managing risks around electronic checks no laws or … · 2017-11-21 · managing risks around...

TRANSCRIPT

No

ve

mb

er

15,

2017

NEACH

Big East Banking Conference

Managing Risks Around Electronic Checks

No Laws or Regulations!

This session provides an overview of various aspects of the check payments systems

including legal and rules framework for check image exchange. Responsibility for compliance with image exchange rules and/or legal, operational and regulatory requirements applicable to check image exchange remains at all times with the financial institution participating in check image exchange and/or the individual or company using a check image exchange service.

This presentation and the information contained herein is not intended as legal or compliance advice or recommendation to any person or company.

This document could include technical inaccuracies or typographical errors and individual users are responsible for verifying any information found in this presentation.

Financial institutions should consult with their legal counsel regarding legal and operational requirements applicable to any check image exchange program they may offer or in which they participate.

2

Disclaimer

Session Overview• ECCHO Overview• Highlights of Final Regulation CC and Proposal

– Electronic Check and Electronic Returned Check • Definition• Warranties

– Expeditious Return• Notice of non-payment and in-lieu of return

– New Indemnifications• Electronically Created Item• Remote Deposit Capture

– RFC on Presumption of Alteration

• Check Trends

3

ECCHO Overview• Electronic Check Clearing House Org

– Not-for-profit, created in 1990– Owned by its membership

• Current membership – approximately 2,800– Every depository financial institution is eligible for

membership• Only DFIs are eligible for membership

– All ECCHO members have equal coverage under rules– Only national private sector Image Rules Organization– Vendor and solution independent

• Rules designed to work with all solutions– ECCHO Rules apply to Check Image Exchanges between

ECCHO Members– Three functions – Rules, Advocacy and Education

• NCP Program

4

Regulation CC• Background

– Fed issued Requests for Comment on changes to Regulation CC in 2011 and 2014• Fed amending Subparts C and D of Regulation CC to facilitate

banking industry’s ongoing transition to fully-electronic check collection and return process

– Issued May 31, 2017 • Takes effect on July 1, 2018• Final Rule and overview can be found at • https://www.eccho.org/eccho-sb-memo

– Also requested comment on presumption of alteration for certain disputes

– Proposed revisions to Subpart B remain outstanding• Joint authority with Fed and CFPB over Subpart B

5

• Extends Reg CC Coverage to Electronic Checks– Images of original paper checks– Forward collection and unpaid returns

• Creates New Warranties for Electronic Checks– No duplicate payments– Information accurately represents all of the

information from front and back of paper check

Regulation CC Highlights

6

Electronic Check Definition• Electronic Check and Electronic Returned

Check – An electronic image of, and electronic information derived

from, paper check or paper returned check • Exchanged under an agreement between banks • Conforms with ANS X9.100-187 or banks can agree to

other standard– Check image and information must be “derived” from

paper check• Image must be created from paper item• ECIs (defined below) are not electronic checks

• Electronic check/electronic returned check now subject to Regulation CC, Subpart C

7

• Expeditious Returns– Shifts liability from paying bank to BOFD if BOFD

does not arrange for return of checks electronically by “commercially reasonably means”• Applies to paper checks and electronic checks

