management’s discussion and analysis of … sap, the commissioner's reserve valuation method...

TRANSCRIPT

Annex 1

A-1

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF PICA

AS OF AND FOR THE THREE MONTHS ENDED MARCH 31, 2009

(See Annex A for definitions of certain terms used in this Management‘s Discussion and Analysis)

Summary of Principal Differences between SAP and GAAP

The financial information for The Prudential Insurance Company of America (―PICA‖) in this

Management‘s Discussion and Analysis has been prepared in accordance with SAP. SAP differs in certain

respects, which in some cases may be material, from GAAP.

The significant differences between SAP and GAAP are noted below:

The SAP financial statements of PICA are not consolidated with those of its subsidiaries. The

value of its subsidiaries are recorded as Preferred Stock, Common Stock and Other Invested

Assets.

Under SAP, policy acquisition costs, such as commissions, and other costs incurred in

connection with acquiring new business, are expensed when incurred; under GAAP, such costs

are deferred and amortized either over the expected lives of the contracts, based on the level and

timing of either gross margins, gross profits or gross premiums, depending on the type of

contract.

Under SAP, the Commissioner's Reserve Valuation Method is used for the majority of

individual insurance reserves; under GAAP, individual insurance policyholder liabilities for

traditional forms of insurance are generally established using the net level premium method.

For interest-sensitive policies, a liability for policyholder account balances is established under

GAAP based on the contract value that has accrued to the benefit of the policyholder. Policy

assumptions used in the estimation of policyholder liabilities are generally prescribed under

SAP; under GAAP, policy assumptions are based upon best estimates as of the date the policy is

issued, with provisions for the risk of adverse deviation.

Under SAP, the Commissioner's Annuity Reserve Valuation Method is used for the majority of

individual deferred annuity reserves; under GAAP, individual deferred annuity policyholder

liabilities are generally equal to the contract value that has accrued to the benefit of the

policyholder, together with liabilities for certain guarantees under variable annuity contracts.

Under SAP, reinsurance reserve credits taken by ceding entities as a result of reinsurance

contracts are netted against the ceding entity‘s policy and claim reserves and unpaid claims;

under GAAP, reinsurance recoverables are reported as assets.

Under SAP, an interest maintenance reserve ("IMR") is established to capture realized

investment gains and losses, net of tax, on the sale of bonds and is amortized into income over

the remaining years to expected maturity of the assets sold or impaired; under GAAP, no such

reserve is required. See discussion under ―Impairments of Bonds‖ related to changes in PICA‘s

impairment policy.

Under SAP, an asset valuation reserve ("AVR") based upon a formula prescribed by the NAIC

is established as a liability to offset potential investment losses, and changes in the AVR are

charged or credited directly to surplus; under GAAP, no such reserve is required.

Under SAP, investments in bonds and preferred stocks are generally carried at amortized cost;

A-2

under GAAP, investments in bonds and preferred stocks, other than those classified as held to

maturity, are carried at fair value.

Under SAP, certain assets designated as non-admitted are excluded from assets by a direct

charge to surplus; under GAAP, such assets are carried on the balance sheet with appropriate

valuation allowances.

Under SAP, surplus notes are recorded as a component of surplus; under GAAP, surplus notes

are recorded as a liability.

Under SAP, an extraodinary distribution approved by PICA‘s regulator may be recorded as a

return of capital; under GAAP, the distribution is recorded as a dividend when PICA has

undistributed retained earnings.

Under SAP, goodwill is subject to admissability limits and is amortized over a period not to

exceed ten years; under GAAP, goodwill is subject to impairment testing and not amortized.

Under SAP, income tax expense is based upon taxes currently payable. Changes in deferred

taxes are reported in surplus and subject to admissability limits; under GAAP, changes in

deferred taxes are generally recorded in income tax expense.

Under SAP, charges recorded for pension and postretirement health benefits only include

charges for vested employees; under GAAP, charges for pension and postretirement health

benefits include charges for both vested and non-vested employees.

Under SAP, deposits to universal life contacts and limited payment contracts are credited to

revenue; under GAAP, such deposits are reported as policyholder account balances.

Under SAP, interest-related other-than-temporary impairments for bonds are determined based

primarily upon the Company‘s intent to sell; under GAAP, interest-related other-than-temporary

impairments for debt securities are based primarily upon whether we intend to sell the security

or more likely than not will be required to sell the security before recovery of its amortized cost

basis.

Overview

PICA is one of the largest insurance companies in the United States. The principal products and services of

PICA include individual life insurance and annuities, group insurance and pension and retirement products and

related services and administration. The results in the analysis below include the results of the Closed Block

business, which comprises the assets and related liabilities of the Closed Block, defined below. The principal

executive offices of PICA are located in Newark, New Jersey.

At March 31, 2009, PICA's admitted assets were $228 billion (including $80 billion held in separate

accounts), compared to $237 billion (including $88 billion held in separate accounts) at December 31, 2008.

Excluding separate accounts, assets were primarily comprised of a mix of bonds, mortgage loans, contract loans,

cash and short-term investments, and equity investments designed to match the cash flow requirements of

insurance liabilities.

Demutualization

On the date of the demutualization, PICA converted from a mutual life insurance company to a stock life

insurance company and became a direct, wholly owned subsidiary of PH, a wholly owned subsidiary of PFI.

The demutualization was carried out under PICA‘s Plan of Reorganization, dated as of December 15, 2000, as

A-3

amended.

On the date of the demutualization, PFI completed an initial public offering of its Common Stock, as well as

the sale of shares of Class B Stock, a separate class of common stock, through a private placement. In addition,

on the date of the demutualization, PH, which owns the capital stock of PICA, issued $1.75 billion in senior

secured notes (the "IHC debt"). A portion of the IHC debt was insured by a bond insurer.

The Plan of Reorganization required PICA to establish and operate a regulatory mechanism known as the

―Closed Block.‖ The policies that are included in the Closed Block (the "Closed Block Policies") are specified

participating individual life insurance policies and individual annuity contracts that were in force on the date of

the demutualization and on which PICA was paying or expected to pay experience-based policy dividends. The

Closed Block is designed generally to provide for the reasonable expectations of holders of participating

individual life insurance policies and annuities included in the Closed Block for future policy dividends after

demutualization by allocating assets that will be used for payment of benefits, including policyholder dividends,

on these policies. The Plan of Reorganization provided that PICA may, with the prior consent of the

Commissioner, enter into agreements to transfer to a third party all or any part of the risks under the Closed

Block Policies. As of December 31, 2008, PICA had reinsurance agreements covering 90% of the Closed Block

Policies, including 17% with an affiliate.

Results of Operations

Net (Loss) Income

2009 to 2008 Three Month Comparison. Net income (loss) increased $710 million from $238 million of net

loss for the three months ended March 31, 2008 to net income of $472 million for the three months ended March

31, 2009. The increase in net income (loss) between years was primarily driven by an increase in operating

income before income taxes of $501 million principally driven by an increase of $361 million in the Retirement

business between periods mainly as a result of the termination during the first quarter of 2009 of funding

agreements previously issued by PICA to PFI. The termination of these funding agreements resulted in a net

gain of $285 million for PICA. Operating income before income taxes in the individual life and annuity business

increased $57 million between periods primarily driven by a $232 million net gain due to negative reinsurance

treaty experience related to the modified co-insurance (―MODCO‖) agreements of the Closed Block business.

These MODCO agreements require payment from the reinsurers in the event of unfavorable investment

experience in the Closed Block business that is not absorbed by adjustments to policyholder dividends. As a

result of this negative reinsurance treaty experience, future positive experience would require payments to the

reinsurer. Also contributing to the gain between periods was a reduction in the 2009 dividend scale related to the

Closed Block business. Partially offsetting these gains was a decrease in deferred premiums between years

related to a reserve valuation basis change and an increase in minimum death benefit guarantee reserve charges.

Corporate and other business operating income before taxes increased $49 million between periods primarily

driven by an increase in affiliated bond income mainly due to the note established as a result of PFI‘s

contribution of Prudential Securities Group, LLC (―PSG Holdings, LLC‖) to PICA during the fourth quarter of

2008 and a decline in interest expense on borrowed money. Additionally, group insurance operating income

before taxes increased $23 million between years, which primarily reflects the favorable experience in the group

life, disability and long-term care businesses.

The income tax provision decreased from $45 million to ($120) million between years and was mainly due to

the following two items: (1) a decline in the PICA‘s effective tax rate primarily driven by permanent tax

adjustments in the current period, principally the exclusion of the net gain resulting from the termination of

funding agreements previously issued by PICA to PFI, and (2) the net benefit from the release of liabilities

previously provided for uncertain tax positions as a result of the settlement of an IRS examination in 2009,

including a decrease in interest expense accrued on uncertain tax positions.

A-4

Net income (loss) also included a decrease in net realized capital (losses) of $44 million, from ($330) million

for the three months ended March 31, 2008 to ($286) million for the three months ended March 31, 2009. Net

realized capital losses included $534 million and $494 million of other-than-temporary impairments for the three

months ended March 31, 2009 and 2008, respectively. The decline in net realized capital losses is further

discussed below under ―Capital (Losses)‖. See discussion under ―Impairments of Bonds‖ related to changes in

PICA‘s impairment policy.

