market decode: why bonds (still) matter, even when rates ... · even longer-dated bonds that mature...

TRANSCRIPT

Market Decode: Why Bonds Still Matter When Interest Rates Are Rising

With Matthew Diczok, Head of Fixed Income Strategy, Merrill Lynch

Wealth Management

Please see important information at the end of this program. Filmed on 2/28/18.

One of the top questions we receive from clients these days is, now that interest

rates finally appear to be rising, does it still makes sense to own bonds? In our view

the answer is yes.

Many people are aware that when interest rates are rising, even if it’s slow and

gradual, prices for the bonds they currently hold will typically go down in value.

That’s because when rates are going up, investors can now buy new bonds at the

higher interest rate—also known as the coupon rate—and that makes older bonds

with lower coupon rates less attractive, thus pushing down their price on the open

market.

While this is an important point to be aware of, it doesn’t make bonds any less

essential to a well-diversified portfolio.

A key reason for this is simple: Because (try as we might) we can’t predict the future

with certainty.

We can make educated forecasts based on what we know about the economy and the

markets at any given time. But things can always and often do—play out differently

than expected, including the direction of interest rates.

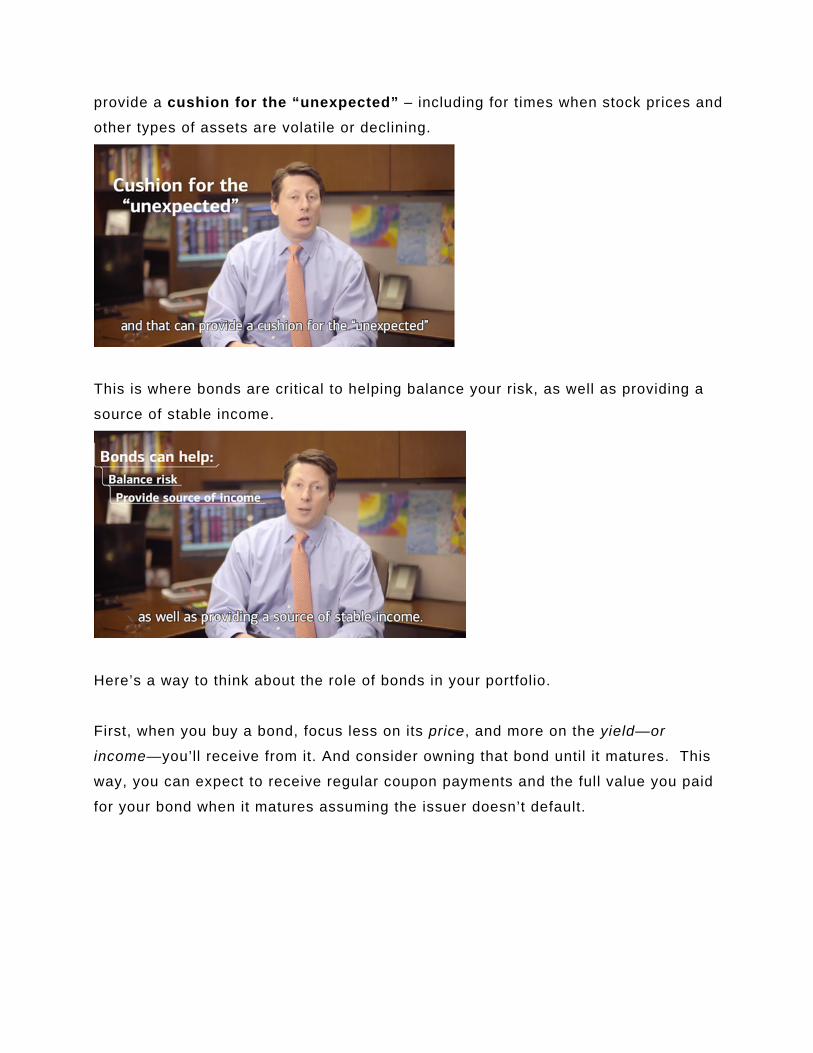

This makes it’s important to build portfolios that are broadly diversified, and that can

provide a cushion for the “unexpected” – including for times when stock prices and

other types of assets are volatile or declining.

