manufacturing outlook 2013 - uhy-us.com · • download a copy of the powerpoint presentation ......

TRANSCRIPT

MANUFACTURING OUTLOOK 2013

WELCOME

2

Opening commentary

AGENDA

3

9:00AM—9:25AM EST Opening Commentary / What is Driving American

9:25AM—9:55AM EST Global Manufacturing Economic Forecast

9:55AM—10:20AM EST Shale Oil & Gas: A New Chapter in Domestic

Manufacturing

10:20AM—10:35AM EST Refreshment Break

10:35AM—11:00AM EST Medical Devices: Bringing Your Products to Market

11:00AM—11:25AM EST Maximizing Momentum for Automotive Suppliers

11:25AM—11:45AM EST Panel Discussion

ATTENDEE CHECKLIST

4

CPE materials • On-site: pick up at the registration desk (sign in, complete/return

evaluation form, pick up certificate) • On-line: email us

Feedback (forms in attendee booklet) Questions

• On-site: fill out question cards (we will collect later) • On-line: click the link to email your questions

Keep a look out for a post-event email

• Download a copy of the PowerPoint presentation • Link to view the webcast video

Pre-register for 2013 (2014 Outlook)

Get on our Manufacturing Insider mailing list

ABOUT UHY LLP

National Facts

• 15 offices across the U.S.

• More than 1,000 employees

• Ranked one of the Top 25 professional services firms by Accounting Today

• Reviewed by the PCAOB on a regular basis and received outstanding results

International Facts

• UHYI established in 1986 and based in London, UK

• Member firms in more than 250 cities in over 81 countries

• More than 6,800 member firm employees

• Ranked among the Top 25 largest international accounting and consultancy networks (by fee income)

Manufacturing Practice • Aerospace & Defence

• Automotive

• Consumer Products

• Distribution

• Industrials

U.S LOCATIONS

6

GEORGIA

ATLANTA

Five Concourse Parkway

Suite 2450

Atlanta, GA 30328

Telephone: 678-602-4400

Fax: 678-602-4300

ILLINOIS

CHICAGO

30 S. Wacker Dr.

Suite 1330

Chicago, IL 60606

Telephone: 312-578-9600

Fax: 312-346-6500

MARYLAND

COLUMBIA

6851 Oak Hall Lane

Suite 300

Columbia, MD 21045

Telephone: 410-720-5220

Fax: 410-381-2524

MICHIGAN

Metropolitan Detroit

FARMINGTON HILLS

27725 Stansbury Boulevard

Suite 200

Farmington Hills, MI 48334

Telephone: 248-355-1040

Fax: 248-355-1084

STERLING HEIGHTS

12900 Hall Road

Suite 500

Sterling Heights, MI 48313

Telephone: 586-254-1040

Fax: 586-254-1805

MISSOURI

ST. LOUIS

15 Sunnen Drive

Suite 100

St. Louis, MO 63143

Telephone: 314-615-1200

Fax: 314-647-8304

NEW JERSEY

OAKLAND

153 Bauer Drive

Oakland, NJ 07436

Telephone: 201-337-0009

Fax: 201-337-4462

NEW YORK

ALBANY

66 South Pearl Street

Suite 400

Albany, NY 12207

Telephone: 518-449-3166

Fax: 518-449-5832

NEW YORK

UHY Advisors NY, Inc.

19 West 44th Street

New York, NY 10036

Telephone: 212-381-4700

Fax: 212-354-6445

-and-

UHY Advisors FLVS, Inc.

19 West 44th Street

New York, NY 10036

Telephone: 646-746-1120

WHITE PLAINS

800 Westchester Avenue

Suite North 641

Rye Brook, NY 10573

Telephone: 914-697-4954

Fax: 914-697-7583

TEXAS

DALLAS

1717 Main, Suite 2400

Dallas, TX 75201

Telephone: 214-243-2900

Fax: 214-243-2929

HOUSTON

UHY Advisors TX, LLC

12 Greenway Plaza, Suite

200

Houston, TX 77046

Telephone: 713-960-1706

Toll-free: 800-949-1706

Fax: 713-960-9549

-and-

UHY Advisors SALT, LLC

3555 Timmons, Suite 1100

Houston, TX 77027

Telephone: 713-548-0900

Fax: 713-407-3760

WASHINGTON D.C.

WASHINGTON

1325 G Street NW

Suite 500

Washington, D.C. 20005

Telephone: 202-609-6100

GLOBAL NETWORK

7

Taiwan

Vietnam

Europe

Albania

Austria

Belarus

Belgium

Bulgaria

Czech Republic

Croatia

Cyprus

Denmark

Estonia

Finland

France

Germany

Greece

Guernsey

Hungary

Ireland

Isle of Man

Italy

Latvia

Lithuania

Luxembourg

Malta

Netherlands

Norway

Poland

Portugal

Romania

Russian Federation

Slovakia

Slovenia

Spain

Sweden

Switzerland

Turkey

Ukraine

United Kingdom

Middle East & Africa

Azerbaijan

Angola

Bahrain

Egypt

Israel

Jordan

Kenya

Republic of Kuwait

Lebanon

Mauritius

Morocco

Nigeria

South Africa

Tunisia

UAE

Americas

Argentina

Brazil

Canada

Chile

Colombia

Dominican Republic

Ecuador

El Salvador

Jamaica

Guatemala

Mexico

Peru

Puerto Rico

United States

Uruguay

Venezuela

Asia-Pacific

Australia

Bangladesh

China (inc Hong Kong)

India

Indonesia

Kazakhstan

Japan

Korea (Rep. of)

Malaysia

New Zealand

Pakistan

Singapore

UHY International

Member Offices

8

Every morning in the Savannah…

HUNTED

9

Every morning in the Savannah…

HUNTER

Highlights From UHY’s 2012 Outlook (November, 2011) Thomas Alongi Partner & National Manufacturing Practice Leader UHY LLP

MANUFACTURING OUTLOOK 2013

General Facts

We made the statement that “U.S. manufacturing is at a moment of truth” Indicators were positive based on manufacturing survey: 83% of manufacturers expected increasing production in 2012, 57% were optimistic on the 2012 economic outlook. Biggest uncertainty by respondents TAXES AND REGULATION!!

HIGHLIGHTS FROM OUR 2012 OUTLOOK

11

HIGHLIGHTS FROM OUR 2012 OUTLOOK

12

M&A “Market should continue to improve for sellers in 2012, even with the U.S. experiencing sluggish growth in the 3% range.”

- UHY November 2011

0

100

200

300

400

500

600

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2009 2010 2011 2012

Number of Private Equity Deals

Source: The Private Equity 3Q 2012 Breakdown; PitchBook.com

Source: Thompson Financial

5.2

7.3 7.6 8.5

0.0

2.5

5.0

7.5

10.0

2009 2010 2011 2012

U.S. Middle Market Value to EBITDA Multiple (Less Then $500M)

HIGHLIGHTS FROM OUR 2012 OUTLOOK

13

M&A “Lots of cash on the sidelines that must be put to work in 2012.”

