managing india. managing indian? mastering complexity · pdf filethe global magazine for...

TRANSCRIPT

The

glob

al m

agaz

ine

for d

ecis

ion-

mak

ers

by R

olan

d Be

rger

Str

ateg

y Co

nsul

tant

s DO

SSIE

R:M

anag

ing

Indi

a. M

anag

ing

Indi

an?

Issu

e 15

thin

k:ac

t

The global magazine for decision-makers Issue 15

ROLAND BERGER STRATEGY CONSULTANTS

Jürgen Hambrechton European management culture

Martin Walseron justice andinjustice, moneyand independence

Philip Kotler reinvents himself. The world of finance in upheaval.The art of productive conflicts.

Mastering complexityIndia and its companies

can do more than just cheap

07_15gb_01_Umschlag_aussen 18.06.2010 13:20 Uhr Seite 1

… and therefore we would like to congratulate the following winners from the German round of our “Best of European Business” awards for successfully finding this path:

Dr. Jürgen Hambrecht, CEO of BASF SE, as best “European Manager”; Hartmut Ostrowski,CEO of Bertelsmann AG, for winning the “Strong Leadership” prize; and also both HOCHTIEFAktiengesellschaft and Symrise AG as recipients of our “Growth Despite Crisis” award.

We believe that Europe’s companies have both the chance and the potential to make the coming years a European decade.

We think so!Is there a European path to successful management?

07_15gb_02_03_Editorial 18.06.2010 13:19 Uhr Seite 2

3

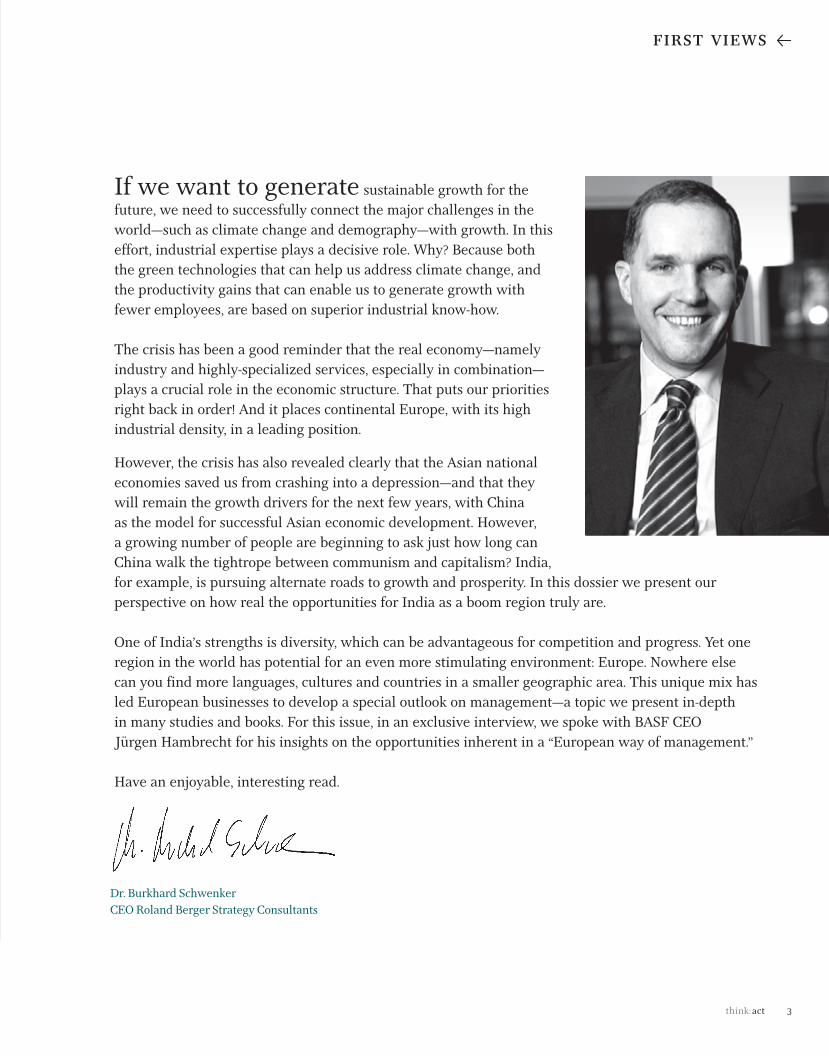

Dr. Burkhard SchwenkerCEO Roland Berger Strategy Consultants

If we want to generate sustainable growth for thefuture, we need to successfully connect the major challenges in theworld—such as climate change and demography—with growth. In thiseffort, industrial expertise plays a decisive role. Why? Because boththe green technologies that can help us address climate change, andthe productivity gains that can enable us to generate growth withfewer employees, are based on superior industrial know-how.

The crisis has been a good reminder that the real economy—namelyindustry and highly-specialized services, especially in combination—plays a crucial role in the economic structure. That puts our prioritiesright back in order! And it places continental Europe, with its high industrial density, in a leading position.

However, the crisis has also revealed clearly that the Asian nationaleconomies saved us from crashing into a depression—and that theywill remain the growth drivers for the next few years, with China as the model for successful Asian economic development. However, a growing number of people are beginning to ask just how long canChina walk the tightrope between communism and capitalism? India,for example, is pursuing alternate roads to growth and prosperity. In this dossier we present our perspective on how real the opportunities for India as a boom region truly are.

One of India’s strengths is diversity, which can be advantageous for competition and progress. Yet oneregion in the world has potential for an even more stimulating environment: Europe. Nowhere else can you find more languages, cultures and countries in a smaller geographic area. This unique mix hasled European businesses to develop a special outlook on management—a topic we present in-depth in many studies and books. For this issue, in an exclusive interview, we spoke with BASF CEO Jürgen Hambrecht for his insights on the opportunities inherent in a “European way of management.”

Have an enjoyable, interesting read.

first views f

07_15gb_02_03_Editorial 18.06.2010 13:19 Uhr Seite 3

p contents

Mission deregulation. Sergey Tigipko is Ukraine’s new vice primeminister. He is prescribing his country a significant reform program—even if it causes some discomfort. Page 8

A new way to new ideas. The easiest source of inspiration for companies is their customers. However, many fail to successfullyrealize these ideas. We reveal some who have. Page 34

The meaning of justice. Renowned German author MartinWalser discusses this and other issues with Alexander Mettenheimer,CEO of private bank Merck Finck & Co. Page 58

Kotler on service marketing. The marketing guru tells think:actthat sustainability and smart communication are the key to successfulmarketing for professional services. Page 44

4

think:act is published in five languages (English, German, Chinese, Russian and Polish)

07_15gb_04_05_Inhalt 18.06.2010 13:18 Uhr Seite 4

5

contents f

food for thought

6 Football: a billion-euro marketThe beautiful game is now abooming global business.

8 Sometimes politics can’t be popular Sergey Tigipko’s fight for reform in Ukraine

10 Locking hornsWhy management conflictsshould not always be avoided

dossier

14 The thrill of complexityas seen by Pietari Posti

16 India innovates differentlyWhy India’s companies cando more than just cheap

20 Waking the giantIndia’s agricultural market is nowattracting international investors.

22 A lot of white shelvesLocal stores still dominate India’s retail trade.

25 Thirst for oilIndia’s role in the global search for crude

28 Trying to fuel the growthIndia’s government looks to domestic oil.

31 Praise to the motherWhy are Indian CEOs so successful in global corporations?

industry report

34 Customer consultingCustomers provide the ideas—howcompanies reap the benefits

42 The big realignmentHow increased banking regulationcould bring new opportunities

44 “All muscle and no fat”Philip Kotler explains how tomarket professional services.

47 Journalism: first draft of historyExclusive: think:act turns five. CNN says congratulations.

48 Future marketsArtificial photosynthesis and microscopes for molecules

business culture

50 Bracing for litigationManagement is a risky business. We investigate D&O insurances.

52 Benefiting from diversityBASF CEO Jürgen Hambrecht on European management

56 Work in progress

58 “Only money grants independence”Exclusive: author Martin Walser in discussion with leading banker Alexander Mettenheimer

61 “Don’t settle”What drives Steve Jobs?

regulars

3 First views62 Service | Credits

The country is booming—this much we know. Butfor some time now, there has been a great dealmore behind India’s growth than just an outsourc-ing destination for the developed world. Compa-nies such as Tata are developing their own identi-ty, while top Indian managers have experiencedsuccess in businesses around the world. AndIndia’s markets offer considerable growth oppor-tunities for American or European firms. In thisdossier, we take a closer look at the dynamics ofa country that is currently changing the world.

MANAGING INDIA.

MANAGING INDIAN?

DOSSIER #15

“The real interest in India is tofind the next practice. To find theunexplored innovative idea—one that can change the game.”

BILL MCDERMOTT, SAP

“India is not just about IT or business processoutsourcing. We see it as an incubator for giantglobal corporations driven by IT strategy.”

F. WARREN MCFARLAN, HARVARD BUSINESS SCHOOL

DossierManaging India. Managing Indian? Starting on page 13

!

Articles that are marked with thissymbol can also be listened to on ouraudio CD (page 63).

07_15gb_04_05_Inhalt 18.06.2010 13:18 Uhr Seite 5

6

The 2010 FIFA World Cup, to be held in South Africa, shows once again that football has become aworldwide business. The World Cup is a playground for iconic brands such as Adidas and Nike. Top clubs are now run like companies, with the aim of conquering growth markets. But here, just as in the business world, “the result is everything!”

seasons was the average employmentperiod of a team manager in the topEuropean leagues in 2009. England’sPremier League relies the most on long-term collaboration (9.7 years), whichhas proved successful in recent years.The German Bundesliga had the fastestturnover in coaches.

3.46

Mobile professionals: In the last several years, players in Europe’s five top leagues haveincreasingly demonstrated a willingness to switch teams. On average, football stars leave theirclubs 3.47 times over a 10-season period; in 2006, that figure was 3.28. Italians are the mostmobile, averaging 4.24 transfers a decade. With an average of 4.21 moves over the same timeperiod, African players show a similar inclination to seek new challenges.

