market dynamics in india - consumer trends and momentum

DESCRIPTION

Market DynamicsTRANSCRIPT

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

June 2015

© Euromonitor International

2

With a total GDP of Rs125 trillion (US$2.0 trillion) in

2014, India stood as the ninth largest economy

globally. Average annual real GDP growth of 7.0%

between 2000-2014 surpassed the global average of

3.8% and the Asia Pacific average of 6.3% over the

same period. Robust growth reflects strong and rising

levels of domestic consumption, export

competitiveness and high government spending.

In purchasing power parity (PPP) terms, India

overtook Japan in 2006 to become the third largest

economy globally, after China and the US, implying

that Indian consumers have far better capacity to

acquire goods than their Japanese counterparts.

The country offers both growth and volume

advantages to businesses, as its forecast annual real

GDP growth of 5.8% over 2015-2030 will be the

highest among the 10 biggest markets globally. Its

expected total GDP of US$8.8 trillion by 2030 will

make it the world's third largest economy globally, in

US$ terms - more than the expected sizes of Brazil

and Russia combined.

0

2

4

6

8

10

12

India China Brazil Russia

% r

eal

GD

P C

AG

R

Real GDP % CAGR 2000-2014 and 2015-2030

2000-2014 2015-2030

0 10,000 20,000 30,000 40,000 50,000 60,000

Russia

Brazil

Japan

Indonesia

India

US

China

US$ billion

Total GDP in PPP Terms 2030

Russia Brazil Japan Indonesia India US China

India now world's third largest economy in PPP terms

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

© Euromonitor International

3

0 50,000 100,000 150,000

Brazil

Russia

Indonesia

US

India

China

Middle-class households (‘000)

Number of Middle-Class Households 2014/2030

2014 2030

0 25 50 75 100

Hi-Fi Stereo

Internet-Enabled…

Personal Computer

Refrigerator

Motorcycle

Cable TV

Bicycle

Cooker

Colour TV Set

Mobile Telephone

% households

Top 10 Consumer Durables in India(% Households) 2014/2030

2014 2030

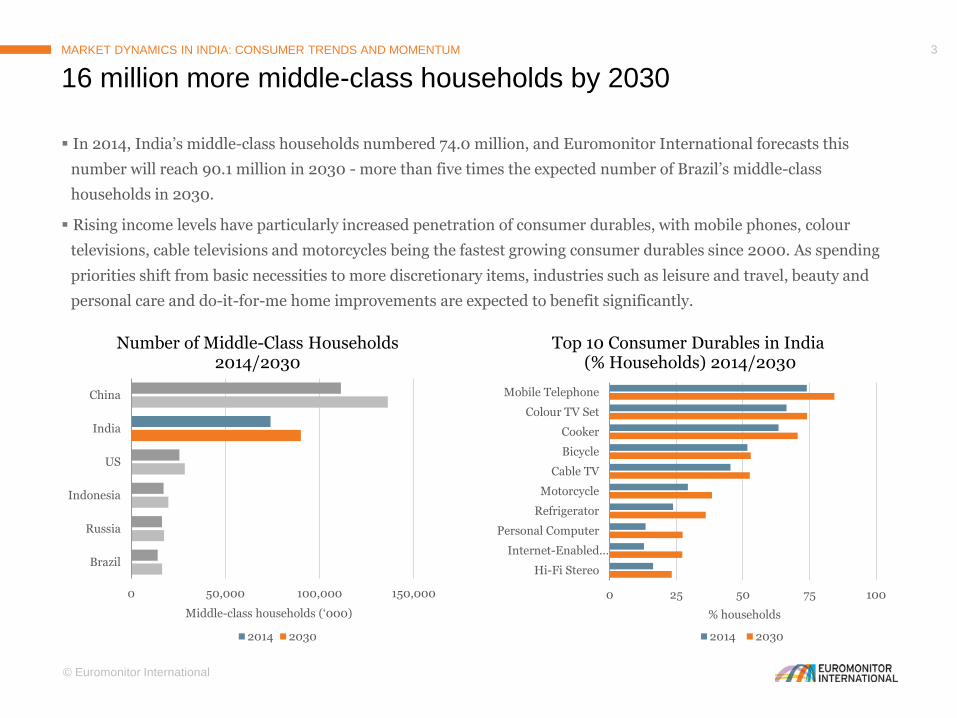

In 2014, India’s middle-class households numbered 74.0 million, and Euromonitor International forecasts this

number will reach 90.1 million in 2030 - more than five times the expected number of Brazil’s middle-class

households in 2030.

