management information and accounting system and ... · costing, target costing, kaizen costing,...

TRANSCRIPT

AMERICAN JOURNAL OF SOCIAL AND MANAGEMENT SCIENCES ISSN Print: 2156-1540, ISSN Online: 2151-1559, doi:10.5251/ajsms.2015.6.1.17

© 2015, ScienceHuβ, http://www.scihub.org/AJSMS

1

Management Information and Accounting System and organizational Performance in Nigeria

Omiunu, Ojinga Gideon

Africa Regional Centre for Information Science, University of Ibadan, Ibadan, Nigeria.

Unicorn Academics and Organisation Developmental Research Centre, Nigeria P.O.Box, 20671, UI Post Office, Ibadan, Oyo State, Nigeria.

E-mail: [email protected]; [email protected]

Tel: +2348051779079, 8029219415

ABSTRACT

The study investigated management information and accounting system and organizational Performance in Nigeria. The study adopted the empirical survey research design. A convenient sampling was used to select South West from the geopolitical zones and Oyo State from the states in the South West zone, and a total of one hundred (100) respondents were selected for the study. Information and data were obtained through the help of the questionnaire. The questionnaire was validated and tested through the Cronbach Alpha, and provided a reliability analysis of 0.75. Data obtained were analysed using the SPSS and statistical tools used were frequency, percentage, Spearman’s Correlation and binary logistic regression analysis. The findings of the study revealed that organisation in Nigeria have low and poor culture towards the deployment and use of Management accounting and information systems. Some demographic characteristics were observed to be significant in the use of MAS, while none was significant in the use of MIS. Furthermore, there was no significant relationship between management accounting systems and management information systems (p>0.05). There was no significant relationship between management accounting systems and organizational performance (p>0.05). There was no significant relationship between management information systems and organizational performance (p>0.05). The use of Management Information systems in organization does have significant influence on the effectiveness of management accounting system used (p<0.05). The study recommended that organizations in Nigeria should deploy and use management accounting and information system to enhancing their business performance and also making it globally competitive especially in this competitive environment.

Key Words: Management Accounting System, Information System, Organisation Performance, Nigeria

INTRODUCTION

Organisation performance measurement has attracted attention and has generated lots of arguments as there have been no universally recognised measures of this

concept. Performance vary across a wide range of organisation and organisation activities. According to Croteau & Bergeron (2001), both the subjective and objective measurements have been deployed to evaluating organisations’ performances. The

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

2

subjective measurement is based upon the perception of the organisations’ owners while the objective data measurement is based on the financial data of the organisations and the financial tools been deployed and used in the organization include the return on Investment, return on expenditures, return on capital expenditure, among others. There is a shift in the trend of such measurement from the financial tools to the non-financial tools especially among organisations that do not deal directly with money. To this end, focus on organizational performance has shifted from the financial perspective to a non-financial perspective (Tatichi, Cagnazzo & Botarelli, 2008).

Whether financial or non financial measurement, Etemadi, Dilami, Bazaz and Parameswaranit (2009) have stated that, organisational performance is linked to management accounting system and practices. Management accounting systems are systems tailored to increase organization’s effectiveness by providing information that can assist managers in fulfilling the goals of the organizations (Horngren, Foster & Datar, 1994). It is an important management technique that ensures resource use efficiency among organization (International Federation of Accountants, 1998). The main objective of the Management accounting systems has been to provide information for costing products and for promoting efficiency in the use of labour and materials (Johnson & Kaplan, 1987). Examples of such Management Accounting System (MAS) are standard costing and flexible budgeting for cost control, cost allocation and product cost measurements; incremental analysis for decision-making; measurement of profit, contribution and return on investments for performance monitoring; and the full integration of internal cost accumulation

systems with the external financial reporting systems (Ajibolade, 2013).

Furthermore, there is also a link between management accounting system and management information system (Etemadi et al., 2009). This link can be conceptualized from the main fact that information about financial aspects of organization are provided for managerial activities and fulfilling organizational goals and objectives. Management Information System is an integrated user-machine system meant for providing information, to support the operations, management, analysis & decision-making functions in an organization. Management accounting information is a part of this information that would be provided to aid organization success. Kucera, Skorecova and Szovics (2003) have stated that managerial accounting provides information for processing and utilization to organizations’ management information system. Thus, Management accounting systems and practices is an integral part of the management information systems for organizational development. This kind of information provided from the accounting aspect of the organization is what Grande, Estébanez, and Colomina (2011) called Accounting information system.

Accounting Information Systems (AIS) are a tool (such as Sales Management Systems, Inventory Control Systems, budgeting systems, Management Reporting Systems (MRS), and Personnel (HRM) systems) which, when incorporated into Information and Technology systems (IT), were designed to help in the management and control of organisations’ economic-financial area (Grande et al., 2011). In addition, the stunning advance in technology has opened

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

3

up the possibility of generating and using accounting information from a strategic viewpoint. This kind of information is needed to deal with a higher degree of uncertainty in the competitive market ( El Louadi, 1998). Thus, there is a dare need for organizations to improve their systems and data processing capacity to match their information needs with regards to the financial or accounting information need so as to enhance their performance. Howbeit, Grande et al., (2011) clearly noted that organizations are faced with various challenges in the use of management accounting information system, which makes its use difficult.

