marci l. ryvicker, cpa, cfa harrisburg, pa april 2011 please see page 82 for rating definitions,...

Post on 20-Dec-2015

214 views

TRANSCRIPT

Marci L. Ryvicker, CPA, CFA

Harrisburg, PA

April 2011

Please see page 82 for rating definitions, important disclosures and required analyst certifications.

Wells Fargo Securities, LLC does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of the report and investors should consider this report as only a single factor in making their investment decision.

Cable: A Look At Trends & OpportunitiesCable: A Look At Trends & OpportunitiesPast, Present and FuturePast, Present and Future

22

AGENDAAGENDA

Source: Company websites, and Wells Fargo Securities, LLCSource: Company websites, and Wells Fargo Securities, LLC

I.I. SUBSCRIBER TRENDS SUBSCRIBER TRENDS

II.II. ARPU TRENDSARPU TRENDS

III.III. 2010 THEMES2010 THEMES

IV.IV. OPPORTUNITIES FOR GROWTHOPPORTUNITIES FOR GROWTH

V.V. INVESTOR FOCUSINVESTOR FOCUS

VI.VI. WHAT ABOUT…..?WHAT ABOUT…..?

VII.VII. YOUR QUESTIONSYOUR QUESTIONS

33

SUBSCRIBER TRENDSSUBSCRIBER TRENDS

Source: Company websites, and Wells Fargo Securities, LLCSource: Company websites, and Wells Fargo Securities, LLC

BASIC VIDEOBASIC VIDEO

HIGH SPEED DATAHIGH SPEED DATA

TELEPHONY TELEPHONY

BASIC VIDEOBASIC VIDEO

100

92

95

98

97

0%

10%

20%

30%

40%

50%

60%

70%

80%

FY 2

005

FY 2

006

FY 2

007

FY 2

008

FY 2

009

FY 2

010

88

90

92

94

96

98

100

102

Cable DBS Telco Total Multichannel Subscribers55

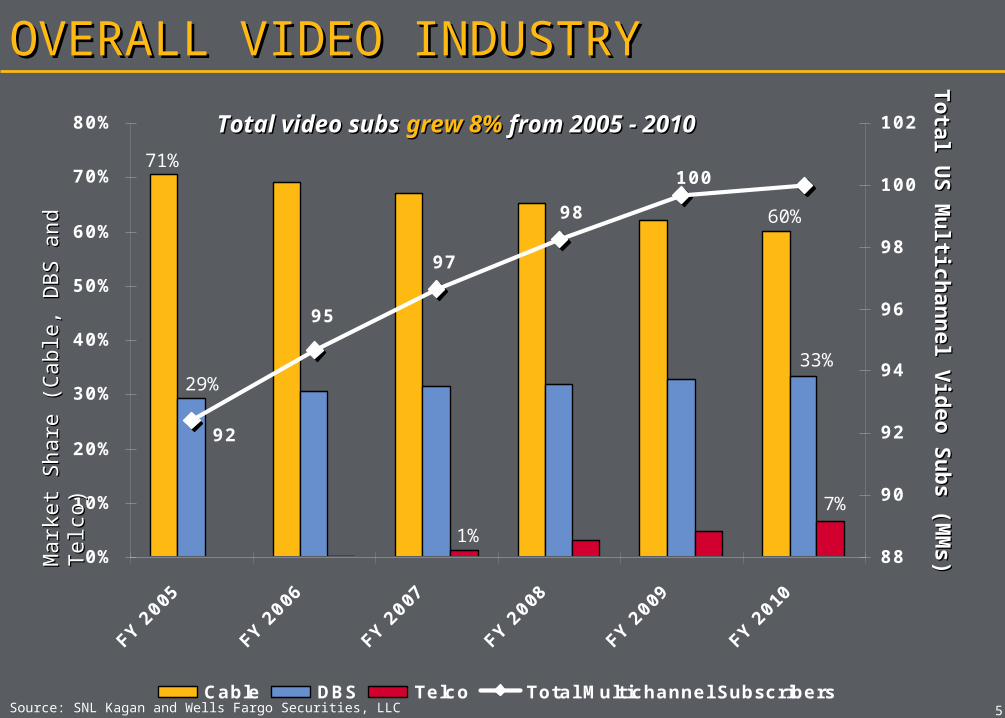

OVERALL VIDEO INDUSTRYOVERALL VIDEO INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC

Mark

et

Share

(C

able

, D

BS a

nd T

elc

o)

Mark

et

Share

(C

able

, D

BS a

nd T

elc

o)

Tota

l US

Mu

ltich

an

nel V

ideo S

ub

s (M

Ms)

Tota

l US

Mu

ltich

an

nel V

ideo S

ub

s (M

Ms)

Total video subs Total video subs grew 8%grew 8% from 2005 - from 2005 - 2010201071%

29%

1%

7%

33%

60%

104103

102101

100

92

95

98

97

0%

10%

20%

30%

40%

50%

60%

70%

80%

FY 2

005

FY 2

006

FY 2

007

FY 2

008

FY 2

009

FY 2

010

FY 2

011E

FY 2

012E

FY 2

013E

FY 2

014E

FY 2

015E

FY 2

016E

86

88

90

92

94

96

98

100

102

104

106

Cable DBS Telco Total Multichannel Subscribers

66

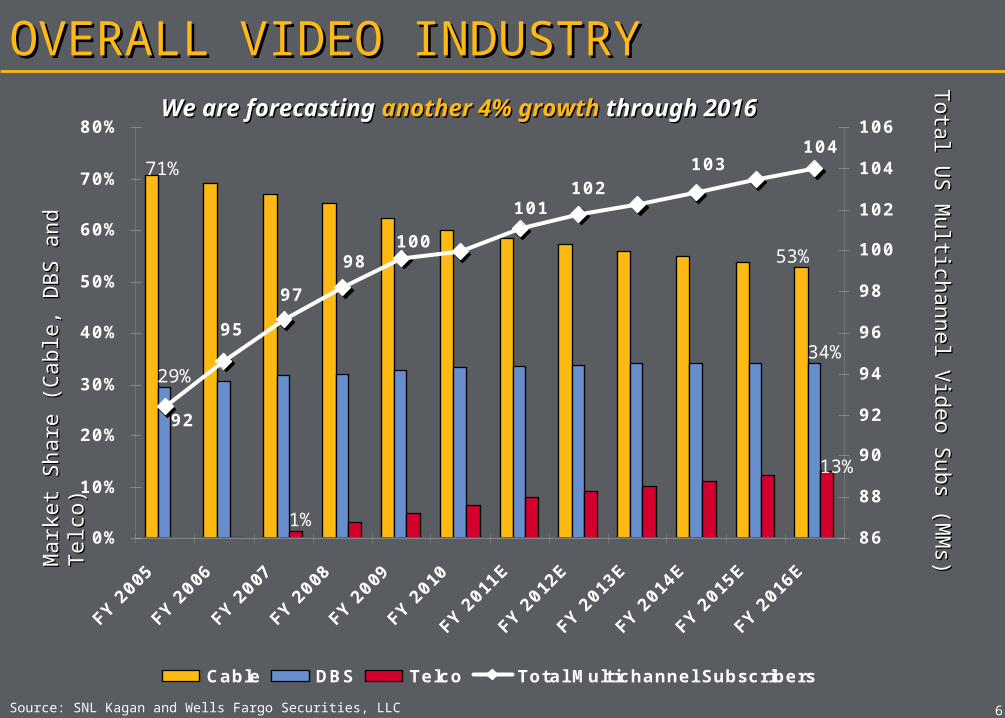

OVERALL VIDEO INDUSTRYOVERALL VIDEO INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC

Mark

et

Share

(C

able

, D

BS a

nd T

elc

o)

Mark

et

Share

(C

able

, D

BS a

nd T

elc

o)

Tota

l US M

ultich

annel V

ideo S

ubs (M

Ms)

Tota

l US M

ultich

annel V

ideo S

ubs (M

Ms)

We are forecasting We are forecasting another 4% growthanother 4% growth through through 20162016

71%

29%

1%

53%

34%

13%

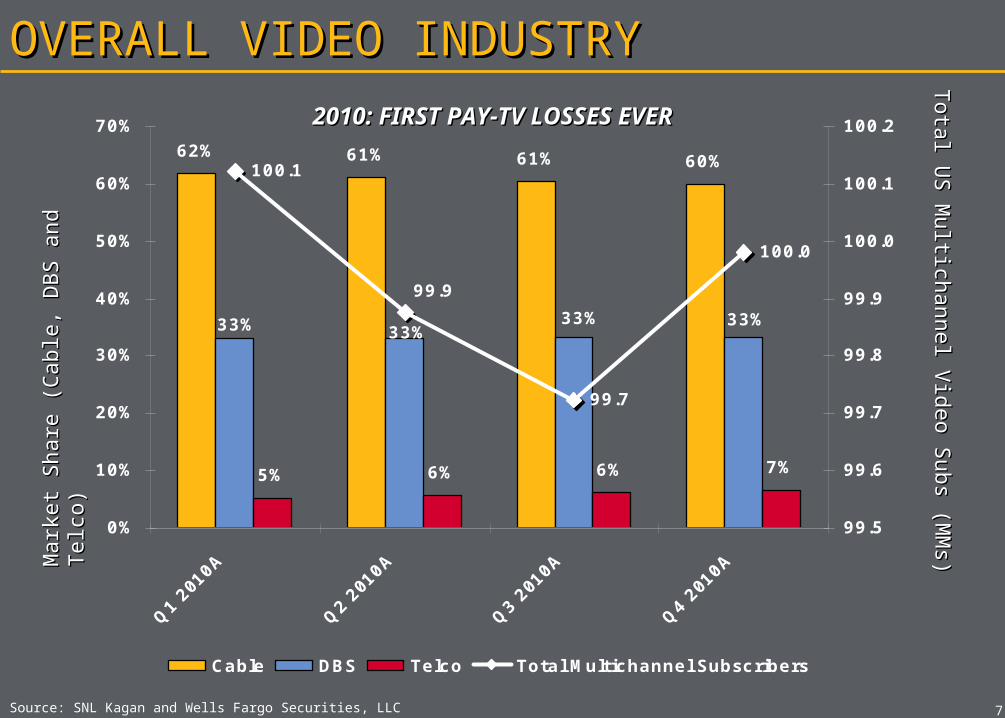

62% 61% 61% 60%

5% 6% 6% 7%

33%33%33% 33%

100.1

99.7

100.0

99.9

0%

10%

20%

30%

40%

50%

60%

70%

Q1

2010

A

Q2

2010

A

Q3

2010

A

Q4

2010

A

99.5

99.6

99.7

99.8

99.9

100.0

100.1

100.2

Cable DBS Telco Total Multichannel Subscribers

77

OVERALL VIDEO INDUSTRYOVERALL VIDEO INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC

Mark

et

Share

(C

able

, D

BS a

nd T

elc

o)

Mark

et

Share

(C

able

, D

BS a

nd T

elc

o)

Tota

l US M

ultich

annel V

ideo S

ubs (M

Ms)

Tota

l US M

ultich

annel V

ideo S

ubs (M

Ms)

2010: FIRST PAY-TV LOSSES EVER2010: FIRST PAY-TV LOSSES EVER

Company Basic Subs Y/Y Change Net Adds Y/Y Change Market Share

1 Comcast 22,802 (3.2%) (757) (21.5%) 23%

2 Time Warner Cable 12,422 (3.4%) (437) (108.1%) 12%

3 Cox 4,868 (3.7%) (185) 32.2% 5%

4 Charter 4,520 (6.3%) (304) (43.2%) 5%

5 Cablevision 3,314 (1.6%) (53) (5.0%) 3%

6 Brighthouse 2,187 (3.4%) (76) (73.4%) 2%

7 Suddenlink 1,193 (3.7%) (15) 49.8% 1%

8 Mediacom 1,193 (3.6%) (45) 43.8% 1%

9 Insight 692 (3.4%) (25) (383.9%) 1%

10 CableOne 647 (3.3%) (22) (4,300.0%) 1%

88

TOP CABLE VIDEO PROVIDERSTOP CABLE VIDEO PROVIDERS

Source: SNL Kagan and Wells Fargo Securities, LLC

2010 Top Cable Provider Snapshot2010 Top Cable Provider Snapshot

Note: Figures in thousands, except percentage data

Company Basic Subs Y/Y Change Net Adds Y/Y Change Market Share

1 DirecTV 19,223 3.6% 663 (29.4%) 19%

2 DISH Network 14,133 0.2% 33 (92.2%) 14%

3 Verizon FiOS 3,472 21.4% 611 (35.2%) 3%

4 AT&T U-Verse 2,985 44.6% 921 (9.6%) 3%

99

TOP DBS/TELCO VIDEO PROVIDERSTOP DBS/TELCO VIDEO PROVIDERS

Source: SNL Kagan and Wells Fargo Securities, LLC

2010 Top DBS/Telco Provider Snapshot2010 Top DBS/Telco Provider Snapshot

Note: Figures in thousands, except percentage data

HIGH SPEED DATAHIGH SPEED DATA

80

76

71

65

56

45

0%

10%

20%

30%

40%

50%

60%

70%

FY 2

005

FY 2

006

FY 2

007

FY 2

008

FY 2

009

FY 2

010

40

45

50

55

60

65

70

75

80

85

Cable DSL Fiber Total Broadband Subscribers

1111

OVERALL HSD INDUSTRYOVERALL HSD INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC

Mark

et

Share

(C

able

, D

SL

and F

iber)

Mark

et

Share

(C

able

, D

SL

and F

iber)

Tota

l US B

roadband S

ubscrib

ers (M

Ms)

Tota

l US B

roadband S

ubscrib

ers (M

Ms)

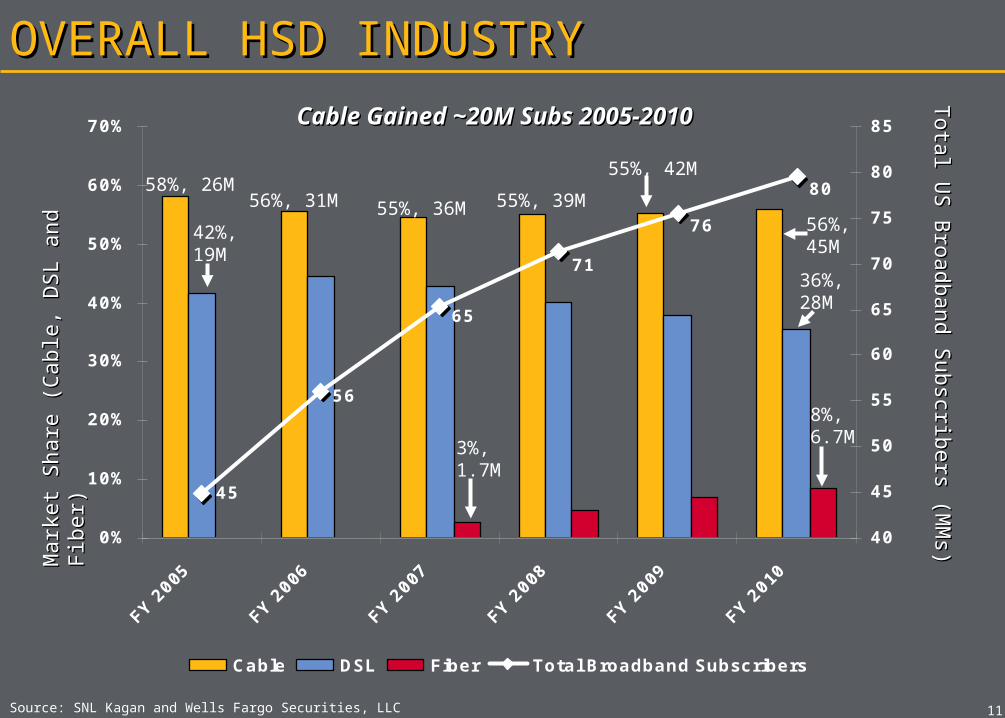

58%, 26M56%, 31M 55%, 36M 55%, 39M

55%, 42M

56%, 45M

8%, 6.7M

42%, 19M

3%, 1.7M

36%, 28M

Cable Gained ~20M Subs 2005-2010Cable Gained ~20M Subs 2005-2010

101

9895

9288

8480

76

71

65

56

45

0%

10%

20%

30%

40%

50%

60%

70%

FY 2

005

FY 2

006

FY 2

007

FY 2

008

FY 2

009

FY 2

010

FY 2

011E

FY 2

012E

FY 2

013E

FY 2

014E

FY 2

015E

FY 2

016E

40

50

60

70

80

90

100

110

Cable DSL Fiber Total Broadband Subscribers

1212

OVERALL HSD INDUSTRYOVERALL HSD INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC

Mark

et

Share

(C

able

, D

SL

and F

iber)

Mark

et

Share

(C

able

, D

SL

and F

iber)

Tota

l US B

roadband S

ubscrib

ers (M

Ms)

Tota

l US B

roadband S

ubscrib

ers (M

Ms)

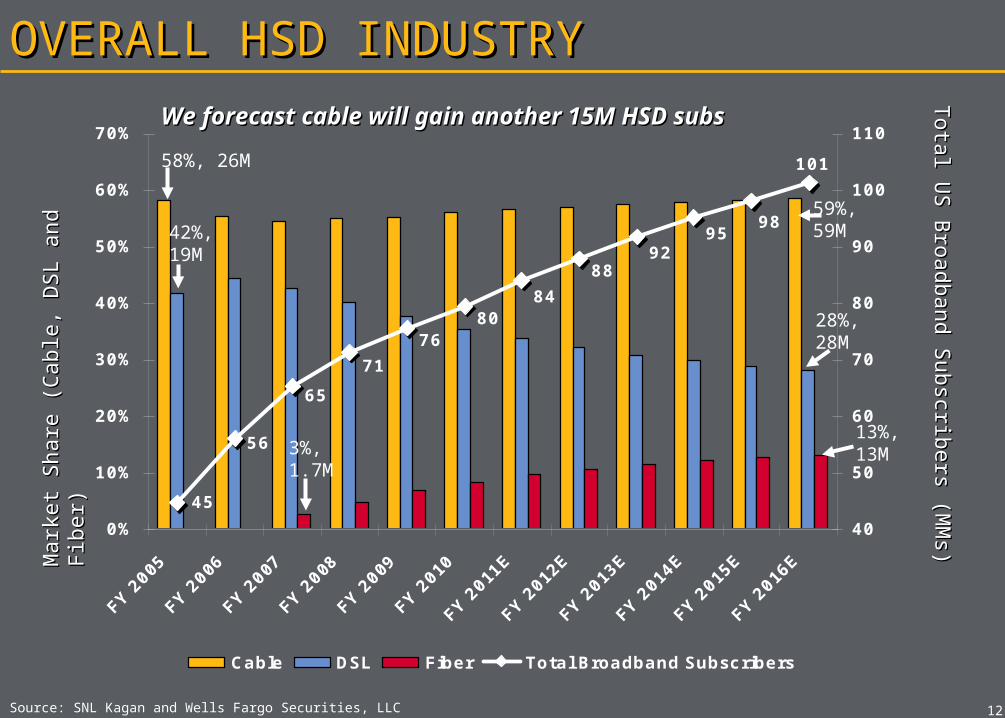

59%, 59M

28%, 28M

13%, 13M

58%, 26M

42%, 19M

3%, 1.7M

We forecast cable will gain another 15M HSD subsWe forecast cable will gain another 15M HSD subs

56% 56% 56% 56%

37% 36% 36%

7% 8% 8% 8%

36%

79.5

78.4

77.4

76.8

0%

10%

20%

30%

40%

50%

60%

Q1

2010

A

Q2

2010

A

Q3

2010

A

Q4

2010

A

75.0

75.5

76.0

76.5

77.0

77.5

78.0

78.5

79.0

79.5

80.0

Cable DSL Fiber Total Broadband Subscribers

1313

OVERALL HSD INDUSTRYOVERALL HSD INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC

Mark

et

Share

(C

able

, D

SL

and F

iber)

Mark

et

Share

(C

able

, D

SL

and F

iber)

Tota

l US B

roadband S

ubscrib

ers (M

Ms)

Tota

l US B

roadband S

ubscrib

ers (M

Ms)