Change in Statutory Capital and Surplus

2009 to 2008 Three Month Comparison. Statutory capital (surplus plus asset valuation reserve) decreased

$309 million, from $7,679 million at December 31, 2008 to $7,370 million at March 31, 2009. The change in

capital and surplus for the three months ended March 31, 2009 was primarily driven by:

A ($651) million change in net unrealized capital (losses) mainly due to losses on derivative instruments

and unaffiliated bond losses during the first quarter of 2009. The change in net unrealized (losses) is

further discussed below under ―Capital (Losses)‖; and

A ($223) million change in net deferred taxes. For interim reporting, the change in net deferred taxes is

computed using an estimated annual effective tax rate. This rate is computed as the ratio of projected

change in net deferred tax assets for the entire year over projected statutory pre-tax net income for the

year. The rate used for interim reporting will vary period over period as projected reversal and

generation of deferred tax assets or liabilities and projected statutory pre-tax income for the year is

updated based on the best information available as of the reporting date.

Partially offset by:

A $472 million of net income, as discussed above.

The remaining $93 million change in capital and surplus during the three months ended March 31, 2009 was

driven by a decline in certain non-admitted assets, such as the prepaid pension asset and non-admitted deferred

taxes. Additionally, changes in the valuation basis of reserves in individual life accounted for the remaining

change in capital and surplus.

Revenues

2009 to 2008 Three Month Comparison. Total revenues increased $208 million from $5,711 million for the

three months ended March 31, 2008 to $5,919 million for the three months ended March 31, 2009. The increase

in total revenues was primarily driven by an increase in other income of $373 million, from income of $150

million for the three months ended March 31, 2008 to income of $523 million for the three months ended March

31, 2009. The increase in other income is mainly due to the termination of funding agreements contracted

between PICA and PFI. The termination of these funding agreements resulted in a net gain of $285 million for

PICA. Additionally, the increase in other income was driven by a favorable $172 million change in adjustments

related to the MODCO agreements of the Closed Block business. The adjustments are based on formulas set

forth in these MODCO agreements that are mainly affected by investment experience. However, the net increase

in other income due to these MODCO agreements is more than offset by the net of similar adjustments in

premiums, benefits, expenses and dividends to policyholders. As a result, excluding the impact of negative

reinsurance treaty experience, the MODCO agreements of the Closed Block have a minimal impact on net gain

from operations. As discussed above under ―Net (Loss) Income‖ negative reinsurance treaty experience will

result in a net gain for PICA, which is recorded through premiums. Also contributing to the increase in revenues

was an increase between periods in net investment income, including IMR amortization, of $98 million from

$1,797 million for the three months ended March 31, 2008 to $1,895 million for the three months ended March

A-5

31, 2009. The increase in net investment income was mainly driven by an increase in bond income. The increase

in other income and net investment income was partially offset by a decline in premiums of $263 million

between years from $3,764 million for the three months ended March 31, 2008 to $3,501 million for the three

months ended March 31, 2009. The change in premiums was primarily driven by:

A $245 million decline in the retirement business mainly due to a decline in separate account deposits by

institutional investors between years. Partially offsetting the decline was an increase in general account

contributions, which correlates with a shift to investments that offer more stable returns;

A $129 million decrease in individual life and annuity premiums was primarily driven by a decline in

deferred premiums related to the reserve valuation basis change in the individual life segment as discussed

above under ―Change in Statutory Capital and Surplus‖. Partially offsetting the decline was an increase in

premiums in the Closed Block business as a result of adjustments to the MODCO agreements, including the

impact of the negative reinsurance treaty experience.

Partially offset by:

A $77 million increase in premiums primarily due to growth in the group life and long term care businesses

in the current year.

A $34 million increase between years in the international insurance business principally driven by higher

premiums assumed from Prudential of Japan as a result of growth in the business.

Benefits

2009 to 2008 Three Month Comparison. Total benefits, surrenders and fund withdrawals decreased $212

million, from $5,190 million for the three months ended March 31, 2008 to $4,978 million for the three months

ended March 31, 2009. The decrease in total benefits, surrenders and fund withdrawals was primarily due to a

decrease of $215 million in the individual life and annuity business mainly driven by lower contract values

between years as a result of the equity market decline. Additionally, benefits, surrenders and fund withdrawals

in the retirement business declined $181 million mainly due to a decline between years in the level of large

withdrawals in the separate accounts by institutional investors. Partially offsetting the decline in separate

account withdrawals in the retirement business was an increase in traditional GIC withdrawals between periods.

In addition there was an increase of $166 million between years in the group insurance business primarily due to

an increase in surrenders and withdrawals.

Net (Decrease) Increase in Reserves

2009 to 2008 Three Month Comparison. Reserves increased $585 million for the three months ended March

31, 2009, compared to an increase of $1,043 million for the three months ended March 31, 2008. The decrease

of $458 million in the change in reserves between years was primarily due to a decrease of $564 million in the

retirement business mainly due to the increase in withdrawals of traditional GIC‘s as discussed under

―Benefits‖. Partially offsetting the decrease in reserves in the retirement business was an increase of $72 million

between years in the Group Insurance business primarily driven by increase in policy loans and growth in the

group life business.

Commissions

2009 to 2008 Three Month Comparison. Commissions decreased $6 million from $137 million for the three

months ended March 31, 2008 to $131 million for the three months ended March 31, 2009. The change

between years was primarily driven by a decline in sales of institutional investor products in the retirement

business.

A-6

Other Expenses

2009 to 2008 Three Month Comparison. Other expenses increased $103 million from $30 million for the

three months ended March 31, 2008 to $133 million for the three months ended March 31, 2009. The increase

in other expenses was mostly due to reserve adjustments on reinsurance assumed related to the Allstate annuity

acquisition. These adjustments were mostly offset by net premiums, benefits, withdrawals and policyholder

dividends assumed as part of the reinsurance of the Allstate business.

.

Net Transfer (From) To Separate Accounts

2009 to 2008 Three Month Comparison. Net transfer from separate accounts were $1,129 million for the

three months ended March 31, 2009, compared to $1,351 million for the three months ended March 31, 2008.

The $222 million change between years was principally driven by a decline in surrenders and withdrawals in the

retirement business as previously discussed under ―Benefits‖.

Dividends to Policyholders

2009 to 2008 Three Month Comparison. Dividends to policyholders increased $58 million from $525

million for the three months ended March 31, 2008 to $583 million for the three months ended March 31, 2009.

The increase was primarily driven by changes in certain adjustments related to the reinsurance of the Closed

Block business, as discussed above under ―Revenues.‖ Partially offsetting the increase due to the reinsurance

related adjustments was a decrease in accrued policyholder dividends as a result of a lower dividend scale in the

current year.

Income Tax (Benefit) Provision

2009 to 2008 Three Month Comparison. The income tax (benefit) provision declined $165 million between

years from a provision of $45 million for the three months ended March 31, 2008 to a benefit of ($120) million

for the three months ended March 31, 2009. The decline in income taxes between years was primarily driven by

the following two items: (1) a decline in PICA‘s effective tax rate as a result of certain permanent adjustments in

the current period, principally the exclusion of the net gain resulting from the termination of funding agreements

previously issued by PICA to PFI as discussed above under "Net (Loss) Income," and the net benefit from the

release of liabilities previously provided for uncertain tax positions as a result of the settlement of an IRS

examination in 2009, including a decrease in interest expense accrued on uncertain tax positions.

Capital (Losses)

2009 to 2008 Three Month Comparison. Net realized capital (losses) after taxes and contribution to the

IMR, decreased $44 million, from net realized capital (losses) of $330 million for the three months ended March

31, 2008 to net realized capital (losses) of $286 million for the three months ended March 31, 2009. The

following table sets forth the components of net realized capital (losses):

Three Months Three Months

Ended

March 31,

Ended

March 31,

2009 2008 Change

($ in millions)

Bonds…………………….……………………………….. $ (204) $ (338) $ 134

Equity securities………………………………………….. (222) (92) (130)

Derivative instruments……………………………………. 315 103 212

A-7

Other……………………………………………………… (63) 10 (73)

Gross realized capital (losses)………………….. (174) (317) 143

Less capital gains tax ………………….……………… 21 - 21

Less IMR transfers, net of tax…………………………….. 91 13 78

Net realized capital (losses)…..…………………… …... $ (286) $ (330) $ 44 (92)

103

10

The change in net realized capital (losses) was driven by $534 million of other-than-temporary

impairments for the three months ended March 31, 2009. The other-than-temporary impairments for the three

months ended March 31, 2009 consisted of $303 million related to bonds, $230 million related to common stock

and $1 million related to preferred stocks. Partially offsetting these other-than-temporary impairments were

realized net gains in derivative instruments for the three months ended March 31, 2009. Other-than-temporary

impairments for the three months ended March 31, 2008 were $494 million and included $441 million related to

bonds and $51 million related to common stocks and $2 million related to preferred stock. Other-than-

temporary impairments recorded on bonds for the three months ended March 31, 2008 included $365 million

related to asset-backed securities collateralized by sub-prime mortgages. For a further discussion on other-than-

temporary impairments, see ―Impairments of Bonds‖ below.

Net unrealized capital losses increased $651 million for the three months ended March 31, 2009 compared

to an increase of $344 million for the three months ended March 31, 2008. The increase during the first quarter

of 2009 was primarily driven by unrealized losses on derivative instruments mainly due to realized net gains on

derivatives in the current period as discussed above. By realizing these gains, a corresponding offset to change

in unrealized capital (losses) occurs. Additionally, unrealized unaffiliated bond losses were $217 million for the

three months ended March 31, 2009. The unrealized losses on bonds resulted primarily from an increase in

NAIC 6 rated debt securities. Statutory accounting policy requires that NAIC 6 rated debt securities be recorded

at fair value. For further discussion on change in unrealized capital losses on bonds see ―Impairments of Bonds‖

below. Also, a decrease in affiliated common stocks contributed to the net unrealized capital losses during the

first quarter of 2009 primarily driven by a net loss in PICA‘s insurance subsidiary, PLI, mainly due to individual

annuity losses. Partially offsetting these unrealized losses was the tax benefit related to unrealized (losses). The

unrealized capital (losses) in 2008 were principally driven by unrealized losses on common stock and other

invested assets mainly as a result of equity market declines.