In addition, organizational culture in the use of management accounting and information systems is low and poor, and this has affected management control systems and management practices and have also affected their performance as they have no record of how resource are used (input and output) in the organization (Etemadi et al., 2009). In addition, Aziz et al (2014) reveal that most managers tend to have bad attitudes towards record keeping and resource management, thus bad organizational culture in the management information and accounting system. Organisational culture especially towards management accounting and information system may affect whether it is been practiced or not and thus affecting their performance (Etemadi et al., 2009). To this end, this study seeks to investigate management information and accounting system and organizational Performance in Nigeria. The following research questions drive the study:

i. Do organization in Nigeria have positive and good culture towards management

accounting and information systems practices?

ii. What are the types of management accounting systems used among organization in Nigeria?

iii. What are the types of management information systems used among organization in Nigeria?

iv. What are the organizational and owners characteristics that may influence the use and non use of management accounting systems?

v. What are the organizational and owners characteristics that may influence the use and non use of management information systems to enhance Management accounting systems and practices?

Research Hypotheses: The study would also test the following hypotheses at 0.05 level of significance:

HO1: There is no significant relationship between management accounting systems and management information systems

HO2: There is no significant relationship between management accounting systems and organizational performance

HO3: There is no significant relationship between management information systems and organizational performance

HO4: The Use of Management Information systems in organization does not have significant influence on the

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

4

effectiveness of management accounting system use.

Previous Studies

Hilton and Platt (2011) stated that management accounting is the process of identifying, measuring, analyzing, interpreting and communicating information in pursuit of organization’s goals. Management accounting is integral part of management process. It provides internal (financial and non-financial) information of the past, present, and future of an organization; and also provides external monetary and non-monetary measurement of the environment of the organization (Etemadi et al., 2009). Timeliness of management accounting system enables managers to respond to events quickly and provide them rapid feedback for effective decision-making. Example of management accounting practices are standard costing and flexible budgeting for cost control, cost allocation and product cost measurements; incremental analysis for decision-making; measurement of profit, contribution and return on investments for performance monitoring; financial management, cost management, effective budgeting and costing, and the full integration of internal cost accumulation systems with the external financial reporting systems (Ajibolade, 2013). Also, Sunarni (2013) added that there are new management accounting techniques, these include activity based costing, target costing, kaizen costing, balance scorecard and others. Abdel-Kader and Luther (2006) stated that the most notable innovative management accounting techniques are activity based techniques, strategic management accounting and the balance scorecard.

Kucera et al (2003) had stated that management accounting provides information for processing and utilization to organisation’s management information system. This implies that management information system is an important part of organization management accounting practices effectiveness. Examples of Management Information Systems are Sales Management Systems, Inventory Control Systems, budgeting systems, Management Reporting Systems (MRS), Personnel (HRM) systems), among others. The importance of management information system to management accounting systems is seen in the assertion of Etemadi et al. (2009) that management accounting system and management information system are linked together in any organization.

Howbeit, Lund (2003) states that organization’s culture affects management and managerial activities such as management information systems and management accounting systems practices, and thus can affect employees and the organizational performance. This made organizational culture to be an important factor in the relationship effect or link between management accounting systems and management information systems in organizations. This gave a base for this study. To this end, the study investigated management information and accounting system and organizational performance in Nigeria

Theoretical Underpinning: Three models from Laudon, Laudon and Dash (2006) were deployed, adapted and used to support this study. These are the model showing the functions of an information system, the interdependence between organizations and information systems, and DaimlerChrysler’s Agile Supply Chain.

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

5

Fig 1: Functions of an information system.

Adapted from Laudon, Laudon and Dash (2006) An information system such as the management information system contains information about an organization and its surrounding environment. Three basic activities—input, processing, and output—produce the information organizations need. Feedback is output returned to appropriate

people or activities in the organization to evaluate and refine the input. Environmental factors such as customers, suppliers, competitors, stockholders, and regulatory agencies interact with the organization and its information systems. Also, of importance to this study is the interdependence between organizations and information systems.

Fig 2: The interdependence between organizations and information systems

Adapted from Laudon, Laudon and Dash (2006) In contemporary systems, there is a growing interdependence between a firm’s information systems such as management information system and its business capabilities such as organizational performance. Changes in strategy, rules, and business processes increasingly require changes in hardware, software, databases,

and telecommunications. Often, what the organization would like to do depends on what its systems will permit it to do. The DaimlerChrysler’s Agile Supply Chain was also of importance to this study.

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

6

Fig 3: DaimlerChrysler’s Agile Supply Chain Adapted from Laudon, Laudon and Dash (2006) DaimlerChrysler studied every step in the organisation’s production and sales process, starting with the first stage of design and ending with its service and repair; it then builts a series of information systems that automated and streamlined all of its transactions with the suppliers. An Integrated Volume Planning system gathers sales data and sends them back to production planning systems and from there to suppliers so that they can adjust deliveries of parts and production to make exactly the right amount of the products that are actually selling in dealer showrooms. In

addition, from figure 3, it is observed that organization faced some challenges in deploying Management information systems. Conceptual Framework for the Study: Management accounting systems was one of the organizational subsystems that facilitated control of resources and enhance the performance of organizations (Chia, 1995). In addition, its operation could be more efficient with the help of management information system and thus increasing its effect on organizational performance. Figure 4 provides the conceptual framework for the study.

Fig 4: Conceptual Model for MIS-MAS Organisational Performance Enhancement

Source: The Author

Management

Accounting

Management

Information

Socio-

Demographic

Management

Accounting

Organisational

Performance

Organisational

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

7

METHODOLOGY

The study adopted the empirical survey research design. Although the study was an organizational study however, owners’ socio-demographical characteristics were also put into consideration. A convenient sampling was used to select the South West from the geopolitical zones and Oyo State from the states in the South West zone, and a total of one hundred (100) respondents were selected for the study. Information and data were obtained through the help of the questionnaire. The questionnaire has seven major sections namely demographic characteristics, organizational culture in the use of MAS, organizational culture in the use MIS, use of MAS, use of MIS, MAS effectiveness, and organisational performance. In addition, the questionnaire was validated and tested and provided a

reliability analysis, using the Cronbach Alpha, of 0.75. In addition, the various constructs of the study also gave reliability analysis of organizational culture in the use of MAS (0.83), organizational culture in the use MIS (0.79), use of MAS (0.72), use of MIS (0.71), and MAS effectiveness (0.81). These revealed that they were reliable for this study and to be used by other studies. Data obtained were analysed using the SPSS and statistical tools such as frequency, percentage, Spearman’s Correlation and binary logistic regression analysis were also used for analysis.