Source: PFPO – The Professional Football Players’ Observatory

Chelsea FC! 268.9 million

Source: Deloitte

The football clubs with the highest revenuesworldwide in the 2007/2008 season

Growth market Asia With 85 million active players, Asia represents the biggestcontingent within FIFA, football’s global governing body. However, with this figure equivalent to just 2.2 percent ofthe total population, it has the lowest participation ratewithin the FIFA confederations.

Football: a billion-euro market

p food for thought

WORLD OF NUMBERS

FC Bayern München! 295.3 million

FC Barcelona! 308.8 million

Source: PFPO – The Professional Football Players’ Observatory

07_15gb_06_07_Zahlen 08.06.2010 9:15 Uhr Seite 6

7

food for thought f

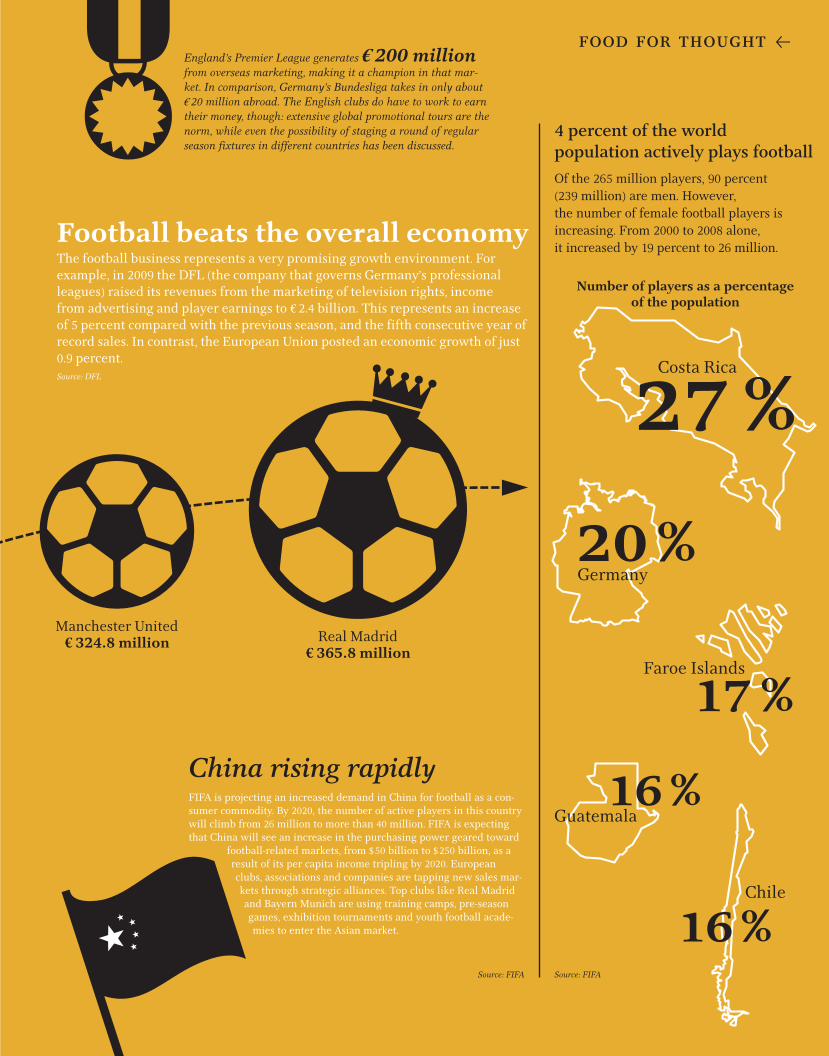

Football beats the overall economyThe football business represents a very promising growth environment. Forexample, in 2009 the DFL (the company that governs Germany’s professionalleagues) raised its revenues from the marketing of television rights, income from advertising and player earnings to ! 2.4 billion. This represents an increaseof 5 percent compared with the previous season, and the fifth consecutive year ofrecord sales. In contrast, the European Union posted an economic growth of just0.9 percent. Source: DFL

England’s Premier League generates ! 200 millionfrom overseas marketing, making it a champion in that mar-ket. In comparison, Germany’s Bundesliga takes in only about!20 million abroad. The English clubs do have to work to earntheir money, though: extensive global promotional tours are thenorm, while even the possibility of staging a round of regularseason fixtures in different countries has been discussed.

4 percent of the world population actively plays football Of the 265 million players, 90 percent (239 million) are men. However, the number of female football players isincreasing. From 2000 to 2008 alone, it increased by 19 percent to 26 million.

FIFA is projecting an increased demand in China for football as a con-sumer commodity. By 2020, the number of active players in this countrywill climb from 26 million to more than 40 million. FIFA is expectingthat China will see an increase in the purchasing power geared toward

football-related markets, from $50 billion to $250 billion, as aresult of its per capita income tripling by 2020. Europeanclubs, associations and companies are tapping new sales mar-kets through strategic alliances. Top clubs like Real Madridand Bayern Munich are using training camps, pre-seasongames, exhibition tournaments and youth football acade-mies to enter the Asian market.

China rising rapidly

Source: FIFA

Number of players as a percentage of the population

Costa Rica

27 %

20 %

17 %

16 %

16 %

Germany

Faroe Islands

Guatemala

Chile

Manchester United! 324.8 million Real Madrid

! 365.8 million

Source: FIFA

07_15gb_06_07_Zahlen 08.06.2010 9:15 Uhr Seite 7

8

p food for thought

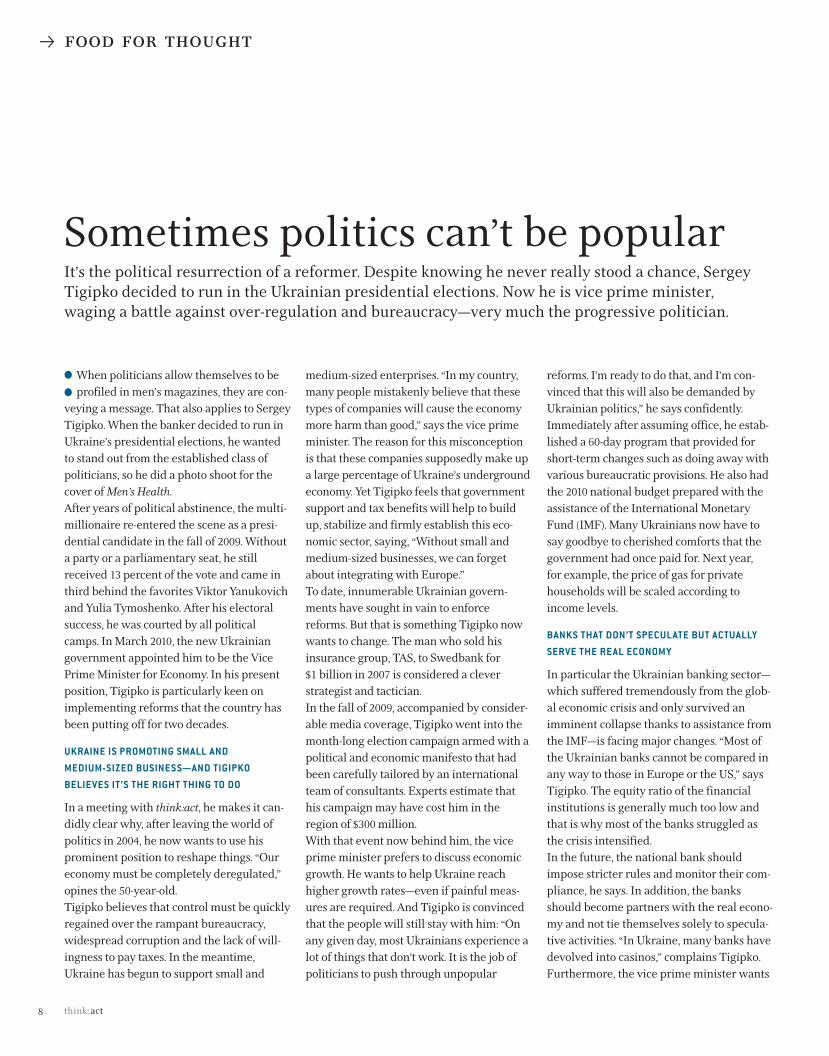

When politicians allow themselves to beprofiled in men’s magazines, they are con-

veying a message. That also applies to SergeyTigipko. When the banker decided to run inUkraine’s presidential elections, he wantedto stand out from the established class ofpoliticians, so he did a photo shoot for thecover of Men’s Health.After years of political abstinence, the multi-millionaire re-entered the scene as a presi-dential candidate in the fall of 2009. Withouta party or a parliamentary seat, he stillreceived 13 percent of the vote and came inthird behind the favorites Viktor Yanukovichand Yulia Tymoshenko. After his electoralsuccess, he was courted by all politicalcamps. In March 2010, the new Ukrainiangovernment appointed him to be the VicePrime Minister for Economy. In his presentposition, Tigipko is particularly keen onimplementing reforms that the country hasbeen putting off for two decades.