This is where bonds are critical to helping balance your risk, as well as providing a

source of stable income.

Here’s a way to think about the role of bonds in your portfolio.

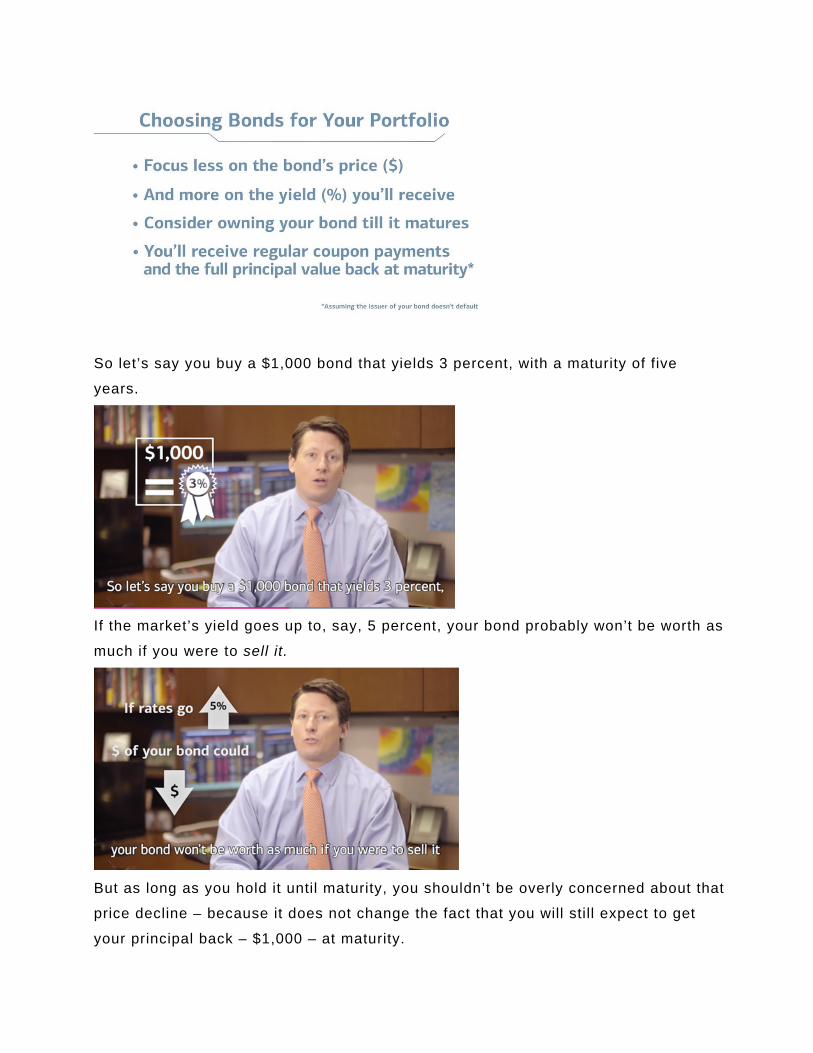

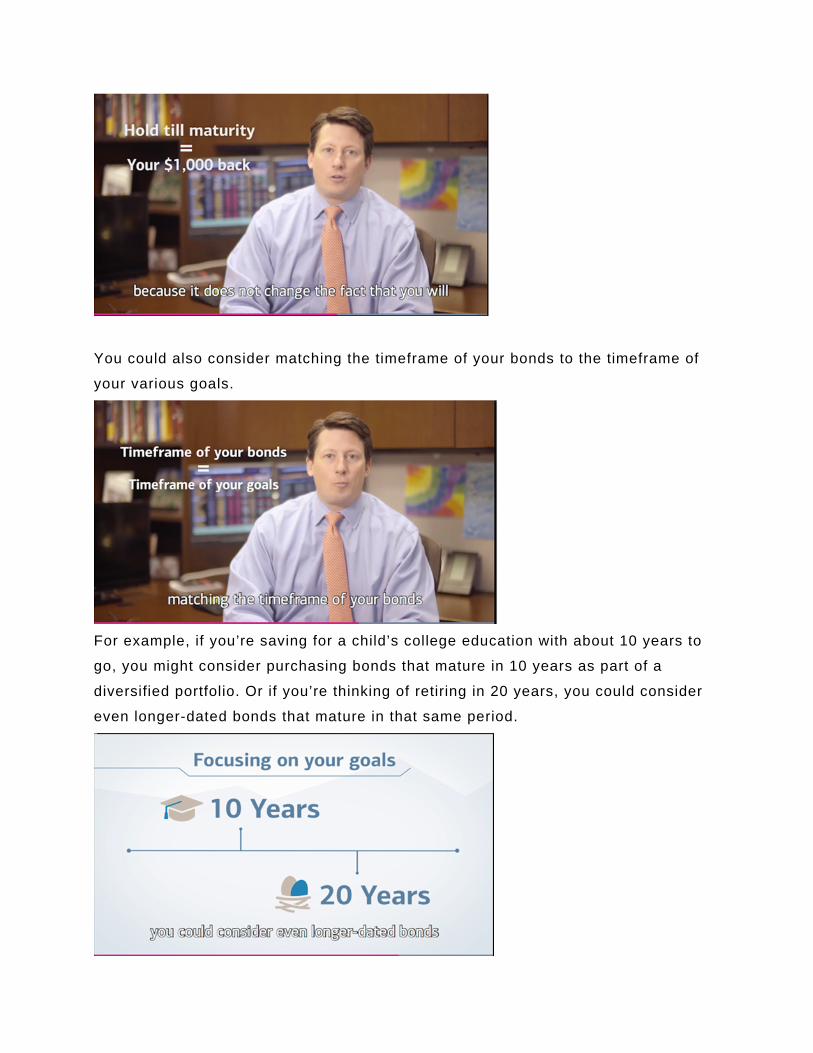

First, when you buy a bond, focus less on its price, and more on the yield—or

income—you’ll receive from it. And consider owning that bond until it matures. This

way, you can expect to receive regular coupon payments and the full value you paid

for your bond when it matures assuming the issuer doesn’t default.

So let’s say you buy a $1,000 bond that yields 3 percent, with a maturity of five

years.

If the market’s yield goes up to, say, 5 percent, your bond probably won’t be worth as

much if you were to sell it.

But as long as you hold it until maturity, you shouldn’t be overly concerned about that

price decline – because it does not change the fact that you will still expect to get

your principal back – $1,000 – at maturity.