RESULTS

Research Question One: Do organization in Nigeria have positive and good culture towards management accounting and information systems practices?

Table 4.1: Distribution of organizational culture in management accounting and information systems use

Type of Organisations Total Accounting systems practices are integral culture in our organization Disagreed Agreed Total

Medicine Construction Telecomm Education Agriculture Others 4(50.0%) 4(50.0%) 8(100.0%)

15(57.7%) 11(42.3%) 26(100.0%)

2(25.0%) 6(75.0%) 8(100.0%)

0(.0%) 6(100.0%) 6(100.0%)

6(66.7%) 3(33.3%) 9(100.0%)

32(97.0%) 1(3.0%) 33(100.0%)

59(65.6%) 31(34.4%) 90(100.0%)

Management accounting practices is a continuous activity in the organisation Disagreed Agreed Total

4(50.0%) 4(50.0%) 8(100.0%)

15(57.7%) 11(42.3%) 26(100.0%)

1(14.3%) 6(85.7%) 7(100.0%)

4(66.7%) 2(33.3%) 6(100.0%)

6(66.7%) 3(33.3%) 9(100.0%)

28(87.5%) 4(12.5%) 32(100.0%)

58(65.9%) 30(34.1%) 88(100.0%)

Lack of accountability and record keeping of resource use exists Disagreed Agreed Total

6(75.0%) 2(25.0%) 8(100.0%)

11(42.3%) 15(57.7%) 26(100.0%)

5(71.4%) 2(28.6%) 7(100.0%)

6(100.0%) 0(.0%) 6(100.0%)

5(55.6%) 4(44.4%) 9(100.0%)

18(58.1%) 13(41.9%) 31(100.0%)

51(58.6%) 36(41.4%) 87(100.0%)

Management accounting practices and information system are meant for top management position Disagreed Agreed Total

6(75.0%) 2(25.0%) 8(100.0%)

11(42.3%) 15(57.7%) 26(100.0%)

6(75.0%) 2(25.0%) 8(100.0%)

6(100.0%) 0(.0%) 6(100.0%)

3(33.3%) 6(66.7%) 9(100.0%)

7(21.2%) 26(78.8%) 33(100.0%)

39(43.3%) 51(56.7%) 90(100.0%)

We don’t really need information system to manage our activities in the organisation Disagreed Agreed Total

7(100.0%) 0(.0%) 7(100.0%)

9(36.0%) 16(64.0%) 25(100.0%)

8(100.0%) 0(.0%) 8(100.0%)

5(100.0%) 0(.0%) 5(100.0%)

3(33.3%) 6(66.7%) 9(100.0%)

10(31.3%) 22(68.8%) 32(100.0%)

42(48.8%) 44(51.2%) 86(100.0%)

Things can be done manually so there is no need for any information system Disagreed Agreed Total

8(100.0%) 0(.0%) 8(100.0%)

22(84.6%) 4(15.4%) 26(100.0%)

7(100.0%) 0(.0%) 7(100.0%)

1(20.0%) 4(80.0%) 5(100.0%)

9(100.0%) 0(.0%) 9(100.0%)

20(62.5%) 12(37.5%) 32(100.0%)

67(77.0%) 20(23.0%) 87(100.0%)

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

8

The distribution of organizational culture in the management Accounting and information system use by organization is presented in table 4.1. The result revealed that, 41.4% stated that, lack of accountability and record keeping of resource use exists in their organization with construction having the highest percentage (57.7%). In addition, 34.4% stated that accounting systems practices are integral culture in their organization; the educational and the telecommunication sector has the highest percentage of 100% and 75% respectively. Also, 34.1% stated that they have made management accounting practices a continuous activity in their organization, with telecommunication sector having the highest percentage (85.7%).

Also, 56.7% stated that Management accounting practices and information system are meant for top management position with organisations belonging to the other

category having the highest percentage of 78.8. In addition, 51.2% stated that management accounting practices is not really necessary in their organization with organisations belonging to the other category having the highest percentage of 68.8. Furthermore, 23% stated that things can be done manually so there is no need for any information system with the educational sector having the highest percentage (80%). This implied that, to an extent, organisations in Oyo State, Nigeria have a fair culture of management accounting and information systems practices, however, these practices is low and would not allow them to tap into the benefit of MIS and MAS.

Research Question Two: What are the types of management accounting systems used among organization in Nigeria?