, 43M

, 29M

, 6M

, 28M

, 45M

, 7M

Cable gained 3 M HSD subs in Cable gained 3 M HSD subs in 20102010

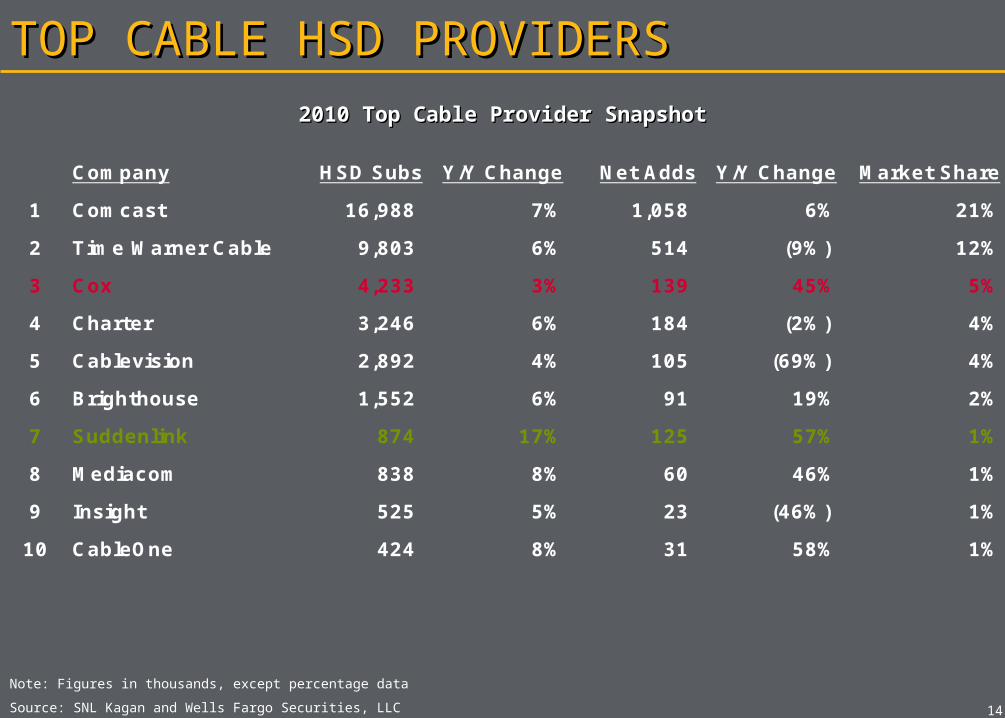

Company HSD Subs Y/Y Change Net Adds Y/Y Change Market Share

1 Comcast 16,988 7% 1,058 6% 21%

2 Time Warner Cable 9,803 6% 514 (9%) 12%

3 Cox 4,233 3% 139 45% 5%

4 Charter 3,246 6% 184 (2%) 4%

5 Cablevision 2,892 4% 105 (69%) 4%

6 Brighthouse 1,552 6% 91 19% 2%

7 Suddenlink 874 17% 125 57% 1%

8 Mediacom 838 8% 60 46% 1%

9 Insight 525 5% 23 (46%) 1%

10 CableOne 424 8% 31 58% 1%

1414

TOP CABLE HSD PROVIDERSTOP CABLE HSD PROVIDERS

Source: SNL Kagan and Wells Fargo Securities, LLC

2010 Top Cable Provider Snapshot2010 Top Cable Provider Snapshot

Note: Figures in thousands, except percentage data

Company HSD Subs Y/Y Change Net Adds Y/Y Change Market Share

1 AT&T 16,310 3% 521 (27%) 21%

AT&T U-Verse 2,612 45% 806 (10%) 3%

AT&T DSL 13,698 (2%) (285) (59%) 17%

2 Verizon 8,392 2% (828) (251%) 11%

Verizon FiOS 4,082 19% 649 (32%) 5%

Verizon DSL 4,310 (8%) (477) (18%) 5%

3 Qwest 2,914 (2%) (60) (147%) 4%

4 CenturyTel 2,394 7% 158 (14%) 3%

5 Frontier 1,697 (4%) 61 9% 2%

6 Windstream 1,303 15% 171 11% 2%

1515

TOP TELCO HSD PROVIDERSTOP TELCO HSD PROVIDERS

Source: SNL Kagan and Wells Fargo Securities, LLC

2010 Top Telco Provider Snapshot2010 Top Telco Provider Snapshot

Note: Figures in thousands, except percentage data

TELEPHONYTELEPHONY

76

79

8182

83

86

0%

10%

20%

30%

40%

50%

60%

70%

FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY 2010

70

72

74

76

78

80

82

84

86

88

Cable Telco Wireless Total Cable/Telco Phone Subs

1717

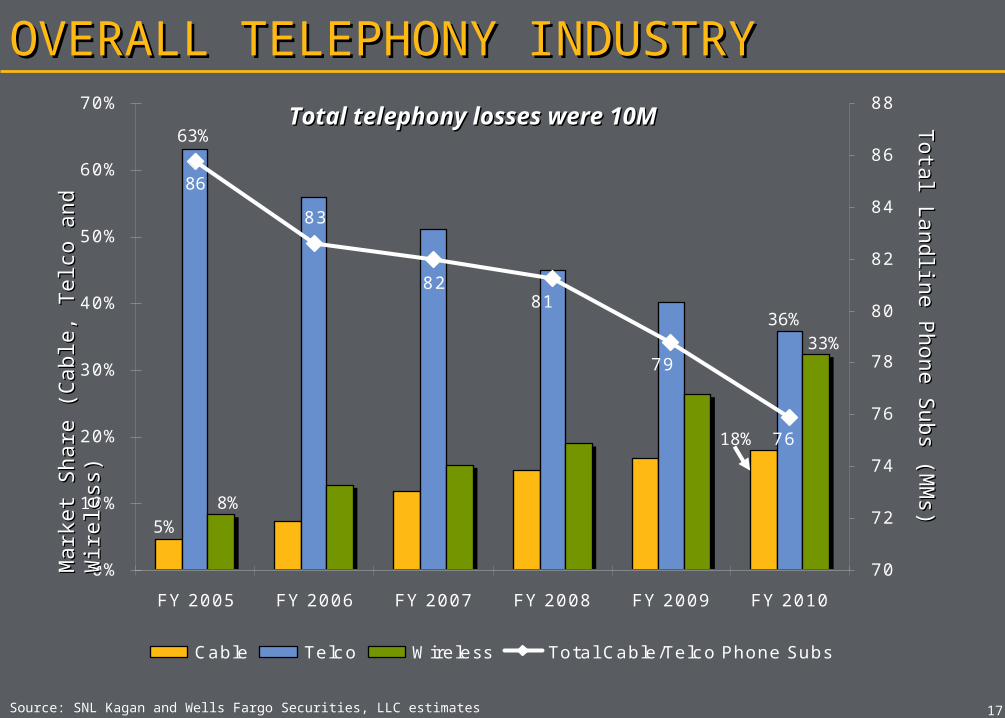

OVERALL TELEPHONY INDUSTRYOVERALL TELEPHONY INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Mark

et

Share

(C

able

, Telc

o a

nd W

irele

ss)

Mark

et

Share

(C

able

, Telc

o a

nd W

irele

ss) T

ota

l Landlin

e P

hone S

ubs (M

Ms)

Tota

l Landlin

e P

hone S

ubs (M

Ms)

Total telephony losses were 10MTotal telephony losses were 10M

8%5%

18%

36%33%

63%

86

65666769717376

798182

8386

0%

10%

20%

30%

40%

50%

60%

70%

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

E

FY 2012

E

FY 2013

E

FY 2014

E

FY 2015

E

FY 2016

E

-

10

20

30

40

50

60

70

80

90

100

Cable Telco Wireless Total Cable/Telco Phone Subs

1818

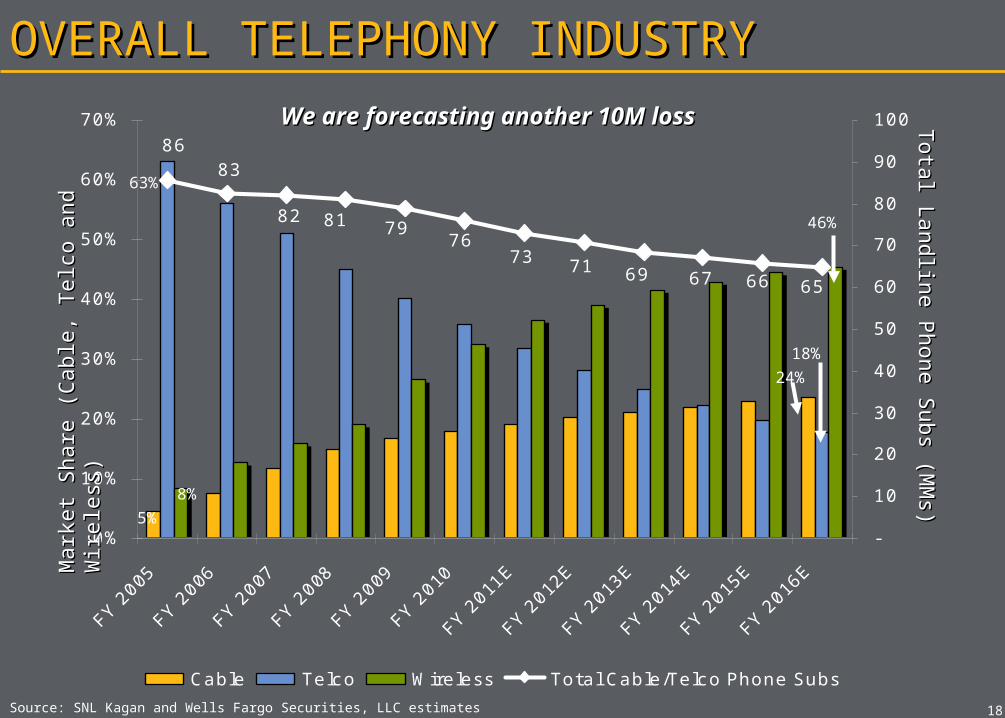

OVERALL TELEPHONY INDUSTRYOVERALL TELEPHONY INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Mark

et

Share

(C

able

, Telc

o a

nd W

irele

ss)

Mark

et

Share

(C

able

, Telc

o a

nd W

irele

ss) T

ota

l Landlin

e P

hone S

ubs (M

Ms)

Tota

l Landlin

e P

hone S

ubs (M

Ms)

We are forecasting another 10M We are forecasting another 10M lossloss

5%

8%

63%

18%

24%

46%

75.9

78.1

76.3

77.4

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Q1

2010

A

Q2

2010

A

Q3

2010

A

Q4

2010

A

74.5

75.0

75.5

76.0

76.5

77.0

77.5

78.0

78.5

Cable Telco Wireless Total Subs

1919

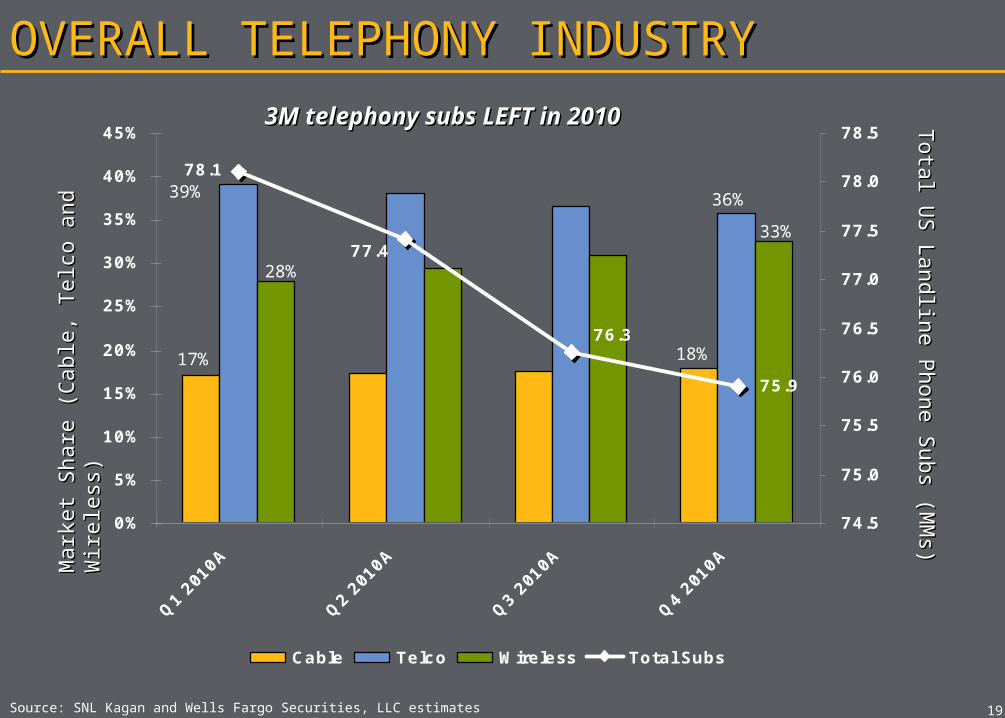

OVERALL TELEPHONY INDUSTRYOVERALL TELEPHONY INDUSTRY

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Tota

l US La

ndlin

e P

hone S

ubs (M

Ms)

Tota

l US La

ndlin

e P

hone S

ubs (M

Ms)

3M telephony subs LEFT in 20103M telephony subs LEFT in 2010

17%

28%

39%

33%

36%

18%

Mark

et

Share

(C

able

, Telc

o a

nd W

irele

ss)

Mark

et

Share

(C

able

, Telc

o a

nd W

irele

ss)

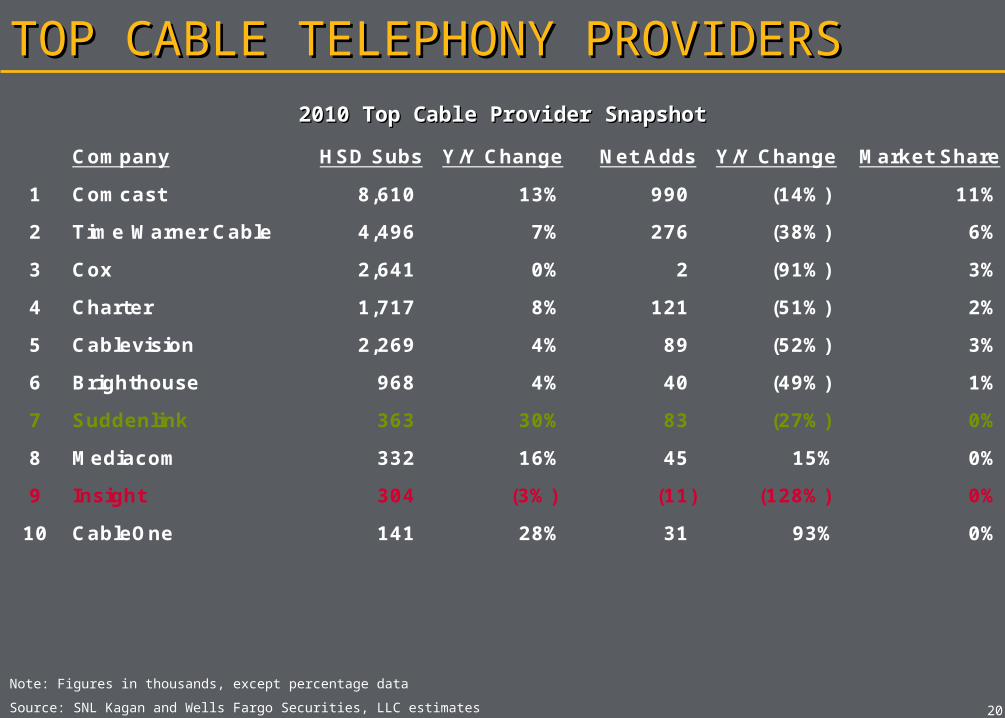

Company HSD Subs Y/Y Change Net Adds Y/Y Change Market Share

1 Comcast 8,610 13% 990 (14%) 11%

2 Time Warner Cable 4,496 7% 276 (38%) 6%

3 Cox 2,641 0% 2 (91%) 3%

4 Charter 1,717 8% 121 (51%) 2%

5 Cablevision 2,269 4% 89 (52%) 3%

6 Brighthouse 968 4% 40 (49%) 1%

7 Suddenlink 363 30% 83 (27%) 0%

8 Mediacom 332 16% 45 15% 0%

9 Insight 304 (3%) (11) (128%) 0%

10 CableOne 141 28% 31 93% 0%

2020

TOP CABLE TELEPHONY PROVIDERSTOP CABLE TELEPHONY PROVIDERS

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

2010 Top Cable Provider Snapshot2010 Top Cable Provider Snapshot

Note: Figures in thousands, except percentage data

2121

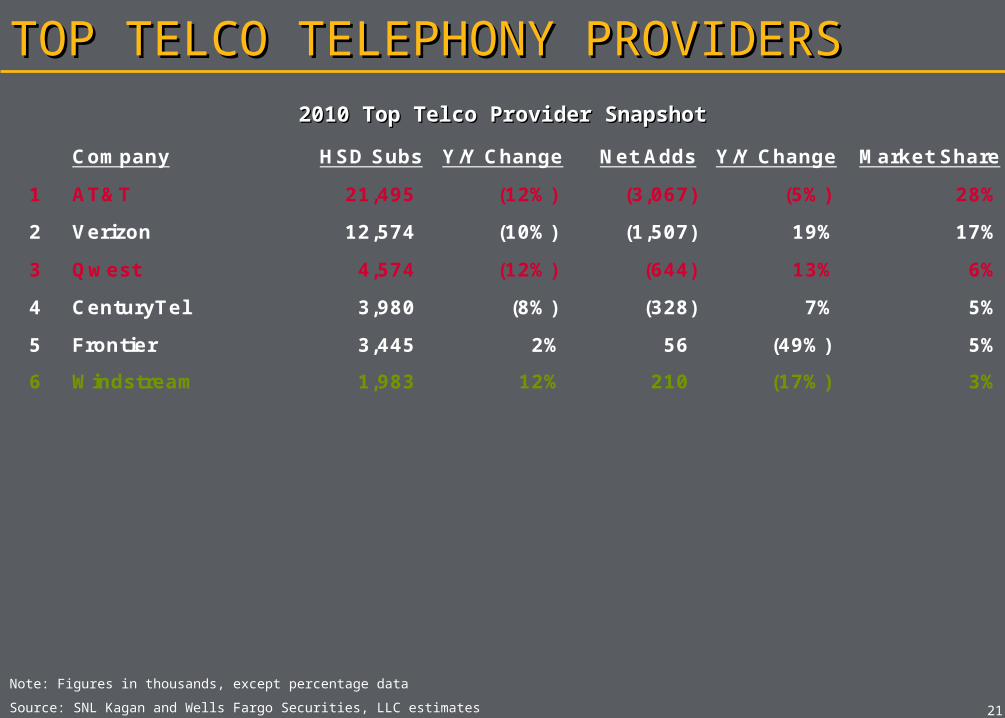

TOP TELCO TELEPHONY PROVIDERSTOP TELCO TELEPHONY PROVIDERS

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

2010 Top Telco Provider Snapshot2010 Top Telco Provider Snapshot

Note: Figures in thousands, except percentage data

Company HSD Subs Y/Y Change Net Adds Y/Y Change Market Share

1 AT&T 21,495 (12%) (3,067) (5%) 28%

2 Verizon 12,574 (10%) (1,507) 19% 17%

3 Qwest 4,574 (12%) (644) 13% 6%

4 CenturyTel 3,980 (8%) (328) 7% 5%

5 Frontier 3,445 2% 56 (49%) 5%

6 Windstream 1,983 12% 210 (17%) 3%

2222

ARPU TRENDSARPU TRENDS

TOTAL ARPUTOTAL ARPU

BASIC VIDEOBASIC VIDEO

HIGH SPEED DATAHIGH SPEED DATA

TELEPHONY TELEPHONY

TOTAL ARPUTOTAL ARPU

$108

$124

$134

$117

$0

$20

$40

$60

$80

$100

$120

$140

$160

2007

2008

2009

2010

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2424

TOTAL ARPUTOTAL ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Avera

ge T

ota

l A

RPU

Avera

ge T

ota

l A

RPU

Y/Y

Gro

wth

Y/Y

Gro

wth

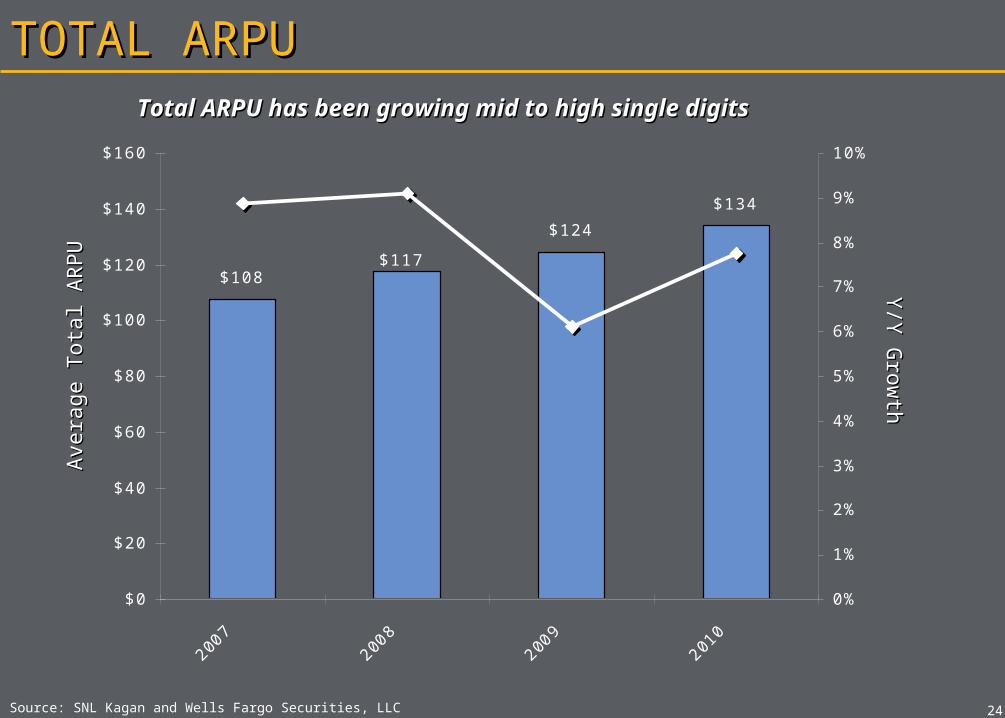

Total ARPU has been growing mid to high single Total ARPU has been growing mid to high single digitsdigits