- UHY November 2011

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

2007 2008 2009 2010 Q1 Q2 Q3 Q4 Q1 Q2

2011 2012

Sideline Cash (Billions of Dollars)

Source: Federal Reserve; federalreserve.gov

HIGHLIGHTS FROM OUR 2012 OUTLOOK

14

Global Markets “Opportunities abound in oversees markets with continued growth

in the BRIC countries.” - UHY November 2011

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Brazil Russia India China

Real GDP Forecast for BRIC Economies

2010 2011E 2012FSource: IBGE, Russian Federal State Statistics Service, Indian Central Statistical Organization, National Bureau of Statistics of China; estimates (E) and forecasts (F)

HIGHLIGHTS FROM OUR 2012 OUTLOOK

15

Automotive “Build where you sell” OEM directive will continue to help U.S.

suppliers.” - UHY November 2011

“Several years ago companies thought they could supply the whole world from facilities in China. Now, suppliers are being told by the Big Three automakers and original equipment manufacturers that they have to have operations in the United States if they want to be in the American marketplace.” - October 5, 2012 article Mellisa Anders

HIGHLIGHTS FROM OUR 2012 OUTLOOK

16

Automotive “Operational efficiency will become a greater concern with rising

production demand.” - UHY November 2011

Based on U.S. Federal Reserve data, suppliers are running at 78 percent capacity utilization as of August 2012. To meet production demand of approximately 14 million units many suppliers are running overtime, incurring shortages of materials and expedited freight costs.

78.5%

75.0%

64.6%

68.6%

72.5% 74.8%

78.0%

60%

65%

70%

75%

80%

85%

2008 2009 2010 2011 2012

Industrial Manufacturing Production and Capacity Utilization

What is Driving American Manufacturing? Thomas Alongi Partner & National Manufacturing Practice Leader UHY LLP

MANUFACTURING OUTLOOK 2013

WHY AMERICAN MANUFACTURING IS IMPORTANT?

18

• Difficult to balance trade - Manufacturing accounts for 86% of U.S. goods exported

• Manufacturing accounts for 72% of all R&D spending

• Manufacturing employs 63% of all domestic scientist and engineers

• Each manufacturing Job supports as an average 2.9 other jobs in the economy

• Vital to long term national security

Source: ITIF (information Technology & Innovation Foundation)

IN THE NEWS

19

WHAT’S DRIVING AMERICAN MANUFACTURING?

20

Currency Exchange

-20%

-10%

0%

10%

20%

30%

40%

50%

2008 2009 2010 2011 2012

BRIC Countries Percent Change in Exchange Rate to USD

Brazilian Real Russian Ruble Indian Rupee Chinese Yuan

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2008 2009 2010 2011 2012

Euro and Yen Percent Change in Exchange Rate to USD

Euro Japanese Yen

WHAT’S DRIVING AMERICAN MANUFACTURING?

21

Rising Global Supply Chain Costs • Rising foreign labor costs

• Transportation costs

• Energy costs

• Carrying inventory really does cost money

WHAT’S DRIVING AMERICAN MANUFACTURING?

22

Developing Foreign Markets (BRIC)

• Increased demand = Increased production = Rising labor costs = Rising standard of living

• Manufacturing in foreign markets now is more strategic than just a means to export to developed markets like the U.S.

WHAT’S DRIVING AMERICAN MANUFACTURING?

23

Foreign Politics/Regulations

WHAT’S DRIVING AMERICAN MANUFACTURING?

24

Lower Cost of Capital and Investment • Currently a low interest rate environment • Depressed commercial real estate • State and local tax incentives

CHALLENGES TO SUSTAINING AMERICAN MANUFACTURING?

25

• Combating foreign currency manipulation

• Increasing U.S. regulations and related costs

• Keeping attention focused on manufacturing

• Foreign trade policies

• Training skilled labor for tomorrow’s manufacturing jobs

ACTION PLAN TO SUSTAINABLE AMERICAN MANUFACTURING

26

• Reduced corporate tax rate

• Government policies to support more fair free trade

• Fund low skilled and high skilled manufacturing labor programs

• Make R&D credit permanent

• Tax credits to support investments in new equipment

• Federal government must place a strategic focus

on the manufacturing sector

DEVELOPING A GROWTH STRATEGY

27

You Need to Establish A

Business Strategy To

Take Advantage of Reshoring/ Backshoring

Opportunities

#1 • Strategy – Product & Market Position

#2 • Understand the Market Landscape

#3 • Assess Your Operations

#4 • Understand Financial & Cost Constraints

#5 • Mobilize – Prepare Processes & Personnel

#6 • Launch and Form Strategic Relationships

DEVELOPING A GROWTH STRATEGY

28

Confirm your Business Direction, Purpose & Scope: • Where is our industry in the market growth curve and can we still make

a profit?

• What innovative changes have/are occurring in our industry?

• Which Customers and Products drive our economic engine?

• Which Customers and Products drive our bottom line expenses?

• What are the emerging industry sectors and what opportunities are there that fit our capabilities?

UNDERSTAND MARKET LANDSCAPE

29

MARKETING STRATEGIES

30

• There are a variety of methodologies, tools and approaches • The most successful approaches include the following:

1. Analysis of your business operations – SWOT

2. Analysis of VERTICAL and HORIZONTAL

market expansion strategies

3. CURRENT Market Analysis

4. COMPETITIVE Market Analysis

5. TARGET Market(s) Research and Analysis

6. Identification, development and introduction of INNOVATIVE Products/Solutions for Market Growth

RESOURCES

31

Identify online opportunities to introduce your company, your capabilities, strengthens, etc. Examples:

• On-Line Customer / Supplier Bid Sites for Manufacturing www.mfg.com/en/ www.custompartsonline.com/ www.tobidit.com/ www.contractauction.com/ www.sourceauthority.com/

• Aerospace Suppliers http://www.aerospacesuppliers.com/

• Economic and Area Development http://www.areadevelopment.com/BusinessGlobalization/directory2011/us-companies-reshoring-operations62239.shtml

CONTACT INFORMATION

32

Thomas Alongi, CMA, CPA Partner & National Manufacturing

Practice Leader UHY LLP

586 843 2581

Global Manufacturing Economic Outlook James F. Peters, Jr. Chief Executive Officer Tactical Allocation Group, LLC

MANUFACTURING OUTLOOK 2013

ABOUT TAG

34

WHAT WE DO

35

The founders of Tactical Allocations Group, LLC (“TAG”) began their Proactive Investment Management style for fixed income investments in 1988. TAG’s “total return” approach sought to capture the value added from fixed income principal changes. Today, TAG applies their proactive investment management across more than 30 asset classes globally in TAG’s Tactical Portfolios. TAG’s portfolios are built exclusively with asset class specific, exchange-traded products to capture the full impact of their tactical allocation decisions.

TACTICAL ASSET ALLOCATION

36

Price and value often diverge, creating opportunity. Tactical Asset Allocation is a dynamic investment management style that adjusts asset allocations to TAG’s forward view of the relative risks and returns of various asset classes. This is distinguished from Strategic Asset Allocation, a mechanical, passive process of rebalancing the portfolios back to their original allocations; the weakness of this approach is its failure to allow for new information.