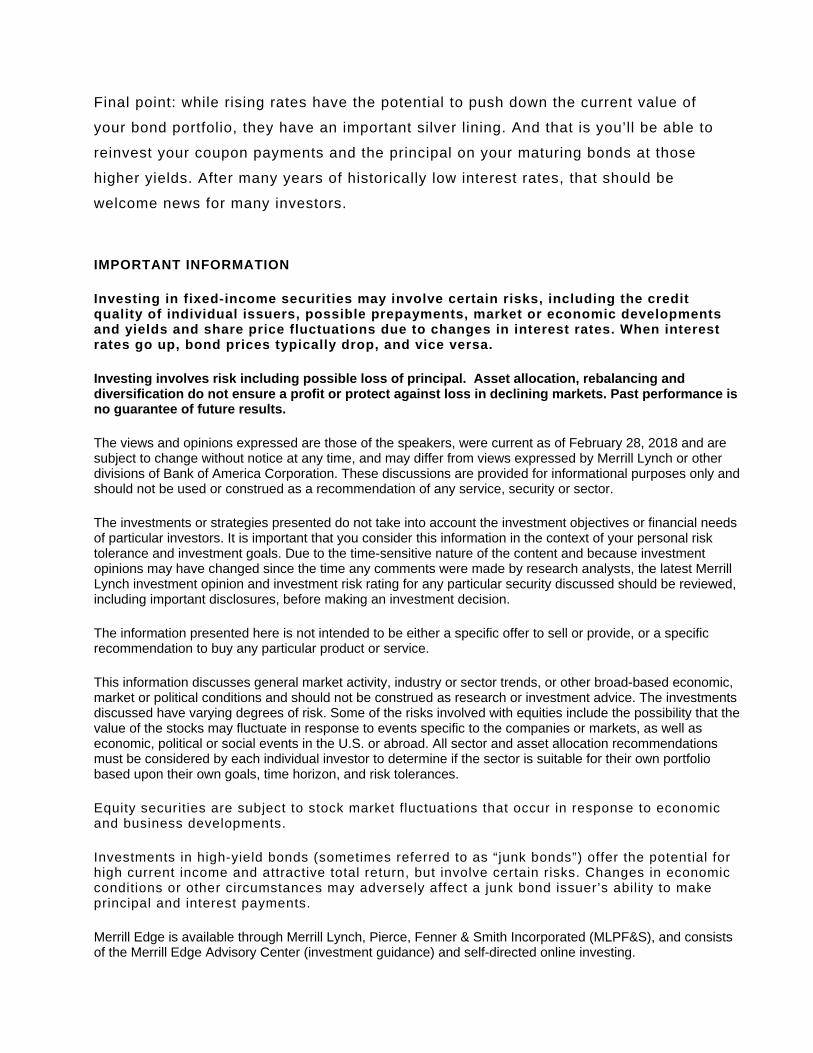

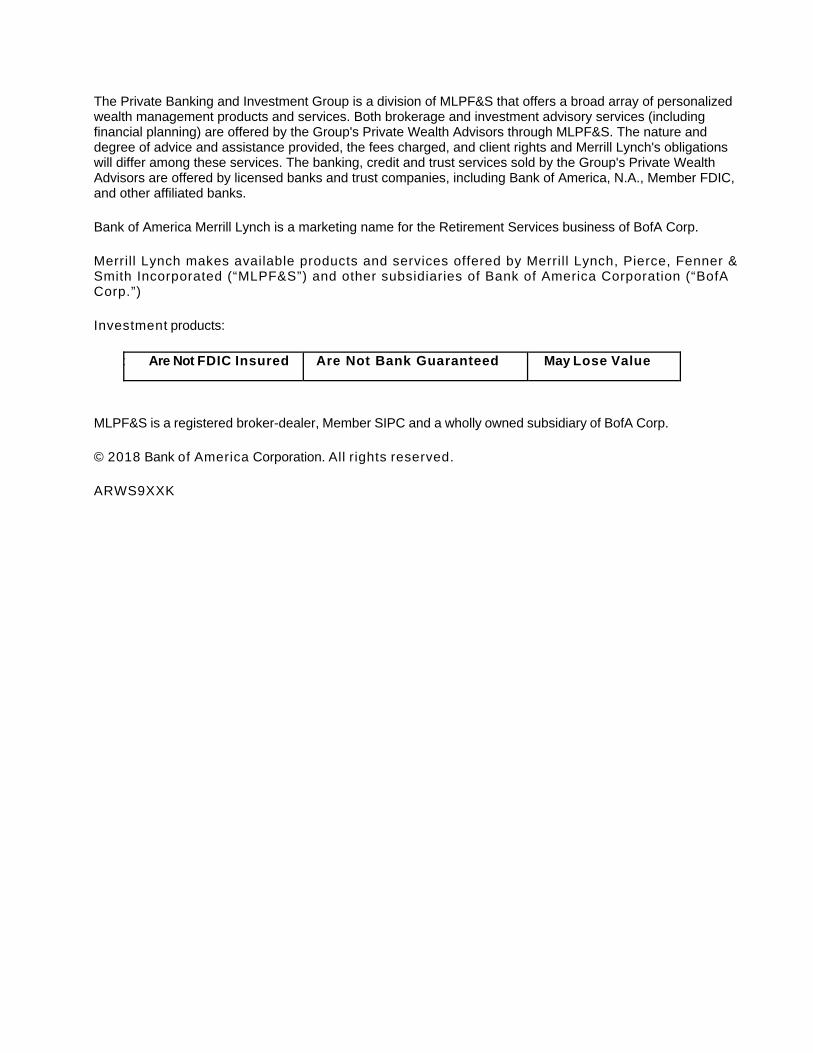

You could also consider matching the timeframe of your bonds to the timeframe of

your various goals.