$108

$124$134

$142$151

$160$170

$179$189

$117

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2007

2008

2009

2010

2011E

2012E

2013E

2014E

2015E

2016E

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2525

TOTAL ARPUTOTAL ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Avera

ge T

ota

l A

RPU

Avera

ge T

ota

l A

RPU

Y/Y

Gro

wth

Y/Y

Gro

wth

We expect growth to stabilize in the mid single digit We expect growth to stabilize in the mid single digit rangerange

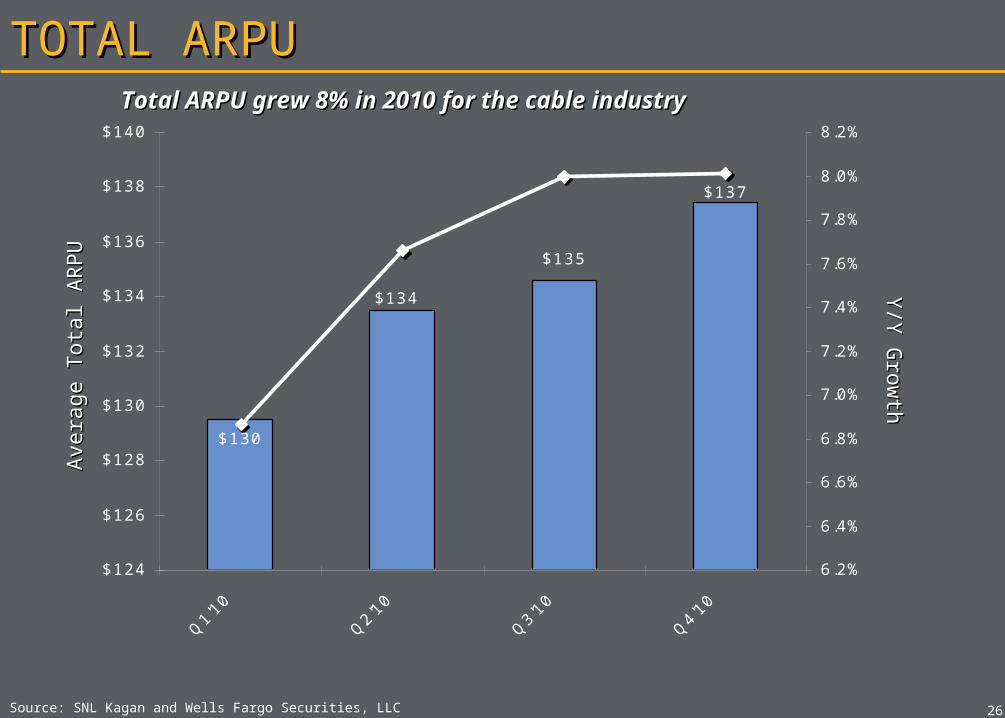

$135

$137

$130

$134

$124

$126

$128

$130

$132

$134

$136

$138

$140

Q1'1

0

Q2'1

0

Q3'1

0

Q4'1

0

6.2%

6.4%

6.6%

6.8%

7.0%

7.2%

7.4%

7.6%

7.8%

8.0%

8.2%

2626

TOTAL ARPUTOTAL ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Avera

ge T

ota

l A

RPU

Avera

ge T

ota

l A

RPU

Y/Y

Gro

wth

Y/Y

Gro

wth

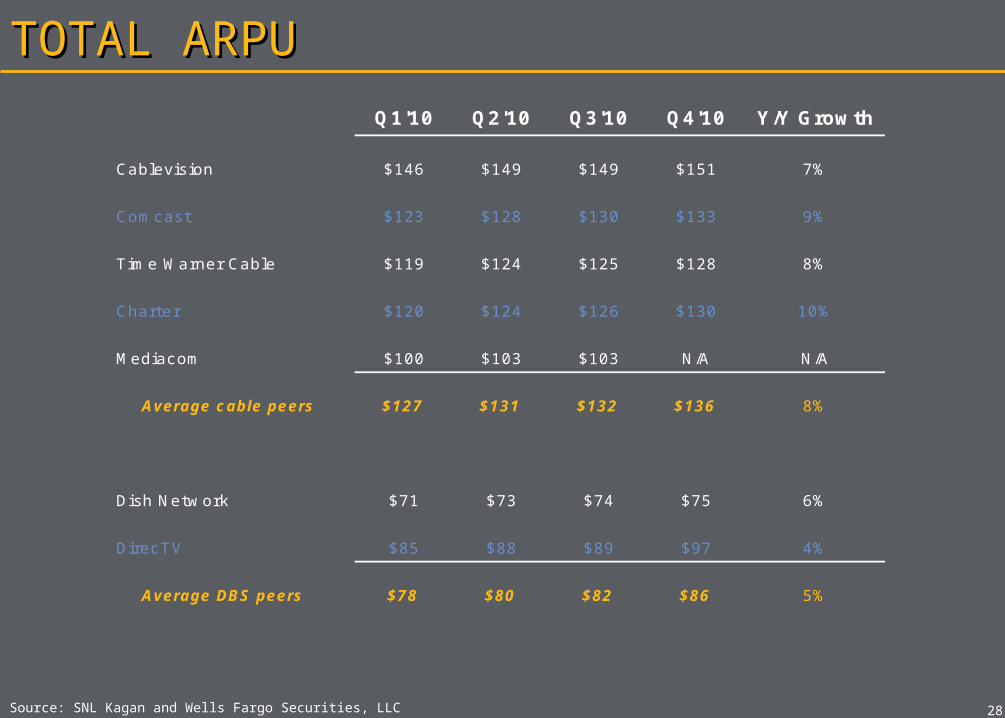

Total ARPU grew 8% in 2010 for the cable industryTotal ARPU grew 8% in 2010 for the cable industry

2007 2008 2009 2010 2011E 2012E 2013E 2014E 2015E 2016E CAGR

Cablevision $121 $133 $140 $150 $156 $164 $172 $180 $188 $196 5%

Comcast $102 $111 $118 $128 $137 $147 $155 $165 $174 $184 6%

Time Warner Cable $100 $108 $115 $124 $134 $143 $153 $164 $175 $187 7%

Charter $93 $105 $114 $125 N/A N/A N/A N/A N/A N/A N/A

Mediacom $91 $95 $99 N/A N/A N/A N/A N/A N/A N/A N/A

Average cable peers $101 $110 $117 $132 $142 $151 $160 $170 $179 $189 6%

Y /Y Change 9% 6% 12% 8% 6% 6% 6% 5% 6%

Dish Network $66 $69 $70 $74 $78 $79 $82 $84 $87 $89 3%

DirecTV $79 $84 $86 $89 $93 $97 $100 $103 $106 $109 3%

Average DBS peers $73 $77 $78 $82 $86 $88 $91 $93 $96 $99 3%

2727

TOTAL ARPUTOTAL ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Note: N/A – Not available; CAGR is a 6-year CAGR between 2011E and 2016E

2828

TOTAL ARPUTOTAL ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Q1'10 Q2'10 Q3'10 Q4'10 Y/Y Growth

Cablevision $146 $149 $149 $151 7%

Comcast $123 $128 $130 $133 9%

Time Warner Cable $119 $124 $125 $128 8%

Charter $120 $124 $126 $130 10%

Mediacom $100 $103 $103 N/A N/A

Average cable peers $127 $131 $132 $136 8%

Y /Y Change 12% 13% 13% 13%

Dish Network $71 $73 $74 $75 6%

DirecTV $85 $88 $89 $97 4%

Average DBS peers $78 $80 $82 $86 5%

BASIC VIDEOBASIC VIDEO

$73$77 $78

$77$73$70

$66

$82

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2007

2008

2009

2010

0%

1%

2%

3%

4%

5%

6%

7%

8%

Cable Avg Satellite Avg Cable Y /Y Change Satellite Y /Y Change

3030

VIDEO ARPUVIDEO ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

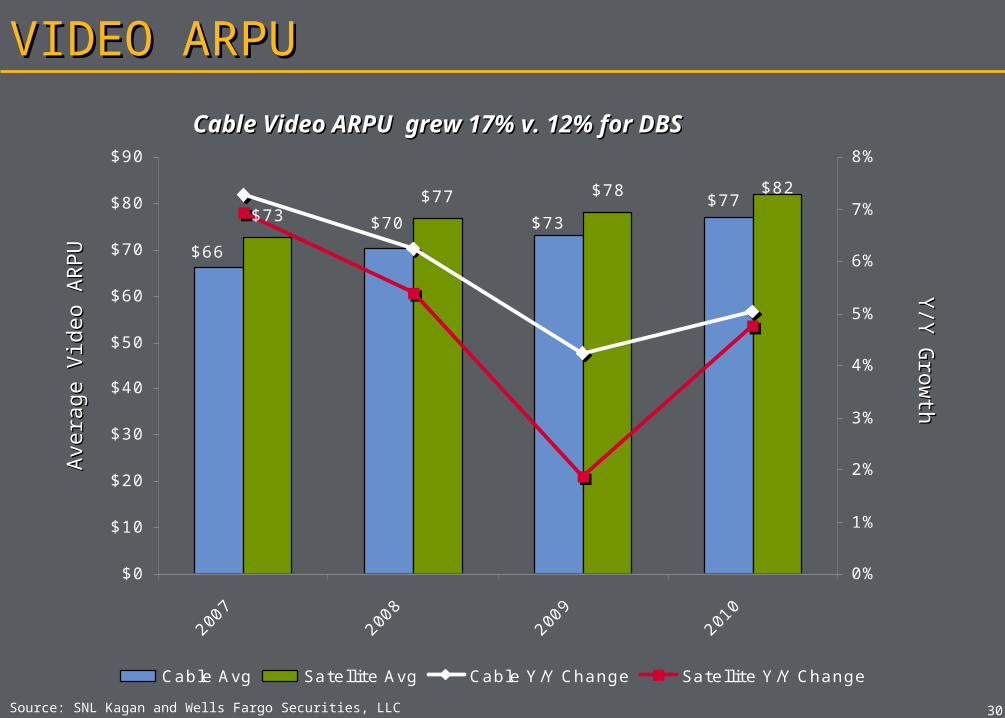

Cable Video ARPU grew 17% v. 12% for Cable Video ARPU grew 17% v. 12% for DBSDBS

Avera

ge V

ideo A

RPU

Avera

ge V

ideo A

RPU

Y/Y

Gro

wth

Y/Y

Gro

wth

$73$77 $78

$86 $88 $91$93 $96

$99$98$94

$91$87

$84$80$77

$73$70

$66

$82

$0

$20

$40

$60

$80

$100

$120

2007

2008

2009

2010

2011E

2012E

2013E

2014E

2015E

2016E

0%

1%

2%

3%

4%

5%

6%

7%

8%

Cable Avg Satellite Avg Cable Y /Y Change Satellite Y /Y Change

3131

VIDEO ARPUVIDEO ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Avera

ge V

ideo A

RPU

Avera

ge V

ideo A

RPU

Y/Y

Gro

wth

Y/Y

Gro

wth

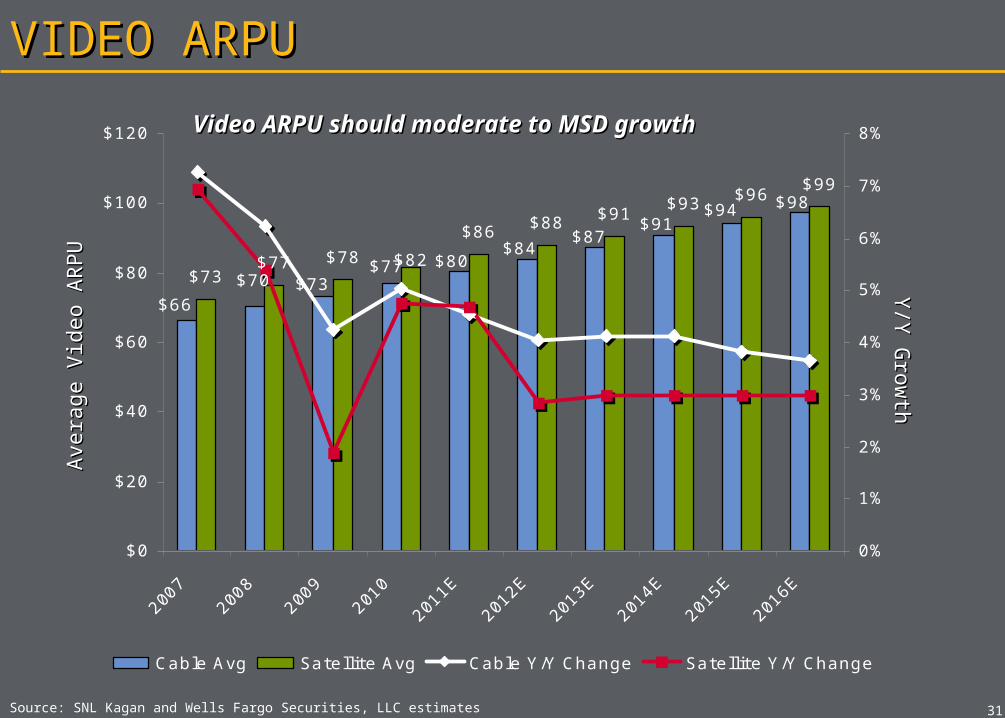

Video ARPU should moderate to MSD Video ARPU should moderate to MSD growthgrowth

3232

VIDEO ARPUVIDEO ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Cable Video ARPU grew 5% v. 4% for DBSCable Video ARPU grew 5% v. 4% for DBS

Avera

ge V

ideo A

RPU

Avera

ge V

ideo A

RPU

Y/Y

Gro

wth

Y/Y

Gro

wth

$78

$80

$82

$78$77$77

$76

$86

$70

$72

$74

$76

$78

$80

$82

$84

$86

$88

Q1'1

0

Q2'1

0

Q3'1

0

Q4'1

0

0%

1%

2%

3%

4%

5%

6%

Cable Avg Satellite Avg Cable Y /Y Change Satellite Y /Y Change

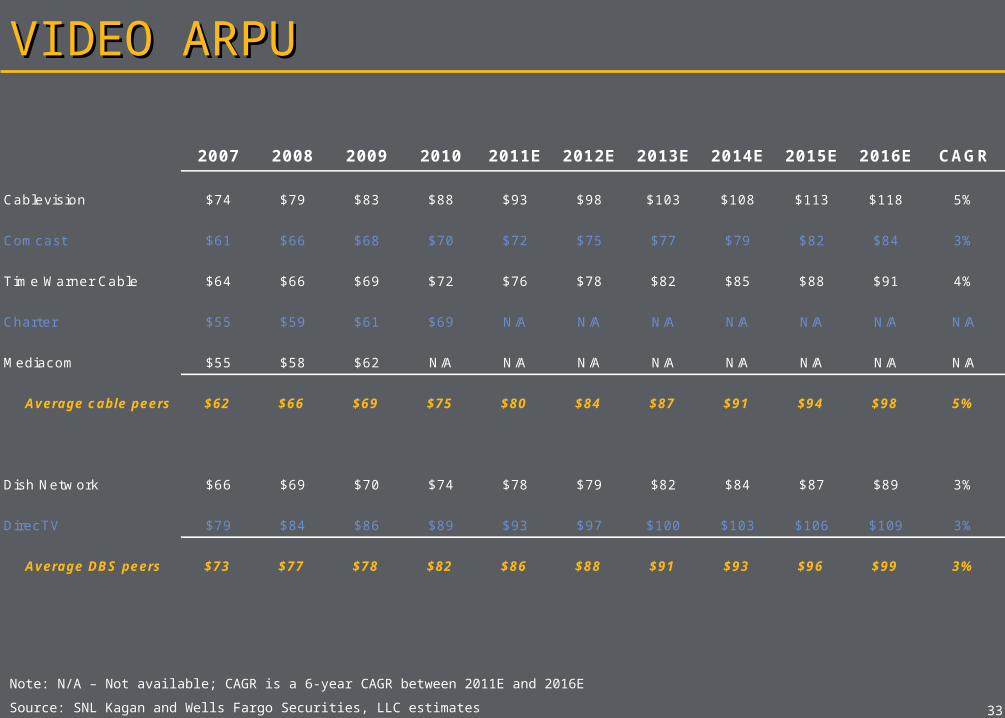

2007 2008 2009 2010 2011E 2012E 2013E 2014E 2015E 2016E CAGR

Cablevision $74 $79 $83 $88 $93 $98 $103 $108 $113 $118 5%

Comcast $61 $66 $68 $70 $72 $75 $77 $79 $82 $84 3%

Time Warner Cable $64 $66 $69 $72 $76 $78 $82 $85 $88 $91 4%

Charter $55 $59 $61 $69 N/A N/A N/A N/A N/A N/A N/A

Mediacom $55 $58 $62 N/A N/A N/A N/A N/A N/A N/A N/A

Average cable peers $62 $66 $69 $75 $80 $84 $87 $91 $94 $98 5%

Y /Y Change 6% 5% 9% 7% 4% 4% 4% 4% 4%

Dish Network $66 $69 $70 $74 $78 $79 $82 $84 $87 $89 3%

DirecTV $79 $84 $86 $89 $93 $97 $100 $103 $106 $109 3%

Average DBS peers $73 $77 $78 $82 $86 $88 $91 $93 $96 $99 3%

3333

VIDEO ARPUVIDEO ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Note: N/A – Not available; CAGR is a 6-year CAGR between 2011E and 2016E