Table 4.2: Distribution of Types of Management Accounting Practices among Organisation

What are type of Management Accounting Practices used

Type of Organisation Total Medicine Construction Telecomm Education Agriculture Others

Financial management Disagreed Agreed Total

6(100.0%) 0(.0%) 6(100.0%)

13(50.0%) 13(50.0%) 26(100.0%)

6(75.0%) 2(25.0%) 8(100.0%)

6(100.0%) 0(.0%) 6(100.0%)

3(33.3%) 6(66.7%) 9(100.0%)

25(75.8%) 8(24.2%) 33(100.0%)

59(67.0%) 29(33.0%) 88(100.0%)

Cost management Disagreed Agreed Total

6(75.0%) 2(25.0%) 8(100.0%)

18(69.2%) 8(30.8%) 26(100.0%)

8(100.0%) 0(.0%) 8(100.0%)

6(100.0%) 0(.0%) 6(100.0%)

9(100.0%) 0(.0%) 9(100.0%)

23(69.7%) 10(30.3%) 33(100.0%)

70(77.8%) 20(22.2%) 90(100.0%)

Effective budgeting and costing Disagreed Agreed Total

6(75.0%) 2(25.0%) 8(100.0%)

22(84.6%) 4(15.4%) 26(100.0%)

6(75.0%) 2(25.0%) 8(100.0%)

6(100.0%) 0(.0%) 6(100.0%)

9(100.0%) 0(.0%) 9(100.0%)

28(84.8%) 5(15.2%) 33(100.0%)

77(85.6%) 13(14.4%) 90(100.0%)

Cost allocation and product cost measurements Disagreed Agreed Total

5(71.4%) 2(28.6%) 7(100.0%)

18(69.2%) 8(30.8%) 26(100.0%)

8(100.0%) 0(.0%) 8(100.0%)

6(100.0%) 0(.0%) 6(100.0%)

5(55.6%) 4(44.4%) 9(100.0%)

19(57.6%) 14(42.4%) 33(100.0%)

61(68.5%) 28(31.5%) 89(100.0%)

Return on investments Disagreed Agreed Total

6(75.0%) 2(25.0%) 8(100.0%)

24(92.3%) 2(7.7%) 26(100.0%)

8(100.0%) 0(.0%) 8(100.0%)

6(100.0%) 0(.0%) 6(100.0%)

5(55.6%) 4(44.4%) 9(100.0%)

20(60.6%) 13(39.4%) 33(100.0%)

69(76.7%) 21(23.3%) 90(100.0%)

Which of the type of MAS do organization use? New MAS Traditional MAS Total

0 (.0%) 8 (100.0%) 8 (100.0%)

0 (.0%) 26 (100.0%) 26 (100.0%)

5 (62.5%) 3 (37.5%) 8 (100.0%)

0 (.0%) 6 (100.0%) 6 (100.0%)

0 (.0%) 9 (100.0%) 9 (100.0%)

15 (46.9%) 17 (53.1%) 32(100.0%)

20 (22.5%) 69 (77.5%) 89 (100.0%)

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

9

The distribution of respondents by the types of management accounting system deployed by organisations is presented in table 4.4. The result revealed that financial management was most deployed and used by organisations (33%) with the Agricultural sector (66.7%) having the highest percentage of respondents who used it in their organization. Cost allocation and product cost measurements are also used by organisations (31.5%) with the Agricultural sector (44.4%) having the highest percentage of respondents who used it in their organization. The result also showed that 23.3% perform return on investments for performance monitoring with the agricultural sector (44.4%) having the highest percentage of respondents who used it in their organization.

In addition, 22% of the organisations stated that they use cost management in their organization as a management accounting practice with the construction sector having

the highest percentage of 30.8. Furthermore, 14.4% only use effective budgeting and costing as a management accounting practice in their organization. In addition, 77.5% used the manual means of management accounting system and practice while only 22.5% used the new and modernized MAS such as the activity based costing, target costing, kaizen costing, balance scorecard, among others. This implied that, although organisations owners use the financial management, cost allocation and product costing, return to investment, cost management, and effective budgeting and costing as the major management accounting practice, the result of the study revealed that financial management was most used.

Research Question Three: What are the types of management information systems used among organization in Nigeria?

Table 4.3: Types of Management Information System Used

Type of Organisations Total Medicine Construction Telecomm Education Agriculture Others

Inventory Control Systems Disagreed Agreed Total

0(.0%) 8(100.0%) 8(100.0%)

4(15.4%) 22(84.6%) 26(100.0%)

0(.0%) 8(100.0%) 8(100.0%)

0(.0%) 6(100.0%) 6(100.0%)

0(.0%) 9(100.0%) 9(100.0%)

8(24.2%) 25(75.8%) 33(100.0%)

12(13.3%) 78(86.7%) 90(100.0%)

budgeting systems Disagreed Agreed Total

0(.0%) 7(100.0%) 7(100.0%)

4(15.4%) 22(84.6%) 26(100.0%)

0(.0%) 8(100.0%) 8(100.0%)

0(.0%) 6(100.0%) 6(100.0%)

0(.0%) 8(100.0%) 8(100.0%)

8(24.2%) 25(75.8%) 33(100.0%)

12(13.6%) 76(86.4%) 88(100.0%)

Management Reporting Systems Disagreed Agreed Total

0(.0%) 7(100.0%) 7(100.0%)

2(7.7%) 24(92.3%) 26(100.0%)

0(.0%) 7(100.0%) 7(100.0%)

0(.0%) 6(100.0%) 6(100.0%)

0(.0%) 7(100.0%) 7(100.0%)

5(15.2%) 28(84.8%) 33(100.0%)

7(8.1%) 79(91.9%) 86(100.0%)

Personnel (HRM) systems Disagreed Agreed Total

0(.0%) 7(100.0%) 7(100.0%)

4(15.4%) 22(84.6%) 26(100.0%)

0(.0%) 7(100.0%) 7(100.0%)

0(.0%) 6(100.0%) 6(100.0%)

0(.0%) 9(100.0%) 9(100.0%)

7(21.2%) 26(78.8%) 33(100.0%)

11(12.5%) 77(87.5%) 88(100.0%)

The distribution of the types of management information system practices among organisations is presented in table 4.3. The

result revealed that, 91.9% stated that the Management Reporting Systems was most used in their organisation with organisations