UKRAINE IS PROMOTING SMALL AND MEDIUM-SIZED BUSINESS—AND TIGIPKOBELIEVES IT’S THE RIGHT THING TO DO

In a meeting with think:act, he makes it can-didly clear why, after leaving the world ofpolitics in 2004, he now wants to use hisprominent position to reshape things. “Oureconomy must be completely deregulated,”opines the 50-year-old. Tigipko believes that control must be quicklyregained over the rampant bureaucracy,widespread corruption and the lack of will-ingness to pay taxes. In the meantime,Ukraine has begun to support small and

medium-sized enterprises. “In my country,many people mistakenly believe that thesetypes of companies will cause the economymore harm than good,” says the vice primeminister. The reason for this misconceptionis that these companies supposedly make upa large percentage of Ukraine’s undergroundeconomy. Yet Tigipko feels that governmentsupport and tax benefits will help to buildup, stabilize and firmly establish this eco-nomic sector, saying, “Without small andmedium-sized businesses, we can forgetabout integrating with Europe.” To date, innumerable Ukrainian govern-ments have sought in vain to enforcereforms. But that is something Tigipko nowwants to change. The man who sold hisinsurance group, TAS, to Swedbank for $1 billion in 2007 is considered a cleverstrategist and tactician. In the fall of 2009, accompanied by consider-able media coverage, Tigipko went into themonth-long election campaign armed with apolitical and economic manifesto that hadbeen carefully tailored by an internationalteam of consultants. Experts estimate thathis campaign may have cost him in theregion of $300 million. With that event now behind him, the viceprime minister prefers to discuss economicgrowth. He wants to help Ukraine reachhigher growth rates—even if painful meas-ures are required. And Tigipko is convincedthat the people will still stay with him: “Onany given day, most Ukrainians experience alot of things that don’t work. It is the job ofpoliticians to push through unpopular

reforms. I’m ready to do that, and I’m con-vinced that this will also be demanded byUkrainian politics,” he says confidently.Immediately after assuming office, he estab-lished a 60-day program that provided forshort-term changes such as doing away withvarious bureaucratic provisions. He also hadthe 2010 national budget prepared with theassistance of the International MonetaryFund (IMF). Many Ukrainians now have tosay goodbye to cherished comforts that thegovernment had once paid for. Next year, for example, the price of gas for privatehouseholds will be scaled according toincome levels.

BANKS THAT DON’T SPECULATE BUT ACTUALLYSERVE THE REAL ECONOMY

In particular the Ukrainian banking sector—which suffered tremendously from the glob-al economic crisis and only survived animminent collapse thanks to assistance fromthe IMF—is facing major changes. “Most ofthe Ukrainian banks cannot be compared inany way to those in Europe or the US,” saysTigipko. The equity ratio of the financialinstitutions is generally much too low andthat is why most of the banks struggled asthe crisis intensified. In the future, the national bank shouldimpose stricter rules and monitor their com-pliance, he says. In addition, the banksshould become partners with the real econo-my and not tie themselves solely to specula-tive activities. “In Ukraine, many banks havedevolved into casinos,” complains Tigipko.Furthermore, the vice prime minister wants

Sometimes politics can’t be popularIt’s the political resurrection of a reformer. Despite knowing he never really stood a chance, SergeyTigipko decided to run in the Ukrainian presidential elections. Now he is vice prime minister, waging a battle against over-regulation and bureaucracy—very much the progressive politician.

:

07_15gb_08_09_FFT2_Sergej 18.06.2010 13:17 Uhr Seite 8

9

food for thought f

to promote greater involvement from for-eign banks. “Anyone who operates accordingto honest commercial practices is welcometo do business here,” he says. “I support acombination of European, Russian andUkrainian banks. It’s good for the competi-tion and it’s the only way to revive the busi-ness sector,” Tigipko emphasizes. He would also like to see a similar mix inother segments of the Ukrainian economy.“The political realm and other branches of

the economy missed opportunities in thepast to introduce Ukrainian products innewly created markets like China andIndia,” he says, criticizing his predecessors.In the last five years, neither the country’spresident nor any of the heads of state hadconsidered it necessary to visit these coun-tries. While other nations sent trade delega-tions to Asia, the old Ukrainian leadershipignored the emerging world powers to alarge extent. Tigipko sees good prospects in

these sales markets, especially for the metal,chemical, and agricultural industries. The vice prime minister relies on his imageof a successful manager. Wearing an immac-ulately tailored dark suit, he asserts, “Oldpoliticians cannot serve new politics.” Tigipko represents change—and embodiesit, too. Men’s Health readers learned that thespry, athletic-looking man swims and jogson a daily basis.Meanwhile, other media also regularly carrystories about his domestic life with his fam-ily. His wife Viktoria describes her husbandas the “protector of the family.” Not only doeshe chop wood and perform minor repairs onthe house and car, he also packs the picnicbasket for family outings. This kind ofbehavior goes a long way in Ukraine. During the election campaign and the peri-od in which the government was beingformed, various political camps courtedTigipko in an attempt to win him over totheir side. Former Prime Minister YuliaTymoshenko had offered him many lucra-tive positions, even the job of prime minis-ter. All he would have had to do in returnwas support her in the run-off elections.However, Tigipko, ever the tactician, choseto maintain a low profile, which proved tobe a smart move. After Viktor Yanukovichwas elected president, the new leadershipappointed Tigipko as the vice prime minis-ter. In this strategy, Ukrainian experts seeTigipko preparing for another run at thepresidential office the next time around.Under President Yanukovich and Prime Min-ister Asarov, both of whom are over 60 yearsold, his prospects seem better than theywould have been under the ambitious andyounger Yulia Tymoshenko..

“In Ukraine, many banks have devolved into casinos.”Sergey Tigipko

You can also listen to this articleon our audio CD (page 63).

This portrait is based on an interview thatNina Jeglinski, dpa correspondent in Kiev, conducted exclusively for think:act.

07_15gb_08_09_FFT2_Sergej 18.06.2010 13:17 Uhr Seite 9

07_15gb_10_12_FFT3_Konflikte 18.06.2010 13:16 Uhr Seite 10

1 1

food for thought f

US President Barack Obama has learnedtwo things this year. Firstly, anyone who

wants change must also be able to acceptchange; and secondly, the most painfulblows often come from one’s own camp. As avisionary Democratic, Obama had expectedthe Republicans’ resistance to his healthcare reform plan—but that the stiffest oppo-sition might come from his own party proba-bly came as more of a surprise. Suddenly,the calls of “Yes, we can” rising from theparty faithful were mixed with whistles andeven booing. Several key delegates in hisown party opposed his plan to providehealth insurance for all Americans.Nevertheless, with one show of strength, thepresident ultimately imposed his will on hisopponents, both internally and externally.Obama can live with the fact that he is nolonger loved by every member of the Demo-crat Party. He has demonstrated the strengthof his leadership and, as a result, definitivelystabilized his position in the Americanpower hierarchy.

WHEN CONFLICTS GO UNSTATED,THE RESULT IS OFTEN STALEMATE

Obama’s experience is also played out regu-larly in companies all over the world. One’sown ranks are seldom closed. On the manag-ing boards of large corporations, it is practi-cally unheard of for all the members to be ofone mind. And it is precisely when ground-breaking decisions need to be made that dif-fering opinions and methods frequently collide. This can often be exhausting, but italso has positive effects for the company.

In fact, a difference of opinion at the highestlevel can be most beneficial because itforces everyone involved to strive to find thebest solution.In the past, conflicts of these kinds wereavoided. Management teams often workedside by side in the same company fordecades. The members of these teams kneweach other well enough to know what theycould, and couldn’t, get each of the others toagree to. Friends and enemies alike kneweverything they needed to know about theattitudes, strengths and influence of theirassociates at the top. Topics that might leadto disagreement were simply glossed over,often creating an atmosphere of resignationand stalemate. Of course, these differencesin ideas, approaches, and interests alwaysexisted, they were simply never articulated,meaning that their positive effects werenever realized.These days, managers often spend no longerthan four or five years in the employment ofa single company, which increases thepotential for conflict: executives must strug-gle to get their ideas adopted and establishthemselves in their team’s power structure.This is good for companies because it rousesthem from the unproductive slumber of“business as usual.”Accordingly, one of the most rapidly grow-ing companies in the world deliberatelybuilds conflict into its management culture:even when they are working together in agarage, refining their ideas for a new kind ofsearch engine, Google founders Larry Pageand Sergey Brin would accept no lazy

compromises. Each idea, each step was chal-lenged. No decision was taken until it hadsurvived a process of constructive conflict.This culture has been deliberately carriedover to the behemoth corporation theyfounded. The success of Google vindicatesthe approach of Page and Brin—especiallysince the company is also highly successfulon the employment market. It seems thattalented workers do not want a cossetedexistence at any price.

ANYONE CAN CONTRADICT—EVEN THE SEASONED WARHORSES

Micropolitical sensitivities, born of age dif-ferences, for example, are completely disre-garded. In order to make disagreement pro-ductive, it is important to refrain from treat-ing older employees with kid gloves as well.Google CEO Eric Schmidt has personalexperience of this. He often recounts how heargued with founders Brin and Page abouttechnical questions, even while interview-ing for the job. The founders are in theirmid-30s now, while Schmidt is 20 years theirsenior. But the veteran manager, who hadalready contributed substantially to the suc-cess of Sun and Apple, remembers this inter-view as one of the most entertaining he hadhad in a long time. And Brin and Pagerespected the opposition of this experiencedbusinessman, who never avoids an argu-ment and is even prepared to question hisown views.As CEO, Schmidt continues to propagate thisculture, which is based on questioningeverything and hiring the most widely

Locking hornsAccording to conventional wisdom, conflict in management should be avoided. But is this reallytrue? Can struggles between the top managers of a company also be constructive? They can—provided they are properly managed, as shown in the case of Google, among others.

:

You can also listen to this articleon our audio CD (page 63).

07_15gb_10_12_FFT3_Konflikte 18.06.2010 13:16 Uhr Seite 11

1 2

p food for thought

diverse people possible to pursue theirobjectives with commitment and passion.He actively promotes a culture of confronta-tion and discussion in the company. Forexample, important decisions must alwaysbe made by at least two people. The result:no solution is reached without prior discus-sion. Managers and employees at Google areexpected to pursue the widest possiblerange of goals, and then defend themagainst opposing objectives. According toSchmidt, this energy through friction is thesource of the dynamism in a growing com-pany like Google.In other corporations, while argument is notexplicitly sought, it is used to generate a con-structive outcome. Take food giant Kraft, forexample. CEO Irene Rosenfeld is combativeby nature. When she took over the job, shepromised that she would create growth.Rosenfeld promptly replaced half of themanagement team, with no regard for loss-es, to ensure support for her strategy, beforeradically restructuring the entire company.Then came the economic crisis and herpromise of growth crumbled. She was forcedto sell the US frozen-pizza business to arch-rival Nestlé.