A TACTICAL WORLD

37

BUSINESSES OPERATE IN A TACTICAL WORLD • Businesses are ever evolving

• Businesses adjust to benefit from new opportunities

• Portfolios must adjust to benefit from new opportunities

EUROPE GLOBAL DRAG

38

MASSIVE DEBT BURDEN

39

$10

$14

$15

$31

$122

$200

$204

$243

$279

$287

$419

$1,272

$2,176

Austria

Denmark

Netherlands

Cyprus

Belgium

Ireland

U.K

Greece

Portugal

Germany

France

Italy

Spain

Source: www.zerohedge.com, TAG

Data as of December 31, 2011

Debt (in Trillions)

MASSIVE DEBT BURDEN

40 Source: Bloomberg Finance, L.P., IMF, TAG

-5% 15% 35% 55% 75% 95% 115% 135% 155% 175%

Swiss

Netherlands

Cyprus

Spain

Austria

Germany

United Kingdom

France

Belgum

Ireland

Portugal

Italy

Greece

100%

82%

74%

66%

65%

52%

162%

120%

108%

105%

85%

85%

68%

Data as of December 31, 2011

Debt as Percent of GDP

REFINANCING CLIFF

41 Source: Bloomberg Finance, L.P., TAG

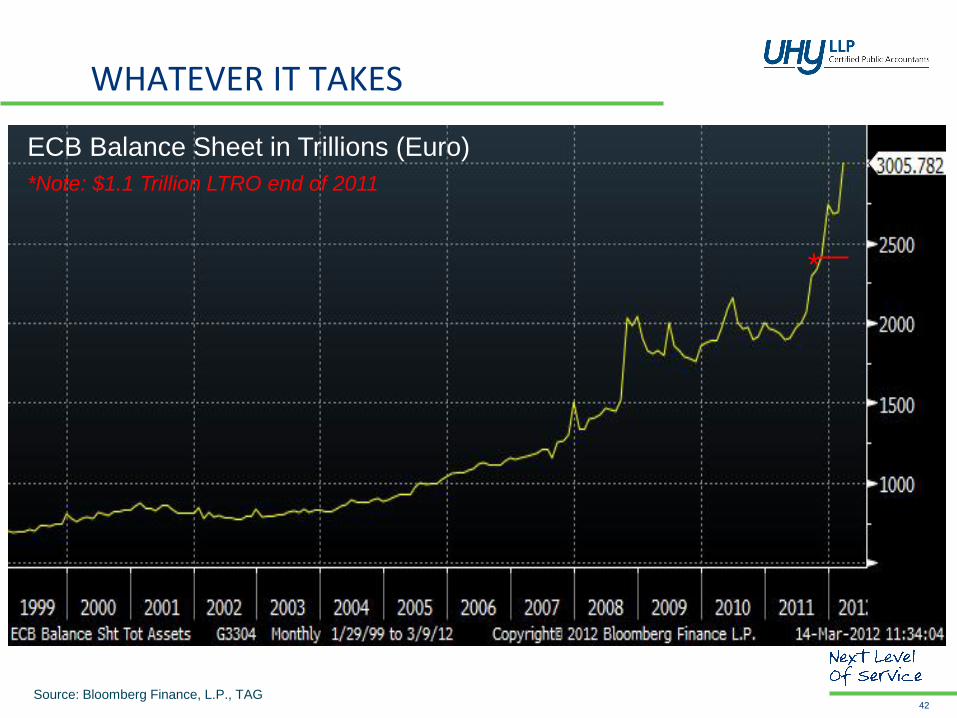

WHATEVER IT TAKES

42 Source: Bloomberg Finance, L.P., TAG

ECB Balance Sheet in Trillions (Euro)

*Note: $1.1 Trillion LTRO end of 2011

*

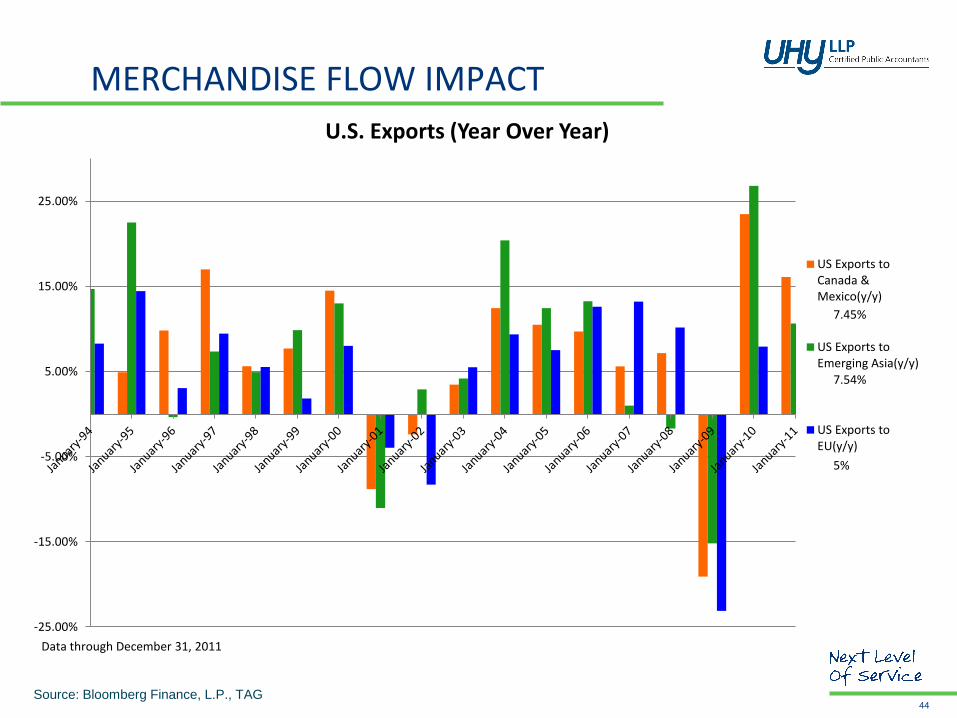

MERCHANDISE FLOW IMPACT

43 Source: Bloomberg Finance, L.P., TAG

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

US Exports toCanada &Mexico($m)

US Exports toEmerging Asia($m)

US Exports toEU($m)

22%

Data through August 31, 2012

23%

21%

U.S. Exports

In M

illio

ns

($)

MERCHANDISE FLOW IMPACT

44 Source: Bloomberg Finance, L.P., TAG

Data through December 31, 2011

-25.00%

-15.00%

-5.00%

5.00%

15.00%

25.00%

US Exports toCanada &Mexico(y/y)

US Exports toEmerging Asia(y/y)

US Exports toEU(y/y)

7.45%

5%

7.54%

U.S. Exports (Year Over Year)

CAPITAL FLOW IMPACT

45 Source: Bloomberg Finance, L.P., TAG

115,000.00

135,000.00

155,000.00

175,000.00

195,000.00

215,000.00

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

U.S. Capital Expenditures with Year Over Year Overlay

CapEx y/y (%) Capital Expenditures

y/y => "Negative"

y/y =>"Positive"

CAPITAL FLOW IMPACT

46 Source: Bloomberg Finance, L.P., TAG

CAPITAL FLOW IMPACT

47 Source: Bloomberg Finance, L.P., TAG

FOREIGN DIRECT INVESTMENT

48 Source: Bloomberg Finance, L.P., TAG

EMERGING EUROPE HOPE

49 Source: Bloomberg Finance, L.P., TAG

0

5000

10000

15000

20000

25000

30000

Russia FDI($m)