3434

VIDEO ARPUVIDEO ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

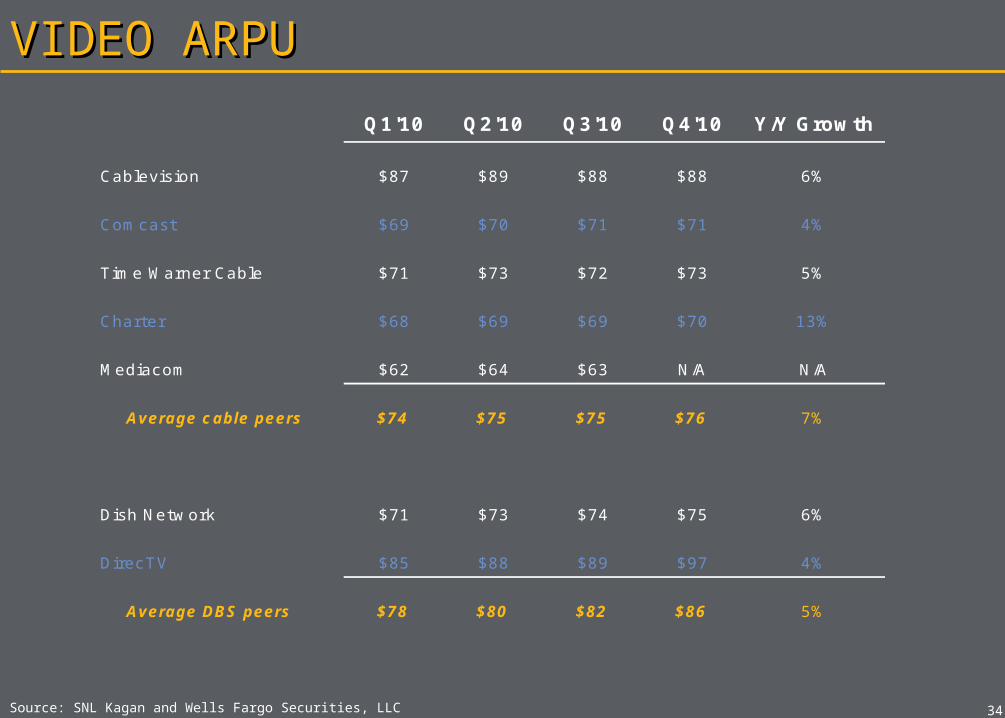

Q1'10 Q2'10 Q3'10 Q4'10 Y/Y Growth

Cablevision $87 $89 $88 $88 6%

Comcast $69 $70 $71 $71 4%

Time Warner Cable $71 $73 $72 $73 5%

Charter $68 $69 $69 $70 13%

Mediacom $62 $64 $63 N/A N/A

Average cable peers $74 $75 $75 $76 7%

Y /Y Change 9% 10% 10% 9%

Dish Network $71 $73 $74 $75 6%

DirecTV $85 $88 $89 $97 4%

Average DBS peers $78 $80 $82 $86 5%

HIGH SPEED DATAHIGH SPEED DATA

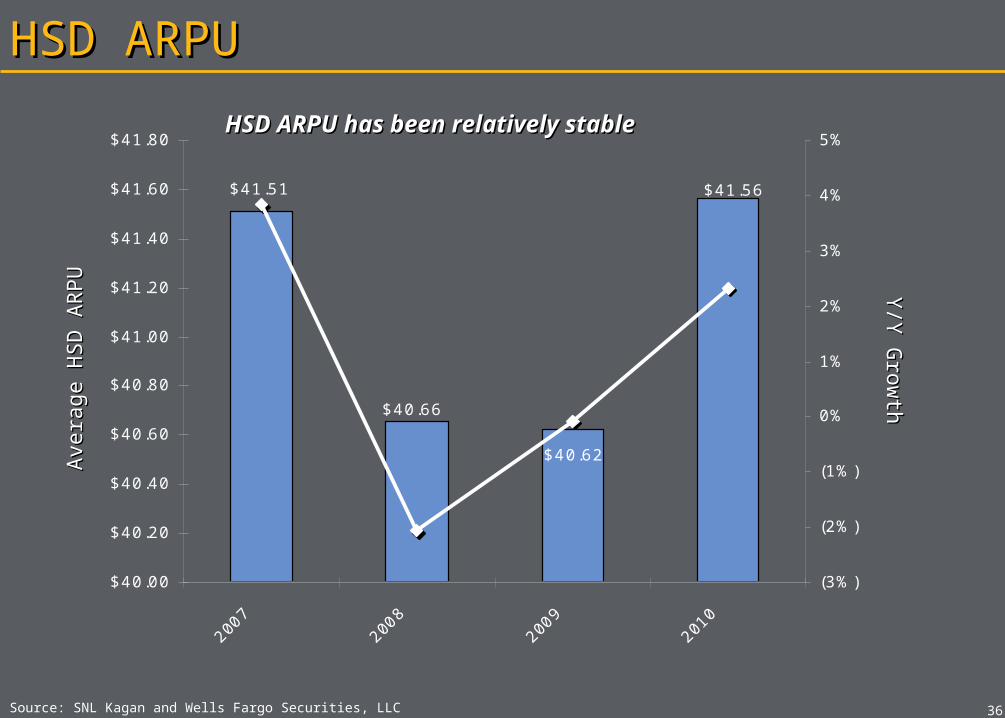

$40.62

$41.51 $41.56

$40.66

$40.00

$40.20

$40.40

$40.60

$40.80

$41.00

$41.20

$41.40

$41.60

$41.80

2007

2008

2009

2010

(3%)

(2%)

(1%)

0%

1%

2%

3%

4%

5%

3636

HSD ARPUHSD ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Avera

ge H

SD

AR

PU

Avera

ge H

SD

AR

PU

Y/Y

Gro

wth

Y/Y

Gro

wth

HSD ARPU has been relatively stableHSD ARPU has been relatively stable

3737

HSD ARPUHSD ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Avera

ge H

SD

AR

PU

Avera

ge H

SD

AR

PU

Y/Y

Gro

wth

Y/Y

Gro

wth

$48.97

$40.62

$46.45

$43.94$41.51

$45.19

$41.56

$47.71

$42.63$40.66

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

2007

2008

2009

2010

2011E

2012E

2013E

2014E

2015E

2016E

(3%)

(2%)

(1%)

0%

1%

2%

3%

4%

5%We are We are conservatively conservatively forecasting slight forecasting slight increasesincreases

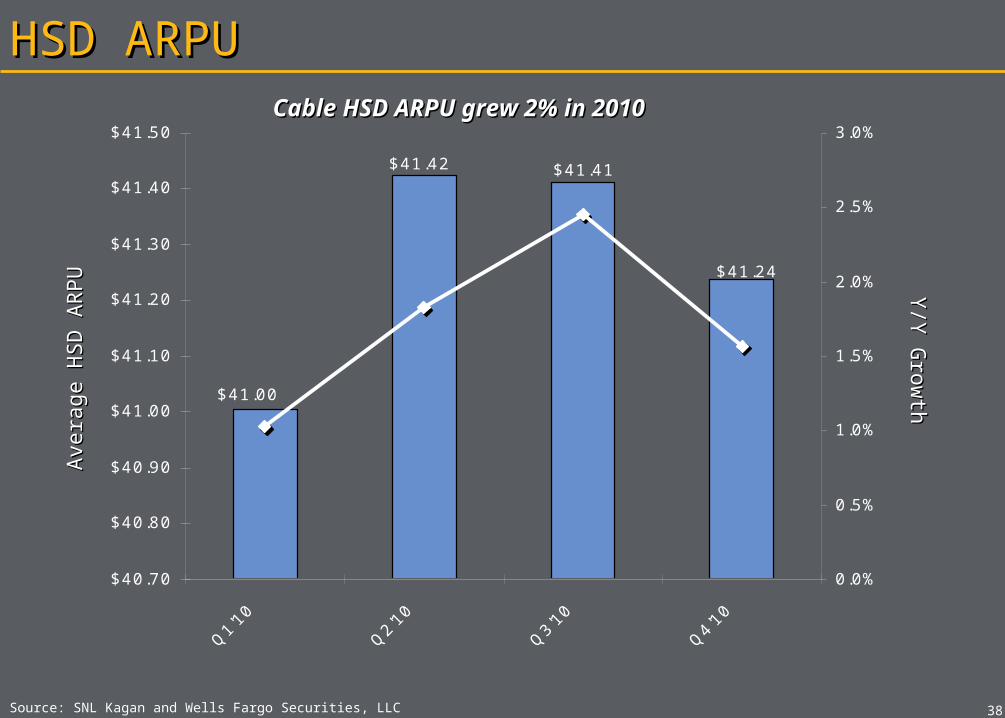

$41.41$41.42

$41.24

$41.00

$40.70

$40.80

$40.90

$41.00

$41.10

$41.20

$41.30

$41.40

$41.50

Q1'1

0

Q2'1

0

Q3'1

0

Q4'1

0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3838

HSD ARPUHSD ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Avera

ge H

SD

AR

PU

Avera

ge H

SD

AR

PU

Y/Y

Gro

wth

Y/Y

Gro

wth

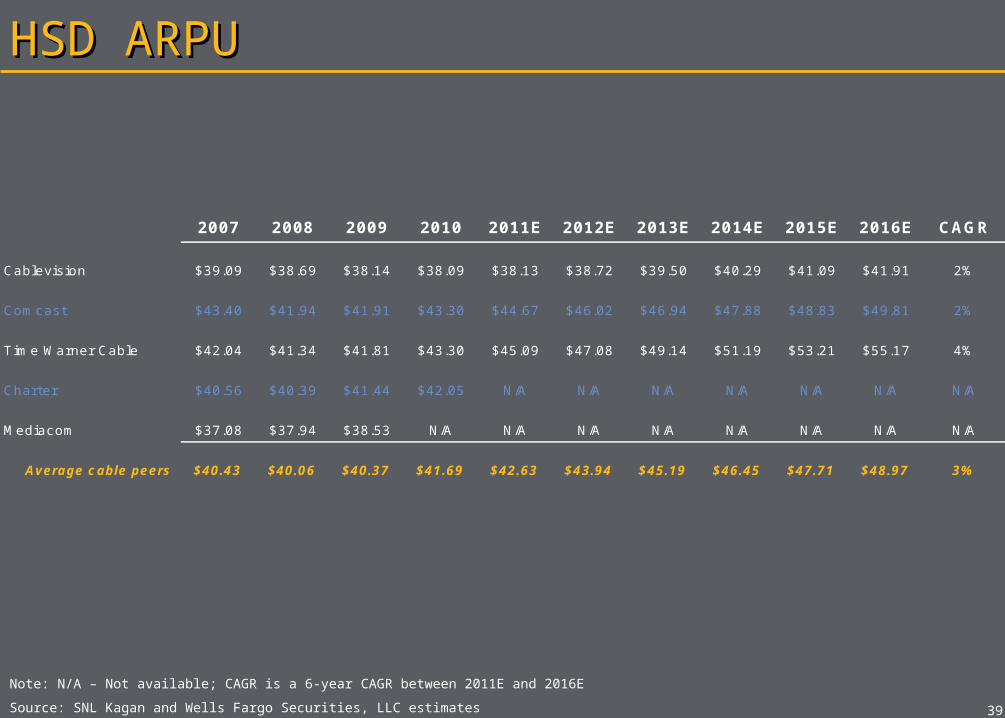

Cable HSD ARPU grew 2% in 2010Cable HSD ARPU grew 2% in 2010

3939

HSD ARPUHSD ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

2007 2008 2009 2010 2011E 2012E 2013E 2014E 2015E 2016E CAGR

Cablevision $39.09 $38.69 $38.14 $38.09 $38.13 $38.72 $39.50 $40.29 $41.09 $41.91 2%

Comcast $43.40 $41.94 $41.91 $43.30 $44.67 $46.02 $46.94 $47.88 $48.83 $49.81 2%

Time Warner Cable $42.04 $41.34 $41.81 $43.30 $45.09 $47.08 $49.14 $51.19 $53.21 $55.17 4%

Charter $40.56 $40.39 $41.44 $42.05 N/A N/A N/A N/A N/A N/A N/A

Mediacom $37.08 $37.94 $38.53 N/A N/A N/A N/A N/A N/A N/A N/A

Average cable peers $40.43 $40.06 $40.37 $41.69 $42.63 $43.94 $45.19 $46.45 $47.71 $48.97 3%

Note: N/A – Not available; CAGR is a 6-year CAGR between 2011E and 2016E

4040

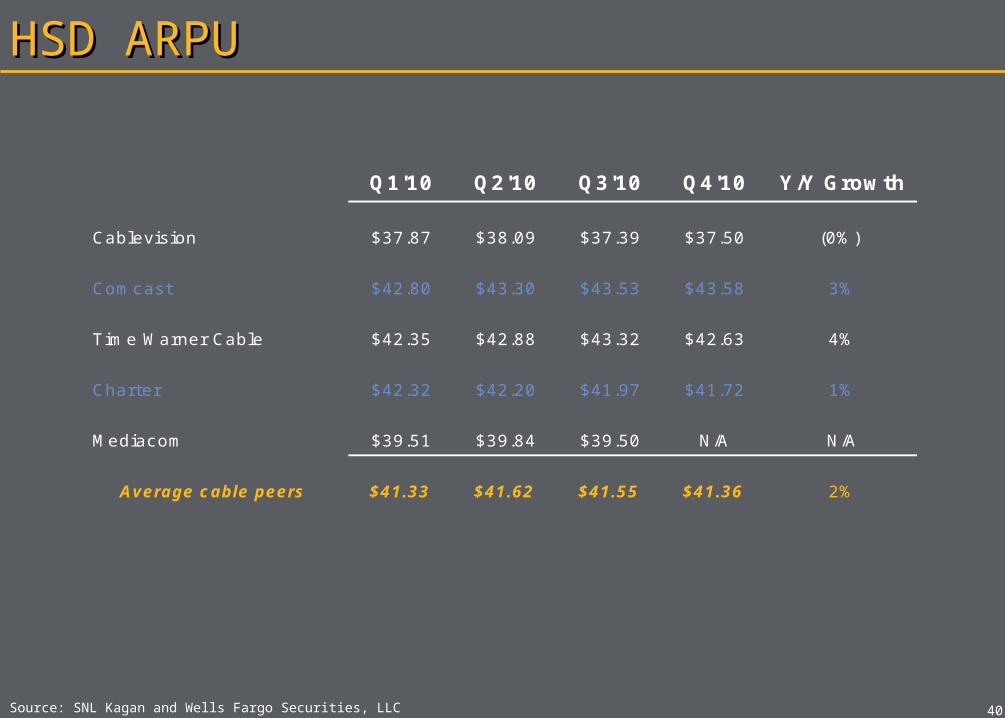

HSD ARPUHSD ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Q1'10 Q2'10 Q3'10 Q4'10 Y/Y Growth

Cablevision $37.87 $38.09 $37.39 $37.50 (0%)

Comcast $42.80 $43.30 $43.53 $43.58 3%

Time Warner Cable $42.35 $42.88 $43.32 $42.63 4%

Charter $42.32 $42.20 $41.97 $41.72 1%

Mediacom $39.51 $39.84 $39.50 N/A N/A

Average cable peers $41.33 $41.62 $41.55 $41.36 2%

TELEPHONYTELEPHONY

4242

TELEPHONY ARPUTELEPHONY ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Avera

ge T

ele

phony A

RPU

Avera

ge T

ele

phony A

RPU

Y/Y

Gro

wth

Y/Y

Gro

wth

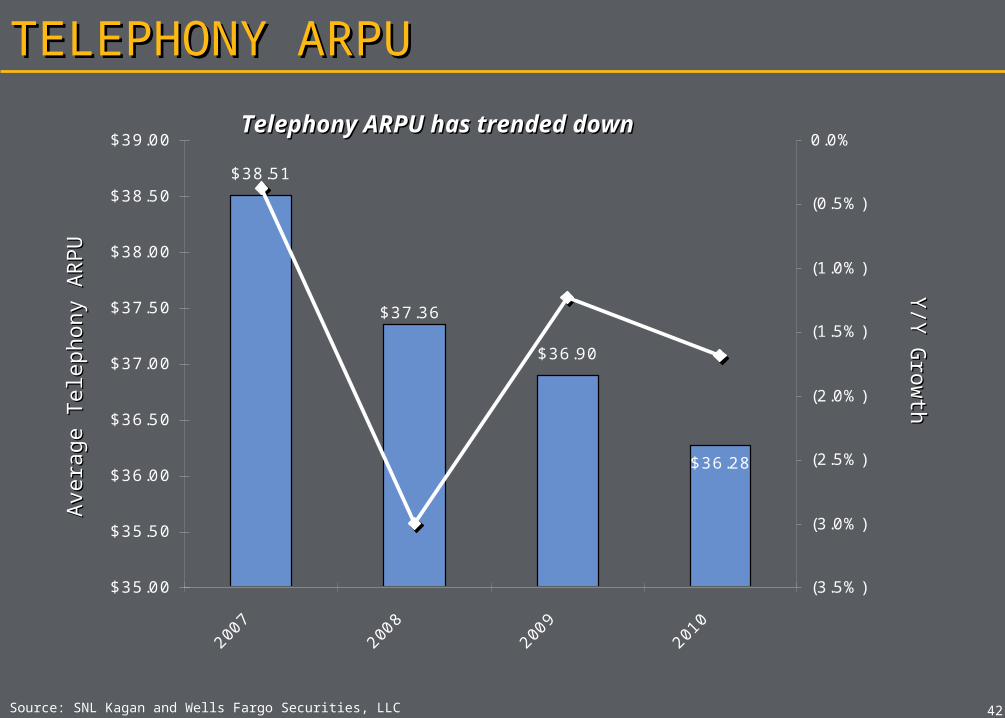

$38.51

$36.90

$36.28

$37.36

$35.00

$35.50

$36.00

$36.50

$37.00

$37.50

$38.00

$38.50

$39.00

2007

2008

2009

2010

(3.5%)

(3.0%)

(2.5%)

(2.0%)

(1.5%)

(1.0%)

(0.5%)

0.0%Telephony ARPU has trended downTelephony ARPU has trended down

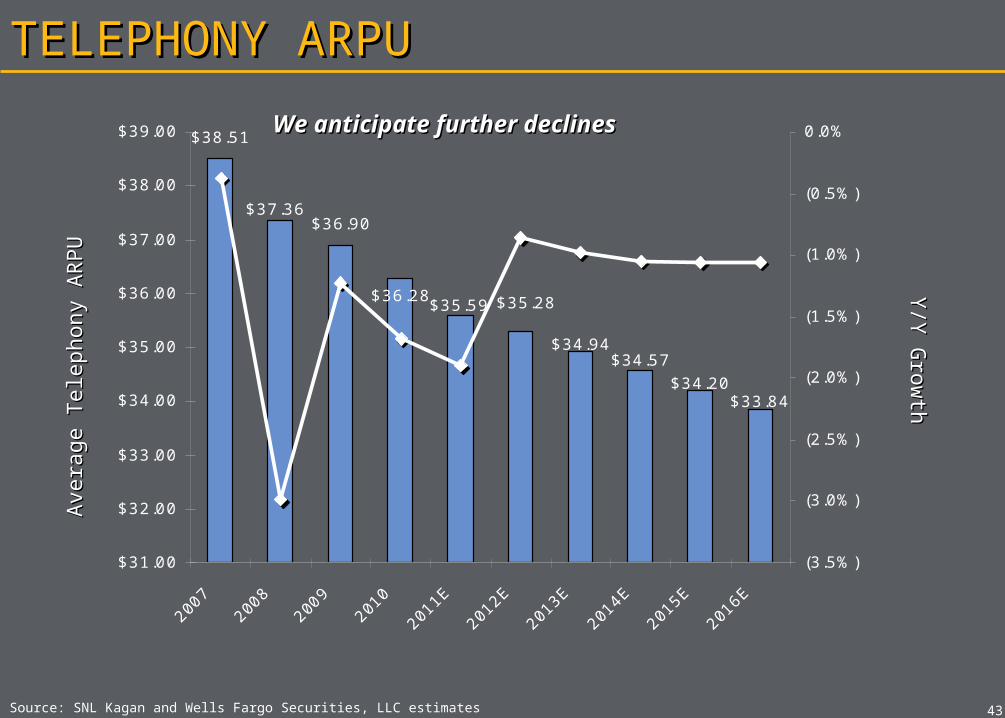

$38.51

$36.90

$36.28

$34.57

$33.84

$35.28

$34.94

$37.36

$35.59

$34.20

$31.00

$32.00

$33.00

$34.00

$35.00

$36.00

$37.00

$38.00

$39.00

2007

2008

2009

2010

2011E

2012E

2013E

2014E

2015E

2016E

(3.5%)

(3.0%)

(2.5%)

(2.0%)

(1.5%)

(1.0%)

(0.5%)