Investment Results

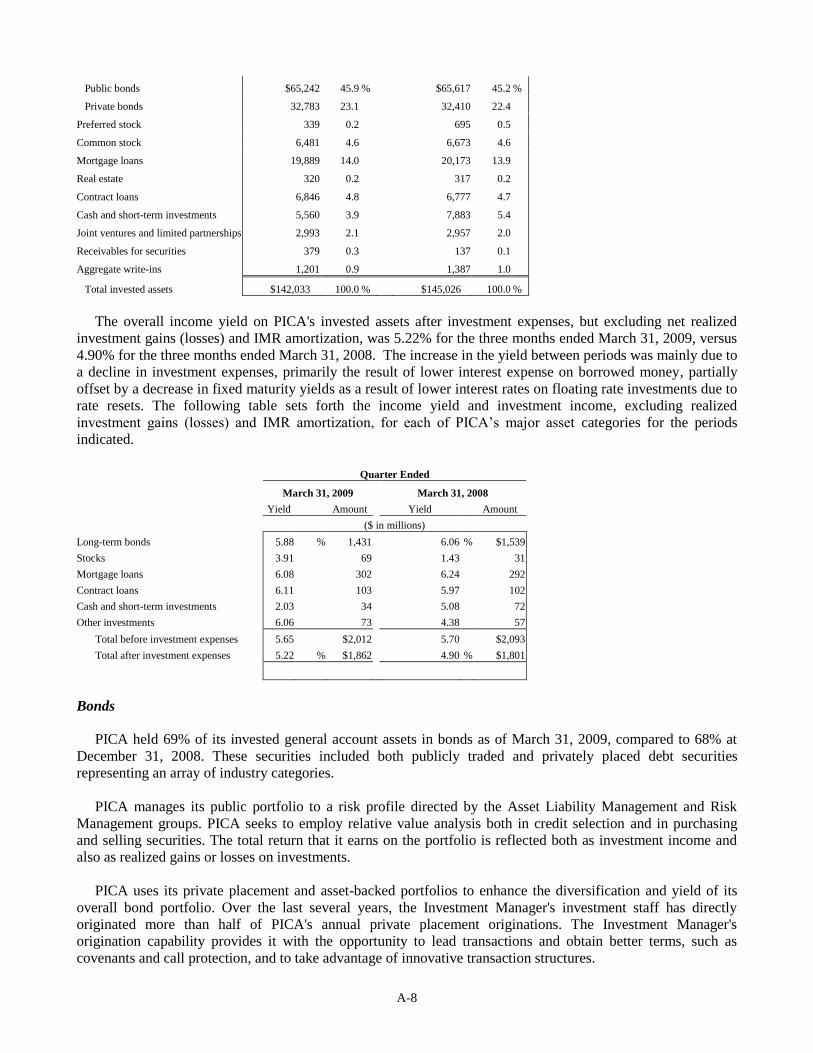

Summary of Investments

PICA's general account investment portfolio consists of public and private bonds, mortgage loans, equity

securities, contract loans, real estate and other invested assets. The composition of PICA's portfolio reflects,

within the discipline provided by its risk management approach, its need for competitive results and the

selection of diverse investment alternatives available primarily through its Investment Manager. The size of

PICA's portfolio enables it to invest in asset classes that may be unavailable to the typical investor.

The following table sets forth the composition of PICA's invested assets as of the dates indicated in

accordance with SAP.

March 31, 2009 December 31, 2008

Carrying % of Carrying % of

Amount Total Amount Total

($ in millions)

Long-term bonds

A-8

Public bonds $65,242 45.9 % $65,617 45.2 %

Private bonds 32,783 23.1 32,410 22.4

Preferred stock 339 0.2 695 0.5

Common stock 6,481 4.6 6,673 4.6

Mortgage loans 19,889 14.0 20,173 13.9

Real estate 320 0.2 317 0.2

Contract loans 6,846 4.8 6,777 4.7

Cash and short-term investments 5,560 3.9 7,883 5.4

Joint ventures and limited partnerships 2,993 2.1 2,957 2.0

Receivables for securities 379 0.3 137 0.1

Aggregate write-ins 1,201 0.9 1,387 1.0

Total invested assets $142,033 100.0 % $145,026 100.0 %

The overall income yield on PICA's invested assets after investment expenses, but excluding net realized

investment gains (losses) and IMR amortization, was 5.22% for the three months ended March 31, 2009, versus

4.90% for the three months ended March 31, 2008. The increase in the yield between periods was mainly due to

a decline in investment expenses, primarily the result of lower interest expense on borrowed money, partially

offset by a decrease in fixed maturity yields as a result of lower interest rates on floating rate investments due to

rate resets. The following table sets forth the income yield and investment income, excluding realized

investment gains (losses) and IMR amortization, for each of PICA‘s major asset categories for the periods

indicated.

Quarter Ended

March 31, 2009 March 31, 2008

Yield Amount Yield Amount

($ in millions)

Long-term bonds 5.88 % 1,431 6.06 % $1,539

Stocks 3.91 69 1.43 31

Mortgage loans 6.08 302 6.24 292

Contract loans 6.11 103 5.97 102

Cash and short-term investments 2.03 34 5.08 72

Other investments 6.06 73 4.38 57

Total before investment expenses 5.65 $2,012 5.70 $2,093

Total after investment expenses 5.22 % $1,862 4.90 % $1,801

Bonds

PICA held 69% of its invested general account assets in bonds as of March 31, 2009, compared to 68% at

December 31, 2008. These securities included both publicly traded and privately placed debt securities

representing an array of industry categories.

PICA manages its public portfolio to a risk profile directed by the Asset Liability Management and Risk

Management groups. PICA seeks to employ relative value analysis both in credit selection and in purchasing

and selling securities. The total return that it earns on the portfolio is reflected both as investment income and

also as realized gains or losses on investments.

PICA uses its private placement and asset-backed portfolios to enhance the diversification and yield of its

overall bond portfolio. Over the last several years, the Investment Manager's investment staff has directly

originated more than half of PICA's annual private placement originations. The Investment Manager's

origination capability provides it with the opportunity to lead transactions and obtain better terms, such as

covenants and call protection, and to take advantage of innovative transaction structures.

A-9

The following table sets forth the composition of PICA's long-term bond portfolio by industry category as of

the dates indicated.

March 31, 2009 December 31, 2008

% of Estimated % of Estimated

Amortized Total Fair Amortized Total Fair

Cost Cost Value Cost Cost Value

($ in millions)

US governments $4,463 4.6 % $5,123 $4,354 4.4 % $5,399

All other governments 1,625 1.7 1,826 1,738 1.8 2,003

Political subdivisions of states, territories, & possessions 0.0 0.0

(direct & guaranteed)

Special revenue & special assessment obligations & 6,783 6.9 7,245 7,265 7.4 7,741

non guaranteed obligations of agencies

Public utilities 7,200 7.3 6,822 7,333 7.5 6,962

Industrial & miscellaneous (unaffiliated) 73,829 75.3 62,693 72,213 73.7 61,504

Credit tenant loans (unaffiliated) 59 0.1 61 60 0.1 62

Parent, subsidiaries and affiliates 4,066 4.1 4,002 5,064 5.1 5,139

Total long-term bonds $98,025 100.0 % $87,772 $98,027 100.0 % $88,810

As of March 31, 2009, Industrial & miscellaneous (unaffiliated) included approximately $8.8 billion ($4.9

billion fair value) of securities collateralized by sub-prime mortgages. While there is no market standard

definition, we define sub-prime mortgages as residential mortgages that are originated to weaker quality

obligors as indicated by weaker credit scores, as well as mortgages with higher loan to value ratios, or limited

documentation. The significant deterioration of the U.S. housing market, high interest rate resets, and relaxed

underwriting standards for some originators of sub-prime mortgages have led to higher delinquency rates,

particularly for those mortgages issued in 2006 and 2007. The following table sets forth the composition of our

asset-backed securities as of March 31, 2009 by credit quality, and for asset-backed securities collateralized by

sub-prime mortgages, by year of issuance (vintage).

A-10

__________ (1) Our enhanced short-term portfolio is used primarily to invest cash proceeds of securities lending and repurchase activities, and cash generated from

certain trading and operating activities. The investment policy statement of this portfolio requires that securities purchased for this portfolio have a remaining expected average life of 2 years or less when acquired.

The table above provides ratings assigned by nationally recognized rating agencies, as of March 31, 2009,

and reflect credit rating downgrades on asset-backed securities collateralized by sub-prime mortgages processed

by the rating agencies in 2009. The following tables set forth the percentage, based on amortized cost, of our

asset-backed securities collateralized by sub-prime mortgages attributable to the Financial Services Businesses

by lowest rating agency rating, as of the dates indicated.

Asset-Backed Securities Collateralized by Sub-prime Mortgages Lowest Rating Agency Rating

AAA AA A BBB

BB and

below

December 31, 2008 24 % 23 % 12 % 20 % 21 %

March 31, 2009 8 % 19 % 13 % 16 % 44 %

In making our investment decisions, rather than relying solely on the rating agencies‘ evaluations, PICA

assigns internal ratings to our asset-backed securities based upon our dedicated asset-backed securities unit‘s

independent evaluation of the underlying collateral and securitization structure, including any guarantees from

monoline bond insurers. The $8.8 billion ($4.9 billion fair value) of asset-backed securities collateralized by

sub-prime mortgages as of March 31, 2009 represents a $0.8 billion decrease from $9.6 billion as of December

31, 2008, primarily reflecting principal paydowns and other-than-temporary impairments recognized.