HOW ROSENFELD WEATHERED THE STORM AS KRAFT CEO

Suddenly, the warrior found herself alone.Rosenfeld’s critics within the company andamong shareholders balked at her growthstrategy in particular: she wanted to buy theBritish chocolate manufacturer Cadbury to

close the gap on Nestlé. Suddenly, no onebelieved she could pull the deal off and hersupport within the company collapsed. Keyinvestor Warren Buffett humiliated her withan open letter calling upon Kraft sharehold-ers to overthrow the single-minded boss.But Rosenfeld was not intimidated, and inthe end, with much diplomacy, she got herway. After six months of takeover poker,Cadbury was hers and Kraft was still in hotpursuit of rival Nestlé. Rosenfeld owed hervictory not only to her persistence, but inequal measure to her ability to fight anapparently overwhelming opponent for asolution that would benefit the company. And this is important, too: good managersmust not only be able to create visions, theymust also be able to realize them, even inthe face of opposition from the managementor supervisory board. They may causeoffense along the way because, at this levelof management, there are losers as well aswinners. Refusing to acknowledge thismeans that all too often unpleasant deci-sions are avoided.With that said, it is inevitable that some dif-ferences of opinion in business will notalways be beneficial for everyone. An inter-nal conflict often ends with a shortannouncement in the finance section of thenewspapers along the lines of “The manage-ment is leaving the company by mutual con-sent.” But this result does not necessarilyhave to be detrimental to the company.When managers disagree, not only is it usu-ally the best solution that wins through, but

also the person who is best able to imple-ment it. Of course, this person also tends tobe someone who does not give up easilyunder pressure.One manager who will be leaving his com-pany in the near future is easyJet boss AndyHarrison. He is one of the main protagonistsin a massive conflict of visions with majorityshareholder and founder of the airline, Ste-lios Haji-Ioannou. He has said publicly thathe wanted the group to grow more slowly.Instead of continuing to invest, he wanted todistribute a dividend. The company man-agers had other ideas.

EVERY SUCCESSFUL CLASH ENHANCES THE PROFILE OF A TOP MANAGER

Harrison and his colleagues on the manage-ment board had previously shied away fromthis change in strategy, and had evidentlyestimated correctly. In 2009, easyJet wasamong the very few airlines in the worldthat posted a profit. But this did not mollifyHaji-Ioannou. He recently resigned his posi-tion as non-executive director under protest.Despite this, Harrison will still leave thecompany. His position in financial circleshas been clearly established through his dif-ference of opinion with the founder of thecompany. Harrison has enhanced his profileas an independent, top-level manager—something he will undoubtedly benefit fromin future disputes, whether at easyJet orelsewhere. One thing his managementboard colleagues now know for sure—he isnot one to avoid a good argument..

07_15gb_10_12_FFT3_Konflikte 18.06.2010 13:16 Uhr Seite 12

The country is booming—this much we know. Butfor some time now, there has been a great dealmore behind India’s growth than just an outsourc-ing destination for the developed world. Compa-nies such as Tata are developing their own identi-ty, while top Indian managers have experiencedsuccess in businesses around the world. AndIndia’s markets offer considerable growth oppor-tunities for American or European firms. In thisdossier, we take a closer look at the dynamics ofa country that is currently changing the world.

MANAGING INDIA.

MANAGING INDIAN?

DOSSIER #15

“The real interest in India is tofind the next practice. To find theunexplored innovative idea—one that can change the game.”

BILL MCDERMOTT, SAP

“India is not just about IT or business processoutsourcing. We see it as an incubator for giantglobal corporations driven by IT strategy.”

F. WARREN MCFARLAN, HARVARD BUSINESS SCHOOL

07_15gb_13_DOS_Einstieg 18.06.2010 13:16 Uhr Seite 13

1 4

D O S S I E R #1 5

The thrill of complexityas seen by Pietari Posti

Pietari Posti may be Finnish, but his illustration that opens our dossier sec-tion is based very much on an Indian aesthetic. Like the goddess Shiva,India’s top managers sometimes seem to have more than one pair of arms—not only are they dealing with the complexities and problems in Indian socie-ty, but they are actually finding clever solutions to them. To do this, they areoperating on an increasingly international scale, while the global players ofthis world have long discovered the attractive markets India has to offer. Thisdossier looks at both their opportunities and restrictions as well as dis-cussing whether there is such a thing as an Indian management model.

07_15gb_14_15_DOS_Illu 18.06.2010 13:14 Uhr Seite 14

Managing India. Managing Indian? D O S S I E R #1 5

07_15gb_14_15_DOS_Illu 18.06.2010 13:14 Uhr Seite 15

1 6

THEY ARE ASKING THEMSELVES the really bigquestions: how do you invent a reliable mode of trans-port for millions who don’t own a car? How do youconnect a billion people who earn less than $1,500 ayear on average? How do you show people who can’tread how to open a bank account and make wiretransfers—in regions where the nearest bank is 200kilometers away? It is not only the country’s leadingdecision makers who are asking these questions—Indian businesses are, too. And they not only are theyfinding the right answers, but they are also earningmoney with them. “There are no precedents for ourproblems—their sheer scale puts them beyond any-thing in human experience. So let us find our ownsolutions!” India’s leading industrialists have heededthis call to arms from strategy guru C. K. Prahalad,and they are finding solutions that are inconceivablein the West. It is in the emerging nation of India thatthe business models of the future are being config-ured today.

India’s industrial production is growing at anaverage rate of 15 percent a month. Sales of cars byTata Motors or Maruti Suzuki India have risen by 25percent in the last year. Most manufacturing concernsin all sectors of industry are approaching the limits oftheir capacity. India’s major corporations are growingby as much as 40 percent. In almost every industry,managers are struggling to keep up with demand.

At the same time, they are planning a takeoveroffensive. Arcelor and Corus were just the beginning.While the multinationals in the West are weakened,the management teams of Indian companies, likeauto parts supplier Bharat Forge, electrical equipmentmanufacturer Crompton Greaves, engineering firmLarsen & Toubro, or pharmaceutical developer Dr.Reddy’s are gearing up to change not only their coun-try, but also its position in the world, for good. Lead-ing the charge is Ratan Naval Tata, chairman of the

s

D O S S I E R #15 Managing India. Managing Indian?

India innovates differentlyThey can do more than just cheap. Indian companies are developing business models fromwhich their Western counterparts might learn a thing or two. In particular, they are thinking innovatively—not so much in terms of technology, more about their customers’ budgets.

Tata Group, India’s economic colossus. No other con-cern has had such a pervasive effect on the Indianeconomy and society as this empire, which wasfounded in 1868 by Jamsetji Tata. Tata products andservices are ubiquitous in India. The businessesowned by this family-held company generatebetween 3 percent and 5 percent of the country’sgross national product.

ALL INDIANS ARE PROUD of Tata’s success. Likeno other business in India, the threads of tradition andthe future, trust and incorruptibility, profit and socialresponsibility, are held firmly in the hands of theunassuming Ratan Tata. He has already unleashedone revolution, when, at the end of the last millenni-um, he transformed the elephant that was Tata into apouncing tiger. The tiger’s first leap took it into the ter-ritory of the world’s biggest steel producers. Now it isgathering itself for an attack on one of the most fero-ciously contested reserves of the old industrializednations—the production of luxury cars.

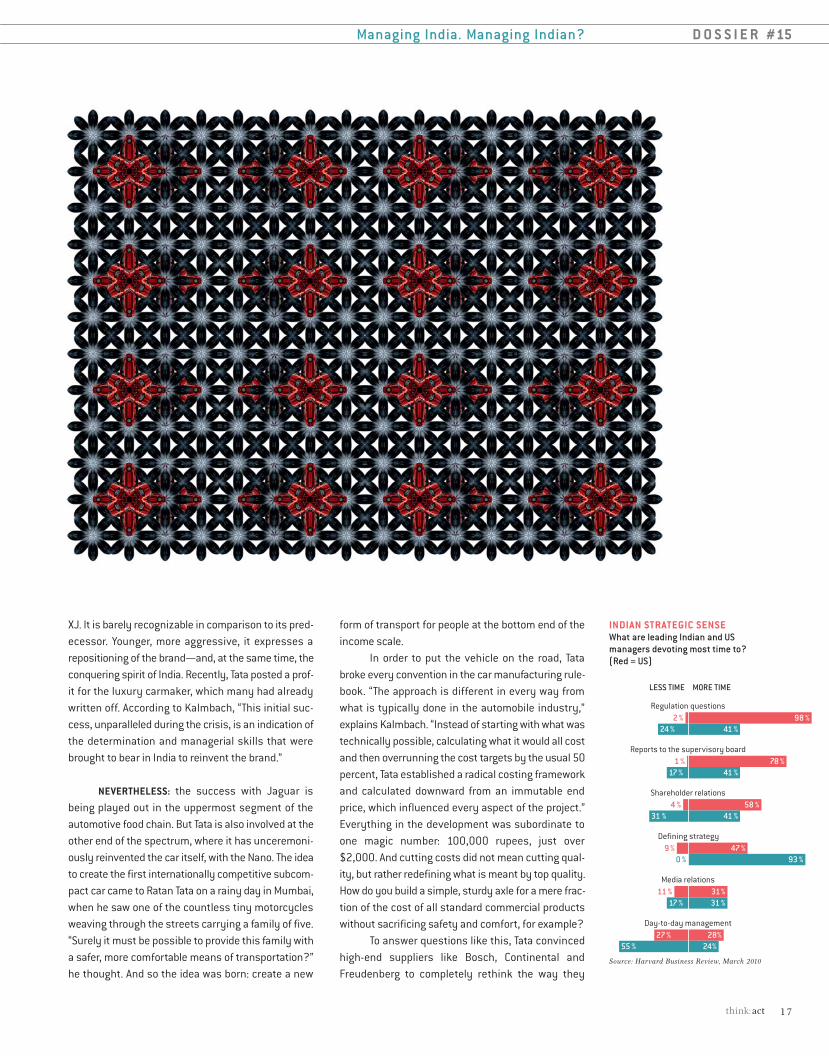

“The acquisition of Jaguar Land Rover by TataMotors is the expression of a new self-confidence,”says Ralf Kalmbach, head of the Competence CenterAutomotive at Roland Berger Strategy Consultants.“Their unassailable domination of the commercialvehicle sector at home has given them a sense ofbelief that they can compete at the top of the interna-tional automobile business.” After 40 years of resist-ance to change, and having fallen into the wronghands, the British luxury brand Jaguar looked as if itwould follow its venerable, elderly customer base intoextinction. Then came Tata. “With his clear vision,Ratan Tata showed the former colonial power how itsonce revered status symbol can be driven into thefuture,” continues Kalmbach.