Regulation CC Highlights

8

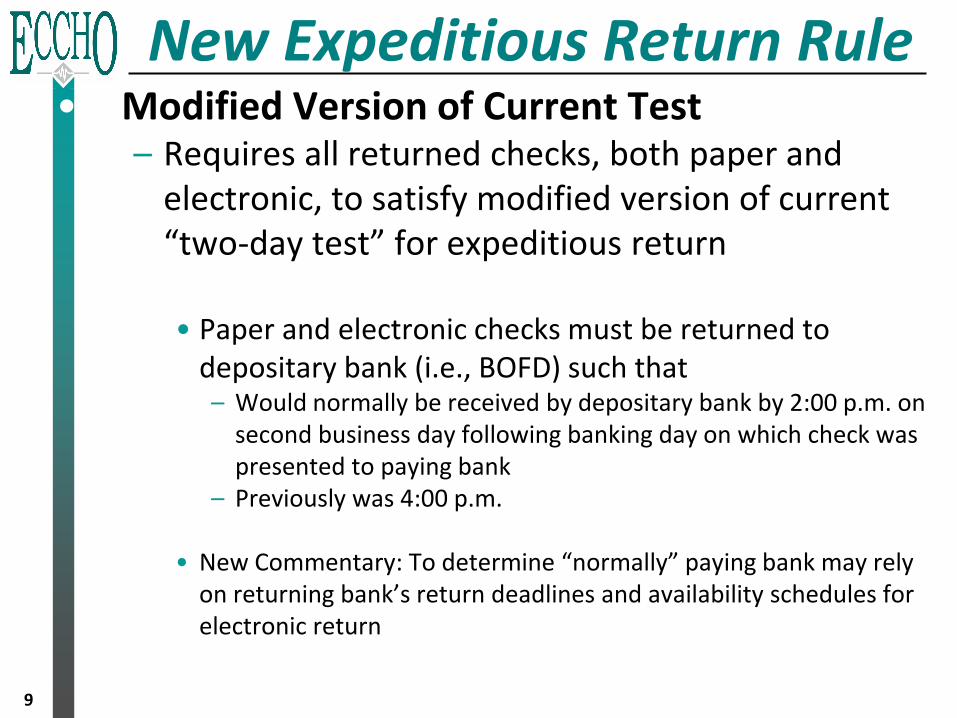

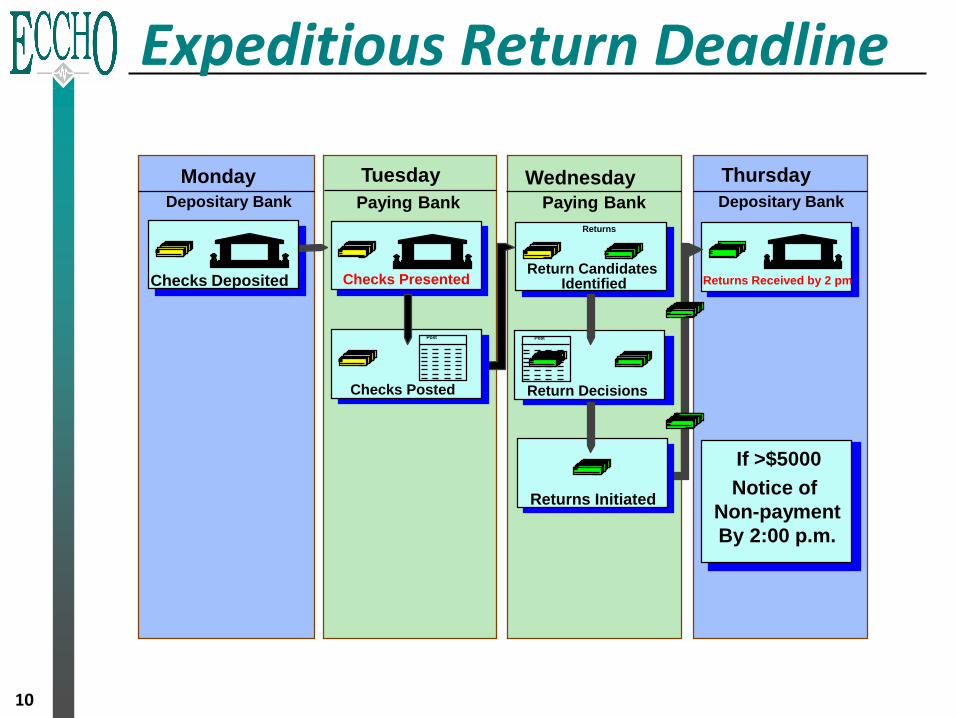

New Expeditious Return Rule• Modified Version of Current Test

– Requires all returned checks, both paper and electronic, to satisfy modified version of current “two-day test” for expeditious return

• Paper and electronic checks must be returned to depositary bank (i.e., BOFD) such that– Would normally be received by depositary bank by 2:00 p.m. on

second business day following banking day on which check was presented to paying bank

– Previously was 4:00 p.m.

• New Commentary: To determine “normally” paying bank may rely on returning bank’s return deadlines and availability schedules for electronic return

9

Expeditious Return Deadline

Thursday

Returns Received by 2 pm

Notice of

Non-payment

By 2:00 p.m.