As of March 31, 2009, Industrial & miscellaneous (unaffiliated) included approximately $0.8 billion ($0.4

billion fair value) of externally managed investments in the European market. At December 31, 2008,

externally managed investments in the European market were approximately $0.8 billion ($0.5 billion fair

value). The externally managed investments in European markets, included in the above table, reflects PICA‘s

March 31, 2009

Lowest Rating Agency Rating

Vintage AAA AA A BBB

BB and

below

Total

Amortized

Cost

Total

Fair

Value

($ in millions)

Collateralized by sub-prime mortgages:

Enhanced short-term portfolio (1)

2009 .............................................................. $ $

$ $ $ $ $ 2008 .............................................................. 2007 .............................................................. 86 14 35 30 702 867 524 2006 .............................................................. 324 386 233 472 993 2,408 1,808

2005 .............................................................. 33 1 19 53 43

2004 & Prior ................................................. Total enhanced short-term portfolio .................... 443 400 269 502 1,714 3,328 2,375

All other portfolios

2009 .............................................................. 2008 .............................................................. 2007 .............................................................. 31 18 393 442 179

2006 .............................................................. 153 103 168 383 1,416 2,223 928 2005 .............................................................. 21 262 232 204 237 956 448

2004 & Prior ................................................. 95 899 430 272 144 1,840 955

Total all other portfolios ................................... 300 1,282 830 859 2,190 5,461 2,510

Total collateralized by sub-prime mortgages ....... 743 1,682 1,099 1,361 3,904 8,789 4,885 Other asset-backed securities:

Collateralized by auto loans .............................. 738 64 7 99 9 917 876

Collateralized by credit cards ............................ 186 1,029 1,215 845 Externally managed investments in the

European market 206 581 787 411

Other asset-backed securities ............................ 767 85 81 112 133 1,178 985

Total asset-backed securities ....................... $ 2,434 $ 1,831 $ 1,393 $ 3,182 $ 4,046 $ 12,886 $ 8,002

A-11

investment in medium term notes that are collateralized by portfolios of assets primarily consisting of European

fixed income securities, including corporate bonds and asset-backed securities as well as derivatives. As of

March 31, 2009 none of the underlying investments were securities collateralized by U.S. sub-prime mortgages,

and most of the underlying investments were rated investment grade.

As of March 31, 2009, Industrial & miscellaneous (unaffiliated) included $7.4 billion ($6.3 billion fair

value) of commercial mortgage-backed securities. At December 31, 2008, commercial mortgage-backed

securities were $7.5 billion ($6.2 billion fair value). Weakness in commercial real estate fundamentals, along

with a decrease in the overall liquidity and availability of capital have led to a very difficult refinancing

environment and an increase in the overall delinquency rate on commercial mortgages in the commercial

mortgage-backed securities market. Difficult conditions in the global financial markets and the overall economic

downturn continue to put additional pressure on these fundamentals through rising vacancies, falling rents and

falling property values. In addition, we have recognized several market factors related to commercial mortgage-

backed securities issued in 2006 and 2007, including less stringent loan underwriting, higher levels of leverage

and collateral valuations that are generally no longer realizable. To ensure our investment objectives and asset

strategies are maintained, we consider these market factors in making our investment decisions on securities in

these vintages. The following table sets forth the composition of our commercial mortgage-backed securities as

of March 31, 2009 by credit quality and by the year of issuance (vintage).

As of March 31, 2009, based on amortized cost, approximately 95% of the commercial mortgage-backed

securities attributable to PICA have estimated credit subordination percentages of 20% or more, and 70% have

estimated credit subordination percentages of 30% or more. The subordination percentage represents the current

weighted average estimated percentage of the capital structure subordinated to our investment holding that is

available to absorb losses before the security incurs the first dollar loss of principal. The estimated

subordination percentage includes an adjustment for that portion of the capital structure that has been effectively

defeased by US Treasury securities.

Commercial Mortgage-Backed Securities -Subordination Percentages by Rating and Vintage March 31, 2009

Lowest Rating Agency Rating

Vintage AAA AA A BBB

BB and

below

2009 ............................................................. — % — % — % — % — % 2008 ............................................................. 28 — — — —

2007 ............................................................. 29 — — — —

2006 ............................................................. 30 — — — — 2005 ............................................................. 28 — — — —

2004 & Prior ................................................ 35 24 30 26 21

The following table sets forth the amortized cost of our AAA commercial mortgage-backed securities as of

the dates indicated, by type and by year of issuance (vintage).

March 31, 2009

Lowest Rating Agency Rating

Vintage AAA AA A BBB

BB and

below

Total

Amortized

Cost

Total

Fair

Value

($ in millions)

2009 .............................................................. $ $ $ $ $ $ $ 2008 .............................................................. 10 10 8

2007 .............................................................. 970 19 989 774

2006 .............................................................. 2,582 2,582 2,094

2005 .............................................................. 1,906 1,906 1,619

2004 & prior .................................................. 1,733 98 57 8 4 1,900 1,759

Total commercial mortgage backed

securities .............................................. $

7,201 $ 98 $ 76 $ 8 $ 4 $ 7,387 $ 6,254

A-12

AAA Rated Commercial Mortgage-Backed Securities – Amortized Cost by Type and Vintage

March 31, 2009

Super Senior AAA Structures Other AAA Structures

Vintage

Super

Senior

(shorter

duration

tranches)

Super

Senior

(longest

duration

tranche) Mezzanine Junior

Other

Senior

Other

Subordinate

Other

Total AAA

Securities at

Amortized

Cost

(in millions)

2009 .............................................................. $ — $ — $ — $ — $ — $ — $ — $ — 2008 .............................................................. 10 — — — — — — 10 2007 .............................................................. 945 25 — — — — — 970

2006 .............................................................. 1,804 748 — — — — 30 2,582 2005 .............................................................. 1,404 485 — — — — 17 1,906 2004 & Prior ................................................. 81 27 — — 1,296 3102 19 1,733

Total ..................................................... $ 4,244 $ 1,285 $ — $ — $ 1,296 $ 310 $ 66 $ 7,201

Certain of PICA‘s bonds are supported by guarantees from monoline bond insurers. As of March 31,

2009, $1.5 billion, or 2%, of general account bonds were supported by guarantees from monoline bond insurers.

At December 31, 2008, $1.7 billion, or 2% of the general account bonds were supported by guarantees from

monoline bond insurers. As of March 31, 2009, 31% of these investments had A credit ratings or higher,

reflecting the credit quality of the monoline bond insurers. Management estimates, taking into account the

structure and credit quality of the underlying investments and giving no effect to the support of these securities

by guarantees from monoline bond insurers, that 42% of the $1.5 billion would have investment grade credit

ratings. Additionally, $1.1 billion of the $1.5 billion of securities supported by bond insurance were asset-

backed securities collateralized by sub-prime mortgages, $0.2 billion were other asset-backed securities and $0.2

billion were municipal bonds. Management estimates that 24% of the asset-backed securities collateralized by

sub-prime mortgages, 75% of the other asset-backed securities, and all of the municipal bonds would have

investment grade credit ratings giving no effect to the support of these securities by guarantees from monoline

bond insurers. As of March 31, 2009, the bond insurance is provided by five insurance companies, with no

company representing more than 36% of the overall amortized cost of the securities supported by bond

insurance.

The following table sets forth the amortized cost and fair value of our fixed maturity investments supported

by guarantees from monoline bond insurers as of March 31, 2009.

March 31, 2009

($ in millions)

Amortized

Cost

Fair

Value

Fixed maturities guaranteed by monoline bond insurers Asset-backed securities:

Collateralized by sub-prime mortgages $ 1,057 $ 650

Other 217 171

Total asset-backed securities 1,274 821

Municipal bonds 211 218

Total $ 1,485 $ 1,039

The SVO of the NAIC evaluates the investments of insurers for regulatory reporting purposes and assigns

bonds to one of six categories called "NAIC Designations." NAIC designations of "1" or "2" include bonds

considered investment grade, which include securities rated Baa3 or higher by Moody's or BBB- or higher by

S&P. NAIC Designations of "3" through "6" are referred to as below investment grade, which include securities

rated Ba1 or lower by Moody's and BB+ or lower by S&P. As a result of time lags between the funding of

investments, the finalization of legal documents, and the completion of the SVO filing process, the bond

A-13

portfolio generally includes securities that have not yet been rated by the SVO as of each balance sheet date.

Pending receipt of SVO ratings, the categorization of these securities by NAIC designation is based on the

expected ratings indicated by internal analysis.

The fair values of public bonds are based on quoted market prices or prices obtained from independent

pricing services. In order to validate reasonability, prices are obtained from multiple independent services where

available and are also reviewed by our internal asset managers through comparison with directly observed recent

market trades or comparison of all significant inputs used by the pricing service to our observations of those

inputs in the market. For investments in private bonds, this information is not available. For these private

bonds, the fair value is determined typically by using a discounted cash flow model, which relies upon the

average of spread surveys collected from private market intermediaries who are active in both primary and

secondary transactions and takes into account, among other factors, the credit quality of the issuer and the

reduced liquidity associated with private bonds. In determining the fair value of certain bonds, the discounted

cash flow model may also use unobservable inputs, which reflect PICA‘s own assumptions about the inputs

market participants would use in pricing the asset.