Rising income levels have particularly increased penetration of consumer durables, with mobile phones, colour

televisions, cable televisions and motorcycles being the fastest growing consumer durables since 2000. As spending

priorities shift from basic necessities to more discretionary items, industries such as leisure and travel, beauty and

personal care and do-it-for-me home improvements are expected to benefit significantly.

16 million more middle-class households by 2030

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

© Euromonitor International

4

Discretionary spending is expenditure by consumers or

households on consumer categories such as transport,

leisure and eating-out, other than that of essentials such

as food and non-alcoholic beverages and housing.

The shifting priorities of the Indian middle class are

evident in the shift in spending habits. Consumers are

now moving beyond the basic necessities.

As the modernisation of India’s agricultural sector will

create more efficient food supply chains thereby reducing

grocery prices, spending on necessities is expected to fall.

Rising incomes will increase consumers’ appetite for

discretionary spending. This spending capacity is

improving for rich, middle-class and poorer Indian

households alike.

In 2014, discretionary spending absorbed 41% of the

overall budgets of low-income Indian households (decile

1). This category attracted 55% of the total outgoings of

middle-income homes (decile 5) that year and 67% of the

total expenditure of high-income households (decile 10).

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2014 2030

Va

lue

sha

re

Share of Wallet by Category 2000/2014/2030

Discretionary spending

Spending on food and non-alcoholic beverages and housing

Share of wallet shifts towards discretionary spending

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

© Euromonitor International

5

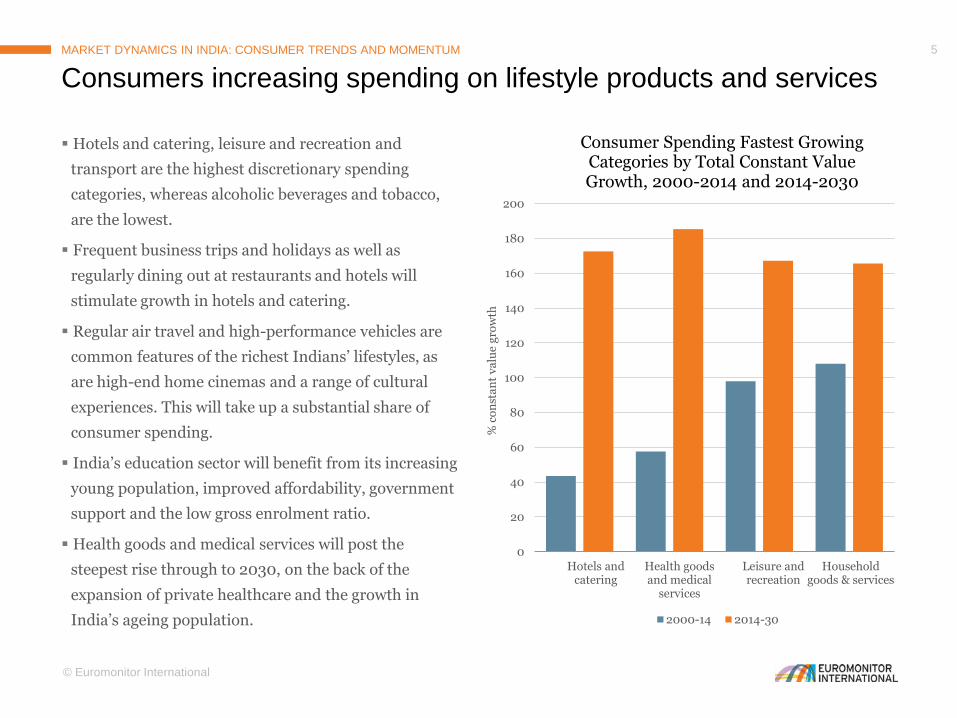

Hotels and catering, leisure and recreation and

transport are the highest discretionary spending

categories, whereas alcoholic beverages and tobacco,

are the lowest.

Frequent business trips and holidays as well as

regularly dining out at restaurants and hotels will

stimulate growth in hotels and catering.

Regular air travel and high-performance vehicles are

common features of the richest Indians’ lifestyles, as

are high-end home cinemas and a range of cultural

experiences. This will take up a substantial share of

consumer spending.

India’s education sector will benefit from its increasing

young population, improved affordability, government

support and the low gross enrolment ratio.