The result was revealed at the last GenevaMotor Show in the shape of new flagship model, the

“I expect the Tatas to bemuch larger in 100 yearsthan they are now. Butmore importantly, I hopethe group of companies willbe the most respected inIndia—on the basis of ourprocesses, our productsand our value systems.”R ATA N TATA , C H A IR M A N, TATA S ONS

TATA GROUP, TATA MOTORSTata Motors, a part of the Tata Groupempire, is India’s largest carmaker and amarket leader in the commercial vehiclessector. The company has generated enormous interest, not only with its acquisition of Jaguar Land Rover, but also by producing the cheapest microcarin the world: the Nano.

Commercial vehicle sales from March to April 2010 in comparison withthe same period last year:

+38.31%Midsize and heavy commercial vehicles(M&HCVs) up 33.55 percent; light vehicles up 42.67 percent

Dec.Nov. Jan. Feb. Mar. Apr. May

Stock market price for Tata MotorsThe price per share for Tata Motors has risen in the last few months. Investors evidently appreciate the company’s strategy.

You can also listen to this articleon our audio CD (page 63).

07_15gb_16_19_Dos1_Titelstory 18.06.2010 13:13 Uhr Seite 16

1 7

form of transport for people at the bottom end of theincome scale.

In order to put the vehicle on the road, Tatabroke every convention in the car manufacturing rule-book. “The approach is different in every way fromwhat is typically done in the automobile industry,”explains Kalmbach. “Instead of starting with what wastechnically possible, calculating what it would all costand then overrunning the cost targets by the usual 50percent, Tata established a radical costing frameworkand calculated downward from an immutable endprice, which influenced every aspect of the project.”Everything in the development was subordinate toone magic number: 100,000 rupees, just over$2,000. And cutting costs did not mean cutting qual-ity, but rather redefining what is meant by top quality.How do you build a simple, sturdy axle for a mere frac-tion of the cost of all standard commercial productswithout sacrificing safety and comfort, for example?

To answer questions like this, Tata convincedhigh-end suppliers like Bosch, Continental andFreudenberg to completely rethink the way they

Managing India. Managing Indian? D O S S I E R #15

XJ. It is barely recognizable in comparison to its pred-ecessor. Younger, more aggressive, it expresses arepositioning of the brand—and, at the same time, theconquering spirit of India. Recently, Tata posted a prof-it for the luxury carmaker, which many had alreadywritten off. According to Kalmbach, “This initial suc-cess, unparalleled during the crisis, is an indication ofthe determination and managerial skills that werebrought to bear in India to reinvent the brand.”

NEVERTHELESS: the success with Jaguar isbeing played out in the uppermost segment of theautomotive food chain. But Tata is also involved at theother end of the spectrum, where it has unceremoni-ously reinvented the car itself, with the Nano. The ideato create the first internationally competitive subcom-pact car came to Ratan Tata on a rainy day in Mumbai,when he saw one of the countless tiny motorcyclesweaving through the streets carrying a family of five.“Surely it must be possible to provide this family witha safer, more comfortable means of transportation?”he thought. And so the idea was born: create a new

98 %41 %

78 %41 %

58 %41 %

47 %93 %

31%31 %

28%24%

2 %24 %

1 %17 %

4 %31 %

9 %0 %

11 %17 %

27 %55 %

Source: Harvard Business Review, March 2010

Regulation questions

INDIAN STRATEGIC SENSEWhat are leading Indian and US managers devoting most time to? (Red = US)

Reports to the supervisory board

Shareholder relations

Defining strategy

Media relations

Day-to-day management

MORE TIMELESS TIME

07_15gb_16_19_Dos1_Titelstory 18.06.2010 13:13 Uhr Seite 17

1 8

produced high-value auto parts. “For many parts sup-pliers, the Nano became a test laboratory for a busi-ness model, to discover how it is possible to makemoney with parts for simple, inexpensive, environ-mentally friendly vehicles,” Kalmbach explains. “TheNano was a wake-up call to the automotive industry, awarning to finally change their strategy of expectingcustomers to buy a bigger, and thus more expensive,model every time they changed cars.” Because that isprecisely what is not working any more. “The car man-ufacturers in the US, Europe and Japan will neveragain see absolute growth in their traditional battle-ground of big, expensive vehicles,” says Kalmbach.“The growth of the future is taking place in the emerg-ing nations, with small, affordable cars that allow mil-lions to move around.”

Yet even Tata had to learn that dispensing withtime-honored development structures in the automo-bile industry is a feat of strength that can only bepulled off when pursued utterly without compromise.“Time and again, the development of the Nanoreached a point at which it seemed impossible to holdto the upper price limit of 100,000 rupees,” saysKalmbach. “But Ratan Tata had given his word to theworld. And against this background, he forbade hisorganization to waver from its goal. His maxim: a promise is a promise!”

BHARTI, INDIA’S LARGEST telecommunicationsprovider, has turned the practice of amassing hugerevenues from millions of small transactions into anart form, by enabling an impoverished population tojoin a communications network. India is the fastest-growing mobile telephone market in the world. Thereare currently 500 million cellular phones in use, andby 2013 this figure is expected to top 900 million.More than 120 million current users are supplied byBharti Airtel. No one in the world offers a cheaper priceper minute—currently half a US cent. Revenue per callis minuscule. But Bharti Airtel is making enormousprofits as more and more customers in rural areas arebrought into the fold. At the moment, the company isregistering an impressive 100,000 new customersevery working day.

While India’s current strength has grown out ofits role as a service outsourcing provider for the First

World, Bharti has outsourced almost 90 percent of itscorporate processes to Western providers. Since itsfoundation, the company has been growing so rapidlythat Indian technological capacities have not beenable to keep pace. “We realized that we can capitalizeon the strength of our partners by outsourcing,”explains Jagbir Singh, Group CTO Mobility Networks ofBharti Airtel.

Network development and operation, networkdesign and system optimization, everything is doneby Ericsson. With a constant stream of multi-billion-dollar orders, it has been India’s Bharti that kept thecrisis-wracked European mobile wireless companyafloat. Other contractors, including Nokia SiemensNetworks and IBM, are also dependent on the boomof the Indian model for success.

The profits that this business model generatesare so enormous that Bharti Airtel is preparing toexpand into markets that the conventional telecom-munications providers have studiously avoided untilnow. Most recently, the company paid $9 billion foraccess to the African market. Its acquisition of sharesin Kuwaiti telecom provider Zain is the second-largestin India’s history—and it comes with another 45 mil-lion customers.

Bharti is also currently planning to enter thebanking services sector. An estimated 41 percent ofall Indians do not have their own bank account. Con-ventional big banks have no idea how to manage theenormous number of tiny bank accounts withoutmaking a loss. Bharti does. With its mobile technolo-gy, the company has the access and the capacity toreceive deposits, store the amounts and managewithdrawals made by more than 100 million residentsin the rural reaches of the country—the customerspay by cell phone.

The technology for mobile payment is providedby the company A Little World, which is one of themost creative technology providers in the world.Headquartered in Mumbai, A Little World has alreadyrevolutionized the mobile payment sector severaltimes. The latest phenomenon is the Zero-Platform.This technology converts a smartphone, a lockboxand a fingerprint scanner into a portable bank branch,which enables rural India to connect to the bank net-work and obtain microcredits. Eventually, they expect

D O S S I E R #15 Managing India. Managing Indian?

“The Indian telecommunica-tions market is currentlygoing through a hypercom-petitive phase, but we arestill making a profit. Simul-taneously, we will continuedeveloping detailed plans toexpand into marketsbeyond the borders of Indiaand southern Asia.”S U NIL BH A R T I MI T TA L , FOU N DE R , C H A IR M A NA N D GROU P C EO, BH A R T I E N T E R P RIS E S

BHARTI AIRTEL was founded in 1985 bySunil Bharti Mittal. Today, it is India’slargest mobile wireless network operatorand one of the fasting-growing telecom-munications companies in the world. It iscurrently expanding massively through-out the African continent. Bharti Airtel wasrecently named in Businessweek as oneof the six most successful technologycompanies in the world.

Sales were up 7% on the previous year, to 396 billion Indianrupees, in fiscal year 2009/2010. The EBITDA rose by 6 percent.

2006 2007 2008 2009

Sales growthThe four-year trendshows Bharti Airtel iscontinually expanding.

116.

2 bi

ll.

185.

2 bi

ll.

270.

2 bi

ll.

369.

6 bi

ll.

Volume in rupees; Source: Businessweek

07_15gb_16_19_Dos1_Titelstory 18.06.2010 13:13 Uhr Seite 18

1 9

to connect 50 million customers in this fashion. Todate, they already have three million.

Smart mobility, cheap telecommunication,mobile banking services—these products are not justuseful, but they also enable people in even theremotest corners of the world to become entrepre-neurs themselves.

According to C. K. Prahalad, this is the key toIndia’s social development. “The poor must be able tojoin forces with others as entrepreneurs. And compa-nies must earn money by providing the poor withentrepreneurial opportunities.” Indian businessesintend to make a profit from precisely this kind ofempowerment. The results are a flourishing entrepre-neurial culture, a rapidly growing middle class and anoptimistic outlook for the poor.