Turkey FDI($m)

Poland FDI ($m)

Czech FDI($m)

Foreign Direct Investment

GREAT CHINA DEBATE

50

GDP ACTUAL/PROJECTED

51 Source: CEIC, Xininua News, HSBC, TAG

0

2

4

6

8

10

12

14

16

2004 2005 2006 2007 2008 2009 2010 2011 2012e

Target

Actual

Perc

en

t

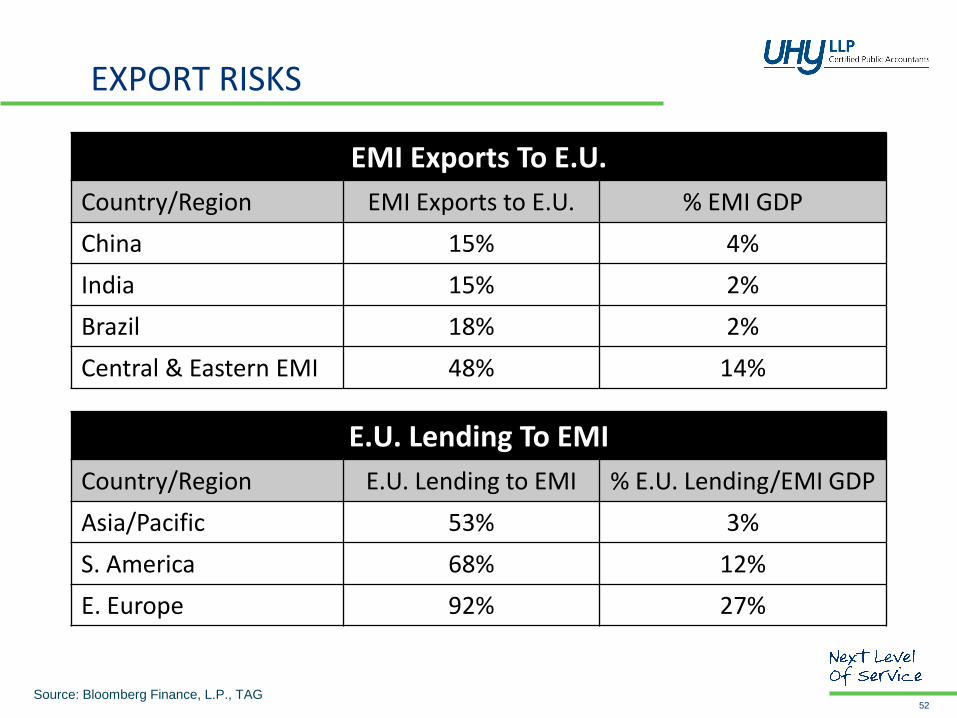

EXPORT RISKS

52 Source: Bloomberg Finance, L.P., TAG

EMI Exports To E.U.

Country/Region EMI Exports to E.U. % EMI GDP

China 15% 4%

India 15% 2%

Brazil 18% 2%

Central & Eastern EMI 48% 14%

E.U. Lending To EMI

Country/Region E.U. Lending to EMI % E.U. Lending/EMI GDP

Asia/Pacific 53% 3%

S. America 68% 12%

E. Europe 92% 27%

MONETARY EASING

53 Source: Bloomberg Finance, L.P., TAG

5

7

9

11

13

15

17

19

21

China (Reserve Requirement "RRR")

Red Dot = Projected Additional 200 Basis Point Reduction

FISCAL STIMULUS

54

1. Infrastructure Pull Forward

2. SME Tax Reform

3. Expanded Foreign Direct Investment (FDI)

CAPACITY TO STIMULATE

55

Source: *IMF

**Includes China, Brazil, India, Russia, Korea, South Africa, Mexico and Taiwan

Chart Source: BCA Research

MARKET DOESN’T BELIEVE

56 Source: http://www.zerohedge.com/sites/default/files/images/user3303/imageroot/2012/08/20120815_ms1.png

WILL ECONOMY HOLD?

57

MANUFACTURING SLOWING

58 Source: Bloomberg Finance, L.P., TAG

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

110.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Industrial Production Year/Year with Industrial Level Overlay

Industrial Production % Industrial Production

Negative

Positive

MANUFACTURING SLOWING

59 Source: Bloomberg Finance, L.P., TAG

115,000.00

135,000.00

155,000.00

175,000.00

195,000.00

215,000.00

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

Capital Expenditures with Year Over Year Overlay

CapEx y/y (%) Capital Expenditures

y/y => "Negative"

y/y =>"Positive"

MANUFACTURING SLOWING

60 Source: Bloomberg Finance, L.P., TAG

25.00

35.00

45.00

55.00

65.00

75.00

85.00

95.00

105.00

115.00

125.00

Auto Supply Days

Average=66

Negative

Positive

CONSUMER EXHAUSTION

61 Source: Bloomberg Finance, L.P., TAG

12.00

13.00

14.00

15.00

16.00

17.00

18.00

19.00

20.00

21.00

22.00

Consumer Debt to Income

Consumer Debt to Income

Old Paradigm

New Paradigm

PERSISTENT HIGH UNEMPLOYMENT

62 Source: Bloomberg Finance, L.P., TAG

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

Unemployment with U-6

Unemployment U-6

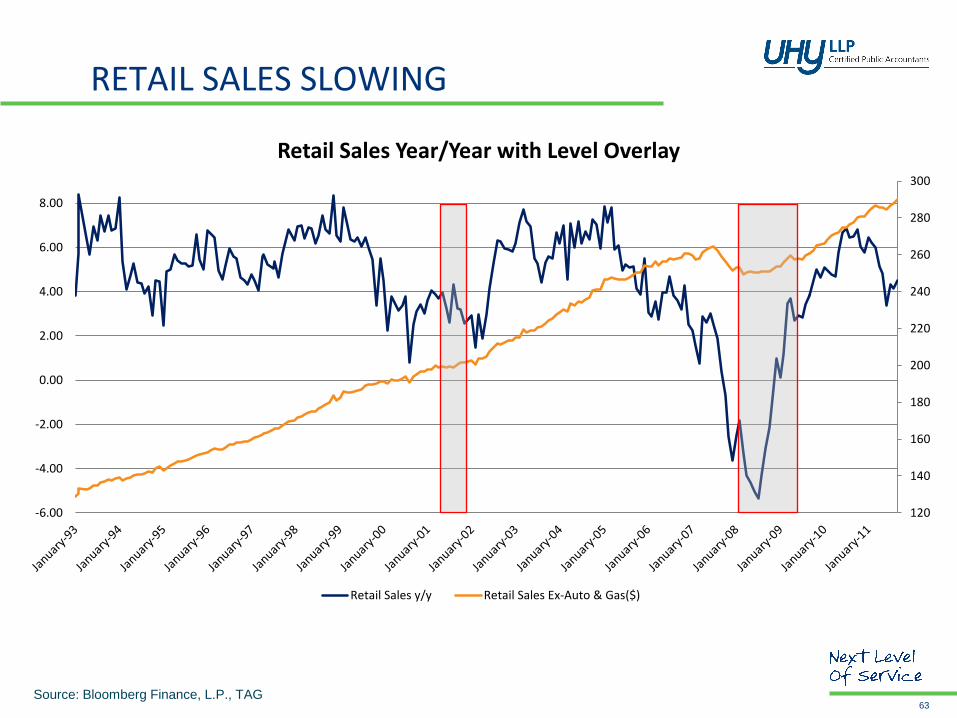

RETAIL SALES SLOWING

63 Source: Bloomberg Finance, L.P., TAG

120

140

160

180

200

220

240

260

280

300

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

Retail Sales Year/Year with Level Overlay

Retail Sales y/y Retail Sales Ex-Auto & Gas($)