Health goods and medical services will post the

steepest rise through to 2030, on the back of the

expansion of private healthcare and the growth in

India’s ageing population.

0

20

40

60

80

100

120

140

160

180

200

Hotels andcatering

Health goodsand medical

services

Leisure andrecreation

Householdgoods & services

% c

on

sta

nt

va

lue

gro

wth

Consumer Spending Fastest Growing Categories by Total Constant Value Growth, 2000-2014 and 2014-2030

2000-14 2014-30

Consumers increasing spending on lifestyle products and services

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

© Euromonitor International

6

So who are these consumers?

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

How are Indian consumers distributed across our five consumer types?

• Ambitious

• Tech-savvy

• Capable

• Self-assured

Undaunted Striver (16%)

“I want to be and have the best.”

• Busy

• Confident

• Image-conscious

• Status-driven

Restless Spender (16%)

“My life is hectic but exciting.”

• Cautious

• Moderate

• Balance-seeking

• Frugal

Prudent Pragmatist (23%)

“I think carefully before making decisions.”

• Family-orientated

• Guarded

• Ambivalent

• Modest

Humble Homebody (21%)

“Family matters most to me.”

• Content

• Independent

• Minimalistic

• Comfortable

Secure Traditionalist (24%)

“I do not need much to be happy”

© Euromonitor International

7

Consumers contributing the most to discretionary spending

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

Undaunted Strivers and Restless Spenders both earn high incomes, prefer to buy brand names and enjoy shopping.

Undaunted Strivers and Restless Spenders are the most tech-savvy groups. Both are highly active online and on social media and make sure they purchase the latest technology.

Who enjoys shopping? Who spends their money on brand names and luxury products? Who is the technophile?

Share of Population 2011

Undaunted Striverand Restless

Spender32%

Prudent Pragmatist, Secure Traditionalist and

Humble Homebody68%

© Euromonitor International

8

Rapid urbanisation, rising disposable incomes and less

spare time for urban working couples are supporting

demand for prepared meals, which are more convenient

and increasingly becoming a part of their daily lives.

This has raised demand for packaged food, which is

seeing faster year-on-year volume growth than fresh

food.

The average age of first marriage will increase by around

two years for both men and women over 2012-2030;

from 24.5 to 26.5 years for men and from 18.9 to 21.0

years for women.

This will widen the window of opportunity for packaged

food manufacturers, as according to Euromonitor

International’s Global Consumer Trends survey, the 20-

29 years age group is the biggest contributor to ready

meals sales in India.

These unmarried singles prefer packaged food over fresh

food because of its convenience in terms of preparation

time.

Ready meals and snack bars will see tremendous growth

exceeding overall packaged food growth over the forecast

period.

0

2

4

6

8

10

12

14

16

18

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65+

% s

ha

re

Age (years)

Age Group Purchasing Ready Meals for Own Consumption on Weekly Basis in 2011

Packaged food appeals to time-starved consumers

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

0

200

400

600

800

1,000

1,200

2009 2012 2015 2018

Ind

ex 2

00

9=

100

Packaged Food: Retail Growth Indices by Selected Category 2009-2019

Ready Meals Snack Bars Packaged Food

© Euromonitor International

9

However, convenience, faster-paced lives and

lifestyle changes are impacting health, body and

mind and potentially becoming a cause of many

chronic and cardiovascular diseases.

India is witnessing a rising obesity trend. With

growing urbanisation incomes its citizens are

becoming obese. The overweight population is

expected to reach 23% of the total population by

2030.

Among the reasons for the growing number of

diabetes and obesity cases is an increasing

tendency towards sedentary lifestyles that have

accompanied growing economic prosperity, as

well as genetic predisposition in a country

already known for its sweet tooth.

In 2015, India has an estimated 77.0 million

pre-diabetics, a precursor to Type 2, the most

common type of the disease. The majority of

diabetes cases are in southern India and the

metros.