If >$5000

Monday

Checks Deposited

Tuesday

Checks Presented

Wednesday

Return Decisions

Return CandidatesIdentified

Returns

Post

Returns Initiated

Depositary Bank Paying Bank Paying Bank Depositary Bank

Checks Posted

Post

10

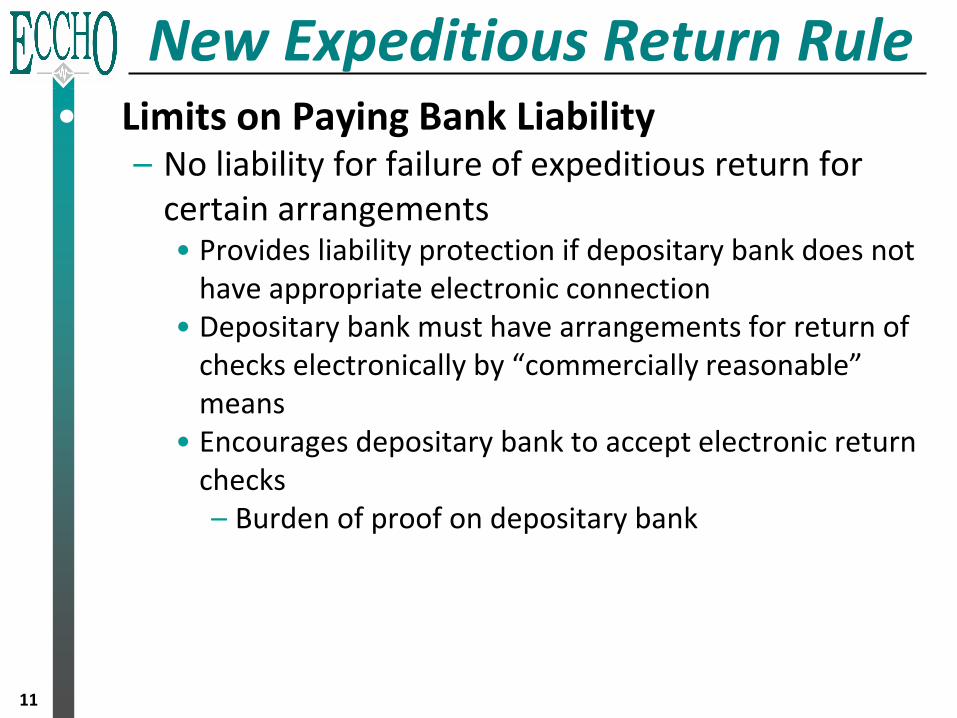

New Expeditious Return Rule• Limits on Paying Bank Liability

– No liability for failure of expeditious return for certain arrangements • Provides liability protection if depositary bank does not

have appropriate electronic connection• Depositary bank must have arrangements for return of

checks electronically by “commercially reasonable” means

• Encourages depositary bank to accept electronic return checks– Burden of proof on depositary bank

11

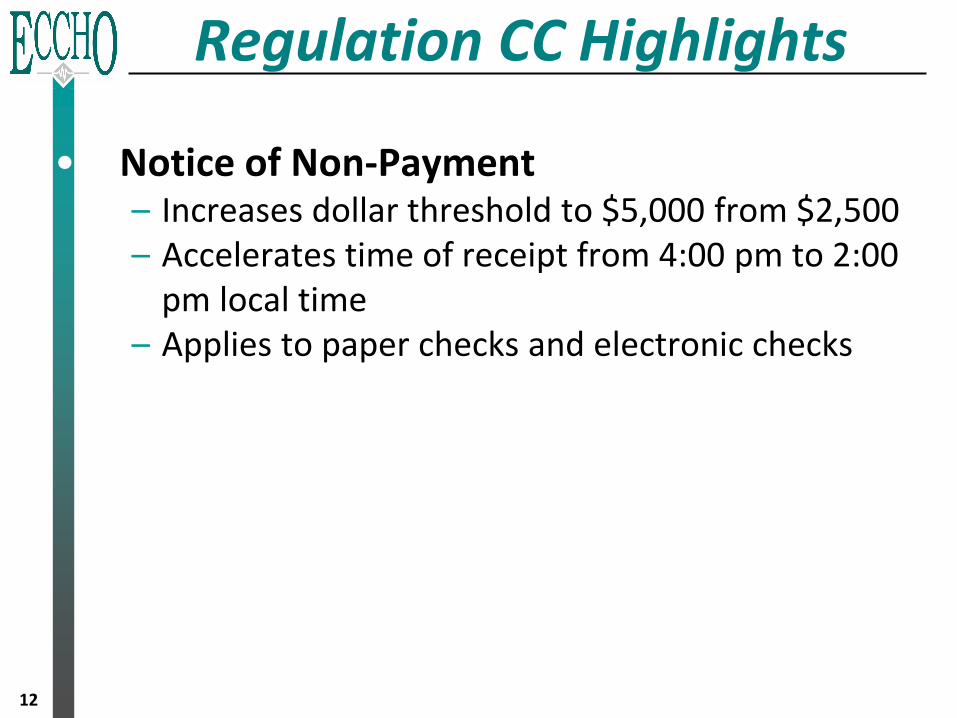

• Notice of Non-Payment– Increases dollar threshold to $5,000 from $2,500– Accelerates time of receipt from 4:00 pm to 2:00