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

10

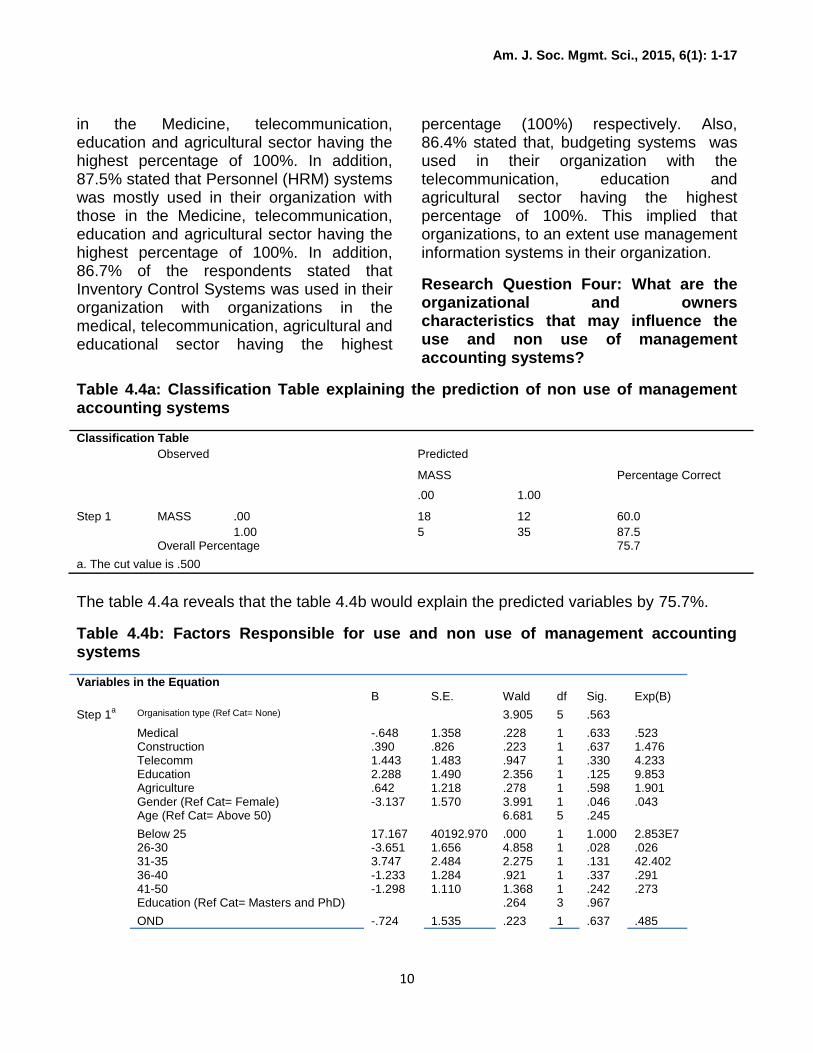

in the Medicine, telecommunication, education and agricultural sector having the highest percentage of 100%. In addition, 87.5% stated that Personnel (HRM) systems was mostly used in their organization with those in the Medicine, telecommunication, education and agricultural sector having the highest percentage of 100%. In addition, 86.7% of the respondents stated that Inventory Control Systems was used in their organization with organizations in the medical, telecommunication, agricultural and educational sector having the highest

percentage (100%) respectively. Also, 86.4% stated that, budgeting systems was used in their organization with the telecommunication, education and agricultural sector having the highest percentage of 100%. This implied that organizations, to an extent use management information systems in their organization.

Research Question Four: What are the organizational and owners characteristics that may influence the use and non use of management accounting systems?

Table 4.4a: Classification Table explaining the prediction of non use of management accounting systems

Classification Table

Observed Predicted

MASS Percentage Correct

.00 1.00

Step 1 MASS .00 18 12 60.0

1.00 5 35 87.5 Overall Percentage 75.7

a. The cut value is .500

The table 4.4a reveals that the table 4.4b would explain the predicted variables by 75.7%.

Table 4.4b: Factors Responsible for use and non use of management accounting systems

Variables in the Equation

B S.E. Wald df Sig. Exp(B)

Step 1a Organisation type (Ref Cat= None) 3.905 5 .563

Medical -.648 1.358 .228 1 .633 .523 Construction .390 .826 .223 1 .637 1.476 Telecomm 1.443 1.483 .947 1 .330 4.233 Education 2.288 1.490 2.356 1 .125 9.853 Agriculture .642 1.218 .278 1 .598 1.901 Gender (Ref Cat= Female) -3.137 1.570 3.991 1 .046 .043 Age (Ref Cat= Above 50) 6.681 5 .245 Below 25 17.167 40192.970 .000 1 1.000 2.853E7 26-30 -3.651 1.656 4.858 1 .028 .026 31-35 3.747 2.484 2.275 1 .131 42.402 36-40 -1.233 1.284 .921 1 .337 .291 41-50 -1.298 1.110 1.368 1 .242 .273 Education (Ref Cat= Masters and PhD) .264 3 .967 OND -.724 1.535 .223 1 .637 .485

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

11

HND -.068 .979 .005 1 .945 .934 First Degree -.281 1.151 .060 1 .807 .755 Years of business operation(Ref Cat= Above 10 Years)

.159 2 .924

Below 5 tears -22.061 28132.706 .000 1 .999 .000 6-10 years -.377 .947 .159 1 .690 .686 Religion (Ref Cat= Islam and Others) .904 .854 1.121 1 .290 2.469 Number of Employees .871 .426 4.174 1 .041 2.390 Constant -1.736 1.937 .803 1 .370 .176

The result in table 4.4b reveals that gender, age (26-30 Years) and number of employees are significant (p<0.05). Gender (Male) explains the 4% of the odds of not deploying MAS in an organization, age (26-30 Years) also explains 2% of the odds of not deploying MAS, howbeit, number of employees explains 39% of the odds of deploying MAS in organization. Therefore, the higher the number of employees, the

greater the tendency for the organization to use MAS, because employee number is most often proportional to size of organization. Research Question Five: What are the organizational and owners characteristics that may influence the use and non use of management information systems?