For example, if you’re saving for a child’s college education with about 10 years to

go, you might consider purchasing bonds that mature in 10 years as part of a

diversified portfolio. Or if you’re thinking of retiring in 20 years, you could consider

even longer-dated bonds that mature in that same period.

Final point: while rising rates have the potential to push down the current value of

your bond portfolio, they have an important silver lining. And that is you’ll be able to

reinvest your coupon payments and the principal on your maturing bonds at those

higher yields. After many years of historically low interest rates, that should be

welcome news for many investors.

IMPORTANT INFORMATION

Investing in fixed-income securities may involve certain risks, including the credit quality of individual issuers, possible prepayments, market or economic developments and yields and share price fluctuations due to changes in interest rates. When interest rates go up, bond prices typically drop, and vice versa.

Investing involves risk including possible loss of principal. Asset allocation, rebalancing and diversification do not ensure a profit or protect against loss in declining markets. Past performance is no guarantee of future results.

The views and opinions expressed are those of the speakers, were current as of February 28, 2018 and are subject to change without notice at any time, and may differ from views expressed by Merrill Lynch or other divisions of Bank of America Corporation. These discussions are provided for informational purposes only and should not be used or construed as a recommendation of any service, security or sector.

The investments or strategies presented do not take into account the investment objectives or financial needs of particular investors. It is important that you consider this information in the context of your personal risk tolerance and investment goals. Due to the time-sensitive nature of the content and because investment opinions may have changed since the time any comments were made by research analysts, the latest Merrill Lynch investment opinion and investment risk rating for any particular security discussed should be reviewed, including important disclosures, before making an investment decision.

The information presented here is not intended to be either a specific offer to sell or provide, or a specific recommendation to buy any particular product or service.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. The investments discussed have varying degrees of risk. Some of the risks involved with equities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. All sector and asset allocation recommendations must be considered by each individual investor to determine if the sector is suitable for their own portfolio based upon their own goals, time horizon, and risk tolerances.

Equity securities are subject to stock market fluctuations that occur in response to economic and business developments.

Investments in high-yield bonds (sometimes referred to as “junk bonds”) offer the potential for high current income and attractive total return, but involve certain risks. Changes in economic conditions or other circumstances may adversely affect a junk bond issuer’s ability to make principal and interest payments.

Merrill Edge is available through Merrill Lynch, Pierce, Fenner & Smith Incorporated (MLPF&S), and consists of the Merrill Edge Advisory Center (investment guidance) and self-directed online investing.

The Private Banking and Investment Group is a division of MLPF&S that offers a broad array of personalized wealth management products and services. Both brokerage and investment advisory services (including financial planning) are offered by the Group's Private Wealth Advisors through MLPF&S. The nature and degree of advice and assistance provided, the fees charged, and client rights and Merrill Lynch's obligations will differ among these services. The banking, credit and trust services sold by the Group's Private Wealth Advisors are offered by licensed banks and trust companies, including Bank of America, N.A., Member FDIC, and other affiliated banks.

Bank of America Merrill Lynch is a marketing name for the Retirement Services business of BofA Corp.

Merrill Lynch makes available products and services offered by Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”) and other subsidiaries of Bank of America Corporation (“BofA Corp.”)

Investment products:

t Are Not FDIC Insured Are Not Bank Guaranteed May Lose Value

MLPF&S is a registered broker-dealer, Member SIPC and a wholly owned subsidiary of BofA Corp.

© 2018 Bank of America Corporation. All rights reserved.

ARWS9XXK