THE MOST INNOVATIVE EXAMPLE: Reliance Indus-tries. You can buy practically anything in the branchstores of India’s largest retailer—from vegetables toan education to gasoline. But what sets the $30 bil-lion company apart from other retail giants is itsastounding degree of vertical integration: not onlydoes Reliance tailor and sell suits under its own brandname, it also produces the fabrics from which suitscan be made, the cotton threads from which the fab-rics can be made and the machines for producing thethreads. In this way, the company offers severalpoints of contact for the business ideas of people asentrepreneurial “prosumers.” This year, Reliance wasthe only retailer included in Fast Company magazine’slist of the world’s most innovative businesses, andthis example shows why.

MORE AND MORE INDIAN banks are providing thenecessary startup capital for those who have no moresecurity to offer than a business idea and the courageof their vision. Since Muhammad Yunus developed theconcept of microcredits, the bank service of grantingthese tiny sums of money is attracting the fastest-growing clientele in the world. Recently, it has alsobeen gaining ground beyond India’s borders: the US,Spain and Germany are all copying this system ofstate aid to the “New Poor” of the First World.

After 300 years of economic stagnation, avibrant nation has awoken and is reinventing itself at

staggering speed, with boundless creativity and commercial energy. There are, of course, many prob-lems in India, for which solutions are still to be found.Take conventional electricity, for example, which isstill twice as expensive as in China, while rail travelcosts three times as much. But these problems areno longer intractable burdens—they have become thenext selling point for the next innovative businessmodel. India is making its own solutions with bothvision and pragmatism, creating business solutionsthat are being gratefully adopted by an increasingnumber of other emerging countries.

Managing India. Managing Indian? D O S S I E R #15

DOING WELL BY DOING GOOD How India’s elite social entrepreneurs live

Adulation on the streets, loyalty from theiremployees, respect from their competitors—not many captains of industry around theworld can lay claim to these accolades. ButIndian bosses can. The reason? Many of themare serious about social responsibility. Theircommitment to social causes “goes farbeyond the interests of their companies,”says Peter Cappelli, from the Wharton Schoolof Business. He recently conducted what isprobably the most comprehensive survey ofleading Indian managers ever undertaken:“Every executive we interviewed describedthe most important purpose of his companyin terms of a social mission. And not in orderto make money from it.” According to the sur-vey, shareholder value is ranked fourth ontheir list of priorities.

For example, Bharti Airtel wants to put mobilephones in the hands of people for whom anychance of telecommunication was a pipedream, until now. Indian banks, such as ICICIBank, provide starting capital for people whohave not had access to credit. Pharmaceuti-

cal manufacturer Dr. Reddy’s plans to makehealthcare affordable all over the worldthrough inexpensive medicines. And Infosysintends to show the world India deserves aplace alongside global technology leaders. Inshort: profits are a by-product, not the pri-mary purpose of a company’s activity.Many top companies have put their moneywhere their social ideals are. For example, 65percent of the profits of every company in theTata Group goes to charitable foundations;only 3 percent goes to the family. While thecompany executives live in demonstrablymodest style, their foundations financeIndia’s leading universities and researchinstitutions, campaign for education, health,food and clean drinking water. Dr. Reddy’sfinances healthcare for more than 40,000children. Infosys equips entire hospitals andschools with IT services and has launched anationwide program to develop IT skillsamong young people—a visionary idea thatmight benefit First World countries as well, asthey struggle to replace their declining tech-nical workforce. “Indian companies are notjust successful in addition to doing good forsociety. There is plenty of evidence to sug-gest that they are so successful becausethey do good,” Cappelli states. And the population expresses its appreciationto those who run these companies. Ratan Tatahas not only been awarded the “Padma Vibhushan”—India’s second-highest civilianhonor—he has also been voted the mosttrustworthy man in India.

“India’s large companies dowell because they do good.”Peter Cappelli, Wharton School of Business

07_15gb_16_19_Dos1_Titelstory 18.06.2010 13:13 Uhr Seite 19

2 0

THE ONLY SOUND that travelers hear in the ruralareas of Rajasthan, a state located in northwesternIndia, is the chugging of motorized pumps. The watercanals stemming from the days of the “Green Revolu-tion” that took place shortly after 1965 are old and thepumps don’t look much younger either. Their maincompetition are the oxen that pull long chains to liftbuckets full of water out of the wells. Most of whatgrows on the small plots is destined to feed the own-ers and their families.

Around 730 million Indians lead an existenceas subsistence farmers out in the countryside. Theywork on 120 million farms, with 60 percent of themworking on plots of land that are less than one hectarein size. India’s agricultural sector is still far frommatching the economic growth already achieved byits service and industrial sectors. While automobilesuppliers from around the world have manufacturingoperations in the industrial stronghold of Pune, andmore IT programmers work in Bangalore than in Sili-con Valley, agriculture in some parts of India has notchanged much since pre-industrial times. Millions ofwell-trained engineers, physicists and doctors haveallowed the service sector to now account for morethan half of India’s gross domestic product. In con-trast, Indian agriculture accounts for only 17 percentof the total economy–a trend that has been decreas-ing for years.

DESPITE, OR BECAUSE OF THAT, the Indian marketis highly appealing to agricultural companies theworld over. One reason is the sheer scope of it: afterChina, India is the world’s second-biggest market. “Forour company, India is a key market,” says SekharNatarajan, CEO of Monsanto India, a subsidiary of US-based Monsanto, which is involved in the seed busi-ness. Fertilizer and pesticide producers also haveIndia in their sights. There are more than 1.1 billion

s

D O S S I E R #15 Managing India. Managing Indian?

Waking the giantIndia is one of the world’s biggest agricultural markets. Until now, small-scale farmersworked the fields, but now farming companies from around the world are increasinglyheading to India, hoping that its agricultural sector will evolve into a growth driver.

Indians to be fed, prosperity is increasing, especiallyin urban centers, and eating habits are adapting toWestern standards. “Urbanization and the demand forhigh-quality food is one of the growth drivers forIndia’s agricultural market,” points out Kapil Mehan,CEO of Tata Chemicals. The subsidiary of India’sbiggest corporate conglomerate focuses solely on thedomestic market in the agricultural business.

WHEN IT COMES TO FERTILIZERS, for example,India is the world’s second-biggest market. Besidesstate-run and local, privately held suppliers, interna-tional companies have had a foothold here for quitesome time. The US-based seed producer Pioneerentered the market more than 30 years ago and sup-plies 1.5 million customers in India. Part of the mar-keting strategy includes public-private partnershipsin which companies and the government work togeth-er with farmers. In February, Pioneer, along with theagricultural authorities in the state of Uttar Pradesh,initiated a collaborative project to train farmers. “Webelieve that new seed types and services associatedwith their use are critical to making India’s agriculturemore productive,” says Pioneer CEO Paul Schickler.

However, the collaboration between the gov-ernment and business does not function as well else-where. “Right now, it’s the government especially thatis stepping on the brakes,” reports Michael Timm, anagriculture expert with Roland Berger Strategy Con-sultants. And that despite the fact that the Indian gov-ernment had made the country an agricultural trend-setter for a while. In the 1960s, the Green Revolutionbrought progress to the fields. After periods of droughtand widespread famine, the socialist governmentstepped up its efforts and pushed ahead with theplanting of high-yield crops that could be harvestedseveral times a year. The massive use of pesticidesand mineral-enriched fertilizers as well as the expan-

“For our company,India is a key market.”Sekhar Natarajan, CEO, Monsanto India

07_15gb_20_21_Dos2_Agrar 18.06.2010 13:12 Uhr Seite 20

Managing India. Managing Indian? D O S S I E R #15

2 1

sion of irrigated land have left behind obvious marks,though. For example, tremendous environmentalproblems related to over-fertilization are an everydayissue in India.

To make matters worse, little has changed interms of technology since the days of the Green Rev-olution. Very little remains of what was once progres-sive technology. The archaic pipe systems are losinghuge amounts of water by today’s standards, and themost prevalent types of towing vehicle in many partsof the country come in the form of water buffalo andzebu cattle. “The utilization of machinery is still verylow,” emphasizes Timm.

WHEN COMPARED INTERNATIONALLY, agriculturalproductivity in India does not measure up well.According to the World Bank, India only grows one-third of China’s volume in rice and only half of theamount produced by much smaller countries like Viet-nam and Indonesia. In addition, the weak infrastruc-ture prevents exports from being successful. Accord-ing to the World Bank, transporting grapes from Indiato the Netherlands is twice as expensive as fromChile, even though India is only half the distance.

That is why improved efficiency is so impor-tant. One rupee invested in agricultural developmentwould generate 9.5 rupees for the economy in termsof economic performance. However, the US-basedInternational Food Policy Research Institute hasdetermined that the additional subsidization of fertil-izer by the same amount would only generate 0.85rupees. Intelligent watering systems that would addfertilizer drop-by-drop directly into the water couldreduce costs while simultaneously protecting theearth from over-fertilization. “Instead, farmers justthrow the nitrogen-based fertilizer on to the fields bythe kilogram and wait for it to rain,” Timm says.

Despite this, the government’s reform-orientedzeal has visibly faltered over the years. It considersitself more as a protective institution that shields thearmy of small-scale farmers from fluctuating marketprices. “They represent millions of critical votes,”explains Timm. These Indian farmers are not part of

the group benefiting from the boom. In fact, they hopethat the subsidies will be enough just to survive. Withmore than 300 million Indians living under the pover-ty line, that’s not always the case.

Climate change is exacerbating the situationand, in 2009, the country saw its strongest monsoonsin almost four decades. To top it off, the population isgrowing; the government estimates that by 2017,there will be almost 1.3 billion people living in India.