Changing lifestyles taking their toll…

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

50,000

70,000

90,000

110,000

130,000

150,000

170,000

2000 2005 2010 2015 2020 2025 2030

Num

be

r o

f p

eo

ple

Number of Diabetic Patients (Aged 20-79 Years) 2000-2030

Number of Diabetic Patients (Aged 20-79 Years)

5

10

15

20

25

2000 2005 2010 2015 2020 2025 2030

Pe

rce

nta

ge

of

ove

rall

po

pu

latio

n

Diabetic Prevalence and Overweight Population 2000-2030

% Population Aged 20-79 Years - Diabetes Prevalence

% Population Aged 15+ Years - Overweight Population (BMI 25-30kg/sq m)

© Euromonitor International

10

India is now one of the world’s most dynamic

markets for weight management products. While

higher-end options, such as custom-made weight

loss programmes, are starting to make inroads,

the market for lower-priced weight management

products, such as better for you reduced fat or

reduced sugar offerings, requires significant

development.

According to Euromonitor International’s Global

Consumer Trends survey, a large majority of

Indian respondents expressed the high

importance of physical exercise in terms of

wellbeing.

While India has not fully adopted the “cult of thinness”,

there is certainly pressure to be slim and this promotes

growth of weight management products.

The strong growth of weight management has been

driven by the emergence of a consumer type that

Euromonitor refers to as the “undaunted striver.”

“Undaunted strivers” are also highly likely to go to the

gym, and therefore consume protein supplements and

sports nutrition.

…and driving strong growth in health and wellness products

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

0

20

40

60

India China US UK Japan France Germany Russia

Per

cen

tag

e

Survey 2013 :When thinking about health, how important is regular exercise to you?

Very Important ImportantNeither Important nor Unimportant UnimportantNot at all Important

3

5

7

9

11

13

15

17

2014-2015 2015-2016 2016-2017 2017-2018 2018-2019

% v

alu

e g

row

th

Weight Management vs Consumer Health: Forecast Value Growth 2014-2019

Consumer Health Weight Management

Weight Loss Supplements

© Euromonitor International

11

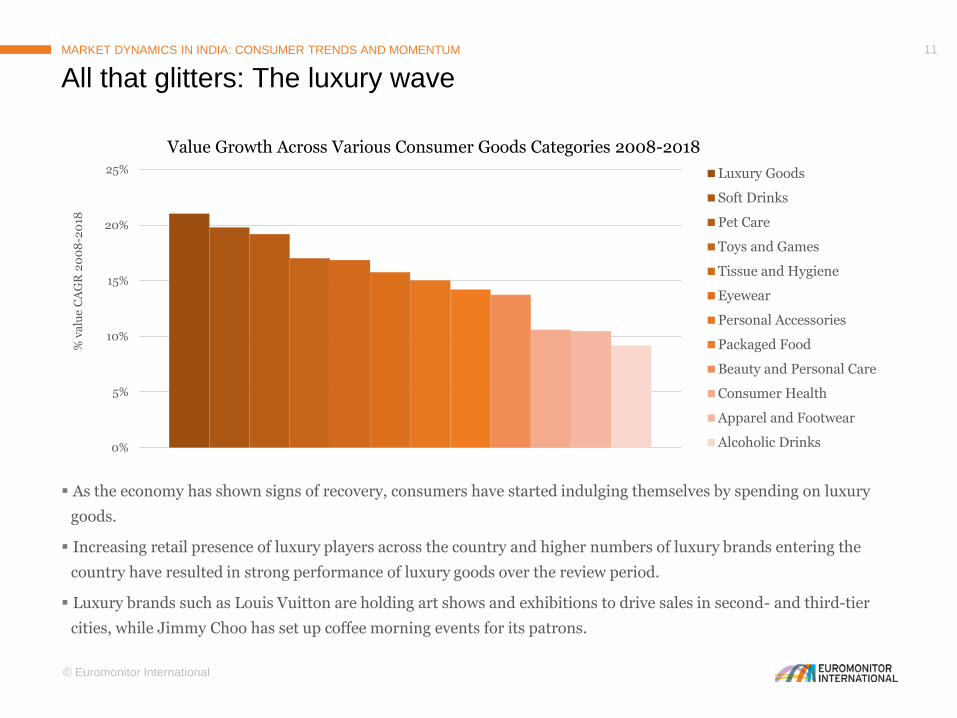

As the economy has shown signs of recovery, consumers have started indulging themselves by spending on luxury

goods.

Increasing retail presence of luxury players across the country and higher numbers of luxury brands entering the

country have resulted in strong performance of luxury goods over the review period.

Luxury brands such as Louis Vuitton are holding art shows and exhibitions to drive sales in second- and third-tier

cities, while Jimmy Choo has set up coffee morning events for its patrons.