CONSUMER CONFIDENCE DOWN

64 Source: Bloomberg Finance, L.P., TAG

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Jun

e-7

7

Jun

e-7

8

Jun

e-7

9

Jun

e-8

0

Jun

e-8

1

Jun

e-8

2

Jun

e-8

3

Jun

e-8

4

Jun

e-8

5

Jun

e-8

6

Jun

e-8

7

Jun

e-8

8

Jun

e-8

9

Jun

e-9

0

Jun

e-9

1

Jun

e-9

2

Jun

e-9

3

Jun

e-9

4

Jun

e-9

5

Jun

e-9

6

Jun

e-9

7

Jun

e-9

8

Jun

e-9

9

Jun

e-0

0

Jun

e-0

1

Jun

e-0

2

Jun

e-0

3

Jun

e-0

4

Jun

e-0

5

Jun

e-0

6

Jun

e-0

7

Jun

e-0

8

Jun

e-0

9

Jun

e-1

0

Jun

e-1

1

Jun

e-1

2

Consumer Confidence

Consumer Confidence

Average = 92.97

+1 Standard Deviation

+2 Standard Deviations

-1 Standard Deviation

-2 Standard Deviations

GREAT HOUSING HOPE

65

RECORD LOW INVENTORY

66 Source: Bloomberg Finance, L.P., TAG

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

12.00

13.00

140

190

240

290

340

390

440

490

540

590

New Home Supply (Months) with Inventory Overlay

New Homes Inventory New Home Supply Months

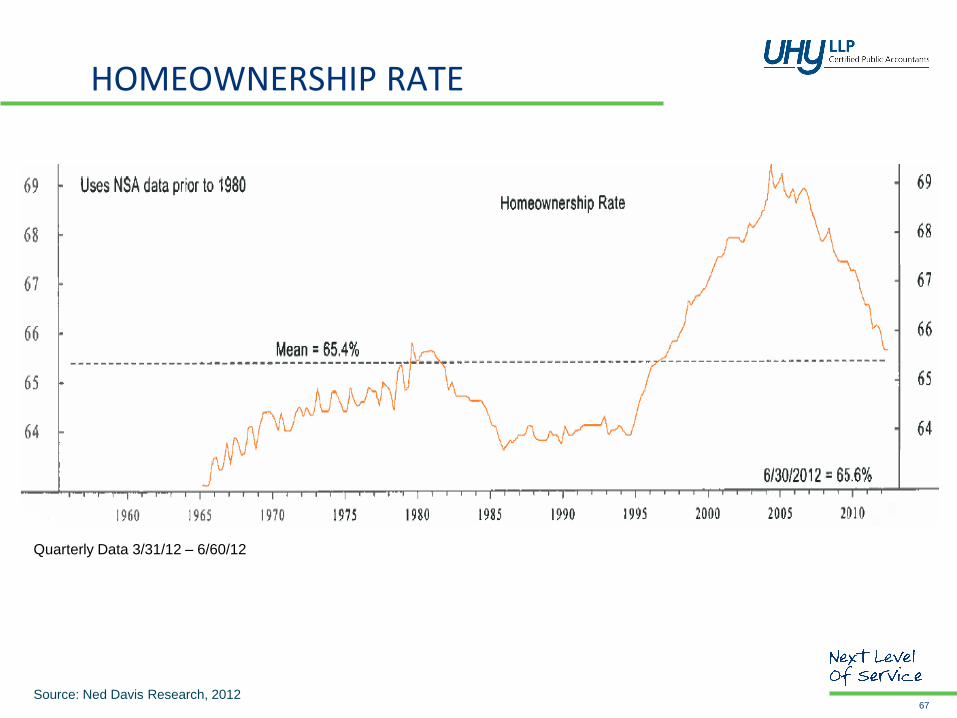

HOMEOWNERSHIP RATE

67 Source: Ned Davis Research, 2012

Quarterly Data 3/31/12 – 6/60/12

HOUSE PRICES

68 Source: http://www.jparsons.net/housingbubble/

PERMITS & STARTS

69 Source: Bloomberg Finance, L.P., TAG

0

500

1000

1500

2000

2500

3000

475

975

1475

1975

2475

Building Permits & Housing Starts

Permits Housing Starts

ECONOMIC IMPACT

70 Source: Bloomberg Finance, L.P., TAG

Housing Starts & Jobs

Housing Starts (yellow) & Unemployment (green)

ECONOMIC IMPACT

71 Source: Bloomberg Finance, L.P., TAG

Housing Starts & Consumer Confidence

Housing Starts (yellow) & Consumer Confidence (green)

ECONOMIC IMPACT

72 Source: Bloomberg Finance, L.P., TAG

Consumer Confidence & GDP

Consumer Confidence (yellow) & GDP (green)

ECONOMIC IMPACT

73 Source: Bloomberg Finance, L.P., TAG

Consumer Consumption

2%

7%

12%

17%

22%

27%

32%

37%

42%

Gas & Energy

Motor Vehicles & Parts

Clothing

Recreation

Food & Food Svc

Medical Care

Housing

TAG’S INVESTMENT COMMITTEE

74

James F. Peters, Jr. Chief Executive Officer

Paul J. Simon Chief Investment Officer

Joseph Styrna, CFA, CMT

Senior Research Analyst Gene Huang, PhD

Special Advisor

• Global Macro Team

• Forty plus years of asset management experience, with a CPA background

• Published author and speaker on financial markets

• Global Micro Team

• Twenty three years global analyst experience

• Frequent contributor to national financial media outlets

• Global Micro Team

• Thirteen years analyst experience

• Member of the CFA Institute and Market Technicians Association (MTA)

• Global Macro Team

• Chief Economist, Federal Express

• More than two decades global economic experience

TAG’S PORTFOLIO ADVISOR

75

Kevin A.W. Sheard Portfolio Advisor

Kevin is responsible for financial consulting services to families & institutions. Encompassing a comprehensive planning approach, he works with clients to develop their investment objectives, develops financial modeling and advises clients on their Portfolio construction to achieve their objectives. During his twelve year career, Kevin was a Trader of various securities at Fidelity Investments where he then became a Financial Planning Consultant. He later managed a $275 million dollar client base as a Financial Consultant at Charles Schwab & Co. In his leisure, Kevin enjoys the outdoors as a member of Ducks Unlimited and Trout Unlimited and was a ski coach for the Michigan Special Olympics. Kevin earned a Bachelor of Science degree in Sociology from Northern Michigan University.