0.0%

4343

TELEPHONY ARPUTELEPHONY ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Y/Y

Gro

wth

Y/Y

Gro

wth

Avera

ge T

ele

phony A

RPU

Avera

ge T

ele

phony A

RPU

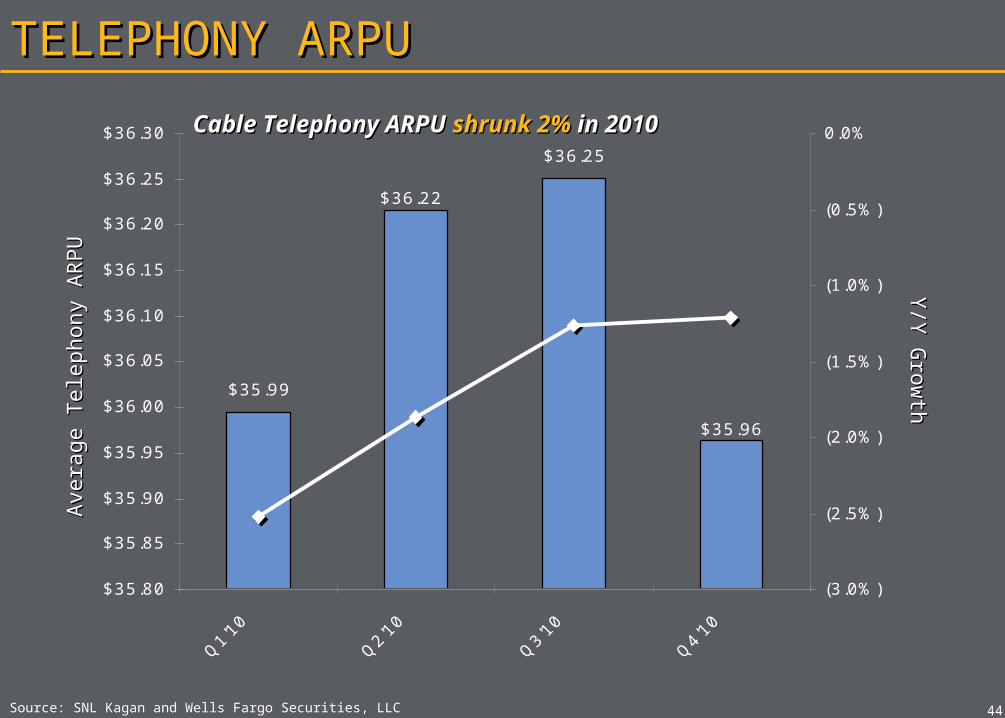

We anticipate further declinesWe anticipate further declines

$35.99

$36.25

$36.22

$35.96

$35.80

$35.85

$35.90

$35.95

$36.00

$36.05

$36.10

$36.15

$36.20

$36.25

$36.30

Q1'1

0

Q2'1

0

Q3'1

0

Q4'1

0

(3.0%)

(2.5%)

(2.0%)

(1.5%)

(1.0%)

(0.5%)

0.0%

4444

TELEPHONY ARPUTELEPHONY ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Avera

ge T

ele

phony A

RPU

Avera

ge T

ele

phony A

RPU

Y/Y

Gro

wth

Y/Y

Gro

wth

Cable Telephony ARPU Cable Telephony ARPU shrunk 2%shrunk 2% in 2010 in 2010

4545

TELEPHONY ARPUTELEPHONY ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Note: N/A – Not available; CAGR is a 6-year CAGR between 2011E and 2016E

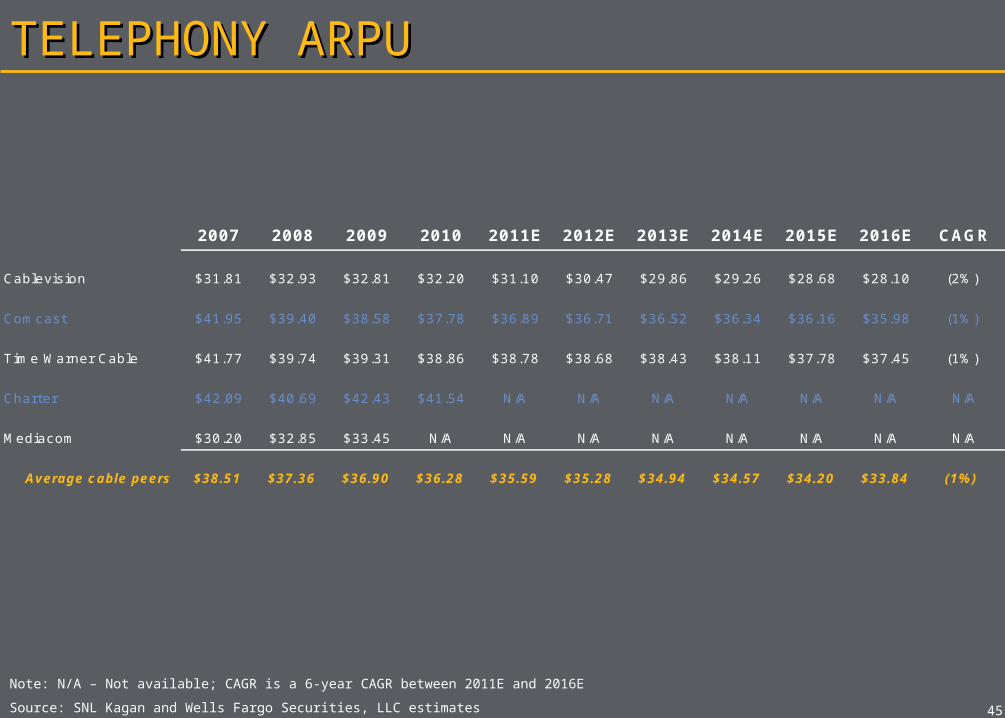

2007 2008 2009 2010 2011E 2012E 2013E 2014E 2015E 2016E CAGR

Cablevision $31.81 $32.93 $32.81 $32.20 $31.10 $30.47 $29.86 $29.26 $28.68 $28.10 (2%)

Comcast $41.95 $39.40 $38.58 $37.78 $36.89 $36.71 $36.52 $36.34 $36.16 $35.98 (1%)

Time Warner Cable $41.77 $39.74 $39.31 $38.86 $38.78 $38.68 $38.43 $38.11 $37.78 $37.45 (1%)

Charter $42.09 $40.69 $42.43 $41.54 N/A N/A N/A N/A N/A N/A N/A

Mediacom $30.20 $32.85 $33.45 N/A N/A N/A N/A N/A N/A N/A N/A

Average cable peers $38.51 $37.36 $36.90 $36.28 $35.59 $35.28 $34.94 $34.57 $34.20 $33.84 (1%)

4646

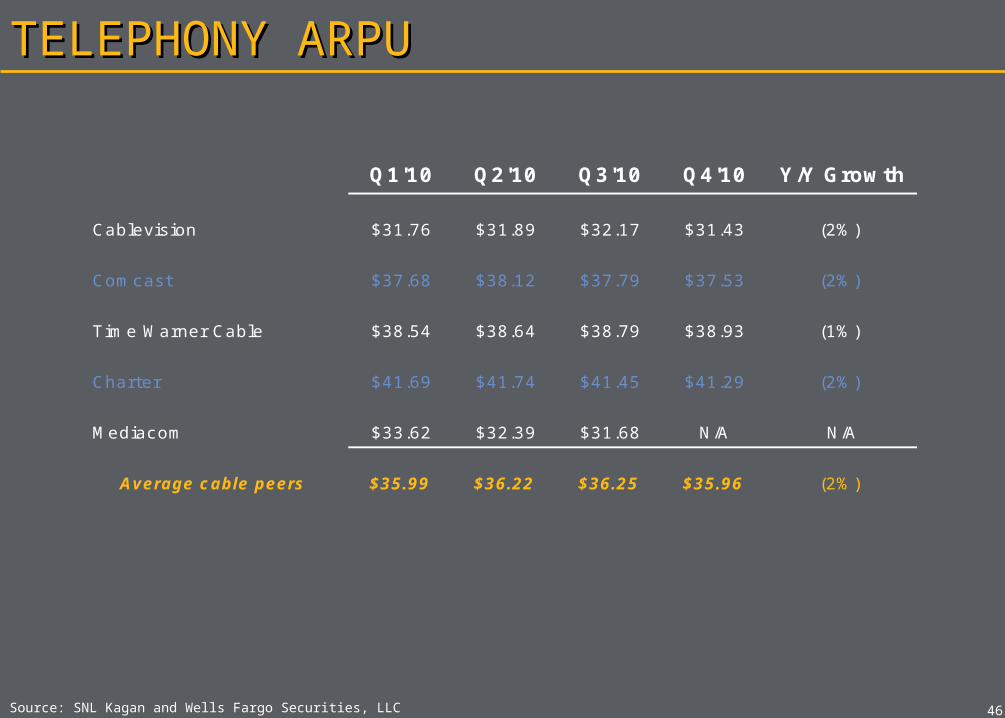

TELEPHONY ARPUTELEPHONY ARPU

Source: SNL Kagan and Wells Fargo Securities, LLC

Q1'10 Q2'10 Q3'10 Q4'10 Y/Y Growth

Cablevision $31.76 $31.89 $32.17 $31.43 (2%)

Comcast $37.68 $38.12 $37.79 $37.53 (2%)

Time Warner Cable $38.54 $38.64 $38.79 $38.93 (1%)

Charter $41.69 $41.74 $41.45 $41.29 (2%)

Mediacom $33.62 $32.39 $31.68 N/A N/A

Average cable peers $35.99 $36.22 $36.25 $35.96 (2%)

4747

2010 THEMES2010 THEMES

TITLE 2TITLE 2

OVER THE TOPOVER THE TOP

THE ECONOMYTHE ECONOMY

COMCAST-NBCUCOMCAST-NBCU

TITLE 2TITLE 2

4949

TITLE 2TITLE 2

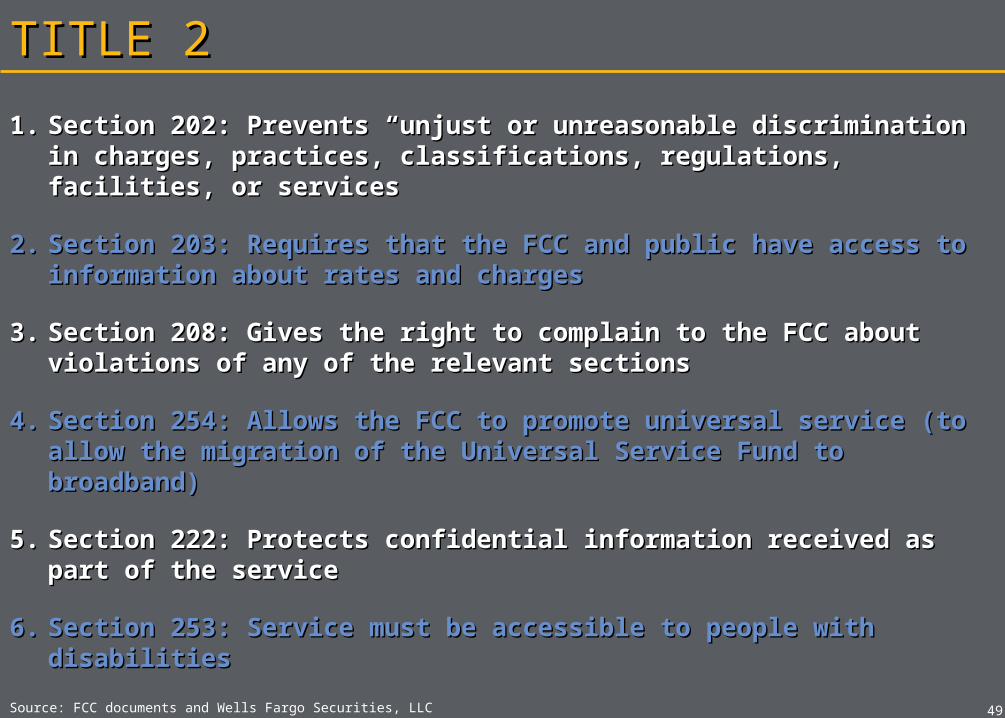

1.1. Section 202: Prevents “unjust or unreasonable discrimination Section 202: Prevents “unjust or unreasonable discrimination in charges, practices, classifications, regulations, facilities, or in charges, practices, classifications, regulations, facilities, or servicesservices

2.2. Section 203: Requires that the FCC and public have access to Section 203: Requires that the FCC and public have access to information about rates and chargesinformation about rates and charges

3.3. Section 208: Gives the right to complain to the FCC about Section 208: Gives the right to complain to the FCC about violations of any of the relevant sectionsviolations of any of the relevant sections

4.4. Section 254: Allows the FCC to promote universal service (to Section 254: Allows the FCC to promote universal service (to allow the migration of the Universal Service Fund to allow the migration of the Universal Service Fund to broadband)broadband)

5.5. Section 222: Protects confidential information received as Section 222: Protects confidential information received as part of the servicepart of the service

6.6. Section 253: Service must be accessible to people with Section 253: Service must be accessible to people with disabilitiesdisabilities

Source: FCC documents and Wells Fargo Securities, LLC

5050

TITLE 2 LITETITLE 2 LITE

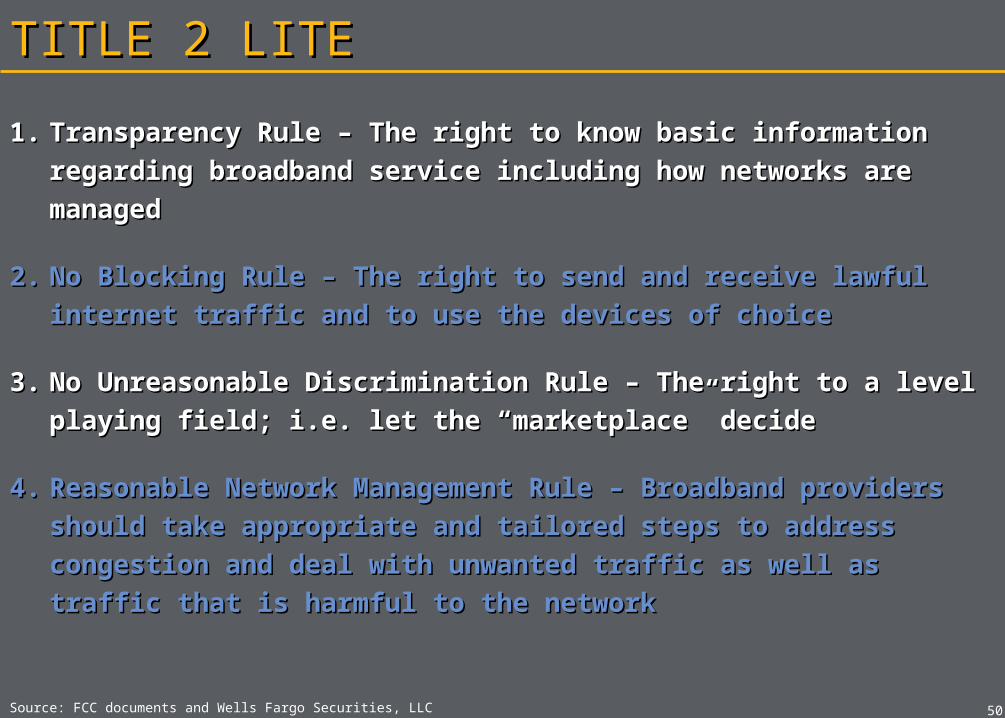

1.1. Transparency Rule – The right to know basic information Transparency Rule – The right to know basic information

regarding broadband service including how networks are regarding broadband service including how networks are

managedmanaged

2.2. No Blocking Rule – The right to send and receive lawful No Blocking Rule – The right to send and receive lawful

internet traffic and to use the devices of choiceinternet traffic and to use the devices of choice

3.3. No Unreasonable Discrimination Rule – The right to a level No Unreasonable Discrimination Rule – The right to a level

playing field; i.e. let the “marketplace” decideplaying field; i.e. let the “marketplace” decide

4.4. Reasonable Network Management Rule – Broadband providers Reasonable Network Management Rule – Broadband providers

should take appropriate and tailored steps to address should take appropriate and tailored steps to address

congestion and deal with unwanted traffic as well as traffic congestion and deal with unwanted traffic as well as traffic

that is harmful to the networkthat is harmful to the network

Source: FCC documents and Wells Fargo Securities, LLC

5151

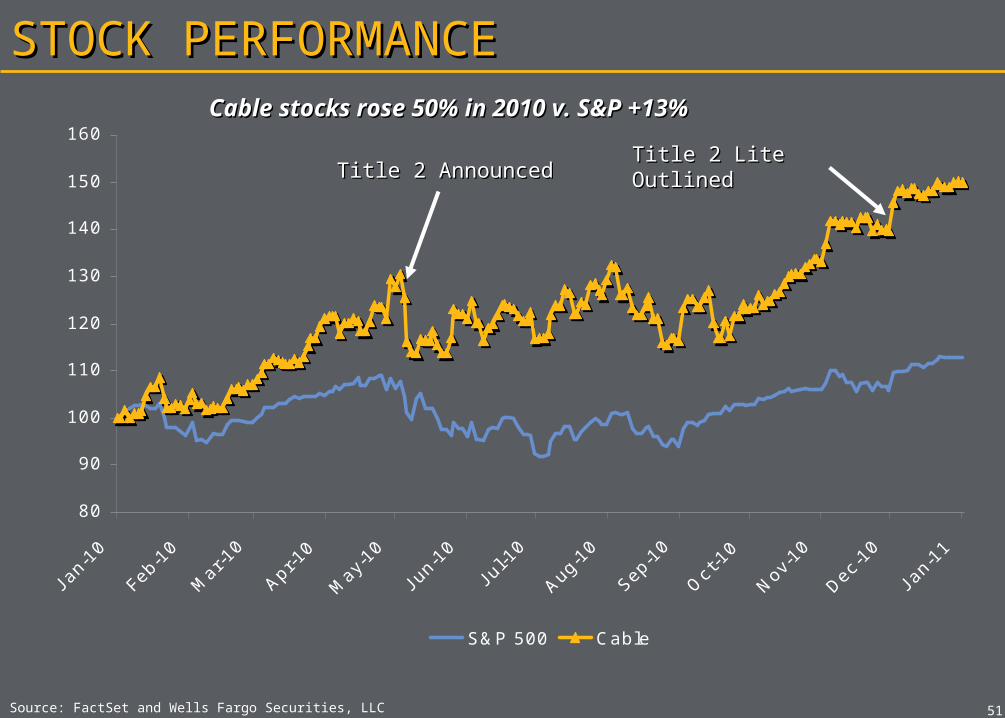

STOCK PERFORMANCESTOCK PERFORMANCE

Source: FactSet and Wells Fargo Securities, LLC

80

90

100

110

120

130

140

150

160

J an-

10

Feb-

10

Mar

-10

Apr-1

0

May

-10

J un-

10

J ul-1

0

Aug-1

0

Sep-1

0

Oct

-10

Nov

-10

Dec-1

0

J an-

11

S&P 500 Cable

Title 2 AnnouncedTitle 2 AnnouncedTitle 2 Lite OutlinedTitle 2 Lite Outlined

Cable stocks rose 50% in 2010 v. S&P Cable stocks rose 50% in 2010 v. S&P +13%+13%

OVER THE TOPOVER THE TOP

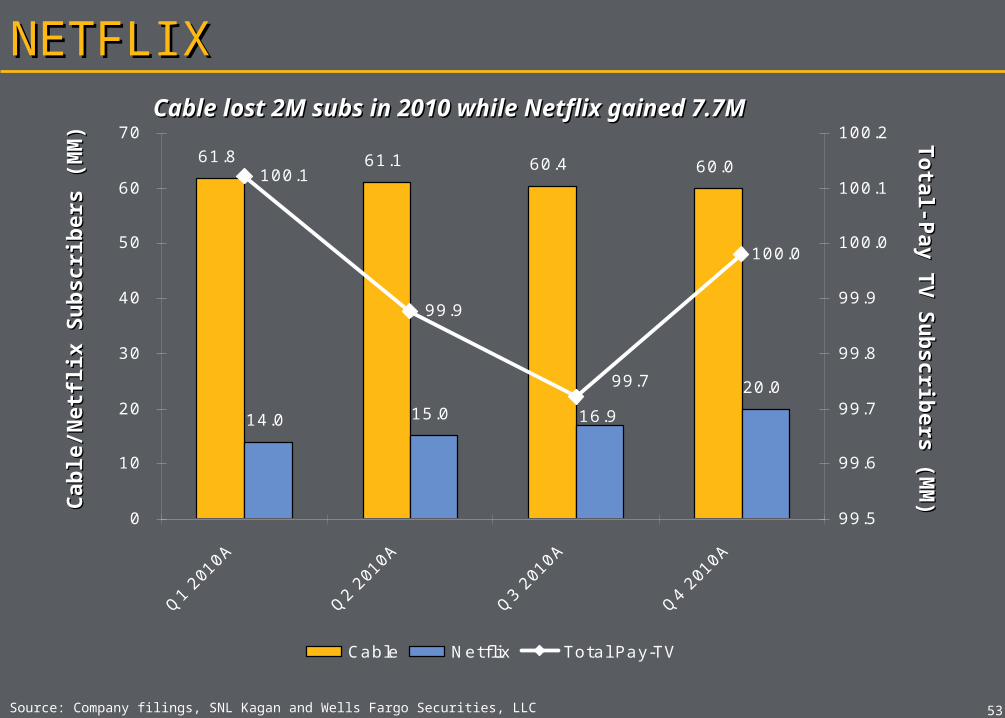

61.8 61.1 60.4 60.0

14.0 15.0

20.0

16.9

100.1

99.9

99.7

100.0

0

10

20

30

40

50

60

70

Q1 2

010A

Q2 2

010A

Q3 2

010A

Q4 2

010A

99.5

99.6

99.7

99.8

99.9

100.0

100.1

100.2

Cable Netflix Total Pay-TV

5353

NETFLIXNETFLIX

Source: Company filings, SNL Kagan and Wells Fargo Securities, LLC

Tota

l-Pay T

V S

ub

scrib

ers

(MM

)Tota

l-Pay T

V S

ub

scrib

ers

(MM

)Cab

le/N

etfl

ix S

ub

scri

bers

(M

M)