All that glitters: The luxury wave

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

0%

5%

10%

15%

20%

25%

% v

alu

e C

AG

R 2

00

8-2

018

Value Growth Across Various Consumer Goods Categories 2008-2018

Luxury Goods

Soft Drinks

Pet Care

Toys and Games

Tissue and Hygiene

Eyewear

Personal Accessories

Packaged Food

Beauty and Personal Care

Consumer Health

Apparel and Footwear

Alcoholic Drinks

© Euromonitor International

12

In 2014, India’s savings ratio stood at 31% of total disposable

income - ranking the third highest globally, after China’s 39%

and Iran’s 33%. Indian consumers’ saving and wealth

accumulation patterns are largely influenced by the country’s

social and cultural traits, where debt is typically perceived as

an avoidable luxury.

Family-orientated Indian consumers direct a significant

proportion of their savings towards acquiring physical assets

such as real estate and gold over their working lives. Both of

these are seen as secure investments and contribute towards

improving their social status.

0 10 20 30 40 50

Hong Kong

Singapore

India

Iran

China

% disposable income

Countries with Highest Savings Ratios 2014

Hong Kong Singapore India Iran China

0%

20%

40%

60%

80%

100%

1990 1995 2000 2005 2010 2011 2012 2013 2014 2015 2016 2020 2025 2030

Sh

are

of a

nn

ua

l d

isp

osa

ble

in

co

me

pe

r ca

pita

Consumer Savings and Expenditure as Share of Annual Disposable Income per Capita 1990-2030

Consumer Expenditure Annual Savings

The Indian consumer is not just about spending…

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

© Euromonitor International

13

A significant proportion of total household savings in

India are directed towards home purchases, as the

penetration of mortgage products in India remains

low.

Indeed, some 93% of homeowners in India in 2014

did not have a mortgage. This is significantly higher

than China (77% in 2014) and the Asia Pacific

average of 84% in the same year.

Home Ownership by Tenure (‘000) 2014

Home Owners Without Mortgage

Home Owners With Mortgage

Rented

Others

-10

0

10

20

30

0

5

10

15

20

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

% y

-o-y

gro

wth

% y

-o-y

gro

wth

Real Jewellery vs Annual Savings:% Y-o-Y Growth 2000-2018

Real Jewellery - Retail Value RSP Annual Savings

A constant value CAGR of 7% in India’s annual

savings over 2000-2014 has led to an 11% constant

value CAGR in retail sales of real jewellery. Real

jewellery is not only considered a personal accessory

in India, but is also valued as a secure investment.

The personal accessories category therefore

registered the second highest retail value sales after

apparel and footwear in India in 2014.

Gold connection JEWELLERY: Dual commodity

“Real” purchaseHOME OWNERSHIP: An outright purchase

Gold and real estate remain top priorities among savers

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

© Euromonitor International

14

India’s urban landscape will be primarily defined by 41

major cities that will surpass one million in population by

2025. These cities will drive demand for products and

services.

Per capita income levels in these 41 cities will be

significantly higher. Approximately 36% of households

with over US$15K in disposable income will be from these

cities while only 13% of India’s total population will live in

these 41 cities.

The population of six mega cities will surpass 10 million by

2025.

Over 1/3rd of India’s richest households will reside in 41 major cities

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

Population and Disposable Income Split 2025

HyderabadBangalore

Chennai

Mumbai

Delhi

Megacities: Cities with

population >10 million

Megacities,2025

Kolkata

Dhanbad Patna Jaipur

Amritsar Bhopal Pune

Allahabad Thriruvanthapuram Surat

Asansol Thrissur Ahmedabad

Jabalpur Malappuram Nasik

Jamshedpur Kozhikode Visakhapatnam

Varanasi Coimbatore Vadodara

Madurai Nagpur Kannur

Meerut Kochi Agra

Ludhiana Indore Ghaziabad

Faridabad Kanpur Lucknow

Rajkot Vijayawada

Cities with population between 1 and 10 million by 2025

Outer circle: Population

Inner circle: Disposable Income

© Euromonitor International

15

The prominent urban regions of India are

expected to be connected by “urban corridor”

projects linking Indian megacities across the

country

The current largest corridor under development -

the Delhi-Mumbai Industrial Corridor - at a cost

of US$90 billion - will be the largest

infrastructure project in India's history. This will

be a 920 mile dedicated freight corridor and will

feature dozens of brand new cities along with new

ports and airports. It is designed to cut the

logistical costs of manufacturing goods, making

India a global manufacturing hub.