Monsanto came to learn that small-scale farm-ers are an absolute necessity. The company is cur-rently working on obtaining the first approval forgenetically engineered vegetables in India. Howeverafter nationwide protests, India’s Minister of the Envi-ronment, Jairam Ramesh, relented. “The public isagainst it,” he realized in early February andannounced a moratorium. However, the head of Monsanto in India is still hopeful that his companycan roll out new seed types on the market some day,as he believes that high-yield seeds are prerequisitesfor agriculture to be more productive in India.

IMPETUS FOR INNOVATION is already coming fromthe private sector, such as in the form of contractfarming. Containing provisions pertaining to qualityand quantity, contracts are being negotiated by glob-ally active food companies on-site with farmers in allmajor sales markets, including in India, too. For exam-ple, McCain Foods, a US-based company, has beenworking with 400 farmers in the state of Gujarat forseveral years. They plant potatoes that McCain thenprocesses into frozen French fries in nearby factoriesto be sold to McDonald’s subsidiaries throughoutIndia. “Urbanization and consumption patterns thatare strongly oriented to Western habits certainly sup-port such models,” says Michael Timm. “But to date,such contracts are rare in India.”

Executing such contracts is no simple mattereither. McDonald’s came to India in the mid-1990s andneeded several years to set up a functioning supplychain. But the effort paid off, and not only for the fast-food chain; in Gujarat, agricultural growth is matchingthe rest of India’s rapidly expanding economy.

“We believe that newseed types and servic-es associated withtheir use are critical tomaking India’s agricul-ture more productive.”Paul Schickler, CEO, Pioneer

Arable land in hectares per person

India as an agriculturalproblem area

Sources: World Development Indicators Database, Datamonitor, Roland Berger

Australia

Canada

Russia

USA

Brazil

Thailand

India

China

0.16

0.28

0.10

0.35

0.61

0.88

1.39

2.52

07_15gb_20_21_Dos2_Agrar 18.06.2010 13:12 Uhr Seite 21

D O S S I E R #15 Managing India. Managing Indian?

07_15gb_22_24_Dos6_Consumergoods 18.06.2010 13:11 Uhr Seite 22

You can also listen to this articleon our audio CD (page 63).

Managing India. Managing Indian? D O S S I E R #15

2 3

INDIA IS TRULY A COLORFUL country. But thosewho base their impressions on consumer experiencesin food stores won’t see much of this color—the coun-try’s shelves have a distinct lack of it. Oil is sold intransparent plastic bottles without any labels, whilesugar and rice are available in brown paper bags orburlap sacks. Surprisingly, many products are dis-played entirely without brand names.

For multinationals, this brandlessness repre-sents an opportunity. Innovative sectors such asprocessed foods and personal care, in particular, arestill highly underdeveloped, according to an analysisconducted by Roland Berger Strategy Consultants andits Indian partner company, the Tata Strategic Man-agement Group. When it comes to soaps, detergentsand lotions, Indians spent $8.7 billion in 2008, whichis projected to increase by almost 20 percent annu-ally. Also, the $115 billion processed foods market(2007) is expected to almost triple by 2016.

Forecasts suggest that in 2025, India will bethe world’s fifth-largest consumer goods market—leaping up from 12th place in 2007. “Despite that, Indiais still not high enough on the priority list amongmany international consumer goods manufacturers,”says Andreas Bauer, head of consumer goods andretail at Roland Berger Strategy Consultants. A recentNielsen Global Consumer Confidence Study revealedthat India had already moved into second place in thespring of 2010.

After India’s economy had grown by 9 percentannually between 2007 and 2008, the country stillmanaged to grow by about 7 percent in the crisisyears. However, economists are back to projecting afigure of 8 percent for 2010—and an average growthrate of 6.3 percent annually until 2030. One reasonfor the surprisingly stable trend is that the Indianeconomy is bolstered by rapidly increasing domesticdemand. Domestic consumption already accounts for

s

A lot of white shelvesThe world’s multinationals want to move in on India’s retail trade. Their biggest competitors aren’t Indian companies, but the local mom-and-pop stores that are proving to be masters in logistics and customer focus.

more than two-thirds of the gross national product (in China, it is less than one-third). In other words,Indians are buying their way out of the crisis.

GOVIND SHRIKHANDE, CEO of Shopper’s Stop, oneof India’s biggest retail chains, is also seeing a gradualupswing in consumer behavior after the economiccrisis and the terror attacks in Mumbai. “They (Indianconsumers) are certainly loosening their pursestrings. They were on a shopping diet for a long time.”Shopper’s Stop operates 28 department stores inaddition to several subsidiaries of the stylish Hyper-CITY supermarkets. And these are not just located indowntown Mumbai or in Gurgaon, one of Delhi’s mostmodern suburbs, where almost all Indian and foreigncompanies have their headquarters. In the future,Shrikhande wants to penetrate into new regions and cities, such as Aurangabad, Amritsar and Coimbatore—places that the international businesselite haven’t heard much about to date.

In India, consumer business focused for a longtime on a small, affluent class that formed the cus-tomer base for Gucci boutiques, Armani flagshipstores and Bentley dealerships. Luxury goods manu-facturers should continue making good money fromthis class in the next few years, however the majorbusiness lies in transforming the masses living inrural areas to brand consumers. Ultimately, only 28percent of India’s 1.14 billion people live in cities. “Themarket for luxury goods is largely developed,” opinesAndreas Bauer. “The future focus is on average peopleand high-volume business.”

IN THE LAST DECADE, India’s rural economy grewup to 40 percent faster than in the cities. Now, ruralregions account for more than 50 percent of the GNP.The purchasing and economic power stemming fromthe countryside is increasing steadily, fueled by

“They are certainlyloosening their pursestrings. They were on a shopping diet fora long time.”Govind Shrikhande, CEO, Shopper’s Stop

07_15gb_22_24_Dos6_Consumergoods 18.06.2010 13:11 Uhr Seite 23

2 4

D O S S I E R #15 Managing India. Managing Indian?

tremendous, government-driven economic stimulusand infrastructure programs. It is anticipated that by2025 more than 300 million of the rural poor willbecome members of the lower middle class.

As a result, their consumer behavior maychange, too. To date, most Indians tend to shop in atraditional way. Only 6 percent of the consumer goodsbusiness is handled through modern warehouses andsupermarkets. Instead, the majority of this tradetakes place in “kirana stores”—small shops with nar-row shelves and a limited selection, located on theground floor of almost every Indian apartment build-ing. The kirana stores (also known as mom-and-popstores) are usually family operated. They benefit fromminimal personnel costs, geographic proximity tocustomers and their excellent service (includinghome deliveries). Especially important is the fact thatthey offer competitive prices, in contrast to the sametype of stores in Europe.

THIS EXPLAINS WHY THE TRULY GREAT retail revo-lution has not happened yet. According to estimatesmade by the Retailers Association of India, salesthrough modern retail channels will increase byaround 20 percent in fiscal year 2009/2010. Fasterrestructuring is also being prevented by the fact thatforeign companies are prohibited from making directinvestments. Walmart, Carrefour and other globalplayers can officially hold only a minority stake in joint ventures with Indian partners. Shopper’s Stop CEO Govind Shrikhande also doesn’t expect the investment barriers to be raised in the next sev-eral years, even though the entry of international

companies into the Indian economy could do somegood. Specifically, they would bring with them “inter-national best practices,” he says.

As it is, for the next 20 years, kirana stores arelikely to remain fixtures in India’s consumer reality,believes Bauer. Companies that want to be success-ful on the Indian consumer market can choosebetween a presence as a niche brand and developing“a bona fide Indian business model.” This wouldencompass the entire value chain, from production allthe way to setting up a multi-level distribution sys-tem. For international companies without historicalroots in India, integrating themselves into the kiranastores’ distribution network is no simple matter.According to industry experts, doing retail businessin a city like Mumbai alone would require contractswith several dozen wholesalers and distributors.

Nevertheless, penetrating the market is notimpossible. How a medium-sized European companycan get a foothold in this booming area of growth hasbeen demonstrated by Perfetti Van Melle, the confec-tionery manufacturer and producer of the mint-flavored candy, Mentos. Perfetti Van Melle holds ashare of about 30 percent in India’s candy market.There are two main reasons for the firm’s success:first, its advertising commercials carry a distinctlyBollywood aesthetic; second, Perfetti Van Melle sup-plies more than a million retailers and shops, andinstead of offering candies in large packages, it madethe canny decision to sell its Mentos in small mono-packs that cost just a few cents.

Herein lies one of the main challenges for inter-national companies—designing their products andprocesses in such a manner that they are appealingand affordable to Indians. The mobile phone giantNokia experienced a flop a few years ago when itattempted to sell phones at something approachingthe level of “Western” prices. Then it developed the1100 model that, thanks to its dustproof case andintegrated flashlight, was tailored to the needs ofIndia’s rural population. What’s more it only cost $10.This strategy helped Nokia to acquire an impressivemarket share in India of 60 percent (of a total 800million mobile phone owners) and also gave its inter-national strategy a boost; the Nokia 1100 has becomea global bestseller.

Income distribution of the population by household

Purchasing power of Indian consumers on the rise

Source: World Development Indicators Database, Datamonitor, Roland Berger; figures starting with 2009/10 are based on estimates.

Premium >12

Mass Affluent 2.4–12

Mass 1.1–2.4

Basic >1.1

2005/2006 2009/10

132

53

17

2

114

75

28

4

78

103

47

8

Income measured in 100,000 rupees

2013/14

07_15gb_22_24_Dos6_Consumergoods 18.06.2010 13:11 Uhr Seite 24

Managing India. Managing Indian? D O S S I E R #15

ON DECEMBER 4 LAST YEAR, when oil baronsaround the world gathered in India’s IT capital Banga-lore for the annual World Oil & Gas Assembly (WOGA),the pressing concern in the minds of the attendeeswas not just whether recoverable supplies willdecrease faster than they can be replaced with alter-native sources. The big issue was the need for analternative business model. “We need evolution in thisbusiness rather than revolution,” said Tony Hayward,CEO of British Petroleum. He was endorsed by KhalidA. Al-Falih, CEO of Saudi Aramco, the world’s largest oilcompany. “Three Ts—technology, talent and team-ing—can do a lot to meet the resource shortfall,” saidAl-Falih. Mukesh Ambani, India’s top oil man and oneof the hosts at the event, couldn’t agree more. Despitethe lack of direct resources, his company—RelianceIndustries Limited (RIL)—has become a major forcein the South Asian oil market.