pm local time– Applies to paper checks and electronic checks

Regulation CC Highlights

12

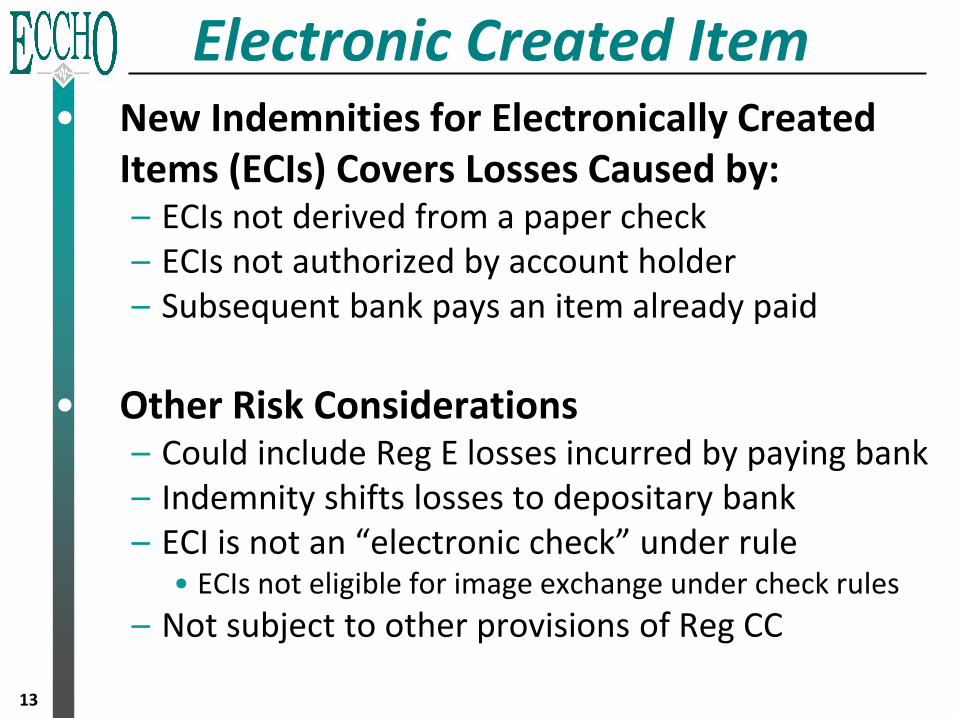

• New Indemnities for Electronically Created Items (ECIs) Covers Losses Caused by:– ECIs not derived from a paper check– ECIs not authorized by account holder– Subsequent bank pays an item already paid

• Other Risk Considerations– Could include Reg E losses incurred by paying bank– Indemnity shifts losses to depositary bank– ECI is not an “electronic check” under rule

• ECIs not eligible for image exchange under check rules

– Not subject to other provisions of Reg CC

Electronic Created Item

13

Electronically Created Item

• What is an ECI?– Electronic Image that has all attributes of electronic

check/electronic returned check but was created electronically and not derived from paper check • Also know as: Electronic Payment Order (EPO)

– Never existed in paper form and does not meet Reg CC definition of electronic check• ECI cannot be used to create substitute check that is legal

equivalent14

CH

EC

K W

RIT

ER

PAYING

BANK

INTERMEDIARY

BANK

COLLECTING

BANK (BOFD)

ImageImage Image

Statement

Image

RDC

DE

PO

SIT

OR

CH

EC

K W

RIT

ER

ECI

Remittance

Data

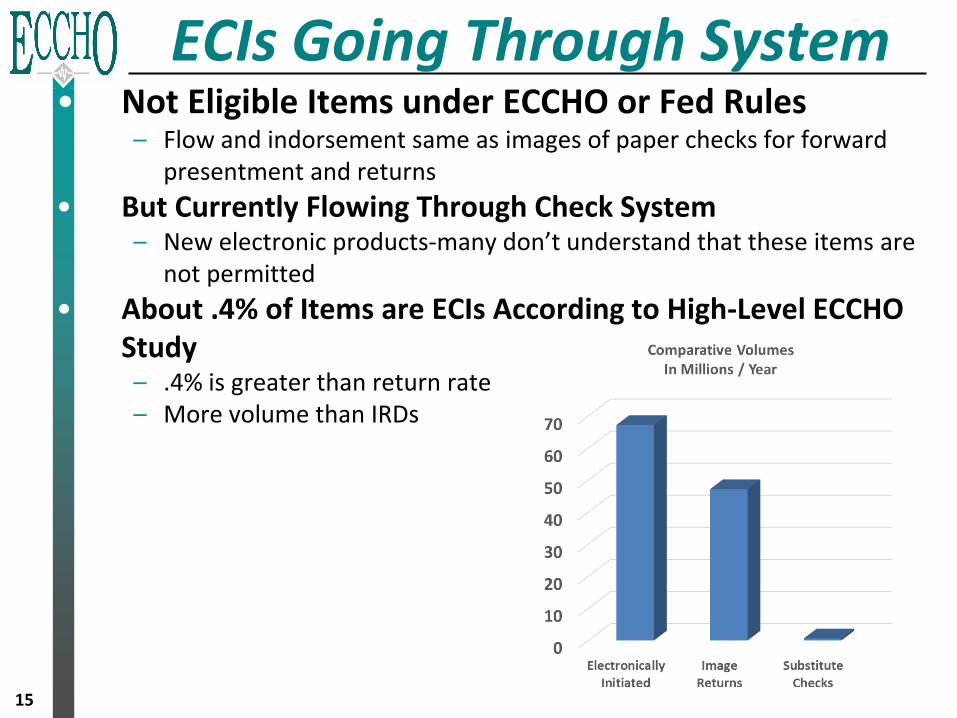

ECIs Going Through System• Not Eligible Items under ECCHO or Fed Rules

– Flow and indorsement same as images of paper checks for forward presentment and returns

• But Currently Flowing Through Check System– New electronic products-many don’t understand that these items are

not permitted

• About .4% of Items are ECIs According to High-Level ECCHO Study– .4% is greater than return rate– More volume than IRDs