[email protected] (248) 283-2520

DISCLOSURES

76

This Global Manufacturing Economic Forecast presentation has been provided by Tactical Allocation Group, LLC (“TAG”) for informational purposes only and should not be considered as investment advice or a recommendation for any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. This material contains the current opinion of the manager and such opinions are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Risk Disclosures and Additional Information: Past performance is not an indication of future results. Investment return and principal value will fluctuate, so that your investment, if sold, may be worth more or less than the original cost. Investing in non-U.S. securities may entail higher risk due to non-U.S. currency fluctuations and political or economic uncertainty that may be especially heightened when investing in emerging markets. Diversification does not ensure against loss. All investments involve a risk of loss. Information contained in this document (other than TAG’s performance information) has been obtained from sources believed to be reliable, but not guaranteed. Neither the information nor any opinion expressed herein constitutes a recommendation to invest in accordance with a particular portfolio or a solicitation for the sale or purchase of any particular security. For a more complete description of TAG’s investment process and fees, consult TAG's Disclosure Brochure. A complete list of firm composite descriptions is available upon request. Tactical Allocation Group, LLC 139 S. Old Woodward Avenue, Birmingham, MI 48009 (248) 283-2520 | www.tagportfolios.com | [email protected]

© 2012 Tactical Allocation Group, LLC. All rights reserved

77 77 77 77 77 77 77 77 77 77 77 77 77 77 77 77 77 77 77 77 77 77

James F. Peters, Jr.

Chief Executive Officer Tactical Allocation Group, LLC

248 283 2520

CONTACT INFORMATION

Shale Oil & Gas Production: A New Chapter in Domestic Manufacturing Wayne Wilson Managing Director UHY Advisors Texas ,LLC

MANUFACTURING OUTLOOK 2013

OVERVIEW

79

• The Hype • Impact on Natural Gas Price

• Impact on Power Generation

• Impact on Raw Materials

• Challenges to Impacts

THE HYPE

80

• Will Change the Design of Cities in the Future

• Will Change the Automotive Industry Forever

• Bigger than the Internet

• Could Change the World

• Significant Environmental Benefits

IMPACT ON NATURAL GAS PRICE

81

• Shale has grown to about 25% of natural gas production

• Shale production quadrupled from 2007-2010 from 1.3 TCF to 5.3 TCF

• Projected to be 46% of US natural gas production by 2035

• Prices have fallen from over $10 per MMBTU in 2008 to less than $3 in 2012.

• Shale production pivotal to any forecast for natural gas production

PRICE PER MMBTU OF GAS VS. COAL

82

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00Ja

n-0

9

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

Pri

ce p

er

MM

btu

Henry Hub NYMEX Future Price

CAPP NYMEX Future Price per MMBtu

IMPACT ON POWER GENERATION

83

• US is historically a coal generation nation

• Coal accounted for 57% of power generation in US in 1985

• Coal=34% and Gas=32% in May 2012

• Reason is falling natural gas prices combined with increasing environmental costs of coal

• Capital cost for conventional coal is over 3X that of conventional combined cycle natural gas

IMPACT ON RAW MATERIALS

84

• Natural gas as feedstock for chemicals and plastics

• 30+% increase in ethylene

• Downstream industries include everything from clothing and textile mills to beverages and pharmaceuticals

• Impact of lower plastic prices is widespread

• Potential future impacts of plastic alternatives to wood or metal manufacturing

CHALLENGES TO IMPACTS

85

• Globalization of Natural Gas Market

• Impact of Low Prices on Shale Gas Producers

• Supply Demand Equilibrium

• Increased Environmental Regulation

• Other Government Interference

CONTACT INFORMATION

86

Wayne Wilson

Managing Director UHY Advisors Texas, LLC

713 407 3831

REFRESHMENT BREAK

87

Will reconvene in 15 minutes

Medical Devices: Bringing Your Product to Market Timothy M. McCarthy Senior Counsel Clark Hill PLC

MANUFACTURING OUTLOOK 2013

89

What are the five top concerns of medical device manufacturers?

1. Medical device tax.

2. Medical device tax.

3. Medical device tax.

4. Medical device tax.

5. Medical device tax.

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

90

The medical device tax:

• 2.3 per cent on sale of any medical device.

• By manufacturer, producer, or importer.

• Effective January 1, 2013.

• Exemptions for eyeglasses, contact lenses, hearing aids, and devices generally purchased by general public at retail.

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

91 91

The medical device tax: Issues

1. Efforts to repeal:

• Stock prices are down because of the tax.

• Obamacare benefits for hospitals could result in higher volumes.

2. Treatment of kits.

3. Contracts and rebates.

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

92 92 92 92

The sixth top issue to medical device manufacturers:

6. FDA approval

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

93 93 93 93 93 93 93

FDA approval:

• Average time for premarket notification clearance (510(k)) has increased.

• Average time for approval of a premarket approval application (PMA) has doubled since 2008

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

94 94 94 94 94 94 94 94 94 94 94 94

What the FDA is doing:

• Budget for device review has increased from $120M to $292M.

• 240 additional full-time employees.

• Clear, meaningful metrics to be used.

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

95 95 95 95 95 95

The seventh top issue to medical device manufacturers:

7. Patent protection

• Develop a patent strategy • Consider patent problems:

― Lag time to issue ― Increased costs

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

96 96 96 96 96 96 96 96 96

Patent protection of your medical device during development:

1. Get good non-disclosure agreements.

2. File early for patent protection.

• Especially after March 16, 2013.

3. File for all alternate designs.

4. Claim all possible users.

5. Consider design patents.

6. Joint development agreements.

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

97 97 97 97 97 97 97 97 97 97 97 97 97 97 97

Patent protection of your medical device after obtaining a patent. 1. Cease-and-desist letter.

2. Infringement lawsuit.

3. ITC proceeding.

4. Licensing.

Consider the advice of Abraham Lincoln.

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

98 98 98 98 98 98 98 98 98 98 98 98 98 98 98 98 98 98 98

Protection of your IP all the time.

1. Employee relationship:

a. Defining role of employee and scope of duties. b. Assignments of inventions from employees and

partners. c. Protect from use of IP from employee’s prior job. d. Non-competition clauses.

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99 99

Protection of your IP all the time.

2. Trade secrets:

a. Keep secret information secret. b. Restrict disclosure within the company. c. NDAs with suppliers.

3. If it truly is a trade secret, treat it like a trade

secret. 4. Non-compete agreements.

MEDICAL DEVICES: BRINGING YOUR PRODUCT TO MARKET

100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100

Tim McCarthy Senior Counsel

Clark Hill

[email protected] 312 985 5561

CONTACT INFORMATION

Maximizing Momentum For Automotive Suppliers Anthony Pratt Director Of Forecasting, Americas R.L. Polk & Co.

MANUFACTURING OUTLOOK 2013

© 2012 R. L. Polk & Co. All rights reserved.

Anthony Pratt Director of Forecasting, The Americas

August 2012

“5 Trends in 5 Minutes”

The 6 Burning Forecasting Questions:

© 2012 R. L. Polk & Co. All rights reserved.

1) “What is Polk’s forecast?”

2) “How has consumer behavior changed?”

3) “Should suppliers be cautious about capital investment?”

4) “How does the ‘European Crisis” threaten you?”

5) “Will China continue to drive growth?”

6) “What else should you be watching?”