AMBANI, WHO HAS SET UP a giant 580,000-bar-rels-per-day refinery in the city of Jamnagar in west-ern Indian state of Gujarat, is now aggressivelyimporting crude oil and is looking for overseas acqui-sitions to meet the growing demand. Low productionand logistic costs will drive further expansion of Indi-an refining capacity, says a senior consultant on oiland energy from Roland Berger Strategy Consultants.“Proper investment planning and controlling as wellas cost-conscious global sourcing will be key to fur-ther success of downstream players,” he adds. Indiancrude oil demand of 161 mt per year (2009) has beengrowing at 4.8 percent over the last five years.

Buzz about RIL’s international expansionbecame louder when it raised around $700 million byselling its treasury shares. “RIL is reviewing a numberof global opportunities for growth in its core busi-ness,” says a company spokesperson. “The difficultoperating environment of the past year has madeavailable several interesting opportunities, where an

Thirst for oilIndian oil companies go globetrotting in search for crude, which means that the globalexploration heat is growing. Meanwhile, the Indian home market is still rather restricted.

investment by a strategic operator of industrialassets can add substantial value.” The company’sattempt to acquire assets of LyondellBasell was seenas a brave step by an Indian private company toexpand. Reliance also signed a deal with Colombianstate oil firm Ecopetrol for two deepwater blocks inColombia.

AND IT IS NOT JUST RELIANCE. All major Indian oilcompanies—government and private—have steppedup the exploration heat around the world. Essar, Video-con and ONGC Videsh have been tapping into the glob-al oil pool with some success.

In the absence of resources, the low-costrefineries could become the main attraction for for-eign companies to India. At the moment, Indian com-panies are focusing on upstream activities to secureoilfield assets, says Narendra Taneja, oil expert and acommentator with Upstream, the world’s largest oiland gas newspaper. He calls it a battle for energysecurity, especially as almost 75 percent of India’scrude requirements are met through imports, conser-vatively billed at $124 billion a year. Twenty yearsfrom now—when India is expected to consume morethan double of what it does now—its crude import billis likely to soar to more than $248 billion.

Oil analysts say the fight for world oil is global,but that special attention should be paid to the activ-ities of major Chinese oil companies. China consumesmore than one-third of global oil supplies.

Recent experience has shown that Indian com-panies are often losing out to the Chinese. In August2009, India’s largest public-sector oil company, ONGC,lost its bid to acquire Swiss oil exploration firm AddaxPetroleum. It lost to Sinopec, a subsidiary of ChinaPetrochemical Corporation. China’s second-largest oilcompany shelled out $7.2 billion to seal the deal.Again in December 2009, ONGC lost its bid to developIraq’s giant Halfaya oilfield to a consortium backed by

s

OIL- AND PETROCHEMICAL-RELATED INDUSTRIES: DIFFERENT PROBLEMS

2 5

07_15gb_25_27_Dos4_Oel 18.06.2010 13:10 Uhr Seite 25

2 6

D O S S I E R #15 Managing India. Managing Indian?

07_15gb_25_27_Dos4_Oel 18.06.2010 13:10 Uhr Seite 26

2 7

Managing India. Managing Indian? D O S S I E R #15

China National Petroleum, which easily undercut theIndian company’s offer of $1.76 per barrel.

Despite a war chest of $283.5 billion in theshape of foreign reserves, for years it has been out-bid for overseas energy acquisitions. And what’sworse, says ONGC chairman RS Sharma, India doesnot even have a sovereign wealth fund, which is cru-cial for acquiring global energy assets. It has been reli-ably learned that the Indian Finance Ministry couldeventually agree to set up a $20 billion sovereignfund to help Indian oil and gas explorers compete withtheir international rivals.

EVEN AS THE INDIAN COMPANIES start a global oilshopping tour, the entry of international players inIndia has remained restricted. The retail oil marketcontinues to be subsidized and controlled by the gov-ernment. However in recent times, it has shown signsof loosening its grip. “We do expect a new form of reg-ulation which improves the balance between afford-able fuels for the public competitiveness of Indian oil-cos and necessary subsidization by the Indian state.This should enable state owned companies as well astheir private competitors to succeed,” says WalterPfeiffer, oil expert and partner at Roland Berger Strategy Consultants. “Lower subsidization will drivesignificant efforts to increase efficiency across alldownstream operations.”

Sustainable biofuel is seen as a direct alterna-tive to oil and gas in the country. “India has regionswhich could perfectly profit from investments in sustainable second generation biofuels,” says theexpert. The government has already decided todecrease the dependency on crude oil imports and isencouraging investment in alternative areas that aresustainable in the long run. The country’s bio-dieselprocessing capacity is estimated at 600,000 tons peryear. Bio-diesel in India is virtually a non-starter. Thereare many reasons for that, the main ones being the non-availability of vegetable oil and governmentpolicies. The edible oils are in short supply, and thecountry has to import up to 40 percent of its requirements.

The Indian bio-fuel policy was announced inDecember 2009. The government has set a target of20 percent by 2017 for the blending of bio-fuels—

bio-ethanol and bio-diesel. Addressing concerns, ithas declared that bio-diesel production will be takenup from non-edible oil seeds in waste, degraded andmarginal lands. Bio-ethanol already enjoys a conces-sional excise duty of 16 percent, and bio-diesel isexempted from excise duty.

AS THE INDIAN ECONOMY continues to growquickly, its energy needs are mounting rapidly. It isclear that Indian oil companies will not be able to meetthe requirement, and soon the market will be openedfor international players. The central question is whenand how.

INDIA AND ITS OIL

• Oil India plans to disinvest by selling 11 percent of its equity.

• Essar has projects in Vietnam, Myanmar,Madagascar and Nigeria.

• Videocon and BPCL have oil blocks in Mozambique.

• Reliance is present in Oman, East Timor, Australia, Peru, Columbia, Kurdistan and Yemen.

• A $20 billion sovereign fund is expected tohelp Indian oil and gas explorers compete withtheir Chinese rivals.

07_15gb_25_27_Dos4_Oel 18.06.2010 13:10 Uhr Seite 27

D O S S I E R #15 Managing India. Managing Indian?

2 8

ON APRIL 03, 2010, India’s largest public-sectorcommercial enterprise, Indian Oil Corporation (IndianOil), entered into a joint venture with Taiwan’s TSRCCorporation and Japan’s Marubeni Corporation to setup a state-of-the-art styrene-butadiene rubber (SBR)unit at Panipat, an industrial town around 130 kmfrom New Delhi. The unit, with a capacity of 120,000metric tons per annum, is expected to produce high-quality synthetic rubber used in the manufacture ofautomotive tires, conveyors and fan belts.

This is one of the many projects that haverecently been signed between leading internationalcompanies and India’s public-sector petrochemicalcorporations. The country has a major unexploitedmarket with immense growth potential. India’s cur-rent per capita consumption of polyester is 1.4 kg andit accounts for 3.1 percent of the total world polymerconsumption of 200 million tons per year.

HOWEVER, IN RECENT TIMES, there have beeninstances when these agreements haven’t lastedlong. Some foreign players have withdrawn from keyprojects. In 2009, French petrochemical major Totalpulled out its investment from a venture to set up agreenfield refinery-cum-petrochemical project wortharound $7.1 billion in Vizag in the southeastern stateof Andhra Pradesh. Apart from Indian public-sectorgiants like GAIL, OIL and HPCL, the venture boastedMittal Energy as one of its partners.

“Indian projects are continuously delayed. Itwill be a challenge to make them happen on schedule,within budget,” says Arjen de Leeuw den Bouter ofRoland Berger Strategy Consultants. The Indian petro-chemical sector, which is one of the country’s faster-growing industry segments, at 13 percent per annum,faces a number of challenges as it tries hard to attractforeign partners. High costs of energy and raw mate-rials, and access to basic infrastructure, are amongthe major troubles of this sector. India’s chemical

s

Trying to fuel the growthThe government of India is trying hard to change the image of the petrochemical sectorin the country. It is offering sops and tax holidays to attract foreign players.

industry currently operates out of 25 major clusters,with the western states accounting for 65 percent ofthem. The states of Gujarat and Maharashtra are hostto most of the refining, petrochemical and down-stream chemical complexes.

THE PRODUCTS FROM THESE STATES are facingsteep competition from cheap Middle Easternproducts. “The single most importantquestion is how the Indian petro-chemical industry, especially onthe west coast, is able to com-pete with Middle Eastern prod-ucts. This will be extremely dif-ficult, and tariff barriers seemto be India’s only defense,”says de Leeuw den Bouter.

In order to enable Indiato leverage the critical successfactors for the development ofthe chemical industry, the gov-ernment has launched specialeconomic zones (SEZ) calledPetroleum, Chemicals and Petro-chemicals Investment Regions(PCPIR).

IT IS PROVIDING BENEFITS such as better roadand rail linkages and income tax holidays for 10 yearsto attract investment in these clusters. According toTata Strategic Management Group (TSMG), the PCPIRpolicy is expected to open up tremendous businessopportunities in the chemical and petrochemical sec-tor. Both the central and state governments haveannounced incentives such as fast-track clearancefrom respective ministries to induce public-privatepartnerships and continued fiscal benefits. The gov-ernment plans to establish three PCPIRs with a likelyinvestment of $92 billion (as estimated by TSMG). In

OIL- AND PETROCHEMICAL-RELATED INDUSTRIES: DIFFERENT PROBLEMS

07_15gb_28_30_Dos3_Chemie 18.06.2010 13:09 Uhr Seite 28

Managing India. Managing Indian? D O S S I E R #15

2 9