Another such project under consideration is a

new industrial corridor between Mumbai and

Bangalore.

However, such developments are expected to

present complex social concerns such as issues of

huge land acquisition.

Another obstacle that might lead to delay is

India’s complex bureaucracy. There is also an

urgent need to focus on social developments along

the corridors between cities.

The rise of the “mega region”

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

Major Industrial Corridors in India by 2025

Delhi-Mumbai

Mumbai-Nagpur

Hyderabad-Hindupur

Srikakulam-NelloreBangalore-Belgaum

Mehsana-Valsa

© Euromonitor International

16

While the proportion of the rural population has been falling over the last two decades, India remains a

predominantly rural country with over 66% of households still living in rural areas.

A model for rural development called "rurbanisation" has been adopted that has focused on providing all the civic

and infrastructure facilities available in big towns and cities to arrest migration. This has the potential to raise rural

prosperity and bring down the burden on large cities and towns facing overcrowding.

This process has accelerated the convergence in consumer habits between urban and rural India. In fact, packaged

food consumption is rising faster in rural areas than in cities. There is likely to be an acceleration in the

“rurbanisation” trend, making rural and urban India more homogeneous in terms of consumer behaviour, while the

differences that exist within individual cities are expected to increase.

Yet India’s “soul” remains in its villages

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

0

5

10

15

20

25

30

65%

66%

67%

68%

69%

70%

71%

72%

73%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Sh

are

of

pa

cka

ge

foo

d

va

lue

sale

s in

ru

ral

are

as

Sh

are

of

rura

l p

op

ula

tio

n

Rural Population vs. Sales of Packaged Food in Rural Areas 2000-2014

Share of Rural Population in Total Population Share of Packaged food in Rural areas

© Euromonitor International

17

Traditional retailers such as kiranas (local independent retailers),

haats (open markets) and melas (fairs) play a vital role in the

distribution of many goods in India.

Although the share of traditional retailers has declined slightly, the

majority of packaged food in India is sold through kiranas, hence

having a solid presence in this channel is key to success.

The majority of Indians, particularly in rural areas, lack access to

modern retailing formats and still shop in them because kiranas

give credit and are prepared to deliver even the smallest orders.

Correspondingly, companies need to design strategies that meet the

needs of the rural population and are designing new products and

tools to tap into the rural market.

An interesting example is “Project Shakti” launched by Unilever in

2000. Unilever focused on empowering women, known as Shakti

Ammas, who act as distributors and brand-builders for Unilever.

Similarly, packaging is an area of key focus for manufacturers.

Small pack sizes help boost sales in impulse categories, such as

sweet and savoury snacks and confectionery, and flexible packaging

improves the affordability of such products.

Focus on traditional channels key to success in rural markets

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

Courtesy of Hindustan Unilever Ltd

Packaged Food Distribution Breakdown 2014

Other GroceryRetailers

TraditionalGrocery Retailers

© Euromonitor International

18

According to the latest survey on future spending priorities conducted by Euromonitor International in 2014, a large

majority of respondents under the age of 45 expressed an intention to increase their spending on new technology.

Indian men, in particular, are eager to increase their technology purchases, making them a prime target for

companies seeking to grow their technology sales.

Interestingly, even low-income Indian men are increasing spending - close to half of Indian male respondents under

24 who earn less than US$2,500 a year and over half of those earning between US$2,500 and US$10,000 a year plan

to increase their spending on new technology.

Young consumers plan to further increase tech spending

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

0

5

10

15

20

25

30

35

40

45

50

55

15-29 30-44 45-59 60+ All demographics

% o

f re

spo

nd

ents

Interest in Spending on New Technologies, 2013

Source: Euromonitor International consumer survey, GCT Survey 2013

Note: Showing percentage of respondents who indicated that they were interested in spending ion new technologies

© Euromonitor International

19

Despite India’s huge growth potential, India’s

tough business environment remains a major

discouragement for investors.

The dearth of investments and slow regulatory

approvals have led to unstable electricity supply,

inadequate transport networks in cities and rural

areas and low mobile telephone and internet

penetration rates. Meanwhile, complex regulatory

frameworks, stringent red tape, lack of

governance and rigid labour market result in

higher costs for businesses.