“5 Trends in 5 Minutes”

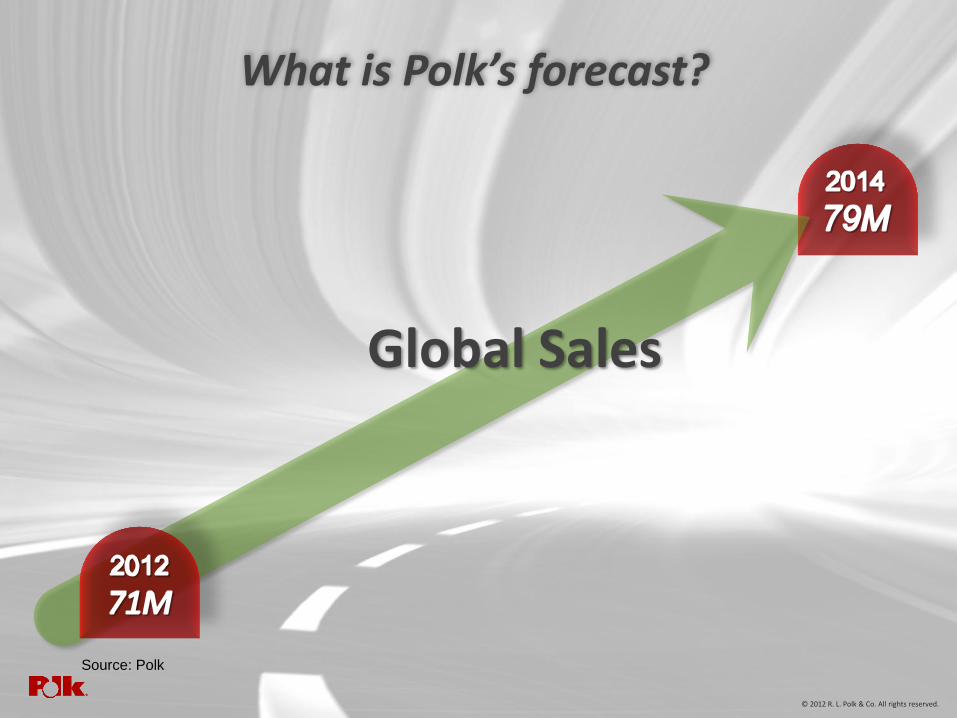

What is Polk’s forecast?

© 2012 R. L. Polk & Co. All rights reserved.

“5 Trends in 5 Minutes”

Global Sales

What is Polk’s forecast?

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 106

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

WE CEE NAFTA Asia-Pacific/Middle East Latin America Africa

Global Light Vehicle Registration Volumes: 1995 - 2017

What is Polk’s forecast?

34% growth between 2012 and 2017

Approaching 100 million units by 2020

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

“5 Trends in 5 Minutes”

U.S. Sales

What is Polk’s forecast?

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

“5 Trends in 5 Minutes”

What is Polk’s forecast?

© 2012 R. L. Polk & Co. All rights reserved.

Millions of Units

7

8

9

10

11

12

13

14

15

16

17

2007 2008 2009 2010 2011 2012F 2013F 2014F 2015F 2016F 2017F

13.2

10.3

11.5

12.6

14.3

15.2 16.0 16.0 16.0

15.5

16.0

U.S. Sales likely to peak at 16 million units through 2017

Source: Polk

“5 Trends in 5 Minutes”

What is Polk’s forecast?

© 2012 R. L. Polk & Co. All rights reserved.

Risks outweigh opportunities: “Falling off the financial cliff”

14.3

15.2

16.0 16.0 16.0 15.5

14.1

14.5

15.0

15.4 15.5 15.4

13.5

14

14.5

15

15.5

16

16.5

2012F 2013F 2014F 2015F 2016F 2017F

Upside Baseline Downside

14.5

15.5

16.3 16.2

15.9

16.3

Source: Polk

“5 Trends in 5 Minutes”

N.A. Assembly

What is Polk’s forecast?

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

“5 Trends in 5 Minutes”

What is Polk’s forecast?

© 2012 R. L. Polk & Co. All rights reserved.

Millions of Units

2007 2008 2009 2010 2011 2012F 2013F 2014F 2015F 2016F 2017F

7

9

11

13

15

17

19

North American Production: Expansion likely

16.2 16.9 16.8 16.9 15.1

12.6

8.6

11.9

13.1

15.0

15.4

Source: Polk

“5 Trends in 5 Minutes”

What is Polk’s forecast?

© 2012 R. L. Polk & Co. All rights reserved.

17% 16% 12%

13% 18% 22%

70% 66% 66%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2002 2012 2022

Canada Mexico USA

Assembly Investment: “Canada is world’s most expensive”

Source: Polk

“5 Trends in 5 Minutes”

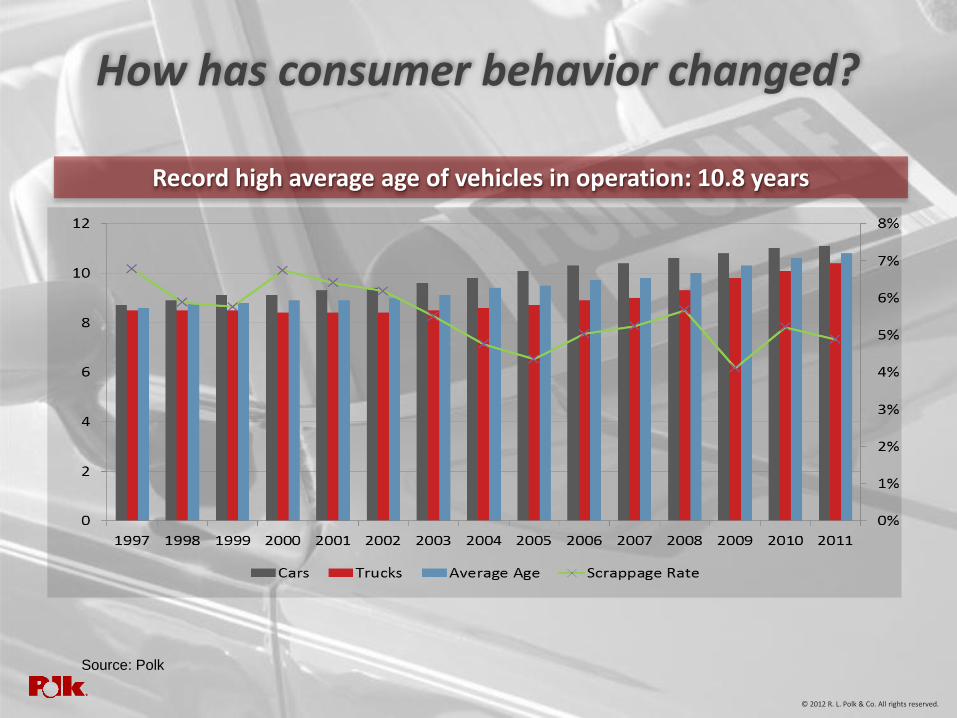

How has consumer behavior changed?

© 2012 R. L. Polk & Co. All rights reserved.

“5 Trends in 5 Minutes”

How has consumer behavior changed?

© 2012 R. L. Polk & Co. All rights reserved.