Cab

le/N

etfl

ix S

ub

scri

bers

(M

M)

Cable lost 2M subs in 2010 while Netflix gained Cable lost 2M subs in 2010 while Netflix gained 7.7M7.7M

5454

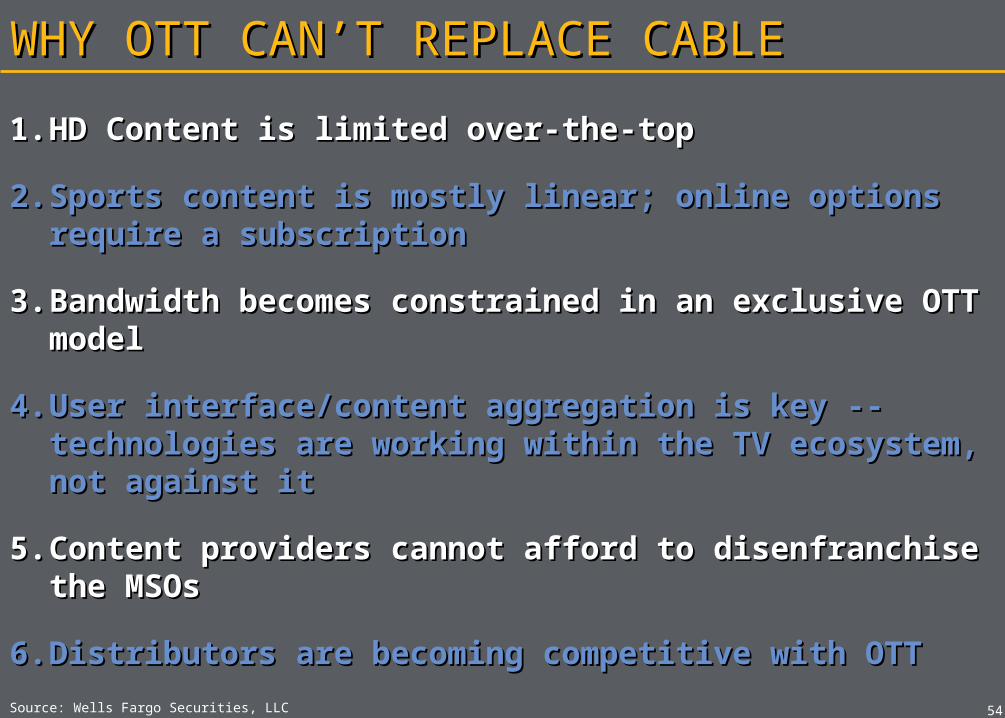

WHY OTT CAN’T REPLACE CABLEWHY OTT CAN’T REPLACE CABLE

1.1. HD Content is limited over-the-topHD Content is limited over-the-top

2.2. Sports content is mostly linear; online options Sports content is mostly linear; online options require a subscriptionrequire a subscription

3.3. Bandwidth becomes constrained in an exclusive Bandwidth becomes constrained in an exclusive OTT modelOTT model

4.4. User interface/content aggregation is key -- User interface/content aggregation is key -- technologies are working within the TV ecosystem, technologies are working within the TV ecosystem, not against itnot against it

5.5. Content providers cannot afford to disenfranchise Content providers cannot afford to disenfranchise the MSOsthe MSOs

6.6. Distributors are becoming competitive with OTTDistributors are becoming competitive with OTT

Source: Wells Fargo Securities, LLC

5555

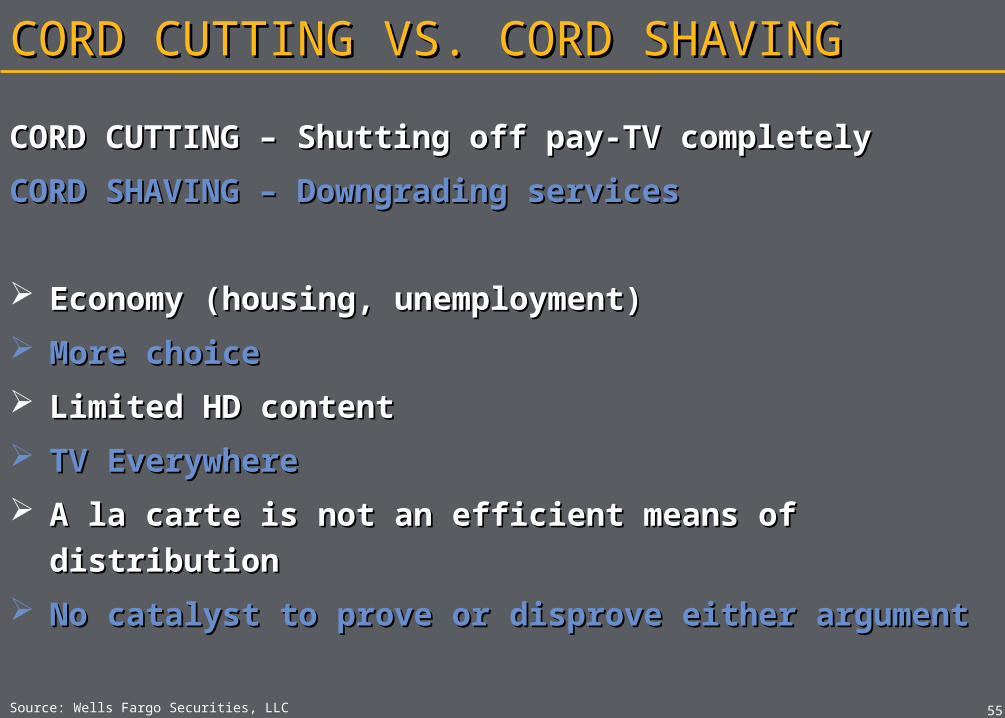

CORD CUTTING VS. CORD SHAVINGCORD CUTTING VS. CORD SHAVING

CORD CUTTING – Shutting off pay-TV completelyCORD CUTTING – Shutting off pay-TV completely

CORD SHAVING – Downgrading servicesCORD SHAVING – Downgrading services

Economy (housing, unemployment)Economy (housing, unemployment)

More choiceMore choice

Limited HD contentLimited HD content

TV EverywhereTV Everywhere

A la carte is not an efficient means of distributionA la carte is not an efficient means of distribution

No catalyst to prove or disprove either argumentNo catalyst to prove or disprove either argument

Source: Wells Fargo Securities, LLC

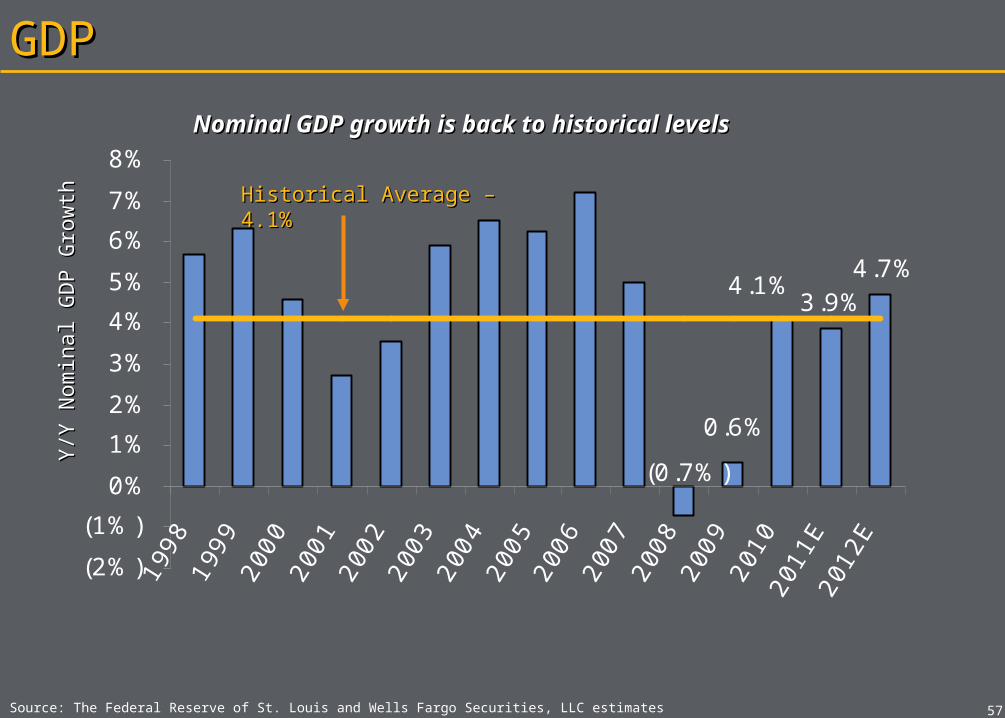

THE ECONOMYTHE ECONOMY

(0.7%)

4.1%3.9%

4.7%

0.6%

(2%)

(1%)

0%

1%

2%

3%

4%

5%

6%

7%

8%199

8199

9200

0200

1200

2200

3200

4200

5200

6200

7200

8200

9201

0201

1E

201

2E

5757

GDPGDPY/Y

Nom

inal G

DP G

row

thY/Y

Nom

inal G

DP G

row

th

Historical Average – 4.1%Historical Average – 4.1%

Source: The Federal Reserve of St. Louis and Wells Fargo Securities, LLC estimates

Nominal GDP growth is back to historical Nominal GDP growth is back to historical levelslevels

5858

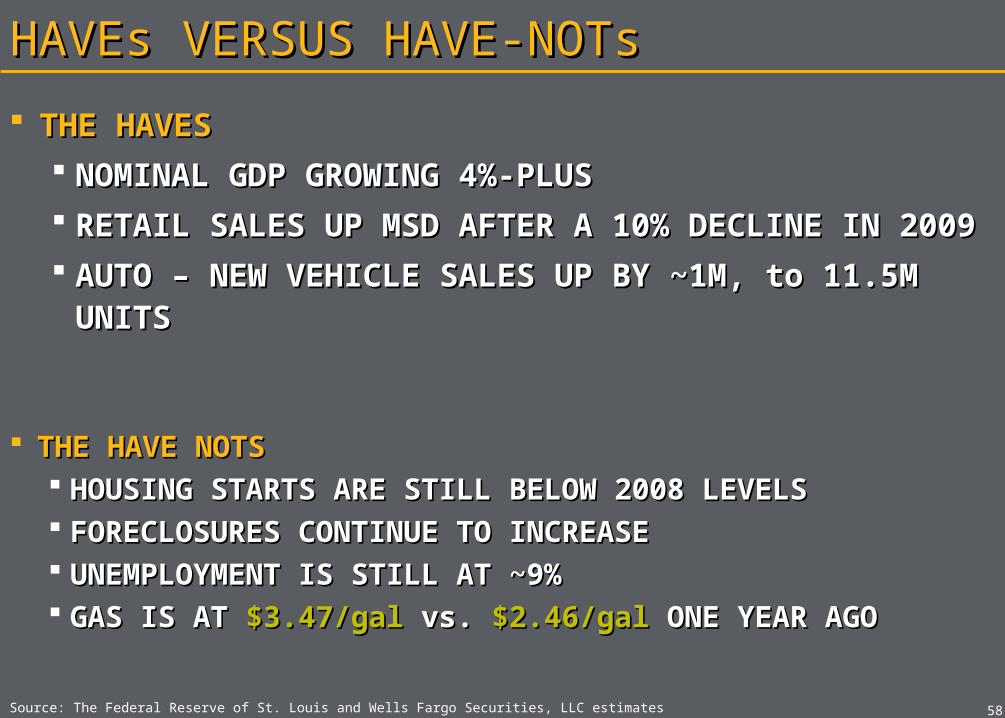

HAVEs VERSUS HAVE-NOTsHAVEs VERSUS HAVE-NOTs

THE HAVE NOTSTHE HAVE NOTS HOUSING STARTS ARE STILL BELOW 2008 LEVELSHOUSING STARTS ARE STILL BELOW 2008 LEVELS FORECLOSURES CONTINUE TO INCREASEFORECLOSURES CONTINUE TO INCREASE UNEMPLOYMENT IS STILL AT ~9%UNEMPLOYMENT IS STILL AT ~9% GAS IS AT GAS IS AT $3.47/gal$3.47/gal vs. vs. $2.46/gal$2.46/gal ONE YEAR AGO ONE YEAR AGO

THE HAVESTHE HAVES NOMINAL GDP GROWING 4%-PLUS NOMINAL GDP GROWING 4%-PLUS RETAIL SALES UP MSD AFTER A 10% DECLINE IN RETAIL SALES UP MSD AFTER A 10% DECLINE IN

20092009 AUTO – NEW VEHICLE SALES UP BY ~1M, to 11.5M AUTO – NEW VEHICLE SALES UP BY ~1M, to 11.5M

UNITSUNITS

Source: The Federal Reserve of St. Louis and Wells Fargo Securities, LLC estimates

0

500

1,000

1,500

2,000

2,500

1998199

9200

0200

1200

2200

3200

4200

5200

6200

7200

8200

9201

0

2011E

2012E

5959

HOUSING STARTSHOUSING STARTS

Source: The Federal Reserve of St. Louis and Wells Fargo Securities, LLC estimates

Historical Average – 1.4MHistorical Average – 1.4M

U.S

. H

ousi

ng S

tart

s (‘

00

0s)

U.S

. H

ousi

ng S

tart

s (‘

00

0s)

2010A: 590k2010A: 590k

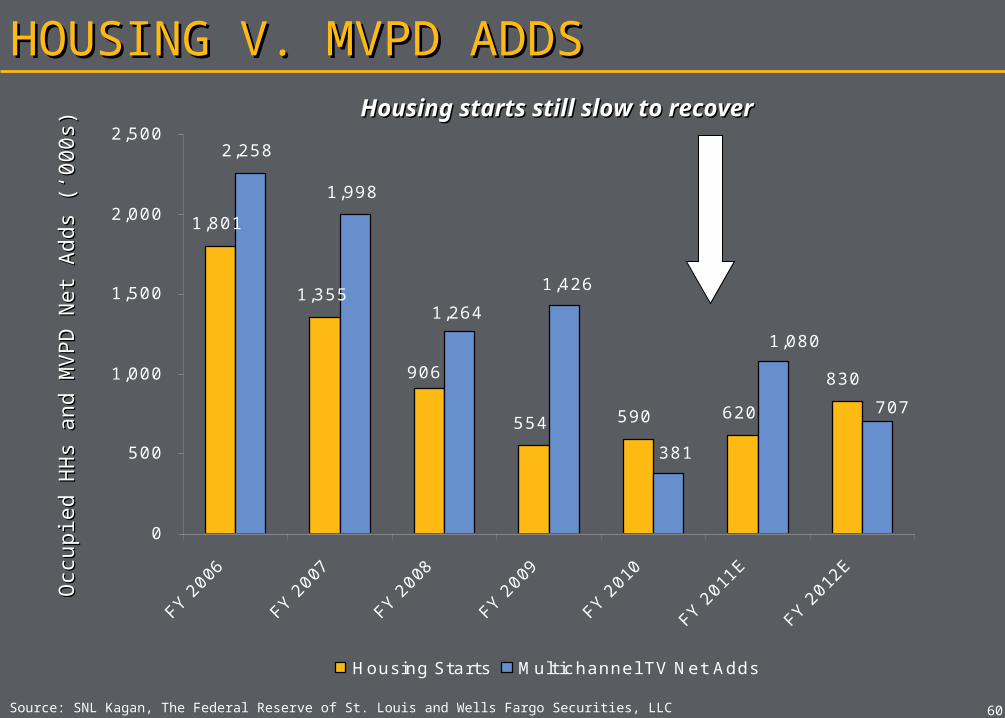

The housing market has been slow to recoverThe housing market has been slow to recover

1,801

1,355

554 590 620

830

2,258

1,998

906

1,426

381

1,264

707

1,080

0

500

1,000

1,500

2,000

2,500

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

E

FY 2012

E

Housing Starts Multichannel TV Net Adds

6060

HOUSING V. MVPD ADDSHOUSING V. MVPD ADDSO

ccupie

d H

Hs

and M

VPD

Net

Adds

(‘0

00

s)O

ccupie

d H

Hs

and M

VPD

Net

Adds

(‘0

00

s)

Source: SNL Kagan, The Federal Reserve of St. Louis and Wells Fargo Securities, LLC

Housing starts still slow to recoverHousing starts still slow to recover

0%1%2%3%4%5%6%7%8%9%

10%

1998

1999200

0200

1200

2200

3200

4200

5200

6200

7200

8200

9201

0

2011E

2012E

6161

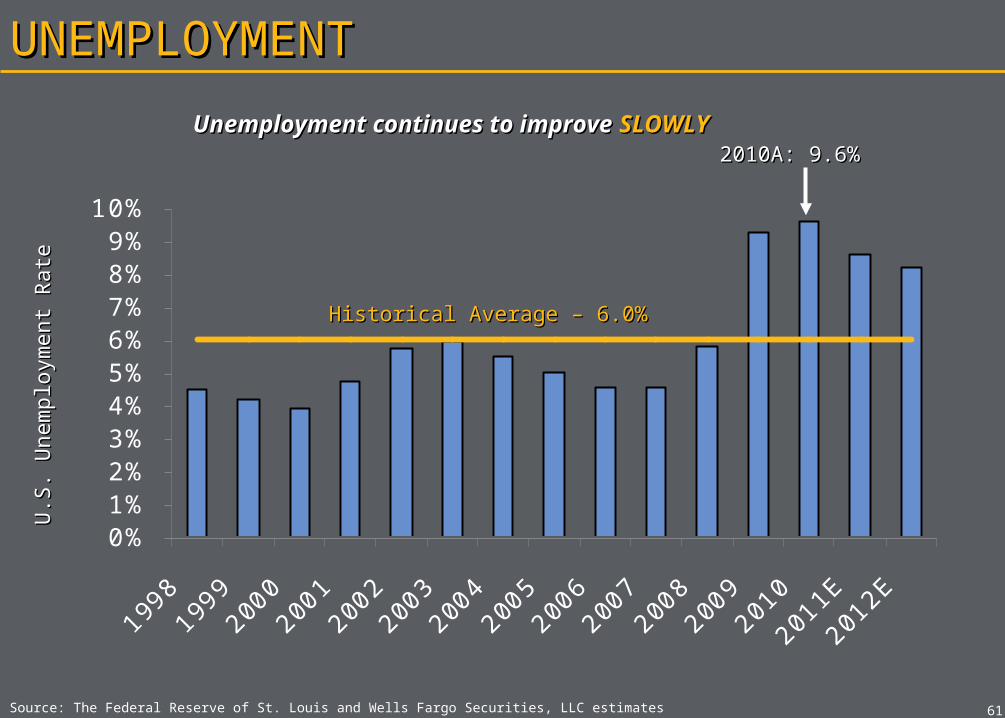

UNEMPLOYMENTUNEMPLOYMENTU

.S. U

nem

plo

ym

ent

Rate

U.S

. U

nem

plo

ym

ent

Rate

Historical Average – 6.0%Historical Average – 6.0%

2010A: 9.6%2010A: 9.6%

Source: The Federal Reserve of St. Louis and Wells Fargo Securities, LLC estimates