The following tables set forth PICA's public and private bond portfolios by NAIC rating as of the dates

indicated.

Public Bonds by Credit Quality

March 31, 2009 December 31, 2008

Rating % of Estimated % of Estimated

NAIC Agency Amortized Total Fair Amortized Total Fair

Rating Equivalent Cost Cost Value Cost Cost Value

($ in millions)

1 Aaa, Aa, A $41,233 63.2 % $38,989 $42,697 65.1 % $40,894

2 Baa 15,534 23.8 12,852 15,901 24.2 13,255

Subtotal Investment Grade $56,767 87.0 $51,841 $58,598 89.3 $54,149

3 Ba 4,389 6.7 3,416 4,059 6.2 3,027

4 B 2,874 4.4 1,800 2,292 3.5 1,484

5 C and lower 1,072 1.7 564 624 0.9 435

6 In or near default 140 0.2 151 44 0.1 47

Subtotal Below Investment Grade $8,475 13.0 % $5,931 $7,019 10.7 % $4,993

Total $65,242 100.0 % $57,772 $65,617 100.0 % $59,142

Private Bonds by Credit Quality

March 31, 2009 December 31, 2008

Rating % of Estimated % of Estimated

NAIC Agency Amortized Total Fair Amortized Total Fair

Rating Equivalent Cost Cost Value Cost Cost Value

($ in millions)

1 Aaa, Aa, A $11,063 33.7 % $10,517 $10,705 33.0 % $10,299

2 Baa 15,906 48.5 14,556 15,653 48.3 14,305

Subtotal Investment Grade $26,969 82.2 $25,073 $26,358 81.3 $ 24,604

A-14

3 Ba 3,545 10.8 3,061 3,681 11.4 3,120

4 B 1,484 4.6 1,193 1,536 4.7 1,193

5 C and lower 456 1.4 333 418 1.3 326

6 In or near default 329 1.0 340 417 1.3 425

Subtotal Below Investment Grade $5,814 17.8 % $4,927 $6,052 18.7 % $ 5,064

Total $32,783 100.0 % $30,000 $32,410 100.0 % $29,668668

The amortized cost of PICA's below-investment grade bonds as of March 31, 2009 totaled $14.3 billion, or

14.6% of amortized cost of total bonds, compared to $13.1 billion, or 13.3% of total bonds, as of December 31,

2008.

PICA maintains separate monitoring processes for public and private bonds and creates watch lists to

highlight bonds that require special scrutiny and management. The public bond asset managers formally review

all public bond holdings on a quarterly basis, and more frequently when necessary, to identify potential credit

deterioration, whether due to ratings downgrades, unexpected price variances, and/or industry specific concerns.

For private placements, the Investment Manager's credit and portfolio management processes help ensure

prudent controls over valuation and management. The Investment Manager uses separate pricing and

authorization processes to establish "checks and balances" for new investments. The Investment Manager

applies consistent standards of credit analysis and due diligence for all transactions, whether they originate

through its own in-house origination staff or through agents. The Investment Manager's regional offices closely

monitor the portfolios in their regions. The Investment Manager sets all valuation standards centrally and

assesses the fair value of all investments quarterly.

Impairments of Bonds

All bonds with unrealized losses are subject to review to identify other-than-temporary impairments in value.

In evaluating whether a decline in value is other-than-temporary, PICA considers several factors including, but

not limited to the following:

the reasons for the decline in value (credit event, currency or interest rate related, including general

spread widening);

PICA's ability and intent to hold its investment for a period of time to allow for recovery of value;

PICA's intent to sell its investment before recovery of the cost of the investment;

the financial condition of and near-term prospects of the issuer; and the extent and the duration of the

decline.

In the second quarter of 2008, effective January 1, 2008, PICA, for its statutory reporting, implemented the

guidance as outlined in Interpretation 06-07 in the Statutory Accounting Practices & Procedures Manual for

evaluating interest related other-than-temporary impairments. Under statutory accounting, the term "interest

related" includes a declining value due to both increases in the risk free interest rate and general credit spread

widening. An interest related impairment is deemed other-than-temporary when PICA has the intent to sell an

investment, at the reporting date, before recovery of the cost of the investment. An interest related decline

where PICA does not have the intent to sell is deemed temporary and an impairment is not recorded.

Previously, for statutory accounting and reporting, PICA followed its GAAP other-than-temporary impairment

policy for evaluating bond other-than-temporary impairments, under which impairments were generally not

differentiated between interest related and non-interest related. By making the change to follow statutory

accounting principles for evaluating interest-related bond impairments, other-than-temporary interest-related

A-15

bond impairments previously recorded by PICA during the first quarter of 2008 were reduced by $131 million in

its financial statements as of second quarter 2008. This adjustment has not been retroactively reflected in the

first quarter 2008 results in the accompanying ―Statutory Statements of Operations and Changes in Capital and

Surplus‖. Prior to 2008, the impact of differences in statutory accounting principles and PICA's GAAP

impairment policies were considered immaterial on PICA's financial results.

Effective January 1, 2008, PICA voluntarily early adopted SSAP No. 98 ―Treatment of Cash Flows When

Quantifying Changes in Valuation and Impairments, an Amendment to SSAP No. 43" ("SSAP No. 98"). At the

time PICA voluntarily early adopted SSAP No. 98, SSAP No. 98 had a required adoption date of January 1,

2009. On April 17, 2009, the NAIC deferred the mandatory implementation date of SSAP No. 98 to periods

ending on or after September 30, 2009. The deferral of SSAP No. 98 does not address the accounting by

companies that early adopted SSAP No. 98. In light of the deferral of the mandatory adoption date, PICA

modified its impairment policy, on a prospective basis beginning in the first quarter of 2009, to follow the

guidance of SSAP No. 43 "Loan-backed and Structured Securities," which continues to apply, prior to the

adoption of SSAP No. 98.

Under SSAP No. 43, an other-than-temporary impairment has occurred when the undiscounted future cash

flow value of the security is less than the cost basis, at which point the cost basis of the security is written down

to the undiscounted future cash flow value, with no provision for recording interest-related other-than-temporary

impairments to the IMR. SSAP No. 98 required that, upon the determination that an other-than-temporary

impairment has occurred, the cost basis of the security should be written down to fair value. SSAP No. 98 also

provided that credit related other-than-temporary losses should be recorded to Realized Gains (losses) with an

adjustment to the AVR while interest related other-than-temporary losses should be applied directly to the IMR.

Application of SSAP No. 43 for the three months ended March 31, 2009 resulted in other-than-temporary

impairments, recorded to Realized Gains (Losses), on loan-backed and structured securities held at March 31,

2009 of $43 million, which would have been approximately $1.2 billion higher under the application of SSAP

No. 98. However, changes in unrealized losses would have been $0.2 billion lower under the application of

SSAP No. 98. While management believes SSAP No. 98 will be modified or further deferred, absent such a

change or further deferral of the mandatory adoption of SSAP No. 98 for periods ending on or after September

30, 2009 or other regulatory developments, or absent PICA requesting and obtaining a specific permitted

practice from the New Jersey Department of Banking and Insurance (―NJDOBI‖), PICA would recognize this

incremental amount of other-than temporary impairments related to these securities in its results and surplus for

the nine months ended September 30, 2009.