15

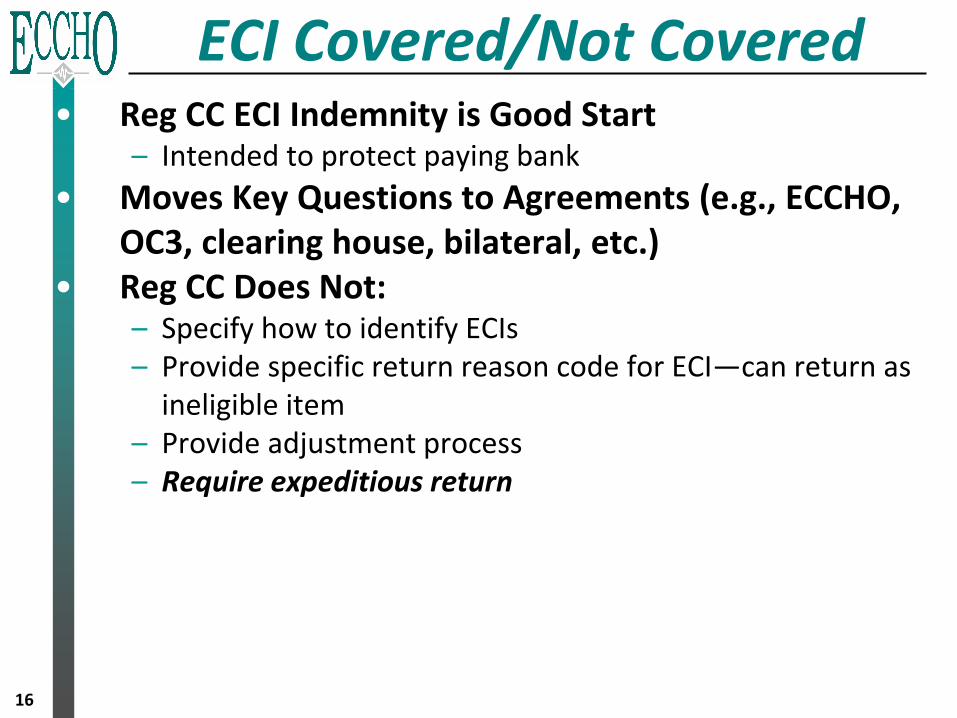

ECI Covered/Not Covered• Reg CC ECI Indemnity is Good Start

– Intended to protect paying bank

• Moves Key Questions to Agreements (e.g., ECCHO, OC3, clearing house, bilateral, etc.)

• Reg CC Does Not:– Specify how to identify ECIs– Provide specific return reason code for ECI—can return as

ineligible item– Provide adjustment process– Require expeditious return

16

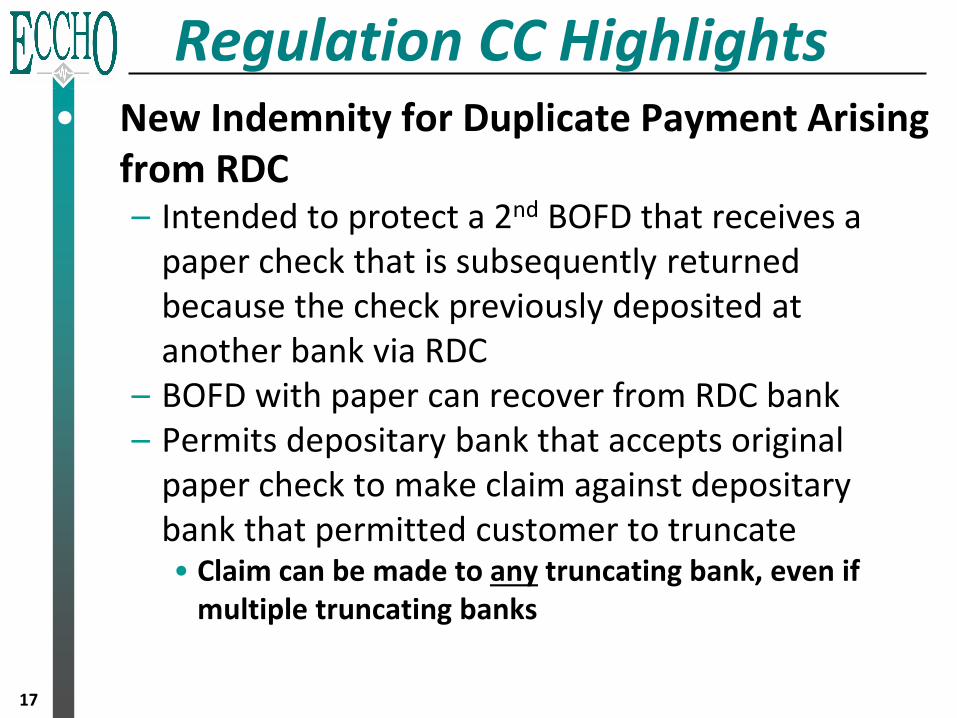

• New Indemnity for Duplicate Payment Arising from RDC– Intended to protect a 2nd BOFD that receives a

paper check that is subsequently returned because the check previously deposited at another bank via RDC