Table 4.5a: Classification Table explaining the prediction of non use of management information systems

Classification Table

Observed Predicted

MISS Percentage Correct

.00 1.00

Step 1 MISS .00 13 13 50.0

1.00 6 41 87.2 Overall Percentage 74.0

a. The cut value is .500

The table 4.5a reveals that the table 4.5b would explain the predicted variables by 74%. Table 4.5b: Factors Responsible for use and non-use of management information systems

Variables in the Equation

B S.E. Wald df Sig. Exp(B)

Step 1a Organisation type (Ref Cat= None) 1.014 5 .961

Medical -.351 1.026 .117 1 .732 .704 Construction .005 .734 .000 1 .994 1.005 Telecomm .202 1.108 .033 1 .855 1.224 Education .641 1.079 .352 1 .553 1.898 Agriculture .656 1.081 .369 1 .544 1.928 Gender (Ref Cat= Female) 1.071 .928 1.333 1 .248 2.919 Age (Ref Cat= Above 50) 5.541 5 .354 Below 25 20.902 40192.

970 .000 1 1.00

0 1.195E9

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

12

26-30 2.251 1.527 2.173 1 .140 9.496 31-35 -.076 1.453 .003 1 .958 .927 36-40 -.563 1.023 .303 1 .582 .569 41-50 1.539 .927 2.757 1 .097 4.659 Education (Ref Cat= Masters and PhD) 2.807 3 .422 OND 1.411 1.274 1.226 1 .268 4.099 HND -.128 1.023 .016 1 .900 .880 First Degree 1.314 .944 1.937 1 .164 3.720 Years of business operation(Ref Cat= Above 10 Years)

1.561 2 .458

Below 5 tears 19.533 28302.059

.000 1 .999 3.042E8

6-10 years -.953 .762 1.561 1 .211 .386 Religion (Ref Cat= Islam and Others) -.505 .658 .589 1 .443 .604 Number of Employees -.181 .287 .396 1 .529 .835 Constant .384 1.426 .073 1 .788 1.468

The table 5.5b shows that there are no relationships between variables in the study (p>0.05). This implies that socio-demographic characteristics do not really have influence on the use and non use of MIS in organizations in Nigeria.

Test of Hypotheses

HO1: There is no significant relationship between management accounting systems and management information systems

Table 4.6: Correlation Analysis for Hypothesis One

N Mean Std. Deviation

r-value p-value

Management Accounting System 93 .5161 .50245 -.010 .927 Management Information System 96 .6146 .48925

Valid N (listwise) 92

The test of hypothesis one reveal that there is no significant relationship between management accounting systems and management information systems (p>0.05)

HO2: There is no significant relationship between management accounting systems and organizational performance

Table 4.7: Correlation Analysis for Hypothesis Two

N Mean Std. Deviation r-value p-value

Management Accounting System

93 .5161 .50245 .163 .156

Organisation Performance

83 3.2228E6 3.48307E6

Valid N (listwise) 77

The test for hypothesis two shows that there is no significant relationship between management accounting systems and organizational performance (p>0.05).

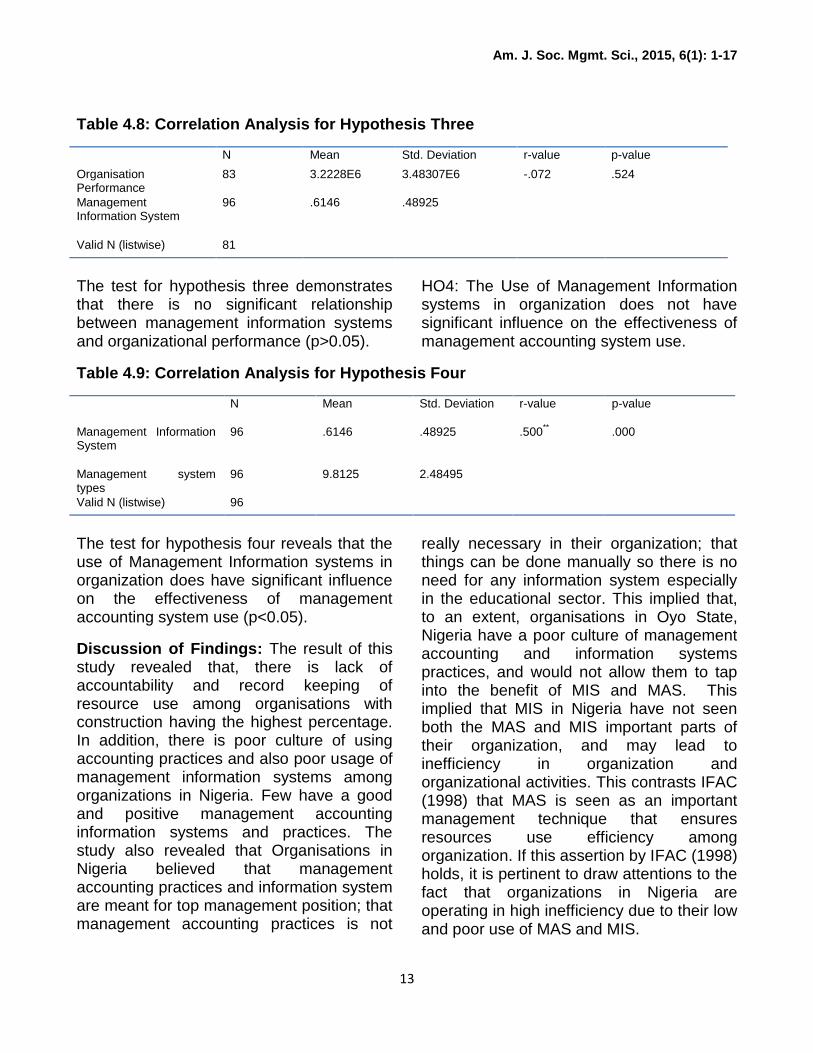

HO3: There is no significant relationship between management information systems and organizational performance