In the World Bank’s Ease of Doing Business

(Doing Business) 2015 report, India ranked

142nd out of 189 countries, as businesses struggle

with the country’s complex start-up procedures,

relatively high taxes, difficulties in obtaining

electricity connection and construction permits

and enforcing contracts. At 142nd, India lags

behind many of its Asia Pacific counterparts,

notably China (90th), Indonesia (114th) as well as

Pakistan (128th).

0 50 100 150 200

Protecting Minority Investors

Getting Credit

Registering Property

Trading Across Borders

Getting Electricity

Resolving Insolvency

Paying Taxes

Starting a Business

Dealing with Construction Permits

Enforcing Contracts

India’s Ranking in Doing Business Index 2015

Out of 189 Countries

Despite reforms, business environment remains difficult

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

© Euromonitor International

20

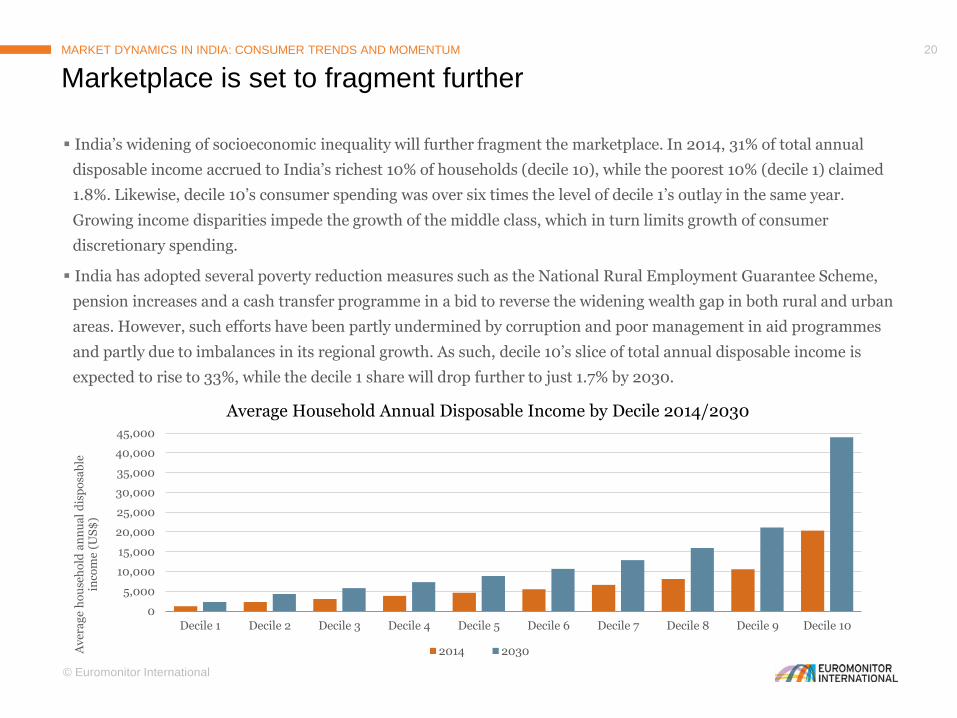

India’s widening of socioeconomic inequality will further fragment the marketplace. In 2014, 31% of total annual

disposable income accrued to India’s richest 10% of households (decile 10), while the poorest 10% (decile 1) claimed

1.8%. Likewise, decile 10’s consumer spending was over six times the level of decile 1’s outlay in the same year.

Growing income disparities impede the growth of the middle class, which in turn limits growth of consumer

discretionary spending.

India has adopted several poverty reduction measures such as the National Rural Employment Guarantee Scheme,

pension increases and a cash transfer programme in a bid to reverse the widening wealth gap in both rural and urban

areas. However, such efforts have been partly undermined by corruption and poor management in aid programmes

and partly due to imbalances in its regional growth. As such, decile 10’s slice of total annual disposable income is

expected to rise to 33%, while the decile 1 share will drop further to just 1.7% by 2030.

Marketplace is set to fragment further

MARKET DYNAMICS IN INDIA: CONSUMER TRENDS AND MOMENTUM

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Decile 1 Decile 2 Decile 3 Decile 4 Decile 5 Decile 6 Decile 7 Decile 8 Decile 9 Decile 10

Av

era

ge

ho

use

ho

ld a

nn

ua

l d

isp

osa

ble

in

com

e (U

S$

)

Average Household Annual Disposable Income by Decile 2014/2030

2014 2030

THANK YOU FOR READINGThis is an extract from the full Euromonitor International report Mega to Micro: Trends

Shaping India’s Consumers.