– BOFD with paper can recover from RDC bank– Permits depositary bank that accepts original

paper check to make claim against depositary bank that permitted customer to truncate• Claim can be made to any truncating bank, even if

multiple truncating banks

Regulation CC Highlights

17

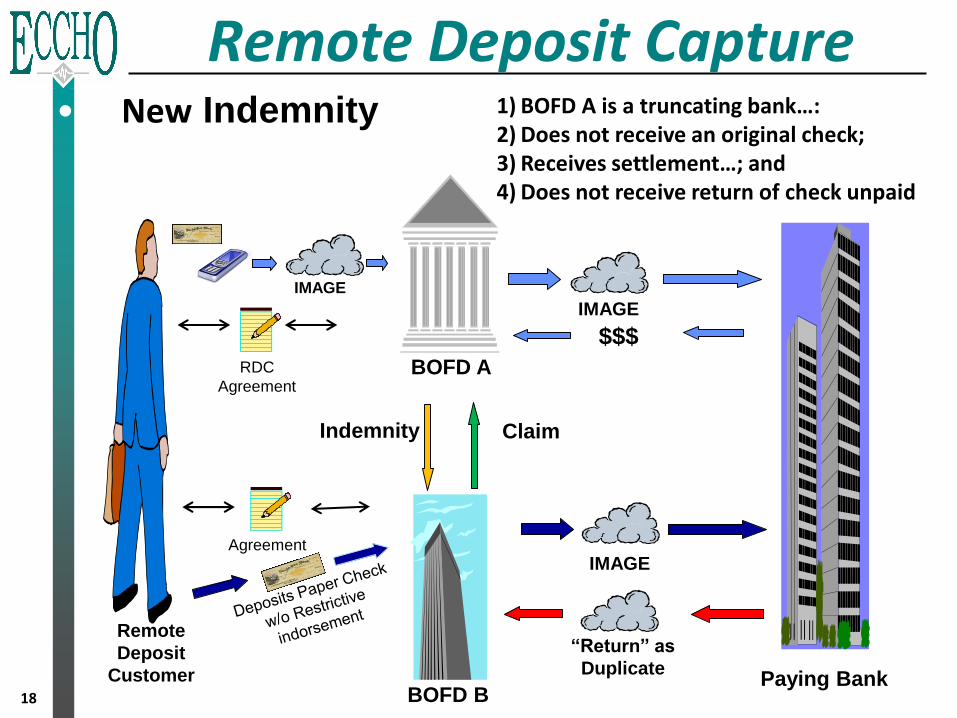

18

Remote Deposit Capture

BOFD A

Paying Bank BOFD B

Remote

Deposit

Customer

Indemnity Claim

IMAGE

IMAGE

RDC

Agreement

“Return” as

Duplicate

IMAGEAgreement

$$$

• New Indemnity 1) BOFD A is a truncating bank…:2) Does not receive an original check;3) Receives settlement…; and4) Does not receive return of check unpaid

19

Remote Deposit Capture

BOFD A

Paying Bank BOFD B

Remote

Deposit

Customer

Indemnity Claim

IMAGE

IMAGE

RDC

Agreement

“Return” as

Duplicate

IMAGEAgreement

$$$

• Indemnity Claim

1) BOFD A is an RDC bank & makes indemnity;

2) BOFD B accepts original paper for deposit; and

3) BOFD B receives a return unpaid

Remote Deposit Capture

20

BOFD A

Paying Bank

BOFD B

Remote

Deposit

Customer

Indemnity?

Claim

IMAGE

IMAGE

RDC

Agreement

“Return” as

Duplicate

IMAGE

Agreement

RDC

Agreement

IMAGE

BOFD C

Claim

Adjust or Claim as

Duplicate (not return)

$$$

o

r

$$$

RDC Making Claim• Who Can Make Claim?

– Indemnified bank (accepting original paper check) can make claim against RDC bank that permitted customer to truncate

• How to Make Claim?– Final Rule does not:

• Provide instruction on how to make claim to RDC bank• Address how indemnified bank can identify RDC bank

21

RDC Making Claim• Fed Left Many Issues For Banks to Determine

– Use return code/return system?– Use adjustment code/adjustment system?– Timing/deadlines for claims? For info requests?– How get all info you need?

• Who RDC bank was?• Proof the indemnified bank actually has original item?• Within indemnified bank, get paper where it needs to

go?