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

13

Table 4.8: Correlation Analysis for Hypothesis Three

N Mean Std. Deviation r-value p-value

Organisation Performance

83 3.2228E6 3.48307E6 -.072 .524

Management Information System

96 .6146 .48925

Valid N (listwise) 81

The test for hypothesis three demonstrates that there is no significant relationship between management information systems and organizational performance (p>0.05).

HO4: The Use of Management Information systems in organization does not have significant influence on the effectiveness of management accounting system use.

Table 4.9: Correlation Analysis for Hypothesis Four

N Mean Std. Deviation r-value p-value

Management Information System

96 .6146 .48925 .500** .000

Management system types

96 9.8125 2.48495

Valid N (listwise) 96

The test for hypothesis four reveals that the use of Management Information systems in organization does have significant influence on the effectiveness of management accounting system use (p<0.05).

Discussion of Findings: The result of this study revealed that, there is lack of accountability and record keeping of resource use among organisations with construction having the highest percentage. In addition, there is poor culture of using accounting practices and also poor usage of management information systems among organizations in Nigeria. Few have a good and positive management accounting information systems and practices. The study also revealed that Organisations in Nigeria believed that management accounting practices and information system are meant for top management position; that management accounting practices is not

really necessary in their organization; that things can be done manually so there is no need for any information system especially in the educational sector. This implied that, to an extent, organisations in Oyo State, Nigeria have a poor culture of management accounting and information systems practices, and would not allow them to tap into the benefit of MIS and MAS. This implied that MIS in Nigeria have not seen both the MAS and MIS important parts of their organization, and may lead to inefficiency in organization and organizational activities. This contrasts IFAC (1998) that MAS is seen as an important management technique that ensures resources use efficiency among organization. If this assertion by IFAC (1998) holds, it is pertinent to draw attentions to the fact that organizations in Nigeria are operating in high inefficiency due to their low and poor use of MAS and MIS.

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

14

The result of this study reinforced the work of Etemadi et al. (2009) that organizational culture in the use of management accounting and information systems are low and poor, and these have affected management control systems and management practices and have also affected their performance as they have no record of how resource are used (input and output) in the organization. The result of this study also supported Aziz et al (2014) that most managers tend to have bad attitudes towards record keeping and resource management, thus bad organizational culture in the management information and accounting system.

The result of this study also revealed that financial management was most deployed and used among organization in Nigeria especially in the Agricultural sector. Other accounting system practices used among organization in Nigeria are cost allocation and product cost measurements, return on investments for performance monitoring, cost management and effective budgeting and costing. The manual means of management accounting system and practice are deployed the most among organizations in Nigeria than the new and modernized MAS such as the activity based costing, target costing, kaizen costing, balance scorecard, among others

Furthermore, the result of the study disclosed that organizations, to an extent use management information systems in their organization, however, management Reporting Systems was the most used in organisation in Nigeria especially in organization in the Medicine, telecommunication, education and agricultural sector. Other management information systems used by organizations include: Personnel (HRM) systems

especially in the Medicine, telecommunication, education and agricultural sector; Inventory Control Systems especially in the medical, telecommunication, agricultural and educational sector; budgeting systems was used in their organization especially among the telecommunication, education and agricultural sector. This supported Etemadi et al. (2009) that organisational culture especially towards management accounting and information system may affect whether they practice it or not and thus affecting their performance.

Besides, the result of this study divulged that gender and age (26-30 Years) exert significant influence on the possibility of not deploying Management Accounting System in organization in Nigeria while number of employees explains the possibility of orgnisation in Nigeria to deploying Management Accounting System. It could concluded from the result of this study that the higher the number of employees, the greater the tendency for the organization to use MAS, because employee number is most often proportional to size of organization.

Furthermore, socio-demographic characteris tics do not really have influence on the use and non use of MIS in organizations in Nigeria. There was no significant relationship between management accounting systems and management information systems. There was no significant relationship between management accounting systems and organizational performance. This contrasts Laudon et al (2006) and Etemadi et al. (2009) that organisational performance is linked to management accounting system and practices. This revealed that the low

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

15

and poor deployment and use of better MAS strategies have not set into impetus the organizational performance. This implies that organizations in Nigeria are still lacking behind in the global world in the use of and the trends of management Accounting System.

There was no significant relationship between management information systems and organizational performance. Finally the result of this study revealed that the use of Management Information systems in organization does have significant influence on the effectiveness of management accounting system use. This could be because of the low and poor organisational culture towards management information systems and management accounting systems. This bolstered Lund (2003) that an organization’s culture affect management and management activities such as management information systems and management accounting systems practices, and thus can affect employees and the organizational performance. This augments Etemadi et al. (2009) that there is a link between management accounting system and management information system, thus making MAS more effective in its use and operation. This is because it provides a better platform to create, search, manage, query and use information on management accounting activities. This supported Kucera et al. (2003) that managerial accounting provides information for processing and utilization to organizations’ management information system.