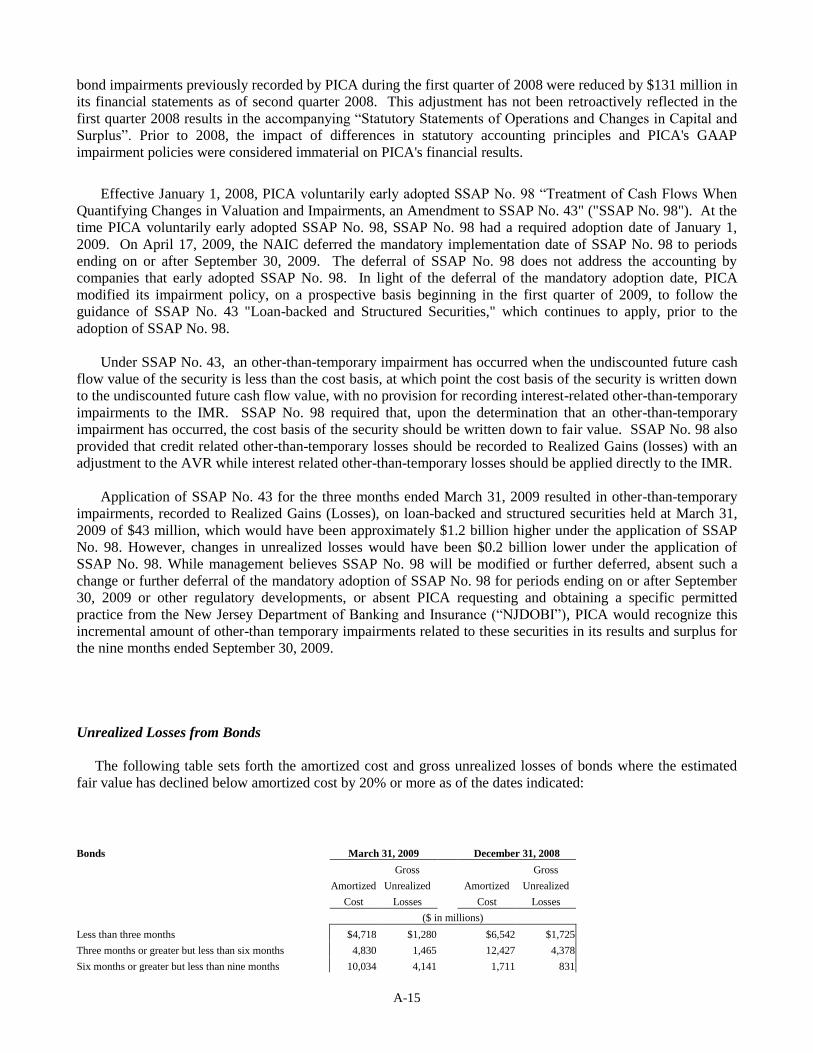

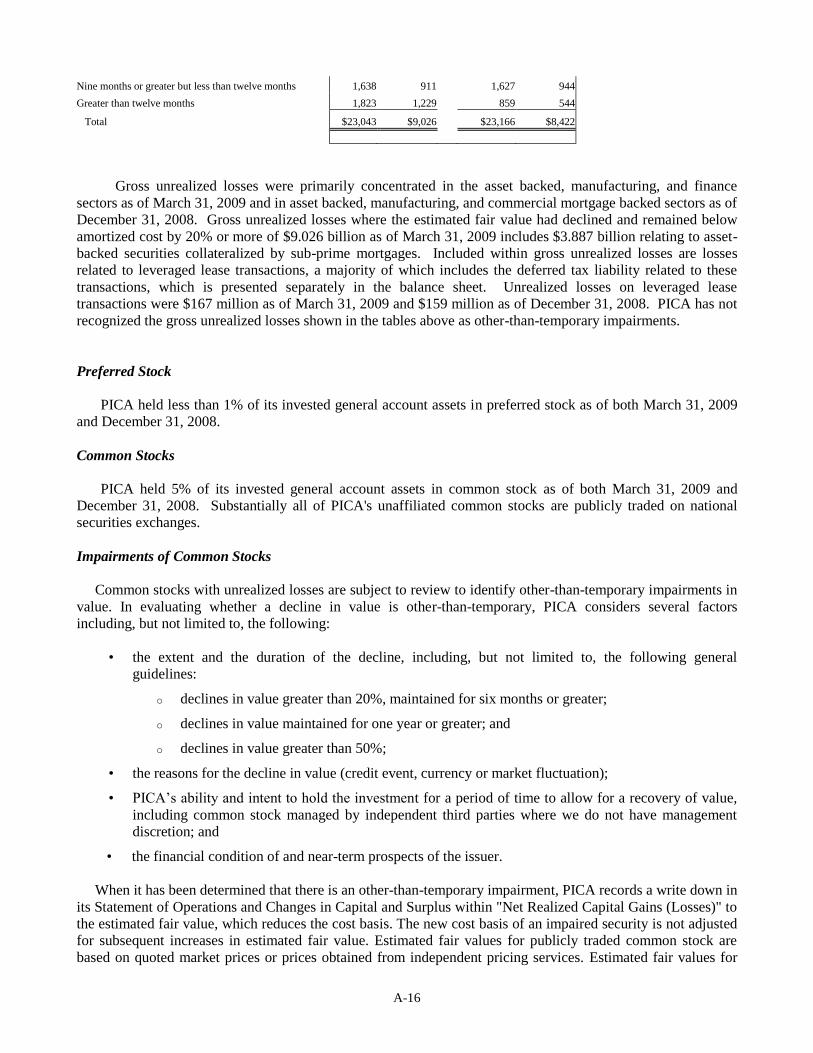

Unrealized Losses from Bonds

The following table sets forth the amortized cost and gross unrealized losses of bonds where the estimated

fair value has declined below amortized cost by 20% or more as of the dates indicated:

Bonds March 31, 2009 December 31, 2008

Gross Gross

Amortized Unrealized Amortized Unrealized

Cost Losses Cost Losses

($ in millions)

Less than three months $4,718 $1,280 $6,542 $1,725

Three months or greater but less than six months 4,830 1,465 12,427 4,378

Six months or greater but less than nine months 10,034 4,141 1,711 831

A-16

Nine months or greater but less than twelve months 1,638 911 1,627 944

Greater than twelve months 1,823 1,229 859 544

Total $23,043 $9,026 $23,166 $8,422

Gross unrealized losses were primarily concentrated in the asset backed, manufacturing, and finance

sectors as of March 31, 2009 and in asset backed, manufacturing, and commercial mortgage backed sectors as of

December 31, 2008. Gross unrealized losses where the estimated fair value had declined and remained below

amortized cost by 20% or more of $9.026 billion as of March 31, 2009 includes $3.887 billion relating to asset-

backed securities collateralized by sub-prime mortgages. Included within gross unrealized losses are losses

related to leveraged lease transactions, a majority of which includes the deferred tax liability related to these

transactions, which is presented separately in the balance sheet. Unrealized losses on leveraged lease

transactions were $167 million as of March 31, 2009 and $159 million as of December 31, 2008. PICA has not

recognized the gross unrealized losses shown in the tables above as other-than-temporary impairments.

Preferred Stock

PICA held less than 1% of its invested general account assets in preferred stock as of both March 31, 2009

and December 31, 2008.

Common Stocks

PICA held 5% of its invested general account assets in common stock as of both March 31, 2009 and

December 31, 2008. Substantially all of PICA's unaffiliated common stocks are publicly traded on national

securities exchanges.

Impairments of Common Stocks

Common stocks with unrealized losses are subject to review to identify other-than-temporary impairments in

value. In evaluating whether a decline in value is other-than-temporary, PICA considers several factors

including, but not limited to, the following:

• the extent and the duration of the decline, including, but not limited to, the following general

guidelines:

o declines in value greater than 20%, maintained for six months or greater;

o declines in value maintained for one year or greater; and

o declines in value greater than 50%;

• the reasons for the decline in value (credit event, currency or market fluctuation);

• PICA‘s ability and intent to hold the investment for a period of time to allow for a recovery of value,

including common stock managed by independent third parties where we do not have management

discretion; and

• the financial condition of and near-term prospects of the issuer.

When it has been determined that there is an other-than-temporary impairment, PICA records a write down in

its Statement of Operations and Changes in Capital and Surplus within "Net Realized Capital Gains (Losses)" to

the estimated fair value, which reduces the cost basis. The new cost basis of an impaired security is not adjusted

for subsequent increases in estimated fair value. Estimated fair values for publicly traded common stock are

based on quoted market prices or prices obtained from independent pricing services. Estimated fair values for

A-17

privately traded common stock are determined using valuation and discounted cash flow models that require a

substantial level of judgment.

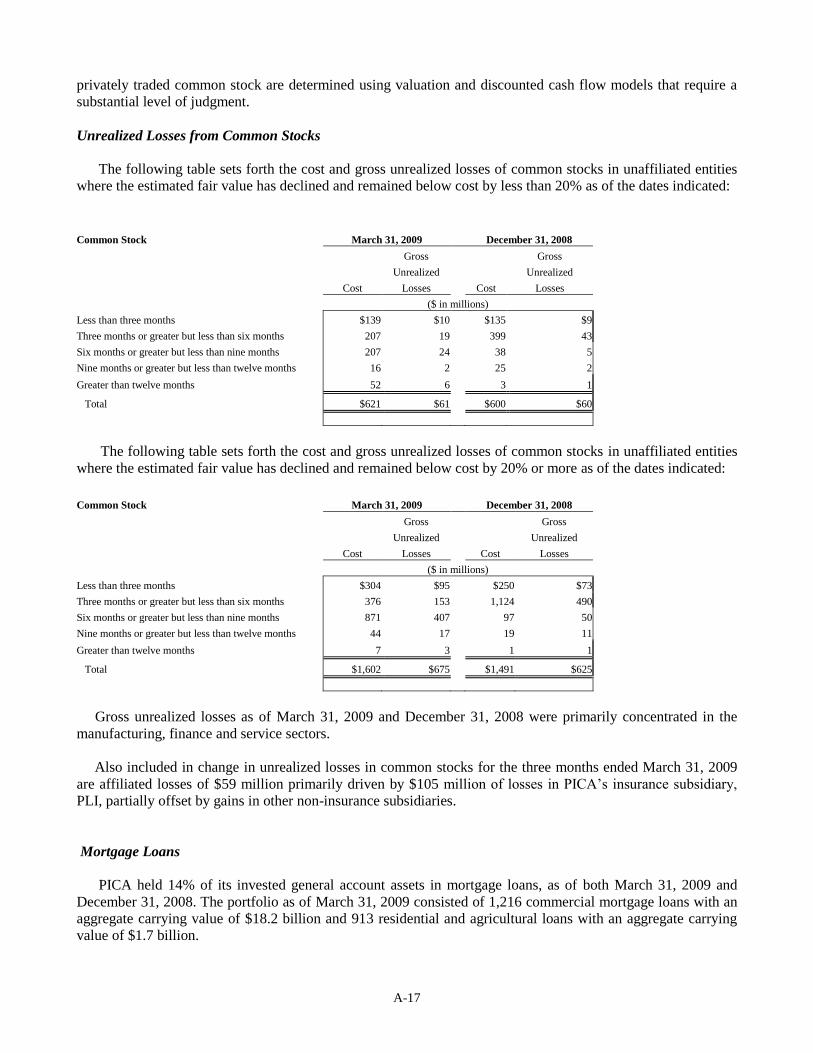

Unrealized Losses from Common Stocks

The following table sets forth the cost and gross unrealized losses of common stocks in unaffiliated entities

where the estimated fair value has declined and remained below cost by less than 20% as of the dates indicated:

Common Stock March 31, 2009 December 31, 2008

Gross Gross

Unrealized Unrealized

Cost Losses Cost Losses

($ in millions)

Less than three months $139 $10 $135 $9

Three months or greater but less than six months 207 19 399 43

Six months or greater but less than nine months 207 24 38 5

Nine months or greater but less than twelve months 16 2 25 2

Greater than twelve months 52 6 3 1

Total $621 $61 $600 $60

The following table sets forth the cost and gross unrealized losses of common stocks in unaffiliated entities

where the estimated fair value has declined and remained below cost by 20% or more as of the dates indicated:

Common Stock March 31, 2009 December 31, 2008

Gross Gross

Unrealized Unrealized

Cost Losses Cost Losses

($ in millions)

Less than three months $304 $95 $250 $73

Three months or greater but less than six months 376 153 1,124 490

Six months or greater but less than nine months 871 407 97 50

Nine months or greater but less than twelve months 44 17 19 11

Greater than twelve months 7 3 1 1

Total $1,602 $675 $1,491 $625

Gross unrealized losses as of March 31, 2009 and December 31, 2008 were primarily concentrated in the

manufacturing, finance and service sectors.