22

Other Highlights• Rejected Deposit

– Bank that rejects check submitted for deposit (i.e. ATM) may send customer substitute check

• Bank makes Check 21 warranties and indemnification, regardless of whether bank received consideration for substitute check

• Same Day Settlement– Retains current SDS rule and only applies to paper presentment– Settlement of presentment of electronic checks governed by

agreement of parties

• Indorsements– Eliminates Appendix D – Indorsement, Reconverting-Bank

Identification and Truncation Bank Identification Standards– Refer to X9 industry standards for indorsement for paper check

(X9.100-111), substitute check (X9.100-140) and electronic check (X9.100-187)

23

Request for Comment• Presumption of Alteration

– Requested comment whether Regulation CC should adopt evidentiary presumption as to whether, in cases of doubt, check should be presumed to be altered rather than forgery• Dollar amount or payee on substitute check or electronic check • Presumption may be overcome by preponderance of evidence that

check was forged or is as issued by drawer• Presumption does not apply if original check is made available

– Also considering• Whether alteration presumption should apply to claim that date of

check was altered• Whether presumption should apply if bank claiming presumption

destroyed original check

24

Request for Comment• ECCHO Comment Letter

– ECCHO facilitated industry discussions and provided industry comment letter to Fed on August 1, 2017• Industry group letter supported presumption• Note: ECCHO Rules include a similar provision for past

several years

25

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

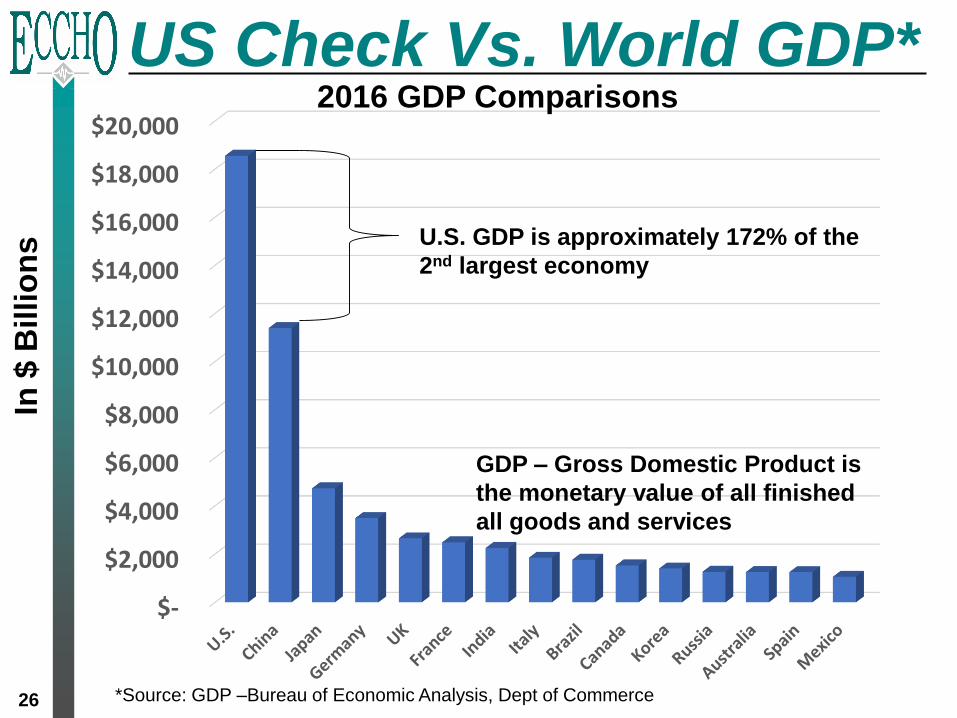

US Check Vs. World GDP*In

$ B

illi

on

s

2016 GDP Comparisons

26

GDP – Gross Domestic Product is

the monetary value of all finished

all goods and services

*Source: GDP –Bureau of Economic Analysis, Dept of Commerce

U.S. GDP is approximately 172% of the

2nd largest economy

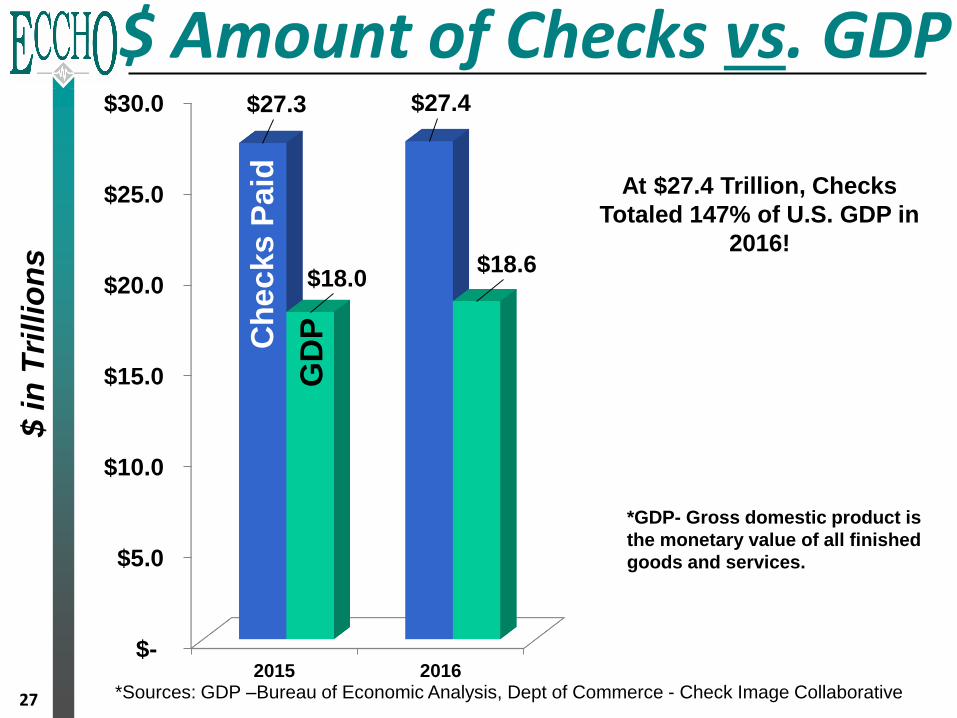

$-

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

2015 2016

$27.3 $27.4

$18.0 $18.6

27 *Sources: GDP –Bureau of Economic Analysis, Dept of Commerce - Check Image Collaborative