Record high average age of vehicles in operation: 10.8 years

Source: Polk

“5 Trends in 5 Minutes” © 2012 R. L. Polk & Co. All rights reserved.

How has consumer behavior changed?

Ownership length: 71 months (and rising?)

Source: Polk

“5 Trends in 5 Minutes” © 2012 R. L. Polk & Co. All rights reserved.

How has consumer behavior changed?

Loan terms over 5 years: 46%

Source: TransUnion

“5 Trends in 5 Minutes”

Customers are returning!

© 2012 R. L. Polk & Co. All rights reserved.

How has consumer behavior changed?

“5 Trends in 5 Minutes”

Should suppliers be cautious about capital investment?

© 2012 R. L. Polk & Co. All rights reserved.

© 2012 R. L. Polk & Co. All rights reserved. 119

Global light vehicle production % change: 2012 vs. 2011

Should suppliers be cautious about capital investment?

Production volumes growing in 2012; excluding Europe

31%

18% 15%

10% 9% 8% 7% 7%

- 6%

-20.0%

0.0%

20.0%

40.0%

Africa Japan N. Amer. China E. Euro. Asia Rest World S. Amer, EU27

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 120

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1995 2000 2005 2010 2015

Should suppliers be cautious about capital investment?

Global Light Vehicle Production Volumes (000)

Global production volumes approaching 100 million vehicles

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

“5 Trends in 5 Minutes”

Should suppliers be cautious about capital investment?

Loyalty Rate Over Time (% Loyal to Manufacturer) © 2012 R. L. Polk & Co. All rights reserved.

43.3

44.8 46.2

45.0

42.9 41.5

40.6 40.0 39.8

36

38

40

42

44

46

48

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9

Loyalty: Declines the longer a consumer owns a vehicle

Source: Polk

% L

oya

l to

Ma

nu

factu

rer

Number of years owned

“5 Trends in 5 Minutes”

Should suppliers be cautious about capital investment?

© 2012 R. L. Polk & Co. All rights reserved.

Loyalty: New vehicle launches typically increase conquest sales

Source: Polk

“5 Trends in 5 Minutes”

Should suppliers be cautious about capital investment?

© 2012 R. L. Polk & Co. All rights reserved.

The battle for U.S. market share!

U.S. Market Share Forecast by Manufacturer Source: Polk

© 2012 R. L. Polk & Co. All rights reserved.

Should suppliers be cautious about capital investment?

Proceed with caution!

“5 Trends in 5 Minutes”

How does the European crisis threaten you?

© 2012 R. L. Polk & Co. All rights reserved.

“5 Trends in 5 Minutes”

2007 2011 % Change

VW 12.5% 15.4% 3.0%

Nissan 2.4% 4.4% 1.9%

Hyundai 2.4% 3.6% 1.2%

Skoda 3.6% 4.5% 0.9%

Kia 2.0% 2.7% 0.7%

Ford 10.3% 10.3% 0.1%

Peugeot 8.7% 8.5% -0.2%

Citroen 7.5% 7.3% -0.2%

Renault 9.9% 9.6% -0.2%

Mazda 1.8% 1.2% -0.6%

Opel/Vxh. 10.6% 9.4% -1.2%

Fiat 7.8% 6.6% -1.2%

Toyota 7.0% 4.9% -2.1% EU27 Market Share: 2007 vs. 2011

How does the European crisis threaten you?

EU 27 market share “winners” and “losers”

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 127

Mill

ion

s

13.6 13.7 13.0 12.8

11.9 12.2 12.8 13.3 13.6 13.8

5.1

2.99 3.6

4.3 4.6 4.9 5.5 5.98

6.5 7.1

0

2

4

6

8

10

12

14

16

2008 2009 2010 2011 2012F 2013F 2014F 2015F 2016F 2017F

Western Euro. Central/Eastern Euro.

European New Light Vehicle Registrations: 2008 - 2017

How does the European crisis threaten you?

Euro crisis impacts all economies

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

128

GDP Contributors to Growth 2011 2012 2013

GDP Growth: 1.5 -0.2 1.4

o Private Consumption 0.1 -0.2 0.5

o Government Consumption -0.1 0.0 0.2

o Fixed Investment 0.3 -0.3 0.4

o Net Exports 1.1 0.8 0.2

o Chg. In Inv + Stat. Discr. 0.1 -0.5 0.2

European Union Real GDP Growth by Components: 2011 - 2013

How does the European crisis threaten you?

Exports buffering OEMs from struggling home market

© 2012 R. L. Polk & Co. All rights reserved.

Source: Feri

© 2012 R. L. Polk & Co. All rights reserved. 129

European New Light Vehicle Production Volumes: 2008 - 2017

How does the European crisis threaten you?

0

2

4

6

8

10

12

14

16

18

2008 2009 2010 2011 2012F 2013F 2014F 2015F 2016F 2017F

Central / Easter Europe Western Europe

Mill

ion

s

Exports partially offsetting decline in home market

14.5

12.0

13.5 14.0 12.9

13.2 14.1

14.7 15.0 15.4

7% Export 8%

Export

12% Export

6.0 4.8

5.5 6.1 6.4 6.9

7.6 8.1 8.6 8.9

18% Export

39% Export

25% Export

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 130

How does the European crisis threaten you?

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

A great deal of risk and uncertainty!

“5 Trends in 5 Minutes”

Will China continue to drive growth?

© 2012 R. L. Polk & Co. All rights reserved.

© 2012 R. L. Polk & Co. All rights reserved. 132

Will China continue to drive growth?

59% China Growth

(35% CTG)

34% U.S. Growth (13% CTG)

34% Global Growth

56% BRIC Growth

(55% CTG)

Sales % growth: 2011 vs. 2017

© 2012 R. L. Polk & Co. All rights reserved.

Source: Polk

© 2012 R. L. Polk & Co. All rights reserved. 133

Will China continue to drive growth?

China Light Vehicle Registration Volumes: 2008 - 2017

“Lower tier” Chinese cities will drive growth

6.2

10.2

13.0 13.1 14.6

15.6 17.1

18.2 19.5

20.8

0

5

10

15

20

25

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

© 2012 R. L. Polk & Co. All rights reserved.

Gov’t Stimulus

Source: Polk

“5 Trends in 5 Minutes”

What else should you be watching?

© 2012 R. L. Polk & Co. All rights reserved.

To download this presentation and to access more of

our Forecasting publications and analyses, please visit:

www.polk.com/forecasts

136 136 136 136 136 136 136 136 136 136 136 136 136 136 136 136 136 136 136 136 136 136

Anthony Pratt

Director Of Forecasting, Americas; R.L. Polk & Co

248 728 7000

CONTACT INFORMATION

PANEL DISCUSSION

137

Questions and answers

ATTENDEE CHECKLIST

138

CPE materials • On-site: pick up at the registration desk (sign in, complete/return

evaluation form, pick up certificate) • On-line: email us

Feedback (forms in attendee booklet) Questions

• On-site: fill out question cards (we will collect later) • On-line: click the link to email your questions

Keep a look out for a post-event email

• Download a copy of the PowerPoint presentation • Link to view the webcast video

Pre-register for 2013 (2014 Outlook)

Get on our Manufacturing Insider mailing list

CONCLUDING THOUGHTS

139

Thank you!