Also included in change in unrealized losses in common stocks for the three months ended March 31, 2009

are affiliated losses of $59 million primarily driven by $105 million of losses in PICA‘s insurance subsidiary,

PLI, partially offset by gains in other non-insurance subsidiaries.

Mortgage Loans

PICA held 14% of its invested general account assets in mortgage loans, as of both March 31, 2009 and

December 31, 2008. The portfolio as of March 31, 2009 consisted of 1,216 commercial mortgage loans with an

aggregate carrying value of $18.2 billion and 913 residential and agricultural loans with an aggregate carrying

value of $1.7 billion.

A-18

The Investment Manager originates commercial mortgages using dedicated investment staff and a network of

independent companies through various regional offices across the country. All commercial mortgage loans are

underwritten consistently with PICA's standards using a proprietary quality rating system that has been

developed using the Investment Manager's experience in commercial real estate and mortgage lending. The loan

portfolio strategy emphasizes diversification by property type and geographic location.

The following table sets forth the breakdown of the mortgage loan portfolio by geographic region as of the

dates indicated.

March 31, 2009 December 31, 2008

Carrying % of Carrying % of

U.S. Regions: Value Total Value Total

($ in millions)

Pacific $6,505 32.7 % $6,661 33.0 %

South Atlantic 4,263 21.4 4,435 22.0

Middle Atlantic 3,296 16.6 3,409 16.9

West South Central 1,373 6.9 1,370 6.8

East North Central 1,367 6.9 1,381 6.9

Mountain 1,064 5.3 995 4.9

New England 790 4.0 793 3.9

West North Central 536 2.7 508 2.5

East South Central 360 1.8 367 1.8

Subtotal – U.S. Regions $19,554 98.3 % $19,919 98.7 %

Other 335 1.7 254 1.3

Total mortgage loans $19,889 100.0 % $20,173 100.0 %

Of the mortgage loan portfolio as of March 31, 2009, the states with the most significant concentrations of

mortgage loans were California and New York, with $5.2 billion and $2.0 billion, respectively.

The stress experienced in the global financial markets and unfavorable credit market conditions that began in

the second half of 2007 and continued and substantially increased throughout 2008 and into 2009 led to a

decrease in the overall liquidity and availability of capital in the commercial mortgage loan market, and in

particular a decrease in activity by securitization lenders. These conditions have led to greater opportunities for

more selective originations by portfolio lenders such as our general account. While we have begun to observe

some weakness in commercial real estate fundamentals, delinquency rates on our commercial mortgage loans

have been relatively stable in recent years. However, continued difficult conditions in the global financial

markets and the overall economic downturn could put additional pressure on these fundamentals through rising

vacancies, falling rents and falling property values. As of March 31, 2009, our general account investments in

commercial mortgage loans attributable to the Financial Services Businesses had an average debt service

coverage ratio of 1.92 times, and an average loan-to-value ratio of 57%.

The following table sets forth the amortized cost of investments in mortgage loans as of March 31, 2009 by

loan to value and debt service coverage ratios.

A-19

March 31, 2009

Debt Service Coverage Ratio (1)

Greater

than 2.0x

1.8x to

2.0x

1.5x to

1.8x

1.2x to

1.5x

1.0x to

1.2x

Less than

1.0x

Total

Mortgage

Loans

% of

Total

Mortgage

Loans

Loan to Value Ratio (in millions)

0% - 50% ................................................... $ 4,290 821 1,142 856 122 125 7,356 37.0%

50% - 60% ................................................. 795 546 1,062 451 218 115 3,187 16.0

60% - 70% ................................................. 635 466 1,318 1,582 213 — 4,214 21.2

70% - 80% ................................................. 140 476 582 1,007 422 109 2,736 13.7

80% - 90% ................................................. 20 21 268 1,003 267 37 1,616 8.1

90% - 100% ............................................... 164 — 29 95 175 6 469 2.4

Greater than 100% ..................................... — 33 — — 191 87 311 1.6

Total mortgage loans .................................. $ 6,044 2,363 4,401 4,994 1,608 479 19,889 100.0%

Percentage of total

mortgages .................................................... 30.4 11.9 22.1 25.1 8.1 2.4

100.0%

_________ (1) The majority of the collateral values used in the calculation of the loan-to-value ratios are based upon the appraised value of the property at the time of

loan origination.

The following table sets forth the breakdown of our mortgage loan portfolio by year of origination as of

March 31, 2009.

March 31, 2009

Year of Origination

Gross

Carrying

Value

% of Total

($ in millions)

2009 $225 1.1 % 2008 3,332 16.8

2007 4,750 23.9

2006 3,202 16.1 2005 1,997 10.0

2004 and prior 6,383 32.1

Total collateralized loans $19,889 100.0 %

The Investment Manager performs ongoing surveillance of the portfolio and places loans on watch list status

based on a predefined set of criteria. Loans are placed on early warning status in cases where the Investment

Manager detects that the physical condition of the property, the financial situation of the borrower or tenant, or

other market factors could lead to a loss of principal or interest. Loans are classified as closely monitored when

there is a collateral deficiency or other credit events that may lead to a potential loss of principal or interest.

Loans not in good standing are those loans where there is a high probability of loss of principal, such as when

the loan is in the process of foreclosure or the borrower is in bankruptcy. Workout and special servicing

professionals manage the loans on the watch list.

The following table shows the respective amounts of PICA's mortgage loan portfolio that are in good

standing, are in good standing with restructured terms, have interest overdue more than three months but are not

in foreclosure, and are in the process of foreclosure, as of the dates indicated.

March 31, December 31,

2009 2008

Carrying Carrying

Value Value

($ in millions)

A-20

Good standing $19,887 $20,168

Good standing with restructured terms 1 2

Interest overdue more than three months, not in foreclosure 1 3

Foreclosure in process — —

Total mortgage loans $19,889 $20,173

Joint Ventures and Limited Partnerships

PICA's investments in joint ventures and limited partnerships were $3.0 billion as of both March 31, 2009

and December 31, 2008. The following table sets forth the composition of PICA's joint ventures and limited

partnerships by type, as of the dates indicated.

March 31, 2009 December 31, 2008

Carrying % of Carrying % of

Value Total Value Total

($ in millions)

Joint venture and Limited partnership interests in real estate $388 13.0 % $411 13.9 %

Joint venture and Limited partnership interests in common stock 1,024 34.2 954 32.2

Joint venture and Limited partnership interests in fixed income 662 22.1 706 23.9

Joint venture and Limited partnership interests - other 919 30.7 886 30.0

Total joint ventures and limited partnerships $2,993 100.0 % $2,957 100.0 %

Government Sponsored Entities

Our exposure to Fannie Mae and Freddie Mac includes investments in short-term and long-term debt

securities issued by these government sponsored entities as well as investments in residential mortgage-backed

securities supported by guarantees from these government sponsored entities. During the third quarter of 2008

Fannie Mae and Freddie Mac were placed into U.S. government conservatorship. The following table sets forth

the amortized cost and fair value of our investments in short-term and long-term debt securities issued by these

government sponsored entities as of the date indicated.

March 31, 2009

Amortized Cost Fair Value

($ in millions)

Short-term debt securities ....................................................................................... $ 735 $ 735

Long-term debt securities ........................................................................................ 556 645

Total investment in debt securities issued by government sponsored

entities ................................................................................................................... $ 1,291 $ 1,380

As of March 31, 2009, long-term bonds attributable to PICA include $5.6 billion of publicly traded pass-

through securities with guarantees from Fannie Mae or Freddie Mac and AAA credit ratings.

Liquidity and Capital Resources

A-21

Liquidity

PICA's principal cash flow sources from insurance, annuities and guaranteed products are premiums and

annuity considerations, investment and fee income, and investment maturities and sales. PICA supplements

these cash inflows with financing activities. PICA‘s cash outflow requirements principally relate to benefits,

claims, dividends paid to policyholders, and payments to contract holders in connection with surrenders,

withdrawals and net policy loan activity. Benefits include the payment of benefits under life insurance, annuity

and guaranteed products. PICA‘s uses of cash also include commissions, general and administrative expenses,

purchases of investments, and debt service and repayments in connection with financing activities, as well as

dividend payments to its parent, PH.

Some of PICA's products, such as guaranteed products offered to institutional customers, provide for

payment of accumulated funds to the contract holder at a specified maturity date unless the contract holder

elects to roll over the funds into another contract with PICA. PICA regularly monitors its liquidity requirements

associated with policyholder and contract holder obligations so that it can manage cash inflows to match

anticipated cash outflow requirements.