Unemployment continues to improve Unemployment continues to improve SLOWLYSLOWLY

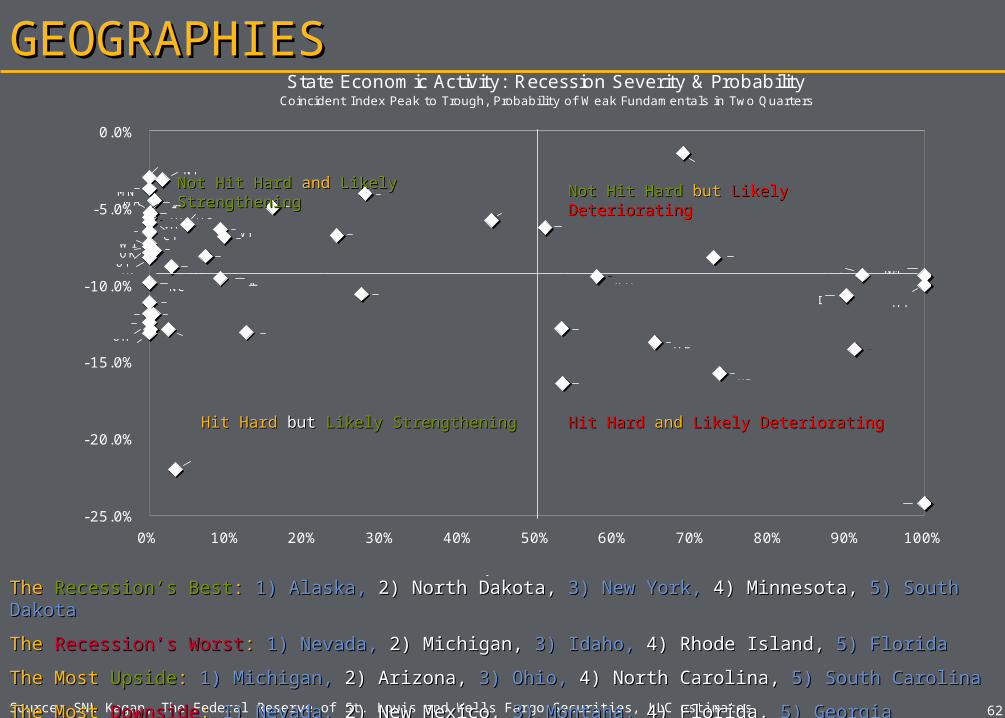

State Economic Activity: Recession Severity & ProbabilityCoincident Index Peak to Trough, Probability of Weak Fundamentals in Two Quarters

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

B - Not Severe Recession, Weak Economic Fundamentals

NV

TN

MNIA

MI

SC

IN

CA

NY

SD

NH, AR

OH

KY

NC

MA

MD

WV

OKUT

CT

DEORAL

ME

KSWY

PA

AK

LATX MS

NJ

ND

MO

HI

WA

IDRI

FL

VT

MT

NM

NE

GACO

WI

VA

C - Severe Recession, Improving Economic Fundamentals D - Severe Recession, Weak Economic Fundamentals

A - Not Severe Recession, Improving Economic Fundamentals

Probability of Weak Fundamentals

Severi

ty o

f R

ece

ssio

n

IL

AZ

State Average: -9.3%

6262

GEOGRAPHIESGEOGRAPHIES

Source: SNL Kagan, The Federal Reserve of St. Louis and Wells Fargo Securities, LLC estimates

The The Recession’s BestRecession’s Best: : 1) Alaska,1) Alaska, 2) North Dakota,2) North Dakota, 3) New York,3) New York, 4) Minnesota,4) Minnesota, 5) South Dakota5) South Dakota

The The Recession’s WorstRecession’s Worst: : 1) Nevada,1) Nevada, 2) Michigan,2) Michigan, 3) Idaho,3) Idaho, 4) Rhode Island,4) Rhode Island, 5) Florida5) Florida

The Most The Most UpsideUpside:: 1) Michigan, 1) Michigan, 2) Arizona, 2) Arizona, 3) Ohio, 3) Ohio, 4) North Carolina, 4) North Carolina, 5) South Carolina5) South Carolina

The Most The Most DownsideDownside:: 1) Nevada, 1) Nevada, 2) New Mexico, 2) New Mexico, 3) Montana, 3) Montana, 4) Florida, 4) Florida, 5) Georgia5) Georgia

Hit Hard Hit Hard and and Likely DeterioratingLikely DeterioratingHit HardHit Hard but but Likely StrengtheningLikely Strengthening

Not Hit HardNot Hit Hard butbut Likely Deteriorating Likely DeterioratingNot Hit HardNot Hit Hard andand Likely StrengtheningLikely Strengthening

6363

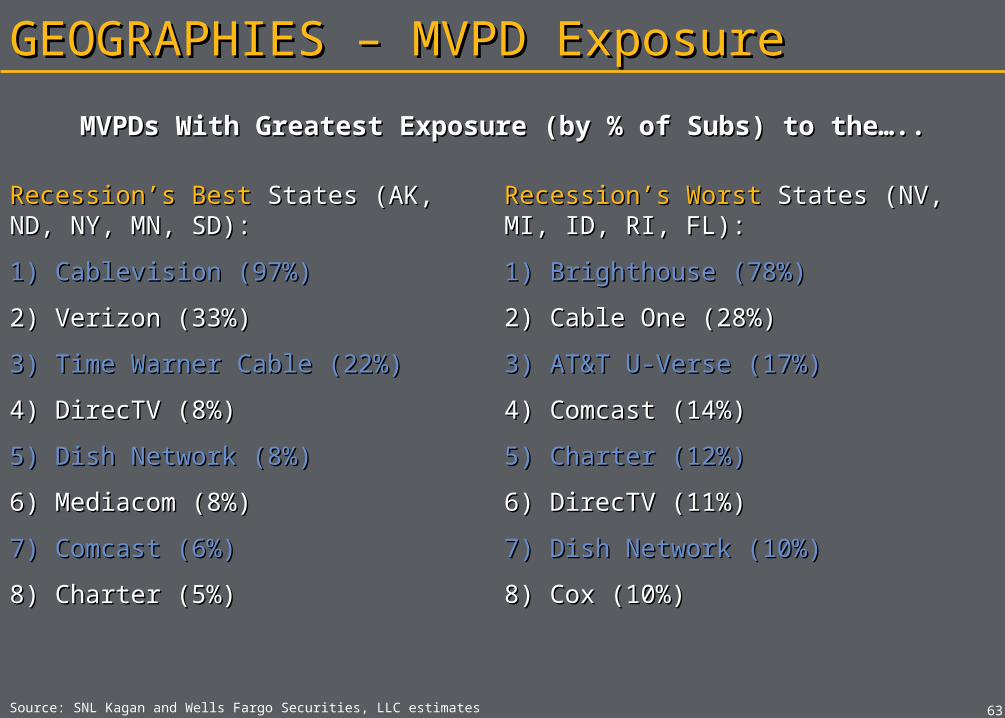

GEOGRAPHIES – MVPD ExposureGEOGRAPHIES – MVPD Exposure

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Recession’s BestRecession’s Best States (AK, ND, NY, States (AK, ND, NY, MN, SD):MN, SD):

1) Cablevision (97%)1) Cablevision (97%)

2) Verizon (33%)2) Verizon (33%)

3) Time Warner Cable (22%)3) Time Warner Cable (22%)

4) DirecTV (8%)4) DirecTV (8%)

5) Dish Network (8%)5) Dish Network (8%)

6) Mediacom (8%)6) Mediacom (8%)

7) Comcast (6%)7) Comcast (6%)

8) Charter (5%)8) Charter (5%)

Recession’s WorstRecession’s Worst States (NV, MI, ID, States (NV, MI, ID, RI, FL):RI, FL):

1) Brighthouse (78%)1) Brighthouse (78%)

2) Cable One (28%)2) Cable One (28%)

3) AT&T U-Verse (17%)3) AT&T U-Verse (17%)

4) Comcast (14%)4) Comcast (14%)

5) Charter (12%)5) Charter (12%)

6) DirecTV (11%)6) DirecTV (11%)

7) Dish Network (10%)7) Dish Network (10%)

8) Cox (10%)8) Cox (10%)

MVPDs With Greatest Exposure (by % of Subs) to the…..MVPDs With Greatest Exposure (by % of Subs) to the…..

6464

GEOGRAPHIES – MVPD ExposureGEOGRAPHIES – MVPD Exposure

Source: SNL Kagan and Wells Fargo Securities, LLC estimates

Most UpsideMost Upside States (MI, AZ, OH, NC, States (MI, AZ, OH, NC, SC):SC):

1) Insight (32%)1) Insight (32%)

2) Time Warner Cable (27%)2) Time Warner Cable (27%)

3) Cox (24%)3) Cox (24%)

4) Charter (19%)4) Charter (19%)

5) AT&T U-Verse (15%)5) AT&T U-Verse (15%)

6) DirecTV (14)6) DirecTV (14)

7) Dish Network (13%)7) Dish Network (13%)

8) Verizon FiOS (0%)8) Verizon FiOS (0%)

Most DownsideMost Downside States (NV, NM, MT, States (NV, NM, MT, FL, GA):FL, GA):

1) Brighthouse (74%)1) Brighthouse (74%)

2) Mediacom (15%)2) Mediacom (15%)

3) Comcast (10%)3) Comcast (10%)

4) AT&T U-Verse (9%)4) AT&T U-Verse (9%)

5) DirecTV (9%)5) DirecTV (9%)

6) Cox (9%)6) Cox (9%)

7) Dish Network (8%)7) Dish Network (8%)

8) Verizon FiOS (7%)8) Verizon FiOS (7%)

MVPDs With Greatest Exposure (by % of Subs) to the…..MVPDs With Greatest Exposure (by % of Subs) to the…..

COMCAST-NBCUCOMCAST-NBCU

6666

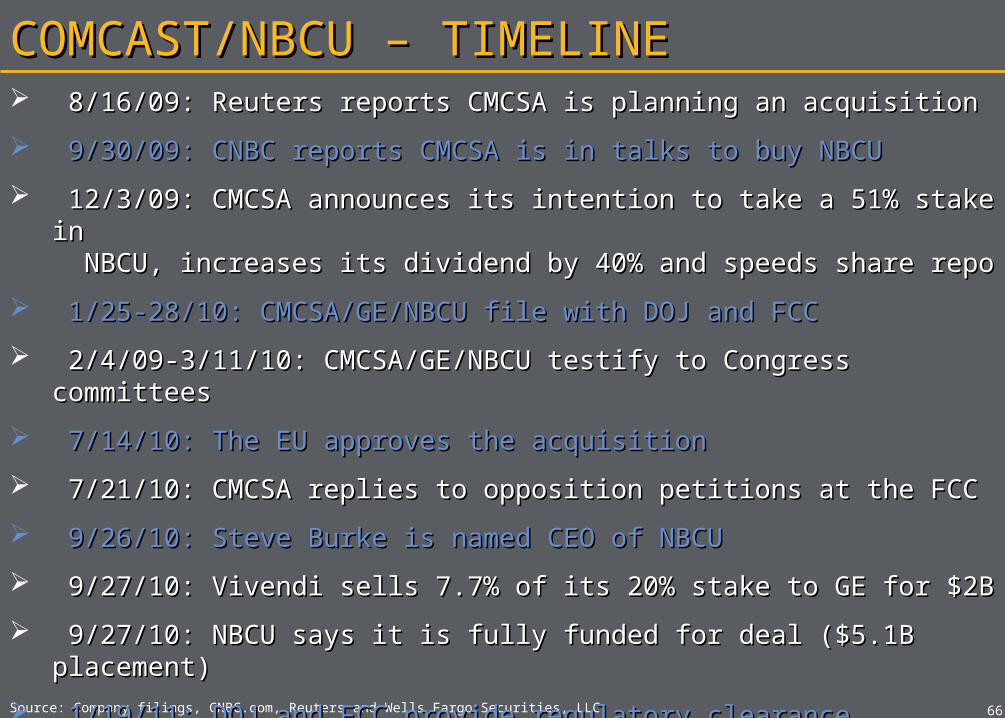

COMCAST/NBCU – TIMELINECOMCAST/NBCU – TIMELINE

Source: Company filings, CNBC.com, Reuters and Wells Fargo Securities, LLC

8/16/09: Reuters reports CMCSA is planning an acquisition8/16/09: Reuters reports CMCSA is planning an acquisition

9/30/09: CNBC reports CMCSA is in talks to buy NBCU9/30/09: CNBC reports CMCSA is in talks to buy NBCU

12/3/09: CMCSA announces its intention to take a 51% stake in12/3/09: CMCSA announces its intention to take a 51% stake in NBCU, increases its dividend by 40% and speeds share repo NBCU, increases its dividend by 40% and speeds share repo

1/25-28/10: CMCSA/GE/NBCU file with DOJ and FCC1/25-28/10: CMCSA/GE/NBCU file with DOJ and FCC

2/4/09-3/11/10: CMCSA/GE/NBCU testify to Congress committees2/4/09-3/11/10: CMCSA/GE/NBCU testify to Congress committees

7/14/10: The EU approves the acquisition7/14/10: The EU approves the acquisition

7/21/10: CMCSA replies to opposition petitions at the FCC7/21/10: CMCSA replies to opposition petitions at the FCC

9/26/10: Steve Burke is named CEO of NBCU9/26/10: Steve Burke is named CEO of NBCU

9/27/10: Vivendi sells 7.7% of its 20% stake to GE for $2B9/27/10: Vivendi sells 7.7% of its 20% stake to GE for $2B

9/27/10: NBCU says it is fully funded for deal ($5.1B placement)9/27/10: NBCU says it is fully funded for deal ($5.1B placement)

1/19/11: DOJ and FCC provide regulatory clearance1/19/11: DOJ and FCC provide regulatory clearance

1/28/11: CMCSA/NBCU officially closed1/28/11: CMCSA/NBCU officially closed

60

70

80

90

100

110

120

130

140

150

160

J an-

09

Mar

-09

May

-09

J ul-0

9

Sep-0

9

Nov

-09

J an-

10

Mar

-10

May

-10

J ul-1

0

Sep-1

0

Nov

-10

J an-

11

Mar

-11

S&P 500 CMCSA

6767

COMCAST/NBCU – STOCK PRICECOMCAST/NBCU – STOCK PRICE

CNBC reports that CMCSA is planning to CNBC reports that CMCSA is planning to buy 51% of NBCUbuy 51% of NBCU

CMCSA announces it will CMCSA announces it will acquire 51% of NBCUacquire 51% of NBCU

GE reports Q3 reports GE reports Q3 reports and that NBCU deal will and that NBCU deal will close by year-endclose by year-end

Deal officially Deal officially closescloses

Source: FactSet and Wells Fargo Securities, LLC

CMCSA is +57% since the deal was “leaked” v. the S&P, CMCSA is +57% since the deal was “leaked” v. the S&P, +27%+27%

6868

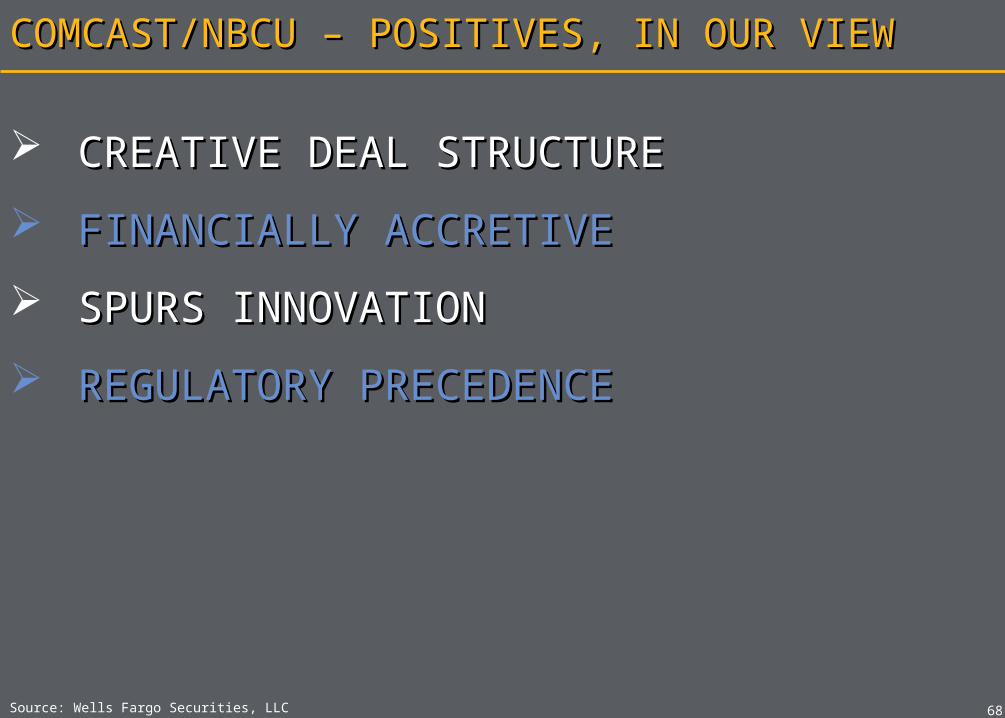

COMCAST/NBCU – POSITIVES, IN OUR VIEW COMCAST/NBCU – POSITIVES, IN OUR VIEW

Source: Wells Fargo Securities, LLC

CREATIVE DEAL STRUCTURECREATIVE DEAL STRUCTURE

FINANCIALLY ACCRETIVEFINANCIALLY ACCRETIVE

SPURS INNOVATIONSPURS INNOVATION

REGULATORY PRECEDENCEREGULATORY PRECEDENCE

6969

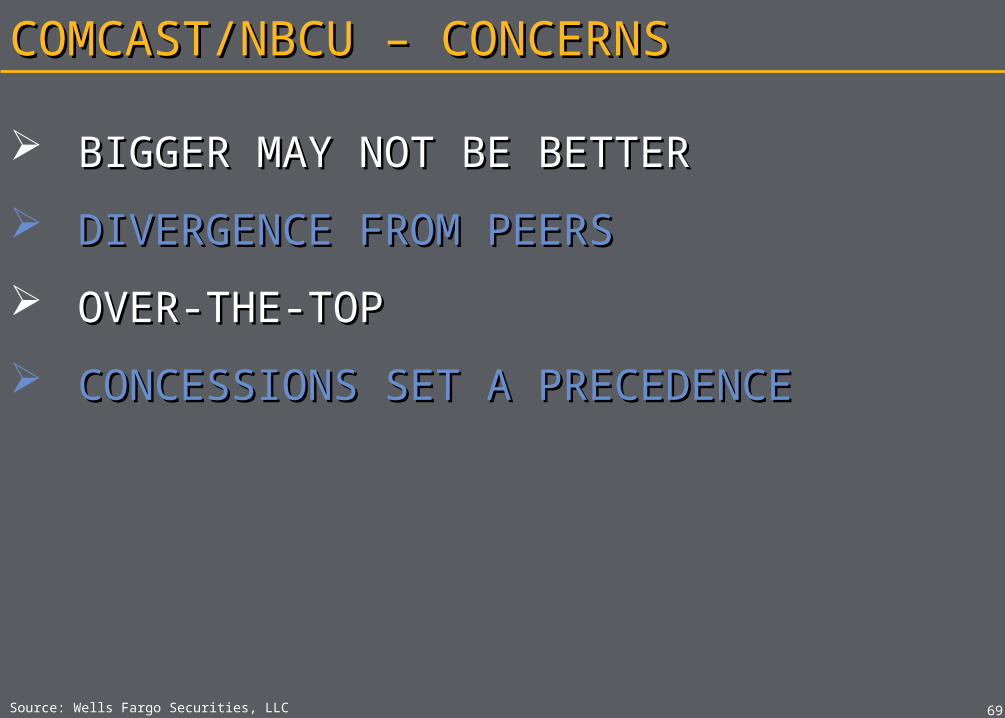

COMCAST/NBCU – CONCERNS COMCAST/NBCU – CONCERNS

Source: Wells Fargo Securities, LLC

BIGGER MAY NOT BE BETTERBIGGER MAY NOT BE BETTER

DIVERGENCE FROM PEERSDIVERGENCE FROM PEERS

OVER-THE-TOPOVER-THE-TOP

CONCESSIONS SET A PRECEDENCECONCESSIONS SET A PRECEDENCE

7070Source: Wells Fargo Securities, LLCSource: Wells Fargo Securities, LLC

OPPORTUNITIESOPPORTUNITIES

7171

RESIDENTIAL HSDRESIDENTIAL HSD

Source: Wells Fargo Securities, LLCSource: Wells Fargo Securities, LLC

ARPUARPU

USAGE BASED PRICINGUSAGE BASED PRICING

‘ ‘NAKED’ HSD SUBSCRIBERSNAKED’ HSD SUBSCRIBERS

TVE – WHY IS IT IMPORTANT?TVE – WHY IS IT IMPORTANT?