At $27.4 Trillion, Checks

Totaled 147% of U.S. GDP in

2016!

*GDP- Gross domestic product is

the monetary value of all finished

goods and services.

$ Amount of Checks vs. GDP$ i

n T

rill

ion

s

GD

PCh

eck

s P

aid

28

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

U.S

. C

he

cks

201

6

Aggregate GDP of

These 7 Countries = <

U.S. Check Dollars

In 2016 UK Faster

Payments Totaled $1.5

Trillion or 5.5% of U.S.

Check Dollars

In $

Bil

lio

ns

2016 GDP Comparisons

*Sources: GDP –Bureau of Economic Analysis, Dept of Commerce and 2016 Federal Reserve payments Study

US Check Vs. World GDP*

29

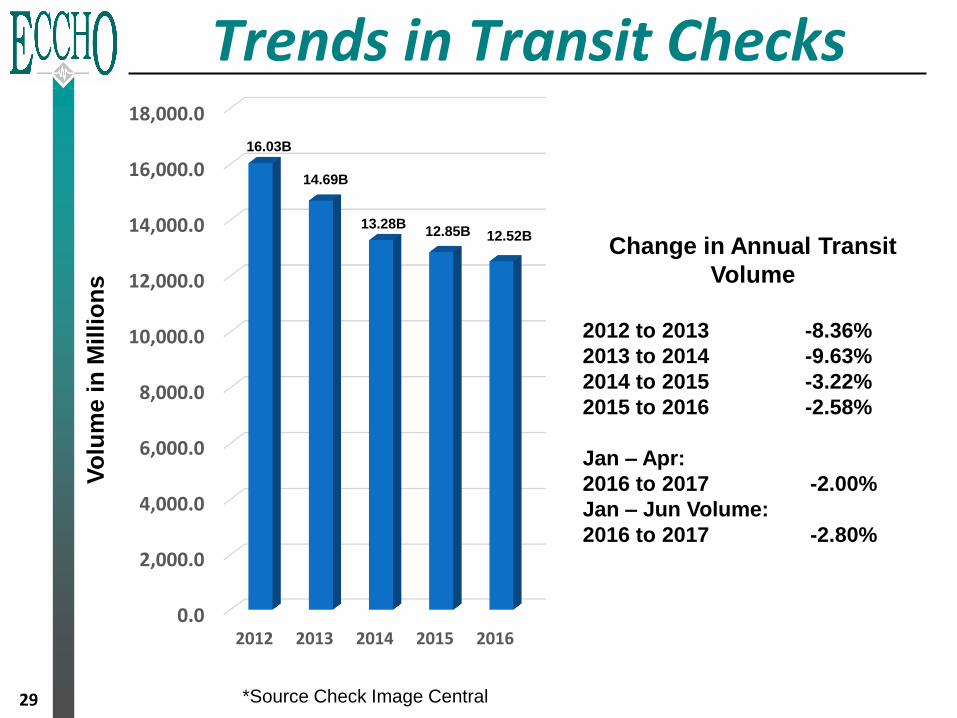

Trends in Transit Checks

0.0

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

12,000.0

14,000.0

16,000.0

18,000.0

2012 2013 2014 2015 2016

Change in Annual Transit

Volume

2012 to 2013 -8.36%

2013 to 2014 -9.63%

2014 to 2015 -3.22%

2015 to 2016 -2.58%

Jan – Apr:

2016 to 2017 -2.00%

Jan – Jun Volume:

2016 to 2017 -2.80%

16.03B

Vo

lum

e in

Mil

lio

ns

14.69B

13.28B12.85B 12.52B

*Source Check Image Central

$-

$5,000

$10,000

$15,000

$20,000

2012 2013 2014 2015 2016

30

Trends in Transit Check $s

Change in Annual Transit

Dollars

2012 to 2013 -4.68%

2013 to 2014 -6.31%

2014 to 2015 + .83%

2015 to 2016 + .47%

Jan – Apr Dollars:

2016 to 2017 +2.52%

Jan – Jun Dollars:

2016 to 2017 +3.12%

$21.4TD

oll

ars

in

Billi

on

s

$20.4T

$19.1T $19.3T $19.4T

*Source Check Image Central

Wrap-Up and Questions

31

Thank You!

Electronic Check Clearing House Organization

www.eccho.org

David Walker

ECCHO

214.273.3201