foreign companies to enter UK public procurement markets. Mechanisms of market entry can be summarized as follows.

Direct strategies

• Direct sales. This strategy involves competing for contracts advertised by the UK public sector in sources other than the OJEC. For this approach to be successful, information is necessary on contract opportunities, which may be advertised at a local level.

• Foreign marketing agency. This strategy involves the employment of specialist companies in the UK to market foreign products in the UK public market.

• Merger~acquisition. The takeover of an existing UK company provides a further mechanism for public markets. Evidence suggests that foreign direct investment has been adopted by larger enterprises, and that considerable success has been achieved in entering public procurement markets (eg pharmaceuticals).

• Direct marketing. Attendance at conferences and trade fairs may be a useful approach for foreign firms to adopt in alerting public organizations to their product base.

Indirect strategies

• Wholesaler. Public sector organizations purchase a range of lower-value goods (eg stationery) through domestically based wholesalers. Consequently, export of goods to UK-based wholesalers provides a mechanism for foreign firms to enter both UK public and private sector markets simultaneously, without the require- ment to invest in extensive market research.

• Agents. A number of organizations have indicated that market entry by non-national firms may be considerably enhanced by employ- ing specialist agents with detailed knowledge of UK public contracting opportunities.

• Licensing. This approach may be an optimum market penetration strategy for small firms with new products but limited resources to bid for public contracts directly. Choice of licensee will depend upon selecting firms with established links and expertise in bidding for UK public contracts.

• Joint production. This involves work-sharing arrangements with a firm based in the UK. This

205

A Cox

strategy enables the partners to compete for public contracts in both countries and reduces the costs of acquiring market information for each partner. Assembly o f products in the host country. Whilst this approach may not be of direct relevance to SMEs, foreign direct investment has been adopted by large foreign companies (eg motor vehicle sector) to access UK public and private markets. Supply of components and subcontract work. Extensive opportunities exist for non-national firms to operate as subcontractors to companies in receipt of UK public contracts. Subcontractors may be required to operate according to defined standards (eg ISO 9000 series). Information on subcontract opportunities is available using published directories such as the European Procurement Directory and the European Utilities Procurement Directory (Earlsgate Press, 1995a, b).

Conclusions Public procurement in the UK is significant and relatively centralized in comparison with many other EC states. The market for public goods and services is relatively open, and current government policy is to extend competition and private sector provision to a wider range of activities, which have traditionally been conducted in house. These obser- vations, in conjunction with broader procurement policies emphasizing value for money, suggest that, in theory, there are considerable opportunities for foreign firms to obtain UK public contracts.

This analysis suggests, however, that a number of barriers exist and that initiatives need to be adopted to support non-national firms attempting to enter the UK public market. The main recommendations are as follows.

A major problem confronting foreign firms attempting to enter UK public markets concerns information about contracting opportunities, and the scope for collaboration with existing UK suppli- ers to the public sector. To obtain relevant infor- mation, measures can be taken to ensure that foreign firms have adequate access to EC-wide information sources within their home country. Examples here include access to the TED system, the EC Business Cooperation Network (BC-Net), the Europartneriat and the European Economic Interest Grouping.

The foregoing analysis suggests that extensive market opportunities exist for non-UK firms that are not regulated by the EC Directives. Enhancing market entry could be achieved by:

• The provision of professional consultancy help to manufacturing and service businesses. In the UK for example, the Department of Trade and Industry provides confidential guidance and

206

advice through independent consultants in key management areas including business planning, design, financial and management information and marketing and quality. This policy approach is designed to enable firms, especially SMEs, to locate market opportunities without incurring the costs of extensive market research. A similar approach, using advisors with expertise of UK public purchasing, could enhance market entry for foreign firms, particularly in relation to contracts falling below the threshold of the EC Public Procurement Directives. The establishment of specialized information centres. Many public organizations produce publications outlining market opportunities and contact points for potential suppliers. In addition, information is produced on the techni- cal standards, safety standards and contractor selection criteria that they employ in contracting. Finally, public authorities often indicate that speculative approaches are welcomed from potential suppliers seeking business with the authority. These findings suggest a role for national information centres, supplementing the existing European information centres, with relevant documentation and contact information for UK public purchasing bodies.

In the absence of this more proactive approach by intermediary institutions like the EC and national governments, it is difficult to see how many of the continuing barriers to non-national market entry outlined here can be overcome. In the end, however, even these initiatives will be stillborn unless suppliers pursue overseas market share. Legislation and information on its own cannot force either suppliers or purchasers to interact. They must decide to do this for themselves by behaving proact- ively.

Acknowledgement The author would like to thank Matthew Uttley, Centre for Defence Economics, University of York, for research assistance in the preparation of this paper.

References Atkins, W S (1988) The Costs o f Non-Europe in Public Sector

Procurement European Commission, Brussels Buigues, P, Ilzkovitz, F and Lebrun, J-F (1990) The Impact o f the

Internal Market by Industrial Sector: the Challenge for the Member States Commission of the European Communities, Belgium

Cox, A (1993) Public Procurement in the EC. Vol 1: The Single Market Rules and the Enforcement Regime After 1992 Earlsgate Press, Boston

Earlsgate Press (1995) The European Procurement Directory Earlsgate Press, Boston

Earlsgate Press (1995) The European Utilities Procurement Directory Earlsgate Press, Boston

Market entry and non-national suppliers

EC (1989) Public Procurement in the Excluded Sectors, Bulletin of the European Communities Supplement 6/88, Commission of the European Communities, Brussels

Hartley, K and Cox, A (1995) The Costs of Non-Europe in Defence Procurement European Commission, Brussels (forth- coming)

Hartley, K and Uttley, M R H (1994) 'The Single European Market and public procurement policy: the case of the United Kingdom' Public Procurement Law Review 4 114-125

Irish Export Board (1990) Guide to Public Procurement: United Kingdom Irish Export Board, Dublin

NHS Management Executive (1993) Standards of Business Conduct for NHS Staff

OECD (1990) OECD Economic Surveys: United Kingdom OECD, Paris

O'Brien, G (1993) 'Public procurement and the small or medium enterprise' Public Procurement Law Review 2 82-92

SEMA Group (1992) Study on SME Participation in Public Procurement Brussels

Watson, G (1993) Intergovernmental Relations in the Member States of the European Community: A Bibliographical Study Guide Earlsgate Press, Boston

207