Conclusion and Recommendations: The result of this study revealed that organizations in Nigeria have low and poor culture towards management accounting and information systems practices; preferred and used the traditional management

accounting practices (if at all they use) than the new and modernized ones. In addition, gender and age (26-30 Years) exerted significant influence on the possibility of not deploying Management Accounting System in organization in Nigeria while number of employees explains the possibility of organisation in Nigeria to deploying Management Accounting System. Socio-demographic characteristics do not really have influence on the use and non use of MIS in organizations in Nigeria. This implies that demographic characteristics of organization and owners do not have significant importance on MIS deployment (of which educational level should have positive influence). This shows that the Nigeria education system have not deployed the effective use and imbibe ICT into its curriculum to enhance Nigerians productivity and make them compete even at the global level.

Furthermore, there was no significant relationship between management accounting systems and management information systems. There was no significant relationship between management accounting systems and organizational performance. There was no significant relationship between management information systems and organizational performance. Finally the result of this study revealed that the use of Management Information systems in organization does have significant influence on the effectiveness of management accounting system use.

From this study, various recommendations could be made. These include:

i. Workshops and training for organization should be organized by either government or private

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

16

organizations interested in the development of organizations. In some cases, this may be a collaborative effort between the two (public and private) so as to provide necessary training and teachings needed by organization to enhance their growth and development.

ii. Necessary trainings and teachings that should inculcated into such workshop organized are the need for effective management accounting systems and practices in organizations; the need of use of management information systems. Howbeit, it will be necessary when the bodies and individuals providing such trainings and teachings show them the practical aspects of both the MAS and MIS so as not to lead to confusion.

iii. Also, the benefits of the MAS and the use of MIS to enhance MAS and their performance should be revealed to organizations.

iv. Some factors are to be put into considerations (such as gender differences, age of owners, and also of organization, numbers of employees) in such trainings and workshops to make sure appropriate information and solution are delivered to the right persons and group of persons.

v. Furthermore, organizations in Nigeria should endeavour to put into practice by deploying and using management accounting and information system to enhance their business growth and development and also making

it globally competitive especially in this competitive environment.

vi. The use of ICT or information systems such as management information system in various systems should be inculcated even in the educational sector. This should involve a practical training and teaching of students to enhance the use of ICT and information system even at individual level and organisation level.

REFERENCES

Abdel-Kader, M and Luther, R. (2006).Management Accounting Practices in the British Food and Drinks Industry, British Food Journal, Vol.108.pp.336-357

Ajibolade S. O. (2013), Drivers of Choice of Management Accounting System Designs in Nigerian Manufacturing Companies, International Journal of Business and Social Research (IJBSR), Volume -3, No.-9.

Aziz N., Hui W.S., and Mahmud. (2014), Exploring the Attitude of Managers towards Key Performance Indicators (KPIs) in Response to Public Sector Change: A Rasch Analysis, Journal of Economics, Business and Management, Vol. 3, No. 1, DOI: 10.7763/JOEBM.2015.V3.166 119

Chia, Y. M. (1995). Decentralization, Management Accounting System (MAS) Information Characteristics and Their Interaction Effects on Managerial Performance: A Singapore Study. Journal of Business Finance & Accounting, 22(6), 811-830.

Croteau A. and Bergeron F., (2001), An information technology triology: Business Strategy, technological deployment and Organisational performance, Journal of strategic information systems 10 (2001) 77-99, Elsevier.

El Louadi M. (1998), The relationship among organisation structure, information technology and information processing in

Am. J. Soc. Mgmt. Sci., 2015, 6(1): 1-17

17

small Canadian firms, Canadian Journal of Administrative Science, vol. 15, n. 2: 99-180.

Etemadi H., Dilami Z. D., Bazaz M.S. and Parameswaran R. (2009), Culture, management accounting and managerial performance: Focus Iran, Advances in Accounting, incorporating Advances in International Accounting, 25:216–225, journal homepage: www.elsevier.com/locate/adiac

Grande E. U., Estébanez R. P., and Colomina C.M. (2011), The impact of Accounting Information Systems (AIS) on performance measures: empirical evidence in Spanish SMEs, The International Journal of Digital Accounting Research Vol. 11, pp. 25 – 43, ISSN: 1577-8517

Hilton, R. W. and Platt E. D. (2011). Managerial Accounting: creating value in Global business Environment. 9th edition. Global Edition. McGraw Hill International Edition.

Horngren, C. T., Foster, G. & Datar, S. M. (1994). Cost accounting: A managerial emphasis. Prentice-Hall. New Jersey.

International Federation of Accountants (1998). Statement of management accounting concepts. Retrieved January 18, 2006 from http://www.ifac.org/members/downloads/MAPS-1Accounting concepts pdf.

Johnson, H. T. & Kaplan, R. S. (1987) Relevance lost: The rise and fall of management accounting. Massachusetts: Harvard Business School Press.

Kucera M., Skorecova E., and Szovics P. (2003), Managerial Accounting as a source of information for product cost management in managerial information systems, Agricultural Economics, Czech, 49, (8), 357-360

Laudon K., Laudon J., and Dass R., (2006). Management Information System, Prentice Hall, Azimuth Interactive Inc.

Lund, D. (2003). Organizational culture and job satisfaction. The Journal of Business & Industrial Marketing, 18(2), pp. 219-237.

Sunarni C.W. (2013), Management Accounting Practices and the Role of Management Accountant: Evidence from manufacturing Companies throughout Yogyakarta, Indonesia, Review of Integrative Business Economics Research Vol 2(2)

Taticchi, P, Cagnazzo, L & Botarelli, M. (2008), Performance measurement and Management for SMEs: a literature review and a reference framework for PMM design‟ POMS 19th Annual Conference La Jolla, California, U.S.A, 9-12 May.