Source: Company websites and Wells Fargo Securities, LLCSource: Company websites and Wells Fargo Securities, LLC

CUSTOMER RETENTIONCUSTOMER RETENTION

POTENTIAL SUBSCRIPTION MODELPOTENTIAL SUBSCRIPTION MODEL

ADDITIONAL ADVERTISING $sADDITIONAL ADVERTISING $s

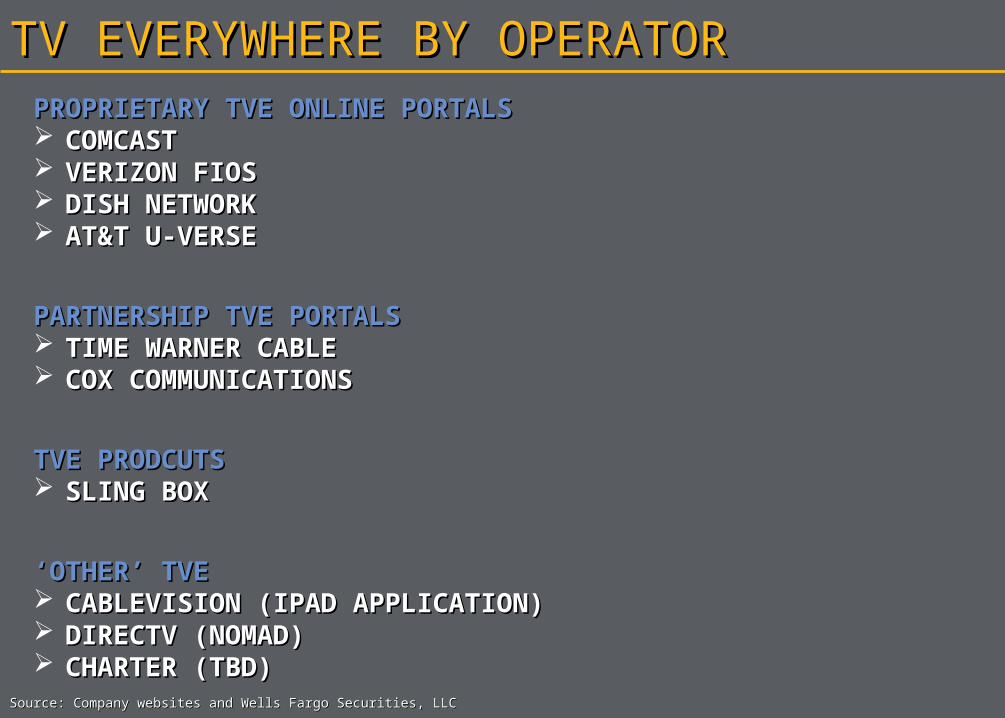

TV EVERYWHERE BY OPERATORTV EVERYWHERE BY OPERATORPROPRIETARY TVE ONLINE PORTALSPROPRIETARY TVE ONLINE PORTALS COMCASTCOMCAST VERIZON FIOSVERIZON FIOS DISH NETWORKDISH NETWORK AT&T U-VERSEAT&T U-VERSE

PARTNERSHIP TVE PORTALS PARTNERSHIP TVE PORTALS TIME WARNER CABLETIME WARNER CABLE COX COMMUNICATIONSCOX COMMUNICATIONS

TVE PRODCUTSTVE PRODCUTS SLING BOXSLING BOX

‘‘OTHER’ TVEOTHER’ TVE CABLEVISION (IPAD APPLICATION)CABLEVISION (IPAD APPLICATION) DIRECTV (NOMAD)DIRECTV (NOMAD) CHARTER (TBD)CHARTER (TBD)

Source: Company websites and Wells Fargo Securities, LLCSource: Company websites and Wells Fargo Securities, LLC

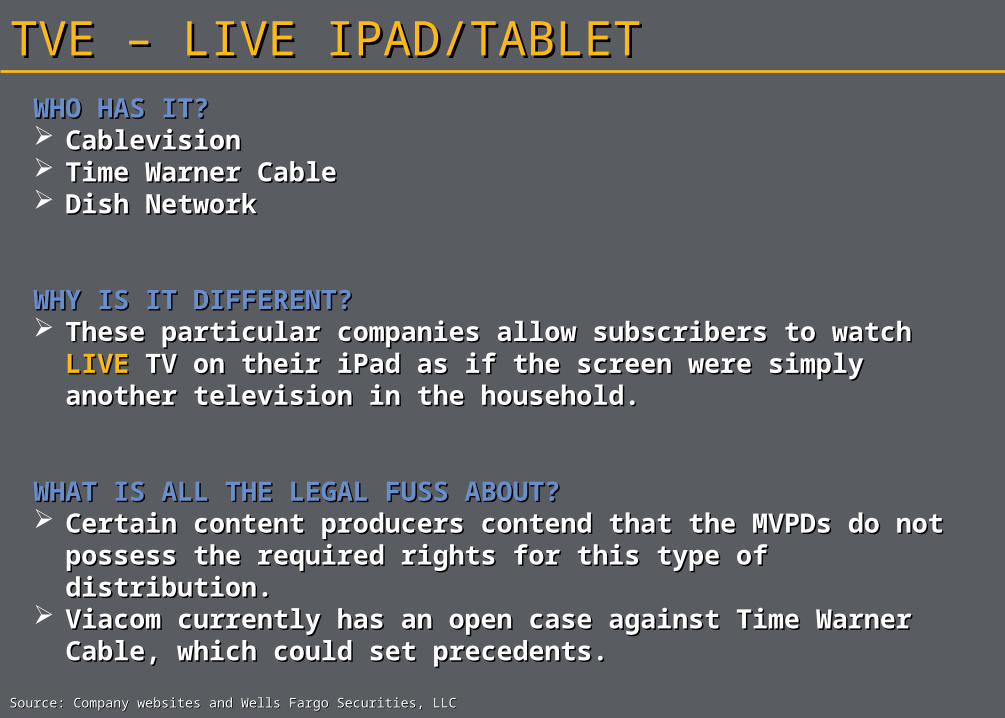

TVE – LIVE IPAD/TABLETTVE – LIVE IPAD/TABLETWHO HAS IT?WHO HAS IT? CablevisionCablevision Time Warner CableTime Warner Cable Dish NetworkDish Network

WHY IS IT DIFFERENT?WHY IS IT DIFFERENT? These particular companies allow subscribers to watch These particular companies allow subscribers to watch LIVELIVE

TV on their iPad as if the screen were simply another TV on their iPad as if the screen were simply another television in the household.television in the household.

WHAT IS ALL THE LEGAL FUSS ABOUT?WHAT IS ALL THE LEGAL FUSS ABOUT? Certain content producers contend that the MVPDs do not Certain content producers contend that the MVPDs do not

possess the required rights for this type of distribution.possess the required rights for this type of distribution. Viacom currently has an open case against Time Warner Viacom currently has an open case against Time Warner

Cable, which could set precedents.Cable, which could set precedents.

Source: Company websites and Wells Fargo Securities, LLCSource: Company websites and Wells Fargo Securities, LLC

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

'91-'9

2

'92-'9

3

'93-'9

4

'94-'9

5

'95-'9

6

'96-'9

7

'97-'9

8

'98-'9

9

'99-'0

0

'00-'0

1

'01-'0

2

'02-'0

3

'03-'0

4

'04-'0

5

'05-'0

6

'06-'0

7

'07-'0

8

'08-'0

9

'09-'1

0

0

10

20

30

40

50

60

Cable Ad $s Broadcast Ad $s

Cable Ratings ABC/CBS/NBC Broadcast Ratings

ADVERTISINGADVERTISING

Source: Company websites and Wells Fargo Securities, LLCSource: Company websites and Wells Fargo Securities, LLC

Ad S

pend (

$M

M)

Ad S

pend (

$M

M)

Avera

ge P

rimetim

e V

iew

ersh

ip (M

Ms o

f HH

s)A

vera

ge P

rimetim

e V

iew

ersh

ip (M

Ms o

f HH

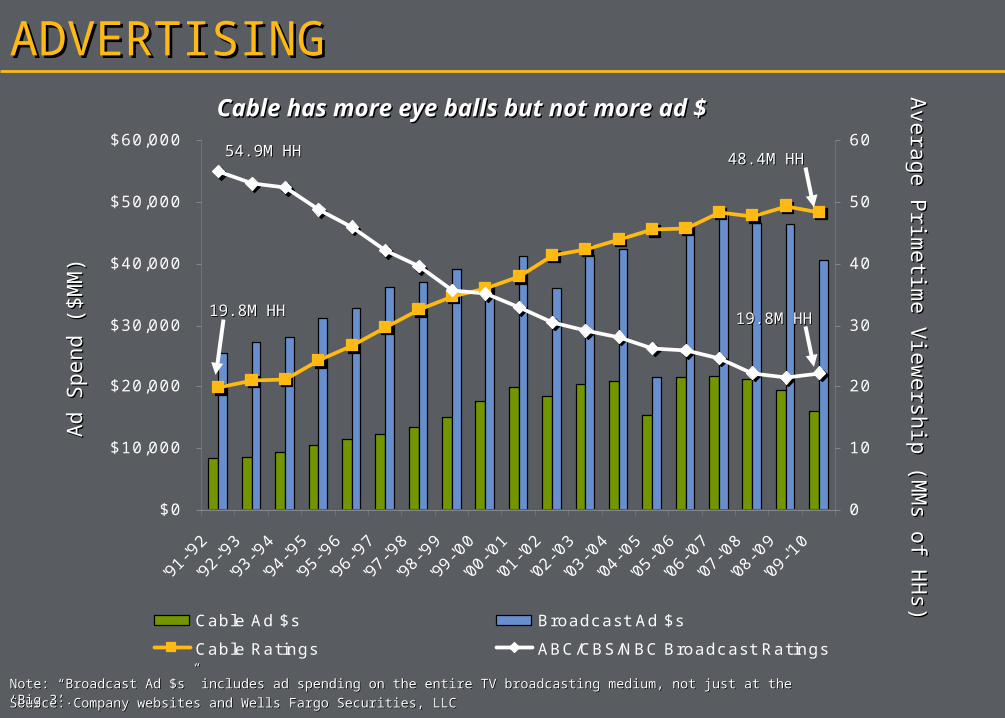

s)Cable has more eye balls but not more ad Cable has more eye balls but not more ad $$

Note: “Broadcast Ad $s” includes ad spending on the entire TV broadcasting medium, not just at the ‘Big 3’.Note: “Broadcast Ad $s” includes ad spending on the entire TV broadcasting medium, not just at the ‘Big 3’.

54.9M HH54.9M HH 48.4M HH48.4M HH

19.8M HH19.8M HH 19.8M HH19.8M HH

$8.20

$5.15

$7.01

$16.09

$14.07

$4.18

$10.07

$13.20

$2.97

$6.94

$8.74

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

Early AM Daytime Early News Prime-time Late Evening Daytime Late Fringe Prime Access Daytime Early/late

Fringe

Prime-time

Broadcast Networks Syndication Cable

Television

ADVERTISING – CPM COMPARABLESADVERTISING – CPM COMPARABLES

Source: Company websites and Wells Fargo Securities, LLCSource: Company websites and Wells Fargo Securities, LLC

2009 Average TV CPM Rates2009 Average TV CPM Rates

Both broadcast and syndication have higher CPMs than cableBoth broadcast and syndication have higher CPMs than cable

COMMERCIAL SEGMENTCOMMERCIAL SEGMENT

Source: Company websites and Wells Fargo Securities, LLCSource: Company websites and Wells Fargo Securities, LLC

HIGHER ARPUHIGHER ARPU

HIGHER MARGINSHIGHER MARGINS

“ “BETTER VALUE” PROPOSITION, IN OUR BETTER VALUE” PROPOSITION, IN OUR VIEWVIEW

CELLULAR BACKHAULCELLULAR BACKHAUL

7878

OPPORTUNITIESOPPORTUNITIES

Source: Company websites, and Wells Fargo Securities, LLC

RESIDENTIAL HSDRESIDENTIAL HSD

TV EVERYWHERETV EVERYWHERE

ADVERTISINGADVERTISING

COMMERCIALCOMMERCIAL

7979

INVESTOR FOCUSINVESTOR FOCUS

Source: Company websites, and Wells Fargo Securities, LLC

SUBSCRIBERSSUBSCRIBERS

PROFITABILITYPROFITABILITY

CAPITAL RETURNSCAPITAL RETURNS

CAPITAL INTENSITYCAPITAL INTENSITY

M&AM&A

COMPETITIONCOMPETITION

8080

CAPITAL RETURNSCAPITAL RETURNS

Source: Company websites, and Wells Fargo Securities, LLCSource: Company websites, and Wells Fargo Securities, LLC

SHARE REPURCHASESSHARE REPURCHASES

Cablevision ($0.5B, 5% of shares outstanding)Cablevision ($0.5B, 5% of shares outstanding)

Comcast ($3B, 5% of shares outstanding)Comcast ($3B, 5% of shares outstanding)

DirecTV ($6B, 17% of shares outstanding)DirecTV ($6B, 17% of shares outstanding)

Dish Network ($1B, 10% of shares outstanding)Dish Network ($1B, 10% of shares outstanding)

Time Warner Cable ($4B, 17% of shares outstanding)Time Warner Cable ($4B, 17% of shares outstanding)

RECURRING DIVIDENDRECURRING DIVIDEND

Cablevision (1.52% Yield)Cablevision (1.52% Yield)

Comcast (1.88% Yield)Comcast (1.88% Yield)

Time Warner Cable (2.65%Yield)Time Warner Cable (2.65%Yield)

Note: Yields and current share repurchase plans as of 4/18/11Note: Yields and current share repurchase plans as of 4/18/11

8181

WHAT ABOUT…..?WHAT ABOUT…..?

Source: Company websites, and Wells Fargo Securities, LLC

THE ECONOMYTHE ECONOMY

WIRELESS DATAWIRELESS DATA

PROGRAM COSTSPROGRAM COSTS

OVER THE TOPOVER THE TOP

TELEPHONYTELEPHONY

REGULATORY ENVIRONMENTREGULATORY ENVIRONMENT

QUESTIONS?QUESTIONS?

83

DisclosuresDisclosures

83

To view price charts for all companies rated in this document, please go to https://www.wellsfargo.com/research or write to 7 Saint Paul Street, 1st Floor, R1230-011, Baltimore, MD 21202

ATTN: Research Publications Additional Information Available Upon Request

I certify that:1) All views expressed in this research report accurately reflect my personal views about any and all of the subject securities or issuers discussed; and 2) No part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by me in this research report.Wells Fargo Securities, LLC maintains a market in the common stock of Belo Corp., Cablevision Systems Corp., CBS Corporation, Clear Channel Outdoor Holdings, Inc., Comcast Corporation, DISH Network Corporation, Entercom Communications Corp., Gray Television, Inc., Lamar Advertising Company, LIN TV Corporation, Saga Communications, Inc., Sinclair Broadcast Group, Inc., The DIRECTV Group, Inc., Time Warner Cable Inc. Wells Fargo Securities, LLC or its affiliates managed or comanaged a public offering of securities for CBS Corporation, Gray Television, Inc., LIN TV Corporation, Time Warner Cable Inc. within the past 12 months. Wells Fargo Securities, LLC or its affiliates intends to seek or expects to receive compensation for investment banking services in the next three months from Belo Corp., CBS Corporation, Comcast Corporation, DISH Network Corporation, Gray Television, Inc., LIN TV Corporation, Sinclair Broadcast Group, Inc., The DIRECTV Group, Inc., Time Warner Cable Inc. Wells Fargo Securities, LLC or its affiliates received compensation for investment banking services from CBS Corporation, Clear Channel Outdoor Holdings, Inc., Comcast Corporation, Gray Television, Inc., LIN TV Corporation, Sinclair Broadcast Group, Inc., Time Warner Cable Inc. in the past 12 months. Wells Fargo Securities, LLC and/or its affiliates, have beneficial ownership of 1% or more of any class of the common stock of CBS Corporation, Clear Channel Outdoor Holdings, Inc. CBS Corporation, Clear Channel Outdoor Holdings, Inc., Comcast Corporation, Gray Television, Inc., LIN TV Corporation, Sinclair Broadcast Group, Inc., Time Warner Cable Inc. currently is, or during the 12-month period preceding the date of distribution of the research report was, a client of Wells Fargo Securities, LLC. Wells Fargo Securities, LLC provided investment banking services to CBS Corporation, Clear Channel Outdoor Holdings, Inc., Comcast Corporation, Gray Television, Inc., LIN TV Corporation, Sinclair Broadcast Group, Inc., Time Warner Cable Inc. CBS Corporation, Clear Channel Outdoor Holdings, Inc., Comcast Corporation currently is, or during the 12-month period preceding the date of distribution of the research report was, a client of Wells Fargo Securities, LLC. Wells Fargo Securities, LLC provided noninvestment banking securities-related services to CBS Corporation, Clear Channel Outdoor Holdings, Inc., Comcast Corporation. Gray Television, Inc. currently is, or during the 12-month period preceding the date of distribution of the research report was, a client of Wells Fargo Securities, LLC. Wells Fargo Securities, LLC provided nonsecurities services to Gray Television, Inc. Wells Fargo Securities, LLC received compensation for products or services other than investment banking services from CBS Corporation, Clear Channel Outdoor Holdings, Inc., Comcast Corporation, Gray Television, Inc. in the past 12 months. Wells Fargo Securities, LLC or its affiliates may have a significant financial interest in Belo Corp., Cablevision Systems Corp., CBS Corporation, Clear Channel Outdoor Holdings, Inc., Comcast Corporation, DISH Network Corporation, Entercom Communications Corp., Gray Television, Inc., Lamar Advertising Company, LIN TV Corporation, Saga Communications, Inc., Sinclair Broadcast Group, Inc., The DIRECTV Group, Inc., Time Warner Cable Inc.

84

DisclosuresDisclosures

84

STOCK RATING1=Outperform: The stock appears attractively valued, and we believe the stock's total return will exceed that of the market over the next 12 months. BUY2=Market Perform: The stock appears appropriately valued, and we believe the stock's total return will be in line with the market over the next 12 months. HOLD3=Underperform: The stock appears overvalued, and we believe the stock's total return will be below the market over the next 12 months. SELL

SECTOR RATINGO=Overweight: Industry expected to outperform the relevant broad market benchmark over the next 12 months.M=Market Weight: Industry expected to perform in-line with the relevant broad market benchmark over the next 12 months.U=Underweight: Industry expected to underperform the relevant broad market benchmark over the next 12 months.

VOLATILITY RATINGV = A stock is defined as volatile if the stock price has fluctuated by +/-20% or greater in at least 8 of the past 24 months or if the analyst expects significant volatility. All IPO stocks are automatically rated volatile within the first 24 months of trading.As of: 4/18/2011 45% of companies covered by Wells Fargo Securities, LLC Equity Research are rated Outperform. Wells Fargo Securities, LLC has provided investment banking services for 38% of its Equity Research Outperform-rated companies. 52% of companies covered by Wells Fargo Securities, LLC Equity Research are rated Market Perform.Wells Fargo Securities, LLC has provided investment banking services for 47% of its Equity Research Market Perform-rated companies. 3% of companies covered by Wells Fargo Securities, LLC Equity Research are rated Underperform. Wells Fargo Securities, LLC has provided investment banking services for 42% of its Equity Research Underperform-rated companies.

Important Information for Non-U.S. Recipients EEA – The securities and related financial instruments described herein may not be eligible for sale in all jurisdictions or to certain categories of investors. For recipients in the EEA, this report is distributed by Wells Fargo Securities International Limited (“WFSIL”). WFSIL is a U.K. incorporated investment firm authorized and regulated by the Financial Services Authority. For the purposes of Section 21 of the UK Financial Services and Markets Act 2000 (“the Act”), the content of this report has been approved by WFSIL a regulated person under the Act. WFSIL does not deal with retail clients as defined in the Markets in Financial Instruments Directive 2007. The FSA rules made under the Financial Services and Markets Act 2000 for the protection of retail clients will therefore not apply, nor will the Financial Services Compensation Scheme be available. This report is not intended for, and should not be relied upon by, retail clients.

Marci L. Ryvicker, CPA, CFA

Harrisburg, PA

April 2011

Please see page 82 for rating definitions, important disclosures and required analyst certifications.

Wells Fargo Securities, LLC does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of the report and investors should consider this report as only a single factor in making their investment decision.

Cable: A Look At Trends & OpportunitiesCable: A Look At Trends & OpportunitiesPast, Present and FuturePast, Present and Future