In addition, PICA has several subsidiaries that are subject to regulatory limitations on the payment of

dividends to PICA.

The liquidity of PICA's operations is also related to the overall quality of its investments and its asset-

liability management.

PICA is subject to regulatory limitations on the payment of dividends. New Jersey insurance law provides

that, except in the case of extraordinary dividends or distributions, all dividends or distributions declared or paid

by PICA may be declared or paid from unassigned surplus, as determined pursuant to SAP, less unrealized

capital gains and revaluation of assets. PICA must notify the Commissioner of its intent to pay a dividend. If the

dividend, together with other dividends or distributions made within the preceding twelve months, would exceed

a specified statutory limit, PICA must also obtain the prior non-disapproval of the Commissioner.

The current statutory limitation applicable to New Jersey life insurers for ordinary dividends generally is the

greater of 10% of the prior calendar year‘s statutory surplus or the prior calendar year‘s statutory net gain from

operations (excluding realized capital gains).

Moreover, the Commissioner is authorized to disallow the payment of any dividend or distribution that

would otherwise be permitted under the statutory limit set forth above if it determines that a company does not

have a reasonable surplus as to policyholders relative to its outstanding liabilities and adequate to its financial

needs or if it finds such company to be in a hazardous financial condition. In addition to these regulatory

limitations, the terms of the IHC debt also contain restrictions potentially limiting dividends by PICA applicable

in the event the Closed Block business is in financial distress and other circumstances that may be paid by

PICA.

During the fourth quarter of 2008, PFI contributed PSG Holdings, LLC, valued at approximately $2.2

billion, to PICA as a capital contribution. PSG Holdings, LLC owns PICA's joint venture interest in Wachovia

Securities Financial Holdings, LLC, as well as other wholly owned businesses, principally the global

commodities group.

On December 4, 2008, PFI announced its intention to exercise its right under a "lookback" option to put its

joint venture interest in Wachovia Securities Financial Holdings, LLC to Wells Fargo & Co. which completed

its merger with Wachovia Corporation on December 31, 2008. Under the terms of the joint venture agreements,

PICA management expects closing of the put transaction would occur on or about January 1, 2010. The full

value PICA expects to receive related to the ―lookback‖ option is not yet reflected in PICA‘s capital levels as

A-22

the investment is carried at book value. Under the terms of the joint venture agreements, Wells Fargo may elect

to pay the proceeds from exercise of the ―lookback‖ put either in cash, Wells Fargo common stock or a

combination of the foregoing.

PICA estimates the proceeds from the exercise of the ―lookback‖ put to be approximately $5 billion, based

on a January 1, 2010 closing, the terms of the joint venture agreements and PICA‘s assessment of market

conditions and retail brokerage firm valuations at the relevant valuation date of January 1, 2008; however the

amount of such proceeds has not been finally determined and could be more or less. The after-tax gain on sale

would be reflected in the capital and surplus of PICA and, while there can be no assurance, PICA estimates that

the statutory reporting impact from the realization of the value of its investment in the Wachovia Securities joint

venture upon closing of the put transaction in January 2010 would be a contribution of in excess of 100 points to

the RBC ratio of PICA as of the end of 2010.

Notwithstanding the terms of the joint venture agreements governing the ―lookback‖ put, PICA has from

time to time had discussions with Wells Fargo concerning a possible early settlement of the ―lookback‖ put.

The proceeds received upon any early settlement would take into account the time value of money, the benefits

and certainty provided by an early resolution and the form of consideration to be received. Taking into account

these factors, it could be expected that PFI may agree to an amount less than the amount that would be

recognized under a closing of the put transaction on or about January 1, 2010. Absent an early settlement, PFI

intends to exercise the ―lookback‖ put as described above.

In connection with the establishment of the Wachovia Securities joint venture, Wachovia Securities, LLC

issued a subordinated promissory note in the principal amount of $417 million, which is held by PICA. This

note bears interest, payable quarterly, at the three month London inter-bank rate (LIBOR) plus 105 basis points.

Under the terms of the joint venture agreements, this note becomes payable, together with accrued and unpaid

interest, within thirty days of termination of the joint venture.

On December 30, 2008, PICA entered into an agreement with PSG Holdings LLC, in which PSG Holdings,

LLC promises to pay PICA on March 30, 2010 the principal sum of $2.1 billion, together with simple interest

thereon per annum. The note, in the amount of $2.1 billion, related to this agreement is reported in Assets in

―Bonds‖ and is secured by the investment in Wachovia Securities.

The other wholly owned businesses in PSG Holdings, LLC, principally our global commodities group,

continue to maintain sufficiently liquid balance sheets, consisting mostly of cash and cash equivalents,

segregated client assets, and short-term receivables from clients, broker-dealers, and exchanges.

On December 24, 2008 PICA received a capital contribution of $150 million from its ultimate parent, PFI.

PICA has received a request pursuant to the documentation for the disposition of PFI‘s property and

casualty operations completed in 2003 to deposit into a trust cash or securities for the purpose of securing

insurance liabilities that were to have been transferred to PICA following completion of the disposition but that

have not been so transferred. PICA estimates that the amount of cash or securities to be deposited is

approximately $500 million, and PICA is allowed to satisfy a portion of this requirement through the deposit of

promissory notes received from the purchaser at the time of the disposition. PICA management believes that the

deposit of these assets is not a material liquidity event for PICA.

Net cash provided by operations was $466 million and $384 million for the three months ended March 31,

2009 and March 31, 2008, respectively. The fluctuation between years was primarily driven by a decrease in

benefits and claims paid.

Net cash (used in) provided by investing activities was ($334) million and $1,545 million for the three

months ended March 31, 2009 and March 31, 2008, respectively. The fluctuation between years was principally

A-23

driven by a decrease in net cash flows related to investments in bonds. PICA‘s cash flows from investment

activities result from repayments of principal, proceeds from maturities and sales of invested assets and

investment income, net of amounts reinvested. The primary liquidity risks with respect to these cash flows are

the risk of default by debtors or bond insurers, our counterparties‘ willingness to extend repurchase and/or

securities lending arrangements and market volatility. We closely manage these risks through our credit risk

management process and regular monitoring of our liquidity position.

Net cash (used in) financing activities was ($2,455) million and ($1,636) million for the three months ended

March 31, 2009 and March 31, 2008, respectively. The fluctuation was mainly driven by payments made on

borrowed money.

PICA's management believes that its sources of liquidity are adequate to meet its current cash requirements

and reasonably foreseeable contingencies, particularly considering the liquidity of its investment portfolio.

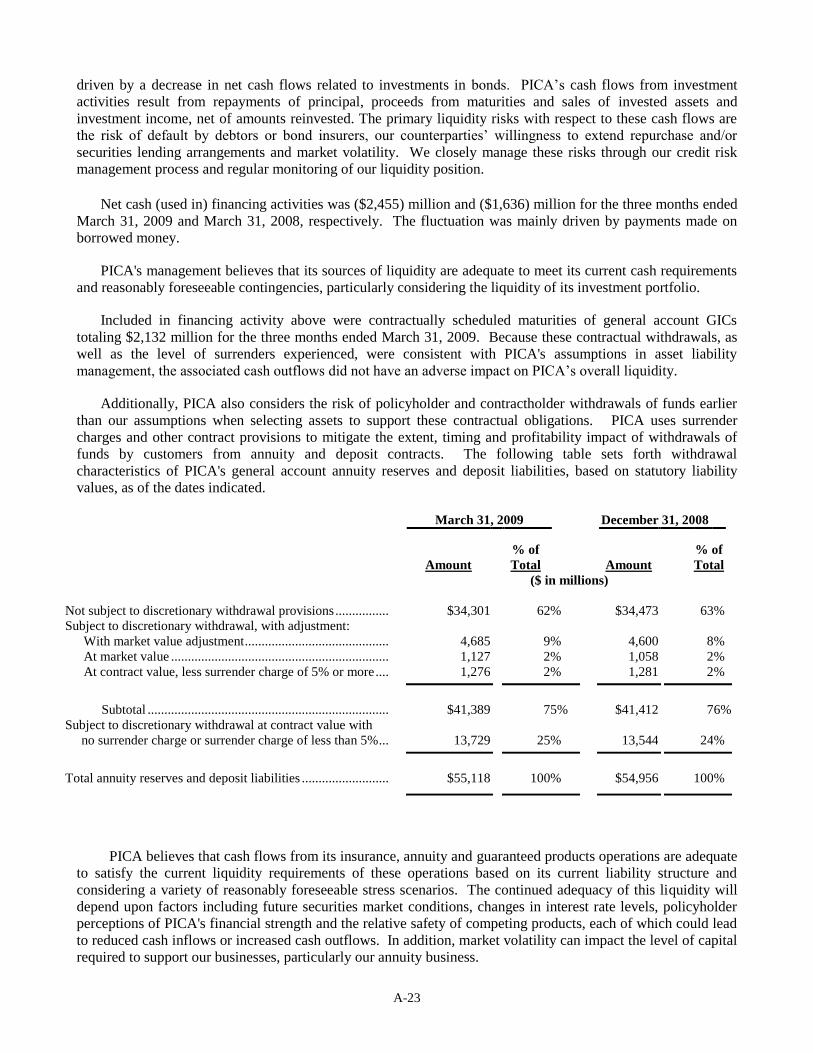

Included in financing activity above were contractually scheduled maturities of general account GICs

totaling $2,132 million for the three months ended March 31, 2009. Because these contractual withdrawals, as